Abstract

Together, Penrosean and Barnean resource-based logic make up the dominant theoretical approach to understanding firm growth. While extant literature focuses on a common lineage between Penrosean theory and the resource-based view (RBV), we explicate divergence at these origins of resource-based theorizing and subject the growth implications of each to meta-analytic testing. RBV’s central tenets concern resources that meet valuable, rare, inimitable, and nonsubstitutable (VRIN) criteria, while Penrose’s theory discusses the versatility of resources. Theoretically, VRIN resources allow firms to exploit unique opportunities, while versatile resources allow firms to recombine resources in novel ways to create growth. Using meta-analytic techniques, we find that versatile resources are associated with higher levels of growth, whereas VRIN resources are not. We offer novel insights into alternative characteristics of resources derived from the same conceptualization of the firm, add greater specificity to the performance construct, and open up avenues for new theorizing on firm growth that is more closely aligned with Penrose’s theory.

Introduction

Firm growth, a foundational topic of management research, is broadly defined as the increase in a firm’s size from one point in time to another (Chandler, 1962; Penrose, 1959/1995). Growth is important for economic development and employment (Birch, 1981; Moran & Ghoshal, 1999), allows new firms to establish legitimacy in order to survive (Stinchcombe, 1965), and constitutes an explicit goal and signal of success (Eisenhardt & Schoonhoven, 1990). Yet despite hosts of empirical studies on the topic, narrative assessments of the field of firm growth have pointed to fragmentation and stalled theoretical development (Gilbert, McDougall, & Audretsch, 2006; Lockett, Wiklund, Davidsson, & Girma, 2011).

We suggest that this stalled theoretical development is born from confusion in the dominant theoretical approaches used to explain growth. Resource-based approaches have come to dominate theoretical frameworks in firm growth (C. G. Brush, Greene, Hart, & Haller, 2001; Gilbert et al., 2006; Pettus, 2001; Zupic & Drnovsek, 2014). A recent bibliometric analysis of over 400 growth papers identified Penrose’s (1959/1995) book The Theory of the Growth of the Firm as the most cited reference in the growth literature, followed closely by Barney’s (1991) article “Firm Resources and Sustained Competitive Advantage” (Zupic & Drnovsek). Barney developed the relationship between valuable, rare, inimitable, and nonsubstitutable (VRIN) resources and competitive advantage, whereas Penrose focused on, among other things, the combination of versatile resources to create growth. However, the growth literature has not been sufficiently cognizant of important differences between the Barnean and Penrosean approaches and has tended to conflate them. Growth literature tends to link Barney’s antecedent of VRIN resources to Penrose’s outcome of firm growth. This is a conceptual and empirical mismatch.

In this paper, we flesh out the theoretical arguments of the relationship between resources and growth according to these distinct theoretical lenses. Using meta-analysis, we then test the extent to which each of these approaches holds up to empirical scrutiny. Given the theoretical confusion and stalled development, meta-analysis is an ideal empirical technique to advance firm growth research in general and test divergent resource-based approaches in particular. Meta-analysis provides unique ways of bringing order to large and fragmented fields (Combs, Ketchen, Crook, & Roth, 2011) and allows for the testing of specific hypotheses with statistical accuracy and generalizability (Lipsey & Wilson, 2001). As a result, meta-analysis provides a powerful means to test and compare the efficacy of the Barnean and Penrosean approaches.

We make the following contributions to the literature. First, we develop a detailed theoretical argument on how Barney’s VRIN approach to resources (which we also refer to as resource-based view, or RBV) translates into growth. Specifically, VRIN resources are said to allow for the exploitation of unique growth opportunities (Alvarez & Busenitz, 2001) and protect first-mover advantages after the exploitation of these opportunities (cf. Peteraf, 1993). We propose that extant RBV research builds on the implicit assumption that growth and competitive advantage are concomitant 1 and then show that this assumption does not necessarily hold up. We make a valuable contribution to the growth literature because, theoretically and empirically, we point to the boundaries and limitations of the most common conceptual approach. We also contribute to RBV more generally by specifying suitable outcomes in resource-based research (cf. Eisenhardt & Martin, 2000).

Second, we develop the concept of versatility as a distinctly Penrosean characteristic of resources. In doing so, we elaborate and test a central aspect of Penrose’s theory that has received limited attention (cf. Lockett et al., 2011). 2 This provides a resource characteristic that can be contrasted with VRIN and is particularly suitable for explaining growth. In developing the versatility concept, we also synthesize differing views regarding resource fungibility. 3 We suggest that both generic and tradable resources (externally fungible) and firm-specific but redeployable resources (internally fungible) are associated with versatility as they offer a relatively broad range of potential services.

Third, our meta-analytic approach allows us to empirically pit Barney’s VRIN characteristics of resources against Penrose’s versatility characteristic. As a result, we provide guidance regarding the appropriateness of applying these theoretical approaches to growth studies. Our findings support the Penrosean approach but not the Barnean. Despite the prevalence of RBV in the growth literature, future resource-oriented growth studies would benefit from building more directly upon Penrosean theory. The results also suggest that growth may not be the most suitable performance outcome for VRIN studies. While VRIN may be more suitable for efficiency- and advantage-based performance outcomes—for what it was originally intended (Barney, 1991)—growth represents a unique performance outcome that requires dedicated theorizing.

Theoretical Development

The theoretical frameworks applied in the studies underlying our meta-analysis provide guidance to our theoretical framework. Our review and a recent bibliometric analysis (Zupic & Drnovsek, 2014) found that resource-based approaches dominate the field. Penrosean resource-based theory and RBV share some common foundations. Both view firms as a collection of idiosyncratic resources and see resource endowments as useful for developing products, services, and strategies (Barney, 1991; Penrose, 1959/1995; Wernerfelt, 1984). In both Penrosean theory and RBV, the idiosyncratic nature of resource endowments stems from the particular history and development of resource collections within firms. Heterogeneity in resources across firms can explain performance differences although firms operate in identical environmental conditions.

While commonalities between RBV and Penrose’s theory are often emphasized (Armstrong & Shimizu, 2007; Barney, Ketchen, & Wright, 2011; Kor & Mahoney, 2004; Mahoney & Pandian, 1992), they differ in critical ways. According to RBV, VRIN resources create sustainable competitive advantage since valuable resources allow firms to implement efficient strategies and isolating mechanisms prevent imitation of these strategies (Barney, 1991; Peteraf, 1993). In contrast, Penrose (1959/1995) emphasizes versatility in terms of the range of services that resources can provide to entrepreneurial managers. These distinctions often lack clarity in the literature. VRIN and versatility arguments are frequently intertwined to predict growth. This is unfortunate and hampers theoretical development.

RBV Characteristics of Resources: VRIN

According to RBV, firms that possess bundles of resources that are VRIN will enjoy sustained competitive advantages and, consequently, superior firm performance (Barney, 1991; Wernerfelt, 1984). The value and rarity of resources allow firms to create new economic value, while inimitability and nonsubstitutability provide the isolating mechanisms that lock in rents associated with those resources (Barney; Peteraf, 1993; Rumelt, 1984). Recent studies assessing RBV have been largely supportive of its predictive power on performance. While Newbert suggested that RBV “has only received modest support overall” (2007: 121), Crook, Ketchen, Combs, and Todd (2008) employed meta-analysis and found a substantial correlation (r = .29) between VRIN resources and performance.

