Abstract

The Behavioral Theory of the Firm suggests that performance below an aspiration triggers problemistic search that can lead to organizational change and risk-taking. This compelling perspective has spawned considerable empirical examination of diverse strategic outcomes as firms’ responses to performance feedback. However, empirical studies have provided inconsistent evidence of problemistic search effects on various organizational search outcomes. This empirical controversy is likely attributed to the fact that most research has considered problemistic search as a firm-level and relatively routinized process with a high degree of automaticity in firms’ responses to performance feedback while overlooking the role of managerial agency. Rather than viewing problemistic search as an automatic firm-level process, we believe that behavioral responses are shaped, at least partially, by top executives, notably CEOs. To this end, we first examine whether problemistic search effects vary across a range of organizational change and risk outcomes. We then explore whether the relative size of firm and CEO effects varies across different search outcomes. Using a multilevel approach, we show not only the heterogeneity in problemistic search effects on different organizational outcomes but also heterogeneity in the relative size of firm and CEO effects on these outcomes. While firm effects are substantial in directing some strategic decisions, as proposed by the problemistic search model, CEO effects are large for certain organizational outcomes, such as changes in resource allocation. This study serves as a jumping-off point for future theorizing and empirical work on problemistic search that incorporate the role of managerial agency.

Keywords

Introduction

The Behavioral Theory of the Firm (BTOF) (Cyert & March, 1963) provides a compelling perspective on why firms initiate change and undertake risk. It argues that organizational decision makers use aspirations to evaluate performance and that performance below aspirations triggers problemistic search (Cyert & March, 1963). Building on this theoretical model, many empirical studies have shown that performance below aspirations acts as a “master switch” (Greve, 2003a: 76) that triggers a wide variety of organizational change and risk outcomes, such as new product introduction (Gaba & Joseph, 2013; Parker, Krause, & Covin, 2017), innovation (Greve, 2003b), alliance partner selection (Shipilov, Li, & Greve, 2011), acquisitions and divestitures (Desai, 2016; Iyer & Miller, 2008; Kuusela, Keil, & Maula, 2017), research and development (R&D) (Chen, 2008; Vissa, Greve, & Chen, 2010; Ye, Yu, & Nason, 2021), knowledge investment (Ben-Oz & Greve, 2012), resource allocation (Sengul & Obloj, 2017), and new market entry (Ref & Shapira, 2017).

Despite the prominence of this perspective, the current literature on problemistic search has at least two limitations. First, there has been inconsistent support for the problemistic search effect on diverse proxies of organizational change and risk, the two central behavioral outcomes examined in the problemistic search literature (Kacperczyk, Beckman, & Moliterno, 2015; Posen, Keil, Kim, & Meissner, 2018). While some studies have shown a positive relationship between a firm's performance below aspiration and its propensity to change or take risk, others have found a negative or null relationship (for a detailed review, see Kotiloglu, Chen, & Lechler, 2021; Posen et al., 2018; Shinkle, 2012). This highlights a need to systematically examine problemistic search effects across different organizational outcomes and points to potential issues regarding how the problemistic search model was conceptualized or tested in prior studies.

Second, the existing literature on problemistic search has primarily assumed “a high degree of automaticity in firms’ response to performance feedback and an overly routinized process of search” (Posen et al., 2018: 231), while overlooking the role of managerial agency. That is, most research has assumed that different firms will take similar strategic actions in response to similar performance feedback without accounting for the impact of idiosyncratic managerial agency in firm decision making. Emphasizing this, Greve (2018: 96) recently argued that “what is not sufficiently explained is how the individual managerial experience and myopic cognitions aggregate to influence firm-level decisions, especially when performance below aspiration levels indicates a need for change…”. Indeed, the Carnegie School (Cyert & March, 1963; March & Simon, 1958; Simon, 1947) has long emphasized the important role of managerial agency in firm decision making and spawned significant research related to how managerial characteristics affect firm decisions and outcomes (Hambrick & Mason, 1984). Despite this, there have been only a few studies (i.e., Blagoeva, Mom, Jansen, & George, 2020; Cho, Arthurs, Townsend, Miller, & Barden, 2016; Lim & McCann, 2014; Titus, Parker, & Covin, 2020; Tuggle, Sirmon, Reutzel, & Bierman, 2010; Wangrow, Kolev, & Hughes-Morgan, 2019) theorizing and integrating the role of managerial agency into the problemistic search model. While insightful, these studies have not answered the critical question about whether the relative size of firm and CEO effects varies across different search outcomes.

