Abstract

The phenomenon of a platform owner entering its complementor spaces has been growing and, given its potential impact on the dynamics of competition in platform-mediated industries, has captured the interest of entrepreneurs, scholars, and policy makers. Empirical studies on the consequences of such platform owner entry have been scant so far and show mixed results for complementors. Drawing on competitive dynamics theory, our paper revisits an implicit assumption held in extant studies that allows us to hypothesize on dissimilar entry modes across owners, to study the implications of entry mode differences. We argue that how an owner enters its complementor spaces drives the level of competitive pressure that such an entry exerts on the affected complementors. In turn, this determines the size and valence of the repercussions on complementors’ product performance as well as their responses. Drawing on platform theory, we argue that an owner’s mode of entry into complementor spaces relates to that owner’s approach to platform governance. Using a unique panel dataset of health and fitness mobile apps in the Apple iOS and Google Play store, our results support our prediction that the mode of entry plays a significant role in the resulting complementor dynamics. We find contrasting modes of entry and resulting dynamics that arise between a platform that follows a closed and reigning approach to governance and one that follows an open and laissez-faire approach. Our findings help explain apparent contradictions in prior studies and extend our understanding of this increasingly common phenomenon in platform-mediated industries.

Keywords

Introduction

Research on digital platforms continues to grow as they occupy an increasingly important share of our economy (Chen, Yi, Li, & Tong, 2022; McIntyre & Srinivasan, 2017; Nambisan & Baron, 2013). Recently, scholars have devoted attention to within-platform dynamics and the inner workings of digital platforms (e.g., Kapoor & Agarwal, 2017; Rietveld, 2018; Rietveld & Eggers, 2018; Tavalaei & Cennamo, 2020). In particular, the phenomenon of a platform owner entering its complementor spaces by offering products and services seemingly similar to those of its complementors has been significantly on the rise, reshaping intraplatform dynamics. For example, Apple has over a dozen of its own mobile apps in the iOS App Store, and Amazon offered thousands of its own branded products in 2020, tripling the number offered in 2018. Given this rapid growth, an emerging strand of scholars has begun to examine this phenomenon, due to its potentially important implications for platform strategies and policies (e.g., Foerderer, Kude, Mithas, & Heinzl, 2018; Wen & Zhu, 2019; Zhu & Liu, 2018).

However, extant studies on the topic offer mixed evidence regarding complementor performance resulting from owner entry (Rietveld & Schilling, 2021; Zhu, 2019). On the one hand, some scholars find negative impacts of such entry (e.g., Gawer & Cusumano, 2002; Wen & Zhu, 2019). For instance, Zhu and Liu (2018) find that the affected third-party sellers on the Amazon platform experienced a significant drop in product sales after Amazon entered their market spaces, leading to a decrease of 57% in these sellers’ sales ranking position. Adding a direct competitor, especially one who exerts significant power (Boudreau & Hagiu, 2009), can pose a substantial competitive threat to the affected complementors, negatively influencing their performance. On the other hand, other scholars point to positive impacts for complementors after their platform owner entered their market spaces (e.g., Foerderer et al., 2018; Li & Agarwal, 2017). Foerderer et al. (2018) find that following Google’s entry into the photo category, consumer demand increased for all complementors in the space, due to a platform owner’s decision to enter a particular product space bringing heightened visibility and attention to that domain, raising consumer interest, and ultimately enlarging the market (Li & Agarwal, 2017). These spillover benefits, akin to the effect of “a rising tide lifting all boats,” can act as a cooperative force, positively influencing the affected complementors’ performance.

The ambiguities found in the extant empirical evidence are prompting a growing call for research, to investigate what drives these contradictory complementor performance outcomes resulting from owner entry (Rietveld & Schilling, 2021; Zhu, 2019). By integrating platform literature with the theory of competitive dynamics—an established strategy perspective long used to explore the effects of new market entry on existing players (Chen & MacMillan, 1992; Hsieh & Vermeulen, 2014; Porter, 1980)—our paper responds by addressing the gap in our current understanding of the phenomenon. We question an implicit assumption held in most prior platform research—namely, that the “mode of entry” in each case of owners entering complementor spaces is basically the same. Competitive dynamics scholars contend that how a new player enters an existing market determines the level of competitive pressure the existing players face, ultimately influencing their performance and response (e.g., Chen & Miller, 1994; Ferrier, Smith, & Grimm, 1999; Nadkarni, Chen, & Chen, 2016; Smith, Ferrier, & Ndofor, 2001). Considering the contradictory findings in the few empirical studies to date on the consequences of platform owner entry, we conceptualize such entry as a complex set of dynamics that entail both competitive and cooperative forces on the affected complementors. We then focus on how an owner’s mode of entry into complementor spaces shapes the association between its entry and the resulting performance and response of the affected complementors.

A platform owner’s mode of entry into complementor markets is likely to closely relate to the owner’s approach to platform governance. Platform governance refers to the extent to which a platform cedes decision rights to complementors or other stakeholders, regarding platform attributes and arrangements (Boudreau, 2010; Chen et al., 2022; Karhu, Gustafsson, & Lyytinen, 2018; Schilling, 2009; Tiwana, 2014). A platform’s approach to governance is conceptualized as relatively stable, relating to the “conditions for ordered rule and collective action” (Stoker, 1998: 17). 1 A central question in platform governance concerns managing the tension between a decentralized, “open and laissez-faire” approach that devolves decision rights to platform stakeholders on the one hand and, on the other hand, a centralized, “closed and reigning” approach that reserves most rights for the platform owner (Tilson, Lyytinen, & Sørensen, 2010; Wareham, Fox, & Cano Giner, 2014). We expect the owners’ approach to platform governance to manifest in how they enter complementor spaces. As different owners have different approaches to governance structure (e.g., Chen, Pereira, & Patel, 2021; Schmeiss, Hoelzle, & Tech, 2019; Tschang, 2021), we argue that the observed mode of entry will likely vary across owners who enter their complementor spaces—hence, the degree of competitive pressure on complementors is also likely to vary across owners. The different levels of competitive pressure that varying modes of owner entry exert on existing complementors will result in different performance repercussions and complementor responses.

Our empirical setting is the health and fitness (H&F) app ecosystem on two major mobile platforms: the Apple iOS and Google Play app stores. We chose this setting because it is an ideal opportunity to explore our research questions. Apple and Google released their own H&F apps, Apple Health and Google Fit, almost simultaneously. However, the platform owners differ markedly in their approaches to platform governance, which their modes of entry into their respective complementor spaces manifested. Apple pursues a closed, reigning approach to platform governance (Chen et al., 2021; Karhu et al., 2018; Parker & Van Alstyne, 2018), evident in how the company released its Apple Health app and underlying technologies. Apple gave little choice to the users and complementors regarding when and how to use its product and related technologies, tightly controlling access and usage. Google pursues an open and laissez-faire governance approach (Chen et al., 2021; Karhu et al., 2018; Parker & Van Alstyne, 2018) in stark contrast to Apple’s. When introducing the Google Fit app and its related technologies, Google gave users and complementors ample choice regarding when and how to access and use its product and underpinning technologies. We leveraged the different entry modes when Apple and Google released their H&F apps on their respective platforms to compare their respective complementors before and after owner entry.

To make our comparison groups as similar as possible, we employed matching analysis and restricted our sample to the apps that multihomed (i.e., appeared on both platforms). This allowed us to account for possible selection bias that might correlate with inherent product or complementor heterogeneities. In addition, we supplemented our quantitative panel data analysis with qualitative content analysis of online developer discussion forums, press releases, and insights from semistructured interviews with industry participants. Our analysis supports our prediction that differences in the mode of entry, performance, and repercussions can be substantial. The performance and response from the affected complementors significantly vary with the owner’s mode of entry and the resulting competitive pressure on complementors.

Our paper expands the platform literature in several ways. We reconcile seemingly contradictory findings in previous research on platform owner entry into complementor spaces (e.g., Foerderer et al., 2018; Gawer & Cusumano, 2002; Wen & Zhu, 2019; Zhu & Liu, 2018). By integrating the theory of competitive dynamics into platform literature, our paper relaxes the implicit assumption in prior studies. We explicitly consider the possibility that platform owners can differ in terms of their “mode of entry” into their complementor spaces, likely reflecting their approaches to platform governance. We show how this heterogeneity in entry mode is an important contingency, associated with differences in complementor performance and responses resulting from the owner’s entry. Our study clarifies the coopetitive (cooperative-competitive) dynamics that can be in play when an owner enters its complementor spaces, an important set of intraplatform dynamics that enrich our understanding of the inner workings of platforms (e.g., Kapoor & Agarwal, 2017; McIntyre & Srinivasan, 2017; Rietveld & Eggers, 2018; Zhang, Li, & Tong, 2022). Our paper also sheds light on platform governance by illustrating how different approaches to platform governance intervene in this coopetitive relationship between owner and complementors. Our results inform the key trade-off that platform governance approaches engender—namely, value capture versus platform growth. Specifically, we extend the existing understandings of platform governance by documenting the relationship between governance and mode of entry into complementor spaces and, by extension, of the performance and responses of complementors associated with an owner’s entry. Our results show that owner entry, when done with different approaches to platform governance, can result in opposite performance repercussions on the affected complementors and distinct levels of engagement with the platform, post-owner entry. Platform owners may want to factor in these findings when making entry decisions. Complementors’ response to platform owner entry can have important consequences for the growth of the platform over time. Our findings here can further expand the recent discussion relating to the role of complementors’ agency in platform markets (e.g., Chen et al., 2022; Rietveld, 2018).

Our study also informs the research on competitive dynamics. Most studies in this field derive from traditional industry contexts. However, digital platforms exhibit unique characteristics, market structure, and dynamics. In particular, the symbiotic relationship between platform owners and complementors implies that traditional understandings of competitive dynamics might not automatically apply to the situation of platform owner entry. For example, our finding that platform owner entry can result in positive outcomes for competing complementors can significantly modify the core argument in traditional competitive dynamics—namely, that the effect of a new entry on the existing players is bound to be negative or, at best, nil. Furthermore, extant studies on competitive dynamics argue that the competitive pressure a new entrant poses on the existing players varies with the aggressiveness primarily associated with the level of resources that the entrant possesses, vis-à-vis the existing players (Chen & Miller, 1994; Ferrier et al., 1999). Our paper complements extant literature by unraveling another factor important in a platform market—that is, platform governance, which can ultimately determine the type of competitive pressure on complementors.