While growth studies are often silent on precisely how VRIN resources are connected to growth, conceptually, RBV proposes several avenues. First, VRIN resources allow firms to exploit extant opportunities inaccessible to firms with non-VRIN resources. For instance, special knowledge or technical capabilities may allow for the development of new products or the entry into new markets (Prahalad & Hamel, 1990). Firms lacking these valuable and inimitable resources will be unable to pursue similar growth strategies to the same extent (cf. Barney, 1991). Alvarez and Busenitz (2001) argue that the cognitive ability of entrepreneurs is an inimitable resource that facilitates opportunity recognition and exploitation. Individuals without this VRIN cognitive ability will be unable to match the same level of success in their pursuit of new opportunities. Beyond creating the potential for first-mover status (cf. Lieberman & Montgomery, 1988), VRIN resources should allow firms to achieve sustained growth. If a firm possesses VRIN resources, the same isolating mechanisms that preserve rents may also allow firms to continue to generate value in a new sector without the threat of market erosion. These ex post limits to competition (Peteraf, 1993) are absent in imitable resources and are cornerstones of sustainable competitive advantage. While firms with non-VRIN resources also pursue opportunities, both the ex ante type of opportunity and the ex post competition protection will be limited. Firms that pursue opportunities based on VRIN resources will be able to gain first-mover advantages in unique markets and enjoy sustained growth as the market develops.

Second, VRIN resources enable firms to grow their existing products and services. Firms with VRIN resources can generate more value for customers than competitors with non-VRIN resources (Peteraf & Barney, 2003). Increased customer value from VRIN resources drives subsequent demand for the use of those VRIN resources (Peteraf, 1993). Because VRIN resources are rare and inimitable, those few firms who control them and supply them to the market have greater growth opportunities (Peteraf & Barney). VRIN resources also allow firms to implement efficient strategies (Barney, 1991) that enable firms to lower prices and drive market expansion. While firms with non-VRIN resources may pursue similar strategies, their inability to match the strategic initiatives of firms with VRIN resources or to protect gains from their own initiatives will limit their growth prospects relative to firms with VRIN resources.

Finally, while growth and competitive advantage are generally considered concomitant in the RBV literature, recent research has elaborated on VRIN resources’ value creation capacity independent of the resources’ ability to capture value (Peteraf & Barney, 2003). While it is generally agreed that VRIN resources provide limits on appropriation by competitors in ways that non-VRIN resources do not (cf. Barney, 1991; Peteraf, 1993), how different internal stakeholders may appropriate the value created by VRIN resources remains an open question. The value creation perspective has argued that, unlike other performance outcomes that need to be negotiated amongst a complex web of potentially powerful stakeholders (Coff, 1999), growth may not be subject to the same appropriability concerns. Growth directly reflects the value created by a firm, whereas many other aspects of performance (i.e., profitability) are recorded after value has been distributed among different stakeholders (Crook et al., 2008). Thus, it can be argued that growth provides a particularly salient performance outcome for testing the competitive advantage predictions of RBV. For these reasons, we hypothesize:

Hypothesis 1: VRIN resources will have a stronger impact on growth than non-VRIN resources.

Penrosean Characteristic of Resources: Versatility

According to Penrosean theory, growth is associated with two different resource uses. First, excess resources can be put to productive use. Because of the indivisibility of resources, there are always underutilized resources in any organization, and entrepreneurial managers look for ways to deploy them. As noted by Penrose, “There is no reason to expect that it would be possible to make them come out even, so to speak” (1955: 534). Thus, underutilized and excess resources create both the incentives and the means for expansion.

Second, resources used for one purpose can be redeployed for new and more productive applications. Penrose writes, “A firm has an incentive not only to engage in operations large enough to eliminate pools of idle resources, but also to use the most valuable specialized services of its resources as fully as possible” (1959/1995: 63). As managers learn about current resources under their control and new resources brought into the organization, they discover ways of generating new services out of these resources. Thus, new knowledge generates both incentives and means for expansion in a way that is reminiscent of Schumpeter’s (1934) understanding of the driver of growth at the level of the economic system. As Moran and Ghoshal (1999) note, firms withdraw resources from current uses to put them into new and more valuable resource combinations.

Any single resource provides an array of potential services that can be utilized and combined in novel ways (Penrose, 1959/1995: 76). Resources inherently differ in the range of potential services they provide. Some resources offer few applications (i.e., a narrow range of potential services), while others can be more easily redeployed into alternative uses (i.e., a broad range of potential services). Penrosean theory refers to resources offering a broad range of potential services as versatile. Versatile resources increase a firm’s combinative possibilities and, thus, expand its productive opportunity set. Penrose writes,

It becomes clear that the flexibility and versatility of its own resources are the important factors governing the possibilities of its expansion. So long as there are profitable production opportunities open anywhere in the economy, a firm can take advantage of them if its resources are versatile. (1955: 539)

Versatile resources allow managers to undertake a broader set of strategic actions (Kim & Bettis, 2014). Furthermore, since versatile resources have lower transaction costs in their structuring, bundling, and leveraging (Sirmon, Hitt, & Ireland, 2007), they enable firms to change growth strategies over time. The ability to quickly shift resources allows firms to adapt in rapidly changing environments (Kraatz & Zajac, 2001) and to swiftly pursue emergent opportunities (Sapienza, Autio, George, & Zahra, 2006). In contrast, resources that are not versatile can be used only for specific initiatives and lock firms into set strategic directions (cf. Ghemewat, 1991). Nonversatile resources lose value over time because they are not easily reconfigured or put to new uses (Mauri & Michaels, 1998). For instance, reliance on existing knowledge over new combinations can create path dependencies, lead to an overemphasis on local search, and prevent the exploration of new growth opportunities (Katila & Ahuja, 2002; March, 1991).

While Penrosean theory provides limited information regarding the versatility of different resources, the literatures on resource fungibility and fungible resources provide some guidance. Resources with little specificity that are tradable between firms are considered fungible since there are fewer costs involved with their transfer (Russo, 1991). Resources such as cash (Kim & Bettis, 2014), unabsorbed slack (Mishina, Pollock, & Porac, 2004), commodities (Nelson & Barley, 1997), or generic human resources can be exchanged and utilized readily across firms. We refer to this as external fungibility. Others suggest that resources that can be redeployed easily between uses within a firm are fungible. This includes uniquely developed and sticky assets with a broader range of uses. Firm-specific assets, such as brands (Anand & Delios, 2002), technologies (Danneels, 2007; Parkhe, 1992), and experiential learning (Kumar, 2009), generate a range of productive services that will be useful in arenas beyond their current use. We refer to this as internal fungibility. Internally fungible resources allow firms to diversify (Teece, 1982), internationalize (Kumar), and develop new lines of business (Anand & Singh, 1997).

The distinction between resources that are internally or externally fungible is critical in an RBV framework because, by definition, firms cannot build competitive advantage on resources that are easily traded between firms and, thus, externally fungible (Dierickx & Cool, 1989). This is less of a concern for the Penrosean perspective because both classes of fungible resources are associated with versatility, which is the key consideration. Generic and tradable resources offer a wide range of potential services to a firm—as do assets that are firm specific but redeployable. These versatile resources make more strategic actions and opportunities available to the firm, while nonversatile resources limit exploitable opportunities and constrain strategic adaptation. Thus, we propose the following hypothesis:

Hypothesis 2: Versatile resources (those with internal or external fungibility) will have a stronger impact on growth than nonversatile resources.

Method

Literature Search and Sample

Meta-analysis is well suited to bring clarity to the fragmented growth field, to evaluate strategy theories (Combs et al., 2011), and to specifically test the link between resources and performance (Crook et al., 2008). In order to identify studies for inclusion in our meta-analysis, we conducted a thorough review of the literature. First, we searched for the word growth in the titles, abstracts, and keywords of relevant journals identified in the review of growth by Shepherd and Wiklund (2009) and extended the time period to cover the last 25 years. 4 Second, we did a targeted search combining the term growth with resource in leading research databases, including EBSCO Business Source Premier, Social Sciences Citation Index, and ProQuest Dissertations & Theses Database. This resulted in a total pool of 1,407 articles.

