Abstract

Given that many organizations are competitive and finance centered, organizational leaders may lead with a primary focus on bottom-line attainment, such that they are perceived by their subordinates as having a bottom-line mentality (BLM) that entails pursuing bottom-line outcomes above all else. Yet, the field is limited in understanding why such a leadership approach affects employees’ positive and negative contributions in the workplace. Drawing on social exchange theory, we theorize that supervisors high in BLM can influence employees’ felt obligation toward the bottom line, which in turn can influence employees’ task performance and unethical pro-organizational behavior (UPB). We also examine employee ambition as a moderator of this process. Using three-wave, multisource data collected from the financial services industry, our results revealed that high-BLM supervisors elevate employee task performance as well as UPB by motivating employees’ felt obligation toward the bottom line. Furthermore, we found that employee ambition served as a first-stage moderator, such that the mediated relationships were stronger when employee ambition was high as opposed to low. Our findings break away from the dominant dysfunctional view of BLM and provide a more balanced view of this mentality.

Keywords

In a business context, the term “bottom line” represents performance metrics that are tied to an organization’s profitability (Greenbaum, Mawritz, & Eissa, 2012; Wolfe, 1988). As such, it is not surprising that in highly competitive business environments, leaders regularly focus on bottom-line outcomes as a means of ensuring organizational success and survival and creating increases in shareholder value (Cushen, 2013; Krippner, 2011). Frontline supervisors, in particular, often emphasize bottom-line attainment as a way of motivating their employees’ productivity (Latham & Locke, 2007; Rodgers & Hunter, 1991; Yukl, 2013). For example, a supervisor may encourage employees to obtain high customer satisfaction ratings, to produce a certain quantity of widgets, to bill a certain number of hours, or to sell a dollar value in products because these performance metrics help the organization’s financial success. However, a supervisor’s focus on such metrics could develop into a bottom-line mentality (BLM), which reflects “one-dimensional thinking that revolves around securing bottom-line outcomes to the neglect of competing priorities” (Greenbaum et al., 2012: 344). For these supervisors, their BLMs encapsulate a way of operating with tunnel vision, such that they focus on the results that count “while everything else is disregarded” (Wolfe, 1988: 145).

Although attending to bottom-line outcomes is frequently viewed as beneficial for both organizational and employee productivity (e.g., Friedman, 2007), an emerging body of research suggests that supervisor BLM can be detrimental to organizational functioning (e.g., Bonner, Greenbaum, & Quade, 2017; Greenbaum et al., 2012; Mawritz, Greenbaum, Butts, & Graham, 2017). For example, extant research suggests that supervisor BLM contributes to employees’ social undermining of coworkers (Greenbaum et al., 2012), unethical proleader behaviors (Mesdaghinia, Rawat, & Nadavulakere, 2019), and supervisors’ abuse of deviant employees (Mawritz et al., 2017). However, the literature has not sufficiently considered when and why supervisor BLM affects employees’ work contributions and whether these contributions could include “bright-side” outcomes. Such research considerations are needed to advance the emerging BLM literature, as they would provide the management discipline with recommendations as to when and why supervisors’ high BLM may help or harm organizations and address the belief that bottom-line attainment is closely aligned with organizational success (e.g., Davidsson, Steffens, & Fitzsimmons, 2009; Friedman, 2007).

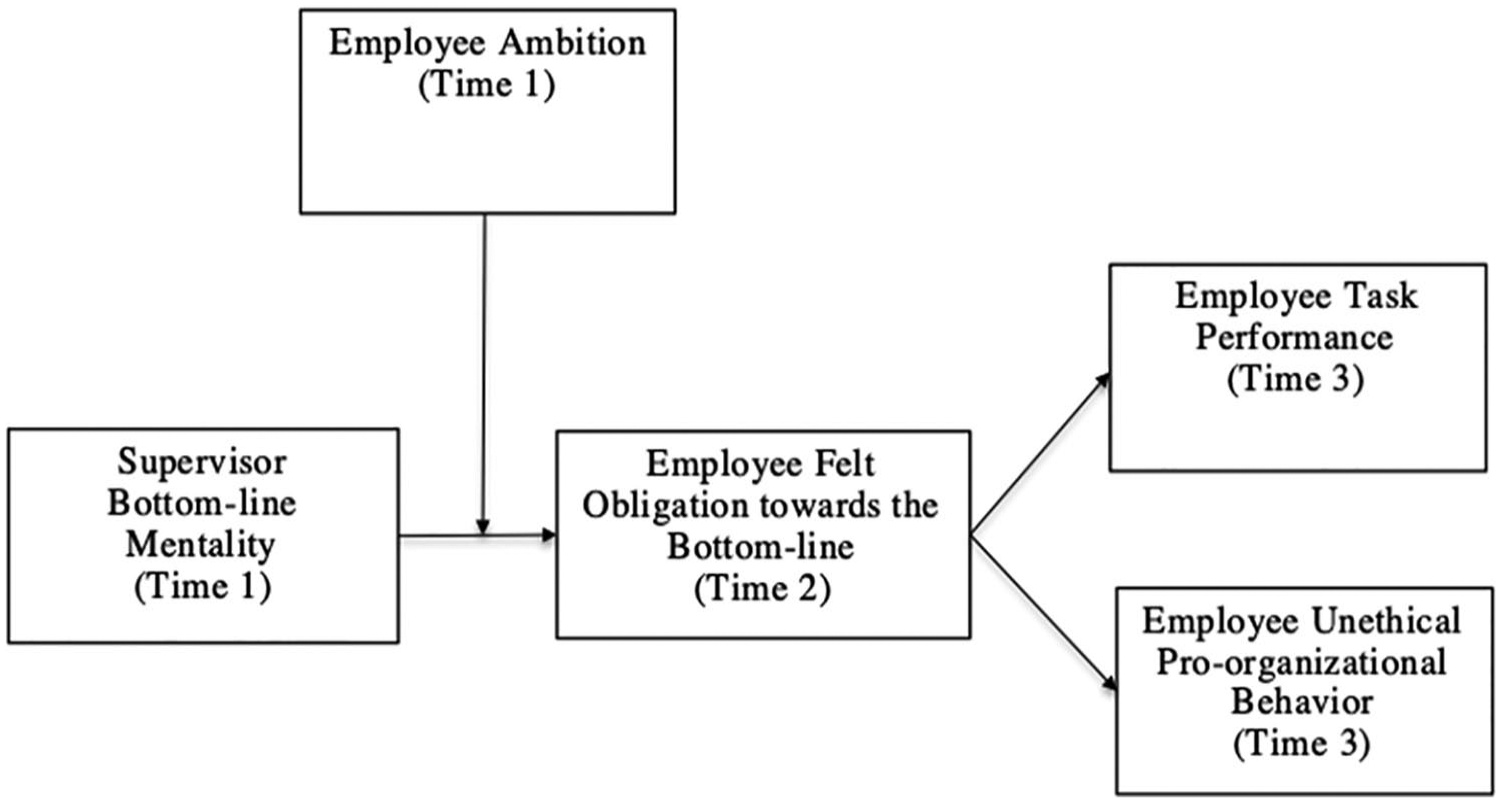

Accordingly, our goal in this study is to provide a more balanced, or functional, view of the supervisor BLM concept. To do so, we draw on social exchange theory (Emerson, 1976) to first explain the indirect relationships between supervisor BLM and employees’ contributions at work in the forms of (a) task performance and (b) unethical pro-organizational behavior (UPB; “actions that are intended to promote the effective functioning of the organization or its members . . . and violate core societal values, mores, laws, or standards of proper conduct”; Umphress & Bingham, 2011: 622). The theory suggests that social exchanges between supervisors and employees consist of bidirectional transactions in which supervisors provide exchange resources to employees (e.g., information, support, rewards), which are then reciprocated by the employees (Cropanzano & Mitchell, 2005). The theory also explains that the social exchange process encompasses specific feelings of obligation (Emerson, 1976), which in turn drive associated behavioral responses. Accordingly, we draw on social exchange theory to propose that supervisors high in BLM provide employees with valuable information regarding how to succeed in the workplace (e.g., Wolfe, 1988). In turn, these supervisors instill in their employees a sense of felt obligation (or responsibility) toward the bottom line (i.e., the belief that one should care about and be responsible for the organization’s bottom line), which represents the exchange process that subsequently motivates task performance and UPBs.

