Abstract

Using property rights theory to examine the characteristics that enable family firms to exclude rivals from their competitive space, we explain why the family form of governance is often selected instead of the nonfamily form of governance and what determines the scale and scope of family firms. Family-centered nonpecuniary goals allow family firms to capture rights to common property opportunities that nonfamily firms find unattractive. Furthermore, the development and deployment of non-tradeable, immobile, inimitable, and indivisible human and nonhuman resources enable family firms to protect their property rights from competitors. Finally, because family members act as owners and managers, family firm governance can reduce the cost of monitoring as well as the possibility of opportunistic behavior and underinvestment of family resources.

Family firms, which are defined by the ownership control and management involvement of two or more family members of a firm and by a vision of how the firm will provide transgenerational benefits to the family (Chua, Chrisman, & Sharma, 1999), are globally ubiquitous (La Porta, Lopez-de-Silanes, & Shleifer, 1999). Studies estimate that between 54% and 90% of US firms with employees are family firms (Astrachan & Shanker, 2003; Villalonga, Amit, Trujillo, & Guzmán, 2015). Aldrich and Cliff (2003) provide similar estimates of family firms worldwide. Combined, the literature and empirical evidence suggest that many firms start as family firms, and a significant percentage become family firms over time and maintain family involvement throughout their existence. For example, using the above definition, Chua, Chrisman, and Chang (2004) estimate that in the US, 77% of new ventures with employees start as family firms, and 81% of established small firms can be classified as family firms based on ownership, management involvement, and intention for transgenerational succession.

However, key questions of theoretical and practical significance remain to be answered, such as why so many firms are started as family firms and why so many firms adopt or continue to exhibit the defining features of the family form of organization over time. In this article, we provide some preliminary answers to these questions by developing a theory of the family firm that integrates classical (Alchian & Demsetz, 1972; Barzel, 1989; Demsetz, 1967, 2002; Libecap, 1989) and modern (Grossman & Hart, 1986; Hart & Moore, 1990) property rights theory with the goals, governance, and resource framework from the family business literature (Chua, Chrisman, Steier, & Rau, 2012; Chrisman, Sharma, Steier, & Chua, 2013). Consistent with the central questions associated with a theory of the firm (Conner, 1991; Holmstrom & Tirole, 1989), we follow Chrisman, Chua, Le Breton-Miller, Miller, & Steier (2018: 171) in arguing that a theory of the family firm should explain “why family firms exist along with other organizational forms,” especially in comparison to nonfamily forms of organization. Bearing in mind that variations exist among family firms, we devote most of our attention to this question, and, in doing so, address the advantages and disadvantages of the family form of organization. We also address what determines the limits or boundaries of family firms in terms of their scale (size) and scope (product-market coverage). In exploring the boundaries of family firms, we explain how their advantages and disadvantages determine the environments they occupy.

As we attempt to explain the existence and boundaries of family firms in comparison to nonfamily firms, two points should be emphasized. First, we recognize that family firms are heterogeneous (Daspit, Chrisman, Ashton, & Evangelopoulos, 2021; Daspit, Chrisman, Skorodziyevskiy, Davis, & Ashton, 2023). Therefore, our theory captures central tendencies and comparative features of family firms rather than invariant characteristics or distinctions. Second, in discussing these tendencies, we do not compare hierarchical governance with market governance as does transaction cost theory (e.g., Williamson, 1989). Instead, we compare the different forms of hierarchical governance represented by family and nonfamily firms and discuss why the family form might be selected rather than the nonfamily form and why family firms might be better or worse positioned for growth over time, given the relative advantages and disadvantages of the goals, governance, and resources they possess. We argue that in comparison to nonfamily firms, the existence of family firms as well as the limits to their scale and scope are a function of the advantages and disadvantages of the goal-based, governance-based, and resource-based mechanisms of exclusion they use to capture property rights associated with the pursuit of opportunities and prevent competitors from appropriating those property rights.

In this article, exclusion is defined as a firm’s ability to manage property rights in a way that establishes market barriers that restrict competitors from pursuing the same set of opportunities. The essence of exclusion lies in limiting market competition, which can be achieved through actions that either reduce the benefits or increase the costs for other firms seeking to exploit an opportunity. Family firms achieve goal-based exclusion, an ex-ante limit to competition (Peteraf, 1993), by targeting market opportunities that offer family-centered nonpecuniary (FCN) benefits or returns that compensate for pecuniary returns that are below the threshold typically expected by nonfamily firms (König, Kammerlander, & Enders, 2013; Zellweger, Kellermanns, Chrisman, & Chua, 2012). Furthermore, governance-based exclusion enables families to transfer their goals to the firm and protect it from opportunistic behavior and underinvestment. Opportunistic behavior occurs when resources are allocated in ways that do not align with the family’s pecuniary or FCN goals, and underinvestment arises when resource owners lack incentives to invest resources in the firm (Grossman & Hart, 1986; Hart & Moore, 1990). Finally, when the property rights to critical resources tied to family ownership and control are non-tradable, imperfectly mobile, inimitable, and indivisible (Barney, 1991, 1995), family firms can utilize resource-based exclusion, an ex-post limit to competition (Peteraf, 1993), which allows family firms to prevent nonfamily competitors from imitating family-specific resources.

Shane and Venkataraman (2000) argue that new fields should be built on features that distinguish them from mainstream disciplines. We contribute to the literature by using the logic of property rights to develop a theory of the family firm that builds on the most important distinguishing features of family firms: goals, particularly the family-centered nonpecuniary (FCN) goals that generate socioemotional wealth (SEW) (Gómez-Mejía, Haynes, Núñez-Nickel, Jacobson, & Moyano-Fuentes, 2007) and idiosyncratic opportunities; governance, which is characterized by a family’s collaborative ability to maintain strong residual rights of claimancy and control; and family resources which are based on the tacit knowledge of family members, particularly those who make up the dominant coalition of the firm. Each of these characteristics has been discussed in the literature to varying degrees, but this article is the first to use the three in combination to explain why the family form of organization might be chosen over the nonfamily form, and to explain the limits of the scale and scope of family firms.

Therefore, in this article, we take the first steps toward a theory of the family firm by using property rights theory to explain how and why advantages pertaining to goals, governance, and resources prevent competitive appropriation and lead entrepreneurs to select the family rather than the nonfamily form of organization. We conclude by explaining the limits to family firms’ scale and scope and discussing the implications of our theory for future research.

Property Rights Theory

Property rights theory deals with contracts and the economic exchanges associated with those contracts (Barzel, 1989; Cheung, 1970; Coase, 1960; Libecap, 1989). The theory suggests that owners bear the full costs and benefits of exchange when property rights are effectively delineated and protected. Property includes tangible and intangible resources. Property rights include the ability to use property, appropriate income from the use of property, and transfer property at an owner’s discretion. Underlying these rights is the ability to exclude (or include) others from exercising those rights (Demsetz, 1967; Merrill, 1998; Schulze & Zellweger, 2021). The right or ability of exclusion is a necessary condition for contracting because, without it (Hart & Moore, 1990), there is nothing to govern or exchange (Cheung, 1970). In multigenerational family firms, property rights represent the ability of family owners to use and appropriate the benefits of the property, transfer those rights transgenerationally to other family members, and exclude parties outside the family from appropriating those rights. Thus, in multigenerational family firms, property rights extend beyond current owners to include future owners.

Property rights are either owned by specific parties (i.e., private property) or are open to capture by parties without current ownership (i.e., common property). Common property refers to property that lacks a clear owner and where exclusion has not been achieved. Market opportunities, for instance, can be considered common property before a firm internalizes them, as they exist without being claimed by anyone. In this respect, we follow Barzel (1989) in focusing on de facto property rights, recognizing that the control of property rights can extend beyond their legal forms. As Foss and Foss (2005) note, business owners may engage in strategies to reduce incentives and/or increase costs for others attempting to capture the value associated with their property. In this sense, exclusion—the essence of property rights—can be achieved in the marketplace by anything that reduces the expected returns or increases the expected costs for market competitors.

