Abstract

Over the past decade, the rise of blockchain technology has led to the emergence of a growing number of decentralized platforms that are governed less by platform owners and more through community efforts. The emergence of blockchain platforms offers a unique opportunity to examine alternative structures for platform governance and to develop a theory around the value of centralized, semi-decentralized, and decentralized governance. Drawing on mechanism design theory, we evaluate the tradeoffs between centralization and decentralization and hypothesize semi-decentralization as a higher performing governance structure. Empirical evidence from the blockchain industry shows that decentralization has an inverted U-shaped relationship with platforms’ market capitalization, developer attention, and development activity. We further examine factors driving the decentralization of platform governance and find that digital platforms of the infrastructure layer—relative to those of the application layer—have a tendency to become more decentralized. This tendency, nevertheless, can be offset by experienced leaders to achieve semi-decentralization. Overall, this study contributes new insights on the characteristics, antecedents, and consequences of effective platform governance.

Keywords

The most successful companies of our time—Alphabet, Amazon, Apple, Facebook, and Microsoft—are owners of digital platforms. Digital platforms are digital systems that facilitate communications, interactions, and innovations to support economic transactions and social activities (Cennamo, 2019; Constantinides, Henfridsson, & Parker, 2018; Gawer, 2014; McIntyre & Srinivasan, 2017; Thomas, Autio, & Gann, 2014). Over the past several decades, digital platforms have redefined business models, disrupted established industries, helped launch new products and services, and created enormous value for society (Cusumano, Gawer, & Yoffie, 2019; Evans & Schmalensee, 2016; Parker, Van Alstyne, & Choudary, 2016). As digital platforms rise to dominance, platform owners have accumulated substantial power and influence, and they often play essential roles in leading key stakeholders to create value for their platform ecosystems (Boudreau, 2010; Kyprianou, 2018; Reischauer & Mair, 2018; Rietveld, Schilling, & Bellavitis, 2019; Wareham, Fox, & Giner, 2014). Without effective checks and balances, however, platform owners can sometimes direct digital platforms to pursue activities that benefit themselves at the expense of other stakeholders (Cohen, 2019; Srnicek, 2017; Van Dijck, Poell, & De Waal, 2018; Zuboff, 2019). Over time, stakeholders are becoming increasingly concerned with the growing power of platform owners and with problems caused by power imbalances between platform owners and other stakeholders. Chris Dixon, a prominent venture capitalist, makes the following observations: “Over time, the best entrepreneurs, developers, and investors have become wary of building on top of centralized platforms. We now have decades of evidence that doing so will end in disappointment. In addition, users give up privacy, control of their data, and become vulnerable to security breaches. These problems with centralized platforms will likely become even more pronounced in the future” (Dixon, 2018).

To shed light on platform governance, we draw on mechanism design theory to examine the benefits and limits of centralized and decentralized governance structures. According to mechanism design theory, an effective governance structure should leverage individual incentives and local information to achieve desirable outcomes (Hurwicz, 2008; Maskin, 2008; Mookherjee, 2006; Myerson, 2008). To leverage individual incentives, a governance structure should ensure that platform owners and participants can realize their respective goals and interests through digital platforms (Hurwicz, 1973; Hurwicz & Reiter, 2006). To leverage local information, a governance structure should seek to leverage all available information to achieve effective governance processes and outcomes (Hurwicz, 1973; Hurwicz & Reiter, 2006). Both centralization and decentralization have their respective benefits and limits. In a fully centralized governance structure, platform owners enjoy exclusive governance control, allowing them to shape governance processes and outcomes (Boudreau, 2010; Rietveld et al., 2019). Concentrating governance power among platform owners, however, may disadvantage platform participants (e.g., third-party developers and end users) and alienate them, as platform owners can prioritize their own interests over those of stakeholders (Arrieta-Ibarra, Goff, Jiménez-Hernández, Lanier, & Weyl, 2018; Posner & Weyl, 2018; Zhu, 2019). In a fully decentralized governance structure, in contrast, platform participants collectively enjoy full governance control, allowing them to represent their perspectives and leverage their local information through platform governance (Ostrom, 1990). Distributing governance power too widely, however, can also reduce the likelihood of collective action and the speed of decision making (Hardin, 1968; Olson, 1965). Given these tradeoffs, we suggest that a moderate level of decentralization is more likely to achieve incentive compatibility, improve informational efficiency, and help ensure desirable governance outcomes.

Our mechanism design perspective builds on and extends extant research on platform governance. Platform governance research focuses on the structuring of decision-making authority and control rights to ensure effective value creation and fair value distribution (e.g., Tiwana, Konsynski, & Bush, 2010). A key aspect of governance is the degree of decentralization (Bresnahan & Greenstein, 2014; Sambamurthy & Zmud, 1999; Xue, Ray, & Gu, 2011), which refers to the extent to which governance rights and control are shared between platform owners and platform participants (e.g., Bardhan, 2002; Faguet, 2014; Walch, 2019). In sharing governance control with platform participants, platform owners are more likely to credibly commit to the pursuit of overall welfare rather than their own interests, mitigating concerns over power imbalances in digital platforms. In extreme forms of decentralization, there may be no platform owners, and platform participants collectively enjoy full governance control. Existing research on platform governance, however, often focuses on centralized governance while paying less attention to decentralized governance (Boudreau, 2010; Kyprianou, 2018; Reischauer & Mair, 2018; Rietveld et al., 2019; Wareham et al., 2014). Given the growing complexity and shared responsibilities associated with governing digital platforms (Stigler Committee on Digital Platforms, 2019), it is essential to investigate decentralized governance and its implications for the future of the platform economy. In this study, therefore, we focus on examining the characteristics, consequences, and antecedents of decentralized governance.

However, it is often challenging to study alternative governance structures either because most digital platforms tend to have similar centralized governance structures or because different platforms in different domains may be too heterogeneous to be comparable. The rise of blockchain platforms offers a unique opportunity to examine alternative governance structures. Blockchain platforms are part of a vibrant ecology that is generally built from the same foundational technology, blockchain technology, allowing for meaningful comparisons across platforms. Moreover, different platforms have experimented with drastically different governance structures, and they therefore provide sufficient variation for examining the efficacy of alternative governance structures (e.g., Beck, Müller-Bloch, & King, 2018; De Filippi & Loveluck, 2016; Hsieh, Vergne, & Wang, 2018; Schmeiss, Hoelzle, & Tech, 2019). For instance, Ripple is a blockchain-based cross-border payment platform with a relatively centralized governance structure, in which its sponsoring company—Ripple—controls the project and sponsors major developments. Through centralized governance, Ripple can benefit from clear leadership, but it may also marginalize and alienate other stakeholders. Ripple has often been criticized for its centralization (Armknecht, Karame, Mandal, Youssef, & Zenner, 2015). In contrast, Bitcoin exemplifies the quest for pure decentralization, from which no single entity enjoys substantial governance control (Böhme, Christin, Edelman, & Moore, 2015; Nakamoto, 2008). The problem, however, is that its key stakeholders often fail to reach agreements, leading to one deadlock after another (De Filippi & Loveluck, 2016).

For our empirical analyses, we collect two waves of data from CoinCheckup.com and derive three primary sets of findings. First, we find that the degree of decentralization has an inverted U-shaped relationship with platforms’ market capitalization such that the midrange of decentralization is more likely to be associated with higher levels of market performance. Second, we examine additional indicators of platform performance—developer attention, development activity, and social media followers—and find that they all have an inverted U-shaped relationship with the degree of decentralization. Third, we examine antecedents to platforms’ governance structures and find that platforms of the infrastructure layer—relative to those of the application layer—tend to be more decentralized. We further find that experienced leaders can help platforms of the infrastructure layer offset the tendency to become overly decentralized and bring decentralization to more performance-enhancing levels.

Overall, this study contributes new insights to platform governance and especially to the benefits and limits of centralized and decentralized governance. First, it recognizes the tradeoffs between centralization and decentralization and identifies semi-decentralization as an effective structure for achieving shared governance (see also Fan & Zietsma, 2017; Ostrom, 2010). It extends existing studies on centralized governance and suggests that platform owners may benefit from giving up some governance control to platform participants (see also Hippel & Krogh, 2003). It also cautions existing studies on increasingly decentralized governance and suggests that decentralized platforms may benefit from concentrating some governance control among key individuals or organizations (see also O’Mahony & Ferraro, 2007). Second, this study contributes to an understanding of the origins of high-performing governance structures. It suggests that design constraints and strategic leadership can interact to determine the structure of platform governance (Dattée, Alexy, & Autio, 2018). In particular, it highlights the roles of experienced leaders in steering digital platforms to adopt high-performing governance structures (see also Daily, McDougall, Covin, & Dalton, 2002). Third, this study identifies the need to examine platform governance not just from the perspective of platform owners but also from the perspectives of other stakeholders (see also Arrieta-Ibarra et al., 2018). It also illustrates the potential usefulness of mechanism design theory in identifying the key characteristics of high-performing governance structures (Hurwicz & Reiter, 2006). Overall, we believe that this study contributes novel insights on the shared governance of digital platforms and especially on the benefits and limits of decentralized governance, an emerging mode of platform governance in the digital economy.

Theory and Hypotheses

Platform Governance

Digital platforms often require contributions from various actors with diverse perspectives and goals (Darking, Whitley, & Dini, 2008; Jacobides, Cennamo, & Gawer, 2018; Nambisan, 2017). For instance, a digital platform may need its platform owners to manage its core technology and governance systems, third-party developers to build innovative applications on top of its core technology, and end-users to utilize its core and complementary services. However, governing a diverse set of actors to pursue activities and outcomes that are acceptable to all can be especially challenging (Ostrom, 1990; Simcoe, 2014). Through the structuring of decision-making authority and control rights, effective platform governance can help align incentives, coordinate actions, mitigate conflicts, and foster a common identity and thus can be critical to platform performance (Di Tullio & Staples, 2013; Gawer & Phillips, 2013; Kyprianou, 2018; Reischauer & Mair, 2018; Tiwana et al., 2010; Wareham et al., 2014).

To help identify the nature and characteristics of effective platform governance, we draw on mechanism design theory to evaluate alternative governance structures. Mechanism design theory takes a design perspective and can thus be especially valuable in the search for high-performing governance structures (Mookherjee, 2006). It recognizes the roles of incentives and informational constraints in platform governance and emphasizes the importance of achieving incentive compatibility and informational efficiency (Hurwicz, 2008; Hurwicz & Reiter, 2006; Maskin, 2008; Mookherjee, 2006; Myerson, 2008). A governance structure is incentive compatible when it enables stakeholders to realize their own interests and preferred outcomes while achieving overall platform objectives. A governance structure is informationally efficient when it economizes on the costs of gathering, communicating, and leveraging local information. With higher levels of incentive compatibility and informational efficiency, a digital platform can leverage individual incentives and local information to achieve effective governance processes and outcomes, potentially enhancing platform performance (Hurwicz & Reiter, 2006; Maskin, 2015; McFadden, 2009).

