Abstract

This study examines the influence of firms’ internal control weakness (ICW) reported under the Sarbanes-Oxley Act (SOX) on their subsequent divestiture decisions and the performance of these decisions. We argue that following ICW disclosure, firms are inclined to pursue corporate divestitures because such divestitures can reduce organizational complexity and help remedy firms’ ICW. We also propose that the positive influence of ICW disclosure on divestitures is stronger when a firm has recently appointed a CEO but weaker when there is a higher prevalence of ICW within the industry. Furthermore, we investigate the dual performance implications of divestitures following ICW disclosure. Although these divestitures, compared to divestitures not following ICW disclosure, are associated with higher stock market performance, they are also associated with slower sales growth for firms’ core businesses. We present empirical evidence that supports our arguments using a sample of S&P 1500 firms from 2003 to 2020. This study advances corporate strategy research by highlighting the role of ICW in shaping corporate divestiture decisions and documenting the multifaceted performance implications of such divestitures.

Introduction

Internal control, as a subset of organizational control processes (EI Mahdy & Thiruvadi, 2014), encompasses a firm’s processes and procedures aimed at “ensuring the accuracy and completeness of the accounting records that underpin financial statements and their related disclosures” (Krishnan, 2005: 1). Section 302 of the Sarbanes-Oxley (SOX) Act requires management teams to evaluate the effectiveness of a firm’s internal control (Securities and Exchange Commission [SEC], 2003) and disclose any identified internal control weakness (ICW) to investors. Existing research suggests that a key cause of ICW is high organizational complexity (Bedard & Graham, 2014; Ge & McVay, 2005; Schneider, Gramling, Hermanson, & Ye, 2009), which often arises from interdependencies among diverse business operations (Doyle, Ge, & Mcvay, 2007; Zhou, 2011, 2013; Zhou & Wan, 2017).

The disclosure of ICW often carries significant negative implications for firms (Chalmers, Hay, & Khlif, 2019), including problematic operations and management, potential damage to their legitimacy, penalties from regulatory agencies, and adverse effects on interactions with stakeholders (Beneish, Billings, & Hodder, 2008). Thus, following an ICW disclosure, firms and their managers are motivated to remediate the weakness (Haislip, Masli, Richardson, & Sanchez, 2016; Haislip, Masli, Richardson, & Watson, 2015). In a separately evolving literature, management scholars have documented that firms frequently undertake corporate divestitures to reduce the organizational complexity associated with managing a large portfolio of businesses (Karim, 2006; Shimizu & Hitt, 2005). Corporate divestitures involve adjustments to a firm’s ownership and business portfolios through sell-offs, carve-outs, and spin-offs of business units or the sale of corporate assets (Feldman, 2023; Vidal, 2021). Despite divestitures being an important and effective strategic action in reducing organizational complexity and potentially addressing ICW, management scholars have paid little attention to the role of ICW in shaping divestiture decisions.

This omission is surprising, as firms may actively remediate ICW through divestitures. For instance, in 2004, Goodyear Tire & Rubber Co. disclosed a material weakness in its internal controls. In 2005, the firm sold its profitable adhesives resins business to a French company. CEO Robert Keegan commented that this unit was not the core of the firm’s main tire businesses and that selling it helped simplify the organization and allowed it to refocus on its tire businesses. 1 More recently, in its 2019 annual report, Stericycle, Inc., a U.S.-based business-to-business services company specializing in compliance-based solutions for health, safety, and environmental protection, disclosed its ICW related to IT controls and its Environmental Solutions operation. In its 2020 annual report, Stericycle reported two remediation actions: formalizing the IT Global Risk and Compliance office responsibilities within the IT function and divesting Environmental Solutions. The report noted, “As disclosed in Form 8-K dated April 6, 2020, the Company completed the divestiture of the Environmental Solutions disposal group. As a result of this divestiture, the material weaknesses impacting the Company as of December 31, 2019 . . . no longer impacted the Company subsequent to April 6, 2020.”

Given the importance of internal control to organizations and the anecdotal evidence, this study investigates the effects of a firm’s ICW disclosure on its divestiture decisions and the performance implications of such decisions. We first propose that following ICW disclosure, firms may undertake divestiture activities to reduce organizational complexity and rectify their ICW because divestitures represent one of the most effective means of reducing interdependence, streamlining operations, and thus addressing ICW (Brauer, 2006). We also contend that the positive impact of ICW disclosure on divestitures is more pronounced when the firm has recently appointed a new CEO because new CEOs are less likely to be held accountable for the initial diversification into the divested business (Chiu, Johnson, Hoskisson, & Pathak, 2016) but are strongly motivated to restore organizational legitimacy (Gomulya & Boeker, 2014). However, the positive influence of ICW disclosure on divestitures becomes weaker when such disclosure is prevalent within the industry because the prevalence of ICW in the industry attenuates the damage to the focal firm’s reputation and legitimacy, consequently diminishing its motivation to address ICW through divestitures.

Furthermore, we investigate the dual performance implications—financial market performance and product market performance—of divestitures following ICW disclosure versus divestitures that do not follow such a disclosure. We argue that divestitures following the disclosure of ICW yield dual performance outcomes. On the one hand, compared to divestitures not occurring after ICW disclosure, those following ICW disclosure are linked to higher stock market performance for the divesting firm. This outcome reflects that divestitures create a favorable impression as they help fix ICW, leading investors to respond positively to the divestiture announcement after ICW disclosure. On the other hand, divestitures following ICW disclosure might result in slower growth for the divesting firm’s core business. To reduce organizational complexity and resolve ICW concerns, a firm may initiate divestitures of businesses that enjoy synergy with its core operations. This, in turn, may diminish some of the benefits stemming from this interdependence, ultimately affecting the growth of the firm’s core businesses (Anand, 2011; Penrose, 1959). We find robust empirical support for our theoretical predictions by analyzing a sample of S&P 1500 firms from 2003 to 2020.

This study makes two main contributions to the literature. First, it extends corporate strategy research by highlighting the significant role of firms’ ICW in corporate divestiture decisions, thus enriching our understanding of the antecedents and consequences of corporate divestitures. Despite internal control being a crucial form of organizational control that significantly shapes firm behavior and performance, this topic has remained understudied by management scholars. Our study suggests that firms may undertake divestitures in response to ICW disclosure, providing new insights into the drivers of divestiture decisions. In addition, our examination of the financial and product market performance outcomes of divestitures following ICW disclosure, compared to those not following ICW disclosure, reveals nuanced performance implications of divestitures. Although divestitures following ICW disclosure are generally viewed more favorably by investors, they may potentially erode a firm’s competitiveness by diminishing the synergies with its core businesses. This examination adds to the evolving body of research that unveils the inconsistent performance consequences of divestitures (Feldman, 2014; McKendrick, Wade, & Jaffee, 2009; Vidal & Mitchell, 2018).

Second, this study contributes to the internal control literature by extending its prevailing focus on tactical responses and stakeholder reactions to ICW disclosure (Chalmers et al., 2019; Hammersley, Myers, & Shakespeare, 2008). By examining divestitures as a strategic response to ICW disclosure, our study highlights the potential drawbacks of undertaking divestitures following ICW disclosure (i.e., declining sales growth in the core business) and broadens our understanding of the unintended consequences of ICW disclosure.

Literature Review

Internal Control Weakness and Mandated Disclosure

An important type of organizational control, internal control involves the management of organizational activities in accordance with established policies and plans (Child, 1973). It is designed to assess risks, prevent fraud, and ensure the accuracy and completeness of information in financial statements and disclosures. As financial statements and disclosures include a great amount of information about management, organization, operations, IT technology, and many other important dimensions within a firm, internal control concerns not only finance and accounting but also organization and management (Chalmers et al., 2019; Haislip et al., 2016; Paletta & Alimehmeti, 2018; Pandey, Andres, & Kumar, 2022).

After a series of highly publicized corporate fraud cases (e.g., Enron and WorldCom), the U.S. Congress enacted the SOX Act in 2002 to improve the reliability of the information in financial disclosure and to ensure that investors are informed about weaknesses in firms’ internal control systems. Section 302 of the SOX Act requires management to assess the operating effectiveness of the firm’s internal controls and the accuracy of disclosure, report their assessment results, and explain any crucial changes in these controls since the last Form 10-K or Form 10-Q filing (SEC, 2003). Section 404 of the SOX Act requires a firm’s independent auditor to issue a separate report stating its opinions on the effectiveness of the firm’s internal controls and management’s evaluation of the effectiveness of internal controls.

If firms identify any significant ICWs, they must disclose those weaknesses to the public in their filings. An ICW disclosure poses an immediate threat to a firm (Hammersley et al., 2008). It suggests that the firm’s information in public financial reports is biased and/or unreliable, indicating not only significant deficiencies in accounting and finance functions but also poor general management of the firm. Consequently, stakeholders will doubt the firm’s legitimacy and adjust their assessment of the firm downward.

In addition, managers are generally held responsible for the presence of ICW (Wu & Tuttle, 2014). Specifically, the SOX Act stipulates that managers have legal responsibility for the accuracy and completeness of the information included in the firm’s public filings and for the effectiveness of its internal control (Hawkins, 2006; Wu & Tuttle, 2014). Therefore, managers must disclose any weakness they identify and do so in a timely manner. However, managers are not held legally liable for the presence of ICW. In addition, given that the causes of such weakness are under the control of the firm’s managers (Ashbaugh-Skaife, Collins, & Kinney, 2007; Ge & McVay, 2005), managers are required to report the remediation plans for the disclosed ICW. The filing dates of quarterly and annual reports to regulators are often considered the deadlines for addressing ICW.

Existing research, particularly in accounting, has devoted much attention to unpacking the antecedents of ICW, such as organizational complexity, rapid organizational changes, poor investment in internal control, and management incentives (Ashbaugh-Skaife et al., 2007; Doyle et al., 2007). It has also investigated the consequences of mandatory ICW disclosure and suggested that stakeholders may react negatively to firms’ ICW disclosure (Hammersley et al., 2008). For example, ICW disclosure may lead to stock price declines (Beneish et al., 2008), increased costs of capital (Ashbaugh-Skaife, Collins, Kinney, & Lafond, 2009) and debt (Dhaliwal, Hogan, Trezevant, & Wilkins, 2011), reduced analyst confidence in firms’ financial statements (Asare & Wright, 2012), and tighter monitoring by lenders (Costello & Wittenberg-Moerman, 2011).

More recent research has departed from the exclusive focus on stakeholder reactions to mandatory ICW disclosure and instead examined the influence of ICW on firms’ investment decision outcomes. For instance, Cheng, Dhaliwal, and Zhang (2013) found that firms with ICW are associated with low investment efficiency due to the potentially high information asymmetry within the firm. Similarly, some research (e.g., Darrough, Huang, & Zur, 2018; Harp & Barnes, 2018) suggests that firms with ICW tend to make suboptimal acquisition decisions, relying on poor-quality information generated by ineffective internal control. Consequently, acquisitions by firms with ICW are associated with poorer performance outcomes than those by firms without ICW.

