Abstract

How do firms alter their strategic actions when targeted by different types of activist shareholders? We argue that hedge fund activists threaten firms in ways that lead them to conserve resources and to scale back and simplify their strategic actions, which refer to long-run competitive actions requiring substantial investment. By comparison, corporate shareholder activists bestow firms with new resources and freedoms that increase their flexibility to expand and complexify their strategic actions. Using a matched sample and difference-in-differences methodology, we find support for our theory: Firms targeted by hedge fund activists decrease the intensity and complexity of their strategic actions, while firms targeted by corporate shareholder activists increase the intensity and complexity of those actions. Our study contributes to research on shareholder governance and competitive dynamics by highlighting the differential effects of activist shareholders on targeted firms’ strategic actions.

Keywords

As activist shareholders have become increasingly active in launching campaigns against new target companies, a lively discussion is unfolding about whether the regulatory freedoms that some of these shareholders enjoy should be constrained. “The [U.S.] regulatory framework designed more than 50 years ago,” warns renowned corporate lawyer Martin Lipton’s firm, “is anachronistic, lags behind disclosure rules in every other modern economy, and is in urgent need of reform” (Emmerich, Norwitz, & Savitt, 2021). Backed by recent academic works showing that certain types of financially motivated activist shareholders can impair the social responsibility of companies (DesJardine & Durand, 2020) and hurt their employees (G. Chen, Meyer-Doyle, & Shi, 2020), policy makers are being urged to consider regulations that both require earlier disclosures of activism campaigns and make it harder for activists to coordinate and exert control when targeting public corporations. Yet, while scholars have shown that shareholders vary widely in their investment approach and influence on firms (Boh, Huang, & Wu, 2020; Connelly, Tihanyi, Certo, & Hitt, 2010; Hoskisson, Hitt, Johnson, & Grossman, 2002), we lack understanding about similar variations among activist shareholders. As we argue, identifying these disparities is critical to tease apart the various ways that different types of activist shareholders impact targeted firms.

In this study, we examine the effects of two distinct forms of shareholder activism—hedge fund activism and corporate shareholder activism—on targeted firms’ strategic actions. Both hedge funds activists and corporate shareholder activists use their equity positions in targeted firms to enforce changes that seek to advance the activists’ agenda. However, whereas hedge fund activists use activism mostly to maximize targeted firms’ short-term market values (Aguilera & Jackson, 2003; Klein & Zur, 2009), corporate shareholder activists leverage activism to augment and improve the long-term sales and vitality of their own core business. As we unpack, corporate shareholder activism differs from equity-based partnerships, where firms invest passively (Goerzen, 2007); strategic alliances, where firms become consensual partners (Rothaermel & Boeker, 2008); corporate venture capital investment, where firms invest in new entrepreneurial ventures (Dushnitsky & Lenox, 2006); and hostile takeovers, where firms seek full control of target firms.

We focus on the heterogeneous influences of hedge fund activism versus corporate shareholder activism on the intensity and complexity of firms’ strategic actions. In contrast to tactical actions, which are short-term oriented and not resource intensive, strategic actions, such as acquisitions and partnerships, are long-run competitive moves that require substantial investment (Chen, Smith, & Grimm, 1992; Connelly, Tihanyi, et al., 2010). Strategic action intensity captures the number of strategic actions that a firm undertakes to gain competitive advantage over industry rivals (Shi & DesJardine, in press), while strategic action complexity refers to the diversity and novelty of those actions (Connelly, Tihanyi, Ketchen, Carnes, & Ferrier, 2017). We explore strategic action intensity and strategic action complexity for two reasons. First, strategic action intensity and complexity are broad dimensions that capture an array of corporate actions, allowing us to unpack various differences between how hedge fund activists and corporate shareholder activists affect targeted firms’ strategies. In comparison, using a single action, such as new product introductions or acquisitions, would limit our ability to compare these two types of activist shareholders. Second, strategic action intensity and complexity are critical to a firm’s long-term performance and competitiveness, making these important strategic considerations for activist shareholders.

We investigate the differential effects of hedge fund activism and corporate shareholder activism on firms’ strategic action intensity and strategic action complexity using a difference-in-differences (DID) design, where we use propensity score matching (PSM) to identify non-targeted control firms separately for (a) firms targeted by hedge fund activists and (b) firms targeted by corporate shareholder activists. In support of our theory, relative to non-targeted firms in the post-activism period, firms targeted by hedge fund activists decrease the intensity and complexity of their strategic actions, whereas firms targeted by corporate shareholder activists increase the intensity and complexity of those actions.

Our theory and results contribute to two areas of research. First, although numerous studies show that shareholders in general can have differential influences on firms (e.g., Boh et al., 2020), little work has considered heterogeneity among activist shareholders specifically. We advance research on shareholder activism by assessing the differential firm-level effects of hedge fund activism and corporate shareholder activism. Our findings show that examining heterogeneity among activist shareholders is crucial to understanding the full range of consequences of shareholder activism.

Second, we extend competitive dynamics research (M.-J. Chen & Miller, 2012; Shi & DesJardine, in press) by highlighting the effects that hedge fund activists and corporate shareholder activists have on the intensity and complexity of firms’ strategic actions. Connelly and colleagues (2019); Connelly and colleagues (2010); and Connelly and colleagues (2017) have investigated the influence of institutional investors on firms’ competitive actions, which include both strategic and tactical actions, while others have studied the effects of activists on corporate outcomes other than competitive moves (e.g., David, Hitt, & Gimeno, 2001). Despite substantial evidence that activist shareholders can drastically affect targeted firms’ strategic decisions and outcomes (DesJardine & Durand, 2020), the effects of activist shareholders on firms’ competitive strategies have been overlooked. Our study provides new insights into how a firm’s activist owners can shape its strategic actions.

Conceptual Background

Comparing Hedge Fund Activism and Corporate Shareholder Activism

Shareholder activism manifests when shareholders take actions with the explicit intention of influencing the management of a targeted firm (Goranova, Abouk, Nystrom, & Soofi, 2017). To achieve their objectives, activist shareholders can employ a range of tactics, including shareholder proposals, “vote no” campaigns, calling special shareholder meetings, and meeting privately with managers (Goranova & Ryan, 2014). Beyond these direct interventions, activist shareholders can also send powerful messages to firms simply by acquiring their stock (DesJardine & Durand, 2020). Given that activist shareholders have different goals and tactics (e.g., Shi & DesJardine, in press), we now explain the two major forms of shareholder activism that we seek to unpack in this study: hedge fund activism and corporate shareholder activism.

Hedge fund activism

Hedge fund activists make money for themselves by buying stakes in public corporations and then persuading or forcing those corporations’ boards and managers to make changes that can improve their share prices (Ahn & Wiersema, 2021). Unlike passive hedge funds, which may employ a variety of trading strategies, hedge fund activists are motivated to actively intervene in corporate affairs (DesJardine, Marti, & Durand, in press). Typically, hedge fund activists target only a few companies at one given time; by concentrating their holdings, these activists focus intently on the companies they target and are strongly incentivized to influence management, which differentiates them from investors with more diversified portfolios who sometimes lack incentives to directly engage boards and managers.

Hedge fund activists’ demands can vary widely and are often folded together under single activism campaigns, whereby the targeted firm is expected to produce multiple changes to its business. For example, a hedge fund activist may demand that a targeted firm replace certain directors, divest various assets or entire business units, and redistribute more cash to shareholders through dividends or buybacks. A range of tactics may be employed to enforce these demands, including private discussions with managers and directors, public campaigns to draw widespread attention to the proposed changes and managerial inadequacies, and proxy fights to enable other shareholders to weigh in on the proposed changes (Gantchev, 2013).

Over several decades, finance scholars have widely studied the effects of hedge fund activism (Denes, Karpoff, & McWilliams, 2017), while management scholars have paid less attention, at least until recently (G. Chen et al., 2020; S. Chen & Feldman, 2018; DesJardine & Durand, 2020; DesJardine et al., in press; Shi, Connelly, Hoskisson, & Ketchen, 2020; Wiersema, Ahn, & Zhang, 2020). The dominant focus so far has been on how these activists can improve targeted firms’ share prices by intervening with demands aimed at reforming corporate governance, improving operational efficiency, and narrowing corporate scope. In contrast, we know surprisingly little about whether hedge fund activism alters a firm’s range of competitive actions.

Corporate shareholder activism

Corporate shareholder activism is an emerging form of activism and thus the focus of far less research than hedge fund activism. Corporate shareholder activism occurs when a nonfinancial corporation acquires shares of another firm with the intent to alter the affairs of the targeted firm. Compared with alliances and equity-based partnerships, which are generally cooperative in nature and jointly determined by both firms entering the partnership (Goerzen, 2007), corporate shareholder activism may occur nonconsensually. Corporate shareholder activism is indicated by a nonfinancial corporation filing a Schedule 13D with the U.S. Securities and Exchange Commission (SEC), just as hedge fund activists do, with the goal of intervening with the decisions of targeted firms.

In comparison to hedge fund activists, corporate shareholder activists utilize an activism strategy primarily to augment and improve the long-term sales and vitality of their own business. Such a strategy may involve building research or product capabilities, developing new management practices, or altering product-market decisions within the targeted firm (Allen & Phillips, 2000). By influencing targeted firms at arm’s length, without obtaining full control, corporate shareholder activism also differs from hostile takeovers, which are nonconsensual and entail the activist (i.e., the acquirer) taking full control of the targeted firm. In the context of hostile takeovers, acquirers are required to register material information related to a merger or acquisition by filing Form S-4 with the SEC rather than the Schedule 13D used for activism. 1

Similar to hedge fund activists, corporate shareholder activists often achieve their goals by making various demands on targeted firms, though with longer horizons. Estimating corporate shareholder activists’ horizons is difficult because ownership under the 5% Schedule 13D threshold is not tracked in the United States; however, based on our analysis, we found the average holding period to be approximately 4 years, with occurrences of longer periods, such as Cisco’s roughly 10-year campaign at WMware from 2007 to 2018. Due to their longer holding periods and broader strategic goals, corporate shareholder activists should favor larger and more structural changes that can alter a target company’s business and industry position rather than changes that seek to maximize short-term returns to shareholders. For example, starting in 2015, GE acted as a corporate shareholder activist when its Medical Systems Information Technologies business became the largest shareholder in genetics testing firm NeoGenomics by acquiring an 11.5% stake. In the years after NeoGenomics was first notified of GE’s intent to alter its strategic trajectory, it did not change its dividend or share repurchase policy or divest assets but added significant new lab capacity, expanded from the United States to Europe, and strengthened its product development. Therefore, albeit with different objectives and tactics, corporate shareholder activists may also shape the corporate actions of targeted firms.

