Abstract

Corporate diversification, a major strategic management research topic, has been influenced significantly by resource-based theory. In this review, the authors make two main contributions to this literature. First, they discuss the historical development of corporate diversification research employing the resource-based theory perspective and related concepts, highlighting important insights to date. They then review this literature and discuss its main contributions. Second, the authors identify open issues and suggest opportunities for future contributions and describe ways that research on corporate diversification using the resource-based theory perspective could be further enriched by integration with theoretical insights culled from the organizational economics, new institutional economics, and industrial organization economics literatures.

Since the pioneering work by Wernerfelt (1984) and Barney (1991), the resource-based theory’s (RBT’s) impact on the field of strategic management, as well as many other academic disciplines, has been enormous. The roots of RBT can be traced to a number of intellectual origins, including Phillip Selznick in the 1950s and even as early as David Ricardo in the 19th century. Earlier developments notwithstanding, Edith Penrose’s (1959) seminal work The Theory of the Growth of the Firm is widely regarded as providing an important intellectual lineage for RBT (Kor & Mahoney, 2004). In her work, Penrose explored the relationship between firm resources and firm growth. In a departure from neoclassical microeconomics, she noted that firms should be conceptualized as an administrative framework consisting of a bundle of resources, and thus, she concluded that the growth of a firm is limited by this crucial aspect of a firm. Penrose’s work not only represents an important research tradition in the subsequent development of RBT but also serves to provide a theoretical underpinning for the study of firm growth in the form of corporate diversification from the perspective of firm resources and capabilities.

Our review focuses on the impact of RBT on corporate diversification research in strategic management. 1 The topic of corporate diversification represents one of the most important research areas in the field of business (Hoskisson & Hitt, 1990; Palich, Cardinal, & Miller, 2000). Research on corporate diversification first captured the attention of industrial organization (IO) economists who examined the relationship between diversification and market power (e.g., Arnould, 1969; Berry, 1971; Gort, 1962; Utton, 1979). Theoretically, organizational economists approached the topic of corporate diversification largely premised on agency theory and transaction cost economics (e.g., Jensen & Meckling, 1976; Williamson, 1975). At the same time, strategic management scholars were also attracted to the study of corporate diversification. Rumelt’s (1974) pioneering research was the most notable work on the topic that spawned many subsequent studies (e.g., Bettis, 1981; Christensen & Montgomery, 1981; Hoskisson, 1987). Although strategic management scholars also drew on insights developed in IO economics and organizational economics to study corporate diversification, the most important contributions stemming from strategic management scholars centered on investigating whether or not related diversification would benefit firm performance.

While corporate diversification was first studied from an IO economics perspective, subsequent development in diversification research from an organizational economics perspective was complemented with and challenged by the rise of RBT in the diversification literature in strategic management. The introduction of RBT in the 1980s and 1990s, along with closely related ideas, such as distinctive competence (Hitt & Ireland, 1985), dominant logic (Prahalad & Bettis, 1986), and core competence (Prahalad & Hamel, 1990), offered a unified theoretical framework for the broad corporate diversification research stream that emphasizes the importance of firm resources. In addition, because RBT offered a novel theoretical lens to view corporate diversification, RBT quickly emerged as the key theoretical foundation that fueled a thriving development of the diversification literature in strategic management. It is important to note that such a research focus on relatedness in corporate diversification was uniquely developed in the strategic management field, given the theoretical focus based on RBT that was not found in economics and finance literatures. Although previous work focused on descriptive treatises of diversification in the United States (Berry, 1971; Gort, 1962) and the United Kingdom (Utton, 1979) from the IO economics perspective, Rumelt’s work published in 1974 predominantly emphasized the importance of relatedness and firm performance. Once RBT paradigm was proposed, its impact propelled more work specifically focused on relatedness. Interestingly, recent advances in RBT appear to point toward a potential integration with organizational economics such that a firm’s core resources (from RBT) influence incentives to pursue asset-specific investments (Wang & Barney, 2006). Additionally, further integration of RBT and new institutional economics may be especially fruitful for corporate diversification research through comparing diversification effects in different cross-country institutional contexts (Wan & Hoskisson, 2003).

Our article posits that the developmental path of corporate diversification research based on RBT continues to hold a great deal of promise for the future enrichment of the literature. This development includes the expansion of corporate diversification in many countries, especially those that have institutional environments vastly different from that of the United States, including emerging and transition economies (Hoskisson, Eden, Lau, & Wright, 2000). Research focused on national institutional differences and corporate diversification is largely based on the theoretical insights developed in the new institutional economics 2 and related disciplines (e.g., Guillén, 2000; Khanna & Palepu, 2000; Peng, 2003; Wan & Hoskisson, 2003). At the same time, recent theoretical advances in RBT indicate that exploring the intersection between RBT and organizational economics holds great promise (e.g., Wang & Barney, 2006). Such theoretical development has the potential to offer fruitful opportunities for RBT to further enrich research on corporate diversification, especially in relation to comparative, cross-country research.

In the remainder of our article, we discuss the past accomplishments of the corporate diversification literature premised on RBT and closely related concepts, which also allows us to identify open issues and unanswered questions in this literature. Accordingly, we examine future opportunities, especially in relation to theoretical and research integration between RBT and other conceptual frameworks, to help advance the research on corporate diversification.

Historical Development of RBT and Diversification Research

Early research relying on a resource-based perspective (Penrose, 1959) did not capture a great deal of attention in the field of economics; however, such theoretical progress was intriguing to strategy researchers who were interested in understanding variance in firm growth and performance from an organizational-level perspective (e.g., Barney, 1986a, 1986b, 1991; Conner, 1991; Dierickx & Cool, 1989; Rumelt, 1984; Wernerfelt, 1984). This line of research in strategic management eventually developed into RBT (Mahoney & Pandian, 1992; Peteraf, 1993). In essence, two fundamental assumptions underlie RBT. First, different firms possess different bundles of resources and capabilities, and some firms within the same industry may perform certain activities better than the others based on these resource differences (Barney, 1991; Dierickx & Cool, 1989). Second, resource differences among firms can be persistent (less mobile) due to rarity and difficulties in acquiring or imitating those resources and capabilities (Barney, 1986a, 1991; Reed & DeFillippi, 1990). Such premises are in stark contrast to the neoclassical economics assumption that assets are comparatively mobile across firms.

Penrose’s focus on firm growth and the subsequent development of RBT provided a much needed theoretical basis for an important, new theoretical perspective for diversification research. First and foremost, it is firm resources (rather than market factors) that limit the potential growth and the choice of businesses for a firm (Penrose, 1959). In other words, a firm will have an incentive to diversify if it possesses the necessary, excess resources to make diversification economically feasible (Teece, 1982; Wernerfelt, 1984). In addition, although resource immobility prevents other firms from easily acquiring or imitating a firm’s resources, it also implies that a firm may find it difficult to sell some of its excess unique resources in the market (Lippman & Rumelt, 1982; Nelson & Winter, 1982). In contrast, transferring such resources to related businesses within a firm represents an optimal strategy because the marginal costs of using these resources within the existing industry are often minimal, but the benefits of using them in another business unit can be substantial (Barney, 1997; Porter, 1985). As such, RBT suggests that a firm’s level of diversification and its performance are significantly influenced by its resources and capabilities.