Theory and Hypotheses

Platform Governance on Digital Platforms

Extant platform literature suggests that platform governance can substantially shape the performance and behavior of complementors (Claussen, Kretschmer, & Mayrhofer, 2013; Rietveld, Schilling, & Bellavitis, 2019; Zhang et al., 2022). Platform governance refers to the extent to which a platform cedes decision rights regarding platform attributes and arrangements to complementors and other stakeholders in the platform (e.g., users; Boudreau, 2010; Chen et al., 2021; Chen et al., 2022; Karhu et al., 2018; Schilling, 2009; Tiwana, 2014). The goal of platform governance is to orchestrate and nurture the ecosystem of complementors and other stakeholders for the platform’s value creation and appropriation (Karhu et al., 2018; Wareham et al., 2014). A platform’s approach to governance is conceptualized as relatively stable, encompassing a wide array of platform-wide practices and strategies, such as content policies, resource distribution, terms of service, technical aspects—for example, application programming interfaces (APIs) and software development kits (SDKs), algorithms, and pricing schemes (Plantin, Lagoze, Edwards, & Sandvig, 2018; Tiwana, 2014). We therefore expect platform governance to be reflected in the owners’ mode of entry, when making inroads into their complementor spaces. While we consider a platform owner approach to governance as relatively stable, there might be cases in which platforms change their approach to governance over time. We discuss some of these cases in the discussion section of the paper.

A central distinction in platform governance exists between a decentralized, “open and laissez-faire” approach that devolves decision rights to platform stakeholders and, on the other hand, a centralized, “closed and reigning” approach that reserves most rights to the platform owner (Chen et al., 2021; Chen et al., 2022; Karhu et al., 2018; Tilson et al., 2010; Wareham et al., 2014). Extant studies show that platform governance can vary from a fully open and decentralized approach to one that is fully closed and centralized (Schilling, 2009; West, 2003). Both decentralization and centralization have their respective benefits and drawbacks (Chen et al., 2021; Chen et al., 2022). On the one hand, a centralized approach characterizing closed and reigning governance can empower platform owners, who retain tight control over platform access and usage, core interactions, and value distribution (Boudreau, 2010; Chen et al., 2021; Chen et al., 2022; Rietveld et al., 2019). This allows prioritizing the owner’s interests over those of other stakeholders and capturing a higher fraction of the value its platform creates (Chen et al., 2021; Zhu, 2019). The drawback is that such behavior could alienate and discourage other stakeholders on the platform, due to concerns about the effects of the power imbalance that favors the platform (Arrieta-Ibarra, Goff, Jiménez-Hernández, Lanier, & Weyl, 2018; Chen et al., 2021). On the other hand, a decentralized approach associated with open and laissez-faire governance devolves decision rights to platform participants, providing them with better opportunities to make decisions consistent with their preferences and interests (Chen et al., 2021). As complementors can make decisions that align better with their incentives, they have room to capture more of the value the platform creates. Therefore, such an open and laissez-faire platform will likely incentivize complementors to engage because of “enhanced incentive compatibility” (Chen et al., 2021: 1311). Thus, a decentralization approach can facilitate platform growth in terms of the number of complementors and users, which, however, may not be the best strategy for value appropriation from the owner’s perspective, at least in the short run.

The Competitive Dynamics of Platform Owner Entry Into Complementor Spaces

The theory of competitive dynamics (Chen & MacMillan, 1992; Hsieh & Vermeulen, 2014; Porter, 1980) provides a useful framework for analyzing the performance repercussions and responses of complementors upon entry of a platform owner into their spaces. Scholars have studied the impact a new entrant can have on the existing competitive dynamics, focusing on the association between how an entrant enters an existing market and the level of competitive pressure it exerts on the existing players, with the resulting impact on the players’ performance. This research primarily argues that the degree of competitive pressure the entrant exerts is a function of its level of resources (vis-à-vis the existing players) and the aggressiveness with which the entrant seeks to capture value (Chen & Miller, 1994; Ferrier et al., 1999). Even if the entrant does not immediately carry out aggressive actions to gain ground in the market, an entrant’s vast resources can influence the behavior of the existing players, who understand that the new entrant has the potential to exert competitive pressure at any moment (Karakaya & Yannopoulos, 2011). An entrant’s high level of aggressiveness on entry sends an unmistakable signal to the existing players that the new entrant came ready to put up a fight and conquer. Entry aggressiveness relates to a series of actions by the entrant designed to increase its product’s advantage and visibility, such as promotions, advertising, and price cutting. Ultimately, these actions aim to maximize the new entrant’s market share and capture value by luring customers away from the existing players in the market (Ferrier et al., 1999).

Competitive dynamics theory was formulated largely during the 1980s and 1990s before management research focused on the peculiarities of platform markets. However, today, these markets occupy a prominent place in management research and practitioner interests. Our existing understanding of competitive dynamics thus requires important adjustments in the context of entry into platform markets—particularly, the increasingly common situation of a platform owner entering its own complementor spaces. Such cases represent significant departures from the situations and studies that gave rise to competitive dynamics theory, potentially leading to different outcomes and, thus, calling for this extension of the theory. As we detail below, the entry of a platform owner into its complementor spaces is not simply the entry of a new competitor with vast resources into a market that other firms already inhabit.

Digital platforms present unique characteristics that may exhibit different market dynamics from those in traditional industries. A platform owner tends to be larger and more resource-rich than most complementors, and the level of power and influence that the owner exerts over its complementor markets is far greater than that of a typical new market entrant (Boudreau & Hagiu, 2009; Claussen et al., 2013). The owner’s power on a digital platform has been compared to the “bouncer’s right” (Strahilovetz, 2006). In traditional settings, a new entrant can influence the behavior of the existing players mainly through adjusting prices or promoting its product—for instance, it can lower its price, which will likely produce some reaction from the incumbents. Therefore, the effect is indirect; the existing players would react to the entrant’s success in attracting customers with its price-setting and promotions. However, when a platform owner enters its complementor spaces, the options do not just shrink to investments in attracting users. A platform owner also has a direct influence on complementor behavior because the owner sets the rules by which complementors must play (Boudreau & Hagiu, 2009). For instance, a platform owner may require complementors to adopt specific new technology standards or protocols when releasing its product, as often happens when mobile apps must adapt their products to the new changes introduced when the owner launches a new operating system. This change can directly shape the operations and technological priorities of complementors on digital platforms. A platform owner entering its complementor spaces can influence the existing complementors not only through its effect on users but also directly, by modifying the technologies and the set of rules that affect the operations of incumbent complementors. Thus, new possibilities open, beyond those that extant competitive dynamics theory contemplates.

In addition, on digital platforms, a close association exists among entry aggressiveness, the level of competitive pressure the owner exerts, and an owner’s approach to platform governance. We argue and expect that platforms that pursue a closed, reigning approach to governance will enter complementor spaces deploying more aggressive strategies and exerting more competitive pressure than those that pursue an open, laissez-faire approach to governance.

In their attempts to enter complementor markets, platforms with a closed and reigning approach to governance will likely tightly control usage of and access to the owner’s product and its underpinning technologies, exercising significant control and restricting how users and complementors can use the product and related technologies. For example, an owner could promote its product prominently on the landing page of the platform over those of complementors and, in addition, make technological or operational changes in the platform that require complementors to comply. Owners may also tie platform-level services and programs to the use of the owner’s product (Zhu & Liu, 2018) while constraining complementors from leveraging or integrating with the owner product or its underlying technologies. For instance, when entering its complementor spaces, Amazon has favored its own products (e.g., offering free shipping through its platform-wide service, Prime, or giving them priority and prominent space on its web pages or in search results) (Zhu & Liu, 2018). Such practices can siphon consumer attention away from the affected complementors’ product and toward the owner’s. Further, this approach can curb opportunities for complementors to benefit from the positive spillovers that result from owner entry, such as enhanced visibility and attention to that domain, which can lead to market expansion. By enacting tight controls over the usage and access to its product and technology, such owner can capture much of its entry’s newly created value, thus restricting complementors’ residual value capture. Hence, in entries carried out by platforms with a closed and reigning approach to governance, competitive forces are likely to dominate cooperative forces, intensifying the competitive pressure on complementors. Thus, such entry is likely to be negatively associated with the product performance of the affected complementors. The level of entry aggressiveness and competitive pressure on the existing firms can be, at least theoretically, far greater in the case of platform owner entry than an entry in a nonplatform setting, given that a platform owner can directly influence the rules of the game that both users and complementors must follow, in addition to having much greater resources and valuable information.

Platforms with an open and laissez-faire approach to governance are likely to give ample discretion to users and complementors in their incursions into complementor spaces, exercising limited control over how platform participants can use the owner’s product and its underlying technologies. This can beget significant possibilities for complementors to capture a part of the value that the owner’s product introduction creates. For instance, an owner could release a product in a complementor market that serves as a “hub,” to which complementors can easily connect their products, amplifying their offerings and allowing them to create new services. Generous access to the owner’s product and its underpinning technologies can allow high and customizable levels of integration that complementors can use to enhance their own products, to their advantage. This integration can benefit complementors because the owner’s product likely leverages the owner’s built-in asymmetric advantage and deeper knowledge of the platform. For instance, the owner’s product could feature a tighter and smoother interface and compatibility with new or upcoming features in the platform’s main operating system. These improvements and opportunities can increase consumer satisfaction and enhance demand for all complementor products in the affected markets, producing positive spillovers from the owner’s entry. Moreover, owners with an open and laissez-faire approach to governance would also refrain from giving their products unfair advantages over those of complementors, making siphoning user attention away from the complementor products less likely. Hence, in entries carried out by platforms with an open and laissez-faire approach to governance, the cooperative forces will likely predominate over the competitive forces, resulting in relatively low competitive pressure on the affected complementors. Such an entry is thus likely to be positively associated with the product performance of the affected complementors, unlike what happens with a new market player entering a traditional industry, in which case the effect on the existing players is bound to be negative or, at best, nil. The entry by an owner with an open and laissez-faire approach creates a new range of possible behaviors and outcomes that can affect complementors positively.

