Abstract

This study examines how the forward-looking Management Discussions and Analysis (MD&A) disclosure affects Merger and Acquisition (M&A) outcomes. Based on a sample of U.S. public firms for the period 1997–2018, we find that firms with more forward-looking information in MD&As are more likely to become M&A targets. The combined returns of the acquirer and the target around the deal announcement are higher in deals involving target firms with more forward-looking MD&A disclosures. The positive effects on M&A outcomes are more pronounced when forward-looking disclosures are deemed more credible and the underlying meanings are expressed more articulately, regardless of the tone. Targets with more forward-looking disclosures are associated with lower bid premiums, higher acquirer returns, and superior acquirer post-acquisition performance, measured by long-term buy-and-hold returns and financial improvements. Our results, robust to quasi-natural experiments and alternative measures, highlight the role of forward-looking information in reducing uncertainty and improving M&A efficiency.

Introduction

Mergers and Acquisitions (M&As) are essential economic activities in capital markets. The number and volume of M&A deals have grown exponentially over the past several decades. The number of M&A deals was just over 10,000 in 1990 and increased to over 57,000 in 2021, with a total value of over $5.2 trillion. 1 M&As, aligned with corporate-level strategies, are among firms’ most crucial capital allocation decisions. They are usually economically significant (Netter et al., 2011) and have vital implications for firms’ strategic competitiveness, various stakeholders, and corporate governance.

Acquirers assess and screen prospective target firms through a due diligence process and gather public information of the targets (Kim et al., 2020; Skaife & Wangerin, 2013). Information uncertainty about the financial position of the targets and the expected deal quality presents a substantial barrier to M&A activities. Hence, many studies examine how target firms’ information disclosure affects M&A decisions. These studies show that information quality plays a significant role in both the U.S. (McNichols & Stubben, 2015; Skaife & Wangerin, 2013) and global M&As (Francis et al., 2016). However, these studies typically focus on historical information on target firms’ disclosures. Despite the importance of forward-looking information in predicting prospects after acquisitions, little research has investigated the consequences of forward-looking information disclosure in M&A activities.

To fill this research gap, this study examines whether forward-looking information in the Management Discussion and Analysis (MD&A) of potential targets affects M&A outcomes. The MD&A section is an essential component of annual reports. While financial statements include historical information and are audited by external auditors, the MD&A section is more flexible and narrative. The Securities and Exchange Commission (SEC) mandates that the MD&A section includes managerial commentary on trends and events expected to materially affect liquidity, capital resources, and future operations (SEC, 2003). This requirement provides a channel for managers to describe their perspectives of the firm, such as prospects and strategic plans, in the MD&A section. The recent SEC amendments to the MD&A disclosure rules reiterate that “the development of MD&A disclosure…is important to providing investors and others an accurate understanding of the company’s current and prospective financial position and operating results” (SEC, 2020). Forward-looking disclosures in the MD&A section may contain information relevant to outsiders. Li (2008) finds that the tone of forward-looking disclosures in MD&As has significant predictive power for future financial outcomes. Cho and Muslu (2021) suggest that forward-looking MD&A disclosures help improve the information environment. Hence, we predict that forward-looking MD&A disclosures increase the visibility of targets and enhance acquirers’ information sets. However, the credibility of forward-looking MD&A disclosures is a concern because they are not immediately verifiable or audited (Athanasakou & Hussainey, 2014). Managers have both incentives and discretion regarding the content (Athanasakou & Hussainey, 2014) and the tone of such disclosures (Schleicher & Walker, 2010). This is even true under safe harbor protection, which shields firms’ forward-looking statements from legal liabilities (Cazier et al., 2020). Therefore, the role of the target’s forward-looking disclosure in M&A decisions remains an empirical question.

We recognize that MD&A is not the only channel for communicating forward-looking information. However, our study focuses on the MD&A section rather than other completely voluntary channels, such as conference calls, due to its semi-voluntary nature. This unique characteristic allows firms to tailor disclosures to their strategic communication needs while adhering to regulatory guidelines, making MD&A an insightful channel for examining forward-looking information. Although firms may face litigation risks when including forward-looking details in 10-K filings (Rogers et al., 2011), their willingness to disclose such information despite these risks may signal higher transparency. In contrast, entirely voluntary channels, such as conference calls, often involve real-time interactions and only available for some firms. By comparison, 10-K filings provide a standardized format accessible to all firms, enhancing the generalizability of our analysis. 2

We examine the research question using a sample of U.S. listed firms from 1997 to 2018. Our baseline results support the view that forward-looking MD&A disclosures provide information relevant to M&A investment decisions. First, forward-looking information in MD&As significantly enhances a prospective target firm’s visibility. Specifically, a one-standard-deviation increase in a firm’s forward-looking MD&A disclosures increases the likelihood of receiving an M&A bid by 11.22%. Second, deals based on more forward-looking MD&A disclosures are associated with higher acquisition synergy. A one-standard-deviation increase in forward-looking intensity above its mean is associated with a 12.68% increase in the combined deal announcement returns between the acquirer and target. To address endogeneity concerns and establish causality, we leverage two quasi-natural experiments: safe harbor provisions and the SEC’s amendments to Regulation S-K. These experiments strengthen the evidence of a causal relationship between forward-looking MD&A disclosures and M&A outcomes. The above effects still hold after controlling for target’s financial reporting quality and alternative information sources of forward-looking information, such as earnings announcements, management forecasts, conference calls, and non-GAAP earnings. Additionally, a falsification test using narrative historical information mitigates the concern that historical information in the MD&A section drives our results. The results are also robust to alternative measures of forward-looking information.

The positive effects of forward-looking MD&A disclosures on M&A outcomes differ cross-sectionally. The effects are more pronounced when (i) the forward-looking MD&A disclosures are more credible (the potential targets provide more accurate management forecast and are subject to more rigorous monitoring by institutional shareholders and financial analysts), and (ii) the forward-looking MD&A disclosures are expressed in a more articulate manner, employing more definitive tone and greater readability, though the direction of tone appears irrelevant. These results support the notion that forward-looking information enhances the transparency of target firms and thereby influences M&A outcomes. We also explore whether and how forward-looking MD&A disclosures affect deal characteristics. We document that forward-looking information in MD&A is associated with a lower bid premium, a lower probability of a negotiation deal, and higher announcement returns for the acquirer shareholders but insignificant announcement returns for the target shareholders. Moreover, we find that forward-looking information in MD&A is associated with positive post-acquisition performance in terms of long-term buy-and-hold returns and financial performance. Taken together, these results further explain the high acquisition synergy observed (Raman et al., 2013). Next, we investigate the horizon of forward-looking information and find that short-term forward-looking primarily drive our findings. Finally, we analyze changes in MD&A forward-looking disclosures for target firms involved in merger buzz, comparing the year before and after deal announcements across subgroups categorized by deal completion and competition levels between acquirers and targets. This sheds light on whether firms strategically increase forward-looking disclosures to enhance acquisition appeal while balancing proprietary costs.

This study contributes to existing literature in several ways. First, it deepens our knowledge the informational role of narrative disclosures in general and MD&A disclosures in particular. Narrative disclosures provide credible and valuable decision-relevant information (Francis et al., 2002; Kim et al., 2023). They are essential for understanding human behavior’s motivations and economic impacts (Shiller, 2017) and providing value-relevant information to outside equity investors (Li, 2010). Beyer et al. (2010) show that the corporate disclosure’s linguistic (as opposed to numerical) component is a potentially essential and complementary source of firm-specific information relevant to outsiders. The recent literature has found that a firm can use other firms’ MD&A narratives for investment decisions. For example, a peer’s MD&A narratives change a firm’s capital investment, inventory decisions (Cho & Muslu, 2021), and investment efficiency (Durnev & Mangen, 2020). We extend this stream of literature by showing that a firm’s MD&A disclosure can be relevant to another firm, a potential acquirer in our setting. However, narrative disclosures are usually evaluated in terms of readability (Li, 2008), disclosure quality (Chen et al., 2019), disclosure similarity (Brown & Tucker, 2011), and tone (Durnev & Mangen, 2020; Hanley & Hoberg, 2010). Our study focuses on the narrative forward-looking information, which is particularly important for investment decisions. We supplement existing studies (Bochkay & Levine, 2019; Muslu et al., 2015) by showing how forward-looking information affects other firms’ acquiring decisions.

Second, we extend the current understanding of M&A decisions. As vital corporate investment decisions, M&As have attracted the attention of practitioners and academia. The existing literature demonstrates various information-related factors that improve the efficiency of M&A decisions, including the availability of private targets’ financial statements (Chen, 2019), targets’ accounting quality (Marquardt & Zur, 2015; McNichols & Stubben, 2015), readability of target firms’ annual reports (Balachandran et al., 2025), information flow facilitated by common auditors between acquirers and targets (Cai et al., 2016; Dhaliwal et al., 2016), and the PCAOB inspections on target firms’ auditors (Kim et al., 2020). This study adds to the literature by redirecting the focus to the usefulness of forward-looking information in M&A decisions.

Third, prior research shows that specialized M&A staff (Gokkaya et al., 2023), shared auditors (Cai et al., 2016), shared analysts (Cortes & Marcet, 2023), and external regulators (Johnson et al., 2023) can alleviate uncertainties and are associated with higher synergy. We join and supplement this stream of literature on how a target’s forward-looking MD&A disclosures help generate higher acquisition synergy. In our primary analyses, we focus on synergy, rather than acquirer returns, to evaluate overall value creation in M&As. According to the auction theory (Martin & Shalev, 2017), the availability of target information reduces bidders’ uncertainty about the target’s common value, enhancing bidders’ reliance on synergistic gains and improving acquisition efficiency. Thus, rather than the potential wealth transfer from target shareholders to acquirer shareholders, we emphasize the effect of target information in expanding the overall size of the pie, which is crucial for resource allocation efficiency in the market for corporate control. Our further analysis of the distribution of wealth between acquirer and target shareholders shows that the acquisition synergy is enjoyed by the acquirer shareholders only.

The remainder of this paper is organized as follows. The next section reviews the relevant literature and develops the research hypotheses. Following this, we describe the sample, data, and descriptive statistics. The section “Empirical Analysis” presents the model specifications and empirical results. The last section presents our concluding remarks.

Literature Review and Hypothesis Development

Firms make various investment decisions, among which the M&A decision is most critical due to its significant implications for stakeholders, corporate governance, and capital allocation. Multiple factors complicate and drive the acquisition decision (Yaghoubi et al., 2016), which typically involves a dynamic process that lasts from months to years. A typical M&A deal begins with identifying potential target candidates that fit the strategic objectives, followed by a preliminary screening of the candidates. The acquirer then conducts a lengthy due diligence process, which provides an extensive understanding of the target and forms the basis of target valuation and potential synergies (Koller et al., 2010). A lengthy M&A process involves significant uncertainties, which may adversely affect acquisition outcomes (Bonaime et al., 2018; Chen et al., 2024). According to the real options theory, firms postpone their M&A activities in response to economy-wide political uncertainty (Bonaime et al., 2018), individual firm-specific political uncertainty (Chen et al., 2024), and cash flow uncertainty (Garfinkel & Hankins, 2011). The existing literature finds that the target’s information disclosure and accounting quality help alleviate information uncertainties and improve M&A efficiency (Marquardt & Zur, 2015; McNichols & Stubben, 2015; Raman et al., 2013; Skaife & Wangerin, 2013). Nevertheless, these studies primarily concentrate on historical information disclosed by target firms. In contrast, we examine how forward-looking information alleviates the adverse effects of uncertainty on M&As.