Diversification: RBT and Theory and Research in Strategic Management

From the perspective of RBT, diversification research posits that related diversification can lead to superior firm performance, compared to that of a focused strategy, because firms can maximize their resources across several businesses to realize additional returns. Operational economies of scope as afforded by related diversification facilitate a firm to assemble a portfolio of businesses that are mutually reinforcing, as critical resources can be shared among business units (Barney, 1997). When viewing the benefits of diversification from this perspective, firms with related diversification strategies can outperform those with unrelated diversification strategies. To the extent that the key to superior performance from a diversification strategy is contingent on the ability to share resources, a firm that is diversified into unrelated businesses is unlikely to have resources that can be useful for all its business units. At the same time, it becomes challenging for the firm’s top management to manage an increasingly diverse business portfolio (Grant, Jammine, & Thomas, 1988; Hill & Hoskisson, 1987; Jones & Hill, 1988). Taken together, diversification researchers employing RBT perspective tend to suggest that levels of diversification likely exhibit an inverted U-shaped relationship with firm performance (Palich et al., 2000). In essence, diversification research premised on RBT holds that strategic interrelationships based on resource relatedness shared by business units within the firm contribute to superior performance and thus increase firm value to the point where resources become too complex to manage or business units become unrelated.

RBT and Diversification Research in Other Disciplines Compared

To date, various disciplines have contributed to our knowledge of diversification, but such knowledge has been accompanied by each discipline’s own theoretical paradigms and corresponding research agendas (Hoskisson & Hitt, 1990). The fields of IO economics and finance have continued to follow the general economics assumption of relative market perfection and thus view diversification as a largely unnecessary, suboptimal, or even illegitimate decision induced by managers’ self-interested motives. In a relatively perfect market, IO economics views corporate diversification as an anomaly, and consequently, firms are unlikely to derive long-term abnormal profits from diversification (Scherer, 1980). The field of finance has largely embraced the agency theory perspective to study diversification. This worldview of relative market perfection assumes that diversification has no place in a “rational” world, and so the presence of diversification is a manifestation of agency costs (e.g., Amihud & Lev, 1981). As a consequence, diversification is rightly and appropriately discounted by the (perfect) market according to the logic of financial economics. It is therefore not surprising to find that the field of finance is largely silent on the issue of related diversification. However, if the market is not perfect, then abnormal returns from diversification become possible. In fact, some recent studies in finance (e.g., Campa & Kedia, 2002; Villalonga, 2004) found that the diversification discount may not be caused by diversification once the underlying factors leading to firm diversification are taken into account.

In contrast to research stemming from various economics perspectives, RBT operates on the assumption that the market is imperfect, and as such, it is natural that there are important theoretical complementarities between RBT and transaction cost economics in general and with relevance to diversification specifically. To the transactional cost paradigm, diversification is an outcome of high exchange hazards in the (imperfect) market. In line with the core domain of the field of management, RBT, though recognizing the relevance of transaction costs in the imperfect market, emphasizes the central role of the firm and managers in creating value based on such market imperfections. Firms formulate and implement strategies to create and extract value from the resources they possess. Managers no longer are inherently self-interested but, rather, are potentially the key resource if a diversification strategy is to create value. As organizational stewards, firm executives create synergistic value from firm resources as one of the hallmarks of good management. Viewed from this perspective, diversification, and especially related diversification, is not just a symbol of transaction cost minimization but has the potential to add significant value to the firm. In this regard, RBT’s contribution is significant in that it offers a strong theoretical logic that can explain and examine diversification in general and related diversification in particular.

Diversification research rooted in strategic management has been interested in the importance of resources and related diversification for over a quarter of a century. Early works in connection with related diversification explored the idea of economies of scope and resource sharing among diversified firms (e.g., Hoskisson, 1987; Nayyar, 1993). Explicit attention by diversification researchers to the crucial importance of resources was first evident in the works of Rumelt (1982), Wernerfelt (1984), and Barney (1991). Viewed from RBT perspective, corporate diversification can be seen in a new light. In explaining why related diversification leads to higher performance than either focused strategy or unrelated diversification, Rumelt posited that the success of related diversification lies in firm-level capabilities such as the economies of shared factors of production. He called such elements that enable diversification “core factors.” According to his view, highly idiosyncratic core factors induce relatedness among the sharing businesses and also indicate the presence of intangible assets; thus, a relationship exists between core factor idiosyncrasy and firm performance. Likewise, Wernerfelt (1984) noted the importance of firm resources and how they provide a basis for understanding important issues about firm growth and diversification, such as the firm’s current resources on which diversification should be based and the resources that should be developed through diversification.

Barney’s (1991) article, although not addressing diversification specifically, offered a crucial theoretical reasoning to explain why firms diversify. It reiterated the importance of resource immobility and resource heterogeneity to argue that, when resources are bundled strategically, a firm’s competitive advantage can be long lasting. To the extent that the resources are valuable, rare, imperfectly imitable, and nonsubstitutable, a firm can utilize its resources to optimally diversify into new businesses. These resources cannot be easily purchased in the open market (Barney, 1986b), and so a firm has to rely on existing resources to diversify (Barney, 1991). The RBT perspective on diversification is not based on the premise of economics that external market failure encourages firms to engage in internal growth; rather, it provides an internal resource perspective that underscores firms’ motivation to maximize their resources by diversifying into (related) businesses. This premise represented a new, important theoretical worldview in the study of diversification. Several theoretical works closely related to RBT were also developed in the 1980s. Among those that had more direct relevance to diversification research are distinctive competence (Hitt & Ireland, 1985), dominant logic (Prahalad & Bettis, 1986), and core competence (Prahalad & Hamel, 1990). Like RBT, these works emphasized the role of internal resources in explaining diversification. Subsequent application and development of these theoretical arguments and concepts in diversification research had continued to complement the central tenets of RBT.

Reviewing Research Incorporating RBT and Diversification

To provide a systematic review of relevant research examining RBT’s influences on corporate diversification research, we first reviewed relevant insights appearing in management and international business journals. We used the EBSCO database, ABI/Inform database, and Google Scholar to search for all articles that were published since 1980. We began the search from 1980 because diversification research prior to this period was mostly premised on IO economics and organizational economics. We searched key words and phrases including diversification, diversified, multi-business, multi-product, scope of the firm, and business group in the titles, keywords, or abstracts of published works. We then examined each article to determine if it was theoretically premised on RBT or closely related concepts in its core argument. This process yielded 64 articles. Journals where articles are identified include leading journals such as Academy of Management Journal, Academy of Management Review, Journal of Management, and Strategic Management Journal, as well as other outlets where diversification scholars publish their works such as Asia Pacific Journal of Management, Journal of Management Studies, and Organization Studies. Table 1 provides a summary of these articles.

