Abstract

This study examines the relationship between government corruption and corporate social responsibility (CSR). While existing research in CSR has suggested that reduced moral incentive is a key reason for firms’ low CSR engagement in regions with high government corruption, we postulate that government corruption in the region where a firm is headquartered also decreases its instrumental motivation to engage in CSR. The instrumental value of CSR will significantly decrease due to the diminished returns, which come from decreased stakeholder reciprocation and increased risk of becoming a rent-seeking target of corrupt officials. We furthermore suggest that the negative effect of government corruption on CSR may change depending on the levels of firm political risk, financial performance, and firm sales to government, which alter the returns of CSR. The findings, based on a sample of publicly listed US firms and political corruption data from the US Department of Justice during the 2003 through 2013 period, support our arguments. Our study contributes to CSR literature by highlighting and testing the instrumental perspective to examine the influence of government corruption on CSR.

Keywords

Incorporating stakeholder interests and broad social goals into firm decision making has become a rapidly growing theme (Aguilera, Rupp, Williams, & Ganapathi, 2007; Wang, Tong, Takeuchi, & George, 2016). A central question is why a firm pursues corporate social responsibility (CSR)—defined as “a business organization's configuration of principles of social responsibility, processes of social responsiveness, and policies, programs, and observable outcomes as they relate to the firm's social relationships” (Wood, 1991: 693). Researchers have developed a host of theoretical arguments regarding CSR value creation and risk reduction functions that account for this process (Aguinis & Glavas, 2012; Surroca, Tribó, & Waddock, 2010). CSR contributes to firm value via direct resource provision from stakeholders such as employees (Turban & Greening, 1997), customers (Lev, Petrovits, & Radhakrishnan, 2010), and the government (Wang & Qian, 2011). CSR also creates moral capital by acting as insurance-like protection when a firm confronts events such as being the target of litigation (Godfrey, Merrill, & Hansen, 2009; Koh, Qian, & Wang, 2014) or short sellers (Jia, Gao, & Julian, 2020).

The argument for value creation and preservation functions of CSR is built on the premise that all stakeholders appreciate CSR and reciprocate by lending their support to firms that practice it (Bosse, Phillips, & Harrison, 2009). However, firms face not only stakeholders who care about societal interests at large but also self-regarding stakeholders who focus on their own interests (Bridoux & Stoelhorst, 2014). Under certain situations, CSR may create opportunities for some self-regarding stakeholders to extract higher rents from firms (Barney, 2018; Ramírez & Tarziján, 2018). For instance, while governments encourage socially responsible actions, care about stakeholder interests, and reward firms with outstanding CSR (e.g., Flammer, 2018; Kassinis & Vafeas 2006; York, Vedula, & Lenox, 2018), officials could leverage their authority to pursue personal gains (Bo, 2006; Shleifer & Vishny, 1993). Officials with private intent may extract rents from firms via a range of tactics, such as not providing operating licenses or construction permits, performing frequent and strict inspections, and discontinuing government goods or services. Such extortionate practices could lead to the outright expropriation of firm assets. It is unclear how a firm's CSR is influenced by the private interests of stakeholders such as a corrupt government.

In this study, we seek to advance our understanding of how government corruption affects firms’ motivation to CSR engagement. Existing research has maintained that firms have two distinctive motivations for CSR engagement. On one hand, firms can be motivated to support stakeholders because doing so can improve their reputation and social image. This line of research emphasizes the instrumental value of performing CSR (Aguinis & Glavas, 2012; Donaldson & Preston, 1995; Harrison, Bosse, & Phillips, 2010; Jones, Harrison, & Felps, 2018). On the other, firms can be driven by the normative motivation to perform socially responsible behaviors (Donaldson & Preston, 1995). The normative perspective focuses on the moral evaluation, judgment, and prescription of human actions to understand CSR (Jones & Wicks, 1999; Muller & Kolk, 2010; Scherer & Palazzo, 2007). Earlier studies tend to focus on the influence of government corruption on CSR from a normative perspective, suggesting that in countries where government corruption is prevalent, firms and their stakeholders have weak social norms and values, which undermine the firms’ motivation to engage in CSR (Chantziaras, Dedoulis, Grougiou, & Leventis, 2020; Ioannou & Serafeim, 2012; Ucar & Staer, 2020). Ioannou and Serafeim (2012) contend that a country's government corruption combined with laws and regulations reduces firm CSR engagement within the global market through the spread of unethical practices. Ucar and Staer (2020) suggest that because salient government corruption weakens the norms of taking stakeholders into account, firms are unlikely to show a high level of CSR engagement. Nonetheless, these insights emphasize the normative aspect of CSR motivation; what remains less explored is how self-seeking behavior by government officials alters firms’ CSR via the instrumental motive. If stakeholders act opportunistically, firms’ motivation to invest in CSR could be impaired, as the nonresponse from stakeholders increases the cost of CSR. Jones, Harrison, and Felps (2018: 378) argue, “Among the most important of these costs is the possibility that a stakeholder will not abide by the norms of communal sharing despite the firm's generous sharing of resources.”

While Jones and colleagues (Jones, 1995; Jones et al., 2018) have recognized the premise of the instrumental motive of CSR, extant literature has not formally theorized such insights with testable hypotheses and appropriate research designs. Our study aims to fill this intellectual void by focusing on the influence of government corruption on CSR. Indeed, government corruption not only suggests that public officers may appropriate firms using their authority but also indicates that regulatory stakeholders are unlikely to maintain the reciprocity norms in interacting with firms. Rose-Ackerman and Palifka (2016: 9) observe that “in many cases the corrupt official acts inconsistently with his or her mandate, and second, even if he or she only takes acceptable actions in response to a payoff, the official has sold a benefit that was not supposed to be provided on the basis of willingness to pay.”

Specifically, we integrate CSR research with corruption literature to argue that firms reduce their CSR investment in response to government corruption because of decreased stakeholder reciprocity and increased risk of becoming government rent-seeking targets. The reason is that it is difficult for firms to establish a stable and mutually cooperative relationship with the corrupt government, and officials will not reward firms with superior CSR. Moreover, firms with a strong “ability to pay” (e.g., high current or expected future profits) may attract government attention and become targets for rent extraction by public officials (Svensson, 2003). Firms are likely to understate profits by altering financial policies, such as holding less cash (Caprio, Faccio, & McConnell, 2013; Smith, 2016). Accordingly, firms in regions prevalent with government corruption may reduce their CSR engagement, as socially responsible activities make self-regarding stakeholders (i.e., corrupt officials) aware that the firms have abundant discretionary resources that can be expropriated.

To better understand the effect of government corruption on firm CSR through an instrumental perspective, we investigate three boundary conditions: firm political risk, financial performance, and firm sales to government. These contextual factors capture the degree to which the value of CSR will be more or less pronounced for firms headquartered in regions with high government corruption. When the potential degree of stakeholder reciprocity is low and government rent seeking is high, the cost of CSR will be strengthened. Results from the US Department of Justice—based on a sample of US publicly listed firms from 2003 to 2013 with a refined measure of government corruption at the federal judicial district level—provide support for our predictions.

Our contributions are twofold. First, we advance the CSR research by theorizing how self-seeking behavior of a stakeholder undermines a firm's instrumental motivation to engage in CSR. As a departure from previous studies that highlighted the normative influence of government corruption on CSR (e.g., Luo, 2006; Ucar & Staer, 2020), we emphasize the instrumental motivation for CSR, contending that government corruption may reduce firm CSR due to diminishing returns of social engagement. Our three boundary conditions provide a further test of the mechanism by altering a firm's instrumental motivation. By doing so, we seek to address scholars’ call for more investigations of “the evolution or change of views on CSR . . . within a national context” (Wang et al., 2016: 540, emphasis added).

Second, our study enriches corruption research. In his seminal review, Cuervo-Cazurra (2016: 35) maintains that “the consensus about the impact of corruption is not as clear.” In this study, we propose that it is imperative to move beyond the focal firm-centric cost by considering the community-based costs of corruption. Ultimately, firms are members of a broader community, and a self-seeking stakeholder's behavior can spill over to erode the social infrastructure of the whole community. Additionally, we introduce a much-refined measure to capture government corruption at the federal judicial district level, which aims to address the challenge in the literature that “corruption is notoriously difficult to measure” (p. 37).

Theoretical Background

Instrumental and Normative Motives of Socially Responsible Actions

Stakeholders are individuals or groups who are affected by, or whose actions can directly affect, a firm's operations (Freeman, 1984). The emergence of stakeholder theory, as a well-received paradigm, has led to the development of several perspectives regarding a firm's motivation to engage in social initiatives, including the descriptive, instrumental, and normative motives (Donaldson & Preston, 1995). The descriptive aspect of stakeholder theory explains how firms actually behave. The instrumental aspect, however, articulates the potential consequences if firms behave in a socially responsible or irresponsible way. Last, the normative aspect is concerned with the moral propriety of firm behaviors (Jones, 1995). Jones and Wicks (1999) categorize research in stakeholder theory into two broader categories: social science–based instrumental theory and ethics-based normative theory. Scholars have developed instrumental and normative accounts of stakeholder theory, arguing that the instrumental and normative motives for a firm's social initiatives are complementary and mutually supportive (Aguilera et al., 2007; Donaldson & Preston, 1995).

Broadly speaking, the instrumental stakeholder perspective contends that firms’ engagement in socially responsible activities is motivated by instrumental value (Clarkson, 1995; Harrison et al., 2010; Jones, 1995). This view suggests that by establishing mutually trusting and cooperative relationships with stakeholders, firms can achieve competitive advantages due to the potential benefits, such as greater consumer support (Lev et al., 2010), stronger employee commitment (Greening & Turban, 2000), and better relationships with governments (Kassinis & Vafeas, 2006; Wang & Qian, 2011). Moreover, the instrumental value of CSR can work as an insurance policy for buffering firms against potential loss (Godfrey et al., 2009). Aside from the instrumental motivation, firms can engage in CSR due to normative reasons, which specify their moral obligations to the interests of all stakeholders (Clarkson, 1995). The normative motive focuses on the fair treatment of other stakeholders and what firms ought to do. This view contends that developing mutual trust and cooperating with stakeholders are morally desirable behaviors. From this perspective, firms’ engagement in CSR is an outcome of the belief in the intrinsic value of these actions (Jones & Wicks, 1999; Muller & Kolk, 2010).

Thus, a firm's social engagement may not only have morally sound ethical cores (normative motive) but also lead to satisfactory outcomes (instrumental motive). By recognizing the normative and instrumental motives simultaneously, the stakeholder theory aims to understand how “stakeholder relationships governed by the norms of traditional ethics—for example, fairness, trustworthiness, loyalty, care, and respect—will lead to improved financial performance” (Jones et al., 2018: 371). The central argument of this stream of research is that to improve financial performance, the primary payoff to a firm for engaging in socially responsible activities is that the firm enjoys relationships with stakeholders who positively reciprocate and that the cooperation of such stakeholders, in aggregate, creates value (Bosse et al., 2009: 453). However, the existing research has not investigated a firm's response in terms of CSR when one stakeholder group does not behave reciprocally but seeks self-interests instead—for example, when government officers misuse or even abuse authority to achieve private interests.