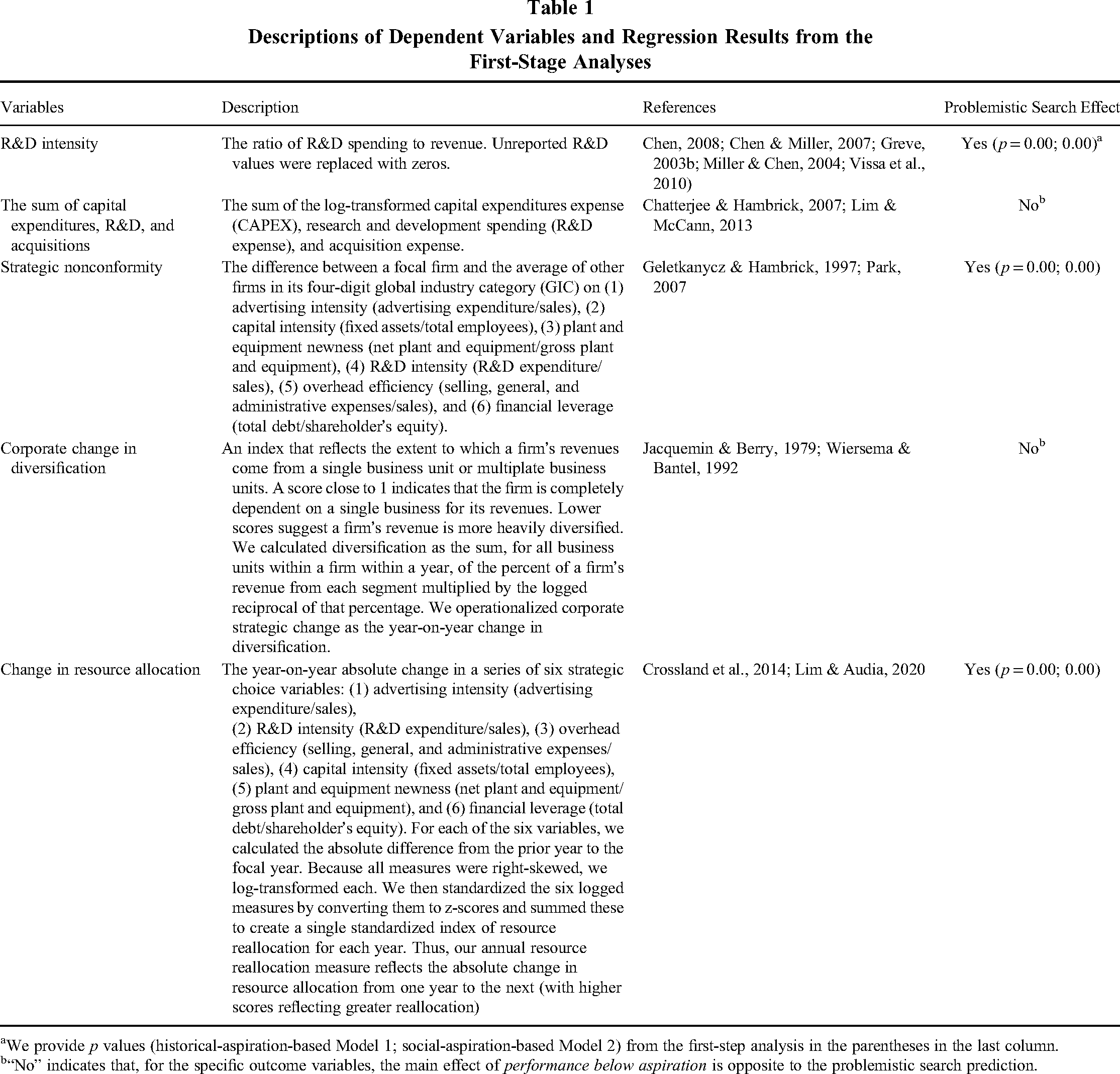

To this end, we take an empirical approach to address two interrelated questions. The first question is: Do the effects of problemistic search, or performance below aspiration, vary across different organizational change and risk outcomes? Answering this question can help disentangle the possible causes underlying the empirical controversy on problemistic search effects in prior studies. If we find differing relationships between performance below aspiration and a variety of search outcomes in a single study, then there are potential boundary conditions and contingencies that can be used to extend the problemistic search model. Specifically, we examine a set of organizational change and risk outcomes that have been widely investigated in the relevant literature, including R&D intensity (Chen, 2008; Chen & Miller, 2007; Greve, 2003b; Vissa et al., 2010); the sum of capital expenditures, R&D, and acquisitions (Chatterjee & Hambrick, 2007; Lim & McCann, 2013); strategic nonconformity (Geletkanycz & Hambrick, 1997; Park, 2007); corporate change in diversification (Jacquemin & Berry, 1979; Wiersema & Bantel, 1992); and change in resource allocation (Crossland, Zyung, Hiller, & Hambrick, 2014; Lim & Audia, 2020).

Building on this, our second question addresses the automaticity assumption of problemistic search by considering the (varying) size of the effects that CEOs and firms have on different outcomes of problemistic search. Specifically, we ask: Do CEOs affect the link between performance below aspiration and search outcomes, and if so, do CEO effects relative to firm-level effects vary across different search outcomes? If, as generally presented in the extant literature, problemistic search is a firm-level phenomenon with a high level of automaticity, then CEOs should have a limited impact on the link between performance below aspiration and organizational search outcomes. If this is the case, there would be little reason to investigate how managers impact problemistic search. In contrast, if the CEO effect on problemistic search is meaningful and if the relative size of firm and CEO effects varies across different search outcomes, then it underscores the need to extend the current problemistic search model by incorporating managers’ characteristics and decision-making perspectives.

To investigate these questions, we build on a long history of research in the organizational sciences that has used various forms of variance decomposition to identify the categories of factors that explain the most variance in outcomes of interest, such as those considering the relative importance of industry- vs. corporate-level factors on business unit performance (Bowman & Helfat, 2001; McGahan & Porter, 1997, 2005; Rumelt, 1991) or agentic versus contextual factors in determining firm-level outcomes (Lieberson & O’Connor, 1972; Mackey, 2008; Quigley & Hambrick, 2015). Building on the most recent work in these adjacent areas (Meyer-Doyle, Lee, & Helfat, 2019; Misangyi, Elms, Greckhamer, & Lepine, 2006; Quigley & Graffin, 2017), we use a multilevel approach to estimate the relative size of firm and CEO effects on the outcomes of problemistic search.

Based on an analysis of Standard and Poor's (S&P) 1500 firms from 1992 to 2018, we find that (1) the effects of problemistic search vary across different organizational change and risk outcomes; (2) both firms and CEOs are substantially related to variance in the effects of problemistic search; (3) the relative size of firm and CEO effects varies across different search outcomes; and (4) counter to prevailing theory focused on firm factors, we find CEOs explain more variance than firm factors in the effect of problemistic search on some organizational change and risk outcomes, particularly when the performance is measured against historical aspirations.

This study makes several contributions to the problemistic search literature. First, by demonstrating the varying effects of problemistic search on multiple organizational change and risk outcomes within a single study, it helps to reconcile the inconsistency of the empirical evidence on problemistic search effects. Specifically, it deviates from prior studies’ focus on the empirical issues (e.g., differences in contexts or measures of aspirations across empirical studies) in explaining the inconsistency (e.g., Bromiley & Harris, 2014) and instead highlights potential issues of the problemistic search model. Put differently, this study suggests that some extension or reconceptualization of problemistic search is crucial to gaining a more comprehensive understanding of firm decision making. Second, we document the relative size of firm and CEO effects in problemistic search. Though our results affirm the importance of firm-level factors, the focus of the original model, we also demonstrate that CEO factors are meaningful. Beyond this, we demonstrate the heterogeneity in the relative size of firm versus CEO effects on different organizational change and risk outcomes. Based on these findings, we offer a set of ideas regarding how to extend the problemistic search model by incorporating managerial agency into the (sub)processes of problemistic search. These together serve as a jumping-off point for future theorizing and empirical research on problemistic search.

Further, this study also contributes to the literature on CEO effects. Prior CEO effects studies (e.g., Lieberson & O’Connor, 1972; Mackey, 2008; Quigley & Hambrick, 2015) have generally focused on performance outcomes and are typically silent about how CEOs affect these outcomes. Joining a few recent works (Meyer-Doyle et al., 2019; Wernicke, Sajko, & Boone, in press), this study considers how much impact CEOs have on an important mechanism through which CEOs ultimately influence firm performance outcomes, namely problemistic search. Furthermore, while prior studies have generally focused on the CEO effects in the context of firm performance (e.g., Mackey, 2008; Quigley & Hambrick, 2015) or a particular strategic action such as acquisitions (e.g., Meyer-Doyle et al., 2019), our study extensively examines CEO effects on a set of strategic actions driven by problemistic search. It not only shows that CEOs may matter more for some strategic actions than others but also suggests that CEOs may matter more when firms focus on historical aspirations than when they attend to social aspirations. These are important additions to the literature because while it has long been understood that leaders matter more or less depending on the context (Hambrick & Finkelstein, 1987), our study demonstrates that leaders also matter more or less depending on the specific strategic actions and aspiration types under investigation.

Background

Problemistic Search and Managerial Agency

The problemistic search model predicts a positive relationship between a firm's performance feedback and its tendency to initiate change or undertake risk. While this theoretical prediction is both parsimonious and appealing, empirical evidence on this prediction has been mixed. Indeed, while many studies found support for a negative relationship between a firm's performance feedback and its propensity to change or take risk (e.g., Baum, Rowley, Shipilov, & Chuang, 2005; Chen, 2008; Gaba & Joseph, 2013; Greve, 2003a; Shipilov et al., 2011), others showed a positive or null relationship between the two (e.g., Audia & Greve, 2006; Iyer & Miller, 2008; Miller & Bromiley, 1990; Wiseman & Bromiley, 1996).

