Abstract

Corporate foundations (CFs) are increasingly prominent vehicles for channeling commercial resources toward social causes. However, their pursuit of social missions may be shaped by the strategic priorities of their corporate sponsors. Drawing on a longitudinal panel dataset of 214 Chinese corporate foundations from 2009 to 2022, we examine how changes in sponsor firms’ business portfolios are associated with inconsistency in CFs’ philanthropic engagement, and identify organizational conditions under which this association is attenuated. We find that as sponsor firms adjust their business portfolios, their CFs are more likely to alter their portfolios of philanthropic activities, indicating a destabilizing association. This association is weaker when CF executives have stronger nonprofit backgrounds and when foundations receive a greater proportion of funds from non-corporate donors. Furthermore, we document an asymmetric pattern consistent with activity compartmentalization: under these organizational conditions, changes in sponsor firms’ business portfolios are less strongly associated with changes in mission-related activities than with changes in mission-unrelated activities. These findings contribute to research on dependency management by identifying organizational conditions associated with reduced sensitivity to sponsor firms’ business changes, and by highlighting a form of buffering within prosocial activities under conditions of close oversight.

Introduction

The nonprofit sector has witnessed a significant shift towards adopting business models and practices (Battilana, Lee, Walker, & Dorsey, 2012; Hwang & Powell, 2009), contributing to the rise of corporate foundations (CF) in recent decades. In the United States, CFs accounted for around 9% of total foundation giving and one-third of total corporate giving in 2018 (Candid, 2020). In emerging markets such as China, CFs have experienced rapid growth over the past 2 decades, with their share of the total charitable foundation population increasing from 2% in 2004 to 20% in 2020, representing 15% of total foundation giving (G. Chen, Wang, & Sun, 2021). As a distinct form of nonprofit organizations established by corporate entities, CFs channel financial resources and business expertise from sponsor firms into philanthropic endeavors. Unlike the often ad hoc nature of direct corporate giving, CFs are expected to pursue social objectives in a more structured and sustained manner, given their formal nonprofit status and regularized philanthropic programming (Brown, Helland, & Smith, 2006; Westhues & Einwiller, 2006).

Despite their potential to leverage private sector resources for social good, concerns persist regarding CFs’ effectiveness in fulfilling their societal promises (e.g., Boodoo, Henriques, & Husted, 2022; Koushyar, Longhofer, & Roberts, 2015; Rey-Garcia, Sanzo-Perez, & Álvarez-González, 2018). As nonprofit entities with tax-exempt status, CFs are expected to advance social missions as their core organizational purpose (Gee, Nahm, Yu, & Cannella, 2023; Moore, 2000). However, prior research has focused primarily on the strategic benefits CFs provide to sponsor firms—such as enhancing corporate image or managing stakeholder relations (e.g., Gehringer, 2021; Westhues & Einwiller, 2006)—while devoting less attention to how CFs pursue their social missions over time. Emerging scholarship suggests that corporate affiliation may shape CFs’ priorities in ways that align philanthropic engagement with evolving business interests rather than with advancing social goals (Maclean, Harvey, Yang, & Mueller, 2021; Pamphile, 2022; Seo, Luo, & Kaul, 2021). These concerns point to the need to examine how sponsor relationships may constrain CFs in sustaining their pursuit of social missions, and under what organizational conditions such constraints may be attenuated.

Resource dependence theory (RDT) provides a useful lens for understanding how organizations respond to external demands while pursuing their own objectives (Pfeffer & Salancik, 1978). Organizations reliant on powerful actors for critical resources may face tensions when resource providers’ interests diverge from their own goals (Davis & Cobb, 2010; Ozturk, 2021; Wry, Cobb, & Aldrich, 2013). This tension may be particularly salient for nonprofits that depend financially on corporate sponsors whose business priorities do not always fully align with nonprofit missions (Ebrahim, Battilana, & Mair, 2014; Jacobs, Kreutzer, & Vaara, 2020). A recurring concern raised in recent studies is the prevalence of inconsistent social actions—patterns in which philanthropic activities deviate from prior commitments (e.g., Grimes, Williams, & Zhao, 2019; Koushyar et al., 2015; Meijs, 2010). For instance, CFs have been found to engage capriciously in philanthropic activities and are less likely to provide ongoing support to the same social beneficiaries (Koushyar et al., 2015). Such inconsistency undermines sustained engagement with social causes and limits the development of long-term social solutions, and is thus criticized for jeopardizing pursuit of social missions (Cranenburgh & Arenas, 2014; Meijs, 2010; Ranucci & Lee, 2019). These observations highlight a central challenge in CFs’ dependency relationships: responding to sponsor firms’ evolving priorities may coincide with reduced continuity in supporting social beneficiaries who often lack influence over resource allocation decisions. While existing literature recognizes that dependence on corporate sponsors can constrain nonprofit autonomy, the processes through which such dependence is associated with inconsistency in philanthropic engagement—and the organizational conditions under which these associations may vary—remain insufficiently specified.

Although prior research emphasizes the importance of managing dependence in nonprofit–corporate relationships (e.g., Koushyar et al., 2015), the mechanisms through which CFs operate under such dependence remain less clear. RDT identifies two broad approaches to mitigating external constraints: reducing dependence on constraining actors (e.g., corporate sponsors) or buffering organizational activities from external influence without necessarily reducing dependence (e.g., Oliver, 1991; Wry et al., 2013). Yet, both approaches may be structurally constrained in the CF context. First, cultivating alternative dependencies sufficient to offset the dominance of sponsor firms may be difficult when resource asymmetries are entrenched and sponsor firms control critical financial and organizational resources (Casciaro & Piskorski, 2005). Second, buffering strategies often rely on limiting information flows or managing perceptions (Oliver, 1991; Pfeffer & Salancik, 1978), which may be difficult when organizations operate under close oversight. CFs are typically established by and closely affiliated with sponsor firms, which frequently retain substantial oversight over their philanthropic activities (Brown et al., 2006; Pamphile, 2022). Under such conditions, conventional dependency-reduction and symbolic buffering approaches may be constrained. Against this backdrop, we examine two related questions: How are sponsor firms’ evolving business priorities associated with inconsistency in CFs’ philanthropic engagement? And under what organizational conditions can this association be attenuated?

We begin by examining the dynamics through which sponsor firms’ evolving business priorities may shape changes in CFs’ philanthropic activity portfolios. One important source of such inconsistency lies in changes in sponsor firms’ business portfolios and the resulting shifts in stakeholder environments. As sponsor firms expand into or withdraw from particular industries, they encounter new stakeholder groups with distinct expectations and social norms (Campbell, 2007; Kang, 2013; Marquis, Glynn, & Davis, 2007; Su & Tsang, 2015). These shifts may entail changing emphasis placed on different types of philanthropic activities, particularly when firms seek alignment between philanthropic engagement and newly salient business domains. Because CFs depend heavily on sponsor firms for financial and administrative support, changes in sponsor firms’ business portfolios may be reflected in corresponding adjustments in CFs’ philanthropic portfolios. Accordingly, we hypothesize that changes in sponsor firms’ business portfolios are positively associated with changes in their CFs’ philanthropic activity portfolios. This association reflects a potential tension: alignment with evolving corporate priorities may coincide with reduced continuity in supporting special social causes or beneficiaries over time.

We next examine organizational conditions under which this association is weaker. Given the structural constraints faced by CFs—including critical resource dependence and close oversight by sponsor firms—we focus on two interrelated mechanisms: the presence of nonprofit-oriented forces and activity compartmentalization within philanthropic portfolios. Specifically, we propose that the presence of executives with nonprofit backgrounds and the presence of non-corporate funding partners are associated with reduced responsiveness of CFs’ philanthropic portfolios to changes in sponsor firms’ business portfolios. These nonprofit-oriented forces may introduce evaluative criteria and accountability structures that emphasize long-term social objectives, shaping how discretion over philanthropic resource allocation is exercised once such governance features are in place (Teegen, Doh, & Vachani, 2004). In this sense, our theorizing concerns how existing organizational conditions are associated with observable patterns of response, rather than assuming that these conditions are purposively adopted to resist corporate influence.

At the same time, CFs remain dependent on sponsor firms for critical resources, such that outright noncompliance with sponsor priorities may be costly. Under conditions of close oversight, conventional buffering tactics that rely on concealment or symbolic compliance may be difficult to sustain (Drees & Heugens, 2013; Oliver, 1991). We therefore examine activity compartmentalization—distinguishing “mission-related” from “mission-unrelated” activities—as a viable form of buffering within the philanthropic portfolio. Inconsistency in mission-related activities may conflict more directly with CFs’ stated social commitments, whereas mission-unrelated activities may provide a comparatively flexible domain in which adjustments can occur with lower perceived costs. Accordingly, we propose that when nonprofit-oriented forces are present, the association between sponsor firms’ business changes and changes in philanthropic portfolios is weaker for mission-related activities than for mission-unrelated activities. This asymmetric pattern is consistent with a buffering mechanism in which adaptation within philanthropic portfolios is more concentrated in domains involving fewer tensions, while core mission activities exhibit greater stability.

To test these arguments, we compiled a proprietary panel database of all Chinese CFs founded by publicly listed companies between 2009 and 2022. Analyzing 16,765 grant-making projects, we find support for our theoretical expectations. First, changes in sponsor firms’ business portfolios are positively associated with changes in CFs’ philanthropic portfolios. Second, this association is weaker when CF executives have nonprofit backgrounds and when CFs receive a greater proportion of funding from non-corporate donors. Third, the moderating effects of these organizational conditions are more pronounced for mission-related activities than for mission-unrelated activities, consistent with activity compartmentalization within philanthropic portfolios.

Our study makes three contributions. First, we contribute to research on organizations pursuing social missions under conditions of resource dependence by identifying a dynamic pathway through which corporate dependence is associated with inconsistency in philanthropic engagement. Rather than portraying sponsor influence as uniformly dominant, our findings suggest that sponsor firms’ business changes constitute one important source of variation in philanthropic portfolios. Second, we contribute to research on dependency management by examining organizational conditions associated with reduced sensitivity to sponsor firms’ business changes in contexts characterized by entrenched power asymmetries and close oversight. Third, we extend research on buffering by identifying a form of compartmentalization within prosocial activities—distinguishing mission-related from mission-unrelated domains—that is associated with differential stability under external pressure. This mechanism supports CFs and, more broadly, mission-driven organizations, to accommodate shifting environmental demands while sustaining their core mission efforts.

