Abstract

Earnings announcement returns tend to be volatile when a significant amount of information remains unknown to investors prior to the announcement. The informativeness of earnings announcements—measured by the return volatility during the announcement period relative to the pre-announcement period—reflects the extent of information not publicly disclosed ex ante. Consistent with the view that information plays a crucial role in stock pricing, we find a positive correlation between the informativeness of earnings announcements and expected stock returns in the U.S. market from 1977 to 2022. This effect is more pronounced among younger firms, firms with higher return volatility, and during periods of heightened investor risk aversion. Additionally, we find supporting evidence that reductions in information supply, driven by Regulation FD, lead to higher expected stock returns.

Keywords

Introduction

Beginning with the seminal work of Beaver (1968), numerous studies have examined the information content of earnings announcements, as reflected by the abnormal return variance on announcement dates. This body of literature has successfully identified a variety of significant economic determinants of earnings announcement informativeness (EAI), encompassing a wide range of market conditions and firm-level characteristics (e.g., Atiase, 1985; DeFond et al., 2007; Landsman et al., 2012; Pevzner et al., 2015). Despite this progress, a significant research gap remains regarding the economic consequences of varying levels of earnings announcement informativeness. Given that EAI has increased substantially since 2001 (Beaver et al., 2018, 2020) and plays a significant role in financial markets, it is essential to understand its economic implications. In this study, we investigate the impact of EAI on expected stock returns, which are central to firm valuation.

Informative earnings announcements often indicate that investors lacked sufficient information prior to the announcement, and a firm’s information disclosure practices may contribute to this information deficiency. As demonstrated by Beaver et al. (2020), the upward trend in EAI among U.S. stocks in the new century can be attributed to the increasing volume of concurrent disclosures (e.g., earnings guidance) accompanying earnings announcements. Assuming the total amount of information possessed by the firm remains unchanged, the bundled release of information during earnings announcements suggests that some information could have been disclosed earlier. For instance, earnings guidance could be issued more promptly to create a more equitable information environment for investors (Ertan et al., 2025; Rogers & Van Buskirk, 2013). 1

Given their association with limited pre-announcement information availability, informative earnings announcements may imply higher expected stock returns. Generally, when investors lack sufficient information, they tend to avoid stock investments to protect themselves unless prices are low enough to justify the associated risk premium (Easley & O’Hara, 2004). In specific situations where pre-announcement information disclosures are minimal—due to bundled disclosure practices—investors may have a limited understanding of the firm. Consequently, they may perceive the firm’s stock as highly risky, leading to increased return uncertainty, particularly for younger firms and among risk-averse investors (Cohen et al., 2007; Diamond & Verrecchia, 1991; Jorgensen & Kirschenheiter, 2003; Levi & Zhang, 2015; Stoumbos, 2023). As a result, investors demand a premium to compensate for low information availability (Amihud & Mendelson, 1989; Barber et al., 2013; Campbell et al., 2001; Da Silva, 2019; Pevzner et al., 2015; Savor & Wilson, 2016).

However, one could argue that informative earnings announcements do not necessarily lead to higher expected stock returns. First, an abundance of information is not always in investors’ best interest. Excessive disclosures can harm a firm if exploited by competitors or if they result in increased agency costs (Hermalin & Weisbach, 2012). Other unintended consequences of excessive disclosures include reduced liquidity for long-term investors (Monnet & Quintin, 2017), diminished private information production, compromised risk-sharing, and the promotion of destabilizing beauty-contest incentives (Goldstein & Yang, 2017). In contrast, moderate disclosures can alleviate capital market pressure on managers and mitigate their myopic behavior (Arif & De George, 2020; Fu et al., 2020). Second, informative earnings announcements imply that earnings reports have high precision, which can help reduce a firm’s beta or covariance risk (Amir & Levi, 2019; Evans, 2016; Livnat & Zarowin, 1990). Third, information risk may be negligible to investors due to market competition or portfolio diversification (Hughes et al., 2007). Given the debate outlined above, there is a need for more empirical evidence.

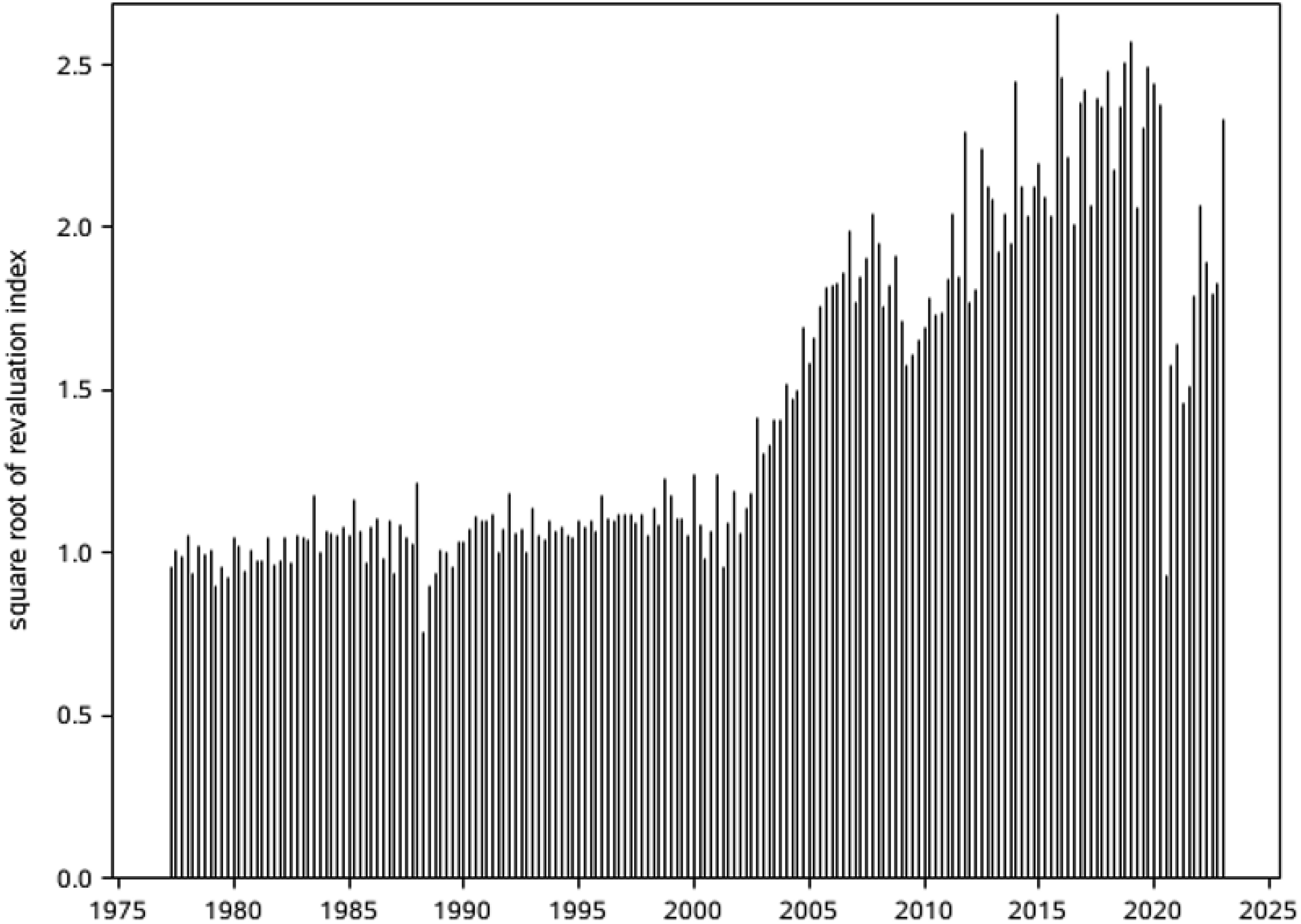

In this study, we measure EAI using Atiase’s (1985) revaluation index, calculated as the ratio of return volatility during earnings announcements to normal return volatility in the absence of news. A higher index indicates less pre-announcement information availability and more information revealed on the announcement date (Atiase et al., 1989; Efendi et al., 2016; El-Gazzar, 1998). This index closely aligns with the measure developed by Beaver (1968), with the additional consideration of estimation errors in risk loadings. Consistent with Beaver et al. (2020), we observe a notable increase in earnings announcement informativeness—measured by the average revaluation index—after 2001. Our analyses indicate that earnings announcement informativeness is inversely related to pre-announcement information disclosure levels, as captured by the normal information flow measure proposed by Thomas et al. (2022), the number of analyst forecasts, and the frequency of management guidance. This evidence supports our assertion that earnings announcement informativeness reflects previously undisclosed information.