Research on forward-looking information typically focuses on earnings forecasts and MD&A disclosures (Bochkay & Levine, 2019; Bozanic et al., 2018; Chen et al., 2019). In an M&A setting, acquirers need comprehensive information rather than just earnings-related information. As Davis and Tama-Sweet (2012) mention, MD&A provides incremental information on earnings announcements instead of merely rehashing information found elsewhere. Arguably, it is the most widely read section beyond financial statements (Li, 2010). Supporting this, Bernard et al. (2020) document that bidders actively download target firms’ SEC filings around M&A announcements, suggesting that MD&A in 10-K reports could also be an important resource for acquirers. As an integral section of the 10-K filing, the MD&A section (Item 7) is expected to provide a narrative explanation of known trends, events, commitments, plans, and uncertainties that are likely to affect a company’s liquidity, capital resources, and future operations (SEC, 2003). The MD&As are intended to provide (1) a narrative explanation of a company’s financial statements and other statistical data and (2) management with the flexibility to describe the financial matters impacting the registrant (SEC, 2008).

Although a required section of an annual report, the SEC does not mandate the format and content of MD&A disclosures. Forward-looking disclosures in MD&As, usually narrative, describe factors that may materially affect a company’s operations based on managers’ perceptions. As the examples in online Appendix A show, the format and content of the disclosures are flexible. Firms may discuss various issues, such as operation-related factors, economy-wide factors, and policy uncertainties. Extant literature documents that forward-looking information improves the information environment and is value-relevant for outside investors. This line of research provides evidence that forward-looking MD&A disclosures are associated with more informative future performance, more relevant valuation (Muslu et al., 2015), and more accurate earnings forecasts than quantitative financial variables (Bochkay & Levine, 2019). Forward-looking information also influences firms’ operational-level resource allocation decisions regarding sales target setting (Bouwens & Kroos, 2017), cost elasticity (Chen, Kama, & Lehavy, 2023), peer firms’ capital investment and inventory decisions (Cho & Muslu, 2021), and rivals’ real investment decisions and investment efficiency (Durnev & Mangen, 2020). We expect potential target’s forward-looking information to influence the acquirer’s decisions in an M&A setting.

Forward-looking disclosures in MD&As can provide decision-relevant information for acquirers in different phases. First, managers may portray business plans in MD&As. Such forward-looking information can enhance visibility by reducing acquirers’ information-searching costs when identifying potential targets. In other words, acquirers can judge the strategic fitness of a potential deal more easily. Second, in the due diligence process, acquirers obtain significant information from the perspectives of potential targets’ operational, financial, and legal status quo. Forward-looking MD&A disclosures provide hints regarding due diligence. The acquirer can then cross-verify information from other sources, mitigating the target’s information uncertainty at relatively low searching costs. Following this argument, we expect firms with more forward-looking MD&A disclosures to be more likely identified as potential targets. Therefore, our first hypothesis is as follows:

The quantity of forward-looking MD&A disclosure is positively associated with the probability of receiving a bid.

Forward-looking information can also influence the valuation of expected synergies. Existing literature indicates that uncertainty negatively affects acquirer announcement returns and post-acquisition performance (Bonaime et al., 2018; Chen and Kim et al., 2023). More firm-specific target information improves acquirer returns and the expected value of the combined firms. Previous research has investigated whether and how accounting information improves acquisition decisions. This line of research finds that acquirers can more precisely evaluate a target with high financial reporting quality (Skaife & Wangerin, 2013), high accounting quality (McNichols & Stubben, 2015), and private targets that mandatorily disclose their financial statements (Chen, 2019). Another line of research documents positive acquisition announcement returns when financial intermediaries deemed to reduce information asymmetry are involved in the M&A process (Cai et al., 2016; Cortes & Marcet, 2023; Dhaliwal et al., 2016; Kim et al., 2020) and specialized M&A staff are employed (Gokkaya et al., 2023). The above research shows that financial and general information sharing help improve deal valuation. MD&A disclosures are more flexible than financial statement disclosures and can be used by managers to supplement audited financial statements (Brown et al., 2024). Thus, we expect forward-looking information to lessen the information uncertainty of the target and to improve post-acquisition performance. Therefore, we propose the following hypothesis:

The quantity of forward-looking MD&A disclosure is positively associated with the acquisition synergy.

However, the above hypotheses are not without tension. One may argue that the forward-looking information in MD&As can be ineffective for the following reasons. First, MD&As are not subject to audits and lack credibility. Generally, the auditor’s responsibility for MD&As is limited to reading them to identify material inconsistencies in the audited financial statements (AICPA, 2010). Second, the SEC does not specify the format and content of MD&A disclosures. Thus, they may include boilerplate disclaimers and disclosures, generic languages, and immaterial details (SEC, 2003). Some managers may use repetitive disclosures over time (Li, 2019). Therefore, forward-looking MD&A disclosures may not be as informative as expected. Third, managers may be reluctant to issue specific projections because they may be held accountable later (Healy & Palepu, 2001). Thus, they are willing to issue forward-looking information as long as they have control over the metrics they disclose (Bozanic et al., 2018), discouraging managers from revealing decision-relevant information in MD&As.

Sample and Model Specification

Sample

Sample Description

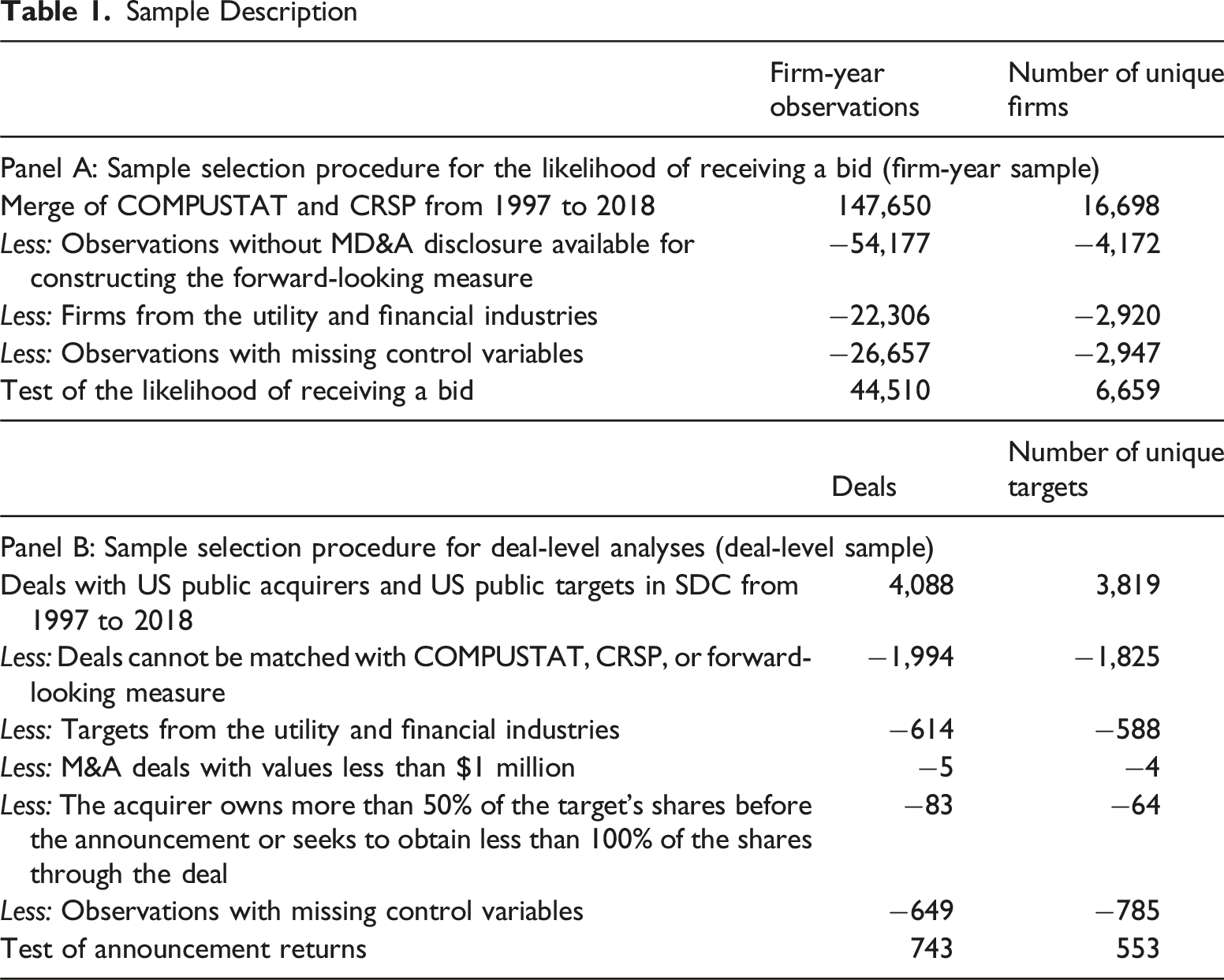

H2 examines the acquisition synergy associated with enhanced forward-looking information. Therefore, a deal-level sample is employed to test it. Panel B of Table 1 presents the sample screening procedure. We begin with deals with U.S. public acquirers and targets in SDC during the sample period. Deals that do not match Compustat, the CRSP, or forward-looking measures are excluded. Following prior literature, we discard deals with targets from financial or utility industries and deals with a value of less than $1 million. We require the acquirer to control less than 50% of the target before the announcement and to seek 100% of the shares through the deal. After dropping observations with missing control variables, we obtain a sample of 743 deals of 553 unique firms.

Measuring Forward-Looking MD&A Disclosures

Following Muslu et al. (2015), we download 10-K reports from the websites of Loughran and McDonald, who follow the procedure outlined in online Appendix B to parse these reports. 4 Next, the JAVA program is used to extract the MD&A sections. 5 After extracting the MD&A section from 10-K filings, we construct forward-looking MD&A disclosures using the following two steps. First, we parse the MD&A documents at the sentence level, following Muslu et al. (2015), as a sentence is the smallest integral unit of text. We tag a sentence in the MD&A section as forward-looking if it includes one or more forward-looking keywords or conjugations, according to the forward-looking word list developed by Muslu et al. (2015). Sentences referencing a year after the filing are also identified as forward-looking. Second, we construct the key variables, namely, forward-looking sentences (FLS) and forward-looking intensity (FLI). FLS is the logarithm of one plus the number of forward-looking sentences in the MD&A section. FLI is the number of forward-looking sentences in the MD&A section divided by the number of sentences in the annual report’s MD&A section. In other words, FLI (FLS) captures forward-looking information in relative (absolute) terms. Thus, we use FLI throughout the analysis because it implicitly controls for the total information content of MD&A. The results using FLS are also provided for robustness checks.