Drawing on mechanism design theory, we further identify platform layers and experienced leaders as potential antecedents of governance structures. Digital platforms at different layers often face different incentives and informational constraints, which may lead to the adoption of specific governance structures to improve incentive compatibility and informational efficiency (Hurwicz & Reiter, 2006; Mookherjee, 2006). In addition, experienced leaders can shape governance structures. They can become mechanism designers and steer digital platforms to adopt high-performing governance structures.

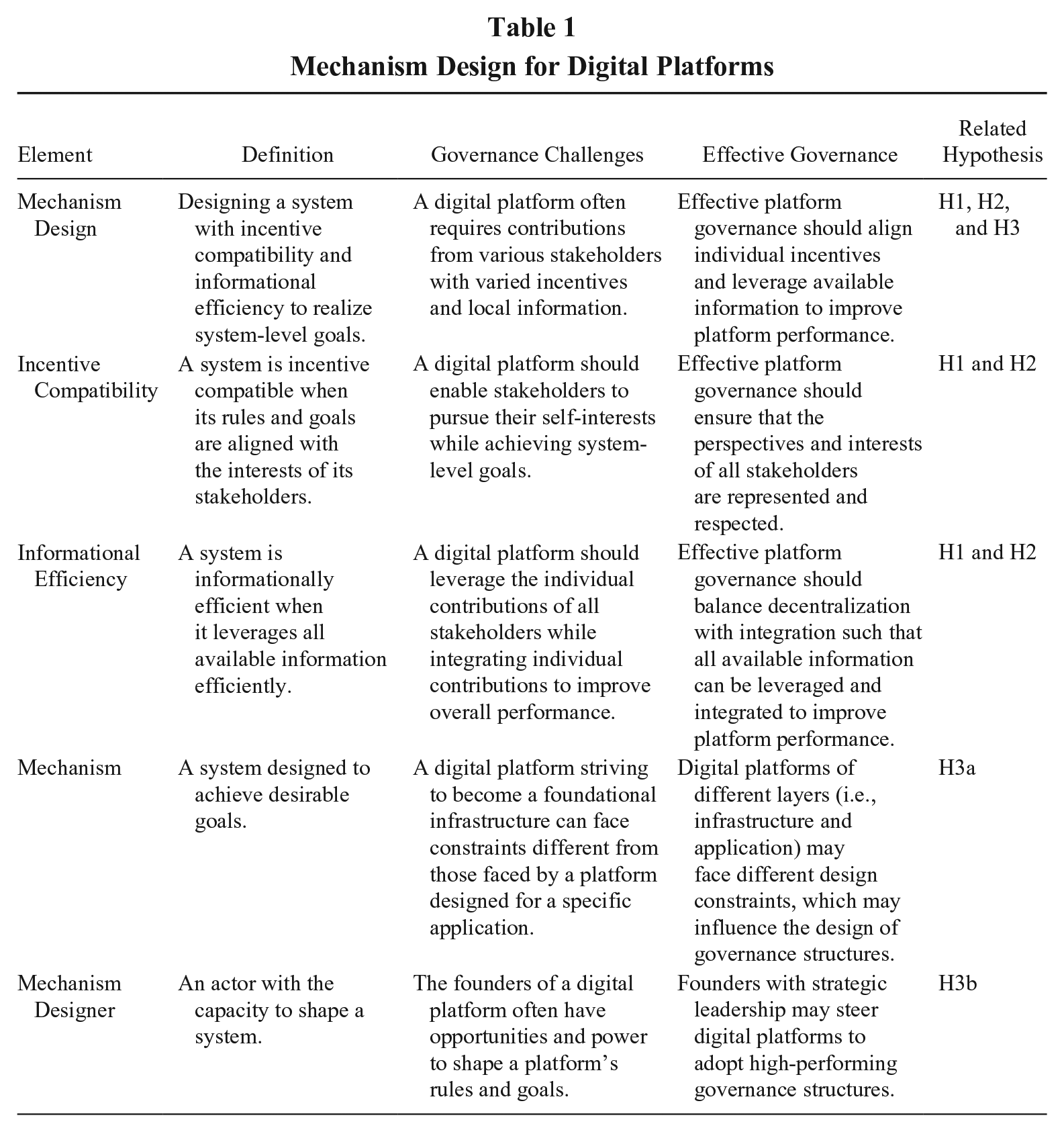

Furthermore, mechanism design theory recognizes the importance of ensuring outcomes desired not just by platform owners but also by other stakeholders (Maskin, 2008), pointing to potential concerns over the rising power of platform owners (Hurwicz, 2008) and the declining power of other stakeholders in platform ecosystems (Arrieta-Ibarra et al., 2018). 1 Therefore, following mechanism design theory, we focus on identifying governance structures that can help improve the overall welfare of all stakeholders in platform ecosystems. Overall, mechanism design theory offers a new perspective through which to understand the characteristics, antecedents, and consequences of alternative governance structures. Table 1 lists the key elements of mechanism design and their relationships to our hypotheses.

Mechanism Design for Digital Platforms

Decentralized Governance and Platform Performance

According to mechanism design theory, effective governance structures cater to the incentives and interests of key stakeholders and leverage available information to ensure effective governance processes and outcomes (Hurwicz & Reiter, 2006; Mookherjee, 2006). With higher incentive compatibility and informational efficiency, digital platforms are more likely to provide stronger incentives for key stakeholders to join their ecosystems and to leverage local information to improve platform ecosystems, potentially enhancing network effects and platform performance (Di Tullio & Staples, 2013; Jacobides et al., 2018). Since market capitalization is a comprehensive, forward-looking measure of platform performance, we expect digital platforms with more effective platform governance to exhibit higher levels of market capitalization (see also Bebchuk, Cohen, & Ferrell, 2008; Gompers, Ishii, & Metrick, 2003). 2

Some digital platforms adopt more centralized governance structures, from which platform owners take control of platform governance. With concentrated governance rights and control, platform owners can make decisions more quickly and take more decisive actions to ensure effective governance processes and outcomes. Without sufficient checks and balances, however, platform owners may at times act in their own interests rather than in the best interests of all stakeholders (Hurwicz, 2008; Mookherjee, 2006; Rahman, 2012). From time to time, platform owners have indeed abused their power and taken actions that have hurt users and third-party businesses (Cohen, 2019; Srnicek, 2017; Van Dijck et al., 2018; Zuboff, 2019). When platform owners act opportunistically at the expense of others, platform participants may become disenchanted. They may refrain from contributing to platforms or defect to other alternatives (Arrieta-Ibarra et al., 2018; Posner & Weyl, 2018), potentially hurting platform performance, especially over the longer term.

Through decentralization, digital platforms can enhance the power of platform participants while reducing that of platform owners. With decentralization, digital platforms can create a structure through which platform participants can influence, monitor, and engage with platform owners (Cheibub, Gandhi, & Vreeland, 2010; Hurwicz, 2008), motivating platform owners to pursue activities and outcomes that may be more acceptable to all. Through decentralized governance, furthermore, platform participants can take part in goal setting and decision making, allowing them to represent their perspectives and protect their interests. As a result, digital platforms are more likely to incorporate their perspectives and interests into platform design and governance. With decentralized governance, digital platforms are more likely to maximize the overall welfare of all participants rather than the residual profits of platform owners, potentially enhancing incentive compatibility. Furthermore, platform participants can leverage local information, knowledge, and initiative to help improve the informational efficiency of governance processes (Ostrom, 1990, 2000, 2010). Overall, we suggest that decentralized governance may increase incentive compatibility and informational efficiency, enabling digital platforms to improve their governance processes and overall platform performance (Hurwicz & Reiter, 2006).

Although some degree of decentralization is generally beneficial, an overly decentralized governance structure—like an overly centralized one—can also be counterproductive. In extreme forms of decentralization, there may be no platform owners, and platform governance is achieved through collective community efforts. When governance rights are broadly distributed, however, individual participants may have little power to shape governance outcomes and may thus become less engaged in governance processes (Ostrom, 1990). Overly dispersed governance rights, therefore, may fail to mobilize collective actions to ensure effective platform governance (Hardin, 1968; Olson, 1965). Another problem with over-decentralization concerns the fact that consensus can become too difficult to achieve, as platform participants may hold vastly diverse perspectives and interests (De Filippi & Loveluck, 2016; Eisenhardt, 1989; Wareham et al., 2014). Platform participants may not be able to reach consensus on issues regarding platform governance and evolution, resulting in fragmentation and deadlocks that may hurt all parties (De Filippi & Loveluck, 2016; Wareham et al., 2014). For instance, Kyprianou (2018) offers some case evidence suggesting that when given complete freedom, platform participants may sometimes engage in improper activities that may diminish the value of platform ecosystems.

Given the merits and limits of both centralization and decentralization, we hypothesize that semi-decentralization is more likely to be associated with superior platform performance. A semi-decentralized governance structure is characterized by giving community members freedom and rights to participate in platform governance while having some key organizations or individuals sponsor and shape platform governance. When digital platforms make governance open to all, community members can represent their interests and leverage their local information through governance processes. When digital platforms give some organizations or individuals more governance control while restraining their power through decentralization, these key parties can help ensure effective governance processes and outcomes. For instance, they can be helpful in co-developing community boundaries, influencing social relations, and steering actions (Reischauer & Mair, 2018). With key parties ensuring effective governance, digital platforms do not need to depend solely on the ad hoc participation and contributions of community members. In difficult and contentious situations, they may be less likely to reach deadlocks, as key organizations and individuals can take control of governance processes to overcome impasses while maintaining checks and balances through decentralization (Eisenhardt, 1989; Faraj, Kudaravalli, & Wasko, 2015; Fleming & Waguespack, 2007; O’Mahony & Ferraro, 2007). With semi-decentralization, digital platforms can create a healthier structure for incorporating variegated perspectives and available information to achieve shared governance (Fan & Zietsma, 2017; Ostrom, 2010).

In sum, we hypothesize that a semi-decentralized governance structure allows digital platforms to strike a better balance between centralization and decentralization and thus is more likely to be associated with superior platform performance. As a result, we expect the degree of decentralization to have an inverted U-shaped relationship with platform performance. We therefore propose the following hypothesis:

Hypothesis 1: There is an inverted U-shaped relationship between decentralization and a digital platform’s market performance.