Despite the vast heterogeneity among shareholders, we know little about whether different types of activist shareholders exert distinct influences on the firms they target. Some work has suggested that different nonactivist shareholders can affect firm outcomes in distinct ways but has overlooked activist shareholders. For example, Boh et al. (2020) consider how corporate investors and family investors differentially affect firms’ innovation performance, others show dedicated and transient institutional investors have different effects on firms’ competitive actions (Connelly, Tihanyi, et al., 2010) and their research and development spending (Bushee, 1998), and Hoskisson et al. (2002) show pension fund investors and professional investment funds affect the methods by which firms innovate. Existing research has thus established heterogeneity among shareholders but has examined different types of activist shareholders in silos. Goranova and Ryan (2014: 1244) warn such an approach is problematic, as “the equivocal findings of prior research” may be driven by scholars aggregating “different shareholder demands by multiple types of investors utilizing divergent activism methods.” With this in mind, we examine the heterogeneous influence of hedge fund activists and corporate shareholder activists on targeted firms’ strategic action intensity and complexity.

Strategic Action Intensity and Strategic Action Complexity

Competitive strategy encompasses the set of discrete competitive actions that a firm undertakes to gain a competitive advantage in its industry (M.-J. Chen, 1996). Firms use two major types of competitive actions: strategic competitive actions and tactical competitive actions. Strategic competitive actions (“strategic actions” for short) require a substantial commitment of resources to specific projects that are challenging to implement and reverse (Smith, Grimm, Gannon, & Chen, 1991). When profitable, such actions tend to return value predominantly in the long run (Connelly, Tihanyi, et al., 2010; DesJardine & Shi, 2021). Examples of strategic actions are captured by business expansions through acquisitions, joint ventures, mergers, and new partnerships. By comparison, tactical competitive actions (“tactical actions” for short) involve fewer resources and are easier to implement and reverse (Shi & DesJardine, in press; Smith et al., 1991). Examples of tactical actions include cutting prices, increasing prices, and launching marketing campaigns (Connelly, Tihanyi, et al., 2010).

Our study focuses on strategic actions for three reasons. First, compared with simpler tactical actions, strategic actions can be difficult and ambiguous, making it more likely for activists to either aid or impair managers in these actions. For instance, a corporate shareholder activist’s knowledge and expertise will be of less value when a targeted firm’s managers are contemplating a tactical price change than when they are planning and implementing a strategic joint venture. Second, the intense demands required to undertake strategic actions and the substantial implications of these moves for organizations make it likely that managers will closely account for pressures they face from activist shareholders. When such moves incur large blunders and missteps, they pose considerably more harm to managers and firms than misplaced tactical actions. Thus, activist shareholders are more likely to trigger changes in strategic actions than in tactical actions. Third, compared with tactical actions, strategic actions are far more consequential for a firm’s long-term performance and competitiveness, making them more meaningful to study when considering how different activists affect target firms. Following these reasons, we study changes in strategic actions across two dimensions: intensity and complexity.

Strategic action intensity refers to the number of strategic actions that a firm undertakes in a given time period. Long studied in competitive dynamics research (M.-J. Chen & Miller, 2012), firms increase their strategic action intensity by quickly undertaking more strategic actions, such as engaging in more acquisitions or more joint ventures. However, since initiating more strategic actions requires additional attention and investment, firms must have the requisite resources and horizons to increase the intensity of these actions (e.g., DesJardine & Shi, 2021).

Strategic action complexity refers to the diversity and consistency of strategic actions that a firm undertakes over time. Whereas firms increase their strategic action intensity by repeatedly undertaking the same set of actions, they increase their strategic action complexity by undertaking different actions from what they have used in the past (Connelly et al., 2017). Existing research shows the learning and performance benefits of repeatedly undertaking the same types of strategic actions, such as acquisitions (Haleblian, Kim, & Rajagopalan, 2006). Accordingly, Connelly et al. (2017) find that higher levels of competitive complexity—comprising strategic and tactical actions—initially hamper financial performance, as firms must invest in learning and developing new types of actions, but increase firm performance over time as managers with more complex competitive repertoires hone the ability to employ more diverse moves to outperform competitors (Fox, Simsek, & Heavey, in press; McNamara, Luce, & Tompson, 2002). Given the heavy upfront costs, however, firms must be willing to sacrifice efficiency gains and be open to a high risk of failure in order to increase strategic action complexity.

Hypotheses

Hedge Fund Activism and Strategic Actions

Hedge fund activists pose a salient and severe threat to managers of targeted firms (DesJardine & Durand, 2020). Upon targeting companies, hedge fund activists will propose their own plans and strategies for improving shareholder returns, emphasizing where existing managers have fallen short. Some hedge fund activists are even more direct, criticizing managers personally. For example, when targeting Corteva in 2021, hedge fund activist Starboard Value wrote of the company’s CEO, Jim Collins, that “if Corteva were looking to hire a new CEO and Jim was proposed as a candidate, based on his track record, we would not interview him” (Root, 2021). Such personal and public attacks can damage managers’ reputations and, potentially, their future career prospects (e.g., board appointments).

According to threat rigidity theory, such an outside threat can induce rigidness in managerial decision-making and restrict new actions (Staw, Sandelands, & Dutton, 1981). Specifically, the threat rigidity view proposes two predictions regarding responsive behavior, namely, restriction in information and constriction in control. At the organizational level, these responses can result in reduced information processing, increased centralized control, and resource conservation (Shimizu, 2007; Staw et al., 1981). Shi, Connelly, and Cirik (2018: 1895), for instance, find that the threat of downward stock pressure from short sellers causes managers to become more conservative in terms of growth actions, arguing that they “attempt to reduce the amount and type of information that comes across their desks.” When facing high-pressure situations, managers will look to reduce their information load and tighten resource expenditures, causing them to rely more on existing, well-learned, and dominant activities rather than engage in new actions.

Filled with uncertainty and idiosyncrasies, each strategic action is distinct, and executing successfully requires detailed information processing and dedicated resources. Although firms can learn how to conduct a strategic action—and realize some benefit from that learning—each additional strategic action benefits from a tailored process. For example, before initiating a formal partnership, a firm must identify its distinct need, seek potential partners, vet those partners, negotiate terms, and formalize a partnership agreement, similar to the multistep process for acquisitions. The possible variance at each individual step of the process means that strategic actions are unlikely to become either well learned or dominant in the sense of threat rigidity theory (Staw et al., 1981).

We expect that managers whose firms are under threat will hesitate to undertake strategic actions, as they look instead to conserve corporate resources. Following threat rigidity theory, the considerable investment that strategic actions require before producing positive financial returns to firms (Connelly, Tihanyi, et al., 2010) will be especially unattractive when managers face intense pressure from a hedge fund activist. Acquisitions, alliances, and new product introductions require thoughtful planning, thorough integration, and committed resources that must later be recouped through synergies and increased business (Connelly, Shi, Hoskisson, & Koka, 2019). Chattopadhyay, Glick, and Huber (2001) argue that managers’ perceptions of threat can intensify concerns about efficiency and cost cutting. As hedge fund activists challenge targeted firms to enhance their efficiency and immediate returns (DesJardine & Durand, 2020), managers will look to curtail investment in new strategic actions.

Reducing the intensity of strategic actions will also be appealing by instilling managers with greater certainty in their response. Threat rigidity theory assumes that managers under threat will aim to reduce their information burden. Yet, the inherent uncertainty in the financial returns from strategic actions demands that managers thoroughly analyze and successfully execute these investments. For example, between a firm beginning the acquisition process and formalizing an acquisition, its corporate objectives can change, consumers’ evolving needs may make the target less attractive, external financing constraints may arise, or macroeconomic shifts can make the deal less profitable. Acquisitions can also fail as a result of having identified the wrong targets in the first place or facing challenges in postacquisition integration. Overall, the returns from strategic actions can be risky and unattractive (DesJardine & Shi, 2021); therefore, managers must spend considerable effort to process all of the related information before making informed strategic decisions. Thus, when under threat from a hedge fund activist, managers looking to reduce their information burden and curtail resource output will scale back the number of strategic actions.

Hypothesis 1: Firms targeted by hedge fund activists decrease the intensity of their strategic actions.

Beyond affecting the number of strategic actions undertaken, hedge fund activists may also shape targeted firms’ capacity to initiate more complex actions. Prior studies show that a key enabler of competitive complexity is resource slack (Carnes, Xu, Sirmon, & Karadag, 2019), which refers to the unused stock of flexible and largely undifferentiated resources that firms can deploy to pursue a range of organizational efforts. Such slack—in the form of managers’ time and corporate finances—buffers organizations from internal and external pressures. In doing so, slack affords organizations the capacity to experiment with strategic innovation, such as new, complex, competitive moves (Ferrier, 2001) and other explorative initiatives with uncertain returns and high rates of failure.

Hedge fund activism hinders strategic action complexity by reducing targeted firms’ resource slack. For some, such slack is seen as a costly liability because it hinders corporate efficiency; when resource slack is present, resources are underutilized, making room for short-term financial performance to improve (George, 2005). With a focal interest in pursuing efficiency enhancements, hedge fund activists fall cleanly into the camp that slack should be reduced, as their campaigns have been shown to result in employee layoffs (G. Chen et al., 2020), spending cutbacks (DesJardine & Durand, 2020), and asset sales (Chen & Feldman, 2018)—all initiatives aimed at reducing resource slack in target firms.

As hedge fund activists reduce targeted firms’ resource slack, managers will tend to rely more on well-learned activities than initiate new creative actions (Staw et al., 1981). Using strategic actions that are already familiar to the organization will reduce managers’ information and resource burdens, compared with the costs of learning and implementing new diverse actions. This repeating of known activities is especially valuable as managers in resource-constrained firms direct their attention and efforts toward addressing the activist and its campaign. Therefore, following a hedge fund activist campaign, managers of targeted firms are both unlikely to have the resources necessary to explore new options and unwilling to accept the information and resource burdens of pursuing those new paths. Instead, the preference will be to simplify strategic actions to “save costs, avoid disturbing customers (and provoking rivals), appease shareholders, and allow managers to capitalize on their strengths” (Connelly et al., 2017: 1154).

