Abstract

This study extends current knowledge on competition and corporate defense by investigating how firms transfer risk in response to their firm-specific multimarket and structural competitive conditions. Drawing on the theory of multimarket competition, we propose an inverted U–shaped relationship between multimarket competition and risk transfer. We also propose that, for the sake of gaining a competitive edge, the extent to which a firm manages risk will tend to be opposite to that of its competitors. Last, we propose that egocentric industry concentration will moderate the relationship between multimarket competition and risk transfer besides its direct effect. Analysis of reinsurance usage in the US property and casualty insurance industry strongly supports our model and shows that firm-specific competitive conditions are salient to a firm's risk transfer level.

Keywords

Offense wins games . . . defense wins championships.

—Paul William “Bear” Bryant, American college football player and coach

The good fighters of old first put themselves beyond the possibility of defeat, and then waited for an opportunity of defeating the enemy.

—Sun Tzu, The Art of War

Competition involves defense and offense. Yet despite the dichotomy of interfirm rivalry, the existing literature on competitive behaviors has focused predominantly on offensive moves at the firm level. Defensive moves have received little attention, with a few exceptions that have examined the timing, likelihood, or speed of response in dyadic action-reaction, with the view being more as counterattack than true defense. Herein, we define defensive actions as those purposely used by firms to maintain stability and protect against threats that may lead to undesired outcomes. The lack of research on defensive moves is problematic because knowledge of offensive actions may not be easily extended to defensive actions. It is also widely recognized that the role of defense in competition is equally as important, if not more so, than offense. In his landmark work, Porter (1980) wrote, “An effective competitive strategy takes offensive or defensive action in order to create a defendable position against the five competitive forces.” Chen and MacMillan (1992: 539) also observed that “firms constantly undertake offensive and defensive actions in their struggle for competitive advantage.”

The present study seeks to advance knowledge about defensive actions under rivalry, focusing on risk transfer in a multimarket context. Risk transfer refers to the effort of transferring part or all of the responsibility for bearing the financial consequences of a risk to another party via insurance or other contracts. An example is ExxonMobil, which announced in early 2022 that it had purchased oil spill insurance to shield potential damages related to all of its petroleum operations in Guyana. Similarly, through their credit risk transfer programs, Fannie Mae and Freddie Mac had a combined mortgage insurance coverage of $534 billion for safeguarding their unpaid principal balance over the 2013 through 2020 period. Risk transfer represents a crucial means of defense, particularly under conditions where competition is intense. The reason is that rivalries erode markups, making it difficult for firms to “pass through” to customers any cost increases caused by market shocks (Bodnar, Dumas, & Marston, 2002). Transferring risk enables firms to smooth earnings and “undertake competitive pricing in the output market without significantly reducing margins” (Brown, 2001: 421).

Studying risk transfer within a multimarket context is of theoretical interest for future research on multimarket competition and risk management. First, strategy scholars interested in multimarket competition have regarded risk as central to the logic of mutual forbearance. Multimarket competition or multimarket contact (MMC) denotes situations in which firms compete against one another concurrently in two or more markets (Haveman & Nonnemaker, 2000). As articulated by Yu and Cannella (2013: 77), “firms that meet each other in many markets may hesitate to fight vigorously because the prospects of local gain are not worth the risk of general warfare.” Despite the known risk effect of MMC, studies in this area have not explicated how multimarket firms are likely to shield against the potential “risk of general warfare” by adjusting their risk exposure. This neglect is surprising because the indispensability of risk management as part of a business strategy has been emphasized in the strategy literature (Palmer & Wiseman, 1999; Ruefli & Collins, 1999). As Miller (1998: 497) noted, “if we conceptualize strategy as the alignment of the firm with its external environment . . . then the measurement and management of [risk] exposures are central concerns for strategists.”

Second, although finance research has conceptually explored why risk management is necessary under rivalry (e.g., Froot, Scharfstein, & Stein, 1993), the literature contains very few empirical investigations of the topic. The few empirical studies that do exist reveal inconsistent findings. For example, studies have shown that competitive engagement can relate to risk exposure positively (Allayannis & Ihrig, 2001) or indirectly (Bartram, Brown, & Minton, 2010). The mixed findings can be attributed to the very nature of competition—a notion that has been considered multifaceted in organization theory (Chen, 1996; Gnyawali & Madhavan, 2001). Early work on the impact of competition on risk management typically relies on an aggregate approach by considering competition as a trait of the market that is the same for all firms in the industry (e.g., Adam, Dasgupta, & Titman, 2007; Adam & Nain, 2013). In these studies, competition is measured by the number of firms, the concentration ratio, or the Herfindahl index of an industry. The aggregate approach, however, as noted by Baum and Korn (1996: 256), “neglects variations in firms’ strategic interactions that depend on firm-specific competitive conditions.”

Our study aims to contribute to the two research fronts by developing and testing a theoretical model on how firm-specific competitive conditions in a multimarket context may affect corporate risk transfer. In doing so, our study also provides an opportunity to bridge the two intellectual camps, which have developed independently of each other. This investigation is also practically important given that the need for risk transfer is heightened in today's increasingly volatile market prompted by, for example, the COVID-19 pandemic, supply chain disruptions, economic downturns, emergence and diffusion of new technologies, and global political unrest.

Our study is different from previous work in two important ways. First, our interest in firm-specific competition in a multimarket context deviates from most studies on risk management, which focused mainly on single-market industries (where firms face a uniform environment) but fell short of explaining multipoint companies. Second, the present study departs from prior research in explicitly accounting for the effects of the multimarket and structural aspects of firm-specific competition. The multimarket aspect of firm-specific competition is grounded in the Austrian school of economics (Chen & Miller, 2015; Jacobson, 1992), which views competition as an ongoing process (Hayek, 1946/2016) during which “the participants are continually testing their competitors” (Kirzner, 1973: 12); it refers to competition as a consequence of the market contacts of a firm and its knowledge through past interactions. Rooted in the tradition of industrial organization economics (Bain, 1956; Porter, 1980), the structural aspect of firm-specific competition stresses the state or the situation of the objective environment; it refers to competitive pressure and opportunities (or lack of opportunities) as defined by the specific market structure facing a firm.

In our model, the multimarket aspect is captured by the pattern of firm-to-firm interactions, as reflected in the state of MMC (cf. Baum & Korn, 1996), while the structural aspect is captured by the inclusion of two market structural factors: contenders’ risk transfer level and egocentric industry concentration. Note that while our conceptualization of structural competition concurs with the aggregate tradition in assuming a uniform effect of market structure at the market or industry segment level, we adopt a refined approach by taking into account variations in firm business portfolios. That is, firms that diversify into different markets are situated in different industry segments and thus face diverse structural conditions when aggregated up to the firm level.

The contribution of our study is threefold. First, by distinguishing the two components of firm-specific competition, our study unveils much finer-grained effects of competition on risk transfer than what has been previously documented. To the best of our knowledge, our study is the first to investigate within a systematic framework the joint effects of MMC and structural competitive conditions on risk transfer level. Second, our study extends the literature on MMC by uncovering how MMC is related to risk exposure. Different from previous studies that primarily investigated the impact of MMC on the level of sales or profitability, we theorize and lend support to the idea that MMC also introduces risk because it influences the ability of firms to pass through business shocks to customers. Since expected return (e.g., average profitability) and risk (e.g., volatility of profitability) represent two distinct performance targets, our findings on the effect of MMC complement previous studies in shedding new light on the risk incentives of firm behavior in a multimarket context. Third, our theory advances the understanding of risk transfer behavior, an action widely undertaken in practice by firms for defense but one that remains underresearched in the competitive behavior literature. An investigation of this underexplored defensive action is likely to balance a predominant interest in the field in offensive actions and inform a more holistic view of competitive activity.

We test our hypotheses using data on 2,074 property and casualty (PC) insurance companies in the United States over a 25-year period. The US insurance industry is suitable for investigating risk transfer in a competitive environment for several reasons. First, the industry is characterized by intense competition and the frequent use of reinsurance—an insurance contract purchased by an insurer from another insurer or a group of insurers. Insurance is a widely adopted risk transfer method by corporations. Nevertheless, data on corporate demand for insurance in most industries are not readily available (Mayers & Smith, 1990). “Within the insurance industry, reinsurance purchases are like traditional insurance purchases by industrial corporations” (Mayers & Smith, 1990: 20). Due to extensive disclosure requirements, insurers in the United States systematically report their reinsurance purchases. Second, insurers commonly offer various products in a number of geographical locations and concurrently compete with the same rivals in multiple markets. Our data contain the breakdown of direct premiums written from all product lines in all states and territories of all US PC insurers, enabling us to investigate factors on the basis of geographic-business segments that influence the whole competitive landscape (see the Methods section for a detailed discussion). This geographic-business approach is practically meaningful because, for many companies like insurers, business lines and locations are not independent. For example, the demand (and hence competition) for a given insurance product (e.g., earthquake insurance) can be much higher in one region than another (e.g., California, which is earthquake prone and highly populated, vs. North Dakota). Therefore, our unique data enable us to capture MMC at a finer-grained level than what is usually reported.

Theory and Hypotheses

Risk Transfer as a Value-Creating Strategy

Risk transfer as a defensive vehicle has been routinely used by organizations in almost all industries. For example, at the end of 2009, Travelers entered into two reinsurance agreements each valued at $250 million, with Longpoint Re II Ltd., to transfer the risk of future catastrophic hurricane losses. In 2012, General Motors reduced its pension risk by offloading >$25 billion pension obligations for its retired white-collar workers to Prudential Financial through a group annuity contract.

Theoretical and empirical studies have suggested several motivations for risk transfer. First, as noted by Miller (1998), risk-averse organizational stakeholders such as managers are eager but unable to fully diversify their personal risk of firm-specific investments because they have a disproportionate share of their personal wealth linked to the performance of their company. In this regard, risk transfer can improve firm value because it lowers risk and thus reduces the additional compensation required by these stakeholders for their risk bearing. Second, external financing (debt and equity financing) is commonly known to be more costly than internal financing because of the imperfections of capital markets (Froot et al., 1993). Risk transfer can lower the frequency of internal cash flow shortfalls and thus reduce the need to raise funds from the outside, which curtails the expected financing costs of new projects. Third, risk transfer can mitigate agency problems, such as the underinvestment problem in which equity holders of a financially distressed firm tend to forgo positive net present value projects when the expected gain from a project mainly accrues to debt holders (Myers, 1977). Risk transfer allows firms to smooth income and reduce default probability. If a firm is less likely to fail, equity holders will be less likely to reject good investment opportunities because they can maintain all or the majority of the returns.