Government Corruption and Firm Responses

Government corruption refers to incidences in which officials leverage their authority to improve their personal welfare (Rose-Ackerman, 1999). When corruption is prevalent, government officials actively misuse their power to increase their welfare via bribes, fraud, extortion, and favoritism (Luo, 2005; Rodriguez, Uhlenbruck, & Eden, 2005; Rose-Ackerman, 1999). For example, officials may approach firms and demand “consulting fees” when firms request public services such as land acquisition, business permits, and infrastructure permits. Individuals who work for government agencies can ask firms for additional payments by delaying or rejecting such firms’ requests for public services. These corrupt individuals could be elected as presidents, low-level managers, or ordinary officials. Regardless of their levels of authority, one commonality is that such individuals are incentivized to ask for additional fees beyond the amounts required to conduct regular business (Rodriguez et al., 2005).

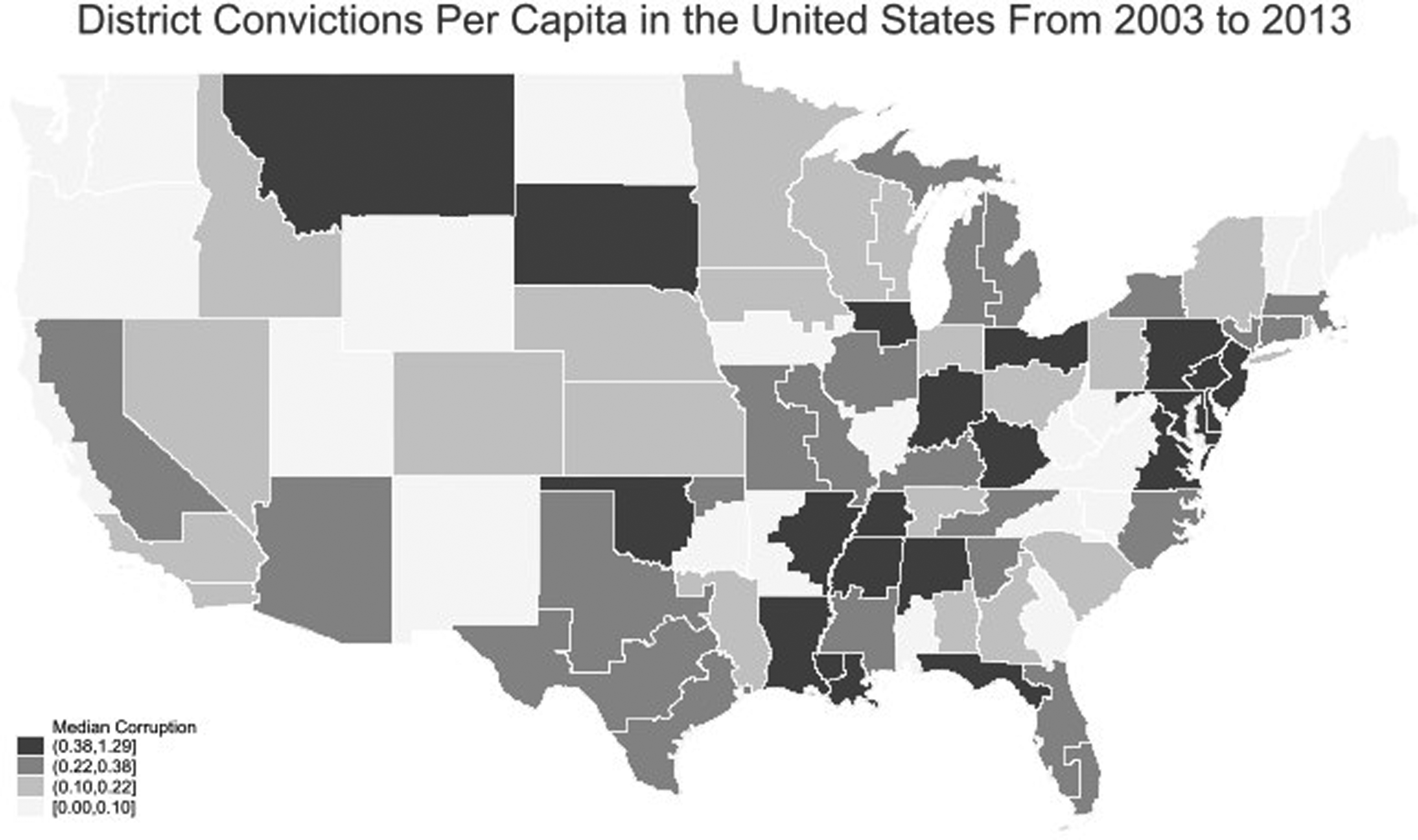

Although government corruption is widely observed in emerging economies, it exists in developed economies. During the 1990 through 2002 period, more than 10,000 US officials at the federal, state, and lower levels of government were convicted for acts of corruption, such as bribery, conflicts of interest, campaign finance violations, bid rigging, and obstruction of justice (Glaeser & Saks, 2006). Cases of government corruption abound. In 2012, United Airlines initiated a nonstop flight between Newark Liberty Airport and Columbia, South Carolina, as David Samson, the chairman of the Port Authority, had a weekend vacation home in South Carolina. This “personal flight” led to a loss of almost US$1 million (Levenson, 2017). Crucially, even within a given country such as the United States, the extent of government corruption varies across regions (Figure 1). Our study focuses on government corruption in the federal judicial district where a firm is headquartered, which includes convictions at federal, state, and lower levels of officials.

District Convictions per Capita in the United States From 2003 to 2013

The costs of government corruption on firms are substantial. The economic costs of government corruption around the world have been estimated to range from US$1.5–$2 trillion (Lawder, 2016). Essentially, a firm's ability to pay—which can be revealed by financial conditions (e.g., revenues, profit, and cash flow)—affects how governments and politicians treat the firm, such as how to select targets and demand different amounts of bribes (Huang & Yuan, 2021; Svensson, 2003). Olken and Barron (2009) find that officials tend to charge higher bribes if they notice that firms’ products have a higher market value (e.g., steel as opposed to agricultural produce).

To counter government appropriation, firms may respond to the risk of becoming a target of a corrupt government by undertaking certain strategic actions. Smith (2016) finds that government corruption prompts firms to hold less cash and increase leverage. Caprio et al. (2013) show that firms may hold fewer liquid assets when they operate within countries with a higher threat of political corruption. Also, they may demonstrate less innovation (Ellis, Smith, & White, 2020; Huang & Yuan, 2021), acquire targets in less corrupt areas (Nguyen, Phan, & Simpson, 2020), and report less favorable earnings (Chen, Jiang, Lu, & Yu, 2021). These actions are undertaken to shield a firm's wealth, reducing the possibility of being seen as a target with a strong ability to pay rent. In this study, we postulate that available choices for firms to manage government corruption are not limited solely to financial decisions and may include decisions such as CSR investment as well. In what follows, we develop hypotheses illustrating how government corruption will reduce firm CSR.

Hypotheses

Government Corruption and Firm CSR

Following the CSR research and corruption literature, we postulate that government corruption will influence firm CSR via normative and instrumental motives. First, as noted in previous studies, the normative motive of CSR reduces for firms headquartered in regions with high government corruption. These firms would like to demonstrate commitment to socially desired behaviors because they think that taking care of stakeholders and developing mutual trust with these entities are the right things to do and are morally desirable behaviors (Muller & Kolk, 2010; Treviño & Weaver, 1994). However, when faced with government corruption, individuals tend to think that they are not treated fairly (Fehr & Gächter, 2000) and they are not willing to trust others (Rothstein & Eek, 2009), as corruption hurts the stakeholders’ belief in a political system. Instead, they become calculative and focus more on self-interest. Psychology research has suggested that this mindset can adversely affect one's moral values (Small, Loewenstein, & Slovic, 2007). Consistent with the normative argument, Muethel, Hoegl, and Parboteeah (2011) demonstrate that government corruption diminishes managers’ tendency to show care to others in society. Luo (2006) argues that multinational enterprises’ perceptions of host country corruption decrease their philanthropic contributions, since perceived corruption increases these firms’ focus on ethics. Similarly, Chantziaras and colleagues (2020) show that socially desired norms, as captured by regions with high religiosity and low corruption, foster ethical behaviors and firm CSR disclosures.

Second, we build on the instrumental stakeholder perspective to argue that government corruption will reduce CSR investment, as its return will be low and will increase firms’ risk of becoming the target of government corruption. The instrumental perspective of CSR suggests that prosocial behaviors allow firms to achieve competitive advantages, because such behaviors cultivate close and mutually beneficial stakeholder relationships (Bosse et al., 2009; Jones et al., 2018; McWilliams & Siegel, 2001). As the most prominent and influential actors, governments have strong capacities to influence firm strategies via their control and provision of resources such as “providing the physical infrastructure and markets that firms use and operate in, promulgating laws and regulations that influence the way firms do business, and impose taxes and other financial costs on firms” (Kassinis & Vafeas, 2006: 146). Government instruments such as regulations, subsidies, and pollution penalties are key drivers of corporate social and environmental practices (e.g., Bansal & Roth, 2000; Kassinis & Vafeas, 2006; Wang et al., 2016). However, in a region with a relatively high level of corruption, it will be difficult for firms to develop stable and mutually cooperative government relationships. This reduces the value of CSR since the self-interested government may not reciprocate with firms by channeling resources such as tax exemptions and financial support (e.g., Ioannou & Serafeim, 2012). Also, firms headquartered in regions with high levels of corruption may receive negative evaluations from other stakeholders due to the unlawful acts. Auditors, for example, may ask firms for higher fees, and these firms would experience a heightened likelihood of a going concern opinion from their auditors (Jha, Kulchania, & Smith, 2021; Xu, Mao, & Petkevich, 2019).

Moreover, corrupt officials may use a variety of ways to extract rents from firms with a high level of CSR. As noted earlier, public officials have a desire for information regarding firms’ economic rents and vulnerability to expropriation. CSR may act as a surrogate for this information as it reflects a firm's discretional expenses and wealth associated with a strong performance (Lys, Naughton, & Wang, 2015). As with other strategic actions, CSR is not free, and firms must have sufficient internal resources to support it (Buchholtz, Amason, & Rutherford, 1999; Seifert, Morris, & Bartkus, 2004). Hence, corrupt officials may deem that firms with substantial CSR have “the ability to pay” and thus target them for rent seeking (Svensson, 2003). These officials may reject firms’ requests for certain resources or use their authority to disrupt operations (Svensson, 2003). Officials can also delay or even reject firms’ demand for public services to solicit additional money. To reduce the rent seeking of these officials, firms may keep a lower profile by decreasing their CSR investment.