Taken together, a platform owner’s mode of entry into its complementor markets—which its approach to platform governance largely determines—will drive the competitive pressure the entry exerts on the affected complementors, tilting the balance between competitive and cooperative forces of platform owner entry and ultimately determining the valence of such entry’s impact. It then follows:

Hypothesis 1a: The entry of a platform owner with a closed and reigning approach to governance is negatively associated with the affected complementors’ product performance. Hypothesis 1b: The entry of a platform owner with an open and laissez-faire approach to governance is positively associated with the affected complementors’ product performance.

Competitive dynamics theory also informs the existing market players’ response to the entry of a new player in their market (Bengtsson & Marell, 2006; Gatignon, Anderson, & Helsen, 1989; Karakaya & Yannopoulos, 2011). This is of utmost importance in platform settings due to the symbiotic relationship between a platform owner and its complementors. Complementors play a key role in platform growth when they engage with and invest in the platform, focusing their resources and continued efforts on producing and providing value-adding complementary products through the platform (Boudreau, 2012; Jacobides, Cennamo, & Gawer, 2018; Saadatmand, Lindgren, & Schultze, 2019; Wang & Miller, 2020). Firms are constantly scouting their focal and adjacent markets and competitors, and the observed and expected market dynamics inform their actions (Smith et al., 2001). The conceptualization of adjacent markets depicts them as the set of markets that firms could feasibly consider when trying to grow outside of their focal market (Zook & Allen, 2003). While early conceptualizations of adjacent markets include a geographical dimension, this has become less relevant for today’s digital markets. More recent conceptualizations emphasize the closeness of required technological capabilities and customer needs (Lehmberg, Dhanaraj, & White, 2019). In the context of digital platforms, the specific segment of a product category in which the firm competes (e.g., sports games) represents the core, focal market of a complementor firm while adjacent markets are related focal markets in that product category that present demand and capability requirements overlapping those of the firm’s focal market (e.g., in the example above, the rest of the market segments in the broader “games” category, such as action games or adventure games). This conceptualization, in line with recent work, emphasizes the need for adjacent markets to be feasible for a firm given its capabilities and experience in the focal market. As Lehmberg et al. (2019: 1430) note, adjacent markets “are adjacent in the sense that the technological requirements to enter a new adjacent market build on the requirements for previous markets, and the additional technological challenges required for entry into this new adjacent market are relatively modest.”

This conceptualization leads us to expect a complementor’s decision to continue investing in or to divest from its focal and adjacent markets after an owner’s entry to be associated with the level of competitive pressure the entry exerts on the complementor; the level of competitive pressure can affect the complementor’s expected market position and value appropriation potential (e.g., Bracha & Fershtman, 2013). A new entrant in the focal market, particularly if large and/or well-endowed, always adds uncertainty and brings the possibility of a change in competitive dynamics and market positions in the focal and adjacent markets, which, due to their closeness in terms of demand and technical requirements, should also be within the reach of the new entrant. When the entry of a new player poses substantial competitive pressure, the existing players may either confront it directly, as a preemptive measure or to regain lost ground, or avoid direct competition, such as by shifting their investments toward more distant markets or unrelated product categories (Barnett, 1993; Baum & Korn, 1996; Edwards, 1955). Competitive dynamics theory suggests that when the existing players believe that they are stronger than the new entrant, they will likely go on the offensive and confront the entrant directly with a “tit-for-tat” strategy, aiming at surpassing the entrant’s offerings to neutralize the threat. However, when they perceive the level of resources and visibility of the new entrant to be much larger than their own, the existing firms are unlikely to fight head-to-head against the aggressive entrant. As the magnitude of the threat that the new entrant represents increases, particularly in situations where the entrant benefits from large power and resource asymmetry, the existing firms will likely find it increasingly difficult to respond (Dasgupta & Stiglitz, 1980; Smith et al., 2001). Existing players cannot easily find effective competitive actions against the entrant (Chen & Hambrick, 1995; Young, Smith, & Grimm, 1996) and, thus, face the prospects of a deteriorating market position and increased risk of market viability (Hannan & Carroll, 1992). Such a situation discourages the existing players from investing in the focal market and adjacent markets that are likely targets of a resource-rich entrant. Doing so becomes increasingly risky and appears to be a “lost battle.” Retreats from the market will likely intensify among the existing players (Baum & Korn, 1996; van Witteloostuijn & van Wegberg, 1992).

The case of a platform owner with a closed and reigning approach to governance entering a complementor market resembles the scenario above. As noted earlier, a platform owner typically has a much larger resource base than its complementors and significant power and influence over them (Boudreau & Hagiu, 2009). A reigning platform owner will enter the market decisively and aggressively, intensifying competitive pressure on complementors and, thus, lowering their value-appropriation potential. The disadvantageous asymmetry they face will cause complementors to find continuing to invest in the focal and adjacent markets less attractive. They will likely substantially reduce their level of investment in these markets (Boone, 2000). The owner’s forceful exercise of power and control will reinforce the complementors’ perception of the closed and reigning governance approach as detrimental to their prospects, leading them to reduce their level of engagement in markets they consider at risk.

However, we expect a different situation when the entrant into complementor spaces is a platform owner with an open and laissez-faire approach to governance. In this case, the owner’s entry will be perceived as nonaggressive and even offering possibilities to “enlarge the pie,” bringing opportunities to all players. Competitive dynamics theory posits that the firms’ incentives to further invest in the focal and adjacent markets will likely increase when new conditions enhance their positions and increase chances to appropriate value (e.g., Boone, 2000; Nalebuff & Brandenburger, 1996). Pursuing an open, laissez-faire approach will lead the owner to exert mild or minimal competitive pressure on existing complementors and to provide them with new opportunities to grow their business through exploiting technological synergies and benefiting from the market space’s enhanced visibility. Thus, complementors’ engagement in the focal and adjacent markets will likely not diminish; indeed, given complementors expectation of positive spillover benefits from the owner’s entry, it could even increase.

Taken together, we argue that the owner’s mode of entry into complementor spaces, a reflection of the approach to platform governance, will result in markedly different engagement strategies from the affected complementors, thereby leading to different levels of investment into the markets they consider at risk of being affected by owner entry. This will particularly apply to complementors that have first-hand experience with both platforms—that is, those whose apps have multihomed. Multihoming would allow complementors to experience or witness owner entry and its consequences in each case and convey a much clearer perception of and specific reference points for the risks and benefits of entry by each type of platform owner. It then follows:

Hypothesis 2a: The entry of a platform owner with a closed and reigning approach to governance to a focal complementor market is negatively associated with the affected complementors’ investment into the focal and adjacent markets. Hypothesis 2b: The entry of a platform owner with an open and laissez-faire approach to governance to a focal complementor market is positively associated with the affected complementors’ investment into the focal and adjacent markets.

Data and Methods

Empirical Context: H&F Mobile Ecosystem

Our empirical context comprises two leading mobile platforms in the United States: the Apple iOS and Google Play app stores. Apple and Google launched their app stores in July 2008 and October 2008, respectively. These two players dominate the market, fiercely competing against each other while jointly capturing over 90% of the market share on mobile platforms. In 2020, Apple and Google had around 2 million apps for download in their respective stores.

Our paper focuses on a single mobile app category, H&F, to mitigate concerns over possible confounding effects that could come from combining different categories (e.g., Foerderer et al., 2018; Shaheer & Li, 2020). The H&F category offers an ideal setting to explore our research questions, for several reasons. First, it is an established category. The H&F category ranks 8th in size out of 25 categories in the Apple iOS app store and 11th out of 35 categories in the Google Play app store. Second, the H&F category is relatively fragmented and fiercely contested. No single firm or even a small number of firms dominates the market, making it suitable for exploring within-platform dynamics. Third, platform owner entry into complementor markets took place in H&F in the two app stores just 1 month apart. Apple and Google launched their own mobile H&F apps, respectively labeled Apple Health and Google Fit, with functionality overlapping that of some third-party apps in their stores. However, due to their contrasting approaches to platform governance, the specific mode of entry that each platform owner employed in its incursion into its respective complementor market starkly contrasts with the other’s. Thus, we can examine the role of entry mode heterogeneity in platform owner entry. (The main differences appear in the section “Apple Health and Google Fit Release” below.) Finally, the launch of Apple Health and Google Fit did not affect all H&F apps equally. The H&F category can be divided into subcategories, based upon a focal area of business and its primary purpose (e.g., running apps, nutrition apps, mental apps). At their initial launches in 2014, Apple Health and Google Fit did not cover all the H&F subcategories; thus, their effect varied by subcategory. This heterogeneous subcategory effect enables us to use some H&F subcategories as a control to explore the consequences of platform owner entry.

Data

Given the emerging state of research on platform owner entry into complementor spaces, we conducted a large-scale quantitative analysis together with qualitative examination, to elucidate the underlying mechanisms and to better interpret our quantitative results.

Quantitative dataset

We constructed a unique dataset from three sources. First, our primary data came from the leading mobile analytic intelligence company, Apptopia, upon which other studies of mobile platforms have relied (e.g., Chen et al., 2022; Chen, Wang, Cui, & Li, 2021; Shaheer & Li, 2020). We acquired data on app performance in the form of the numbers of downloads estimated from ranking data that Apple and Google provide (Apple and Google do not publicly disclose download data for individual apps, but they provide ranking data based upon the number of downloads). Prior studies use app download estimates as proxies for app performance (e.g., Carare, 2012; Chen et al., 2022; Garg & Telang, 2013; Shaheer & Li, 2020). We combined these data with app metadata (e.g., app description, app release date, app reviews and ratings, and app portfolio) gathered through manual collection and web scrawling from official app stores and other mobile analytic sites (e.g., App Annie Store Stats and Sensor Tower).