Research evidence supports the view of a positive impact of risk transfer on firm value as a defensive strategy. This body of research has not only investigated corporate risk transfer under various industries, such as electricity utilities (Aïd, Chemla, Porchet, & Touzi, 2011), oil and gas (Haushalter, 2000), insurers (Lin, Yu, & Peterson, 2015), and banks (Hankins, 2011), but also emphasized organizational characteristics such as financial leverage (He & Ng, 1998), firm size (Nance, Smith, & Smithson, 1993), ownership structure (Mayers & Smith, 1990), and growth options (Graham & Rogers, 2002) as key determinants of risk transfer level.

Rivalry constitutes another important determinant of risk transfer. Evidence shows that increased competition can reduce slack (Gil & Ruzzier, 2018), disturb firm performance (Andrevski & Ferrier, 2019), and increase the likelihood of organizational failure (Ingram & Inman, 1996). Under such conditions, firms have an incentive to protect their financial stability by acting defensively. Defensive actions refer to actions used by firms to protect themselves from threats that may result in adverse consequences. This type of action differs from attacks, which aim to disrupt competitors. Defensive actions play several roles as part of a firm's competitive arsenal. Besides their functions in stabilizing cash flow and enhancing firm resilience, these actions can be used in conjunction with other firm activities, such as investment, to gain an edge over competitors (a point on which we elaborate later).

Thus far, research on the effects of competition on risk transfer is limited, as existing studies have largely treated competition as a structural property of the overall market. For example, Adam et al. (2007) predict that the risk transfer choice of a firm will depend on the aggregate risk transfer decisions of all other firms in the industry, irrespective of whether they actually encounter one another competitively. However, given their particular domains of action, different firms may confront different sets of competitors in their own markets. Contacts between a firm and its competitors can shape the risk dynamics in corresponding markets but not necessarily in the whole industry (cf. Gimeno & Woo, 1999; Nomani, 1990). All else being equal, the distinct product market competition facing a firm is therefore likely to impose an impact on its risk transfer that differs from that facing another firm, even though they operate in the same industry.

Risk Transfer Level and MMC

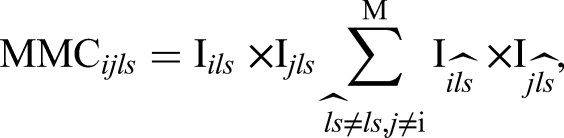

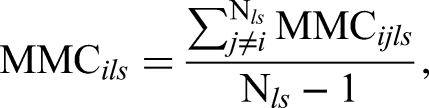

We focus on MMC to address the multimarket aspect of firm-specific competition. MMC gauges competition through the configuration of a firm's pairwise contacts with its competitors. Two firms have a contact or market overlap when they both operate in the same market. As the number of shared markets between the pair increases, the potential of tension also increases, which “stems from firms interacting and striving in the same environments and for the same resources” (Fuentelsaz, Gomez, & Polo, 2002: 250). An assault by one of the firms in the business domain of the other may thus trigger retaliation by the latter in the aggressor's territory. The move and countermove, premised on rational analysis, are not necessarily a one-to-one correspondence but can spill over across markets and spaces, oftentimes in a dynamic and reiterative fashion. In this regard, MMC is neither a structural nor a relational property of interfirm rivalry in that it accounts for the “history of prior interactions” (a departure from the structural aspect of rivalry) and the rationality of decision making (a departure from the relational aspect of rivalry) (Kilduff, 2019). The unique theoretical focuses of MMC also render it different from the social network analysis approach (Tsai, Su, & Chen, 2011). While like the latter in its emphasis on the information benefits stemming from a firm's competition network contacts, MMC considers the effects of footholds and mutual forbearance related to these contacts (Haveman & Nonnemaker, 2000)—two mechanisms that are beyond the focus of the social network analysis approach.

Research has established that MMC is a strong and significant predictor of the intensity of interfirm rivalry (Baum & Korn, 1996; Haveman & Nonnemaker, 2000). At low levels of MMC, a firm will often have an incomplete picture of its multipoint competitors because of limited opportunities for interaction. The lack of knowledge will blur orders of domination in the market and obscure norms between rivals. Without well-defined “rules of the game,” firms may actively explore unknown areas and launch aggressive actions. As MMC increases, the growing coinciding operations of a firm with its rivals will incentivize the firms to stake out their territories. Hence “uncalled for” defection and turf wars can occur frequently. Increased competition will further motivate firms to establish footholds in rivals’ markets to enhance their knowledge of competitor behavior and strengthen their retaliation or deterrence abilities.

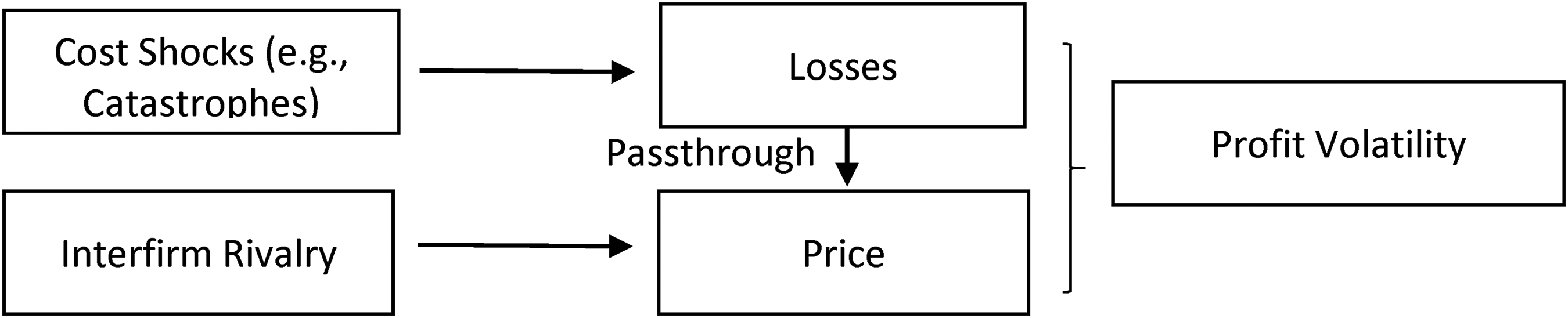

Rivalry among competitors in the same markets will increase pricing uncertainty and profit volatility due to the uncertain pass-through of a cost shock to price (Figure 1). Note that business risk and rivalry are both important to profit volatility, but neither alone is sufficient. If there is just rivalry and no cost shock, under conditions of general equilibrium, rivalry will determine the optimal price and expected return in the market: either high or low depending on the intensity of rivalry. There will not be much profit volatility unless the intensity of rivalry facing a firm may suddenly increase or decrease, which would be very unusual. If there are only cost shocks and no rivalry (e.g., in a monopoly market), then firms can simply change their prices to cover losses incurred by the shocks. In other words, losses can be passed through to customers without much impact on profit volatility. For our focal firms in the study (PC insurance companies), a major business risk that they face is the occurrence of an unanticipated catastrophe. If there is no rivalry (e.g., if only one firm operates in each niche market), insurers can simply adjust their prices to cover the losses caused by the catastrophe. As prices co-vary closely with cost shocks, profit volatility will be low. However, if firms concurrently encounter one another in several markets and face a cost shock, then intense competition between a firm and its rivals in multiple markets will result in an erosion of pricing power, which will become more serious as MMC increases. When this happens, price does not effectively correlate with the level of production, and the pass-through of a cost shock to product price is less likely and uncertain (Allayannis & Ihrig, 2001), leading to high profit volatility. As heightened MMC increases risk, firms are expected to react defensively by adjusting their level of risk transfer upward accordingly.

Causes of Profit Volatility

Although greater market overlap increases the likelihood of rivalries, after a certain inflection point, more market interactions do not necessarily result in more aggressive actions. The mutual forbearance hypothesis, grounded in MMC theory (Edwards, 1955; Greve, 2008; Haveman & Nonnemaker, 2000), maintains that the intensity of competition between multipoint rivals can be dampened if firms have mutual recognition of their interdependence. Beyond a certain threshold, multiple points of contact raise the possibility of collusion because this offers firms incentives to avoid the outbreak of an all-out war by taking forbearance actions. Extant theory suggests that familiarity and deterrence (Haveman & Nonnemaker, 2000) may help explain the outcome of mutual forbearance as a result of a high degree of MMC (Jayachandran, Gimeno, & Varadarajan, 1999). Familiarity is a gauge of the extent to which a firm is acquainted with the strategies, business scopes, and actions of rivals. Deterrence is a firm's ability to retaliate against rivals with credible threats to cause serious financial damage.

Overall, we predict an inverted U-shaped effect of MMC on risk transfer ratio. At low to moderate levels of MMC, firms will be more likely to benefit from risk transfer as an ex ante defense strategy because the competitive pressure that results from MMC within this range outweighs the role of multimarket interactions as a deterrent to aggressive actions. Risk transfer allows firms to smooth cost fluctuations, lower income volatility, and charge competitive prices. This function of risk transfer offers firms flexibility, making their output choice less subject to the impact of market shocks (Brown, 2001). When MMC reaches a high level, it provides additional opportunities for firms to observe and detect their rivals’ behavior. Furthermore, it generates additional channels for retaliation that form a credible threat to deter aggressive actions, facilitating mutual forbearance and leading to less rivalry. As firms refrain from aggressive competition, we expect that the risk transfer level will be low, due to lower competitive risk and a stronger ability to adjust prices to market shocks. Therefore, we predict the following: Hypothesis 1: MMC and risk transfer level are curvilinearly related such that the relationship is initially positive, but after reaching a maximum, a greater number of markets in which a firm meets with its rivals across all markets has a negative impact on the firm's risk transfer level.

Risk Transfer Level and Competitors’ Risk Transfer Decisions

Along with MMCs, the degree of competition that a firm faces is a function of the structural attributes of its market context, such as the level of risk aversion of rivals as a whole. Two contradicting views exist concerning how firms may act in response to competing firms (cf. Deephouse, 1999; Miller & Chen, 1996).

On one hand, behavioral and institutional scholars posit that firms have a tendency to mimic or converge toward their competitors for uncertainty reduction or legitimacy reasons (Cyert & March, 1963; DiMaggio & Powell, 1983). Conformity may arise in the insurance industry due to mimetic and coercive pressures in the market. For insurance firms, transferring out too much or too little risk is undesirable because excessive risk transfer will drive up cost (e.g., loading in the context of insurance purchase) and lower profitability, whereas inadequate reinsurance protection could jeopardize an insurer's financial stability. As the magnitude and frequency of catastrophes (e.g., pandemics, acts of God, or human-made disasters) are often difficult to predict, insurers may benefit from following the risk transfer practice of their peer firms, given that imitation may help enhance legitimacy and reduce information search costs for loss prediction (DiMaggio & Powell, 1983). The matched risk transfer level or benchmarking may also facilitate insurers’ regulatory compliance with, for example, capital requirements and help meet the expectations of auditors and other important stakeholders.