Despite the extensive research on ICW in other domains, the broader management field has not paid sufficient attention to this crucial phenomenon. As a result, our understanding of how ICW impacts firms’ strategic decisions and outcomes remains limited. Although divestitures are recognized as an important and effective strategic action for reducing organizational complexity (a primary driver for ICW), management scholars have generally overlooked the impact of ICW on divestiture decisions.

Antecedents and Performance Consequences of Divestitures

Antecedents

Divestitures are high-impact strategic actions (Brauer, 2006). Prior studies have devoted much effort to understanding the economic explanation for firm divestitures. For example, some studies have suggested that firms may undertake divestitures to respond to industry-level factors, such as slow industry growth, fierce competition, and threats to their competitive position (Berry, 2010; Chatterjee, Harrison, & Bergh, 2003; Feldman, 2014; Lee & Madhavan, 2010). Other studies have investigated firm-level drivers of divestitures, including business units’ poor performance or poor fit with the overall corporate strategy (Brauer, 2008; Capron, Mitchell, & Swaminathan, 2001; Shimizu, 2007), misallocation of corporate resources (Hoskisson & Johnson, 1992; Karim, 2006; Karim & Mitchell, 2004), and corporate governance issues related to disciplining managers using boards of directors, CEO duality, and managerial ownership (Donaldson & Lorsch, 1983; Lant, Milliken, & Batra, 1992; McNamara, Moon, & Bromiley, 2002; Sanders, 2001). These studies collectively highlight the rationale of improving corporate economic efficiency underlying divestitures, explicitly or implicitly pointing to performance considerations as one fundamental driver for firm divestitures.

Despite the prominence of the economic explanation for firm divestitures, other scholars have highlighted the impact of government regulators on divestitures (e.g., Filatotchev, Buck, & Zhukov, 2000; Hoskisson, Johnson, Yiu, & Wan, 2001; Rajagopalan & Spreitzer, 1996). For example, firms tend to divest more business units when antitrust policies are tightened (Shleifer & Vishny, 1991) or when the proceeds from divestitures become tax-free (Hoskisson & Hitt, 1990). Also, firms tend to engage in more asset restructuring in response to industry deregulation policies (Hoskisson, Cannella, Tihanyi, & Faraci, 2004). Although these studies clearly underscore the important role of government regulators in divestitures, our understanding of noneconomic drivers influencing divestitures remains relatively limited (Brauer, 2006; Moschieri & Mair, 2008).

Performance consequences

Given their critical importance for firms, scholars have devoted significant attention to understanding the performance consequences of divestitures (see Brauer, 2006, for a review). Some studies have focused on the short-term performance implications, such as the stock market’s reaction to divestiture announcements. For instance, Feldman (2014) found that the divestiture of a firm’s legacy business is associated with higher stock market performance. Similarly, Chen and Feldman (2018) observed that activist-driven divestitures are more positively linked to stock market performance.

Another line of inquiry examined relatively long-term performance outcomes but yielded mixed findings. On the one hand, some studies report positive effects of divestitures on divesting firms’ performance. For instance, Montgomery and Thomas (1988) found that divestitures enhance the performance of divesting firms. Hoskisson and Johnson (1992) discovered that divesting firms experience an increase in performance two years after divestitures compared to nondivesting firms. Feldman, Amit, and Villalonga (2016) found that divestitures enhance the value of family firms. These positive performance effects reflect the idea that divestitures can enhance the economic efficiency of divesting firms. On the other hand, prior research has shown that divestitures can lead to decreased performance of divesting firms (Bergh, 1995; Hite & Owers, 1983; Wright & Ferris, 1997). More recently, Feldman (2014) found that the divestiture of a firm’s legacy business is associated with poor post-divestiture operating performance due to disruption of the firm’s remaining businesses.

Notably, some studies have attempted to reconcile the conflicting empirical evidence. For example, Markides (1995) highlighted the role of divestiture timing, suggesting that proactive divesting firms experience performance increases after divestitures, whereas reactive divesting firms experience the opposite effect. Pashley and Philippatos (1990) proposed that the effect of divestiture on firm performance may depend on the life-cycle stage of the divesting firm.

Despite the significance of internal control to firms, the current literature has yet to consider the performance implications of divestitures following ICW disclosure. This study first investigates the impact of a firm’s ICW disclosure on its divestiture decisions. It then explores the dual performance implications—financial market and product market performance—of divestitures following ICW disclosure versus those not following such disclosure.

Theory and Hypotheses

ICW Disclosure and Divestitures

We propose that following ICW disclosure, firms are likely to initiate divestitures of assets. This is because divestitures can serve as effective remedial measures for ICW by simplifying and streamlining the firm’s portfolio of businesses. Among the various factors contributing to ICW, organizational complexity—defined as “a large number of parts that interact in a nonsimple way” (Simon, 1962: 468)—has been identified as the primary precursor of ICW (Bedard & Graham, 2014; Schneider et al., 2009). Research suggests that organizational complexity arises primarily from high interdependencies among business units, including frequent internal transactions and extensive sharing activities among these units (Larsen, Manning, & Pedersen, 2013; Levinthal, 1997; Rawley, 2010; Zhou, 2011). Such an elevated level of interdependencies among business units increases the necessity for and the difficulty of coordination, thereby leading to ICW. Organizational complexity can also complicate the identification of ICW causes and solutions.

Divestitures can reduce the number of business units, thereby diminishing interdependencies and the need for coordination among multiple businesses (Decker & Mellewigt, 2012; Hoskisson & Turk, 1990; Keats & Hitt, 1988). Following divestitures, the level of interdependency and coordination requirements among business units decrease, leading to enhanced communication efficiency and more effective joint decision-making within the firm (Bosse, Harrison, & Hoskisson, 2022; Simon, 1991). In the context of ICW, divestitures can contribute to an improved control environment and strengthened risk assessment. These gains then enhance the accuracy and completeness of information in the firm’s public statements and disclosures, facilitate the mitigation or remediation of ICW, and can even prevent ICW from recurring in the future. Moreover, divestitures have the potential to assist firms in restructuring, refocusing, and expanding their core businesses (Hamilton & Chow, 1993). ICW may lead managers to assess whether a firm’s operations have become overly complex and may have exceeded the efficient scale or scope. Divestitures can aid firms in downsizing or narrowing their focus, reducing complexity, and realigning their remaining operations with their core businesses (Dranikoff, Koller, & Schneider, 2002).

Despite being an effective remedy, divestitures are not the only response to ICW. Firms may also adopt tactical alternatives, such as hiring new CFOs or accountants, upgrading IT systems, and amending accounting and operational practices. In contrast to tactical alternatives, divestitures, as a strategic approach, entail significant reallocation of firm resources and changes in structures (Karim, 2006). Nevertheless, divestitures offer distinct advantages over tactical alternatives as a remedy after ICW disclosure. ICW disclosure can jeopardize a firm’s and its managers’ reputation and legitimacy (Haislip et al., 2016, 2015). It can also result in diminished confidence and unfavorable reactions from investors (Beneish et al., 2008). Consequently, firms face considerable pressure to respond promptly to their ICW disclosure. In contrast to tactical approaches, divestitures constitute major strategic decisions with profound implications for firm competitiveness (Mulherin & Boone, 2000) and thus garner significant attention from firm investors. Investors are likely to perceive firms initiating divestitures after ICW disclosure as proactively addressing the weakness. Additionally, divestitures can generate cash flows, enabling firms to increase their investments in internal control measures. These factors contribute to improving investors’ perception and impression of firm management (Pollock, Rindova, & Maggitti, 2008), which helps restore the firm’s reputation and legitimacy after the harm resulting from ICW disclosure.

One might wonder if divestitures are an effective remedy for ICW, and if ICW disclosure jeopardizes a firm’s reputation and legitimacy, why do firms wait to divest until after ICW disclosure? This hesitation can be attributed to the aforementioned wide-ranging implication of divestitures and the fact that divestitures of business assets often signify prior (possibly poor) diversification decisions by firms (McNamara et al., 2002). As a result, managers generally exhibit reluctance toward undertaking divestitures due to their extensive implications (e.g., Chiu, Pathak, Hoskisson, & Johnson, 2022). In other words, firms may refrain from proactive divestitures to mitigate ICW before its disclosure. Combining these arguments, we hypothesize that:

Hypothesis 1: A firm’s disclosure of internal control weakness is positively associated with its subsequent divestiture activities.

The Moderating Role of Divestiture Motivation

As previously discussed, despite being an effective remedy for ICW, firms and their managers are not always motivated to undertake divestitures in response to ICW disclosure. In this section, we examine factors influencing firms’ motivation to rectify ICW through divestiture. Specifically, we explore two moderators influencing the motivation to use divestitures as a remedy for ICW: the presence of a newly appointed CEO in the firm and the prevalence of ICW in the industry.

Newly appointed CEOs

We argue that the presence of a newly appointed CEO will strengthen the relationship proposed in Hypothesis 1, as such CEOs are more inclined to pursue divestitures in response to firms’ ICW disclosure compared to their more entrenched counterparts. This inclination stems from the new CEOs’ motivation to create a positive impression among investors in their new leadership roles (Westphal & Graebner, 2010). The salience of ICW disclosure provides a strategic opportunity for these CEOs to demonstrate their managerial competence and value (Chen, Luo, Tang, & Tong, 2015). As such, these executives are more likely to be proactive in addressing ICW and tend to prioritize divestitures over other tactical solutions. The high visibility associated with divestitures aligns with new CEOs’ tendency to opt for bold, assertive moves to impress investors and make a strong impact early in their tenure. In addition, the cash flows generated from divestitures provide new CEOs with a means to increase firm revenues and potentially bolster investment in internal control measures.

Furthermore, divestitures of assets often imply that the initial acquisition of these assets was potentially a mistake. Some entrenched CEOs might prefer to retain underperforming assets rather than divest them because the divestitures of these businesses could be perceived as an admission of past errors (Markides & Singh, 1997; McNamara et al., 2002). However, this would not be a concern for new CEOs because the assets slated for divestitures were typically established under the leadership of their predecessors. Even if investors perceive divestitures as an acknowledgment of past mistakes, they are likely to attribute these mistakes to the previous CEO rather than the current one. Additionally, new CEOs typically have limited emotional attachment to the assets or divisions to be divested (Hayward, Shimizu, Antonio, & Oats, 2006; Ross & Staw, 1993). Thus, new CEOs are likely to resort to divestitures as a remedial measure and view them as a tool to rebuild the firm’s reputation among investors after ICW disclosure.

In contrast, long-tenured CEOs might not be motivated to address ICW through divestitures. This reluctance may stem from the fact that these CEOs could have been directly involved in the diversification decisions that led to the ICW, and divestitures could be perceived as an admission of poor strategic decisions (McNamara et al., 2002). In addition, there tends to be a lower level of information asymmetry between long-tenured CEOs and investors. As a result, these CEOs may shy away from drastic strategic actions such as divestitures, which could otherwise be leveraged to foster positive impressions among investors following the ICW disclosure. Thus, we predict:

Hypothesis 2: The relationship between a firm’s disclosure of internal control weakness and subsequent divestiture activities is stronger when the firm has a newly appointed CEO.