To reconcile this inconsistency, some scholars have begun to focus on empirical issues related to how the theoretical prediction was tested, such as differences in measures of key constructs including risk and aspirations (e.g., Bromiley & Harris, 2014; Kacperczyk et al., 2015; Wiseman & Bromiley, 1996) and empirical contexts (Posen et al., 2018; Shinkle, 2012) across studies. Other studies have tried to reconcile these mixed findings by attending to the theoretical issues related to the boundary conditions of the problemistic search model; they have examined firm-specific moderating factors, such as firm size (Audia & Greve, 2006), slack and proximity to bankruptcy (Chen & Miller, 2007), governance arrangement (Lim & McCann, 2014), organization structure (Joseph, Klingebiel, & Wilson, 2016), and resource constraints (Kuusela et al., 2017). Although insightful, these studies have generally considered problemistic search as a firm-level and relatively routinized process while overlooking the role of managerial agency. This is somewhat surprising given that the BTOF in which the problemistic search model is rooted has long emphasized the crucial role of dominant coalitions in firm decision making. According to Cyert and March (1963), it is the dominant coalition's interests and preferences that guide an organization's attention and responses to particular stimuli, such as performance shortfalls (Gavetti, Greve, Levinthal, & Ocasio, 2012).

Promisingly, a few recent studies have started to incorporate the role of managerial agency by examining how executives’ attributes, such as CEO cognitions (Wangrow et al., 2019), power (Blagoeva et al., 2020), duality (Tuggle et al., 2010), status (Cho et al., 2016), entrepreneurial orientation (Titus et al., 2020), and TMT characteristics (Kolev & McNamara, 2020), influence firm problemistic search. These studies have generally treated executives’ characteristics as moderators in the relationship between performance feedback and firm search outcomes. A few other studies have focused on how a firm's coalitions of actors (Desai, 2016; Hu, He, Blettner, & Bettis, 2017; Lim & McCann, 2014) bound the conditions under which underperformance leads to search.

Though some progress has been made in understanding the mixed problemistic search effects and the role of managerial agency in problemistic search, the literature still faces limitations. First, prior empirical research has not systematically examined whether the effects of problemistic search vary across different organizational change and risk outcomes in a single study. Doing so can help disentangle several empirical issues underlying the empirical controversy, such as the differences in samples, construct measurements, and contexts. Second, because problemistic search is generally viewed as a firm-level phenomenon, prior studies did not consider how much CEOs affect the search process and whether CEOs matter more for some search outcomes than others. Answering these questions can facilitate future theorizing and empirical work on problemistic search that incorporates the role of managerial agency.

The Role of Firms Versus Leaders

Research in management has firmly established the relative importance of leaders, and CEOs in particular, to firm outcomes while also highlighting that their impact may differ substantially across various settings (Crossland & Hambrick, 2007, 2011; Finkelstein & Boyd, 1998; Hambrick & Finkelstein, 1987; Lieberson & O’Connor, 1972; Meyer-Doyle et al., 2019). Beginning in the early 1970s (Lieberson & O’Connor, 1972), studies of the “CEO effect” have found that CEOs are responsible for a substantial proportion of the variance in firm outcomes (Mackey, 2008; Quigley & Hambrick, 2015), with estimates of their impact ranging from 14% (Lieberson & O’Connor, 1972; Wasserman, Anand, & Nohria, 2010) to perhaps as much as 38.5% (Hambrick & Quigley, 2014). Studies have also demonstrated that the CEO effect is increasing over time, both in terms of measured effects on outcomes such as return on assets (ROA) (Quigley & Hambrick, 2015) and on more subjective measures such as investor perceptions of CEO importance (Quigley, Crossland, & Campbell, 2017).

Furthermore, separate from the studies that specifically examine the CEO effect size, other research in this area has shown that managers have substantial leeway to carve their strategic path. For example, several studies have demonstrated the role of executive power in enacting strategic decisions (Adams, Almeida, & Ferreira, 2005; Child, 1972; Finkelstein, 1992; Haynes & Hillman, 2010; Ocasio, 1994). More recent work has documented the effect of CEOs’ personalities on important strategic decisions and firm outcomes (Gupta, Nadkarni, & Mariam, 2018; Harrison, Thurgood, Boivie, & Pfarrer, 2020; Nadkarni & Herrmann, 2010; Petrenko, Aime, Ridge, & Hill, 2016). Other studies have shown that CEOs affect their firms in unique ways, such that the perception of CEO characteristics affects how other firms attack focal firms in competitive dynamics (Hill, Recendes, & Ridge, 2019). Collectively, these studies highlight how managerial agency can shape firm outcomes.

However, just because adjacent literature has well documented that CEOs matter in firm decision making, we cannot automatically conclude that CEOs matter in problemistic search. Given that most work on problemistic search has still taken the “automaticity” assumption for granted, thus assuming away the role of managerial agency, we believe it is important to examine the relative size of firm and CEO effects on different organizational change and risk outcomes of problemistic search. To do so, we borrow from the CEO effects literature and take an empirical approach.

Method

Data and Sample

We started by selecting all firms in Execucomp from 1992 to 2018. Execucomp covers the S&P 1500 and some additional firms that are retained after leaving the index or added for the years just prior to joining. We then excluded financial firms (SIC 6000–6999), utility firms (SIC 4900–4999), and public administration firms and conglomerates (SIC 9100-9999) from the sample as these firms are subject to unique regulatory supervision that could drive firm decisions (Kayhan & Titman, 2007; Vanacker, Collewaert, & Zahra, 2017). We also excluded observations listed in the four-digit SIC industries with less than four firms for a given year (Chen & Miller, 2007) and observations that did not have a fiscal year ending in December to avoid cross-loading years. We gathered firm financial data from Compustat. Our final sample includes 20,374 firm-year observations for 3,815 CEOs within 1,844 firms. Our sample size is consistent with recent CEO effects studies using comparable periods (Fitza, 2014; Quigley and Graffin, 2017).

Dependent Variables

As described above, the empirical studies on problemistic search have modeled the relationship between the distance of performance below aspiration and different organizational change and risk outcomes. Thus, we focus on multiple outcome variables that are widely studied in the problemistic search literature and that can be measured and applied in a common sample of S&P firms. Specifically, we examine five proxies of organizational change and risk outcomes as summarized in Table 1.

Descriptions of Dependent Variables and Regression Results from the First-Stage Analyses

We provide p values (historical-aspiration-based Model 1; social-aspiration-based Model 2) from the first-step analysis in the parentheses in the last column.

“No” indicates that, for the specific outcome variables, the main effect of performance below aspiration is opposite to the problemistic search prediction.

Independent Variable

To calculate the distance of performance below aspiration, we first constructed the aspiration measure. Previous research uses several performance indicators to operationalize aspiration levels, such as ROA (Audia & Greve, 2006; Chen & Miller, 2007; Shimizu, 2007) and market share (Baum et al., 2005). We choose ROA not only given its salience in firm strategic decision making (Greve, 2003a; Posen et al., 2018; Shinkle, 2012) but also because ROA is a generic performance aspiration that conforms to our measures of broad change and risk undertaken by the firms (Greve, 2018). Consistent with the prior literature (Baum et al., 2005; Chen & Miller, 2007; Miller & Chen, 2004), we treated a firm's historical aspiration separately from its social aspiration, where historical aspiration was measured as the average performance over the prior 2 years (e.g., Arrfelt, Wiseman, & Hult, 2013), and social aspiration was calculated as the weighted average performance of peer S&P 1500 firms belonging to the same four-digit SIC industry based on the similarity between the focal firm and the target firm (Baum et al., 2005). Specifically, our size-weighted social aspiration used the absolute difference in size between the focal firm and the peer firm to discount attainment discrepancy and thus placed a higher weight on the performance of firms who are closer to the focal firm's size while including all firms in the same industry. Such operationalization represents a more fine-grained reference group that provides greater comparability to the focal firm in terms of product similarity and size similarity, as comparability is one of the most important factors influencing decision makers’ formation of organizational reference groups for social comparison (Greve, 2003a).

