Abstract

Family firms take different strategic actions because of their desire to grow and preserve socioemotional wealth (SEW), but pursuing SEW also generates what we call SEW resources that deliver advantages in certain contexts. We develop and test this idea with respect to corporate social responsibility (CSR). We theorize that SEW resources such as reputation, strong stakeholder relationships, and long-term orientation help family firms better leverage symbolic CSR to enhance short-term firm performance and better leverage substantive CSR to enhance long-term firm performance. Regression analyses on a 20-year panel of S&P 500 firms provide supportive evidence. Findings indicate that family firms not only “do it differently” to preserve SEW; they sometimes “do it better” because of SEW.

Keywords

Introduction

Family firms comprise around 65% of all businesses and generate more than half of the world’s gross domestic product (IFERA, 2003). Not only are family firms significant in number and impact, they also act differently (e.g., Berrone, Cruz, Gómez-Mejía, & Larraza-Kintana, 2010; Chrisman & Patel, 2012). A major driver of such differences is their concern with socioemotional wealth (SEW), which is the stock of nonfinancial affective value family firms accumulate (Gómez-Mejía, Cruz, Berrone, & De Castro, 2011; Gómez-Mejía, Haynes, Núñez-Nickel, Jacobson, & Moyano-Fuentes, 2007). SEW is an umbrella term capturing family owners’ desire to maintain control, extend control transgenerationally, identify with the firm, bond with stakeholders, and enhance family-members’ emotional ties (Berrone, Cruz, & Gómez-Mejía, 2012). Family owners are loss averse with respect to their SEW, which often leads family firms to forgo lucrative new ventures and other growth opportunities that might place SEW at risk (Gómez-Mejía et al., 2007; 2011).

While it is clear that family firms are influenced by family owners’ desire to build and preserve SEW (Gómez-Mejía et al., 2011), SEW can also generate resources (Naldi, Cennamo, Corbetta, & Gómez-Mejía, 2013). In particular, three dimensions of SEW—family owners’ desire for identification with the firm, meaningful (or “binding”—Berrone et al., 2012) stakeholder relationships, and transgenerational control—foster what we call SEW resources—respectively, favorable corporate reputations (Deephouse & Jaskiewicz, 2013), strong stakeholder relationships (Miller & Le Breton-Miller, 2005), and long-term orientations (LTOs) (Sirmon & Hitt, 2003; Strike, Berrone, Sapp, & Congiu, 2015). As with all strategic resources, value depends on context (Brouthers, Brouthers, & Werner, 2008). Naldi et al. (2013), for example, show that family firms’ SEW resources deliver advantages in “industrial districts” where reputation, collaboration and reciprocity, and long-term commitments are strategically valuable.

We submit that SEW resources are not only beneficial in certain industries, they can also enhance family firms’ ability to implement and leverage certain strategies. Family firms do not just “do it differently” to preserve SEW, they sometimes “do it better” because of SEW. The strategy we consider is corporate social responsibility (CSR). CSR strategies involve voluntary social, environmental, or stakeholder activities that positively impact the community, society, and/or planet (Dahlsrud, 2008). Four decades of research on the CSR–firm performance relationship has produced weak and mixed results, leading many to focus on the conditions under which CSR aids firm performance (e.g., Barnett, 2007; Vishwanathan, van Oosterhout, Heugens, Duran, & Van Essen, 2020). As Barnett (2007: 795) put it, “the unique and dynamic characteristics of firms and their environments preclude stability in financial returns to CSR across firms and time, so we should not expect to empirically discern a consistent financial benefit—essentially, a universal rate of return.” Our theory is that because of SEW resources, family ownership is among the unique characteristics that help some firms better leverage CSR.

CSR can be symbolic or substantive (e.g., Okhmatovskiy & David, 2012). Symbolic CSR is when firms make statements about CSR that are decoupled from actions or take actions that are decoupled from stakeholders’ concerns (Bromley & Powell, 2012; Wijen, 2014). Symbolic CSR can involve positive CSR actions, but such actions are self-serving and designed to enhance short-term performance by distracting stakeholders from concerns (Stevens, Kevin Steensma, Harrison, & Cochran, 2005). Substantive CSR strategies, in contrast, involve commitment to addressing stakeholders’ concerns backed by meaningful investment in and implementation of CSR. Substantive CSR strategies are others-serving and reflect a holistic intent to positively shape a societal or environmental context (Campbell, 2007). Though substantive CSR is more costly, it addresses core stakeholder concerns over the long term (Walls, Phan, & Berrone, 2011).

Moving beyond efforts to test whether family firms do more or less CSR (e.g., Cruz, Larraza-Kintana, Garcés-Galdeano, & Berrone, 2014), we submit that—because of SEW resources—family firms reap more “bang for their buck” from CSR strategies. Research suggests that the performance outcomes from certain complex strategic decisions such as CSR can be improved when (1) the firm and its strategic statements are credible (Du, Bhattacharya, & Sen, 2010), (2) the firm can rely on reciprocal commitments from stakeholders (Bosse, Phillips, & Harrison, 2009), and (3) the firm is committed long term to its strategic decisions (Flammer & Bansal, 2017). Such conditions are nurtured by SEW resources such as favorable reputations, strong stakeholder relationships, and LTO—all hallmarks of family firms (e.g., Berrone et al., 2010; Miller & Le Breton-Miller, 2005; Sirmon & Hitt, 2003). Thus, while pursuing SEW might not directly benefit family firms financially (Gómez-Mejía et al., 2011), the SEW resources that are generated allow family firms to better leverage symbolic CSR in the short run and substantive CSR in the long run.

We test our theorizing using a panel of S&P 500 firms from 1994 to 2015 and adopt principal components analysis (PCA) (e.g., Prakash, Ravi, & Zhao, 2017) to extract symbolic and substantive components (e.g., Delmas, Etzion, & Nairn-Birch, 2013; Marquis & Qian, 2014) from the widely used Kinder, Lydenberg, and Domini (KLD) data (e.g., Krüger, 2015; Waddock & Graves, 1997). Because family ownership drives the pursuit of SEW and hence the accumulation of SEW resources, we test whether family ownership moderates the CSR–firm performance relationship and whether there are temporal differences that depend on CSR strategy. Fixed-effects panel regression results show that relationships between (a) symbolic CSR and short-term firm performance (at the end of the year) and (b) substantive CSR and long-term firm performance (2 through 5 years later) increase with family ownership.

Our study’s theoretical contribution is that SEW is more than affective value placed at risk by strategic decisions; resources generated in the pursuit of SEW can change the outcome from certain strategic decisions. This insight is important because, while prior research recognized that the pursuit of SEW generates resources (e.g., Deephouse & Jaskiewicz, 2013; Gómez-Mejía et al., 2011), how SEW resources impact firm outcomes was largely unknown. SEW resources offer competitive advantages in certain industries (Naldi et al., 2013), but the idea that they might change the outcome of a strategic decision remained unexplored. Many view SEW negatively because it spurs conservative strategic decisions (e.g., Kellermanns, Eddleston, & Zellweger, 2012), but our theory and evidence are more nuanced, suggesting that resources generated in the pursuit of SEW interact with certain strategies—CSR in our case—to enhance family firms’ ability to implement and capitalize on those strategies. A key implication is that there are likely other strategic decisions that benefit from SEW resources and thus deliver more “bang for the buck.”

We also offer two empirical advances. First, there is a long and inconclusive debate about the relationship between CSR and firm performance (e.g., Margolis, Elfenbein, & Walsh, 2009; Orlitzky, Schmidt, & Rynes, 2003) that is hampered by methodological issues surrounding how to best measure CSR (Carroll, Primo, & Richter, 2016; Prakash et al., 2017). By demonstrating the presence of symbolic and substantive CSR components within the KLD data, we offer a measurement approach others can use to test theory involving this important theoretical distinction. Second, we illustrate temporal differences between the performance implications of symbolic and substantive CSR strategies. While important theoretical advances have been made describing temporal differences (e.g., Ortiz-de-Mandojana & Bansal, 2016), empirical tests involving time lags of more than 2 years and differentiating temporally between CSR dimensions have not followed.

SEW Dimensions and Resources

Family firms make strategic decisions that are consistently different from those made by nonfamily firms (see Gómez-Mejía et al., 2011, for a review), and the main reason is family owners’ desire to build and preserve SEW (Gómez-Mejía et al., 2007). As an “umbrella” term for the stock of affective value that family owners generate, it has several dimensions, including (1) controlling the firm, (2) extending control transgenerationally, (3) building meaningful (or “binding”) relationships with stakeholders, (4) identifying with the firm, and (5) deepening emotional ties among family members (Berrone et al., 2012).

The behavioral agency model (BAM) suggests that family owners are loss averse regarding their SEW and adopt conservative strategies to protect it even if doing so hurts financial performance (Gómez-Mejía et al., 2007; 2011). Family firms invest less in potentially profitable strategic actions such as diversification, acquisitions, or internationalization because such actions require outside human and financial capital that might undermine the family’s control and, ultimately, its SEW (Gómez-Mejía, Makri, & Kintana, 2010; Gómez-Mejía et al., 2007; Gómez-Mejía, Patel, & Zellweger, 2018). More recent theorizing suggests family owners’ decisions are not solely driven by potential SEW losses but are “mixed gambles” wherein family owners weigh both potential SEW losses and potential financial gains relative to a reference (or starting) point. This approach explains why family firms increase unrelated acquisition activity (Gómez-Mejía et al., 2018) and R&D investment (Chrisman & Patel, 2012) when performing below their reference point (often prior performance) or willingly give up some SEW for a big financial payoff via an Initial Public Offering (Kotlar, Signori, De Massis, & Vismara, 2018).

However, both the BAM and mixed gambles treat potential gains or losses to socioemotional or financial wealth as fixed for each strategic decision (Bromiley, 2009). Family and nonfamily firms confront the same potential financial gains (losses), but family firms confront additional concerns regarding potential SEW losses (gains) (Gómez-Mejía et al., 2011). Neither approach, however, considers the possibility that SEW is more than affective value placed at risk by strategic decisions. Advancing this research stream, we argue that actions family firms take to build and preserve SEW also generate what we call SEW resources that can change the potential financial gains (losses) from strategic decisions.

