Abstract

Existing studies on subunit power largely rely on the premise that a firm’s subunits are connected through resource exchanges. In this study, we introduce two novel constructs—market periphery and market overlap—to capture the power of subunits that do not directly involve resource exchanges. Drawing on resource dependence theory, we advance a subunit power approach to argue that the dependence of the firm on its subunits for sales can help predict headquarters’ decision on subunit exits in the form of divestiture, dissolution, or spin-off. Using subunit data of a population of U.S. insurance groups in a longitudinal setting, we find that market periphery and overlap increase the hazard of subunit exit. However, a subunit’s relative sales growth reduces the positive effect of overlap on its hazard of exit, whereas external linkage lessens the positive effect of periphery on its hazard of exit.

Introduction

Scholars have long emphasized the importance of subunit power in the headquarters-subunit relationship (Hickson, Hinings, Lee, Schneck, & Pennings, 1971; Pfeffer & Salancik, 1978), which may affect headquarters’ strategic decisions (Ambos, Andersson, & Birkinshaw, 2010), such as subunit exit (Xia & Li, 2013). There are two possible approaches to identify subunit power: the interdependence-based approach and the market dependence–based approach. Most existing studies adopt the interdependence-based approach, which relies on the premise that resource (economic) exchanges exist among sister subunits because they engage in different value chain activities (Balcaen, Ooghe, & Manigart, 2011; Dörrenbächer & Gammelgaard, 2011). This approach views exchange networks within a firm as a source of subunit power (Andersson, Forsgren, & Holm, 2007; Cook, 1977; Cook & Emerson, 1978), indicating that the relative power of a subunit over another is its network centrality in the exchange networks (Hickson et al., 1971). Although this approach of subunit power within a firm is appealing, its application scope to understand headquarters’ decisions is limited because it does not explain the relative power of subunits that do not involve resource exchanges.

In this study, we advance a market dependence–based approach of subunit power, drawing on resource dependence theory (RDT; Pfeffer & Salancik, 1978). This approach is important for two reasons. First, it provides complementary insights to existing studies for a more complete understanding of subunit power because it highlights the fact that an individual actor’s power may not always originate from dyadic relationships or exchange networks (Finkelstein, 1992; Kehoe & Tzabbar, 2015; Tzabbar & Kehoe, 2014). Observations show that unlike subunits in manufacturing firms, in which sister subunits may serve as suppliers or buyers to manage different value chain activities, subunits in many service industries—such as airline (Gimeno & Woo, 1996), fast food (Kalnins, 2004), hospital (Boeker, Goodstein, Stephan, & Murmann, 1997), and insurance (Li & Greenwood, 2004)—rarely exchange their resources for inputs or outputs directly with one another because they engage in the same value chain activity (i.e., sales to end markets). The market dependence–based approach focuses on multiunit firms that depend on portfolios of business-geographic markets for survival (Gimeno & Woo, 1996), whereby the relative importance of each niche market shapes the relative power of a subunit that manages the niche market (Nienhüser, 2008; Pfeffer & Moore, 1980).

Second, the market dependence–based approach allows us to extend RDT to capture the relative power of subunits that engage in the same chain activity to understand headquarters’ decisions beyond existing studies. We raise the following question: How does subunit power affect headquarters’ decisions on subunit exits? As important strategic decisions made by headquarters, subunit exits—including subunit dissolution, divestiture, or spin-off—have received substantial research attention in the organization and strategy literatures (Brauer, 2006; Mitchell, 1994; Xia & Li, 2013). Building on the notion of multiplicity of market dependence (a combined dependence on business and geographic markets), we extend RDT by introducing two constructs—market periphery and market overlap—to capture the relative power of subunits. Market periphery refers to the extent to which the business-geographic market of a subunit is noncore in the firm’s market portfolio. Subunits that manage a firm’s peripheral businesses are less powerful owing to their lack of criticality (Pfeffer & Davis-Blake, 1987). Meanwhile, market overlap denotes the extent to which the business-geographic market of a subunit overlaps with those of other subunits in the firm’s market portfolio. Subunits with higher degrees of market overlap are less powerful owing to their substitutability (Jacobs, 1974).

Building on this conceptualization of subunit power, we propose that subunits in managing peripheral and overlapping markets are more vulnerable to headquarters’ exit decisions because the firm depends less on them for survival. However, less powerful subunits may change their disadvantaged positions by taking actions to increase the dependence of the firm on the subunits (Emerson, 1962) or by enhancing their abilities to gain resources and maintain operational stability (Pfeffer & Salancik, 1978). To understand the boundary conditions of the proposed relationship between subunit power and exit decision, we introduce a subunit’s relative sales growth and external linkage as moderators because these factors may enhance the subunit’s position within the firm and thus alter the proposed relationship.

Our study makes two main contributions. First, we expand the vistas of the RDT literature (for reviews, see Hillman, Withers, & Collins, 2009; Wry, Cobb, & Aldrich, 2013), which has typically focused on power relations between firms, by investigating power relations within the firm (the headquarters-subunit relationship) and advancing a subunit power perspective. From this perspective, we add to RDT by developing market periphery and overlap as two novel constructs to capture the power of subunits that engage in the same value chain activity. This contribution is important because earlier studies have heavily relied on the premise that sister subunits are also exchange partners (Hickson et al., 1971).

Second, our theorization of subunit power broadens the research scope by building on the observation that sister subunits may not directly involve resource exchanges. It provides an avenue for research on subunit exit by drawing attention to certain types of subunit power (periphery and overlap), which are novel to the RDT and subunit exit literatures. In addition, we introduce the relative sales growth and external linkage of the subunit as moderators in the proposed subunit power–exit relationship, in response to the repeated calls for clarifying the boundary conditions of RDT (Hillman et al., 2009; Pfeffer, 2003).

Theoretical Background

Market Dependence and Subunit Power

Power has been a central theme in RDT (Pfeffer, 2003; Wry et al., 2013). Rooted in theories on exchange and power (e.g., Blau, 1964; Emerson, 1962; Hickson et al., 1971; Jacobs, 1974; Thompson, 1967), RDT emphasizes the importance of external dependence as a source of subunit power to the understanding of organizational adaptation to the external (market) environment (Pfeffer, 2003: xi–xii). Market dependence refers to the extent to which the proportion of a firm’s sales comes from a given market (Gimeno, 1999). From this perspective, a firm’s internal distribution of power among its subunits is, at least partly, attributed to its control over external dependence contexts, such as the end markets. As Pfeffer and Salancik (1978: 230) pointed out, “those subunits most able to cope with the organization’s critical problems acquire power in the organization.” These critical problems often result from environmental dependencies, constraints, and uncertainties. For example, when market demand is unstable, marketing departments are more likely to gain power (Nienhüser, 2008; Pfeffer & Moore, 1980; Salancik & Pfeffer, 1974). However, the RDT literature is silent on how subunits that engage in the same value chain activity gain power within the firm.

We argue that the dependent relationship between headquarters and subunits within multiunit firms provides an opportunity to advance RDT for a more nuanced understanding of subunit power. A multiunit firm may rely on its relatively independent subunits to manage different niche markets (Kochman, 1975; Thompson, 1967). As such, the relative importance of a niche market for the firm’s survival determines the power of the subunit that manages the niche market. This argument is in line with the RDT perspective that the internal distribution of subunit power can be defined by the dependence of firms on certain environments (markets) for resources (outputs; Nienhüser, 2008; Pfeffer & Salancik, 1978).

Moreover, by differentiating the relative importance of each niche market, a more nuanced understanding of subunit power within RDT is possible. One of the ways to define subunit power is to identify a firm’s critical niche markets (Lawrence & Lorsch, 1969). As noted by Castrogiovanni (1991: 547), “examination of similarities and differences across organizational subunits requires analysis of their respective subenvironments.” Kochman (1975) found that subenvironments were better predictors of power concentration among subunits than the total environment. In multiunit firms, subunit sales are specific to different niche markets. Thus, subunit power can be defined in terms of the relative importance of these niche markets managed by the specific subunits, on which the firm depends for outputs. In this paper, we develop two constructs to capture the relative importance of each niche market and subunit power: market periphery and market overlap.

Multiplicity of Market Dependence and Dimensions of Subunit Power

Scholars have long differentiated two power-dependence dimensions: criticality and substitutability of external (e.g., market) resources (Jacobs, 1974; see also Pfeffer & Salancik, 1978: 46–51). The criticality of the resource refers to the ability of an actor to continue functioning in the absence of the resource. A market is critical to the organization when the market can affect whether the firm can exist without it (Frooman, 1999). Substitutability denotes the extent to which resources provided by an actor can be replaced by other actors (Emerson, 1962; Tremblay, Côté, & Balkin, 2003). The level of substitutability among actors will be high if their operations are overlapped in the same market and compete for the same customer resources. Pfeffer and Davis-Blake (1987) explicitly suggest that an actor’s power position can be defined by these two theoretical constructs. That is, a subunit’s relative power can be determined by its critical position (Pfeffer, 1981) and nonsubstitutable position to provide a resource to the organization (Hickson et al., 1971; Jun & Armstrong, 1997).

