Abstract

We examine environmental discourse in conference calls and the relation between this discourse and firm value. We measure the amount of environmental discourse as the frequency count of environmentally-related topics in the transcripts of conference calls. We argue that greater environmental discourse in conference calls indicates firms’ prioritization of environmental issues. Evidence indicates that greater amounts of environmental discourse are associated with lower share price and higher cost of capital, which we interpret as reflecting the relatively higher costs of environmentally responsible operations in excess of firm-specific benefits. Additional analysis examining general environmental, social, and governance (ESG), especially social and governance, discourse shows that it is associated with lower cost of capital and higher share price, suggesting that prioritization of social and governance issues does not imply higher operational costs and indeed may signal firm-specific value creation.

Introduction

As regulators struggle with the types and amount of environmental, social, and governance (ESG) disclosure that should be required, an important consideration is the use of such information by investors and whether it creates costs or benefits for the firm. Motivated by the increasing attention from investors and regulators on environmental matters, we study whether discussion of environmental issues in conference calls is associated with firm value and cost of capital. Our study considers the amount of environmental discussion in conference calls as a proxy for the extent to which firms prioritize environmental issues and view them as integral to investors’ valuation and investment processes. Prior research (e.g., Clarkson et al., 2013; Plumlee et al., 2015) has studied the relation between environmental disclosure and firm value; however, discussion in conference calls differs importantly from the voluntary disclosure setting. Because conference calls are time constrained, discussion of particular topics in conference calls can be viewed as a signal of the relative priorities of firms and their investors.

Focusing on the conference calls occurring in conjunction with firms’ announcements of periodic performance, we first address whether and how the amount of discussion regarding environmental matters has evolved and how this evolution compares with the amount of discussion of more general ESG topics, especially social and governance, which are also referred to as corporate social responsibility (CSR) topics. 1 We then examine whether a relation exists between firm valuation and the amount of discussion accorded to environmental matters.

The past decades have seen a vast growth in environment-related investments. The move by investors toward sustainability-focused companies has been characterized by the CEO of the world’s largest asset manager as a “tectonic shift” (Blackrock, 2021). It is reasonable to expect that such a massive shift in capital allocation would correspond to important economic benefits and costs accruing to affected firms and that firm-investor discourse regarding economic impact would increase in importance. Accordingly, we expect some relation between the amount of firm-investor environmental discourse and financial measures such as firm value and cost of capital.

Although conference call discourse differs from disclosures issued in mandatory or voluntary publications, the amount of environmentally-focused discourse could have an impact similar to that of environmental disclosures. Specifically, similar to greater amounts of voluntary disclosure, greater amounts of environmentally-focused discourse should result in a reduction of information asymmetry and a corresponding increase in firm value similar to that found in some research on environmental disclosure in stand-alone or integrated reports (e.g., Plumlee et al., 2015). 2 Moreover, to the extent that environmentally-focused discourse is generally focused on positive aspects of firms’ efforts, greater amounts of discourse could result in incorporation into firm valuations of indirect or long-horizon financial returns. For example, discussion of a firm’s efforts to reduce emissions and waste could result in the inclusion in the traditional terminal value calculation of some quantifiable aggregated societal benefits of environmentally responsible behavior.

Alternatively, greater amounts of environmentally-focused discourse—however positive—could have a negative valuation impact, for example, by increasing uncertainty from the perspective of maximizing shareholder value. Such uncertainty would arise because investments that mitigate environmental damage are typically costly. Moreover, the benefits of environment-protecting investments accrue to society as a whole, but the financial costs are primarily borne by the firm. At the extreme, prioritizing the environment could result in firms potentially undertaking negative net present value (NPV) projects or even shifting fundamental objectives to no longer prioritize maximizing financial return on investment. Overall, whether and how environmental discourse in conference calls relates to firm value and cost of capital is an open empirical question.

Our study is similar to, but distinct from, the work of Dhaliwal et al. (2011), Clarkson et al. (2013), and Plumlee et al. (2015). Dhaliwal et al. (2011) examine whether initial voluntary disclosure about firms’ CSR (corporate responsibility activities) is associated with the cost of capital. Clarkson et al. (2013) examine the impact on firm value of voluntary environmental disclosure reported in CSR reports and corporate websites for firms in five environmentally sensitive industries. Finally, the work of Plumlee et al. (2015) studies the relationship between environmental disclosure and share price and cost of capital for firms in five non-sensitive and sensitive environmental industries. Although these studies add to the understanding of the impact of voluntary environmental disclosure on capital market outcomes by documenting that such disclosures improve firm valuation (Clarkson et al., 2013; Plumlee et al., 2015) and lower cost of capital (Dhaliwal et al., 2011; Plumlee et al., 2015), they may not be directly applicable to the setting of environmental disclosure in conference calls.

Indeed, various factors suggest that discussion of environmental issues in the conference call setting may differ from the disclosure settings examined in prior research. First, the content of conference calls, which involve direct real-time participation of senior managers such as the CEO and the CFO, may be less restrained than firm-authored disclosures (Davis et al., 2015). Comments by senior managers in a conference call about environmental and general ESG issues might be less guarded and more nuanced than environmental disclosure in standalone or integrated reports. Second, conference calls are two-way communications between managers and analysts, where analysts have the opportunity to question managers regarding information or concerns about topics of interest, including environmental and general ESG topics. The self-serving biases observed in narrative disclosure—for example, the biased language and tone of firms’ environmental disclosures in annual reports (Cho et al., 2010)—may differ in the conference call setting. Finally, as noted above, direct real-time participation of senior managers means that conference calls are time constrained. Unlike disclosure reports where length is relatively unbounded, conference call discussions occur within a given period of time—usually an hour or less. As such, the content of such calls can be viewed as a signal of priorities. Overall, the amount of discussion in conference calls about firms’ environmental performance may itself provide value-relevant information beyond the information provided in other channels of communication.

We address our research questions using computerized textual analysis of conference call transcripts of 147,359 conference calls from 2006 to April 2020. Our measure of environment-related content is based on frequency counts of keywords focused on environmental issues. Data indicate that the average mention of environmental phrases increased dramatically from 0.657 in 2006 to 3.437 in 2020 and that there is an increased focus on specific environmental issues compared to general aspects of ESG. Discussion of environmental issues has also become more pervasive. Only 20.08% of firms’ conference calls included any mention of environmental topics in 2006, compared to 43.62% in 2020. The increase in amount and pervasiveness has not been linear, with a spike in amount and pervasiveness in 2010 and 2011. 3

Our analysis provides evidence of a positive relation between cost of capital and the amount of environmental discourse, controlling both for environmental performance and environmental disclosures in firm reports, suggesting that greater discussion about environmental issues in conference calls increases uncertainty about financial outcomes. 4 We also find an inverse relation between the amount of environmental discourse and firm value. The economic implications of our findings are intuitive: It is rational to assume that prioritizing investments for reasons other than value maximization will yield returns that are lower than investments chosen solely for value maximization.

Additional analysis indicates that the decrease in firm value is more pronounced for firms that prioritize environmental discussion and have poor environmental performance. This finding suggests that financial costs for environmentally responsible operations are higher for worse environmental performers because prioritization of the environment would incur an even greater degree of costly investment for these firms. Finally, across all analyses, the amount of environmental discourse in the remarks portion of the calls dominates that in the Q&A portion as an explanatory factor for cost of capital and share price.