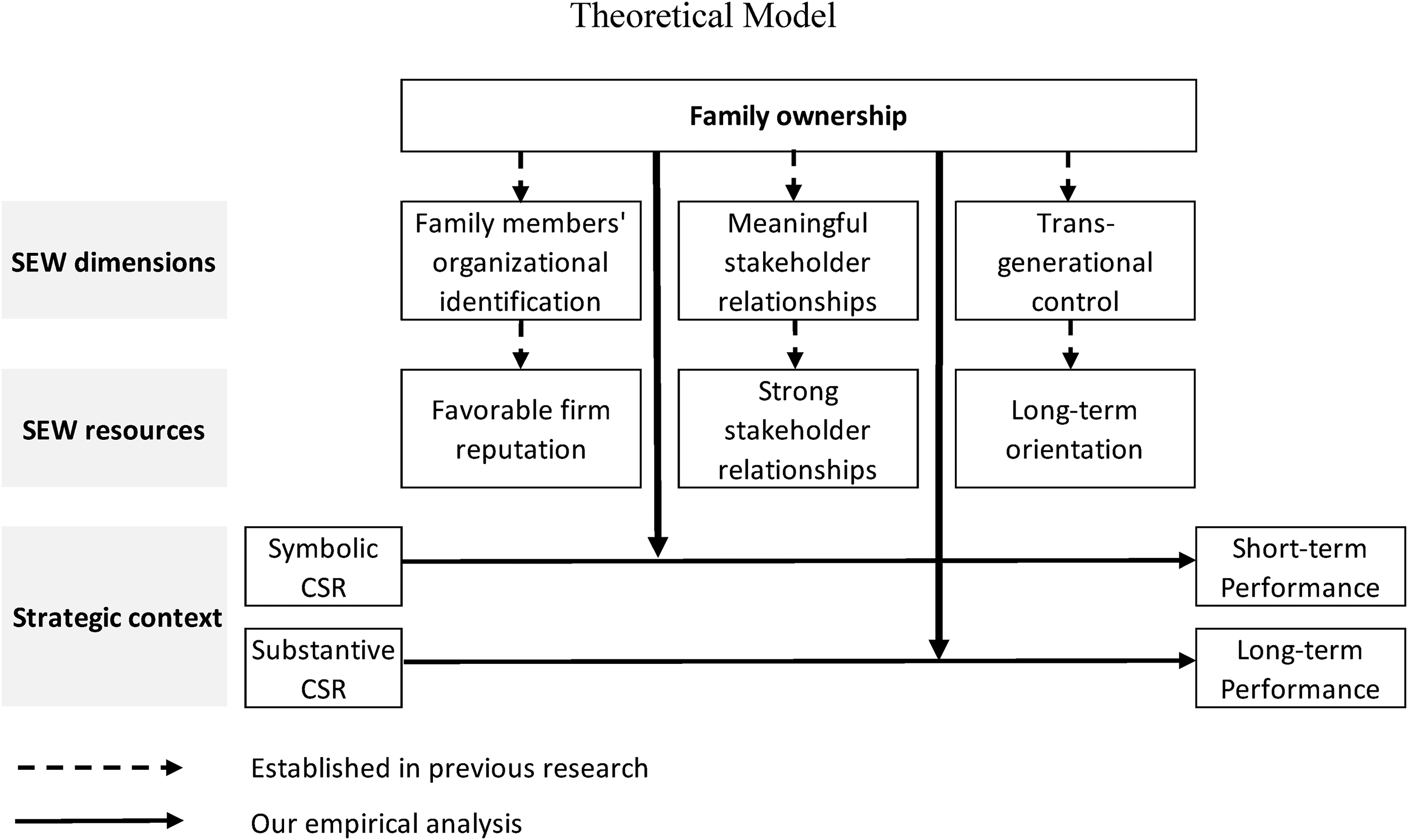

We are not the first to recognize that SEW can have a “bright side” (Kellermanns et al., 2012), and efforts to build and preserve SEW generate resources that have strategic value in certain industries (e.g., Naldi et al., 2013). Our insight is that the SEW resources family owners generate in their pursuit of SEW can change outcomes from certain strategies—CSR in our example. Three SEW dimensions appear particularly relevant for generating resources that enable firms to leverage CSR strategies. The theoretical links among SEW dimensions and SEW resources and their influence on CSR are depicted in Figure 1.

Theoretical Model

The first SEW dimension that generates a SEW resource is family owners’ identification with the firm (Berrone et al., 2012), which fosters emotional satisfaction and pride. Social identity theory states that people define themselves within their social environment relative to their membership in social groups that are salient to them and work to enhance and protect social groups they identify with (Ashforth & Mael, 1989). Applied to family firms, the theory implies that family owners identify more strongly with the firm than do shareholders or managers in nonfamily firms, and thus, family owners are more concerned with the firm’s reputation and take actions to improve it (Zellweger, Nason, Nordqvist, & Brush, 2013). In surveys across eight countries, Deephouse and Jaskiewicz (2013) found that family-owned firms score higher on corporate reputation, and these effects are even stronger when the family’s name is in the business name and a family member is active in management. A favorable reputation can be strategically valuable, for example, by increasing customer loyalty (Walsh, Mitchell, Jackson, & Beatty, 2009), attracting alliance partners (Dollinger, Golden, & Saxton, 1997), and reducing transaction costs (Standifird, 2001).

The second SEW dimension that generates a SEW resource is family owners’ desire for meaningful stakeholder relationships (Berrone et al., 2012). With the exception of outside investors whose interests can clash with family owners’ desire to protect SEW (Berrone et al., 2010), this SEW dimension leads family firms to engage in proactive stakeholder activities that satisfy demands from employees, suppliers, community leaders, and other stakeholders—even if such demands are costly and distract from maximizing firm performance (Cennamo, Berrone, Cruz, & Gómez-Mejía, 2012; Gómez-Mejía et al., 2011). Several studies show that family firms invest in strong stakeholder relationships. Miller and Le Breton-Miller (2005), for example, showcased 24 industry-leading family firms and revealed their strong connections with internal and external stakeholders. Studies of Canadian (Miller, Le Breton-Miller, & Scholnick, 2008), Chinese (Yeung, 2000), and Singaporean (Yeung & Soh, 2000) firms show that family firms engage with customers, suppliers, and/or bankers more frequently, intensely, and personally than managers in nonfamily firms, and such cooperative intentions improve clients’ relationship satisfaction (Rose, 2016). Pursuing strong stakeholder relationships leads to greater stakeholder trust (Corbetta & Salvato, 2004), which reduces transaction costs (Dyer & Singh, 1998), improves coordination and knowledge sharing (Uzzi, 1997), attracts better quality partners (Jones, Harrison, & Felps, 2018), and fuels collaboration (Miller & Le Breton-Miller, 2005).

A third SEW dimension that generates a relevant SEW resource is family owners’ desire for transgenerational control, which gives them an LTO (Lumpkin & Brigham, 2011) involving patient capital (Sirmon & Hitt, 2003). Strike et al. (2015) found that unlike Chief Executive Officers (CEOs) in nonfamily firms, who avoid long-term commitments with uncertain outcomes as they approach retirement (e.g., Antia, Pantzalis, & Park, 2010; Kang, 2014), CEOs in family firms invest in long-term strategic actions such as international growth despite pending retirement, Chief Executive Officer (CEO) is also a family member. Unlike CEOs in nonfamily firms, family CEOs in family firms are not restrained by their remaining organizational tenure. As part of their SEW, they embrace an LTO to set up the next generation for success (Berrone et al., 2012). Such an LTO means that the firm can pursue strategies that take years to implement without fear that pressure to meet quarterly earnings forecasts might force managers to abandon such efforts (Flammer & Bansal, 2017). An LTO also interacts with strong stakeholder relationships by giving stakeholders confidence that the firm will not reverse course suddenly or violate stakeholder trust for short-term gain, which increases stakeholders’ loyalty and willingness to make reciprocal long-term commitments (Bosse et al., 2009; Bosse & Coughlan, 2016). Not surprisingly, family firms’ LTO is a strategically valuable resource in industries where value creation depends on firms working collaboratively with committed stakeholders over long time periods (Naldi et al., 2013).

Overall, most studies view family owners’ pursuit of SEW as something that leads to conservative strategic actions (Gómez-Mejía et al., 2011) except when firm survival is threatened (Chrisman & Patel, 2012; Gómez-Mejía et al., 2018) and that such actions, on average, have no obvious benefit for financial performance (Kellermanns et al., 2012). Evidence also suggests, however, that pursuing SEW generates what we call SEW resources that are strategically valuable in certain industrial contexts (Naldi et al., 2013). What is not known is whether the SEW resources that come with family ownership might be leveraged to change expected outcomes from certain strategies. Our focus is on CSR strategies.

CSR Strategies, SEW Resources, and Firm Performance

CSR is an increasingly important strategic domain where SEW resources might logically enhance firm performance. CSR involves strategies businesses undertake along voluntary social, environmental, or stakeholder dimensions that positively impact the community, society, and/or planet (Dahlsrud, 2008). It involves “context-specific organizational actions and policies that take into account stakeholders’ expectations and the triple bottom line of economic, social, and environmental performance” (Aguinis, 2011: 855). Examples include philanthropy and community commitments, minority and diversity programs, and ethics and environmental responsibility policies, among others (Montiel, 2008). While CSR strategies were initially viewed as “do-good” activities that distract organizations from their financial goals, many firms have deployed CSR strategically in ways that enhance financial performance while simultaneously advancing social and/or environmental outcomes (Barnett & Salomon, 2012; Freeman, Wicks, & Parmar, 2004). However, after over 40 years of empirical studies, meta-analyses (e.g., Margolis et al., 2009; Wang, Dou, & Jia, 2016), and reviews (e.g., Malik, 2015), it is clear that “returns to CSR are contingent, not universal” (Barnett, 2007: 797). Our theory is that family ownership is one such contingency because it entails SEW resources that enable family firms to better deploy and leverage CSR strategies.

Relative to nonfamily firms, family firms engage less in strategic actions such as R&D spending, diversification, and international growth (e.g., Gómez-Mejía et al., 2010; 2011; 2018), but evidence of such differences with respect to CSR is mixed. Family firms appear to care about CSR and avoid corporate social irresponsibility (Dyer & Whetten, 2006), protect local communities (Berrone et al., 2010), and treat employees like family (Block, 2010). However, employees receive less training and pay (Cruz et al., 2014), and family firms often fail to protect nonfamily shareholders (Claessens, Djankov, Fan, & Lang, 2002). Overall, differences between family and nonfamily firms with respect to CSR remain elusive (e.g., Cruz et al., 2014), but even if family and nonfamily firms engage in similar levels of CSR, our theorizing suggests that the SEW resources that come with family ownership enable family firms to leverage their CSR strategies better. Regardless of whether or how much nonfamily firms engage in CSR, family firms should garner “more bang for the [CSR] buck.”