When owners do not bear the full costs and/or benefits of exchange (i.e., when they are shifted or made available to other parties), externalities are said to occur (Demsetz, 2002). Externalities, which are reciprocal in nature, are the value consequences of actions one party takes that affect other parties either positively or (more usually) negatively. In this article, we focus on externalities that exist among firms through competitive actions and among individuals through self- or other-interested behavior. Although the Coase theorem (1960) shows that when transaction costs are zero it is possible to fully delineate property rights and eliminate externalities, transaction costs are never zero. Thus, since property rights are never fully delineated, every action has the potential to create reciprocal costs or benefits for other parties. For example, product development could generate negative externalities for competitors through the loss of sales but might generate positive externalities if R&D spillovers create new opportunities (Alnuaimi & George, 2016).

Exclusion

Exclusion helps protect the firm from negative externalities generated by other firms by forestalling actions that those parties may believe are beneficial to them but damaging to the focal firm (Coase, 1960). A firm’s ability to exclude competitors from creating negative externalities is important for protecting its property rights. Drawing on property rights theory, we define exclusion as a firm’s actions that prevent or limit other parties’ ability to imitate or expropriate the property rights a firm uses to exploit market opportunities. As noted above, the essence of exclusion lies in limiting market competition by either reducing the perceived gain associated with an opportunity or increasing the perceived costs of exploiting it.

Exclusion can be achieved either by deploying resources that competitors cannot imitate or by building barriers or exploiting preexisting barriers that limit competitors’ entry into the marketplace. Notably, some resources that prevent imitation are inherently non-tradable in the market (Barney, 1986), and some barriers may stem from initiatives aligned with non-market resources. Thus, we adopt the adage that success comes not only from winning battles but also from breaking the enemy’s resistance without fighting (i.e., The Art of War by Sun Tzu, Chapter 3). In that respect, our theory explains why some family firms can survive even when they do not achieve the same level of pecuniary returns as nonfamily firms.

Coase (1960) suggested that the right of exclusion is essential but not unlimited. Exclusion is vital because an inability to exclude could prevent owners from fully using their property, depreciate its transfer value (Alchian & Demsetz, 1972; Demsetz, 1967), and/or reduce the rents obtainable from it because of, for example, competitive imitation (Foss & Foss, 2005). Thus, the ability to exclude is a fundamental condition for property ownership (Merrill, 1998). Indeed, Demsetz (1967) contends that exclusion distinguishes private ownership from common ownership as defined above. In keeping with this distinction, we view business opportunities that have not been exploited as common property and base our theoretical arguments on how family owners exclude nonfamily agents from access to the rights associated with opportunities exploited by using the human and nonhuman assets of the family firm and on how family owners minimize externalities from the actions of other parties.

While exclusion has not always been the central construct, it has been widely recognized in the literature. For example, the strategic management literature argues that firms utilize isolating mechanisms (Lippman & Rumelt, 1982) to protect, limit, or prevent other firms from imitating the resource configurations that represent their strategy. This aligns with the logic of resource-based theorists who suggest that excluding competitors by developing valuable, rare, imperfectly imitable, and non-substitutable resources/capabilities is key to sustained competitive advantage (Barney, 1991, 1995). Moreover, scholars recognize that firms are often motivated to use strategic initiatives to create ex-ante and ex-post limits to competition (Peteraf, 1993) and prevent competitors from developing adequate responses (Andrevski & Miller, 2022; Chen & Hambrick, 1995). So, firms can intentionally target emerging or neglected market opportunities that competitors are not incentivized to capture because of the specificity or the magnitude of required investments or the lack of sufficient pecuniary returns (Chen & MacMillan, 1992).

Meanwhile, in the property rights literature, exclusion occupies a central position and can take multiple forms. Classic property rights theorists argue that exclusion stems from enforcing property rights that are multifaceted and partitionable (Alchian, 1977; Ostrom, 1990). The literature recognizes that firm decision-makers are expected to manage the partitioning of property rights so that the firm can discover and exploit new opportunities that generate and sustain superior performance (Kim & Mahoney, 2005, 2010). We theorize that family firms benefit from three bases of exclusion: goal-based, governance-based, and resource-based. These bases of exclusion constrain nonfamily firms by limiting the pecuniary returns associated with the opportunities (i.e., goal-based exclusion) or increasing the costs involved in accessing or appropriating the opportunities (i.e., governance- or resource-based exclusion).

Goal-based exclusion

We define goal-based exclusion as actions taken to achieve goals that create ex-ante limits to competition. Kirzner (1973) suggests that the extent to which firms are alert to the value of an opportunity determines who initially captures the associated property rights. Likewise, a firm’s goals shape the opportunities it seeks and remains alert to identify. For instance, Casio intentionally focuses on market segments with low pecuniary returns in the watch industry (Glasmeier, 2000). This allows the company to identify emerging opportunities in these market segments and ensure that traditional Swiss watch companies that focus on high-end market opportunities will not pose a competitive threat (Raffaelli, 2013). As explained below, because family firms pursue both pecuniary and FCN goals, the set of opportunities that allows those goals to be achieved is wider than the set of opportunities available to nonfamily firms, which are unable to trade off the achievement of FCN goals for the achievement of pecuniary goals (Chua & Schnabel, 1986; Osakwe, Chua, & Chrisman, 2022).

Governance-based exclusion

As the property rights literature has long noted, firms’ ability to exclude others from appropriating their property rights depends on how well they can enforce those rights (Umbeck, 1981). Therefore, we define governance-based exclusion as the internal organization of firms that allows them to enforce their property rights. Studies recognize that different types of governance mechanisms provide various degrees of property rights protection and that effectively enforcing property rights facilitates the ability of firms to obtain the full benefits from their property (Schulze & Zellweger, 2021). Of particular importance here is the notion that effective governance is an essential condition for aligning a firm’s activities with the pursuit of opportunities and ensuring that key resources are properly managed and protected (Foss, Klein, Lien, Zellweger, & Zenger, 2021; Kim & Mahoney, 2010). However, enforcing property rights is costly (Coase, 1960). The costs of enforcement include the financial costs of implementing, maintaining, and utilizing enforcement mechanisms and their effects on incentives (Holmstrom, 1999). To determine the viability of opportunities, owners must compare the cost of enforcement mechanisms against enforcement benefits (Coase, 1960). One example of governance-based exclusion is employee ownership, which can mitigate the problems of employees engaging in opportunistic behavior and underinvesting in their human capital and lead to higher job satisfaction, greater organizational commitment, and lower employee turnover (Buchko, 1993). Indeed, this is a source of advantage for family firms, which uniquely combines the characteristics of investor ownership with management ownership within one or more families (cf. Chua et al., 1999; Hansmann, 1988).

Governance-based exclusion in family businesses serves two essential functions. First, family governance provides the foundation for transferring the family’s goals to the business, ensuring that the business can pursue market opportunities that might offer FCN returns but lower pecuniary returns while maintaining long-term viability. Using the language of property rights theory, family ownership provides advantages in dealing with enforcement problems because it facilitates collaboration among members of the dominant coalition in the selection of compatible goals and the exclusion of incompatible goals (Ben-Shahar, Carmeli, Sulganik, & Weiss, 2023; Chua et al., 1999). In addition, governance-based exclusion reduces the potential for opportunistic behavior and underinvestment by family members, which explains why family-based resources can be deployed in ways that nonfamily firms cannot easily replicate. Unlike resource-based exclusion, the focus here is on the methods of investing resources and deriving returns from those investments, rather than on rights to the inherent attributes of the resources themselves.

Notably, opportunistic behavior may be present in family firms when resources are allocated based on objectives that are misaligned with the vision of the dominant coalition. Relational contracting focused on trust can facilitate monitoring of family agents but these same relationships can make it difficult to sanction family managers who behave opportunistically (Pollak, 1985). Overall, the empirical evidence suggests that opportunistic behavior is less likely to be present in family firms (Chrisman, Chua, & Litz, 2004; Chrisman, Chua, Kellermanns, & Chang, 2007). Moreover, informal agreements rather than formal contracts with rigid specifications should make monitoring less costly (cf. Jaskiewicz, Uhlenbruck, Balkin, & Reay, 2013).

According to Hart and Moore (1990), underinvestment occurs when resource owners (e.g., family employees) fear that the firm will dissipate their resources, including their human capital, which leads them to underinvest in developing those resources. We argue that family governance reduces the problem of underinvestment in family resources for family members, who hold residual claims to firm outcomes, making their investment less susceptible to appropriation. However, family governance can have a positive or negative influence on underinvestment among nonfamily employees, depending upon whether they are treated as well as family members who work in the firm (Verbeke & Kano, 2012).