On the other hand, a structural view on competition suggests that “imitative behavior can be dysfunctional or even pathological” (Lieberman & Asaba, 2006: 367) because conformity will provoke similar competence development, resulting in heightened competition (Baum & Haveman, 1997; Porter, 1991; Wang & Shaver, 2014). A primary insight of the structural perspective is that the extent to which a firm can stay ahead of its rivals “rests mainly on how well it positions and differentiates itself in an industry” (Hoskisson, Hitt, Wan, & Yiu, 1999: 426). The conceptual model of Froot et al. (1993) on risk management strategy offers a view similar to the differentiation proposition.

A firm will possess a significant advantage if it has more cash flows than its rivals to invest in high-profit opportunities. If most firms do not control risk or transfer only a small portion of their positions, then the sensitivity of their cash flows and investment to a negative common shock will be high. Upon occurrence, a cost shock will drain aggregate cash flows, damp aggregate output, and raise the equilibrium price. Under this condition, a firm will have an incentive to use risk transfer as a means of defense because it helps reduce production costs (Adam et al., 2007). Furthermore, risk transfer allows a firm to retain additional capital and invest more in those states in which its rivals have limited capabilities to capture high-profit opportunities.

By contrast, if the industry risk-shedding level is high or most firms transfer much of their risk exposure, then the equilibrium price will be low. Such an effect is due to the high ensuing aggregate cash flows and aggregate output level. Under this circumstance, as the industry as a whole is not highly sensitive to a cost shock, a firm will gain more from speculating than risk transfer. The model of Adam et al. (2007) illustrates that retaining risk allows a firm to enjoy real option benefits of production flexibility that can provide a gain greater than the loss of cost reduction from risk transfer. Specifically, when a cost shock occurs, a noncedant can reduce its production volume to adjust to the already-low price of a commodity. In the absence of a cost shock, a noncedant retains additional funds for investment and can thus secure a higher market share than its risk-ceding competitors. The interplay between firms’ risk transfer choices suggests that a firm has the incentive to initiate a risk transfer action opposite to the decision of its rivals.

While there is reason to believe that the differentiation effect should outdo the conformity effect in our context for risk transfer, we propose two competing hypotheses because how a firm will transfer risk vis-à-vis its competitors is ultimately an empirical question. Hypothesis 2a: The risk transfer level of a firm is negatively correlated with its competitors’ risk transfer level.

Hypothesis 2b: The risk transfer level of a firm is positively correlated with its competitors’ risk transfer level.

Risk Transfer Level and Egocentric Industry Concentration

Industry concentration refers to the extent to which industry market shares are concentrated among a small set of large firms. Although this structural characteristic is not particularly useful in predicting how likely firms will be to respond to their specific rivals (Chen, 1996), it is certainly useful in explaining firm behavior, such as their corporate risk decisions, in response to competitive pressure of the overall industry (Bain, 1956; Turner, Mitchell, & Bettis, 2010).

In this study, we are interested in egocentric or firm-specific industry concentration (hereafter, industry concentration), which is defined as the concentration of the industry segments in which a focal firm has operations. Industrial organization economics (Caves, 1972) suggests that concentration may suppress competition for a couple of reasons. First, shifts in market dynamics caused by increasing concentration bestow power on dominant firms, thereby lowering the risk of affronts and provocations by others (Dobrev, Kim, & Carroll, 2002). Second, in a highly concentrated industry, the stakes of firms at risk incentivize them to coordinate and refrain from directly competing with their rivals (Turner et al., 2010). High concentration also minimizes the cost of monitoring and signaling, which makes collusion more likely (Basdeo, Smith, Grimm, Rindova, & Derfus, 2006). When an industry is less competitive, transferring risk is less needed for defending against external threats, as reduced competition gives a firm more pricing power to adjust its output so that a cost shock can be incorporated into its product price more easily. As prices and costs co-vary more closely, a firm is subject to lower profit volatility. In line with this argument, Allayannis and Weston (1999) note that in less competitive industries, ceteris paribus, firms are less likely to hedge with foreign currency derivatives. Our study differs from Allayannis and Weston in that we focus on the intensity of structural competition attributable to firm-specific industry concentration, whereas Allayannis and Weston use industry-level price-cost margin to proxy for the overall market competitiveness. Moreover, we do not assume a uniform industry market structure, bearing in mind the diversity of firm-specific competition in a multimarket environment. Specifically, we propose the following hypothesis: Hypothesis 3: The risk transfer level of a firm is negatively correlated with its firm-specific industry concentration.

Moderating Role of Industry Concentration

Industry concentration and MMC may interact to influence the use of risk transfer as a form of corporate defense. The influence of MMC on risk transfer, as explained earlier, is made through its effects on cost pass-through via rivalry and mutual forbearance, both of which may change as industry concentration increases. When MMC is low to medium, increased rivalry is the major concern for risk transfer decisions. Over this range of MMC, if concentration is low, then even leading market players hold only small shares of the industry. The lack of domination will add incentives to firms with low MMC to behave aggressively in hopes of gaining larger market shares and profitability. As concentration increases, dominant firms will emerge, and they will fence off territories of control and wield power to decrease competition. The solidification of market structure will curb the competitive aggressiveness of firms with low MMC, which will make cost pass-through easier to achieve. Together, these arguments suggest that, at low to medium levels of MMC, industry concentration will negatively moderate the positive relationship between MMC and risk transfer ratio.

When MMC is medium to high, mutual forbearance starts to determine risk transfer decisions. Over this range of MMC, if industry concentration is high, then firms possess strong abilities to deter rivals owing to their high stakes in the market (Areeda & Turner, 1979). A more concentrated industry thus increases the credibility of retaliation expectations, which deters excessively aggressive behavior. As concentration decreases, collusion (and consequently cost pass-through) becomes harder because coordination of activities across markets is easier for a few oligopolists than for many firms (Bernheim & Whinston, 1990). These arguments suggest that at medium to high levels of MMC, high industry concentration will magnify the negative relationship between MMC and risk transfer ratio. Therefore, we hypothesize the following: Hypothesis 4: Firm-specific industry concentration moderates the inverted U–shaped relationship between MMC and risk transfer such that (a) an increase in industry concentration will alleviate the positive effect of MMC on risk transfer at low to moderate levels of MMC and (b) an increase in industry concentration will aggravate the negative effect of MMC on risk transfer at moderate to high levels of MMC.

Methods

Sample

We tested our hypotheses using the National Association of Insurance Commissioners (NAIC) data on PC insurance groups under common ownership and single unaffiliated insurers in the United States from 1995 to 2019. The NAIC, formed in 1871, is a voluntary association of the chief insurance regulators of all states in the United States, the District of Columbia, and five US territories (American Samoa, Guam, Northern Mariana Islands, Puerto Rico, and the Virgin Islands). It mandates all active public and private insurance firms and their affiliates conducting business in the United States to file annual statutory financial statements prepared in conformity with statutory accounting principles. We aggregated the NAIC data on affiliated firms at the group level “because insurers formulate investment and risk management strategies at the overall corporate level” (Cummins, Dionne, Gagne, & Nouira, 2009: 148).

The data set compiled by the NAIC provides detailed information that allows us to construct measures on organizational characteristics, such as firm size, leverage, and performance, as well as firm-specific competitive factors that can influence an insurer's reinsurance purchase decisions. Our data set is unique in the sense that the Exhibit of Premiums and Losses (Statutory Page 14) of the database contains extensive and detailed information on the breakdown of direct premiums written (transaction values) from L = 28 product lines in the S = 58 geographical areas for all insurers in each year, which is unavailable for many other industries. In total, there are 1,624 ( S × L = 58 geographical areas × 28 business lines) niche markets (geographic-business segments) in the US PC insurance industry according to our data.

For the purpose of this study, we focused on the risk transfer of primary insurers via reinsurance purchase and investigated how their market overlap with other insurers affected the level of their reinsurance usage. We followed A.M. Best in defining a primary insurer as one whose reinsurance assumed from nonaffiliates is <75% of the direct premium written plus reinsurance assumed from affiliates (Cole, Lee, & McCullough, 2007). We excluded from our sample observations that (1) have missing data or (2) report either negative reinsurance or negative or zero surplus, assets, premiums, losses, or expenses. The resulting sample is an unbalanced panel of 23,643 observations (2,074 distinct insurers) for 25 years. Our sample accounts for 95.4% of total industry premium volume from 1995 to 2019.

Dependent Variable

Reinsurance is a commonly used risk transfer method by insurers to transfer catastrophic risk and stabilize profits. We used the level of reinsurance usage to measure reinsurance demand, which is calculated as the percentage of premiums ceded to reinsurers over the sum of the direct premium written and the reinsurance premium assumed (Cole & McCullough, 2006). As a common practice, many primary insurers are both insurers and reinsurers of others. This widely used measure properly represents the proportion of loss exposures that a primary insurer passes to another insurer, a reinsurer, or a group of reinsurers. When this ratio is 0, the primary insurer transfers none of its underwriting risk and does not purchase any reinsurance. When this ratio is 1, the primary insurer transfers 100% of potential losses associated with its business and entirely removes its risk exposure. This circumstance may happen when an insurer completely withdraws from the insurance market. In most cases, the reinsurance ratio is between 0 and 1.

Independent Variables

Multimarket contact. We employed a count measure, the most common measure of MMC, which adds the number of markets in which a focal firm meets its rivals (Fuentelsaz & Gómez, 2006; Gimeno & Woo, 1996). A count measure of MMC indicates the number of markets in which firms engage with one another and the degree to which they overlap. Let the indicator I

ils

= 1 if insurer i is competing in market (l,s) with a positive direct premium written and 0 otherwise, where l represents product line l and s denotes state s. Similarly, if insurer j is competing in market (l,s), I

jls

= 1 and 0 otherwise. Insurers i and j have a contact (shared market) in market (l,s) if both have positive premiums (sales) in line l (l = 1, 2, . . . , L) and state s (s = 1, 2, . . . , S). In this case,

Level of reinsurance usage of competitors. Competitors’ reinsurance usage was calculated as the average reinsurance ratio of competitors. Although most PC insurers in the United States encounter one another simultaneously in multiple markets, they also meet with a small number of single-point competitors. Therefore, to study how the reinsurance levels of different competitors may shape a focal firm's reinsurance purchase, we calculated the average reinsurance ratios of multimarket and single-market competitors of a focal insurer.