The present discussion suggests that in addition to the normative motive through moral obligations, government corruption can influence firm CSR via the instrumental mechanism as well. The instrumental perspective asserts that as government corruption becomes a concern, socially desired activities do not generate the intended outcomes and will put firms at a higher risk of becoming corrupt officials’ rent-seeking targets. Overall, we propose the following:

Hypothesis 1: The level of government corruption in the region where a firm is headquartered will be negatively related to firm CSR.

Boundary Conditions: Firm Exposure to Government Rent Seeking

Our first hypothesis maintains that government corruption influences a firm's motivation to engage in CSR via normative and instrumental motivations. While both motives are crucial, our study focuses on the instrumental motive of CSR, as prior research has already investigated the normative motive (Ioannou & Serafeim, 2012; Luo, 2006; Ucar & Staer, 2020). To further demonstrate the instrumental mechanism, we have identified a set of firm-level contingencies that can affect the cost-benefits of CSR: firm political risk, financial performance, and firm sales to government. We expect that boundary conditions that make firms more (less) sensitive to the influence of government officials will strengthen (weaken) the main effect.

Firm Political Risk

Firm political risk refers to the firm-level measure of the extent of uncertainty faced by firms associated with politics, which covers a range of political matters: economic policy, budget, environmental and trade policy, institutions and political process, health, security and defense, tax policy, technology and infrastructure, government funding, and so on (Garcia-Canal & Guillén, 2008; Kingsley, Bergh, & Bonardi, 2012). Firms facing higher political risk tend to actively engage in political campaigns, forge stronger connections with politicians, and invest more in lobbying activities (Hassan, Hollander, van Lent, & Tahoun, 2019). Hassan et al. (2019) find that firm-level variation drives more than 90% of the variance in political risk.

We contend that the benefits of CSR engagement for a firm headquartered in a region with high government corruption may further decrease when the firm faces a higher level of political risk, which would intensify the negative relationship between government corruption and firm CSR. By definition, when a firm faces considerable uncertainty in the political environment, the firm will be more vulnerable to the influence of government and its officials. Research shows that political risks can compound contractual difficulties and impair a firm's operations (Oxley, 1999; Phene & Tallman, 2012). Facing such uncertainties in the political environment, firms are unlikely to believe that corrupt officials will follow the reciprocity norms even if they commit CSR. Instead, firms will opt to devote more resources to actively engage in political activities to manage the risk (Hassan et al., 2019). Moreover, high levels of political risk prompt firms to recognize that government officials, particularly the corrupt ones, play a salient role in determining their businesses’ survival (Henisz, 2000). The reason is that for corrupt officials, should a firm refuse to cooperate, rent-seeking government officials may retaliate against the firm. Thus, the level of political risk facing a firm is likely to amplify the effect of government corruption by magnifying the firm's political cost and decreasing the return of CSR. Under this condition, the firm is likely to further decrease CSR engagement.

Yet the impact of government corruption on CSR will be limited when a firm faces less political risk. Low political risk suggests that the overall political environment is relatively stable. Under this condition, a firm does not have an imperative need to avoid interacting with the government (Henisz & Delios, 2001; Holburn & Zelner, 2010). Also, the presence of low political risk may mitigate a firm's concern about the corrupt government and encourage the firm to think that the government will likely maintain the reciprocity norms in its interaction with the firm. Thus, the firm will be less likely to greatly diminish its CSR. From the firm's perspective, it remains acceptable and rewarding to be socially engaged.

Hypothesis 2: Firm political risk will strengthen the negative relationship between government corruption and firm CSR.

Financial Performance

Aside from political risk, firm financial performance is another boundary condition that changes the effect of government corruption through influencing the payoffs of CSR. From the instrumental stakeholder perspective, CSR engagement can provide firms with a competitive advantage to differentiate themselves from competitors, as it helps build cooperation with stakeholders (e.g., Jones, 1995). However, firms headquartered in regions with a high level of government corruption will not be rewarded adequately by such CSR engagement because corrupt government officials may not reciprocate. This is particularly true for well-performing firms, given that they generally do not need CSR to differentiate themselves. Moreover, a firm's financial performance is an easy-to-access and direct indicator for external actors, including governments, to know the firm's operating effectiveness and potential discretionary financial resources. Because a well-performing firm has rich financial and physical resources, the firm is an attractive target for corrupt government officials (Svensson, 2003). Consider the case in which a firm is headquartered in an area with prevalent government corruption. If the firm is committed to a range of CSR activities, government officials with private intent can easily identify the firm as a rent-seeking target. Notably, this tendency would be heightened if the firm has superior financial performance. To mitigate the risk of being appropriated, a firm with good performance will have stronger motivation to diminish its CSR engagement.

In contrast, the influence of government corruption on CSR will be reduced when a firm has less satisfactory performance. Poorly performing firms not only have fewer resources to engage in socially responsible activities but also are less likely to gain support from stakeholders via CSR. Generally speaking, stakeholders expect better-performing firms to contribute more to society but expect poorly performing firms to improve business operations (Wang & Qian, 2011). The less satisfactory performance suggests that a firm has limited resources and less ability to pay. Thus, stakeholders may not lend their support to such a poorly performing firm. While self-interested government officials could approach the firm to seek rent, low performance provides the firm a good excuse for not entertaining such requests. Thus, the poorly performing firm may be less susceptible to the influence of government corruption in determining its CSR.

Hypothesis 3: Firm financial performance will strengthen the negative relationship between government corruption and firm CSR.

Firm Sales to Government

Finally, firm sales to government may alter the effect of government corruption on CSR. While most firms operate within the private sector, governments are prominent clients for many companies. For example, in 2019, the US government spent $4.45 trillion in procurement—approximately the size of Japan's gross domestic product. The extent to which a firm has governments as clients can induce the firm to weigh the potential benefits and costs of engaging in CSR. Specifically, a firm that makes more sales to governments has incentives to develop closer and more cooperative relationships with government agencies as compared with firms that do not rely on governments as their main customers. These cooperative relationships can encourage the government and officials to reciprocate and reward firms with superior CSR. This is crucial as CSR can help a firm compete to obtain government contracts. Because CSR activities can build a trustworthy, reputable, and reliable image, a firm would stand out among competitors when securing contracts (Du & Bhattacharya, 2011; Flammer, 2018; Hillman & Keim, 2001). Moreover, a firm with high sales to governments can leverage its ties to counter corrupt officials’ asking for bribes. As these business relationships allow a firm to know the decision makers in government, the firm with high sales to governments will be more able to maneuver the situation of government corruption. A firm, for example, can ask higher-level officials to mediate or intervene. Meanwhile, by making sales to government, a firm can create a mutual dependence to mitigate the adverse effect of corruption. That is, if corrupt officials ask exorbitant bribes that put the firm's survival in danger, government will suffer too. Eventually, it is difficult to find a substitute firm immediately. Hence, firms with more sales to the government will be less susceptible to the influence of government corruption in deciding their CSR.

Conversely, a firm that makes trivial or even no sales to government may act differently. Such a firm does not depend on the government for its survival, nor does it desire to build a trustworthy and reliable image with the government (Homburg, Stierl, & Bornemann, 2013). From the firm's perspective, the cost of conducting CSR is already high. Substantial CSR activities will not attract government rewards and instead make the firm a more visible target. Because trivial sales to governments prompt a firm to recognize the interaction with government as riskier while having lower return, we expect that a firm with limited government sales will be more influenced by government corruption in deciding its CSR engagement.

Hypothesis 4: Firm sales to government will weaken the negative relationship between government corruption and firm CSR.

Methods

Data and Sample

We test our arguments by gathering data from several reliable sources. We first identified our sample firms from Compustat during the 2003–2013 period. We excluded firms operating within the industries of financial services (Standard Industrial Classification [SIC] codes 6000–6999) and utilities (SIC 4900–4999) following prior research (Yuan, Lu, Tian, & Yu, 2020). Compustat provides firm financial and other information (e.g., headquarters locations). We acquired data on government corruption from the US Department of Justice, while firm CSR information was from MSCI STATS. Other data sources include the Center for Research in Security Prices, Execucomp, and I/B/E/S. Merging the information from these sources resulted in a sample of 1,779 firms with 11,865 firm-year observations. Appendix A online provides the definitions of our variables. Appendix B presents the summary statistics for convictions per capita at the district level.

Dependent Variable

Our dependent variable is CSR. We measured this variable using corporate social performance since it reflects a firm's level of engagement with the various social, ethical, and legal issues associated with stakeholders (Mattingly & Berman, 2006; Wood, 1991). Specifically, we utilized the following six dimensions from MSCI STATS to capture a firm's social commitment: environment, human rights, community relations, employee relations, product characteristics, and diversity. MSCI STATS uses a number of reliable data sources: company filings, surveys, government and nongovernment organization sources, media sources, and direct communications with firm officers. MSCI STATS has sector-specific analysts rate each dimension using a proprietary framework of positive and negative indicators once it acquires the relevant information. For each category, a firm receives a score of 1 if it has the corresponding strength or concern and 0 otherwise. Each dimension is standardized to make the scores comparable across dimensions and over time, since the numbers of strengths and concerns may change over time. CSR is measured as the difference between adjusted total strengths and adjusted total concerns.1 This variable is time varying, with higher values denoting that a firm is more committed to socially responsible activities.

Independent and Moderating Variables

Our independent variable is government corruption measured at the federal judicial district level. In contrast with earlier research using either subjective assessments or self-reported indicators to measure government corruption, we used an objective indicator—conviction data—following recent research (Butler, Fauver, & Mortal, 2009; Smith, 2016). To this end, we obtained information on convictions from the Public Integrity Section of the US Department of Justice. Each year the Public Integrity Section publishes the Report to Congress on the Activities and Operations of the Public Integrity Section, documenting convictions within 94 federal judicial districts. District-level convictions provide more fine-grained information on government corruption. Following Smith (2016), we measured government corruption using the number of convictions scaled by the population within each judicial district (i.e., convictions per capita). We used firms’ zip codes from Securities and Exchange Commission filings to locate firms’ Federal Information Processing Standard codes and identified their judicial districts. Although government corruption is measured at the judicial district level, this indicator captures corrupt officials from federal, state, and lower regional levels (Butler et al., 2009; Glaeser & Saks, 2006).

We have suggested three boundary conditions that may moderate the effect of government corruption on CSR. One is firm political risk. Applying a textual analysis approach, Hassan et al. (2019) collected 178,173 quarterly conference calls from a set of US public firms forming a firm-specific, time-varying index capturing the extent to which managers recognize either substantial or limited political risks within their operating contexts. Topics such as “economic policy and budget,” “trade,” and “institutions and political process” are incorporated to generate this measure. Higher values indicate greater political risks perceived by a firm. We accessed these data from the Firm-Level Risk website (https://www.firmlevelrisk.com/home). Second, financial performance is measured as a firm's return on assets adjusted by industry (two-digit SIC). Third, firm sales to government is measured as firm revenues from the sales of goods or services to US federal, state, or local governments scaled by total sales. We used data from USAspending.gov and Compustat Segments to create this variable. The index with a higher value suggests that a firm depends more heavily on government during a given year.