Diversification Articles Premised on Resource Based Theory and Closely Related Concepts

Note: For the primary research area, 1 = types of resources, 2 = resource sharing, 3 = financial performance, 4 = dynamic capabilities, 5 = knowledge/organizational searching, and 6 = the institutional environment, as delineated in Figure 1.

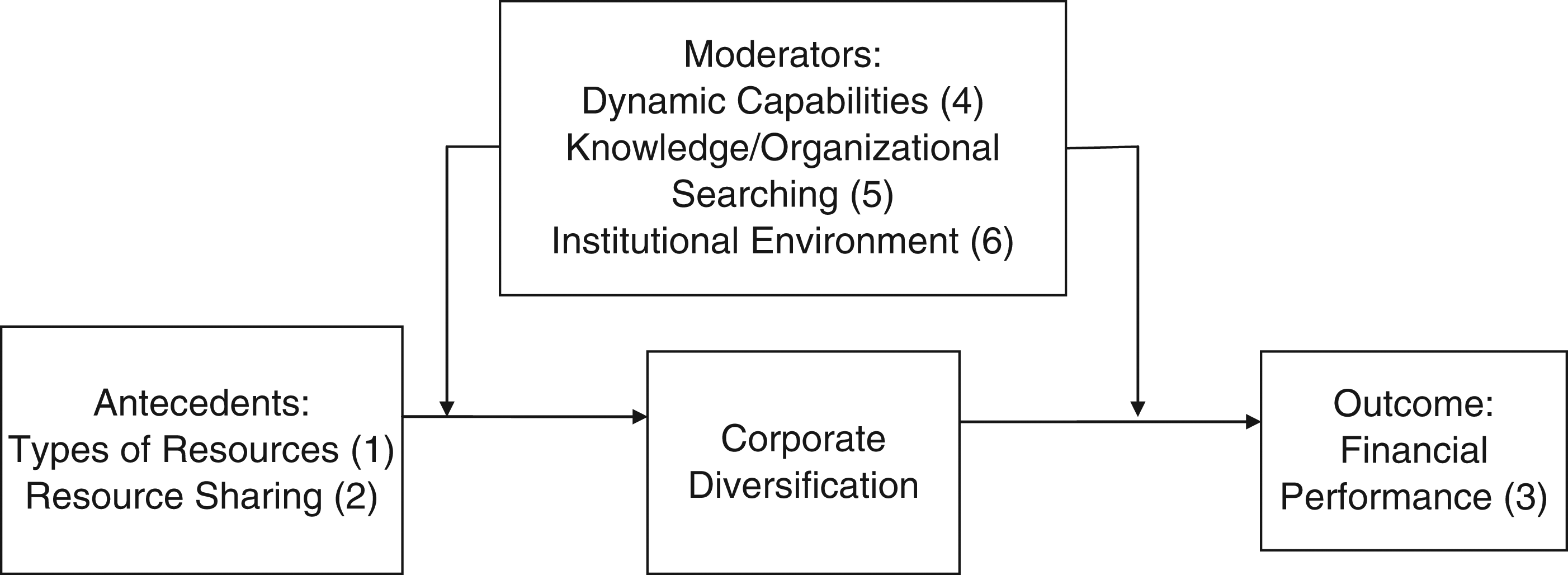

Following previous reviews published in the Journal of Management (e.g., Combs, Ketchen, Shook, & Short, 2010), we outline antecedents, outcomes, and moderators of key relationships in corporate diversification research incorporating RBT. Figure 1 provides a conceptual map of this research corresponding to each of the articles coded in Table 1, and we also note key themes that emerged through the development of this research stream. Antecedents of corporate diversification focus on key themes related to (1) types of resources and (2) resource sharing. The key outcome in corporate diversification research focuses on (3) financial performance. Key moderators of antecedents and consequences of corporate diversification include (4) dynamic capabilities, (5) knowledge/organizational searching, and (6) the institutional environment in which diversification decisions are made. Consequently, our review focuses on these major themes surrounding diversification research incorporating RBT.

A Conceptual Map of Diversification Research Integrating the Resource-Based Theory

Antecedents of Corporate Diversification

Types of resource

Early articles using RBT perspective to empirically study diversification were particularly interested in the relationship between types of resources and diversification. Many efforts examined how a specific type of resource or capability, especially intangible ones in keeping with the theoretical emphasis of RBT, affects corporate diversification. One prominent example was the decision-making abilities, especially in relation to cognitive complexity, of top managers. The importance of top managers in affecting corporate diversification had already been emphasized in an early study by Prahalad and Bettis (1986). Ginsberg’s (1989, 1990) subsequent studies likewise directed the attention of the diversification research to the importance of managers’ sociocognitive complexity. Likewise, Wiersma and Bantel (1992) found that top managers’ cognitive perspectives are associated with the propensity to change in diversification level, and Calori, Johnson, and Sarnin (1994) showed that CEO cognitive complexity affects the breadth of the business portfolio.

Because different types and modes of corporate diversification exist, research efforts also looked at how different types of resources may be linked to types or modes of corporate diversification. For example, Chatterjee’s (1990) study identified a set of factors to help managers at diversified firms choose the mode of diversification that would minimize the utilization costs of excess resources in new markets. This study found that utilization costs differ for different types of resources when they are used in dissimilar modes of diversification. Similarly, Chatterjee and Wernerfelt (1991) examined the link between types of resources and types of diversification. This line of research helped draw the attention to the importance of understanding a firm’s various resources and clarify the link between types of resources and modes and types of diversification.

Resource sharing

Many studies focusing on types of resources assume explicitly or implicitly that firms diversify primarily to utilize excess resources. However, the presence of excess resources is not the only motivation for diversification. The desire to share resources among business units may also encourage firms to diversify in order to reap synergistic benefits. This focus built a more direct link to the study of related diversification, as the motive to share firm resources basically implies the diversification will be related. To understand firms’ diversification patterns into new industries, Farjoun (1994) found that because firms can more efficiently utilize their resources by sharing across similar products, they diversify within related groups of industries in terms of types of human skills and expertise. This research thereby underscores the importance of resource sharing in determining type of diversification used (related diversification). The study by Govindarajan and Fisher (1990) also showed that high levels of resource sharing play an important role in influencing the effectiveness of a firm’s business-level strategy. In a related vein, economies of scope are also found to be an important factor affecting diversification benefits (e.g., Nayyar, 1993; Nayyar & Kazanjian, 1993).