Resource-based exclusion

Exclusion can also stem from the possession of idiosyncratic resource bundles (Barney, 1991, 1995) that competitors cannot access, appropriate, or imitate. The property rights literature recognizes that firms do not “own” physical resources, but rather “own” property rights associated with physical resources (Foss & Foss, 2005; Kim & Mahoney, 2010). Some of these bundles of property rights are exclusive to the owner, while others are non-exclusive and can be accessed by more than one party simultaneously (Barzel, 1989). Competitive success depends in part on maximizing exclusive resources and minimizing non-exclusive resources. In family firms, resource-based exclusion is a function of socially complex family relationships that restrict the exchange of social capital and tacit knowledge to members of the family.

Resource-based theorists have long claimed that resource attributes might affect the nature of market competition (e.g., Barney, 1991, 1995). For instance, Barney (1986) argues that factor markets are imperfect, making some resources non-tradable, thus preventing competitors from obtaining comparable resources in the market (Chi, 1994). Resources can also be path-dependent, causally ambiguous, and socially complex, and might, therefore, create isolating mechanisms (Lippman & Rumelt, 1982), which prevent competitive imitation (Dierickx & Cool, 1989). Given these considerations, resource-based exclusion stems from the unique attributes of certain resources that can create ex-post limits to competitors’ attempts at appropriation or imitation. For instance, brand reputation creates firm-specific advantages that are difficult for competitors to imitate. Family firms have natural advantages in this regard because of the close and long-term association of the family with the firm. Consequently, consumers and investors tend to trust them more than nonfamily firms (Deephouse & Jaskiewicz, 2013; Lude & Prügl, 2019), which significantly enhances customers’ purchase intentions (Jaufenthaler, Kallmuenzer, Kraus, & De Massis, 2025). For instance, since its founding in 1886, SC Johnson has remained under the leadership of the Johnson family. The company’s branding prominently features the phrase “A Family Company,” directly invoking its family identity. This positioning has helped cultivate consumer trust, framing the company as values-driven and customer-oriented.

Summary

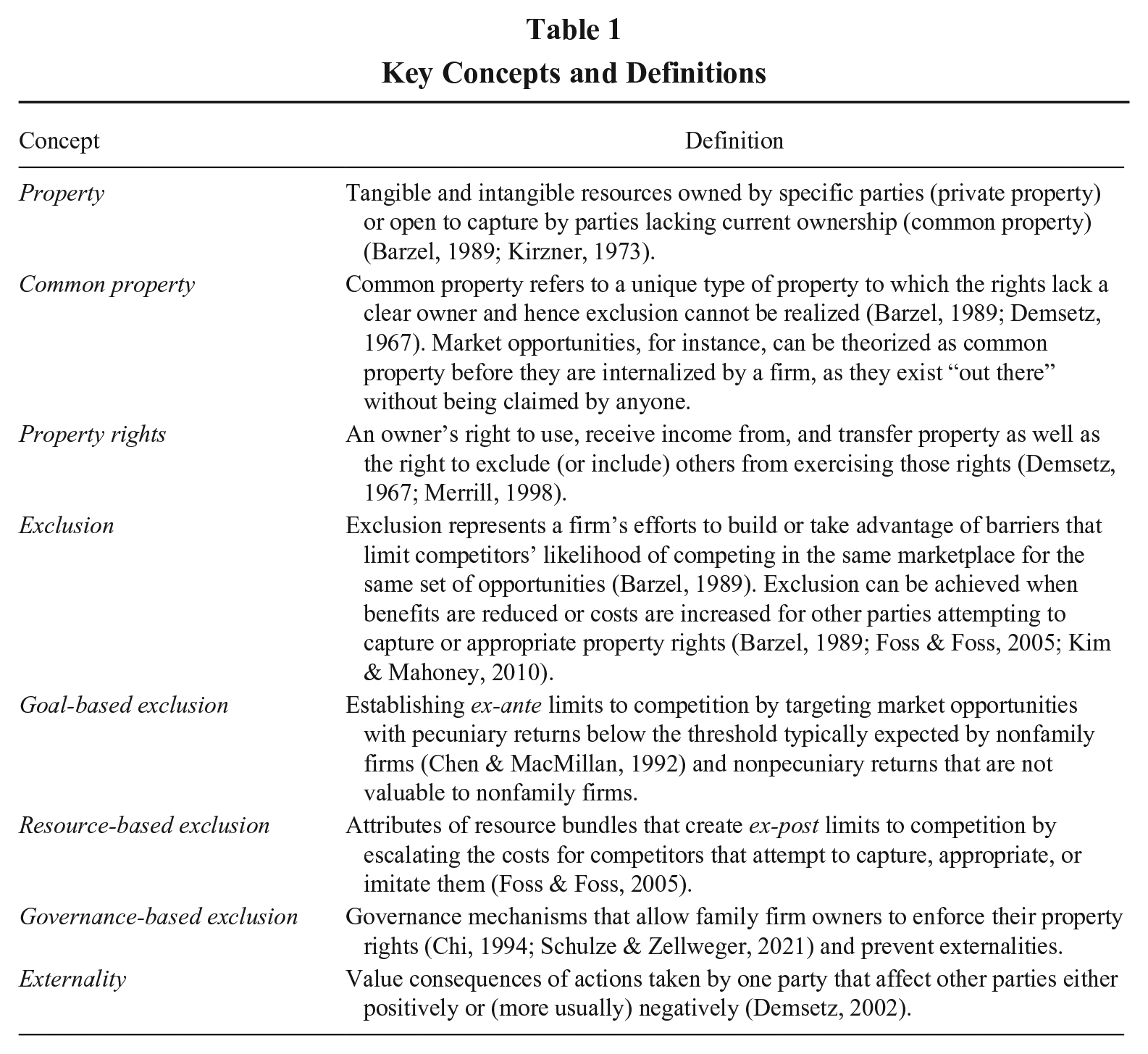

In summary, to realize the benefits of property rights associated with business opportunities, family firms must, to the extent possible, identify opportunities that competitors are unable to access, exploit residual rights of claimancy and control in ways that restrict or limit opportunistic behavior and underinvestment in family resources, and deploy intangible family resources to prevent competitors from imitating the resources used to seize opportunities. Table 1 summarizes the key concepts and their definitions, and the following section applies those concepts to the development of a theory of the family firm.

Key Concepts and Definitions

Advantages of the Family Form of Organization Compared to the Nonfamily Form of Organization

In this section, we develop a theory that seeks to explain why entrepreneurs might select the family form of organization rather than the nonfamily form. This involves comparing family and nonfamily firms to explain why family firms exist, why they are prevalent among the population of organizations, and why they could be expected to endure over time.

In the economics literature, the focus has been on reasons why firms might be better suited than markets in performing economic functions such as producing goods and services (Coase, 1937; Conner, 1991; Holmstrom & Tirole, 1989). Note that the comparison is not according to the outcome (e.g., profit) but according to the method or factor that causes the outcome (e.g., transaction costs). However, as noted above, to develop a theory of the family firm, we must compare two alternative forms of hierarchical organization, namely family and nonfamily firms. To accomplish this purpose, we must, therefore, consider the advantages and disadvantages of family and nonfamily firms to understand when and why one type of organization might be more attractive than the other. Since we focus on why family firms exist, our discussion leans more toward an explanation of the advantages of that choice, although we also discuss the disadvantages of family firms here and in the discussion section.

Goal-Based Exclusion

When markets are in equilibrium, risk-adjusted total returns are assumed to be equal for all opportunities (Fama & French 2004; Fama & Miller 1972). However, it has been demonstrated that assets can earn both pecuniary and nonpecuniary returns, meaning that in at least some instances, total returns can have both pecuniary (e.g., ROI, ROA) and nonpecuniary (e.g., reputation) components (Chua & Schnabel, 1986). This suggests that, in equilibrium, opportunities that provide nonpecuniary returns will have lower pecuniary returns than opportunities that do not provide nonpecuniary returns (Chua & Schnabel, 1986). In this respect, it has been recognized that family firms may derive various nonpecuniary returns, in particular FCN returns, from family ownership and control that are either not available or not as valuable to nonfamily firms (Zellweger et al., 2012) and have no market value outside of their value to the family. As mentioned above, in this article, we focus on family-centered nonpecuniary (FCN) returns that emanate from the affective benefits of family ownership and control of a firm, such as the ability to behave unilaterally and idiosyncratically, to act altruistically to family members, and to engage in transgenerational succession (Berrone, Cruz, & Gómez-Mejía, 2012; Chua et al., 1999; Gómez-Mejía et al., 2007; Schulze, Lubatkin, Dino, & Buchholtz, et al., 2001). Thus, as pointed out by Chua et al. (2018), to assess the overall performance of family firms, it may be necessary to account for these FCN returns, the accumulation of which leads to SEW, which is the stock of affective benefits associated with family control (Gómez-Mejía et al., 2007).