Theoretical Background

Nonprofits’ Reliance on Corporate Sponsors and the Potential Impact on Social Performance

Resource dependence theory (RDT) emphasizes how organizations are shaped by their reliance on external actors for critical resources (Pfeffer & Salancik, 1978). When organizations depend on powerful resource providers, they may face pressures to accommodate externally imposed demands that do not fully align with their own objectives (Davis & Cobb, 2010; Kraatz & Block, 2008; Wry et al., 2013). Such dependence has been associated with reduced organizational autonomy and potential tensions in goal pursuit (e.g., Ashraf, Ahmadsimab, & Pinkse, 2017; Ebrahim et al., 2014; Hallen, Katila, & Rosenberger, 2014).

This tension may be especially salient in relationships between nonprofits and corporate sponsors. Nonprofits are legally and normatively expected to advance social missions as their primary objectives. Regulatory frameworks typically require independent governance boards to oversee adherence to these missions (Moore, 2000). At the same time, reliance on corporate sponsors for financial support may coincide with pressures to align philanthropic engagement with business priorities, creating potential misalignment between social commitments and commercial interests (e.g., Ebrahim et al., 2014; Grimes et al., 2019; Jacobs et al., 2020; Khieng & Dahles, 2015). Empirical evidence suggests that charitable foundations with stronger corporate affiliations sometimes exhibit patterns of funding allocation that differ from those of independent foundations (Rey-Garcia et al., 2018).

Although prior research recognizes corporate dependence as a potential constraint on nonprofit autonomy, fewer studies unpack how such dependence is reflected in patterns of philanthropic engagement over time. Recent work highlights inconsistent social actions—defined as deviations from prior commitments—as a critical concern for CFs’ social performance (Cranenburgh & Arenas, 2014; Koushyar et al., 2015; Meijs, 2010). Many social issues require sustained engagement to produce meaningful outcomes, and discontinuity in philanthropic activity may limit the development of long-term solutions (Ranucci & Lee, 2019). For example, comparative evidence shows that beneficiaries of CFs are less likely to receive consecutive-year support than those funded by independent foundations (Koushyar et al., 2015). In addition, qualitative studies suggest that shifts in corporate priorities may coincide with interruptions to ongoing philanthropic initiatives that have potential to generate social impact (Pamphile, 2022). This lack of long-term orientation raises doubts about CFs’ capacity to foster social innovation or effectively address root social causes (Cranenburgh & Arenas, 2014; Meijs, 2010; Ranucci & Lee, 2019), inviting accusations of hypocrisy and challenges to their legitimacy as nonprofit organizations (Ruth & Strizhakova, 2012). These observations raise questions about how resource dependence may be associated with instability in philanthropic portfolios, and about the organizational conditions under which such associations may vary.

Mechanisms for Mitigating External Constraints in Resource Dependency

Given the potential influence of corporate sponsors, a central question concerns how organizations operate under dependence while retaining commitment to their core objectives. The dependency management literature identifies two broad approaches to addressing external constraints. One approach focuses on restructuring dependency relationships to reduce the relative power of constraining actors, for example through resource diversification, mergers or acquisitions, joint ventures, or coalition-building (Hillman, Withers, & Collins, 2009; Oliver, 1991; Pfeffer & Salancik, 1978). These strategies aim to rebalance interdependencies and reduce vulnerability to any single actor. However, such approaches may be structurally constrained in nonprofit settings. Mergers, acquisitions, or joint ventures are often legally restricted for nonprofit entities (Mendoza-Abarca & Gras, 2019), and cultivating diversified funding sources can entail significant administrative burdens and uncertainty (Chikoto & Neeley, 2014). In the case of CFs, sponsor firms frequently provide the majority of financial resources as well as critical nonfinancial resources, such as workplace facilities and organizational manpower, limiting the feasibility of materially reducing dependence (Westhues & Einwiller, 2006).

A second approach emphasizes buffering—limiting the extent to which external demands penetrate core organizational activities without necessarily reducing dependence (Pfeffer & Salancik, 1978; Oliver, 1991). Prior research describes buffering tactics such as symbolic compliance (e.g., Meyer & Rowan, 1977; Oliver, 1991), selective disclosure (e.g., Briscoe & Murphy, 2012), or impression management (e.g., Chaganti, Brush, Haksever, & Cook, 2002; Weber, Heinze, & DeSoucey, 2008). These tactics often rely on restricting information flows or decoupling formal structures from underlying practices (Oliver, 1991; Pfeffer & Salancik, 1978). However, buffering through concealment may be difficult when organizations operate under close and ongoing scrutiny from resource providers.

CFs typically function under such scrutiny. Sponsor firms often retain representation on CF governance boards and maintain oversight over financial allocations (Brown et al., 2006; Pamphile, 2022). Moreover, regulatory requirements mandate detailed annual reporting of philanthropic activities, increasing transparency to funders and other stakeholders (Tremblay-Boire, 2020). Under these conditions, conventional forms of symbolic buffering may be constrained.

Taken together, these insights suggest that CFs operate in a context characterized by entrenched dependence and close oversight, where materially reducing dependence may be infeasible and concealment-based buffering may be difficult. This setting provides a theoretically meaningful context for examining how variation in organizational conditions and their enabled buffering mechanisms can help CFs sustain their pursuit of long-term social missions.

Hypothesis Development

Shifts in Sponsor Firms’ Business Activities and Corporate Foundations’ Inconsistent Social Actions

For CFs, inconsistent social actions are reflected in variation in their engagement across philanthropic domains over time—initiatives that directly serve social causes and are typically implemented through grant-making to beneficiaries. Philanthropic activities constitute the primary means through which foundations advance their stated social commitments and generate societal benefits, distinct from administrative activities that are necessary for internal operations yet do not directly support social causes. Our study therefore focuses on instability in CFs’ philanthropic portfolios across consecutive years.

The business case for corporate philanthropy often emphasizes alignment between philanthropic engagement and business interests, such as strengthening public image, reinforcing product branding, or cultivating stakeholder relationships operational environments (Porter & Kramer, 2006). When sponsor firms adjust their business portfolios, they may enter new markets, interact with new stakeholder groups with distinct expectations and social norms, or withdraw from prior domains (e.g., Campbell, 2007; Marquis et al., 2007). These shifts can alter the stakeholder environments within which firms operate, potentially changing expectations regarding appropriate forms of corporate engagement (Kang, 2013; Su & Tsang, 2015). To address these shifts, firms often reprioritize prosocial initiatives to align with newly relevant stakeholder groups. For instance, a firm entering the pharmaceutical and medical sectors may steer its CF toward health-related initiatives, while one expanding into the energy sector might emphasize environmental sustainability projects.

To leverage CFs for strategic benefits, firms use their financial control and oversight authority to capture CFs in redirecting their focus in philanthropic activities. Because CFs depend on sponsor funding, they must respond to these evolving demands or risk losing support of financial and organizational resources. Firms enforce this control by determining whether to continue funding existing CF projects or to redirect funds to new initiatives aligned with revised strategic priorities. Prior research finds that firms may reduce or withdraw support from social initiatives perceived as misaligned with their evolving business needs (Cranenburgh & Arenas, 2014; Kaplan, 2020). Beyond financial means, administrative authority also reinforces corporate influence. Corporate leaders from sponsor firms often sit on CF boards, overseeing foundation operations and issuing directives to CF managers (Brown et al., 2006). This oversight often results in direct instructions to initiate or terminate projects—sometimes overriding CF managers’ judgments about the social value of these projects (Pamphile, 2022).

Taken together, these arguments suggest that as sponsor firms adjust their business portfolios, CFs correspondingly adjust their philanthropic activity portfolios to reflect evolving business imperatives. This positive association reflects a potential tension: alignment with evolving business priorities may coincide with reduced continuity in supporting particular social causes or beneficiaries over time.

Hypothesis 1: Changes in a sponsor firm’s portfolio of business activities are positively associated with changes in its CF’s portfolio of philanthropic activities.

Mitigating Mechanisms: Nonprofit-Oriented Forces and Compartmentalization of Mission-(Un)Related Activities

Building on the baseline expectation that sponsor firms’ business changes are associated with instability in CFs’ philanthropic portfolios, we next examine organizational conditions under which this association may be attenuated. Rather than assuming deliberate resistance to sponsor influence, we focus on how variation in governance composition and funding structure shapes how external demands are interpreted, evaluated, and enacted once foundations operate under conditions of dependence.

RDT suggests that organizational responses to external demands are shaped not only by power asymmetries but also by the evaluative criteria and monitoring structures embedded within governance arrangements (Oliver, 1991; Pfeffer & Salancik, 1978). Following this logic, we argue that CFs’ autonomy is preserved when nonprofit-oriented forces participate in monitoring organizational actions and reinforce accountability for social objectives. We focus on two such conditions: the presence of executives with nonprofit backgrounds and the presence of non-corporate funding partners. These nonprofit-oriented forces—operating within and alongside the foundation—introduce professional norms, philanthropic expertise, and accountability expectations that emphasize long-term commitment to social causes. Because they are socialized into nonprofit logics and value sustained engagement with social beneficiaries (Teegen et al., 2004), they are more likely to view abrupt, business-driven shifts in philanthropic emphasis as potentially inconsistent with advancing social aims. As a result, when such forces are present, the evaluative framework through which corporate demands are assessed differs from that of foundations governed solely by corporate-oriented actors. Consequently, patterns of philanthropic adjustment in response to sponsor firms’ business changes may diverge across foundations with different governance and funding configurations.

At the same time, CFs remain structurally embedded in dependency relationships with sponsor firms. Continued resource reliance and close oversight mean that outright noncompliance with sponsor priorities may be costly, potentially jeopardizing access to critical resources. Under these constraints, adaptation is likely to occur—but it need not occur uniformly across all domains of philanthropic activities. Responsiveness to sponsor firms’ business changes may instead be distributed unevenly across different types of philanthropic activities.