To develop the key constructs of subunit power (i.e., periphery and overlap), we introduce the concept of multiplicity of market dependence to capture multiple niche markets that are divided by different lines of business and geographic locations. Dependence as a multidimensional concept has been traditionally distinguished as either business dependence or geographic dependence. Although each type of dependence constitutes a part of a firm’s market dependence, they work together to affect the firm’s adaptation process by entering or exiting a niche market. The multiplicity approach relies on a comprehensive construct to capture the multiple aspects of the dependence phenomenon, in contrast to using multiple dependence constructs separately. To consider the multiplicity of market dependence as a source of subunit power, we adopt a geographic-business approach (Gimeno & Woo, 1996; Kalnins, 2004), which combines these two dimensions of dependence. For example, if an actor (subunit or firm) operates in two geographic markets with two lines of business, the actor will manage four niche markets (Jayachandran, Gimeno, & Varadarajan, 1999).

We therefore define an actor’s market portfolio as the combination of its business and geographic markets. For multiunit firms, this approach is particularly important because a subunit’s business dependence is inseparable from its geographic location (Mayers & Smith, 1994). 1 Since market portfolios vary between a multiunit firm and each of its subunits as well as among these subunits, the multiplicity approach allows us to identify the relative importance or power of a subunit within the firm in terms of the subunit’s market portfolio against the firm’s market portfolio. Building on this insight, we define market periphery as the extent to which a subunit’s market portfolio is less critical in the firm’s overall portfolio for the firm’s survival. Meanwhile, we define market overlap as the extent to which a subunit’s market portfolio overlaps those of its sister subunits in the firm’s portfolio.

These two constructs not only capture the extent of a firm’s dependence on a given niche market but also reflect the relative power of the subunit that manages the niche market on behalf of the multiunit firm. This approach is in line with that notion that criticality can be embodied in a more central or core position, whereas substitutability reflects the overlap of alternative actors in the same position (Jacobs, 1974). A subunit is less powerful when its market portfolio is less critical for the firm’s survival or when its market portfolio is substitutable by those of its sister subunits (cf. Pfeffer & Davis-Blake, 1987).

A Perspective of Subunit Power on Exit and Its Boundary Conditions

Although the headquarters and subunits are mutually dependent, a hierarchical structure exists between the headquarters and its various subunits. Corporate headquarters at the top of the hierarchy may empower and rely on subunits to manage certain markets. The headquarters also has the right to make a strategic decision and take actions on retaining or divesting a subunit. A subunit exit is often a corporate-level decision, as the headquarters has to manage the subunit portfolio effectively to ensure the success of the firm as a whole. Aghion and Tirole (1997) differentiate between formal authority (the right to decide) and real authority (the effective control over decisions): In the headquarters-subunit relationship, the former represents the power of headquarters, and the latter corresponds to the power of the subunit, given the subunit’s inferior rank in the organizational hierarchy; specifically, headquarters has the right to decide where to compete and operate, whereas the subunit’s power reflects its ability to influence the headquarters’ strategic decision (Dörrenbächer & Gammelgaard, 2011).

In the context of subunit exit, on one hand, the headquarters is the decision maker that evaluates each subunit and decides whether to retain it in the firm’s portfolio. On the other, subunit power may serve as an important constraint when the firm headquarters makes an exit decision. From the subunit power perspective, subunits that control critical and nonsubstitutable resources will have power, and the headquarters will consider the subunit power when making a strategic decision (Nienhüser, 2008; Pfeffer & Salancik, 1978). We argue that subunit exit decisions are likely to be constrained by a firm’s dependence on the critical and nonreplaceable markets. Subunits with high scores of market periphery or market overlap are often in a power-disadvantaged position. Subunits holding a peripheral market position of the firm face a higher hazard of exit because the headquarters relies more on core subunits for critical resources. Moreover, a subunit with a high level of market overlap with sister subunits has more difficulty in maintaining the headquarters-subunit relationship because its business operations can be replaced by the sister subunits (Bae & Gargiulo, 2004; Xia, 2011).

However, theoretical predictions are often subject to a particular set of boundary constraints. RDT has been criticized for its “ambiguities around its boundary conditions” (Hillman et al., 2009: 1406; see also, Casciaro & Piskorski, 2005). Thus, scholars call for more research considering the boundary conditions of RDT (Finklestein, 1997; Hillman et al., 2009; Pfeffer, 2003). Our study extends this stream of inquiry by revealing the strength of periphery and overlap predictions. To examine how predictions of the subunit power perspective vary across individual subunits, we introduce two moderators: the relative sales growth (year-to-year increase in a subunit’s sales relative to other firms in the same industry) and external linkage (the number of reinsurance deals made by a subunit with other firms outside the focal firm). Although market periphery and overlap put subunits at a disadvantage in power, some of these subunits may alleviate the disadvantage by increasing their market growth or maintaining operational stability. That is, their positive effects on subunit exit may diminish to the extent that a subunit’s power is enhanced by its relative sales growth and external linkage.

Hypotheses

To examine the subunit power perspective advanced in this study, we take advantage of a unique research setting—insurance groups in the U.S. property liability insurance industry—for two reasons. First, from the firm’s perspective, insurance subunits are diversified across multiple geographic locations and business lines (Li & Greenwood, 2004). Thus, the headquarters relies on these subunits to manage the portfolio of market dependence (Mayers & Smith, 1994). Second, from the subunit’s perspective, group affiliation is highly valued by subunits in the insurance industry because they can benefit from economies of scale, internal capital markets, knowledge and expertise, natural hedging opportunities, and enhanced market visibility and reputation (Fiegenbaum & Thomas, 1993; Powell, Sommer, & Eckles, 2008; Regan, 1997). Observations show that an insurance group may strategically reorganize its market position by eliminating one or more of its subunits through divestiture, spin-off, or bankruptcy, if necessary (Ligon & Thistle, 2007; Phillips, Cummins, & Allen, 1998). All these characteristics indicate that the insurance industry provides an ideal setting to investigate the power mechanism behind the exit decision made by the headquarters.

Market Periphery

Periphery emphasizes the criticality of a market position in which subunits are central or peripheral in managing a firm’s overall market portfolio. Firms are likely to divide their structures into specialized subunits to manage specific niche markets in response to the pressure of environmental heterogeneity (Kochman, 1975; Lawrence & Lorsch, 1967). Although external opportunities may also drive firms to diversify in various directions, multiunit firms strive to enhance their core competencies. As such, subunits are often organized around the central businesses of the firm. Some subunits are placed at the core of the firm’s niche markets that are critical to the firm’s survival, whereas others are at the edge. Central markets convey power to subunits (Pfeffer, 1981; Provan, Beyer, & Kruytbosch, 1980) in multiunit firms (Hickson et al., 1971; Sambharya & Banerji, 2006) because they control the market or critical resource that affects “the ability of the organization to continue functioning . . . in the absence of the market for the output” (Pfeffer & Salancik, 1978: 46).

The corporate divestiture literature suggests that refocusing and asset disposal are often necessary to enhance a firm’s overall market position (Brauer, 2006; Johnson, 1996). However, an exit decision is subject to the pool of available choices associated with potential outcomes provided by individual subunits (Birnbaum, 1985; Molm, 1997). When making an exit decision, the headquarters will evaluate and compare the criticality of each subunit to enhance the firm’s overall competitiveness. In application of Molm’s (1997) analysis of constraints on the use of power, the use of power by a firm can be restrained by the firm’s own dependence if the subunits can provide substantial rewards to the firm. A firm’s dependence on a subunit will increase with the criticality of the subunit’s position that is the core to the firm’s market portfolio. Such dependence, in turn, is likely to reduce the subunit’s hazard of exit.

Specifically, the headquarters is likely to put more weight on subunits that manage central markets given that these markets are more critical to the firm’s survival as a whole than are those that manage peripheral markets. For example, AXA Group, a French multinational insurance firm, restructured its business portfolio in the early 21st century. It shut down a number of its U.S. subunits as a way to concentrate activities on its core business in retail and small commercial insurances in Western Europe and Asia (Howard, 2003). More recently, ZIMRE sold its stake in its Malawi subunit (United General Insurance Company) to focus on its core business in reinsurance (Mwanawashe, 2014). Organizational decisions are largely a reflection of the constraint of dominant actors who have control over critical resources, such as revenue (Nienhüser, 2008; Pfeffer & Salancik, 1978). Thus, the exit decision made by the firm is constrained by its outcome or competitiveness. The exclusion of central subunits is more likely to substantially undermine the ability of the firm to function or even survive (Frooman, 1999; Nienhüser, 2008; Pfeffer & Salancik, 1978) than the exclusion of peripheral subunits. These arguments lead to the following hypothesis:

Hypothesis 1: A subunit’s market periphery increases the hazard rate of its exit.

Market Overlap

Subunit power can be enhanced when the firm has no alternative to a subunit’s operations in certain markets (Harpaz & Meshoulman, 1997). The lack of alternatives creates high dependency on the subunit and thus increases its power (Emerson, 1962; Jacobs, 1974). By contrast, a subunit’s power will be reduced when its market position can be replaced by other subunits. When two or more subunits within the same firm share or partially share their market portfolios, they are considered substitutable alternatives (Astley & Sachdeva, 1984; Bae & Gargiulo, 2004). Patterns of substitutable subunits within a firm are likely to influence patterns of intraorganizational competition (Castrogiovanni, 1991). That is, the common dependence of sister subunits on the same market can result in rivalry within the firm. Several studies have demonstrated that sister subunits or divisions within a multiunit firm may compete in the same market (Kalnins, 2004; N. Phelps & Fuller, 2000), which is also evident in insurance groups (Mayers & Smith, 1994; Phillips et al., 1998; Regan & Tzeng, 1999).