Prevalence of ICW among peers

We also argue that the prevalence of ICW among industry peers weakens the relationship proposed in Hypothesis 1. The occurrence of ICW among industry peers mitigates the damage to the focal firm’s reputation and legitimacy resulting from its ICW disclosure. This, in turn, diminishes the firm’s tendency to pursue divestitures as a remedial measure.

Research suggests that an object receives more attention and becomes more salient when it stands out relative to its peers (Fiske & Taylor, 1991; Jones & McGillis, 1976). This phenomenon extends to the firm level, where, for example, a firm involved in misconduct attracts less attention and is less salient when more industry peers engage in similar wrongdoing (Zavyalova, Pfarrer, Reger, & Shapiro, 2012). In the context of ICW, when a greater number of industry peers experience ICW, the focal firm with ICW becomes less conspicuous. Investors may attribute the cause of ICW to more general factors, such as the industry environment, rather than specific mistakes by firm management. Consequently, they may be more forgiving and inclined to give firm management the benefit of the doubt. In addition, when ICWs are widespread among industry peers, the management team of the focal firm is also likely to distance itself from the firm’s ICW and attribute these issues to broader factors. Therefore, a firm may not experience substantial damage to its reputation and legitimacy following ICW disclosure if many of its industry peers make ICW disclosures.

When firms do not face an immediate need to improve their reputation and legitimacy, they are more inclined to either abstain from responding or opt for tactical solutions to ICW. Indeed, resorting to divestitures to address ICW and cultivate a favorable impression among investors may carry considerable costs. For instance, divestitures may cause the firm to incur substantial financial costs, including transaction fees, legal expenses, and costs associated with separating business units (Berry, 2013). Moreover, divestitures could result in the loss of economies of scale previously enjoyed when operating as a larger entity, leading to higher per-unit costs in the remaining business units and adversely impacting overall efficiency and profitability (Feldman, 2014). In addition, as divestitures can be perceived as an admission of past poor diversification decisions, firms may refrain from using them as remedial measures (McNamara et al., 2002). Consequently, unless firms face a pressing need to rectify their ICW—a situation less likely when ICWs are prevalent across the industry—they may either opt not to respond or choose tactical solutions, such as hiring additional qualified personnel over strategic ones, such as divestitures, to address their issues. Hence, we hypothesize that:

Hypothesis 3: The relationship between a firm’s disclosure of internal control weakness and subsequent divestiture activities is weaker when there are more industry peers disclosing internal control weakness.

Divestitures Following ICW Disclosure and Stock Market Performance

We argue that investors will tend to react more favorably to divestiture announcements following an ICW disclosure than those not following such a disclosure. When a firm announces a divestiture after disclosing ICW, investors are likely to view the divestiture as the firm’s earnest effort to address its problems. These divestitures also signal to the market that the firm has been proactive in identifying and resolving the root causes of the ICW. Furthermore, such an announcement suggests that managers have opted for strategic actions rather than tactical solutions. Additionally, divestitures can significantly streamline internal coordination within firms, reduce organizational complexity, and facilitate the restructuring and refocusing of businesses, allowing for effective and efficient remediation of ICW. Investors may, therefore, perceive the business refocusing as enhancing the firm’s competitiveness and prospects. With the expected cash flow from divestitures, investors can anticipate increased firm revenue, at least in the short term.

In contrast, divestitures that do not follow an ICW disclosure can present challenges for investors who are trying to discern the true motive behind the decision and assess its long-term value (Brauer & Wiersema, 2012; Schijven & Hitt, 2012). Divestitures often involve a high level of ambiguity and lack of transparency regarding their value creation prospects and the firm’s underlying motives (Brauer & Wiersema, 2012; Lee & Madhavan, 2010). Whereas some divestitures are motivated by a desire for long-term value creation, others may be a response to poor cash flow, unpromising prospects, incongruence among business units, private managerial interests, or past misguided acquisition decisions (Brauer, 2006; Haynes, Thompson, & Wright, 2003). Firms rarely disclose the underlying motives for their divestiture decisions in their announcements; they may even release unrelated positive news simultaneously to bolster investor perceptions of divestitures about which they are not confident (Gamache, McNamara, Graffin, Kiley, Haleblian, & Devers, 2019). Consequently, investors may adopt a relatively conservative stance toward divestitures lacking a clear motive. Overall, investors tend to react more favorably to divestiture announcements following an ICW disclosure than those not following such disclosure. These arguments lead to the following hypothesis:

Hypothesis 4: Relative to other divestitures, divestitures following a firm’s disclosure of internal control weakness are associated with a more positive stock market reaction upon divestiture announcement.

Divestitures Following ICW Disclosure and Divesting Firms’ Core Business Growth

Although divestitures following a firm’s ICW disclosure can elicit positive reactions from investors, they can also disrupt some of the synergy arising from the interdependencies across the firm’s businesses. Firms engage in diversification to achieve synergy (Ahuja & Novelli, 2017; Arrow, 1974; Penrose, 1959). Specifically, they diversify into businesses that can share inputs, processes, or outputs and enable the firm to realize economies of scope (Rumelt, 1974). They may also diversify into businesses along the value chain in an effort to reduce transaction costs (Williamson, 1975). The interdependence among these units necessitates a high level of coordination, including communication, joint decision-making, and information processing, especially when dealing with complex information and knowledge (Anand, 2011; Kim & Anand, 2018; Marschak & Radner, 1972). Such coordination and interdependence among business units inevitably increase organizational complexity, making firms susceptible to ICW.

When firms turn to divestiture to address ICW, they may inadvertently sacrifice some of the synergy derived from the interdependency of their business units. For instance, when firms divest upstream or downstream businesses, they may be compelled to seek external suppliers for inputs to their core business or external distributors for their products. Consequently, firms may incur additional transaction costs related to supplier search, contract negotiation, quality monitoring, and inter-firm coordination, among other activities (Ahuja & Novelli, 2017; Anand, 2011; Hill & Hoskisson, 1987; Williamson, 1975). Furthermore, firms may face higher costs when utilizing external suppliers or distributors as opposed to internal ones, in addition to dealing with uncertainty when coordinating inter-firm transactions or maintaining stable relationships.

When firms contemplate engaging in divestitures, they may consider divesting both core and noncore businesses, although noncore businesses are more commonly targeted (Brauer, 2006; Zuckerman, 2000). A firm’s core business typically serves as the nucleus of its knowledge, resources, and synergy creation (Kumar, 2013; Teece, 1982). Much interdependency and coordination occur between the core business and other subsidiary units. These subsidiary business units often tailor their operational processes and structures to align with the core business’s requirements (Anand, 2011; Kim & Anand, 2018)—and this synergy is lost when these units are divested. Indeed, prior research has demonstrated that divestitures can disrupt finely tuned routines, knowledge, and practices (Feldman, 2014; Semadeni & Cannella, 2011) and negatively impact relationships between employees and other stakeholders (Bettinazzi & Feldman, 2020; Gopinath & Becker, 2000). Therefore, while the core business typically benefits the most from the synergy generated from its subsidiary units, divesting these businesses can subsequently harm the core business.

Besides noncore businesses, assets in the core business may become targets for divestiture (Brauer, 2006). Divesting these assets can disrupt the synergy within the core business, particularly between the divested assets and the remaining components. This loss of synergy arises from the interconnected nature of core business assets, whereby each component contributes to the overall performance and success of the core business (Feldman, 2014). Additionally, divesting core business assets may diminish the sales associated with those assets, further impacting the core business’s overall performance.

In sum, whether divesting assets from the core or noncore businesses, and regardless of their role in causing ICW, such actions can reduce organizational complexity and potentially address ICW. However, they inevitably disrupt synergies arising from interdependencies between the divested assets and the core business. As a result, divestitures following a firm’s ICW disclosure may hinder the growth of its core business. In contrast, divestitures that do not follow an ICW disclosure may be pursued as a means to enhance economic efficiency (Brauer, 2006). Such efforts could involve divesting business units with poor performance or those that do not align well with the overall corporate strategy (Capron et al., 2001; Shimizu, 2007) or optimizing the allocation of corporate resources (Karim, 2006; Karim & Mitchell, 2004). Such actions are less likely to have a detrimental effect on the firm’s core business compared to divestitures following ICW disclosure. Thus, we predict that:

Hypothesis 5: Relative to other divestitures, divestitures following a firm’s disclosure of internal control weakness are associated with slower post-divestiture growth of the firm’s core business.

Data and Method

Sample and Data

We constructed a longitudinal dataset of all firms listed in the S&P 1500 index from 2003 to 2020. Our data started in 2003 because U.S. public firms were first required to disclose internal control assessments after the SOX Act of 2002. We collected divestiture data from Securities Data Corporation (SDC) Platinum. All of the divestitures included in this study were eventually completed. We collected ICW data from Audit Analytics. We collected firm financial data from Compustat and the Center for Research in Security Prices (CRSP), board data from BoardEx, CEO compensation data from ExecuComp, and business segment sales data from the Compustat Segment database. After matching all variables used in this study, our sample consists of 4,958 divestiture deals involving 1,160 firms in the 2003–2020 period.

Dependent Variables

Number of divestitures

Following prior research on divestitures (e.g., Hoskisson, Johnson, & Moesel, 1994; Sanders, 2001; Vidal & Mitchell, 2015), we used the number of divestitures in a given year as our dependent variable to measure a firm’s divestiture activity. Divestitures in our sample include sell-offs, spin-offs, and liquidations conducted by firms. The most common divestiture activity is sell-off, accounting for 97.3% of divestitures in our sample. Firms may have motivations for spin-offs that are different from those for other types of divestitures (Parhankangas & Arenius, 2003). In a robustness check, we excluded spin-offs and obtained results similar to our main findings.