Nonpecuniary goals are likely to exist in family and nonfamily firms (cf. Cyert & March, 1963; Chrisman & Patel, 2012). As they are common to both, these goals generally do not differentiate family firms from nonfamily firms (Chua, Chrisman, De Massis, & Wang, 2018). However, FCN goals are not common to both and indeed only exist in family firms. Thus, as our theory is developed in a comparative sense, we intentionally focus on family-centered nonpecuniary (i.e., FCN) goals as a driver of the distinctiveness between family and nonfamily firms.

Scholars who study the differences between family and nonfamily firms have focused on variations in goals, because goals tend to be one of the key reasons for the differences in strategic behavior of family and nonfamily firms (e.g., Duran, Kammerlander, van Essen, & Zellweger, 2016; Patel & Fiet, 2011; Skorodziyevskiy, Chandler, Chrisman, Daspit, & Petrenko, 2024; Skorodziyevskiy, Sherlock, Su, Chrisman, & Dibrell, 2024). For example, scholars argue that family firms are more reluctant than nonfamily firms to engage in strategic change in some instances, and more willing in others, because of the concerns for the nonpecuniary SEW endowments associated with firm ownership (e.g., Berrone et al., 2012; Chrisman & Patel 2012; Gómez-Mejía et al., 2007). Thus, studies acknowledge that FCN goals and returns (i.e., SEW) are important in family firm decision-making, acting in a way that is similar to the endowment effect (Gómez-Mejía et al., 2007; Zellweger et al., 2012) by increasing the value of the firm for the family through ownership rather than market value or price.

Because achieving FCN goals creates value for the family, family firms may engage in trade-offs between achieving pecuniary and FCN goals (Chrisman, Memili, & Misra, 2014). In fact, the literature suggests that this trade-off or “family effect” may lead family firms to accept lower pecuniary returns on their investment than nonfamily firms (Chua et al., 2018; Osakwe et al., 2022; Zellweger, 2007). Based on this reasoning, we argue that since family firms value FCN returns more than nonfamily firms (cf. Berrone et al., 2012; Gómez-Mejía et al., 2007), they may be willing to accept lower pecuniary returns if an investment also yields FCN returns. As suggested above, we recognize that all firms have nonpecuniary goals that can yield nonpecuniary returns for stakeholders (Cyert & March, 1963), but we assume that nonpecuniary goals other than FCN goals, which are exclusive to family firms, are, on average, equally important to family and nonfamily firms, essentially canceling each other out. Thus, consistent with the family firm literature, we focus only on pecuniary and FCN goals and assume family firms pursue pecuniary and FCN goals while nonfamily firms pursue only pecuniary goals (Chua et al., 2018). For the sake of parsimony, and because of their assumed equal importance, we do not discuss further the nonpecuniary goals or returns that can exist for both family and nonfamily firms, including those associated with the private benefits of control as discussed in the finance literature (e.g., Jensen & Meckling, 1976; Morck, Shleifer, & Vishny, 1988) or with social responsibility as discussed in the management literature (e.g., Carroll, 1979). Using this basis for comparison in our theorizing, we assume the total returns of family firms equal the sum of their pecuniary and FCN returns, whereas the total returns of nonfamily firms equal their pecuniary returns only. Furthermore, we also assume that family and nonfamily firms benefit from achieving goals and that, on average, both types of firms can attain similar levels of benefits from goal achievement, which we equate with their required return. We illustrate this simple equality assumption below using NFF to denote nonfamily firms and FF to denote family firms:

If, as we assume, nonfamily firms are more likely to pursue pecuniary goals in comparison to family firms (e.g., Burkart, Panunzi, & Shleifer, 2003; Chua et al., 1999, 2018; Gómez-Mejía et al., 2007), they should be expected to focus on opportunities that lead to the achievement of pecuniary goals because their total required returns, which are analogous to the cost of capital, come entirely from the achievement of pecuniary goals. Thus:

On the other hand, family firms are assumed to seek both pecuniary and FCN goals. When the returns attached to the achievement of both types of goals are valued, as is the case in most family firms, an ability and willingness to trade off pecuniary returns for FCN returns, or vice versa, to achieve required total returns exists, although there are limits to the trade-off because family firms must still achieve a minimum level of pecuniary returns to survive (cf., Chua et al., 2018; Chua & Schnabel, 1986; Osakwe et al., 2022). Thus,

If we then substitute Equations (2) and (3) into equation (1) we obtain the following equation:

Again, assuming both types of firms gain similar levels of benefits from goal achievement, Equation (4) is equivalent to:

Therefore, since FCN returns can be a valuable substitute for pecuniary returns (Chua & Schnabel, 1986; Osakwe et al., 2022), the required pecuniary returns (or cost of capital) for family firms will be less than the required pecuniary returns for nonfamily firms as long as required FCN returns of family firms are greater than zero. In this case:

Schumpeter (1934) notes that it is possible to order opportunities from high to low based on the pecuniary returns they can generate. Thus, even though family firms are likely to require some threshold levels of both pecuniary and FCN returns (Chua et al., 2018), they should be able to select from a wider pool of potential opportunities than nonfamily firms that cannot trade off one type of return for the other to achieve their goals. In other words, compared to family firms, nonfamily firms will more likely be attracted to opportunities that yield pecuniary returns that meet the requirements of their pecuniary goals because the pecuniary returns of nonfamily firms are the sole determinants of their total required returns. Assuming that the total required returns of family and nonfamily firms are comparable, the minimum pecuniary returns required by family firms must be lower because they obtain FCN returns as well. This expands the set of opportunities available to family firms compared to nonfamily firms. Unless nonfamily firms are willing to accept lower total returns from competition than family firms, they will be effectively excluded from the pursuit of opportunities that have expected pecuniary returns that fail to meet their required total returns. Put differently, as suggested in the following proposition, one of the reasons family firms are more prevalent than nonfamily firms is that their FCN goals open opportunities for them from which nonfamily firms are largely excluded.

Proposition 1: In comparison to nonfamily firms, family firms have a wider pool of opportunities available that will meet their goals.

Similarly, FCN goals can provide family firms with access to long-term opportunities from which nonfamily firms are economically excluded (Lumpkin & Brigham, 2011). We treat long-term opportunities separately because perhaps the most important FCN goal, and indeed a defining feature of family firms, is transgenerational sustainability, a vision to keep the firm under family ownership and control across multiple generations of the family (Chua et al., 1999). Thus, considering long-term opportunities is crucial for our theory. In comparison, nonfamily firms are likely to focus more on shareholder wealth maximization and short-term opportunities. Owners and managers of any type of firm have a finite lifespan, and the concern of nonfamily owners and managers for future generations of unrelated owners and managers is likely to be less than in family firms where future owners and managers are usually related by blood to current owners and managers. If the time horizon of nonfamily firms is shorter than it is for family firms, the discount rates of nonfamily firms for evaluating the value of long-term opportunities should be higher. If family firms attach lower discount rates to the pecuniary returns of long-term opportunities, the range of projects that meet the cost of capital of family firms should be wider than the range of projects that meet the cost of capital of nonfamily firms.