Decentralization and Developers

From the perspective of platform owners, semi-decentralization enhances market performance and is thus beneficial. However, mechanism design theory focuses on attaining outcomes that are not just desired by platform owners but also preferred by other platform participants, pointing to the need to look beyond platform owners (Hurwicz & Reiter, 2006; Maskin, 2015). Nevertheless, most studies on platform governance take the perspectives of platform owners and focus on identifying governance mechanisms that can help platform owners achieve their goals (e.g., Boudreau, 2010; Kyprianou, 2018; Reischauer & Mair, 2018; Rietveld et al., 2019; Tiwana et al., 2010; Wareham et al., 2014) while paying less attention to other stakeholders (see also Jacobides et al., 2018). If we start to consider the perspectives of other stakeholders, we may need to examine their respective welfare. Given the importance of developers to early-stage platform ecosystems, we consider the perspective of developers as an initial step (Boudreau, 2012; Parker & Alstyne, 2018; Wareham et al., 2014). In particular, we focus on examining whether decentralized governance can help attract developer attention and facilitate development activity.

Developers—both internal and external—often contribute greatly to platform development and performance. Developers can help digital platforms improve their core and complementary technologies, allowing digital platforms to sustain technological leadership, create network effects, and attract more developers (Clements & Ohashi, 2005; Gawer & Cusumano, 2014; Gupta, Jain, & Sawhney, 1999; Subramaniam, Sen, & Nelson, 2009). However, developers—especially external ones—may not enjoy sufficient rights and control over platform governance and often have limited opportunities and means to shape platform governance (Adler, 2001; O’Mahony & Ferraro, 2007). With limited to no governance rights, external developers are often at the mercy of platform owners and may not be able to fully protect their rights and interests on digital platforms. In contrast, platform owners often enjoy centralized governance control and can direct digital platforms to pursue actions to advance their own interests even when such actions are not in the best interests of external third-party developers. For instance, Facebook, LinkedIn, and Twitter have arbitrarily shut down many of their application programming interfaces (APIs) to advance their own objectives without consulting third-party developers building applications on top of these APIs.

Third-party developers and businesses are highly dependent on their hosting platforms. External developers can engage with a digital platform in multiple ways such as by following a platform’s technical development, making technical suggestions and contributions, or building applications on top of the platform (Boudreau, 2012; Hertel, Niedner, & Herrmann, 2003). Before engaging with a digital platform, external developers often want to be assured that their contributions will be taken seriously and that their access to the platform cannot be easily cut off by the platform owner (Dixon, 2018). In deciding whether to join a platform ecosystem, they often consider the platform’s governance structure. They are more likely to attend to and engage with a digital platform with an effective governance structure.

By promoting effective shared governance, semi-decentralized governance structures can help align incentives, coordinate actions, mitigate conflicts, and foster a common identity (Di Tullio & Staples, 2013; Dixit, 2009; Gawer & Phillips, 2013; Wareham et al., 2014; Williamson, 2005). A digital platform with a semi-decentralized governance structure is more likely to achieve incentive compatibility such that developers can be assured that their rights, interests, and contributions will be protected on the platform ecosystem. Moreover, a platform with a semi-decentralized governance structure is more likely to achieve informational efficiency, as it can leverage the creativity and initiative of developers and coordination and integration provided by some central parties. By promoting shared governance, such a platform can ensure fair and effective governance processes so as to foster collective action, resolve coordination problems, and promote fairness and excellence (Di Tullio & Staples, 2013; Markus, 2007; Ostrom, 2000). Overall, we suggest that semi-decentralization can help promote shared governance and thus help digital platforms attract external third-party developers.

Similarly, we suggest that semi-decentralized governance structures may facilitate rapid technical development. Most blockchain-based platforms rely on open-sourcing as a primary mode of development, and they try to attract developers from open-source communities to contribute to their continued development (Antonopoulos, 2017; Antonopoulos & Wood, 2019; Narayanan, Bonneau, Felten, Miller, & Goldfeder, 2016). Often, developers contribute to the technical development of a digital platform by pushing commits to its open-source repositories (Narayanan et al., 2016). In open-source repositories, a commit is a bundle of proposed changes to open-source code, and the number of commits serves as one of the most important indicators of a platform’s development activity (Grewal, Lilien, & Mallapragada, 2006; Stewart, Ammeter, & Maruping, 2006).

We expect semi-decentralized governance structures to help balance flexibility with control in facilitating development activities (Almirall & Casadesus-Masanell, 2010; Song & Chen, 2014; Tilson, Lyytinen, & Sørensen, 2010; Wareham et al., 2014). When a digital platform is too centralized, it may have clear goals and coordination, but it may fail to tap into the freedom and creativity of the broader developer community. When a digital platform is fully decentralized, developers often self-select to work on problems of their own choosing on an ad hoc basis, allowing developers to enjoy complete freedom and flexibility. However, unplanned and uncoordinated development activities can become too random and less predictable, and developers may then fail to undertake or coordinate activities to achieve overall platform objectives (Felin & Zenger, 2014). In contrast, digital platforms characterized by semi-decentralization are more likely to balance decentralization with centralization and flexibility with control. They may be better able to leverage the local creativity and contributions of individual developers and the global coordination and integration provided by central parties. For instance, Wareham et al. (2014) offer some case evidence of the importance of balancing the decentralization of decision-making authority to individual developers through creative freedom with the centralization of some governance control through training and certification by platform owners.

Overall, we suggest that digital platforms that are moderately decentralized are more likely to promote effective shared governance and thus may be more likely to attract developer attention and engagement. Moreover, such platforms are more likely to balance control with flexibility to facilitate platform development and may thus enjoy more development activity. We therefore propose the following hypothesis:

Hypothesis 2: Decentralization has an inverted U-shaped relationship with (a) a digital platform’s developer attention and with (b) development activity.

From the perspective of platform owners, it is also essential to encourage external developers to join their ecosystems and undertake technical activities to improve core and complementary technologies (Parker & Alstyne, 2005, 2018; Parker, Van Alstyne, & Jiang, 2017). Developer attention and development activity are often considered to be “a leading indicator of where future value will be created and captured” (Shen, Spencer, Garg, & Deeter, 2019). Therefore, we also expect developer attention and development activity to be associated with platforms’ market performance.

Platforms, Leaders, and Decentralization

If semi-decentralized governance structures are associated with superior platform performance, then why would all digital platforms not adopt such governance structures? To answer this question, we draw on mechanism design theory to suggest that design constraints and mechanism designers may influence the adoption of governance structures (Hurwicz & Reiter, 2006; Mookherjee, 2006). We first suggest that digital platforms of the infrastructure layer have a tendency to become overly decentralized. We then examine the roles of strategic leadership in offsetting this tendency to bring decentralization to more performance-enhancing levels.

We suggest that digital platforms at different layers may face different design constraints, which may influence the design of governance structures (see also Constantinides et al., 2018; Dattée et al., 2018; de Reuver, Sørensen, & Basole, 2018). The Internet, for instance, is a foundational platform of the infrastructure layer, and it is governed in a relatively decentralized manner (Cerf, 2012; Johnson, Crawford, & Palfrey Jr., 2004). In contrast, platforms built on top of the Internet infrastructure such as Uber and Twitter tend to be much more centralized. In the blockchain industry, similarly, platforms that are building decentralized infrastructures tend to be more decentralized while those with more specific applications tend to be more centralized (Chen & Bellavitis, 2020). For instance, Ethereum is a blockchain infrastructure with a relatively decentralized governance structure (Antonopoulos & Wood, 2019). In contrast, Basic Attention Token is an Ethereum-based application-specific platform with a relatively centralized governance structure. 3

We suggest that digital platforms of the infrastructure layer tend to be more decentralized than those of the application layer (see also Simcoe, 2014). Digital platforms of the infrastructure layer provide the common foundations for various platforms with diverse applications (Tilson et al., 2010). They feature characteristics of public goods, requiring them to be more open and neutral to all parties to generate maximal social welfare and network effects (Simcoe, 2014). They also tend to be more generative (Dattée et al., 2018; Yoo, Henfridsson, & Lyytinen, 2010) and can benefit from permissionless innovations (Cerf, 2012) that may come from distant and unexpected contributors (Afuah & Tucci, 2012). Furthermore, they are often too important to be controlled by any single entity, driving them to become more decentralized and democratic (Davidson, De Filippi, & Potts, 2018). When they are overly centralized, their platform owners can enjoy too much power to influence too many actors and activities, potentially leading to unintended systemic problems (Cheibub et al., 2010). Decentralization can help reduce power imbalances and restore a balance of power on digital platforms (Dixon, 2018). As stakeholders demand to take part in platform governance to ensure fair processes and outcomes, digital platforms of the infrastructure layer tend to become more decentralized.

In contrast, digital platforms of the application layer are more likely to be more centralized. Digital platforms of the application layer are often designed to serve more specific stakeholders with more specialized goals. They are less likely to create systemic problems, allowing their platform owners to negotiate for more governance rights and control (Cohen, 2017). Moreover, they often have more well-defined value propositions, and thus platform owners may want to retain more control over the evolution of their platform ecosystems (Dattée et al., 2018). Furthermore, platform owners are more likely to have specialized knowledge and capacities to exert effective governance control. As a result, digital platforms of the application layer tend to be less open and less decentralized. 4

In sum, we suggest that digital platforms of the infrastructure layer tend to be more decentralized than those of the application layer. We therefore propose the following hypothesis:

Hypothesis 3a: Digital platforms of the infrastructure layer tend to be more decentralized than those of the application layer.

Although digital platforms of the infrastructure layer have a tendency to become more decentralized or even overly decentralized, some manage to balance decentralization with centralization to achieve a more balanced governance structure. We suggest that strong strategic leadership can play an important role in shaping platforms’ governance structures and that strong leaders can steer digital platforms—especially those of the infrastructure layer—to adopt high-performing governance structures (Lee & Cole, 2003; Mockus, Fielding, & Herbsleb, 2002; O’Mahony & Ferraro, 2007; Ostrom, 2000). First, community members may value the leadership of experienced leaders, especially in “difficult or ambiguous situations” (O’Mahony & Ferraro, 2007: 1090), such that strong leaders can enjoy more governance rights. In particular, community members may value leaders with technical and organizational contributions, allowing them to have more governance control (Faraj et al., 2015; Fleming & Waguespack, 2007; O’Mahony & Ferraro, 2007). Second, experienced leaders are more likely to have the power and skills to lead user and developer communities. Governing digital platforms of the infrastructure layer can be especially challenging given the various demands of their broad and diverse stakeholders (O’Mahony & Ferraro, 2007). Leaders with strong managerial and technical experience are more likely to enjoy formal and informal power (French & Raven, 1959) to help them lead their communities. Third, experienced leaders are more likely to understand their roles and opportunities in shaping governance structures (Kwee, Van Den Bosch, & Volberda, 2011). Given the early-stage nature of most blockchain-based platforms, strong leaders can have substantial discretion in the design of governance structures (Daily et al., 2002). When leaders recognize the value of semi-decentralized governance structures, they can steer their platforms to adopt such governance structures.