Additionally, hedge fund activists often lack the strategic expertise needed to help managers of targeted firms expand the complexity of their competitive repertoires. Although hedge fund managers have deep financial expertise, they are not general managers trained in corporate strategy. Rather, an activist fund manager’s tools favor financial engineering, such as initiating share repurchases, reconfiguring a firm’s capital structure, or implementing other balance sheet restructuring initiatives. Because implementing more complex strategic actions requires in-depth knowledge and experience in an organization, hedge fund activists find it difficult to propose complex strategic initiatives for targeted firms. One CEO we interviewed asserted, “The challenge, from my perspective, came because the [hedge fund] activist didn’t have a lot of experience running a company.” When reflecting on how the hedge fund proposed cutting back spending in parts of the business, the CEO explained, They don’t think through, “OK, it’s an incredibly complex process. How do you manage motivation, morale in making that happen, caring for customers along the way, what contractual obligations?” They just haven’t run a business, so they don’t know all the complexities involved.

With resource constraints propelling managers to reduce their information and resource loads, and limited strategic expertise to draw on from the activist, managers in targeted firms will tend to exploit rather than experiment with their competitive strategies, leading to reductions in the complexity of strategic actions.

Hypothesis 2: Firms targeted by hedge fund activists decrease the complexity of their strategic actions.

Corporate Shareholder Activism and Strategic Actions

Corporate shareholder activism is a unique form of activism, in that it creates an opportunity rather than a threat (Chattopadhyay et al., 2001). Corporate shareholder activists purchase shares with the intent to bolster the targeted firms’ business, in hopes that doing so will also strengthen the competitiveness of the activists’ core business. This approach differs markedly from that of hedge fund activists, which, with demands that pressure management and strain corporate resources, pose a direct threat to the managers of targeted firms. Headlines of activism campaigns in newspapers readily capture this distinction, describing hedge fund campaigns as a “fight,” “battle,” or “clash” between the activist and management, and corporate shareholder activism as an “opportunity” or “investment.” Instead of stripping resource slack out of targeted firms, corporate shareholder activists can provide an influx of resources and support that extends managers’ freedom to invest in more actions than they otherwise would. Connelly, Hoskisson, Tihanyi, and Certo (2010: 1567) comment, “[T]he arrival of a corporate blockholder provides fresh capital that the firm may use to facilitate growth.”

Bolstered by the support that accompanies a corporate shareholder activism campaign, managers in targeted firms will be more willing to increase their firms’ strategic action intensity. Upon investing in a targeted firm, corporate shareholder activists often express a clear objective to support and strengthen the targeted firm’s business and industry position over the long term. For example, after acquiring 19.99% of CASI Pharmaceuticals’ shares in 2014, Spectrum Pharmaceuticals communicated its plans to share its resources, including its successful drugs, with CASI to help the company take a leading position in China’s pharmaceuticals market. Spectrum Pharmaceuticals’ CEO stated, “We are impressed with the management team at CASI and their expertise in China, and look forward to sharing in the success of our drugs in this important market” (SEC, 2014).

Unlike hedge fund activists, corporate shareholder activists may invest in a targeted firm for a very long time period. Given the longer investment horizons of corporate shareholder activists, managers of targeted firms will become more open to the costs and long payback periods associated with ramping up strategic actions. As well, being no longer under threat but enjoying the resource support from an engaged and, hopefully, constructive investor, managers will have more bandwidth to absorb the heavy information costs that come from properly planning and undertaking more strategic actions. As a result, we expect the following:

Hypothesis 3: Firms targeted by corporate shareholder activists increase the intensity of their strategic actions.

In contrast to the reductions in slack that follow hedge fund activism, corporate shareholder activism can increase targeted firms’ resource slack in multiple ways. For example, by making an official investment, corporate shareholder activists allow targeted firms to access new capital that they can use to pursue a variety of strategic objectives. Moreover, given that many corporate shareholder activists are large and well-established corporations, gaining the formal support of these corporate allies means that targeted firms can benefit from newly available deep knowledge and expertise, capabilities and network partners, and managerial advice and counsel.

As corporate shareholder activists expand the pool of resources for targeted firms, managers of these firms will experience more discretion to experiment with new and diverse strategic actions that the organization may not have already internally mastered. The formal support of the corporate shareholder activist acts as a resource buffer, alleviating the pressures that might otherwise constrain managers from risking strategic missteps, granting them instead the confidence to explore more complex strategic moves.

Beyond bestowing managers with more discretion that increases their willingness to try new actions, corporate shareholder activists can offer useful strategic expertise—by offering their advice, counsel, and knowledge. These insights will increase the ability of managers in targeted firms to expand into new areas. For example, Boh et al. (2020) found that concentrated corporate shareholders support other firms’ innovation processes by serving as rich and reliable sources of personal and external information about other industries. Similarly, Choi, Park, and Hong (2012) found that foreign investors provide insights into advanced foreign technology and sophisticated managerial know-how to help firms gain access to foreign markets.

In our context, such resource sharing may be especially useful, given that corporate shareholder activists often have competitive repertoires that differ from those of targeted firms; therefore, when information is shared, it becomes easier for managers to initiate new strategic actions that they otherwise may have limited knowledge about (Fox et al., in press). For example, when GE invested in NeoGenomics, managers in the smaller and less experienced NeoGenomics operations gained access to the extensive competitive insights and repertoire honed by the goliath GE, including through a formal GE-appointed directorship. Beyond simply controlling knowledge and experience, many corporate shareholder activists will be motivated to help targeted firms utilize their insights (e.g., through directorships or other arrangements) since doing so can bolster the business of both firms, as evidenced by the earlier quote by Spectrum Pharmaceuticals’ CEO. Continuing our example, in the initial filing disclosing its activist stake in NeoGenomics, GE required that they be permitted to make suggestions and give advice to NeoGenomics regarding various matters and issues that they deem relevant for purposes of their investment in NeoGenomics. Such discussions and advice may concern NeoGenomics’ operations, business strategy, assets, financial performance, capital structure, strategic and extraordinary transactions, management, governance and other matters.

2

By bestowing new resources and insights that enable managers to experiment in more effective ways, and increasing their discretion to do so, corporate shareholder activists will bolster the complexity of targeted firms’ competitive strategies.

Hypothesis 4: Firms targeted by corporate shareholder activists increase the complexity of their strategic actions.

Methodology

Identifying Firms Targeted by Hedge Fund Activists and Corporate Shareholder Activists

Beginning our data collection, we follow existing research (Cheng, Huang, Li, & Stanfield, 2012; DesJardine & Durand, 2020) by using Schedule 13D and 13D/A filings to identify firms that hedge funds and nonfinancial corporations have targeted for activism. Schedule 13D is a mandatory form that investors must file with the SEC when acquiring more than 5% of any class of a company’s publicly traded securities if the investor intends to influence the management or control of the company. Subsequently, when the ownership changes by 1% or more, the beneficial owner must amend the Schedule 13D with a 13D/A form. We obtain 13D and 13D/A filings from the Audit Analytics Shareholder Activism database. In the 13D and 13D/A filings, shareholders must disclose their “purpose of transaction.” Following Shi et al. (2020), we retain 13D and 13D/A filings where the purpose of transaction is classified as “control,” “concerns,” or “disputes.” 3 We exclude cases with a disclosed goal of “support,” “agreements,” “discussions,” or “other” because such goals do not express intent to directly influence managerial decisions, which is our focus.

The Audit Analytics database provides the names of 13D and 13D/A filers (i.e., activist shareholders). Based on filer names, we identify activism by hedge funds and nonfinancial corporations. A filer is considered a hedge fund activist if it is listed on the Lipper/TASS or Hedge Fund Research (HFR) database, which together cover most hedge funds. A filer is considered a corporate shareholder activist if it is among the nonfinancial (all industries outside Standard Industrial Classification [SIC] codes 6000–6999) firms listed in the Compustat universe. Although coverage by Audit Analytics begins in 2000, we retain hedge fund and corporate shareholder activism events that took place after 2004 because data coverage from RavenPack, which we use to measure our dependent variables, begins in 2004.

From these sources, we collected data on 1,142 hedge fund activism campaigns and 129 corporate shareholder activism campaigns. Among firms that were targeted multiple times, we focus only on a firm’s first activism campaign so that the post-activism period does not overlap with another pre-activism period. To avoid the potential overlapping effects of each form of activism, we excluded firms that were targeted by both types of activists within the same 6-year period. After applying these inclusion criteria and excluding firms with missing data, our final sample includes 567 firms targeted by hedge fund activists and 69 firms targeted by corporate shareholder activists between 2004 and 2017. Among the 69 corporate shareholder activists, 15 of them were competitors of targeted firms.

Identifying and Matching Control Firms

To avoid biases from potential time trends in strategic action intensity and complexity and the endogenous selection of targeted firms, we apply DID regressions. We first adopt PSM to separately identify control firms for two groups of treatment firms: (a) firms targeted by hedge fund activists and (b) firms targeted by corporate shareholder activists. The pool used to identify control firms includes all nonfinancial firms with valid matching variables in the Compustat database that were not targeted by any activist during our sample period.

We use the following matching criteria to identify control firms separately for firms targeted by a hedge fund activist and for those targeted by a corporate shareholder activist. We begin by including firm size (measured as the natural logarithm of total assets) and leverage (measured as the ratio of total liabilities to total assets) because activist shareholders tend to target smaller and more leveraged firms (Greenwood & Schor, 2009). Next, we include dividends (measured as the ratio of total dividends paid to market value) because targeted firms tend to pay lower dividends. We then include return on assets (ROA; measured as earnings before interest, taxes, depreciation, and amortization scaled by total assets at the beginning of the fiscal year). We add Tobin’s Q (measured as the ratio of a firm’s market value of assets to the book value of assets) since activists tend to target firms with greater potential for stock price appreciation (Klein & Zur, 2009). We add institutional ownership concentration (measured as the Herfindahl-Hirschman index of institutional ownership) because the success of shareholder activism often depends on the support of institutional investors. Institutional ownership data are from Thomson Reuters Institutional (13F) Holdings. Prior strategic actions may also influence whether a firm is targeted by an activist shareholder. We thus match on firms’ prior strategic action intensity (measured as the logarithm of 1 plus the number of strategic actions in the year prior to activism).

Last, to identify the control group for firms targeted by hedge fund activists, we include as a matching variable geographic intensity of hedge fund assets (measured as the ratio of total assets under management by hedge funds to total market capitalization of listed firms in a state). The number of assets managed by hedge funds in a state should positively relate to the likelihood of firms in the state being targeted by hedge fund activists. Yet, this variable should not directly influence a firm’s strategic actions, making it a suitable exclusion restriction in our matching. We collect the total assets under management of hedge funds in each state using the Lipper/TASS database, which provides information on assets under management by hedge funds. In unreported results, the coefficient for geographic intensity of hedge fund assets (β = 4.02, p = .003) is positive and significant in predicting the likelihood of a firm being targeted by hedge fund activists; however, the coefficient for this exclusion restriction is not statistically significant when used to predict our dependent variables, making it a valid exclusion restriction.