Specifically, an insurance group, or fleet, may own multiple subunits, which can be highly specialized with substantial overlap in their business composition or portfolios. Concurrently, these subunits may be co-located in the same geographic market, even though certain subunits are more business diversified than others because of factors such as managerial discretion, market opportunity, and/or resource availability (Mayers & Smith, 1994). Market overlap that increases the internal competition of subunits for the same internal and external resources may generate negative outcomes, thereby reducing the firm’s overall benefit. Kalnins (2004) found that a multiunit firm was reluctant to establish new subunits in the market managed by its incumbent subunits to avoid internal competition.

The existence of substitutable subunits may mitigate the power of each subunit because alternative sources of a resource reduce the power of the actor who controls the resource or market (Emerson, 1962; Pfeffer & Salancik, 1978). For example, when American International Group sold one of its subunits, 21st Century Insurance, to Farmers Insurance Group in 2009, 21st Century Insurance was featured with high business overlap with other subunits in American International Group. 2 The essential implication is that if a subunit does not strive to differentiate its markets from those of its sister subunits, its power may diminish the extent that the headquarters is able to depend on its sister subunits as alternatives to stabilize the flow of resources. Headquarters may divest or dissolve certain subunits to support others within the firm to enhance the firm’s profitability as a whole. Hence, a subunit is likely to face the threat of exit insofar as sister subunits operate in the same market. The firm may use a subunit to replace another if their markets are highly overlapped. Therefore, we expect,

Hypothesis 2: A subunit’s market overlap increases the hazard rate of its exit.

Relative Sales Growth as a Moderator

We argued that subunits with high scores of market periphery or overlap are more likely to face the threat of exit (per Hypotheses 1 and 2) due to their disadvantaged power position. According to the power-dependence analysis (Birnbaum, 1985; Blau, 1964; Emerson, 1962), one of the ways for actors in a power-disadvantaged position to gain power is to take actions to increase the dependence of others on the actors. Multiunit firms are likely to pay attention to the capability of each subunit and rely on those subunits that are better able to stabilize the outputs (sales) to the market (Pfeffer & Salancik, 1978) when making an exit decision. Building on this insight, we further argue that when these subunits grow fast, the positive effect of market periphery and overlap on their hazard of exit can be substantially reduced.

For a less powerful (peripheral or substitutable) subunit, a higher level of relative sales growth can increase the dependence of the firm on the subunit for two reasons. First, according to Pfeffer and Salancik (1978: 2), “the key to organizational survival is the ability to acquire and maintain resources.” Relative sales growth reflects such ability of a subunit, as compared with those of other firms in the same industry, to attract new customers and increase purchases by existing customers, which is often used as the most important criterion to evaluate subunit capability (Delios, Xu, & Beamish, 2008; Kim, Lu, & Rhee, 2012; Robinson & Pearce, 1983). As a result, firms can be reluctant to divest, dissolve, or spin off those less powerful subunits that are also characterized by a high growth rate in the industry.

Second, the rapid growth of less powerful (peripheral or substitutable) subunits increases their relative importance in the firm’s market portfolio because they are capable of increasing and maintaining customers to stabilize the flow of resources on behalf of the firm. Accordingly, high levels of growth are likely to enhance the power position of less powerful subunits within the firm. The enhanced position, in turn, can serve as a constraint of headquarters’ exit decisions. By contrast, a subunit with a low growth rate coupled with its peripheral or substitutable market position will have an even greater hazard of exit because the disruptive effect on the firm’s growth can be minimized. Taken together, we expect,

Hypothesis 3: A subunit’s relative sales growth will reduce the positive effect of periphery on the hazard rate of its exit.

Hypothesis 4: A subunit’s relative sales growth will reduce the positive effect of overlap on the hazard rate of its exit.

External Linkage as a Moderator

Dependencies on external environment are the central source of uncertainty and constraint (Nienhüser, 2008; Pfeffer, 2003: 67). As a response, subunits may take actions to cope with the uncertainty to secure stability (Emerson, 1962). External linkages, or the ties that reach out to tap the capacities of other organizations, have been viewed as useful means to serve this purpose (Ahuja, 2000; Das & Teng, 2002; Pfeffer & Nowak, 1976; C. C. Phelps, 2010). For insurance firms and their subunits, although they compete for the same resources, they also cooperate to manage market risk via reinsurance contracts (Cole & McCullough, 2006; Mayers & Smith, 1990; Plantin, 2006). The contract allows one insurer, called the primary insurer (i.e., an insurance firm or an insurance subunit), to cede part or all of its originally written insurance business to another insurer, called the reinsurer (Cole, Lee, & McCullough, 2007). Such contracts that link to different firms not only help subunits better survive catastrophic shocks that may lead to a liquidity crunch 3 but also enhance their positions within the firm because these risk-transaction ties may offer business opportunities when reinsurance partners trade underwriting risks when their total risks exceed their targets.

We argue that a subunit’s external linkage may minimize the effect of periphery or overlap on its hazard of subunit exit because of its ability to maintain operational stability. External linkage enables subunits to mitigate risk through risk sharing (Das & Teng, 1998) and risk transfer (Mayers & Smith, 1982) to avoid disruptive events that may destabilize the subunit’s business operations (Bae & Gargiulo, 2004; Das & Teng, 2002). In the insurance industry, risk sharing, or pooling, involves grouping of different insurers’ loss exposures through reinsurance contracts to reduce business uncertainty. In contrast, risk transfer takes place through a reinsurance agreement where the primary insurer cedes part or all of its business exposures to the reinsurer. The failing propensity of a subunit can be a major concern in turbulent industries where the nature of the business is highly risky. In such industries, including that of insurance itself, the stability of subunits can be extremely important to the firm because unexpected catastrophic shocks may jeopardize its survival as a whole. Reinsurance contracts enable the subunit to have the advantage of sharing and transferring potential risk outside the multiunit firm when a catastrophic shock occurs. For example, reinsurers paid out two thirds of the insured losses (>$20 billion) of the terrorist attacks of September 11, 2001 (Insurance Information Institute, 2015). As such, although subunits with high scores of periphery or overlap have a greater hazard of exit (as we argue above), if they are able to share the operational risk with other firms to maintain stability, the concerns of the headquarters on the subunit’s odds of failure in a tough market will be alleviated. Taken together, we hypothesize the following:

Hypothesis 5: A subunit’s external linkage will reduce the positive effect of periphery on the hazard rate of its subunit exit.

Hypothesis 6: A subunit’s external linkage will reduce the positive effect of overlap on the hazard rate of its subunit exit.

Method

Sample

As noted, we used a population of U.S. property liability insurance groups and their established subunits to test our hypotheses. The database employed in the study was the annual statement filed by insurance firms to the National Association of Insurance Commissioners (NAIC). The NAIC, which started in 1871, is an association of chief insurance regulators from 50 U.S. states, the District of Columbia, and five U.S. territories (i.e., American Samoa, Guam, Northern Marlana Islands, Puerto Rico, and the Virgin Islands). This database provides several important advantages to the present study. First, all insurance firms writing policies in the United States are required to register with the NAIC and follow the local regulations in which they operate. Second, subunits in the insurance market can be identified annually; as such, the formation, history, and exit of all subunits can be traced over time across all niche markets. Third, extensive and detailed information is available at the subunit level. These advantages permit a multiplicity approach to analyze geographic-business markets and test certain nuances of the perspective on uneven power distribution that would otherwise be impossible.

Our sample included all subunits formed by U.S. property liability groups between 1990 and 2011. We tracked the annual status of each subunit from its founding year to either the year of its exit or the year 2012, whichever occurred first. This approach is in line with the sampling procedure described by Park and Ungson (1997). Insurance groups with only one subunit during the study period were omitted because these firms are similar to independent firms. Observations were also deleted if the closure of a subunit was caused by the dissolution of the group itself. Our final sample consisted of 12,897 observations, covering 1,523 subunits owned by 420 distinct property liability insurance groups. Of the 1,523 subunits, 594 (39%) experienced exit in three forms (divestiture, dissolution, and spin-off) by the end of 2012. We report aggregate and separate test results.

Dependent Variable and Estimation Method

We analyzed subunit exit using the Cox proportional hazards model, a semiparametric event-history technique that allows for longitudinal data and time-varying covariates while imposing no specification on the functional form of the underlying distribution (Greene, 1997; Wooldridge, 2002). Previous studies have used this model to estimate the hazard rate of subunit divestiture (Shimizu, 2007). In the present paper, the dependent variable was measured as the hazard rate (or the instantaneous probability) of cutting off a subunit at time t, coded 1 when the subunit exit took place or 0 otherwise. The hazard rate is defined as

where Pr is the probability of an event (the subunit exit of subunit i in this study) between time t and (t + Δt), given that the subunit stays with the group before t. h0(t) is denoted as the baseline hazard function; X(t) is the vector of covariates at time t; and β is a vector of regression parameters; therefore, the Cox model takes the following form:

We estimated β by using STATA’s maximum likelihood procedure with the cluster option by group affiliations. Robust estimation was applied to correct for possible nonindependence across subunits belonging to the same group. The Cox regression model considers the right-censored cases, which, in the setting of the present paper, may occur when subunits remained group members at the end of 2012 (Wooldridge, 2002).

As a complementary analysis, we also employed a frailty model with a gamma random effect to evaluate the potential unobservable firm heterogeneity. Separate analyses were carried out for the complete sample and a subsample excluding the last 5 years, as the 2008 U.S. financial crisis and the subsequent global recession from 2008 to 2012—the worst since the Great Depression of the 1930s—could have forced firms to care more about survival (vs. growth). The results of the complementary analysis (see Tables 2 and 3, Model 8) indicate that heterogeneity is more of a concern for the complete observation period, suggesting that our theoretical framework may be better suited to explain exit decisions under nonextreme circumstances. For this reason, we interpret our results based on the analysis of the prerecession period.