Furthermore, we propose that the indirect effects of supervisor BLM on task performance and UPB will be influenced by employee ambition (i.e., “persistent and generalized striving for success, attainment, and accomplishment”; Judge & Kammeyer-Mueller, 2012: 759). Social exchange theory suggests that individuals differ in the degree to which they endorse reciprocity norms, such that those oriented toward social exchanges carefully attend to exchange resources that are relevant to them (Cropanzano & Mitchell, 2005). Because individuals with high levels of ambition are generally seeking career advancement, success, and resource attainment (Judge & Kammeyer-Mueller, 2012), we theorize that compared to employees low on ambition, highly ambitious employees will be more likely to attend to the exchange resources provided by supervisors high in BLM and, therefore, more likely to feel a sense of obligation toward the bottom line, which subsequently increases their task performance and UPB (see Figure 1).

Research Model

Our study makes several contributions to the management literature. First, we challenge the prevailing view regarding the dark side of BLM. Specifically, our research contributes to the literature by examining supervisor BLM in relation to an outcome that directly helps the organization (namely, task performance). Second, we examine supervisor BLM through a new theoretical lens. Seminal work on BLM has relied on social cognitive theory to explain how supervisors high in BLM influence their employees’ behaviors (e.g., Greenbaum et al., 2012). However, research has shown that social cognitive perspectives may be insufficient for understanding the depths of relational considerations between supervisors and employees (Wo, Ambrose, & Schminke, 2015). Therefore, we add substance to BLM theorizing by offering social exchange theory as a new theoretical perspective for understanding why supervisor BLMs may increase employees’ task performance and unethical actions intended to benefit the organization (i.e., UPB). Third, we provide a more nuanced explanation for the effects of supervisor BLM and contribute to the literatures on both BLM and ambition by suggesting that ambition may be a double-edged sword—it may increase the likelihood that a supervisor’s BLM results in employees’ heightened task performance via felt obligation, but it may also encourage UPB. Finally, our study offers practical implications for organizations and their members in better understanding the complexity of BLMs in business environments. Perhaps, supervisor BLM should not be discouraged because it motivates employees to perform; however, such a leadership approach should be used with caution because of its potential influence on UPB.

Theoretical Background and Hypotheses

The three pillars of an organization’s performance are people, profit, and planet (Norman & MacDonald, 2004). However, consistent with the BLM literature (Greenbaum et al., 2012; Wolfe, 1988), BLM supervisors focus on the “profit” aspect of the triple bottom line and ignore other competing aspects (i.e., people and environmental considerations, both of which are related to ethics). Irrespective of a supervisor’s exact bottom-line metrics, supervisors high in BLM can be dysfunctional because they engender an exclusionary, sole focus on outcomes that help the bottom line to the possible detriment of competing priorities (e.g., upholding ethics; Bonner et al., 2017; Greenbaum et al., 2012; Mawritz et al., 2017; Wolfe, 1988). In this regard, extant research has shown that supervisor BLM contributes to dysfunctional organizational outcomes, such as abusive supervision, social undermining, and unethical proleader behaviors (Greenbaum et al., 2012; Mawritz et al., 2017; Mesdaghinia et al., 2019). Together, these studies draw attention to the potential dark side of supervisor BLM.

However, in business, securing bottom-line outcomes is highly important to the organization’s success (Davidsson et al., 2009; Friedman, 2007). In fact, economic considerations serve as the bedrock of organizational responsibilities (Friedman, 2007). Accordingly, organizations hire supervisors to fulfill the profitability motives of the organization (Grojean, Resick, Dickson, & Smith, 2004). Supervisors are specifically responsible for motivating employees to obtain performance outcomes that support the organization’s economic vitality (Bayo-Moriones & Larraza-Kintana, 2009; Cornelissen, Heywood, & Jirjahn, 2014). In this respect, a supervisor’s BLM may serve as a strategy for fulfilling the organization’s profitability motives. By intensely focusing on bottom-line outcomes, supervisors high in BLM are not distracted by considerations that are irrelevant to bottom-line attainment (e.g., Shah, Friedman, & Kruglanski, 2002; Shah & Kruglanski, 2002) and thus may be successful in reaching bottom-line objectives (e.g., Bélanger, Lafreniére, Vallerand, & Kruglanski, 2013). Additionally, supervisors high in BLM may be beneficial to the extent that they set clear standards with subordinates. Under these supervisors, subordinates receive clear signals and specific instructions that their efforts should support the organization’s bottom-line success.

Supervisor BLM, Employee Felt Obligation Toward the Bottom Line, and Employee Contributions

Social exchange theory suggests that employees have interpersonal exchanges with their immediate supervisors (Emerson, 1976) that are characterized by reciprocity (Gouldner, 1960). The theory suggests that supervisors and employees have interdependent interactions (Blau, 1964), in which supervisors provide employees with exchange resources (e.g., information, support, rewards) that are reciprocated. The exchange resources create in employees the feelings of obligation, referred to as felt obligation, which then motivates behaviors that are meant to reciprocate. Thus, reciprocity functions as a social exchange rule (Cropanzano & Mitchell, 2005; Gouldner, 1960), and felt obligation, which represents a psychological state reflecting obligations to be personally responsible for an event, situation, or work context (Cummings & Anton, 1990), acts as an important mediating mechanism in social exchanges between supervisors and their employees (Eisenberger, Armeli, Rexwinkel, Lynch, & Rhoades, 2001). Consistent with these tenets, past research has demonstrated that various relational characteristics of work can drive domain-specific felt obligation in employees, which then eventuates in associated attitudes and behaviors (Morrison & Phelps, 1999). For instance, Fuller, Marler, and Hester (2006) revealed that a leader’s focus on change was positively related to employees’ felt obligation for change and subsequent change-oriented contributions (e.g., voice, proactive behavior).

Accordingly, we draw on social exchange theory to suggest that supervisor BLM can drive a sense of obligation in employees to care about the organization’s bottom line, which then eventuates in behaviors that are perceived to aid in the organization’s bottom-line attainment (i.e., task performance and UPB). We suggest that supervisors high in BLM propagate employees’ felt obligation toward the bottom line and subsequent behaviors because these supervisors provide employees with important exchange resources in the form of social information that directs employees in how to succeed and survive in the organization. Because supervisors are often responsible for interpreting and encoding the organization’s profitability goals and then conveying these expectations to their employees (e.g., Grojean et al., 2004), employees are inclined to pay attention to supervisors’ strategies for succeeding within the organization (Berscheid, Graziano, Monson, & Dermer, 1976). Supervisors high in BLM provide clear and direct guidance as to what is most important in the organization (Greenbaum et al., 2012) and offer a straightforward, simplistic approach to succeeding by prioritizing bottom-line attainment above all else (Wolfe, 1988). With employees being inundated with organizational information and competing demands (e.g., Smith & Tracey, 2016), the high-BLM supervisor’s clear standards and direct approach to success may be viewed as desirable for reducing employees’ uncertainty and clarifying performance desires (e.g., Shah et al., 2002).

High-BLM supervisors also have elevated behavioral expectations regarding their employees’ work efforts; they expect their employees to do whatever they can to contribute to bottom-line success (Mawritz et al., 2017) and tend to carefully monitor their employees’ behaviors to ensure they are working to promote bottom-line attainment (Wolfe, 1988). BLM supervisors’ behaviors, which include showing a sole concern for profits (Greenbaum et al., 2012), demonstrate to employees that working to obtain the bottom line is of utmost importance and is a key to success. As such, supervisor BLM drives employees’ perceptions that they should attend to bottom-line objectives (Mesdaghini et al., 2019) and that accolades and rewards will go to employees who are deemed “winners” in obtaining the bottom line (Greenbaum et al., 2012).