Following the literature (e.g., Miller & Chen, 2004), we used a spline function to split the performance feedback measure into two variables. The first is our independent variable, performance below aspiration, calculated as the value of performance minus aspiration for those observations with performance below aspiration and zero otherwise. Values were multiplied by negative one (−1), so that larger numbers represent an increasing performance shortfall relative to aspiration. We are primarily interested in performance below aspiration as a trigger of problemistic search. The other variable from the performance feedback split measure, coded as performance above aspiration, equals performance minus aspiration when performance is above or equal to aspiration and is set to zero otherwise. This variable is used as a control variable in our main analysis.

Control Variables

We include a focused set of control variables that directly affect search outcomes as documented in the BTOF literature—a firm's slack and proximity to bankruptcy (Chen & Miller, 2007; Posen et al., 2018), as prior studies using variance decomposition approaches generally included very few or no control variables (e.g., Misangyi et al., 2006). Firm slack represents a firm's available resources to initiate change or undertake risk. Following Chen and Miller (2007), we measured it as the combination of the standardized current ratio (current assets divided by current liabilities) and the working capital to sales ratio. Because approaching bankruptcy may trigger a firm's survival threat and make the firm rigid in its actions (Staw, Sandelands, & Dutton, 1981), we controlled for proximity to bankruptcy, measured using the Ohlson Index as it is one of the most well-established measures to predict the probability of firm bankruptcy (Ohlson, 1980; Wowak, Hambrick, & Henderson, 2011). Though controls are generally not included in most variance decomposition studies, the inclusion of firm slack and proximity to bankruptcy provides a more rigorous test of the firm versus CEO effects in explaining problemistic search as we can control for the variance attributable to search driven by slack (Cyert & March, 1963) and threat rigidity (Staw et al., 1981). However, excluding these controls does not meaningfully change our results.

To control for potential heterogeneity across years, we also included a set of year dummies. We also tried to include a set of industry dummies and did not find the addition of the industry dummies changes our results in any qualitatively meaningful ways (we discuss this issue in the Results section). All continuous variables were winsorized at 2% to adjust for outlier values (Christensen, Dhaliwal, Boivie, & Graffin, 2015; Dixon & Yuen, 1974).

Model

We take a two-step approach to answer the two interrelated research questions presented above. In the first step, we examine and compare the effects of problemistic search on different organizational change and risk outcomes as listed in Table 1. We focus on whether we could demonstrate significant effects of problemistic search (i.e., a positive relationship between performance below aspiration and search outcomes). In the second step, for the subset of outcome variables where we can observe significant effects of problemistic search, we examine how much variance in the positive relationship between performance below aspiration and search outcomes is attributable to the firm vs. the CEO and whether the relative size of firm and CEO effects varies across different search outcomes.

One methodological approach for dealing with the mixing of individual- and group (firm)-level variables is to adopt an approach more often associated with education psychology and organizational behavior, i.e., Hierarchical Linear Model (HLM) (Bryk & Raudenbush, 1992). HLM is most familiar in strategy and organization studies for its ability to attribute the variance in a dependent variable to nested groups (Misangyi et al., 2006; Short, Ketchen, Bennett, & du Toit, 2006). For example, Misangyi et al. (2006) and Short et al. (2006) used the approach to identify what percentage of variance in business-unit performance is attributable to the industry, corporate, or business-unit level. We employed the “mixed” procedure in STATA 15.1 to develop our HLM approach. 1 We lagged predictor variables by one year to reflect the causal direction in our analyses.

In addition to examining the variance in fixed-effect categorical variables, HLM can decompose the variance attributable to distinct groups in continuous independent variable effects (e.g., Arrfelt et al., 2013). In other words, HLM can decompose the variance in a model's regression coefficients as well as variance in a model's intercept. For example, Misangyi et al. (2006) decomposed the variance in the slope of industry capitalization into the industry and corporate effects when predicting business-unit profitability. Misangyi and colleagues used the technique, referred to as a random regression coefficient (RRC) model in other HLM work (Bryk & Raudenbush, 1992), to better explore the magnitude of their industry and firm effects, and to analyze whether industry or firm effect best describes a model to predict ROA. We used this same approach here to explore whether CEOs have a meaningful impact on problemistic search and, if so, how this effect versus the firm-level effect varies across different search outcome variables. To be clear, we decomposed the variance in the coefficient of performance below aspiration into year, firm, and CEO effects when predicting strategic choices driven by problemistic search. We were interested in comparing the proportions of the variance in the coefficient of performance below aspiration attributable to firms and CEOs across different outcome variables.

We used models that have the functional form below:

Thus, the outcomes for CEO i in firm j are as follows:

For each combination of our dependent variables and aspiration specifications, we created four mixed model estimations. The first is a model that holds

Next, we executed a model that included terms for both firm and CEO effects and again calculated the improvement in variance explained using a log-likelihood test. A positive test indicates that the introduction of the term explained incremental variance. Comparing this final model with each of the previous models allows us to determine which factors contribute meaningfully to the model's informativeness and fit.