All time-varying independent variables, moderating variables, and control variables defined here were lagged 1 year to address the concerns of reverse causation.

Independence Variables

Market periphery

An important characteristic of insurance groups is that the organizational environment can be partitioned in terms of the multiplicity of market dependence. Our periphery measure is analogous to the homogeneity (or conformity/change) index used in prior research (e.g., Deephouse, 1999; Kraatz & Zajac, 1996; Nakauchi & Wiersema, 2015). Consistent with the multiplex concept of geographic and business combination (Gimeno & Woo, 1996; Kalnins, 2004), we operationalized periphery along the two market-related dimensions: business lines (26 NAIC categories) and geographic regions (58 NAIC categories). The available NAIC data specify a subunit’s activities in 1,508 (26 × 58) possible business line–region segments or niche markets. Periphery was measured for each year as follows: First, we computed a subunit’s dependence on a specific niche market by dividing sales derived from that niche market by the total sales of the subunit. Second, we calculated the absolute deviation of the subunit’s market portfolio from that of the firm. The scores were then aggregated as follows:

where DPWils is subunit i’s sales from line l in region s; DPWi is the total sales of subunit I; DPWgls is firm g’s sales from line l in region s; and DPWg is the total sales of firm g. A total of 58 regions (s = 1, 2, . . . 58) and 26 insurance lines (l = 1, 2, . . . 26) are used to compute the ratio. A higher value of the variable implies a higher subunit deviation from the firm’s mainstream or central sales domain. An example of the calculation is presented in the appendix.

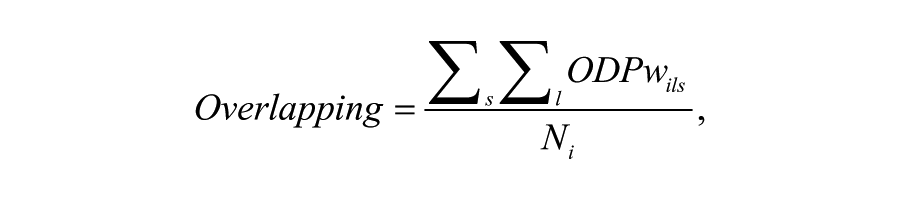

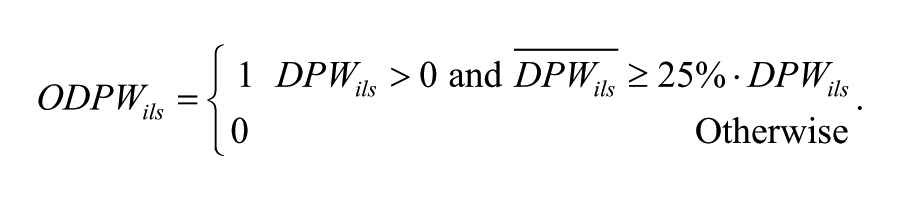

Market overlap

Overlapping refers to the degree to which a subunit has a significant niche market overlap with other subunits in the same insurance group. A significant market overlap was defined as one when group peers’ sales are at least 25% of the focal subunit’s sales in a niche market.

4

where

An example of the calculation is also presented in the appendix.

Moderating Variables

Relative sales growth

We used a percentile ranking to measure a subunit’s relative sales growth compared with all other firms in the market (Ivković & Weisbenner, 2009; Pearce, 1983). For example, a 75th-percentile ranking means that the subunit’s growth in sales is at a rate equal to or faster than 75% of other firms in the property liability insurance industry.

External linkage

This variable was measured as the natural logarithm of the number of unique external reinsurance partners that a subunit had in a particular year. Similar to exchange ties in manufacturing industries, reinsurance alliances allow insurance firms to share risks, stabilize revenue, and explore new opportunities (Cole et al., 2007; Plantin, 2006).

Control Variables

We included several control variables in all analyses at the subunit, firm, and industry levels. At the subunit level, we included the logarithm of total assets to account for subunit size because larger subunits may be more influential to their parents’ decisions. We controlled for subunit financial strength by using a 9-point Likert-type scale based on the A.M. Best rating, ranging from very strong (1) to very weak (9). Previous work shows that the level of leverage affects solvency (Opler & Titman, 1994; Phillips et al., 1998; Safieddine & Titman, 1999). We thus controlled for subunit leverage, which is defined as the ratio of a subunit’s total liabilities over its total assets in a given year. We also controlled for subunit performance because more profitable subunits tend to be more valued by the firm. We computed for the subunit performance as return on assets, defined as the ratio of net income to total assets.

We included three time-varying controls for firm characteristics to account for firm conditions: group leverage, group performance, and group market share. Group leverage was measured as the ratio of a group’s total liabilities over total assets. Group performance was approximated by a group’s return on assets. Group market share was measured as a ratio of a group’s direct premium written to the total industry premium written in a given year.

Finally, we included two industry controls: market munificence and market dynamism. In line with prior studies (Dess & Beard, 1984; Walters, Kroll, & Wright, 2010), we measured market munificence as the regression coefficient from a time-trend regression divided by the mean value of market sales for the preceding 5 years. Munificence in general provides more opportunities for all subunits to acquire market resources. Market dynamism was calculated as the standard error of the regression coefficient divided by the mean value of market sales. Separate munificence (dynamism) indexes were calculated for different niche markets and then averaged for each subunit based on the sales of its business portfolio in a given year.

Results

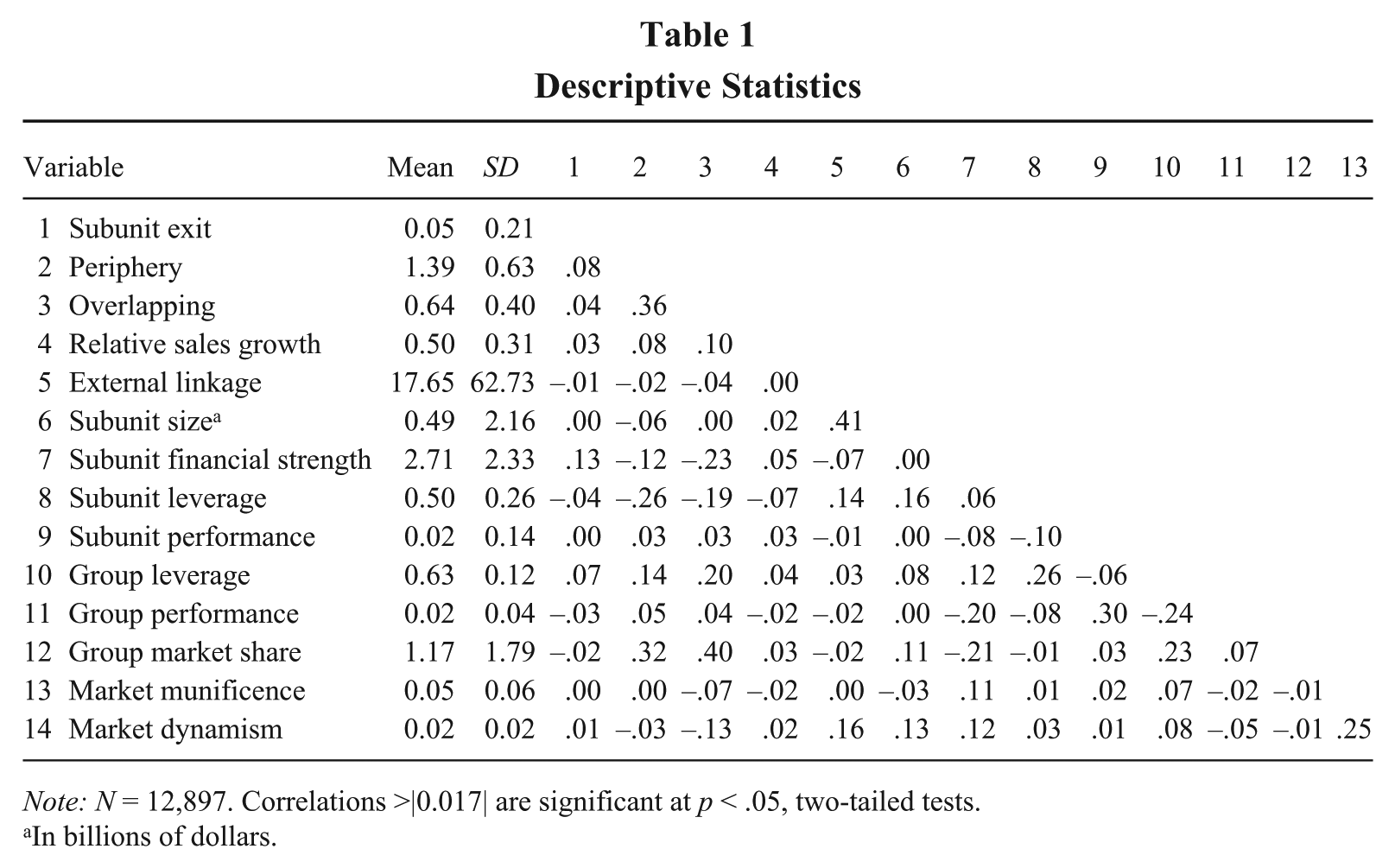

Table 1 provides means, standard deviations, and a correlation matrix for all the study variables. To test Hypotheses 3–6, we mean centered all relevant independent variables before creating the interaction terms to reduce multicollinearity, as suggested by Aiken and West (1991). We checked the variance inflation factors, and the highest was 2.34, which is significantly lower than the rule-of-thumb cutoff of 10. Thus, multicollinearity was not a problem for our regression analyses. For ease of interpretation, all variables reported in Table 1 are not mean centered.