Outcomes of Corporate Diversification

The impact of diversification on firm performance as the primary outcome of diversification received considerable interest in the literature during this period, especially in the 1990s. Hoskisson, Hitt, Johnson, and Moesel (1993) demonstrated that both accounting and financial (stock market returns) measures of performance are influenced by various measures of diversification, although the majority of studies in strategic management use an accounting measure. Also, it is important to point out that the groundwork of this line of research had been laid by Rumelt (1982) and Hitt and Ireland (1986) during the early theoretical foundation period. Similar to research on antecedents to corporate diversification, studies on this topic were interested in the performance impact of type of resources and resource sharing. For example, Markides and Williamson (1996) argued and found evidence that related diversification improves firm performance only when it allows a business to have preferential access to strategic assets, and any competitive advantage is dependent on organizational structures that allow the firm’s divisions to share existing strategic assets and to transfer the competence to build new ones efficiently. Relying on the idea of core competence, Markides and Williamson (1994) found that strategic relatedness is superior to market relatedness when predicting circumstances where related diversifiers outperform unrelated diversifiers. Thus, the relationship between resources and performance is sometimes complex and often involves interactions between resources and capabilities. Farjoun’s (1998) study found that neither skill nor physical bases of relatedness alone has any significant effect on performance; instead, different bases of relatedness complement and extend one another.

In a more recent study, Tanriverdi and Venkatraman (2005) argued that synergies arising from product knowledge relatedness, customer knowledge relatedness, or managerial knowledge relatedness did not improve performance independently. However, when synergies arise from the complementarities of those three types of knowledge relatedness, firm performance was improved. The findings of this study echoed Farjoun’s (1998) suggestion that firms may have to skillfully combine different types of resources to fully harness the benefits of firm resources. The importance of optimal resource combinations, as evidenced from these studies, deepens our understanding about RBT’s core premise that the firm is a bundle of resources. In a similar vein, D’Aveni, Ravenscraft, and Anderson (2004) found that to the extent a business is closely aligned with its parent’s dominant logic, its costs will be lower than those of its competitors and accordingly its performance will be better. As such, they concluded that resource congruence (and RBT) is a better predictor of synergies and competitive advantage at the business level than is output relatedness. However, simply combining resources or adopting a related diversification strategy may not necessarily lead to increased financial benefits. A study by St. John and Harrison (1999) found that firms with manufacturing-related businesses may not be able to enjoy financial benefits from shared resources in manufacturing. However, some firms can realize better performance when they have demonstrated strong commitments to coordination. In this light, their study may serve to underscore the difficulty of realizing the benefits of related diversification beyond simply combining or sharing resources.

Moderators of Corporate Diversification

Dynamic capabilities

The concept of dynamic capabilities (Helfat & Peteraf, 2003; Makadok, 2001; Teece, Pisano, & Shuen, 1997) had significant implications for research on diversification that emerged in the late 1990s and early 2000s. This line of research focused on the dynamic perspective of resources and capabilities to inform diversification or corporate scope largely from a temporal perspective. For example, Galunic and Eisenhardt’s (2001) study viewed corporate divisions as combinations of capabilities and product market areas of responsibilities that may be recombined in various manners. Helfat and Eisenhardt (2004) examined how intertemporal economies of scope, achieved by redeploying resources and capabilities between related businesses over time as firms exit some markets while entering others, help firms diversify into related businesses. Similarly, Døving and Gooderham’s (2008) study demonstrated that dynamic capabilities have a distinct impact on the scope of services. Using the concept of corporate coherence, which is conceptualized as a dynamic interconnectedness between a firm’s technological competencies and its downstream activities, Piscitello’s (2004) study showed that firm performance is positively influenced by corporate coherence. Approaching the relationship between resources/capabilities and diversification from a dynamic perspective, thereby incorporating the elements of change and interdependence into the mix, has led to a richer understanding of the diversification process and subsequent performance implications.

Knowledge/organizational searching

Another important extension of RBT pertains to the emphasis on knowledge with a strong focus on knowledge/organizational searching (Fiol & Lyles, 1985; Grant, 1996; Huber, 1991). Miller’s (2006) study emphasized how a firm’s knowledge base interacts with its product market activity. Miller, Fern, and Cardinal (2007) examined the impact of sources of knowledge on technological innovation within diversified firms. The findings by Pennings, Barkema, and Douma (1994) demonstrated that a firm’s expansions are more persistent when they are related to its core skills and when it has a higher level of diversification experience, underscoring the importance of organization learning and searching. Chang (1996), drawing upon the knowledge-based view, argued that the firm engages in continuous search and selection activities to improve its knowledge base and thus improve its performance. His study demonstrated that the firm’s knowledge base is useful for predicting which businesses a firm enters or exits. In this regard, Chang’s study complements Mosakowski’s (1997) work that offered evidence that diversification can be understood as a process through which firms search for the best use of their resources. Viewed from this perspective, diversification not only may be a result of excess resources but can be viewed as a process of searching for the best use of a firm’s resources across different industries or market segments.

Institutional environment

Hoskisson et al. (2000) identified RBT as one of the most insightful theories for studying emerging economies. An important line of diversification research emerged in recent years that integrated RBT with new institutional economics (e.g., Greif, 2006; North, 1990). This line of research argued that institutional environment is a core component in diversification research and incorporating this element into the literature likely would generate alternative conclusions to the received knowledge of corporate diversification. One aspect that drew considerable attention in this literature was unrelated or conglomerate diversification in the form of business groups in regard to emerging and transition economies.

Business groups “consist of individual firms that are associated by multiple links, potentially including cross-ownership, close market ties (such as inter-firm transactions), and/or social relations (family, kinship, or personal friendship ties) through which they coordinate to achieve mutual objectives” (Yiu, Lu, Bruton, & Hoskisson, 2007: 1551). To account for the rise of business groups in emerging economies, Guillén (2000) and Kock and Guillén (2001) argued that this phenomenon is largely the result of firms accumulating the capability of repeating entry into new businesses, which can be viewed as valuable, rare, and inimitable. In a study on the potential benefits of chaebols (Korean business groups), Chang and Hong (2000) emphasized the within-group resource-sharing and internal business transactions. The authors reckoned that the study extends RBT by exploring resource heterogeneity within business units (group firms) and focusing on the operations of internal markets within diversified corporations. In a similar vein, Yiu, Bruton, and Lu (2005) employed the resource-based and institutional perspectives to examine how Chinese business groups acquire resources and capabilities to prosper. In addition, group firms’ behaviors may differ from those of nongroup firms. For example, Belenzon and Berkovitz’s (2010) study showed that group firms are more innovative than are nongroup firms, especially in industries that rely more on external funding and in groups with more diversified capital sources. The results also suggest that knowledge spillovers are not the main driver of innovation in business groups because firms in the same business group do not have a common research focus and are unlikely to cite each other’s patents.

These studies are in line with the research by Peng and Heath (1996) and Peng, Lee, and Wang (2005) that emphasized resources and institutions in theorizing the growth and scope of firms in transition economies. Similarly, research by Wan and Hoskisson (2003) and Wan (2005) also drew on the institutional perspective and RBT to posit that high levels of diversification improve firm performance when the country’s institutional environment is inadequately developed. In essence, this line of research has provided theoretical arguments and empirical evidence that high levels of diversification, including diversified business groups, can drive resource benefits and improve performance when a country’s institutional environment is still under development.

Our review above highlights the key developments and research focus of RBT-diversification research in strategic management. The next section will identify open issues and suggest opportunities for future contributions.