We screened each article for inclusion on the basis of the criteria of using (1) a quantitative empirical sample and (2) a variable measuring firm growth. This resulted in a refined list of 196 studies. The shrinkage is primarily due to the use of the word growth in contexts outside of firm growth, such as “growth of literature” or “theoretical growth.” Six more studies were removed since they were conducted at the industry level of analysis. This resulted in 190 studies that reflect research explicitly concerned with developing theory on firm growth. We recorded every variable employed in each study for a total of 2,012 variables. Of these variables, several hundred were used in only one study, attesting to the fragmentation of the field.

We then included only variables that were resource related, could be subjected to meta-analysis by reporting bivariate effect sizes, and used established measures of growth, such as sales, assets, and employees (cf. Shepherd & Wiklund, 2009). Nine studies contained no resource-related measure, 42 lacked bivariate effect size data, and 25 used unsuitable growth measures. 5 Of the remaining 114 studies, 4 included multiple samples or reported correlation tables separated by industry and, thus, were treated as separate samples. As a result, we ended up with 123 samples from 113 studies. These samples include 612 bivariate effect sizes (i.e., resource-related effect sizes) and represent data on 38,815 firms.

Coding

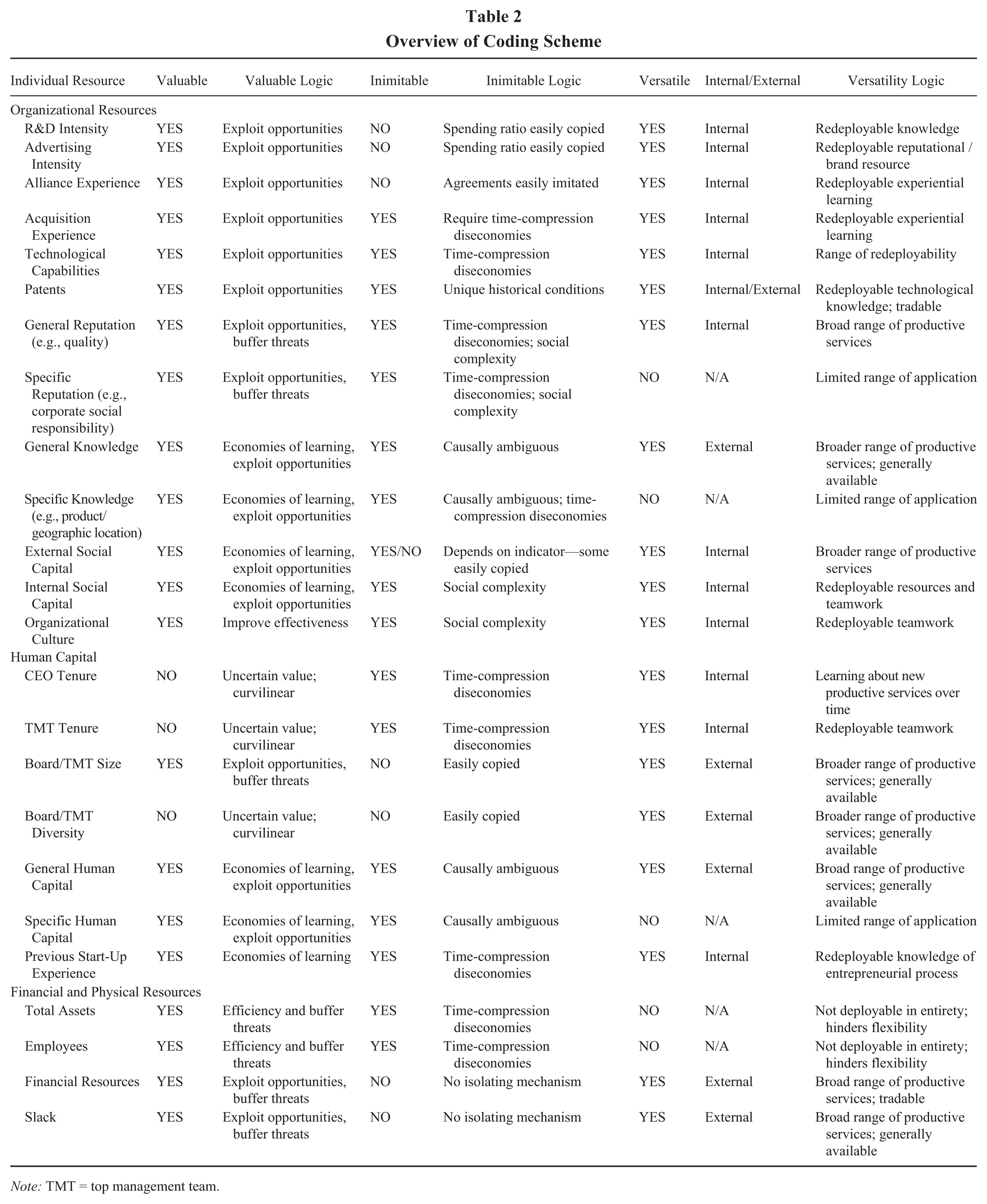

In order to test the impact of alternative resource characteristics, we coded each resource according to VRIN and versatility criteria. First, two authors reviewed items and agreed upon a coding scheme (discussed below). One author then coded the entire set of resources and discussed the result with the second author. Coding disputes were resolved through discussion and by examining precedence in the literature for VRIN and versatility. In order to check the validity of this coding, we had an independent rater who was knowledgeable about resource-based theorizing code a random sample of 10% of all resources identified in the sample. For VRIN resources, there was agreement on 82% of cases (92% for valuable and 90% for inimitable) and a chance-adjusted Cohen’s kappa value of .612 that is significant (Z = 4.81, p < .01). For versatile resources, there was agreement on 80% of cases and a Cohen’s kappa value of .581 that is significant (Z = 4.61, p < .01). As a result of this relatively high level of interrater agreement, we have confidence in our coding scheme. However, we discuss challenges with coding individual items and steps taken to ensure the integrity of our coding scheme in our Robustness Tests section.

For VRIN coding, we closely follow the procedures outlined by Crook and colleagues (2008). Resources were considered inimitable if they were protected by the isolating mechanisms of unique historical conditions, causal ambiguity, or social complexity (Barney, 1991). We followed the assessment by Crook and colleagues on specific resources wherever possible and also conferred with the first author of that article to resolve some uncertainties. Patents were considered to be the result of unique historical conditions, and reputation was considered to be subject to time-compression diseconomies (Dierickx & Cool, 1989). Measures of human capital and organizational knowledge were coded as inimitable since knowledge resources are generally considered to be causally ambiguous (Reed & DeFillippi, 1990; Simonin, 1999). In addition, we considered total asset and employee measures to be inimitable since they represent accumulated assets and, thus, are subject to time-compression diseconomies that cannot be easily imitated (cf. Dierickx & Cool). In line with Crook and colleagues, we coded resource allocation decisions (i.e., R&D/sales or advertising/sales) as imitable since such expenditure ratios can be easily copied. In addition, financial, liquid, and slack resources were considered imitable since they do not have isolating mechanisms (e.g., Barney). Overall, 69% of our measures were deemed to be inimitable, which is virtually identical to previous classifications (Crook et al.).

We then evaluated whether resources were valuable by applying the criteria introduced by Barney: “Resources are valuable when they enable a firm to conceive of or implement strategies that improve its efficiency or effectiveness and when they help firms exploit opportunities or neutralize threats” (1991: 106). Whenever possible, we followed precedent in the assessment of specific resources (Crook et al., 2008). Knowledge and social capital were considered valuable because these resources facilitate the conception of strategies, can result in economies of learning, and can be utilized to take advantage of opportunities (Grant, 1996; Shane, 2000; Yelle, 1979). We also consider total employee and asset measures to be valuable since they buffer firms from survival threats (Levinthal, 1991) and can lead to economies of scale (Wernerfelt, 1984). Following Crook and colleagues, we did not consider resources that have curvilinear relationships with performance—such as management tenure (Henderson, Miller, & Hambrick, 2006) and team heterogeneity (Lau & Murnighan, 1998)—to be valuable. In total, 88% of resources were coded as valuable.