The conditions under which CSR improves firm performance are informed by instrumental stakeholder theory, which argues that strong stakeholder relationships based on mutual trust reduce transaction costs and encourage stakeholders to provide resources on favorable terms (Jones et al., 2018). Thus, a key contingency underlying the CSR–firm performance relationship is that stakeholders need to evaluate the firm favorably before they are willing to validate and respond positively to the firm’s CSR efforts (Nekhili, Nagati, Chtioui, & Rebolledo, 2017). Firms must have what Barnett (2007) calls “stakeholder influence capacity.” Without pre-existing credibility giving firms capacity to influence stakeholders (Servaes & Tamayo, 2013), CSR only raises costs without inspiring favorable stakeholder responses (Barnett, 2007; Barnett & Salomon, 2012). A poor track record with respect to satisfying stakeholder demands causes stakeholders to scrutinize and distrust a firm’s claims about its CSR strategies (Panwar, Paul, Nybakk, Hansen, & Thompson, 2014), which is consistent with evidence that the CSR–firm performance relationship is negative except among firms with credible commitments to CSR (Barnett & Salomon, 2012).

Stakeholder influence capacity requires ongoing engagement that builds relationships (Barnett, 2007), fosters reciprocal commitments (Vishwanathan et al., 2020), and fuels long-term performance (Andriof & Waddock, 2002). Without strong pre-existing relationships, stakeholders such as employees (Bode, Singh, & Rogan, 2015; El Akremi, Gond, Swaen, De Roeck, & Igalens, 2018), suppliers (Cheng, Ioannou, & Serafeim, 2014; El Ghoul, Guedhami, Kwok, & Mishra, 2011), and local community and government leaders (Campbell, 2007; Flammer, 2018) are less willing to trust that CSR actions address real concerns and to reciprocate by providing resources on favorable terms (Bosse et al., 2009). This observation is consistent with meta-analytic evidence showing that strong stakeholder relationships facilitate the link between CSR and financial performance (Vishwanathan et al., 2020).

While there are other SEW resources, such as the ability to reduce owner-manager agency costs (Carney, 2005), family firms disproportionately possess at least three SEW resources—that is, favorable reputations, strong stakeholder relationships, and LTOs (Berrone et al., 2010; Deephouse & Jaskiewicz, 2013; Niehm, Swinney, & Miller, 2008; Strike et al., 2015)—that line up with instrumental stakeholder theory regarding when CSR fuels firm performance (Barnett, 2007; Jones et al., 2018). A favorable reputation and strong stakeholder relationships give firms time to correct errors when they occur (Panwar et al., 2014). An LTO enables implementation of CSR strategies that take years to pay off (Wang & Bansal, 2012). Once implemented, benefits from long-term commitment to CSR are enhanced by strong stakeholder relationships that foster reciprocal commitments of effort (e.g., Bode et al., 2015; El Akremi et al., 2018), resources (e.g., Cheng et al., 2014; El Ghoul et al., 2011), and support (e.g., Campbell, 2007; Flammer, 2018).

SEW resources give family firms a stock of reputational, relational, and patient capital that validates, maintains, and, where necessary, enlists stakeholder support for their CSR efforts. That is, family firms have greater stakeholder influence capacity, which is a key ingredient triggering positive stakeholder responses to CSR (Barnett, 2007) and necessary for getting more “bang for the buck.” Without stakeholder influence capacity, CSR investments fail to trigger favorable stakeholder responses and might, because of their high costs, harm financial performance (Barnett, 2007; Barnett & Salomon, 2012). However, the timing of stakeholder responses likely differs between symbolic and substantive CSR strategies.

Symbolic CSR, SEW Resources, and Short-Term Firm Performance

Symbolic CSR involves positive social and/or environmental actions or communication about such actions that are decoupled from stakeholder concerns (Bowen, 2014; Meyer & Rowan, 1977). There are two forms of decoupling (Bromley & Powell, 2012). Policy-practice decoupling involves communicating positive policies and goals without taking meaningful actions (i.e., symbolic adoption). Means-ends decoupling involves meaningfully implementing positive actions that are not clearly linked to underlying concerns (i.e., symbolic implementation). We focus on the latter because ever-increasing external pressure for transparency and accountability have made policy-practice decoupling rare; means-ends decoupling is more feasible and common (Bromley & Powell, 2012). Wijen (2014) argued that corporate social and environmental management lends itself to means-ends decoupling because causal links regarding these issues are complex and nonlinear, and practices to address them are context dependent.

Accordingly, symbolic CSR involves implementing positive social and/or environmental steps that do not necessarily address stakeholder concerns. Instead, positive CSR actions are self-serving in that they distract from stakeholder concerns (Donia, Ronen, Sirsly, & Bonaccio, 2019). Symbolic CSR acts as a sort of insurance policy that ingratiates stakeholders and deflects concern-related criticisms (Godfrey, 2005; Godfrey, Merrill, & Hansen, 2009). Firms often deploy symbolic CSR strategies to divert attention from their actual (irresponsible) behavior and thus alleviate CSR pressures. An extreme and tragic but powerful example of symbolic CSR is provided by Whiteman and Cooper (2016). They describe a logging company in Guyana that earned a Forest Stewardship Council (FSC) certification to distract from the systematic rape of local women by employees. Equipped with certification, key stakeholders did not scrutinize the company for some time despite widespread knowledge of the rapes. Thus, even in such extreme cases, the short-term effects of symbolic CSR can be positive, but long-term benefits are unlikely because the underlying concerns that symbolic CSR diverts attention from still remain, undermining stakeholders’ commitment and reducing their ongoing contributions (e.g., Bode et al., 2015; Cheng et al., 2014; El Ghoul et al., 2011; Flammer, 2018).

At least two SEW resources—favorable reputations and strong stakeholder relationships—appear well-suited to enable family firms to better leverage symbolic CSR. Meta-analytic evidence shows that reputation is a key factor linking CSR to financial performance (Vishwanathan et al., 2020), and family firms are known to enjoy superior reputations (e.g., Deephouse & Jaskiewicz, 2013; Nekhili et al., 2017). Family firms also invest disproportionately in proactive stakeholder engagement activities that satisfy stakeholder goals—even if these goals are costly and unrelated to firm performance (Gómez-Mejía et al., 2011). Such engagement yields more in-depth knowledge of and interaction with stakeholders (Miller & Le Breton-Miller, 2005) and embeds family firms more deeply in their communities (Niehm et al., 2008), giving them greater capacity to influence stakeholders (Barnett, 2007). Heightened knowledge of and interaction with stakeholders yields greater trust that delivers positive attributions regarding family firms’ CSR actions and gives family firms the credibility needed to gain value from their symbolic CSR (Du et al., 2010). As more trustworthy partners with favorable reputations, family firms’ mishaps are viewed by stakeholders as “honest mistakes” or “bad luck” (Minor & Morgan, 2011). Thus, firms with greater family ownership are more likely to “get away” with symbolic CSR because stakeholders trust that family owners have stakeholders’ best interests at heart (Berrone, Fosfuri, & Gelabert, 2017). A favorable reputation and strong stakeholder relationships imply that symbolic CSR actions that temporarily distract from concerns will be followed by substantive action that addresses concerns (Gill, 2015).

Nonfamily firms also can build favorable reputations and stakeholder relationships (Walsh et al., 2009), but due to their focus on shareholders (Sirmon & Hitt, 2003) and less frequent interactions with nonfinancial stakeholders (Gómez-Mejía et al., 2011), they have difficulties developing and maintaining the same level of reputation and relationship quality (Du et al., 2010). Thus, we believe that because of SEW resources such as favorable reputations and strong stakeholder relationships, family firms’ symbolic CSR strategies are more positively received and thus more likely to positively influence short-term performance. Stated formally:

Hypothesis 1: The relationship between symbolic CSR strategies and short-term firm performance is more positive (or less negative) as family ownership increases.

Substantive CSR, SEW Resources, and Long-Term Value

Substantive CSR strategies involve complete CSR implementation. The firm’s underlying systems and processes are altered in a holistic attempt to eliminate stakeholder concerns and improve the status quo in societal and/or environmental contexts (Weaver, Trevino, & Cochran, 1999). Substantive CSR requires major investment in underlying systems, structures, and processes that are deeply integrated with all aspects of the firm (e.g., Bansal & Roth, 2000), and implementing substantive CSR strategies involves investing in new capabilities (Berrone et al., 2017; Walls et al., 2011). Such investments likely detract from short-term performance (Fombrun & Shanley, 1990) but help reduce waste and pollution, improve work conditions, and strengthen communities (Burke & Logsdon, 1996). Closing the production loop by reusing manufacturing waste, for example, entails substantial upfront costs but can eventually lower input costs (Burke & Logsdon, 1996). While substantive CSR is more costly than symbolic CSR, it is strongly preferred by stakeholders (Walls et al., 2011) and, under the right conditions (Barnett & Salomon, 2012), motivates stakeholders to reciprocate with resource commitments and ongoing support (Vishwanathan et al., 2020).

The long-term commitments required by substantive CSR dovetail with strong evidence that family owners disproportionally possess LTOs (Gómez-Mejía, Nuñez-Nickel, & Gutierrez, 2001; Sirmon & Hitt, 2003). While managers in nonfamily firms attempt to maximize compensation within relatively short tenures (Gómez-Mejía, Tosi, & Hinkin, 1987), family owners adopt transgenerational time horizons that focus on the financial viability of the firm for the next generation (Strike et al., 2015). An LTO should facilitate successful implementation of substantive CSR because such strategies can take years to complete (Flammer & Bansal, 2017; Ortiz-de-Mandojana & Bansal, 2016). Many firms lack the long-term resources—both continuous commitment and patient capital—required to build and integrate the complex systems, structures, and processes necessary to successfully address societal problems with substantive CSR (Bansal & Roth, 2000). Concerns over quarterly earnings and high initial costs, for example, make it difficult to pursue long-term investments in physical assets and systems (Harrison, Bosse, & Phillips, 2010; Sirmon & Hitt, 2003). Failure to invest sufficiently over time can increase costs without yielding benefits (Barnett & Salomon, 2012).

Implementation of substantive CSR is furthered by strong stakeholder relationships that inspire trust and loyalty (Webber & Klimoski, 2004) and yield stakeholder influence capacity (Barnett, 2007); stakeholders will both materially commit to the firm’s efforts—for example, by reducing waste in delivered inputs (Burke & Logsdon, 1996)—and be patient when the firm experiences setbacks (cf. Bosse & Coughlan, 2016). Consistent with evidence that family owners’ desire to maintain and grow SEW fuels strong stakeholder relationships (e.g., Berrone et al., 2010; Gómez-Mejía et al., 2011), family firms’ substantive CSR strategies should receive more ongoing stakeholder support and commitment.