Thus, we suggest that through their sole focus on bottom-line attainment, high-BLM supervisors provide employees with valuable information regarding paths to success. Employees become aware that success (e.g., rewards, promotions, accolades, opportunities) will come to those who take responsibility for bottom-line attainment and work to achieve bottom-line objectives. In this vein, employees of high-BLM supervisors may even believe that their supervisors are supporting the employees’ successes by providing such straightforward guidance about their job responsibilities. Indeed, past research suggests that employees appreciate, and respond well to, supervisors who initiate clear direction and expectations regarding work responsibilities (e.g., Judge, Piccolo, & Ilies, 2004; Northcraft, Schmidt, & Ashford, 2011). In contrast, supervisors low on BLM may take a more multivalent approach and emphasize several, perhaps even conflicting, goals, which can leave employees feeling confused and overloaded in terms of how to function within the organization (Kirmeyer, 1988; Unsworth, Yeo, & Beck, 2014). Thus, employees may see value in the high-BLM supervisor’s direct, clear message of obtaining bottom-line objectives above all else (Wolfe, 1988).

In line with social exchange theory, we suggest that employees will view their BLM supervisor’s clear message as a valuable exchange resource that will need to be reciprocated. In interpersonal interactions between supervisors and employees, when one party provides the other with exchange resources, the resources activate in the recipient feelings of obligation to repay in kind and motivate relevant behavioral responses that are meant to satisfy their felt obligation (Emerson, 1976). As noted earlier, the focus of the exchange resources produces feelings of felt obligation that reflect a similar focus, which then results in corresponding behaviors (Eisenberger et al., 2001; Fuller et al., 2006; Lorinkova & Perry, 2018). Thus, we suggest that the information provided by high-BLM supervisors about the importance of bottom-line attainment will serve as an exchange resource that will influence employees’ felt obligation toward the bottom line.

In turn, as a result of their felt obligation toward the bottom line, employees will strive to achieve behaviors that adhere to their supervisors’ bottom-line expectations. Specifically, we expect this process to result in employees’ enhanced task performance and UPB. Task performance refers to employee actions related to the production of goods or services that support the organization’s objectives (Rotundo & Sackett, 2002). Thus, high performers demonstrate the accomplishment of organizationally delineated tasks (Hu, Erdogan, Bauer, Jiang, Liu, & Li, 2015) and aid in helping an organization attain its bottom-line objectives. Although UPB is also potentially beneficial to an organization’s bottom line, these behaviors capture unethical acts (Umphress & Bingham, 2011; Umphress, Bingham, & Mitchell, 2010). UPB is a unique construct in that it reflects actions that are intended to contribute to or benefit the organization but are also unethical. Examples of such actions include destroying documents that may potentially tarnish the image of the organization and lying to customers if it would benefit the organization (Umphress & Bingham, 2011). Extant research suggests that employees may reciprocate social exchanges with their employer by supporting the organization through UPB (Umphress & Bingham, 2011). Thus, both task performance and UPB represent ways that employees can contribute to their organizations and help the organization attain its bottom-line objectives. Hence, we expect supervisor BLM to propagate employees’ felt obligation toward the bottom line that, in turn, fosters task performance and UPB as a way of reciprocating the supervisor’s bottom-line demands. In line with social exchange theory, these behaviors will allow employees to repay their BLM supervisors, satisfy their felt obligation toward the bottom line, help their organizations secure their bottom-line objectives, and support the outcomes valued by their high-BLM supervisors (see Eisenberger et al., 2001).

Hypothesis 1: Supervisor BLM will have positive and indirect effects on employee (a) task performance and (b) UPB via employee felt obligation toward the bottom line.

The Moderating Effect of Employee Ambition

In addition to providing support for the indirect effects of supervisor BLM on employee task performance and UPB via felt obligation toward the bottom line, social exchange theory suggests that individual-difference variables may play a moderating role (Cropanzano & Mitchell, 2005; Wischniewski, Windmann, Juckel, & Brune, 2009). The theory suggests that individuals differ in the degree to which they attend to obligations to repay and endorse reciprocity (Cropanzano & Mitchell, 2005), which influences the link between the perception of one party’s actions and the recipient’s felt obligation. For example, in comparison to individuals who are low on exchange orientation, those high on this orientation are more likely to respond to situations by considering reciprocity, tracking obligations, and desiring to return exchange resources (e.g., Buunk, Doosje, Jans, & Hopstaken, 1993). Thus, in response to certain events, they are more likely to experience a sense of felt obligation.

In this regard, we identified employee ambition as an individual-difference variable that may influence the social exchange effects of supervisor BLM. Individuals high on ambition are generally on the lookout for attaining resources, career advancement, and success (e.g., Ashy & Schoon, 2010; Jansen & Vinkenburg, 2006; Judge & Kammeyer-Mueller, 2012). More so than those low on ambition, those high on ambition are particularly attuned to resources that can help them to get ahead (e.g., Van Vianen, 1999) and thus are more likely to show reciprocation tendencies toward those who provide them with information on how to achieve success.

We suggest that highly ambitious employees are likely to view supervisor BLM as personally relevant to their desires. Because these employees are more inclined to care about their own success and strive for the attainment of quantifiable outcomes, such as promotions or pay raises (Judge & Kammeyer-Mueller, 2012; McClelland, 1961), they are likely to look to their supervisors for cues on how to succeed in their workplace and to view their supervisors’ focus on bottom-line outcomes as relevant to their own progress and future success. Thus, ambitious employees will be particularly attentive to the exchange resources provided by their high-BLM supervisors. More so than those low on ambition, highly ambitious employees will be particularly attuned to the clear message regarding bottom-line attainment provided by their high-BLM supervisors because this message provides clarity on what it takes to be successful and survive over time. They will attend to their high-BLM supervisors’ espoused values and expectations and will recognize that bottom-line attainment is of primary importance. Ambitious employees may also be more likely than unambitious employees to appreciate the clear direction given to them by their supervisors and view such direction as a signal that the supervisors are supportive of their successes (e.g., Holstad, Korek, Rogotti, & Mohr, 2014). In turn, highly ambitious employees are more likely to respond to high-BLM supervisors with desires to reciprocate because these supervisors are directly relevant to ambitious employees’ desires.

Given that the informational exchange resources provided by BLM supervisors will be especially salient to employees high on ambition, we suggest that ambitious employees will be more likely than those low on ambition to view the exchange resources provided by their high-BLM supervisors as necessitating reciprocity. In line with research that has suggested that a high exchange orientation can influence one’s considerations of reciprocity (e.g., Buunk et al., 1993), ambitious employees will be more likely to attend to the information they receive from their high-BLM supervisors, and therefore, they will be more likely to feel an obligation to help attain bottom-line objectives. Accordingly, these employees will be subsequently motivated to increase their task performance and engage in UPB. In contrast, because employees low on ambition generally have little desire for success and rarely go out of their way to accomplish “more” (Judge & Kammeyer-Mueller, 2012; Van Vianen, 1999), these employees are less likely to view their supervisor’s high BLM as personally relevant and are less likely to attend to the supervisor’s expectations regarding bottom-line attainment. As such, the information conveyed by high-BLM supervisors will be less salient and meaningful to those low on ambition. Consequently, unambitious employees who perceive that their supervisors possess high BLM will be less likely to develop strong feelings of obligation toward the bottom line, which will then limit the extent to which these employees deliver high performance and UPB.

Hypothesis 2: Employee ambition strengthens the positive relationship between supervisor BLM and employee felt obligation toward the bottom line.

Hypothesis 3: Employee ambition moderates the positive indirect effects of supervisor BLM on (a) employee task performance and (b) UPB via employee felt obligation toward the bottom line, such that these indirect effects are stronger when employee ambition is high versus low.

Method

Sample and Procedure

This study was conducted in 34 branches of nine commercial banks across three states in Nigeria, West Africa. Participants included banking employees in various units and different branches of the banks. Because we were interested in studying the effects of supervisor BLM, we limited participation to employees who engaged in transaction activities (i.e., marketing, customer services, cashiering and loans, and investment banking) and had frequent interactions with their supervisors. Access to participants was obtained through managers in each of the banks. Prior to administrating the surveys, 500 employees received a cover letter from the lead author that identified the purpose of the study, provided assurances that their responses would not be shared with their respective banks, and noted that participation was voluntary. Participants were then delivered the surveys with envelopes for them to seal their responses, which were collected on-site by trained research assistants during regularly scheduled work hours.