Cumulative abnormal returns (CAR)

Following prior event studies on divestitures (e.g., Chen & Feldman, 2018; Feldman, Amit, & Villalonga, 2019), we constructed cumulative abnormal returns to measure stock market reaction to divestitures. We identified the divestiture announcement data from SDC Platinum from 2003 to 2020. We collected the daily stock returns from the CRSP database for the estimation window [−800, −551] days before the announcement dates. This time window has been extensively used in prior studies (Anand & Singh, 1997; Feldman, 2014; Feldman et al., 2019). From the estimation window, we calculated firms’ normal stock returns based on their daily stock returns as well as the stock market’s returns. Then, following prior research (Anand & Singh, 1997; Feldman, 2014), we calculated the firm’s abnormal returns within a 3-day event window [−1, +1] around the announcement dates. The cumulative abnormal returns were calculated as the sum of these abnormal returns over the event window. 2

Increase in core business’s sales growth

Sales growth has been widely used as a dependent variable to measure firm growth in prior studies (e.g., Davies, Chun, & Kamins, 2010; Greve, 2008; Stuart, 2000; Zheng, Singh, & Mitchell, 2015). To measure the operational performance of a firm’s core business, we constructed this variable by calculating the core business’s sales growth after the divestiture minus its sales growth before the divestiture in a 5-year time window ([−2, +2] year). Specifically, we calculated the measure as sales growth at year t + 2 minus sales growth at year t – 2. Sales growth in year t was calculated by dividing the difference between sales figures in year t and year t – 1 by the sales figures in year t – 1 (Baum & Wally, 2003; Mishina, Pollock, & Porac, 2004; Rodriguez & Nieto, 2016). This dependent variable captures how growth in sales changed before and after the divestiture. 3 We considered a business segment to be a firm’s core business when that segment was identified as the primary segment in the SDC. In a robustness check, we followed the prior literature (e.g., Bowen & Wiersema, 2005; Kumar, 2013; Mayer, Stadler, & Hautz, 2015; Rumelt, 1974) and defined the core segment as the one generating the largest amount of revenue among all segments. We obtained similar results in this analysis.

Independent Variables

Internal control weakness

Following prior research on ICW (e.g., Doyle et al., 2007; Hammersley et al., 2008), we coded internal control weakness as “1” if a firm discloses a material weakness in a given year, and “0” otherwise. Appendix A provides an example list of ICWs in our sample.

Divestitures following ICW disclosure

To distinguish divestitures following ICW disclosure from those not following ICW disclosure, we tracked whether a firm disclosed a material weakness in a given year. We then coded divestiture following ICW disclosure as “1” if a divestiture was announced by a firm within a year following its disclosure of ICW, and “0” otherwise. The one-year time window has been widely used in both the ICW disclosure and divestiture literature (Brauer, 2006; Chalmers et al., 2019).

Moderators

Newly appointed CEO

The newly appointed CEO variable was coded as “1” if the CEO assumed the role in the year of ICW disclosure, and “0” otherwise. 4

Prevalence of ICW among peers

Following the prior literature (e.g., Marquis & Tilcsik, 2016; Teece, 2007), we defined industry peers as firms sharing the same two-digit SIC codes as the focal firm in a given year. We first counted both the number of industry peers and the occurrences of ICW disclosures within this peer group and then calculated the ratio of peer firms disclosing ICWs in the given year. A higher ratio indicates a greater prevalence of ICWs among peers in the industry.

Control Variables

A firm’s size may affect its divestiture activity because larger firms are generally more complex and more likely to undergo organizational restructuring (Brauer, 2006). Thus, we controlled for firm size using the natural logarithm of total assets. Our results were robust when we used the number of employees to measure firm size. Also, because the literature suggests that underperforming firms have a higher tendency to engage in divestitures, such that the stock market might react differently to such deals (Audia & Greve, 2006; Chen & Miller, 2007; Kolev, 2016), we controlled for Tobin’s Q and return on assets (ROA). Firm leverage can influence the performance implications of divestitures (Kolev, 2016); thus, we controlled for the firm’s cash holding ratio (cash and cash equivalents divided by current liabilities) and debt ratio (the ratio of summated long-term debt and current liabilities to total assets) (Feldman et al., 2016). We also controlled for the number of acquisitions in a given year, as it may affect the firm’s divestiture activity (Humphery-Jenner, Powell, & Zhang, 2019). Consistent with prior research (e.g., Haleblian, McNamara, Kolev, & Dykes, 2012; Hitt, Hoskisson, & Kim, 1997; Wiersema & Bowen, 2008), we controlled for an entropy measure of geographic diversification and business diversification. Industry competition may affect divestiture activity (Brauer & Wiersema, 2012); accordingly, we controlled for industry concentration using the Herfindahl–Hirschman Index (HHI) of firms’ sales based on their two-digit SIC codes.

According to the literature, CEO characteristics may affect firm divestitures. As CEO duality has been found to affect the likelihood of divestiture (Chen & Feldman, 2018), we controlled for CEO duality, coded as “1” if a firm’s CEO was also the chair of its board, and “0” otherwise. CEO origin has also been suggested to affect divestiture likelihood; thus, following the prior literature (Zhu & Shen, 2016), we controlled for its effect by including CEO outsider, coded as “1” if a CEO assumes the position of CEO within two years after they joined the company, and “0” otherwise. We also controlled for CEO age as a proxy for CEO career horizon concerns (Ang, de Jong, & van der Poel, 2014) and CEO tenure as a proxy for experience as CEO (Wowak, Mannor, & Wowak, 2015). The extant literature suggests that different forms of performance-based CEO compensation may exert differential influence on divestitures (Sanders, 2001); we, therefore, controlled for CEO ownership, measured as the percentage of the shares owned by the CEO relative to the total number of outstanding shares of a firm, and CEO option value, measured as the value of the stock options granted during a given year (Sanders, 2001).

As corporate governance can affect divestitures (Feldman et al., 2019; Kolev, 2016), we controlled for board size (i.e., number of directors) and independent ratio, measured as the ratio of the number of outside directors to board size (Hanson & Song, 2000; Kroll, Walters, & Wright, 2008). We also controlled for industry effects by including industry fixed effects (based on two-digit SIC codes), as industry-specific factors could affect divestitures (Brauer & Wiersema, 2012). Lastly, we included year effects to control for temporal and environmental impacts, such as the influence of the general environment.

Analyses and Results

Testing Hypotheses 1–3

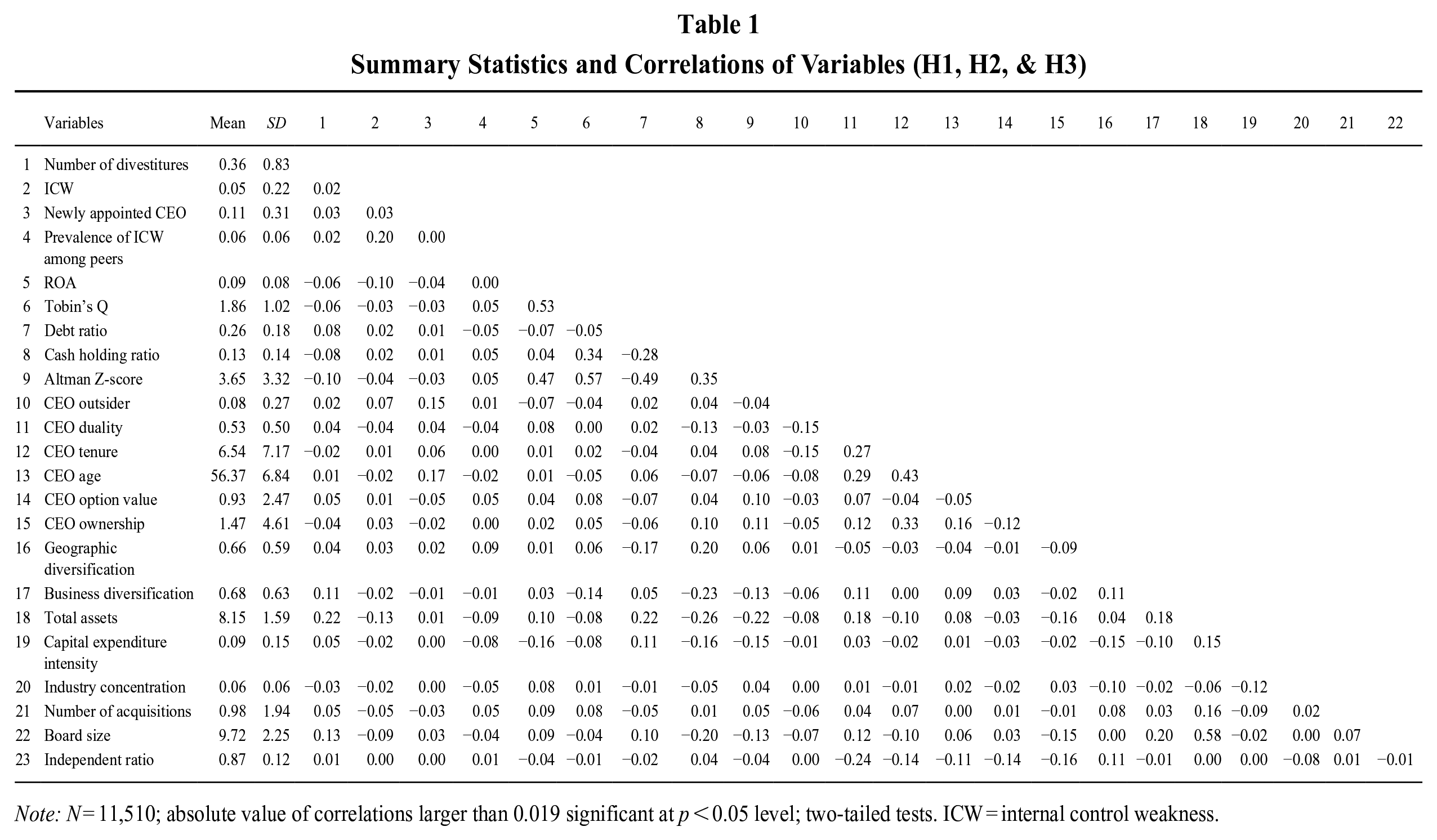

Our dependent variable (i.e., number of divestitures) in testing the first three hypotheses is a count variable. Poisson and negative binomial regressions are often used to estimate count variables. Because we theorize how mandatory ICW disclosure can affect a firm’s divestitures (i.e., the within-firm effects), firm fixed-effects regressions are an appropriate analytical technique. In addition, the Hausman test (p < 0.001) indicates that time-invariant firm heterogeneity may affect firm divestiture decisions, so firm fixed-effects models are more appropriate than random-effects models. Given that negative binomial regressions do not offer true fixed-effects regressions (Allison & Waterman, 2002), we use firm fixed-effects Poisson regressions to test our hypotheses, clustering firm robust standard errors. The independent variable and control variables were all lagged by one year. We report summary statistics and correlations in Table 1. As shown in this table, firms, on average, engage in 0.36 divestitures in a given year. Approximately 5% of firm-year observations have an associated ICW disclosure.

Summary Statistics and Correlations of Variables (H1, H2, & H3)

Note: N = 11,510; absolute value of correlations larger than 0.019 significant at p < 0.05 level; two-tailed tests. ICW = internal control weakness.