While the economic implications of our findings seem intuitive since non–value-motivated operating priorities are unlikely to maximize value, they raise a question of why senior management would signal prioritization of issues that may result in a higher cost of capital and lower firm value. Is it reflective of management misjudging the market reaction to disclosures it expected to be received positively? While archival research cannot reveal management motivations, we conjecture that one answer may be that non-monetary utility (i.e., the rewards of doing the right thing—defined as setting priorities that balance the benefits across time and geography despite higher firm-specific costs) has become a part of the firms’ utility functions. Rather than a simple optimization problem—to maximize shareholder value during current management’s compensation window—the utility function may have evolved into a more multi-dimensional optimization spanning a longer time horizon.

5

The following quotation from a conference call transcript illustrates this notion: We are proud of our efforts to be a leader in using clean energy. It’s the right thing to do for the communities in which we operate and there’s an additional benefit of cost savings for our operations.

6

In other additional analyses, we compare the longer-term market returns for portfolios of firms with greater versus lesser discussion of environmental issues in their conference calls. Consistent with the main findings, the portfolio of firms with more environmental discussion in the call experience lower returns than the portfolio of firms with more discussion. In other words, an investment focused on firms that engage in more (versus less) discussion of environmental issues yields worse returns and lower firm value.

We also compare general ESG discourse to environment-specific discourse in conference calls. Unlike the results for environment-specific discourse—the “E” in “ESG”—greater amounts of general ESG discourse are associated with higher share price and lower cost of capital. One interpretation is that the more general discussions reflect priorities where the benefits accruing directly to the firm (e.g., financial benefits from hiring a more diverse team of employees or reputational benefits from purposefully ensuring fair labor practices along the supply chain) exceed the costs. In other words, prioritization of socially responsible activities likely yields benefits without the commensurate capital investments required by environmentally responsible operations.

Our study contributes to the literature in several ways. First, it adds to the firm valuation literature by providing evidence on the value relevance of the amount of environmental discussion in the context of conference calls. A rich stream of literature examines the value relevance of environmental disclosure. We extend those studies by investigating the relation between the prioritization of environmental issues (proxied by the amount of environmental discussion in conference calls) and firm value. We find that the quantity of environmental discourse in conference calls is value relevant but apparently reflects incremental costs (lower firm value and higher cost of capital). Moreover, an investment in a portfolio of high-discussion (versus low-discussion) firms is associated with lower returns.

Second, our research contributes to the study of conference calls as a disclosure and communication channel. Conference calls arguably provide a richer channel of communication than one-way, firm-authored disclosures such as regulatory filings and written press releases. In conference calls, managers can emphasize topics they believe are relevant to analysts, and subsequently, analysts’ questions signify the topics that merit their attention. Prior research finds that the information disclosed in conference calls reduces analyst forecast errors, increases trading volume, return volatility, and improves intra-industry information transfer (Brochet et al., 2018; Kimbrough, 2005; Matsumoto et al., 2011). We build on that research, demonstrating value relevance of the amount of call content allocated to environmental topics and introduce the perspective of call content signifying priorities. Along the same vein, our study provides evidence of a new information channel that influences analysts’ decisions—conference calls. Specifically, we provide evidence suggesting that analysts incorporate environmental, social, and governance-related discourse on conference calls into their valuation analyses.

Finally, our study contributes to the literature on computerized content analysis of disclosure. Our keyword lists, which are grounded both in current examples and in the prior literature, represent specific topics of disclosures pertaining to environment, social, and governance matters. We utilize the analysis to provide insights into the trends in environmental discourse between 2006 and 2020. Data show that the amount of discussion related to environmental issues increased in conference calls and that there is an increased focus on environmental issues compared to other general aspects of ESG.

Our study should be of interest to practitioners and regulators, given the growing attention to the topic of ESG disclosure generally and environmental disclosures in particular. The Securities and Exchange Commission (SEC) started the process of updating guidance regarding public companies’ disclosure requirements as they apply to climate-related risk to improve the value of such disclosures in 2021 (Securities and Exchange Commission [SEC], 2021). They issued a proposed rule in 2022 (SEC, 2022) and recently announced the time frame for a final ruling in 2023 (SEC, 2023). 7 The International Sustainability Standards Board (ISSB) issued its inaugural standards pertaining to sustainability-related disclosures in June 2023. 8 Our findings of a relation between the amount of environmental discourse and firm valuation may be relevant to those efforts.

Literature Review and Hypothesis Development

The Evolution of Environmental Discourse

The recent increase in investor and regulatory attention to ESG-related matters makes it important to study the relation between environmental discourse and the investment process and capital market outcomes. The incorporation of ESG factors into the investment process can occur in a variety of ways. A survey in 2016 of around 600 portfolio managers and other institutional investors indicates that the most prevalent ways of integrating ESG information in the investment process were engagement/active ownership (i.e., using shareholder power to influence corporate behavior, for example, by communicating with senior management) and full integration into individual stock valuation (i.e., “explicitly includ[ing] ESG factors into traditional financial analysis of individual stocks, for example, as inputs into cash flow forecasts and/or cost-of-capital estimates”; Amel-Zadeh & Serafeim, 2018, 94). 9 Furthermore, these institutional investors indicated that these ways of integration were expected to increase in importance in the coming years (Amel-Zadeh & Serafeim, 2018).

Conference call content signifies firms’ priorities and topics of importance to analysts attending the call, and thus, the proportion of these calls allocated to a given topic is an indicator of its relevance to the fundamental stock valuation process. Our primary focus is environmental discourse, which is often characterized as one important component of ESG and is likely to shed light on firms’ environmental performance. 10 Prior research documents that firm value is affected by environmental performance (Chapple et al., 2013; Cormier et al., 1993; Cormier & Magnan, 1997). In turn, environmental disclosure provides relevant information about environmental performance that may affect the fundamental valuation process (Clarkson et al., 2013; Matsumura et al., 2014; Plumlee et al., 2015). Given the increasing importance of environmental issues, we first explore how the proportion of environmental discourse in conference calls changed over the past years.

Conference calls consist of two portions, a prepared remarks portion, followed by a question-and-answer (Q&A) portion. The former reflects a one-way conversation (albeit presumably constructed with an awareness of the audience’s interest), and the latter reflects a two-way communication between management and audience participants. In the prepared remarks section, the firm’s management effectively sets the agenda, presenting the performance highlights of the period and discussing matters of priority for the firm and presumed relevance to analysts. In the Q&A portion of the conference, the analysts effectively set the agenda by choosing what questions to pose. We explore the amount of environment-related discussion in each portion of the call to understand the relative priority of the topic to managers versus analysts. Thus, our second research question is as follows: How does the proportion of environmental discourse in the remarks portion compare to that in the Q&A portion?

Given the importance of ESG topics, we also examine whether the attention accorded to environmental matters diverges from more general ESG-related discourse: How does the change in the proportion of environmental discourse in conference calls over the past years compare to the change in proportion of other general ESG discourse?

Environmental Discourse and Firm Value

Prior research explores the relation between firm value and environmental disclosures in standalone or integrated ESG reports. While ESG reports clearly differ from earnings conference calls, which are the focus of our study, prior findings may nonetheless be relevant since conference calls can similarly serve to reduce information asymmetry regarding firm performance and priorities. Clarkson et al. (2013) show a positive relation between firm value and environmental disclosure, incremental to environmental performance (measured as Toxics Release Inventory [TRI]), and Plumlee et al. (2015) similarly show an incrementally positive relation between firm value and positive environmental disclosures. In an international setting, Moneva and Cuellar (2009) document a positive but insignificant association between the market value of Spanish firms and environmental disclosures, measured on a set of information about environmental policies and the implementation of environmental management systems disclosed on annual reports. Gamerschlag et al. (2011) focus on German firms and use a self-constructed measure based on global reporting initiative (GRI) guidelines and find a negative but insignificant relation. In these studies, environmental disclosure is used as a proxy for environmental performance. In addition, the former two studies do not incorporate a more direct measure of environmental performance, which limits the ability to assess the impact of different levels of environmental performance, a key determinant of firm value (Clarkson et al., 2013).