To construct our sample, we assembled a panel dataset with all the H&F apps that our primary data provider tracked. At the time of our data purchase, the company tracked the 1,500 most downloaded H&F apps in the Apple iOS app store and the 600 most downloaded H&F apps in the Google Play app store. Product demand from mobile app stores is highly skewed with a long-tail distribution (Chen et al., 2022; Lee & Raghu, 2014). For instance, around 80% of user demand goes to only 20 apps out of the 1.4 million apps on the market (Bresnahan, Davis, & Yin, 2014). Therefore, our sample is large enough to include apps with very different download figures, ranging from the highly successful to others with no downloads. Indeed, several studies examine top-ranked apps using smaller samples than ours (e.g., Ghose & Han, 2014; Li & Agarwal, 2017). Our data covers from July 1, 2014, to December 31, 2015.

From time to time, some apps are removed from the stores, often due to lack of compatibility after system upgrades; we excluded such cases from the analysis. Furthermore, we considered only those apps launched before the actual platform owner entry (that is, the official launch dates for Apple Health and Google Fit), to allow for before-and-after platform-owner-entry comparisons. We restricted the final sample to apps released before July 1, 2014, to have sufficient pre-owner-entry data points, and we followed these apps until the release of the new versions of Apple Health and Google Fit, which came in late 2015 (September 9 and November 10, respectively).

Qualitative dataset

We also conducted two types of qualitative analyses, to deepen our understanding of the context of our research and validate our quantitative results. First, we conducted more than 20 semistructured interviews, each lasting 30–90 min, with app developers and industry experts (e.g., analysts and executives of mobile analytic firms). Second, we performed an exploratory content analysis of online discussion forums for app developers, business press releases, official app store websites and their developer communities, and our minutes from interviews covering the Apple Health and Google Fit releases. We gathered all qualitative information during the months following the respective launches of Apple Health and Google Fit, supplementing our regression results with the qualitative insights detailed below.

Apple Health and Google Fit Release

Apple and Google launched their apps in their respective stores on September 17 and October 28, 2014, respectively. Both Apple Health and Google Fit provided functionality already available from some third-party H&F apps on their platform. Both Apple Health and Google Fit could work as stand-alone apps. Users could now store, record, and track a range of H&F data directly in Apple Health or Google Fit without relying on third-party apps. Simultaneously, Apple and Google shared their product’s underpinning technologies with their complementors, releasing corresponding APIs, through which third-party H&F apps could access the key functions of each owner’s app. For example, third-party H&F apps could directly embed the tracking functionality of Apple Health and Google Fit into their apps or import/export H&F user data from/to Apple Health and Google Fit. Thus, while the owner’s products had functionality that overlapped those of complementor products, they also provided a mechanism for the complementors to take advantage of the possibilities the owner’s new product represented.

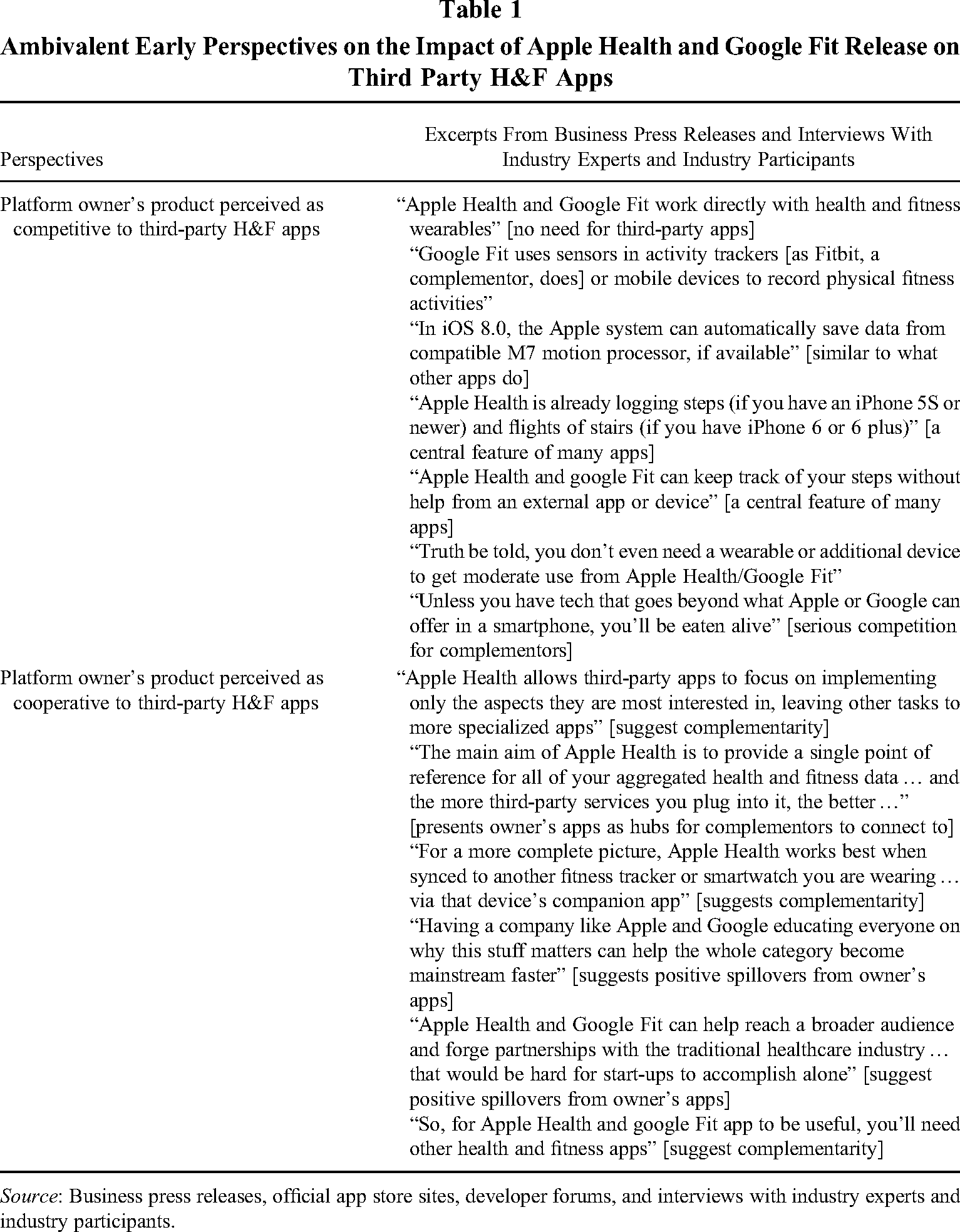

Table 1 provides qualitative evidence of the industry stakeholders’ early reactions. Ambivalent sentiments had prevailed surrounding the potential impacts on the third-party H&F app ecosystems of Apple Health and Google Fit releases. The opinions mixed positive and negative predictions, hinting at considerable uncertainties among industry participants and analysts regarding the ultimate effect that the two apps would have on complementors. By and large, industry participants perceived the launches of Apple Health and Google Fit as equivalent, simply occurring on competing platforms. These ambiguities, also present in extant studies of platform owner entry, highlight the importance of our approach to parse out the role of heterogeneity in owner’s “mode of entry” on the relationship between owner entry and complementor performance.

Ambivalent Early Perspectives on the Impact of Apple Health and Google Fit Release on Third Party H&F Apps

Source: Business press releases, official app store sites, developer forums, and interviews with industry experts and industry participants.

While Apple and Google released their apps almost simultaneously, the specific mode of entry into their respective app stores markedly differed. Apple and Google have pursued a starkly contrasting approach to platform governance (Eaton, Elaluf-Calderwood, Sørensen, & Yoo, 2015; Parker, van Alstyne, & Jiang, 2017). Their respective entry mode in releasing Apple Health and Google Fit reflected this different approach to governance. On the one hand, Apple has been known to pursue a closed and reigning governance approach with tight central control. For instance, Apple has a rigorous quality-review system in place to gatekeep those who wish to publish their apps in iOS, with Apple fully controlling the distribution channel (Benlian, Hilkert, & Hess, 2015; Schaarschmidt, Homscheid, & Kilian, 2019). Apple also reserves most of the rights in appropriating developer innovation in its platform ecosystem, curating the admission of codes by third parties and controlling a set of boundary resources, such as APIs and SDKs, which Apple approves and distributes (Eaton et al., 2015; Parker et al., 2017). Such a closed approach to governance has allowed Apple to claim more of the value created within its platform—for example, Apple charges higher prices than competing platforms, thus obtaining higher margins (Parker et al., 2017). On the other hand, Google has taken a contrasting approach to governance, relatively open and laissez-faire with modest central control (Karhu et al., 2018; Parker et al., 2017). For instance, there is no formal approval process for developers to publish their apps. Furthermore, Google allows the sale of Android apps in app stores other than its own, such as the Amazon app store (Remneland-Wikhamn, Ljungberg, Bergquist, & Kuschel, 2011; Schaarschmidt et al., 2019). Also, Google provides ample access for developers to not only use platform-wide technical interfaces, such as APIs and SDKs, but also integrate or extend them or replace existing components in the Android codebase (Schlagwein, Schoder, & Fischbach, 2010). Google’s open approach, while resulting in lower revenue for the platform compared to Apple’s, has fueled platform growth by attracting a larger number of apps and developers (Parker et al., 2017).

The companies’ distinctive approach to platform governance was visible in the way each entered its complementor space when releasing its H&F app. The differences were striking. Apple tightly controlled access and imposed restrictions on user and developer use of both Apple Health and its related technologies. For example, Apple Health came as a default program on iOS devices, pre-installed in all new iPhones and automatically installed in all existing iPhones (without user permission) during iOS operating system upgrades. Apple did not even allow users to delete the app, effectively resulting in forcing users to have the app on their devices. Apple also kept Apple Health compatibility relatively closed with limited device support, making its Health app available only to iPhones. The company also tightly controlled the Apple Health-related APIs, distributing them only in a standardized format that provided little room for developers to customize or modify. Apple controlled and structured the data types and gave developers no discretion to create custom data types or units, constraining them to use only Apple-approved data types on an official list. Furthermore, Apple did not allow third-party apps to use Apple Health APIs without integrating their products with Apple Health. Apple asked developers to explicitly mention the use of Apple Health APIs in describing their app; failure to comply led to barring their apps from the store. Apple also restricted the data stored using Apple Health APIs. Data exported from Apple Health had to conform to strict Apple specifications and reside only on iPhone devices. Developers could not use in their advertising any information about users’ H&F activities coming from Apple Health APIs. Apple reserved the right to earn on ads that used information coming from Apple Health. It also required developers to share their complete dataset with Apple Health to utilize the Apple Health APIs.