The advantage of family firms over nonfamily firms in the pool of feasible opportunities does not necessarily mean that family firms will be more long-term oriented than nonfamily firms (Chua, Chrisman, Wang, & Wu, 2025). However, family firms will have more long-term opportunities available, which directly address family firms’ desire for transgenerational sustainability (Chua et al., 1999). Furthermore, family firms are less likely to face endgame scenarios in their search for opportunities (Patel & Fiet, 2011) because familial relationships among current and future owners and managers are expected to result in altruistic behavior toward successors, even though altruism may not be reciprocated (Eddleston, Kellermanns, & Sarathy, 2008; Schulze et al., 2001). There is also evidence that discount rates are lower when decisions affect people with close relationships to the decision-maker (Jones & Rachlin, 2006; Rong, Grijalva, Lusk, & Shaw, 2019). This suggests that family firms can gain exclusionary benefits if they have a wider range of long-term opportunities than nonfamily firms. This also suggests that, all else equal, FCN goals can reduce the cost of capital, enabling family firms to survive longer. Thus, we propose:

Proposition 2: The pool of long-term opportunities that meets the goals of family firms will be greater than the pool of long-term opportunities that meets the goals of nonfamily firms.

Although family firms may invest in opportunities from which nonfamily firms are excluded, family firms may also pursue opportunities that offer expected pecuniary returns that are high enough to attract competition from nonfamily firms. In these instances, the ability of family firms to trade off pecuniary and FCN returns to achieve their goals will not protect them from nonfamily competitors. Yet, when the expected returns associated with an opportunity exceed the total required pecuniary returns of family firms, slack can be created, which will not exist, to the same extent, for nonfamily firms that benefit only from achieving pecuniary goals.

As explained earlier, the achievement of FCN goals allows family firms to attain total returns that exceed their pecuniary returns. But if the expected returns, stemming from an opportunity, exceed the goal threshold, it may be possible for family firms to invest the excess pecuniary returns in other activities. Nonfamily firms cannot fully duplicate these investments because they require a higher level of pecuniary returns to achieve the same level of total returns and gain no compensatory benefit from FCN returns. So, if the required pecuniary returns of family firms are lower than the required pecuniary returns of nonfamily firms (Equation 6), and if the expected returns from an opportunity meet the required returns of nonfamily firms, then family firms will be able to obtain the returns required to achieve pecuniary goals and have slack resources available to invest as shown in Equation (7) below.

As suggested by Equation (4) above, these investments can be made in resources that generate either pecuniary returns or nonpecuniary benefits with short-term or long-term payback periods.

In family firms, the most frequent investments tend to be in family human capital (Sirmon & Hitt, 2003). Even when family managers are less capable than individuals from outside the family, investing in family human capital contributes to family firms’ FCN goals as well as the ability to protect their property rights. First, as part of the family system, the human capital of family managers is more difficult for other firms to appropriate compared to the human capital of nonfamily managers working for either family or nonfamily firms. Put differently, family managers are subject to the “family handcuff” owing to their family membership (Gómez-Mejía, Larraza-Kintana, & Makri, 2003: 227). Second, increasing the human capital of family management strengthens the family’s control over nonhuman assets through their expertise in the use of those assets, which helps secure the loyalty of other nonfamily and family employees whose work depends on the use of those assets (Hart & Moore, 1990). Third, investing in family managers can reduce conflicts of interest and information asymmetries, thereby decreasing the need for costly formal control mechanisms (Pollak, 1985). Fourth, family managers can generate higher FCN returns, and at a lower cost, than the additional net pecuniary returns that can be generated by hiring more capable nonfamily managers (Chrisman et al., 2014). Therefore, investing in the human capital of family managers can generate higher total returns (pecuniary + FCN) than investing in the human capital of nonfamily managers. The higher return of this investment may be compounded by an increase in the bonding and bridging social capital of family owners and managers, further protecting family firms’ property rights from expropriation and enabling the capture of additional opportunities (Sirmon & Hitt, 2003).

A family firm might achieve higher total returns by hiring family managers who generate higher FCN returns and lower pecuniary returns than by hiring nonfamily managers who generate higher pecuniary returns but no FCN returns (Chrisman et al., 2014). Ultimately, investing slack pecuniary returns in activities that yield FCN returns could provide exclusionary benefits, making the property rights of family firms more difficult for competitors to appropriate. Hence, goal-based exclusion can enhance governance- and resource-based exclusion, creating complementarities (Hart & Moore, 1990) that are difficult for nonfamily firms to duplicate.

Proposition 3: Family firms that pursue family-centered nonpecuniary goals will have more slack resources than nonfamily firms.

Governance-Based Exclusion

Although investor-ownership is the most widely known form of firm governance, firms may also be owned by their customers or suppliers, as well as the workers who provide the firm with the labor necessary for its productivity (Hansmann, 1988). Family firms represent a hybrid type of governance in which the family, particularly in the early stages of development, represents the firm’s primary source of both capital and labor. As we shall discuss below, the hybrid nature of family firms provides advantages by reducing the possibility of externalities associated with opportunism but can also create disadvantages over time if the interests of the providers of capital and the providers of labor begin to diverge.

In family firms, governance emanates from the owning family’s personalized control and particularistic pursuit of its goals (Carney, 2005). These characteristics provide family firms with the power and legitimacy to make decisions, often without recourse to the wishes of other shareholders or stakeholders. From a property rights perspective, this means that the family’s involvement in governance is a necessary condition for the pursuit of FCN goals or the use of family resources. Conversely, the ability to pursue FCN goals and use family resources tends to increase the value of family ownership (Zellweger et al., 2012), making owners more likely to keep the firm in the family. This is perhaps the greatest strength and weakness of family firms. Family involvement that combines ownership and control, potentially minimizes agency costs and maximizes commitment (Pollak, 1985). However, it also exposes family firms to the potential for principal-principal conflicts if the pecuniary and nonpecuniary interests of family members begin to diverge or personal relationships begin to deteriorate (cf., Eddleston & Kellermanns, 2007; Hansmann, 1988) because of family members’ dual stakes in ownership and management. This problem could be more pronounced in family firms with multiple generations in the business or those operated by multiple families (Chrisman, Madison, & Kim, 2021).

Another type of conflict can occur if family owners succumb to bifurcation bias, a condition that exists when family managers are treated as de facto stewards and nonfamily managers are treated as de facto agents (Verbeke & Kano, 2012). Bifurcation bias can lead to a breakdown in relationships among family firm members and create fault lines between family and nonfamily managers. Bifurcation bias can create managerial disadvantages for family firms if it leads to the avoidance of hiring qualified nonfamily managers or if it creates disincentives for nonmanagers that lead to opportunistic behavior such as shirking (Alchian & Demsetz, 1972). Furthermore, as suggested above, bifurcation bias can increase the risk of underinvestment by nonfamily managers.

Simply put, there are two types of conflicts that damage collective decision-making and create negative externalities in family firms. The first one is of a personal nature either among family members or between family and nonfamily members. The second one is about the priorities between pecuniary and FCN goals and how to achieve them. Both types of conflicts can reduce pecuniary or FCN returns, and often, the two types of conflicts overlap.

Residual claimancy and residual control rights

Classical property rights theory (e.g., Alchian & Demsetz, 1972; Coase, 1960; Demsetz, 1967) defines ownership based on residual claims to income and focuses on externalities associated with negotiating and enforcing contracts, while modern property rights theory (e.g., Grossman & Hart, 1986; Hart & Moore, 1990) defines ownership based on residual rights of control and focuses on factors that may cause holdup when contracts are renegotiated over time. Family governance involves both residual claimancy and residual control rights because family members typically are both owners and managers (Carney, 2005). As such, contracting is facilitated by the familial relationships among members involved in the firm, which usually increases trust, builds social capital, aligns goals, minimizes asymmetric information, and provides natural disincentives for opportunistic behavior (e.g., Pollak, 1985). Chi (1994) suggests that residual claimancy incentivizes owners to control opportunistic behavior (e.g., moral hazard, adverse selection) because they bear the cost of variations in performance and are willing to invest to minimize the problem. Such controls involve contracts that specify the types, levels, and measurement of inputs, outputs, and rewards (Chua, Chrisman, & Bergiel, 2009; Jensen & Meckling, 1976; Fama & Jensen, 1983). However, the desire to maintain family control can lead to excessive risk aversion and a propensity to avoid searching for the financial capital needed for growth (Casson, 1999), leading to resource disadvantages. Thus, an emphasis on the rights of claimancy by some family members and rights of control by other family members can lead to family conflict rather than cohesion.