To reduce potential common-method bias (Podsakoff, MacKenzie, & Podsakoff, 2012), three separate surveys were administered at three different points in time. At Time 1, employees rated their supervisors’ BLM and assessed their own ambition. Three weeks later, at Time 2, employees assessed their felt obligation toward the bottom line. Then, 3 weeks after Time 2, at Time 3, employees rated their own UPB, and supervisors provided ratings of each employee’s task performance. Each survey was given an identification code so that we could match responses across time periods. A total of 225 employees completed all three waves of surveys (for a response rate of 45%) and had their performance rated by their immediate supervisors (n = 181). Of the 181 supervisors, 145 rated only one employee; therefore, nesting was not a serious concern in this study. Nonetheless, to provide a rigorous test of our hypotheses, we followed recommendations from the literature (e.g., Bliese, Maltarich, & Hendricks, 2018; Hsu, Lin, & Skidmore, 2018; McNeish, Stapleton, & Silverman, 2017) and used a design-based modeling approach with corrections for clustering (i.e., parameter-estimate standard errors based on cluster sampling design, TYPE = COMPLEX, ESTIMATOR = MLR in Mplus 7.0). Of the 225 employees, 53% were male, their mean age was 34.09 years (SD = 6.44), and their mean organizational tenure was 4.82 years (SD = 3.95). To improve supervisor response rates, we did not ask supervisors to respond to demographics. However, in terms of gender, the supervisor participants matched that which is typical of the finance industry, with slightly more men than women. Indeed, the National Bureau of Statistics (2019) suggests that in the Nigerian financial industry, 52% of the workforce is male.

Measures

All surveys were administered in English, as this is the official business language in Nigeria, and the study variables were anchored on a 5-point Likert-type scale ranging from strongly disagree (1) to strongly agree (5).

Supervisor BLM

Employees rated supervisor BLM using a four-item scale developed by Greenbaum et al. (2012). A sample item is “My supervisor is solely concerned with meeting the bottom line” (α = .81).

Employee ambition

Employees rated their ambition with a five-item scale by Van Vianen (1999). A sample item is “I would like to move into a higher position/job in the near future” (α = .89).

Employee felt obligation toward the bottom line

Employees rated their felt obligation toward the bottom line using five items adapted from an existing measure of felt obligation (Eisenberger et al., 2001). We adapted the original items to ask employees about their felt obligation toward the bottom line in particular. For example, we changed the item “I feel a personal obligation to do whatever I can to help the organization achieve its goals” to “I feel a personal obligation to do whatever I can to help the organization achieve its bottom line.” (α = .88).

Employee task performance

Supervisors rated each employee’s task performance using Schaubroeck, Lam, and Cha’s (2007) three-item scale (α = .89). A sample item is “This employee performs tasks that are expected of him or her.”

Employee UPB

Employees rated their UPB using Umphress and colleagues’ (2010) six-item scale (α = .88). A sample item is “If it would help my organization, I would exaggerate the truth about my company’s products or services to customers and clients.”

Controls

We controlled for employees’ age, gender (coded 1 = male, 2 = female), and tenure because these demographic variables may be related to performance (Schaubroeck et al., 2007) and UPB (Umphress et al., 2010). In addition, to account for contextual differences between the nine banks, we included eight dummy variables of these banks. We then ran our analyses with and without demographic and dummy variables and found that controlling for them did not meaningfully change or affect our results. Therefore, following the recommendations of Becker (2005), we omitted these variables from subsequent analyses for parsimony (see also, Leroy, Anseel, Gardner, & Sels, 2015; Tepper, Moss, & Duffy, 2011). Finally, we controlled for employees’ perceptions of top management (TM) BLM (Babalola et al., 2019), measured with Greenbaum et al.’s (2012) four-item scale (α = .83). We included TM BLM in our final analyses to rule out potential confounds due to an organization-level BLM.