We therefore argue that activity compartmentalization functions as a viable buffering mechanism within CFs’ philanthropic portfolios. Specifically, CFs can differentiate mission-related and mission-unrelated activities in how adjustments unfold. Mission-related activities, which directly address social issues or beneficiaries articulated in the foundation’s stated mission (Gupta, Palsule-Desai, Gnanasekaran, & Ravilla, 2018; Kouamé, Hafsi, Oliver, & Langley, 2022), constitute the core of a CF’s identity and long-term commitments (Battilana, 2018; Ebrahim et al., 2014). In contrast, mission-unrelated activities fall outside the explicit scope of a CF’s declared mission and are thus less central to its publicly articulated purpose. For example, the Elion Charitable Foundation, whose stated mission centers on environmental protection, undertakes desertification prevention projects (mission-related) while also supporting educational donations (mission-unrelated).

Compartmentalizing mission-(un)related activities provides a structured way to navigate external pressures when concealment-based buffering is infeasible (Drees & Heugens, 2013; Oliver, 1991). Adjustments to mission-related activities directly implicate CFs’ internal priorities and core commitments and may generate stronger legitimacy concerns, both internally and among external stakeholders. Altering such activities risks undermining organizational authenticity and eroding public trust (Grimes et al., 2019). By contrast, adjustments in mission-unrelated activities may carry comparatively lower symbolic and reputational costs, as these domains are less tightly coupled to the foundation’s stated purpose. Accordingly, when nonprofit-oriented forces are present, adaptation to sponsor firms’ business changes may be more likely to occur in mission-unrelated domains, while mission-related activities exhibit greater stability.

Taken together, we propose that nonprofit-oriented forces and activity compartmentalization work in tandem to carve out a space for CFs to retain and exercise autonomy despite pressures from powerful sponsor firms. Nonprofit-oriented forces function as autonomy enablers that shape the evaluative criteria through which corporate demands are assessed, while compartmentalization structures how adjustments are distributed across activity domains, resulting in adaptation that entails fewer conflicts with these evaluative criteria. Even when CFs remain dependent on sponsor firms for critical resources, these conditions may be associated with differential patterns of responsiveness that help sustain core mission efforts while accommodating certain external demands.

Mitigating effects enabled by executives with nonprofit backgrounds

Executives within charitable foundations constitute key actors in philanthropic operations and allocating resources (Ebrahim et al., 2014; Minciullo & Pedrini, 2020). RDT scholars have long recognized high-level managers as central to managing external dependencies by cultivating relationships with key environmental constituents to reduce resource uncertainty (Davis & Cobb, 2010; Hillman et al., 2009). Beyond this relational and resource-maintenance function, executives may also exercise managerial discretion in steering organizational goals under external control pressures—an aspect that has been less explored (Wry et al., 2013). In particular, executives’ professional backgrounds influence how they attend to, interpret, prioritize competing objectives, and thus respond to external demands (Ebrahim et al., 2014; Ocasio, 1997).

Executives with nonprofit backgrounds bring philanthropic expertise and value orientations shaped by sustained exposure to nonprofit norms. Such backgrounds are associated with greater emphasis on long-term engagement with social issues and sensitivity to reputational standing within nonprofit communities (Provan, Beyer, & Kruytbosch, 1980; Teegen et al., 2004). These orientations influence how discretion over philanthropic portfolios is exercised once corporate demands are introduced. When shifts in sponsor firms’ business portfolios create pressures to redirect philanthropic resources, executives with nonprofit backgrounds may assign greater weight to continuity in beneficiary relationships and adherence to stated missions. Consequently, the presence of executives with nonprofit backgrounds is expected to weaken the positive association between sponsor firms’ business changes and changes in CFs’ philanthropic portfolios.

Hypothesis 2a: When a CF’s executives have a higher proportion of nonprofit backgrounds, the positive association between changes in the sponsor firm’s business activities and changes in the CF’s philanthropic activities is weaker.

Importantly, this moderating association is unlikely to be uniform across activity domains. Because mission-related activities embody a CF’s explicitly stated commitments and core values, adjustments in these domains more directly implicate professional norms and legitimacy concerns. Executives with nonprofit backgrounds are therefore more likely to evaluate instability in mission-related activities as misaligned with the CF’s social purpose, motivating them to negotiate with sponsor firms and justify their discretionary decisions to preserve consistency in mission-related activities as righteous and legitimate. As Oliver (1991) contended, organizations are more likely to defy external demands when they can demonstrate the righteousness of their choices.

In contrast, mission-unrelated activities entail lower symbolic costs when adjusted. Nonprofit-oriented executives are more likely to accommodate corporate demands by adjusting mission-unrelated activities, as adapting these activities does not jeopardize the pursuit of the foundation’s central objectives. Moreover, managers can frame such adjustments as responsiveness to changing environmental conditions, thereby minimizing negative perceptions and reputational risks. Accordingly, when CFs face corporate pressures to replace ongoing projects with newly emphasized initiatives, the presence of executives with nonprofit backgrounds should be associated with a stronger dampening effect on changes in mission-related activities than in mission-unrelated activities.

Hypothesis 2b: The moderating effect of executives’ nonprofit backgrounds on the relationship between changes in a sponsor firm’s business activities and changes in its CF’s philanthropic activities is stronger for mission-related activities than for mission-unrelated activities.

Mitigating effects enabled by non-corporate funding partners

Funding structure represents another dimension through which dependence relationships are shaped. Alternative funding sources provide CFs with greater flexibility in resource allocation and introduce additional accountability relationships (Pfeffer & Salancik, 1978; Provan et al., 1980). When CFs receive funds from non-corporate donors such as charitable organizations, governments, or individuals, they operate within a broader network of stakeholders whose expectations center more explicitly on social objectives, thus limiting the extent to which corporate sponsors can unilaterally redirect philanthropic resources.

Non-corporate funders typically provide financial support tied to particular social causes and impose accountability for maintaining alignment with those purposes (Anheier & Ben-Ner, 1997). Because these donors contribute based on aligned interests in addressing specific social issues, CFs can rely on them to sustain relevant projects even when such projects lack full backing from sponsor firms. Moreover, non-corporate funders function as external monitors (Durand & Jourdan, 2012), overseeing foundations’ philanthropic operations to ensure consistency with their commitments. Such funding relationships hold CFs accountable for allocating resources toward their pledged social causes, thereby limiting the reallocation of funds for business purposes. Therefore, the presence of non-corporate funders is expected to weaken the positive association between sponsor firms’ business changes and changes in CFs’ philanthropic portfolios.

Hypothesis 3a: When a CF receives a higher proportion of funds from donors other than firms, the positive association between changes in the sponsor firm’s business activities and changes in the CF’s philanthropic activities is weaker.

As with governance composition, the moderating association of non-corporate funders is likely to vary across philanthropic domains. Specifically, non-corporate funders tend to focus their oversight and accountability on maintaining consistency in mission-related activities, as their shared objectives with CFs often center on the stated social missions. For example, government entities may provide grants to CFs whose committed missions complement public service delivery, while other charitable foundations may donate to CFs to collaborate on and advance similar social missions. Consequently, reallocating resources away from mission-related activities may directly violate funder expectations and jeopardize their trust. CFs hold a stronger bargaining position against such pressures, as maintaining consistency in mission-related activities can be framed as necessary for co-funding or collaboration with nonprofit stakeholders. In comparison, reallocating resources among mission-unrelated activities is less likely to breach the expectations of non-corporate funders and thus entails lower risks of trust erosion or support withdrawal. Accordingly, non-corporate funders impose stronger accountability on CFs for maintaining consistency in mission-related activities, whereas adjustments in mission-unrelated activities are less likely to conflict directly with donor expectations. Therefore, the dampening association of non-corporate funding partners should be stronger for mission-related activities than for mission-unrelated activities.

Hypothesis 3b: The moderating effect of funds from other donors on the relationship between changes in a sponsor firm’s business activities and changes in its CF’s philanthropic activities is stronger for mission-related activities than for mission-unrelated activities.

Data and Methods

Sample

To test our hypotheses, we assembled a dataset comprising three types of annual data: (1) CFs’ grantmaking projects across different social domains; (2) CFs’ demographic and governance information; and (3) sponsor firms’ demographic and financial data.

Data on CFs’ demographic characteristics and grantmaking activities were obtained from the China Foundation Center (CFC), the most authoritative nonprofit information platform in China (Nie, Liu, & Cheng, 2016; Zheng, Ni, & Crilly, 2019). Since the enactment of the Regulation on Foundation Administration (2004) by the State Council, foundations in China have been required to submit audited annual reports in a standardized format—similar to Form 990 in the United States—to the government’s Civil Affairs Departments. The CFC, an independent third-party platform, collects these annual reports disclosed by foundations or Civil Affairs Departments and supplements them with additional information gathered from media sources or other public outlets.