Overall, 63% of our resources are coded as both inimitable and valuable, which is on target with Crook et al. (2008). Since researchers have argued that resources that are inimitable are by definition rare and nonsubstitutable, we follow precedent (Crook et al.) and consider resources that are both inimitable and valuable to have met the VRIN criteria.

Concerning resource versatility, we built on Penrose’s (1955, 1959/1995) definition regarding resources that offer a broad range of services. We then consulted the literatures on internal and external fungibility to arrive at classifications of specific resources. While versatility (or internal and external fungibility) exists on a continuum ranging from completely versatile to completely nonversatile, with most resource classes falling somewhere between these two extremes, we follow Crook et al. (2008) and our prior coding of VRIN resources by using a dichotomous coding of versatile and nonversatile resources.

First, we coded externally fungible resources as versatile. For this reason, financial and slack resources were considered versatile (Kim & Bettis, 2014; Mishina et al., 2004) since they can be easily applied to alternative uses (Penrose, 1959/1995) and provide organizations with flexibility (George, 2005). Individual financial and slack resources include cash (T. H. Brush, Bromiley, & Hendrickx, 2000) and human resource slack (Mishina et al.). However, resources such as total assets or employees cannot be wholly redeployed and may hinder flexibility (Hannan & Freeman, 1984). Thus, they are not considered versatile.

Knowledge resources differ significantly in their ability to be reconfigured into new uses; as such, we relied on the distinction between general and task-specific knowledge in order to code these resources. By definition, general human capital, such as education level, reflects a relatively broad scope of knowledge and can easily be used in alternative settings (Becker, 1964). As a result, general human capital was coded as versatile. On the other hand, task-specific human capital is defined as relevant to a particular activity but has little value outside of that use (Becker). As a result, task-specific human capital (e.g., training in a particular competency, such as marketing or finance; D. Miller, Le Breton-Miller, & Scholnick, 2008) was considered nonversatile. We consider industry experience as not versatile since its reapplication is primarily confined to industry boundaries. Previous start-up experience (Hmieleski & Baron, 2008), however, is considered versatile since this process knowledge can be more broadly redeployed, including across industries (MacMillan, 1986).

Second, we coded internally fungible resources as versatile. While task-specific resources cannot easily be redeployed to alternative uses, Penrose’s theory emphasizes that firm-specific resources may provide a range of potential services within a firm. Penrose (1959/1995: 46, 53) explicitly emphasizes the role of joint experience in allowing for new productive services to become visible, thus expanding the productive opportunity set of the firm. For this reason, we consider top management team tenure (TMT) and CEO tenure as versatile. Penrose (41-42) also emphasizes the collective knowledge of the management team; thus, measures that reflect a greater range of productive services, such as TMT diversity and team size, were coded as versatile. In addition, alliance and acquisition experience are considered versatile since firms are able to generate new productive services from this experiential learning (Kumar, 2009).

Technology resources, while often firm specific, may provide a “technological base” for the firm to expand in new directions (Penrose, 1959/1995: 104-112) and are considered generally to have a relatively broad range of application (Danneels, 2007; Parkhe, 1992). Thus, technology resources, such as patents (Bogner & Bansal, 2007), 6 R&D intensity (Lu & Xu, 2006), and technological competencies (Park & Lou, 2001), are considered versatile. Finally, reputation and investments in brands differ in the range of productive services they provide. We consider general indicators of reputation, such as overall firm quality (Cho & Pucik, 2005) and advertising intensity (e.g., Paul & Wooster, 2008), as redeployable since they can be utilized in the introduction of new products and services (Anand & Delios, 2002). However, reputation for a particular product or characteristic, such as social responsibility (McGuire, Schneeweis, & Branch, 1990), is considered relatively less redeployable to other contexts and, thus, not versatile. In total, 63% of our resources are considered to be versatile.

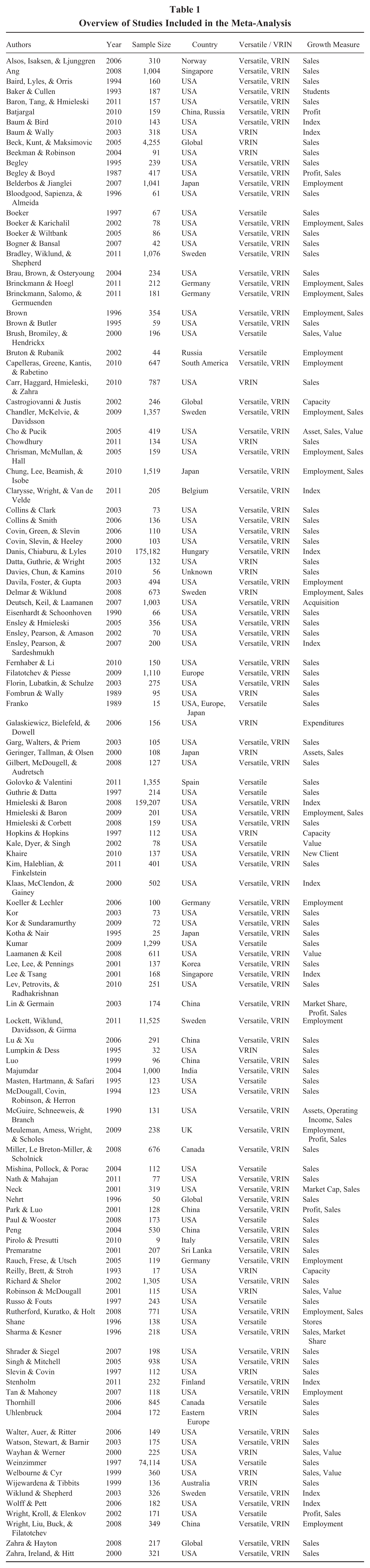

Table 1 provides a summary of each study used in the meta-analysis, identifying not only whether it had VRIN and/or versatile resources represented but also the type of growth measured. Table 2 provides an overview of our coding scheme. We illustrate coding decisions of select resources by presenting the logical connection to definitions of VRIN and versatile resources.

Overview of Studies Included in the Meta-Analysis

Overview of Coding Scheme

Note: TMT = top management team.

Meta-Analytic Procedures

Point estimate correlations

We estimated the mean-corrected effect size (rcor) based on bivariate correlations by using Hunter and Schmidt’s (2004) validity generalization methods and following recommendations for the application of meta-analysis techniques specifically for management research (Geyskens, Krishnan, Steenkamp, & Cunha, 2009). First, we corrected for reliability of measurements. Second, we corrected for artificial dichotomizations (Geyskens et al.). Third, we addressed the nonindependence of effect sizes. While many argue that it is essential to prevent stochastic dependencies by ensuring the independence of effect sizes, the solution of averaging effect sizes from the same study risks inappropriately aggregating dissimilar concepts. 7 In our case, conceptual ambiguity is a greater risk than stochastic dependence. Thus, we use all available effect size information (Carney, Gedajlovic, Heugens, van Essen, & van Oosterhout, 2011; van Essen, van Oosterhout, & Heugens, 2013). 8

Because of the heterogeneous nature of the sample collection procedures in our studies, we utilize random effects models to identify point estimates (Carney et al., 2011). This method corrects for sampling error and provides a sample size weighted average effect size and variance. We compute the homogeneity Q statistic to assess the level of variance in effect size distribution and indicate the existence of potential moderators.

Moderator analysis

Hypotheses 1 and 2 are tested using meta-analytic moderators. Moderators in meta-analysis differ from regression terms in standard regression models. Since our variable of interest is the size of the effect between two variables (resources and growth), meta-analytic moderators test whether this effect is stronger or weaker under certain conditions (VRIN and versatility). We first followed Crook et al. (2008) and divided effect sizes into subgroups in order to compare the mean-corrected effect size in each group.