Governance characteristics of family business

We argue that governance-based exclusion in family firms may lead to fewer instances of opportunistic behavior and underinvestment than in nonfamily firms. Opportunistic behavior occurs when business resources are allocated in ways that deviate from the collective interests of owners. One type of opportunistic behavior occurs when agents deploy resources to serve their personal interests instead of the interests of principals. However, opportunistic behavior in family firms can also arise from activities driven by the pursuit of purely pecuniary or FCN goals that conflict with the collective interests of the family’s dominant coalition, which include the achievement of both pecuniary and FCN goals.

Opportunistic behavior can be controlled through monitoring, which is costly. In family firms, monitoring family agents is easier because of lifelong intimacy and can usually be handled through relational contracting (Klein, Mahoney, McGahan, & Pitelis, 2012) that focuses on negotiated means and outcomes based on trust and informal agreements rather than formal specifications (Gómez-Mejía, Nunez-Nickel, & Gutierrez, 2001). The close relationships among family firms often provide deep knowledge about agents’ behavior, as well as encourage reciprocal altruism that restrains opportunism (Chrisman et al., 2004). These relationships, behaviors, and knowledge are generally unavailable in nonfamily firms. Nonfamily firms may be excluded from pursuing opportunities when substantial contracting (negotiating) and monitoring (policing) costs must be incurred because family governance creates a unique cost advantage that nonfamily firms cannot match.

The second challenge that family firms may be able to mitigate through governance-based exclusion is the problem of underinvestment. As stated above, residual control rights of family firms are vital since these rights may address the challenges associated with contract renegotiation and ensure that individuals who have access and power over the critical assets of the firm have been properly prepared for that role. By ensuring that the individuals who have invested in the assets or whose skills are indispensable to the effective application of the assets have control (Hart & Moore, 1990), problems of holdup (i.e., contract renegotiations that allow one party to appropriate income or control from another party) that encourage underinvestment can be minimized. Transgenerational succession intention, a key FCN goal, helps prevent holdup and generates SEW (Berrone et al., 2012; Chua et al., 1999; Gómez-Mejía et al., 2007). The ability to prevent holdup is important because it allows potential successors to prepare for a leadership role in the family firm from an early age with a lower risk that their human capital investments will be dissipated. Thus, family governance helps mitigate the underinvestment of family members in their human capital in a way that is unavailable to nonfamily firms (cf. Hart & Moore, 1990).

Proposition 4: Family firms have lower governance costs associated with contracting, monitoring, and underinvestment than nonfamily firms.

In addition, residual claimancy and residual control rights, combined with family involvement, may create other governance characteristics in family firms that serve to exclude nonfamily firms and help explain why the family form of governance is so prevalent. As noted, family firms may pursue opportunities from which nonfamily firms are excluded because of the lower level of expected pecuniary returns associated with those opportunities. At the same time, family governance can reinforce goal-based exclusions, because family involvement is thought to promote parsimony in investments and operating costs (Carney, 2005), further increasing the range of opportunities available. Owing to their altruistic tendencies (Schulze et al., 2001), residual claimancy, and pursuit of FCN goals, family managers may also be willing to accept lower immediate compensation in favor of higher long-term compensation or firm valuation.

Thus, through parsimonious governance, family firms may sometimes obtain pecuniary returns comparable to those of nonfamily firms even when the opportunities pursued are not as lucrative. In the language of property rights theory, this means that family firms can exclude rivals not only because nonfamily firms may not be interested in some of the opportunities that family firms are chasing, but also because nonfamily rivals cannot duplicate the cost advantages family firms enjoy. Of course, this assumes that family governance facilitates rather than hampers collective decision-making (Hansmann, 1988). Thus, we propose:

Proposition 5: The governance structures of family firms can more effectively reduce operating costs and investment requirements than the governance structures of nonfamily firms.

Resource-Based Exclusion

Resources can be viewed as bundles of property rights (Foss & Foss, 2005) in that property rights are sanctioned behaviors among decision-makers in the use of potentially valuable resources (Kim & Mahoney, 2010). Similarly, the family business literature recognizes that family-owned and -managed firms may possess valuable family-endowed resources that are rare and difficult to imitate (Habbershon, Williams, & MacMillan, 2003; Sirmon & Hitt, 2003). Using the terminology of property rights theory, family owners can capture a higher level of economic rents from family resources because competitors are largely excluded from access to those property rights (Demsetz, 1967). Unlike goal-based exclusion, which is likely to be important when a family firm targets market opportunities with low pecuniary returns, resource-based exclusion is more likely to be important when a family firm’s resources provide the basis for competitive advantages. Resource-based exclusion is realized when it is costly for competitors to either acquire the resources from factor markets or imitate them. Certain types of family resources, such as family-based social capital, are non-tradable (e.g., Dierickx & Cool, 1989; Gedajlovic & Carney, 2010) and thus are not likely to be obtained by nonfamily firms. In fact, there is simply no factor market in which organizations can bid for family-based social capital (cf. Barney, 1986). In addition, the knowledge resources embedded in family social capital and human capital, are imperfectly mobile, meaning that nonfamily firms would encounter difficulty in acquiring these resources from family firms or duplicating them (cf. Peteraf, 1993). The imperfect mobility of family resources arises from their knowledge-based and socially complex nature, which develops through family members’ long-term engagements in the firm and is embodied in the bonding of family members in a family firm through familial relationships. To convince family members to leave the family firms, nonfamily firms would need to compensate them pecuniarily for their loss of SEW (Berrone et al., 2012). But such compensation may exceed the economic value of family members in the external job market (Chrisman et al., 2014), meaning that nonfamily firms may be unwilling (or unable) to pay such compensation. Taken together, nonfamily firms may be excluded from obtaining certain types of family resources because the value of these resources is firm-specific, meaning that these resources are less valuable and/or more costly to acquire for nonfamily firms than family firms, and that at least part of the value of family-based resources is lost once the family member is separated from the family (Zellweger et al., 2012).

Furthermore, knowledge resources in family firms are often tacit, imperfectly imitable (e.g., Habbershon et al., 2003), and associated with family interactions (Arregle, Hitt, Sirmon, & Very, 2007). These characteristics mean that nonfamily firms face uncertainty and difficulty replicating these resources (Gedajlovic & Carney, 2010). Given that some tacit knowledge is only shared among family members, nonfamily competitors might not understand the kind of knowledge that is responsible for superior performance in the family firm or may not know how it is used. Indeed, owing to causal ambiguity, even family owners may fail to realize the source of their competitive advantages or disadvantages. If so, family owners’ biases toward family-based heritage assets (Verbeke & Kano, 2012) may have hidden benefits as well as costs.

In addition, tacit knowledge, which refers to learned skills and path-dependent organization routines (Ambrosini & Bowman, 2001), is often created, accumulated, and shared since childhood by family members and reinforced by their participation in business activities from an early age (Cabrera-Suarez, De Saa-Perez, & Garcia-Almedia, 2001; Sirmon & Hitt, 2003). Thus, unless nonfamily firms can replicate the early life and growth experiences of the owning family, they are excluded from fully replicating the tacit knowledge generated in a family firm. Furthermore, there are apt to be many different and interrelated types of tacit knowledge linked together in a complex family system, which further increases the difficulty of replication.

The value-creating function of family resources partially relies upon other family resources, and the overall configuration of family-based resources is indivisible in the sense that the economic value of the family firm will rapidly depreciate if a subset of the collection of family resources is removed. For example, two unique types of family resources are patient capital and survivability capital. Patient capital refers to financial resources that are “invested without the threat of liquidation for long periods,” while survivability capital represents pooled financial, human, and capital assets that “family members are willing to loan, contribute, or share for the benefit of the family business” (Sirmon & Hitt, 2003: 343). Patient capital and survivability capital are indivisible from social capital because neither can be obtained unless the family’s social capital is strong. Similarly, social capital is less likely to endure if family members are unwilling to provide the family firm with patient and survivability capital.

Thus, in family firms, family-endowed resources are indivisible such that they are more valuable collectively inside the family firm than separately outside the family firm (cf. Chi, 1994; Hart & Moore, 1990). The complementarity of family resources (cf. Grossman & Hart, 1986) largely stems from the fact that family members often share a converging understanding of the business and often have high trust in each other (Muñoz-Bullón, Sanchez-Bueno, & De Massis, 2020). Trust facilitates alignment of interests and collective decision-making, which Hansmann (1988) suggests are essential for effective ownership. As such, some of the resources found in family firms are likely to be less valuable to nonfamily firms, which generally lack comparable levels of mutual understanding and trust amongst owners, managers, and employees. If family-endowed resources are less valuable in a nonfamily firm context, the incentive for nonfamily firms to appropriate those resources is diminished. In sum, some family resources are non-tradable, imperfectly mobile, imperfectly imitable, and indivisible, all of which helps exclude nonfamily firms from accessing, obtaining, or using these resources to imitate family firms. Thus, we propose:

Proposition 6: Compared to nonfamily firm resources, family firm resources are more likely to be non-tradable, imperfectly mobile, inimitable, and indivisible.