In sum, we suggest that experienced leaders can help offset the tendency for digital platforms of the infrastructure layer to become overly decentralized. Such leaders may help bring decentralization to more performance-enhancing levels. We therefore propose the following hypothesis:

Hypothesis 3b: More experienced leaders can offset the tendency for digital platforms of the infrastructure layer to become overly decentralized.

Method

Data and Sample

To test the proposed hypotheses, we draw data from CoinCheckup.com, an online cryptocurrency portal that tracks most of the blockchain-based platforms publicly traded on cryptocurrency exchanges. As one of the largest sites tracking blockchain-based platforms, CoinCheckup.com aggregates diverse sources of data on a single site. It collects comprehensive information, including data on market performance (e.g., price and circulating supply), platform characteristics (e.g., governance, status, and age), and community backing (e.g., GitHub and social media activities), among others.

We obtained a private API through a data access agreement with CoinCheckup.com and collected data over two major waves. We collected the first wave of data on October 10, 2018 and the second wave on March 1, 2019. Throughout the study, we measured market capitalization using data from the second wave while measuring all other variables using data from the first wave. After merging the two sets of data and excluding observations with missing values, we obtained a final sample of 782 observations with complete data for our analyses.

Measures

Market capitalization

We measure platform performance using the natural log of market capitalization, which is operationalized as the unit price in U.S. dollars multiplied by the circulating supply. Market capitalization is an important indicator of platform performance, and key stakeholders often pay particular attention to it (Burniske & Tatar, 2018). Blockchain-based platforms are unique in that they often have platform-specific tokens. As a result, each platform is usually associated with a market capitalization, allowing one to directly assess the market value of each platform (Chen, 2018; Howell, Niessner, & Yermack, 2019). Without platform-specific tokens, in contrast, one often cannot evaluate the market value of a specific platform even when it is fully owned by a public company, as the market capitalization of a public company is often tied to a number of platforms and products that the company owns (Richard, Devinney, Yip, & Johnson, 2009: 731).

Nevertheless, there may still be two concerns with using market capitalization as a measure of platform performance. The first concern relates to the fact that market capitalization can be influenced by the boom and bust cycle that affects all platforms. Within the blockchain industry, Bitcoin and Ethereum are the dominant platforms, and the market value of most platforms fluctuates with Ether (i.e., the native currency of the Ethereum blockchain) and Bitcoin prices (see also Fisch, 2019). To partial out the effect of market cycles, we also measure market capitalization in Ether and Bitcoin terms. The second concern relates to the fact that market capitalization may not reflect platform performance from the perspectives of other stakeholders. 5 To further address this concern, we examine other indicators of platform performance, including developer attention, development activity, and social media followers.

Decentralization

Decentralization refers to the extent to which power and control in governance structures and decisions are allocated to developers and community members (e.g., Bardhan, 2002; Chen & Bellavitis, 2020; Faguet, 2014; Lee & Edmondson, 2017; Walch, 2019). We assign each platform a decentralization score based on data collected from CoinCheckup.com. While these data are primarily compiled by CoinCheckup.com, CoinCheckup.com encourages others to make corrections to its compilation to potentially leverage the wisdom of the crowd to increase the accuracy of its data. In addition, as CoinCheckup.com uses governance structures as key criteria in its proprietary system for scoring blockchain projects, it has a strong incentive to ensure the accuracy of its data. 6 A platform’s decentralization score is equal to 1 when a platform is defined as Centralized-Hierarchical by CoinCheckup.com—that is, it is sponsored and controlled by a company with a hierarchical decision structure or a hierarchical organization model. A platform’s score is equal to 2 when it is defined as Centralized-Flat by CoinCheckup.com—that is, it is sponsored and controlled by a company with a flat decision structure or a flat organization model. A score of 3 is assigned to a platform defined as Semi-Centralized by CoinCheckup.com. Such a platform is mainly driven by its community but may be backed by key organizations or individuals. A score of 4 is assigned to a platform defined as Decentralized by CoinCheckup.com—that is, it is run completely by its community. Under this mode, power and control are fully decentralized, decisions are reached through consensus, and the community grows organically.

Developer attention

We measure developer attention using the natural log of the total number of GitHub stars, watchers, and forks that a project receives from developers. On GitHub, developers can star a project to “manifest interest or satisfaction,” and “three out of four developers consider the number of stars before using or contributing to a GitHub project” (Borges & Valente, 2018: 112). On GitHub, developers can also watch a project, and they usually do so to monitor a project’s progress. For any project, “having a large pool of watchers is important to recruiting the project’s future contributors and to the health of the project” (Sheoran, Blincoe, Kalliamvakou, Damian, & Ell, 2014: 337). On GitHub, furthermore, developers can fork a project. Through forking, developers can make copies of a project and experiment with changes without affecting the original project. In general, the number of forks is considered to be an important signal of “community interest” (Dabbish, Stuart, Tsay, & Herbsleb, 2012: 1281). By combining these three components, we can better capture the overall attention a project is receiving from developers (Ma, Chen, Zhou, & Xu, 2016).

Development activity

We measure a project’s development activity using the natural log of the number of recent GitHub commits (Grewal et al., 2006; Singh, Tan, & Mookerjee, 2011; Subramaniam et al., 2009). A commit is a bundle of proposed changes to the core technology of a platform on open source repositories, and the number of commits is one of the most important indicators of a platform’s development activity (Grewal et al., 2006; Stewart et al., 2006). The number of recent GitHub commits is measured by the statistical mean of the 4-week simple moving average of commits made over 49 weeks. It is critical to focus on recent commits rather than total commits, as the former better reflect recent development activity.

Social media followers

We include the natural log of the total number of social media followers across Facebook, Twitter, YouTube, and Reddit. In the blockchain industry, most projects release updates through social media. To keep up with new developments, potential developers, users, and investors often follow projects through social media (Fisch, 2019; Mai, Shan, Bai, Wang, & Chiang, 2018). As a result, the number of social media followers is an important indicator of a project’s popularity, engagement, and influence (Hoffman & Fodor, 2010; Lee, Oh, & Kim, 2013). In general, the more social media followers a project has, the more network effects it is generating, potentially contributing to the project’s market value.

Infrastructure layer

A platform of the infrastructure layer aims to become the common infrastructure for a wide variety of applications while a platform of the application layer tends to serve a more narrowly defined application domain (see also Constantinides et al., 2018; Dattée et al., 2018; de Reuver et al., 2018). In the blockchain industry, platforms of the infrastructure layer often have their own independent blockchains, and they often issue native coins on their blockchains (Antonopoulos, 2017; Antonopoulos & Wood, 2019). In contrast, platforms of the application layer often build on existing blockchains, and they often issue tokens on top of existing blockchains (Chen, 2018). Accordingly, we consider platforms with coins as platforms of the infrastructure layer and those with tokens as platforms of the application layer. Regardless of whether a platform is of the infrastructure or application layer, it often allows third parties to build applications on top of it (Chen & Bellavitis, 2020).

Leader experience

A blockchain-based platform may have key leaders who make major organizational and technical contributions. We measure leader experience by an index of project leaders’ managerial and technical experience. We consider both managerial and technical experience, as project leaders’ organizational and technical contributions have been shown to greatly affect the development and evolution of a project (Faraj et al., 2015; Fleming & Waguespack, 2007; O’Mahony & Ferraro, 2007). Managerial experience is defined as the total number of years that a key project leader has been a top manager while technical experience is defined as the total number of years over which a key technical leader has served as a top technology manager (Hambrick & Mason, 1984). 7 We conducted a principal component analysis of these two indicators and used the first factor as our index of leader experience; the first factor explains 78.95 percent of the total variance (see also Custódio, Ferreira, & Matos, 2013).

Fully working product

Since most blockchain-based platforms are still in their early stages, some have a fully working product while others may only have a working prototype. Compared with those without a fully working product (coded as 0), those with one (coded as 1) are more likely to exhibit better market performance and to attract more developers and social media followers (Comino, Manenti, & Parisi, 2007; Subramaniam et al., 2009).

Platform age

Platform age may be associated with platform performance, as time may allow digital platforms to improve their technologies and build network effects (Cennamo & Santalo, 2013). Age is the natural log of the number of months between the first release date and the end of 2018 (Grewal et al., 2006). The first release date is the date on which the first version of a platform is made available to the public.

Number of exchanges

Unlike a public company, which is usually traded on one exchange, a blockchain-based platform is often traded on multiple cryptocurrency exchanges. The number of cryptocurrency exchanges on which a platform is traded affects a platform’s liquidity and access, which may be associated with market performance (Amihud, 2002; O’Hara, 2003).