Similarly, to identify the control group for firms targeted by corporate shareholder activists, we include geographic intensity of acquisitions (measured as the ratio of acquisitions in a state to the total number of firms covered by Compustat in the same state as targeted firms). Firms located in a state with an active takeover market should have a higher likelihood of being targeted by corporate shareholder activists, but this propensity should not directly influence firms’ strategic actions. We thus consider geographic intensity of acquisitions as the exclusion restriction for corporate shareholder activism. We identify the number of acquisitions in each state using the Securities Data Company (SDC) Merger and Acquisition (M&A) database. In unreported results, the coefficient for geographic intensity of acquisitions (β = 0.52, p = .04) is positive and significant in predicting the likelihood a firm is targeted by corporate shareholder activists; however, the coefficient for this exclusion restriction is not statistically significant when used to predict our dependent variables.

We take the following steps to find suitable control firms for each treatment firm. First, we conduct two separate logistic regressions to estimate annual propensity scores for the likelihood a firm is targeted by a hedge fund activist or corporate shareholder activist in a given year, generating a separate score for each form of activism. In each logistic regression, the dependent variable receives 1 if a firm experienced hedge fund (corporate shareholder) activism in year t and 0 otherwise. All matching variables are measured in year t − 1. After calculating propensity scores, we identify three control firms whose propensity scores are closest to that of the treatment firm, requiring that the control firms belong to the same industry (using the four-digit SIC industry classification) as treatment firms in the matching years.

We choose one-to-three matching (where one treatment firm is matched to three control firms) for two reasons. First, matching one treatment firm to one control firm would make our results more sensitive to any change in strategic actions among control firms, increasing the likelihood that the control group (and not the treatment group) drives the findings. Second, matching one treatment firm to more than three control firms would make it more difficult to ensure the balance between the control and treatment firms. To ensure proper balance, we retain only control firms whose propensity scores differ from that of treatment firms by less than 1%. This criterion reduces matching bias while allowing some treatment firms to match with fewer than three control firms. Our final sample includes 1,181 control firms matched to 567 hedge fund activism treatment firms and 182 control firms matched to 69 corporate shareholder activism treatment firms.

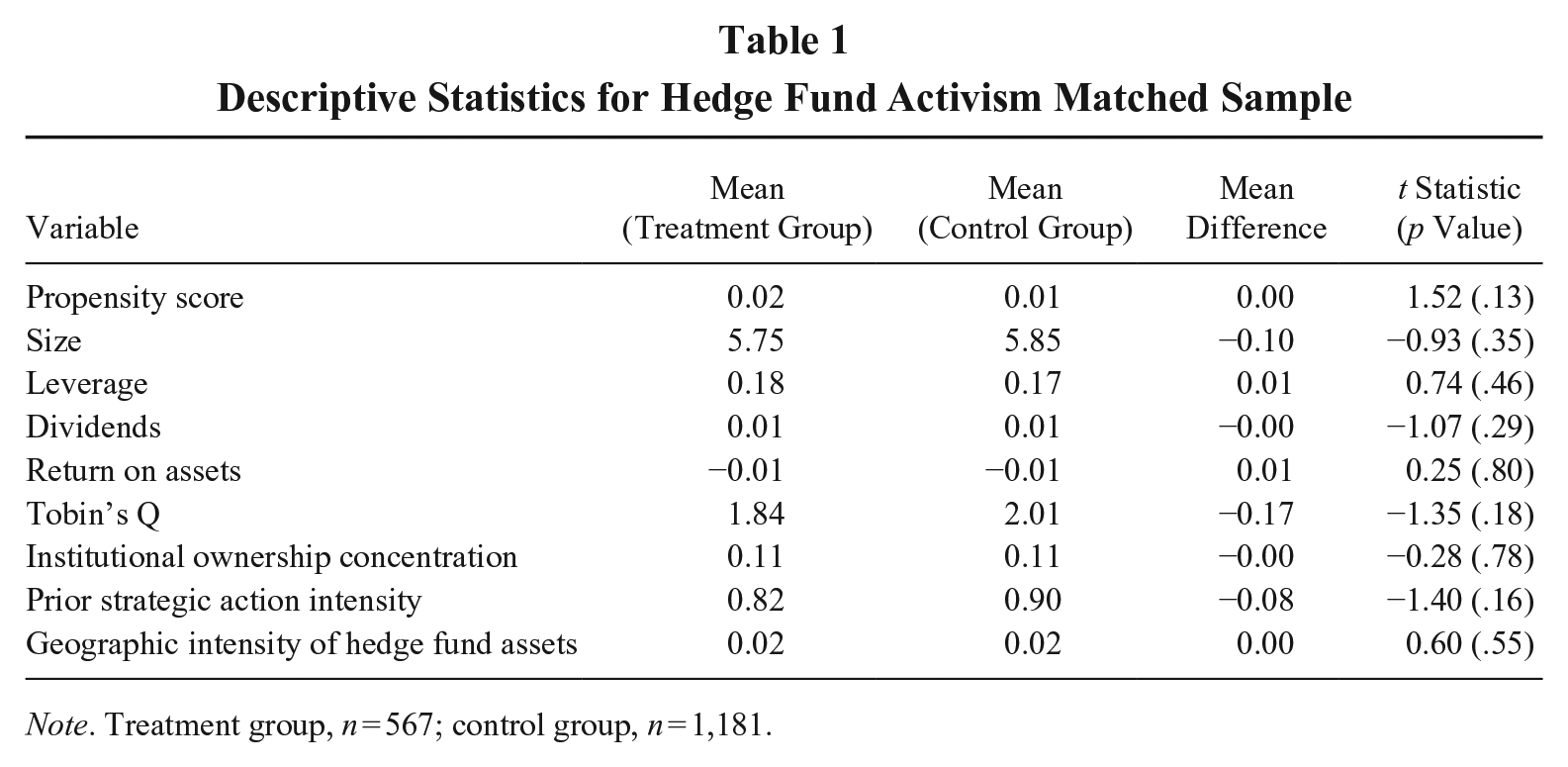

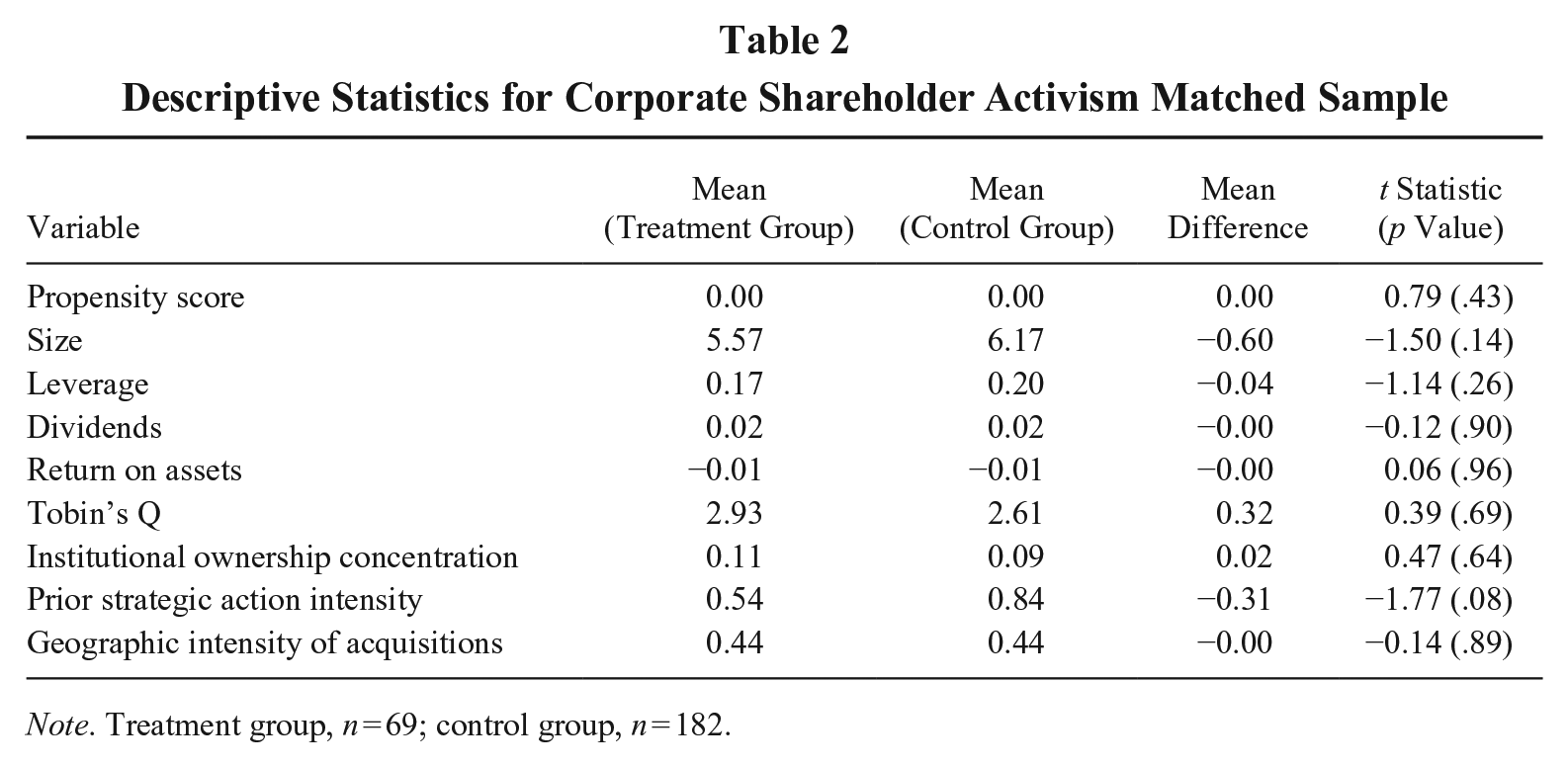

We calculate the mean values for each matching variable for both the treatment groups and control groups, and then compare their statistical differences. Table 1 (hedge fund activism) and Table 2 (corporate shareholder activism) indicate these groups do not significantly differ from each other in terms of matching criteria. In addition, the difference in propensity scores between the treatment group and control group is insignificant for both the hedge fund activism matched sample (t = 1.52) and corporate shareholder activism matched sample (t = 0.79). Moreover, we calculate the standardized percentage bias in propensity scores for the matched samples, which is the percentage difference of the sample means in the treatment group and control group samples as a percentage of the square root of the mean sample variances in the treatment and control groups. We find the standardized percentage bias in propensity scores is 10.20% for the hedge fund activism matched sample, and 13.70% for the corporate shareholder activism sample. The matched samples are largely balanced.