Meta-analytic regression analysis

We also utilize meta-analytic regression analysis (MARA) developed at the individual effect size level to provide a more robust test of our hypotheses (Heugens, van Essen, & van Oosterhout, 2009). MARA is a type of weighted least squares regression analysis developed to assess moderators by examining variance in the effect size distribution (Lipsey & Wilson, 2001). Individual observations (effect sizes) with less variance are given stronger weight by using the inverse of their squared standard error. Rather than relying on differences in subgroup point estimates, meta-regression allows us to test the effect of multiple meta-analytic moderators simultaneously (Carney et al. 2011; Heugens & Lander, 2009; Lipsey & Wilson). As a result, we can answer criticism that meta-analysis is not suitable for assessing multivariate relationships (Guzzo, Jackson, & Katzell, 1987) and examine the relative explanatory power of moderators. As C. C. Miller and Cardinal state, “Analyzing [moderator] variables simultaneously in a multiple regression format allows proper assessment of the relative explanatory power of each variable because those variables directly compete against one another in the same statistical analyses” (1994: 1653). This provides additional information on the relative importance of VRIN compared to versatility.

Meta-regression procedures also allow us to take into account heterogeneity in research designs, growth measurements, and study contexts that may affect effect sizes. To do so, we assigned dummy variables (0, 1) to each effect size depending on study and variable characteristics. Research design items include studies that were cross-sectional and in which growth was not the dependent variable (growth not DV). Since not all measures of growth are highly related (Shepherd & Wiklund, 2009), we examine the choice of growth measurement by coding long-term growth (greater than 5 years) versus short-term growth, relative growth (a percentage or relative to competitors) versus absolute growth, and sales growth (the single most common growth measure in our sample at about 50%) versus alternative growth measures. We take into account context-specific variables, such as whether a sample consisted exclusively of manufacturing (vs. service and mixed) or small (< 100 employees) firms. Since growth may be dependent on macroeconomic factors, we also account for change in gross domestic product (GDP) in each country during the sample time span (World Bank, 2012). If a study did not specify the time of data collection, we average the 2 years prior to the year of publication as a proxy. In order to mitigate the concern of (partial) nonindependence of effect sizes, we use study controls—dummy variables to capture whether particular effect sizes were derived from the same sample. We utilize mixed-effects meta-regression specification, which has less statistical power but is more conservative and appropriate for management research than fixed effects (Carney et al., 2011; Geyskens et al., 2009). To ensure that effect sizes are normally distributed, we employ Fisher’s Z transformation (Fisher, 1928; Hedges & Olkin, 1985).

Results

Table 3 provides an overview of the study-level point estimates and the subgroup analyses. To show the influence of measurement reliability, we present the uncorrected mean effect size (r), the mean-corrected effect size only when reliability information is available for an effect size (rcor), and the corrected effect size using average reliabilities (rcor2). For the sake of simplicity and because individual-level measurement correction is preferred (Geyskens et al., 2009), we discuss rcor.

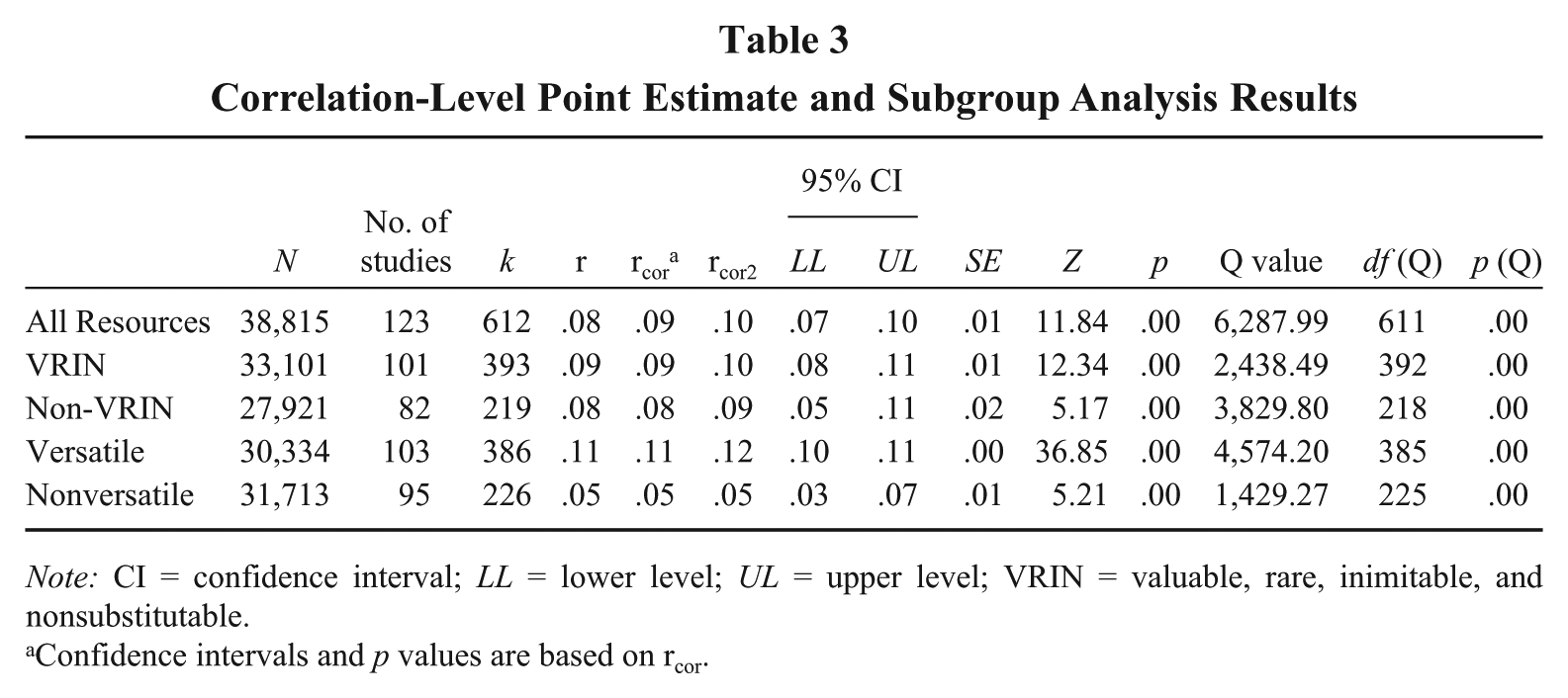

Correlation-Level Point Estimate and Subgroup Analysis Results

Note: CI = confidence interval; LL = lower level; UL = upper level; VRIN = valuable, rare, inimitable, and nonsubstitutable.

Confidence intervals and p values are based on rcor.

Table 3 shows that, as expected, there is a positive correlation between resources overall and growth (.09, p < .01). VRIN resources have a correlation with growth of .09, while non-VRIN resources have a correlation of .08. The 95% confidence intervals between the two groups overlap, so we cannot make any conclusions regarding statistical difference between the two groups. As a result, since VRIN resources do not have a statistically stronger impact on growth, Hypothesis 1 is preliminarily rejected. Versatile resources have a mean effect size of .11 compared to .05 for nonversatile resources, and the 95% confidence intervals of these two groups do not overlap. As a result, Hypothesis 2, which stated that versatile resources would have a stronger relationship to growth, is preliminarily supported.