Results

Descriptive Statistics

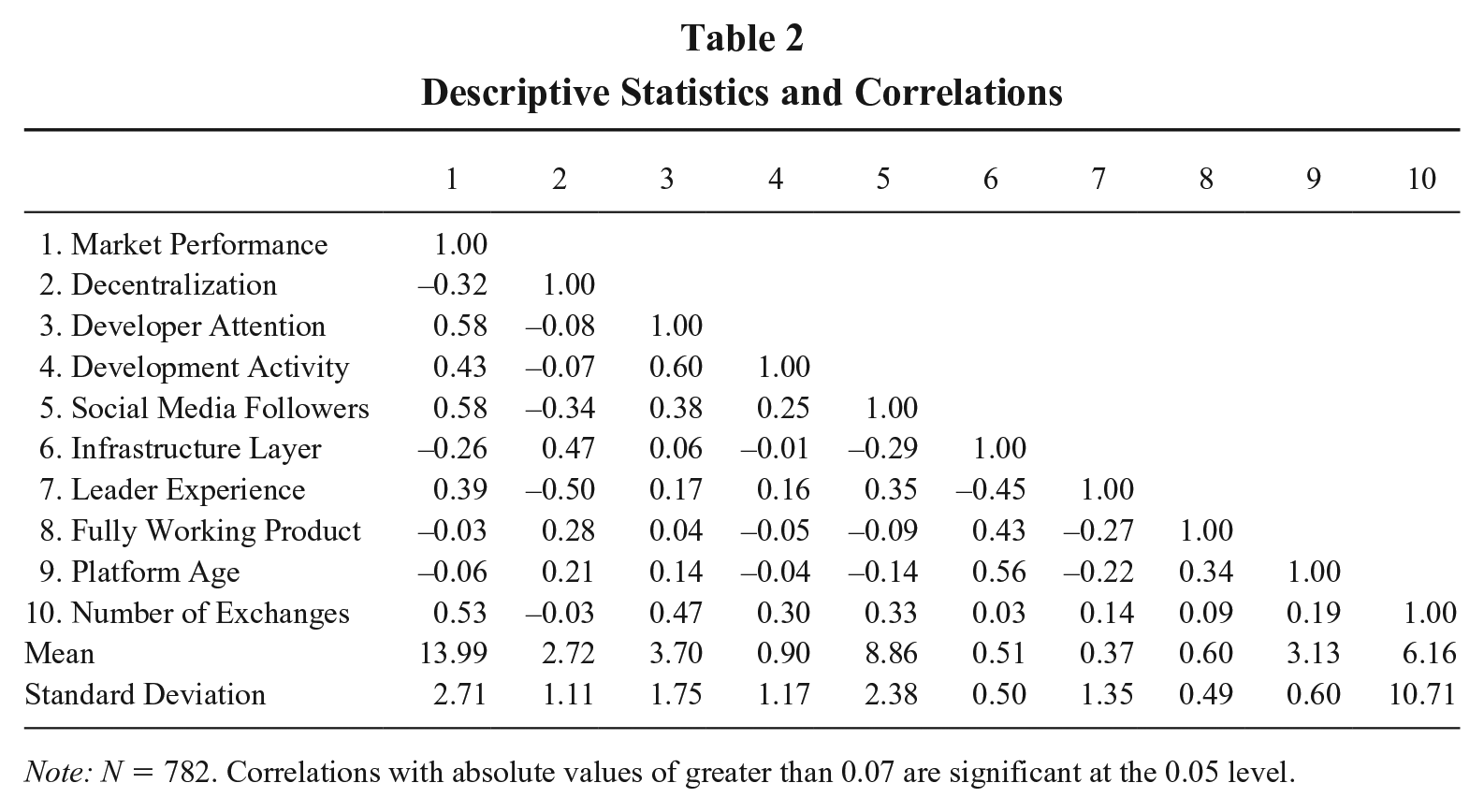

Table 2 shows the descriptive statistics and correlations. According to Table 2, platform performance as measured by market capitalization is negatively correlated with decentralization (r = −0.32, p = 0.000) and positively correlated with developer attention (r = 0.58, p = 0.000), development activity (r = 0.43, p = 0.000), and social media followers (r = 0.58, p = 0.000). Furthermore, Table 2 shows that decentralization is positively correlated with the infrastructure layer (r = 0.47, p = 0.000) and negatively correlated with leader experience (r = −0.50, p = 0.000).

Descriptive Statistics and Correlations

Note: N = 782. Correlations with absolute values of greater than 0.07 are significant at the 0.05 level.

Hypothesis Testing

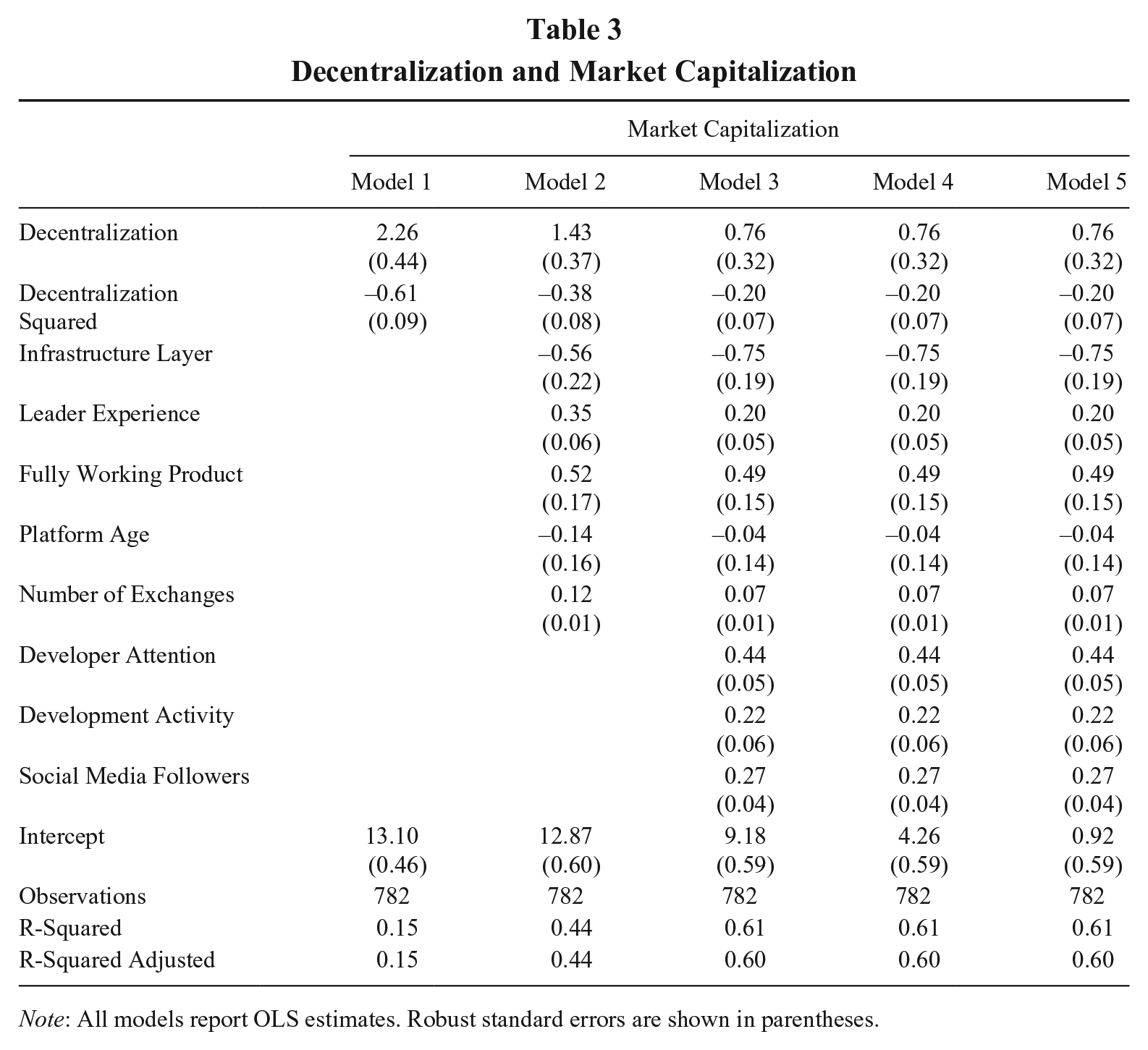

We run a series of ordinary least squares (OLS) regressions with robust standard errors to test the hypotheses. In all regressions, the measure for market performance (i.e., the log of market capitalization) is derived from the second wave of data collection while the remaining measures come from the first wave. In Model 1 of Table 3, we include decentralization and its squared term. In Model 2, we include several control variables. In Model 3, we further include developer attention, development activity, and social media followers. For the first three models, market capitalization is measured in dollar terms. In Models 4 and 5, market capitalization is measured in Ether and Bitcoin units, respectively.

Decentralization and Market Capitalization

Note: All models report OLS estimates. Robust standard errors are shown in parentheses.

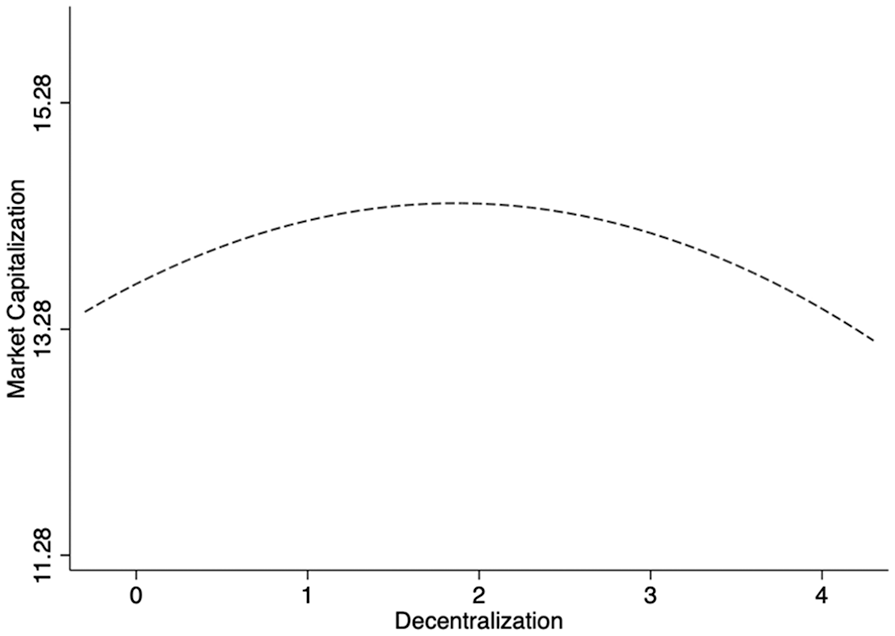

Hypothesis 1 proposes an inverted U-shaped relationship between decentralization and market capitalization. As Table 3 shows, Hypothesis 1 is consistently supported across the models. As Model 3 shows, the linear term for decentralization is positive and significant (β = 0.76, t = 0.32, p = 0.018) while the squared term is negative and significant (β = −0.20, t = 0.07, p = 0.003), confirming the inverted U-shaped relationship. We plot the relationship between decentralization and market performance in Figure 1, which further confirms the inverted U-shaped relationship. Overall, the results show that the midrange of decentralization is associated with better market performance, consistent with Hypothesis 1.

Decentralization and Market Capitalization: The Inverted U-Shaped Relationship

In the blockchain industry, market capitalization may be affected by the boom and bust cycle of the whole industry. Since Ether and Bitcoin prices can be indicators of market cycles (see also Fisch, 2019; Howell et al., 2019), we partial out the potential effects of market cycles by dividing market capitalization (in dollar terms) by the unit price of Ether and Bitcoin, respectively. Model 4 reports the results for market capitalization in Ether units, and Model 5 reports those for market capitalization in Bitcoin units. Since the dependent variable is in log form, scaling the dependent variable by either Ether or Bitcoin prices only changes the intercept without affecting the coefficients. 8 Overall, our results are robust to the use of different price measures.