Instrumental stakeholder theory suggests that, once implemented, an essential way substantive CSR enhances financial performance is by motivating reciprocal behaviors among stakeholders who benefit from and/or appreciate the firm’s CSR strategy (Jones et al., 2018; Vishwanathan et al., 2020). Employees respond to a fair, diverse, and supportive workplace with commitment and organizational citizenship behavior (Bode et al., 2015; El Akremi et al., 2018). Capital providers respond to responsible governance and full disclosures with capital on favorable terms (Cheng et al., 2014; El Ghoul et al., 2011), and community and government leaders respond to CSR with preferential purchasing (Flammer, 2018) and supportive regulation and enforcement (Sharma & Henriques, 2005). However, not all stakeholders respond to CSR (Barnett & Salomon, 2012); they are more likely to reciprocate and do so enthusiastically if they have a strong preexisting relationship with a firm (Barnett, 2007; Bosse et al., 2009; Jones et al., 2018). Bosse and Coughlan (2016) explain that such relationships build “commitment bonds” that help retain stakeholder commitments even if good alternatives become available (i.e., other firms pursuing CSR). Thus, stakeholders’ enthusiasm and commitment in response to substantive CSR should meaningfully increase when backed by strong preexisting stakeholder relationships (Bosse et al., 2009; Jones et al., 2018) that yield stakeholder influence capacity (Barnett, 2007).

While all firms have potential to capture value from their CSR strategies (e.g., Eccles, Ioannou, & Serafeim, 2014; Ortiz-de-Mandojana & Bansal, 2016), many do not (Barnett & Salomon, 2012). In the last year of our data, for example, Citigroup (the owners of Citibank) was near the bottom of the Reputation Institute’s list of “America’s Most Reputable Companies” (rank 149 out of 153) despite having one of the highest substantive CSR scores (i.e., 95th percentile), suggesting Citigroup was unable to benefit from its CSR efforts. Having SEW resources such as an LTO and strong stakeholder relationships should increase trust in and support for the firm’s CSR efforts (Bansal & Roth, 2000; Wang & Bansal, 2012) and allow family firms to implement substantive CSR more successfully and capture more value. Strong stakeholder relationships deliver influence capacity that should multiply stakeholders’ desire to reciprocate based on the firm’s substantive CSR (Barnett, 2007; Jones et al., 2018). Because family owners generate SEW resources as they build and preserve SEW, firms with more family ownership should more successfully implement and better leverage their substantive CSR over the long term. Accordingly, we expect that:

Hypothesis 2: The relationship between substantive CSR strategies and long-term firm performance is more positive (or less negative) as family ownership increases.

Method

Data and Sample

Our sample is a panel of S&P 500 firms from 1994 to 2015 averaging 420 firms per year. An average of 80 firms per year were excluded due to missing data, which is similar to previous family firm (e.g., Villalonga & Amit, 2006) and CSR (e.g., Dyer & Whetten, 2006) studies of S&P 500 firms. Family firms have at least 5% family ownership and one family member who is not the founder involved in ownership, management, or the board (Jaskiewicz, Block, Miller, & Combs, 2017). To identify such firms, we hand-collected ownership, management, and board data from proxy statements (Def 14a) filed with the Securities and Exchange Commission (SEC). We filled in missing data using other publicly available sources, such as news releases (Factiva database) and company websites. Sample firms are 18% family firms, which is comparable to previous research (e.g., Miller, Le Breton-Miller, Lester, & Cannella, 2007).

Financial data come from Compustat. CSR data come from the KLD database, which is well suited for CSR research because it captures multiple CSR categories (Waddock & Graves, 1997). Firms are rated separately on strength and concern indicators in seven major categories—environment, community, human rights, employee relations, diversity, product, and governance—yielding a total of 14 category-level variables. We do not include strengths or concerns related to corporate governance because previous research has shown that this category differs from all others and is not directly associated with CSR (Krüger, 2015), leaving 12 variables depicting strengths or concerns across six categories. We stopped using KLD data after 2008 due to significant changes to the dataset in 2009. 1 This resulted in 5,639 firm-year observations.

Dependent Variable (DV)

To measure firm performance, we focus on accounting returns using return on assets (ROA). ROA depicts the efficiency in which firms generate profits from their assets and is the most common measure of firm performance used in strategic management research (Combs, Crook, & Shook, 2005). Instrumental stakeholder theory suggests that stakeholders respond to CSR either by paying a premium for the firm’s offerings or providing inputs at favorable costs, both of which should positively impact ROA. In robustness tests, we also measure shareholders’ perceptions of the firm’s overall value from CSR strategies using Tobin’s Q.

To capture annual changes, we introduce a 1-year lag of ROA as a control variable in each model. For example, in the Model predicting ROAt+6, we control for ROAt+5. To capture short-term performance, we analyze how CSR strategies affect ROA at the end of the year (e.g., Kang, Germann, & Grewal, 2016). To capture long-term performance, we analyze how CSR strategies affect ROA between 1 and 7 years later. There is agreement that capturing long-term performance requires lags beyond 1 year, especially for CSR strategies where the impact on firm performance can take several years (Bansal, 2005; Eccles et al., 2014; Waddock & Graves, 1997). The literature is not precise regarding number of years, so we use seven to be comprehensive. For instance, the long-term performance effect of CSR strategies in 2008 is analyzed for each year between 2009 (t + 1) and 2015 (t + 7).

Independent Variables

Family ownership is measured as the percentage of stock above 5% directly and indirectly owned by the founding family, where ownership is coded as family ownership only if at least one family member who is not the founder is involved in ownership, management, or the board of directors (e.g., Jaskiewicz et al., 2017). The continuous measure of family ownership (above 5%) is consistent with our theorizing in that greater family ownership implies greater ability to build and preserve SEW and, by extension, generate SEW resources.

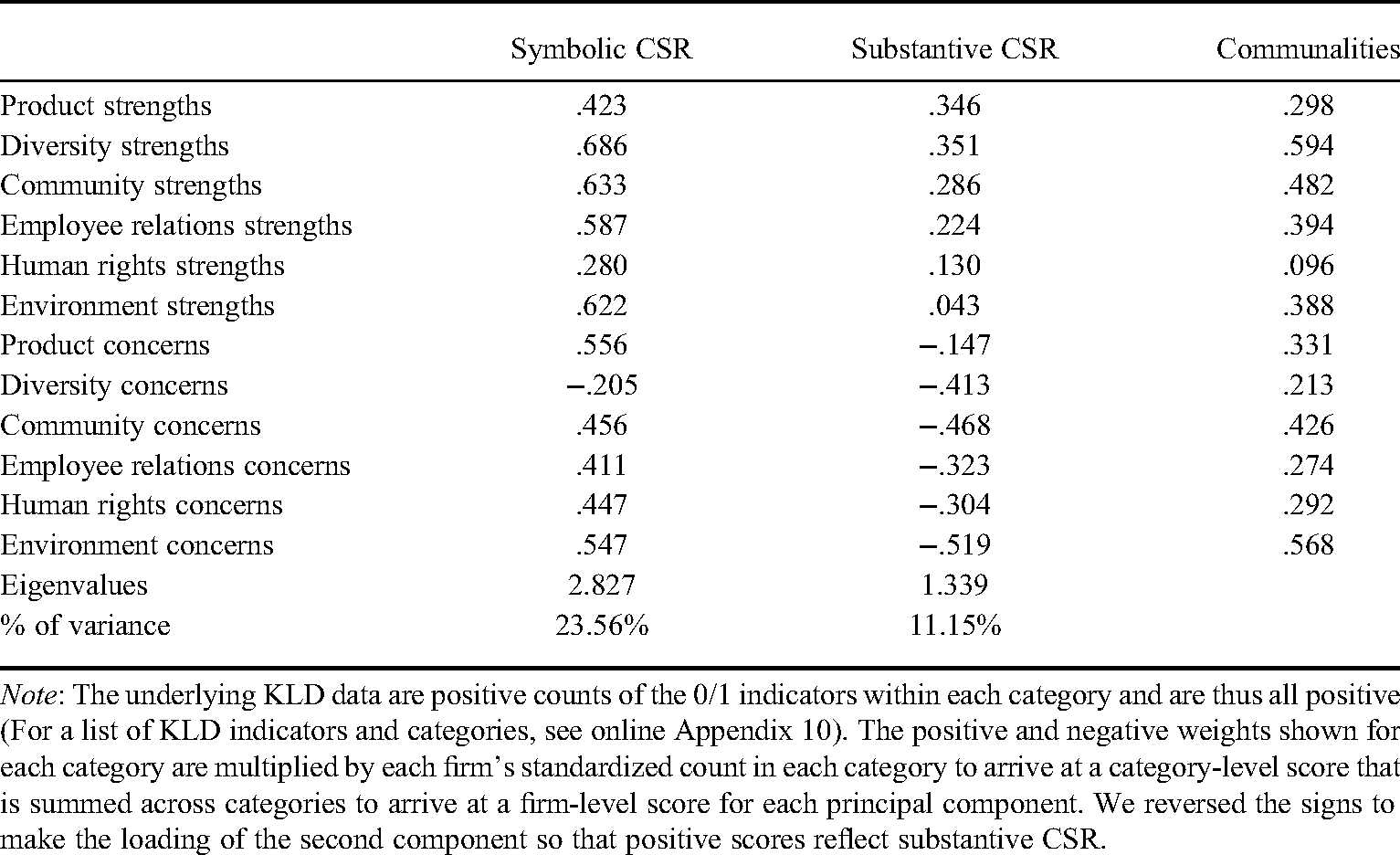

To measure symbolic CSR and substantive CSR, we adopt an approach advocated in finance research (Prakash et al., 2017). Although many studies have offered important insights by adding indicators across the 12 KLD categories (e.g., Waddock & Graves, 1997), scholars have described at least four problems. First, each KLD category has a different number of indicators, so summing them gives more weight to categories with more indicators. For example, employee relations strengths has 12 indicators while human rights strengths has only 4; summing these gives three times more weight to employee relations than to human rights, which might not be theoretically appropriate. Second, the number of indicators per category is not stable over time. A category might have, for example, five indicators in one year and four in the next, leading to different values in different years even when a firm does not change its behavior. Third, summing KLD indicators across categories assumes each is of equal informational value even though some CSR categories (e.g., diversity) might be of more or less importance than others (e.g., environment) as part of a firm’s overall CSR posture (Carroll et al., 2016). Fourth, many studies have summed the KLD category-level variables into a single construct despite emerging evidence that the KLD data map onto at least two distinct constructs (e.g., Delmas et al., 2013; Walls et al., 2011). These problems have received increasing attention (e.g., Carroll et al., 2016), emphasizing the need for a different methodological approach.