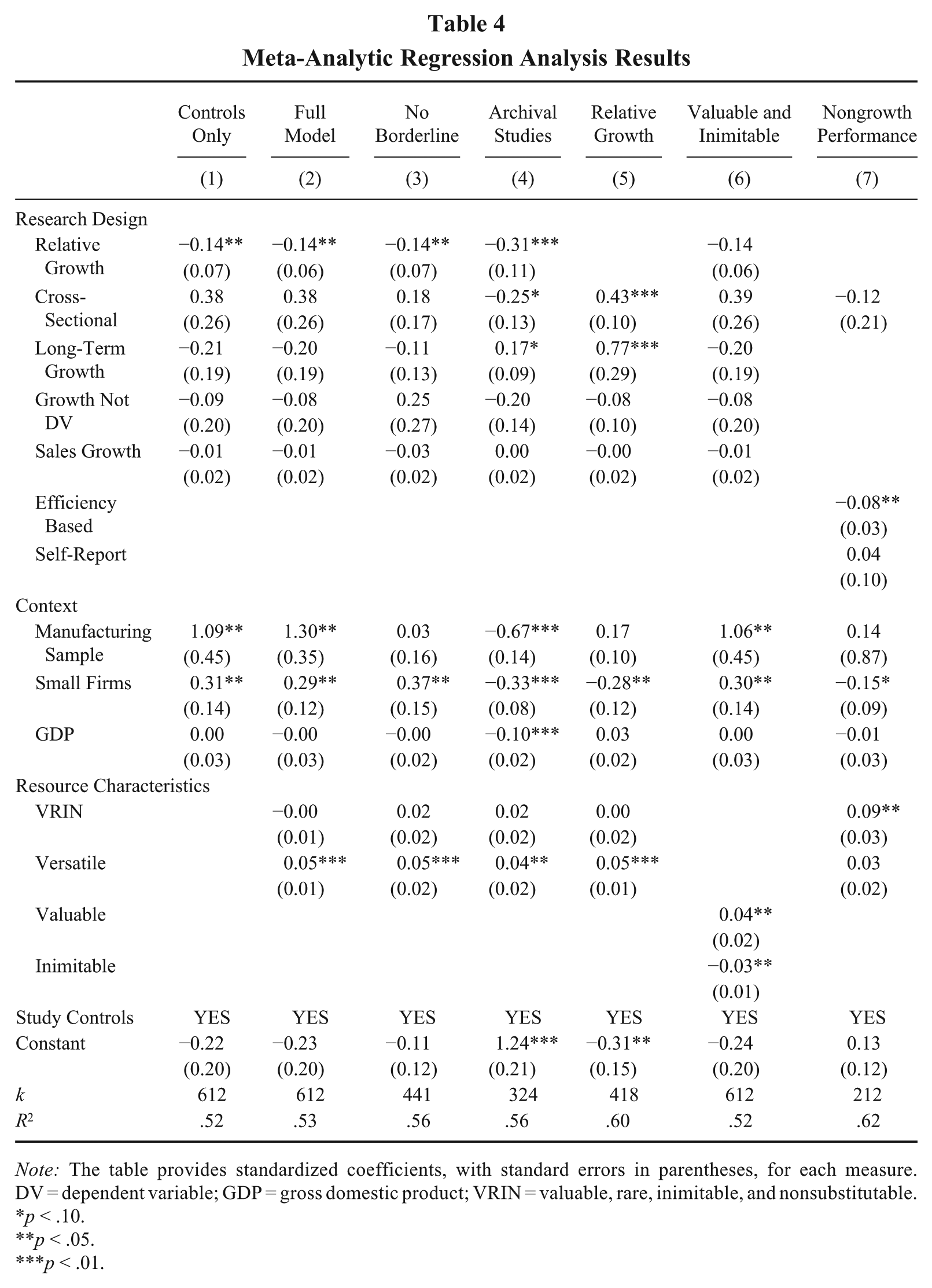

To provide a more robust test of Hypotheses 1 and 2, we present the MARA results in Table 4. Model 1 introduces the research design, context moderators, and study controls. Relative growth is negative and significant, indicating that resources have smaller effects on measures that are growth rates or represent growth relative to competitors. In addition, resources have a stronger effect on growth in manufacturing and in small firms.

Meta-Analytic Regression Analysis Results

Note: The table provides standardized coefficients, with standard errors in parentheses, for each measure. DV = dependent variable; GDP = gross domestic product; VRIN = valuable, rare, inimitable, and nonsubstitutable.

p < .10.

p < .05.

p < .01.

In examining the focal meta-analytic moderators of resource characteristics introduced in Model 2, we see that the regression coefficient of VRIN is negative and the effect is not significant (β = −0.001, p > .1). This provides further confirmation that Hypothesis 1 should be rejected. Next, we see that the coefficient for versatile resources is positive and significant (β = 0.05, p < .01). This indicates that versatile resources have a stronger relationship to growth than nonversatile resources and provides further support for Hypothesis 2.

Robustness Tests

We conducted several additional tests to ensure the robustness of our results. First, we subjected our coding scheme to further scrutiny. Although versatility and VRIN characteristics are conceptually continuous, ranging from high to low, we followed RBV convention and meta-analytic precedence by coding each dichotomously. However, there are individual resources that were considered close to the borderline between versatile and nonversatile or VRIN and non-VRIN. Borderline cases arose from initial coding discussions, coding disputes, and reviewer comments. For versatility, we identified the following variables as borderline: R&D intensity, advertising intensity, alliance experience, acquisition experience, technological capabilities, CEO tenure, previous start-up experience, and patents. In each of these cases, the resources were judged to offer a range of potential services and as such were coded initially as versatile. However, the extent of the versatility may depend on firm-specific or industry conditions and, thus, deserve additional scrutiny. 9 For VRIN resources, we flagged slack resources and financial capital as borderline in terms of imitability. Both are generic resources that do not have isolating mechanisms and, thus, following precedent, they were coded imitable (Crook et al., 2008). However, it is very difficult, practically speaking, for firms to mimic the financial and slack resources of other firms, especially in regards to the large cash holdings of some contemporary industry leaders. 10 We then excluded flagged borderline VRIN and versatile resources and reran the analysis (see Model 3 of Table 4). With this specification, we utilize coding categories that have a Cohen’s kappa value of 1. Our sample is reduced to 441 observations, but versatility remains significant (β = 0.05, p < .01) and VRIN remains insignificant (β = 0.02, p > .1). This provides further confidence in the robustness of our coding schemes and results.

Second, we test our model using only archival variables. The relationship between resources and growth captured from primary survey data collection may artificially inflate effect sizes due to common method bias. 11 Table 4, Model 4 reveals that we do not find any changes regarding the main effects with this subsample analysis—versatility is still positive and significant (β = 0.04, p < .05) and VRIN is still not significant (β = 0.02, p > .1). However, we find that amongst archival studies, resources have a significantly weaker effect in manufacturing samples, in samples of small firms, and during greater GDP growth. Since these effects are positive when including primary samples, this suggests either that there might indeed be some common method bias in studies using self-reporting or that self-reported measures are associated with less measurement error. Finally, since the resource-growth relationship is weaker when using relative performance measures, we ran our model with only relative growth measures to ensure that our results are not sensitive to this type of growth indicator. As Table 4, Model 5 shows, our results remain consistent (versatility: β = 0.05, p < .01; VRIN: β = 0.004, p > .1).

Post Hoc Statistical Analysis

Thanks to the large number of studies and effect sizes identified, we were able to conduct more fine-grained theory tests beyond the actual hypotheses. As noted in our theoretical development, the Penrosean perspective suggests that excess resources provide entrepreneurial managers with both the incentives and the means for expansion. To test this, we located studies including measures of slack and found a total of 37 slack effect sizes. The correlation with growth is .058, but it is not statistically significant (p > .1). Next, we examined a potential interaction effect of versatility and slack. Penrose’s writings could be interpreted as though versatile resources are particularly important when there are also excess resources. We therefore examined all resource effect sizes coming from studies that utilized comparable measures of slack. We examined the mean slack value from 9 studies that directly captured or allowed us to convert debt/equity or debt/assets. We then created a dichotomous variable coded 1 for samples below the median and 0 for samples above the median (since indicators are inverse of slack). We then analyzed 41 resource effect sizes in these 9 samples and found that the correlation with growth for versatile resources was slightly higher in samples with relatively higher slack levels (rcor = .05, p > .1) compared to samples with relatively lower mean slack levels (rcor = .03, p > .1). However, neither of these correlations was significantly different from zero or from each other. As a result, we do not find any support that resource versatility is conditional on the availability of slack resources. Nevertheless, this lack of a result might be associated with the relatively small pool of studies with comparable slack measures.