Control Variables

Our models included a vector of control variables to rule out alternative explanations. First, at the firm level, we included firm size measured as a firm's total sales (logarithm), as firms with higher sales are more resourceful and can be more committed to CSR. Highly leveraged firms could have a reduced capacity to engage in CSR. Thus, we controlled for firm leverage measured as long-term debt over firm assets. We included dividend since it can decrease the firm's discretional resources available for CSR. This is a binary variable that equals 1 if a firm pays out dividends during a given year and 0 otherwise. Since firms with greater market value may have more capacity to support stakeholders, we included Tobin's Q in our models. Because stakeholders may expect more seasoned firms to show greater commitment to CSR, we included firm age in the models. Firms followed by more financial analysts may have higher motivation to engage in CSR. Thus, we measured analyst coverage as the number of financial analysts issuing earnings forecasts for a focal firm during a given year (logarithm) using the information from I/B/E/S.

Additionally, industry and community peers could induce firms to become more socially engaged (Husted, Jamali, & Saffar, 2016; Marquis, Glynn, & Davis, 2007). Following Marquis and Tilcsik (2016), industry CSR was measured as the average CSR of firms within same industry (2-digit SIC). Community CSR was measured by the average CSR of firms within the community, defined as the district where a focal firm was headquartered. We excluded the focal firm in creating these two variables. Moreover, firms located within regions with a larger population of higher income and/or education levels may have greater motivation to support business community stakeholders via CSR. Thus, we included several county-level variables, such as population (logarithm), income (median household income), unemployment (unemployment rate), and educational attainment (proportion of the population aged older than 25 years holding at least a 4-year college degree). We consulted the US Census Bureau to obtain the needed information. Moreover, firms expanding into various geographic markets may rely less on the home region stakeholders for resources. Thus, we measured geographic dispersion using the number of states where firms have affiliates. Finally, we included a set of industry and year dummies to control for the industry and time effects.

Statistical Model

To examine the effect of government corruption on firm CSR, we established the following model:

Results

Table 1 presents our sample distribution and summary statistics. Panel A presents the distribution of our sample according to industry and year. Most firms are manufacturers (54.6%), while some operate within the service (19.4%) and wholesale (13.5%) sectors. Panel B presents the means, standard deviations, and correlations of these variables. As shown, CSR is negatively correlated with government corruption (γ = −0.06, p < .01). We checked the variance inflation factors: the mean value is 1.35 and the highest is 2.38, well below the recommended threshold of 10. Thus, multicollinearity is not a major issue.

Sample Distribution and Summary Statistics

Note: n = 11,865. Correlations with absolute values >.02 are significant at the p < .01 level. CSR = corporate social responsibility; SIC = Standard Industrial Classification.

Testing Hypothesis 1

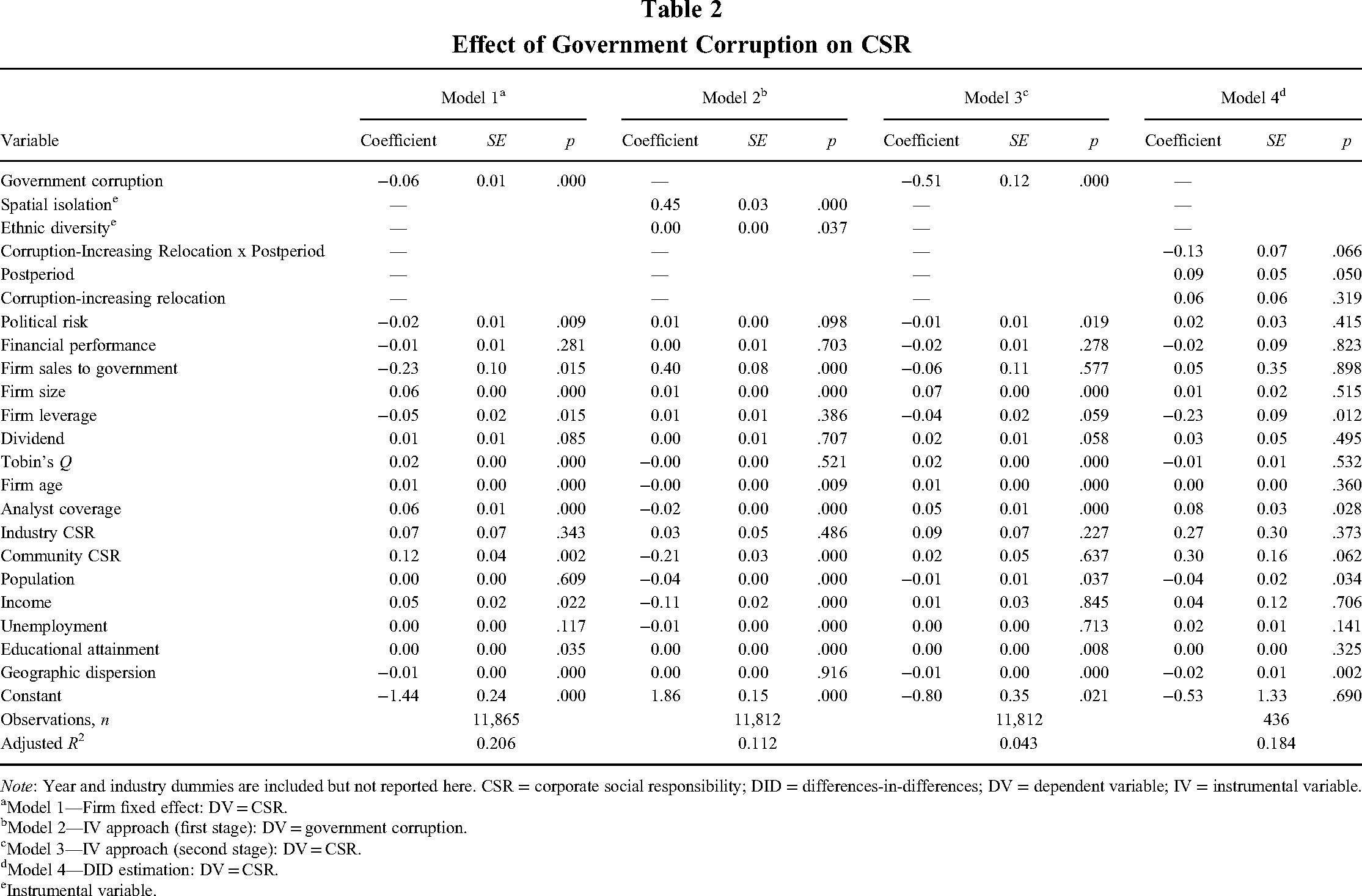

We tested Hypothesis 1 using three estimation methods: a fixed-effects regression, the instrumental variable approach, and a differences-in-differences estimation. Table 2 summarizes these results.

Effect of Government Corruption on CSR

Note: Year and industry dummies are included but not reported here. CSR = corporate social responsibility; DID = differences-in-differences; DV = dependent variable; IV = instrumental variable.

Model 1—Firm fixed effect: DV = CSR.

Model 2—IV approach (first stage): DV = government corruption.

Model 3—IV approach (second stage): DV = CSR.

Model 4—DID estimation: DV = CSR.

Instrumental variable.

Fixed-effects regression

In Model 1 of Table 2, we find a negative and significant estimate of government corruption (β = −0.06, p = .000). In terms of magnitude, this estimate suggests that a 1-SD increase of government corruption will decrease CSR by 10%: 0.25 × (−0.06/0.15) = −0.10. Thus, all else being equal, moving a firm from a district in Northern Illinois (with a mean government corruption level of 0.47) to a district in Minnesota (with a mean government corruption level of 0.11) raises the mean firm CSR by 0.02, an increase of 13%. This provides strong support for Hypothesis 1.

Instrumental Variable

Although we find that firms in regions with prevalent government corruption tend to demonstrate less CSR, these findings might suffer from a potential reverse causality issue. That is, firms with low CSR engagement may also engage in rent-seeking activities (Krueger, 1974), which makes government corruption more salient. To address this concern, we used the instrumental variable approach by considering two indicators: spatial isolation and ethnic diversity. Spatial isolation is a gravity-based index measuring the proportion of residents living within a state but outside its capital. Research maintains that states with more isolated capital cities experience more serious government corruption issues (Campante & Do, 2014), as these states are not closely scrutinized by either citizens or the media. However, ethnic diversity, defined as the extent to which a state has a more diverse population in terms of ethnicity, is positively related to government corruption because citizens from diverse ethnic backgrounds tend to pay greater attention to redistribution issues than to government honesty (Alesina, Baqir, & Easterly, 2002). Crucially, no clear theoretical reason exists for these two variables to directly influence a firm's CSR other than its correlation with government corruption. In employing these two variables, we performed a two-stage least squares estimation. As Models 2 and 3 of Table 2 show that spatial isolation and ethnic diversity are positively related to government corruption (β = 0.45, p = .000, and β = 0.00, p = .037, respectively), while the instrumented government corruption is negatively related to CSR (β = −0.51, p = .000). Hypothesis 1 is therefore further supported. Following the suggestions by Semadeni, Withers, and Certo (2014), we conducted three diagnostic tests of instrumental variables, and these tests confirm the validity of our instruments.4

Differences-in-Differences Analysis

In addition to the instrumental variable approach, we performed a differences-in-differences analysis (Angrist & Pischke, 2009). We expect that firms that move their headquarters may exhibit different tendencies in subsequent CSR engagement to the extent that the government corruption level of the old region differs from that of the new. In our data, we identified 436 relocation cases, among which 199 and 237 were firms moving to regions with lower and higher levels of government corruption, respectively. By leveraging these incidences, we created two dichotomous variables: (1) corruption-increasing relocation distinguishes firms that moved to more corrupt regions versus those that moved to less corrupt regions (1 if a firm relocated to a new region with a higher level of government corruption than the old region and 0 otherwise) and (2) postperiod denoting that the year was before or after the relocation (1 if after relocation and 0 otherwise). According to Model 4 of Table 2, the interaction of corruption-increasing relocation and postperiod is negative and marginally significant (β = −0.13, p = .066), suggesting that changes in government corruption alter firm CSR.