Google took a very different approach, giving users and developers ample freedom in the use of the Google Fit app and its underpinning technologies. Google Fit was not pre-installed, requiring a manual download by users who wanted the app. Those wishing to install Google Fit had to search for the app in the Google Play store and install it on their smartphones as they would any third-party app. Moreover, users could choose to delete the app anytime. Google kept Google Fit relatively open by supporting a wide list of compatible devices across Android-based phones, tablets, wearable gadgets, and the web, as long as the app was signed into a Google account. Google also offered third-party developers ample choice in how to access and use the Google Fit APIs, comprising multiple separate subsets that allowed developers to mix and match for their specific needs. For instance, some of the API subsets focused on sensors, which let developers read raw sensor data on devices or wearables; others focused on recording, which let developers gather, store, or sync data of a user’s physical activities; another focused on history, giving developers access to historical fitness and wellness data and enabling data management to insert, delete, or read the data. Furthermore, developers could use Google Fit technologies in their products without having to ask consumers to install the Google Fit app. In addition, developers were free to customize the data structure and format as they wished or even to share these customized pieces of software with other developers on the platform. Google accepted many types of data from third-party apps, including those data types it did not directly support. Google also did not place specific constraints on using data stored in Google Fit APIs, except to forbid its use for questionable advertising, such as to promote the development of gambling. Moreover, Google did not set any strict requirements for third-party apps to share the data they collected through the Google Fit APIs. In practice, some apps shared their data with Google, while other apps did not share data with Google at all.

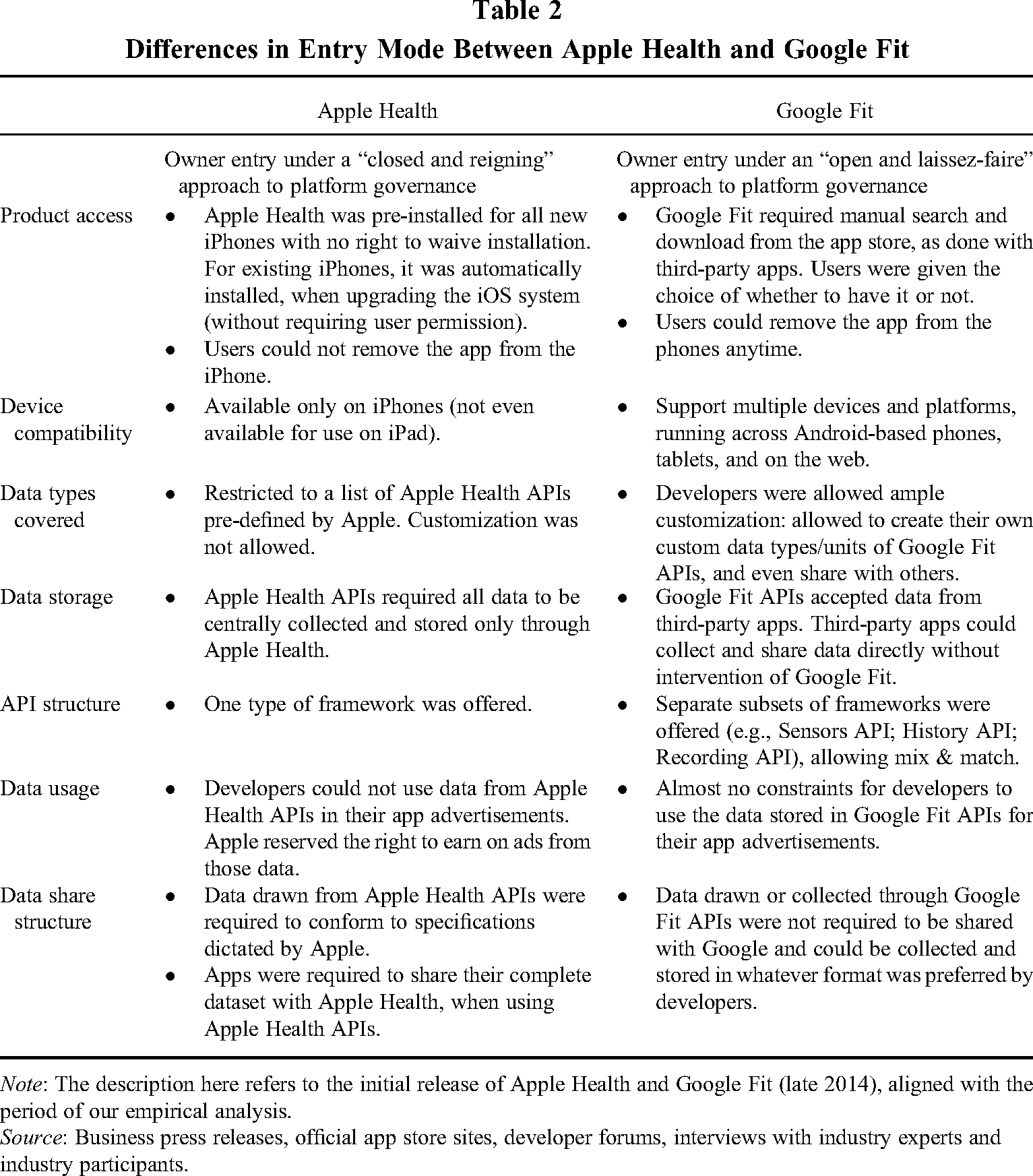

Table 2 summarizes these key differences in owner entry mode between Apple Health and Google Fit, coming from our qualitative examination of the official app stores, news articles, and press releases. Industry participants acknowledged that Google Fit offered more flexibility and compatibility than Apple Health, which placed much emphasis on data security. However, the difference in the mode of entry between Apple Health and Google Fit was much more profound than that, and industry participants did not fully grasp how these differences would shape the H&F app ecosystem differently. Industry participants had largely perceived Google Fit as the counterpart to Apple Health and simply a reflection of the strong rivalry between these platform competitors. The following quote represents the prevalent views of participants: There is no clear winner here. Google has a wide list of compatible devices and partners … Google Fit offers more flexibility; Healthkit offers more security of the sensitive content. But one thing we can surely say is that with Health and Fit, we have officially entered the commercial phase of digital health revolution.

Differences in Entry Mode Between Apple Health and Google Fit

Note: The description here refers to the initial release of Apple Health and Google Fit (late 2014), aligned with the period of our empirical analysis.

Source: Business press releases, official app store sites, developer forums, interviews with industry experts and industry participants.

This sentiment among industry practitioners substantiates the importance of our study’s systematic look at the difference between Apple Health and Google Fit, drawing on a careful quantitative examination using a large-scale panel dataset.

Types of Apps Affected by Apple Health and Google Fit Release

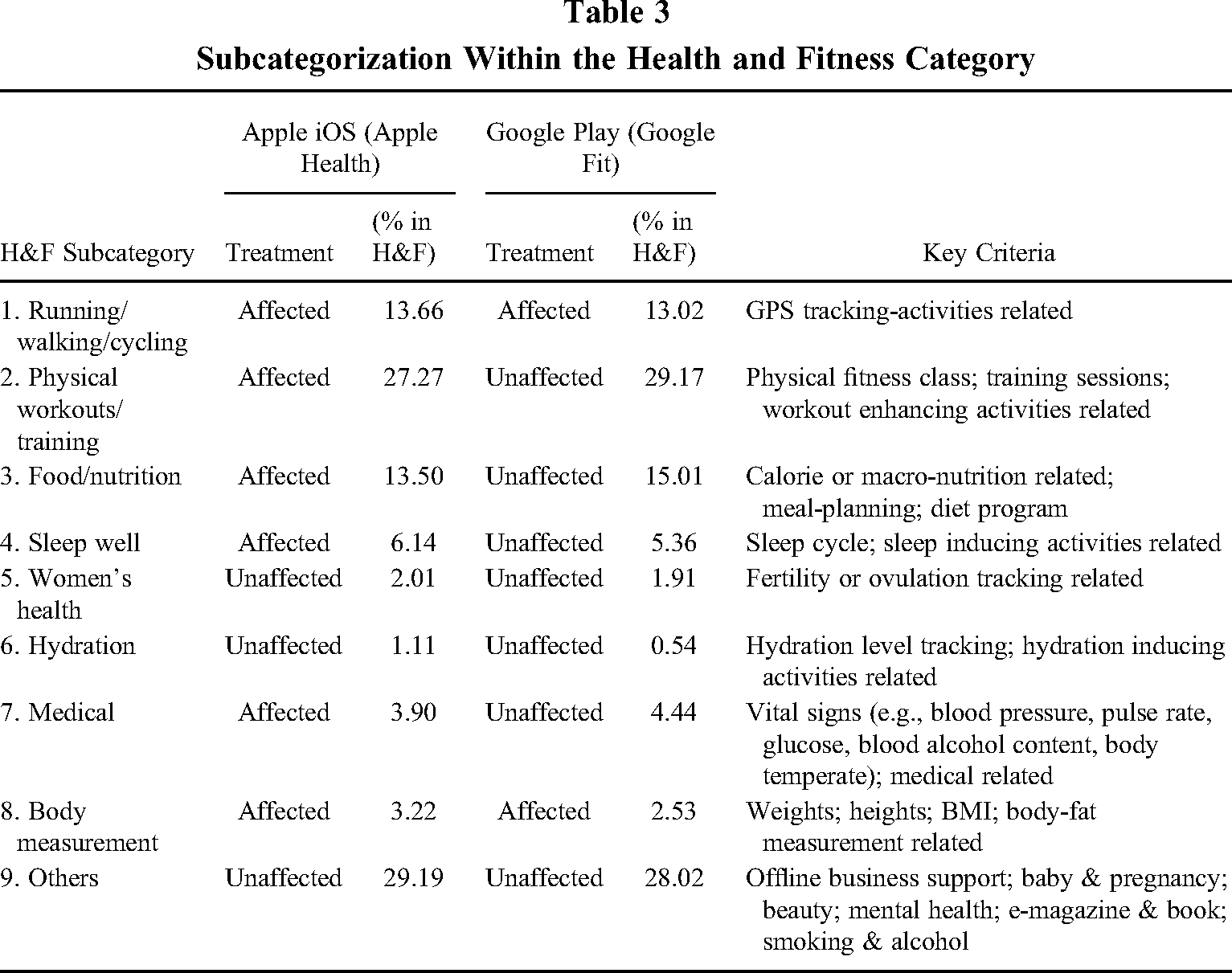

As noted earlier, the apps that belong to the H&F category can be divided into subcategories based upon their primary focus of activity and functionality. Using the descriptions both app stores provided and after consultation with our industry informants, we distinguished nine subcategories within H&F: running/walking (pedometer)/cycling, physical workouts/training, food/nutrition, sleep, women’s health, hydration, medical, body measurement, and others. Table 3 shows a brief description of each subcategory.