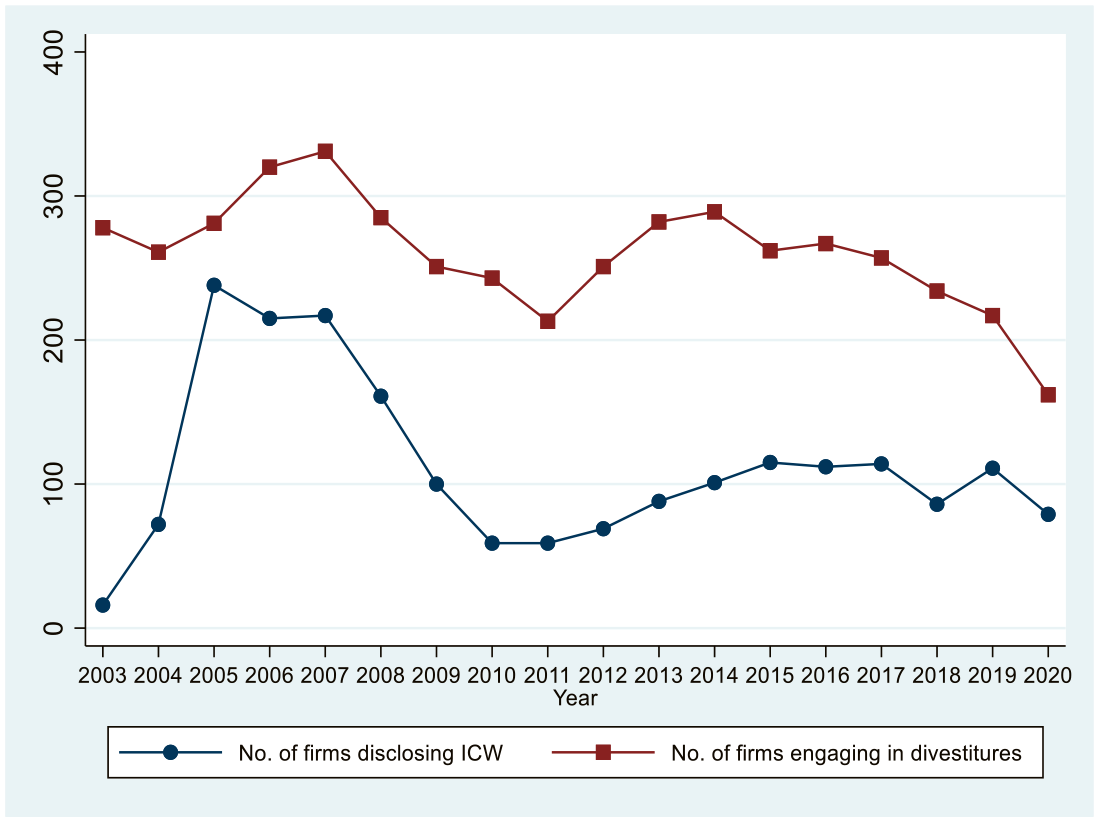

We plot the trend of divestitures and disclosure of ICWs from 2003 to 2020 in Figure 1. The upper line with the square marker is the number of firms that engaged in divestitures, and the lower line with the dot marker is the number of firms that disclosed ICWs. The two lines show similar trends over time, providing some graphic evidence supporting Hypothesis 1.

The Number of Firms Disclosing ICW and the Number of Firms Engaging in Divestitures from 2003 to 2020

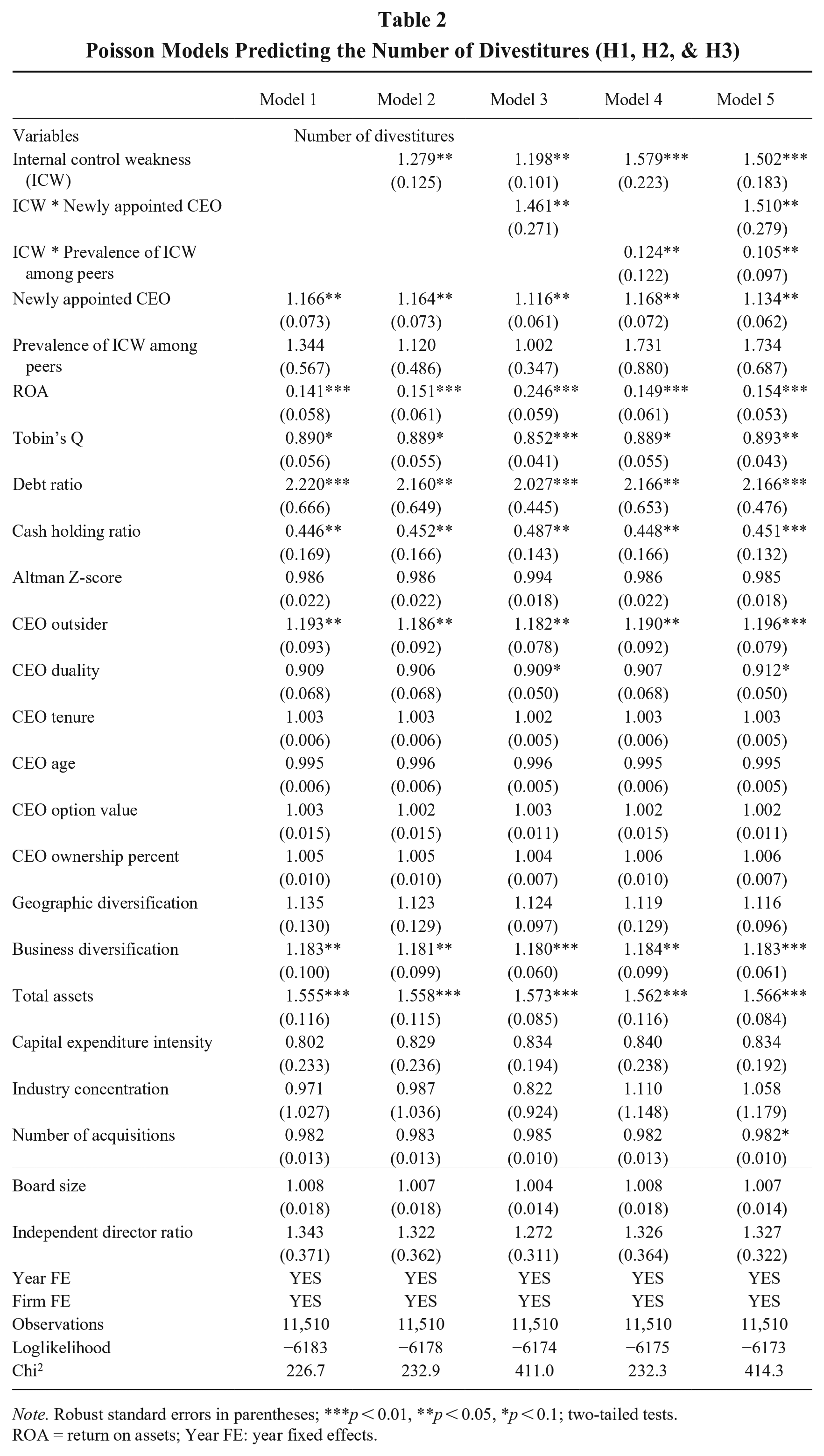

Table 2 reports the test results for the first three hypotheses. The coefficients are incidence rate ratios (IRR) in the Poisson estimator; a coefficient larger than 1 suggests a positive relationship, and a coefficient smaller than 1 indicates a negative relationship. Model 1 includes only control variables; Model 2 includes internal control weakness; Models 3 and 4 further include newly appointed CEO and prevalence of ICW among peers as moderators, respectively; and Model 5 is the full model.

Poisson Models Predicting the Number of Divestitures (H1, H2, & H3)

Note. Robust standard errors in parentheses; ***p < 0.01, **p < 0.05, *p < 0.1; two-tailed tests.

ROA = return on assets; Year FE: year fixed effects.

Hypothesis 1 suggests that a firm’s disclosure of ICW is positively associated with its subsequent divestiture activity. The coefficient estimate of internal control weakness in Model 5 is positive and statistically significant (β = 1.502, p = 0.001), supporting Hypothesis 1. In terms of the size effect, when firms experience ICW, the number of divestitures they undertake is 1.502 times the number when they do not experience ICW.

Hypothesis 2 proposes that the positive relationship between ICW disclosure and subsequent divestiture activities is stronger when a firm has a newly appointed CEO. In Model 5, the coefficient estimate of the interaction term between internal control weakness and newly appointed CEO is larger than 1 and statistically significant (β = 1.510, p = 0.026), supporting Hypothesis 2. In addition, the coefficient estimate of the interaction term between internal control weakness and prevalence of ICW among peers is smaller than 1 and statistically significant (β = 0.105, p = 0.015), supporting Hypothesis 3.

Because the coefficients of interaction terms in nonlinear models do not always represent the true interactions (Ai & Norton, 2003; Hoetker, 2007; Wiersema & Bowen, 2009), we cannot directly interpret them. Following the prior literature (Wiersema & Bowen, 2009), we examine the marginal effect of the independent variable on divestitures across different values of the moderator. We find that the marginal effect of internal control weakness on the number of divestitures is stronger when CEOs are newly appointed (b = 0.591, z = 2.84) than when they are not (b = 0.201, z = 1.94). Similarly, the marginal effect of internal control weakness on the number of divestitures is weaker when the prevalence of ICW among peers is at a high level (i.e., mean plus one standard deviation) (b = −1.672, z = −1.76) compared to a low level (i.e., mean minus one standard deviation) (b = 0.475, z = 3.30). These results imply that ICWs have a stronger positive association with the number of subsequent divestitures when firms have newly appointed CEOs or encounter lower industry ICW prevalence, consistent with the predictions of Hypotheses 2 and 3, respectively.