In a sample of U.S. stocks from 1977 to 2022, portfolio and regression analyses both demonstrate that our measure of earnings announcement informativeness—specifically, the average revaluation index over the past 12 quarters—exhibits a positive correlation with future stock returns. The return spread between the top and bottom deciles of stocks sorted by EAI is 4.80% per year. This difference remains statistically significant even after controlling for other important risk premiums using various risk factor models. Furthermore, the finding remains robust when accounting for earnings quality as measured by discretionary accruals (Dechow et al., 1995; Sloan, 1996).

Further analyses reveal intriguing variations in the EAI premium stemming from firm-level and market-level frictions. First, the EAI premium tends to be lower for more mature firms. Mature firms—characterized by established earnings and operational records—are easier for investors to understand and value. Consequently, investor demand for pre-announcement information is relatively low, which in turn reduces the EAI premium. We measure firm maturity by firm age (Easley & O’Hara, 2004) or by whether the firm pays cash dividends (Grullon et al., 2002). Second, the EAI premium is positively related to information uncertainty, which is captured by return volatility (Gao et al., 2017; Jiang et al., 2005; Li et al., 2021; Lyle, 2025). Higher information uncertainty leads to greater investor demand for information and a higher information risk premium. Finally, the risk premium for low information availability rises when investors exhibit higher levels of risk aversion, measured using the risk aversion data from Bekaert et al. (2022).

Moreover, we find that controlling for firm-level earnings response coefficients (ERC) does not alter our conclusions, indicating that EAI is distinct from ERC. Additionally, EAI differs from post-earnings announcement drift (PEAD). While PEAD is typically attributed to investors’ behavioral biases, the return predictability of EAI stems from investors’ rational pricing of information risk. Our findings remain robust after accounting for prior-quarter earnings surprise—measured either by the 3-day cumulative abnormal returns surrounding the earnings announcement or based on the random-walk earnings model outlined by Chan et al. (1996)—underscoring the unique significance of EAI in explaining future stock returns.

A key concern is that a firm’s EAI and its cost of equity capital may be endogenously determined. To mitigate this concern, we examine Regulation Fair Disclosure (Reg FD), enacted in 2000, which significantly altered the information environment for U.S. firms. Reg FD prohibited U.S. firms from making selective information disclosures but exempted non-U.S. American Depositary Receipt (ADR) firms (Francis et al., 2006; Litvak, 2007). As noted by Easley and O’Hara (2004), the reduction in selective disclosures diminishes investor information availability and heightens information risk. By designating U.S. firms as the treatment group and ADR firms as the control group, we anticipate—and observe—increases in both EAI and expected stock returns for U.S. firms relative to ADR firms following the implementation of Reg FD. Furthermore, using pre-regulation informativeness as a proxy for treatment intensity, we find that firms with more pre-regulation information disclosures experience more pronounced and positive changes in their expected stock returns post Reg FD.

Our study contributes to the literature in three key ways. First, it expands existing research on EAI, which has primarily focused on its determinants rather than its economic consequences. Previous studies often regard informative earnings announcements as beneficial due to their positive correlation with high earnings quality and credibility (e.g., Ball & Brown, 1968; Beaver, 1968; DeFond et al., 2007; Hanlon et al., 2008). However, our study argues that these announcements can be detrimental, as they may be associated with limited pre-announcement information availability (Han & Wild, 2000; Holthausen & Verrecchia, 1988).

Second, our study contributes to the literature on the cost of equity capital by examining specific informational attributes. This line of research has primarily focused on three attributes: information quantity, information precision, and information asymmetry (Schreder, 2018). Our study extends prior literature by demonstrating that the timeliness of information disclosure—indicated by the volume of information released during earnings announcements relative to other periods—can significantly impact the cost of capital.

Finally, our study contributes to research on the economic impact of disclosure regulations (Anilowski et al., 2007). Our investigation of Reg FD confirms that it exerts a “chilling effect” on information availability (Koch et al., 2013), resulting in increased information risk for investors. This evidence has important implications for policymakers seeking to comprehensively evaluate the economic consequences of disclosure policies.

Hypothesis Development

New information about a firm may arrive continuously in small, random doses (Fama, 1970). However, a firm may choose to postpone information disclosure, resulting in a substantial amount of information being released during earnings announcements. This practice renders such announcements highly informative, with very little information disclosed beforehand. Limited firm-provided information can also hinder the ability of information intermediaries (e.g., financial analysts and news media) to generate insights (Francis et al., 2002). Consequently, the shift in information flow—specifically, disclosing pre-announcement information during the announcement period—can enhance EAI but at the cost of reduced pre-announcement information availability. The positive relationship between high EAI and low pre-announcement information availability aligns with the following argument: when investors have only vague expectations about upcoming news, they have much to learn upon the public release of earnings announcement information, leading to significant price reactions (e.g., Holthausen & Verrecchia, 1988; Kim & Verrecchia, 1991a, 1991b).

The uneven temporal distribution of information—evidenced by highly informative earnings announcements—has significant implications for investors. In principle, investors at an informational disadvantage often mitigate risk by avoiding stock investments unless prices are sufficiently low to provide adequate compensation for that risk (Easley & O’Hara, 2004). Specifically, when pre-announcement information disclosure is minimal, investors may perceive asset values as riskier. This perception results in lower stock liquidity and heightened return uncertainty, a concern that is particularly acute for less mature firms and among risk-averse investors (Cohen et al., 2007; Diamond & Verrecchia, 1991; Jorgensen & Kirschenheiter, 2003; Levi & Zhang, 2015; Stoumbos, 2023). As suggested by Easley and O’Hara (2004), less-informed investors end up holding an excessive amount of underperforming stocks and an insufficient amount of outperforming stocks compared to their well-informed counterparts. Consequently, the risks associated with low information availability compel investors to demand a premium. This required compensation for bearing information risk ultimately translates into higher expected stock returns (Amihud & Mendelson, 1989; Barber et al., 2013; Campbell et al., 2001; Da Silva, 2019; Pevzner et al., 2015; Savor & Wilson, 2016).

An alternative perspective posits that more informative earnings announcements may not inherently translate into higher expected shareholder returns. This view is supported by several countervailing arguments. For instance, heightened transparency can sometimes destroy firm value if it reveals proprietary information to competitors or intensifies agency conflicts (Hermalin & Weisbach, 2012). Additional drawbacks may include reduced market liquidity for long-term investors (Monnet & Quintin, 2017), suppressed private information production, reduced risk-sharing efficiency, and the encouragement of short-term market dynamics (Goldstein & Yang, 2017). In contrast, a measured approach to disclosure can shield managers from excessive market pressures and curb short-sighted decision-making (Arif & De George, 2020; Fu et al., 2020). Moreover, high-quality, precise earnings reports could potentially lower a firm’s systematic risk—by reducing its beta or covariance with the market—thereby decreasing rather than increasing expected returns (Amir & Levi, 2019; Evans, 2016; Livnat & Zarowin, 1990). Finally, in well-diversified portfolios, firm-specific information risk may be largely irrelevant, as it can be diversified away (Hughes et al., 2007). Given these competing theoretical channels, the net effect on expected returns remains an unresolved empirical question. Our testable hypothesis is therefore as follows:

There is a positive relationship between EAI and expected stock returns.

Informativeness Measure and Sample Description

The Measure of Earnings Announcement Informativeness

The cornerstone of our measure of earnings announcement informativeness is Atiase’s (1985) revaluation index. This index is a slight variation of Beaver’s (1968) measure and assesses return volatility during earnings announcements in comparison to the normal level of return volatility in the absence of earnings news. It is defined as follows

If there is no significant new information, Mean

Our primary measure of earnings announcement informativeness is the average of the square root of RI over the past 12 quarters

2

The Sample Formation Process

Our primary dataset consists of monthly U.S. stock data spanning from January 1977 to December 2022. Stock return data is sourced from the Center for Research in Security Prices (CRSP), while accounting information and earnings announcement dates are obtained from Compustat, and analyst forecasts are derived from the Institutional Brokers’ Estimate System (IBES). We selected 1977 as the starting point for our sample for two main reasons: first, NASDAQ companies have been included in CRSP since December 1972, and earnings announcement data have been available in Compustat since the fourth quarter of 1971; second, the EAI measure relies on data from the preceding 20 quarters in robustness tests.

Following the methodology established by Fama and French (1992), we integrate the CRSP monthly stock file with the Compustat annual file to construct a monthly stock dataset for cross-sectional analysis. The sample comprises U.S. firms with stock codes of 10 or 11, excluding those in the financial sector (SIC codes 6000–6999), that have at least 24 monthly returns over the preceding 5 years and positive book equity from the most recent fiscal year. For each stock-month, we calculate the EAI measure as the average root of the RI over the prior 12 quarters.