Model Specification: Likelihood of Receiving a Bid

We use the following probit model to investigate the impact of the forward-looking MD&A disclosures of prospective target firms on the likelihood of being targeted based on the firm-year sample:

Following prior studies, we control for several firm-level control variables related to the probability of a firm receiving a bid. First, we include a proxy for managerial effectiveness, measured by the market-adjusted one-year cumulative abnormal return (CAR), as Dhaliwal et al. (2016) predict that managerial ineffectiveness increases the probability of receiving a bid. Second, prior studies predict that firms with an imbalance between growth opportunities and financial resources and illiquid and leveraged firms are more likely to be targets (e.g., Ambrose & Megginson, 1992). Hence, we include a growth-resource “mismatch” indicator (GR_DUMMY), sales growth (SGROWTH), and two proxies of financial constraints (LIQUIDITY and LEVERAGE) as control variables. Third, because acquisition activity clusters in time and industry, we include an indicator (INDBIDS) that equals one if there was a bid in an industry in the previous year, and zero otherwise. Fourth, since small firms lack the resources to bid for the large firms, we control for the effect of firm size, as measured by the natural logarithm of a firm’s book value of total assets (SIZE). Fifth, we control for the effect of firm value, measured by a firm’s market-to-book ratio (MB) and price-to-earnings ratio (PTE), as relatively undervalued targets make good acquisition targets. Sixth, we control for the effects of profitability and investment as measured by a firm’s return on assets (ROA) and investment intensity (INVEST). Seventh, we control for the effect of accounting quality (AQ), as takeover decisions are influenced by the quality of accounting information. Finally, we include industry-fixed effects and year-fixed effects to control for industry and time variations in the probability of receiving a bid.

Model Specification: Acquisition Synergy

H2 investigates whether forward-looking MD&A disclosures enhance acquisition synergy because of increased information disclosure. To test it, we estimate the following ordinary least squares (OLS) regression on the deal-level sample:

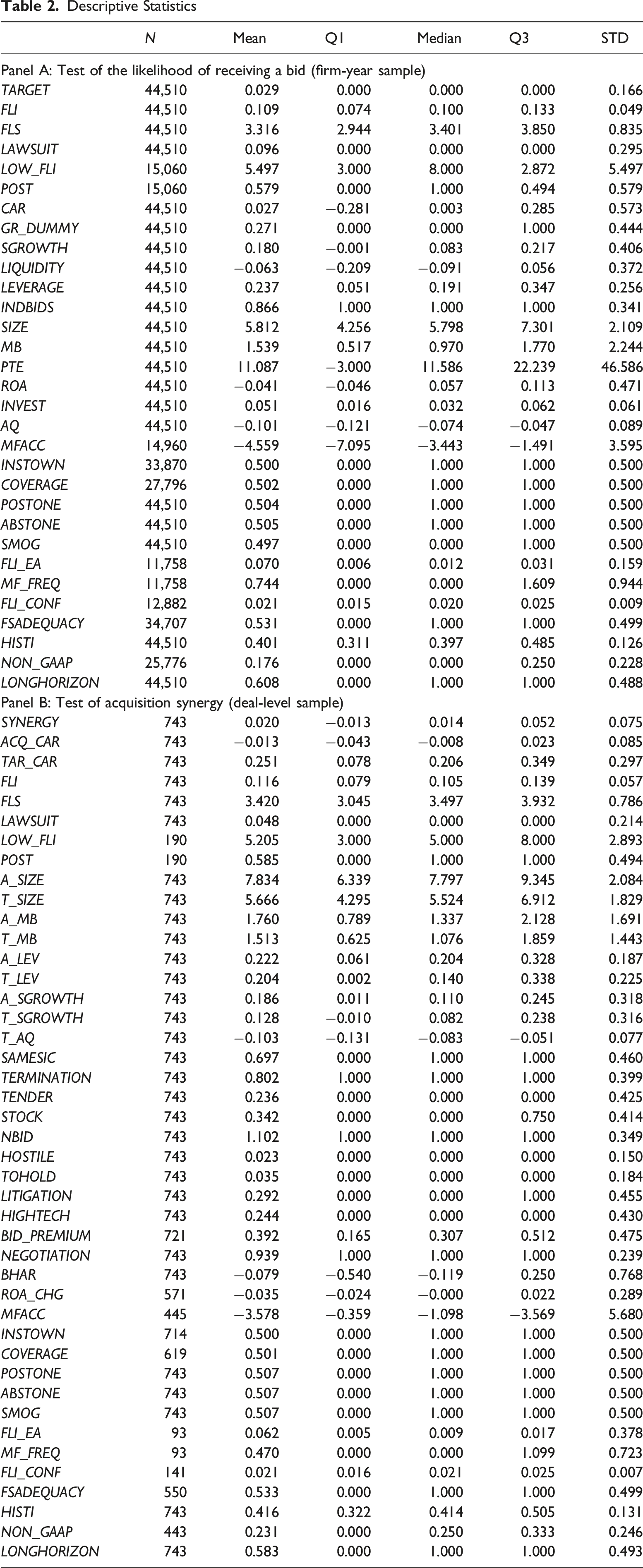

Descriptive Statistics

Descriptive Statistics

The following characteristics are observed. Most sample deals involve acquirers and targets from the same industry (69.7%) and include termination fees (80.2%). The frequency of hostile takeovers is low (2.3%). Only 3.5% of acquirers hold equity ownership before the deal. Approximately 29.2% of the targets operate in high-litigation-risk industries, and about one-quarter of the targets belong to high-tech industries. On average, the acquirers are larger, higher priced, more leveraged, and have greater growth potential than the targets.

Empirical Analysis

Forward-Looking MD&A Disclosures and Likelihood of Receiving a Bid (H1)

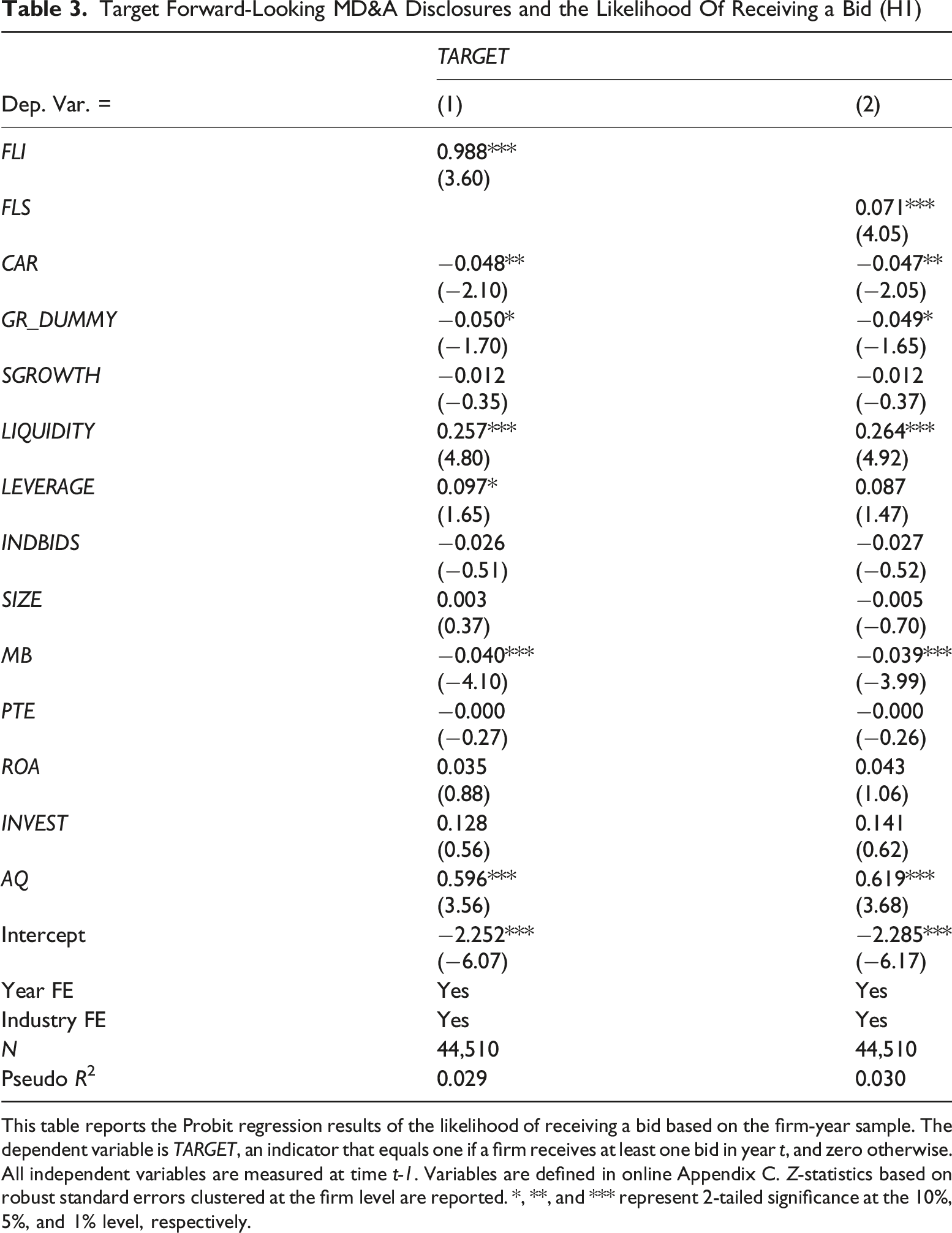

Target Forward-Looking MD&A Disclosures and the Likelihood Of Receiving a Bid (H1)

This table reports the Probit regression results of the likelihood of receiving a bid based on the firm-year sample. The dependent variable is TARGET, an indicator that equals one if a firm receives at least one bid in year t, and zero otherwise. All independent variables are measured at time t-1. Variables are defined in online Appendix C. Z-statistics based on robust standard errors clustered at the firm level are reported. *, **, and *** represent 2-tailed significance at the 10%, 5%, and 1% level, respectively.

Regarding the control variables, we find that firms with higher managerial effectiveness, larger size, and undervalued are more likely to receive M&A bids. Firm’s accounting quality increases the probability of being a target, supporting the incremental effect of forward-looking information. However, inconsistent with predictions, growth-resource “mismatch” decreases the probability of receiving a bid. Although leveraged firms are more likely to be targeted, illiquid firms are less likely, indicating that the effect of financial constraints is uncertain. These results are generally consistent with those of prior studies (Dhaliwal et al., 2016).