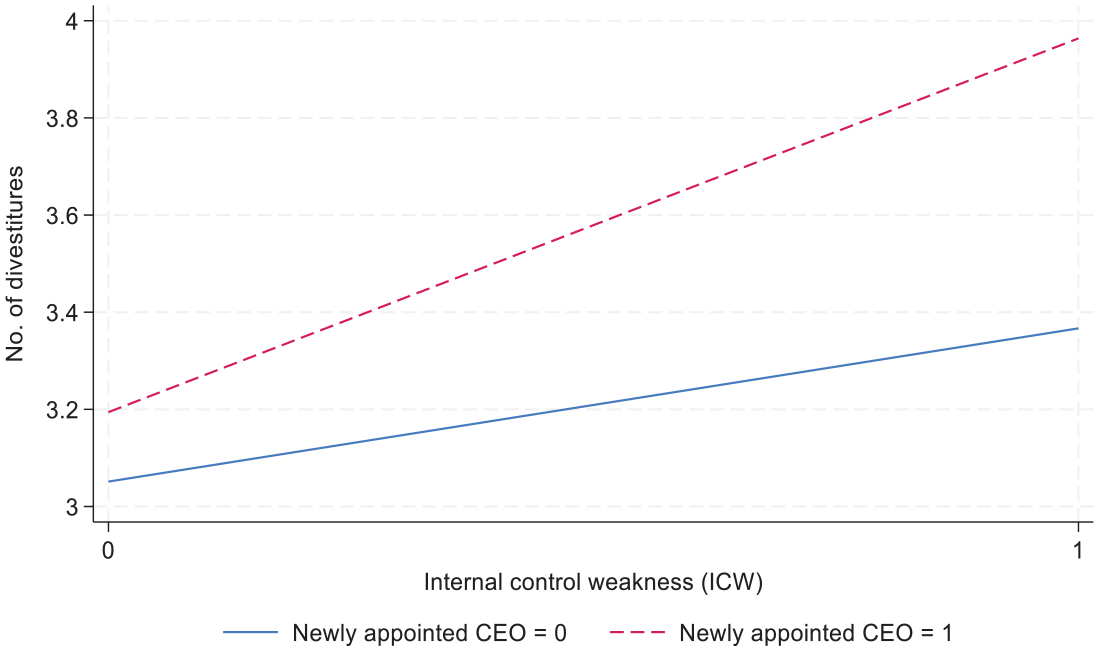

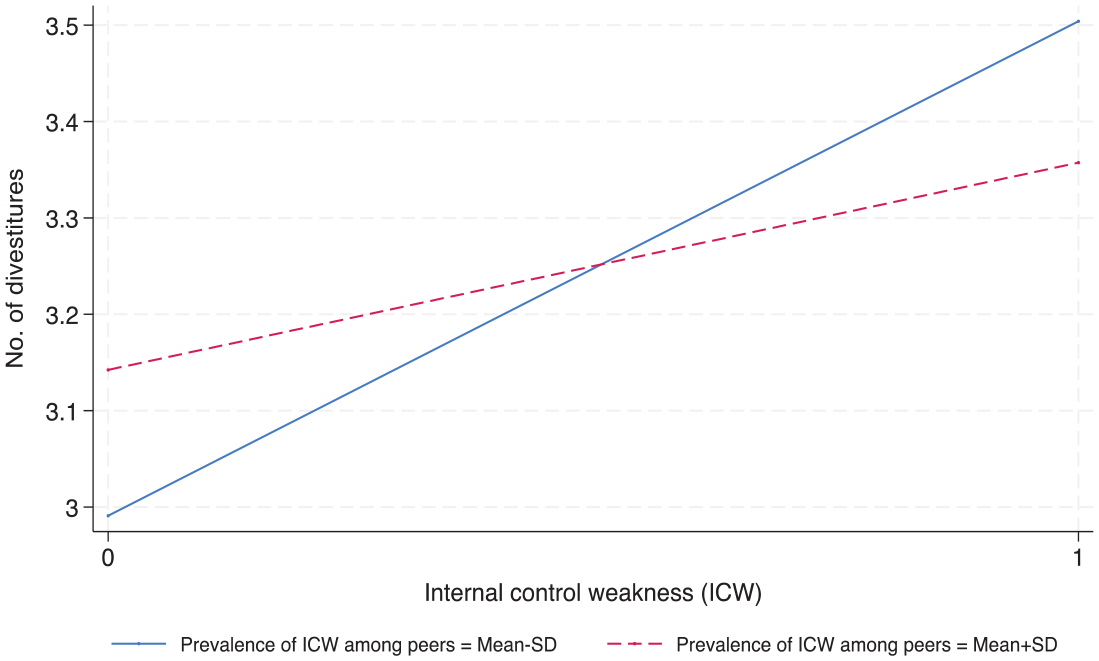

We plot the interactions of newly appointed CEO and ICW disclosure in Figure 2, where the dashed line displays the relationship between ICW disclosure and divestitures when CEOs are newly appointed, and the solid line depicts the relationship when CEOs are not newly appointed. As shown in Figure 2, both lines exhibit upward slopes, with the dashed line (newly appointed CEO = 1) having a steeper slope than the solid line (newly appointed CEO = 0). This suggests that newly appointed CEOs strengthen the positive relationship between ICW disclosure and divestitures. Similarly, we plot the interactions of prevalence of ICW among peers and ICW disclosure in Figure 3, where the dashed line depicts the relationship when the prevalence of ICW among peers is high (i.e., mean plus one standard deviation), and the solid line displays the relationship when the prevalence of ICW among peers is low (i.e., mean minus one standard deviation). As shown in Figure 3, the dashed line (high prevalence of ICW among peers) has a less steep slope than the solid line (low prevalence of ICW among peers). This suggests that the prevalence of ICW among peers weakens the positive relationship between ICW disclosure and divestitures.

The Interaction between ICW Disclosure and Newly Appointed CEOs in Predicting Divestitures

The Interaction between ICW Disclosure and the Prevalence of ICW among Peers in Predicting Divestitures

Testing Hypotheses 4–5

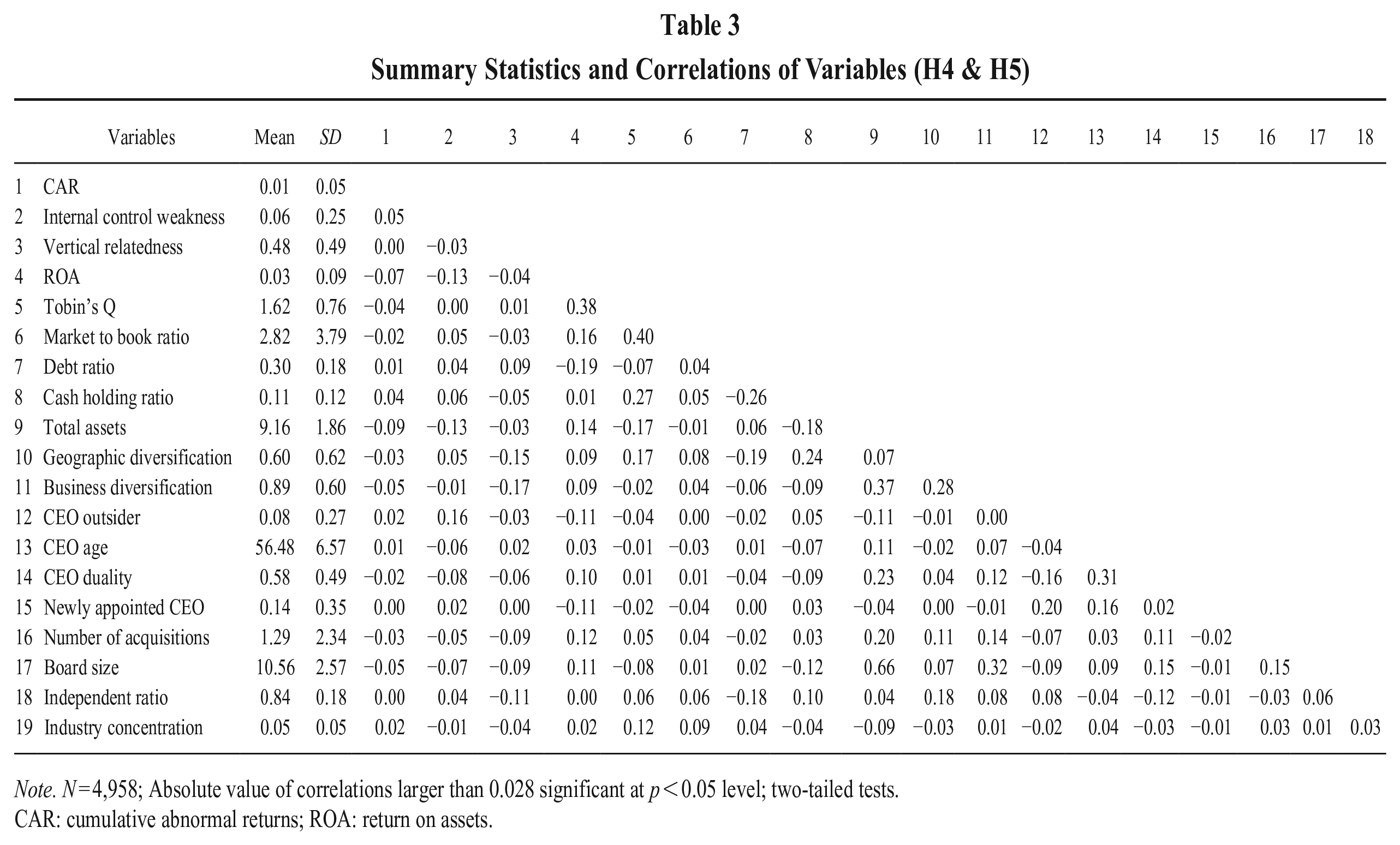

For Hypotheses 4 and 5, our dependent variables, cumulative abnormal returns and increase in core business’s sales growth, are continuous variables. Thus, we adopted ordinary least squares (OLS) regression models to test these hypotheses. Table 3 reports the summary statistics and correlations. As shown in this table, divestitures have an average cumulative abnormal return of 0.01. Approximately 6% of the divestitures in our sample are divestitures following ICW disclosure.

Summary Statistics and Correlations of Variables (H4 & H5)

Note. N = 4,958; Absolute value of correlations larger than 0.028 significant at p < 0.05 level; two-tailed tests.

CAR: cumulative abnormal returns; ROA: return on assets.

As Hypotheses 4 and 5 examine the performance implications of firms’ divestitures, we required the sample firms to have engaged in divestitures during the observation period. This gives rise to a potential sample selection bias—that is, the firms that initiated divestitures might be systematically different from the ones that did not (Greene, 1981). This potential sample selection issue raises concerns about our findings. To address this concern, we adopted a Heckman two-stage model (Heckman, 1979). The first-stage model employed a probit estimator to predict the likelihood of a firm undertaking a divestiture in a given year.

Following existing research (Certo, Busenbark, Woo, & Semadeni, 2016), we needed an exclusion restriction in the first-stage regression. We chose number of divestitures within the focal firm’s industry (based on two-digit SIC codes), excluding those divestitures undertaken by the focal firm in a given year. This variable captures the general trend toward and propensity of divestitures. Although it could affect a focal firm’s divestiture decision (Lieberman & Asaba, 2006; Mulherin & Boone, 2000), it may not directly influence the firm’s divestiture performance. In unreported results, we found that number of divestitures within the focal firm’s industry did not have a statistically significant effect on either of the divestiture performance outcomes—that is, cumulative abnormal returns (β = 0.001, p = 0.318) or increase in core business’s sales growth (β = −0.002, p = 0.734).

We ran the first-stage model using all firms in the S&P 1500 index during the observation period. The results of the first-stage model appear in Appendix B in an online supplementary document. The coefficient of number of divestitures within the industry is positive and significant (β = 0.012, p < 0.01), consistent with our argument. We also found that the coefficient of internal control weakness is positive and significant (β = 0.108, p = 0.034), suggesting that firms with ICW are more likely to engage in divestitures than those without ICW, which is aligned with our key arguments in Hypothesis 1. In addition, from the first-stage model, we generated the inverse Mills ratio and included it in the second-stage model to test our hypotheses.

Before predicting the effect of divestitures following ICW disclosure on post-divestiture performance, we needed to address a potential source of endogeneity: the potential non-randomness of ICW disclosure. Although we followed prior studies in controlling for factors that might potentially affect firm divestiture performance, omitted variables might still affect both the ICW disclosure and firm divestiture performance. Such an omitted variable may cause endogeneity and result in biased estimation. To address this concern, following recent research (e.g., Hendricks, Howell, & Bingham, 2019; Testoni et al., 2022), we adopted a multivariate matching approach—entropy balancing (Hainmueller, 2012).