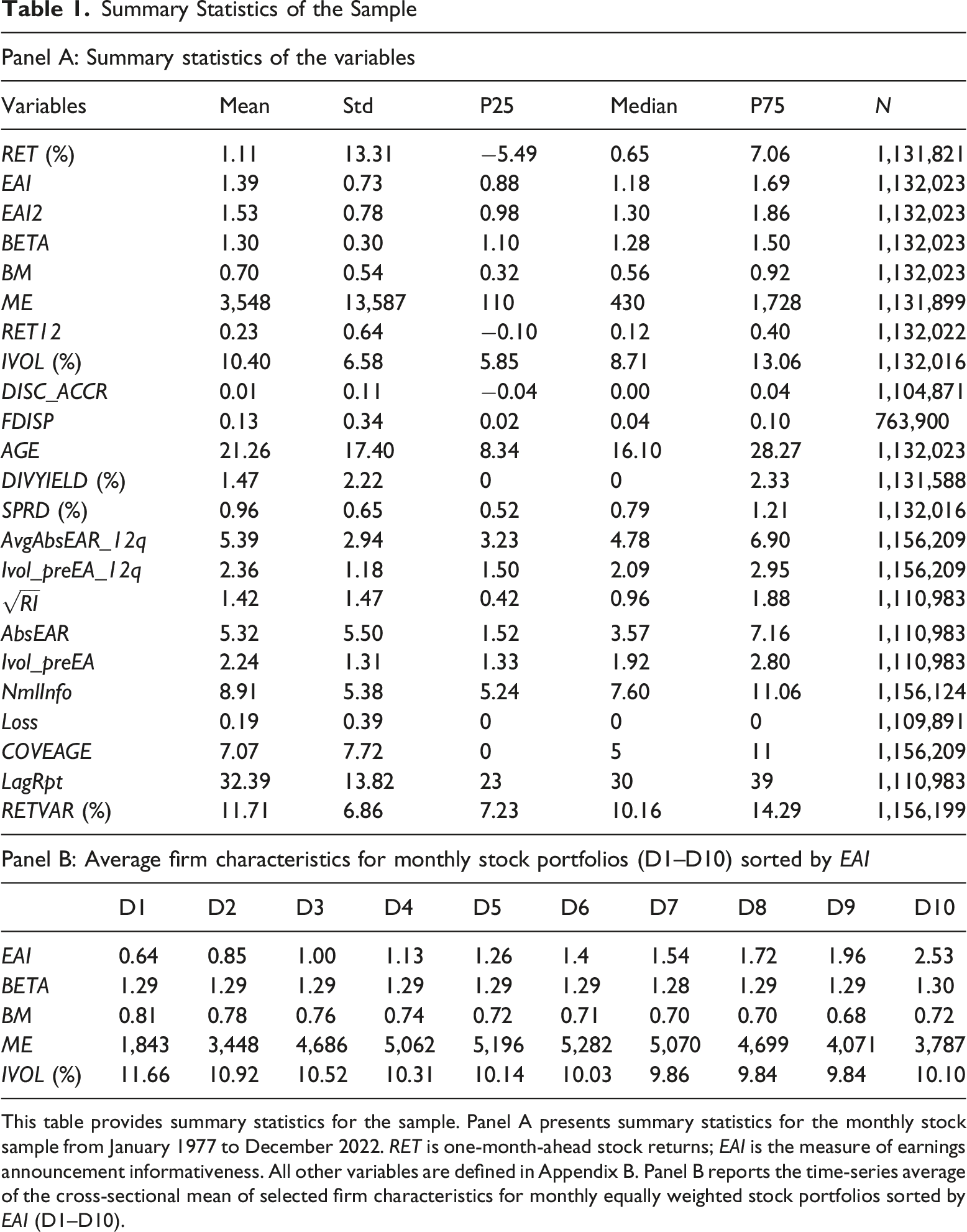

Summary Statistics of the Sample

We calculate various control variables that potentially explain expected stock returns. BETA represents the market beta; BM represents the book-to-market ratio; and ME stands for market equity, a proxy for firm size. The three variables are defined as in Fama and French (1992). RET12 signifies cumulative stock returns from month

Summary Statistics of the Sample

This table provides summary statistics for the sample. Panel A presents summary statistics for the monthly stock sample from January 1977 to December 2022. RET is one-month-ahead stock returns; EAI is the measure of earnings announcement informativeness. All other variables are defined in Appendix B. Panel B reports the time-series average of the cross-sectional mean of selected firm characteristics for monthly equally weighted stock portfolios sorted by EAI (D1–D10).

Empirical Analyses

Determinants of EAI

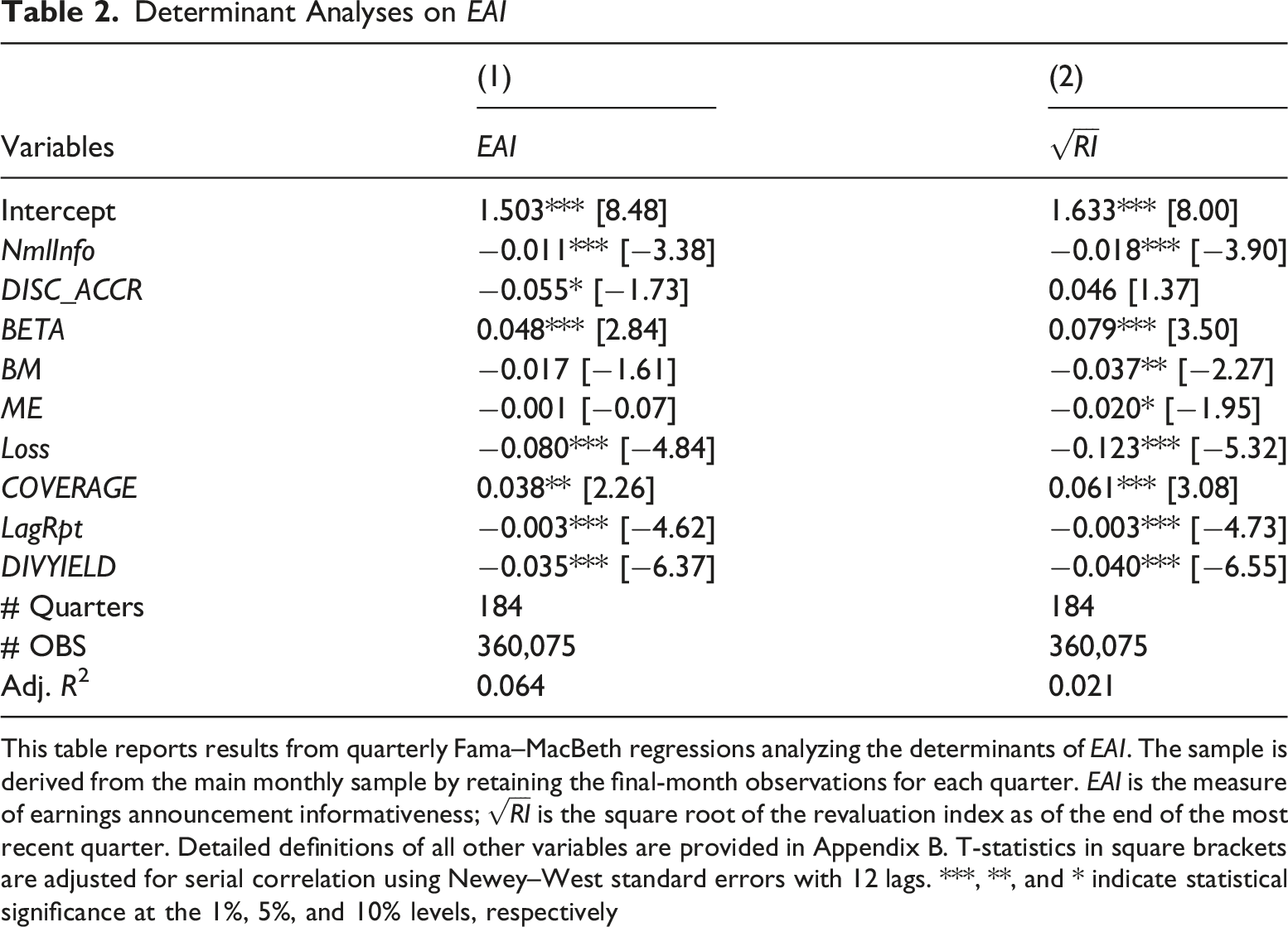

We conduct analyses to identify the factors influencing EAI. The normal information flow (NmlInfo), as defined by Thomas et al. (2022), measures the extent of information disclosures during the pre-announcement period, while discretionary accruals (DISC_ACCR) indicate the quality of earnings disclosure. 4 We anticipate that both variables will exhibit a negative relationship with EAI. This expectation is based on the rationale that a larger pre-announcement information flow renders the upcoming earnings announcement itself less informative, and similarly, lower earnings quality diminishes the informational value of the disclosure.