Descriptive Statistics for Hedge Fund Activism Matched Sample

Note. Treatment group, n = 567; control group, n = 1,181.

Descriptive Statistics for Corporate Shareholder Activism Matched Sample

Note. Treatment group, n = 69; control group, n = 182.

Dependent Variables

Our study’s dependent variables are strategic action intensity and strategic action complexity, which we measure using data from RavenPack. Of RavenPack’s three editions, the Dow Jones edition analyzes relevant information disseminated via Dow Jones Newswires and other Dow Jones news products (e.g., regional editions of the Wall Street Journal, Dow Jones Financial Wires, MarketWatch, and Barron’s), while the Press Release edition mainly covers press releases and regulatory disclosures from the leading global media organizations, including a variety of newswires and press release distribution networks, such as PR Newswire, Canada Newswire, LSE Regulatory News Service, and others. The web edition automatically processes hundreds of thousands of articles a day from leading publishers and web aggregators. RavenPack continuously monitors more than 19,000 sources, including industry and business publishers, national and local news, blog sites, and government and regulatory updates. We rely on data from RavenPack’s Dow Jones and Press Release editions because the web edition starts its coverage several years later than the other editions; thus, using all three editions of RavenPack would reduce our final sample size of hedge fund (corporate shareholder) activism events from 567 (69) to 456 (58).

RavenPack has three additional advantages that have led to its growing use for measuring firms’ competitive actions (e.g., Connelly et al., 2017; Shi & DesJardine, in press). First, RavenPack automatically detects business news and identifies the role of the related entity using proprietary text-positioning algorithms, which makes it straightforward to identify and categorize different firm events. For each story event, RavenPack automatically tags and classifies the topic, group, and subcategory to a set of more than 2,000 predefined event categories. Second, RavenPack allocates each news event a relevance score—ranging from 0 (not relevant) to 100 (very relevant)—to indicate the extent to which a particular firm is the focus of an article or press release, which helps ensure the event was initiated by the focal firm. We retain only news events with a relevance score of 100 to ensure that a firm is the focus of the news. Third, RavenPack provides an event novelty score (ENS) that makes it easy to avoid duplicate counts of the same event. The ENS represents how novel an article or press release is within a 24-hr time window for the same news event with the same story and same entities involved. As a given news story may be reproduced and then disseminated after its initial disclosure, the ENS ranges from 0 (nothing novel) to 100 (most novel). We require the ENS to be 100 to remove all possibilities of duplicate events.

We classify six categories of competitive actions as strategic actions: new product releases, production adjustments, market expansions, acquisitions, strategic alliances, and joint ventures. 4 All these actions have a long-term orientation and require substantial resource commitments. With our final matched samples, those in the hedge fund (corporate shareholder) activism sample undertook 29,187 (3,775) strategic actions 3 years before and after the activism campaigns between 2004 and 2017, with an average of 4.96 (4.41) actions per firm-year.

Our first dependent variable, strategic action intensity, is measured as the total number of strategic actions that a firm announced in a given year. Our second dependent variable, strategic action complexity, comprises three components: strategic action diversity, strategic action repertoire change, and new strategic action types (Connelly et al., 2017). Strategic action diversity is measured using the Shannon index, calculated as

where pi denotes the ratio of strategic actions of category i to the total R categories. Strategic action repertoire change is measured as the difference in the strategic action repertoire from the prior year to the focal year and is calculated in the form of Euclidean distance between the two action repertoires:

where Ci denotes the respective number of strategic actions belonging to category i. As discussed by Connelly et al. (2017), the repertoire change measured by Euclidean distance captures how often a firm’s strategic action repertoire has repeated itself from year t − 1 to year t but does not directly reflect the degree to which firms engage in new categories of strategic actions from year t − 1 to year t. Thus, we used the number of strategic action types that firms used in year t but not in t − 1 as a third component of strategic action complexity: new strategic action types. We standardize and summate strategic action diversity, strategic action repertoire change, and new strategic action types to construct the strategic action complexity index.

Independent Variables

We create two indicator variables for our DID regressions. The first indicator, post–hedge fund (corporate shareholder) activism, equals 1 for the 3 years following an activism campaign (excluding the year the activism took place) and 0 for the 3 years preceding an activism campaign. Although we include alternate windows for robustness, we initially use a 6-year window because a shorter window may not capture changes in strategic actions, whereas a longer window risks the introduction of confounding events that may affect strategic actions. Post–hedge fund (corporate shareholder) activism for control firms is the same as for their matched treatment firms. The second indicator, treatment, equals 1 for treatment firms (i.e., firms targeted by hedge fund activists or corporate shareholder activists) and 0 for control firms. Our independent variables are captured by Post–Hedge Fund Activism × Treatment and Post–Corporate Shareholder Activism × Treatment. Because we control for firm fixed effects and year fixed effects in our models, we do not include the noninteracted treatment or post–hedge fund activism (post–corporate shareholder activism) variables (Shi, Hoskisson, & Zhang, 2017).

Control Variables

We include control variables from our matching process that may also confound a firm’s strategic action intensity and strategic action complexity. Each variable is measured in the manner discussed earlier. As prior studies suggest that larger firms and firms with higher financial performance are more likely to take more strategic actions and have more complex competitive repertoires (Ferrier, 2001), we control for firm size and ROA. Also, as firms that are more indebted have less capacity to borrow funds to initiate strategic actions (Carnes et al., 2019), we control for leverage. We also control for institutional ownership concentration because monitoring by institutional investors may affect firms’ strategic actions (Connelly, Tihanyi, et al., 2010).