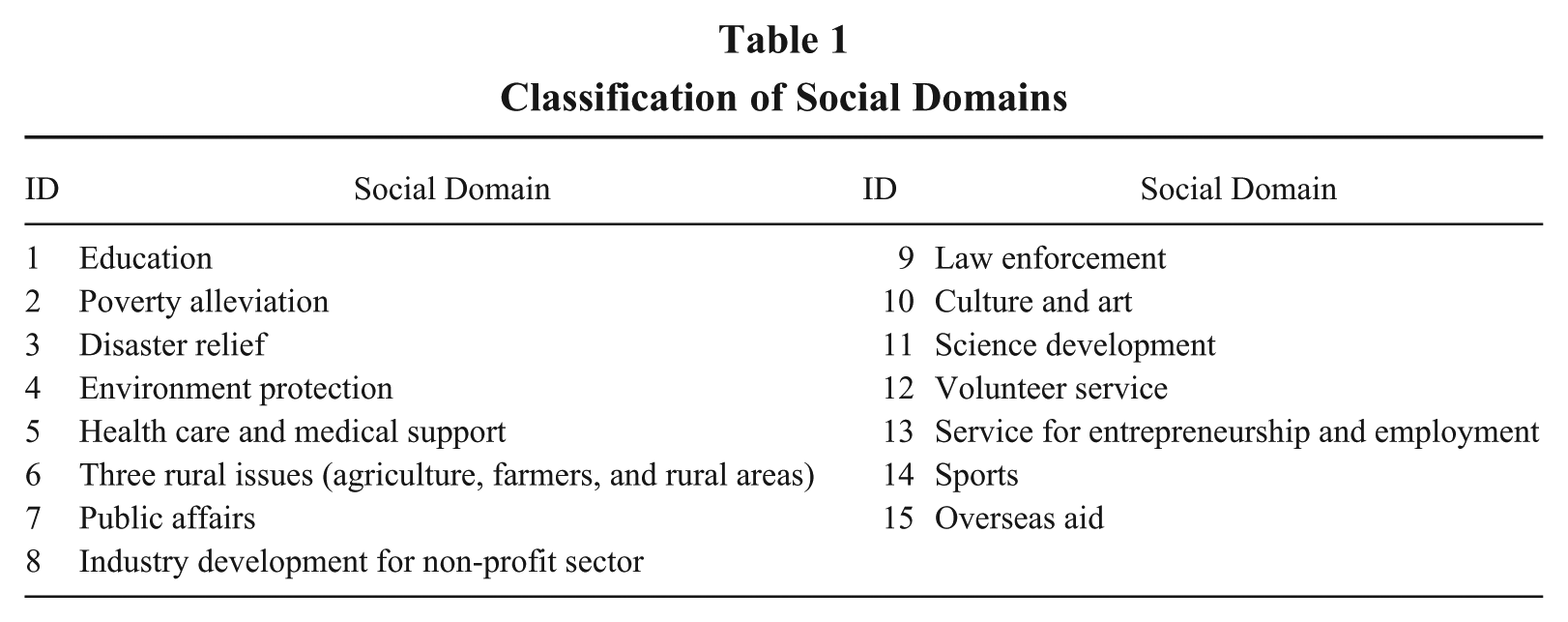

The CFC database contains project-level information on all grantmaking activities carried out by foundations each year, including project names, expenditures, beneficiaries, and descriptive texts. Since 2016, foundations have been required to disclose the social domain of each grantmaking project—which reflect different charitable purposes. While some CFs disclosed full domain information in their post-2016 annual reports, others omitted it partially or entirely. Earlier reports issued before 2016 often lacked this information altogether. To address this gap, we used machine learning to classify the social domains for projects with missing data. Specifically, we trained a TfidfVectorizer-based text classification model using 4,116 grantmaking projects with self-identified social domains and corresponding textual descriptions, covering 15 domain categories (see Table 1). The trained model was then applied to classify the remaining projects to determine the social domains of those projects based on their descriptive texts. To validate the model’s performance, a trained research assistant manually coded a subsample of the grantmaking projects, and we compared those classifications with the machine-assigned results (see Appendix A in the online supplemental materials for details). The consistency between manual and algorithmic classifications provides confidence in the reliability of our domain coding.

Classification of Social Domains

In addition to project-level data, the CFC database provides information on CFs’ basic characteristics, including location, year of establishment, and financial indicators.

Because our theoretical framework centers on the CF–sponsor firm relationship, we restricted our sample to CFs founded by publicly listed companies. We then matched foundation data with sponsor firm data collected from the Wind database, a leading financial database in China that provides detailed background and financial information for all publicly listed companies.

Governance information was manually collected from CFs’ annual reports, which list all individuals sitting on the board, including trustees, president of trustees, and executive officers (directors). However, demographic and professional background data for these individuals were not consistently disclosed. To supplement missing data, we matched individuals’ names to two additional sources: the Wind Personnel Library and the Yishan Database, a platform tracking information on charitable organizations and related activities in China.

After merging all datasets and excluding observations with incomplete key variables, our final sample consists of an unbalanced panel of 865 foundation-firm-year observations covering 214 CFs and their corresponding sponsor firms from 2009 to 2022. For full transparency, we include a detailed breakdown of sample attrition due to missing data in online Appendix B. We also conducted additional analyses to verify that our main results are robust and not driven by sample restrictions.

Dependent Variables

Portfolio change in philanthropic activities

Following prior research, we conceptualize inconsistent social actions as deviations from prior patterns of organizational engagement (Grimes et al., 2019). In the CF context, such inconsistency is reflected in changes in the distribution of grantmaking across social domains from one year to the next (Koushyar et al., 2015; Meijs, 2010; Seo et al., 2021). For example, a foundation focused on environment protection one year may later reduce such funding and redirect support toward projects in other social domains like poverty alleviation. To capture CFs’ inconsistent social actions, and in line with the measurement by Seo et al. (2021), we calculated each CF’s portfolio change in philanthropic activities based on differences in its grantmaking portfolio across different social domains on a year-to-year basis.

Our dataset includes 16,765 grantmaking projects carried out by CFs through 2022, with a median expenditure of 301,576 RMB per project. We aggregated project-level expenditures to the foundation-domain-year level, constructing each foundation’s annual grantmaking portfolio across the 15 social domains. To capture year-to-year changes in philanthropic portfolios, we calculated the reverse of Cosine similarity between each foundation’s domain expenditure vectors in consecutive years. Cosine similarity is widely used to assess similarity between multi-dimensional vectors (e.g., Chu, Deng, & Xia, 2020; Girardi, Hanley, Nikolova, Pelizzon, & Sherman, 2021). A value of 1 indicates identical portfolio composition. We therefore define portfolio change as one minus the Cosine similarity:

where

Portfolio change in mission-(un)related activities

To test Hypotheses 2b and 3b, we distinguished between mission-related versus mission-unrelated activities and analyzed the portfolio change in mission-(un)related activities. Mission-related activities are those aligned with social domains explicitly referenced in a foundation’s formal mission statement (Gupta et al., 2018; Kouamé et al., 2022). To construct these variables, we collected mission statements from CFs’ official websites, annual reports, and the Civil Affairs Departments’ platform (https://chinanpo.mca.gov.cn/). 1 These formal mission statements, usually crafted by nonprofit founders, establish nonprofit status and articulate the foundation’s raison d’être (Berlan, 2018). While some of these statements were articulated with clear mission language like, “Our mission is . . .,” others used phrases like “Our vision/purpose/value is . . .,” “We are dedicated to . . .,” “Our targeted social issues are . . .,” etc. With these textual data, we then identified social domains as specified by the stated missions. Two trained research assistants independently read through the mission statements of all CFs and coded the social domains referenced in each mission statement. Inter-coder agreement was 86%; disagreements were resolved through discussion among the research team.

Not all CFs clearly specified social domains in their mission statements, however. Of the 214 CFs in our sample, 78 articulated their purposes in very general terms, such as “promote harmony of society” and “dedicated to the public well-being.” Among the remaining 136 CFs, 16% announced one social domain associated with their missions, 78% referenced two to four social domains in their mission statements, and 6% referenced five or more social domains. When testing Hypotheses 2b and 3b, we included only those CFs with specified social domains in their mission statements. We constructed Cosine-based measures of year-to-year portfolio change for mission-related and mission-unrelated domains using the same procedure described above, applied to the relevant subsets of domain expenditure vectors:

where

Independent Variables

Portfolio change in business activities

To capture sponsor firms’ portfolios of business activities, we collected product-market segment information from the Wind database, which reports sales that a listed firm generated from different industries in a fiscal year. Previous studies have measured business dissimilarity based on firms’ revenue shares across different product-market segments (e.g., Connelly, Lee, Tihanyi, Certo, & Johnson, 2018; Henderson, 1999). Accordingly, we used the year-by-year change of firms’ sales in different product-market segments to measure each firm’s portfolio change in business activities (abbreviated as business change in the models). The formula followed the same logic as how we computed each CF’s portfolio change in philanthropic activities:

where

Executives’ nonprofit backgrounds

The management team of a foundation typically consists of executive officers (directors), the president of trustees, and trustees. The president and director on the board are the main decision makers for the administration and management of a foundation; thus, we consider these two kinds of officials as foundations’ executives. Based on their demographics and professional information, we assessed these executives’ background. Nonprofit background was coded 1 if the executive had served as an administrator or staff member in a nonprofit entity, such as a charitable organization, social service unit, non-commercial association, or academic institution. The foundation-level measure, executives’ nonprofit backgrounds, was then calculated as the proportion of executives with nonprofit backgrounds within the executive team.

Funds from other donors

The CFC database discloses foundations’ income structures every fiscal year. A CF can obtain financial income from different sources. For the majority of foundation-year observations (around 75% of the total sample), donations from sponsor firms account for more than 90% of foundations’ annual income, indicating a significant reliance on sponsor firms for financial resources. Apart from sponsor firms, a CF may receive donations from other not-for-profit entities such as charitable organizations, the government, and individuals. To measure funds from other donors, we calculated the proportion of each foundation’s annual income derived from those non-corporate donors. This measure captures variation in funding diversification and the relative financial presence of stakeholders beyond the sponsor firm.

Control Variables

We controlled for several variables at both the sponsor firm and foundation levels that prior research suggests may influence philanthropic portfolio stability. At the sponsor firm level, we included sales, calculated as the logarithm of the sponsor firm’s total sales at the end of the fiscal year, to control for firm size. Larger firms may possess greater visibility and resource capacity, which could be associated with philanthropic engagement (Marquis & Lee, 2013). We also controlled for the sponsor firm’s financial volatility, calculated as the 3-year standard deviation of return on assets (ROA), as fluctuations in financial performance may coincide with changes in corporate philanthropic behavior (e.g., Waddock & Graves, 1997).

To account for leadership transitions, we included a dummy variable—top executives’ succession—indicating whether the sponsor firm’s president or CEO changed relative to the prior year. Executive succession has been shown to influence corporate philanthropic strategies (e.g., Luo, Chen, & Chen, 2020). We further controlled for ownership type, given its relevance in shaping philanthropic behavior, especially in emerging markets where state involvement is common (e.g., Li, Song, & Wu, 2015). We coded this variable as 1 for state-owned firms and 0 for private firms. Furthermore, we included the sponsor firm’s advertising intensity, calculated as selling expenses divided by total sales (Wang & Qian, 2011), as firms with higher advertising expenditures may be particularly invested in philanthropic activities as a strategy for image building and market positioning (Zhang, Zhu, Yue, & Zhu, 2010).

At the foundation level, we included net assets of the foundation (logged) to control for foundation size, which may affect the foundation’s grantmaking capacity. We also controlled for the level and pattern of grantmaking in previous years, which may shape current philanthropic behavior due to legacy decisions and path dependence. Specifically, we included the grantmaking level of the last year, measured as the total amount of the CF’s donations divided by its size (net assets) in the last fiscal year. To account for the structure of prior giving, we included grantmaking diversity, measured as 1 minus the Herfindahl index of grantmaking across social domains in the prior year. This index captures whether a CF’s grantmaking was narrowly focused or broadly distributed across causes, which may influence its tendency toward continuity or change (Eilert & Robinson, 2018; Seo et al., 2021).