Forward-Looking MD&A Disclosures and Acquisition Synergy (H2)

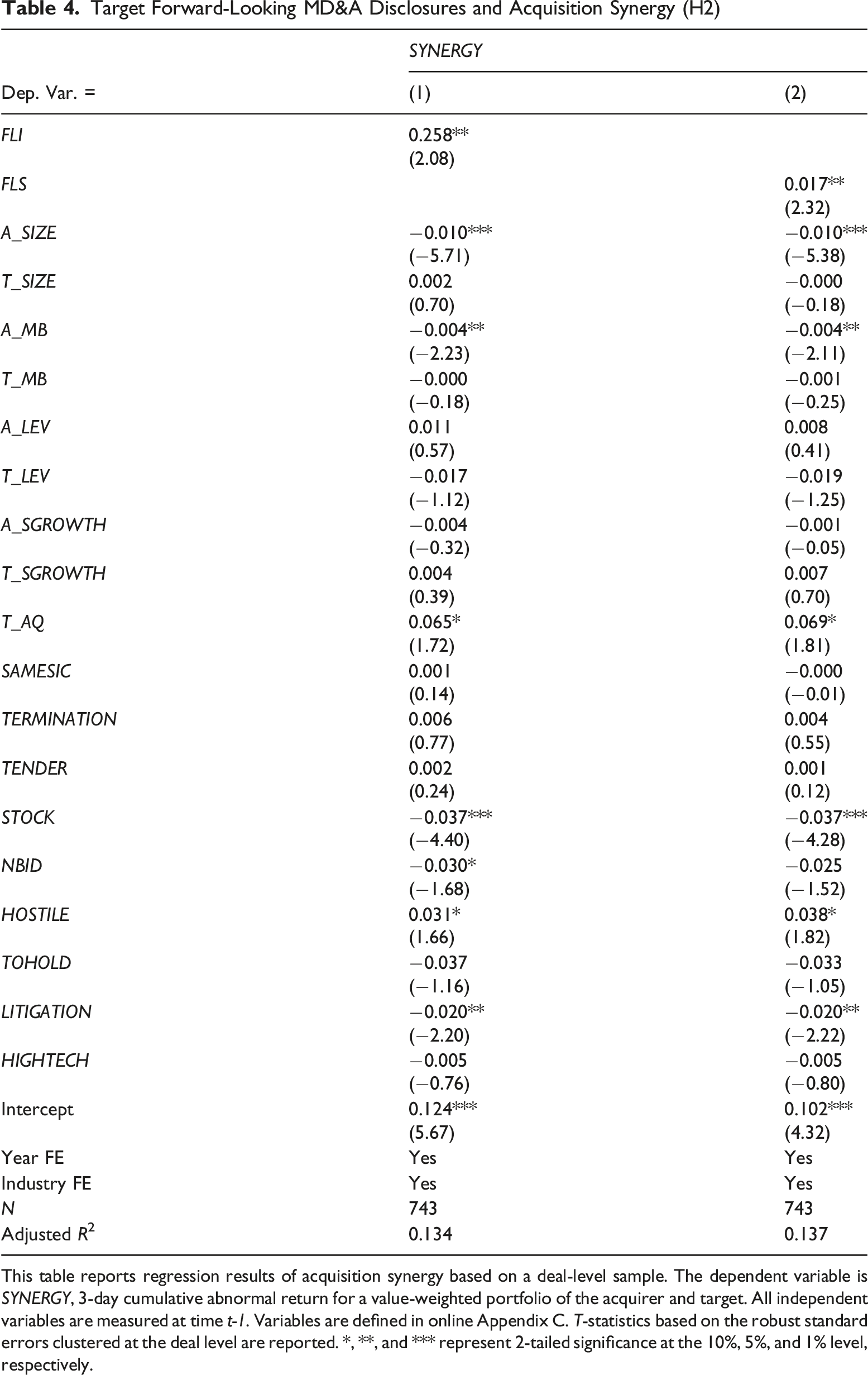

Target Forward-Looking MD&A Disclosures and Acquisition Synergy (H2)

This table reports regression results of acquisition synergy based on a deal-level sample. The dependent variable is SYNERGY, 3-day cumulative abnormal return for a value-weighted portfolio of the acquirer and target. All independent variables are measured at time t-1. Variables are defined in online Appendix C. T-statistics based on the robust standard errors clustered at the deal level are reported. *, **, and *** represent 2-tailed significance at the 10%, 5%, and 1% level, respectively.

The following results for the control variables are noteworthy. First, expected synergies are lower when acquirers are larger, as managers of larger corporations are more likely to be entrenched and, thus, more likely to make value-destroying acquisitions (Moeller et al., 2004). Second, consistent with Bradley et al. (1988), our results indicate that the expected synergies are higher when the targets are larger. Third, stock deals are negatively associated with expected synergies on the acquisition date because a bidding firm offers stock to finance an acquisition when it believes it is overvalued (Myers & Majluf, 1984) and overvalued acquirers engage in poorer acquisitions due to the agency costs of overvalued equity (Jensen, 2005). Fourth, litigation risk decreases expected synergies (Bates & Lemmon, 2003). Finally, accounting quality improves the expected synergies, consistent with McNichols and Stubben’s (2015) finding that accounting information reduces uncertainty and facilitates a more precise valuation of the target.

Tables 3 and 4 provide evidence for our hypotheses and support the positive role of forward-looking MD&A disclosures in facilitating acquisition outcomes with respect to a higher likelihood of receiving a bid (H1) and greater synergy (H2). The results remain robust regardless of whether the quantity of forward-looking information is measured in relative (FLI) or absolute terms (FLS). In the remaining analyses, we report results using FLI for brevity. 6

Quasi-Natural Experiments

The present analysis relates the target’s forward-looking MD&A disclosures to the acquirer’s decisions. In addition, we employ a lead-lag research design. Therefore, reverse causality is less likely to be a concern. However, one may concern that our forward-looking disclosure measure captures unobservable factors that drive both the target’s disclosure decision and the acquirer’s acquisition decision. We employ two quasi-natural experiments to address this potential concern.

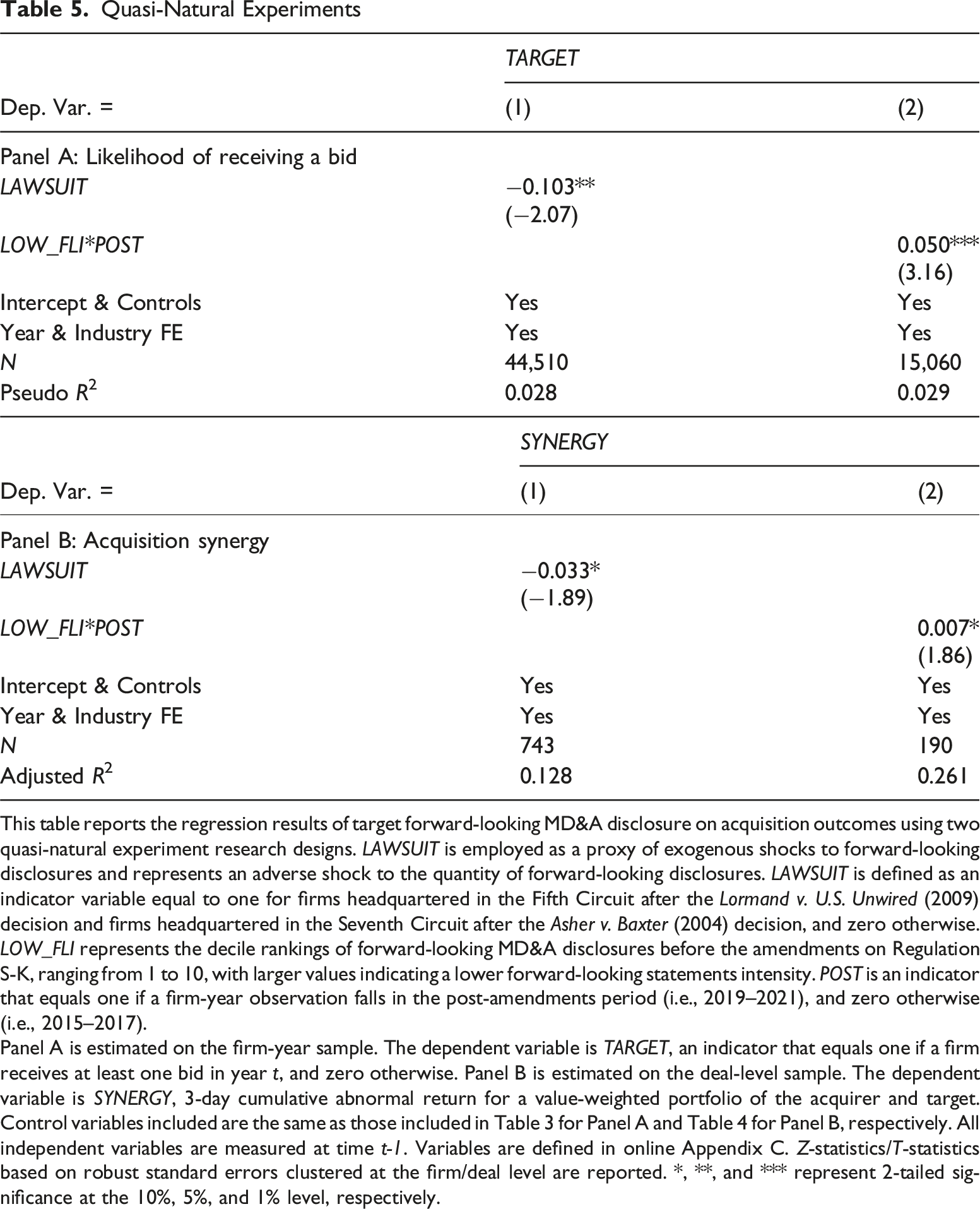

The first natural experiment utilizing variations in safe harbor protections. Firms are reluctant to disclose forward-looking information because they believe that such disclosures expose them to litigation, which brings high costs to fight in court (Skinner, 1995). Thus, federal securities laws have provided safe harbor provisions to encourage the disclosure of qualitative forward-looking statements since the enactment of the Private Securities Litigation Reform Act of 1995 (PSLRA). Johnson et al. (2001) find that safe harbors significantly increase firms’ disclosure of quantitative forward-looking information with no adverse impact on the quality of such information. However, safe harbor protections differ across federal circuits because the efficacy of practice relies on judicial interpretation and enforcement. 7 Following Cazier et al. (2020), we identify court rulings of two cases representing circuit splits to safe harbor provisions: Asher v. Baxter International, Inc., 377 F. 3d 727 (2004) of the Seventh Circuit Court of Appeals and Lormand v. U.S. Unwired, Inc., 565 F. 3d 228 (2009) of the Fifth Circuit Court. Relative to other circuits, these two decisions should result in significantly lower safe harbor protection for firms headquartered in the Seventh and Fifth Circuits, and such litigation risk would discourage firms from providing forward-looking disclosures. 8

Quasi-Natural Experiments

This table reports the regression results of target forward-looking MD&A disclosure on acquisition outcomes using two quasi-natural experiment research designs. LAWSUIT is employed as a proxy of exogenous shocks to forward-looking disclosures and represents an adverse shock to the quantity of forward-looking disclosures. LAWSUIT is defined as an indicator variable equal to one for firms headquartered in the Fifth Circuit after the Lormand v. U.S. Unwired (2009) decision and firms headquartered in the Seventh Circuit after the Asher v. Baxter (2004) decision, and zero otherwise. LOW_FLI represents the decile rankings of forward-looking MD&A disclosures before the amendments on Regulation S-K, ranging from 1 to 10, with larger values indicating a lower forward-looking statements intensity. POST is an indicator that equals one if a firm-year observation falls in the post-amendments period (i.e., 2019–2021), and zero otherwise (i.e., 2015–2017).