Results

Preliminary Analyses

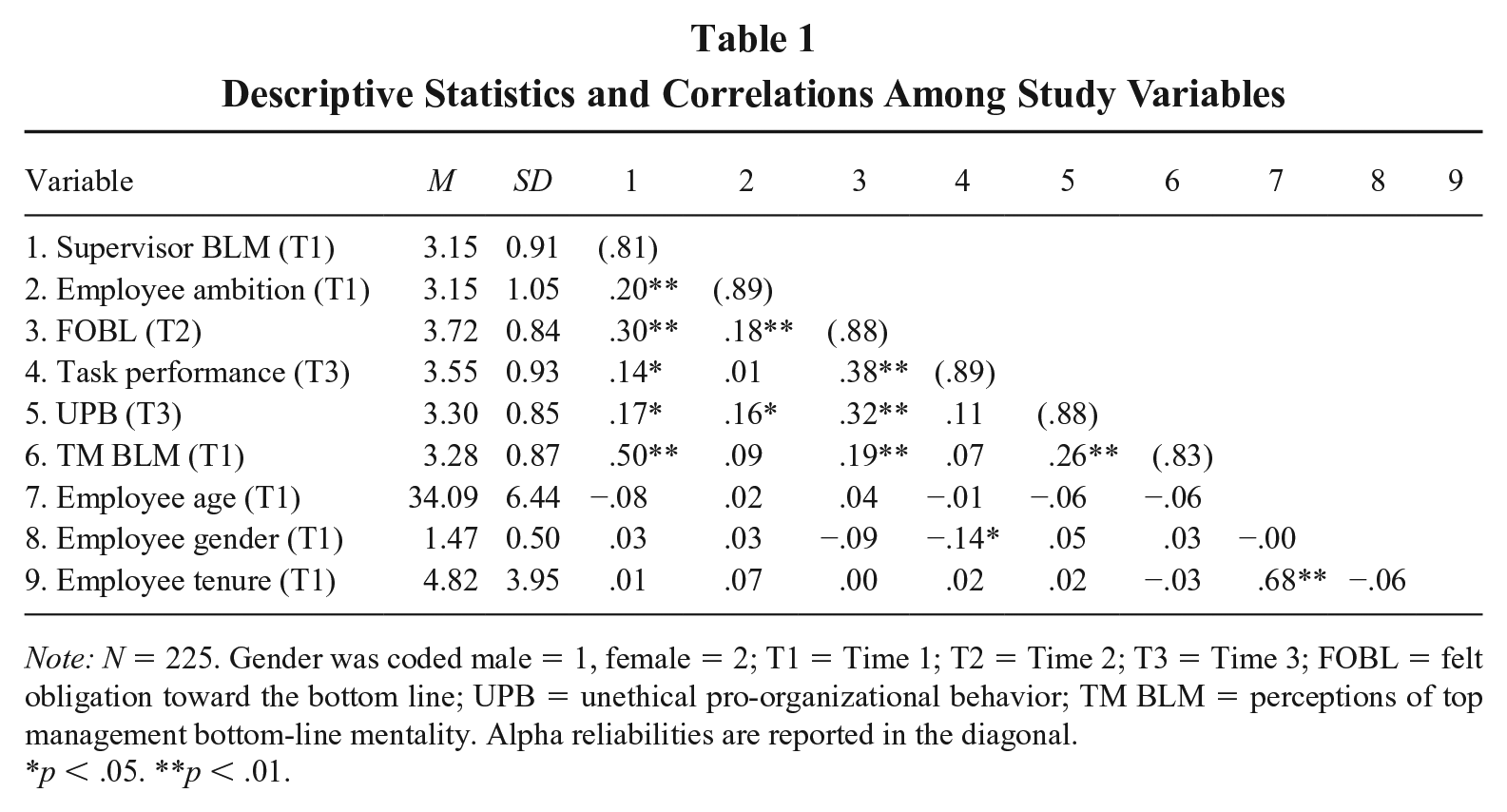

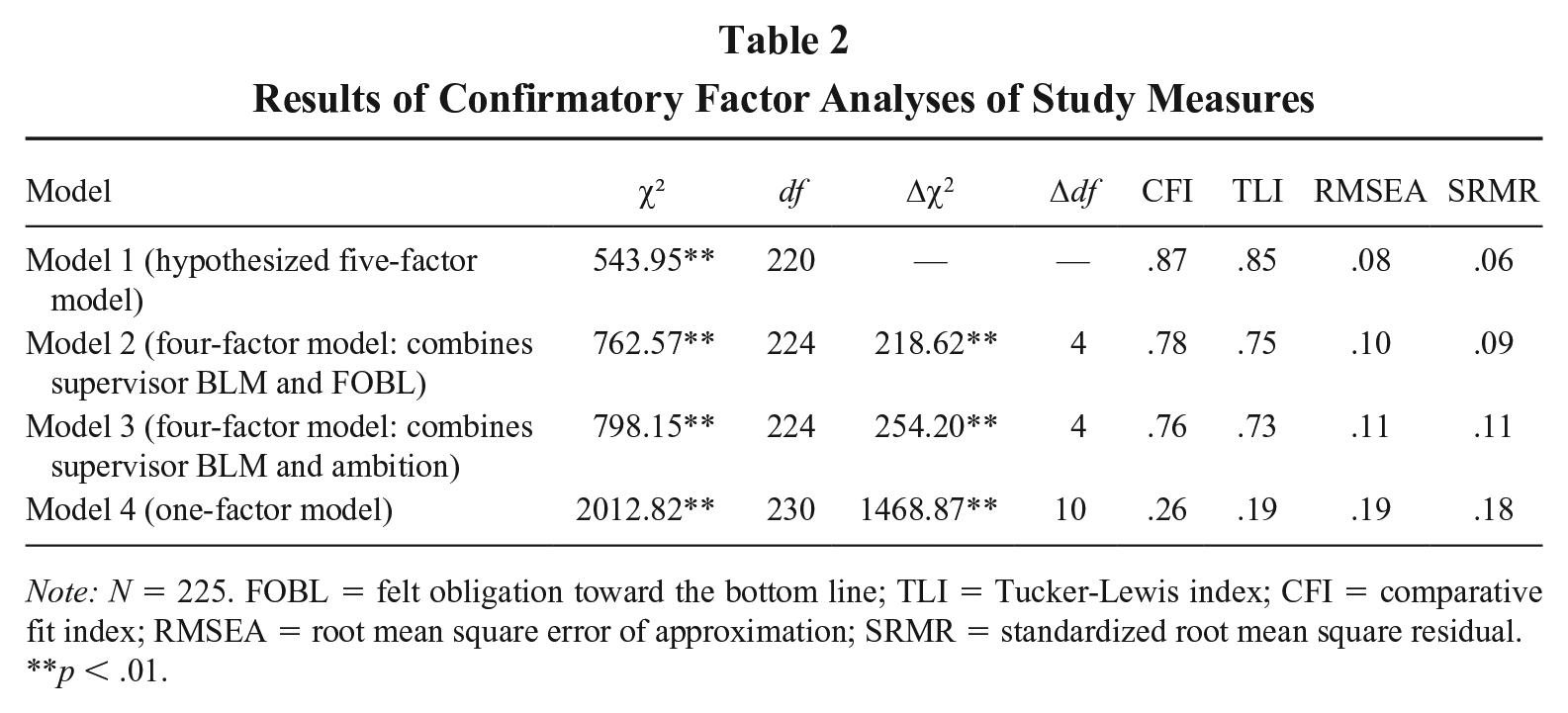

The descriptive statistics and intercorrelation among study variables are presented in Table 1. Before testing our hypotheses, we first conducted a preliminary analysis to assess differences on the substantive variables among the 34 branches in our study. One-way analyses of variance suggested no mean differences for supervisor BLM, F(33, 191) = 1.25, p = .179; task performance, F(33, 191) = .80, p = .770; UPB, F(33, 191) = .67, p = .918; felt obligation toward the bottom line, F(33, 191) = .97, p = .527; and ambition, F(33, 191) = 1.01, p = .458, meaning the present data cannot reject the null hypothesis that each branch is not producing unique variance with respect to our key variables of interest. We then ran a series of confirmatory factor analyses (CFAs) to examine the distinctiveness of our five variables. As shown in Table 2, the CFA results revealed that the hypothesized five-factor model that included supervisor BLM, employee ambition, employee felt obligation toward the bottom line, task performance, and UPB (χ² = 543.95, df = 220, comparative fit index = .87, Tucker-Lewis index = .85, root mean square error of approximation = .08, standardized root mean square residual = .06, p = .000) was statistically significant above and beyond alternate models, including a four-factor model that allowed supervisor BLM and employee felt obligation toward the bottom line to load on one construct (Δχ2 = 218.26, Δdf = 4), another four-factor model that allowed supervisor BLM and employee ambition to load on one construct (Δχ2 = 254.20, Δdf = 4), and a one-factor model that loaded all items on one construct (Δχ2 = 1468.87, Δdf = 10). These results provide empirical support for the distinctive nature of our study variables.

Descriptive Statistics and Correlations Among Study Variables

Note: N = 225. Gender was coded male = 1, female = 2; T1 = Time 1; T2 = Time 2; T3 = Time 3; FOBL = felt obligation toward the bottom line; UPB = unethical pro-organizational behavior; TM BLM = perceptions of top management bottom-line mentality. Alpha reliabilities are reported in the diagonal.

p < .05. **p < .01.

Results of Confirmatory Factor Analyses of Study Measures

Note: N = 225. FOBL = felt obligation toward the bottom line; TLI = Tucker-Lewis index; CFI = comparative fit index; RMSEA = root mean square error of approximation; SRMR = standardized root mean square residual.

p < .01.

Finally, because our data were collected from the same source except for performance, we empirically examined the presence of common-method variance (CMV) using the CFA marker technique recommended in the literature (Podsakoff et al., 2012; Williams, Hartman, & Cavazotte, 2010). We used Kreiner’s (2006) four-item segmentation preference scale (e.g., “I like to be able to leave work behind when I go home”) as a marker variable. We ran a model in which the indicators of the study’s substantive variables were specified to load onto the latent marker variable (χ2 = 631.62, df = 286) and compared it to a model in which they did not load onto the marker variable (χ2 = 661.30, df = 309). The results showed that CMV was not present and so it did not bias the parameters of our model, as evidenced by a nonsignificant chi-square difference test between the two models (Δχ2 = 29.68, Δdf = 23, p = .159).