We further controlled for administrative capacity by including the foundation’s administration expense ratio—calculated as the share of administrative costs in total annual expenditures. These expenses, which include operational overhead and staff compensation, may influence the effectiveness and continuity of philanthropic activity. We also controlled for the foundation’s age, calculated as the number of years since the foundation’s establishment, as older organizations may develop more stable routines and stakeholder relationships.

Finally, to account for unobserved temporal shocks and industry-specific heterogeneity, we included year and industry fixed effects in all models (Galaskiewicz, 1997; Tilcsik & Marquis, 2013). All continuous control variables were winsorized at the 1st and 99th percentiles to mitigate the impact of outliers.

Estimation Strategy

Our data are structured as a foundation-year panel. We employed random-effects models with robust standard errors clustered by foundation to control for repeated observations and unobserved foundation heterogeneity. Random-effects models are preferred over fixed-effects models for several reasons. First, since the governance structure of a CF rarely changes over time, our key independent variables—executives’ nonprofit backgrounds and funds from other donors—exhibit limited within-foundation variation over time, making fixed-effects estimations less informative for testing our hypotheses. Second, the average number of observations per foundation in our sample is approximately 5 years, limiting the statistical efficiency of fixed-effects estimators. Third, our theoretical framework concerns primarily between-foundation variation in governance composition and funding structure, justifying the use of random-effects. Nevertheless, we ran a Hausman test comparing fixed- and random-effects specifications, which indicated no systematic differences in coefficient estimates when testing the baseline hypothesis (prob. > χ2 = 0.3969). Furthermore, we report foundation fixed-effects models as robustness checks, and the main findings remain consistent.

For Hypotheses 2b and 3b, which compare moderating effects across mission-related and mission-unrelated outcomes, we ran seemingly unrelated regressions (SURs) to account for correlated error terms across the two equations (Wooldridge, 2002). After estimating the system, we conducted Wald tests to assess whether the interaction coefficients differ significantly across the two outcome models. Because portfolio change in mission-related activities and portfolio change in mission-unrelated activities differ in scale, we standardized these dependent variables in the SUR analyses to facilitate comparison. Results using raw (unstandardized) values are substantively similar.

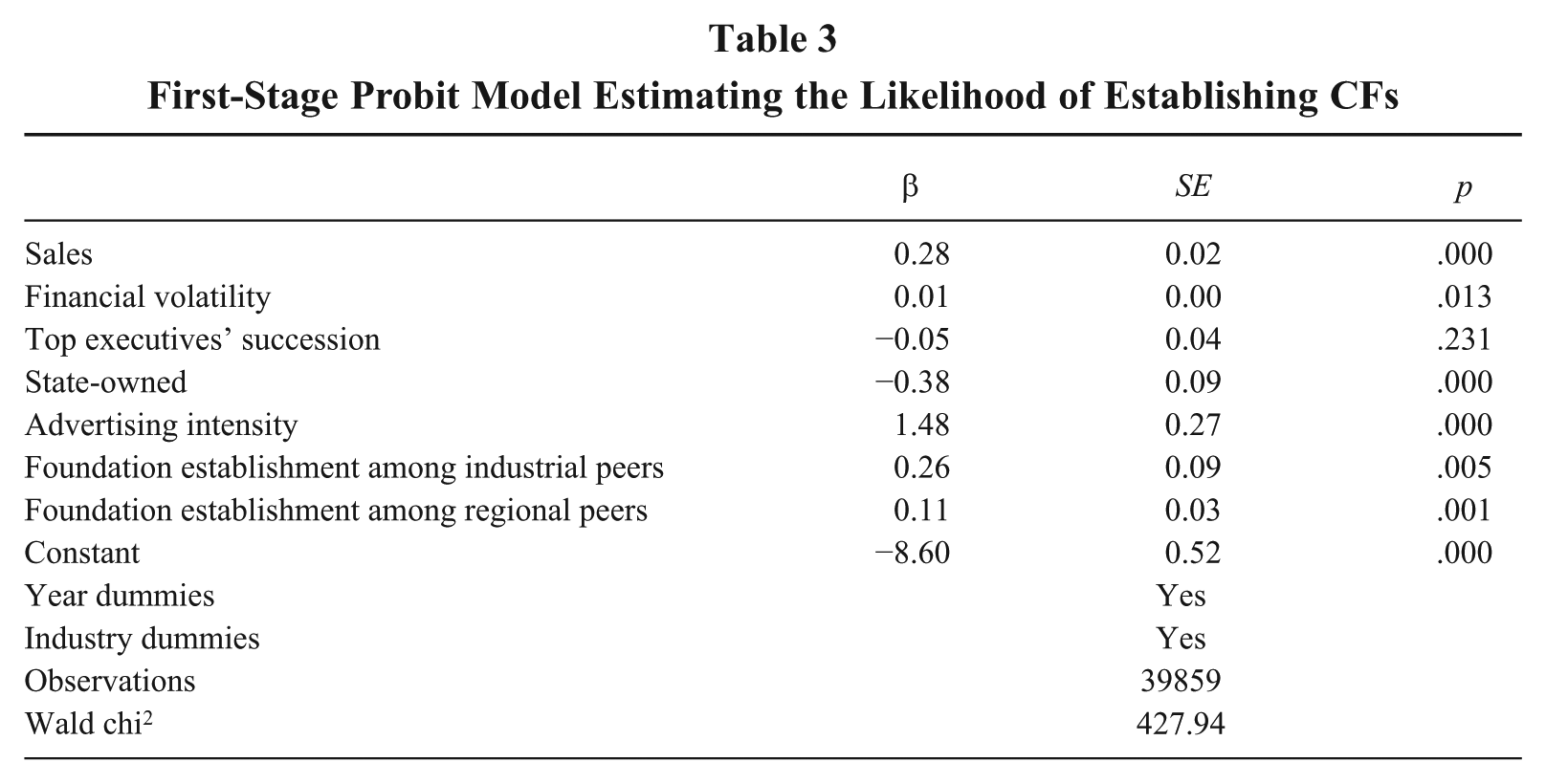

To address potential sample selection concerns—given that our sample included only sponsor firms that established CFs—we employed a Heckman two-step correction. In the first stage, we collected data on all listed firms covered in the Wind database during the period of our observations (2009–2022). We then used a probit model to estimate the likelihood of firms having a CF, controlling for a number of firm-level variables, including sales, financial volatility, top executives’ succession, state-owned, and advertising intensity. The Heckman two-stage approach requires an exclusion restriction, which involves including variables that are conceptually similar to instruments. These instruments should appear in the first-stage model and be related to the probability of selection, but they should not predict the outcome in the second-stage model (Certo, Busenbark, Woo, & Semadeni, 2016; Kennedy, 2008). We included two such instruments: foundation establishment among industry peers, calculated as the number (logged) of industry peers that established CFs by the end of the last year, and foundation establishment among regional peers, calculated as the number (logged) of regional peers that established CFs by the end of the last year. Peers’ adoption of certain corporate social practices—in this case, establishing a CF—may impose institutional pressures on the focal firm, leading it to adopt similar practices to enhance its legitimacy (Campbell, 2007; Marquis et al., 2007). However, such isomorphic pressures during the founding phase are unlikely to directly impact the portfolio change in focal CF’s post-founding philanthropic activities, which is the outcome in the second-stage model.

To further assess the strength of our instruments, we conducted an F-test by regressing the first-stage dependent variable on the instruments alone (e.g., Kotha, Zheng, & George, 2011). The resulting F-statistic was 91.31 (p = .000), indicating a strong relationship between the two instruments and the probability of sample selection. In addition, we performed a correlation analysis between each instrument and the error term from the second-stage regression. Neither foundation establishment among industry peers (r = 0.01, p = .846) nor foundation establishment among regional peers (r = −0.01, p = .838) showed significant correlations with the second-stage error term, supporting the exogeneity of these instruments. Therefore, our chosen instruments meet the key criteria for instrument validity in Heckman models (Certo et al., 2016).