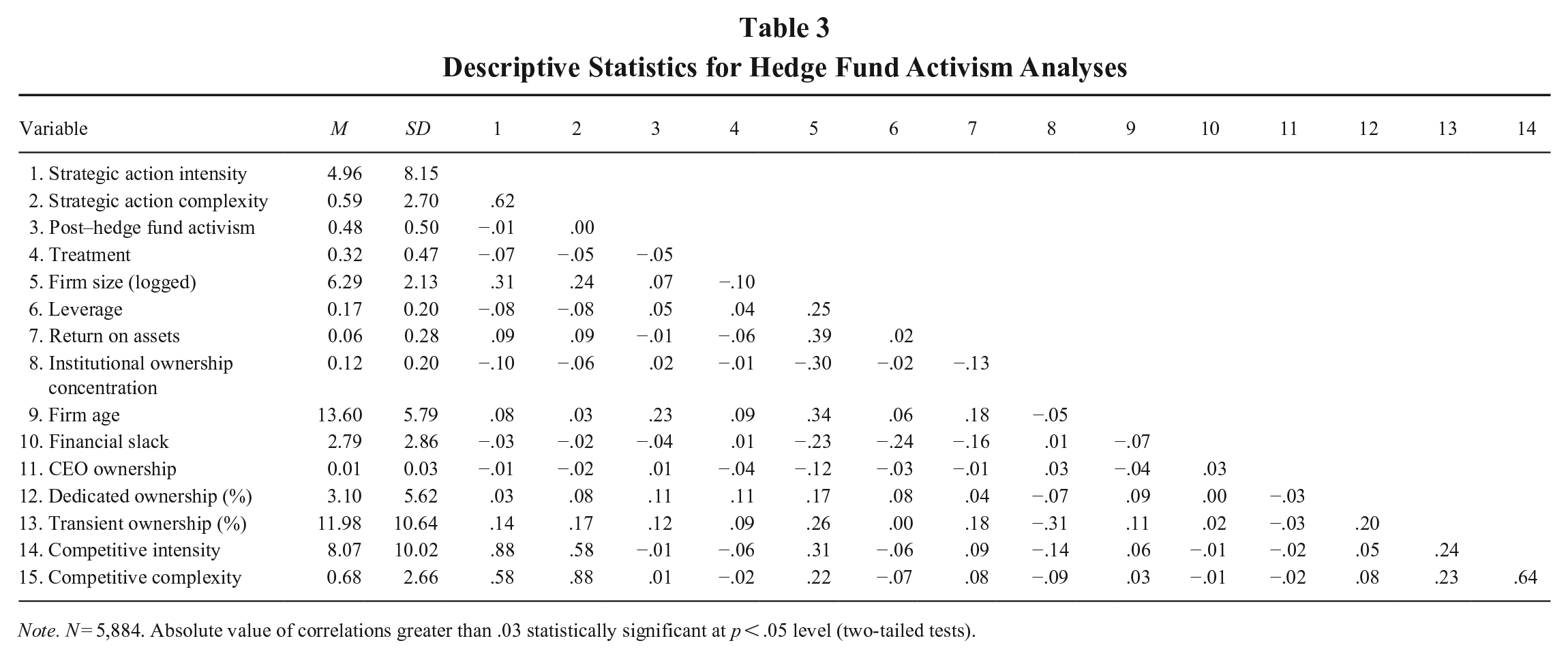

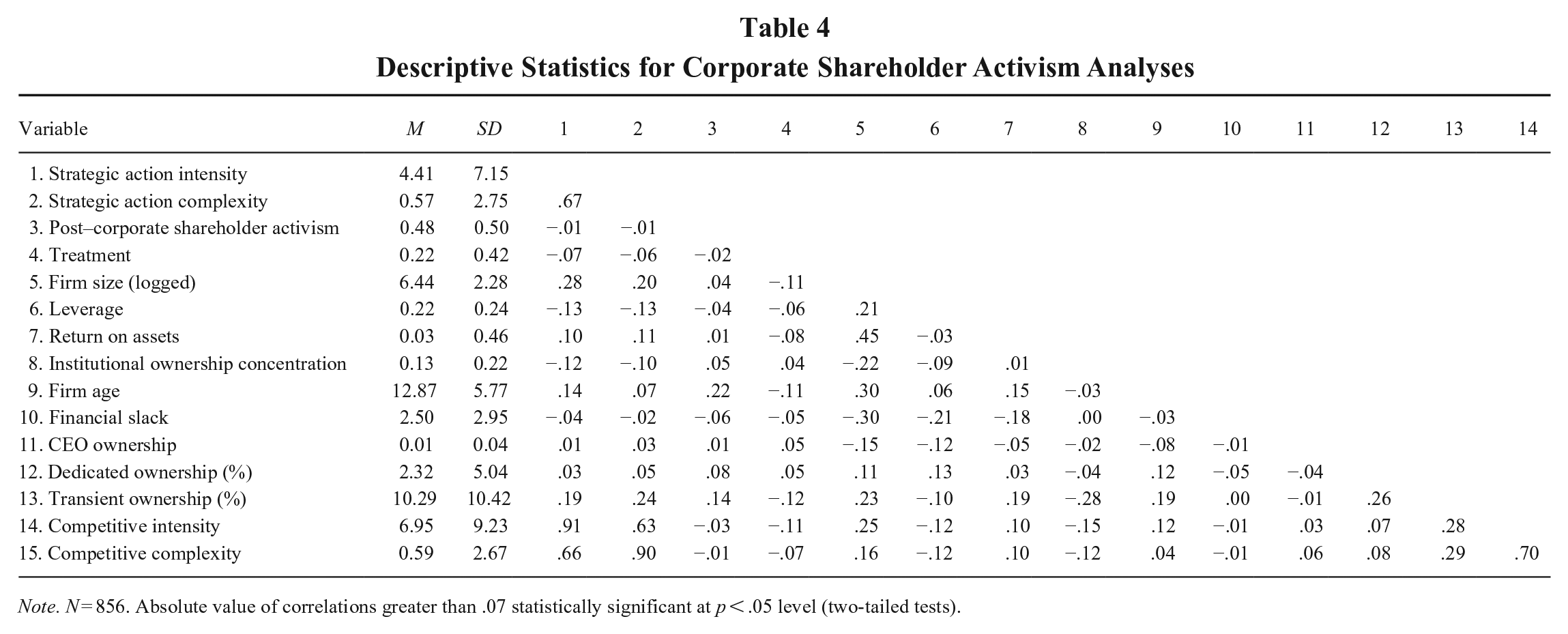

Next, we identify several new variables not used in our matching that may also influence strategic actions. First, we control for a firm’s life cycle by including firm age (measured as the natural logarithm of the number of years since the firm appeared in Compustat) since younger firms tend to take more strategic actions (Miller & Chen, 1994). We add financial slack (measured as the ratio of current assets to current liabilities) to control for firms’ financial capacity for strategic actions (Ferrier, 2001). Using data from Thomson Reuters Insider Trading, we control for CEO ownership (measured as the percentage of shares held by the CEO) because CEO equity ownership can influence strategic decisions (DesJardine & Shi, 2021). Finally, we control for the percentage of holdings by dedicated institutional investors (dedicated ownership) and transient institutional investors (transient ownership) because such investors have been found to influence firm horizons (DesJardine & Bansal, 2019). We follow Bushee (1998) to classify institutional investors into dedicated and transient institutional investors. All continuous variables are winsorized at the 1% level in both tails. Tables 3 and 4 present the descriptive statistics and correlations of the variables used in the hedge fund (corporate shareholder) activism analyses.

Descriptive Statistics for Hedge Fund Activism Analyses

Note. N = 5,884. Absolute value of correlations greater than .03 statistically significant at p < .05 level (two-tailed tests).

Descriptive Statistics for Corporate Shareholder Activism Analyses

Note. N = 856. Absolute value of correlations greater than .07 statistically significant at p < .05 level (two-tailed tests).

Analysis

To capture how shareholder activism affects strategic action intensity and strategic action complexity, we conduct firm fixed-effects DID regressions, which capture within-firm changes in strategic actions while mitigating potential omitted-variable bias arising from time-invariant firm heterogeneity. Because strategic action intensity is a count variable, we use firm fixed-effects Poisson regressions when testing the effects of hedge fund (corporate shareholder) activism on this dependent variable. We select firm fixed-effects Poisson regressions over fixed-effects negative binomial regressions because the latter cannot control for time-variant firm heterogeneity (Allison, 2009; Shi, Ndofor, & Hoskisson, 2021). As strategic action complexity is a continuous variable, we use firm fixed-effects ordinary least squares (OLS) regressions to test hypotheses related to this dependent variable.

Due to missing values for some control variables, our final sample related to hedge fund activism (corporate shareholder activism) has a total number of 8,087 (1,160) observations consisting of 1,748 (251) firms. As we use firm fixed-effects OLS regressions to test hypotheses with strategic action complexity as the dependent variable, we can include all the firms in our analyses. Yet, because fixed-effects Poisson regressions can include only firms with a time-invariant dependent variable (Allison, 2009), we lose 2,203 observations (482 firms) when testing the influence of hedge fund activism on strategic action intensity and 304 observations (72 firms) when testing the influence of corporate shareholder activism on strategic action intensity.

Although the treatment and control firms are similar along the various matching criteria, they could differ in unmatched dimensions that influence the likelihood of a firm being targeted by an activist shareholder. To alleviate potential selection bias from heterogeneity between treatment and control firms, we conduct propensity score weighted firm fixed-effects DID regressions, where weights are based on the propensity score generated from the matching (denoted as ƛ) and calculated as ƛ /(1 − ƛ) (Nichols, 2008). This propensity score reweighting has been used in recent research to mitigate selection bias and to adjust for nonrandom treatment (Shi, Zhang, & Hoskisson, 2019). Our dependent variables are measured in year t + 1, and all other variables are measured in year t.

Results

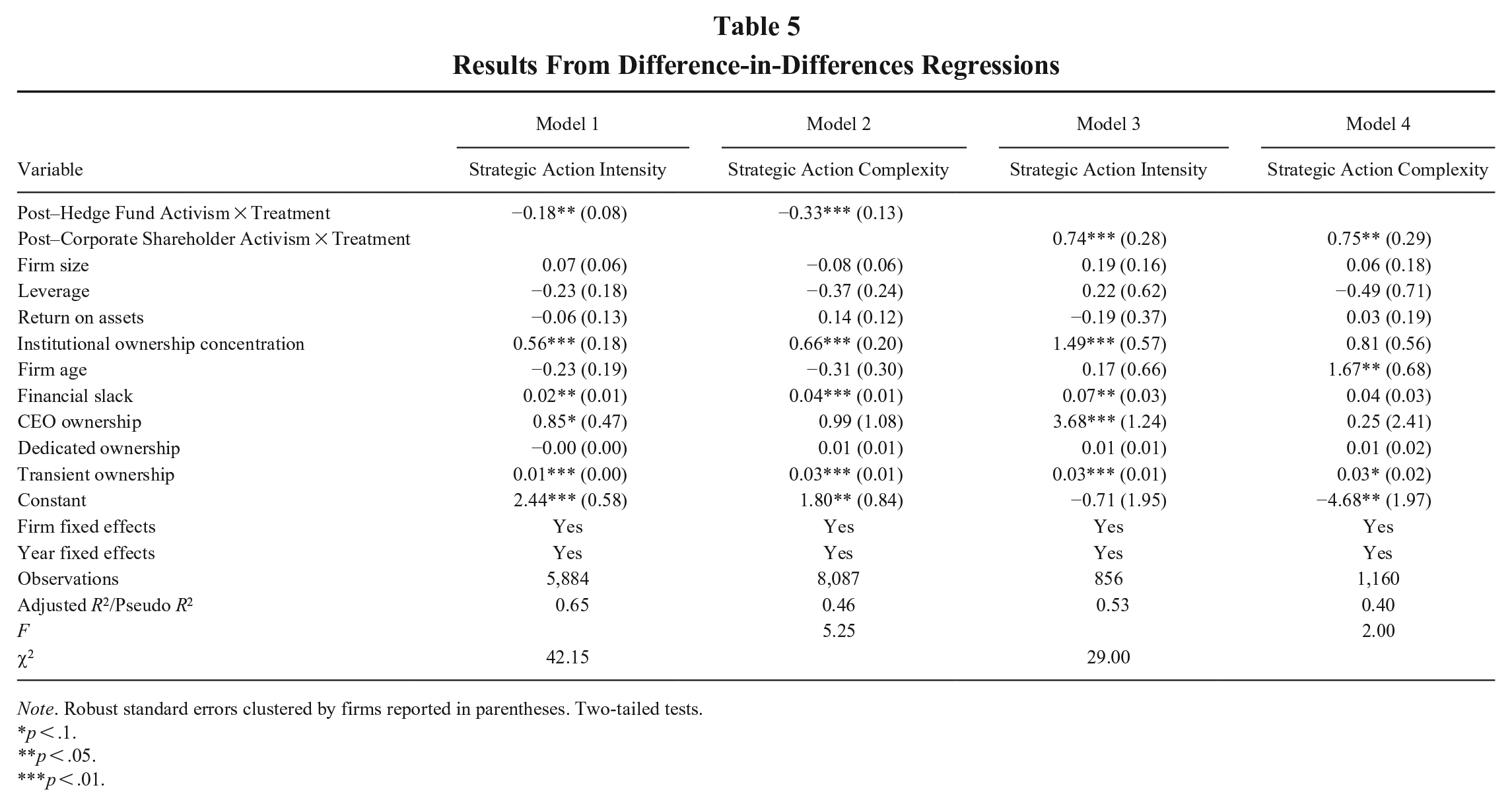

Table 5 reports the results we used to test our hypotheses. Hypothesis 1 predicts that firms experience a drop in strategic action intensity following hedge fund activism. In Model 1, which includes all control variables, the interaction term Post–Hedge Fund Activism × Treatment has a coefficient of −0.18 (p = .02), consistent with Hypothesis 1. In terms of economic magnitude, relative to non-targeted control firms, the strategic action intensity of firms targeted by a hedge fund activist decreases by 16.34% (from 11.63 to 9.73) in the 3 years following hedge fund activism.

Results From Difference-in-Differences Regressions

Note. Robust standard errors clustered by firms reported in parentheses. Two-tailed tests.

p < .1.

p < .05.

p < .01.

Hypothesis 2 suggests that firms will also experience a reduction in their strategic action complexity following hedge fund activism. In Model 2, the coefficient for Post–Hedge Fund Activism × Treatment is negative and significant (β = −0.33, p = .01). Economically, the strategic action complexity index of firms targeted by a hedge fund activist, relative to non-targeted control firms, decreases by 33.33% (from 0.99 to 0.66) in the 3 years following hedge fund activism.

Hypothesis 3 predicts firms will increase their strategic action intensity after being targeted by a corporate shareholder activist. In support of Hypothesis 3, the coefficient in Model 3 for Post–Corporate Shareholder Activism × Treatment is 0.74 (p = .009). Relative to nontargeted control firms, the strategic action intensity of firms targeted by a corporate shareholder activist increases by 109.09% (from 4.73 to 9.89) in the 3 years following corporate shareholder activism.