Entropy balancing differs from other matching approaches, such as propensity score matching and coarsened exact matching, in how it determines the weights for control observations. Based on the nearest distance or coarsened values of matching variables, respectively, propensity score matching and coarsened exact matching include some control observations as matched (assigned a weight of 1) and discard other unmatched observations (assigned a weight of 0). In contrast, the entropy balancing approach identifies a set of continuous weights to ensure that the first, second, and possibly higher moments of the distribution of the matching variables are as similar as possible between the reweighted control observations and treatment observations. In this way, entropy balancing matching reduces covariate imbalance, model dependence, and ultimately estimation bias (Ho, Imai, King, & Stuart, 2007; Iacus, King, & Porro, 2012). Moreover, this technique does not discard any observations as the other matching approaches do.

In this study, the treated firms disclosed ICW, and the control firms did not. Following the prior literature (Chalmers et al., 2019; Doyle et al., 2007; Simon, 1962; Zhou & Wan, 2017), we identified matching variables that could affect the likelihood of a firm experiencing ICW. Appendix C in the online supplementary document reports the descriptive statistics of the matching variables before and after entropy balancing matching. Before the matching, the mean, standard deviation, and skewness of the matching variables were different between the treated and control firms. The continuous weights generated by the entropy balancing led the reweighted control firms to be almost equal to the treated firms regarding the mean, standard deviation, and skewness. Moreover, we included the industry classification indicator (two-digit SIC codes) and year indicator variables in the matching process, so these two variables were the same between treated and reweighted control firms.

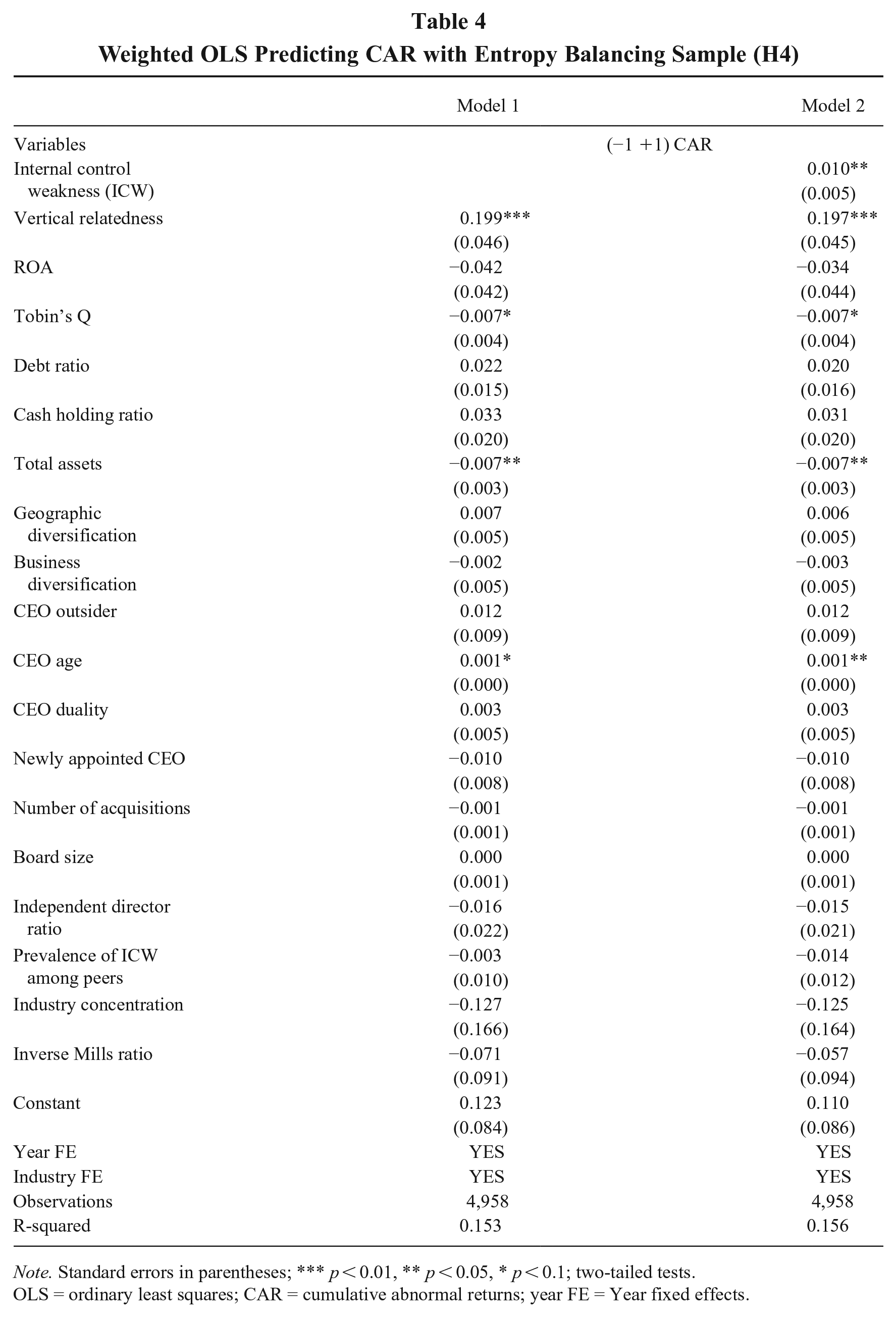

Based on the entropy balancing matched sample, we employed the weighted OLS models to test Hypotheses 4 and 5. Table 4 reports the regression results for cumulative abnormal returns. Specifically, Model 1 includes only control variables, and Model 2 adds internal control weakness to the regression. Hypothesis 4 suggests that divestitures following ICW disclosure are associated with higher cumulative abnormal returns. The coefficient estimate of internal control weakness in Model 2 is positive and significant (β = 0.010, p = 0.036), supporting Hypothesis 4. Compared with divestitures not following ICW disclosure, divestitures following ICW disclosure are associated with a higher cumulative abnormal return—specifically, a 1% difference. If we use the sample firms’ average market value in the divestiture year as a benchmark, the 1% cumulative abnormal return translates into U.S. $325.46 million.

Weighted OLS Predicting CAR with Entropy Balancing Sample (H4)

Note. Standard errors in parentheses; *** p < 0.01, ** p < 0.05, * p < 0.1; two-tailed tests.

OLS = ordinary least squares; CAR = cumulative abnormal returns; year FE = Year fixed effects.

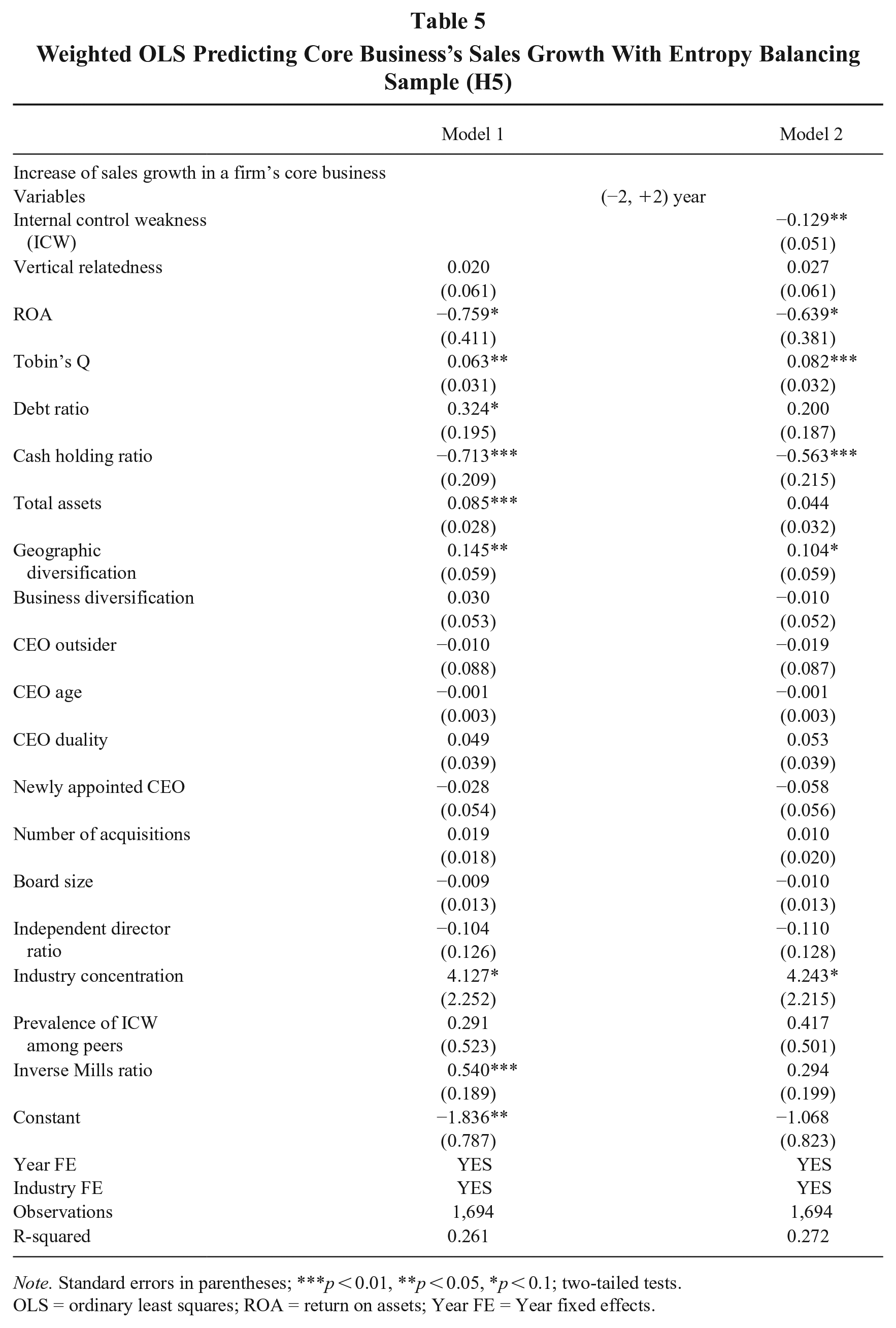

Table 5 reports the regression results for increase of sales growth in a firm’s core business. Specifically, Model 1 includes only control variables, and Model 2 adds internal control weakness. Hypothesis 5 suggests that, compared with divestitures not following ICW disclosure, divestitures following ICW disclosure are associated with a smaller increase in the core business’s post-divestiture sales growth relative to its pre-divestiture growth. The coefficient estimate of internal control weakness in Model 2 is negative and significant (β = −0.129, p = 0.011), supporting Hypothesis 5. Divestitures following ICW disclosure are associated with a smaller increase in the core business’s sales growth (a 12.9% difference) compared to divestitures not following ICW disclosure. This result supports our prediction that to remediate ICW, firms may undertake divestitures that can erode the synergy across their business units and, in turn, hurt their core business’s growth (Bergh, 1995; Feldman, 2014).