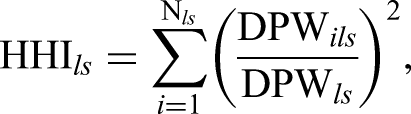

Egocentric industry concentration. To account for a focal insurer's geographic-business market space, we adopted a market space–weighted Herfindahl index widely used in the insurance literature to capture firm-specific structural competition (Berry-Stölzle, Liebenberg, Ruhland, & Sommer, 2012; Liebenberg & Sommer, 2008). Based on the data reported for each business line within each state in the exhibit of premiums and losses (statutory page 14), this market space–weighted concentration faced by insurer i was calculated as follows:

Control Variables

We included a number of control variables at the market and firm levels that may influence an insurer's reinsurance usage. Given that reinsurance allows an insurer to increase underwriting capacity and capture more business opportunities when market opportunities are abundant, we expect insurers to transfer more risk in highly munificent environments. To control for this effect, we used market munificence as a measure of opportunities and options available to firms, following Dess and Beard (1984) and Xia, Yu, and Lin (2019).

We included firm size to control for the potential effect of structural inertia (Hannan & Freeman, 1984) and proxy for an insurer's market size. The correlation of firm size and market size measured by total premium written was as high as 0.89. Firm size was measured by the natural logarithm of the book value of total assets. Reducing cash flow volatility via insurance purchase can mitigate bankruptcy costs and lower a firm's expected tax payments (Nance et al., 1993). Following Lin, Wen, and Yu (2012), to control for the effect of cash flow volatility on an insurer's decision to purchase reinsurance, we calculated an insurer's overall volatility.

A long-term contracting relationship with the same reinsurers reduces information problems and deters opportunism, leading to a low reinsurance cost. Accordingly, we expect a positive correlation between the level of reinsurance usage and the duration of contract relationship. To control for the impact of contract sustainability on reinsurance purchase, following Garven, Hilliard, and Grace (2014), we calculated a reinsurance sustainability index for each insurer at time t, defined as the proportion of premiums ceded over a 3-year period in the (t − 3, t) window to reinsurance providers that are present in all 3 years.

We also controlled the other firm characteristics with the following variables: (1) performance of the firm approximated with return on assets; (2) leverage measured as the ratio of total liabilities over total assets on the balance sheet; and (3) dummy variables to indicate whether a firm is a stock, mutual, or unaffiliated company.

Analysis Model

The reinsurance level in our sample is a fraction, which is always nonnegative and bounded within the unit interval. Since linear regression analysis is not suitable for bounded dependent variables, we chose to use the following fractional logit model (Papke & Wooldridge, 1996):

Results

Estimation Results

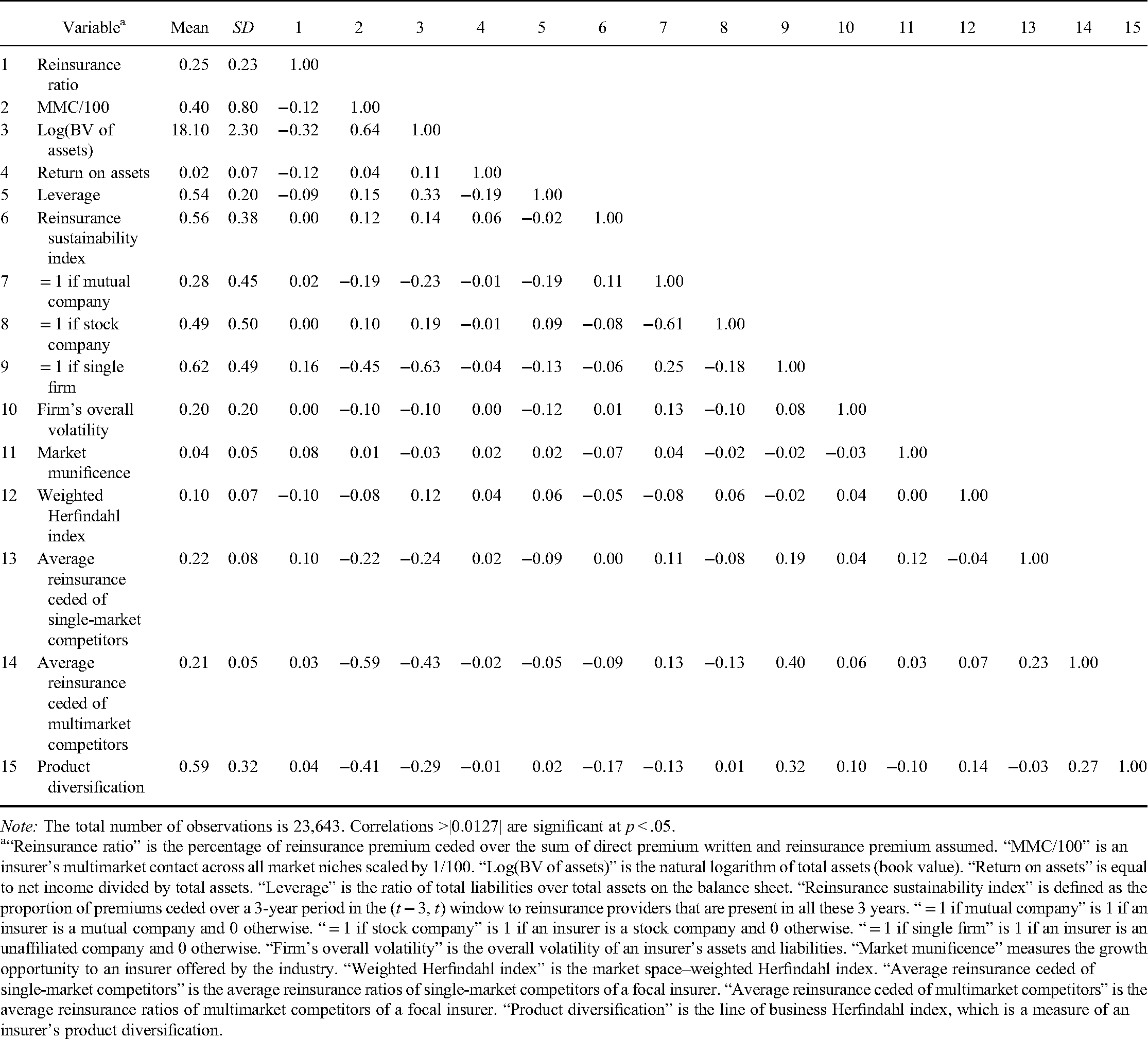

Table 1 presents the descriptive statistics and bivariate correlations matrix for all the study variables. The average level of reinsurance usage is 0.25. That is, a primary insurer, on average, transfers 25% of its total premiums written and assumed from nonaffiliates to its reinsurers.

Descriptive Statistics

Note: The total number of observations is 23,643. Correlations >|0.0127| are significant at p < .05.

“Reinsurance ratio” is the percentage of reinsurance premium ceded over the sum of direct premium written and reinsurance premium assumed. “MMC/100” is an insurer's multimarket contact across all market niches scaled by 1/100. “Log(BV of assets)” is the natural logarithm of total assets (book value). “Return on assets” is equal to net income divided by total assets. “Leverage” is the ratio of total liabilities over total assets on the balance sheet. “Reinsurance sustainability index” is defined as the proportion of premiums ceded over a 3-year period in the (t − 3, t) window to reinsurance providers that are present in all these 3 years. “ = 1 if mutual company” is 1 if an insurer is a mutual company and 0 otherwise. “ = 1 if stock company” is 1 if an insurer is a stock company and 0 otherwise. “ = 1 if single firm” is 1 if an insurer is an unaffiliated company and 0 otherwise. “Firm's overall volatility” is the overall volatility of an insurer's assets and liabilities. “Market munificence” measures the growth opportunity to an insurer offered by the industry. “Weighted Herfindahl index” is the market space–weighted Herfindahl index. “Average reinsurance ceded of single-market competitors” is the average reinsurance ratios of single-market competitors of a focal insurer. “Average reinsurance ceded of multimarket competitors” is the average reinsurance ratios of multimarket competitors of a focal insurer. “Product diversification” is the line of business Herfindahl index, which is a measure of an insurer's product diversification.

To reduce multicollinearity caused by the linear terms of variables and their high-order terms (squared term and the linear and quadratic interactions used to test our hypotheses), we mean centered all relevant variables prior to the formation of the quadratic and interaction terms (Cohen, Cohen, West, & Aiken, 2003). We also checked the variance inflation factors for all regressions. All variance inflation factors are below the recommended cutoff of 10. Therefore, multicollinearity should not be a major issue to our data.