Descriptive Statistics

Note: N = 12,897. Correlations >|0.017| are significant at p < .05, two-tailed tests.

In billions of dollars.

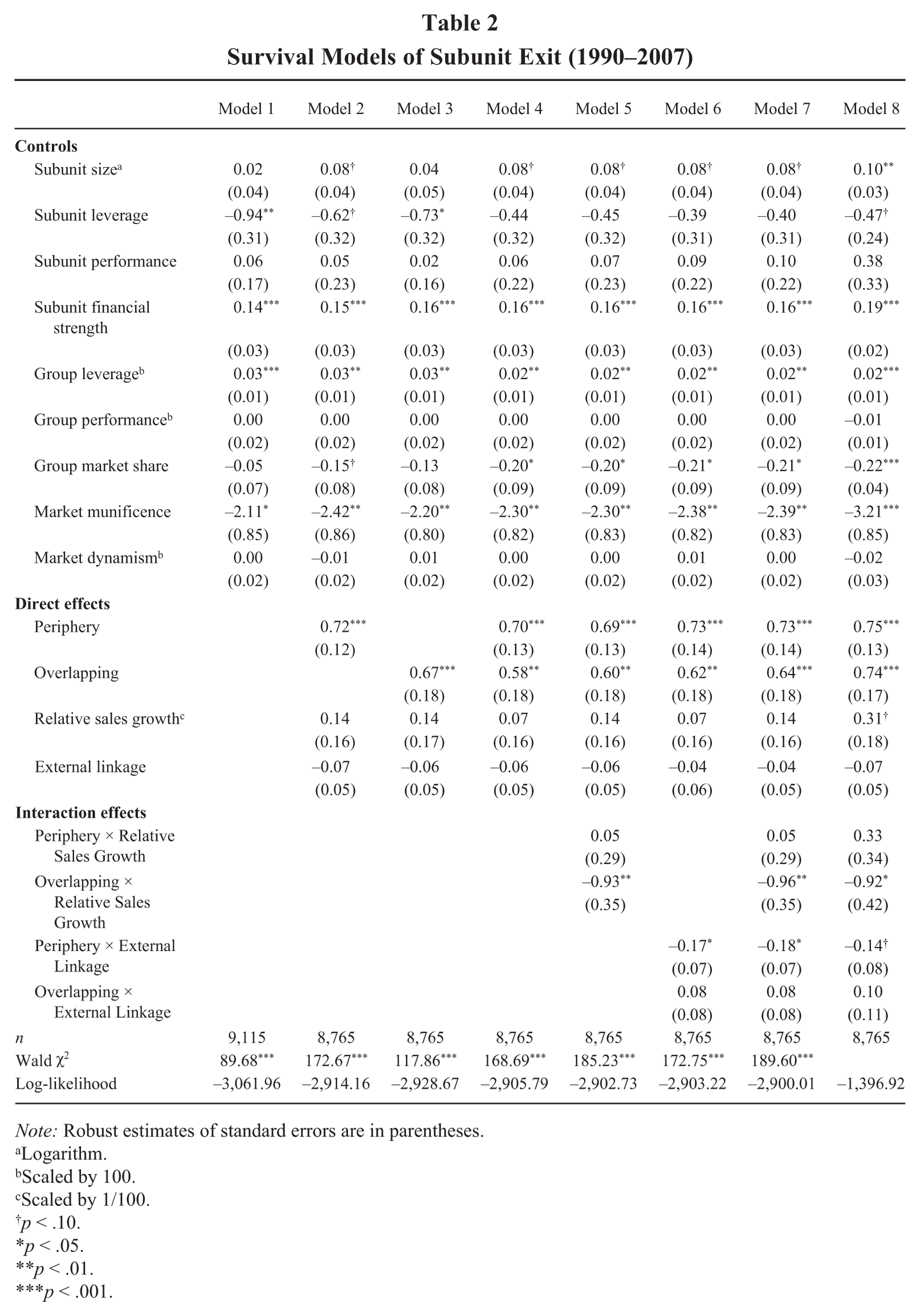

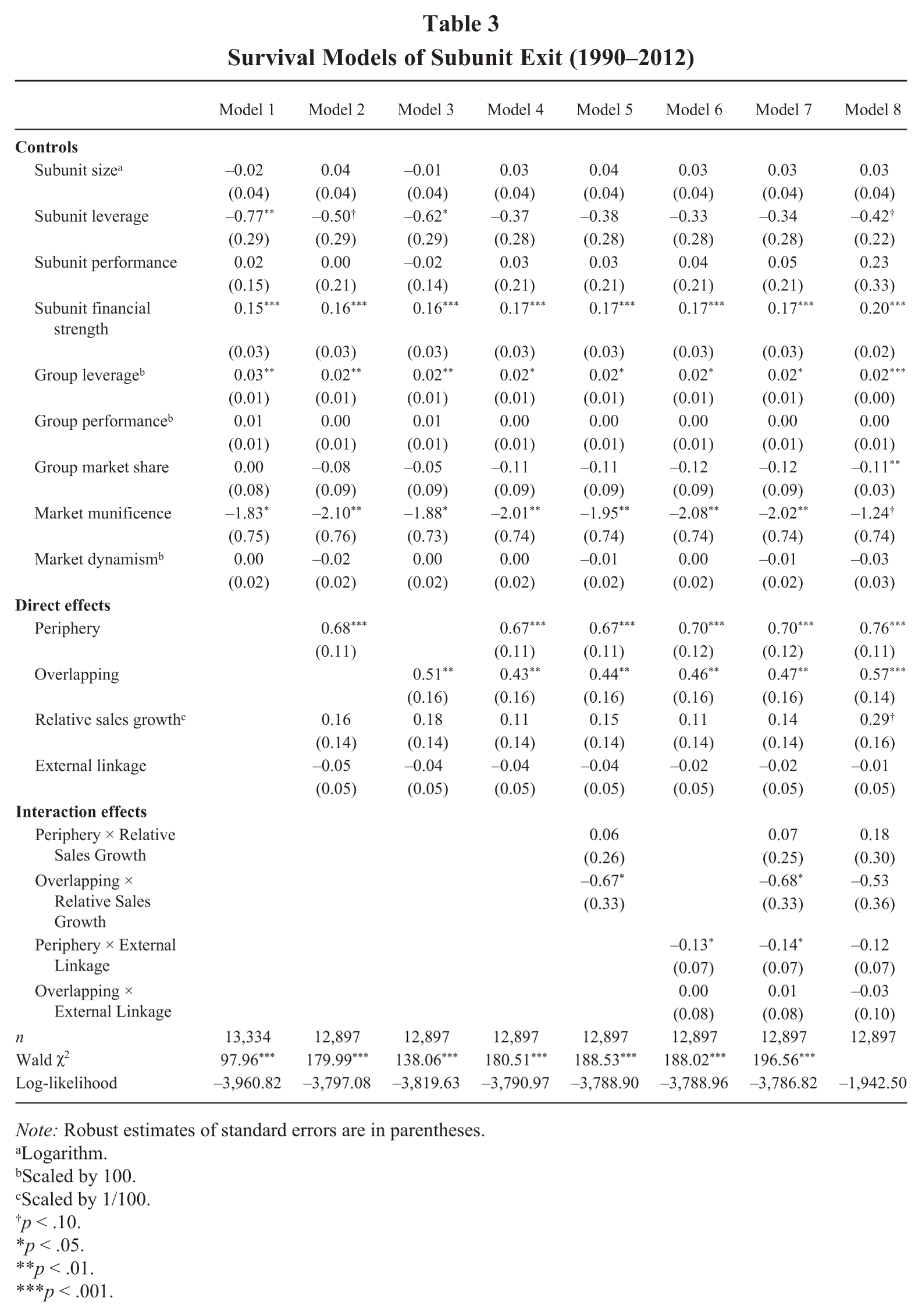

Table 2 reports the results of the robust Cox proportional hazard model for the prerecession period (1990–2007). Table 3 reports the results for the complete observation period. The results are qualitatively the same. As noted, we interpret our results based on Table 2, which removes the influence of the 2008 financial crisis. Model 1 presents the coefficient estimates only for the control variables. Models 2–4 add the main effects for periphery and overlap as well as the two moderating variables. Models 5 and 6 enter the interaction terms. Model 7 includes all variables and interactions simultaneously. Chi-square statistics show that Model 7 corresponds to the best model fit, as compared with the control model. We thus interpret our results based on the full model. Several results of the control variables are noteworthy. First, subunits with weaker financial strength and lower financial leverage face a higher threat of exit. Second, if the firm is in a poor debt position, the hazard of subunit exit increases. Third, higher market munificence reduces the hazard of subunit exit, as expected. Interestingly, subunit performance does not have a significant impact on exit. Although earlier research paid substantial attention to the economic performance of individual subunits as a key determinant of subunit exit (Delios & Ensign, 2000; Shimizu, 2007), this approach alone may be insufficient because a subunit exit can occur for reasons unrelated to the ability of a subunit to meet its performance objectives (Barkema, Bell, & Pennings, 1996; Delios & Beamish, 2001).