Panel A is estimated on the firm-year sample. The dependent variable is TARGET, an indicator that equals one if a firm receives at least one bid in year t, and zero otherwise. Panel B is estimated on the deal-level sample. The dependent variable is SYNERGY, 3-day cumulative abnormal return for a value-weighted portfolio of the acquirer and target. Control variables included are the same as those included in Table 3 for Panel A and Table 4 for Panel B, respectively. All independent variables are measured at time t-1. Variables are defined in online Appendix C. Z-statistics/T-statistics based on robust standard errors clustered at the firm/deal level are reported. *, **, and *** represent 2-tailed significance at the 10%, 5%, and 1% level, respectively.

The second natural experiment is SEC’s amendments on Regulation S-K after 2018, which aimed to modernize, simplify, and enhance MD&A disclosures, potentially influencing their content and nature. By examining this regulatory change, we are able to gain additional insights into the causal relationship between MD&A disclosures and their effects on acquirers’ decision-making. 9

Specifically, we collect MD&A forward-looking disclosure data for 2019–2021 to construct a new sample including 3 years before (2015–2017) and after (2019–2021) the regulatory change. 10 We construct two variables: LOW_FLI and POST. LOW_FLI represents the decile rankings of forward-looking MD&A disclosures before the amendments, ranging from 1 to 10, with larger values indicating a lower forward-looking statements intensity. POST is an indicator that equals one if a firm-year observation falls within the post-amendments period (i.e., 2019–2021), and zero otherwise (i.e., 2015–2017). We include LOW_FLI and the interaction term of POST and LOW_FLI in equations (1) and (2), omitting POST due to year-fixed effects. The results are presented in Columns (2) of Table 5, Panels A and B. The coefficients of LOW_FLI are significantly negative, consistent with our previous findings that lower levels of forward-looking information negatively impact acquisition probability and synergy. More importantly, the coefficients of the interaction terms between POST and LOW_FLI are significantly positive, indicating that this regulatory change raises the likelihood of being targeted for acquisition and enhances acquisition synergy, particularly for firms with lower levels of forward-looking disclosures before the amendments to Regulation S-K. These findings further support the conclusion that forward-looking MD&A disclosures positively impact acquisition efficiency.

Cross-Sectional Analyses: Signals of Forward-Looking Disclosure Credibility

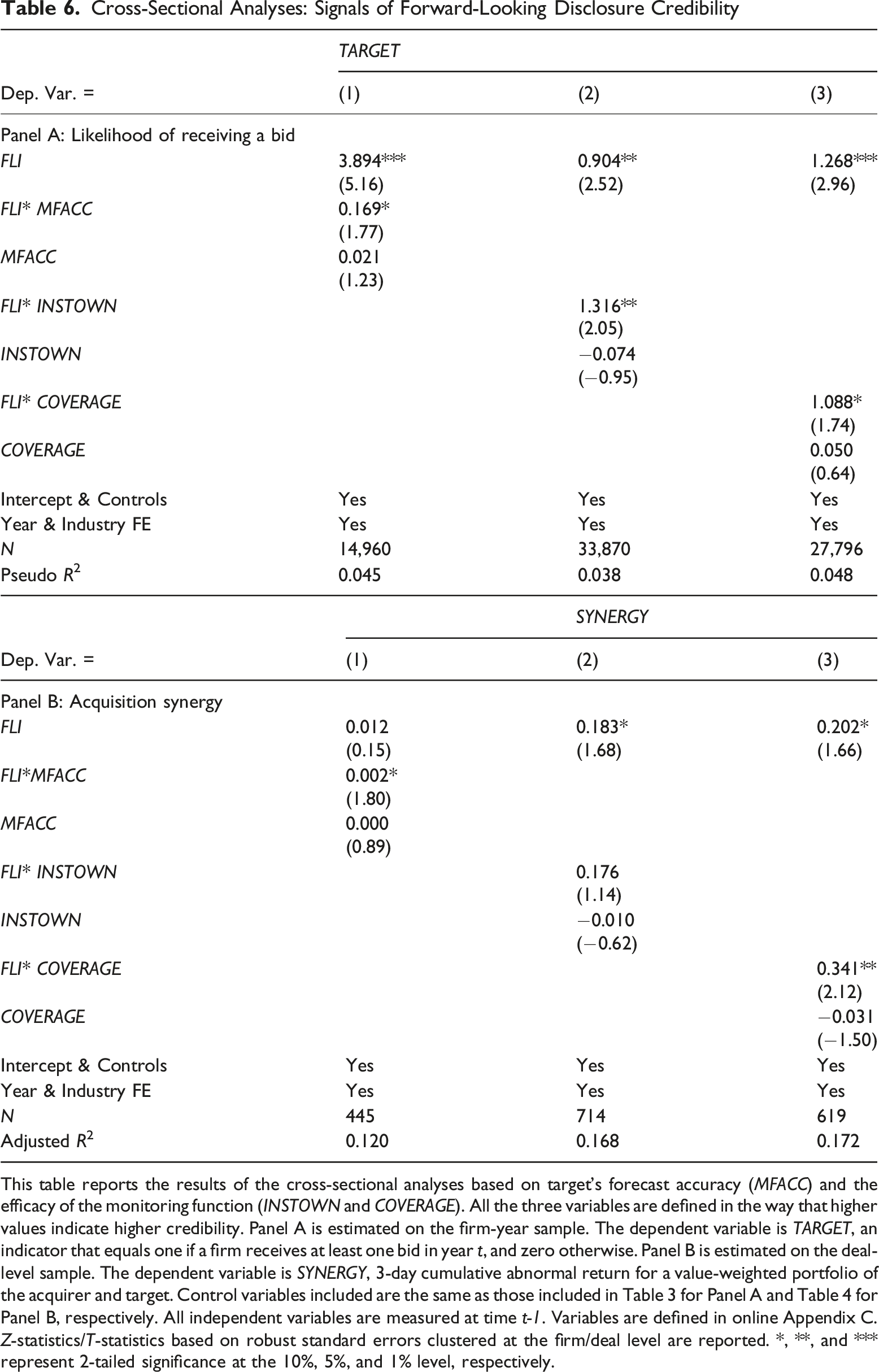

Brown et al. (2024) and Beyer et al. (2010) conjecture that narrative disclosures, such as the forward-looking MD&A disclosures, supplement the audited financial statements and can be a potentially essential and complementary source of relevant firm-specific information to outsiders. However, one may doubt the usefulness of MD&A disclosures because they are not subject to audits and lack credibility. Thus, we conduct several analyses to investigate the cross-sectional differences in the FLI-acquisition efficiency relationship.

Prior research cautions that firms can bias disclosures (Li et al., 2013). Rational managers thus may anticipate bias in targets’ disclosures and choose the extent to which they integrate MD&A information into M&A decision-making accordingly. Therefore, we expect the positive effects of forward-looking MD&A disclosures to be more pronounced in firms with more credible MD&A disclosures. To test this prediction, we introduce a proxy for disclosure credibility and its interaction term with forward-looking MD&A disclosures in our regression models.

Based on the literature, we identify three measures that are deemed to enhance disclosure credibility: management earnings forecasts accuracy (MFACC), institutional ownership (INSTOWN), and analyst coverage (COVERAGE). The first measure, MFACC, captures the accuracy of targets’ management earnings forecasts and reflects management’s commitment to credible forward-looking disclosures. It is defined as the negative absolute value of the difference between management forecasts and the actual earnings per share (EPS) deflated by assets per share (multiplied by 100 for straightforward interpretation) such that a higher value of MFACC is associated with more accurate management forecasts (Durnev & Mangen, 2020). Management forecasts are either a point estimate or the midpoint of the range estimates of the firm’s annual EPS. The other two measures are based on the efficacy of the monitoring function. Firms react to monitoring by improving their disclosure quality because they have the potential to facilitate the detection and discipline of managerial misconduct behavior (Irani & Oesch, 2013). The target’s institutional ownership is likely to improve disclosure credibility because institutional investors have more incentives and expertise to actively monitor management performance than retail investors (Shleifer & Vishny, 1986). We define INSTOWN as an indicator that equals one if the target has above-median total institutional ownership. The second proxy for monitoring efficacy is analyst coverage (COVERAGE), measured by an indicator that equals one if the target has an above-median number of analysts following it, as analysts help reduce information asymmetry and play the role of external monitors for management. Higher values of MFACC, INSTOWN and COVERAGE are associated with higher forward-looking disclosure credibility.

Cross-Sectional Analyses: Signals of Forward-Looking Disclosure Credibility

This table reports the results of the cross-sectional analyses based on target’s forecast accuracy (MFACC) and the efficacy of the monitoring function (INSTOWN and COVERAGE). All the three variables are defined in the way that higher values indicate higher credibility. Panel A is estimated on the firm-year sample. The dependent variable is TARGET, an indicator that equals one if a firm receives at least one bid in year t, and zero otherwise. Panel B is estimated on the deal-level sample. The dependent variable is SYNERGY, 3-day cumulative abnormal return for a value-weighted portfolio of the acquirer and target. Control variables included are the same as those included in Table 3 for Panel A and Table 4 for Panel B, respectively. All independent variables are measured at time t-1. Variables are defined in online Appendix C. Z-statistics/T-statistics based on robust standard errors clustered at the firm/deal level are reported. *, **, and *** represent 2-tailed significance at the 10%, 5%, and 1% level, respectively.

Overall, the results in Table 6 suggest that the enhancement of acquisition efficiency by forward-looking MD&A disclosures is stronger when the target has better disclosure credibility before the acquisition. This finding also implies that managers are not only concerned with the quantity and intensity of MD&A forward-looking information, but at least some of them, are concerned with and can successfully identify the level of its credibility and incorporate it into their M&A practices.