Hypothesis 4 suggests that firms targeted by a corporate shareholder activist also increase their strategic action complexity in the following years. As reported in Model 4, the coefficient for Post–Corporate Shareholder Activism × Treatment is 0.75 (p = .01), supporting Hypothesis 4. Here, relative to non-targeted control firms, firms targeted by a corporate shareholder activist increase their strategic action complexity by roughly 4 times (from 0.25 to 1.00) in the 3 years following corporate shareholder activism.

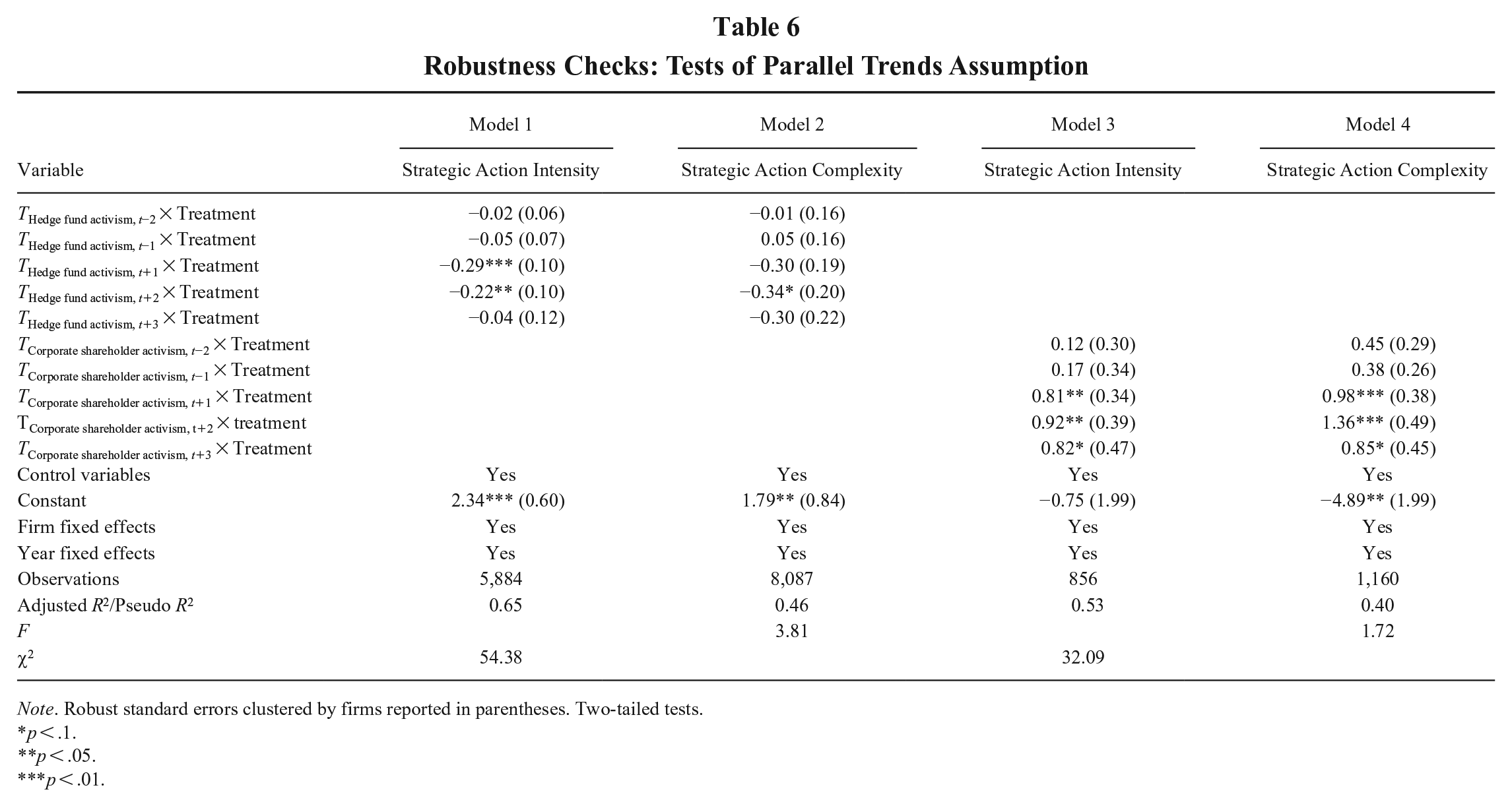

Robustness Checks

We conduct various additional analyses to assess the robustness of our findings. First, we assess whether our empirical context meets the parallel trends assumption of DID regressions. Following Autor (2003), we create six dummy variables for each sample, denoting whether the firm-year is 1, 2, or 3 years before or after the year of each hedge fund activism or corporate shareholder activism event. Using these variables, we replace the interaction term in our main models with the interaction of each dummy variable and treatment and rerun our regressions. As shown in Table 6, the coefficients for THedge fund activism, t−2 × Treatment (β = −0.02, p = .74) and THedge fund activism, t−1 × Treatment (β = −0.05, p = .43) are both not significant with strategic action intensity as the dependent variable, suggesting that there are common trends between the control and treatment groups before hedge fund activism. The coefficients for THedge fund activism, t+1 × Treatment (β = −0.29, p = .003) and THedge fund activism, t+2 × Treatment (β = −0.22, p = .04) are both negative and significant, while the coefficient for THedge fund activism, t+3 × Treatment (β = −0.04, p = .76) is not significant, implying that the reduction in strategic action intensity for treatment firms mainly occurs in the first 2 years following hedge fund activism. Similarly, the coefficients for THedge fund activism, t−2 × Treatment (β = −0.01, p = .94) and THedge fund activism, t−1 × Treatment (β = 0.05, p = .78) are both not significant with strategic action complexity as the dependent variable, again suggesting common trends between the control and treatment groups in the years leading up to hedge fund activism. The coefficient for THedge fund activism, t+2 × Treatment (β = −0.34, p = .08) is negative while the coefficients for THedge fund activism, t+1 × Treatment (β = −0.30, p = .10) and for THedge fund activism, t+3 × Treatment (β = −0.30, p = .18) are both not significant, implying that the reduction in strategic action complexity for treatment firms mainly occurs 2 years following hedge fund activism.

Robustness Checks: Tests of Parallel Trends Assumption

Note. Robust standard errors clustered by firms reported in parentheses. Two-tailed tests.

p < .1.

p < .05.

p < .01.

As reported in Model 3, the coefficients for TCorporate shareholder activism, t−2 × Treatment (β = 0.12, p = .70) and TCorporate shareholder activism, t−1 × Treatment (β = 0.17, p = .61) are both not significant, suggesting that the control and treatment groups have common trends in strategic action intensity before corporate shareholder activism. The coefficients for TCorporate shareholder activism, t+1 × Treatment (β = 0.81, p = .02), TCorporate shareholder activism, t+2 × Treatment (β = 0.92, p = .02), and TCorporate shareholder activism, t+3 × Treatment (β = 0.82, p = .08) are all positive and significant, implying that the increase in strategic action intensity for firms subject to corporate shareholder activism persists for 3 years, which coincides with these activists’ longer holding periods. In Model 4, the coefficients for TCorporate shareholder activism, t−2 × Treatment (β = 0.45, p = .12) and TCorporate shareholder activism, t−1 × Treatment (β = 0.38, p = .14) are both not significant, again suggesting common trends in strategic action complexity among the control and treatment groups in the years leading up to corporate shareholder activism. The coefficients for TCorporate shareholder activism, t+1 × Treatment (β = 0.98, p = .01), TCorporate shareholder activism, t+2 × Treatment (β = 1.36, p = .01), and TCorporate shareholder activism, t+3 × Treatment (β = 0.85, p = .06) are all positive suggesting the increase in strategic action complexity persists throughout the full post–corporate shareholder activism period.

Second, to supplement our main analyses, we test changes in strategic action intensity and strategic action complexity using 4- and 8-year windows (instead of 6-year windows, as in our main analyses) around the hedge fund activism and corporate shareholder activism events. In unreported results (available upon request), we find support for all hypotheses when using the 4-year window. We also find support for all the hypotheses except Hypothesis 4 when using the 8-year window.

Third, we did not initially exclude firms targeted by a corporate shareholder activist that were subsequently acquired within 3 years after the campaign. However, since including such firms may bias our sample, we use the SDC M&A database to identify the 10 firms that were acquired in this window. After dropping these firms from the sample, we continue to find a positive influence of corporate shareholder activism on strategic action intensity (β = 0.81, p = .02) and strategic action complexity (β = 0.61, p = .04). In addition, to ensure that our findings are not driven by potential alliances between corporate shareholder activists and targeted firms, we also use the SDC Alliance database to identify one case where the targeted firm and its corresponding corporate shareholder activist formed an alliance. Dropping this case also does not affect our results.

Fourth, we have conducted propensity score weighted firm fixed-effects regressions to test our hypotheses. Despite the advantages of these models, concerns associated with time-variant firm heterogeneity can remain, leading us to assess the impact threshold for a confounding variable (ITCV). Frank (2000) cautions that the ITCV should not be used for nonlinear models. Since we use firm fixed-effects Poisson regressions to test Hypotheses 1 and 3, we calculate the threshold for the percentage of bias to invalidate our inferences for these models instead of using the ITCV. To invalidate the negative effect of hedge fund activism on strategic action intensity, 27.88% (1,640) of cases would need to be replaced with cases for which there is an effect size of zero. Given that our main regression model explains 65% of the variation in our strategic action intensity variable, our results appear robust to potential correlated omitted variables. Similarly, to invalidate the positive effect of corporate shareholder activism on strategic action intensity, 37.03% (317) of cases would need to be replaced with cases where the effect size is zero. Again, in light of the regression model that explains 53% of the variation in strategic action intensity, the main results seem robust to potential correlated omitted variables.

As we use OLS regression to test Hypotheses 2 and 4, we calculate both the ITCV and the percentage of bias to invalidate our inferences. Here, the ITCV must be 0.011, and 36.24% (2,931) of cases would need to be replaced with a zero effect size to invalidate the negative effect of hedge fund activism on strategic action complexity. The strongest impact factor of any control variable is 0.026 (for firm size); yet, given that our main model explains nearly 46% of the variation in strategic action complexity, we conclude that these findings are again relatively robust to potential correlated omitted variables. Similarly, the ITCV must be 0.029, and 36.29% (421) of cases would need to be replaced with a zero effect size to invalidate the positive effect of corporate shareholder activism on strategic action complexity. Given that our main model explains nearly 40% of the variation in strategic action complexity and the strongest impact factor of any control variable is 0.014 (again for firm size), these findings again appear robust to potential correlated omitted variables.