Second, Penrosean theory notes that through experience, managers learn about new and more effective ways of using and combining resources to expand the productive opportunity set. We conducted analyses using absorptive capacity as a proxy for an organization’s knowledge and ability to learn about its resource base. Absorptive capacity represents a firm’s “ability to recognize the value of new information, assimilate it, and apply it to commercial ends” (Cohen & Levinthal, 1990: 128). We examined both the direct effect and contingent effect of absorptive capacity. Regarding the direct effect, we treat absorptive capacity as its own resource category and find a significant correlation with growth of .15 (p < .01). This provides evidence that organizational learning and knowledge has a relatively strong positive influence on growth compared to other resource effects in our study. Regarding the contingent effect, we examined whether versatile resources were stronger in relatively high absorptive capacity samples. We have 11 studies that measure absorptive capacity in the same manner (R&D expenditure/sales) and, thus, can be directly compared. We recorded the mean value of absorptive capacity reported in the descriptive statistics of each of these studies and calculated the median value across them. We then created a dichotomous variable coded 1 for samples greater than the median and 0 at or below the median. We then analyzed the 44 resource effect sizes in these 11 samples and found that the mean effect size for versatile resources was stronger in relatively high absorptive capacity samples (rcor = .10, p < .05) than in low absorptive capacity samples (rcor = −.01, p > .1). This provides some support for the Penrosean assertion that organizational knowledge and learning may influence a firm’s ability to utilize versatile resources.

Third, in order to explore further the insignificant effect of VRIN on growth, we conducted MARA (see Table 4, Model 6) with the same specifications as our primary model (see Model 2) except that we used inimitable and valuable as separate resource characteristics (and removed VRIN and versatile). We find that valuable resources have a significantly positive effect on growth (β = 0.04, p < .05), while inimitable resources have a significantly negative effect (β = −0.03, p < .05). We return to these results in our discussion.

Finally, we examine the effect of resources on nongrowth-related performance indicators. We identified 41 studies in our sample that include nongrowth performance measures and recorded their effect size with individual resources. Table 4, Model 7 shows the results of the MARA using these 212 effect sizes. We add controls for efficiency and self-reported performance measures. We find that versatility does not have a significant impact on the relationship between resources and performance (β = 0.03, p > .1), while VRIN resources do have a significant effect (β = 0.09, p < .01). This supports previous findings regarding the positive relationship between VRIN resources and performance generally (Crook et al., 2008) and, together with our main results, highlights the unique nature of growth as a performance outcome.

Discussion

Narrative reviews have painted a bleak picture of the firm growth field (Davidsson, Achtenhagen, & Naldi, 2005; Shepherd & Wiklund, 2009). The results of our study indicate that slow knowledge accumulation on firm growth may be due in part to theoretical misapplication. Firm resources are broadly beneficial for growth, but we find systematic differences across resource characteristics. While extant literature has largely treated resources in a similar theoretical vein, we demonstrate that Barney (1991) and Penrose (1959/1995) differ in specifying how resources with certain characteristics are linked to firm outcomes. Furthermore, our results indicate that these distinct strands of resource-based theorizing do not explain growth equally well. In support of Penrose’s theorizing and our Hypothesis 2, we find that versatile resources have a stronger effect on growth than nonversatile resources. On the other hand, contrary to Hypothesis 1, we find no support for the notion that VRIN resources are linked to higher levels of growth than non-VRIN resources. This is an interesting finding, particularly in light of Crook and colleagues’ (2008) finding of a strong positive effect of VRIN resources on performance and the fact that we closely follow their research design. As our post hoc analysis demonstrates, the reason is that growth is a unique performance outcome and that RBV is not equally suited to explain all types of performance.

RBV and Growth

Our findings suggest future growth studies should refrain from using a strict VRIN interpretation of RBV. In RBV, valuable resources allow firms to implement efficient strategies (Barney, 1991: 106), and RBV’s link to competitive advantage mirrors economics’ focus on rents and profitability (Amit & Schoemaker, 1993; Peteraf, 1993). Our post hoc analysis supports the positive relationship between VRIN resources and nongrowth-related performance. Growth, however, does not necessarily concern the implementation of efficient strategies (cf. Barney) or the pursuit of supranormal profits (cf. Foss & Knudsen, 2002). At best, growth is weakly correlated to profitability (Delmar, McKelvie, & Wennberg, 2013; Narayanan, 2012). Growth also does not necessarily concern performance relative to competitors. RBV follows in a tradition that situates the firm in an adversarial relationship with environmental actors (cf. Porter, 1980). Firms seek to control resources that allow them to capture associated rents, protect those resources from external threats, and develop a competitive edge over others in the market place. Growth, on the other hand, can be the result of favorable environmental conditions that benefit an entire industry, or it can be achieved through the use of cooperative strategies (Ang, 2008; Singh & Mitchell, 2005). While competitive dynamics certainly affect growth, a primarily competitive orientation may not be the ideal theoretical framework to explain growth.

Our analysis of the individual characteristics of value and inimitability sheds further insight into the VRIN-growth relationship. We find that valuable resources have a positive influence on growth, but inimitable resources have a negative influence. The contradictory effects of separate VRIN characteristics undermine RBV approaches that treat VRIN characteristics as positively covarying and additive in nature. Our results reveal that VRIN resource characteristics can have opposing effects on the same performance outcome. Exploring such tensions between resource characteristics is a worthwhile pursuit for future RBV research (cf. Gras & Nason, 2013).

The negative effect of inimitable resources is particularly interesting when considered alongside the positive effect of versatility. The isolating mechanisms that create inimitable resources in RBV are the same conditions that make resources less externally versatile and vice versa. In other words, RBV and Penrosean conceptualizations make opposite predictions concerning how resource characteristics relate to growth. Our meta-analytical findings clearly reject the RBV notion and support the Penrosean idea that growth can be fostered by resources that can be easily applied to alternative uses within and between firms. While valuable resources allow firms to create new streams of value and, thus, grow, the isolating mechanisms of RBV (e.g., inimitability) may lock in streams of rent by limiting competition (Peteraf, 1993) at the expense of the flexibility necessary for future resource configuration. This cuts to the core of the difference between performance outcomes: Resource characteristics that are good for profitability may be bad for growth. As a result, firms should develop their resource portfolios differently (protecting from imitation vs. building for versatility) depending on their desired performance outcome (profitability or growth). Our analysis also provides theoretical grounding to the finding from Autio, Sapienza, and Almeida (2000) that firms with more imitable resources had faster rates of international sales growth, which surprised the authors. Our research explains this unexpected finding. More versatile resources are associated with greater growth.

Resource Versatility—Findings and Suggestions for the Future

Our findings indicate that future research on growth would benefit from building on a theoretical basis more closely aligned with Penrosean theory, specifically, the resource characteristic of versatility. Growth requires frameworks distinct from those explaining relative performance differences (cf. Shane & Venkataraman, 2000). Versatile resources provide the means to exploit opportunities when they are recognized, confer the flexibility to adapt to evolving environmental conditions, and enable the pursuit of Schumpeterian resource combinations. Resource versatility stems from the range of potential services that a resource provides and, thus, incorporates not only generic and tradable resources that can be exchanged between firms but also idiosyncratic assets that can be redeployed by a specific firm into new arenas. Since Penrosean growth theory is free of the inimitability criterion, the distinction between externally or internally fungible resources is not important, and we are able to resolve confusion in the fungibility literature with the overarching concept of versatility.