Hypotheses Testing

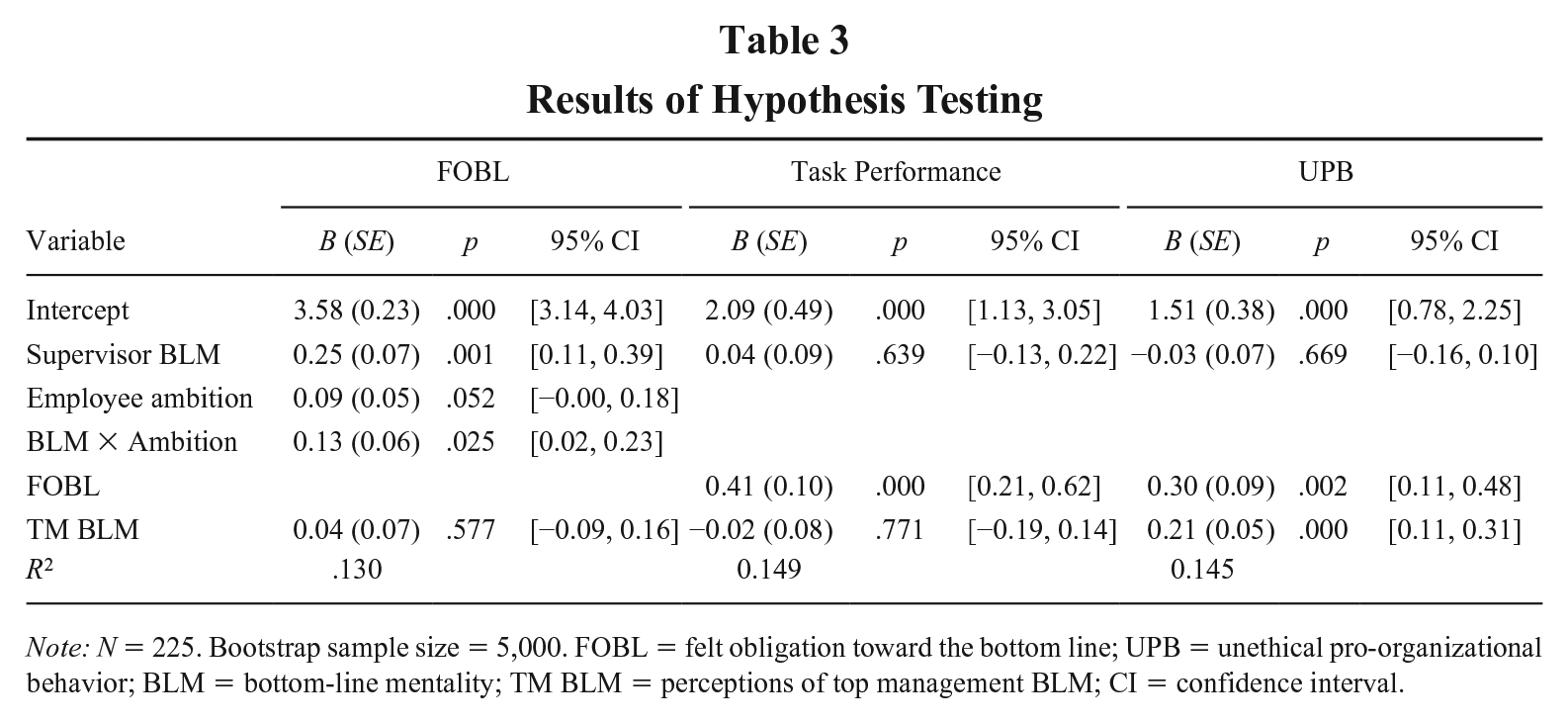

Hypotheses 1a and 1b suggested that employee felt obligation toward the bottom line mediates the relationship between supervisor BLM and employee (a) task performance and (b) UPB. Our results (see Table 3) revealed that supervisor BLM was positively related to employee felt obligation toward the bottom line (B = .25, SE = .07, p < .01), and employee felt obligation toward the bottom line was positively related to employee task performance (B = .41, SE = .10, p < .01) and UPB (B = .30, SE = .09, p < .01). In addition, our results revealed that supervisor BLM was positively related to (a) employee task performance and (b) UPB via employee felt obligation toward the bottom line (task performance: indirect effect = .10, SE = .04, 95% confidence interval [CI] = [.03, .18]; UPB: indirect effect = .07, SE = .03, 95% CI = [.02,.13]). Thus, Hypotheses 1a and 1b were supported.

Results of Hypothesis Testing

Note: N = 225. Bootstrap sample size = 5,000. FOBL = felt obligation toward the bottom line; UPB = unethical pro-organizational behavior; BLM = bottom-line mentality; TM BLM = perceptions of top management BLM; CI = confidence interval.

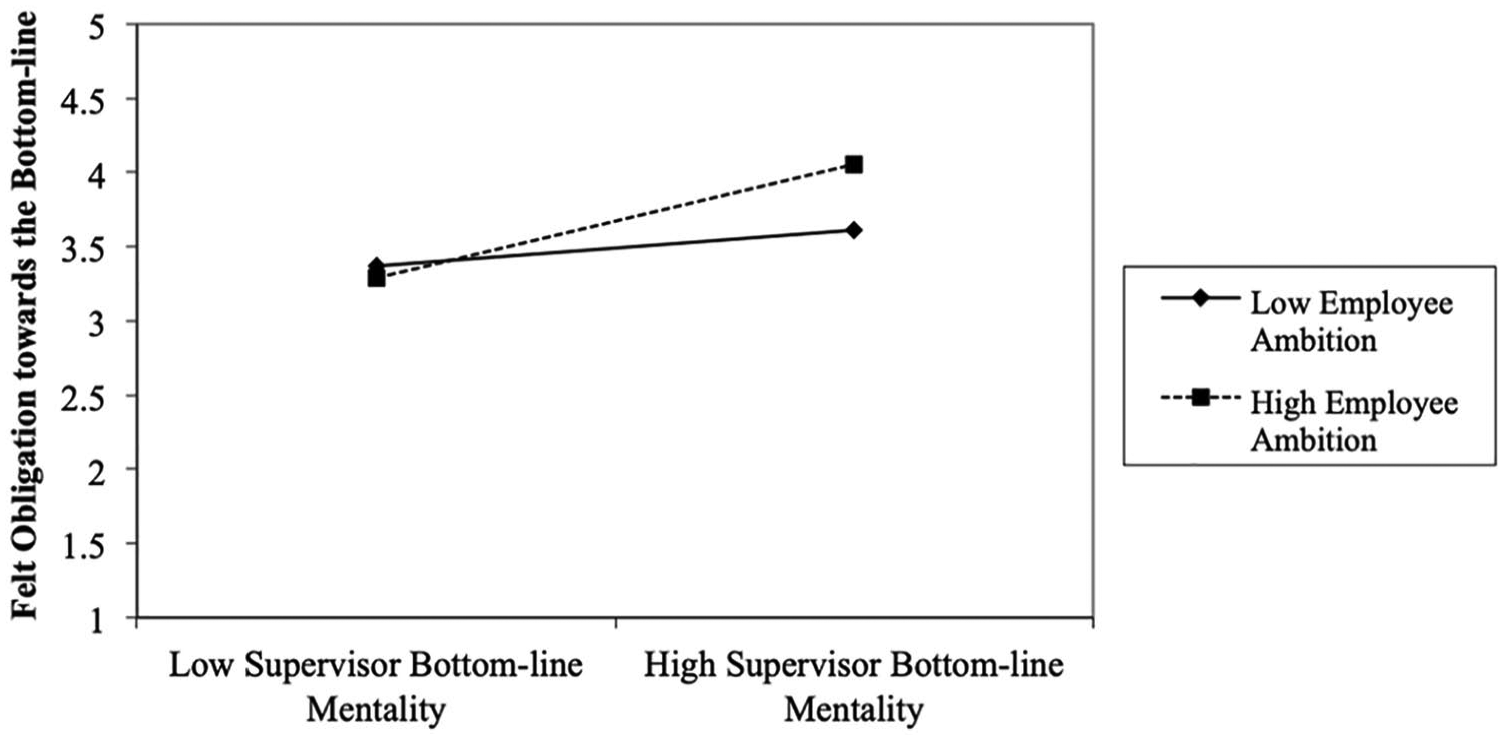

Hypothesis 2 suggested that employee ambition strengthens the positive relationship between supervisor BLM and employee felt obligation toward the bottom line. In support of Hypothesis 2, our results (Table 3) revealed a positive and significant interaction effect between supervisor BLM and employee ambition on employee felt obligation toward the bottom line (B = .13, SE = .06, p = .025). The pattern of this interaction was consistent with our hypothesized direction; the positive relationship between supervisor BLM and employee felt obligation was stronger in the presence of high versus low employee ambition (see Figure 2).

Interactive Effect of Supervisor Bottom-Line Mentality and Employee Ambition on Felt Obligation Toward the Bottom Line