Furthermore, several studies document that ESG information is used in analysts’ valuation analyses. Dhaliwal et al. (2012) demonstrate that standalone ESG reports are associated with more accurate analyst forecasts by complementing financial disclosure. Ioannou and Serafeim (2015) examine the sociological processes that affect the assessments of high-CSR firms by analysts and find that their forecasts became less pessimistic over time. Luo et al. (2015) find that analysts mediate the relationship between corporate social performance information and stock returns. In a recent article, Derrien et al. (2022) examine the consequences of negative ESG incidents on future profitability and find that analysts downgrade their forecasts following negative ESG news.

In sum, the literature examining the relation between environmental disclosure and firm value has focused on voluntary firm-authored ESG reports. 11 As noted, disclosure in written documents differs from discourse in oral communications in conference calls. Disclosures such as ESG reports are generally a more formal (scripted) and less flexible communication channel than conference calls. Moreover, given time constraints in earnings conference calls, the content reflects issues that are important to investors and also firms’ prioritization of issues.

Since environmental discourse is typically focused on environmentally-friendly activities, to the extent that investors with a pro-environment agenda create excess marginal demand for the company’s stock, a positive association between the amount of environmental discourse and firm value would be expected. In addition, to the extent that any disclosures potentially reduce information asymmetry, if discussion about firms’ environmental efforts improves transparency concerning performance, we would expect a positive association between the amount of environmental discourse and firm value. Conversely, the amount of environmental discourse in conference calls could be associated with lower firm value because investments to preserve the environment are typically costly. For example, it is cheaper to dump raw sewage into a river than invest in a wastewater treatment plant. And while the incremental costs are near term and firm-specific, the incremental benefits are longer term and shared across society. Therefore, additional costs incurred by a firm for environmentally-friendly investments could generally be expected to result in a near-term decrease in the value of the investing firm.

If, however, investors’ decisions are based on the firms’ environmental performance and its ESG disclosures to the exclusion of content in conference calls, no association between environmental discourse and firm value would be observed. Thus, we formulate our hypothesis in the null form:

Because of fundamental differences between the prepared remarks portion of firms’ conference calls and the Q&A portion of the call, we further hypothesize that the discourse in each portion is individually informative. In the conference call setting, greater amounts of discourse by managers concerning environmental matters could signal preventive attention that would attract investors that value indirect or long-horizon returns at the benefit of conserving the environment; alternatively, it could signal costly investments and increase investors’ uncertainty concerning firms’ financial prospects. Analysts’ interactions with managers in the Q&A section of conference calls can be informative beyond the manager’s prepared remarks (Matsumoto et al., 2011). More discussion by analysts of environmental matters could either increase or decrease firm value for the reasons described above. This leads to the following hypothesis stated in the null form:

Environmental Discourse and Cost of Capital

Prior research that examines the effect of environmental disclosure on firm value focuses on cost of capital as a potential channel linking these two constructs (Clarkson et al., 2013; Plumlee et al., 2015). As a result, to better understand the mechanism through which environmental discourse in conference calls is associated with firm value, we examine the association between environmental discourse and cost of capital. The theory generally suggests an inverse relation between increased disclosure and cost of capital through a reduction in information asymmetry and estimation risk (e.g., Diamond & Verrecchia, 1991; Richardson & Welker, 2001). Prior research that has addressed the relation between cost of capital and CSR disclosures in firm-authored reports finds a decrease in cost of capital following firms’ initiation of voluntary disclosures of CSR reporting (Dhaliwal et al., 2011). 12 With regard to environmental disclosures in integrated or standalone reports specifically, various arguments support an inverse relation with cost of capital. Environmental disclosures may reflect the firms’ strategy and commitment to eco-friendly activities, improvements to operational efficiency, and other types of process innovation that might result in future competitive advantages that decrease operating risk and thus lower the cost of capital. 13 As a result, voluntary environmental disclosure reflects a mechanism whereby the capital markets can obtain value-relevant information to evaluate environmental performance. Even apart from any future operational effects, environmental disclosures could affect the cost of capital directly “if investors are willing to accept a lower expected return on investments that also fulfill social objectives” (Richardson & Welker, 2001). Especially given the current demand for environmentally-friendly investments, firms could experience a lower cost of capital due to greater investor demand driven by nonquantitative factors. Finally, it has been stated that “climate risk is investment risk,” and “as markets started to price climate risk into the value of securities, it would spark a fundamental reallocation of capital” (Blackrock, 2021). If the amount of firm-investor environmental discourse signifies a firm’s focus on reducing climate risk, we would expect an inverse association between a greater amount of discourse and a reduced cost of capital.

Despite strong arguments suggesting an inverse relation between increased environmental disclosure and cost of capital, findings from prior research are nuanced and context-dependent. Clarkson et al. (2013) find no evidence of a relation between cost of capital and voluntary environmental disclosure, measured on their self-constructed index of different disclosure contents. Similarly, Plumlee et al. (2015) found no relation between the cost of equity and overall environmental disclosure, measured as their self-constructed index of different disclosure environmental contents. However, the analysis by Plumlee et al. (2015) incorporating detailed aspects of environmental disclosure quality—namely, the disclosure’s type (hard or soft) and its nature (positive, neutral, or negative)—yields evidence of an inverse relation between cost of capital and certain types of environmental disclosure. In contrast, Richardson and Welker (2001) provide self-described “surprising” evidence of a positive relation between cost of capital and social disclosure, measured as a score based on a checklist of information of which 24% pertained to environment and energy. Among the possible explanations for the positive relation, the authors note that their disclosure score is based on completeness and does not indicate whether the disclosure is positive or negative. Furthermore, they note that the results could hold if the social disclosure scores were indicative of social responsibility actions that involved consistently negative present value projects increasing the overall risk of the firm (Richardson & Welker, 2001). Similarly, a recent study finds a positive association between climate risk-related disclosure extensiveness in 10-K and cost of capital (Berkman et al., 2024).

In light of the contradictory empirical results regarding the relationship between environmental disclosure and cost of capital, we re-examine the relationship through the lens of firm-investor discourse in conference calls. We expect to see a negative association between greater amounts of environmental discourse and cost of capital if it signals firms’ efforts in lowering environmental risk and if investors are willing to accept indirect or long-term financial returns that benefit social objectives. However, we expect to see a positive association with cost of capital if greater amounts of environmental discourse about firms’ environmentally-friendly activities are perceived by investors as costly investments that do not align with firms’ utility function to maximize shareholder wealth. Given competing expectations regarding the relation between environmental discourse and cost of capital are unclear, we formulate the hypothesis in the null form:

Managers’ prepared remarks and the Q&A portion of conference calls can be individually informative. As such, each portion could shed light on the firm’s efforts to reduce environmental risks, which could decrease or increase cost of capital. We state the hypothesis in the null form:

Methodology and Descriptive Information

Construction of Keyword Lists

Environmental Keywords

Our list of environmental key words is presented in Appendix A. We develop our key words in six steps. First, we focus on environmentally sensitive industries. Seven industries are identified from the prior literature as environmentally sensitive. These industries belong to the following 2-digit Standard Industry Classification (SIC) codes: 20 (food manufacturers), 26 (pulp and papers), 28 (chemicals), 29 (oil and gas), 33 (metals and mining), 49 (utilities), and 58 (eating and drinking places; Clarkson et al., 2008, 2013; Plumlee et al., 2015). We extend this list by identifying five additional industries that are likely to have high pollution propensity as they may adversely impact the natural environment, 2-digit SIC codes: 13 (oil and gas extraction), 35 (industrial machinery & equipment), 36 (electronic & other electric equipment), 37 (transportation equipment), and 38 (instruments & related products). Next, we download financial information from Compustat for firms in these 12 industries for fiscal years 2006, 2012, and 2018 and search for the three largest firms in each industry (by revenues and fiscal year). 14 We then download annual conference call transcripts for the 108 firms from Lexis Nexis and Seeking Alpha. We use these transcripts to conduct manual content analysis and identify 91 environment-related keywords. 15 Subsequently, the keyword list is validated by having one of the researchers randomly select 10 transcripts and reperform manual content analysis. No differences are noted during the validation procedure. Finally, we review the academic and professional literature (Barth & McNichols, 1994; Campopiano & De Massis, 2015; Chen & Bouvain, 2009; Stubbs & Higgins, 2018; U.S. Environmental Protection Agent [EPA], 2021) to identify additional environmental keywords. Specifically, we review the literature and extract environmental topics. From this review, we find 15 additional keywords. In total, our keyword list, presented in Appendix A, consists of 100 keywords.

General ESG Keywords

As noted, our primary interest is in environmental discourse, that is, the “E” in “ESG.” For comparative purposes, we create a list of key words for discourse pertaining to more general ESG topics, especially social and governance, shown in Appendix B. We follow a similar procedure to identify these keywords and identify 29 key words of which 18 are extracted from conference call transcripts and 11 from the prior academic literature (Campopiano & De Massis, 2015; Chen & Bouvain, 2009; Erwin, 2011).

Sample Selection

Sample selection begins with all conference call transcripts from Seeking Alpha between 2006 and April 2020, which yields 147,359 transcripts for conference calls on firm-quarter-level earnings. We select 2006 as the starting date because it is the earliest date for which a comprehensive collection of transcripts exists on Seeking Alpha. We process each conference call transcript to create frequency counts of the environment-related keywords and the more general ESG-related keyword based on keyword lists described in the previous section and use the frequency to indicate the environmental disclosures and more general ESG disclosures.

Plant-year-level emission data from the Environmental Protection Agent (EPA) website are the basis of our measure of pollution performance. To link plants with their parent firms, we first download the TRI data in EPA from 2005 to 2019. Following the study by Xiong and Png (2019), we match TRI data with Compustat by the name of the parent company. 16 We keep only records with a similarity score of 85% or more and then manually validate. 17

Analysts’ forecast data are from I/B/E/S, all other financial data items are from COMPUSTAT, and market data are from CRSP. After deleting firms with non-matching data from COMPUSTAT, CRSP, or I/B/E/S, the sample includes 5,615 firm-years. The detailed sample construction is summarized in Table 1.

Sample Selection.

To compute COC using the Easton (2004) MPEG model, we make sure two-period forward earnings forecast is not smaller than one-period forward earnings forecast and that both of them be positive. bMerging with TRI data (environment performance) does not lead to sample size reduction because for firms that do not report pollution to EPA, they are coded as pollution release equals to zero.

Specification of Empirical Tests of Relation Between Environmental Discourse and Firm Value and Cost of Capital

To test the hypothesis of the relation between environmental discourse and firm value, we employ the following equation, drawing from prior research (e.g., Clarkson et al., 2013; De Villiers & Marques, 2016; Dhaliwal et al., 2011; Plumlee et al., 2015):

where SharePrice is the closing market value per share 10 months after the fiscal year end. EnvDiscourse is the frequency count of environment-specific keywords in the entire conference call for tests of H1 and in the separate components of the call for tests of H2, specifically the prepared remarks section of the call, EnvDiscourse_remarks and the Q&A section of the call, EnvDiscourse_qa. EPS is earnings per share as reported for the fiscal year. BPS is book value per share, measured at the end of the fiscal year as total book value divided by number of shares outstanding. TRI is intra-industry percentile ranking of TRI emission for the year, reported by the EPA, divided by sales. Escore is the Bloomberg environmental disclosure score. Size is natural logarithm of one plus firms’ total assets at the end of the fiscal year. MTB is market-to-book ratio, defined as the market value of equity divided by book value of equity. Length is the total word count of the conference calls. We include industry and year fixed effects to control for macroeconomic shocks and time-invariant industry factors. We also cluster standard errors by firm. Table 2 summarizes variable definitions.

Variable Definitions.

To address the relation between the amount of environmental discourse and cost of capital, we estimate the following equation drawing from prior research (e.g., Clarkson et al., 2013; Dhaliwal et al., 2011; Plumlee et al., 2015):

where CoC is the implied cost of equity capital in 10 months after the fiscal year end, calculated as per the Easton (2004) Modified PEG (MPEG) model. EnvDiscourse is the frequency count of environment-specific keywords in the entire conference call for tests of H3 and in the separate components of the call for tests of H4, specifically the prepared remarks section of the call, EnvDiscourse_remarks, and the Q&A section of the call, EnvDiscourse_qa. TRI is intra-industry percentile ranking of emissions-to-sales ratio. The emissions are collected from the TRI of the EPA. Escore is the Bloomberg environmental disclosure score. 18 Size is natural logarithm of one plus firms’ total assets at the end of the fiscal year. MTB is defined as the market value of equity divided by book value of equity. Leverage is the leverage ratio, defined as the ratio of total debt divided by total assets. Beta is estimated from the market model using the daily CRSP stock returns. LTG is average analyst-forecasted long-term growth rate. 19 Lndisp is analyst forecast dispersion, measured as the logarithm of the standard deviation of analyst estimates of year t earnings divided by the consensus forecast of year t earnings. Length is the total word count of the conference calls. We include industry and year fixed effects to control for macroeconomic shocks and time-invariant industry factors. We also cluster standard errors by firm.

Results

Descriptive Statistics

Table 3 reports the summary statistics of the variables used in our analyses. The mean value of SharePrice indicates the average stock price is $61.540. The value of COC indicates that sample firms’ implied cost of capital is 10.183% on average. The average earnings per share EPS is $2.715, and the average BPS is $21.268. A sample conference call includes an average of 2.657 environment expressions and 1.115 general ESG expressions in total. Both environmental and general ESG expressions are mentioned more in the prepared remarks section (EnvDiscourse_remarks: 1.580; ESGDiscourse_remarks: 0.747) than in the Q&A section (EnvDiscourse_qa: 1.028; ESGDiscourse_qa: 0.359). The value of Escore shows an average Bloomberg environmental disclosure score of 21.230 out of 100 points.

Summary Statistics of Variables in the Cost of Capital Regression.

Note. This table provides sample descriptive statistics for the variables used in our empirical tests.