One approach that mitigates all four problems is principal component analysis (PCA) (Prakash et al., 2017). PCA uses an iterative algorithm to identify a set of weights (wx) called component loadings that can be multiplied by a set of variables (X1−k, where k = the number of variables) to form unobserved latent variables called principal components (C1−k). The principal components represent communality, or shared variance, among the variables. The goal of PCA is to identify a smaller number of components that parsimoniously represent the most important sources of shared variance.

The component loadings, or weights (wx−k), are correlations between the observed variables (X1−k) and unobserved components (C1−k). The first principal component (C1) is a set of weights (wx−k) that maximize total shared variance explained. Each firm’s score on C1 is the sum of the weights for each variable multiplied by the observed value for that firm:

While PCA can produce 12 components from the 12 KLD variables (i.e., 6 categories of strengths and 6 categories of concerns) that explain all of the variance, the goal is to identify a smaller set of components that depict the most important sources of shared variance. The appropriate number of components should be guided by theory and the marginal gain in shared variance explained by the next component. A common rule is to retain all components with eigenvalues greater than 1 (Kaiser, 1960). A component’s eigenvalue is the sum of the squared component loadings (i.e.,

Component Loadings

Note: The underlying KLD data are positive counts of the 0/1 indicators within each category and are thus all positive (For a list of KLD indicators and categories, see online Appendix 10). The positive and negative weights shown for each category are multiplied by each firm’s standardized count in each category to arrive at a category-level score that is summed across categories to arrive at a firm-level score for each principal component. We reversed the signs to make the loading of the second component so that positive scores reflect substantive CSR.

All KLD strengths and concerns except diversity concerns load positively on the first principal component. We label it Symbolic CSR because scores increase with simultaneous increases in both strengths and concerns, which is consistent with mean-ends decoupling wherein positive strengths sit alongside and distract from current stakeholder concerns. As an example, a firm that scored high on symbolic CSR in 2007 was Du Pont Chemical. Its standardized KLD scores for that year were: 2.62/3.67 = environment strengths/concerns; 2.23/2.34 = product strengths/concerns; .55/1.41 = community strengths/concerns; −.14/−.36 = human rights strengths/concerns; .37/.19 = employee relations strengths/concerns; and .77/−.54 = diversity strengths/concerns. Taking the loadings for the first component in Table 1, Du Pont Chemical’s 2007 score for symbolic CSR is:

All KLD strengths load negatively and all KLD concerns load positively on the second principal component. Thus, a firm that scores high on this component has low overall CSR, while the component’s inverse depicts a firm that has many CSR strengths and few concerns (see Table 1). We therefore label the component’s inverse Substantive CSR; it increases as CSR strengths increase and decreases with CSR concerns. Applying Du Pont’s 2007 KLD scores from above to the inverse loadings for Component 2 (as shown in Table 1) yields the following score for substantive CSR:

Because we standardized KLD categories, scores for symbolic and substantive CSR have a mean near 0 and a standard deviation near 1.

Although loadings are mostly positive for the six CSR strengths on both symbolic and substantive CSR, the addition or subtraction of a strength (all else equal) would change the scores by different degrees. Take environment strengths as an example; a one-unit increase (e.g., the indicator for “waste management” went from 0 to 1) with no other changes increases symbolic CSR by .622, but substantive CSR would increase by only .043. If we simultaneously add a one-unit increase in environment concerns (e.g., the indicator for “hazardous waste” went from 0 to 1), however, the symbolic score would increase to 1.169 (i.e., 1 strength * .622 plus 1 concern * .547), but substantive CSR would decrease by −.476 (i.e., 1 strength * .043 plus 1 concern * −.519). The score for symbolic CSR mostly increases with concerns because, for means-ends decoupling to occur (i.e., positive actions that distract from concerns), firms must have concerns that strengths can distract from. For substantive CSR, the highest scores go to firms with few concerns and many strengths. Loadings for concerns are higher-in-magnitude than for strengths, which is consistent with the idea that concerns are hard to address substantively (cf. Carroll et al., 2016). It is possible, however, for firms to score relatively high on both symbolic and substantive CSR. 3M, for example, is repeatedly in the top 95% for both. Firms like 3M score high on symbolic CSR because they have many strengths and simultaneously many concerns, and they score high on substantive CSR because they have many more strengths than concerns.

A concern about KLD is that it does not differentiate between easy versus hard and important versus trivial CSR indicators. Carroll et al. (2016) address this issue directly by estimating a latent CSR score using Bayesian estimation. Although their estimate (called D-SOCIAL-KLD) was derived from the many (nongovernance) individual KLD indicators that we summed into each of the 12 KLD categories, our first principal component (i.e., symbolic CSR) correlates with D-SOCIAL-KLD at r = .78, suggesting that our measures also differentiate meaningfully among easy/hard and important/trivial KLD indicators. 3

Control Variables

Research suggests that Firm size, Firm age, and Firm leverage affect both CSR strategies and firm performance (Margolis et al., 2009). We measure Firm size using the natural log of total assets. Larger firms have economies of scale that can also be harnessed to implement CSR. Firm age is measured as the natural log of the number of years since the firm’s founding. Older firms have more experience implementing CSR (Moore, 2001). Firm leverage is defined as the ratio of long-term debt to total assets (Husted, Jamali, & Saffar, 2016). Leverage enhances performance for firms with sufficient cash flow, but it can leave firms with fewer resources for CSR (Mishra & Modi, 2013). Following McWilliams and Siegel (2001), we include annual Sales growth, level of Diversification, R&D intensity, and Advertising intensity as additional controls. Rapidly expanding Sales growth enhances firm performance by increasing economies of scale, but it might also force managers’ attention away from CSR (Husted et al., 2016). Diversification is measured by the natural logarithm of the number of business segments. Large, diversified firms pay more attention to CSR (Strike, Gao, & Bansal, 2006). R&D intensity, measured as R&D expenditure/sales, is a proxy for growth opportunities. Firm performance increases when firms exploit promising growth opportunities, but such activities might draw managers’ attention away from CSR (Husted et al., 2016). Advertising intensity is measured as the ratio of advertising expenses to sales and indicates that buyers are aware of the firm’s brand and its CSR strategies (Servaes & Tamayo, 2013). Managers invest in advertising to increase awareness and sales, which should improve firm performance, and we expect managers to leverage CSR as part of such efforts. We control for past accounting performance using ROA and firm value using Chung and Pruitt’s (1994) formula for Tobin’s Q. These are important controls because better performing firms might have more financial resources for CSR (Campbell, 2007; Chiu & Walls, 2019). We control for Market cycle with an indicator variable taking the value of 1 for expansionary periods. Munificent environments increase resources for CSR (McWilliams & Siegel, 2001). Data for this variable were obtained from the National Bureau of Economic Research (NBER). Finally, Miller et al. (2007) show that it is important to distinguish family firms from lone founder firms; we thus controlled for Lone-founder ownership using the percentage of stock above 5% owned by a founder when there are no other family members involved in ownership, management, or the board of directors (Jaskiewicz et al., 2017).

Model Specification

As suggested by the Hausman Test, we use year- and firm-fixed effects to control for unchanging firm-level characteristics. Because firms appear annually in our analysis, observations are not independent and standard errors might be biased. We address this issue through robust standard errors. All control and independent variables except ROA are measured at t = 0. For instance, in Model ROAt+3, the DV is measured at time t + 3 while control and independent variables are measured at t = 0. ROA as a control is lagged 1 year so that regression coefficients reflect year-over-year changes in ROA, limiting the potential for both serial correlation and endogeneity from reverse causality. Endogeneity is also investigated using propensity score matching as summarized in the robustness test section.