Results

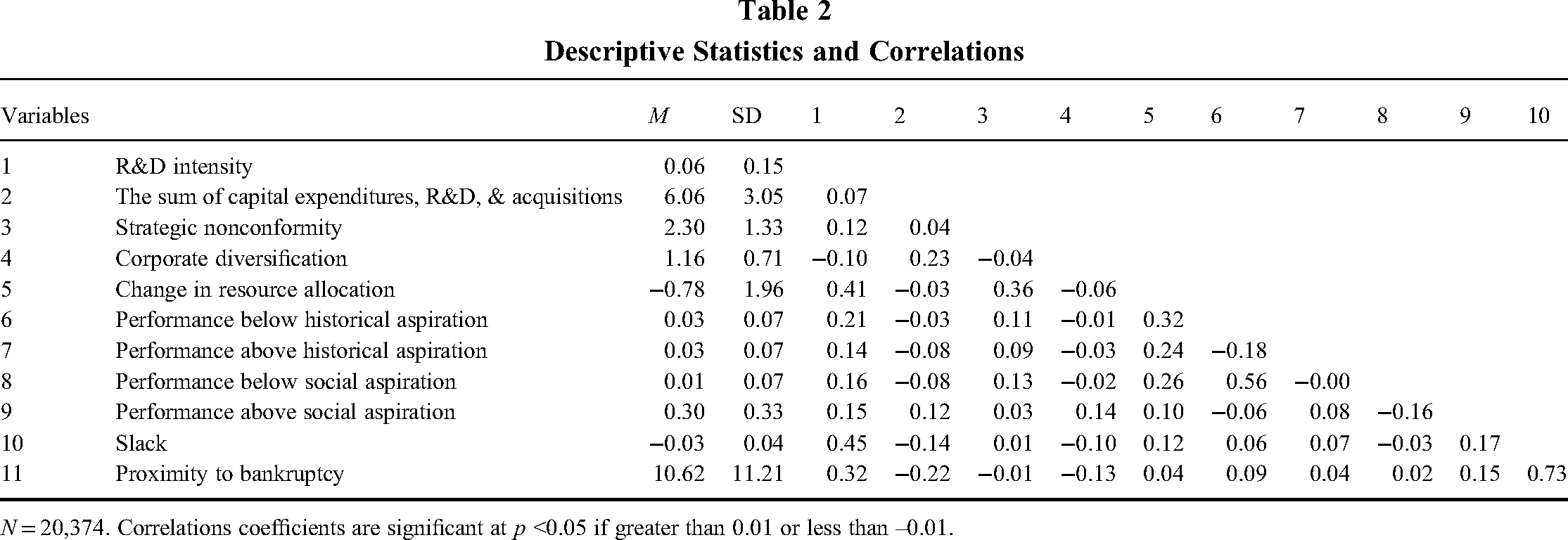

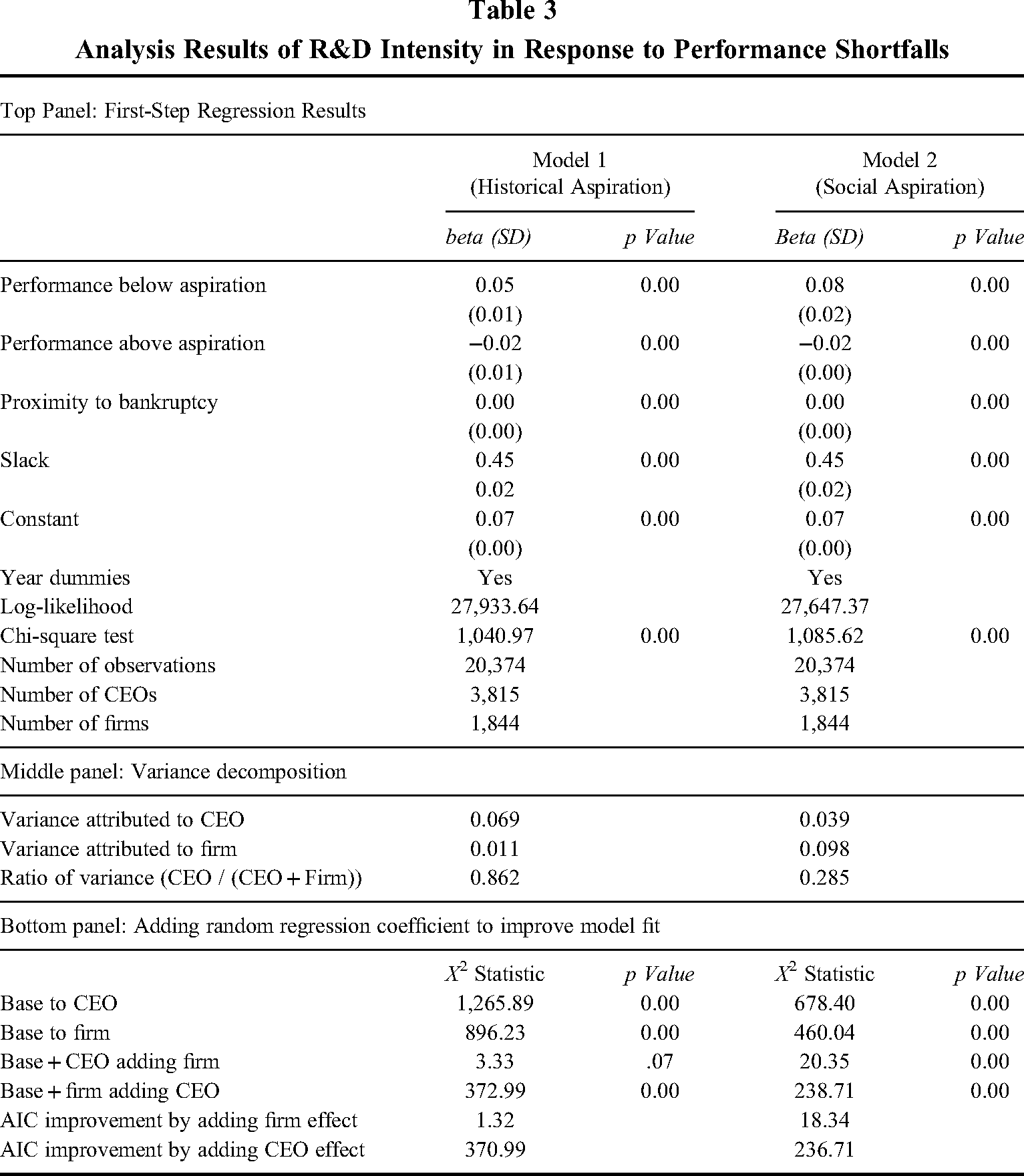

Table 2 reports variable means, standard deviations, and correlations. Since we have five outcome variables, to conserve space and present analysis results more parsimoniously, we present exemplary results using R&D intensity in Table 3 and then summarize the results for the other dependent variables in Table 1 and Table 4. Table 3 includes three panels, the top presenting the result of the first-step analysis regarding the demonstration of the effects of problemistic search on R&D intensity, the middle illustrating the result of the second-step analysis regarding the variance decomposition, and the bottom demonstrating whether the inclusion of the firm or CEO effect improves model fit as indicated by the log-likelihood test.

Descriptive Statistics and Correlations

N = 20,374. Correlations coefficients are significant at p <0.05 if greater than 0.01 or less than –0.01.

Analysis Results of R&D Intensity in Response to Performance Shortfalls

Model Fit Statistics for Different Outcome Variables

Models 1 and 2 of Table 3 report the results based on historical aspirations and social aspirations, respectively. Model 1 shows that performance below aspiration leads to greater R&D intensity (b = 0.05, p = 0.00), which provides support for the problemistic search prediction—as the magnitude of performance below aspiration increases, problemistic search activities increase. It also shows that the p value of the Omnibus chi-squared test is .00, suggesting that the explained variance in the set of data is significantly greater than the unexplained variance overall. In the middle panel, we report that the proportions of the variance in the coefficient performance below aspiration that is attributable to CEOs and firms are 0.069 and 0.011, respectively. 2 A higher variance at the CEO level means that more of the differences across firm-year observations are attributable to CEO factors rather than firm factors. That is, while we find that CEO- and firm-level factors each explain a meaningful portion of the variance in a firm's problemistic search effect on R&D intensity, the CEO effect is over six times the size of the firm effect, accounting for around 86.2% of the total variance explained by both firm and CEO factors. In the bottom panel, we find that the addition of CEO RRCs improves the model's log-likelihood at p < 0.001, as does the inclusion of firm-level RRCs alone. Also, if we include CEO RRCs after the firm effects, the model's log-likelihood improves at p < 0.001 (X2 = 372.99, p = 0.00); if we include firm RRCs after the CEO effects, the model's log-likelihood still improves (X2 = 3.33, p = 0.07), but not nearly as much as when we include the CEO effect after the firm effect.

The results from Model 2, based on social aspirations, again confirm that both CEO- and firm-level factors explain a meaningful portion of the variance in a firm's problemistic search effect on R&D intensity, although the CEO effects are smaller than the firm effects, accounting for 28.5% of the total variance explained by both firm and CEO factors. That is, the CEO effects are larger than firm effects in driving R&D intensity in response to underperformance relative to historical aspirations. In contrast, firm effects are larger than CEO effects in driving R&D intensity when firm performance is measured against social aspirations.