Subcategorization Within the Health and Fitness Category

We set out to identify these subcategories by considering how the app stores listed those apps on their H&F page. While neither Apple nor Google used a specific set of subcategories for H&F, they sometimes listed apps under themes such as Sleep Well, Nutrition, and Workouts. We carefully reviewed titles, app descriptions, and snapshots of those apps, to understand how the app stores sorted them into subgroups. We then looked at how leading mobile analytic sites grouped H&F apps and how H&F journals referred to groups of apps when they reviewed them. We focused particularly on the core functionality of each app and used that together with the groupings the platforms, mobile analytic companies, and H&F journals employed, to produce a comprehensive but parsimonious list of subcategories. For example, we grouped running/walking/cycling apps as one subcategory because they all use the GPS tracker for their core functionality. Also, as was often the case, most apps in this subcategory offer the three capabilities together (running, walking, and cycling), further suggesting that these activities can be grouped as one H&F domain. Last, we polished this subcategorization through iterative discussions with industry experts and informants, looking for mistakes or omissions. We then carefully coded our data by assigning each app to a corresponding subcategory, based on its title, description, and snapshots determining its capabilities. We checked the accuracy of this coding task by drawing a random sample of apps and asking our research assistant to replicate the task. The interrater reliability was over 86%.

The impact of Apple Health and Google Fit varied by subcategory. For instance, at their initial launch, Apple Health and Google Fit both offered tracking as a key functionality, and this functionality covered running activities, thereby directly affecting running apps. However, neither Apple Health nor Google Fit initially included tracking functionality for activities related to women’s health (e.g., tracking fertility or ovulation cycles). Therefore, unlike running apps, the initial release of Apple Health and Google Fit did not directly affect apps focusing on women’s health. We exploited this heterogeneity by subcategory in the extent and timing of each platform owner entry. Our treated group comprises apps whose focal subcategory was directly affected by the owner’s product. Our control group comprises the apps whose primary subcategory was not directly affected by the owner’s product. Apple Health and Google Fit affected different subcategories in H&F within their respective platforms, as Table 3 shows. The initial release of Apple Health in 2014 affected the H&F apps in the subcategories running/walking/cycling, physical workouts/training, food/nutrition, sleep well, medical, and body measurement. It did not affect the remaining three subcategories, women’s health, hydration, and others. The initial release of Google Fit in 2014 affected the H&F apps in subcategories running/walking/cycling and body measurement, while the other seven subcategories remained unaffected.

Based upon this classification, as Table 3 illustrates, we could have run our analyses drawing on affected (unaffected) groups. However, to further account for any potential unobserved heterogeneities that may be associated with assignment to a set of subcategories across these two platforms, we kept our analysis to a common set of affected (and unaffected) subcategories across the two platforms. 2 Therefore, our analyses only consider the subcategories that were commonly affected or unaffected on both platforms. This led us to consider the subcategories running/walking/cycling and body measurement as affected in the analyses of both platforms and the subcategories of women’s health, hydration, and several of the subcategories included in “others” as unaffected apps in both platforms. The subcategory “others,” as seen in Table 3, comprises multiple subgroups, such as baby and pregnancy, mental health, beauty, quitting tobacco and alcohol, and miscellaneous groupings. We thus further scrutinized the others subcategory to make sure that they were classified in the same way in each platform, either affected or unaffected when they corresponded. We excluded from the analysis those that did not meet this condition—these accounted for only 2% or less of the total apps in the “others” subcategory.

Variables

Dependent variables

For Hypothesis 1, our dependent variable is product performance, which we measured as the number of downloads of a given app. Mobile platform markets have a highly skewed long-tailed distribution, so the variable enters the analysis in a natural logarithm form to address that skewness. For Hypothesis 2, our dependent variable is platform investment, which we measured by counting the number of new apps released by complementors in the H&F category, which represent the focal, adjacent markets that are considered at risk of being affected by platform owner entry. We also apply a logarithm transformation to this variable to address skewness in the distribution. 3

Independent variables

We took advantage of the heterogeneous impact of platform owner entry by subcategory within the H&F category, creating a dummy variable, affected apps by platform owner entry. This variable takes the value of 1 for apps whose focal subcategory was affected by an owner’s entry and a value of 0 for apps whose focal subcategory was not affected. To account for possible subcategory heterogeneities, as noted earlier, we restricted our sample to those subcategories that were commonly affected or unaffected across both platforms.

We also computed the variable after platform owner entry to analyze the before-and-after consequences of platform owner entry. This variable takes the value of 0 for the period before the launches of Apple Health and Google Fit and the value of 1 for the periods after those launches. We then interact the variables affected apps by platform owner entry and after platform owner entry to capture the consequences of platform owner entry on affected complementors.

Our key argument captures the variance in the mode of platform owner entry into its complementor spaces, specifically the difference between the decentralized “open and laissez faire” approach that Google followed when launching Google Fit and the centralized “closed and reigning” approach that Apple followed when launching Apple Health.

Control variables

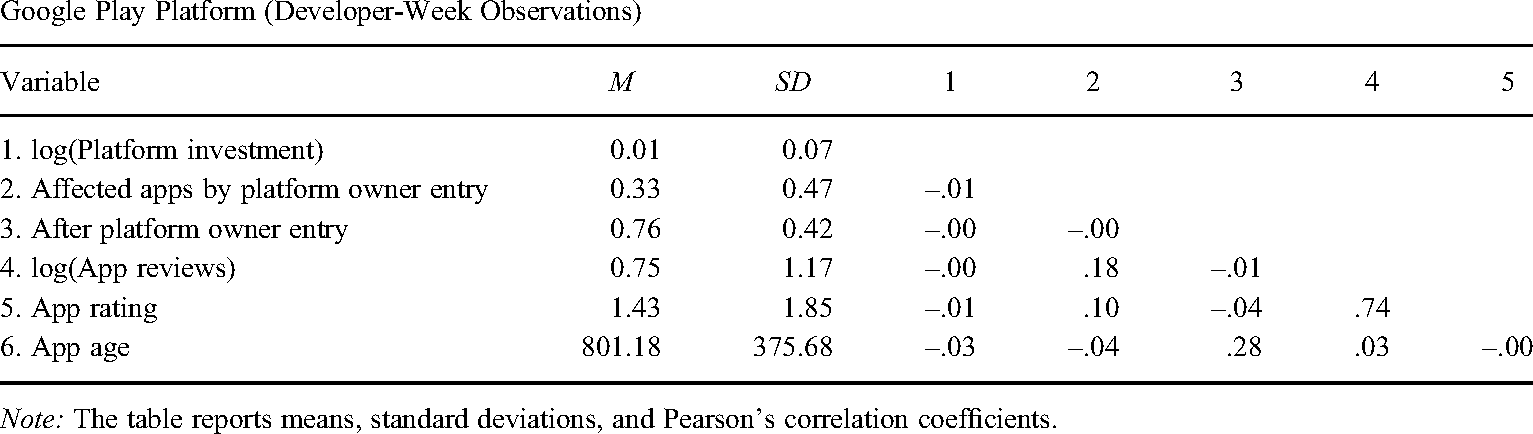

We include a set of control variables that can affect app performance and complementors’ engagement decisions. The variable app age and its square term account for an app’s exponential downward-sloping curve (operationalized as time elapsed since an app was first launched; a proxy for an app’s vintage effect). The variable app reviews is a proxy for an app’s visibility and popularity (measured by the number of reviews an app received in a given week, using a logarithm form to account for skewness). The variable app rating is a proxy for an app’s perceived quality, operationalized as the app’s average review score in a given week on a 0–5 scale, where 0 indicates an app with no rating, as in previous studies (e.g., Zhu & Liu, 2018). Table 4 reports summary statistics and correlations for our variables.

Descriptive Statistics and Correlation

Note: The table reports means, standard deviations, and Pearson's correlation coefficients.

Note: The table reports means, standard deviations, and Pearson's correlation coefficients.

Note: The table reports means, standard deviations, and Pearson's correlation coefficients.

Note: The table reports means, standard deviations, and Pearson’s correlation coefficients.

Our final sample includes, for Apple iOS app store, 13,696 observations at the app-week level and 8,192 observations at the developer-week level and for Google Play app store, 8,640 observations at the app-week level and 5,112 observations at the developer-week level.

Methodology

We use a fixed-effects ordinary least squares (OLS) specification to examine changes associated with a platform owner entry on the performance of affected complementor products and the level of complementor engagement with the focal platform. Previous studies on the topic used a similar research design (e.g., Foerderer et al., 2018; Wen & Zhu, 2019; Zhu & Liu, 2018). We employed fixed effects at the subcategory level and platform level to control for possible unobserved subcategory-specific and platform-week-specific heterogeneities.