While the concept of resource versatility is useful in understanding growth, our results also indicate that there is more to the picture. Performance is generally difficult to explain, and predicting growth has proven particularly elusive (Coad, 2010). Geroski (2000) concluded that growth rates were nearly random. Our meta-analytical findings reject the notion that growth rates are random. However, while our effect sizes (.06 to .12) are on par with other studies of firm-level performance outcomes (Carney et al., 2011; Unger, Rauch, Frese, & Rosenbusch, 2011), the relatively low level of explained variance highlights that current theoretical and methodological approaches fall short of explaining firm growth to any larger extent. Previous research, including this paper, has focused primarily on the resource-related dimensions of Penrose’s theory. We focus on a salient resource characteristic that permeates Penrose’s theory (versatility), but we do not provide a comprehensive treatment of her theory, which she herself admits is complex to test (Penrose, 1959/1995: 213). Explicating additional non-resource-specific concepts embedded in her theory may prove generative for future growth research. For instance, the “productive opportunity set” of the firm, which “comprises all of the productive possibilities that its ‘entrepreneurs’ see and can take advantage of” (Penrose: 28) is a central concept in her theory. According to Penrose, the size of the productive opportunity of a firm is dependent on the ability of managers to develop and combine resources in productive ways rather than on external demand conditions. However, it is important to recall that Penrose’s theory was developed during a post–World War II period of steady economic boom and, thus, competition and demand placed few constraints on firms’ growth prospects (Lockett et al., 2011). However, in today’s uncertain economic conditions, there is a greater burden on managers to conceptualize opportunities and construct new resource uses in order to drive productive opportunity set expansion. For example, Penrose’s idea of the managerial mind-set links well with the recent stream of literature examining entrepreneurial cognition (Grégoire, Corbett, & McMullen, 2011) and managerial capabilities (Kor & Mesko, 2013). Devoting more attention to cognitive, managerial, and other factors that shape and expand the productive opportunity set is likely to lead to theory that is better able to explain growth than a focus on resources alone.

To some extent, other streams of resource-related theorizing have paid greater attention to how growth opportunities are available in the environment. For example, Wernerfelt (1984) drew explicitly on the growth-share matrix concept popularized by the Boston Consulting Group in an effort to examine how firm resources can predict the future growth prospects of a firm. Theorizing about dynamic capabilities, Eisenhardt and Martin (2000) note that resource requirements differ depending on environmental conditions, and in dynamic environments, resources need to be constantly configured (cf. Teece, Pisano, & Shuen, 1997). The concept of resource versatility complements this logic nicely and may serve as a useful resource characteristic in the dynamic capabilities literature stream.

The Penrosean distinction between resources and services is another useful concept for future growth research. An implicit assumption in the growth literature that we reviewed is that firms rely on the resources within their organizational boundaries to generate growth. 12 However, the rise of collaborative interorganizational relationships has demonstrated that firms can leverage resources outside of their boundaries in concert with their own resources to further fuel growth (cf. Gulati, Lavie, & Singh, 2009; Ring & Van de Ven, 1994). In Penrosean terms, firms can utilize services rendered from resources they do not own in order to expand their productive opportunity set. Relaxing the assumption that resources available for growth reside exclusively within the ownership boundaries of the firm is an important avenue to arrive at a more complete understanding of the drivers of contemporary firm growth. Utilizing external resources is likely to create permeable boundaries and may have differential impacts on growth dimensions that are controlled by the firm (e.g., assets and employees) compared to those that are generated (e.g., sales and valuation; Nason, 2014). The decision to utilize internal, external, or a blend of both resources for growth also reveals a firm’s chosen growth mode (McKelvie & Wiklund, 2010). In our review, we examined whether studies made distinctions between growth that is generated organically, through acquisitions, or through hybrid forms (such as joint ventures or alliances; cf. McKelvie & Wiklund). Unfortunately, such distinctions were rare. Clarifying growth mode is important for theorizing to be able to untangle complexity in the phenomenon and keep up with changes in how contemporary firms choose to grow.

The moderators of our MARA also reveal important contextual considerations of industry and firm size for growth research. The strength of relationships between resources and growth varies across industries and firm size. While most growth studies use industry and size control variables, our meta-analysis suggests that firm size and industry should be more directly theorized and isolated in empirical samples. Indeed, these factors may also provide a meaningful basis on which to develop new growth theory.

Our analyses also revealed that the measurement choice of relative or absolute growth indicators influences the strength of the relationship between resources and growth. In analyzing the correlation of a wide set of different growth measures, Shepherd and Wiklund (2009) generally found low correlations and proposed that it might be futile to search for a general theory of growth because different measures seem to capture different facets of a complex phenomenon. Our findings seem to confirm this notion. Different aspects of growth capture different dimensions of the phenomenon and require specific theorizing. We encourage researchers in future growth studies to more carefully consider diversity in growth measures and develop theory tailored to specific growth dimensions (for suggestions, see Shepherd & Wiklund).

More generally, this research provides further support for the need to increase specificity of performance outcomes in strategy theorizing (C. C. Miller, Washburn, & Glick, 2013). Continuing to build theory to explain “performance” broadly while using not only heterogeneous indicators but also entirely distinct concepts prevents term correspondence and knowledge commensurability. This ultimately retards unified theoretical development. While our results suggest that growth is a distinct performance outcome, we suspect that many other performance outcomes also require specific theorizing. Our theorizing and findings indicate that there are critical differences depending on the type of performance outcome analyzed.

Limitations

As with every study, ours includes limitations. First, we may have missed some studies on growth. Conceptually, we approached our study as a means to make sense out of a fragmented field of research and advance theoretical development on firm growth. As a result, we searched for studies to include on the basis of the dependent variable (growth) rather than the independent variable (resources). Thus, we utilize studies that seek to contribute to research on firm growth and inductively identify factors that have been used to explain growth. However, we may have missed studies that did not actively engage in the topic of firm growth but instead simply utilized growth as the empirical indicator for the construct of performance. Second, while we focus on the relationship flowing from resources to growth, it may also be possible that growth allows for the development of resources with certain characteristics. We are not able to tease out such effects in our sample of bivariate effect sizes, but it remains an interesting and important question for future research. Third, we do not have many unpublished studies (only three unpublished dissertations) in our meta-analysis and, thus, may overestimate effect sizes as a result of publication bias. In order to assess this limitation, we used Rosenthal’s (1979) file drawer statistic (also known as fail-safe N) and the preferred Duval and Tweedie’s (2000) trim and fill method. Rosenthal’s file drawer statistic indicates that 4,112 with a null result would be needed to negate the positive effect of resources on growth (5,826 for versatile resources and 1,514 for VRIN). Using Duval and Tweedie’s trim and fill method, we find an adjusted correlation of .027 for all resources and .067 for versatile resources, but both remain significant, indicating that publication bias does not invalidate our conclusions. On the other hand, using trim and fill, we find that the VRIN resources correlation with growth is reduced to .001 and is no longer significant. This indicates that the positive effect of VRIN resources on growth that we find may be due to publication bias.

Conclusion

In this paper, we offer novel insights into alternative characteristics of resources that derive from the same resource-based conceptualization of the firm. Our results indicate that VRIN resources and the efficiency-based logic of RBV do not explain firm growth, while the Penrosean characteristic of resource versatility is linked to higher levels of growth. These insights provide greater specificity to the heterogeneous performance construct and distinguish between distinct strands of resource-based theorizing. Future research on firm growth should seek to build on a resource-based approach that more closely aligns with Penrosean theory.

Footnotes

Acknowledgements

This article was accepted under the editorship of Patrick M. Wright. We would like to thank Editor Bill Schulze for his insightful guidance in the review process, and we appreciate the constructive comments of two anonymous reviewers. The paper has also benefitted from comments on previous versions by Jan Brinckmann, Michael Carney, Russell Crook, Ravi Dharwadkar, David Gras, Mike Hitt, Tom Lumpkin, Alex McKelvie, Scott Newbert, and Marc van Essen. We are thankful for research assistance in later stages of this manuscript by Jérémie Peloso, Rudy Grow, and David Michael. We are grateful for funding provided by the Whitman School of Management and the Fonds de recherche du Québec–Société et culture.

Supplemental material for this article is available with the manuscript on the JOM website.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.