Incomplete Exclusion: The Importance of Goals, Governance, and Resources of Family Firms

The discussion thus far is based on an underlying assumption that entrepreneurs will often choose the family form of organization over the nonfamily form because they can (1) pursue opportunities that have pecuniary returns that are lower than those acceptable to nonfamily firms but offer long-term FCN returns that some entrepreneurs will find attractive, (2) exploit a system of family governance characterized by close family relationships and strong residual rights of claimancy and control that can reduce opportunism and underinvestment, and (3) use non-tradable, imperfectly mobile, inimitable, and indivisible family resources that are difficult to duplicate. All three features directly relate to the multi-generational aspect of family involvement in business. But it is also possible that some family firms might lack or lose some of these exclusionary benefits over time. Below, we discuss incomplete combinations of goals, governance, and resources and explain why organizations with incomplete combinations of these characteristics may be unstable and less likely to continue to compete as family firms in the long-term or, in some cases, survive as firms.

Goals and/or resources without governance

This configuration makes it infeasible for a family to sustain its business operations as a family entity, since without family governance the family lacks the level of residual claimancy and residual control needed to exclude nonfamily stakeholders from determining the firm’s goals or the use of its resources. Put differently, family goals are simply goals and family resources are simply resources without the presence of family governance.

For instance, without strong governance, business decisions may be driven by the preferences and demands of external customers and stakeholders with high bargaining power (cf. Coff, 1999), which may force out FCN goals in favor of purely pecuniary goals. At the same time, the characteristics of these external parties, particularly those embedded in the local community, influence whether economic and noneconomic exchanges are based on enduring relationships or short-term transactions, thereby strengthening or weakening the firm’s ability to enforce governance-based exclusion. For example, founded by the Ferrero family in 1946, Ferrero has worked for decades with the same hazelnut suppliers, key partners in the production of Nutella. Strategic decisions, including the leadership transition from founder Michele Ferrero to his son Giovanni and international acquisitions such as Thorntons in the UK, were partly shaped by input from these trusted, long-standing external partners.

Furthermore, Gersick et al. (1997) note that as a family business evolves over time, its ownership structure often transitions from controlling owners to sibling partnerships, and eventually to cousin consortiums. As ownership becomes increasingly distributed among multiple family members, often through intra-family transgenerational succession, the problem of weak or limited governance-based or goal-based exclusion may arise (cf. Gómez-Mejía et al., 2007). Such family firms are often characterized by multiple later-generation owners who prioritize their personal interests or those of their nuclear families over the collective interests of the extended family. As a result, not only is collective action among family owners hindered, but nonfamily parties may also gain greater influence in decision-making. Indeed, without family governance, a firm cannot be categorized as a family business because while it may be willing to behave as a family firm it will lack the discretionary ability to do so (De Massis, Kotlar, Chua, & Chrisman, 2014).

Governance and resources without goals

This combination represents family firms that use their resources to maximize pecuniary returns without regard to FCN returns, just like nonfamily firms (Chua et al., 2018). Family firms without the willingness to pursue FCN goals may be motivated to obtain additional nonfamily resources, whose presence may mitigate the exclusionary effects stemming from family resources. More importantly, excessive nonfamily resources can give rise to additional contracting, monitoring, and underinvestment issues. That is to say, the exclusionary effects of family resources and family governance will ultimately fade if FCN goals are not present. These family firms are likely to eventually be sold off rather than transferred to the next generation since the former option may be considered more lucrative and, financially, less risky. Thus, this type of family firm is unlikely to be sustainable indefinitely as a family firm because its success is apt to lead to a transition into a nonfamily firm to obtain additional resources for growth or to cash out so that subsequent generations can pursue other opportunities. Without FCN goals, the investor aspects of the firm will tend to crowd out the family aspects of the firm over time, potentially leading to a transition from a family firm to a nonfamily firm. Indeed, many well-known nonfamily firms such as Ben & Jerry’s (US), Perrier (France), Skoda (Czech Republic), and Gucci (Italy), were originally family firms. Interestingly, some families have been known to buy their firms back a few years after selling them. For instance, the Grote family bought back Donatos Pizza from McDonald’s, and the Davidson family bought back Harley-Davidson from AMF. These unique scenarios occur when a nonfamily owner fails to duplicate or improve upon the pecuniary returns achieved by the previous family owner, and/or when the previous family owner is unable to adapt to the loss of SEW associated with the sale of the family firm.

Goals and governance without resources

This combination includes family firms that focus on opportunities with lower pecuniary returns offset by FCN returns and strong family control. However, these family firms lack adequate family resources to exclude competitive appropriation over time. Although the ability to achieve FCN goals through the alignment of interests of family members is one of the reasons why family firms exist alongside nonfamily firms, a lack of family resources may make it difficult to achieve the minimum level of pecuniary returns needed for survival, especially if internal expectations and/or external competition escalate. If a minimum level of pecuniary returns is not achieved, the social, patient, and survivability capital needed to sustain the family firm may be exhausted. Ultimately, there is a higher probability that a family firm without adequate family-based resources could face bankruptcy, liquidation, or closure owing to persistently low performance.

Proposition 7: In the long term, family firms with higher levels of incomplete exclusion will have fewer sustainable advantages than nonfamily firms and thus will be more likely to cease to exist as firms or as family firms.

Boundaries and Contexts of Family Firms

A theory of the family firm needs not only to explain why the family form of organization is selected rather than the nonfamily form, but also to identify the boundaries of the family firm in terms of the limits to its scale and scope (Conner, 1991; Holmstrom & Tirole, 1989). We attempt to address how the scale and scope of family firms might affect the environments that they are best able to occupy. We refer to scale as the size of family firms, while scope refers to the breadth of family firms’ activities. Typically, scale is related to the volume of production, market share, or workforce size, while scope concerns the range of products, geographical presence, and served markets. We discuss the scale and scope of family firms below.

Limits to the Scale and Scope of Family Firms

From a property rights perspective, and in keeping with the requirements of a theory of the firm, goals, governance, and resources help explain the scale and scope of family firms. Indeed, these aspects of a theory of the family firm have frequently appeared in the literature that discusses how SEW endowments influence strategic change in family firms (e.g., Chrisman & Patel, 2012; Gómez-Mejía et al., 2007; Gómez-Mejía, Makri, & Larraza-Kintana, 2010). The FCN goals of family firms require that the family retains ownership and control of the firm’s property rights, a situation that does not exist in nonfamily firms. This limits the extent to which family firms can increase their scale and scope in comparison to nonfamily firms because, at some point, expansion requires that capital be obtained from external sources, and professional nonfamily managers hired. In both instances, family firm owners must sacrifice some amount of their rights of claimancy or control to other investors to grow beyond the level possible using only resources obtained directly from the firm’s internal cash flows and the family. Many family firms are unwilling to grow beyond this point because to do so reduces their FCN returns and strains the capacity of the governance system (Stewart & Hitt, 2012), which can potentially lead to principal-principal agency problems between family and nonfamily owners. Documented examples of family firms with particularly serious principal-principal conflicts include Parmalat in Italy (Enriques & Volpin, 2007) and SARL Peronnet in France (Johnson, La Porta, Lopez-de-Silanes, & Shleifer, 2000).

In contexts where the institutional environment offers weak property rights protection, hiring nonfamily managers can jeopardize the use rights and pecuniary returns of family owners (e.g., Ilias, 2006). Even among larger family firms that have already traded some of their FCN returns for pecuniary returns to grow, the literature shows that there can be limits to their willingness to sacrifice additional FCN returns to continue to grow and develop (e.g., Chrisman & Patel, 2012; Gómez-Mejía et al., 2007). Indeed, research suggests that family firms of all size classes are smaller than comparable nonfamily firms (e.g., Anderson & Reeb, 2003; Cromie, Stephenson, & Monteith, 1995; Kotey, 2005; Villalonga & Amit, 2006).