According to Beaver et al. (2018), the loss dummy (Loss), the number of analysts following (COVERAGE), and the reporting lag (LagRpt)—defined as the number of days between the fiscal period end and the announcement date—capture the temporary nature of losses, the monitoring effects of financial analysts, and information leakage prior to earnings announcements, respectively. Consequently, we expect that earnings announcements will be less informative for firms reporting a loss, more informative for those with greater analyst coverage, and less informative when there is a longer lag between the fiscal period end and the announcement.

In addition, we use market beta (BETA) to capture a firm’s systematic risk, while also controlling for the book-to-market equity ratio (BM) and firm size (ME). We posit that the earnings announcements of high-beta stocks, growth stocks (with lower BM), and smaller firms are more informative, as they help resolve a greater degree of uncertainty regarding the valuation of these particular types of stocks. Finally, the dividend yield (DIVYIELD) reflects the maturity of a firm and the challenge of firm valuation for investors (Grullon et al., 2002). We anticipate this variable will be negatively related to EAI, as there is inherently less uncertainty surrounding a more mature firm in the periods leading up to its earnings announcements.

The sample used in the determinant analyses is derived from our primary monthly sample by retaining observations from the final month of each quarter. The t-statistics in square brackets are adjusted for serial correlations using Newey–West standard errors with 12 lags.

Determinant Analyses on EAI

This table reports results from quarterly Fama–MacBeth regressions analyzing the determinants of EAI. The sample is derived from the main monthly sample by retaining the final-month observations for each quarter. EAI is the measure of earnings announcement informativeness;

Risk Premium of EAI

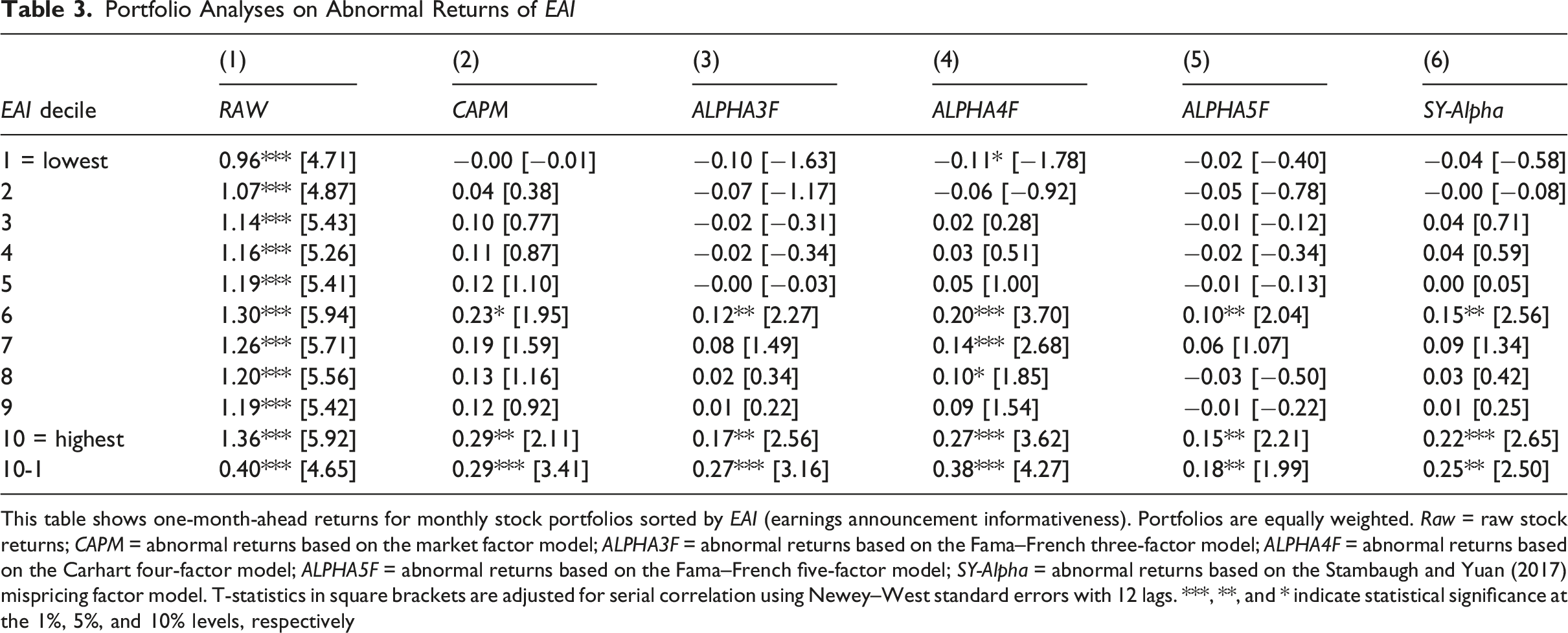

Our hypothesis is that there is a risk premium associated with the informativeness of earnings announcements. We begin by conducting stock portfolio analyses, in which we sort stocks into 10 portfolios based on their EAI and rebalance these portfolios on a monthly basis. Subsequently, we collect one-month-ahead returns for the composite stocks to calculate the equally weighted portfolio returns.

Portfolio Analyses on Abnormal Returns of EAI

This table shows one-month-ahead returns for monthly stock portfolios sorted by EAI (earnings announcement informativeness). Portfolios are equally weighted. Raw = raw stock returns; CAPM = abnormal returns based on the market factor model; ALPHA3F = abnormal returns based on the Fama–French three-factor model; ALPHA4F = abnormal returns based on the Carhart four-factor model; ALPHA5F = abnormal returns based on the Fama–French five-factor model; SY-Alpha = abnormal returns based on the Stambaugh and Yuan (2017) mispricing factor model. T-statistics in square brackets are adjusted for serial correlation using Newey–West standard errors with 12 lags. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% levels, respectively

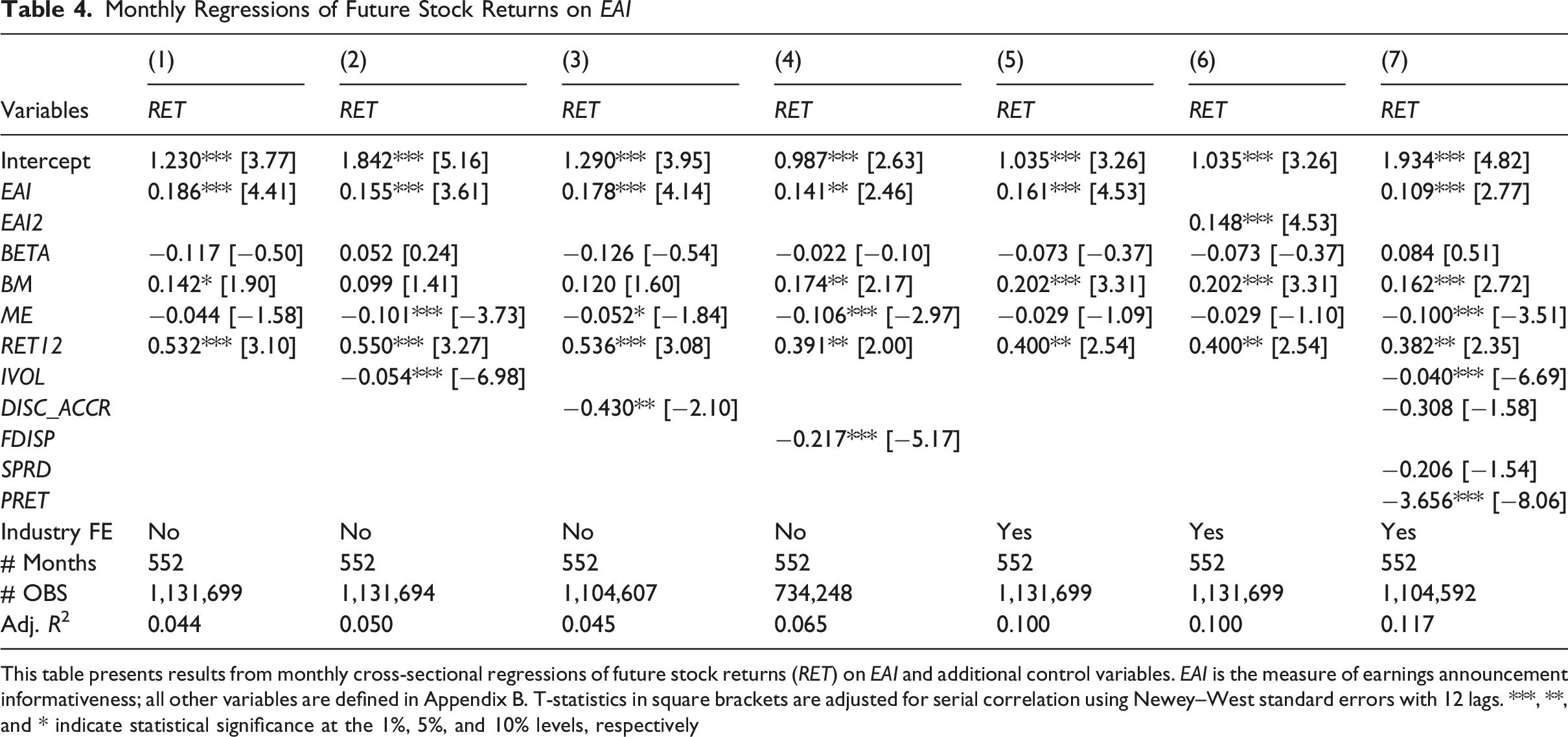

Next, we conduct monthly cross-sectional regressions to further investigate the effect of EAI on future stock returns