Results

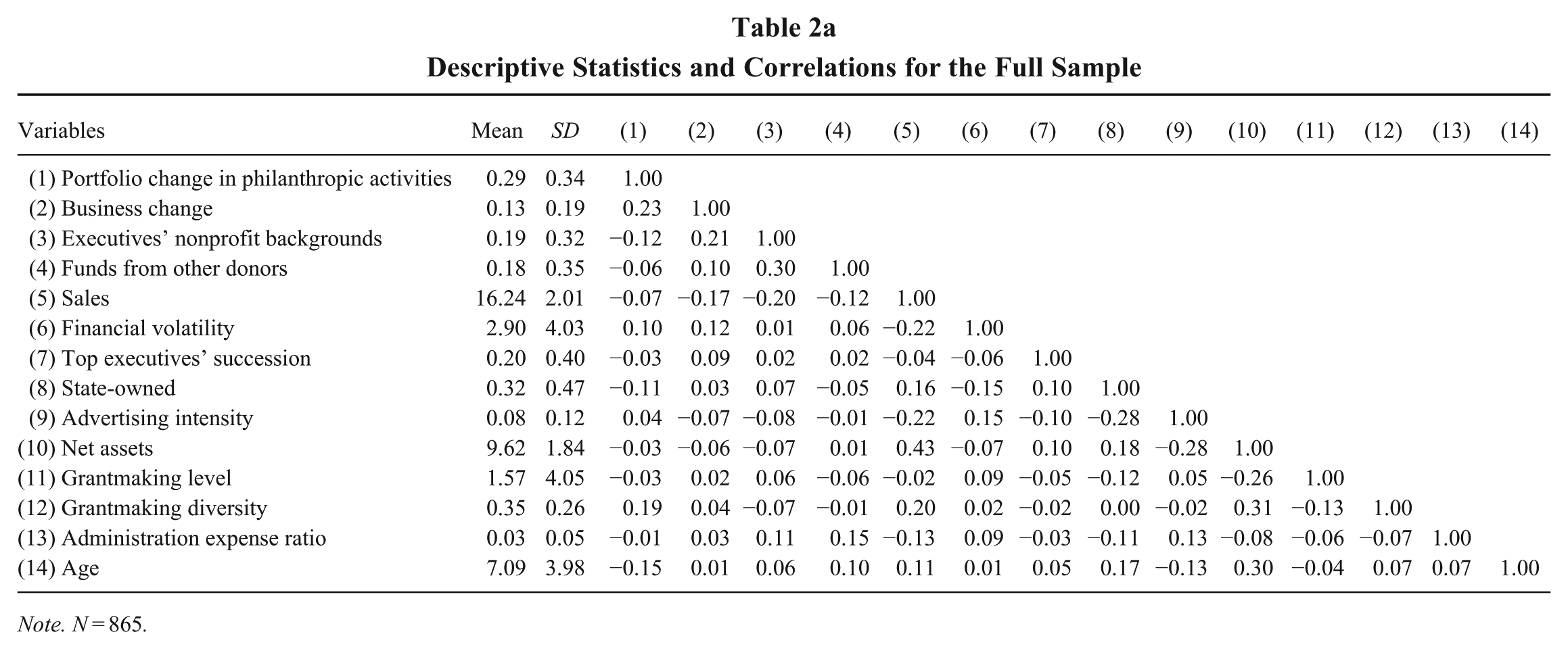

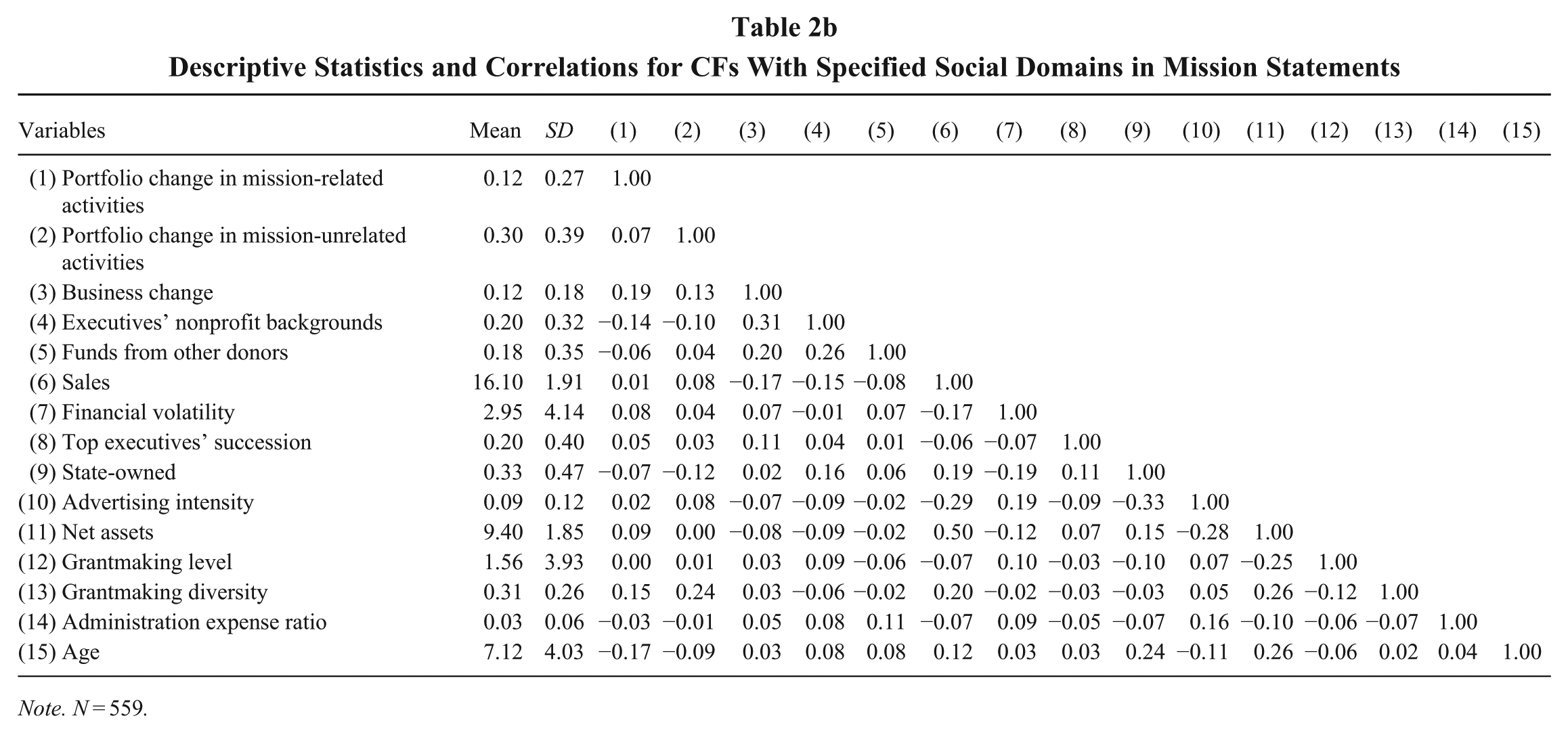

Tables 2a and b present summary statistics and correlation matrices for the full sample and the subsample of CFs with specified mission statements, respectively. We performed a variance inflation factor (VIF) analysis to confirm that multicollinearity was not a concern in our models (mean VIF = 1.22; maximum VIF = 1.63).

Descriptive Statistics and Correlations for the Full Sample

Note. N = 865.

Descriptive Statistics and Correlations for CFs With Specified Social Domains in Mission Statements

Note. N = 559.

Table 3 presents results from the first-stage probit model predicting the likelihood that a firm establishes a CF. Our results show that firms with greater sales (i.e., larger firms) are more likely to establish CFs, consistent with the view that firm visibility and resource capacity are associated with philanthropic structuring. Privately owned firms and firms with higher advertising intensity also show a greater propensity to establish CFs. Additionally, peer adoption at the industry and regional levels is positively associated with CF establishment, consistent with institutional pressures documented in prior research (Campbell, 2007; Marquis et al., 2007).

First-Stage Probit Model Estimating the Likelihood of Establishing CFs

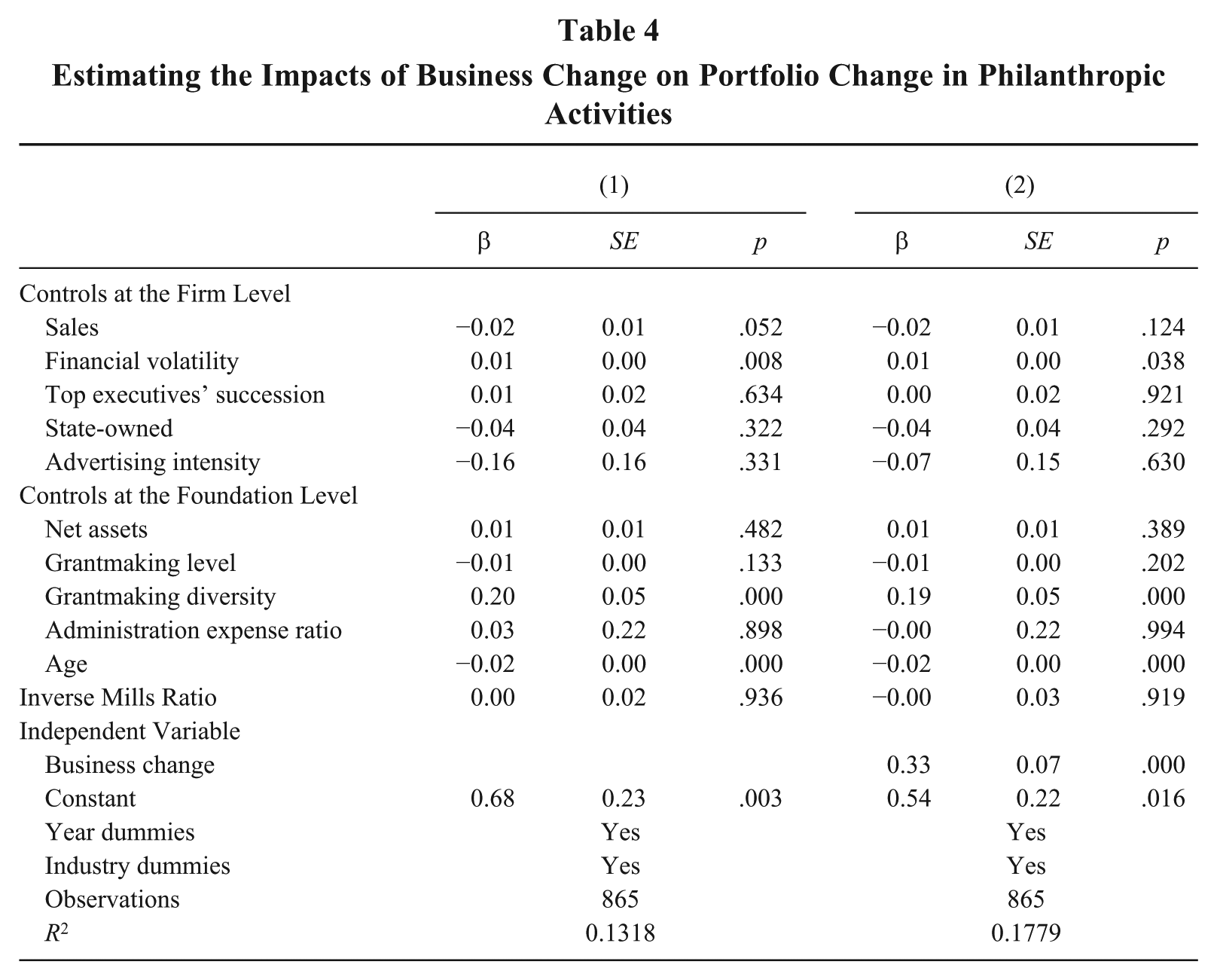

Tables 4 through 6 report results from our second-stage regressions, which include the inverse Mills ratio to correct for potential sample selection bias. Table 4 examines the association between sponsor firms’ business change and CFs’ portfolio change in philanthropic activities. Model 1 is the baseline model with control variables only. As expected, a sponsor firm’s financial volatility is associated with greater instability in CF’s philanthropic activity portfolios. Prior grantmaking diversity is also positively associated with subsequent portfolio change in philanthropic activities. Older CFs, in contrast, exhibit more stable portfolios of philanthropic activities compared with younger foundations.

Estimating the Impacts of Business Change on Portfolio Change in Philanthropic Activities

Estimating the Moderating Effects of Executives’ Backgrounds and Funding Partners on Portfolio Change in Philanthropic Activities

Predicting Mission-Related Activities and Mission-Unrelated Activities Using Seemingly Unrelated Regressions

Model 2 tests Hypothesis 1. Business change is positively associated with portfolio change in philanthropic activities (β = 0.33, p = .000), supporting Hypothesis 1. A 1 standard deviation increase in business change corresponds to a 21.6% increase in mean level of philanthropic portfolio change. While the magnitude of this effect is modest, the results suggest that sponsor firms’ business variation represents one important, albeit not exclusive, source of variation in CFs’ philanthropic instability.