Results

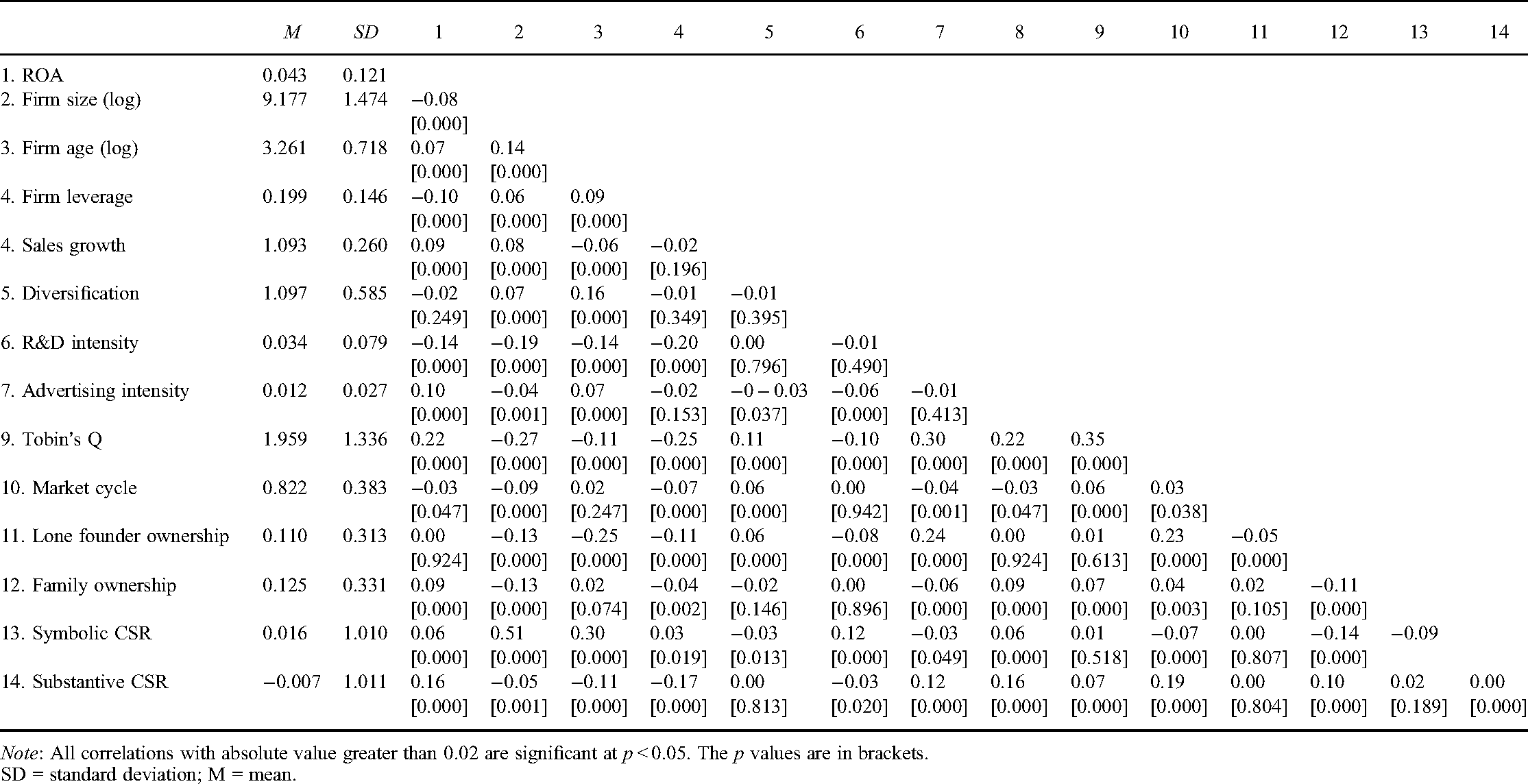

Table 2 presents descriptive statistics and correlations. Family ownership correlates negatively with symbolic CSR and positively with substantive CSR, and substantive CSR correlates positively with ROA. With respect to control variables, firm size, firm age, leverage, diversification, and advertising intensity relate positively to symbolic CSR, whereas sales growth, R&D intensity, Tobin’s Q, market cycle, and lone-founder ownership relate negatively. R&D intensity, advertising intensity, Tobin’s Q, market cycle, and lone-founder ownership relate positively to substantive CSR, whereas firm size, firm age, leverage, sales growth, and diversification relate negatively.

Descriptive Statistics

Note: All correlations with absolute value greater than 0.02 are significant at p < 0.05. The p values are in brackets.

SD = standard deviation; M = mean.

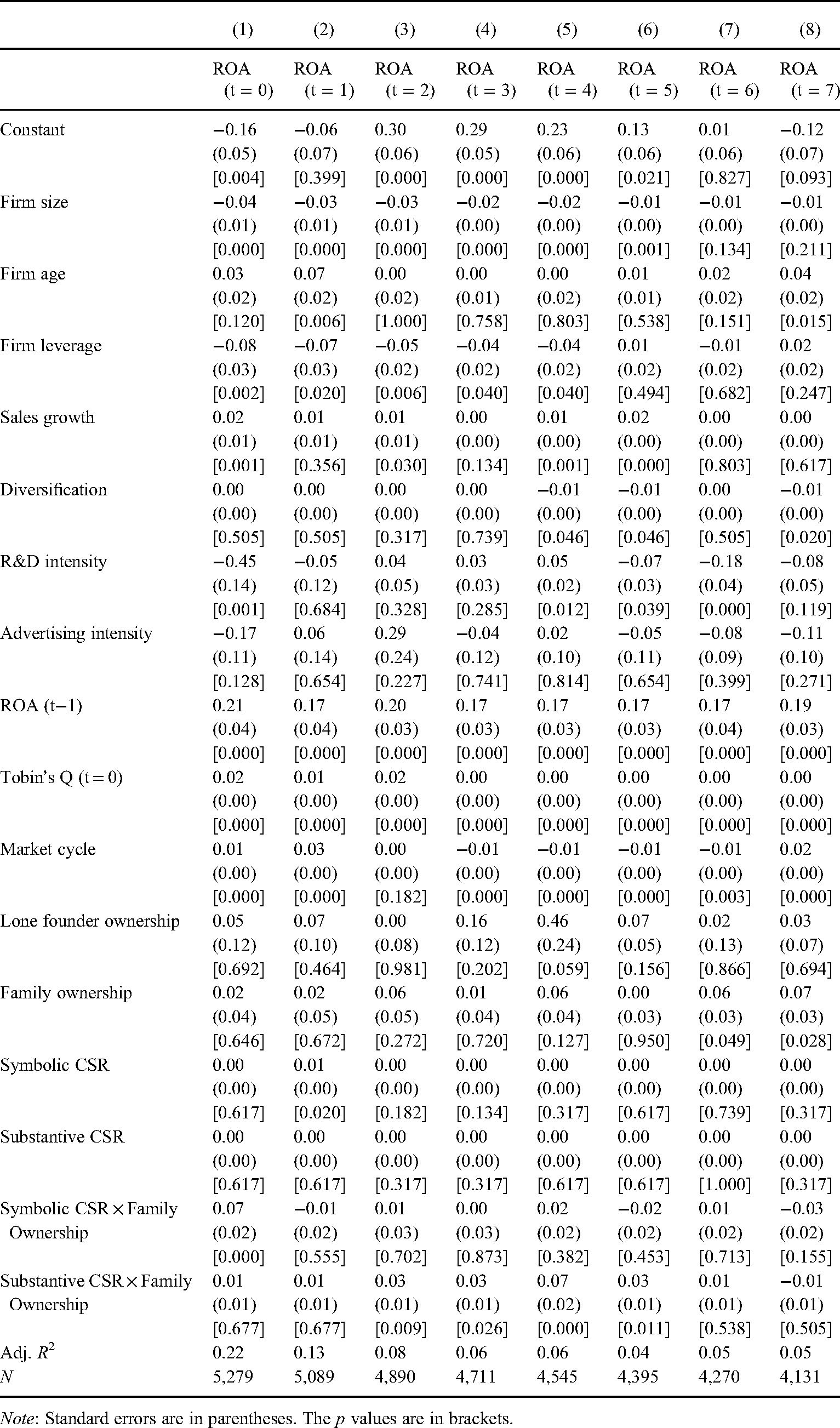

Table 3 presents multivariate analyses of symbolic and substantive CSR on ROA lagged up to 7 years. Each CSR strategy is measured in t = 0. ROAt+1, ROAt+2 … ROAt+7 represent firm performance, 1, 2, up to 7 year(s) after t = 0. The interaction between each CSR strategy and family ownership tests the hypotheses. Hypothesis 1 predicts that family ownership makes the short-term relationship between symbolic CSR and firm performance more positive (or less negative). Family ownership moderates the relationship between symbolic CSR and ROA such that it is significantly more positive in the short term (i.e., the same year), supporting Hypothesis 1 (

Family Firms, CSR Strategies, and Firm Performance

Note: Standard errors are in parentheses. The p values are in brackets.

Hypothesis 2 predicts that family ownership enables a more positive (or less negative) long-term relationship between substantive CSR and firm performance. Family ownership moderates the relationship between substantive CSR and ROA such that this relationship is significantly more positive 2 through 5 years later, supporting Hypothesis 2 (

Effect sizes suggest that increasing symbolic CSR by 10% in year t = 0 relates to a same-year increase in ROA of 0.72 percentage points for the average family firm and no change in ROA for nonfamily firms. A 10% increase in substantive CSR relates to a year t + 3 increase in ROA of 0.74 percentage points for the average family firm and no change in ROA for nonfamily firms. In other words, based on the average ROA in our sample, a 10% increase in substantive CSR translates in 3 years to an ROA of 5.04% for the average family firm and 4.30% for the average nonfamily firm, a 17.2% difference. Overall, family firms appear better equipped to leverage symbolic and substantive CSR strategies to enhance firm performance in the short and long term, respectively.