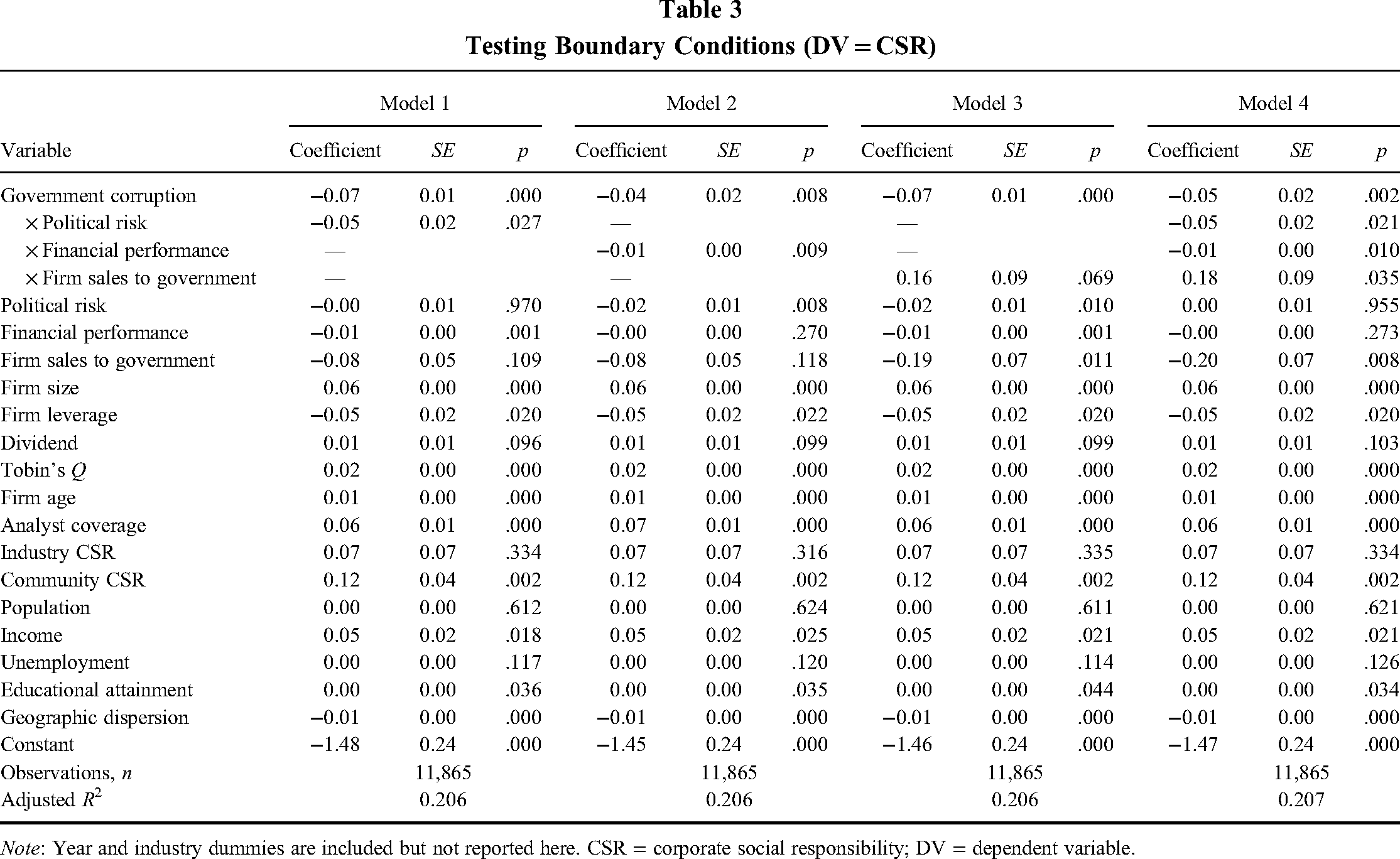

Testing Hypotheses 2 to 4

Hypotheses 2 to 4 examined the boundary conditions of government corruption effects on firm CSR. Hypothesis 2 argues that the negative relationship between government corruption and firm CSR would be strengthened for firms with greater political risk. As Model 1 of Table 3 suggests, the interaction of government corruption and political risk is negative and significant (β = −0.05, p = .027). This estimate suggests that when political risk is at a low level, a 1-SD increase of government corruption will reduce firm CSR by 6%, yet when political risk is at a high level, a 1-SD increase of government corruption will lower firm CSR by 16%. Hypothesis 2 is thus supported.

Testing Boundary Conditions (DV = CSR)

Note: Year and industry dummies are included but not reported here. CSR = corporate social responsibility; DV = dependent variable.

Hypothesis 3 argues that the negative relationship between government corruption and firm CSR would be strengthened for firms with better financial performance. According to Model 2 of Table 3, the interaction of government corruption and financial performance is negative and significant (β = −0.01, p = .009). This suggests that when a firm's financial performance is at a lower level, a 1-SD increase of government corruption will then reduce the firm's CSR by 7%. Yet when a firm's financial performance is at a high level, a 1-SD increase of government corruption will lower the firm's CSR by 14%. Thus, Hypothesis 3 is also supported.

According to Hypothesis 4, firms that rely on the government for sales are less likely to reduce their CSR engagement even if they operate in regions with a government corruption problem. In Model 3 of Table 3, we find that the interaction of government corruption and firm sales to government is positive and marginally significant (β = 0.16, p = .069). This coefficient means that when firms have limited sales to government, then a 1-SD increase of government corruption will lower firm CSR by 12%. However, when firms have more sales to government, the same increase in government corruption would reduce firm CSR by only 10%. Hypothesis 4 is accordingly supported.