Environmental Discourse Over Time

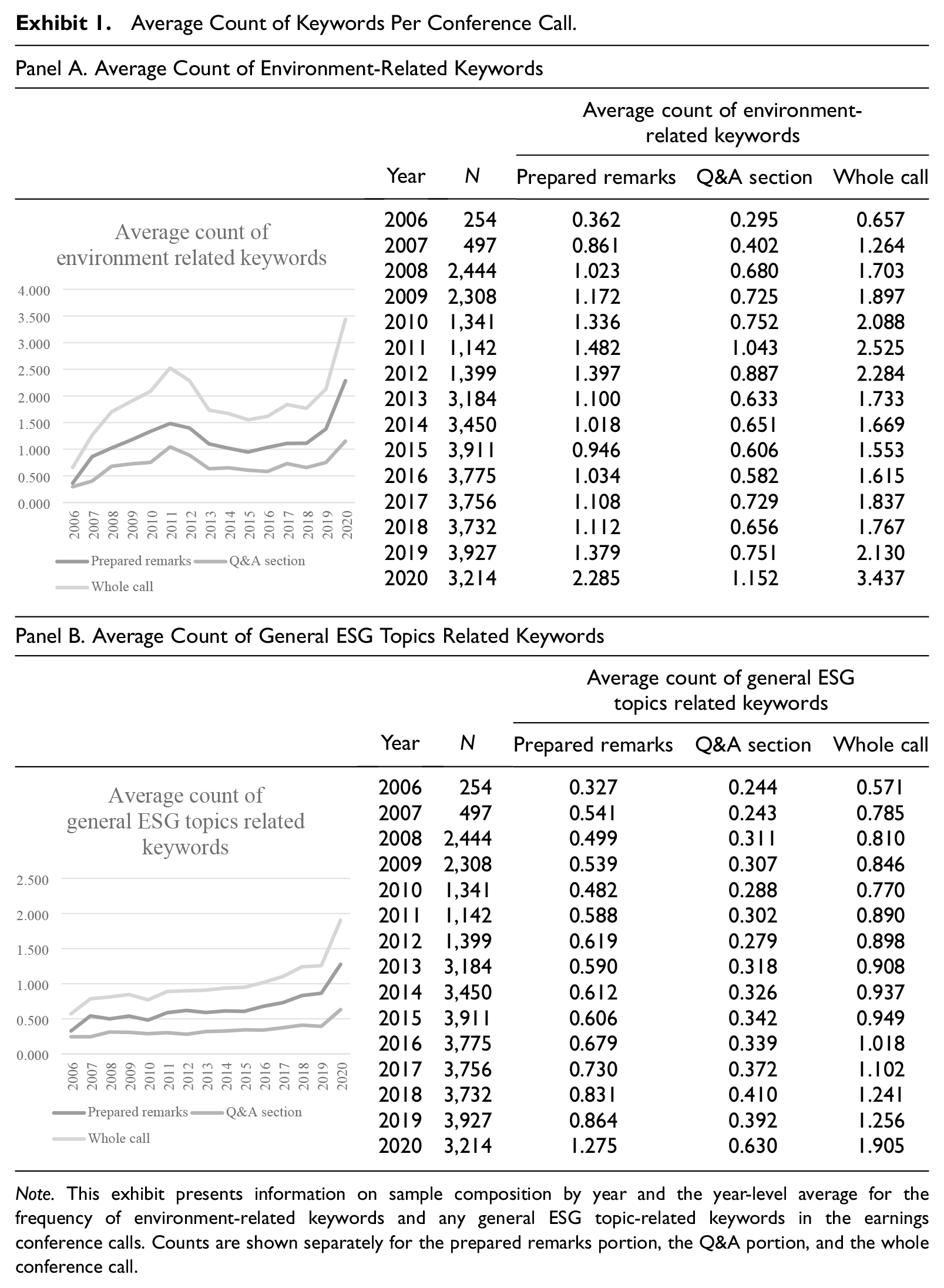

Exhibit 1 Panel A addresses the question of how the proportion of environmental discourse in conference calls has changed over the past years, showing the average number of mentions of environmental phrases by year. In 2006, the average count was 0.657 with 0.362 times in the prepared remarks section and 0.295 times in the Q&A section. By 2020, the average number of mentions of environmental phrases in the conference calls increased to 3.437 in total, with 2.285 times in the prepared remarks section and 1.152 times in the Q&A section.

Average Count of Keywords Per Conference Call.

Note. This exhibit presents information on sample composition by year and the year-level average for the frequency of environment-related keywords and any general ESG topic-related keywords in the earnings conference calls. Counts are shown separately for the prepared remarks portion, the Q&A portion, and the whole conference call.

For comparative purposes, Exhibit 1 Panel B shows the trends in general ESG discussion in conference calls. Similar to environment-specific discourse, there has been gradual rise in the amount of general ESG. The average number of mentions of general ESG phrases in the prepared remarks consistently exceeds that in the Q&A section.