Cross-Sectional Analyses: Transparency vs. Firm Fundamentals

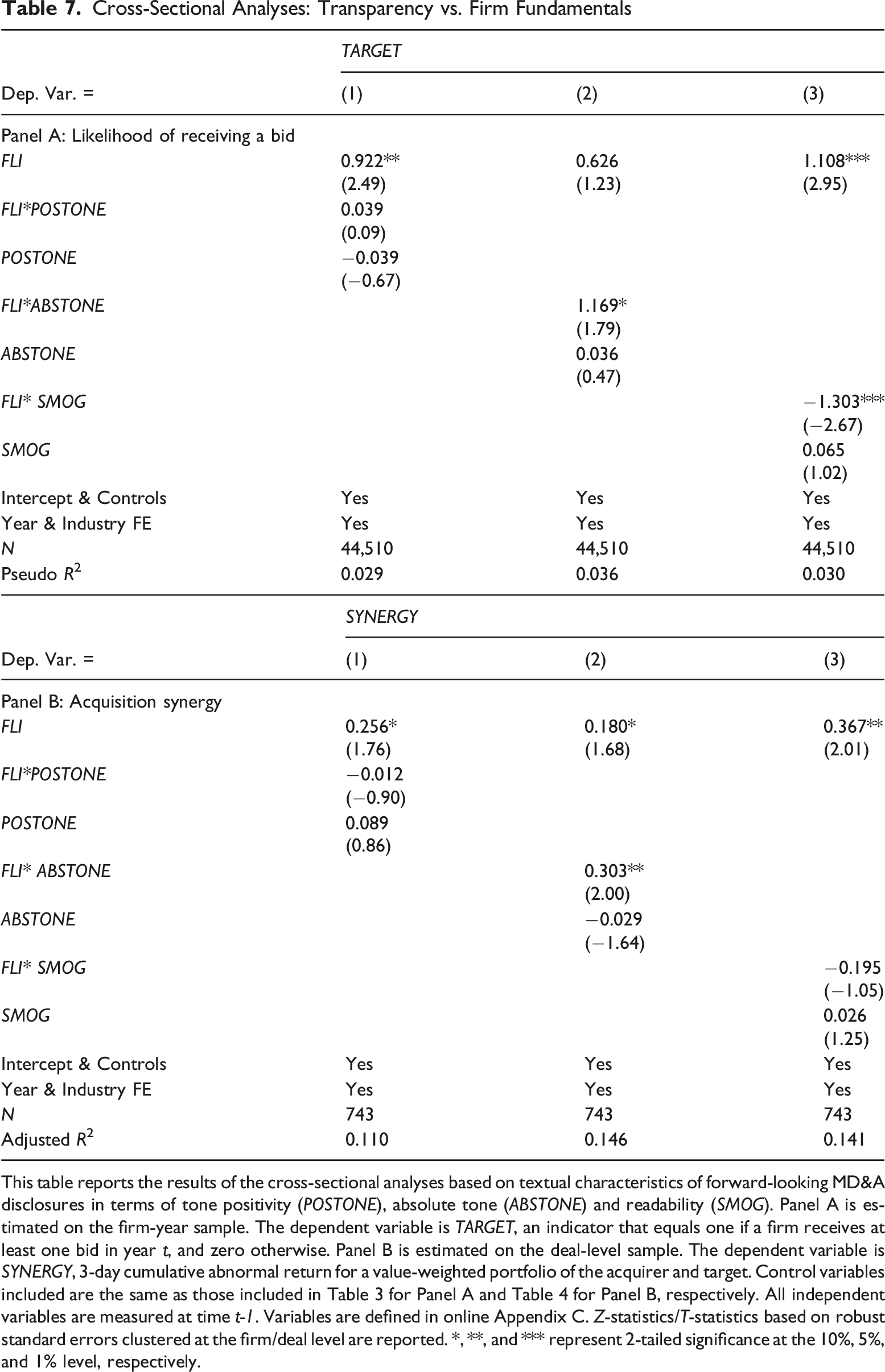

Our main test results demonstrate that more forward-looking information is associated with M&A outcomes, supporting the notion that forward-looking information enhances the transparency of target firms and thereby influences M&A outcomes (i.e., the information transparency story). However, it is also plausible that forward-looking information correlates with underlying firm fundamentals impacting M&A outcomes, despite our controls for various firm characteristics (i.e., the firm fundamental story). Our analysis primarily focuses on the quantity of forward-looking information in MD&As (Muslu et al., 2015). Previous literature suggests that beyond information quantity, the characteristics of narrative disclosures are also decision-relevant (e.g., Durnev & Mangen, 2020; Li, 2010). We are thus motivated to investigate how the contents and articulation of forward-looking information impact M&A outcomes, thereby helping to distinguish between the information transparency story and firm fundamental story.

Specifically, we exam how the impact of forward-looking information varies with tone positivity, tone absoluteness, and disclosure readability. More positive MD&A discussions imply stronger firm fundamentals, while absolute tone and readability are associated with articulate expression. In the information transparency story, we speculate that the effect of forward-looking information is consistent regardless of tone positivity but is more pronounced if the narrative disclosures are expressed in a more articulate way. Conversely, if the firm fundamentals story holds, the relationship between forward-looking information and M&A outcomes should be more evident in firms with more positive MD&A discussions.

Empirically, we adjust equations (1) and (2) to include proxies for tone positivity and articulation, interacting them with forward-looking MD&A disclosures. We use signed tone as a proxy for tone positivity. Specifically, we construct an indicator, POSTONE, which equals one if the target firm exhibits an above-median signed tone (i.e., more positive tone) in its forward-looking statements within the MD&A section, and zero otherwise. The signed tone is calculated as the difference between the number of positive and negative words, based on the sentiment word list constructed by Loughran and McDonald (2011), divided by the total number of words in forward-looking MD&A disclosure. Additionally, we employ two measures for the articulateness of forward-looking disclosures, absolute tone (ABSTONE) and readability (SMOG). The variable ABSTONE is defined as an indicator that equals one if the target has an above-median absolute tone in the forward-looking MD&A disclosure, where the absolute tone is defined as the absolute difference between the number of positive and negative words divided by the total number of words in forward-looking MD&A disclosure. The variable SMOG is defined as an indicator that equals one if the target has an above-median Smog Index in forward-looking MD&A disclosure, where Smog Readability Index is calculated using the following formula: 1.043 × Sqrt (number of complex words × 30/number of sentences) + 3.1291. The higher the Smog Index, the more difficult is the text to comprehend.

Cross-Sectional Analyses: Transparency vs. Firm Fundamentals

This table reports the results of the cross-sectional analyses based on textual characteristics of forward-looking MD&A disclosures in terms of tone positivity (POSTONE), absolute tone (ABSTONE) and readability (SMOG). Panel A is estimated on the firm-year sample. The dependent variable is TARGET, an indicator that equals one if a firm receives at least one bid in year t, and zero otherwise. Panel B is estimated on the deal-level sample. The dependent variable is SYNERGY, 3-day cumulative abnormal return for a value-weighted portfolio of the acquirer and target. Control variables included are the same as those included in Table 3 for Panel A and Table 4 for Panel B, respectively. All independent variables are measured at time t-1. Variables are defined in online Appendix C. Z-statistics/T-statistics based on robust standard errors clustered at the firm/deal level are reported. *, **, and *** represent 2-tailed significance at the 10%, 5%, and 1% level, respectively.

Deal Characteristics

Target Forward-Looking MD&A Disclosures and Deal Characteristics

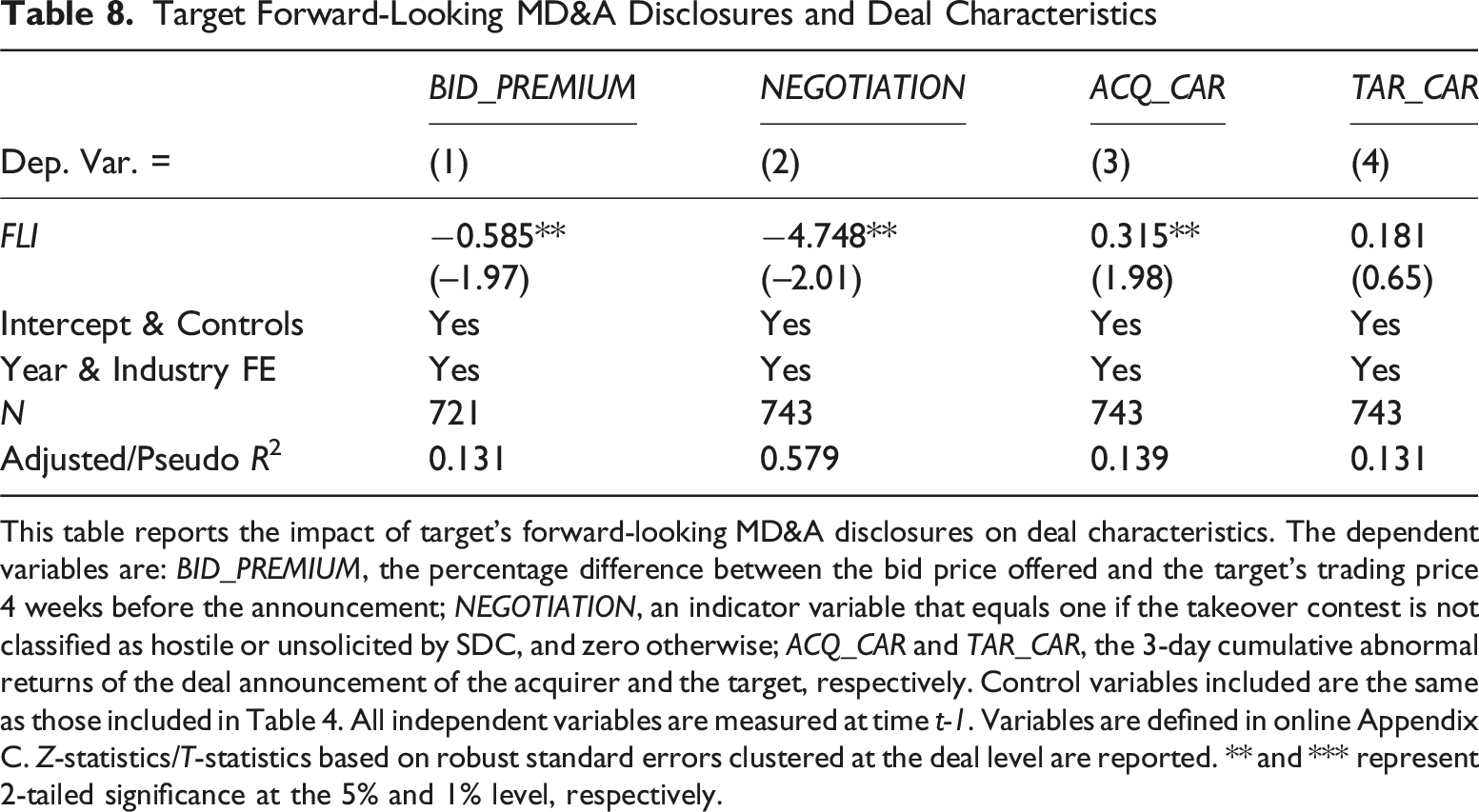

This table reports the impact of target’s forward-looking MD&A disclosures on deal characteristics. The dependent variables are: BID_PREMIUM, the percentage difference between the bid price offered and the target’s trading price 4 weeks before the announcement; NEGOTIATION, an indicator variable that equals one if the takeover contest is not classified as hostile or unsolicited by SDC, and zero otherwise; ACQ_CAR and TAR_CAR, the 3-day cumulative abnormal returns of the deal announcement of the acquirer and the target, respectively. Control variables included are the same as those included in Table 4. All independent variables are measured at time t-1. Variables are defined in online Appendix C. Z-statistics/T-statistics based on robust standard errors clustered at the deal level are reported. ** and *** represent 2-tailed significance at the 5% and 1% level, respectively.