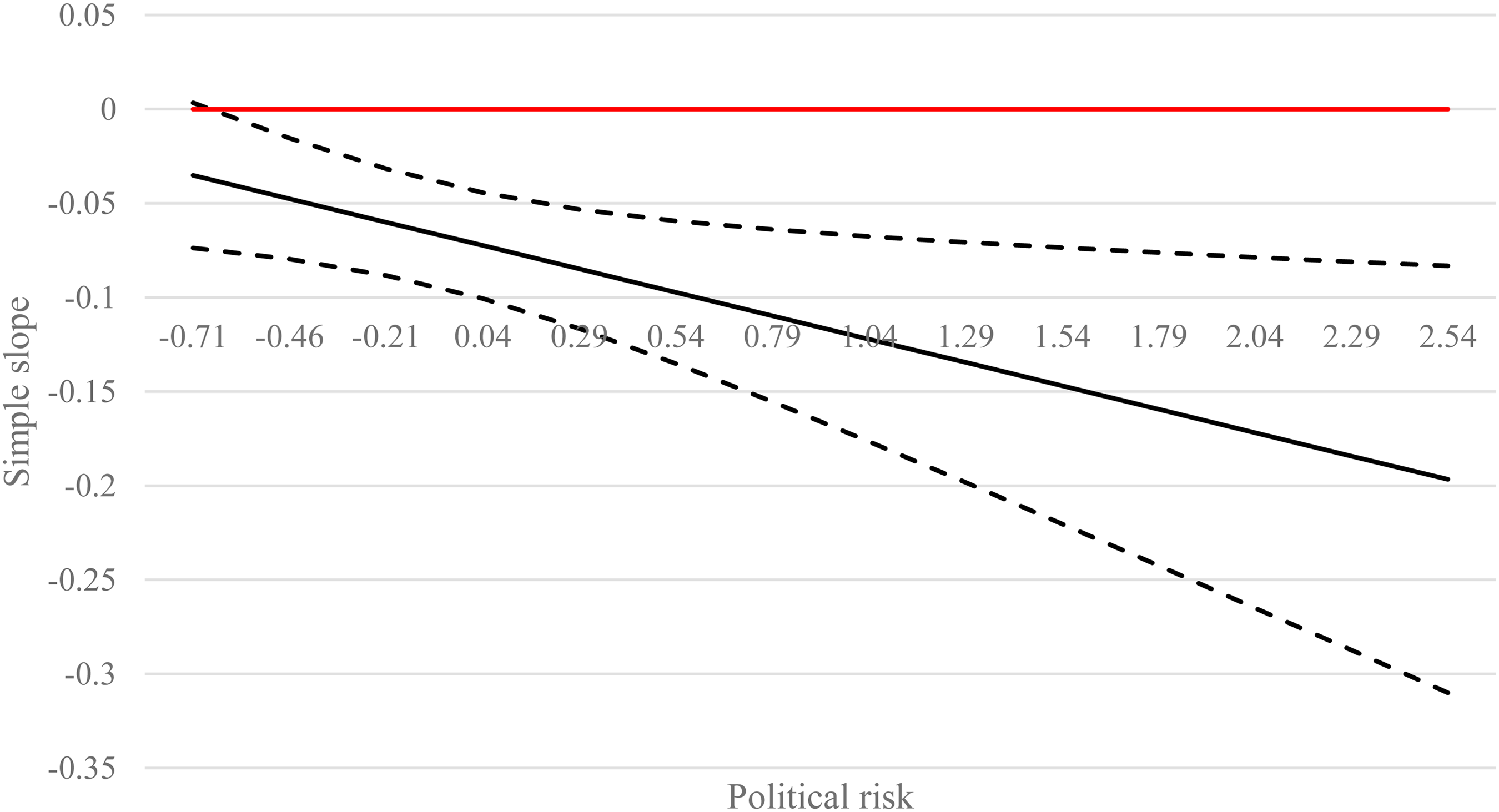

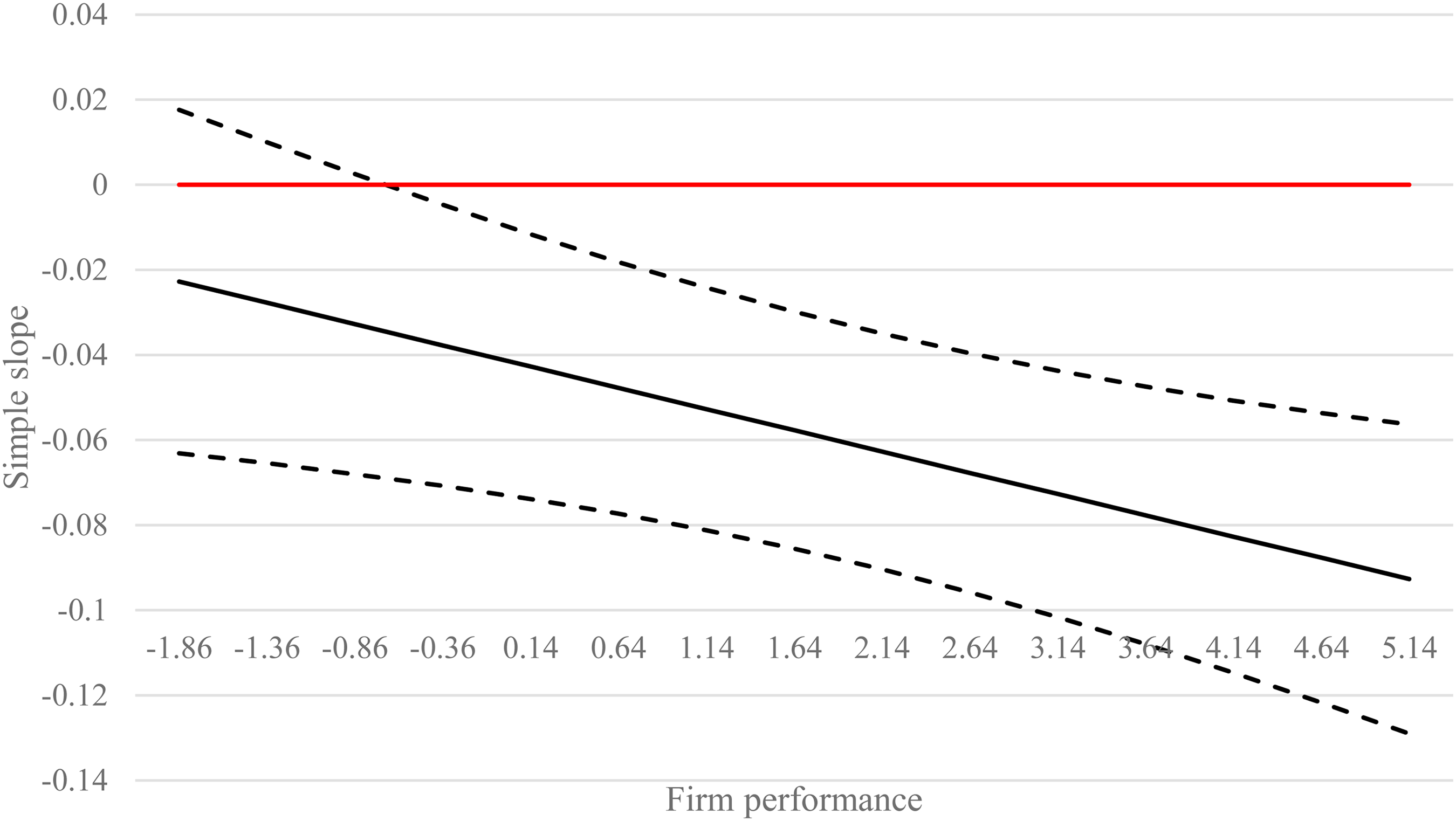

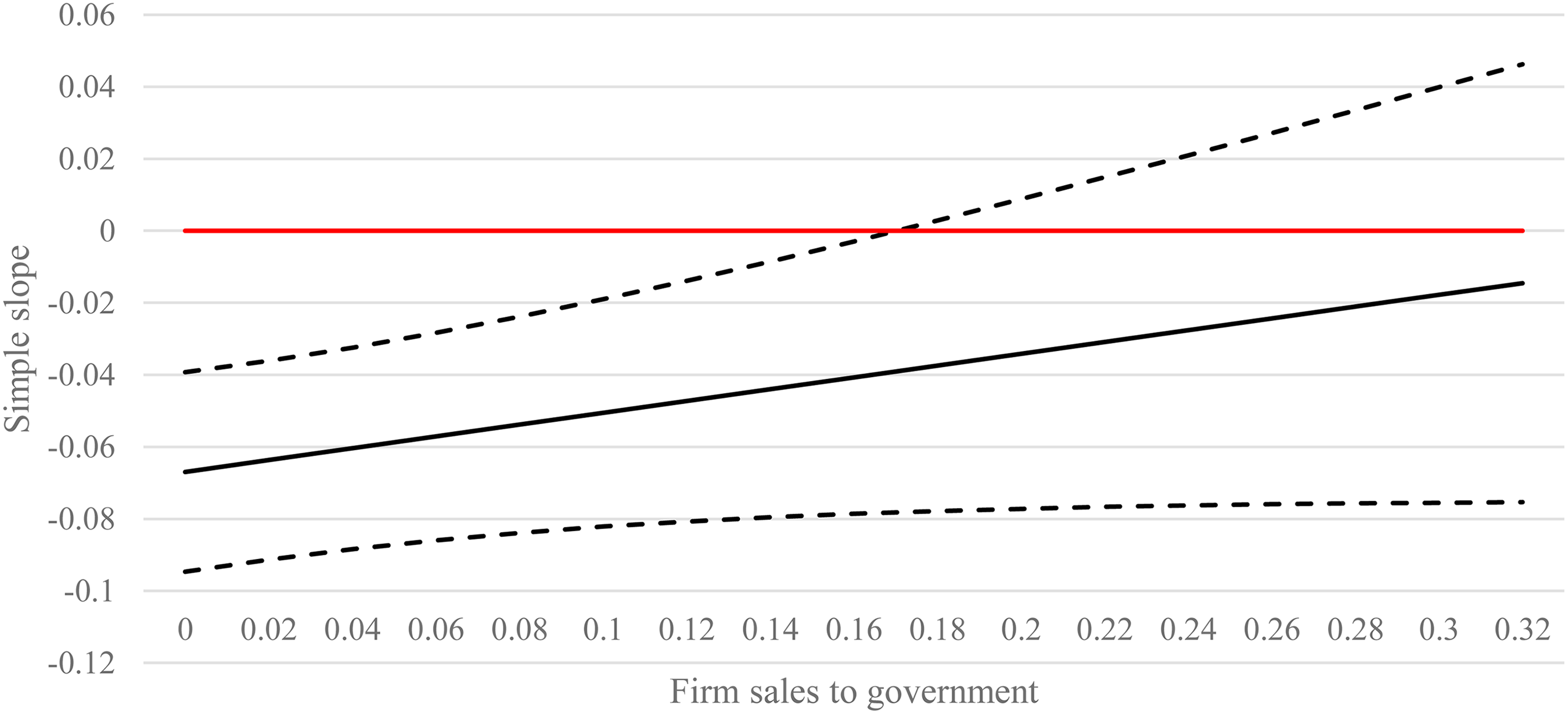

Johnson-Neyman Plots

To better understand how these moderating variables operate, we graphed their effects in Figures 2 to 4 using the Johnson-Neyman plots (Bauer & Curran, 2005; Johnson & Fay, 1950; Johnson & Neyman, 1936). The Johnson-Neyman plots have two dimensions. The x-axis depicts a particular moderating variable, starting from the minimum value to the maximum. The y-axis shows the marginal effect of an independent variable on a dependent variable (dy/dx), which in our case is the marginal influence of government corruption on firms’ CSR. For each plot, we use four lines to show the moderating effect: a black solid line illustrates the marginal effect of an independent variable on a dependent variable; two dash lines demonstrate the 95% confidence interval for each marginal effect; and a red solid line specifies the zero. Hence, any marginal effect whose confidence intervals contain zero would suggest that the moderating variable on that point is not statistically significant. Alternatively, a marginal effect whose confidence intervals exclude zero indicates that the moderating variable on that point is statistically significant.

Johnson-Neyman Plot for the Moderating Effect of Political Risk on the Relationship Between Government Corruption and Corporate Social Responsibility

Johnson-Neyman Plot for the Moderating Effect of Firm Performance on the Relationship Between Government Corruption and Corporate Social Responsibility

Johnson-Neyman Plot for the Moderating Effect of Firm Sales to Government on the Relationship Between Government Corruption and Corporate Social Responsibility

Figure 2 shows that the marginal impact of government corruption on firms’ CSR is not only negative but also strengthened by firm political risk, as the points on the solid black line become smaller when the moderating variable takes higher values. Meanwhile, Figure 2 demonstrates that the moderating effect of government corruption is significant, starting from the minimum value of firm political risk (−0.71) to the maximum (2.54) as the red line and the upper level of the confidence interval intersect at the top left corner of the graph. Thus, Figure 2 indicates that firm political risk magnifies the negative relationship between government corruption and firms’ CSR. Similarly, Figure 3 suggests two points. First, the marginal effect of government corruption is not constant across all values of financial performance. Second, the slope of the marginal effect is negative, meaning that the effect of government corruption becomes more pronounced as firm performance increases, supporting Hypothesis 3. Last, Figure 4 depicts that while firm sales to government can weaken the relationship between government corruption on firms’ CSR, this effect holds only when the moderating variable has the value below 0.18. Thus, when firms heavily rely on the government for their businesses, the instrumental motive of CSR will be less potent. One explanation is that a strong dependence on government may mute the instrumental value of firm CSR.

Supplementary Analyses

Apart from the aforementioned tests, we have performed the following supplementary analyses.