It is important to note that log-likelihood tests do not indicate whether the change in the model is meaningful, based solely on the chi-squared test. Often regression models provide a change in R-squared statistics to aid this interpretation. This creates a challenge for these analyses because there is no agreed-upon approach for calculation of R-squared type statistics in a RRC model (LaHuis, Hartman, Hakoyama, & Clark, 2014). Consequently, we have chosen to show the improvement in the AIC as a sample-size independent way to determine the model's increased informativeness. 3 AIC has the added advantage in that it introduces a penalty based on the number of parameter estimates and, as a result, does not automatically show an improved model fit as additional parameters are added to the model. Improvement (indicated by a decreased value) in the AIC shows that the inclusion of a parameter (or set of parameters in our case) improves the model's explanatory power. In Tables 3 and 4, we present the decreased value in the AIC from the base model to models adding firm effect, CEO effect, or both effects. Any improvement in AIC (i.e., decreased value) greater than 2 is a meaningful improvement, while an improvement greater than 10 represents a substantial improvement over the base model (Burnham & Anderson, 2004). In the bottom panel of Table 3, we do not observe a meaningful improvement in the AIC after the inclusion of the firm effect (1.32) but do find a strong improvement by adding the CEO effect (370.99) to Model 1; in Model 2, we observe a meaningful improvement in the AIC after the inclusion of the firm effect (18.34) and the CEO effect (236.71). The CEO RRC improves the model's informativeness over and above the firm effect, although introducing a firm-specific random coefficient also improves fit.

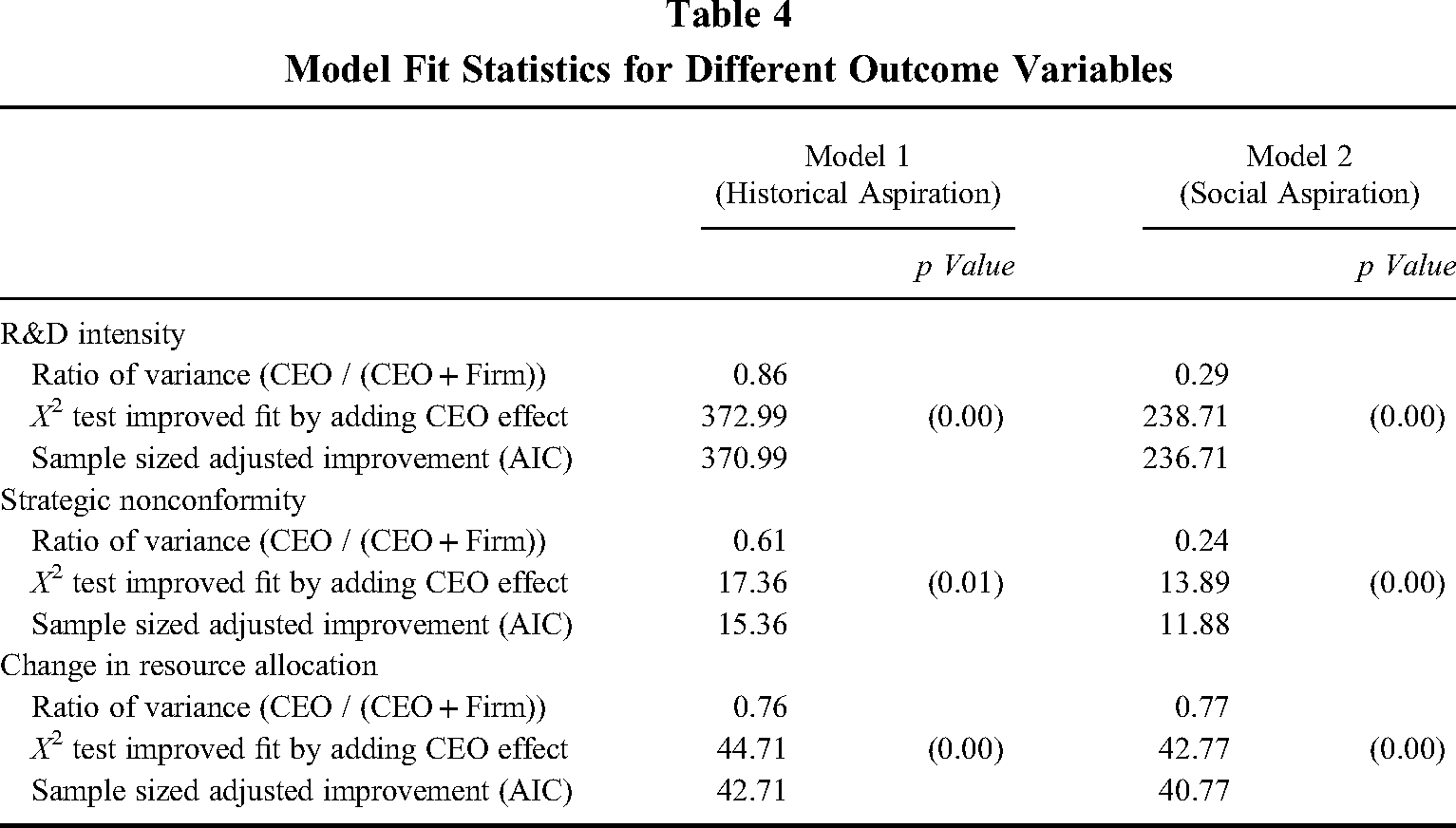

So far, we have reported all results using R&D intensity as the outcome variable. We now turn to the summary of results using other outcome variables. The last column of Table 1 summarizes the first-step analysis results for all outcome variables. Addressing our first research question, we observe meaningful effects of problemistic search on three out of the five outcome variables. These outcome variables are those whose first-step model's Omnibus test achieved p < 0.05, and the estimated coefficient of performance below aspiration is positive at p < 0.05. 4 Specifically, the results based on outcome variables R&D intensity, strategic nonconformity, and change in resource allocation provide support for the problemistic search prediction. Table 4 further summarizes the second-step analysis results for these three outcome variables. We report two models for each outcome variable, one based on historical aspirations and the other social aspirations. We present three important results for each outcome variable: (1) ratio of variance explained by CEO to total variance explained by CEO and Firm, (2) chi-squared test improved fit by adding CEO effect, and (3) model improvement (AIC).

The models based on historical aspirations (Model 1) show that CEOs explain more variance in problemistic search than do firms in the three outcome variables, with the ratio of variance explained by CEO to total variance explained by CEO and Firm higher than 50%, varying from 61% (strategic nonconformity) to 86% (R&D intensity). The results also show a meaningful improvement in informativeness in models based on historical aspirations for all three outcome variables, with an improvement in AIC ranging from 15.36 (strategic nonconformity) to 370.99 (R&D intensity) after introducing a CEO-level RRC.

The models based on social aspirations (Model 2) show that both CEOs and firms explain significant portions of the variance of problemistic search, with CEOs explaining more in terms of change in resource allocation, while firm effects explaining more in terms of R&D intensity and strategic nonconformity. The results also show a meaningful improvement in informativeness (with an improvement in AIC > 2.0) by introducing a CEO-level RRC for all three outcome variables.