Next, we examine another deal characteristic, the sale method (auction versus negotiation), to study the relationship between forward-looking MD&A disclosures and the choice of the sale method. The choice between a hostile or friendly takeover represents a strategic decision for the firms involved (Schwert, 2000). A bidder can assume control of a target firm either through initially negotiating with the target’s board and management or by making a hostile tender offer directly to shareholders. Bidders tend to conduct negotiated acquisitions when confronting high asymmetric uncertainty because private negotiations mitigate the information asymmetry between the bidder and the target, consequently reducing the bidder’s information risks (Raman et al., 2013). These findings suggest a negative relationship between forward-looking MD&A disclosures and transactions through negotiations. We empirically test this relationship by estimating equation (2) with NEGOTIATION as the dependent variable. NEGOTIATION is an indicator variable that equals one if the takeover contest is not classified as hostile or unsolicited by the SDC, and zero otherwise. Column (2) of Table 8 reports the probit regression results of NEGOTIATION on FLI. We find that the coefficient of FLI is significantly negative, indicating that forward-looking MD&A disclosures reduce the likelihood of sales via negotiations, consistent with the notion that forward-looking MD&A disclosures decrease target valuation uncertainty.

Columns (1) and (2) of Table 8 enhance our understanding of the synergistic effects from the perspective of deal characteristics. That is, enhanced forward-looking MD&A disclosures reduce the target’s uncertainty, facilitating a more precise deal valuation and a more efficient method of sale. A follow-up question is how the benefits of forward-looking MD&A disclosures of targets are enjoyed by the acquirers’ and targets’ shareholders. The main results in Table 4 support a positive synergy effect by the forward-looking information. In this section, we examine the distribution of wealth between the acquirers’ and targets’ shareholders by decomposing the combined synergy into acquirer CAR and target CAR, respectively. We replace the dependent variable in equation (2) with 3-day cumulative abnormal returns for the acquirer (ACQ_CAR) and the target (TAR_CAR), respectively. Columns (3) and (4) of Table 8 report the results. The coefficient of forward-looking MD&A disclosures is positive and statistically significant at the 5% level when ACQ_CAR is the dependent variable, while insignificant when TARGET_CAR is the dependent variable. The result indicates that acquirers effectively utilize forward-looking information released by the targets and accordingly share a dominant portion of the deal synergy.

Taken together, the results in Table 8 suggest that the forward-looking information in target’s MD&A disclosures reduces information uncertainty and benefits the acquirers with lower bid premium and higher acquisition announcement returns.

Post-Acquisition Performance

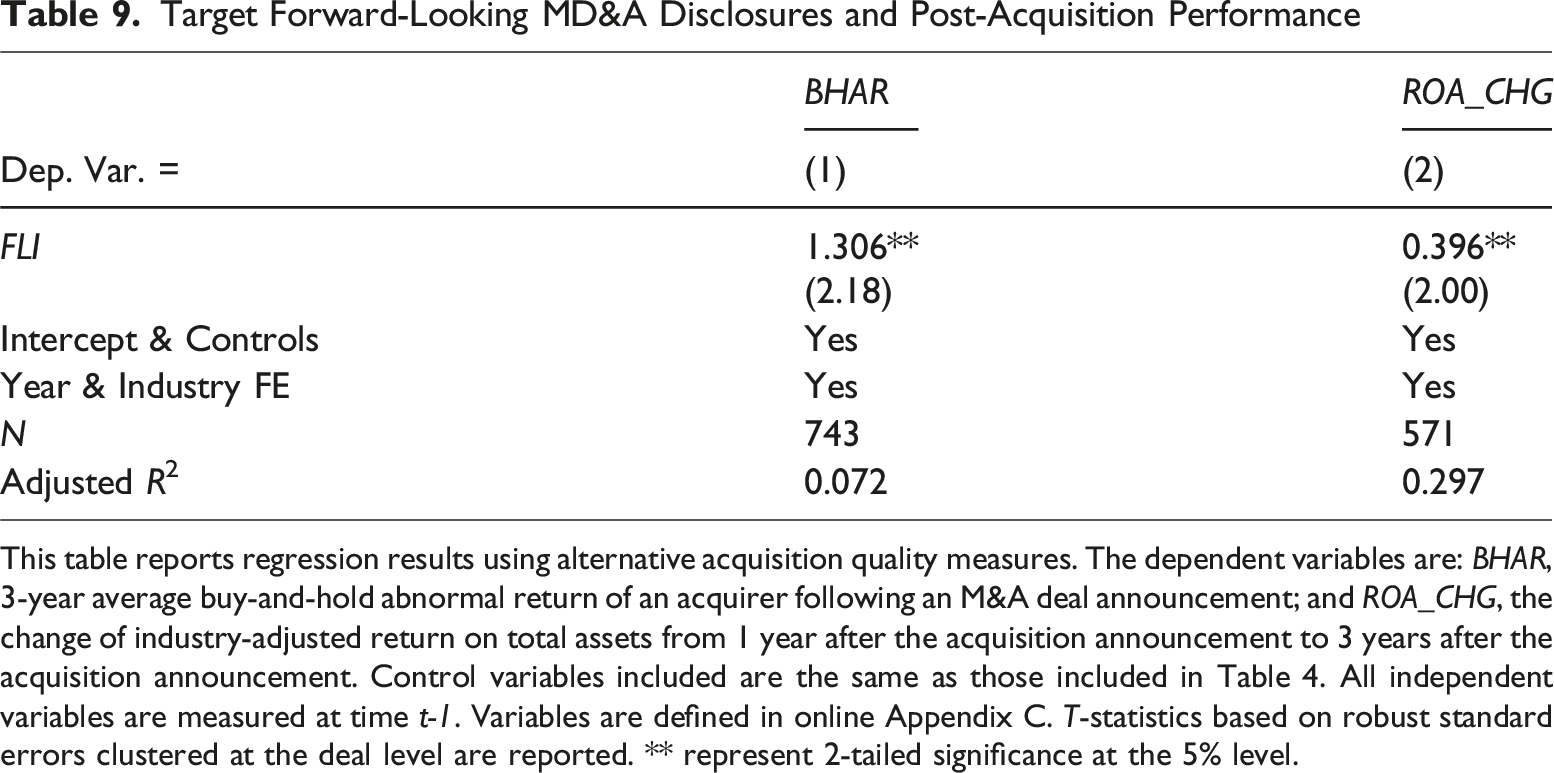

Target Forward-Looking MD&A Disclosures and Post-Acquisition Performance

This table reports regression results using alternative acquisition quality measures. The dependent variables are: BHAR, 3-year average buy-and-hold abnormal return of an acquirer following an M&A deal announcement; and ROA_CHG, the change of industry-adjusted return on total assets from 1 year after the acquisition announcement to 3 years after the acquisition announcement. Control variables included are the same as those included in Table 4. All independent variables are measured at time t-1. Variables are defined in online Appendix C. T-statistics based on robust standard errors clustered at the deal level are reported. ** represent 2-tailed significance at the 5% level.

Robustness Checks

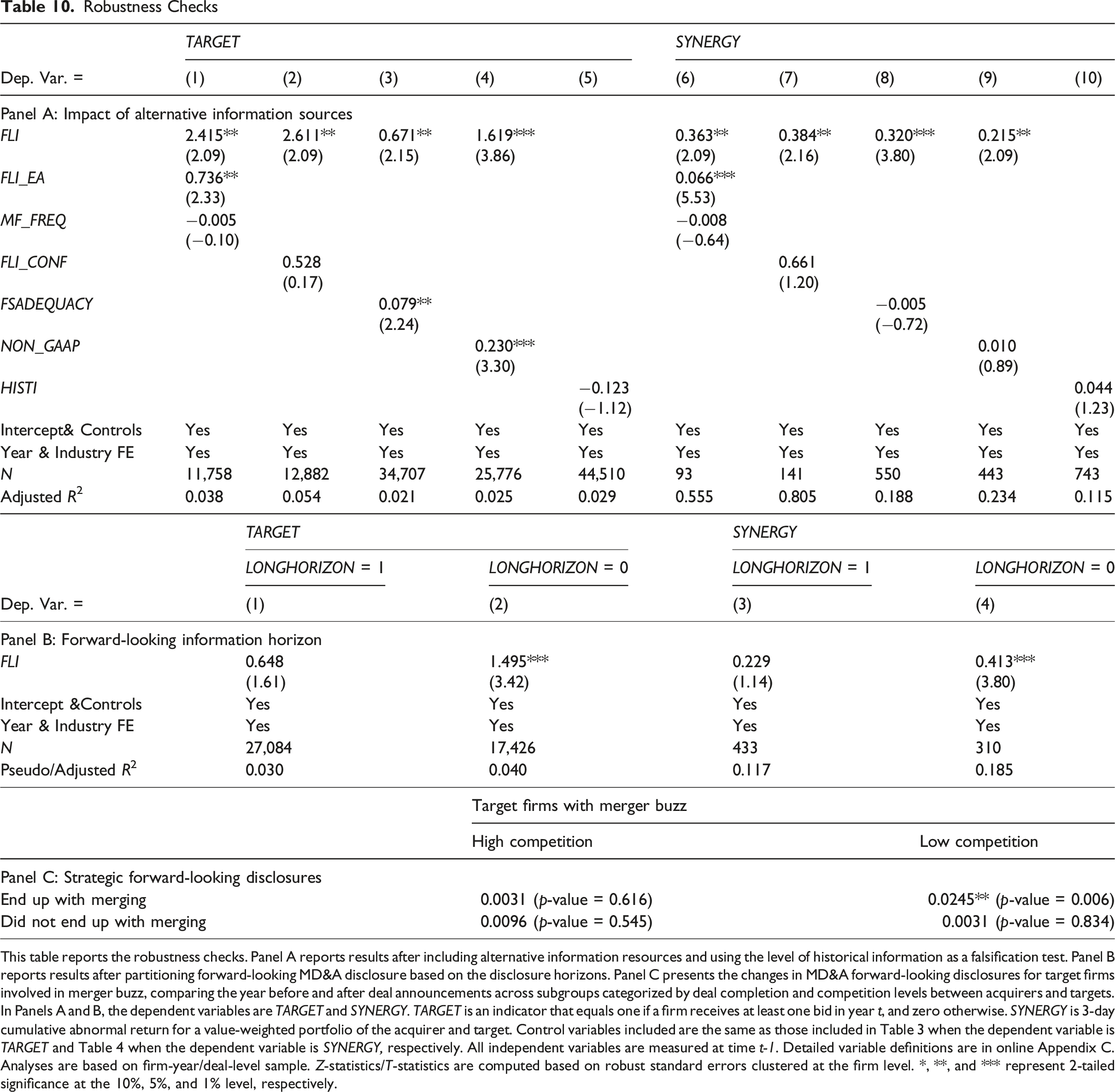

We conduct several robustness checks including controlling for alternative information sources, testing different disclosure horizons and types, using various alternative measures for forward-looking disclosures, and employing a change model to ensure the robustness of our conclusions.