Alternative Government Corruption Measures

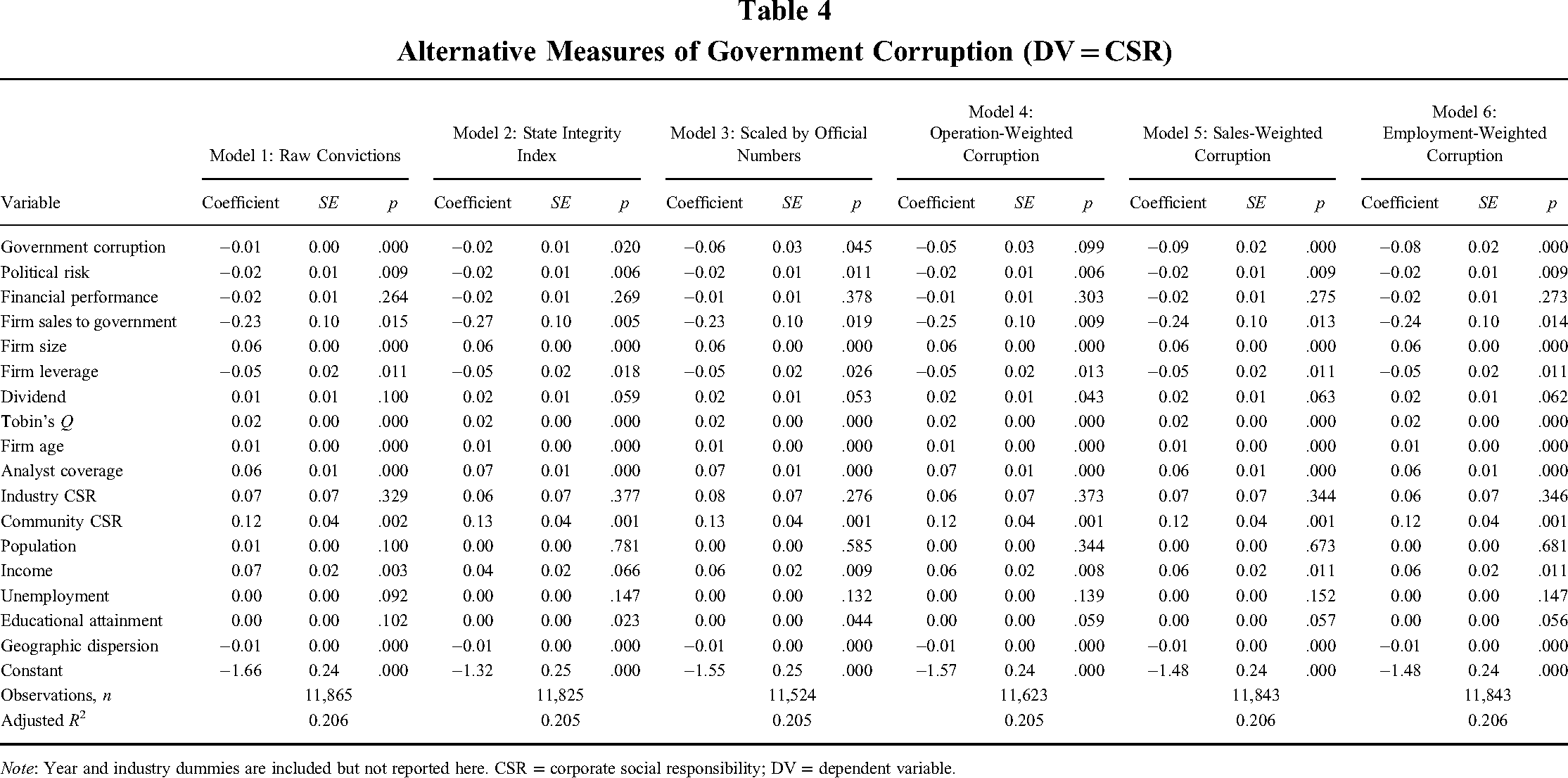

Here we show the robustness of the results by utilizing six alternative measures of government corruption. First, we used the raw convictions within each US federal judicial district as an alternative measure. Second, we employed as another measurement the state integrity index—an indicator developed by Global Integrity, a nonprofit organization that assesses the effectiveness of anticorruption campaigns initiated by US states.5 Third, because a district with more government officials could have more officers convicted, we scaled the number of corruption convictions by the number of government officials within a region. Finally, we constructed three weighted-average measures of government corruption capturing firms’ overall exposure to government corruption. Specifically, we used a firm's operations (i.e., affiliates or subsidiaries), sales, and employment in different states as weights to calculate the firm's overall exposure to government corruption. For a given year t, we multiplied the proportion of a firm's operations within each state k by the government corruption within state k and then summed all values to generate a composite index of operation-weighted corruption. We applied this procedure to compute the sales- and employment-weighted government corruption measures. As Models 1 and 2 of Table 4 show, government corruption as measured by raw convictions and the state integrity index are inversely related to CSR (β = −0.01, p = .000, and β = −0.02, p = .020, respectively). In parallel, the measure using convictions scaled by the number of government officials is negatively correlated with CSR (β = −0.06, p = .045, in Model 3). The coefficient of operation-weighted corruption is negative (β = −0.05, p = .099). The coefficients of sales- and employment-weighted corruption are negative and significant (β = −0.09, p = .000, and β = −0.08, p = .000). These results are consistent with the main findings.

Alternative Measures of Government Corruption (DV = CSR)

Note: Year and industry dummies are included but not reported here. CSR = corporate social responsibility; DV = dependent variable.

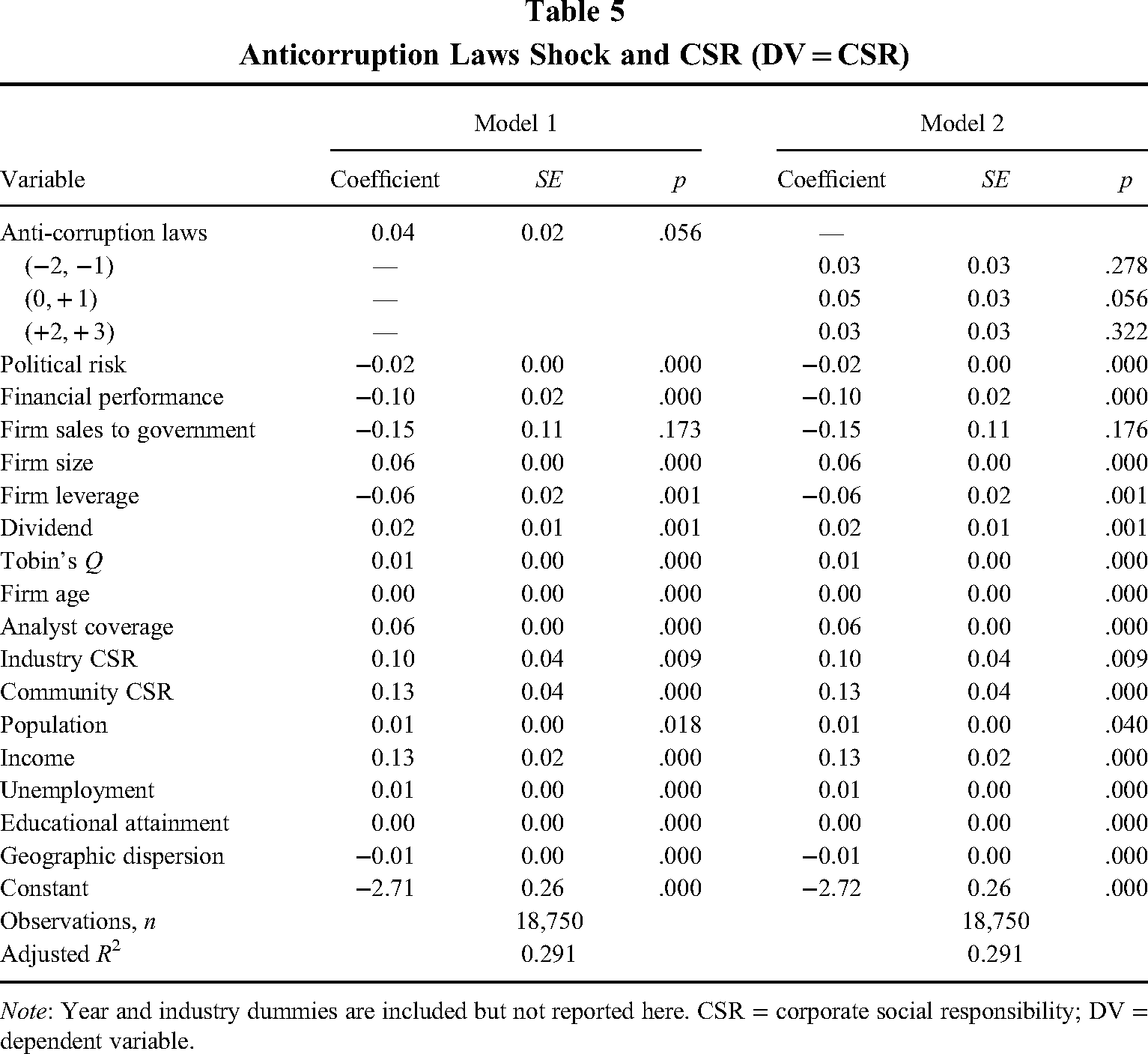

Anticorruption Laws as a Shock

We further qualify the causal relationship between government corruption and CSR by exploiting anticorruption laws as a shock. While US firms are forbidden from bribing foreign governments (i.e., the 1977 Foreign Corrupt Practices Act), domestic regulations designed to curb bribery have not been imposed. An anticorruption law (HB 1690) was enacted in Texas in September 2015 and Florida in October 2016. The implementation of this law creates an opportunity to examine our core argument. We anticipate that the passing of this regulation will ameliorate government corruption and affect firms’ CSR. To test this effect, we generated an indicator variable, anticorruption laws, that took the value of 1 for the year that an anticorruption law was implemented and the subsequent years and 0 otherwise. We decomposed the law enactment into three periods to explore the dynamics of this effect: anticorruption laws (−2, −1), which equals 1 for the time 2 years before the enactment and 0 otherwise; anticorruption laws (0, 1), which equals 1 for observations during the implementation year and 1 year following and 0 otherwise; and anticorruption laws (2, 3), which equals 1 for the time during the second and third years following the enactment and 0 otherwise. As Model 1 of Table 5 shows, the coefficient of anticorruption law is positive and marginally significant (β = 0.04, p = .056), suggesting that the implementation of anticorruption laws boosts a firm's motivation to be socially engaged. Model 2 further indicates that CSR does not increase before the adoption of an anticorruption law but rather after the anticorruption law is enacted—an effect that takes place immediately. These findings suggest that government corruption does affect firm social engagement.

Anticorruption Laws Shock and CSR (DV = CSR)

Note: Year and industry dummies are included but not reported here. CSR = corporate social responsibility; DV = dependent variable.

Validating the Instrumental Mechanism

We performed two additional tests examining if the CSR engagement varied across regions with different levels of government corruption. Prior studies have suggested that government corruption undermines firm operations and performance (e.g., Blackburn & Forgues-Puccio, 2007; Xu et al., 2019). Brown, Smith, White, and Zutter (2019) show that corrupt officials expropriate firm resources, impairing firm value. Government corruption also decreases firms’ research and development (R&D) expenditures (Ellis et al., 2020). Hence, we predict that if a firm spends more on CSR, corrupt officials may then seek opportunities to extract more rent. Following this view, we conjecture that increasing CSR could exacerbate the negative effect of government corruption on firm value and R&D expenditures.6 According to Table 6, government corruption is negatively related to Tobin's Q and R&D expenditure (β = −0.07, p = .032, and β = −0.01, p = .000, respectively). The negative effect of government corruption is more pronounced for firms with high CSR. Thus, increasing CSR could amplify the negative effect of government corruption on firm value and R&D.

Effect of Government Corruption on Firm Value and R&D Investment: Does CSR Matter?

Note: Year and industry dummies are included but not reported here. CAPEX = capital expenditures; CSR = corporate social responsibility; DV = dependent variable; MB = market-to-book ratio; PP&E = property, plant, and equipment; R&D = research and development.