Future Opportunities

Notwithstanding the significant advances made in this line of research to date, there are a number of opportunities for continued theoretical evolution, accompanied by additional empirical effort to continue to build on the contributions of RBT to research in diversification. We draw attention to several open issues. First, although an inverted U-shaped relationship between levels of diversification and firm performance is theoretically appealing, the empirical evidence can be described as mixed at best. The importance of firm resources and capabilities in affecting performance is widely accepted, given the overwhelming evidence, but the same cannot be said in regard to the inverted U-shaped relationship. Even if the superiority of related diversification is valid, the construct of relatedness is still in need of refinement. Extant literature has yet to provide a definitive understanding of this construct. As such, various kinds of relatedness have been suggested, including product relatedness, resource/capabilities relatedness (including technological relatedness), strategic relatedness, managerial perception of relatedness, and institutional relatedness, among others (e.g., Markides & Williamson, 1994; Peng et al., 2005; Stimpert & Duhaime, 1997; Tanriverdi & Venkatraman, 2005). Stronger construct development is needed to provide more precise meaning to this crucial construct in the diversification literature. Otherwise, the presence (or absence) of relatedness will always exist “in the eyes of the beholder.”

While considerable research attention has been paid to types of resources, the owners/controllers of the resources have yet to attract significant research attention. So far, the only groups of owners/controllers that have received substantial research attention are small, public shareholders and top managers. However, most firms are not publicly owned, and the diversification literature knows little about how other types of firms decide on their diversification strategies. This is particularly the case in many parts of the world where solid empirical work has not been accomplished.

While top managers certainly are crucial firm resources, resources provided by other groups of owners such as employees may also be critical to a firm’s competitive advantages (Barney, Wright, & Ketchen, 2001). Wright, Dunford, and Snell (2001) proposed that it requires members of the human capital pool to individually and collectively choose to engage in behavior that will strategically impact a firm. At this point, questions remain regarding how the owners/controllers of the resources and capabilities will affect corporate diversification and, related to this, where those resources and capabilities reside. Moreover, the literatures on dynamic capabilities and knowledge and organizational searching have highlighted the dynamic nature of the diversification process. However, an enriched theoretical framework of such dynamic processes associated with diversification is still lacking. We do not have a clear picture of how such processes evolve in terms of firm resources, knowledge, entries and exits, and performance.

Although there are some pioneering studies looking at diversification and business groups across country institutional environments (e.g., Chang & Hong, 2000; Guillén, 2000; Khanna & Palepu, 2000), this line of research is still in its infancy and many questions remain unanswered (Peng & Delios, 2006). In light of institutional differences across countries, a core proposition of an institution-based view of diversification is that variation in institutional environments enables and constrains different strategic choices including product diversification (Khanna & Palepu, 2000; Peng, 2003; Peng et al., 2005; Wright, Filatotchev, Hoskisson, & Peng, 2005). Differences in country institutional environments will continue to provide fertile ground for probing questions on requisite resource types, resource ownership and control, the intricate relationship between diversification and firm performance, and the more general question on what will determine the scope of the firm around the world in the future.

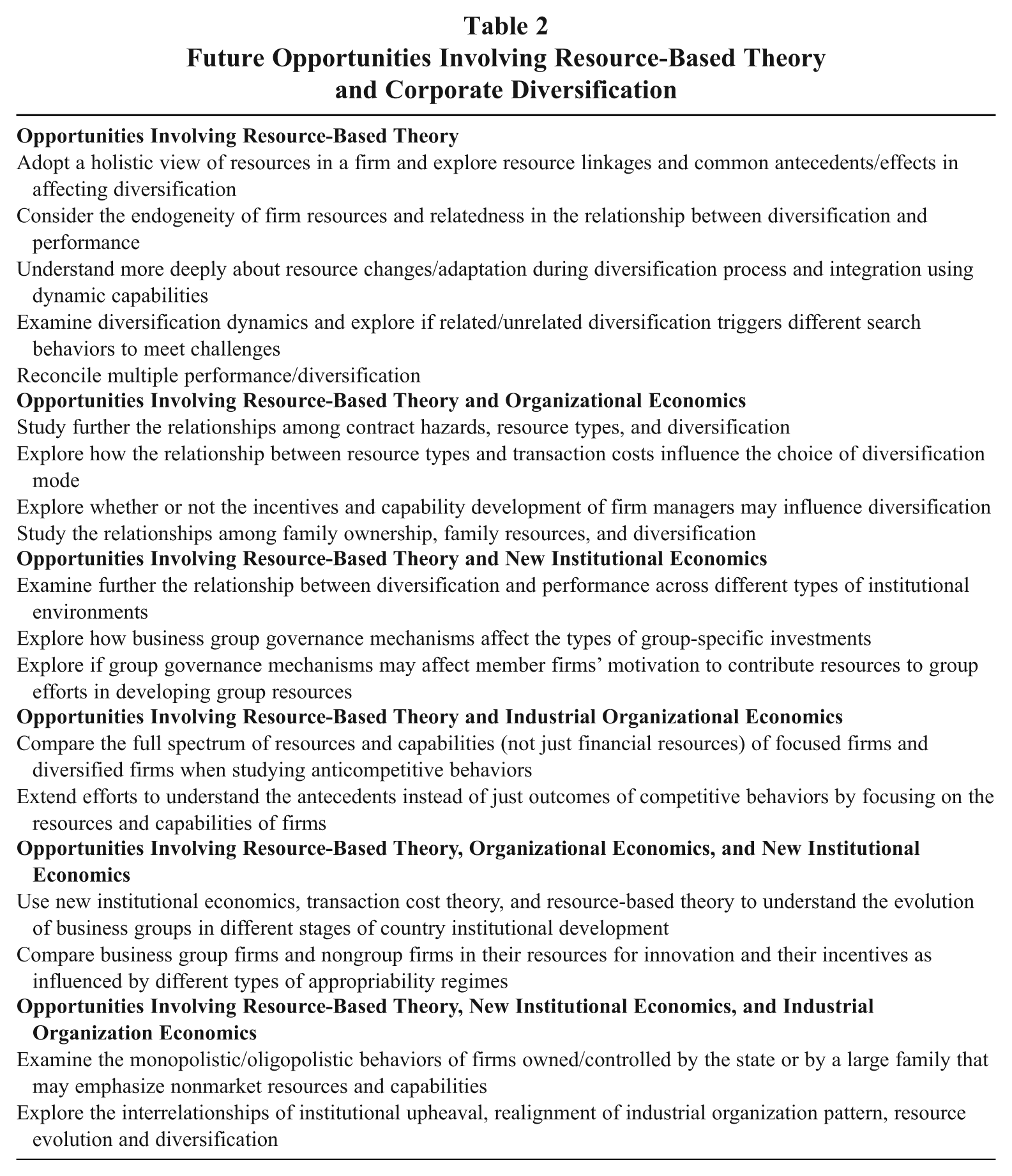

Given the explanatory power of RBT in the diversification literature thus far, few would argue against the continued benefit of employing RBT as the primary theoretical lens to study corporate diversification. However, we posit that integration of RBT with other theoretical frameworks holds the greatest promise to further inform the study of corporate diversification. Given the strong research tradition of IO economics and organization economics, plus the recent emergence of institutional economics, in diversification research, and their shared theoretical heritage with RBT (Conner, 1991), integration between RBT and these theoretical perspectives will be particularly fruitful. Toward this end, we further highlight specific future opportunities to advance the literature. Table 2 provides an overview of promising future opportunities.