While we did not set out to specifically test or demonstrate the differences between the models based on historical and social aspirations, it is interesting to observe that historical and social aspirations seem to play different roles in guiding firm strategic choices. Our results imply that CEOs are more responsive to firm performance feedback based on historical aspirations than social aspirations, in directing search outcomes, such as R&D intensity and strategic nonconformity. As discussed below, these initial findings provide numerous opportunities for future research.

Robustness Checks

We conducted several tests to evaluate the robustness of our results. The first is associated with the use of alternative measures of the aspiration variables. In our main results, we measured historical aspirations based on the average performance over the prior two years, and social aspirations based on the weighted average performance of peer S&P 1500 firms belonging to the same SIC four-digit industry using their size similarity. In supplementary analyses, we incorporated a simplified historical aspiration measure using only performance from the last year and a simplified social aspiration measure using the industry average performance. The results are generally consistent with and qualitatively comparable to our main findings.

Moreover, in our main analyses, we followed the literature (e.g., Misangyi et al., 2006) on variance decomposition approaches to use very few control variables in our models. In other robustness checks, we repeated our analyses with additional controls, including CEO characteristics such as gender, tenure, compensation, duality, and new CEO; firm factors such as size; and industry factors such as munificence, dynamism, concentration, as well as sales growth. The results were substantively unchanged. In addition, in our main analyses, we controlled for the proximity to bankruptcy using the Ohlson index. We observed consistent results when using Altman Z scores to measure the proximity to bankruptcy.

In another robustness check, we added a fourth level effect for industry fixed effects (i.e., decomposing the variance in the coefficient of performance below aspiration into year, industry, firm, and CEO effects when predicting strategic choices driven by problemistic search). We found that it does not change the firm and CEO RRCs in any qualitatively meaningful ways. The addition of industry fixed effects did increase the variance explained by the models, but it did not change the incremental log-likelihood test results or the Akaike Information Criteria (AIC) presented in the main analyses.

Furthermore, to examine whether the CEO effect on problemistic search might be different for new CEOs, we conducted supplementary analyses on a subsample that included only firms led by new CEOs, specifically those with less than three years of tenure in the focal firms. While we did not observe substantial differences in the results in terms of the main effect of problemistic search and firm versus CEO effects in different outcome variables, we did observe that the CEO effects are slightly stronger in the sample with only new CEOs. This finding is consistent with the literature on CEO tenure, suggesting that new CEOs are more inclined to initiate strategic change or undertake risk (Finkelstein, Cannella, & Hambrick, 2009). In addition, since one of the advantages of HLM is that it can accommodate panels where there is no CEO turnover as well as panels with multiple CEO turnovers, to ensure that our results are not contaminated by different numbers of CEO turnovers across firms, we reran our models on panels consisting of firms with at least three CEOs during the observation period and conducted a separate analysis removing CEOs who only served a single year. Although these models provided less statistical power, the size of the CEO effect in driving problemistic search was qualitatively unchanged.

Also, since our main analyses are based on a sample that excluded firms from financial and regulated industries and those that did not have a fiscal year ending in December, in another set of robustness checks, we used a full sample without excluding any observations. Again, we found results consistent with the main findings presented above. Finally, similar to Misangyi et al. (2016), we also verified that our results are unchanged after correcting for the first-degree autocorrelation.

Discussion

In this study, we asked two interrelated questions: (1) Do the effects of problemistic search vary across different organizational change and risk outcomes? and (2) Do CEOs affect the link between performance below aspiration and organizational search outcomes, and if so, do CEO effects relative to firm effects vary across different search outcomes? Using a multilevel approach, we found that (1) the effects of problemistic search vary across different organizational change and risk outcomes; (2) both firm and CEO effects are substantially related to variance in the effects of problemistic search; (3) counter to prevailing theory focused on firm factors, we find CEOs explain more variance than firm factors in the effect of problemistic search on some organizational change and risk outcomes; and (4) there are differential effects based on distinct reference points and search outcomes: CEO effects are generally larger than firm effects when firm performance is measured against historical aspirations, whereas firm effects are larger in driving certain search outcomes (i.e., R&D intensity and strategic nonconformity) when using social aspirations.

Contributions to the BTOF Literature

This study makes several contributions to the BTOF literature. First, by demonstrating that the effects of problemistic search can vary across different organizational change and risk outcomes in a single study, it helps reconcile the inconsistency of the empirical evidence on problemistic search effects. Complementing recent studies that focused on either potential theoretical issues of the problemistic search model by examining its boundary conditions (Audia & Greve, 2006; Chen & Miller, 2007; Joseph et al., 2016; Kuusela et al., 2017; Lim & McCann, 2014) or empirical issues by pointing to differences in contexts or measures of key constructs across studies (e.g., Bromiley & Harris, 2014; Shinkle, 2012; Wiseman & Bromiley, 1996), this study takes a more direct and empirical approach to systematically investigate whether the effects of problemistic search vary across a set of organizational change and risk outcomes. In so doing, it helps demonstrate whether problemistic search effects uniformly apply to various firm outcomes while controlling for certain potential issues related to differences in contexts and aspiration measures. The fact that we did not find meaningful effects of problemistic search on two of the five outcome variables suggests that some extension or reconceptualization of problemistic search is needed to better understand firm decision making.

Second, this study relaxes the assumption of the unitary nature of firm problemistic search and demonstrates the crucial role of managerial agency in the search process. Problemistic search and its assumption of relatively automated responses to performance feedback emanate from the concept of bounded rationality (Cyert & March, 1963; March & Simon, 1958; Simon, 1947), which provided a theoretical counterpoint to the unrealistic assumption of rationality in neoclassical economic theories over a half of a century ago. Nonetheless, automaticity may be an equally unrealistic assumption for organizational search behavior in response to performance feedback (Posen et al., 2018). Complementing recent studies that examined the moderating effects of executives’ characteristics in problemist search (Cho et al., 2016; Desai, 2016; Lim & McCann, 2014; Titus et al., 2020; Tuggle et al., 2010), this study directly tests how much CEOs matter to different organizational change and risk outcomes of problemistic search. Our supporting evidence for the heterogeneity in the relative size of firm versus CEO effects on different organizational change and risk outcomes highlights a potential cause underlying the empirical controversy on problemistic search effects—the heterogeneity of managerial agency, which provides an important direction for future theorizing and empirical work on problemistic search.

An Extension of Problemistic Search

Based on our findings, we offer a set of ideas regarding how to extend the original model by incorporating managerial agency. Following Posen et al.'s (2018) recent call for a process-based view on problemistic search, we discuss how managerial agency can be potentially incorporated into some subprocesses of problemistic search.

Which Goal or Aspiration to Attend?

The salient aspiration against which performance is measured acts as a threshold that should trigger problemistic search. Because the original theoretical claim is relatively broad in terms of what metric a firm would use to assess performance, empirical studies have adopted a wide array of financial and nonfinancial measures of performance and gauged aspirations based on differential reference points, i.e., social versus historical aspirations (Posen et al., 2018; Shinkle, 2012). The sheer diversity of aspiration proxies examined in prior empirical studies appears to have occurred at least partially because the traditional conceptualization of problemistic search largely overlooked the role of managerial agency.