Furthermore, Models 3 to 5 of Table 3 also show that market capitalization is positively associated with developer attention (β = 0.44, t = 0.05, p = 0.000), development activity (β = 0.22, t = 0.06, p = 0.000), and social media followers (β = 0.27, t = 0.04, p = 0.000). According to these results, a 1% increase in developer attention is associated with a 0.44% increase in market performance. A 1% increase in development activity is associated with a 0.22% increase in market performance. A 1% increase in the number of social media followers is associated with a 0.27% increase in market performance. We assess the differences between each pair of coefficients, and our comparisons suggest that the coefficient for developer attention is significantly greater than that for development activity (F = 5.46, p = 0.020) and greater than that for social media followers (F = 5.70, p = 0.017). Overall, developer attention, development activity, and social media followers are strongly associated with market performance—and developer attention has the strongest association. 9

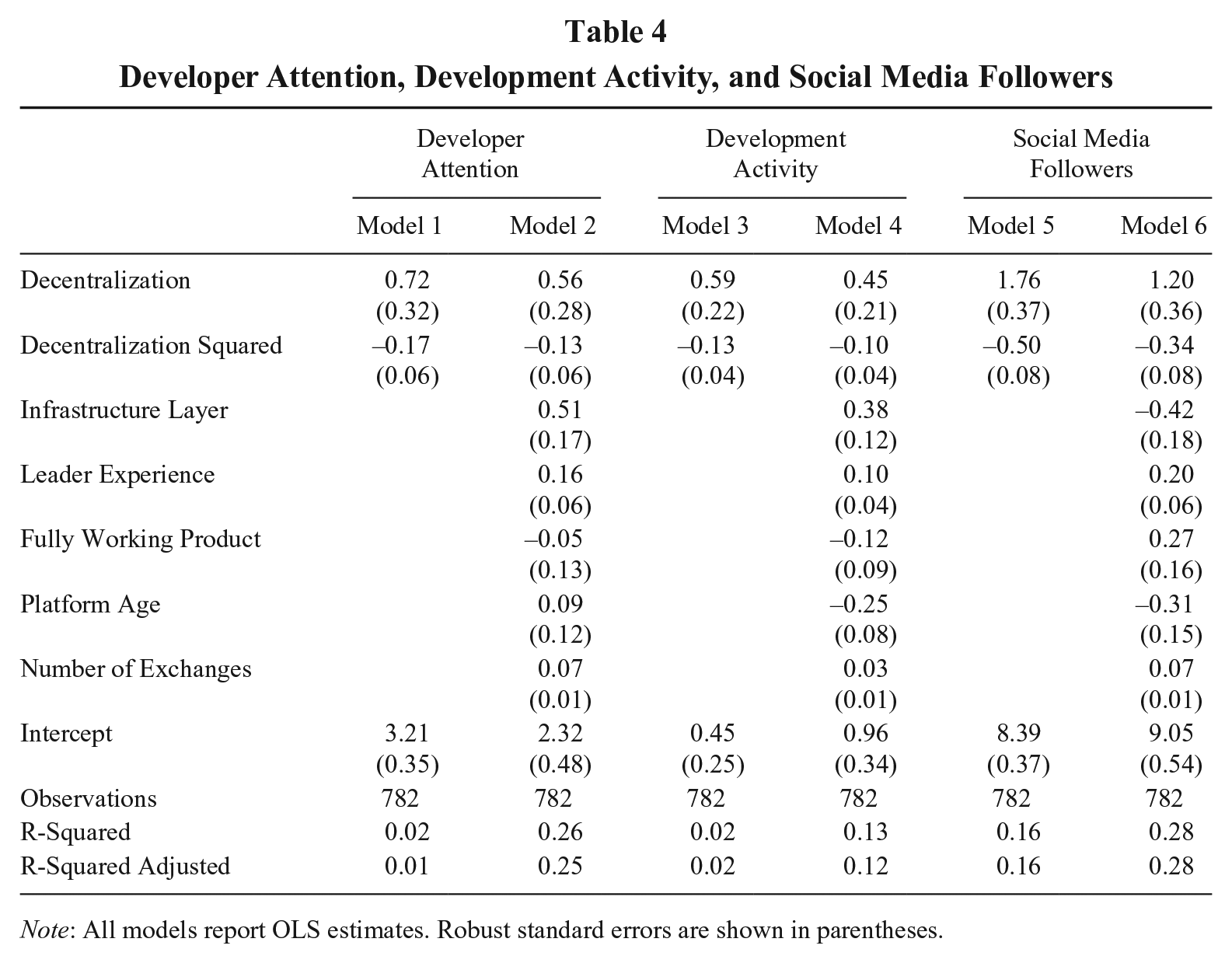

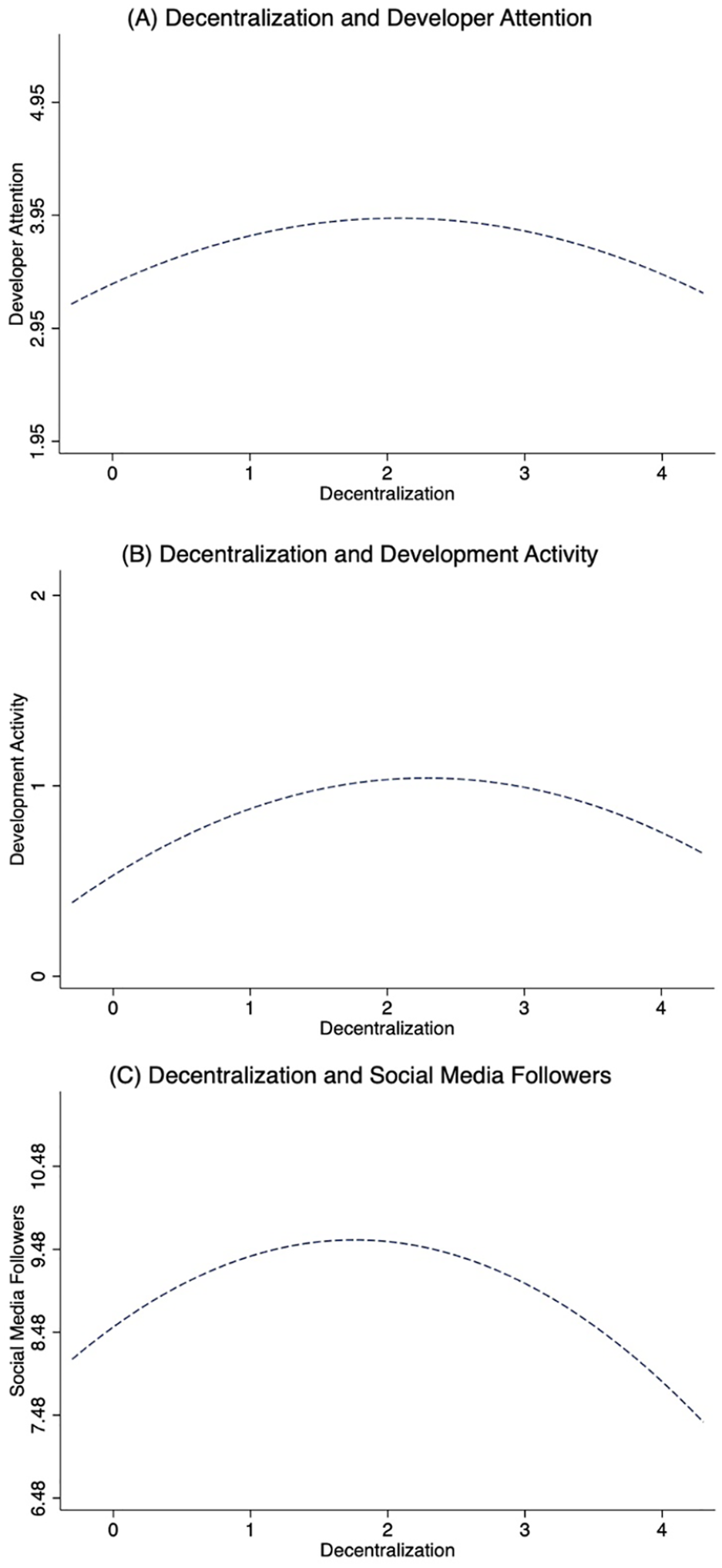

Hypothesis 2 suggests that decentralization has an inverted U-shaped relationship with (a) developer attention and (b) development activity. 10 To test Hypothesis 2, we run a series of OLS regressions with robust standard errors whereby we use developer attention and development activity as the dependent variable, respectively. The results support Hypotheses 2a and 2b. As Model 2 of Table 4 shows, there is an inverted U-shaped relationship between decentralization and developer attention, supporting Hypothesis 2a. Specifically, the linear term for decentralization is positive and significant (β = 0.56, t = 0.28, p = 0.045) while the squared term is negative and significant (β = −0.13, t = 0.06, p = 0.016), confirming the inverted U-shaped relationship. To visualize this relationship, we plot the relationship between decentralization and developer attention in Figure 2(a), further confirming the existence of an inverted U-shaped relationship.

Developer Attention, Development Activity, and Social Media Followers

Note: All models report OLS estimates. Robust standard errors are shown in parentheses.

Decentralization, Developer Attention, Development Activity, and Social Media Followers

As Model 4 of Table 4 shows, Hypothesis 2b is also supported. There is an inverted U-shaped relationship between decentralization and development activity. Specifically, the linear term for decentralization is positive and significant (β = 0.45, t = 0.21, p = 0.034) while the squared term is negative and significant (β = −0.10, t = 0.04, p = 0.018), confirming the inverted U-shaped relationship. To visualize this relationship, we plot the relationship between decentralization and development activity in Figure 2(b), further confirming the existence of an inverted U-shaped relationship.

Although we do not formally hypothesize the relationship between decentralization and social media followers, Model 6 of Table 4 shows that there is also an inverted U-shaped relationship. Specifically, the linear term for decentralization is positive and significant (β = 1.20, t = 0.36, p = 0.001) while the squared term is negative and significant (β = −0.34, t = 0.08, p = 0.000), confirming the inverted U-shaped relationship. To visualize this relationship, we plot the relationship between decentralization and social media followers in Figure 2(c), further confirming the existence of an inverted U-shaped relationship.