Another constraint on the scale and scope of family firms compared to nonfamily firms is strong attachments to the heritage resources developed from the initial investments of the entrepreneurs who founded the firm (Sharma & Manikutty, 2005; Verbeke & Kano, 2012). Growth often involves strategic change (Skorodziyevskiy, Sherlock, et al., 2024), which can entail investments in new assets and divestments of old assets. However, heritage resources may be of special significance to family owners if they generate FCN returns. Furthermore, because family involvement is indispensable to the management of heritage assets, the use of these assets may reinforce the property rights of family owners and reduce the probability that successors will underinvest in their human capital because of fear of holdup (cf. Hart & Moore, 1990). Consequently, family firms will often be reluctant to pursue opportunities that require divestment of heritage assets because this will potentially be inconsistent with the family’s goals, governance, and resources. Moreover, as noted above, if heritage assets are socially complex and tied to the family’s SEW, their value may be underestimated because the FCN value of heritage assets may have a synergistic relationship with their pecuniary value. Thus, the desire to maintain the ownership rights associated with family resources represents a primary factor that limits the scale and scope of family firms in comparison to nonfamily firms.

Proposition 8: The limits to the scale and scope of family firms constrain their growth more than the limits to the scale and scope of nonfamily firms; hence, family firms tend to be smaller.

Opportunities Family Firms Exploit

Studies show that family firms of all sizes (e.g., SMEs, large firms) and scopes can be found and even flourish in virtually any industry and institutional environment (e.g., Gedajlovic, Carney, Chrisman, & Kellermanns, 2012; La Porta et al., 1999; Skorodziyevskiy, Sherlock, et al., 2024; Villalonga & Amit, 2006). This may be because the goals, governance, and resources of family firms provide the advantages (and disadvantages) of both investor-owned and worker-owned firms (cf. Hansmann, 1988). However, it is useful to briefly elaborate on the types of opportunities that are particularly apt to provide family firms with the exclusionary advantages that we have enumerated. These include opportunities that provide lower expected pecuniary returns, higher expected FCN returns, and greater ability to trade off pecuniary and FCN returns, and that enable family firms to maximize the benefits of their governance structure and resources.

First, as Carney (2005) discusses, family firms have advantages in pursuing opportunities characterized by scarcity, low barriers to entry, mature technologies, and high labor intensity. In these environments, pecuniary returns generally approach those associated with perfect competition and thus have lower value to nonfamily firms that gain few, if any, offsetting nonpecuniary benefits. Such environments are especially prevalent in emerging economies (Skorodziyevskiy, 2025), where firms engaging in low-wage production of commodities tend to be located.

Second, in some industries, the very nature of the goods and services themselves provides nonpecuniary returns such as glamour, status, or reputation to owners. Demsetz and Lehn (1985) suggest that sports (e.g., Dallas Cowboys, football; Manchester United, soccer; New York Yankees, baseball) and media businesses (e.g., Fox News) are two prominent examples (see also Burkart et al., 2003). To this list, we would add businesses devoted to collectibles, including art (e.g., Hauser & Wirth, Switzerland) and wine (e.g., E. & J. Gallo Winery, US), which provide nonpecuniary returns through the possession, preservation, and cultivation of the objects themselves, even though the owners may act only as temporary caretakers (Chua & Schnabel, 1986; Le Breton-Miller & Miller, 2015).

Finally, nonpecuniary returns and family resource advantages are potentially high in industries that offer owners unusual potential to involve family members in ways that achieve their goals for transgenerational sustainability (Chua et al., 1999). For example, family firms have traditionally dominated agriculture (e.g., Cargill, Inc., US) and craft (e.g., Fabindia, India) businesses (e.g., Hansmann, 1988; Le Breton-Miller & Miller, 2015; Pollak, 1985), which require long-term training and mentoring to inculcate tacit knowledge and build commitment through master and apprentice relationships. At the same time, family firms benefit from a less expensive and more reliable family labor force, which helps offset the low pecuniary returns that are characteristics of many of these opportunities. This allows family firms to increase not only their scale but also their scope.

Proposition 9: Family firms are more prevalent than nonfamily firms in industrial and institutional contexts where opportunities are characterized by scarce environments, status, reputation, possession effects, or transgenerational sustainability potential.

The importance of FCN returns associated with family social capital and altruism is likely more pronounced in businesses when property rights protection is made more complicated and costly by difficulties in metering productivity. From a property rights view, metering productivity (Alchian & Demsetz, 1972) is directly related to the residual right of claimancy, as challenges in monitoring might enhance the importance of informal governance mechanisms often used in family firms (Chi, 1994). Consistent with our discussion of governance-based exclusion, when it is difficult to monitor business activities directly, involving family members in the firm becomes more advantageous because it reduces the possibility of opportunistic behavior. For example, family firms tend to be prevalent in retail and service industries in which the measurement of productivity must account for both low product and service standardization and the simultaneity of production and consumption (Fang, Memili, Chrisman, & Penney, 2017).

Proposition 10: Family firms are more prevalent than nonfamily firms in industrial and institutional contexts where metering productivity is more difficult.

Like goal- or governance-based exclusion, resource-based exclusion might also vary by industrial or institutional context, which could be responsible for the higher importance of certain types of resources. As family resources are likely to be non-tradable, imperfectly mobile, inimitable, and indivisible, their value is expected to be more pronounced in family firms than similar resources in nonfamily firms. Numerous scholars (e.g., Carney, 2005; Gedajlovic & Carney, 2010; Pearson, Carr, & Shaw, 2008) suggest that, unlike nonfamily firms, family firms might have a unique advantage in obtaining and utilizing family social capital, which facilitates the creation and development of family human capital (cf. Coleman, 1988). Thus, in contexts where privileged access to exclusive networks (Lester & Cannella, 2006), “handshake deals” with business partners (Steier, 2001), and mutual adaptations in business relationships (Bertrand & Schoar, 2006) are valuable, family firms might obtain an advantage over nonfamily firms. In addition, Gedajlovic and Carney (2010) suggest that in contexts where tacit knowledge is important, family firms might have an advantage and thus be more prevalent than nonfamily firms. On the other hand, because the family is limited in size and the intellectual capacity of its members may, over time, regress to the mean, family firms may find long-term survival difficult in contexts where rare and unusual abilities or complex technologies are required (Pollak, 1985). The fate of Wang Laboratories after the ascension of An Wang’s sons and his subsequent death illustrates this dilemma (Kenney, 1992). Therefore, we propose the following:

Proposition 11: Family firms are more prevalent than nonfamily firms in industrial and institutional contexts where social capital and tacit knowledge are highly valued and less prevalent where uncommon abilities or complex technologies are required.

Discussion and Implications

Our purpose is to move closer to a theory of the family firm by considering how family-centered nonpecuniary goals, family governance, and family-endowed resources affect the kinds of advantages and disadvantages that family firms might possess compared to nonfamily firms. Using property rights theory, we explain how the addition of FCN goals allows family firms to capture opportunities that are unavailable to nonfamily firms. We also elaborate on how family governance and family resources might help protect property rights that are not fully delineated in situations where competitors cannot be easily excluded from pursuing those opportunities. Simply put, we argue that in comparison to nonfamily firms, family firms exist because (1) the pursuit of FCN goals provides opportunities unavailable to nonfamily firms, (2) family governance facilitates collective decision-making, which decreases the cost of negotiating and enforcing contracts, and reduces underinvestment in human capital, and (3) they can exploit family-based resources that are untradable, immobile, inimitable, and indivisible. The propositions flowing from our arguments on the existence and boundaries of family firms are summarized in Table 2. Testing the propositions opens new research opportunities.

Summary of Propositions

Our theory can also be used to explore the bases of family firm heterogeneity. Further research is needed to apply our theory in examining how and why exclusion based on combinations of goals, governance, and resources might contribute to family firm heterogeneity (Daspit et al., 2021, 2023) and why they might vary by type of family, family generation, firm size, industry context, and institutional environment. Additionally, as previously mentioned, an incomplete set of exclusions, variations in business scale and scope, and contextual factors related to the opportunities that family firms exploit may be among the primary drivers distinguishing sustainable family firms from short-lived ones.