4

We report robust standard errors clustered around the subcategory level to account for serial correlation of the error term. Our Hypothesis 1 explores the product performance of the affected complementors after platform owner entry; therefore, our analysis for H1 occurs at the app level. Our Hypothesis 2 explores the new product development activities of the affected complementors after platform owner entry, so our analysis for H2 occurs at the developer level. The following equations represent our model of choice, in which i indexes subcategories, j indexes apps, k indexes developers, l indexes platforms, t indexes time (weeks), and u is the error term: log(Product performance

jilt

) = β0 + Affected apps by platform owner entry

jilt

β1 + After platform entry

jilt

β2 + Affected apps by platform owner entry

jilt

× After platform owner entry

jilt

β3 + α

i

× α

l

+ u

jilt

log(Platform investment kilt ) = β0 + Affected apps by platform owner entry kilt β1 + After platform entry kilt β2 + Affected apps by platform owner entry kilt × After platform owner entry kilt β3 + α i × α l + u kilt

Ideally, we would randomly assign complementors to affected and unaffected domains by platform owner entry. Our qualitative evidence (as Table 1 shows) suggests that complementors in our sample might have been unable to anticipate the extent and directionality (positive, negative) of the impact of Apple’s and Google’s entry into the H&F area. As detailed earlier, industry participants were uncertain about the impact that Apple Health and Google Fit would have on complementors, largely considering Apple Health and Google Fit as equivalent offerings happening on competing platforms. There was also scant information or anticipation regarding the precise scope of the impact (i.e., which H&F subcategories would be most affected). For example, the subcategory “women’s health” was not part of the initial 2014 release of Apple Health or Google Fit. However, Apple included it 1 year later when it released an Apple Health update. Industry informants concurred that the primary reason for Apple not including this subcategory in the original release was that most Apple developers were male and inadvertently omitted this subcategory in its initial launch.

Despite this, we conducted additional analyses to further account for potential unobserved heterogeneities that may be associated with belonging to a certain H&F subcategorical domain on each platform, which could potentially create omitted variable bias and selection bias. First, we employed a coarsened exact matching (CEM) analysis (Blackwell, Iacus, King, & Porro, 2009; Iacus, King, & Porro, 2012). The CEM analysis allowed us to pair unaffected apps with affected apps that are similar except for the fact that the latter experienced platform owner entry. We matched affected and unaffected apps on the variables app age, app reviews, app rating, a set of key dimensions that could result in confounding effects. The degree of imbalance is reduced for both samples after matching. For Apple, L1 statistics before matching is 0.14, and it becomes 0.06 after matching (57% reduction in imbalance). For Google, L1 statistics before matching is 0.46, and it becomes 0.16 after matching (65% reduction in imbalance). After applying CEM, we observe no statistically significant differences between the elements of the two groups, suggesting that the two samples are quite similar (see Appendix A for details).

Moreover, we further restrict our analyses to the set of apps that multihome—that is, apps available on both Apple and Google platforms. 5 Multihoming apps that share identical characteristics at the product and developer levels can present a unique setting in the context of a mobile app market wherein comparisons between an identical set of apps are possible (Chen, Zhang, Li, & Turner, 2022). This allows us to better control for any potential differences in product or complementor characteristics that could be associated with the dynamics on different platforms. The resulting comparison groups become thus as similar as possible given our dataset.

Results

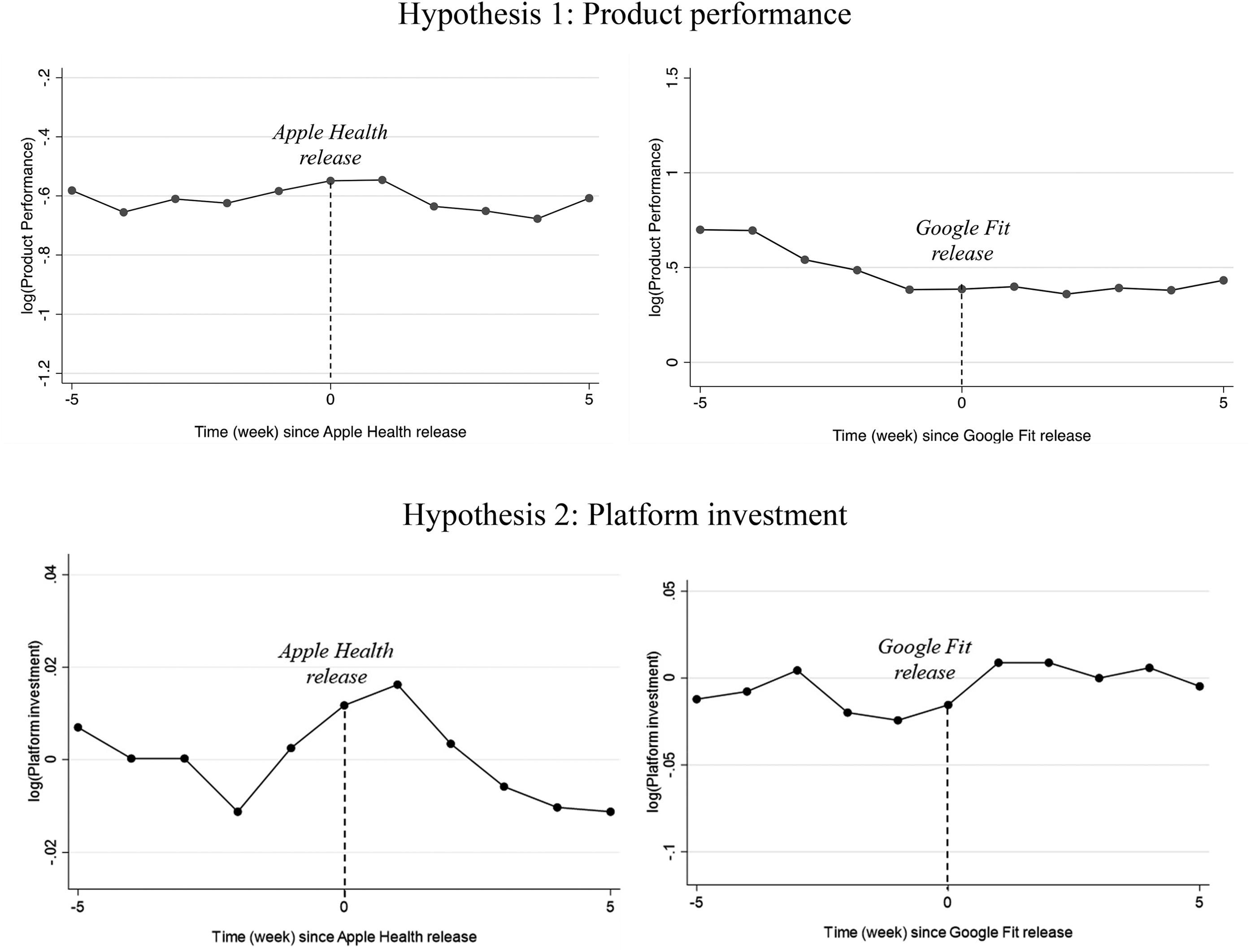

Figure 1 presents the plots of the differences in the outcome variables between affected and unaffected groups. The graphs suggest different patterns before and after platform owner entry for both hypotheses. For Hypothesis 1, the upper-left graph suggests that after owner entry, the affected group in the Apple ecosystem reverses the prior trend and begins to gradually underperform, compared to the unaffected group. The upper-right graph suggests that after owner entry, the affected group in the Google ecosystems reverses a pre-entry declining performance, compared to the unaffected group, and begins a slight upward trend. For Hypothesis 2, the lower-left graph suggests that the relative investment of the affected group in the Apple ecosystem decreases substantially after owner entry, reversing a prior trend. The lower-right graph suggests that the investment of the affected group in the Google ecosystem slightly increases after owner entry, compared to the unaffected group. Even though we do not observe perfectly parallel trends prior to owner entry, our graphs suggest that there are visible ruptures from the prior trend after the owners enter their respective complementor spaces. We then run regression estimates that help us statistically confirm these contrasting results associated with the specific modes of platform owner entry. Table 5 shows our regression results. We split the sample between Apple and Google and ran models separately. This approach allowed the variance to differ across the two different models and facilitated the interpretation of the results.

Difference in Outcome Variables Between Affected and Unaffected Groups Before and After Platform Owner Entry.