Future Opportunities Involving Resource-Based Theory and Corporate Diversification

Resource-Based Theory

Types of resources

A firm’s resources and capabilities are unlikely to exist or operate in isolation. Theoretical exploration mapping or linking a firm’s various resource types to further understand their inner workings will be valuable. Issues such as their interrelationships as well as common antecedents and effects are some of the promising opportunities to understand firm resources from a holistic perspective. Such perspectives may help uncover the overall structure of the resources (e.g., whether it is a hierarchical structure) and the similarity/complementarity nature of the resources. For example, Makri, Hitt, and Lane (2009) examined the influence of two types of knowledge relatedness—knowledge similarity and knowledge complementarity—and the findings suggested that knowledge similarity facilitates incremental renewal, while knowledge complementarity would make discontinuous strategic transformations more likely. Such distinction of different kinds (not just types) of relatedness has the potential to advance the diversification literature further. Going forward, this line of research likely will benefit more from employing a more holistic, overall perspective to understanding how a firm’s various resource combinations affect its diversification strategy than from studying a particular resource or relatedness one at a time.

Diversification–performance relationship

Recent diversification studies have considered the endogeneity issue in the diversification–performance relationship (e.g., Campa & Kedia, 2002; Villalonga, 2004). This line of research argues that diversification may not destroy value because firms choose to diversify. Miller (2004, 2006) incorporated firms’ technological resources and relatedness in his studies that consider endogeneity in the diversification–performance relationship. His studies helped strengthen the argument that related diversification creates value. Few studies have explicitly incorporated firm resources and relatedness when considering the endogeneity of diversification and performance. Future research, especially to lend further support to the importance of related diversification, will benefit from such consideration.

Another opportunity to advance our understanding about the intricate relationship between diversification and performance may lie in a more in-depth understanding of the diversification process and subsequent integration. Only a few studies have accounted for the details of such processes (e.g., Galunic & Eisenhardt, 2001; Martin & Eisenhardt, 2010). These studies suggest that the diversification and integration processes appear crucial in understanding the relationship between diversification, especially related diversification, and firm performance. It is possible that the mixed findings in regard to the value creation of related diversification may critically hinge on such processes (Ahuja & Katila, 2001). Uncovering the processes of diversification and integration is a difficult task, but one that holds great promise in the literature.

Diversification dynamics

More temporal research in the field of diversification is needed, particularly regarding how diversification evolves in firms and industries. For example, in regard to related diversification, past research has examined how firms pursuing related diversification strategies have been able to foster more investment in R&D than do those pursuing unrelated diversification strategies (Baysinger & Hoskisson, 1989; Hitt, Hoskisson, Johnson, & Moesel, 1996; Hoskisson & Hitt, 1988). More research is needed to examine how these strategies help firms meet their future challenges. Perhaps related diversification triggers more search behavior to meet challenges and would be more strongly related to dynamic capabilities. On the other hand, perhaps unrelated diversification would trigger an increasing commitment to the established way of doing things in the past, if firms face an external shock or environmental challenges. Understanding such dynamics will continue to be an important issue as firms ponder entry and exit decisions. As such, more research on these dynamic phenomena using tenets of RBT will be fruitful.

Measurement issues

In the economics-based approach, the assumption of a relatively perfect market leads most studies to employ a market-to-book ratio (or similarly, Tobin’s q) and even stock market abnormal returns. In RBT approach, the main performance measures are accounting-based returns, although market-based returns are sometimes used as supplementary measures. More research needs to be done to examine how type of performance measurement influences this diversification–performance relationship. As for the measurement of diversification, all theoretical perspectives use objectively calculated measures from publicly available data sources (Martin & Sayrak, 2003). These include the simplest business count measure to the more sophisticated Herfindahl index (Berry, 1971; McVey, 1972) and entropy measure (Palepu, 1985). Due to the interest in related diversification, diversification research based on RBT sometimes employs subjective measures (e.g., Rumelt, 1974; Stimpert & Duhaime, 1997; Wrigley, 1970). However, as pointed out by Martin and Sayrak (2003), subjective classification schemes are difficult to be accepted, given research norms in finance. As such, reconciling the measures of performance and diversification may help mitigate the mixed findings between different academic disciplines.

As a further reflection of strategic management’s interest in studying related diversification, Robins and Wiersma (1995) advocated an “objective” resource-based approach to measure interrelationships among the businesses of a firm. According to the authors, because RBT argues for measures of relatedness that are indirectly associated with underlying forms of knowledge or capability, direct measurement is almost impossible. However, it may be possible to develop indirect indicators of their underlying similarities among Standard Industrial Classification industries based on secondary data about industrial activity. This measure is uniquely developed for diversification research premised in RBT perspective. Another recent measure proposed by Lien and Klein (2009) is focused on patterns of related industries measured at the industry level and assumed to measure relatedness at the firm level. Bryce and Winter (2009) have introduced an index that may facilitate the opportunity to explain the direction of diversified expansion, the development of capabilities over time as industries and firms co-evolve, and the role of knowledge in the growth of the firm. Also, it might help us better understand the crucial concept of dynamic capabilities. In a similar vein, Lee and Lieberman (2010) also have developed a dynamic measure of relatedness. Although most research has been done using static measures, more research needs to be done not only between disciplines and perspectives but also using dynamic measures.

Integrating RBT and Organizational Economics

In an editorial note to Bethel and Liebeskind (1998), Barney stated that “traditional diversification research has failed to account for the variety in ownership and organization for firms pursuing a diversification strategy.” Barney’s remark aptly points out a fruitful direction for research on diversification. Although both the organizational economics and RBT perspectives have been widely employed in diversification research, the use of these two theoretical frameworks has largely been separate. We suggest that integrating RBT with organizational economics is a fruitful avenue to build new theories of diversification.

Transaction cost economics

Silverman (1999) noted that transaction cost economics focuses on the choice of contracting alternatives by which a firm can exploit its resources, while RBT approach to diversification assumes that firm-specific resources should be internalized rather than contracted out. His study found that a firm enters markets in which it can exploit its own technological resources and in which it has the strongest resource base, and its diversification decision also is influenced by the severity of hazards surrounding contractual alternatives to diversification. Silverman’s study is likely the first effort to empirically test the role of transaction costs on diversification within the context of RBT. There may also be valuable opportunities in studying vertical relationships as compared to horizontal relationships. Argyres (1996), for example, found that value chain stages were integrated where resource similarities across the stages were considered high. Likewise, there are studies that examine vertical integration and disintegration among firms in certain industries. For example, Jacobides (2005) studied the vertical disintegration of the mortgage banking industry. In such instances, how do resources relate to the restructuring processes as market institutions evolve in an industry? This line of inquiry also relates to the diversification dynamics noted above.