Boundary Conditions of the Normative Motive

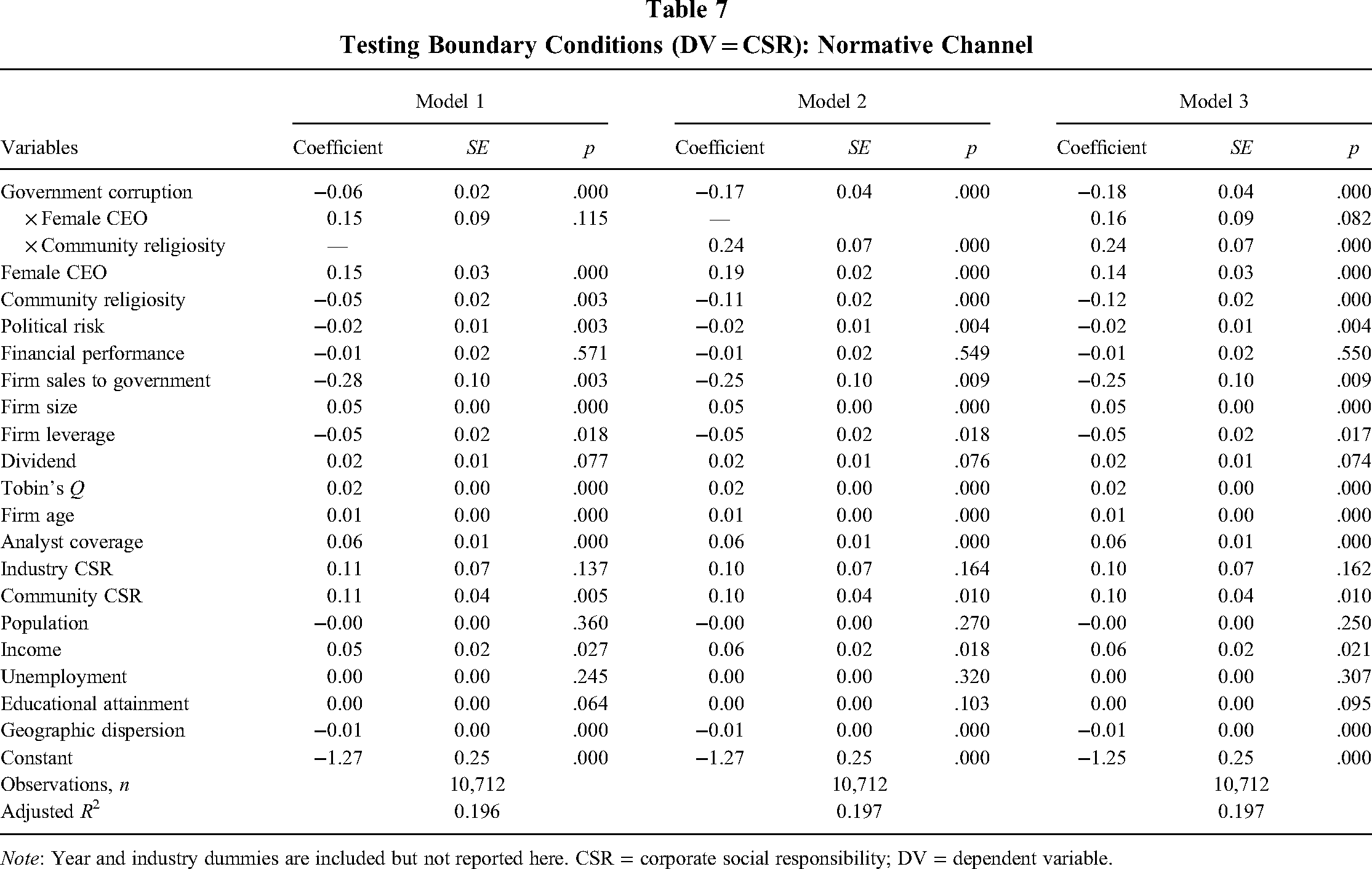

While our focus in this study is instrumental motive, it is helpful to know whether the normative motivation varies according to the level of moral values of firms. Here we used female CEOs and firms headquartered in more religious communities as two boundary conditions to test the normative motive. First, females are more communal, and males are more aggressive while emphasizing achievements in their decisions (Eagly & Wood, 1991). Hence, firms led by female executives tend to exhibit fewer unethical acts (Cumming, Leung, & Rui, 2015) and engage more in CSR (Borghesi, Houston, & Naranjo, 2014). Second, community religiosity denotes the degree that a given region has residents who adhere to particular religions (Lewis & Maltby, 1995). In communities with more religious adherence, firms and their executives are strongly influenced by such religious views and will be more prone to address stakeholders’ needs (Husted et al., 2016; Marquis et al., 2007). The religious community can heighten firms’ normative motive by prompting the firms to embrace the broader community members in their operations. We consequently expect that the influence of local government corruption on firm CSR through decreasing the normative value is weakened for firms led by female CEOs or headquartered in highly religious communities. Table 7 presents the results. In Model 1, the interaction of government corruption and female CEO is positive, even though it is insignificant (β = 0.15, p = .115). In Model 2, we find that the interaction of government corruption and community religiosity is positive and significant (β = 0.24, p = .000). These findings are in line with our expectations.

Testing Boundary Conditions (DV = CSR): Normative Channel

Note: Year and industry dummies are included but not reported here. CSR = corporate social responsibility; DV = dependent variable.

Subsample Analysis

We have performed a set of subsample tests to ensure the robustness of our findings. First, we excluded firms headquartered in the District of Columbia because its corruption is the highest and could drive our results. For a similar reason, we removed firms headquartered in Delaware because companies may be attracted by Delaware's quality of courts and judges. Meanwhile, to address concerns that a firm's CSR engagement may be affected by other states’ corruption levels, we restricted our sample to firms with employees or sales only in their headquartered states (i.e., nondiversifying firms). As summarized in Appendixes C and D online, we find that our results are robust in these analyses.

Finally, we performed additional tests: (1) controlling for firm slack resources and firm lobbying expenses to address the concern that firms use political influence in countering potential government intrusions, (2) using alternative measures of CSR (e.g., Asset4 CSR rating), (3) applying different fixed effects (industry-year fixed effect, industry and state-year fixed effect, and industry-state-year fixed effect), and (4) clustering standard errors at different levels (by industry, firm, firm and district, as well as district and year). The results, which are summarized in Appendixes E to H online, are largely consistent with our main findings.

Discussion

The purpose of this study is to understand how government corruption influences firm CSR. Research on CSR and stakeholder management tends to focus on the positive reciprocity among stakeholders. While useful and crucial, this approach fails to recognize the possibility that some stakeholders may possess private intent to appropriate firms. In the present study, we highlight the possible self-seeking behaviors of the regulatory stakeholder—namely, government. We contend that as government corruption becomes prevalent, firms will consider the risk of social engagement high and the return low. At the same time, the widespread corruption practices can erode the moral foundation of the business community, encouraging social actors to focus on their own matters. Because officials’ self-seeking behaviors can diminish a firm's instrumental and moral motives, we postulate that government corruption will hamper the firm's CSR. To better understand this main effect, we examine several contingencies related to the instrumental motive. In our supplementary analyses, we investigate contingencies pertinent to moral motive. Results based on a sample of US public firms provide support for our claim.

Our study makes two notable contributions. First, we contribute to the CSR literature by recognizing the effect of the self-seeking behavior by regulatory stakeholders on firms. While stakeholder theory has recognized that the interactions between a firm and relevant parties are the key to the firm's success, researchers tend to assume that social actors will always act upon good intent. The consequences of stakeholders’ inappropriate behaviors are thus unknown. In this study, we maintain that the potential self-interested behaviors by a particular stakeholder group—that is, government—can diminish a firm's social engagement. We contend that a high level of CSR commitment can make a firm more noticeable in the eyes of self-seeking officials, thus increasing the risk of CSR. At the same time, because corrupt officials are self-interested, they are unlikely to maintain the norms of fairness when interacting with a firm. To the extent that corruption diminishes the instrumental and moral motives, a firm is less likely to show much CSR in regions where government corruption is prevalent. Our arguments contribute to the CSR literature not only by recognizing the instrumental and moral motives but also by theorizing how the self-seeking behavior by a stakeholder group can harm, impair, and damage the foundation for CSR. By highlighting the corruption of the regulatory stakeholder and its impact on firms, we are able to observe the consequences when the reciprocity norms are not maintained, which enriches the stakeholder research.

Second, our study advances the CSR literature by examining boundary conditions that can alter the instrumental and moral value of social engagement. While scholars on CSR have proposed that firms can be motivated to support stakeholders due to instrumental and moral motives, what remains less clear are the conditions under which the instrumental and moral value of CSR will be more salient to firms. In this study, we investigate three contextual factors that can change the instrumental value of CSR. This not only complements prior research that focuses on the moral consequences of government corruption (Chantziaras et al., 2020; Ioannou & Serafeim, 2012; Luo, 2006) but also advances our understanding of CSR motivation.

In sum, our finding that government corruption diminishes firm CSR suggests that rent seeking by regulators may lead to an unintended consequence—namely, prompting a firm to dissociate itself from other stakeholders. As the firm undercuts its CSR, the decision will compromise the interests of stakeholders and decrease the welfare of members in the business community. On this basis, the cost of corruption is not limited to the focal firm. Instead, the cost could have a ripple effect on the business community as a whole. This spillover effect provides a new vantage to broaden the scope of the literature on CSR.

Our study has several limitations that provide opportunities for future directions. First, to investigate government corruption, we focused on the local regions of firms’ headquarters. Although firms’ headquarters play a pivotal role in strategic decisions (Menz, Kunisch, & Collis, 2015), firms may take actions to address conditions beyond their home regions (Sutton et al., 2021). Future research may examine whether governments in nonlocal regions would amplify or dampen the impact of local government on firm strategies. In parallel, firms are likely to have operations outside their home countries. Research has suggested that these firms could transfer their home region practices to overseas subsidiaries (Kostova & Roth, 2002) or vice versa (Jensen & Szulanski, 2004). We welcome scholars to examine the conditions under which the view held by the home country would be more or less receptive to subsidiaries. Studies investigating such questions can improve our understanding of firms operating within heterogeneous geographic markets.

Second, our study focuses on government corruption by recognizing officials’ private intent as a form of firm-state interaction. Beyond this, firms could cultivate government bonds via personal connections (Hillman, 2005) or political ties (Sun, Mellahi, & Wright, 2012). These relationships can improve firm operations (Cui, Hu, Li, & Meyer, 2018). It will be interesting to know whether firms’ nonmarket actions—such as political donations and social activism—alter the effect of government corruption on firm CSR.

Conclusion

This study investigates the effect of government corruption on CSR. Leveraging the instrumental view of CSR, we propose that the presence of a corrupt government may prompt firms to provide less stakeholder support, as the firms endeavor to reduce the likelihood of being targeted by corrupt officials. We also examine several boundary conditions that alter the proposed effect. Findings based on a sample of US public firms suggest that the exposure to government corruption diminishes firm CSR and that this effect varies by certain contingencies. Thus, the concern of being appropriated by government officials as the regulatory stakeholder group can spill over to undercut firms’ social engagement. This finding suggests that government corruption not only undermines the moral foundation of CSR but also impairs the instrumental value of social engagement via the risk-return rationale. We hope that our study can spur research further investigating the relationship between stakeholders and firm CSR.

Supplemental Material

sj-docx-1-jom-10.1177_01492063231195590 - Supplemental material for Government Corruption and Corporate Social Responsibility: An Instrumental Perspective

Supplemental material, sj-docx-1-jom-10.1177_01492063231195590 for Government Corruption and Corporate Social Responsibility: An Instrumental Perspective by Cuili Qian, David H. Weng, Louise Yi Lu, and Xuejun Jiang in Journal of Management

Footnotes

Acknowledgments

We thank associate editor Sali Li and two anonymous reviewers for their guidance and insights. We also appreciate the helpful feedback from Professor Taiyoung Kim, the seminar participants of Waseda University and Shenzhen University, as well as those from the research frontiers of corporate social responsibility at the University of Electronic Science and Technology of China.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.