Monthly Regressions of Future Stock Returns on EAI

This table presents results from monthly cross-sectional regressions of future stock returns (RET) on EAI and additional control variables. EAI is the measure of earnings announcement informativeness; all other variables are defined in Appendix B. T-statistics in square brackets are adjusted for serial correlation using Newey–West standard errors with 12 lags. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% levels, respectively

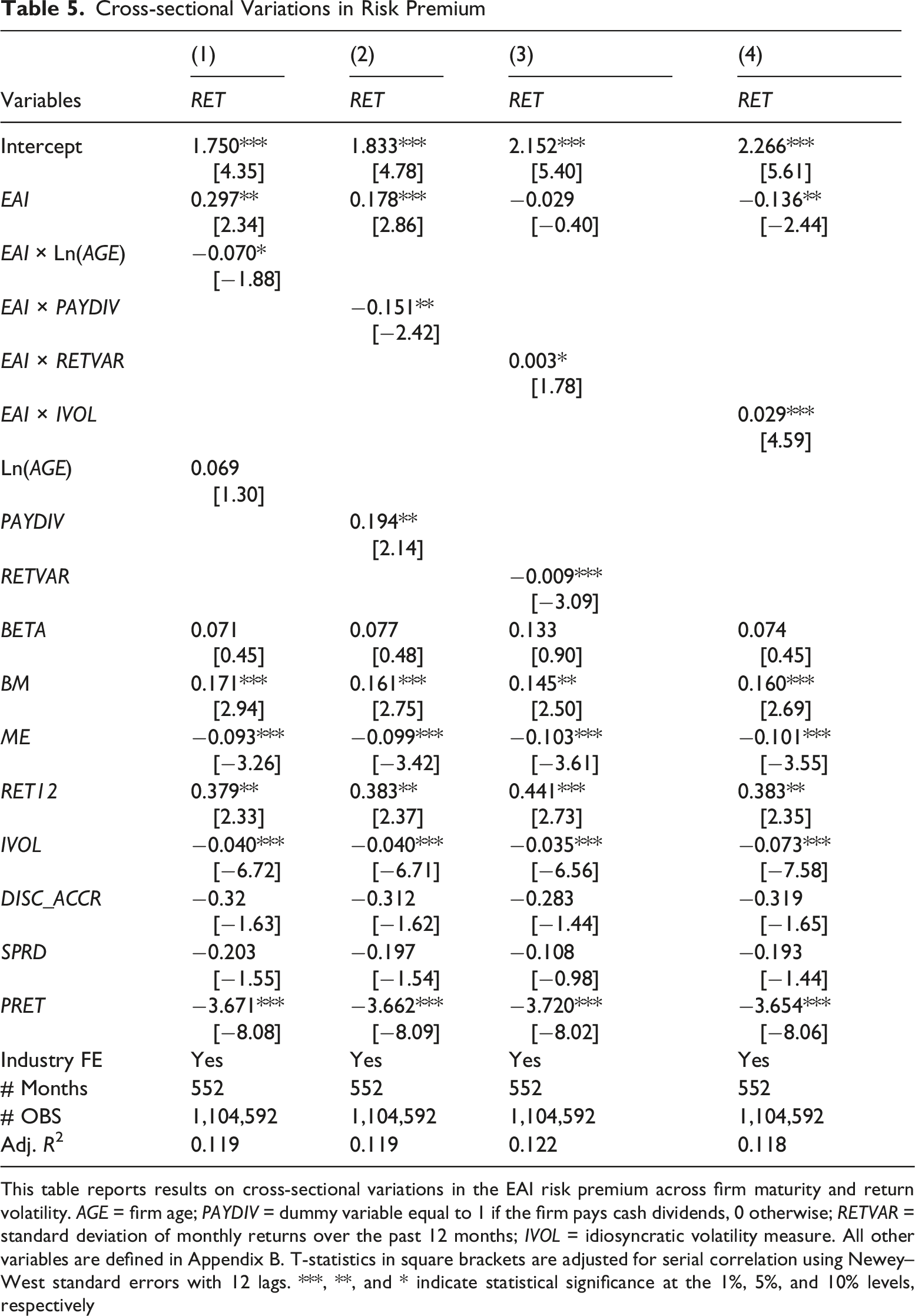

Variations in Risk Premium

This subsection examines variations in the EAI risk premium associated with both firm-level and market-level frictions. Specifically, we inspect firm maturity and information uncertainty as two indicators of firm-level frictions, based on the premise that they increase investors’ demand for information, thereby commanding a higher risk premium. Regarding market-level frictions, we investigate whether the pricing effect of EAI is amplified during periods of heightened investor risk aversion.

We expect a negative relationship between firm maturity and the EAI premium, as greater maturity indicates lower firm-level frictions. If a firm has operated for a long period and follows a stable business model, investors exhibit a lower appetite for information prior to earnings announcements. This is because investors possess tight priors regarding the firm’s value, and the marginal effect of learning from public disclosures or non-public information observed through stock prices is limited. Conversely, for investors in a young firm, lower information availability prior to an earnings announcement poses a more significant valuation challenge. This heightened uncertainty results in investors demanding a higher information risk premium. We use two proxies for firm maturity: firm age and a dividend payment dummy. A long operating history facilitates valuation (Easley & O’Hara, 2004; Kumar et al., 2008), as does the act of paying dividends, which signals financial stability (Grullon et al., 2002).

Furthermore, we expect a positive relationship between return volatility and the EAI premium. A large body of accounting literature interprets return volatility as a manifestation of information uncertainty, stemming either from a poor information environment or from inherent operational complexity (e.g., Gao et al., 2017; Jiang et al., 2005; Li et al., 2021; Lyle, 2025). Higher information uncertainty should command a greater information risk premium. When return volatility is elevated, the potential for both gains and losses in trading increases, thereby heightening investors’ stakes in the firm’s future prospects. In such an environment, investors demand more information to resolve uncertainty and require compensation for bearing the residual risk associated with the lack of information. Return volatility is specifically measured by the standard deviation of monthly stock returns over the past 12 months (RETVAR) or the idiosyncratic volatility from the last month (IVOL), as described in Ang et al. (2006). 10

Cross-sectional Variations in Risk Premium

This table reports results on cross-sectional variations in the EAI risk premium across firm maturity and return volatility. AGE = firm age; PAYDIV = dummy variable equal to 1 if the firm pays cash dividends, 0 otherwise; RETVAR = standard deviation of monthly returns over the past 12 months; IVOL = idiosyncratic volatility measure. All other variables are defined in Appendix B. T-statistics in square brackets are adjusted for serial correlation using Newey–West standard errors with 12 lags. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% levels, respectively