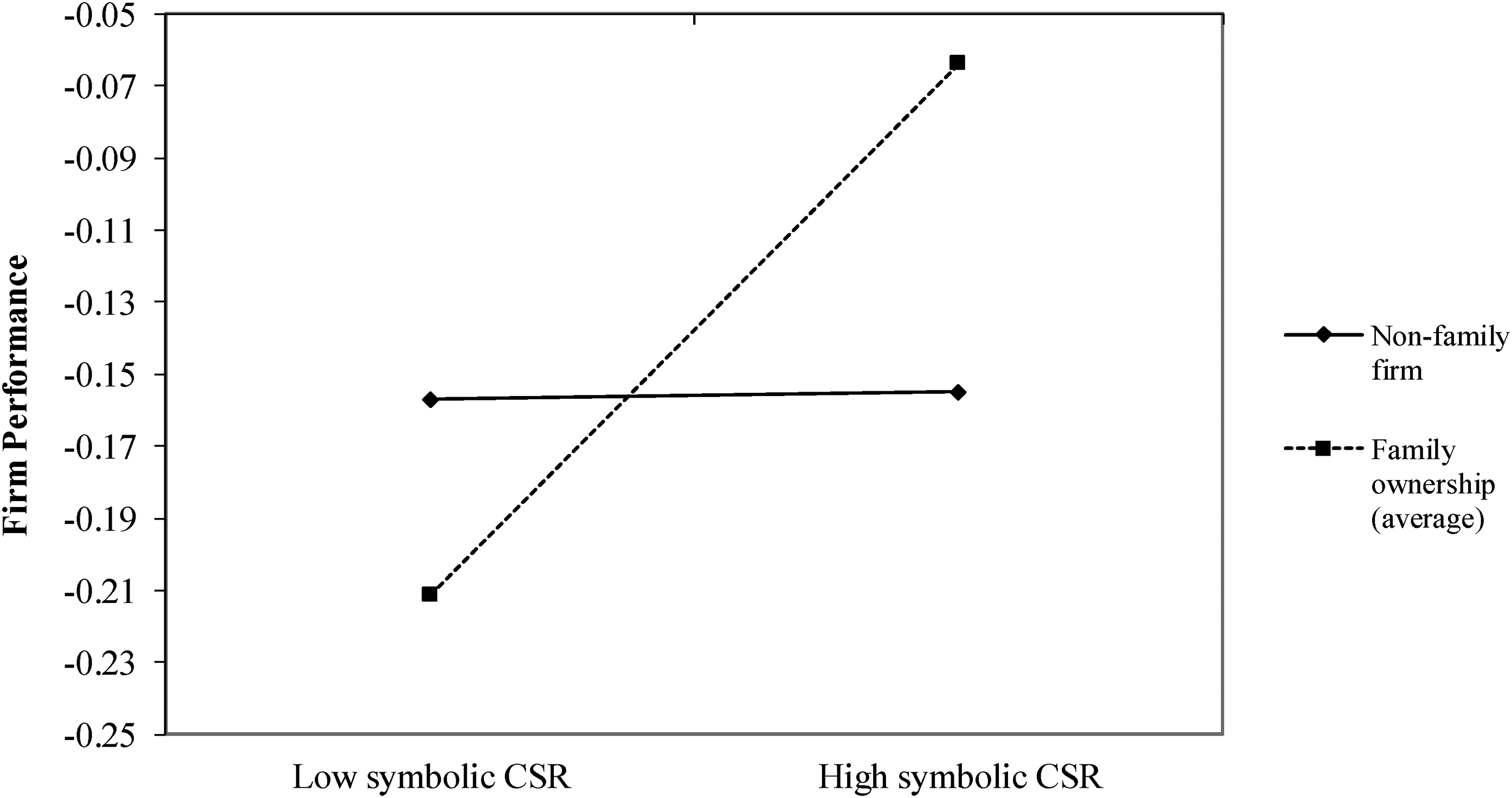

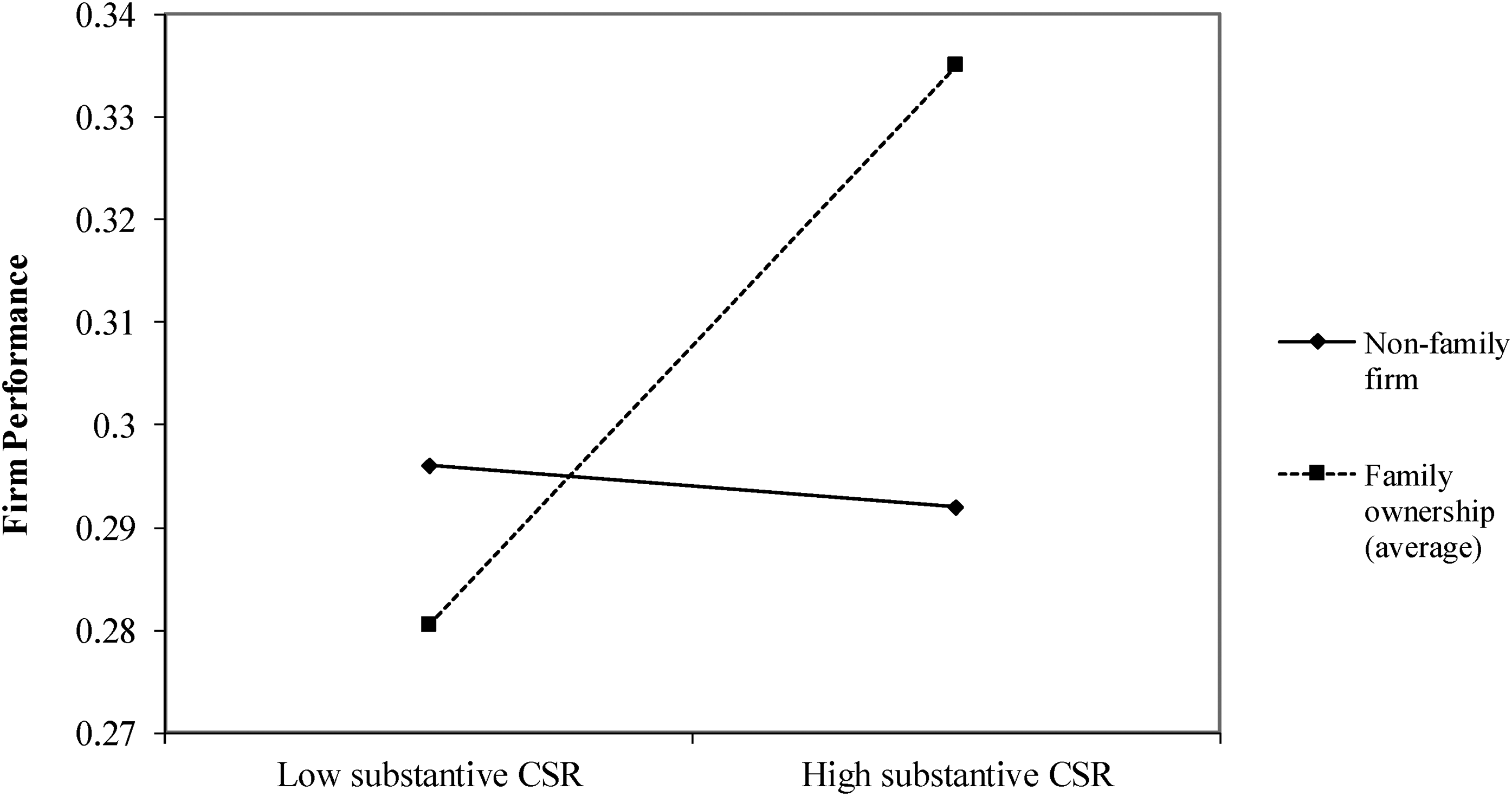

The interaction terms capture variation in CSR–ROA relationships attributable to family ownership, leaving variation attributable to nonfamily firms in the main-effect coefficients for symbolic and substantive CSR. The interaction and main-effect coefficients yield the slopes, respectively, for family and nonfamily firms’ CSR–ROA relationships, which are plotted for symbolic CSR in Figure 2 at t = 0 and for substantive CSR in Figure 3 at t + 3. The t tests reveal that the simple slopes are more positive for family firms for symbolic CSR in t = 0 and substantive CSR in each year between t + 2 and t + 5, inclusive, supporting our theory that family firms receive more “bang for the buck.” Indeed, as shown in the main-effect coefficients for symbolic and substantive CSR in Table 3, relationships between both symbolic and substantive CSR and ROA among nonfamily firms are nonsignificant, which is consistent with theory suggesting that firms need stakeholder influence capacity to benefit from CSR (Barnett, 2007) and evidence that the CSR-performance relationship is negative for many public firms (Barnett & Salomon, 2012).

Interaction Plot for Symbolic CSR, Family Ownership, and Firm Performance (At the End of t = 0)

Interaction Plot for Substantive CSR, Family Ownership, and Firm Performance (in t + 3)

Robustness Tests

We conducted several robustness tests to assess the sensitivity of our results. First, to investigate the robustness of family ownership as a proxy for SEW, we reran the models using an indicator variable coded as family firms equal one if the family owned at least 5% and more than one family members served as managers or board members; results remain unchanged (online Appendix 1). We then split the sample to compare family and nonfamily firm effects separately. This analysis confirmed that symbolic and substantive CSR coefficients for family firms were similar to the interaction terms reported in Table 3 (online Appendix 2a), and symbolic and substantive CSR coefficients for nonfamily firms were similar to the symbolic and substantive CSR (main effect) coefficients reported in Table 3 (online Appendix 2b).

Second, we find mostly nonsignificant relationships between firm performance and symbolic and substantive CSR among nonfamily firms. Of the main effects, only symbolic CSR in t = 1 is significant at p < .10. The same pattern emerges in analyses wherein family and nonfamily effects are averaged by removing the interaction terms (online Appendix 3). At first blush, these insignificant relationships might seem inconsistent with primary studies and meta-analyses suggesting a small positive overall CSR effect on firm performance. However, meta-analysis uses correlations as inputs and cannot control for many unobserved firm-level factors (e.g., good management, corporate culture) that might explain both CSR and superior performance (and thus confound the link between them). Also, many, if not most, studies reporting positive main effects use year- and industry- but not firm-fixed effects (e.g., Awaysheh, Heron, Perry, & Wilson, 2020), which is necessary to control for unobserved firm-level factors. Studies show that the positive overall effects of CSR on firm performance disappear when using more conservative specifications like ours that control for unobserved firm-level heterogeneity (Barnett & Salomon, 2012). Indeed, when we drop the firm fixed-effects specification and instead use industry-effects, symbolic CSR is positively and significantly related to ROA in years t = 0 through t = 7, and substantive CSR is positively related to ROA in years t = 0 through t = 6 (online Appendix 4).

Third, if stakeholders’ collective assessments of the firm improve, or investors anticipate that such assessments will improve, it should fuel investors’ overall evaluation as reflected in Tobin’s Q. We therefore ran the models with Chung and Pruitt’s (1994) formula for Tobin’s Q as the DV. Results mirror those for ROA (online Appendix 5).

Fourth, we needed to exclude the potential that firms with higher family ownership might not be better at leveraging CSR but simply engage in different levels of CSR. To do so, we regressed family ownership and the same set of controls (in Table 3) on symbolic CSR, substantive CSR, and each of the 12 KLD category variables (online Appendices 6 and 7). All coefficients are nonsignificant, suggesting that family firms do not engage in different levels of symbolic CSR, substantive CSR, or any of their underlying activities. The positive performance effect of symbolic CSR and substantive CSR in family relative to nonfamily firms seems to be driven by family firm’s superior ability to deploy and leverage CSR strategies.

Fifth, our measure for symbolic CSR captures the simultaneity of strengths and concerns under the assumption that the former are decoupled from the latter. We found a positive correlation between strengths and concerns within each category except diversity, suggesting means-ends decoupling. Earnest attempts to reduce concerns with strengths would imply a negative correlation. We pursued three additional tests of this assumption. First, we regressed the number of CSR strengths and the same set of controls (in Table 3) on the number of CSR concerns in the following year. The relationship is not significant. Second, because CSR strengths might need several years to address CSR concerns, we reran the regression using 2- and 3-year lags. Again, no effect was found. Finally, it is possible that only firms with high levels of CSR strengths can use them to reduce concerns, so we ran the same regression using only firms in the highest 25th percentile of symbolic CSR (who have many strengths and many concerns). The effect is also insignificant in this subsample. Indeed, only 12 of the 62 firms in the top 25% in symbolic CSR in 2005 saw any reduction in concerns by 2008; five saw an increase, while 45 had no change. These robustness tests provide strong support that, consistent with our measure of symbolic CSR, the vast majority of firms used symbolic CSR to distract from current concerns. Very few firms used strengths to reduce concerns.

Finally, we needed to address endogeneity concerns related to the possibility that results are driven by some untheorized and omitted variable that systematically co-varies with firm ownership, CSR strategy, and firm performance. To investigate this possibility, we used propensity score matching. Each family firm was matched with a similar nonfamily firm based on industry, year, and market capitalization. Rerunning the models using propensity score matching yielded comparable coefficients and significance levels as in our main findings (plus a significant family ownership–substantive CSR interaction at t + 1) (online Appendix 8).