Weighted OLS Predicting Core Business’s Sales Growth With Entropy Balancing Sample (H5)

Note. Standard errors in parentheses; ***p < 0.01, **p < 0.05, *p < 0.1; two-tailed tests.

OLS = ordinary least squares; ROA = return on assets; Year FE = Year fixed effects.

We also performed several supplementary analyses. First, we conducted additional analyses using coarsened exact matching (CEM) to mitigate the nonrandom selection concern regarding the presence of ICW across firms. Similarly, we adopted the CEM approach to test the robustness of our findings on divestiture performance. Our findings are robust to the CEM approach.

Next, we conducted supplementary analyses to explore whether ICW disclosure may have different effects on divestitures depending on the types of ICWs involved. We separated “company-wide” ICWs, which are closely tied to organizational complexity, and “account-specific” ICWs, which are less directly linked to organizational complexity, and reran the analyses. The results indicate that firms are more inclined to pursue divestitures in cases involving “company-wide” ICWs, providing additional support for our proposed mechanism of complexity reduction through divestitures to address ICW (see Appendix D of the online supplementary document).

Furthermore, we conducted supplementary analyses to explore which types of business units are divested following ICW disclosure. These analyses suggest that firms are more inclined to divest (1) foreign businesses than domestic ones and (2) vertically related businesses than nonvertically related ones to remediate ICW. These results validate our proposed mechanism—namely, that firms engage in divestitures to reduce their organizational complexity so as to rectify ICW. We report these supplementary analyses and the associated results in the online supplementary document.

Discussion and Conclusion

This study examines the impact of a firm’s ICW on its divestiture decisions and the related performance implications. We found that firms with ICW disclosure are inclined to pursue corporate divestitures because these actions can reduce organizational complexity and help remedy ICW. In addition, the positive effect of ICW disclosure on divestitures is stronger when a firm has recently appointed a CEO or when there is a lower level of ICW prevalence among industry peers. Furthermore, we showed that divestitures following ICW disclosure, when compared to those not following such disclosures, are associated with higher stock market performance for the divesting firms, yet weaker growth of the divesting firm’s core business.

Contributions to Corporate Strategy Research

Our examination of the role of ICW in shaping divestiture decisions contributes to the corporate strategy literature. Internal control constitutes an indispensable facet of organizational control, generating significant influence over not only a firm’s financial and accounting aspects but also its overall operation and management (Chalmers et al., 2019). Given the increasing influence of shareholders and their demands for heightened executive accountability over the past two decades, internal control has emerged as a vital concern for managers in strategic decision-making. Essentially, an efficient internal control system forms the bedrock of corporate governance (Pandey et al., 2022). Despite its pivotal role in shaping firm strategic decisions and outcomes, internal control has received only limited research attention from management scholars to date. Thus, our research represents a pioneering effort to shed light on the significant effects of firms’ ICW on their divestiture decisions and the associated performance implications.

More specifically, this paper contributes to the divestiture literature by enriching our understanding of the antecedents and consequences of corporate divestitures. First, it complements existing research by investigating a noneconomic factor that triggers divestitures, specifically those aimed at mitigating an immediate reputation and legitimacy threat arising from ICW disclosure. The prevailing divestiture literature has predominantly focused on the organizational goal of enhancing economic efficiency when explaining firms’ divestiture decisions. This includes considerations of pre-divestiture firm performance (Karim, 2006; Sembenelli & Vannoni, 2000; Shimizu & Hitt, 2005) and corporate governance (e.g., McNamara et al., 2002; Sanders, 2001). Joining a burgeoning body of literature exploring noneconomic triggers for divestitures, such as media attacks (Durand & Vergne, 2015) and activist investors (Chen & Feldman, 2018), our investigation into mandatory ICW disclosure as an antecedent to divestitures offers a fresh perspective on the motivations that drive firms to engage in these activities. Relatedly, our study highlights two firm contingencies—the presence of a newly appointed CEO in the firm and the prevalence of ICW in the industry—that can shape firms’ motivations to pursue divestitures in response to ICW.

Second, we integrate a multifaceted performance assessment into our investigation of the implications of divestitures following ICW disclosure. Although regulators are playing an increasingly influential role in shaping firms’ decisions (Henriques & Sadorsky, 1996), and firms often resort to divestitures in response to regulatory changes (Hoskisson & Hitt, 1990; Shleifer & Vishny, 1991), the literature has largely remained silent on the performance implications of these transactions. To the best of our knowledge, this study represents one of the first efforts to explore and compare the multifaceted performance implications of divestitures following regulatory violations with those that do not follow such violations.

By investigating and comparing two distinct performance outcomes of divestitures following ICW disclosure versus those not following such disclosure, this study offers two new insights into the inconsistent findings regarding the performance implications of divestitures in at least two ways. For one, complementing prior studies that have suggested the timing of divestitures (Markides, 1995) or the life-cycle stage of divesting firms (Pashley & Philippatos, 1990) may explain the mixed effects of divestitures on firm performance, our model posits that this inconsistency may stem from various types of drivers for divestitures. Whereas divestitures driven by economic efficiency consideration are likely to be associated with positive post-divestiture performance, divestitures undertaken to repair reputation and legitimacy damage resulting from regulatory violations may be linked to poor post-divestiture performance, such as decreased market growth in the core business of firms pursuing divestitures following ICW disclosure in our context. Future research would be wise to consider a firm’s primary intent (e.g., economic efficiency versus impression management) when evaluating post-divestiture performance.

For another, our findings indicate that, in comparison to other divestitures, those following ICW disclosure elicit more positive stock market reactions for the divesting firm but are associated with a slower growth rate in its core business. This suggests that divestitures with positive short-term performance do not necessarily translate into positive long-term firm competitiveness. Although divestitures may effectively mitigate the immediate threats to the firm’s reputation or legitimacy resulting from ICW disclosure, they could potentially impede the synergy required for long-term growth. Thus, in alignment with the growing body of literature (Feldman, 2014; McKendrick et al., 2009; Vidal & Mitchell, 2018) seeking to reconcile the disparities in the performance outcomes of divestitures, this paper underscores the importance of conducting a comprehensive performance assessment that considers multiple facets, including both short-term and long-term perspectives.

Our findings also raise an intriguing question: If divestitures following mandatory ICW disclosure can potentially hinder the subsequent growth of the divesting firms, why do investors not foresee this outcome and react negatively? A few speculations could shed light on this phenomenon. First, the stock market may exhibit myopic behavior (Laffont & Maskin, 1990; Malkiel, 1989), implying that investors may struggle to anticipate the long-term damage these divestitures might inflict on the divesting firms. Second, investors might be cognizant of the potential harm resulting from these divestitures. However, given that the cost of not addressing ICW can be even higher, investors might tend to react more positively to divestitures following ICW disclosure. These speculations merit further investigation to enhance our understanding of the performance implications of divestitures.

Contributions to the ICW Literature

To some extent, the literature in some other domains, especially accounting, has delved into the outcomes of mandatory ICW disclosure—such as stakeholders exhibiting a negative reaction (Hammersley et al., 2008) and firms experiencing reduced investment efficiency (Cheng et al., 2013). By comparison, it has devoted relatively limited attention to elucidating how these weaknesses influence a firm’s strategic decisions and their subsequent consequences (Kanodia & Sapra, 2016; Leuz & Wysocki, 2016). Our study departs from previous research by revealing how ICW impacts a specific strategic action—divestiture—and subsequent firm performance, thereby contributing to the body of internal control research. Moreover, and contrary to earlier findings suggesting that stakeholders typically react negatively to ICW disclosure (Hammersley et al., 2008), we present a case in which investors exhibit a positive response to divestitures following such a disclosure.

Practical Implications

This study offers several practical implications for firms experiencing ICW and their investors, guiding them in ICW disclosure and subsequent strategic decisions to balance risk management with growth opportunities (Simsek, Li, & Huang, 2021). First, given the significant costs associated with ICW disclosure, firms should implement robust systems to monitor internal controls. This proactive approach is crucial, especially when pursuing diversification strategies, as it can help prevent future occurrences of ICW. Second, managers, particularly long-tenured CEOs, are often reluctant to undertake proactive divestitures. Therefore, it is vital for the board to play an active role in this process, considering proactive divestitures as a potential solution to ICW. Third, the prevalence of ICWs at the industry level might reduce firms’ motivation to pursue divestitures as a remedial measure. However, this scenario could present an opportunity for firms to strategically divest and enhance their internal control standing, potentially gaining favor with investors. Fourth, although divestitures following ICW disclosure can elicit positive reactions from investors, they should be approached cautiously. Such actions may also detract from core business growth. Firms must carefully evaluate the multifaceted performance implications before proceeding with divestiture strategies in response to ICW disclosure. Lastly, when selecting divestiture targets in response to ICW disclosure, firms may find it particularly effective to divest vertically related and foreign business units. Such divestitures can more efficiently reduce organizational complexity and address ICW.

Limitations and Future Research Directions

Given the substantial costs linked to ICW disclosure, one might wonder why firms do not address ICW before its disclosure. It is plausible that some firms have proactively remedied their ICWs beforehand. However, our data do not account for such instances, which is a limitation of our study, as we could only observe disclosed ICW. Future research might fruitfully explore which types of firms tend to proactively take actions to address ICW preemptively. Future research could also examine the implications of internal control for other strategic decisions. For example, firms with poor internal controls may refrain from acquiring foreign targets because their internal control system may not suffice to ensure that these foreign subsidiaries’ business practices are consistent with the focal firm’s corporate policies and standards and that information from the subsidiaries flows to the corporate office both accurately and promptly. Moreover, future research could examine the heterogeneity of ICW. Although organizational complexity is considered one of the most important triggers for ICW (Bedard & Graham, 2014; Schneider et al., 2009), specific weaknesses may be associated with organizational complexity in unique ways. Thus, divestiture may not be a uniformly effective solution for firms seeking to resolve ICW. Future research could delve deeper into whether firms’ adoption of divestiture as a response strategy to ICW disclosure is contingent upon the specific causes of that weakness.

Conclusion

This study highlights the important role of ICW in shaping corporate divestiture decisions and documents the multifaceted performance implications of such divestitures. We believe that our theory and findings contribute to a better understanding of the drivers of firm divestitures and their related consequences. We hope that our work will inspire future management research exploring how ICW and/or other types of regulatory pressures influence firms’ strategic decisions and outcomes.

Supplemental Material

sj-docx-1-jom-10.1177_01492063241274284 – Supplemental material for Internal Control Weakness and Corporate Divestitures

Supplemental material, sj-docx-1-jom-10.1177_01492063241274284 for Internal Control Weakness and Corporate Divestitures by Qiang (John) Li, Songcui Hu and Wei Shi in Journal of Management

Footnotes

Acknowledgements

We would like to thank action editor Zeki Simsek and two anonymous reviewers for their guidance and constructive feedback in developing this manuscript. This research was supported in part by the research fund from CEIBS (AG24ICW).

Supplemental material for this article is available with the manuscript on the JOM website.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.