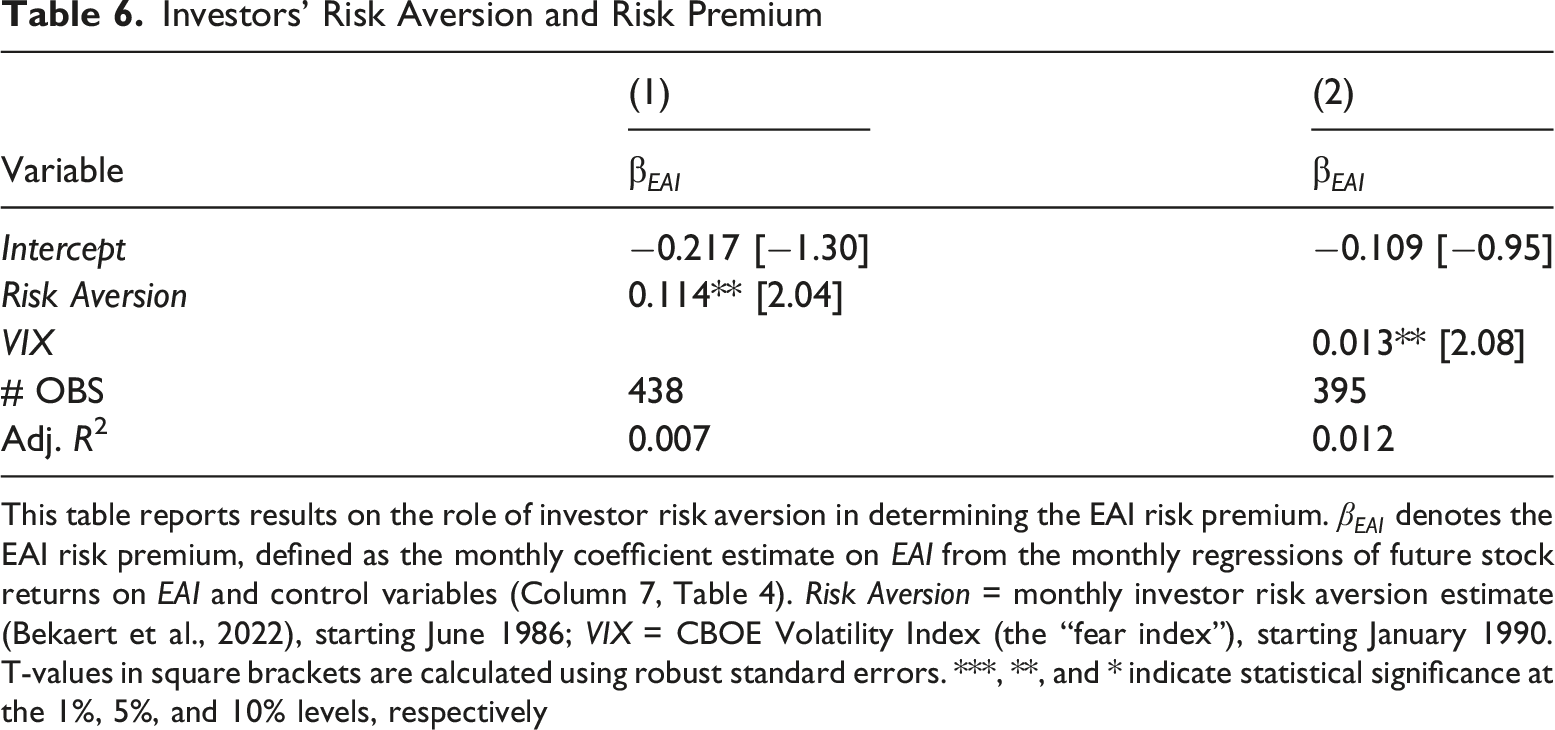

Regarding market-level frictions related to investor risk aversion, we expect a positive relationship with the EAI premium. This is consistent with the fundamental financial principle that higher risk aversion necessitates greater compensation. Each month, a cross-sectional regression of stock returns on EAI and control variables—as shown in column (7) of Table 4—produces a coefficient estimate on EAI denoted as

Investors’ Risk Aversion and Risk Premium

This table reports results on the role of investor risk aversion in determining the EAI risk premium.

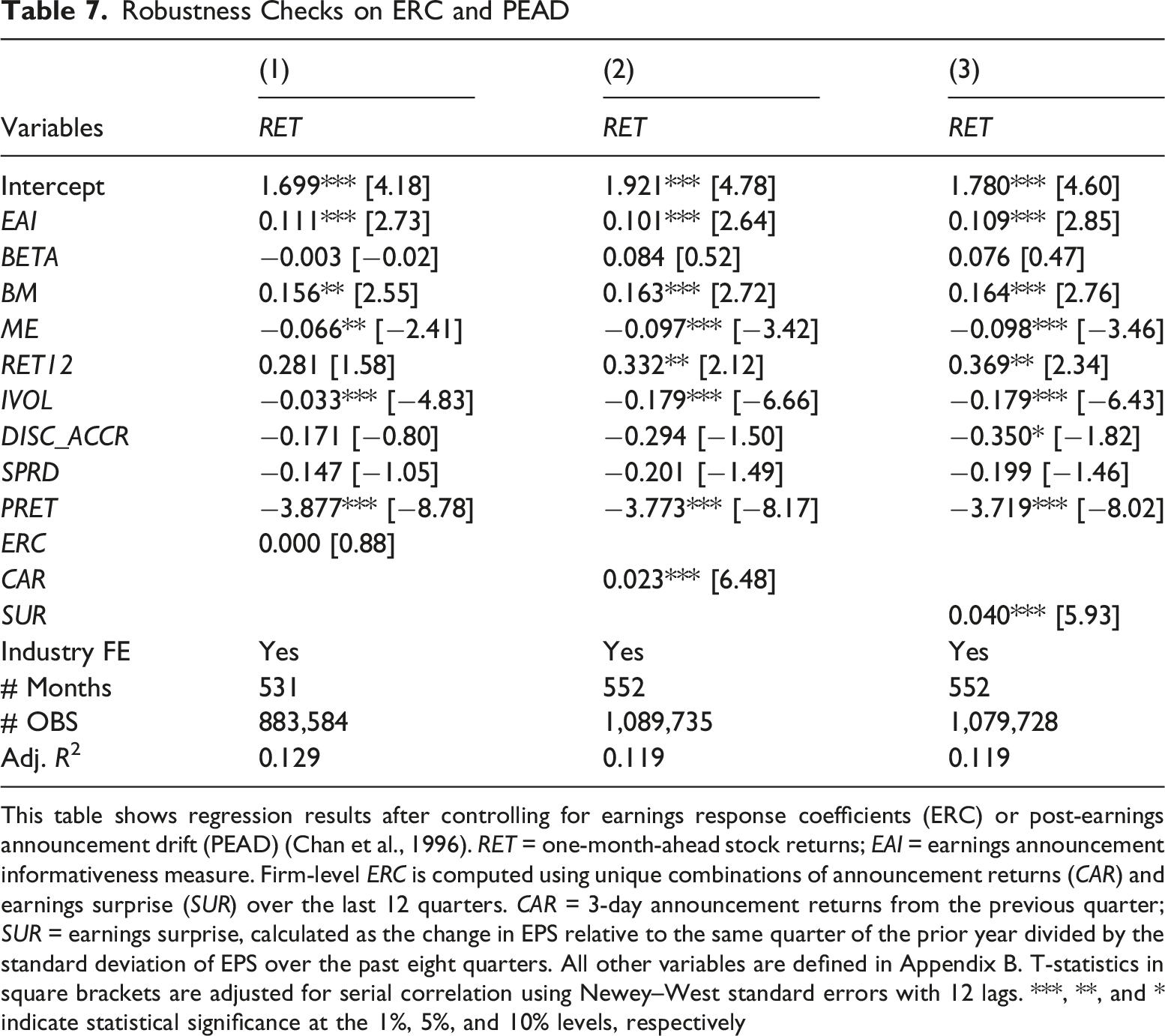

Control for ERC or PEAD

Robustness Checks on ERC and PEAD

This table shows regression results after controlling for earnings response coefficients (ERC) or post-earnings announcement drift (PEAD) (Chan et al., 1996). RET = one-month-ahead stock returns; EAI = earnings announcement informativeness measure. Firm-level ERC is computed using unique combinations of announcement returns (CAR) and earnings surprise (SUR) over the last 12 quarters. CAR = 3-day announcement returns from the previous quarter; SUR = earnings surprise, calculated as the change in EPS relative to the same quarter of the prior year divided by the standard deviation of EPS over the past eight quarters. All other variables are defined in Appendix B. T-statistics in square brackets are adjusted for serial correlation using Newey–West standard errors with 12 lags. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% levels, respectively

To check the robustness of our results with respect to PEAD, we control for CAR or SUR from the preceding quarter. As shown in columns (2) and (3) of Table 7, the coefficient associated with EAI remains statistically significant. It is important to note that PEAD is generally attributed to behavioral biases among investors (Fink, 2021). In contrast, we believe that the return predictability of EAI is a product of investors’ rational response to information risk. Furthermore, while PEAD exhibits an inverse relationship with firm size, our unreported analysis indicates that the return predictability of EAI does not show a significant relationship with firm size. 13