Given the potential for integrating these two theories to inform diversification research, such inquiry likely will be beneficial (Conner & Prahalad, 1996; Madhok, 2002). A particularly fruitful research topic in integrating transaction costs economics and RBT is the diversification mode. Although many studies have examined the diversification mode (e.g., Busija, O’Neill, & Zeithaml, 1997; Kochhar & Hitt, 1998; Lamont & Anderson, 1985), only a few of them have incorporated RBT logic in their examination. Chatterjee (1990) identified factors that lead diversified firms to choose particular diversification modes in order to minimize the cost of utilizing excess resources. Chatterjee and Singh (1999) examined the relationship between diversification type and diversification mode and argued that mode is subject to constraints imposed by resources. These two early efforts are interesting, but there is almost no subsequent research using RBT to understand the diversification mode choice. A promising opportunity in advancing our knowledge on diversification mode lies in integrating RBT and transaction cost economics.

Agency theory

Compared to the agency theory perspective that views firm diversification as a type of firm governance failure, RBT perspective views the motivation of firms to diversify as a maximization of firm resources. Agency theory views managers as a potential problem (Jensen & Meckling, 1976) where diversification may represent empire building, whereas RBT views managers or the managerial team as a critical firm resource (Barney, 1991). It is clear that RBT and agency theory view the nature of corporate diversification in stark contrast. Given the importance of human capital in RBT (Wright, McMahan, & McWilliams, 1994), further understanding of the intricate relationships between incentives and capability development of firm managers and diversification becomes critical. For example, Wang and Barney (2006) argued that diversification reduces the risks associated with the value of core firm resources, thus providing positive incentives for employees to make firm-specific investments. As such, even though the agency theory perspective does not view diversification as value enhancing for the owners of the firm, the authors posited that diversification may lead to indirect benefits for the firm to the extent that employees, as one key organizational stakeholder, become more willing to make firm-specific human capital investments. By combining RBT and the organizational economics perspectives, the understanding of diversification motives is enriched by taking into consideration the role of risks and employee incentives.

The relationship between family ownership and diversification is likely more complex than a strict application of agency theory can predict. For example, because the extent to which family ownership is susceptible to the agency problem is still not totally clear (Gomez-Mejia, Nunez-Nickel, & Gutierrez, 2001; Villalonga & Amit, 2006), the impact of family involvement on diversification is worthy of future investigation. Increasing interest in family involvement is evidenced by Anderson and Reeb’s (2003) study that found that family firms experience less diversification than do nonfamily firms, despite the widely held belief that family owners seek to reduce firm-specific risk through diversification. Similar results were obtained by Gomez-Mejia, Makri, and Kitana (2010). To the extent that one considers the unique resources of family firms that provide advantages over nonfamily firms (Sirmon & Hitt, 2003), the impact on diversification scope and performance for family firms likely will be a rewarding avenue for further research.

Integrating RBT and New Institutional Economics

Using RBT in addition to new institutional economics appears to be fruitful since this literature is premised on many similar concepts germane to organizational economics but operates at the country level of analysis, as indicated in Table 2. Consequently, integrating RBT and new institutional economics may shed light on business groups and firm diversification in different institutional contexts to help understand country-level effects.

Institutional environment

The use of new institutional economics in diversification highlights the importance of incorporating a country’s institutional environment in understanding the type of diversification strategy and performance across countries. For example, Wan and Hoskisson (2003) found that the value of diversification becomes lower in more munificent home country resource environments; on the other hand, diversification brings more value in less munificent resource environments. In a similar vein, Peng et al. (2005) showed how institutions matter in diversification research. They probed that a firm’s product scope depends not only on its product relatedness but also on its institutional relatedness. When taking institutional differences into account, one can observe that a firm that appears to have low product relatedness is actually enjoying common advantages given by high institutional relatedness. In RBT perspective, such an ability to generate synergy from institutional relatedness becomes a valuable and inimitable capability that helps sustain a firm’s competitive advantages (Guillén, 2000; Peng, 2001).

Despite early efforts, diversification research employing new institutional economics and RBT is still in its infancy. In many economies, especially the emerging and transition economies, fast-changing development in the institutional environment demands that firms acquire, manage, exploit, and transfer their resources differently (Meyer & Peng, 2005). Therefore, the relationships among resources, types of diversification, and firm performance are likely to differ among country institutional environments. For example, market capital (e.g., brand awareness) likely is less important than nonmarket capital (e.g., political capital, social capital) in emerging and transition economies, and unrelated diversification based on nonmarket capital or institutional advantage can be value enhancing. Also, types of ownership may have different impacts in different countries. For example, large block ownership may not have the same positive effect on performance in countries with weak institutional environments as commonly expected of block holders. These countries are susceptible to the principal–principal agency problem whereby minority shareholders are exploited by the majority shareholder (Young, Peng, Ahlstrom, Bruton, & Jiang, 2008). Therefore, the block holders are likely more interested in resource grabbing or tunneling rather than resource creation.

Business groups

The emergence and existence of diversified business groups in many economies appear to defy the received knowledge in the field. One mystery of business groups in emerging markets is how they create value through unrelated diversification (Peng, 2001). A major explanation of the value-adding unrelated diversification effect in emerging markets is that product diversification of the business group creates an internal market or resource pool that substitutes the lack of a well-developed system of market institutions as found in developed markets (Khanna & Palepu, 1997, 2000). Members of a business group thus enjoy the advantages of lower cost resources due to cross-subsidization within the group and an inimitable capability to obtain rare domestic and foreign resources (Chang & Hong, 2000; Guillén, 2000).

We believe that the integration of RBT and new institutional economics will continue to be an effective tool to further our knowledge of corporate diversification in different countries. For example, the existence of business groups with implicit or incomplete contracting is found in economies with fewer market-based institutions. Firms in a business group allow for management of such contracting through a hierarchy but go beyond transaction cost economics by tying property rights theory (Hart & Moore, 1990) into the arguments. Independent firms in a business group have property rights, but the distribution of those rights takes place through an authority mechanism. To be effective, these mechanisms need to create trust for member firms to develop group-specific investments in resources from RBT point of view. The types of resources developed in a business group and its member firms, as well as the motivation of the member firms to make the investments, are likely to be different depending on the implicit contract and property rights structure in a business group.