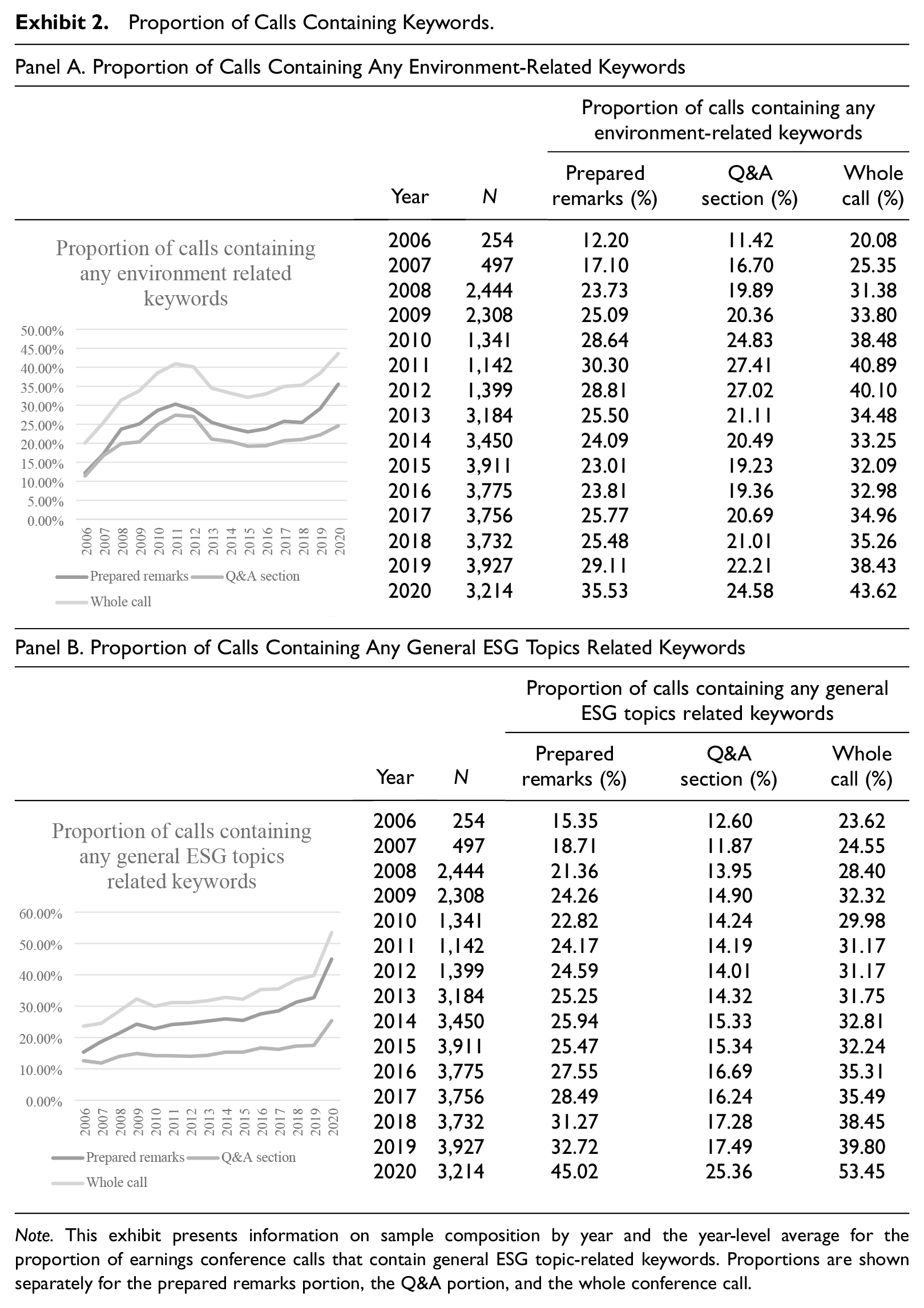

Exhibit 2 Panel A presents the proportion of conference calls containing any mention of environmental matters. In 2006, only 20.08% of firms’ conference calls include any mention of environmental topics, and the proportion of calls containing environment-related keywords is higher for the prepared remarks section (12.20%) than the Q&A section (11.42%). The proportion increases to 43.62% in 2020, and the proportion of calls in which the prepared remarks section contains any environment-related keywords (35.53%) is much higher than the proportion of calls in which the Q&A section (25.48%). The increased pervasiveness has not, however, been consistent, with discourse becoming more pervasive in 2010 and 2011 before declining to pre-2010 levels and then increasing rapidly at the end of the decade. Overall, the proportion of environmental discourse in conference calls increased over the past 15 years. The proportion of environmental discourse in the prepared remarks section consistently exceeds that in the Q&A portion.

Proportion of Calls Containing Keywords.

Note. This exhibit presents information on sample composition by year and the year-level average for the proportion of earnings conference calls that contain general ESG topic-related keywords. Proportions are shown separately for the prepared remarks portion, the Q&A portion, and the whole conference call.

To compare it with general ESG discussion, Exhibit 2 Panel B shows the proportion of conference calls containing any mention of general ESG matters. Similarly, there has been a gradual rise in the proportion of general ESG topics. The proportion of the prepared remarks that include general ESG is consistently higher than that of Q&A section. Taken together, Exhibits 1 and 2 show that there is consistent increase in the discussion of both general ESG topics and specific environmental topics.

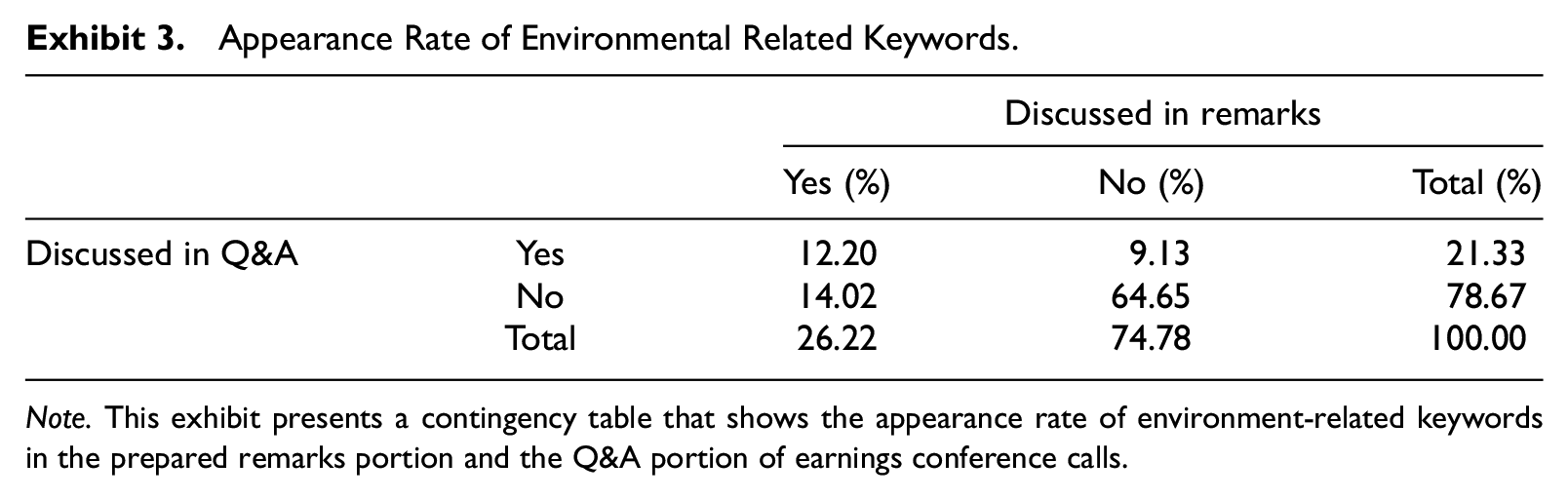

Exhibit 3 presents the joint frequency of conference calls that mention environmental keywords in the prepared remarks portion and Q&A portion. The probability of an environment-related discussion in the Q&A portion if such discussion exists in the remarks portion is 46.53%. 20

Appearance Rate of Environmental Related Keywords.

Note. This exhibit presents a contingency table that shows the appearance rate of environment-related keywords in the prepared remarks portion and the Q&A portion of earnings conference calls.

Environmental Discourse and Share Price

Table 4 shows the regression results for tests of H1 and H2 about whether environmental discourse is incrementally informative beyond firms’ environmental performance and ESG disclosure, and thus related to firms’ share price. The dependent variable is the firm’s share price 10 months after the fiscal year end, 21 and the test variables of interest are the amount of environment-related discourse in the entire conference call (EnvDiscourse), the prepared remarks section (EnvDiscourse_remarks), and the Q&A section (EnvDisourse_qa). The coefficients are significantly negative for the amount of environmental discourse in the entire conference call (EnvDiscourse), in the manager-prepared remarks section of the call (EnvDiscourse_remarks), and in the Q&A section (EnvDisourse_qa). As shown in Column (1), a one-unit increase in the amount of environmental discourse in the total conference call is associated, on average, with a 0.276 decrease in a firm’s share price. The results in Column (2) indicate that a one-unit increase in the amount of environmental discourse in the prepared remarks section of the call is associated with an average decrease of 0.428 in a firm’s share price. Furthermore, Column (3) shows that a one unit increase in the amount of environmental discourse in the Q&A section is associated, on average, with a 0.433 decrease in a firm’s share price. In sum, evidence rejects the null hypothesis of no relation between firm value and the amount of environmental discussion in conference calls or in the two sections of conference calls. Instead, results suggest that prioritizing environmental issues in conference calls has a negative association with firm value. 22

Results of Regression of Share Price on Environmental Discourse.

Note. This table presents coefficients and t-statistics in parentheses from pooled regression of the dependent variable Share Price, on the independent variables listed. Share Price is the company’s closing market value per share measured 10 months after the fiscal year end. EnvDiscourse denotes the keyword count of environment-related disclosure in the whole conference call, while EnvDiscourse_remarks and EnvDiscourse_qa, respectively, represent the frequency of environment-related keywords in the prepared remarks portion and Q&A portion of the conference call. Detailed variable definitions are provided in Table 2. All regressions include year and industry fixed effects. Standard errors are clustered by firm.

, **, and * indicate two-sided significance at the 1%, 5%, and 10% levels, respectively.

Environmental Discourse and Cost of Capital

Table 5 reports the results of tests of H3 and H4, about whether the amount of environmental discussion in conference calls is incrementally informative as indicated by a firm’s cost of capital. The dependent variable is the implied cost of equity capital 10 months after the fiscal year end, estimated using the Easton (2004) MPEG model, and the test variables of interest are EnvDiscourse, EnvDiscourse_remarks, and EnvDiscourse_qa. 23 The coefficients are significantly positive for two of the variables of interest, with EnvDiscourse and EnvDiscourse_remarks, and the economic magnitude of the positive relation with cost of capital is substantial. The results reported in Column (1) imply that one-unit increase in environmental discourse in the conference calls, on average, is associated with a 0.022-unit increase in the firm’s cost of capital. This evidence rejects the null hypothesis of no relation between cost of capital and the overall amount of environmental discussion in conference calls (H3). The results in Column (2) suggest that the cost of capital, on average, increases by 0.041 for each one-unit increase in environmental discourse in the prepared remarks section. We do not find a statistically significant relation between the amount of environmental discourse in the Q&A section and firms’ cost of capital. This evidence rejects the null hypothesis of no relation between cost of capital and the amount of environmental discussion in the separate sections of conference calls (H4). Instead, results generally suggest that prioritizing environmental issues in conference calls is associated with a higher cost of capital. 24

Results of Regression of Cost of Capital on Environmental Discourse.