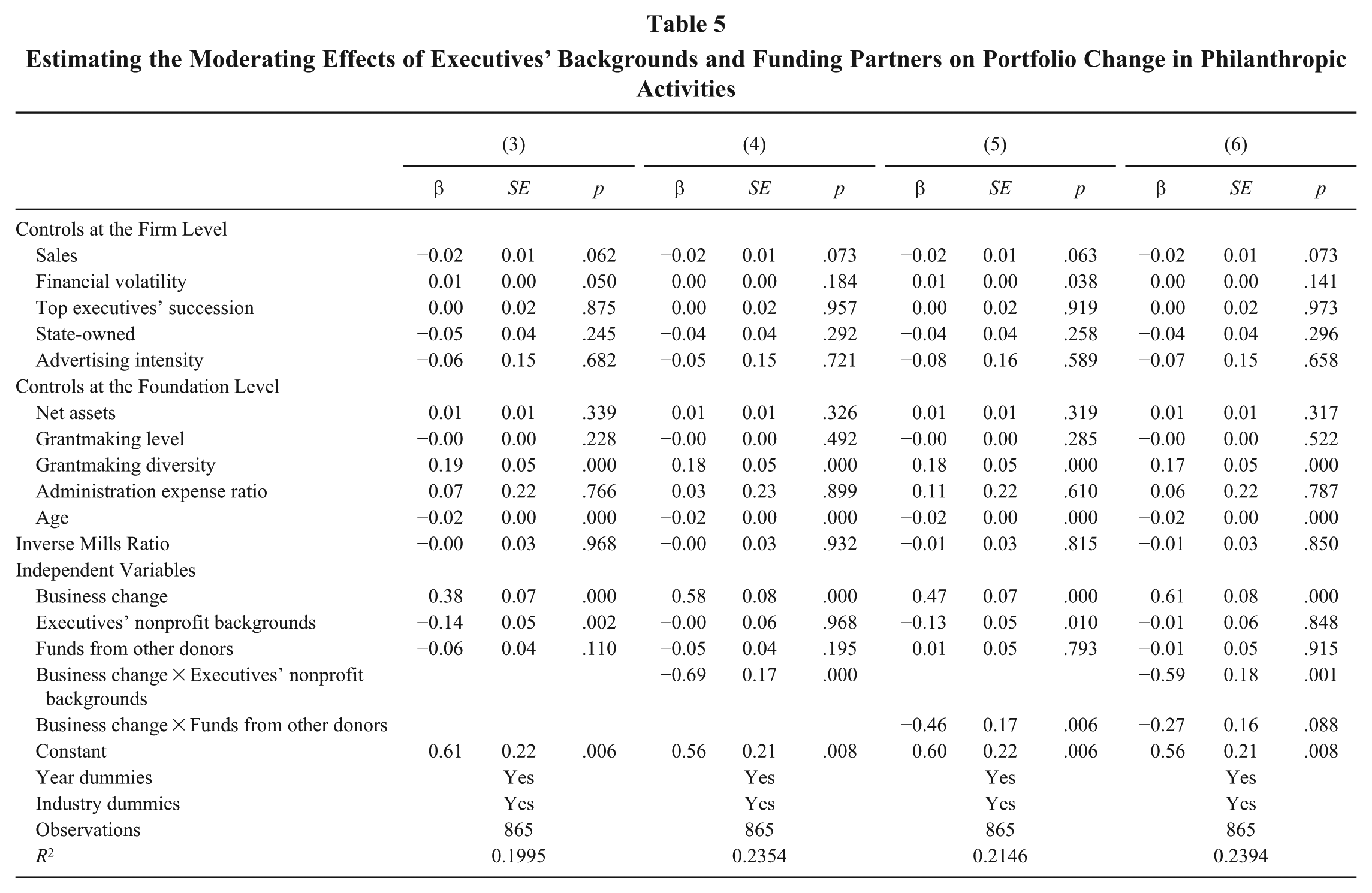

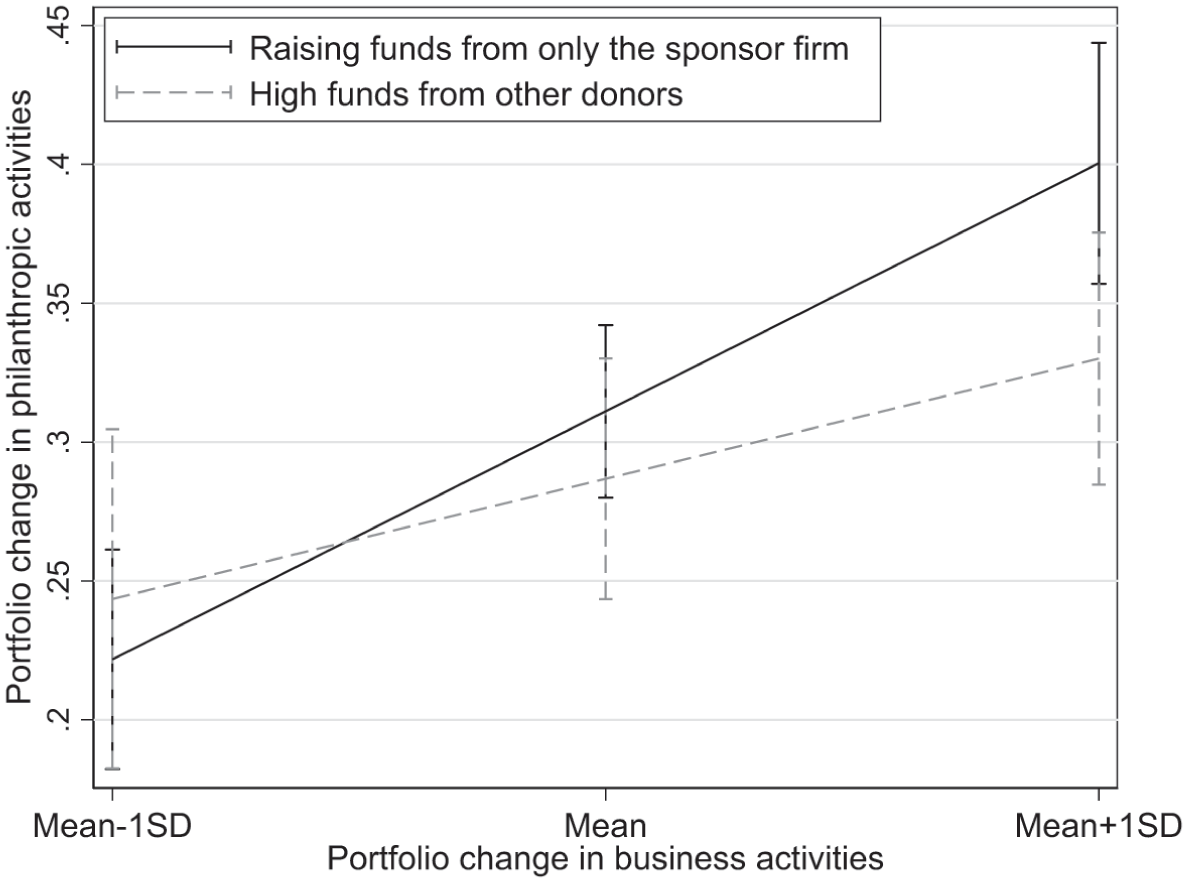

Table 5 examines whether nonprofit-oriented forces are associated with weaker responsiveness of CFs’ philanthropic portfolios to sponsor firms’ business changes. Model 4 includes the interaction between business change and executives’ nonprofit backgrounds. The interaction term is negative and significant (β = −0.69, p = .000), consistent with Hypothesis 2a. This result indicates that the positive association between business change and philanthropic portfolio change is weaker in foundations with a higher proportion of executives with nonprofit backgrounds. Model 5 includes the interaction between business change and funds from other donors. The interaction is negative and significant (β = −0.46, p = .006), consistent with Hypothesis 3a. Model 6 includes both interaction terms simultaneously. In this specification, the interaction between business change and executives’ nonprofit backgrounds remains negative and statistically significant (β = −0.59, p = .001), whereas the interaction with funds from other donors becomes attenuated and marginally significant (β = −0.27, p = .088). This pattern suggests partial overlap between the two moderating conditions in practice, consistent with their moderate correlation (r = 0.30).