Integrating RBT and IO Economics

Early research on diversification largely adopted an IO economics perspective that emphasized diversified firms’ anticompetitive behaviors (Caves, 1981; Montgomery, 1994; Scherer, 1980). For example, in using predatory pricing, a diversified firm can drive existing competitors out of the market or forestall potential entrants by cross-subsidizing (Bolton & Scharfstein, 1990; Scherer, 1980). In contrast, a focused firm, without the ability to cross-subsidize, is less likely to practice, or respond to, predatory pricing for a prolonged period of time. Against the “shallow pockets” of the focused firms, the “deep pockets” of the diversified firms represent a potent weapon in market competition (Bolton & Scharfstein, 1990). However, this view may place too much emphasis on a firm’s financial resources while ignoring the many other types of firm resources and capabilities. From RBT perspective, financial resources, though important, are only one type of firm resource. For a focused firm, even if its overall financial resources may not be as potent as those of a larger, diversified firm, the competitive behavior and outcome may not be as well predicted by IO economics. Notwithstanding the theoretical appeal of the IO economics perspective, empirical studies examining diversified firms’ market power have not observed a strong correlation between diversification and anticompetitive behaviors (e.g., Geroski, 1995; Scherer, 1980). A missing link could be that firms’ competitive behaviors may not simply be shaped by each other’s financial resources, or prices. An incorporation of RBT perspective that emphasizes various firm resources may generate fresh insights to understanding the competitive aspect of diversification.

Integrating RBT, Organizational Economics, and New Institutional Economics

Business group evolution

More research examining issues of dynamics over time among business groups is promising. Hoskisson and colleagues suggested that in the “early stages” of market emergence, new institutional economics is preeminent. However, “as markets mature, transaction cost economics and, subsequently, the resource-based view are more important” (Hoskisson et al., 2000: 252). For example, using transaction cost economics as a base, as market institutions mature and improve, business groups should restructure to become less diversified (Hoskisson et al., 2004). However, anecdotal evidence suggests that business groups remain quite viable in developed economies such as Japan, Sweden, Italy, and Spain, among others. This mystery needs more exploration. For example, using agency theory and RBT, are there stages where business groups change from being focused on dominant family owners who take advantage of minority shareholders (Chang, 2003) to where the resources of the group can be used to solve problems such as improved international diversification? Perhaps business groups change and emphasize internal group capabilities under more transparent governance (Hoskisson, Cannella, Tihanyi, & Faraci, 2004). Previous research has emphasized vertical integration or political capabilities using RBT (Chang & Hong, 2000; Guillén, 2000), but business groups may have other capabilities that will allow them to pursue more competitive strategies (Hoskisson, Kim, White, & Tihanyi, 2004; Kim, Kim, & Hoskisson, 2010). Thus, the dynamics of business group evolution and the capabilities to facilitate international competition, especially by emerging economy firms, remain an important topic for further exploration.

Business group innovation

Another promising avenue for future research relates to innovation by business group (Mahmood & Mitchell, 2004). Most research suggests that diversified firms are likely to invest less in research and development, hence negatively affecting corporate innovation. However, Belenzon and Berkovitz’s (2010) study showed that business group firms are more innovative than are nongroup firms due to the financial resource advantages of the business group. Their study underscores the importance of incorporating the institutional environment to better understand the relationship between firm resources and innovation in business groups. For example, in institutional environments where the appropriability regime is subject to high transaction costs, business group firms may have stronger innovation incentive and access to critical resources (e.g., human and financial resources) compared with independent firms.

Resource ownership and control

In many country environments, critical firm resources are owned and controlled by the state or family. At the same time, extant diversification research has generally assumed that firm resources are owned by small shareholders. When the property rights or ownership of the resources are held by the state or family, it is possible that the diversification behavior of the firms may differ from when they are held by the shareholders. State firms’ diversification strategies may be driven not so much by efficiency or profitability objectives than by social and political objectives. Family firms may pursue a diversification strategy that seeks to maintain family members’ socioemotional wealth (Gomez-Mejia et al., 2010). In studying corporate diversification strategy in institutional environments where property rights and ownership of large firms may take on a different meaning, new theoretical frameworks and insights can be generated when the implicit assumptions of the extant literature are modified or even discarded. For example, Peng and Heath’s (1996) article on the growth of firms in transition economies suggests that due to institutional constraints, neither generic expansion nor acquisition is viable for firms in those countries. Instead, firms have to pursue a network-based strategy of growth that builds on personal trust and informal agreements among managers. Their work has provided a nice starting point on this topic. More research that incorporates resources embedded in different institutional environments will be needed to shed light on this important topic.

Integrating RBT, New Institutional Economics, and IO Economics

The use of the IO economics perspective in diversification research has decreased substantially in recent years (McCutcheon, 1991). In some countries with different institutional environments, the focus and insights of IO economics may find a more ready application. In countries where the state or large families hold substantial control or influence in the economy, oligopolistic or even monopolistic diversification behaviors may dominate. In these types of institutional environments, the most relevant resources and capabilities may be not market based but nonmarket based. As such, marketing or R&D capabilities may be less powerful in firm diversification. Instead, political connections and lobbying, for example, are the key resources and capabilities in firm growth (Hillman, Keim, & Schuler, 2004). Conglomerates are less concerned with the lack of (market) relatedness/synergies in their business portfolios when the key to success is nonmarket relatedness/synergies (such as political connections) that they can reap and leverage.

Many of the formerly planned economies are undergoing various stages of transitioning into market-based economies. This change in the institutional environment provides a valuable opportunity to examine the interrelations among institutional change, realignment, or even total breakdown of the prevailing patterns of industrial organization, resources and capabilities evolution, and the resultant firm growth and diversification strategies. Peng (2003) and Newman (2000) have provided interesting theoretical and conceptual frameworks when they examine firm strategies during institutional upheaval. Future research on RBT and diversification can benefit from drawing upon their frameworks and arguments to advance this line of research and at the same time seek to provide empirical evidence to test the arguments. Integrating these various units of analysis in one study likely poses methodological challenges to diversification researchers. The different levels of constructs in terms of country institutional environment, business group, and firm may require the use of hierarchical linear modeling (or multilevel modeling). Operationalizing these constructs is also challenging. For example, capturing the country institutional environment is not an easy task given its multiple dimensions. Extant research has made good progress (e.g., Henisz & Delios, 2001; Wan & Hoskisson, 2003), but further work is needed to fully capture this elusive but important construct. The definition of business group also needs further conceptualization because a business group can be family based, bank based, or even formed by the government (Yiu et al., 2007). Further conceptualizing this increasingly important construct becomes important. Despite these methodological challenges, potentially richer multilevel theorizing linking these different levels of constructs and their interactions over time certainly offers fruitful opportunities for diversification research in the coming years.

Conclusion

The primary purpose of this article is to assess the contribution of RBT to the study of corporate diversification and to suggest future research opportunities for continued contribution to this important research stream. RBT has provided a conceptual vantage point to explain the diversification decision in a manner unique to the field of strategic management. We chronicle and assess the development of this perspective independent of other theoretical lenses that provide alternative explanations for the diversification decision. While previous efforts mostly built knowledge surrounding diversification by focusing on the unique explanatory elements of RBT, future contributions will benefit from seeking to combine the theoretical power of RBT with other theoretical perspectives such as new institutional economics to offer an even richer understanding of corporate diversification.

Footnotes

1.

Our article uses the term corporate diversification to refer to product diversification only, although the term is sometimes used to include international diversification as well.

2.

Transaction cost economics and agency theory are often also regarded as belonging to the new institutional economics. In this article, we regard them as organizational economics, as their focus is at the organization level. We reserve new institutional economics for the country-level work conducted by Douglas North and others.