Note. This table presents coefficients and t-statistics in parentheses from pooled regression of the dependent variable COC, on the independent variables listed. COC is the implied cost of equity capital (in percentage) 10 months after fiscal year end, estimated using Easton (2004) MPEG model. EnvDiscourse denotes the keyword count of environment-related disclosure in the whole conference call, while EnvDiscourse_remarks and EnvDiscourse_qa represent the frequency of environment-related keywords in the prepared remarks portion and Q&A portion of the conference call, respectively. Detailed variable definitions are provided in Table 2. All regressions include year and industry fixed effects. Standard errors are clustered by firm.

, **, and * indicate two-sided significance at the 1%, 5%, and 10% levels, respectively.

Additional Analysis

Environmental Discourse and Poor Environmental Performance

In this section, we explore whether the decrease in firm value is more pronounced for firms that engage in more environmental discourse but perform poorly in an important environmental metric. Considering our findings in the main analysis suggesting that prioritizing the environment is costly, we expect that the decrease in share price and increase in cost of capital are more severe for firms that prioritize environmental issues in conference calls but have poor environmental performance because prioritization of the environment would incur an even greater degree of costly investment for those firms. We use Equations 1 and 2 and conduct a subsample analysis for high-discuss and low-discuss firms. The high-discuss sample consists of firm-years where the proportion of environmental discourse is in the top 50% by industry and year. The low-discuss sample is made up of firm-years, with environmental discourse in the bottom 50% by industry and year. 25

The results reported in Table 6 provide evidence consistent with the notion that firms with a higher amount of environmental discourse and poor environmental performance suffer a more pronounced decline in share price than firms with a lower amount of environmental discourse and poor environmental performance. For TRI, our proxy for environmental performance, we observe that the coefficient in Column (2) is statistically significant and negative, while the coefficient in Column (1), for firms with a lower amount of environmental discourse and poor environmental performance, is negative but not statistically significant. Table 7 for cost of capital shows a similar pattern suggesting that the increase in cost of capital is more severe for firms with more environmental discourse and higher Toxic Release Inventory (TRI). Together, these results provide support to the notion that environmental discourse implies prioritization of financially costly activities.

Results of Regression of Share Price for High/Low Amount of Environmental Discourse.

Note. This table presents coefficients and t-statistics in parentheses from the subsample regression of the dependent variable Share Price, on the independent variables listed for firm-years with high/low discuss on environment. Share Price is the company’s closing market value per share measured 10 months after fiscal year end. All regressions include year and industry fixed effects. Standard errors are clustered by firm.

, **, and * indicate two-sided significance at the 1%, 5%, and 10% levels, respectively.

Results of Regression of Cost of Capital for High/Low Amount of Environmental Discourse.

Note. This table presents coefficients and t-statistics in parentheses from subsample regression of the dependent variable COC, on the independent variables listed for for firm-years with high/low discuss on environment. COC is the implied cost of equity capital (in percentage) 10 months after fiscal year end, estimated using the Easton (2004) MPEG model. Detailed variable definitions are provided in Table 2. All regressions include year and industry fixed effects. Standard errors are clustered by firm.

, **, and * indicate two-sided significance at the 1%, 5%, and 10% levels, respectively.

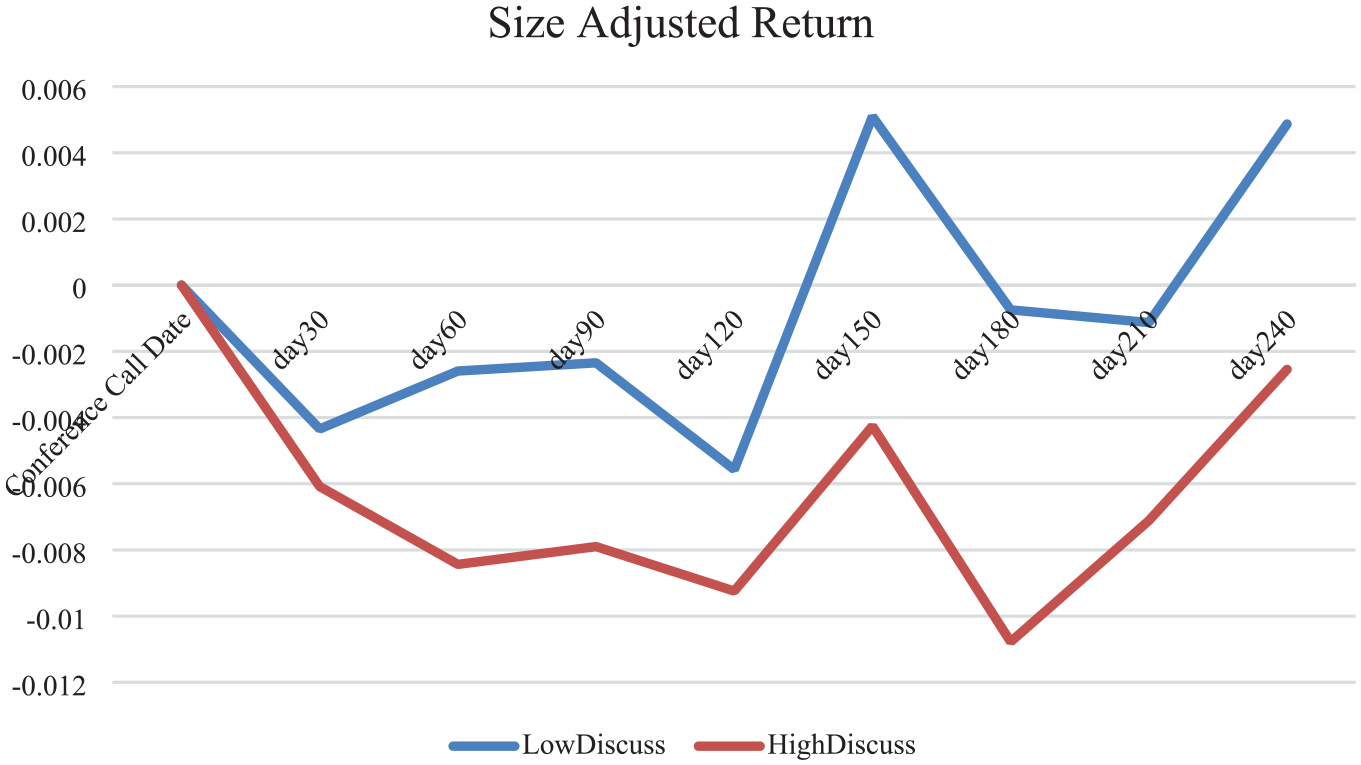

Post-Conference Call Returns

Our main findings show that a greater amount of environmental discussion in conference calls is associated with lower firm value and a higher cost of capital, which suggests that an investment in a portfolio of high-discussion firms would perform worse than an investment in low-discussion firms. To test the relation between the amount of environmental discourse and market return explicitly, we create two portfolios based on the amount of environmental discourse and use size-adjusted returns as the basis for comparison. 26 One portfolio consists of the firms with relatively less environmental discussion (bottom 50% by industry and year), and the other portfolio consists of the firms with relatively more environmental discussion (top 50% by industry and year). Exhibit 4 shows that the return on the less-discussion portfolio is consistently higher than that on the more-discussion portfolio. 27 Together with the results in Tables 6 and 7, our findings imply that placing more emphasis on environmental topics in conference calls is costly, especially for firms with worse environmental performance.