Survival Models of Subunit Exit (1990–2007)

Note: Robust estimates of standard errors are in parentheses.

Logarithm.

Scaled by 100.

Scaled by 1/100.

p < .10.

p < .05.

p < .01.

p < .001.

Survival Models of Subunit Exit (1990–2012)

Note: Robust estimates of standard errors are in parentheses.

Logarithm.

Scaled by 100.

Scaled by 1/100.

p < .10.

p < .05.

p < .01.

p < .001.

Hypotheses 1 and 2 predict that the periphery and overlap of a subunit’s niche markets increase the hazard of its exit, respectively. Model 7 in Table 2 shows that both periphery (β = 0.7310, p < .001) and overlap (β = 0.6449, p < .001) have positive effects on subunit exit, indicating that a one–standard deviation increase in periphery (overlap) over the mean raises the rate of subunit exit by 59% = (e0.7310×(1.4025+0.6354) – e0.7310×1.4025) / e0.7310×1.4025 × 100 (30% = [e0.6449×(0.6378+0.4022) – e0.6449×0.6378] / e0.6449×0.6378 × 100). Thus, the two hypotheses are supported.

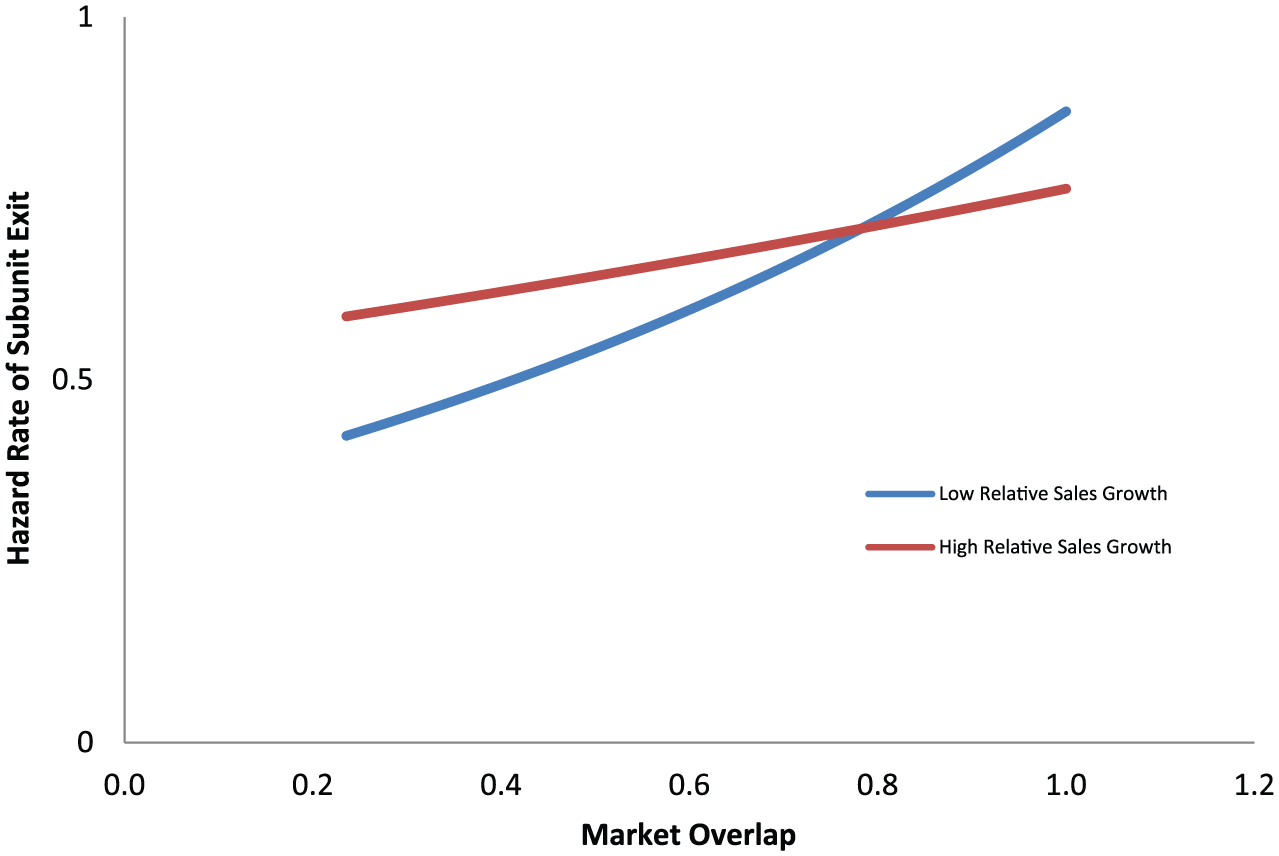

Hypotheses 3 and 4 predict that a subunit’s relative sales growth will reduce the positive effect of periphery and overlap on subunit exit, respectively. The coefficient in Model 7 of Table 2 for the interaction between periphery and relative sales growth is insignificant. It is possible that peripheral subunits focus on areas tangential to the firm; thus, its growth is not much valued by the headquarters. Hypothesis 3 is not supported. However, the coefficient for the interaction between overlap and relative sales growth is negative and significant (β = −0.9584, p < .01). The economic significance of the interaction can be interpreted by comparing the effect of overlap at different levels of relative sales growth (Tzabbar, 2009). When the relative sales growth is low (one standard deviation below the mean), a one–standard deviation increase in overlap over the mean raises the rate of subunit exit by 131%. When the relative sales growth is high (one standard deviation above the mean), a one–standard deviation increase in market overlap over the mean raises the rate of subunit exit by 36%. To facilitate our interpretations, we plotted this integration based on Model 7. We define “high” and “low” as one standard deviation above and below the mean, respectively. As depicted in Figure 1, although the hazard rate of the subunit exit rises as overlap increases for both lines, the positive relationship between overlap and subunit exit was attenuated considerably at high relative sales growth. This finding suggests that the effect of overlap diminishes to the extent that a subunit’s relative sales growth is high, thereby supporting Hypothesis 4.

Interaction Between Overlap and Relative Sales Growth

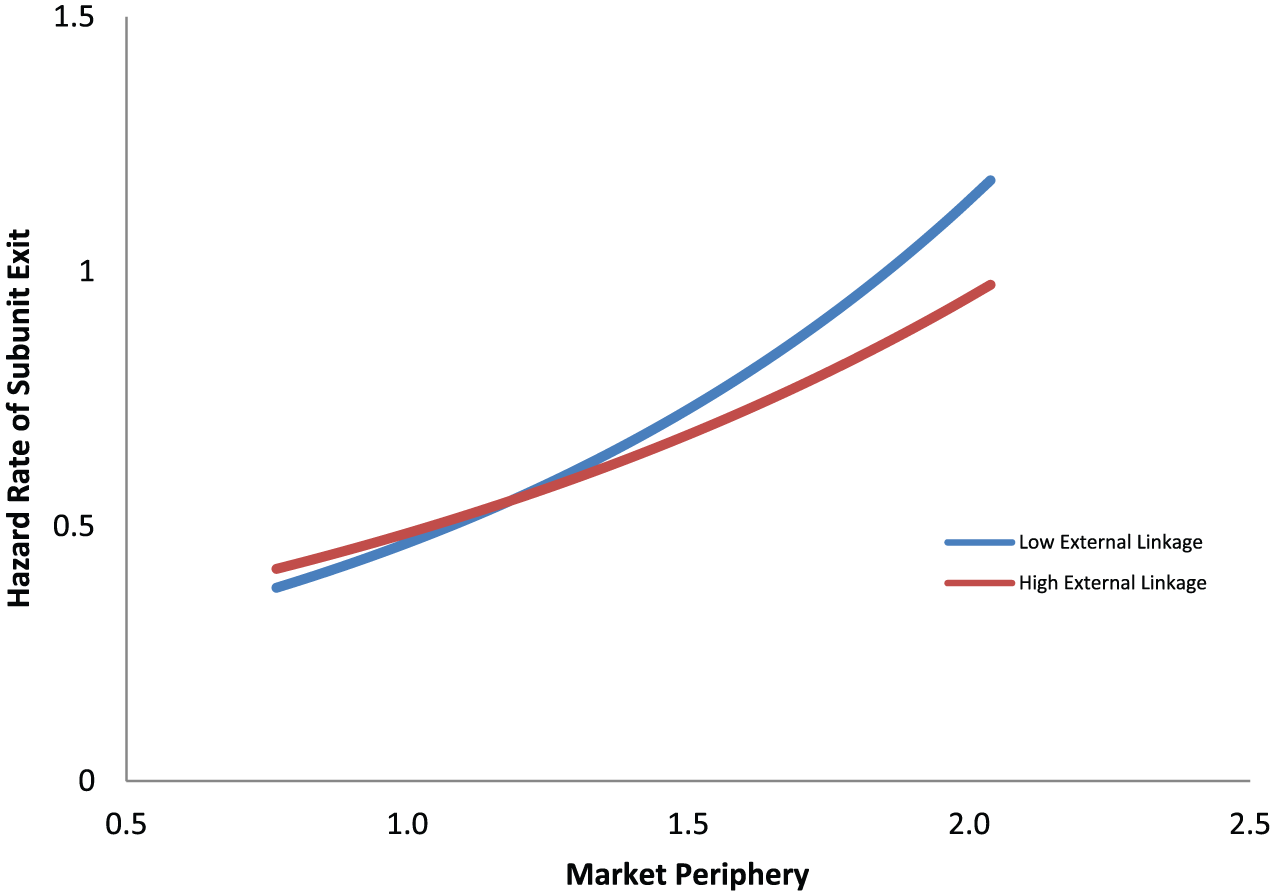

Hypotheses 5 and 6 suggest that a subunit’s external linkage will help reduce the positive effect of periphery and overlap on the hazard of its subunit exit, respectively. Model 7 shows that the coefficient for the interaction between overlap and external linkage is insignificant. Hypothesis 6 is not supported. However, the coefficient for the interaction between periphery and external linkage is negative and significant (β = −0.1763, p < .05). A comparison of the effect of periphery at different levels of external linkage shows that the effect of periphery diminishes to the extent that a subunit has more external linkages. When external linkage is low (one standard deviation below the mean), a one–standard deviation increase in periphery over the mean raises the rate of the subunit exit by 138%. When external linkage is high (one standard deviation above the mean), a one–standard deviation increase in periphery over the mean raises the rate of subunit exit by 58%. Consistently, Figure 2 shows the interaction. Therefore, Hypothesis 5 is supported.