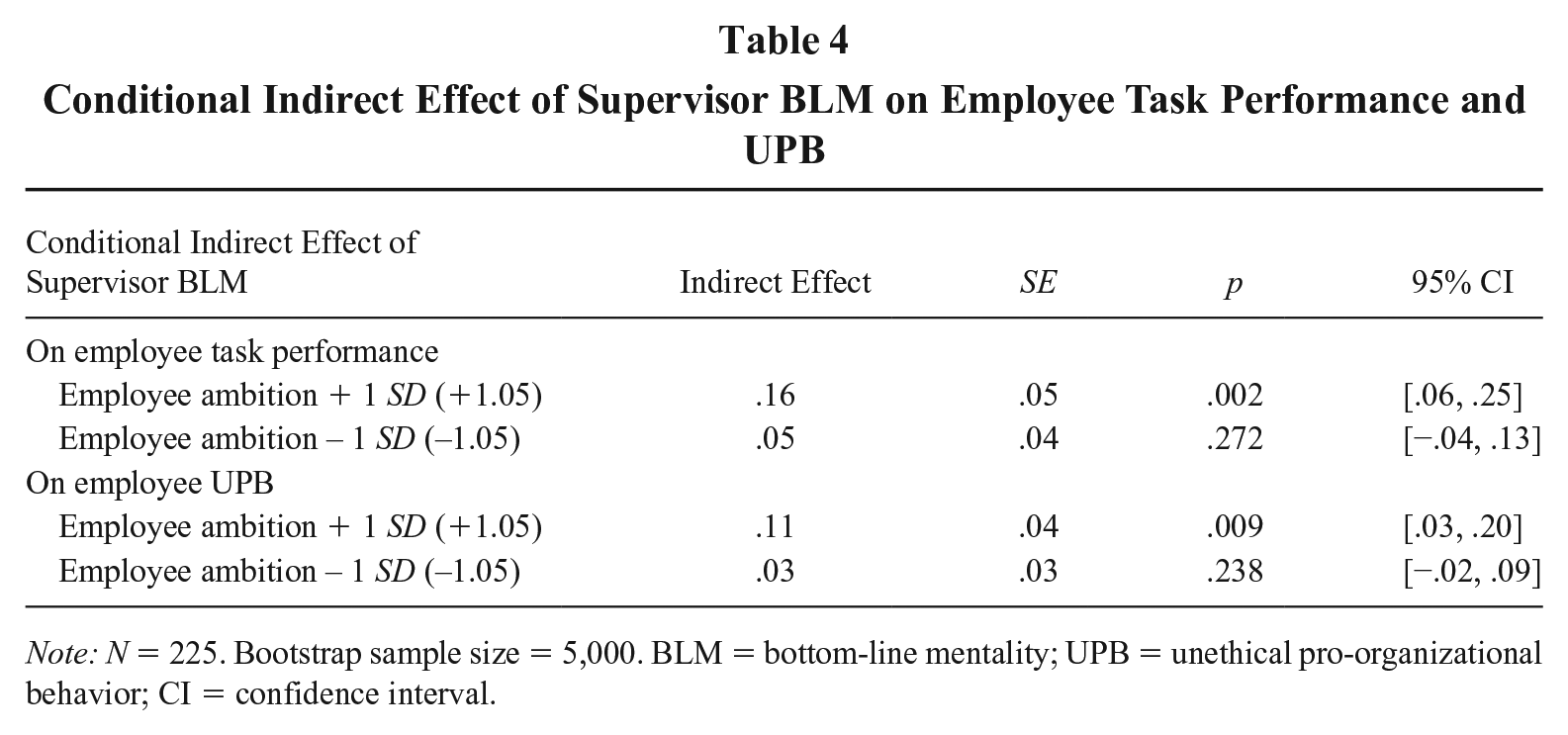

Finally, Hypotheses 3a and 3b suggested that employee ambition strengthens the positive indirect effects of supervisor BLM on employee (a) task performance and (b) UPB. First, our results (see Table 4) demonstrated that the indirect effects of supervisor BLM on employee (a) task performance and (b) UPB through felt obligation toward the bottom line were significant under conditions of high ambition (task performance: conditional indirect effect = .16, SE = .05, 95% CI = [.06, .25]; UPB: conditional indirect effect = .11, SE = .04, 95% CI = [.03, .20]) rather than under conditions of low ambition (task performance: conditional indirect effect = .05, SE = .04, 95% CI = [–.04, .13]; UPB: conditional indirect effect = .03, SE = .03, 95% CI = [–.02, .09]). To provide support that mediation is statistically different for the high and low conditions of the moderator, we assessed the index of moderated mediation using 90% CIs (e.g., Baer et al., 2018; Mawritz et al., 2017). Because the CIs do not cross zero, we found support for Hypotheses 3a and 3b (task performance: index = .05, SE = .02, 90% CI = [.012, .091]; UPB: index = .04, SE = .02, 90% CI = [.002, .072]).

Conditional Indirect Effect of Supervisor BLM on Employee Task Performance and UPB

Note: N = 225. Bootstrap sample size = 5,000. BLM = bottom-line mentality; UPB = unethical pro-organizational behavior; CI = confidence interval.

In sum, our results revealed that supervisor BLM has beneficial effects on employee task performance through felt obligation toward the bottom line and that high employee ambition strengthens these effects. Yet, our results also revealed that supervisor BLM can have ill effects because it encourages UPB, through felt obligation toward the bottom line, particularly when employees are high on ambition.

Discussion

Theoretical Implications

Our research advances the emerging literature on BLM and makes several contributions to the literature. Drawing from social exchange theory, our primary contribution lies in investigating the performance benefits of supervisor BLM. Although it has been implicitly suggested that supervisor BLM might be beneficial at work (Bonner et al., 2017), research explicitly investigating this possibility has largely been absent from the extant literature. In contrast to past research (e.g., Greenbaum et al., 2012; Mawritz et al., 2017), our research takes a more functional, or balanced, view of the supervisor BLM concept by investigating outcomes that may be favorable to the organization. In doing so, we provide empirical evidence showing the link between supervisor BLM and employees’ positive contributions to the organization in the form of task performance. This line of research is important in that it challenges assumptions regarding the detrimental consequences of BLM by suggesting that high-BLM supervisors provide employees with valuable information regarding work priorities, which can have beneficial effects for the organization (namely, enhanced task performance).

We also contribute to the BLM literature by demonstrating that the relationship between supervisor BLM and employees’ work contributions is complex and multifaceted in that “work contributions” can take many forms. Although our findings suggest that supervisor BLM fosters social exchanges with employees that enhance task performance, it can also fuel employees’ unethical contributions in the form of UPB. Specifically, employees with high-BLM supervisors may satisfy their need to contribute to bottom-line attainment via task performance but may also do so in unethical ways as evidenced by their willingness to engage in UPB. For example, they may lie to customers for the benefit of the company. In this regard, our study provides a richer understanding of high-BLM supervisors’ effects and suggests the need for research to adopt a more balanced view of both the good and bad effects of BLMs.

Moreover, we contribute to the burgeoning BLM literature by providing a test of the underlying mechanism that explicates why supervisor BLM enhances employee task performance and UPB. We draw on social exchange theory to identify employees’ felt obligation toward the bottom line as a key mediating mechanism accounting for the aforementioned relationships. Our results suggest that employees respond to high-BLM supervisors with feelings of obligation toward the bottom line, which in turn motivates them to perform at high levels but also to engage in UPB, both of which presumably satisfy their felt obligation. These findings, therefore, suggest that an empirical focus on a bottom-line-specific sense of felt obligation is central to understanding why BLM may generate positive performance-related outcomes as well as potentially unethical outcomes. This is particularly important, given that domain-specific felt obligation has been found to be important in predicting outcomes that support the realization of relevant goals and behaviors (e.g., Fuller et al., 2006; Liang et al., 2012; Lorinkova & Perry, 2018; Morrison & Phelps, 1999).

Finally, we contribute to the literature by demonstrating that employees high on ambition are more likely to attend to the informational exchange resources provided by their high-BLM supervisors, thus making them more likely to develop a strong sense of felt obligation toward the bottom line. Because highly ambitious employees have strong desires to attain success (Judge & Kammeyer-Mueller, 2012), they are more likely to attend to their high-BLM supervisor’s messages for success (i.e., bottom-line attainment) and, thus, develop a stronger sense of obligation to secure the bottom line. In turn, they are more motivated to exert higher levels of task performance and engage in UPB to satisfy their felt obligation. As such, we demonstrated that employee ambition can be both functional and dysfunctional when coupled with supervisor BLM. In doing so, we enrich knowledge of the effects of BLM as well as ambition by identifying individuals who are more likely to be influenced by supervisor BLM.

Practical Implications

Our findings offer practical implications for organizations wishing to make the most of their members’ mind-set and behaviors in the process of pursuing profits. Organizations should recognize that supervisor BLM is a double-edged sword with both cost and benefit implications for employees. As such, it is important to incorporate our findings into management training programs to equip leaders with a more balanced and thorough understanding of how their BLM influence employees. It is also advisable to heighten moral education at work so that when supervisors communicate with employees about the importance of bottom-line pursuits, they also remind employees of the importance of upholding ethics (Treviño & Nelson, 2011).

Additionally, our findings suggest that organizations would benefit from having systems in place to better leverage supervisor BLM when it comes to performance review and reward management. For instance, it is common that organizations resort to performance outcomes that are measurable and quantifiable when rewarding high achievers (Ren, Wood & Zhu, 2014), especially in a competitive business environment. However, a range of human resource management practices should be designed to monitor the (un)ethical conduct of employees, from job design, where ethics codes are written into the job description, to performance evaluations, where a broader range of short-term and long-term criteria are used. Consequently, recognition and rewards for ethical practices should be promoted in the workplace.