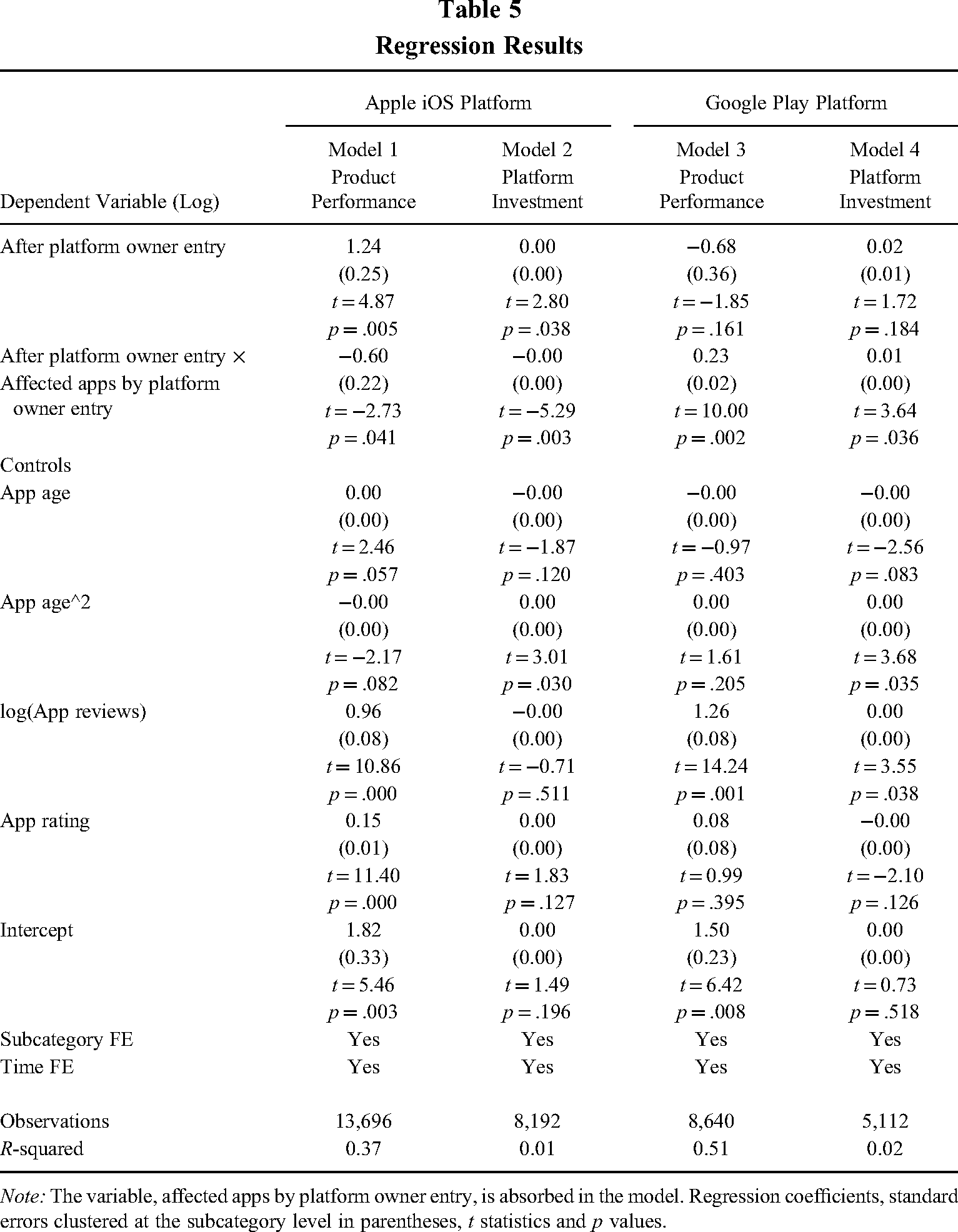

Regression Results

Note: The variable, affected apps by platform owner entry, is absorbed in the model. Regression coefficients, standard errors clustered at the subcategory level in parentheses, t statistics and p values.

Models 1 and 3 test Hypotheses 1a and 1b. Model 1 shows the regression result for Apple, whose mode of entry we have classified as a centralized one, stemming from a closed and reigning approach to platform governance. The coefficient estimate for After platform owner entry × Affected apps by platform owner entry is negative and statistically significant. The apps that the introduction of Apple Health affected experience a significant decrease in downloads, around 60% lower than the unaffected apps. This supports our Hypothesis 1a. Model 3 shows the result for the analysis of Google, whose mode of entry we have classified as decentralized, stemming from an open and laissez-faire approach to platform governance. The coefficient estimate of interest is positive and statistically significant. The apps that the introduction of Google Fit affected experience a significant increase in downloads, around 23% higher than the unaffected apps. This supports our Hypothesis 1b. The difference between the two coefficients of the separate models is statistically significant at a p value of 0.05 level. This marked difference underscores the nuanced coopetitive dynamics that platform owner entry entails, highlighting the role that the specific entry mode has in determining the ultimate valence of the impact of owner entry. Taken together, our findings support Hypotheses 1.

We then test our Hypotheses 2a and 2b in Models 2 and 4, as Table 5 shows. Model 2 shows our regression results for the case of Apple—namely, that complementors decrease their level of investment into their focal and adjacent markets, supporting Hypothesis 2a. Model 4 shows our regression results for the case of Google—namely, that complementors increase their level of investment into the focal and adjacent markets, supporting Hypothesis 2b. The difference between the two coefficients in the separate models is statistically significant at a p value of 0.05 level, lending credence to Hypotheses 2a and 2b.

We conduct additional analyses to address possible alternative explanations and confirm the robustness of our argument.

First, we investigate the number and type of inquiries and replies that developers posted in one of the most representative developer communities, Stack Overflow, to further analyze developers’ perceptions of the differences between Apple Health and Google Fit after their official release. Stack Overflow is the largest online community that developers use to learn, share their software knowledge, and help each other with issues they encounter in writing software. We found close to 2,400 queries posted and answered that related to Google Fit and Google Fit APIs, while only around 650 queries related to Apple Health and Healthkit APIs. This stark difference in the number of queries for the owner H&F app in each platform can be partly explained for the larger market share that Android had and partly by the fact that Google provided developers with much more discretion and latitude to work with its product than Apple did. We then used the Stack Overflow queries dataset to examine differences in perception of Apple Health and Google Fit. Since studies show that people tend to report and comment more on negative aspects of products or services than on positive ones, we reviewed queries and decided to focus on such aspects in the developers’ comments. In particular, we selected words that would imply perceptions of a “controlling and reigning approach” since developers would probably resent that. Scanning the words used, we zeroed in on the following that appeared more frequently than other similar words: “restrict,” “control,” “limit,” “force,” and “prevent.” As our theorizing suggests, we found that the developer queries about the Apple product, the controlling platform, had a larger proportion of those words. Despite having a lower total count of queries, Apple Health totaled 76 queries that included one of the above words. Google Fit only totaled 34 queries: that is, Apple count was around 125% larger than Google’s. We also ran a robust analysis using a larger set of keywords, 27 words defined in the Merriam-Webster Reference as synonymous to the particular meaning of “controlling” that captured our intended meaning here—that is, exercising authority or power. Our results held consistent: Apple count was 56% larger than Google’s, even with this larger set of words.

Second, we include the overall platform market performance in the analysis, measured as the total number of app downloads on each platform, to account for the possibility that our results might have been driven by some difference in the overall platform performance. The results, reported in Appendix B, are still consistent with our main analysis.

Last, we run additional analyses to account for potential spillover effects on product performance that may stem from being present on both platforms. For instance, the performance outcomes of the affected complementors whose apps multihomed might be due in part to learning effects derived from the other platform. To control for this possibility, we conduct a robust analysis by restricting our sample to single-homing apps for Hypotheses 1a and b. The results remain largely consistent with our main analysis. For Google, the coefficient estimate of interest is still positive and significant, and for Apple, the coefficient estimate of interest is still negative with marginal significance (see Appendix C for details).

Discussion and Conclusion

Platform owner entry into complementor spaces is on the rise and can significantly shape intraplatform dynamics and transform the battlegrounds on which complementors compete. However, we still lack a more precise understanding of how platform owner entry affects complementors, as evidenced in the contradictory findings in extant studies on the topic. Research on the consequences of platform owner entry for complementors has produced mixed evidence. Some studies find positive effects on complementor performance (e.g., Foerderer et al., 2018; Li & Agarwal, 2017); others find negative effects (e.g., Gawer & Cusumano, 2002; Wen & Zhu, 2019).

Our paper addresses the gap in extant research by relaxing an implicitly held assumption—namely, that the “mode of entry” is basically the same in each case of owners entering complementor spaces. By drawing on the theoretical lens of competitive dynamics, we bring to the fore the possibility that how an owner enters its complementor spaces determines the level of competitive pressure it exerts on the affected complementors, which in turn ultimately determines the valence of that impact. We further argue that the specific mode of entry that a platform owner deploys when entering a complementor market is likely to reflect the platform’s approach to governance since platform governance is conceptualized as a stable attribute of platforms encompassing a wide array of platform-wide practices and strategies.

In the context of mobile platforms, our results support our prediction that the mode of entry plays a significant role in defining levels of competitive pressure on the affected complementors. We show that platforms with markedly different governance approaches that lead to contrasting modes of entry can result in opposite performance repercussions and responses from complementors. The platform that follows a closed and reigning approach to governance enters its complementor space more aggressively, tightly controlling the access to and usage of its product and technologies. Such an entry mode increases competitive pressure on complementors and can ultimately be detrimental to their performance. In addition, it can lead those complementors to disengage from investing in the focal and adjacent markets where they perceive the risk of owner competition. In contrast, the platform that follows an open and laissez-faire approach to governance enters complementor spaces less aggressively, ceding to complementors decision rights and control of the access and usage of its product and its underlying technologies. Such an entry mode will likely produce positive spillover effects for complementors, leaving them ample room to leverage the owner’s offerings to their advantage. This can ultimately result in a positive influence on the product performance of the affected complementors and, in turn, increase their level of engagement in their focal and adjacent markets, given the heightened opportunities for value appropriation.

Therefore, our results directly respond to recent calls to explain a conundrum in prior research that documents platform owner entry having different, sometimes opposite effects on complementors’ performance (e.g., Rietveld & Schilling, 2021; Zhu, 2019). Our study has implications not only for complementors but also for platform owners. Competition among platforms tends to be intense, due in part to the role of network effects that can lead to winner-take-all scenarios (Chen, Shaheer, Yi, & Li, 2019; Eisenmann, 2007; Schilling, 2002). This reality often leads platform owners to engage in a tit-for-tat competition with rival platforms, including the increasingly more common practice of entering complementor spaces (Zhao, Von Delft, Morgan-Thomas, & Buck, 2020). For example, Google entered more than 80% of the same app spaces that Apple entered (Wen & Zhu, 2019). Since the long-term success of a platform also depends on having a healthy and thriving complementor ecosystem, our findings provide important insights into minimizing the effect on complementors of an owner’s entry into their markets. Platform owners must carefully evaluate the benefits of greater value appropriation coming from an aggressive mode of entry, comparing them to the possible negative effects on their complementors and consequent disengagement from focal and adjacent markets. Our study shows that owner entry need not be detrimental to complementors. Owners can do it in a way that minimizes the effect on complementors or even generates enough spillovers to further incentivize their engagement in the markets.

Our paper also offers implications for platform complementors. Platform owner entry is an increasingly common phenomenon in modern platform industries; thus, complementors should always consider this a likely event when deciding in which market to invest their resources and creative energy. Our study shows that the implications of owner entry for the affected complementors vary greatly (even with similar product offerings from owners), depending upon the mode of entry that owners deploy. Our study can provide a meaningful guidance for complementors when pondering which platforms to enter and how much resources and efforts to allocate in a platform category. Our insights complement findings from the literature focusing on other platform dimensions that complementors should consider, such as platform size (Panico & Cennamo, 2022), platform maturity (Rietveld & Eggers, 2018), platform technological architecture (Saadatmand et al., 2019), and platform legitimacy (Taeuscher & Rothe, 2021).