Interaction Between Periphery and External Linkage

We performed several additional analyses to check the robustness of our results. First, we included the number of subunits and subunit shares in firm sales (defined as the proportional firm sales made by a subunit) as additional controls to test whether our results are sensitive to the number and in-group importance of subunits in the firm. Their inclusion did not change the signs and significance of the results. Second, we winsorized group market share symmetrically at the 2.5% level in each tail to remove the potential influence of big outlier groups. The exclusion of extreme values did not change the patterns of our results.

Supplementary Tests

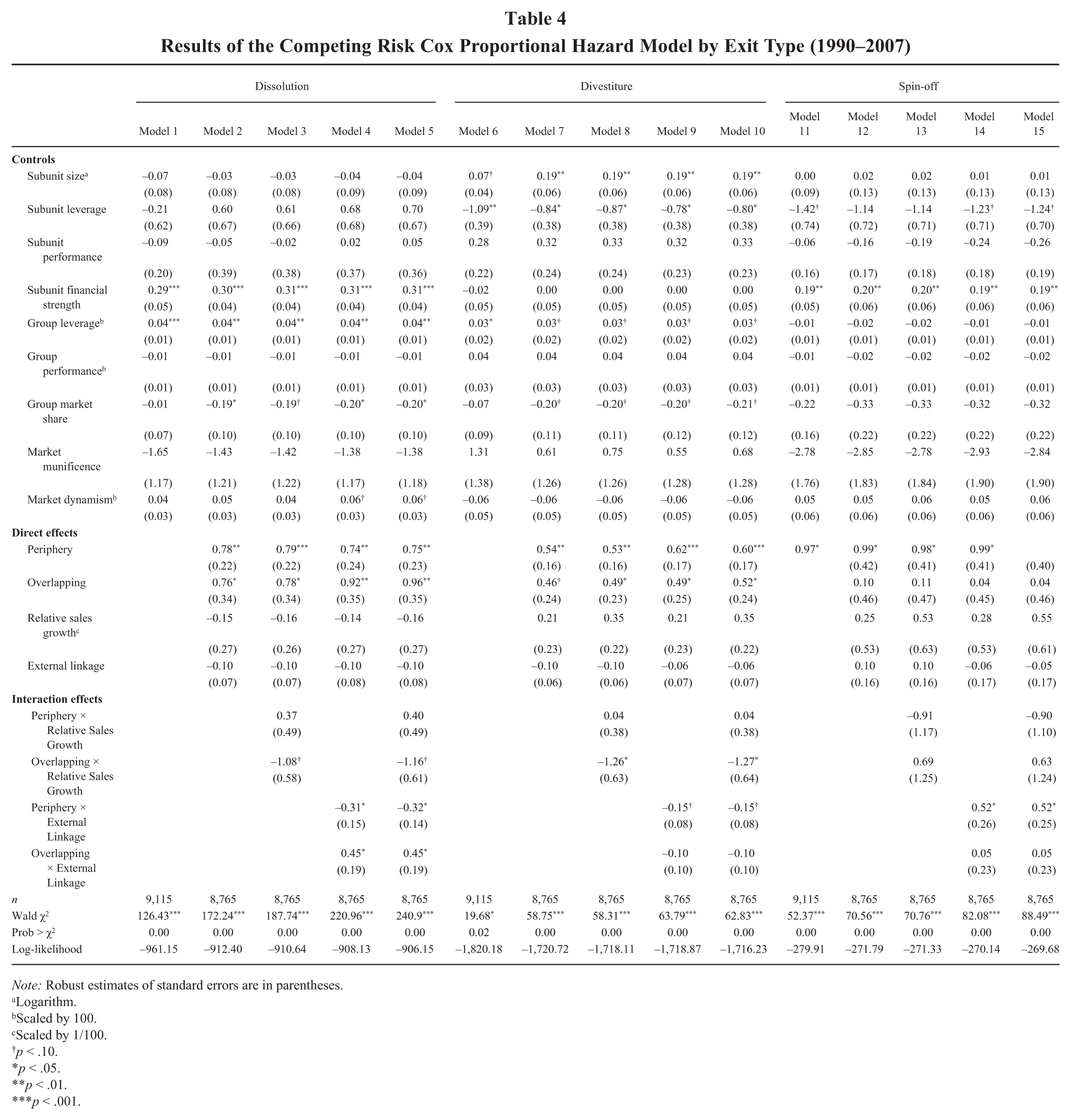

The subunit exit in our sample takes three forms: (1) divestiture, in which the subunit is acquired by another firm (344 cases, 268 cases before 2008); (2) dissolution, in which the subunit is dissolved and no longer in existence (197 cases, 152 cases before 2008); and (3) spin-off, in which the subunit becomes an independent unaffiliated insurer (53 cases, 43 cases before 2008). Additional analyses for the three types of subunit exit were operated as supplementary tests. The results are presented in Table 4. 5

Results of the Competing Risk Cox Proportional Hazard Model by Exit Type (1990–2007)

Note: Robust estimates of standard errors are in parentheses.

Logarithm.

Scaled by 100.

Scaled by 1/100.

p < .10.

p < .05.

p < .01.

p < .001.

In Table 4, Models 1–5, 6–10, and 11–15 represent the estimated results for subunit dissolution, divestiture, and spin-off, respectively. For all three categories, the coefficient for market periphery was positive and significant (Model 5, β = 0.7506, p < .01; Model 10, β = 0.6032, p < .001; Model 15, β = 0.9909, p < .05), which offers additional support to Hypothesis 1. The coefficient for market overlap was positive and significant for dissolution (Model 5, β = 0.9552, p < .01) and divestiture (Model 10, β = 0.5204, p < .05) but not for spin-off. This indicates that firms are hesitant to spin off an overlap subunit, possibly to avoid creating a competitor to their other subunits.

With respect to the moderating effects, the results in Table 4 are mostly consistent for the first two types of exit. The results support Hypothesis 4 for dissolution (Model 5) and divestiture (Model 10), showing that relative sales growth reduces the positive effects of overlap on subunit dissolution and divestiture. The results also confirm Hypothesis 5 for dissolution (Model 5) and divestiture (Model 10), suggesting that external linkage reduces the positive effect of periphery on the hazards of subunit dissolution and divestiture. Although the results indicate certain variations because of the separate tests for the two dependent variables, they are qualitatively consistent with the results reported in Table 2. However, in contrast to Hypothesis 6, the coefficient for the interaction of overlap and external linkage in Table 4 is positive and significant for dissolution (Model 5), which indicates that that external linkage increases the positive effect of overlap on subunit dissolution. One possible reason is that the headquarters may benefit from exit decisions by sharing external linkage among subunits facing internal competition. The coefficient for the interaction of overlap and external linkage is insignificant for divestiture (Model 10). It is likely that firms may attempt to avoid creating direct competition against the retained subunits.

For spin-off, only the interaction of periphery and external linkage is significant (Model 15), yet the coefficient is in the opposite direction of what was predicted. It is possible that the external linkages of subunits may not be equally valued by headquarters. For insurance firms, reinsurance connections—notwithstanding their assorted benefits—may also lead to unsolicited risk exposure due to risk transfer and contagion (Lin, Yu, & Peterson, 2015). In our study, the headquarters may be more concerned with the downside of these linkages made by peripheral subunits and thus allow them to be independent. Yet, one must be cautious of the results given the limited number of spin-offs in our sample.

Conclusion and Future Research

We have advanced a subunit power perspective by introducing market periphery and overlap as two theoretical constructs to explain subunit exit, along with its boundary conditions, and gained considerable empirical support. Pfeffer (2003: xvi) lamented that RDT had become little more than a “metaphorical statement about organizations” because the abundance of ceremonial citations is coupled with a relatively modest number of tests (Wry et al., 2013). One important reason is the lack of appropriate firm-level data to capture the key concepts of power and dependence (Davis & Cobb, 2010; Finklestein, 1997). More recently, organization scholars have made substantial efforts to develop new constructs to capture the different aspects of power and dependence (e.g., Casciaro & Piskorski, 2005; Gulati & Sytch, 2007), which represent a “renaissance” of RDT (Katila, Rosenberger, & Eisenhardt, 2008: 321; see also Hillman et al., 2009). The new conceptualization and constructs (market periphery and overlap) introduced in our study contribute to this trend of theoretical development in RDT by expanding its empirical domains and applications, which have implications for future research.