Our results suggest that incorporating the role of managerial agency will have the potential to specify when which aspiration is salient and attended to. The finding that CEOs are more responsive to underperformance relative to historical aspirations than social aspirations in driving certain strategic actions (i.e., R&D intensity and strategic nonconformity) implies that managers may not equally allocate their attention to different sources of experience when forming aspirations (Blettner, He, Hu, & Bettis, 2015; Hu et al., 2017). We conjecture that firms will allocate more attention to their own experience than others’ experience when adapting their aspirations if these firms have CEOs whose personal interests (e.g., pay, power, or reputation) are more immediately based on how the focal firms perform relative to previous years than based on deviations from the industry norms, and CEOs that have relatively more discretion in departing from their own firms’ past actions than from the industry norms. A recent study by Audia, Rousseau, and Brion (in press) provides some initial evidence of this. Audia and colleagues found that, when forming their aspirations, firms led by powerful CEOs were more likely to use nonconforming reference groups that did not align with investors’ and analysts’ expectations. Similarly, Keum and Eggers (2018) suggested that managers play an active role in setting aspirations. Therefore, we believe a rich avenue for future research is to explore how managers’ characteristics, personality, cognitive structures, traits, compensation, and experiences influence organizational aspiration formation.

Where to Search?

Most empirical studies on problemistic search have left unanswered the question of why firms make a specific form of strategic choices rather than another (e.g., initiate divestitures rather than introduce new products) in response to their underperformance relative to aspirations (Greve, 2018; Hu, Gu, & Xia, in press). This raises an issue regarding how to specify the direction of search. Meanwhile, it is well-established in the BTOF that firms do not have a well-defined ex-ante solution space, i.e., alternative actions, in problemistic search due to bounded rationality (Cyert & March, 1963; March & Simon, 1958; Simon, 1955). The set of solutions or alternative actions must be discovered or searched (Levinthal, 1997).

Our results offer two potential insights into this issue. First, we found the insignificant effect of problemistic search on some search outcomes (e.g., the sum of capital expenditures, R&D, and acquisitions, and corporate change in diversification), inconsistent with some prior findings (e.g., Lim & McCann, 2013). This suggests that firms may search in different directions rather than take uniform actions in response to performance feedback. This further implies that the heterogeneity in search directions across firms may wash out the population effect of problemistic search on certain actions. Second, the finding that CEOs matter more in driving some actions than others underscores that the consideration of managerial agency in problemistic search can help scholars better understand the direction of search. It is well known that managers’ attentional structures and cognitive biases shape the view of managers (Hambrick & Mason, 1984), which, in turn, shapes the direction of search and, consequently, the alternatives chosen from search (Ocasio, 1997). In fact, the research on managerial cognitions (Csaszar & Levinthal, 2016; Gavetti & Levinthal, 2000) has suggested that some firms may search for potential solutions in a more exploratory way than others if they have a mental representation of the environment that facilitates more distant search. Recent studies (e.g., Billinger, Srikanth, Stieglitz, & Schumacher, 2021) have used laboratory experiments to examine how individual managers decide whether and where to search in a complex, combinatorial task. We thus believe that future work integrating managerial agency and its related cognition component into the problemistic search model is crucial to move forward the theory of directed search (Greve, 2018).

In sum, along with a recent call for a more process-oriented view of problemistic search (Posen et al., 2018), the results of this study suggest a number of fruitful research opportunities, both theoretical and empirical, through a greater emphasis on the role of managerial agency in the (sub-)process of problemistic search. This can help us better understand when, how, and why managers matter in firm search behavior.

Contributions to the CEO Effects Literature

This study also makes two contributions to the literature on CEO effects. First, prior studies on CEO effects (e.g., Lieberson & O’Connor, 1972; Mackey, 2008; Quigley & Hambrick, 2015) have generally focused on the amount of variance in firm performance occurring and attributable to various levels (e.g., year, industry, firm, CEO, and random error) but have not examined how these outcomes occur. It could be that CEOs impart their effects on firm outcomes through their personalities and risk preferences (Christensen et al., 2015; Harrison et al., 2020; Petrenko et al.,2016) or by directly responding to conditions at other firms (Connelly, Li, Shi, & Lee, 2020; Hill et al., 2019). Alternatively, CEOs may impact firm outcomes through actively shaping (forming and adjusting) strategies through problemistic search in response to underperformance relative to aspirations. For example, in response to performance shortfalls, some CEOs may invest in more R&D while others cut expenditures. By focusing on CEO effects on different behavioral outcomes of problemistic search, rather than firm performance per se, our study complements a few recent studies (Meyer-Doyle et al., 2019; Wernicke et al., in press) that showed how CEOs impact more proximal outcomes than firm performance. In this regard, our study adds to the body of work showing how CEOs can influence firm performance outcomes through shaping problemistic search.

Second, prior work has generally focused on the CEO effects in the context of firm performance (e.g., Mackey, 2008; Quigley & Hambrick, 2015) or a particular strategic action such as acquisitions (e.g., Meyer-Doyle et al., 2019) by quantifying the amount of variance in firm performance or specific strategic actions attributable to CEOs. By systematically examining CEO effects on a set of strategic outcomes of problemistic search, our study shows that CEO effects also vary considerably across different strategic actions and various aspiration measures. That is, while the research on managerial discretion (Hambrick & Finkelstein, 1987) shows that factors related to the context (both internal and external) of firms can heighten or limit CEOs’ influence, our study demonstrates that leaders also matter more or less depending on the specific strategic actions and performance reference points under investigation.

Limitations

This study contains several limitations that point to opportunities for other future research. We were unable to directly observe firm search processes; thus, following the established methodology in the problemistic search literature (e.g., Baum et al., 2005; Greve, 1998; 2003a; Miller & Chen, 2004), we inferred different organizational actions as search outcomes from problemistic search while controlling for other types of search mechanisms, based on the assumptions that these observed organizational actions, to a lesser or greater degree, represent the outcome of unobserved problemistic search. A direct observation of firm search processes in the future would enhance validity in this line of work. In addition, the outcome variables we included are broad organizational outcomes commonly studied in the S&P context and the BTOF literature. Future work may explore the relative importance of managers versus firm factors in explaining the effect of problemistic search on specific and nuanced organizational outcomes such as new market entry, factory expansion, mergers and acquisitions, and divestitures in other contexts. Furthermore, while we showed the heterogeneity in the effects of problemistic search on different organizational change and risk outcomes, we did not investigate the cause of such heterogeneity. As suggested above, more research attention to how firms direct their search can facilitate answering this question. Lastly, like most prior studies on decomposition of variance in firm outcomes attributable to various levels (Mackey, 2008; Quigley & Hambrick, 2015), while we showed the size of firm versus CEO effects in driving problemistic search, we did not examine whether CEOs matter through their characteristics, personality, cognition structure, compensation, or other factors influencing CEO decision making, as this is beyond the focus of the present study. Similarly, our study does not shed light on why CEOs matter more for certain strategic actions than others or why CEOs are more responsive to performance feedback relative to historical aspirations than social aspirations. Nevertheless, our findings and these limitations offer fruitful avenues for future research.

Footnotes

Acknowledgments

We gratefully acknowledge the in-depth and constructive comments from the Editor Aaron Hill and two anonymous reviewers. The authors would like to thank Justin DeSimone, Michael Withers, and Jeremy Meuser for their help and insights into the use of Hierarchical Linear Modeling and Vilmos Misangyi and Wei Shen for their helpful comments on an earlier version of this paper. Errors remain the responsibility of the authors.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.