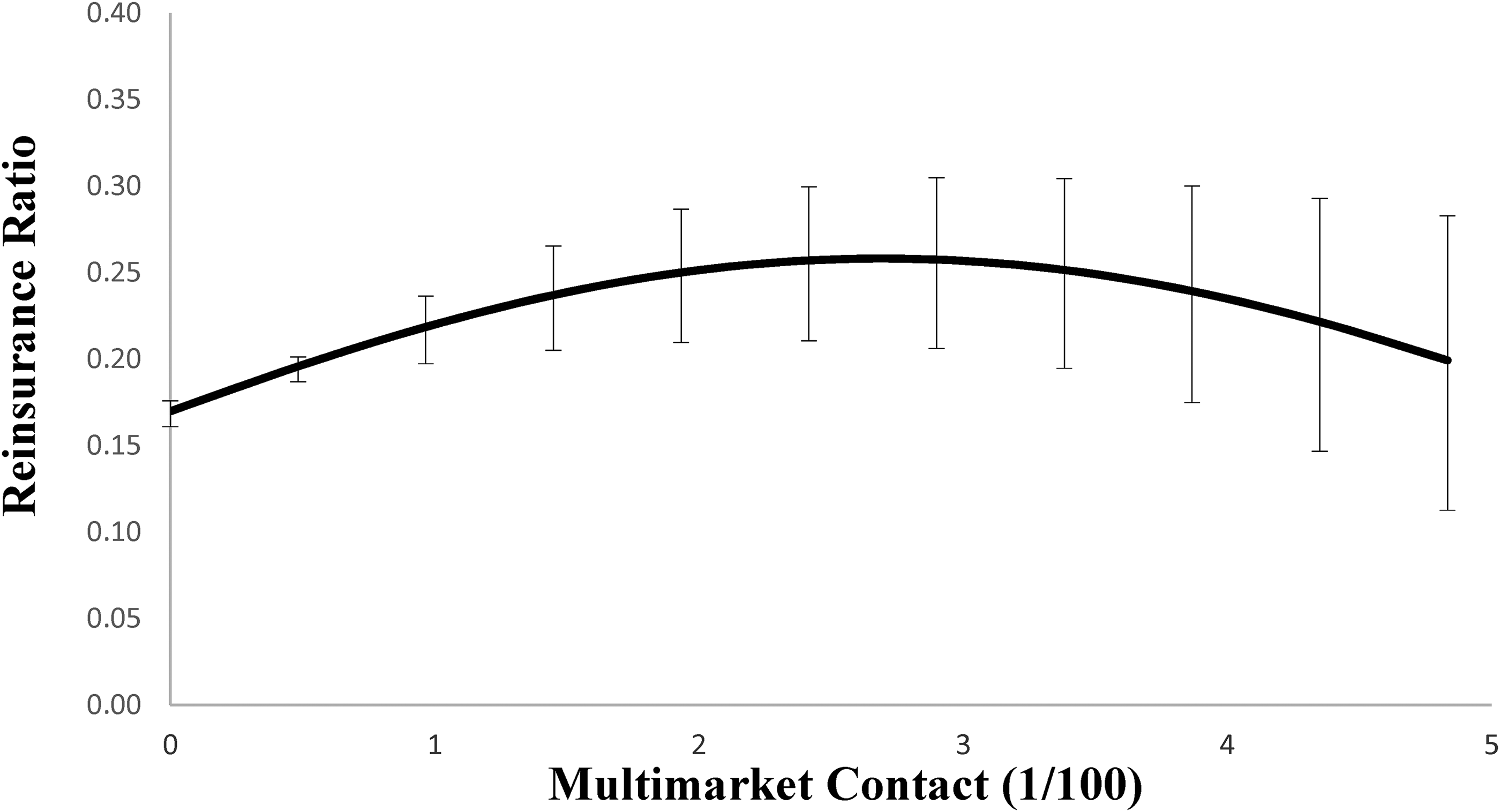

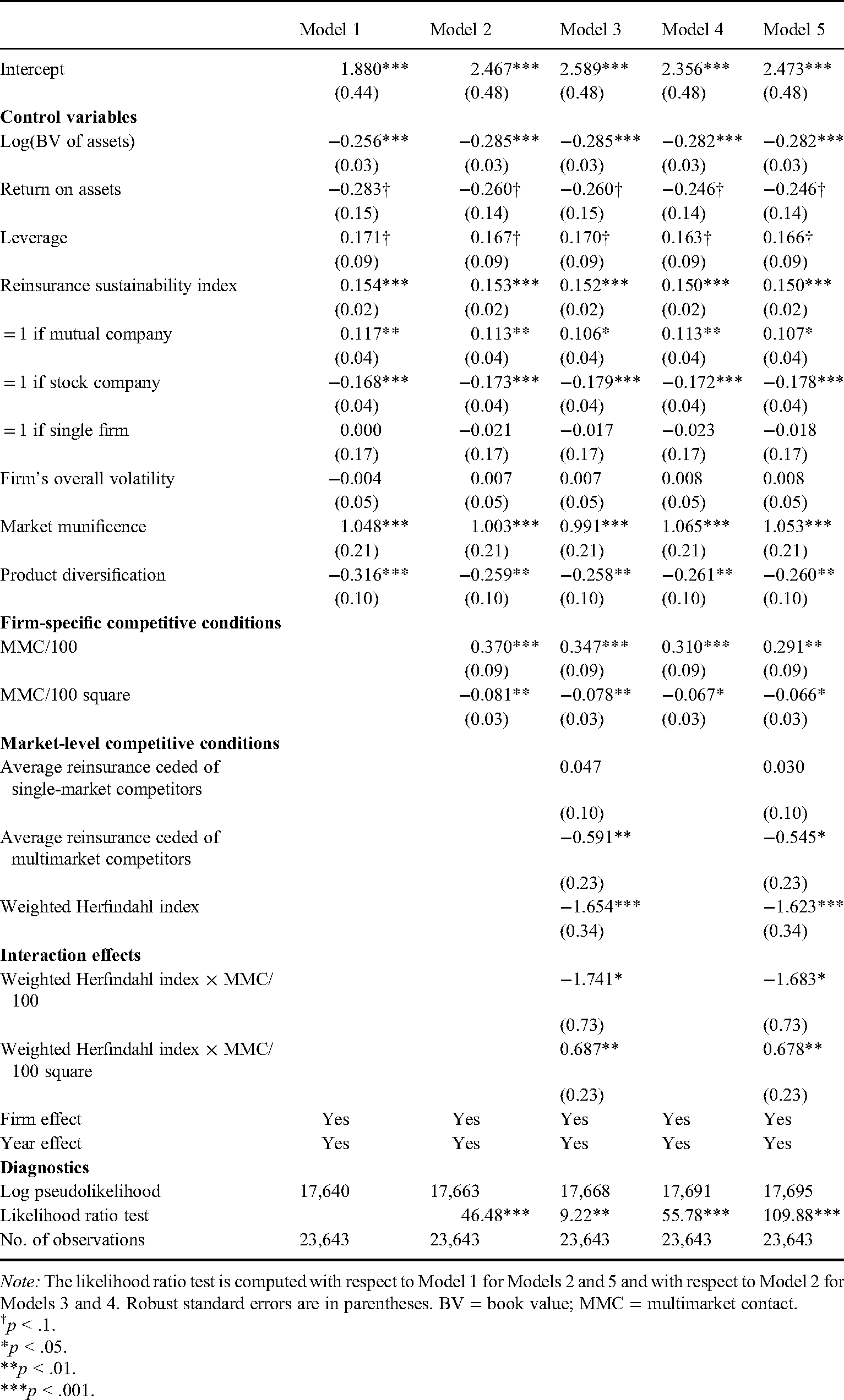

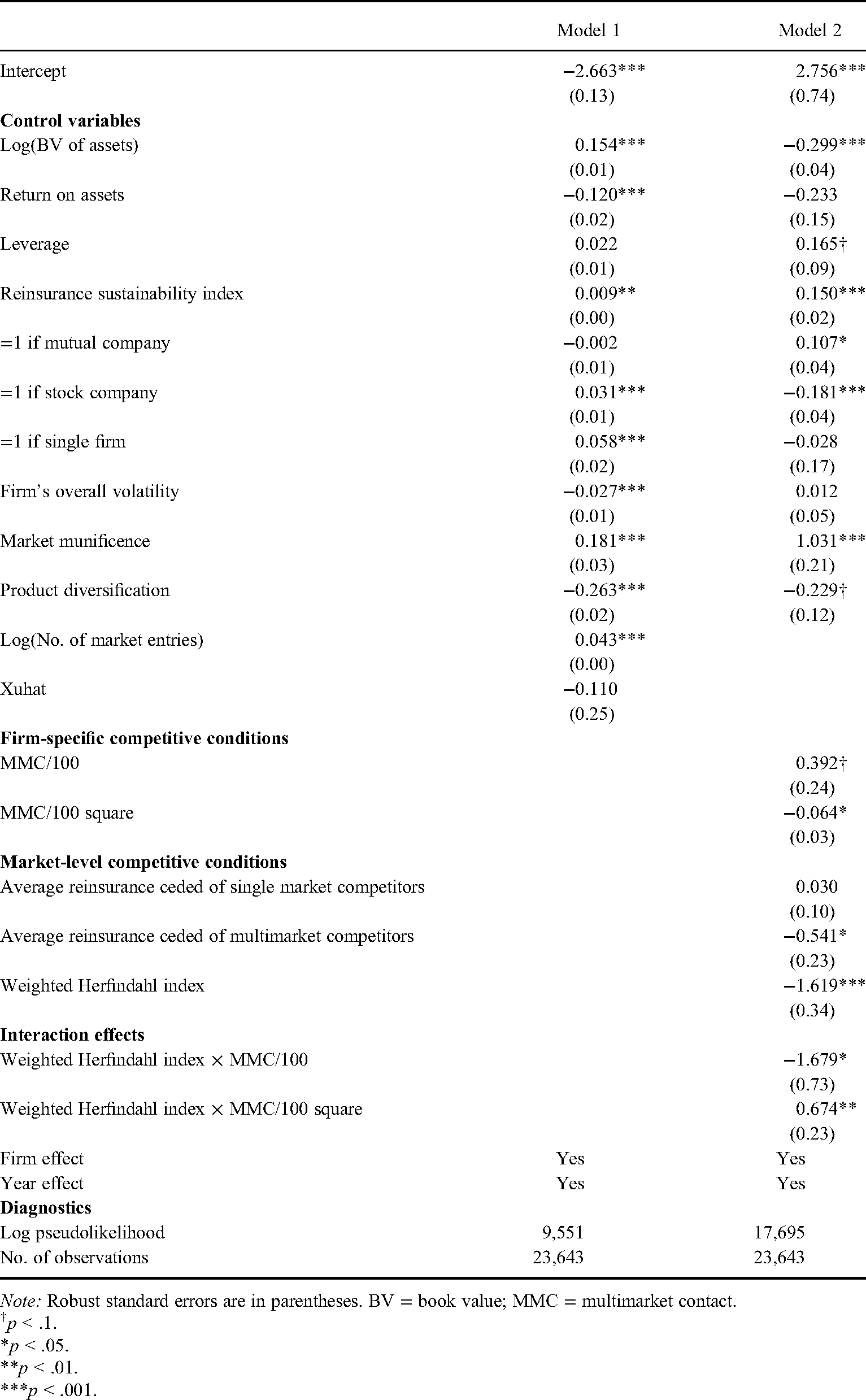

In Hypothesis 1, we predicted that the relationship between MMC and risk transfer is nonlinear. In line with the hypothesis, in Model 5 of Table 2, we find that the coefficient of the linear term for MMC is positive and significant (b = 0.291, p < .01) and the quadratic term is negative and significant (b = −0.066, p < .05). To correctly interpret our results, we followed Haans, Pieters, and He (2016) and Lind and Mehlum (2010) to find out the turning point at which the effect of MMC changes from positive to negative. The turning point occurs at MMC/100 = 2.61, which is well within the range of variation of MMC/100 in our data [0, 4.834], as supported by a 95% confidence interval using Fieller's (1954) method. Figure 2 depicts the quadratic relationship. Given the nonlinearity of the fractional logit model, the marginal effect of an explanatory variable in such a model is nonconstant over the value of the explanatory variable but conditional on the values of all other variables. Therefore, similar to prior studies (e.g., Wadhwa, Freitas, & Sarkar, 2017), we calculated the marginal effect of MMC at several values (from Model 5) with all other variables held at their sample means. When MMC/100 is at 0, 1, 2, 3, and 4, the marginal effect of a 0.1-unit increase in MMC/100 results in changes of 2.82%, 1.62%, 0.56%, –0.44%, and –1.47 (0.49, 0.35, 0.13, −0.11, and −0.33 percentage points) in reinsurance ratio, respectively. Together, these results lend good support to Hypothesis 1, suggesting that at low levels of MMC, increasing MMC increases reinsurance usage due to high competitive pressure, whereas as MMC reaches high levels, insurers practice mutual forbearance to avoid competition and thus purchase less reinsurance. The implied economic impact of these estimates is also substantial. Keeping all other variables at their means, an insurer's reinsurance ratio increases from 17.25% to 24.61% when the MMC level increases from 0 to the inflection point at 2.610. However, when the MMC level increases from the inflection point to the maximum level of MMC at 4.834, the reinsurance ratio decreases from 24.61% to 19.05%.