Additional Controls for Alternative Information Sources

While the focus of our study is the narrative forward-looking disclosures in the MD&A section of 10-K, extant literature has proposed other sources of forward-looking information such as those contained in the management earnings announcement (Bozanic et al., 2018) or management guidance. We thus control for these two types of forward-looking information to check whether the MD&A disclosures are incrementally informative to the acquirers. The variable FLI_EA is employed to capture the forward-looking information delivered in the earning announcement. It is defined as an indicator that equals one if the number of forward-looking words divided by the total number of words in the earnings announcements is above median, and zero otherwise. We construct another variable MF_FREQ to capture the forward-looking information contained in the management guidance. It is defined as the logarithm of management guidance frequency. Furthermore, recognizing conference calls as an important voluntary disclosure channel for managers, we construct the variable FLI_CONF to capture the forward-looking information delivered during conference calls. This variable is calculated as the number of forward-looking words divided by the total number of words delivered during conference calls. Additionally, Brown et al. (2024) suggest that firms utilize the MD&A disclosures when their financial statement disclosure is inadequate. Thus, we include a variable, FSADEQUACY, to control for the information source from the financial statement. FSADEQUACY is defined as an indicator that equals one if the target has an above-median financial statement adequacy score, and zero otherwise. The financial statement adequacy is defined as R 2 from regressing the firm’s stock price on its EPS and book value per share using 20 quarters ending with the fourth quarter of the fiscal year (Brown et al., 2024). Finally, Chen et al. (2025) suggests that public non-GAAP disclosure by target firms is associated with M&A outcomes. Therefore, we also incorporate an additional control variable for non-GAAP disclosure (NON_GAAP). Specifically, we measure the extent of non-GAAP disclosure as the percentage of earnings announcements containing non-GAAP EPS disclosure during the year, using data provided by Bentley et al. (2018). These four measures are employed to capture alternative sources of forward-looking information. We re-estimate equations (1) and (2) to include them as additional control variables.

Robustness Checks

This table reports the robustness checks. Panel A reports results after including alternative information resources and using the level of historical information as a falsification test. Panel B reports results after partitioning forward-looking MD&A disclosure based on the disclosure horizons. Panel C presents the changes in MD&A forward-looking disclosures for target firms involved in merger buzz, comparing the year before and after deal announcements across subgroups categorized by deal completion and competition levels between acquirers and targets. In Panels A and B, the dependent variables are TARGET and SYNERGY. TARGET is an indicator that equals one if a firm receives at least one bid in year t, and zero otherwise. SYNERGY is 3-day cumulative abnormal return for a value-weighted portfolio of the acquirer and target. Control variables included are the same as those included in Table 3 when the dependent variable is TARGET and Table 4 when the dependent variable is SYNERGY, respectively. All independent variables are measured at time t-1. Detailed variable definitions are in online Appendix C. Analyses are based on firm-year/deal-level sample. Z-statistics/T-statistics are computed based on robust standard errors clustered at the firm level. *, **, and *** represent 2-tailed significance at the 10%, 5%, and 1% level, respectively.

To address potential concerns that our results might be driven by overall disclosure levels rather than forward-looking information specifically, we conduct a falsification test using narrative historical information. Given the lack of established historical keyword lists in existing literature, we employ ChatGPT to analyze our MD&A files and develop a set of historical keywords. 13 Following the same approach used for constructing forward-looking information (FLI), we construct the variable HISTI, calculated as the number of historical sentences divided by the total number of sentences in the MD&A section. Replacing FLI with HISTI in equations (1) and (2), we find statistically insignificant coefficients of HISTI, as shown in Columns (5) and (10) of Table 10, Panel A. These results, combined with our controls for historical financial characteristics, further mitigate the concern that historical information in the MD&A section drives our findings.

Forward-Looking Information Horizon

We further investigate whether the horizon of forward-looking information influences M&A decisions. On one hand, short-term forward-looking disclosures may provide less incremental information compared to long-term disclosures. On the other hand, they are more easily verifiable and potentially more reliable. Meanwhile, the usefulness of long-term forward-looking information may depend on acquirers’ focus on immediate post-acquisition integration and their strategic plans.

To examine the effects of disclosure horizons, we categorize forward-looking MD&A disclosures based on their horizon. We identify short- and long-horizon keywords in forward-looking statements according to the keyword list developed by Muslu et al. (2015). We then construct a variable, LONGHORIZON, which is an indicator equal to one if the target firm has above-median level of long-term forward-looking disclosures in the MD&A section. Long-term forward-looking disclosures are measured as the difference between the number of long- and short-horizon keywords, divided by the total word count of the MD&A section. Based on the LONGHORIZON indicator, we divide the sample into two subgroups: those with a long horizon (LONGHORIZON = 1) and those with a short horizon (LONGHORIZON = 0). The results, presented in Panel B of Table 10, show that the coefficients of forward-looking information (FLI) are significantly positive in the short-horizon subgroup (LONGHORIZON = 0) but insignificant in the long-horizon subgroup (LONGHORIZON = 1). This suggests that our findings are primarily driven by short-term forward-looking disclosures.

Strategic Forward-Looking Disclosures

Our above analyses have shown that forward-looking disclosures are associated with higher M&A possibilities. This naturally raises the question of whether firms intentionally provide more forward-looking disclosures to increase their likelihood of becoming acquisition targets and how they balance the associated proprietary costs. To provide some initial insights into this issue, we conduct a preliminary investigation.

Specifically, we examine whether potential target firms involved in merger buzz strategically adjust their forward-looking MD&A disclosures after deal announcements. We define merger buzz as deals identified as withdrawn or rumor in the SDC database. We categorize firms involved in merger buzz into four subgroups based on two dimensions: (1) whether the merger was ultimately completed, and (2) the competition level between acquirers and targets, determined by whether they share the same two-digit SIC code. We present the changes in MD&A forward-looking disclosures for the year before and after the deal announcement for each of the four subgroups, along with corresponding p-values, in Table 10, Panel C.

Our results reveal that target firms facing high competition with acquirers show no significant change in MD&A forward-looking disclosures around deal announcements, regardless whether the merger was ultimately completed. In contrast, for target firms with lower competition with the acquirer, we observe a significant increase in forward-looking information (FLI) for deals ending up with merging, while no significant change is noted for those that did not result in a merger. These findings provide some preliminary evidence that target firms might consciously enhance their disclosures to increase their attractiveness for acquisition, but they also appear to weigh the potential proprietary cost, particularly when they are in direct competition with acquirers.

The Nature of Forward-Looking MD&A Disclosures

Our main analysis shows that an overall increase in forward-looking MD&A disclosures enhances acquisition outcomes. However, we may expect that different types of information do not equally contribute to the acquirer’s decision-making. Thus, it would be interesting to decompose the overall MD&A disclosures and explore the specific aspects of forward-looking information in MD&As that contribute to acquisition outcomes. To achieve this, we group forward-looking sentences based on whether they include keywords related to business operations, finance, macroeconomics, and policy, as described in online Appendix B. Sentences including keywords from more than one group belong to a separate group. While not reported for brevity, we find that among all forward-looking MD&A disclosures, those describing operations-related and financial information are decision-relevant for acquirers, while those related to the macro environment and policy disclosures do not, on average, increase the likelihood of receiving a bid or acquisition synergy. This finding is intuitive because the acquirer may be already aware of the macro environment and policy-related information. In comparison, the operational- and financial-wide information is firm-specific and thus is decision-relevant for the acquirer.

Alternative Independent Variables

In this section, we check the robustness of our results using four alternative measures of the independent variables. The first measure is FLI [t-3, t-1], defined as the number of forward-looking sentences divided by the total number of sentences in the MD&A section over the three fiscal years from t−3 to t-1. The second measure, FLI_WORDS, is constructed based on the number of words instead of sentences and is defined as the number of words in forward-looking sentences divided by the total number of words in the MD&A section. The third and fourth measures are based on alternative forward-looking statement dictionaries. Specifically, FLI_LI and FLI_BOZANIC are defined as the number of forward-looking sentences divided by the total number of sentences in the MD&A section, where forward-looking statements are defined following Li (2010) and Bozanic et al. (2018). Our results remain robust to these alternative forward-looking MD&A disclosure proxies.

Change Model

Next, we employ a change model to mitigate the possibility of spurious correlations due to firm-fixed characteristics. Specifically, we investigate whether a change in forward-looking MD&A disclosure influences the probability of receiving a bid. We estimate a regression of the change in TARGET compared to 1 year earlier on the corresponding change in FLI. We also include the change in firm-level control variables. An ordered logistic regression is employed to estimate the change model. We find that the changes in a firm’s FLI positively predict changes in the likelihood of receiving a bid.

Conclusion

This study investigates the usefulness of narrative disclosures in making M&A decisions. We focus on one type of narrative disclosures, the forward-looking disclosures in the MD&A section and examine whether the target’s forward-looking disclosures reduce uncertainty, and thus improving acquisition outcomes. Our results show that the quantity, in terms of frequency and intensity, of forward-looking MD&A disclosures increases the likelihood of receiving a bid and enhances acquisition synergy. The cross-sectional tests suggest that the positive effects of forward-looking information on M&A decisions and quality are more pronounced when MD&A disclosures are deemed more credible and are expressed unambiguously, regardless of the tone’s direction. This aligns with the notion that forward-looking disclosures enhances information transparency of the target firm. We next conduct a further investigation of the deal characteristics in terms of bid premium, negotiation deal, acquirers’ return and targets’ return. We find that targets with more forward-looking information in MD&A are associated with deal characteristics that are favorable to acquirers. Additionally, deals with more forward-looking disclosures are associated with superior post-acquisition performance in terms of long-term buy-and-hold returns as well as improvement in financial performance. Our main results remain robust to quasi-natural experiments design, alternative forward-looking disclosure measures and additional controls for alternative information sources.

Our findings provide insights in the usefulness of potential targets’ information for acquirers and shed light on the disclosure behavior of potential acquisition targets. The study shows that managers disclose the type and extent of forward-looking information in the MD&A section, which is of interest to a key user group, potential acquirers. Furthermore, our findings carry various policy implications. While MD&A disclosures are not subject to audit, documented decision usefulness suggests that the SEC should encourage such forward-looking, non-boilerplate disclosures.

Supplemental Material

Supplemental Material - Forward-looking Management Discussions and Analysis Disclosure and Merger and Acquisition Outcomes

Supplemental Material for Forward-looking Management Discussions and Analysis Disclosure and Merger and Acquisition Outcomes by Xin Chen, Haina Shi, Yi Zhou, and Xindong (Kevin) Zhu in Journal of Accounting, Auditing, and Finance.

Footnotes

Acknowledgments

We received useful comments from Jeong-Bon Kim, Gerald Lobo, Nancy Su, Ke Wang, GaoGuang Zhou, and participants of Ph.D. seminars and research workshops at Fudan University and City University of Hong Kong. All authors contributed equally. We are grateful for Xiang Gao for his excellent programming support. All errors are our own.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Haina Shi and Yi Zhou are grateful for the support from the National Natural Science Foundation of China (NSFC-72372028 and NSFC-72472032).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.