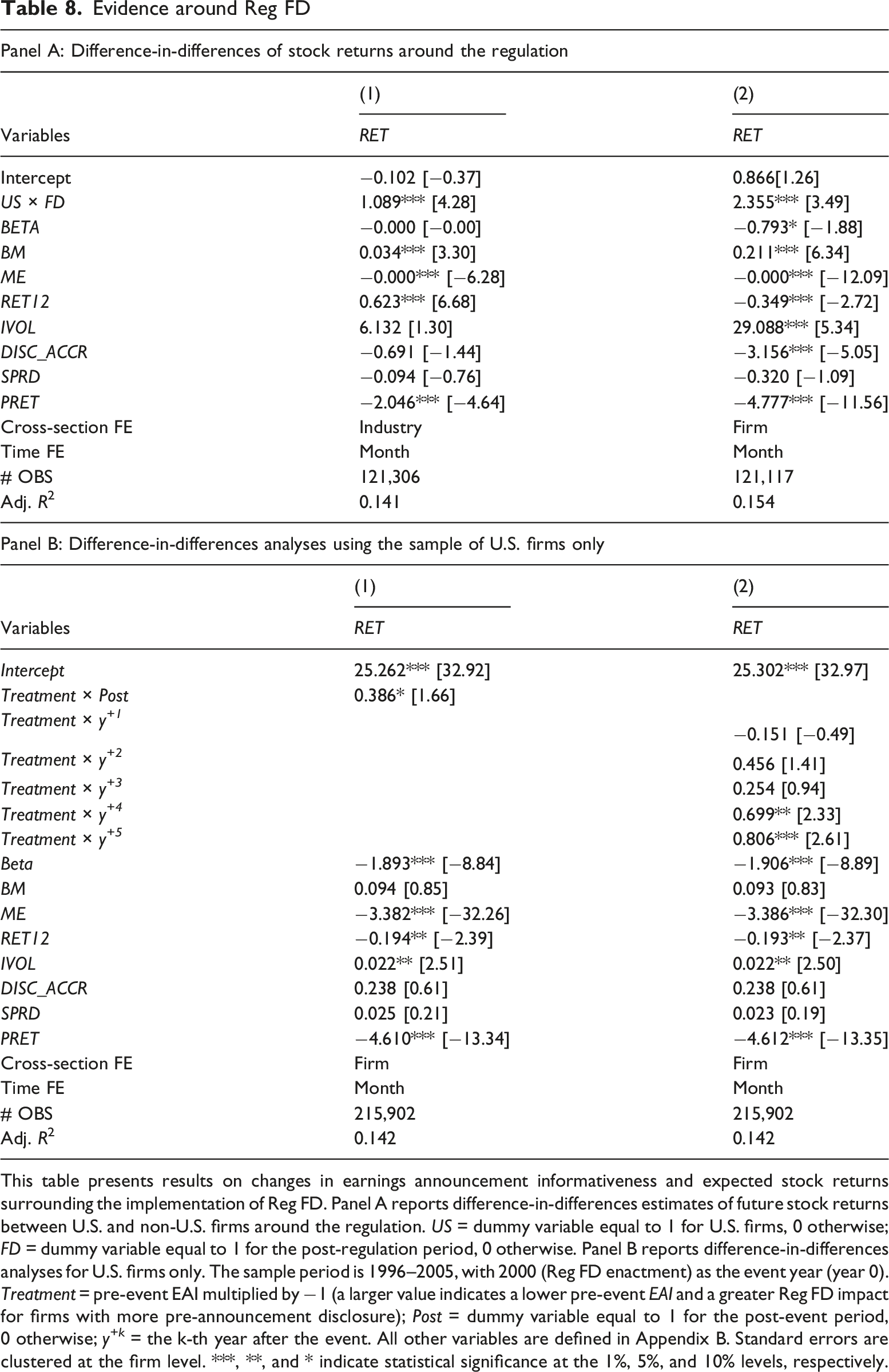

Evidence Around Reg FD

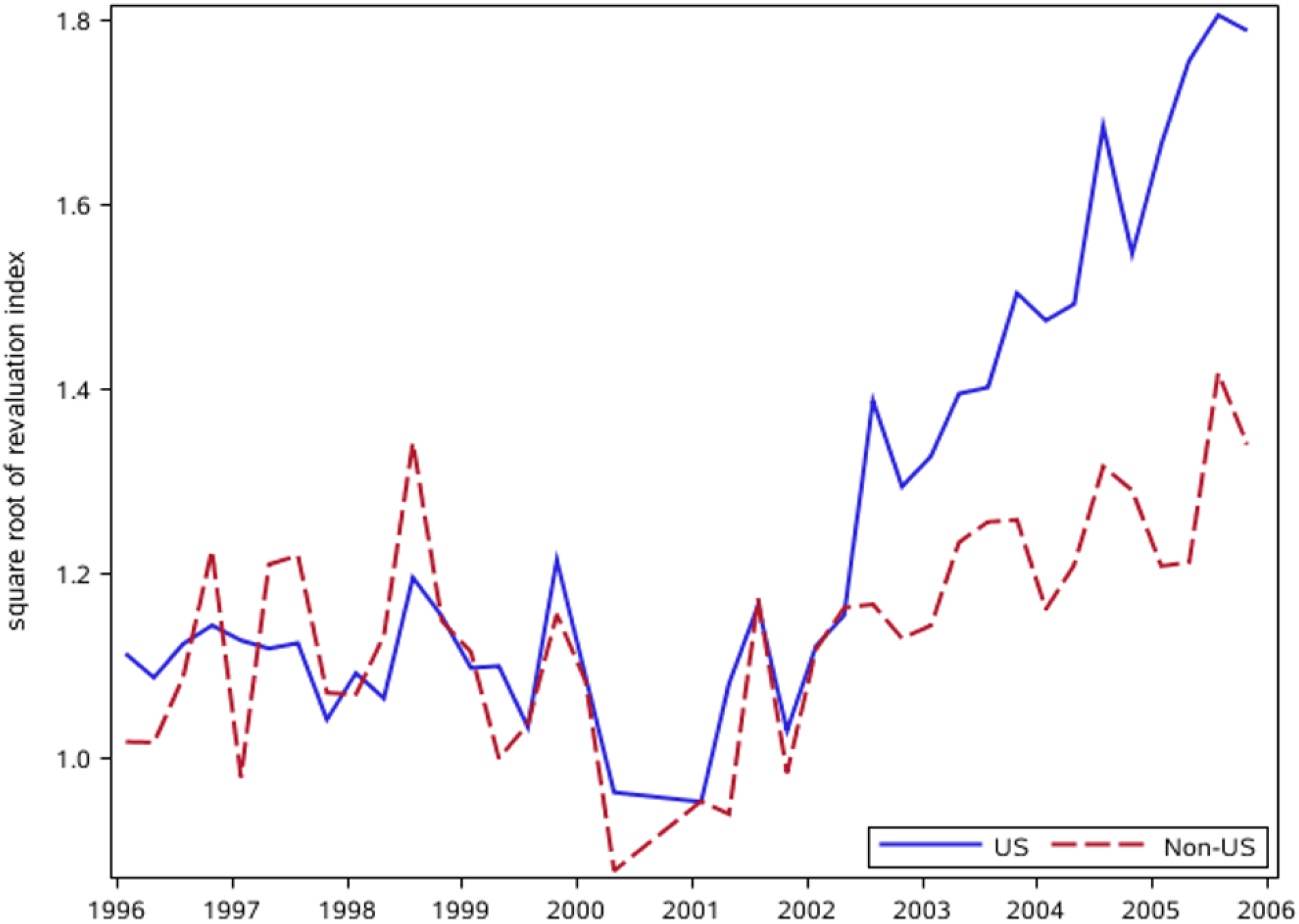

The relationship between EAI and expected stock returns could be endogenous. To strengthen causal inferences, we rely on Reg FD, which became effective on October 23, 2000. This regulation prohibits selective disclosures of material information to investors—including financial analysts and institutional investors—by U.S. firms, while allowing such disclosures for foreign ADR firms (Francis et al., 2006; Litvak, 2007). As a result, investors in U.S. firms have to rely more heavily on public disclosures (Kross & Suk, 2012), making upcoming earnings announcements more informative. This, in turn, elevates information risk and further increases expected stock returns (Easley & O’Hara, 2004).

Following Francis et al. (2006) and Litvak (2007), we conduct a difference-in-difference (DID) test. In particular, we consider U.S. firms as the treatment group and non-U.S. ADR firms as the control group. We analyze the difference between the two groups of firms around Reg FD to determine the relationship between EAI and expected stock returns. The regression model is as follows

The sample comprises monthly data from U.S. and ADR firms (including Canadian companies) spanning the years 1996 to 2005. In accordance with Fama and French (1992), we stipulate that the lagged book equity must be positive and that the lagged stock price exceeds US $5. Following the methodology of Francis et al. (2006), we exclude the last two quarters of 2000 from our analyses, as they are associated with regulatory discussions and implementation. The analyses are confined to a 16-quarter period centered around the enactment of the regulation. This narrow time frame minimizes the influence of unobserved confounding factors (Brogaard et al., 2017).