Effect of Multimarket Contact on Reinsurance Ratio

Results of the Fractional Logit Model Regression Analyses for the Level of Reinsurance Usage

Note: The likelihood ratio test is computed with respect to Model 1 for Models 2 and 5 and with respect to Model 2 for Models 3 and 4. Robust standard errors are in parentheses. BV = book value; MMC = multimarket contact.

p < .1.

*p < .05.

**p < .01.

***p < .001.

Hypotheses 2a and 2b offer competing predictions on the effect of rivals’ risk transfer on a firm's risk transfer level. The coefficient for the average reinsurance ceded of single-point competitors is positive but nonsignificant, and the coefficient for the average reinsurance ceded of multimarket competitors is negative and significant (b = −0.545, p < .05) in Model 5 of Table 2. This finding is consistent with the view that “potential competition (possible harm from aggressive competitive action by rivals) is greater among rivals who meet in multiple domains than among rivals who meet in a single domain” (Haveman & Nonnemaker, 2000: 233). Like before, we also computed the marginal effects of multimarket competitors’ risk transfer at several values. Holding values of all other variables at their mean levels, when the average reinsurance ratio of multimarket competitors is at the levels of 0, 0.16, 0.32, 0.48, and 0.64, a 1–percentage point increase in multimarket competitors’ reinsurance ratio will notably reduce the focal insurer's reinsurance ratio by 0.44%, 0.45%, 0.45%, 0.46%, and 0.47% (0.08, 0.08, 0.08, 0.07, 0.07 percentage points), respectively. The result reveals that an insurer will purchase more reinsurance if its multimarket competitors have a lower level of reinsurance usage. When the industry reinsurance purchase is low, transferring more catastrophic risk allows an insurer to capture high profit opportunities in those states where a cost shock depletes aggregate cash flows of most insurers in the industry. With regard to economic significance and by keeping all other variables at their means, our findings show that moving from one standard deviation below the mean on our multimarket competitors’ reinsurance ratio measure to one standard deviation above decreases an insurer's reinsurance ratio from 19.58% to 18.73%. Thus, our findings support Hypothesis 2a.

We included a weighted Herfindahl index in our regressions to explore the influences of egocentric industry concentration over reinsurance decision. In Model 5 of Table 2, industry concentration relates negatively to reinsurance demand (b = −1.623, p < .001), which supports Hypothesis 3. Holding all other variables at their mean levels, we computed the marginal effects of industry concentration at some different values. When industry concentration is set at 0.30, 0.42, 0.54, 0.66, and 0.78, a 0.01-unit increase in industry concentration will lead to decreases of 1.38%, 1.41%, 1.45%, 1.47%, and 1.49% (0.20, 0.17, 0.15, 0.13, and 0.11 percentage points) in the focal insurer's reinsurance ratio, respectively. This pattern of results suggests that an insurer facing a concentrated industry has low reinsurance usage because it has more pricing power to adjust its price in response to a cost shock, leading to a low profit volatility and reinsurance need. The result is also economically significant. By keeping all other variables at their means, our findings show that moving from one standard deviation below the mean on our egocentric industry concentration measure to one standard deviation above decreases an insurer's reinsurance ratio from 21.06% to 17.38%.

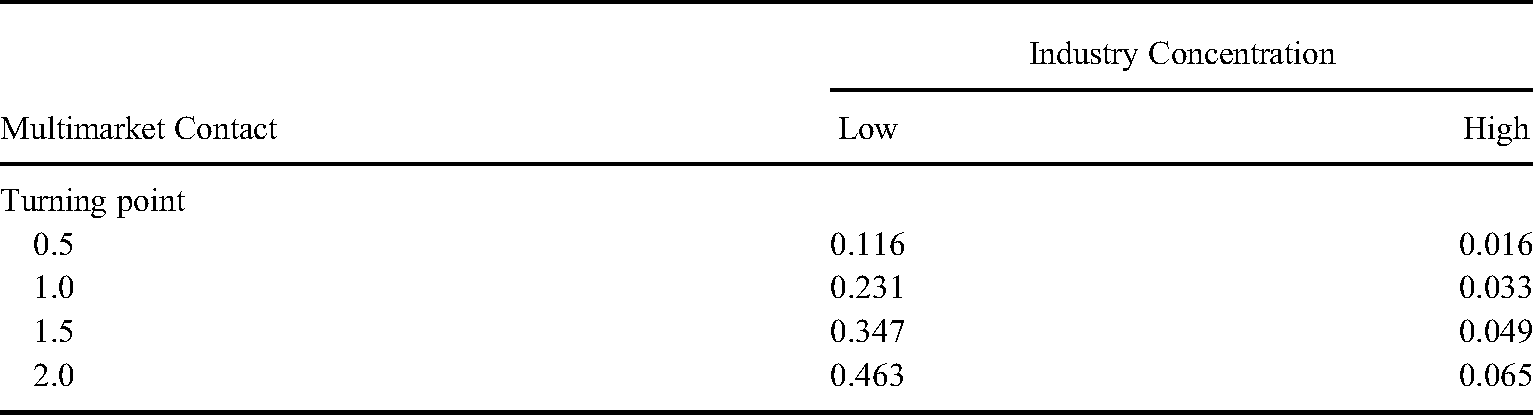

In addition to the main effect, Hypothesis 4 predicts that industry concentration will moderate the relationship between MMC and reinsurance usage. Results show that the coefficient of the interaction between MMC and industry concentration is negative and significant (b = −1.683, p < .05). The coefficient of the interaction between MMC squared and industry concentration is also significant (b = 0.678, p < .01) in Model 5 of Table 2, but the sign is opposite to what Hypothesis 4 predicts. We also conducted a spline regression analysis with the knot being set equal to the inflection point ( = 2.610). The results of the analysis show a consistent pattern of interactions. The nonlinear response function of the fractional logit model complicates the interpretation of the coefficients for the interaction terms because, unlike linear models, we cannot directly infer an enhancing or dampening moderating effect from these coefficients. Following Haans et al. (2016), we separated industry concentration into different levels—low (mean – 1 standard deviation) and high (mean + 1 standard deviation)—and calculated the turning points of the curves at these two levels. As the turning point for the second curve (the one for a high level of industry concentration) is beyond our data range, we computed only the slopes of both the curves at multiple points that are equally distant to the left of each turning point. As shown in Table 3, when industry concentration is high, the slopes of the curve are 0.016, 0.033, 0.049, and 0.065 as MMC/100 decreases by 0.5, 1.0, 1.5, and 2.0 units to the left of the turning point, respectively. When industry concentration is low, the slopes of the points on the curve at the same distance to the left of its turning point are 0.116, 0.231, 0.347, and 0.463. The slopes are thus shallower at the high level of industry concentration when we compare equidistant points from the left of the turning points of both curves. Therefore, industry concentration negatively moderates the positive effect of MMC on reinsurance ratio before the inflection point is reached.