Environmental Discourse and Returns.

General ESG and CSR Discourse

For comparative purposes, we supplement our main analysis of environmental discourse with additional analysis of more general ESG and CSR discourse. (By “general,” we mean not solely and specifically focused on environmental matters.) Appendix C provides two illustrative excerpts from conference calls—one of general ESG discussion and one of environmental discussion. In one call, the speaker mentions Social and Governance topics three times, that is, “human rights” once and “safety” twice. In another call, the speaker talks about the environment three times, mentioning “planet,”“renewable,” and “recycled.”

It is reasonable to expect that the value relevance of social and governance discourse in firms’ conference calls differs from that of environmental discourse. The value of operational and investment activities addressing social topics (e.g., increasing workforce diversity) or governance topics (e.g., anticorruption programs) may be generally more difficult to assess than operational and investment activities addressing environmental topics (e.g., re-engineering products and processes to decrease emissions) because there is a lack of objective benchmarks for what constitutes fair social or governance practices. In contrast, the credibility and transparency of environment-related topics can be assessed against the TRI metric, an objective measure reported by the EPA about firms’ pollution levels.

To explore potential differences in the valuation impact of general ESG and CSR discourse in conference calls, we estimate Equations 1 and 2 substituting the measure of general ESG discourse for the measures of environment-specific discourse. Results in Table 8 show a positive relation between share price and general ESG discourse across the entire call, the remarks portion, and the Q&A portion. Results in Table 9 show a negative relation between cost of capital and general ESG discourse across the entire call, the remarks portion, and the Q&A portion. In contrast with our main results about environmental discourse, these results indicate a more favorable valuation impact of general discussions of social and governance issues. Unlike prioritization of the environment, prioritization of other types of socially responsible activities likely yields firm-specific benefits without the commensurate capital investments required by environmentally responsible operations.

Results of Regression of Share Price on General ESG Discourse.

Note. This table presents coefficients and t-statistics in parentheses from pooled regression of the dependent variable Share Price, on the independent variables listed. Share Price is the company’s closing market value per share measured 10 months after fiscal year end. ESGDiscourse denotes the keyword count of general ESG-related disclosure in the whole conference call, while ESGDiscourse_remarks and ESGDiscourse_qa, respectively, represent the frequency of general ESG-related keywords in the prepared remarks portion and Q&A portion of the conference call. Detailed variable definitions are provided in Table 2. All regressions include year and industry fixed effects. Standard errors are clustered by firm.

, **, and * indicate two-sided significance at the 1%, 5%, and 10% levels, respectively.

Results of Regression of Cost of Capital on General ESG Discourse.

Note. This table presents coefficients and t-statistics in parentheses from pooled regression of the dependent variable COC, on the independent variables listed. COC is the implied cost of equity capital (in percentage) in 10 months after fiscal year end, estimated using the Easton (2004) MPEG model. ESGDiscourse denotes the keyword count of general ESG-related disclosure in the whole conference call, while ESGDiscourse_remarks and ESGDiscourse_qa, respectively, represent the frequency of general ESG-related keywords in the prepared remarks portion and Q&A portion of the conference call. Detailed variable definitions are provided in Table 2. All regressions include year and industry fixed effects. Standard errors are clustered by firm.

, **, and * indicate two-sided significance at the 1%, 5%, and 10% levels, respectively.

Conclusion

The amount of environmental discussion increased substantially from 2006 to 2020, and the amount of such discourse in the prepared remarks portion of conference calls consistently exceeds the amount of discourse in the Q&A portion of the calls. Treating the amount of discourse as an empirical proxy for prioritization, our analysis indicates that a greater amount of environmental discourse is associated with lower share price and higher cost of capital. Results suggest relatively higher costs of environmentally responsible actions. In additional analysis, we find that the relation between firm value and environmental discourse during conference calls is more pronounced for firms that prioritize the environment but have worse environmental performance proxied by industry-adjusted emissions. We also find that a portfolio of firms with greater amounts of environmental-specific discussion in conference calls experience lower returns than a portfolio of firms with lesser amounts of discourse. Overall, these results are consistent with prioritization of environmental issues in conference calls implying firm-specific costly investments for environmentally responsible operations that yield non–firm-specific benefits. In contrast, unlike prioritization of environmental issues, the prioritization of non-capital intensive social and governance issues in conference calls is associated with higher share price and lower cost of capital, highlighting the different economic implications of socially responsible priorities.

Footnotes

Appendix A. Environmental Keyword List C

| Alternative energies | Environmentally | Polluting |

| Alternative energy | Euro 6 | Recoverable |

| Biofuels | Euro 7 | Recyclable |

| Biomass | Global warming | Recycle |

| Biopower | Green development | Recycled |

| Bioprocessing | Green electricity | Recycling |

| Bioproduct | Green energy | Reduces ethylene |

| Bioproducts | Green innovation | Reducing flaring |

| Carbon | Green transformation | Reforestation |

| Carbon(-|–)neutral | Greenhouse gas | Renewable |

| Circular economy | Greenhouse gases | Renewables |

| Clean energy | Hydrocarbons | Reusable |

| Clean gas | Hydropower | Scope 3 |

| Clean technology | ISO 14000 | Solar |

| Cleanup | ISO 26000 | Spills |

| Climate action | Landfill | Substantially green |

| Climate change | Low(-|–)carbon | Superfund |

| Climate goals | Lower(-|–)carbon | Sustainability |

| Climate reporting | Methane reduction | Sustainable agricultural practices |

| CO2 | National Energy Strategy | Sustainable development goals |

| CO2(-|–)neutral | Ozone(-|–)depleting | Sustainable packaging |

| Conservation | Paris Agreement | Sustainable products |

| Decarbonization | Paris climate change | Sustainably managed |

| Decarbonize energy | Paris climate goals | Waste |

| Eco ideas | Paris goals | Waste(-|–)free |

| Eco solutions | Planet | Wind business |

| Emission | Pollutant | Wind capacity |

| Emissions | Pollutants | Wind energy |

| Energy efficiency | Pollute | Wind power |

| Energy efficient | Pollutes | WLTP certification |

| Environmental | Polluted | Zero(-|–)carbon |

Appendix B. General ESG Keyword List

| Anti(-|–)corruption | Global reporting initiative | Safely |

| Code of conduct | Governance | Safety |

| Corporate citizenship | Human rights | Social agenda |

| Corporate responsibility | Impact on society | Social welfare |

| Corporate social responsibility | Integrity | Societal benefit |

| CSR | Prevent discrimination | Societal impact |

| Diversity and inclusion | Reputation | Societal license |

| ESG | Respect for the rules | Society impact |

| Ethical | Responsible company | UN Global Compact |

| Ethics | Responsible corporate citizen |

Appendix C

Appendix D Excerpts From Conference Calls

These excerpts were selected based on an examination of the transcripts of conference calls for a subsample of firms with the highest proportion of environmental discourse in the Q&A portion of the call. The subsample consisted of 50 transcripts (5 from each of 10 industries where the Q&A portion of the transcript contains the highest proportion of environmental-related content). These excerpts illustrate the qualitative nature of the discourse between executives and analysts about environmental topics.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability

Data used in this study are available upon request.