Discussion

Previous research shows that while pursuing SEW often leads family firms to forgo lucrative investment opportunities (e.g., Gómez-Mejía et al., 2010; 2011), it also generates what we call SEW resources that have strategic value in certain industries (Naldi et al., 2013). Our study extends this line of inquiry by recognizing that SEW resources not only have value in certain industries, they can also change outcomes from certain strategic decisions—CSR in our example. Rather than passively comparing mixed gamble decision outcomes comprised of competing SEW and financial losses and gains, SEW resources can change the mix of gains and losses family firms confront. Family firms do more than “do it differently” to preserve SEW; they sometimes “do it better” because of SEW.

Prior research shows that pursuing SEW generates SEW resources such as favorable reputations, strong stakeholder relationships, and LTOs (e.g., Deephouse & Jaskiewicz, 2013; Miller et al., 2008; Strike et al., 2015). Drawing on instrumental stakeholder theory, we theorized that (1) favorable reputations and strong stakeholder relationships help family firms better leverage symbolic CSR in the short term by lending credibility to positive CSR actions, and (2) strong stakeholder relationships and LTOs help family firms better leverage substantive CSR in the long term by easing implementation and enhancing stakeholders’ desire to reciprocate. In support of our theorizing, we found that relative to nonfamily firms, greater family ownership (and thus SEW resources) strengthens relationships between symbolic CSR and short-term (t = 0) performance and between substantive CSR and long term (t + 2 through t + 5) performance.

Our study also illustrates a method for measuring symbolic and substantive CSR and reveals their temporal differences. Methodological challenges measuring CSR are one reason for inconclusive results regarding the CSR–firm performance relationship (e.g., Carroll et al., 2016; Delmas et al., 2013). By surfacing symbolic and substantive components within KLD data and showing that these components have different temporal effects, we set the stage for future researchers to empirically leverage this important distinction and highlight the need for longitudinal designs that capture CSR strategies’ different temporal effects beyond 1 or 2 years. Our theory and results have important implications for future family business research and efforts to better understand links between CSR strategies and firm performance.

Implications for Family Business Research

Our research focused on CSR as an example of a strategic decision where outcomes can be changed by SEW resources. One implication is that there are likely other strategic decisions where SEW resources alter outcomes, and there is merit in future inquiry focused on identifying such decisions. Strategic decisions regarding supply chain integration, alliance formation and management, and innovation, for example, might warrant attention because, like CSR, such efforts might benefit from SEW resources: Favorable reputations attract partners (e.g., Dollinger et al., 1997), effective stakeholder relationships facilitate joint value creation (Dyer & Singh, 1998), and an LTO helps keep innovation on track (Wang & Bansal, 2012).

Our theorizing was built on strong evidence that pursuing SEW generates favorable reputations (e.g., Deephouse & Jaskiewicz, 2013), strong stakeholder relationships (e.g., Miller et al., 2008), and LTOs (Strike et al., 2015) among family firms, and instrumental stakeholder theory linking such resources to firms’ abilities to leverage CSR (Barnett, 2007; Bosse et al., 2009; Jones et al., 2018). Future research might advance by identifying differences among family firms in terms of the specific SEW resources they develop and which SEW resources—or combinations of SEW resources—best leverage different strategies. Our theorizing, for example, implies that a family firm with a favorable reputation and strong stakeholder relationships, but not an LTO, benefits from symbolic CSR but lacks the long-term commitments needed to implement, and benefit from, substantive CSR. Efforts to isolate SEW resources would also dovetail with emerging efforts to explain variance among family owners in terms of the SEW dimensions they pursue (e.g., Brinkerink & Bammens, 2018) and, more broadly, efforts to understand the wide heterogeneity among family firms (e.g., Miller & Le Breton-Miller, 2020).

Implications for CSR Research

Our finding that family but not nonfamily firms, on average, effectively leverage their CSR strategies to enhance firm performance implies that much of the small positive relationship between CSR and firm performance found in prior meta-analyses (e.g., Margolis et al., 2009; Wang et al., 2016) is attributable to the presence of family firms in samples. However, there is also a great deal of variance among nonfamily firms in their ability to leverage CSR (e.g., Barnett & Salomon, 2012). Our focus on family ownership suggests that other types of owners might be a place to advance efforts to explain such variance. For instance, prior research shows that institutional investors enhance environmental performance (Walls, Berrone, & Phan, 2012), suggesting merit in future studies that investigate whether differences among institutional shareholders (e.g., passive versus active) or other kinds of owners (e.g., lone founders) have different effects on the CSR–firm performance relationship.

We also consider whether such effects are temporally different across CSR strategies. Corporate (social) responsibility research (e.g., Waddock & Graves, 1997) differs from (closely related) research on corporate sustainability in its treatment of time (Bansal & Song, 2017). The latter argues that companies that take a long-term perspective are more likely to address sustainability holistically by addressing intertemporal tradeoffs in their strategies (Bansal & DesJardine, 2014). Our findings regarding the long-term benefits of substantive CSR suggests family owners’ LTOs help them address such tradeoffs. Whereas time is a defining characteristic of sustainability research (Bansal, 2005; Bansal & DesJardine, 2014), ours is the first in the corporate (social) responsibility tradition to investigate time implications beyond a year or two and to differentiate temporally among CSR dimensions in terms of financial outcomes. Perhaps substantive CSR can advance future research at the intersection between corporate responsibility and sustainability traditions by shedding light on conditions that foster both responsibility and sustainability (cf. Bansal & Song, 2017).

Our attempt to resolve challenges in the KLD dataset and identify measures that match theory also has implications for future research. First, the different weights the PCA assigned to each KLD category for symbolic and substantive CSR suggest value in more fine-grained approaches to capture complementarities among CSR categories. Diversity provides a particularly interesting example. The comparatively large weights for diversity strengths for substantive CSR and (both) diversity strengths and concerns for symbolic CSR suggest its importance, but the small negative weight for diversity concerns on symbolic CSR suggests that, unlike other KLD categories, no amount of decoupling can overcome diversity concerns. Stated differently, if concerns are raised about a firm’s diversity, relative to other CSR categories, investing in positive counteractions to distract attention appears ineffective. Differences among the category weights thus suggest merit in efforts to understand how each CSR category interacts with others to form overall CSR strategies and influence outcomes.

A second implication from our attempt to resolve challenges in KLD is that PCA might be used to develop more refined CSR measures. To maintain consistency with prior research, we kept all 12 KLD categories and thus did not take advantage of PCA’s ability to identify the “best” variables (i.e., those with high loadings). Taking our last year of KLD data (2008) as an example, symbolic and substantive CSR explain 27.64% and 10.77% of the variance of the 12 variables, respectively. Researchers often drop variables with loadings below .3, which in 2008 are human rights strengths, diversity concerns, and product strengths. Dropping these, symbolic and substantive CSR, respectively, explain 44.06% and 14.59% of the remaining variance (online Appendix 9). Using PCA in this way might help CSR researchers converge on a set of essential variables that best capture firms’ CSR strategies and identify those KLD categories that “act differently” from the others. Indeed, looking at the third to 12th principal component (which we did not use due to low eigenvalues) reveals that a few KLD categories contribute little to the first two components (i.e., substantive and symbolic CSR) and largely “stand alone.” For example, human rights strengths, which has relatively small weights for the first (i.e., symbolic CSR; w = .28) and second component (i.e., substantive CSR; w = .13) dominates the third component (w = .74), suggesting that human rights strengths, while contributing something to the two main CSR constructs, might reasonably be viewed as a distinct construct. The relative weights of different KLD categories, and the extent to which different KLD categories might form additional theoretical constructs, point to value in future efforts to understand how different portfolios of KLD strengths and concerns might “fit” with a particular firm’s competitive capabilities and/or a sector’s institutional norms.

Future Research Implications of Limitations

All studies have limitations and ours is no exception. First, our study focuses on large publicly-listed firms in the United States. We believe, however, that this sample introduces a conservative bias. Robustness tests show that results are strongest among family firms with large family ownership, which is the norm among the vast majority of privately held family firms around the globe. Thus, it is important to learn how much more the performance benefits of symbolic and substantive CSR strategies might be among private firms as this bias implies.

Second, we build upon a stream of research theorizing that family owners’ pursuit of SEW generates SEW resources (Naldi et al., 2013) and showing empirically that family firms have better reputations (Deephouse & Jaskiewicz, 2013), stronger stakeholder relationships (Miller et al., 2008), and adopt LTOs (Strike et al., 2015), but we do not measure these SEW resources. SEW has long served as an unmeasured theoretical construct, and this limitation reinforces the need for emerging efforts to better define and measure the dimensions of SEW (e.g., Berrone et al., 2012) and associated SEW resources.

Third, consistent with studies that describe how firms facing specific concerns (e.g., an oil spill) commonly distract from these by investing in CSR strengths (e.g., donate to marine parks, introduce water recycling protocols), our measure of symbolic CSR assumes that strengths that rise in proportion to concerns are largely decoupled. Indeed, this is one reason the loadings for strengths are relatively larger for symbolic than substantive CSR; strengths must be proportional to the concerns they symbolically distract from. We acknowledge, however, that some proportion of strengths, more so at some than other firms, are probably earnest attempts to reduce concerns. Thus, future efforts to identify the conditions under which firms’ positive actions in the face of concerns are more than symbolic appear warranted.

Finally, we were limited to an institutional context with a developed regulatory framework. Several studies show, however, that firms operating in extractive sectors in less developed countries act irresponsibly, on average, in the absence of environmental regulation and enforcement (e.g., Dam & Scholtens, 2008). This raises questions about whether family firms in such sectors and countries might behave as irresponsibly as their nonfamily peers.

Conclusion

We developed theory suggesting that SEW resources give more credibility to family-owned firms’ symbolic CSR in the short term and support implementation of and multiply reciprocal responses to substantive CSR over time. Evidence that family ownership helps leverage symbolic and substantive CSR over different time periods is consistent with this theorizing. The concept of SEW resources provides an important counterpoint to the conservative strategic stance typically attributed to SEW. SEW resources not only aid performance in certain industries, they can change outcomes from certain strategies. Our study also applies a more refined method for aggregating raw KLD data and draws attention to the temporal implications of different CSR strategies. We hope that these efforts offer a modest step toward better understanding the implications of family ownership and the conditions under which CSR can be leveraged to enhance firm performance.

Footnotes

Acknowledgments

We received substantive feedback on previous versions from Pascual Berrone, Isabelle Le Breton-Miller, Danny Miller, Rajshree Prakash, Pramodita Sharma, Sanjay Sharma, and Ritu Virk. The paper also benefitted greatly from contributions from the Action Editor and three anonymous JOM reviewers.

Supplemental material for this article is available with the manuscript on the JOM website.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.