Analysis of Slopes

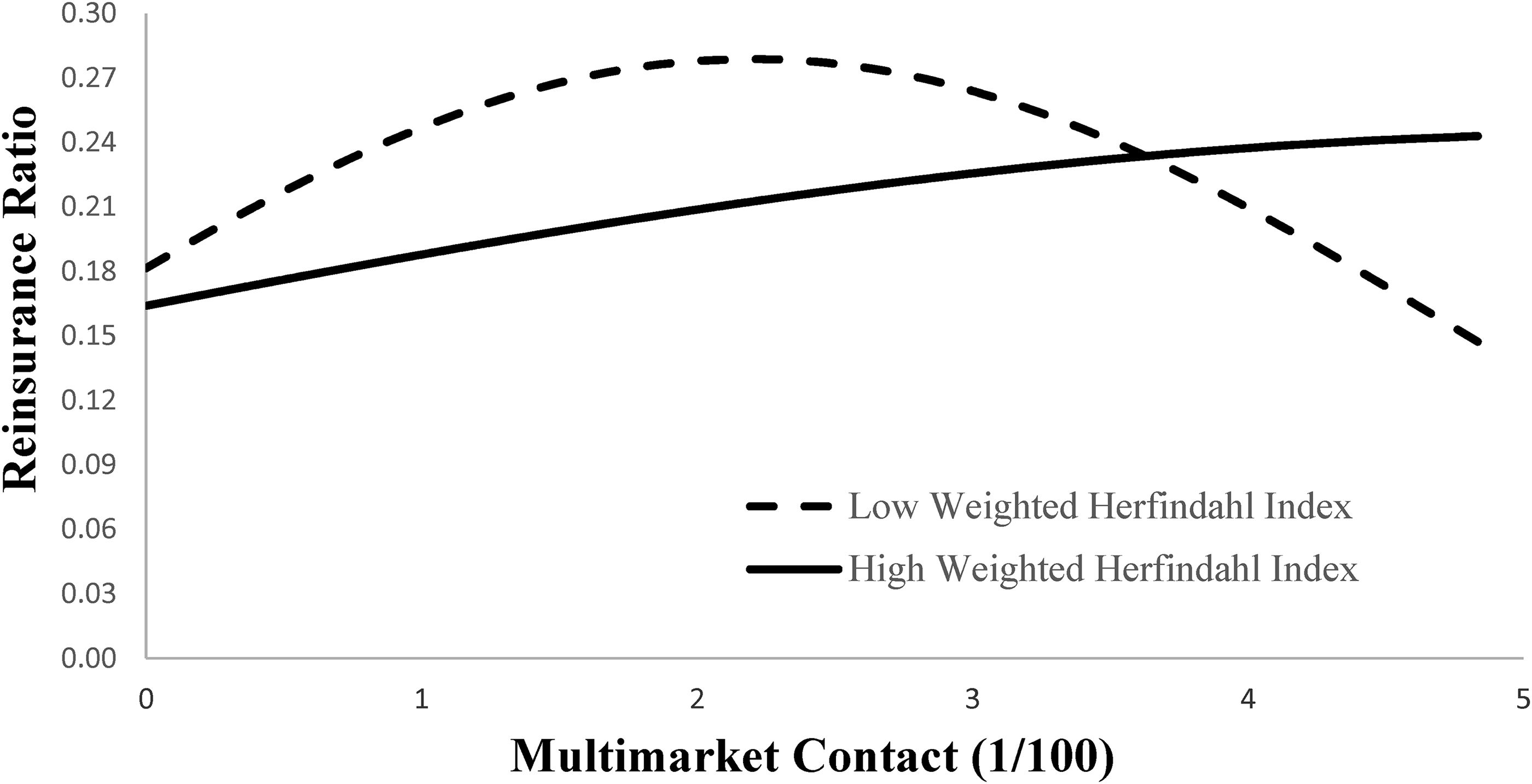

We followed procedures used by Wadhwa et al. (2017) to calculate the differences of marginal effects of a 0.1-unit increase in MMC/100 on reinsurance ratio at low and high levels of industry concentration for a given set of values of MMC. In comparison with that of firms facing low industry concentration, the reinsurance ratio of firms that face high industry concentration is lower by 2.61% and 0.81% (0.50 and 0.27 percentage points) when MMC/100 is 0 and 1 and is higher by 0.66%, 2.08%, and 3.72% (0.12, 0.52, and 0.79 percentage points) when MMC/100 is at 2, 3, and 4, respectively. Figure 3 illustrates the results of the interaction effects based on the parameter values generated by Model 5 of Table 2. The figure shows that at low levels of egocentric industry concentration (mean – 1 standard deviation), an insurer's reinsurance ratio increases from 18.14% to 24.69% (24.69% to 27.79%) when the MMC level increases from 0 to 1 (1 to 2). When the MMC level increases from 2 to 3 (3 to 4), the reinsurance ratio decreases from 27.79% to 26.39% (26.39% to 20.95%). At high levels of egocentric industry concentration (mean + 1 standard deviation), an insurer's reinsurance ratio increases from 16.40% to 18.78% (18.78% to 20.87%) when the MMC level increases from 0 to 1 (1 to 2). When the MMC level increases from 2 to 3 (3 to 4), the reinsurance ratio continues to increase from 20.87% to 22.56% (22.56% to 23.74%).

Interaction between Weighted Herfindahl Index and Multimarket Contact

As previously mentioned, MMC has two effects: (1) enlarged scope of competition, which increases reinsurance demand, and (2) mutual forbearance, which reduces the need for reinsurance. Figure 3 shows that the relative power of the two effects varies across markets with different levels of concentration. When concentration is low, both effects appear to exist, and mutual forbearance becomes more salient at high levels of MMC, resulting in an inverted U–shaped relationship between MMC and reinsurance level, supporting Hypothesis 1. The figure also shows that when industry concentration is high, a firm actually transfers more risk at very high levels of MMC than at low levels. This result indicates that when industry concentration and MMC are both high, risk exposure actually increases. This finding is consistent with the results of Froot et al. (1993), who argue that the risk exposure of a firm depends on the interdependence of its investment opportunities with product market rivals, which “is highest in oligopolies where a limited number of evenly balanced competitors confront each other” (Burgers, Hill, & Kim, 1993: 421). Kovenock and Phillips (1997) and Zingales (1998) show that the risk that underinvestment leads to a loss of investment opportunities and market share to product market rivals is higher in more concentrated industries, where greater interdependence exists in investment decisions. A high level of MMC may deepen this interdependence in a concentrated market. That is, a firm may have more similar operations and greater overlaps of investment opportunities with rivals because of their interactions in multiple battlefields, which amplify a firm's risk exposure (Haushalter, Klasa, & Maxwell, 2007). As a result, an insurer with a high level of MMC will purchase more reinsurance than another with a low level of MMC when industry concentration is high.

Robustness Checks

Endogeneity concern. Endogeneity is a potential issue in our study because a firm's MMC is not random and likely correlated with the disturbance term. Handling endogeneity is “a balancing act” between negligence and overtreatment (sometimes faulty treatment). Indeed, if the endogeneity problem under scrutiny is inappropriately treated, efforts to tackle the problem may create more problems than they solve (Semadeni, Withers, & Certo, 2014). Hence, it is important to diagnose the presence and exact sources of endogeneity, as this effort helps gauge potential bias and facilitates the choice of the proper remedy (Hill, Johnson, Greco, O’Boyle, & Walter, 2021).

In our study, endogeneity may arise from three potential sources. First, a correlated omitted variable may bias our results. To test how strong the impact of the omitted variable would need to be to change the inference about the effects of MMC, we analyzed the robustness of inference to replacement (Frank, Mroulis, Duong, & Kelcey, 2013; Frank et al., 2021) by using the konfound command in Stata. The results show that 46.70% of the estimate would have to be due to bias to invalidate the inference for MMC and that 29.65% of the estimate would have to be due to bias to invalidate the inference that there is a quadratic effect of MMC. In other words, 46.70% (n = 11,041) of cases would need to be replaced with cases for which there is an effect of 0 to invalidate the inference for MMC (29.65% [n = 7,010] for the quadratic term of MMC). Given that our sample includes almost all firms in the US PC insurance industry market (except for a few firms with missing values or problematic data), replacing 46.70% (n = 11,041) of the current cases to invalidate the inference for the linear term of MMC and replacing 29.65% (n = 7,010) of the current cases to invalidate the inference for the quadratic term of MMC is very unlikely, if not impossible. Hence, omitted variable should not be a big concern in our study.

A second endogeneity concern in our research context is simultaneity. That is, while insurers may modify risk transfer in response to competition, the act of risk transfer may reversely affect the state of rivalry. Indeed, an insurer may directly transfer risk to its competitors even though, as our data show, this occurs to only a small fraction of insurers’ market contacts. The consequent coopetition relationships may influence the firm's motivation to use aggressive actions against its competitors. To mitigate this problem, we used a lagged MMC in all regressions. To further isolate the confounding effect of coopetition, we carried out two additional analyses: (1) We ran regressions by adding two additional control variables for the percentage of risk transferred to competitors and the percentage of risk assumed from competitors, and (2) we constructed a new MMC variable by removing coopetition relationships. The results of the additional analyses are consistent with the findings reported in the article. Accordingly, our results are not driven by coopetition relationships.

Third, selection of treatment is likely to be present in our context because MMC is subject to management discretion. That is, organizational decisions that affect MMC may affect the level of reinsurance usage. To address this concern, we employed the two-stage residual inclusion method that is suitable for nonlinear models (Abdurakhmonov, Ridge, Hill, & Loncarich, 2021; Terza, Basu, & Rathouz, 2008). We included in the first-stage model all control variables and an instrument variable (LnEntry), measured as the natural logarithm of the number of new market niches into which an insurer enters in a given year. In our data, LnEntry is significantly and positively correlated with an insurer's level of MMC. The positive coefficient on LnEntry suggests that entering additional new markets results in a higher level of MMC for an insurer. Meanwhile, our empirical analysis shows that LnEntry is not significantly associated with the level of reinsurance usage beyond its indirect effect through MMC. We then included the first-stage residuals (Xuhat) as a regressor in the second-stage regression. A Montiel-Pflueger robust weak-instrument test (F statistic = 1,325.918, p < .001) offers support to the relevance of the instrument. We also performed a Davidson-MacKinnon test of exogeneity on a fixed effect model estimated via the instrument. The statistic is 0.20 (p = .654), which does not reject the null hypothesis that endogeneity has no meaningful effect on our results. The two-stage residual inclusion regressions produce very similar results as those reported in Table 2 (Appendix A). Thus, although completely ruling out the potential effects of firm decisions on MMC is unlikely, the tests indicate that selection of treatment should not be a serious issue in our sample.

Additional robustness tests. We performed a battery of additional robustness tests. First, our sample spans the periods of the financial/insurance industry deregulation (1999–2000), the boom in mortgage-backed securities (2003–2008), and the Great Recession (2008–2010). We constructed three period dummies to capture the potential differentiating effects of these periods on an insurer's reinsurance decision. We then reestimated all regressions by including these three period dummies. Second, an insurer's risk transfer decision is likely to be affected by competitive risk and catastrophic risk. To tease out the effect of catastrophic risk from the competition risk, we constructed a catastrophic risk exposure variable that captures the degree of risk exposure to all catastrophe-prone insurance lines of business and geographic locations and included it in all regressions.

Third, while multiplicity of contacts allows firms to gain knowledge of one another, the extent to which firms may acquire information on their rivals is a function of their positions or embeddedness in the competitive network (Tsai et al., 2011). To make sure that the information benefit from MMC is nonredundant to positional advantages in the competitive networks, following Tsai et al. (2011), we constructed two embeddedness variables—relational competitive embeddedness and structural competitive embeddedness—and included them as additional controls for a robustness test. Fourth, we constructed an alternative MMC measure by following Li and Greenwood (2004) and reran our regressions. Fifth, we conducted conventional two-way fixed effects ordinary least squares with corrected standard errors for heteroskedasticity to reestimate all the models. In all of these robustness tests (untabulated for brevity), our inferences remain unchanged.

Furthermore, there is an argument that mutual forbearance is more likely to happen between firms with asymmetric territorial interests. We therefore followed Gimeno (1999) to construct an additional MMC variable that captures reciprocal market contact relations. Analyses based on the reciprocal MMC measure provide added support to the role of mutual forbearance in risk transfer.

Discussion and Conclusion

This study sets out to better understand how firms transfer risk in response to firm-specific competition. To the best of our knowledge, this is the first study that shows a firm's risk transfer level relates to its MMCs with competitors. Specifically, our findings show that MMC has a curvilinear impact on risk transfer level. Over the range of low MMC, an increase in MMC is accompanied by an increase in risk transfer. However, this effect holds only up to a certain point, after which an increase in MMC yields a reduction of risk transfer ratio. Moreover, a firm's risk transfer decision depends on the overall risk transfer level of its multimarket competitors. Instead of mimicry, differentiation appears to be the dominant strategy adopted by insurers to make reinsurance purchase decisions. Interestingly, our findings provide initial evidence that, besides its direct effect, the state of industry concentration facing a firm moderates the relationship between MMC and risk transfer level. Although an increase in concentration erodes the positive effect of MMC on risk transfer at low levels of MMC, a firm sheds more risk when concentration and MMC are both high.

Theoretical Implications

Our findings concerning industry concentration and MMC suggest a more nuanced view of the effects of competition on risk transfer than what previous research has indicated. Although industry concentration and MMC both relate to intensity of competition, their underlying mechanisms differ in theory. Concentration captures the structural aspect of competition, which, though varying by markets, affects all participants in the same market in an equal fashion. The logic of the concept is built on the availability of growth opportunities (an incentive or a driving force for competition), the presence of dominant firms (a restraining force for competition), or both. As concentration increases, opportunities start to vanish while dominance emerges. Thus, concentration will monotonically reduce competitive activity. By contrast, MMC captures the multimarket aspect of competition, which is contingent on individual firms’ market contacts. The effect of MMC is more complex as when the number of contacts between firms across markets increases, it not only expands the potential for rivalry but also makes firms vulnerable to competitors. The opposite effects associated with the number of contacts thus predict a nonlinear relationship between MMC and competition.