Supplementary Analyses

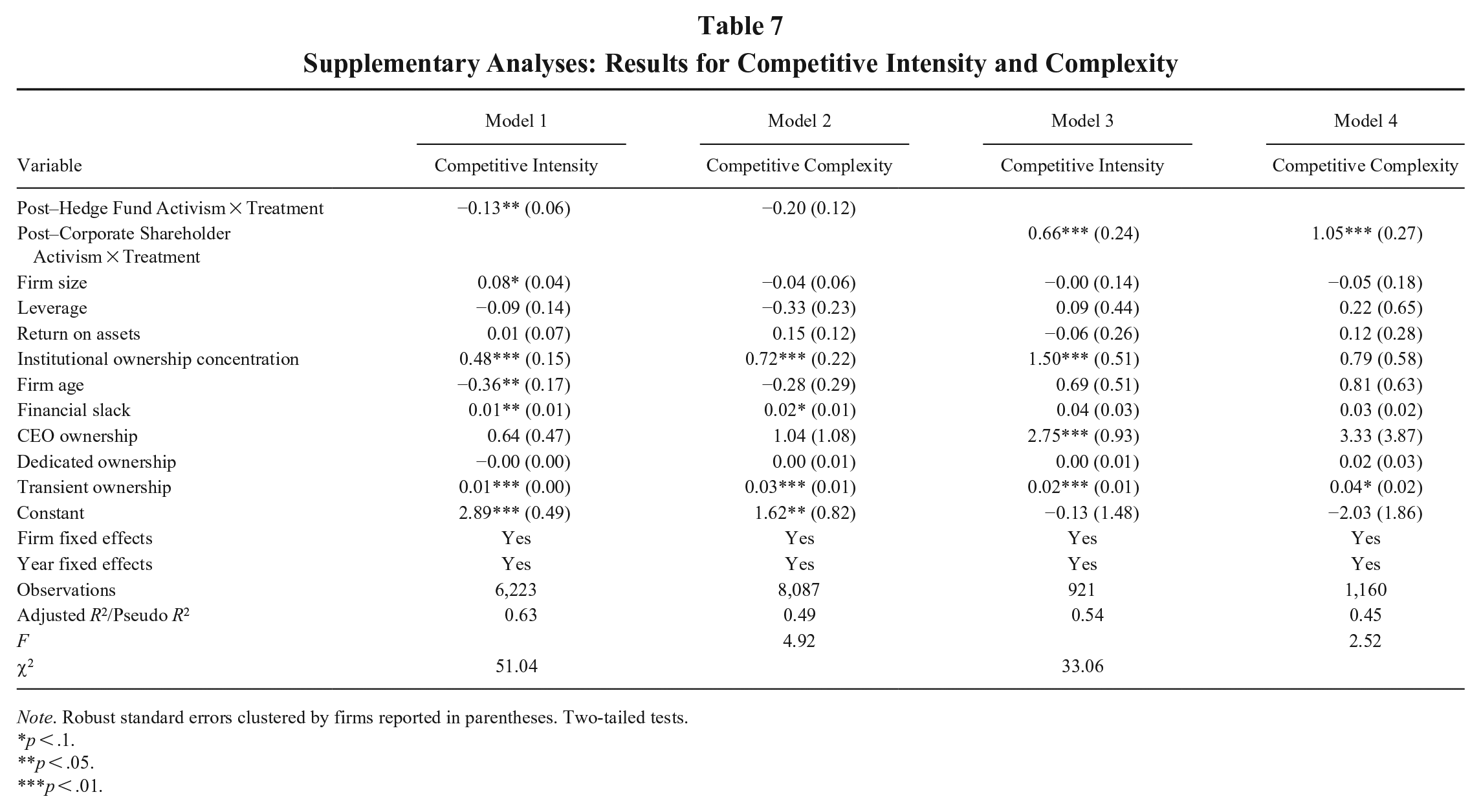

Our analyses so far have focused only on strategic actions. To check whether our findings are robust to the inclusion of tactical actions (i.e., competitive actions related to pricing, marketing, and legal issues 5 ), we include both strategic actions and tactical actions to construct variables for competitive intensity and competitive complexity.

Reported in Table 7, results from Models 1 and 2 show hedge fund activism reduces targeted firms’ competitive intensity (β = −0.13, p = .04) but has no effect on competitive complexity (β = −0.20, p = .11). Results from Models 3 and 4 reveal corporate shareholder activism increases targeted firms’ competitive intensity (β = 0.66, p = .007) and competitive complexity (β = 1.048, p = .000) when considering both tactical and strategic actions.

Supplementary Analyses: Results for Competitive Intensity and Complexity

Note. Robust standard errors clustered by firms reported in parentheses. Two-tailed tests.

p < .1.

p < .05.

p < .01.

Discussion

This study investigates the heterogeneous influence of hedge fund activism and corporate shareholder activism on targeted firms’ strategic actions. Whereas hedge fund activism decreases the intensity and complexity of firms’ strategic actions, corporate shareholder activism increases the intensity and complexity of those actions. These findings are robust to various model specifications, matching procedures, and alternative measurements. We now discuss the implications these findings have for multiple streams of research.

Theoretical Implications

Shareholder activism is a widely studied topic in both management and finance research (for reviews, see Denes et al., 2017; Goranova & Ryan, 2014). Despite the numerous studies that acknowledge heterogeneity among shareholders in general (e.g., Boh et al., 2020), most research has continued to study activist shareholders in silos, considering only one type of activist shareholder at any given time. Given that these prior studies use different observation periods, outcome variables, and analytical models, it is difficult to comprehend the various influences that different types of activist shareholders have on their corporate targets. Our study takes the unusual approach of theoretically highlighting the differences between hedge fund activists and corporate shareholder activists and empirically unpacking their distinct effects on firms’ competitive strategies.

Our study stresses that hedge fund activists and corporate shareholder activists are markedly different. Unlike hedge fund activists, which target companies primarily to maximize immediate returns to shareholders (DesJardine et al., in press; DesJardine & Durand, 2020), corporate shareholder activists intervene largely to bolster their own business and long-term vitality. Given these contrasting objectives and priorities—and the investment horizons over which they seek to accomplish them—our findings show that hedge fund activists and corporate shareholder activists have opposing effects on the strategic actions of target firms. Whereas hedge fund activists reduce and simplify these actions by straining the resources of target firms and constraining managerial discretion, corporate shareholder activists increase and complexify strategic actions by presenting an opportunity that grants more resources to firms and extends managerial leeway to experiment with new activities. Hence, our work underscores the importance of directly considering and contrasting the effects of different forms of activism in single empirical studies.

Beyond comparing these effects between the two types of activists, we further highlight the significant role shareholders play in shaping firms’ competitive strategies. Connelly and colleagues (2019); Connelly and colleagues (2010); and Connelly and colleagues (2017) provide extensive evidence that distinct institutional investors can differentially shape firms’ competitive actions. Yet, such research has focused on the level of ownership by institutional investors that have not taken intervening roles as activists. Our findings indicate that targeting by shareholders who use an activist strategy can also influence firms’ competitive actions. Our study further extends existing research on investor influence by highlighting that targeting by different types of activist shareholders can shape both the intensity and complexity of targeted firms’ competitive strategies.

Lastly, our findings provide a broader scope on corporate blockholders’ effects on target firms. Prior research has shown that corporate blockholdings tend to be negatively associated with target firms’ performance (e.g., Bogert, 1996). Such performance effects are suggested to arise because these large owners are uniquely positioned to expropriate wealth from firms for their own interests. For example, Rosenstein and Rush (1990) find that target firms transfer goods and services at prices that are unusually favorable to corporate blockholders. Such findings reveal that for targeted firms, corporate blockholder “capital comes at a price” (Connelly, Hoskisson, et al., 2010: 1567). Prior studies, however, overlook the idea that corporate blockholders may actively invest in targeted firms for broader strategic purposes, aimed at building the targeted firms’ business rather than exploiting and undermining it. By highlighting the strategic benefits of doing so, and isolating our sample to activism campaigns, we show that the strategies of targeted firms can be bolstered by corporate blockholders.

Opportunities for Future Research

Our study is not without limitations, which we hope present avenues for future research. Foremost, while we have added granularity by distinguishing among different types of activist shareholders, we measured changes in strategic actions at a fairly high level. Given that strategic actions are of different types, and tactical actions add additional variance, it is possible that hedge fund activists and corporate shareholder activists also have differing influences on firms’ individual competitive actions. Consider, for instance, their contrasting strategies to improve sales: Whereas hedge fund activists might lead firms to bolster their marketing efforts, corporate shareholder activists could encourage launching more products. Our measure of strategic actions overlooks such nuances, which are important to consider as future research further unpacks and compares the specific and distinct effects of different types of activist shareholders on corporate strategy.

Second, in addition to hedge funds and nonfinancial corporations, many other types of shareholders use activism to shape corporate affairs to suit their interests. In terms of influencing targeted firms’ strategic actions, activist pension funds are of particular intrigue. Similar to hedge fund activists, activist pension funds need to improve the value of targeted firms to return profits to their investors. However, pension funds also typically espouse more social concerns and, akin to strategic activists, have long investment horizons. Pension funds thus comprise a blend of hedge fund activists and corporate shareholder activists, making it worth considering how they might uniquely shape targeted firms’ strategies. Going one step farther, future research may also study the different tactics employed by various types of activists. Do hedge fund activists have differing effects on targeted firms’ strategic actions when they are more or less aggressive in their campaigns (Wiersema et al., 2020)? Do outcomes differ when campaigns are settled privately or when they conclude by proxy battle (Bebchuk, Brav, Jiang, & Keusch, 2020)?

Finally, in an effort to make the comparisons between the two forms of activism as concrete as possible, we focused our study on the direct effects of hedge fund activism and corporate shareholder activism on strategic actions. Yet, it is likely that multiple factors across various levels of analysis could alter these relationships. In unreported analyses, we explored the role of financial slack but found that it significantly moderates only the relationship between corporate shareholder activism and strategic action intensity. Beyond slack, hedge fund activism may have an even stronger negative effect on strategic actions when managers have little experience with such actions. Future research could shed further light on the effects of shareholder activism on firms’ competitive strategies by accounting for factors that moderate these relationships.

Conclusion

Activist shareholders are facing increased scrutiny for the profound influences they can have on their corporate targets. Many policies that regulate these shareholders, such as disclosure requirements with Schedule 13D filings, pertain to all activist types. And yet, as our study underscores, activist shareholders are not all cut from the same cloth, with their effects on targeted firms varying widely, especially relating to changes in corporate strategy. As managers, policy makers, and investors wrestle to comprehend and navigate the effects of activist shareholders, it is important that they understand and account for activists’ differing objectives, priorities, and investment horizons.