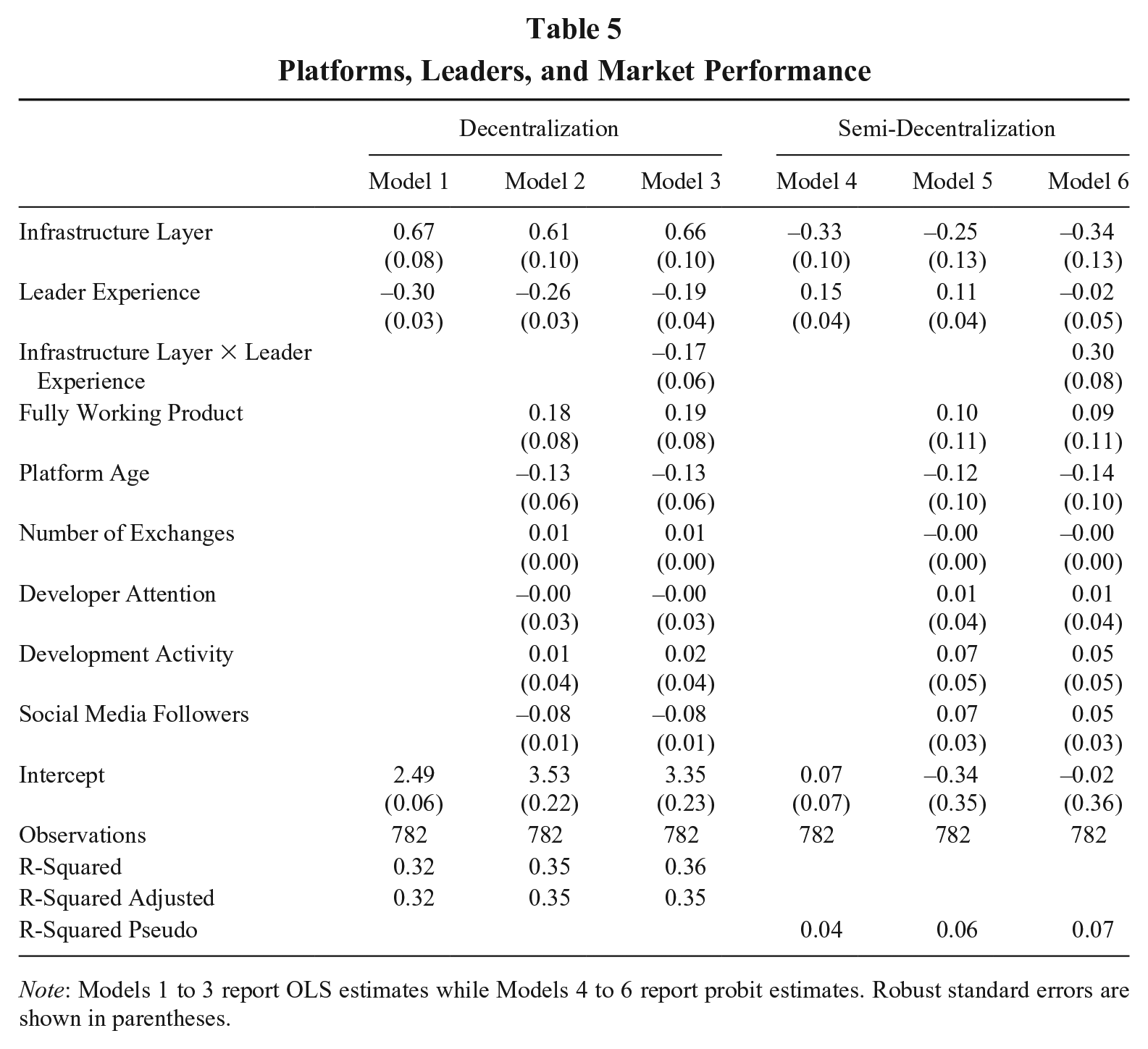

Hypothesis 3a proposes that blockchain-based platforms of the infrastructure layer tend to be more decentralized than those of the application layer. To test Hypothesis 3a, we run a series of OLS regressions with robust standard errors, for which we use decentralization as the dependent variable. As Models 1 to 3 of Table 5 show, the results support Hypothesis 3a. As Model 2 of Table 5 shows, the infrastructure layer is positively associated with decentralization (β = 0.61, t = 0.10, p = 0.000), suggesting that blockchain-based platforms of the infrastructure layer tend to be more decentralized. To further examine whether they tend to become overly decentralized, we create an indicator variable equal to 1 for moderate decentralization (i.e., platforms with a decentralization score of 2 or 3) and equal to 0 otherwise. Using semi-decentralization as the dependent variable, we then run a series of probit regressions with robust standard errors, and the results are reported in Models 4 to 6 shown in Table 5. As Model 5 shows, the infrastructure layer is associated with a lower probability of semi-decentralization (β = −0.25, t = 0.13, p = 0.049). Taken together, these results suggest that platforms of the infrastructure layer are more likely to be more decentralized—and even overly decentralized—than those of the application layer.

Platforms, Leaders, and Market Performance

Note: Models 1 to 3 report OLS estimates while Models 4 to 6 report probit estimates. Robust standard errors are shown in parentheses.

Hypothesis 3b suggests that experienced leaders can offset the tendency for blockchain-based platforms of the infrastructure layer to become overly decentralized and bring these platforms to more appropriate levels of decentralization. OLS regression results with robust standard errors in Models 1 to 3 of Table 5 support Hypothesis 3b. In particular, Model 2 shows that leader experience is negatively associated with decentralization (β = −0.26, t = 0.03, p = 0.000), suggesting that experienced leaders may steer platforms toward more centralization. This finding, however, raises the concern that platforms led by experienced leaders may become overly centralized. Results of the probit regressions help address this concern. According to Model 5 of Table 5, leader experience increases the probability of semi-decentralization (β = 0.11, t = 0.04, p = 0.007), suggesting that experienced leaders may steer platforms toward semi-decentralization rather than full centralization.

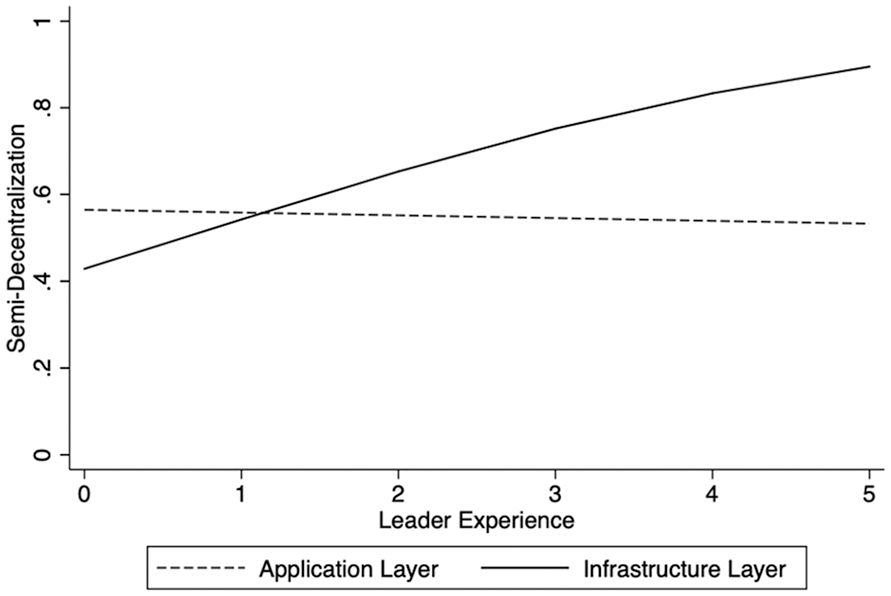

Furthermore, Model 3 of Table 5 shows that leader experience weakens the impact of the infrastructure layer on decentralization (β = −0.17, t = 0.06, p = 0.005), suggesting that experienced leaders can counter the tendency for platforms of the infrastructure layer to become overly decentralized. The results of the probit regressions provide further support for Hypothesis 3b. Model 6 of Table 5 examines the interaction between infrastructure layer and leader experience. An interaction effect of a probit model, however, cannot be evaluated directly from the statistical outputs (Ai & Norton, 2003). To evaluate the interaction effect, we follow Norton, Wang, and Ai (2004) and calculate the average interaction effect, and the result confirms the interaction effect (mean interaction effect = 0.11, mean z = 3.661), lending further support for Hypothesis 3b. To visualize this interaction effect, we plot the relationship between leader experience and semi-decentralization in Figure 3, while setting all other variables at their means. Figure 3 further confirms that leader experience can increase the probability of platforms of the infrastructure layer adopting semi-decentralized governance structures.

Leader Experience and Semi-Decentralization

Discussion

In this study, we draw on mechanism design theory to examine tradeoffs between centralization and decentralization and identify semi-decentralization as an effective governance structure. We further show that digital platforms of the infrastructure layer are less likely to adopt semi-decentralized governance structures while those led by experienced leaders are more likely to do so. Overall, we believe that this study has important implications for the shared governance of digital platforms, for the strategic leadership of digital platforms, and for initial coin offerings (ICOs) of the blockchain industry.

Shared Governance of Digital Platforms

The results of the study show that decentralization has an inverted U-shaped relationship with digital platforms’ market capitalization, developer attention, development activity, and social media followers. Digital platforms with semi-decentralized governance structures usually allow community members to participate in goal setting and decision making. They harness the creativity and diversity of their community members and in turn improve platform governance and performance. Moreover, they often have key organizations or individuals sponsor and shape platform governance such that they are more likely to reach agreements on key decisions. Through semi-decentralization, digital platforms may be better able to improve the balance of power between platform owners and platform participants and to ensure effective value creation and fair value distribution. As a result, semi-decentralization may enable digital platforms to achieve superior platform performance (Davis, Eisenhardt, & Bingham, 2009; Kyprianou, 2018; Reischauer & Mair, 2018; Wareham et al., 2014).

Recognizing the value of semi-decentralization can shed new light on whether and the extent to which dominant platforms may need to decentralize (see also Chen & Bellavitis, 2020; Hippel & Krogh, 2003). Extensive studies have suggested that digital platforms are becoming more and more open (Boudreau, 2010; Nambisan, Siegel, & Kenney, 2018; Parker & Alstyne, 2018). However, most studies have primarily focused on open participation rather than decentralized governance. Yet open participation is not the same as decentralized governance, as platform owners of open platforms can still retain centralized control over platform access, core interactions, and value distribution (see also Boudreau, 2010). When a digital platform is open for participation but centralized in governance, its platform owner can enjoy substantial power and control over other stakeholders in the platform ecosystem. With this study, we suggest that centralized platforms with centralized governance can actually benefit from relinquishing some governance control to other stakeholders in the platform ecosystems. By sharing governance rights and control with platform participants, platform owners can credibly signal their commitments to act in the interests of the overall platform ecosystems. With means to protect their rights and interests, platform participants may become more interested in joining such platform ecosystems and making valuable contributions. As a result, such platform ecosystems may be better able to attract participants, create network effects, and improve overall performance.