Our results suggest that the two aspects of competition may interrelate to influence risk transfer. The need for risk transfer appears to peak when MMC and firm-specific industry concentration are both high. This finding may be explained by Bernheim and Whinston's (1990: 3) observation referring to Edwards’s (1955) seminal work: “[Edwards’s] appealing assertion is that collusive outcomes are easier to sustain with MMC because there is more scope for punishing deviations in any one market. The problem with this argument is that once a firm knows that it will be punished in every market, if it decides to cheat, it will do so in every market.” According to resource partitioning theory (Carroll, 1985), industry concentration may spark off new peripheral opportunities, which will incentivize firms to deviate from the current equilibrium. When the number of markets involved is large, the expected gain from defection in all the markets is likely to be greater than the cost of being punished. In this circumstance, firms face great risk because this market context makes it easy to start and escalate a business war. The diffusion and escalation of competition across markets will hurt all firms involved. Hence, firms have an incentive to transfer more risk to prepare for the worst.

This article advances the theory of MMC and its empirical foundation. MMC is important to a number of firm decisions, such as market entry and exit (Baum & Korn, 1996), internal resource allocation (Sengul & Gimeno, 2013), and investment in technology (Anand, Mesquita, & Vassolo, 2009). In his study on investment banks in the United Kingdom, Shipilov (2009) discloses that MMC can protect against partner noncooperation by acting as a governance mechanism. Adding to this line of research, we show that MMC relates to risk transfer level. This finding has important implications for future MMC research because it indicates the need to consider the risk exposure caused by MMC. Studies have primarily emphasized the effect of MMC on expected economic returns of firms (e.g., sales and profitability) but largely ignored the potential effect that MMC has on the volatility of economic returns. In this regard, our study augments understanding of risk implications of MMC by examining its critical but little explored influence on a firm's risk transfer level. We explicitly recognize that the multipoint effect may be nonmonotonic across the entire range of MMC levels. In doing so, our article extends recent studies that found a nonlinear relationship between MMC and corporate strategy (e.g., Baum & Korn, 1999; Haveman & Nonnemaker, 2000).

This study contributes to the action-based view of rivalry by illuminating the pattern of risk transfer in response to competition. Neoinstitutional theorists argue that firms often imitate other firms in an attempt to gain legitimacy or reduce uncertainty (DiMaggio & Powell, 1983). Interestingly, for risk transfer strategies, the conformity tendency is overshadowed by the differentiation tendency, which motivates a firm to allocate cash flow to its competitors’ weak points, where the latter are relatively cash constrained. This outcome is likely due to two reasons. First, considering the role of risk transfer in controlling losses, uncertainty may be less of a concern for such decisions because risk transfer itself mitigates the need for uncertainty reduction through conformity. Second, it is likely that insurance firms are confident of their own risk management capacities. Rather than being followers, they are inclined to use risk transfer to gain competitive advantage. In this light, our study provides new and important insights into competitive behavior research. Recently, scholars have suggested that rivalry between firms can be more sophisticated than what has been indicated. For example, Gao, Yu, and Cannella (2017) show that firms not only engage in direct contests but also use verbal responses to react to competitors. Our study extends this line of research by showing that, in addition to offensive actions such as predatory price cutting, defensive actions such as risk transfer serve another viable way for firms to achieve competitive advantages.

The earliest documented distinction between offensive and defensive actions dates back to Sun Tzu's The Art of War in fifth-century

Limitations and Future Research

This study has several limitations, which offer directions for future research. First, we examined only one industry. As reinsurance is insurance of insurers, we suspect that our findings may be replicable in industries where insurance is commonly used for risk transfer. For example, in most manufacturing sectors, insurance is extensively used by firms to protect themselves from threats such as pandemic, fire, earthquake, hail, tsunami, flooding, and even human-made catastrophes. These firms also buy insurance for work-related employee death or injuries and product-related liabilities to customers. Our findings may be generalizable to industries where market shocks are a major determinant of firm performance, as market shocks necessitate the use of risk transfer. For example, trading firms may suffer financial losses caused by unfavorable changes in exchange rate. A major operating cost of airline companies is fuel expense; hence, these firms are under pressure to manage negative oil price shocks. Under these market conditions, the decision of risk transfer should resemble that in the insurance industry, as they depend on the same cost pass-through mechanism (Figure 1). Given the relevance of inflection points or “competitive cusp,” as called by Porac, Thomas, and Baden-Fuller (1989), for the practice of risk transfer, research should be dedicated to how the inflection point can change across industries and what contributes to the variations. Second, our study is limited by its focus on reinsurance. Although this focus is well justified, as reinsurance is the most widely used risk transfer vehicle by insurers and offers a better proxy for risk transfer than some other practices, such as use of financial derivatives, which can also be used for speculation (Adam & Nain, 2013), there may be merit in examining the effects of rivalry on other risk transfer techniques.

Third, we restricted our analysis to one defensive action: risk transfer. According to the Awareness-Motivation-Capability (AMC) framework (Chen, 1996), interfirm rivalry is driven not only by the awareness and motivation of competing firms (as captured by the status of MMC examined in this study) but also by their capabilities to act. From this view, strategies such as preemptive mergers and acquisitions and preemptive patenting, which allow firms to undermine rivals’ capabilities by denying their access to critical resources or increasing their costs of procurement, may be counted as defensive actions, as they help suppress competition and reduce the need for risk transfer. This argument is consistent with the notion of resource captivity in research on strategic factor markets, resource picking, and factor-market rivalry (e.g., Barney, 1986; Markman, Gianiodis, & Buchholtz, 2009). In this sense, a firm's defensive system can be multilayered. Studying the relationships between risk transfer and other defensive actions and their joint usage might thus be a promising avenue for future research. For example, it would be interesting to explore (1) the conceptual and/or empirical differences among different types of defensive actions (e.g., risk mitigating vs. preemptive vs. retaliatory), (2) potentially important attributes of defensive actions (e.g., likelihood and speed of defensive responses), and (3) the aggregation of defensive actions (perhaps mixed with offensive actions) to form action repertoires and sequences.

Fourth, the focus of this study is on the multimarket and structural dimensions of firm competition. Recent studies show that firm competition can be relational, driven by affective, sociological, or social psychological factors that are less rational (Kilduff, 2019; Kilduff, Elfenbein, & Staw, 2010). While the notion of MMC does capture some interfirm relationships by taking into consideration firms’ knowledge of one another through past interactions (cf. Kilduff, 2019), it could be fruitful to explore in future research how emotion or psychological impulses associated with relational rivalry—such as those related to history of interaction, tension, identity, reputation, status, and psychological rivals—may affect the risk attitude of managers and subsequently their risk transfer decisions. In addition, our study centers on price levels and pricing power. Although it is beyond the scope of this study, risk transfer level may correlate with discrete pricing events, such as price cut moves. We leave this topic for future research.

Practical Implications

The findings of this study have practical implications for managers. Competition is an important consideration for risk transfer decisions. When competition intensifies, it becomes harder for a firm to maintain control over its prices in response to a cost shock. Chen (1996) and Gnyawali and Madhavan (2001) note that the influence of competition is multidimensional. For risk transfer, firms should consider not only the structure of the market but also their MMCs with others. Our results suggest that managers should be aware that risk magnifies when MMC and industry concentration are both high. Therefore, if possible, firms should avoid getting mired in such a situation; if impossible, they need to transfer more risk to deal with the escalating uncertainty.

Conclusion

In summary, this article contributes to researchers’ understanding of the effect of competition on corporate risk transfer. By measuring MMC and accounting for the structure of markets facing a firm, we highlight the significance of firm-specific competition in explaining a firm's risk transfer. The measures of MMC refine the important idea of product market competition, which has gained considerable attention in the management, finance, and risk management literatures in recent years. Our microfocus on firm-specific competitive conditions and their interactions contribute to the ultimate goal of explaining corporate risk transfer.

Supplemental Material

sj-docx-1-jom-10.1177_01492063221117530 - Supplemental material for Defense in Competition: Multimarket and Structural Effects of Firm-Specific Competition on Risk Transfer

Supplemental material, sj-docx-1-jom-10.1177_01492063221117530 for Defense in Competition: Multimarket and Structural Effects of Firm-Specific Competition on Risk Transfer by Jifeng Yu and Yijia Lin in Journal of Management

Footnotes

Acknowledgments

We are grateful to associate editor Aaron Hill and two anonymous reviewers at the Journal of Management for their helpful and thoughtful comments. All errors remain our sole responsibility.

Two-Stage Residual Inclusion Model

| Model 1 | Model 2 | |

|---|---|---|

| Intercept | −2.663*** | 2.756*** |

| (0.13) | (0.74) | |

|

|

||

| Log(BV of assets) | 0.154*** | −0.299*** |

| (0.01) | (0.04) | |

| Return on assets | −0.120*** | −0.233 |

| (0.02) | (0.15) | |

| Leverage | 0.022 | 0.165† |

| (0.01) | (0.09) | |

| Reinsurance sustainability index | 0.009** | 0.150*** |

| (0.00) | (0.02) | |

| =1 if mutual company | −0.002 | 0.107* |

| (0.01) | (0.04) | |

| =1 if stock company | 0.031*** | −0.181*** |

| (0.01) | (0.04) | |

| =1 if single firm | 0.058*** | −0.028 |

| (0.02) | (0.17) | |

| Firm's overall volatility | −0.027*** | 0.012 |

| (0.01) | (0.05) | |

| Market munificence | 0.181*** | 1.031*** |

| (0.03) | (0.21) | |

| Product diversification | −0.263*** | −0.229† |

| (0.02) | (0.12) | |

| Log(No. of market entries) | 0.043*** | |

| (0.00) | ||

| Xuhat | −0.110 | |

| (0.25) | ||

|

|

||

| MMC/100 | 0.392† | |

| (0.24) | ||

| MMC/100 square | −0.064* | |

| (0.03) | ||

|

|

||

| Average reinsurance ceded of single market competitors | 0.030 | |

| (0.10) | ||

| Average reinsurance ceded of multimarket competitors | −0.541* | |

| (0.23) | ||

| Weighted Herfindahl index | −1.619*** | |

| (0.34) | ||

|

|

||

| Weighted Herfindahl index × MMC/100 | −1.679* | |

| (0.73) | ||

| Weighted Herfindahl index × MMC/100 square | 0.674** | |

| (0.23) | ||

| Firm effect | Yes | Yes |

| Year effect | Yes | Yes |

|

|

||

| Log pseudolikelihood | 9,551 | 17,695 |

| No. of observations | 23,643 | 23,643 |

Note: Robust standard errors are in parentheses. BV = book value; MMC = multimarket contact.

p < .1.

*p < .05.

**p < .01.

***p < .001.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.