Figure 2 illustrates the quarterly average Mean

Evidence around Reg FD

This table presents results on changes in earnings announcement informativeness and expected stock returns surrounding the implementation of Reg FD. Panel A reports difference-in-differences estimates of future stock returns between U.S. and non-U.S. firms around the regulation. US = dummy variable equal to 1 for U.S. firms, 0 otherwise; FD = dummy variable equal to 1 for the post-regulation period, 0 otherwise. Panel B reports difference-in-differences analyses for U.S. firms only. The sample period is 1996–2005, with 2000 (Reg FD enactment) as the event year (year 0). Treatment = pre-event EAI multiplied by −1 (a larger value indicates a lower pre-event EAI and a greater Reg FD impact for firms with more pre-announcement disclosure); Post = dummy variable equal to 1 for the post-event period, 0 otherwise; y +k = the k-th year after the event. All other variables are defined in Appendix B. Standard errors are clustered at the firm level. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% levels, respectively.

The Reg FD effects described above are likely to vary across U.S. firms. To test this conjecture, we conduct DID analyses using the sample of U.S. firms only. Specifically, we use pre-event EAI (multiplied by −1) as a proxy for treatment intensity (denoted as Treatment) from Reg FD. The rationale is that firms with lower pre-event EAI previously disclosed more information prior to their earnings announcements. These firms were subject to a greater impact from Reg FD, as the regulation restricted their ability to engage in such selective disclosure.

Panel B of Table 8 presents the results of regressions controlling for firm and year fixed effects, based on a subsample of monthly U.S. stocks from the period of 1996 to 2005. Column (1) reveals a positive coefficient for the interaction term

Robustness Tests

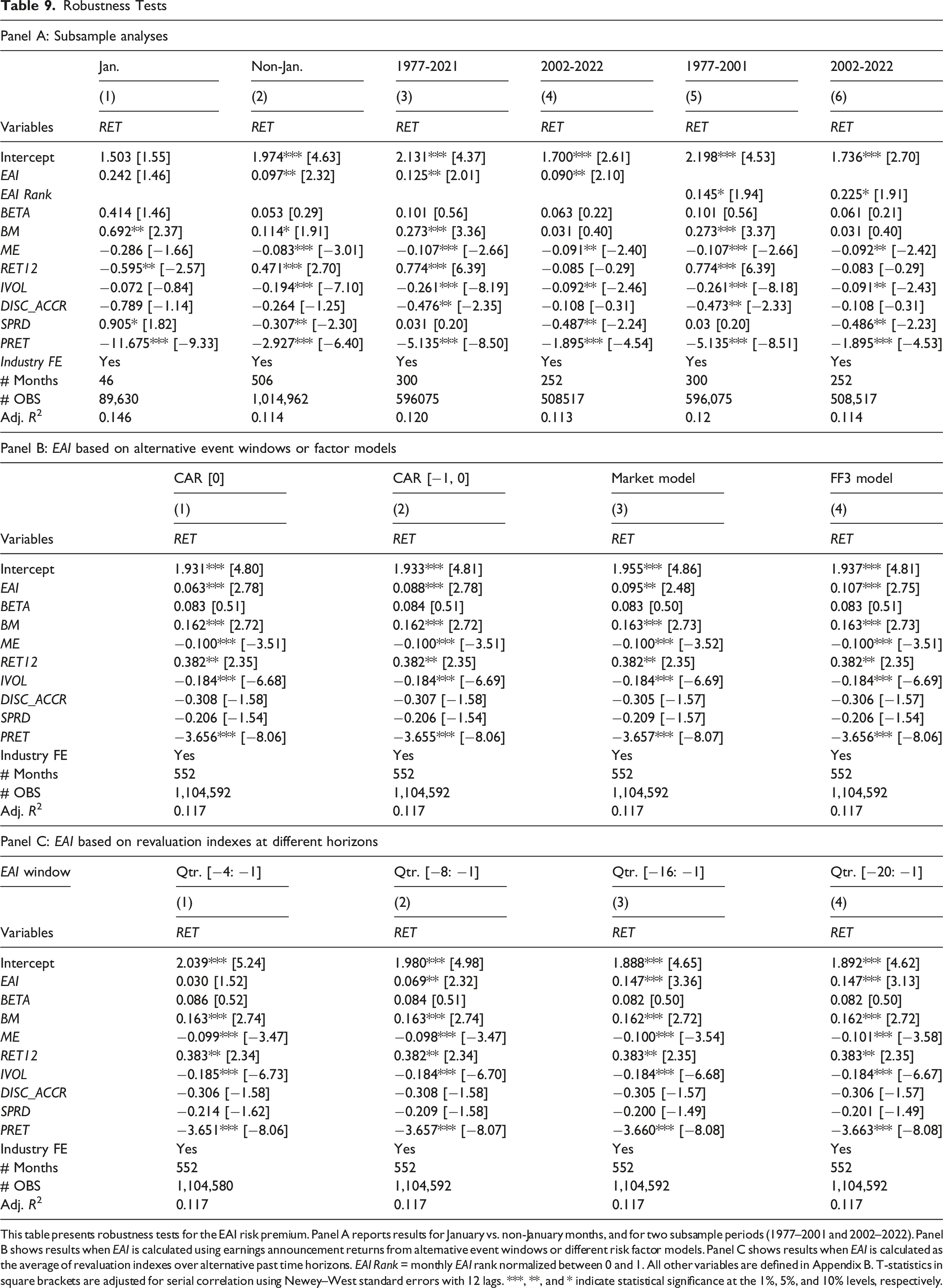

This section presents several robustness tests. Kim (2006) identifies a common risk factor associated with earnings volatility that explains stock returns in January. To distinguish our findings from Kim’s, we must determine whether our results are specific to January. Additionally, it is important to ascertain whether our findings are confined to a particular historical period. Return predictability resulting from mispricing may diminish over time as investors become more informed. 15 However, return predictability stemming from a risk premium can persist across all periods if the associated risks do not dissipate.

Robustness Tests

This table presents robustness tests for the EAI risk premium. Panel A reports results for January vs. non-January months, and for two subsample periods (1977–2001 and 2002–2022). Panel B shows results when EAI is calculated using earnings announcement returns from alternative event windows or different risk factor models. Panel C shows results when EAI is calculated as the average of revaluation indexes over alternative past time horizons. EAI Rank = monthly EAI rank normalized between 0 and 1. All other variables are defined in Appendix B. T-statistics in square brackets are adjusted for serial correlation using Newey–West standard errors with 12 lags. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% levels, respectively.

Panel B demonstrates the robustness of our results across various event windows and risk factor models used to calculate earnings announcement returns. Panel C shows that the results remain robust across different time horizons when measuring the informativeness of earnings announcements. The coefficient estimates on EAI are all statistically significant, based on the average root of revaluation indexes taken over the past 4, 8, 16, and 20 quarters. Thus, EAI seems to have a long-lasting impact on expected stock returns, a characteristic of risk premiums.

Conclusion

Volatile earnings announcements suggest that investors lacked sufficient information about the firm during the pre-announcement period. Limited information availability prior to earnings announcements exposes investors to information risk, as outlined in the theory proposed by Easley and O’Hara (2004). Their theory posits that having more information is preferable to having less at any given moment. If the informativeness of earnings announcements is a function of information that is not disclosed to all investors in advance, rational investors should anticipate a risk premium associated with this lack of information.

Consistent with the aforementioned prediction, the informativeness of earnings announcements is positively correlated with future stock returns in a sample of U.S. stocks spanning from 1977 to 2022. Furthermore, the return premium associated with earnings announcement informativeness is greater for younger firms, those that do not distribute cash dividends, and stocks exhibiting high return volatility. This effect is particularly pronounced during periods of heightened investor risk aversion. Notably, there is robust evidence indicating that, following the implementation of Reg FD, a reduction in information supply led to a higher cost of capital. Our study contributes to the existing literature on the informativeness of earnings announcements by elucidating its economic implications. It underscores the timeliness of information disclosure as a critical factor for investors and provides new insights into the impact of Reg FD on public firms, thereby enriching policy discussions.

Footnotes

Acknowledgments

We thank Xiao-Jun Zhang, Bohui Zhang, Stephen Dimmock, Chuan-Yang Hwang, Simba Xin Chang, Chenkai Ni, and the participants of the 2018 China Finance Review International Conference for their helpful comments.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We acknowledge financial support from the National Natural Science Foundation of China [72221001, 72132006, 72372097, 72521002], National Social Science Fund of China [22AZD034], the Shuguang Program [23SG31], the Program for Innovative Research Team of SUFE, and the MOE Project of Key Research Institute of Humanities and Social Science in University [23JJD790010] and the 111 Project [B18033]. All errors are our own responsibility.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.