It is well recognized that subunit power can be derived from resource exchange within a firm (Hickson et al., 1971). This interdependence-based approach is based on the premise of the existence of resource exchanges among sister subunits. However, this approach of subunit power does not apply to multiunit firms in which sister subunits are relatively independent without much direct economic exchanges. Our study is among the first to establish how the distribution of subunit power is determined by market dependence rather than by resource exchanges among sister subunits, providing a theoretical foundation for future research on subunit power. The distinction between our market dependence–based approach and the existing interdependence-based approach is important because these approaches are not fully exchangeable in explaining organizational outcomes such as subunit exit. Therefore, our study advances the knowledge for a more complete understanding of subunit power in different situations, which allows future research for more integrated approaches.

This study extends RDT on subunit power by working toward a better understanding of the multiplicity of market dependence. Environmental (or market) dependence—which is defined by the importance of a resource and its availability to the firm from the environment (or market)—has been a central concept in RDT (Dess & Beard, 1984). Market dependence can be identified at the firm and subunit levels. However, most studies on resource exchange (i.e., inputs and outputs) have focused on the “total environment” of the firm (Lawrence & Lorsch, 1969), as widely demonstrated in the RDT literature (Casciaro & Piskorski, 2005; Finklestein, 1997; Pfeffer, 1972). Unfortunately, this approach sheds little insight into subunit power, given that subunits gain power primarily from more microscopic subenvironments rather than the total environment of the firm as a whole (Castrogiovanni, 1991).

Our study suggests that capturing subunit power is a critical component of managing the subunit portfolio effectively. Multiunit firms often empower subunits to manage certain niche markets. Given that the importance of a firm’s niche markets varies across geographic locations and business lines, subunits that manage these niche markets may end up with an unevenly distributed power within the firm. Subunits that are better able to manage critical organizational contingencies gain more power within the firm (Nienhüser, 2008; Pfeffer & Salancik, 1978). However, the RDT literature has made limited progress in developing constructs of subunit power determined by the multiplicity of market dependencies, which has hindered our knowledge on the nature of relative subunit power.

Our theorization and examination of periphery and overlap as two indicators of unevenly distributed subunit power is an important step to address this issue. The two constructs capture the core concepts in RDT: credibility and substitutability, respectively. RDT has been widely used to explain alliances, mergers/acquisitions, board composition, interlocks, and executive succession (Hillman et al., 2009). However, it has been rarely used to explain subunit exit, with a few exceptions (e.g., Xia & Li, 2013). Our study extends this inquiry by developing new theoretical constructs and thus provides fresh insights. Considering that a multiunit firm frequently depends on multiple subunits for managing a set of given niche markets, the establishment and presence of competing subunits within a firm become a “puzzle” (Kalnins, 2004). Kalnins found that multimarket firms were reluctant to establish a subunit in their existing markets that had been managed by other subunits of the firm. This finding is echoed by our results on the main effect of market overlap, suggesting that a high degree of overlap among subunits within a multiunit firm increases the exit hazard of a substitutable subunit, indicating the headquarters’ effort to reduce internal competition.

We also explore the boundary conditions of the subunit power perspective, including relative sales growth and external linkage, under which the positive effects of periphery and overlap on subunit exit diminish. This approach directly responds to the repeated calls to extend RDT by identifying the boundary conditions of multiple resource dependencies (Casciaro & Piskorski, 2005; Finklestein, 1997; Pfeffer, 2003). Our results provide a mixed pattern to understand the boundary conditions. Specifically, a subunit’s relative sales growth reduces the positive effect of overlap on subunit exit, whereas external linkage reduces the positive effect of periphery on subunit exit. The findings are consistent with the strategic and dynamic view of relationship termination (Capron, Mitchell, & Swaminathan, 2001; Xia, 2011), which is in contrast with the view of corporate divestiture or alliance termination as failure (Moschieri & Mair, 2008; Park & Russo, 1996; Park & Ungson, 1997). In our view, subunit exit is a dynamic process in response to market dependences. The dynamic view is consistent with the offset argument that firms adapt through substitution (Castrogiovanni, 1991).

In our study, multiunit firms may retain fast-growing subunits even though these subunits compete with their sister subunits in the same niche markets. By contrast, a substitutable subunit is more likely to exit if it is unable to maintain certain levels of relative sales growth. Moreover, although exit decisions tend to refocus on core businesses, headquarters may retain a peripheral subunit with external linkage that can help reduce the risk of its operations. Thus, although the subunit power perspective advanced in our study is to explore the headquarters-subunit power relationship within multiunit firms, it integrates insight from the traditional RDT approach that has largely focused on interorganizational power relations (Hillman et al., 2009). For example, research shows that external contracts are an important source of subunit power within the organization (Pfeffer & Moore, 1980; Salancik & Pfeffer, 1974). The implication of our finding is that certain less powerful (e.g., peripheral) subunits may enhance their power within the firm through the establishment of external linkage.

The empirical evidence also has practical implications. Our study provides a useful lens to help top executives better understand how multiunit firms are structured and organized to manage the multiplicity of market dependence—for example, why a subunit is established and under what conditions it exits. The active management of the subunit portfolio by the firm may result in competitive positioning. For subunit managers, the ability to manage niche markets and create value is important for a subunit to reduce its hazard of exit. As Emerson (1962: 32) indicated, “power to control or influence the other resides in control over the things he values.” As subunits compete for the parent’s attention and support (Bouquet & Birkinshaw, 2008), only those that are more able to create value for the firm are more likely to attract the attention and support of the firm and ultimately survive and grow. However, this does not mean that the membership of a vulnerable subunit is guaranteed to be terminated without considering other contingent factors that may enhance its position. If a peripheral subunit is capable of lowering its operational risk, its hazard of exit can be reduced. Moreover, a subunit that faces internal competition can reduce the hazard by increasing its sales.

Limitations of this study should be noted, which may reveal certain areas in which research on subunit exit would be valuable. First, since we tested our arguments based on a service industry—the U.S. insurance industry—it raises the issue of whether our findings are generalizable. However, insurance groups resemble, in many ways, those multiunit firms in other industries that operate in multiple geographic-business markets. Future research may extend our research framework to other industries. It is also important to note that studies focusing on firms that involve exchanges among subunits should interpret our results with caution. In addition, our results suggest that the multiplicity of market dependence is relevant to understand power distribution among insurance subunits. Nonetheless, the focus of the present study on the end market does not mean that other dependence environments are not important. Instead, our choice is based on the fact that it is, arguably, the most important one for insurance firms. Future research might extend the arguments that we present here to examine how other specific environments (e.g., technological environments for high-tech firms and legal environments for law firms) might affect power relations within firms.

Second, we have examined the generalizability of our theory across the three forms of subunit exit by divestiture to another firm, dissolution by liquidation, and spin-off. The three types of exit are often regarded as qualitatively different outcomes of exit. Dissolution involves the breakup of a subunit by bankruptcy, liquidation, or closure. However, the resources and activities of a dissolved subunit can be recombined into other subunits. By contrast, divestiture represents a change in the ownership of the subunit (Barkema et al., 1996; Delios & Ensign, 2000; Mitchell, 1994), and spin-off leads to the creation of an independent company (Bergh & Sharp, 2015; Woo, Willard, & Baellenbach, 1992). Despite the apparent differences, the results suggest that our theoretical explanations apply to divestiture and dissolution, the predominant forms of exit in our sample. Although our study provides a parsimonious RDT explanation of subunit exit, future research may develop more nuanced theoretical perspectives to explain the different types of exit. In particular, future research may address the question of how subunit power affects the choice of different types of exit.

Third, unlike most previous studies that have focused on the total environment of the firm, our research explores the complex market structures managed by different subunits within the firm. We focused on periphery and overlap as indicators of subunit power. However, the complex nature of a firm’s market structure may determine subunit power in different ways. Future research may examine other aspects of subunit power and their various effects. For example, future research may seek to expand the criticality dimension to understand whether the distribution of subunit power affects subunit performance, executive change and migration, or market expansion at the subunit level. In addition, we investigated only relative sales growth and external linage as moderators of the subunit power effects. An interesting issue for future research is to explore other internal and external boundary conditions of subunit power.

In conclusion, as multiunit firms constantly adapt to environmental change, our study suggests that subunit exit is likely to reflect the relative importance of multiple and complex market structures upon which the firm and its subunits depend for resources, which determinates the distribution of subunit power. The power distribution constructs of periphery and overlap and their boundary conditions introduced in our study are salient for a more nuanced understanding of how firm response to environmental conditions is determined by the critical markets that are managed by different subunits. We invite others to continue this line of research and to explore other types of subunit power and dependence contingencies.

Footnotes

Appendix: Illustration of the Calculation of Market Periphery and Overlap

We consider an insurance group with two subunits, as shown here. The group operates in two insurance lines (L1 and L2) in two regions (R1 and R2). The direct premium written of the group in a given niche market is the sum of the direct premium written by its two subunits in the same niche market. For example, DPWg,1,1 = DPWs1,1,1 + DPWs2,1,1 = 0 + 50 = 50. For Subunit 1, its periphery score is 0.4381 = |0 – 0.1667| + |0.4286 – 0.4333| + |0.2857 – 0.0667| + |0.2857 – 0.3333|, and its overlap score is 0.6667 = (1 + 1)/3. For Subunit 2, its periphery score is 0.1333 = |0.2174 – 0.1667| + |0.4348 – 0.4333| + |0 – 0.0667| + |0.3478 – 0.3333|), and its overlap score is 0.6667 = (1 + 1)/3.

Acknowledgements

This article was accepted under the editorship of Patrick M. Wright.