Limitations and Future Research Directions

As with any study, there are both strengths and limitations in this study. For instance, even though our data were collected via different sources at different points in time, we did not adopt an experimental design that would allow us to draw causal conclusions about the observed relationships. Our theory supports the proposed causal direction of our theoretical model, and our findings support our predictions. Yet, to provide more credence to our causal direction, we recommend that future research use alternative research designs that strengthen causality. Also, even though supervisors rated employees’ performance, we may have introduced some consistency bias (Podsakoff et al., 2012) by having employees rate the rest of our study variables (e.g., supervisor BLM and employee UPB). In this regard, our study design could have been improved by having an external measure of supervisor BLM, perhaps from a higher-level supervisor or one of the focal employees’ coworkers. Relatedly, we assessed employees’ willingness to engage in UPB rather than actual UPB. However, previous research indicates that intentions do translate into actual unethical behavior (Kish-Gephart, Harrison, & Treviño, 2010) and has reported similar results irrespective of whether their predictions were tested using the willingness-to-engage-in-UPB measure or actual-UPB measure (see Umphress et al., 2010). Nonetheless, future research should consider including actual UPB in their theoretical model.

Another possible limitation is that our study participants were from the Nigerian banking industry, which may raise concerns about the generalizability of our findings due to the fact that the specific Nigerian context may be higher than normal with respect to corruption. Yet, there are also benefits to conducting research in such a context. As noted by George, Corbishley, Khayesi, Haas, and Tihanyi (2016), African countries provide a unique context for management researchers to examine how Western-based phenomena or theories play out, given their increasingly growing economy and the influx of Western organizations in the continent (see also Babalola, Stouten, Euwema, & Ovadje, 2018). Also, with respect to context, we collected data from the banking industry. Many high-profile corporate scandals revolve around the banking industry (e.g., Wells Fargo, Deutsche Bank, HSBC), with these scandals occurring in a range of countries (e.g., United States, Germany, Britain). Thus, banking fraud and unethical conduct are prevalent worldwide, regardless of the country. As such, our banking sample in the Nigerian context not only responds to George et al.’s (2016) call but also provides a highly appropriate context for examining supervisor BLM, employee ambition, and potential employee unethical conduct. Nonetheless, future research may benefit from an examination of BLM within other relevant contexts (e.g., sales) across a range of countries and cultures.

More generally, given our reliance on social exchange theory, we also acknowledge that the Nigerian culture, which tends to be collectivistic in nature, may have influenced exchanges between supervisors and their employees and perhaps played a role in the extent to which reciprocity is valued (Gouldner, 1960). Individuals from collectivist cultures attend to exchange norms more so than their counterparts from individualistic cultures (Earley & Gibson, 1998; Mintu-Wimsatt & Madjourova-Davri, 2011; Ng & Feldman, 2015; Shen, Wan, & Wyer, 2011). Therefore, we expect that because members of collectivistic cultures are communal and tend to strive to achieve group goals (Bochner, 1994; Triandis, Bontempo, Villareal, Asai, & Lucca, 1988), the extent to which they respond to high-BLM supervisors with feelings of indebtedness and associated performance outcomes may be increased (Shen et al., 2011). Employees in Nigeria or other collectivistic cultures (e.g., China) may therefore feel a stronger sense of obligation toward the bottom line as a result of having a high-BLM supervisor than those in individualistic cultures (e.g., the United States). Additionally, although social exchange theory provides sound theoretical reasoning for our hypotheses, there are aspects of our theoretical reasoning that are not explicitly captured by our theoretical model. For instance, we do not know if high-BLM supervisors give task direction and if employees of these supervisors are actually rewarded for responding to their supervisor’s bottom-line focus (e.g., via bonuses, increased pay, and promotion). We recommend that future research delve deeper into these possibilities.

Our findings also provide a foundation for future research on BLM to explore additional research questions. Our work provides initial evidence that supervisor BLM may motivate individual employee task performance. We did not, however, incorporate organizational-level antecedents and group-level outcomes into our model due to the individual nature of our research question and data. Yet, it may be possible that the effect of supervisor BLM on performance was influenced by factors at the organizational level or contextual considerations. Thus, to mitigate this concern, we controlled for perceptions of TM BLM in our analyses, which has been shown to represent perceptions of context in past research (Babalola et al., 2019). Our results remained the same with the inclusion of this control variable, which suggests that supervisor BLM has a unique and independent influence on the generation of employees’ social exchange processes and work contributions. We also examined our data to investigate the extent to which the nine banks in our sample produced differences across our substantive variables. Our results revealed that these higher-level effects did not influence our findings. Nevertheless, we believe future research on BLM would benefit from considering organizational-level antecedents of supervisor BLM. For example, future research could investigate organizational reward structures (Pfeffer, 1998), leaders’ rhetoric (Carton, Murphy, & Clark, 2014), and top leaders’ economic values in decision making (Sully de Luque, Washburn, Waldman, & House, 2008) as factors that may prompt supervisors’ high BLM. Such research could also examine how employees’ collective perceptions of supervisor BLM relate to the group’s identity, leadership effectiveness, and group-level performance.

Scholars might also consider the (mis)alignment between employee ratings of supervisor BLM and supervisor ratings of their own BLM. Our specific research question was oriented toward how employees view their supervisors and how these views affect employees’ social exchanges as operationalized by felt obligation. Thus, we did not investigate supervisor’s own ratings of their BLM in our research. Nevertheless, future research could examine the fit between employees’ and supervisors’ ratings of supervisor BLM. Using polynomial regression or difference tests (e.g., Zhang, Wang, & Shi, 2012), it could be that when there is high agreement concerning the supervisor’s high BLM, employees may exhibit the highest level of motivation to secure high performance. With high–low pairings, supervisors and employees may get frustrated with each other because of discrepant views on what is important. Future research could enhance the field’s understanding of the motivational nature of BLM by investigating these possibilities.

Finally, BLM research, to date, has assumed that BLM encapsulates financial considerations to the neglect of competing priorities, including employee well-being, ethical considerations, and other issues, such as environmental responsibility (Greenbaum et al., 2012; Wolfe, 1988). In this regard, the BLM items reflect an orientation toward financial considerations (i.e., the items reflect profits, bottom line, and business) above anything else. In the context of our study, employees may have interpreted the “bottom line” as the branch-level or broader organizational bottom line, thus making it difficult to ascertain whether they understood how their individual performance affects the organization’s bottom line. Although empirical evidence suggests that individual performance contributes to both team and organizational bottom-line outcomes (Chun, Shin, Choi, & Kim, 2013; Liao & Chuang, 2004), future research could modify the BLM items to reflect either branch or organization bottom line based on their research questions. Future research might also consider the implications of BLM with respect to different bottom-line outcomes, such as quality of work life or desires for prestige. As an example, the recent college admissions scandal demonstrated that some parents will go to extreme lengths, ignoring ethical standards, to get their children admitted to prestigious universities (Taylor, Medina, Buckley, & Stevenson, 2019). In fact, these parents paid hefty bribes (forgoing financial considerations and ethics) for the sake of prestige and status. They may have been operating with a BLM but with the specific bottom line being prestige instead of metrics tied to financial outcomes. An examination of BLM with respect to a range of specific bottom-line outcomes would require a modified version of the BLM scale; however, we believe such research could expand management researchers’ and practitioners’ understanding of what happens when people obsessively focus on one dominant outcome.

Conclusion

In this study, we drew on social exchange theory to shift the focus of extant research from BLM’s dysfunctionalities to a more balanced perspective. In particular, we shed light on why and when supervisors’ high BLM enhances employees’ contributions to the organization in the forms of task performance and UPB. We found that high-BLM supervisors stimulate employees’ felt obligation toward the bottom line, leading to heightened levels of task performance and UPB. Furthermore, we found that this process is exacerbated by employees’ high ambition. In light of these findings, we hope future research will continue to concentrate on both the dark and bright sides of supervisor BLM and how to best manage this leadership approach.