Once centralized platforms recognize the potential benefits of decentralized governance, they may be motivated to become more decentralized. For instance, Google’s Android platform has adopted a semi-decentralized governance structure. Google has decentralized Android through open sourcing (Bresnahan & Greenstein, 2014; Karhu, Gustafsson, & Lyytinen, 2018), allowing Android to be evolved by its large user and developer communities. Nevertheless, Google has also recognized the need to exert governance control over Android through the Open Handset Alliance and Google Play to ensure security, compatibility, and consistency. Similarly, Facebook recently proposed a semi-decentralized governance structure for the Libra platform, a blockchain-based digital payment platform. In developing Libra, Facebook has relinquished governance control to an independent organization, the Libra Association, and has restricted its governance power within the association. However, Facebook also recognizes the need to centralize some governance control through the Libra Association to ensure the healthy evolution of the platform (see Libra Association, 2019, for details). By promoting shared governance through semi-decentralization, centralized platforms may be better able to attract users, developers, and other stakeholders, potentially allowing them to enhance their network effects and create more value over the long run. Furthermore, semi-decentralization may also help dominant platforms avoid trust and antitrust issues related to platform monopolies. Overall, we believe that decentralization can be an important strategic consideration for dominant platforms.

Moreover, this study cautions existing studies on decentralized governance and suggests that decentralized platforms may benefit from concentrating some governance control among select people or organizations (see also Chen & Bellavitis, 2020; O’Mahony & Ferraro, 2007). Although decentralization is often touted as the guiding principle of blockchain-based platforms (Walch, 2019), we argue that going too far in terms of decentralization can become counterproductive. With pure decentralization, no organizations or individuals have more power than others such that goal setting and decision making require community members to reach consensus. Without any leadership, however, community members may fail to reach agreements on the future of a project and on how to move a project forward, potentially leading to deadlock. Pure decentralization, therefore, may slow goal setting, decision making, and continued development. Bitcoin, for instance, has manifested some problems associated with pure decentralization. In an attempt to increase scalability, the Bitcoin community has not reached an agreement due to disputes over alternative proposals, preventing Bitcoin’s scaling (De Filippi & Loveluck, 2016). Eventually, certain community members left Bitcoin and spun off new platforms, including Bitcoin Cash, Bitcoin SV, Bitcoin Gold, and Bitcoin Diamond, among others.

Existing research on platform governance tends to take the perspective of platform owners and focuses on identifying governance mechanisms that can help platform owners realize their objectives (e.g., Boudreau, 2010; Kyprianou, 2018; Reischauer & Mair, 2018; Rietveld et al., 2019; Tiwana et al., 2010; Wareham et al., 2014). From the perspective of platform owners, decentralization is simply a means for platform owners to achieve their goals. From this perspective, decentralization is valuable as long as it helps platform owners realize their goals regardless of whether it benefits other platform participants. Although this perspective can greatly inform platform governance, it may have some limitations. First, taking the perspective of platform owners may exclude one from examining decentralized platforms with limited to no involvement from platform owners. However, the past decade has witnessed the emergence of a growing number of fully decentralized platforms with Bitcoin as the leading example (Chen & Bellavitis, 2020). With no platform owners, nevertheless, many decentralized platforms still manage to survive and thrive. Second, when we consider the perspective of platform owners, we may ignore the welfare of other platform participants. As digital platforms become increasingly integrated into social and economic activities, it becomes essential to examine platform governance not just from the perspective of platform owners but also from that of other platform participants.

Once we broaden our perspective, we can start to examine platform governance in a new light. Through this study we show that semi-decentralization can be beneficial not just to platform owners but also to platform participants. For platform owners, semi-decentralization enhances market value and is thus beneficial. For developers, semi-decentralization can mitigate power imbalances, ensure fair value distribution, and thus be beneficial. We believe that studies along these lines can have important implications for the future of the platform economy as digital platforms are increasingly integrated into key social and economic activities. 11

Strategic Leadership on Digital Platforms

Many blockchain-based platforms—especially those of the infrastructure layer with independent blockchains—have the goal of being truly open, decentralized, and permissionless. Such platforms want participation to be open to all, innovation to be truly permissionless, and governance to be fully decentralized (Antonopoulos, 2017; Antonopoulos & Wood, 2019). These platforms thus tend to adopt fully decentralized governance structures. When decentralized platforms are paired with decentralized governance, they truly allow for open and permissionless participation and innovation, allowing these platforms to evolve in organic and unexpected ways—ways that can be good, bad, or ugly (Cerf, 2012; Chen & Bellavitis, 2020). Without effective leadership, however, there is no guarantee that these platforms will evolve in healthy and constructive ways.

Through this study, we argue that the nature of infrastructure-layer platforms renders leadership and governance more—rather than less—important. It would be a mistake to assume that platforms of the infrastructure layer should have no leadership and should be governed in a completely decentralized manner (see also Simcoe, 2014). In this study, we show that pure decentralization can be counterproductive and that strategic leadership can help platforms avoid excessive decentralization. With strong leaders, blockchain-based platforms are more likely to enjoy value-enhancing governance structures that can balance openness with control, thereby allowing them to sustain developer attention, development activity, and market performance.

Nevertheless, there are concerns that experienced leaders may favor centralization over decentralization (Altman & Tushman, 2017) and thus may reduce the openness and decentralization of digital platforms. Such concerns may be valid for platforms of the application layer, as most of them have adopted more centralized governance structures. For platforms of the infrastructure layer, however, we argue that experienced leaders’ preferences for centralization and control may be what is needed to manage the tendency for these platforms to become overly decentralized, thereby bringing decentralization to more performance-enhancing levels. Overall, we show that experienced leaders can considerably help—rather than hinder—digital platforms of the infrastructure layer.

Life after ICOs

Recent studies have shown that ICOs have afforded entrepreneurs a new fundraising mechanism, allowing them to raise funds directly from global investors (Chen, 2018; Fisch, 2019; Howell et al., 2019). For a typical ICO, a new venture tokenizes a project and sells the project-specific token to the public to raise funds to develop the project. Over a few short years, ICOs have helped entrepreneurs in the blockchain industry raise billions of dollars. Recent studies have started to examine performance during ICOs. Performance at the time of ICOs can pave the way for future success, as projects with more funding may be better able to motivate stakeholders to join their platform ecosystems and to invest in the continued development of such platforms.

However, it is also essential to examine performance post-ICO. At the time of an ICO, a project may have just embarked on its entrepreneurial journey with a long road ahead before the project is able to fulfill its vision and potential. Unlike an initial public offering (IPO), an ICO usually happens in very early stages of a project, and funds raised through an ICO are usually used to support the project’s early development. A project with a successful ICO is not yet successful; it must use the funds it raises to carry out continued development. In this respect, ICOs show similarities with crowdfunding—they both help entrepreneurs raise funds to develop and launch their products (Mollick, 2014). However, ICOs are very different from IPOs—IPOs usually occur at much later stages of highly successful ventures and can thus be considered an indicator of success (Certo, Holcomb, & Holmes, 2009). Nevertheless, even for successful IPOs, continued development in the post-IPO phase is still essential to the long-term success of companies (Arend, Patel, & Park, 2014).

Post-ICO performance is critical to blockchain entrepreneurs, who are often concerned with the performance of their projects not only during ICOs but also throughout the life cycles beyond early-stage fundraising. Post-ICO performance is also critical to blockchain investors making investment decisions during the ICO and post-ICO phases. The results of this study suggest that a project’s governance structure may be associated with post-ICO market performance. Effective governance can help align incentives, coordinate actions, mitigate conflicts, and foster a common identity (Di Tullio & Staples, 2013; Dixit, 2009; Gawer & Phillips, 2013; Wareham et al., 2014; Williamson, 2005) and can thus be critical to post-ICO performance. Our findings have implications for both blockchain entrepreneurs and blockchain investors. Blockchain investors must recognize the importance of governance structures and try to invest in projects with more effective governance structures. Blockchain entrepreneurs must understand the importance of governance structures and recognize their unique opportunities to shape their platforms’ governance structures in early stages of their projects. 12

Limitations and Avenues for Future Research

We note several limitations of the current study that may set the stage for future research. First, this study examines a key aspect of governance: the degree of decentralization. However, there are many other aspects that we do not investigate (Kyprianou, 2018; Reischauer & Mair, 2018; Wareham et al., 2014). Given the importance of governance, future research may explore other aspects of governance and determine how they help improve platform performance. Second, this study examines platform governance from the perspectives of platform owners and developers. However, we have not accounted for the perspectives of other important stakeholders. Future studies may continue to draw on mechanism design theory to examine the perspectives of other stakeholders—and those of users especially (Arrieta-Ibarra et al., 2018). Third, this study focuses on one dimension of strategic leadership: leader experience. Future studies may examine other dimensions of strategic leadership and investigate their roles in platform governance throughout the life cycles of digital platforms (Daily et al., 2002). Finally, although we collect data over two waves, we do not have a panel dataset with enough time periods and within variations to allow for panel data analyses. Future studies may thus collect more data over longer time periods to carry out panel data analyses (Certo & Semadeni, 2006).

Conclusion

The past decade has witnessed the emergence of numerous decentralized platforms such as Bitcoin and Ethereum. Unlike centralized platforms, which are owned and governed by platform owners, decentralized platforms can be owned and governed in more decentralized ways, and some have no platform owners and are governed through community efforts. The rise of decentralized platforms has created a unique opportunity to examine the spectrum of centralized and decentralized governance and to assess the nature and characteristics of high-performing governance structures. As digital platforms become increasingly integrated into economic transactions and social activities, it is also essential to examine platform governance not just from the perspective of platform owners but also from the perspectives of other stakeholders. In this study, we draw on mechanism design theory and on data from the blockchain industry to show that semi-decentralized governance structures improve platform performance. In addition, we show that platforms of the infrastructure layer are less likely to adopt semi-decentralized governance structures while those led by experienced leaders are more likely to do so. Overall, we believe that these findings have important implications for the shared governance of digital platforms and especially for the design of high-performing governance structures. Given the growing dominance of digital platforms and the shared responsibilities of platform governance, future studies along these lines can greatly improve our understanding of the characteristics, antecedents, and consequences of effective platform governance and may have important implications for the future development of the platform economy.

Footnotes

Appendix: Glossary

Acknowledgements

We thank William Schulze, the action editor, and two anonymous reviewers for their valuable comments and suggestions. We also thank Sasha Rodivilov and Glen Weyl for their helpful feedback. We thank CoinCheckup.com for providing data for this study and for answering our questions regarding the study data. Any opinions, findings, conclusions, or recommendations expressed in this material are solely those of the authors.