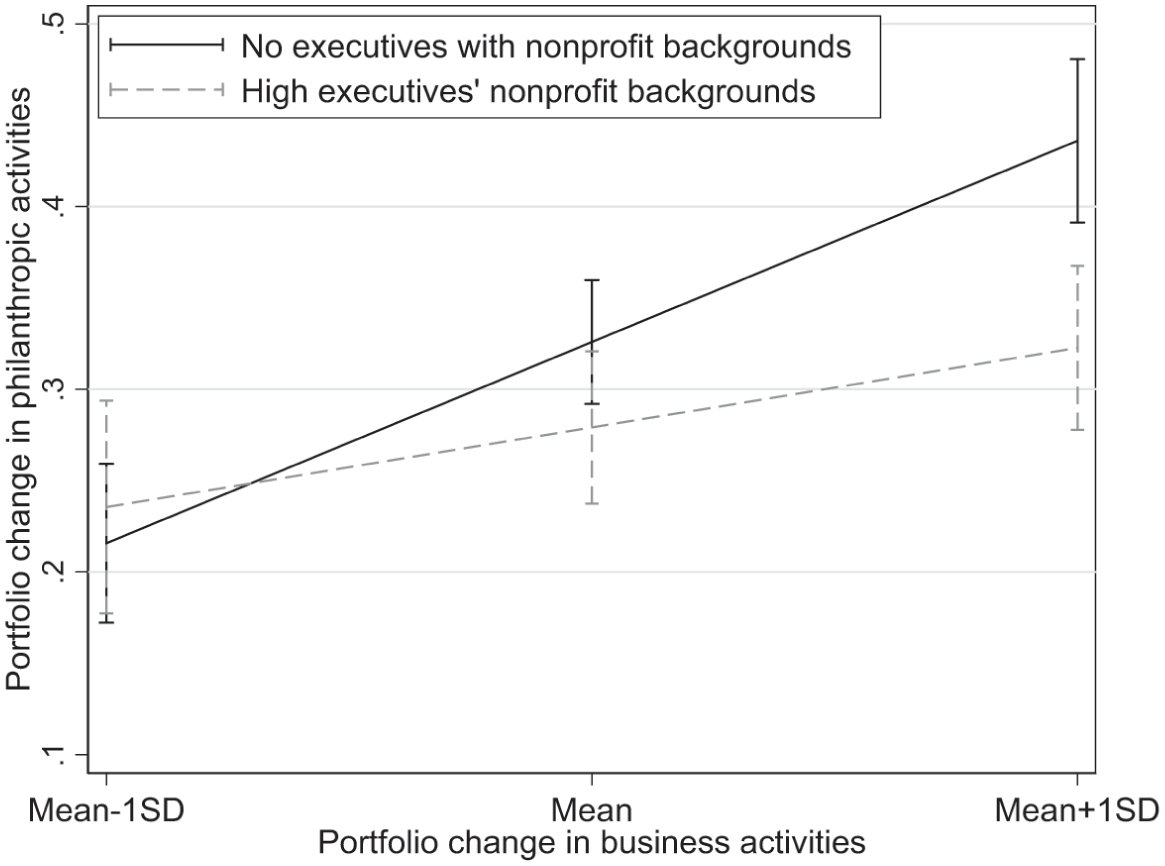

Figures 1 and 2 illustrate these interactions. The positive relationship between business change and portfolio change in philanthropic activities is more pronounced for CFs without nonprofit-background executives or those relying solely on sponsor funding. In contrast, the relationship is notably weaker among CFs with higher proportion of nonprofit-background executives (mean + 1 SD) or with more funds from other donors (mean + 1 SD). Notably, differences across governance and funding configurations are relatively small at lower levels of business change, with clearer separation emerging at higher levels. This pattern suggests that nonprofit-oriented forces are most consequential under conditions of substantial business portfolio shifts.

Moderating Effect of Executives’ Nonprofit Backgrounds

Moderating Effect of Funds From Other Donors

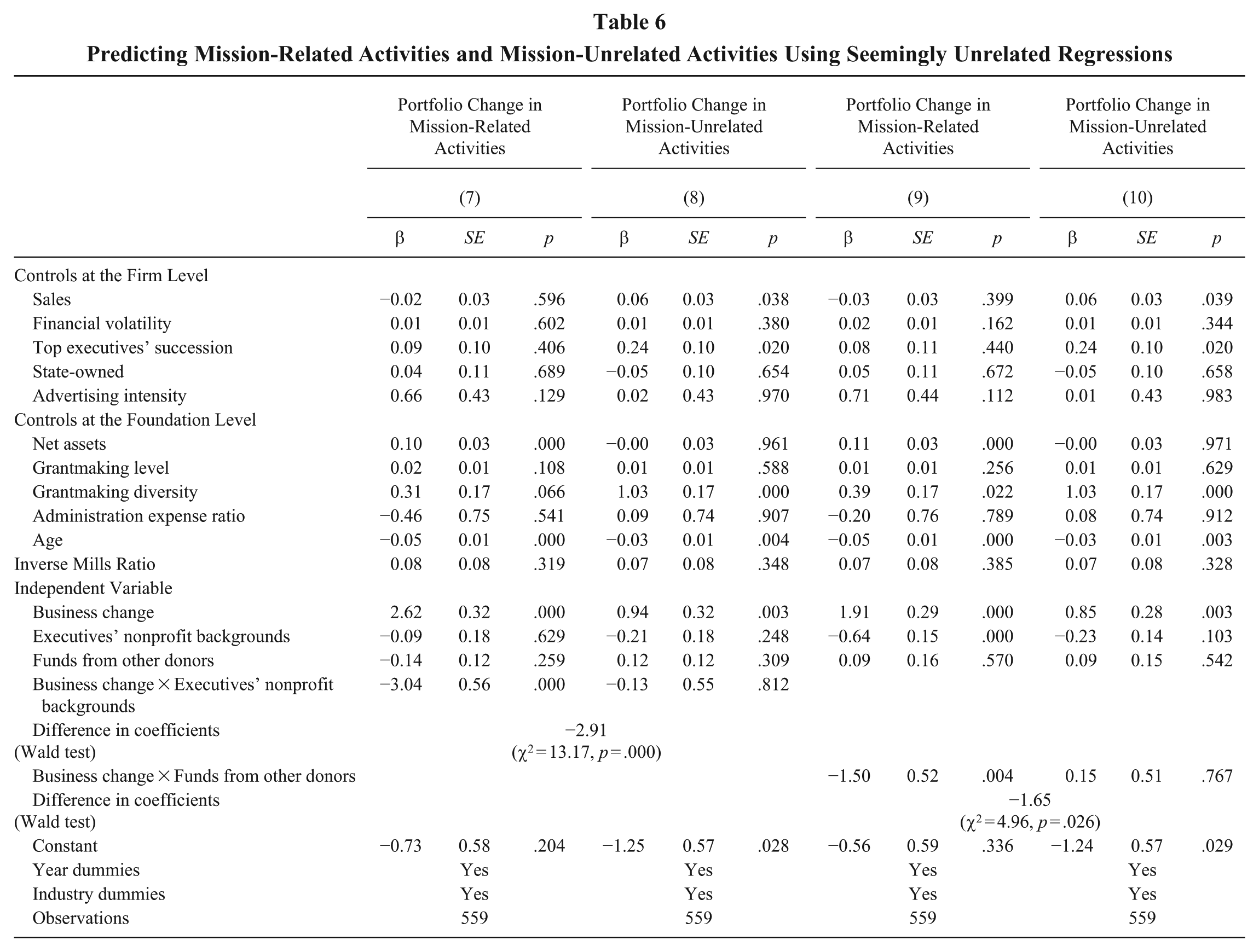

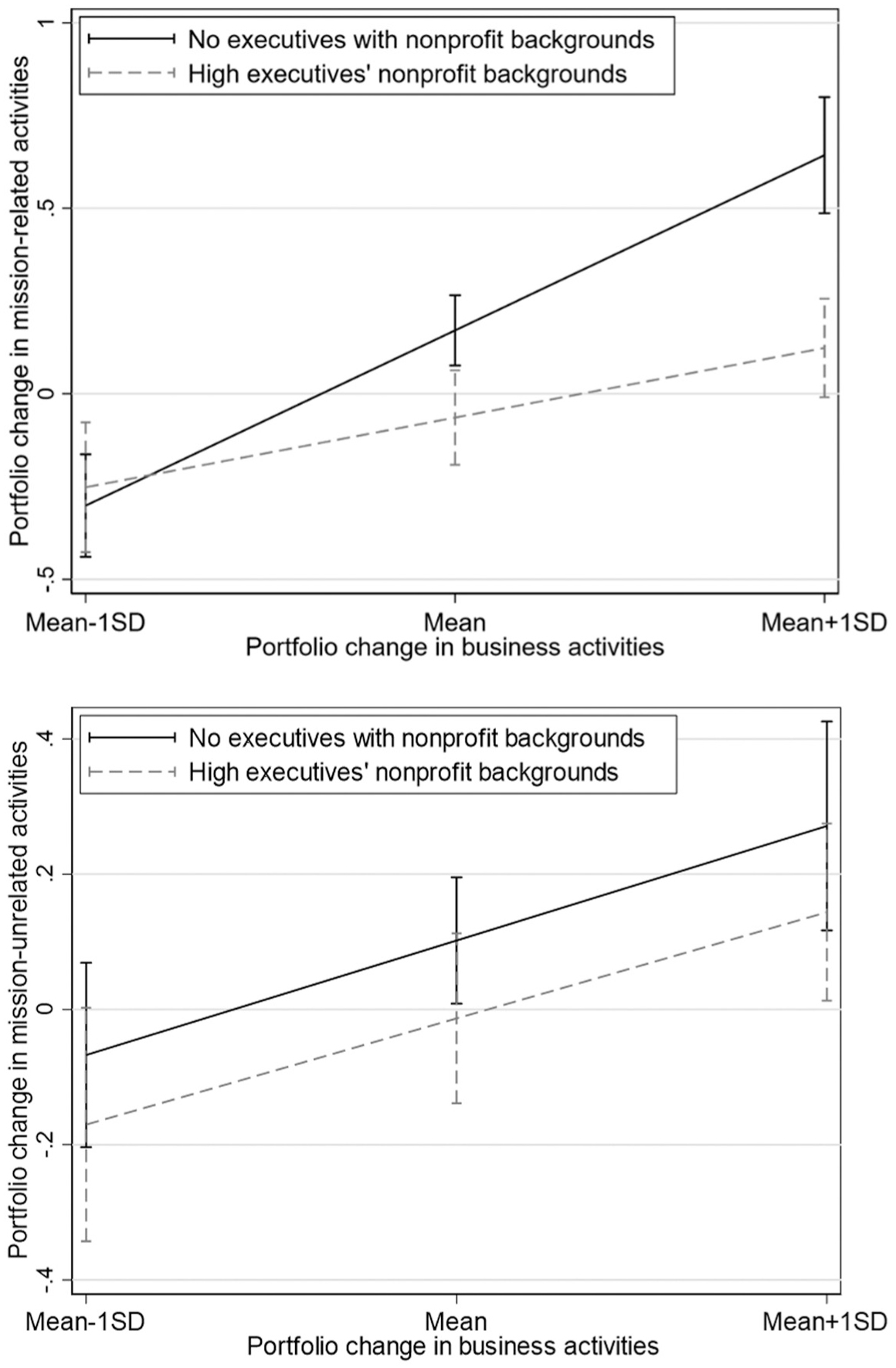

Table 6 presents SUR results comparing moderating effects across mission-related and mission-unrelated activities. Across models, business change is positively associated with portfolio change in both mission-related and mission-unrelated activities, indicating that sponsor firms’ business shifts coincide with compositional changes across CFs’ philanthropic operations. Models 7 and 8 test Hypothesis 2b. The interaction between business change and executives’ nonprofit backgrounds is negative and significant when predicting portfolio change in mission-related activities (β = −3.04, p = .000), but not significant when predicting portfolio change in mission-unrelated activities (β = −0.13, p > .1). A Wald test confirms that the difference between these coefficients is statistically significant (∆ = −2.91, χ2 = 13.17, p = .000). Hence, Hypothesis 2b is supported.

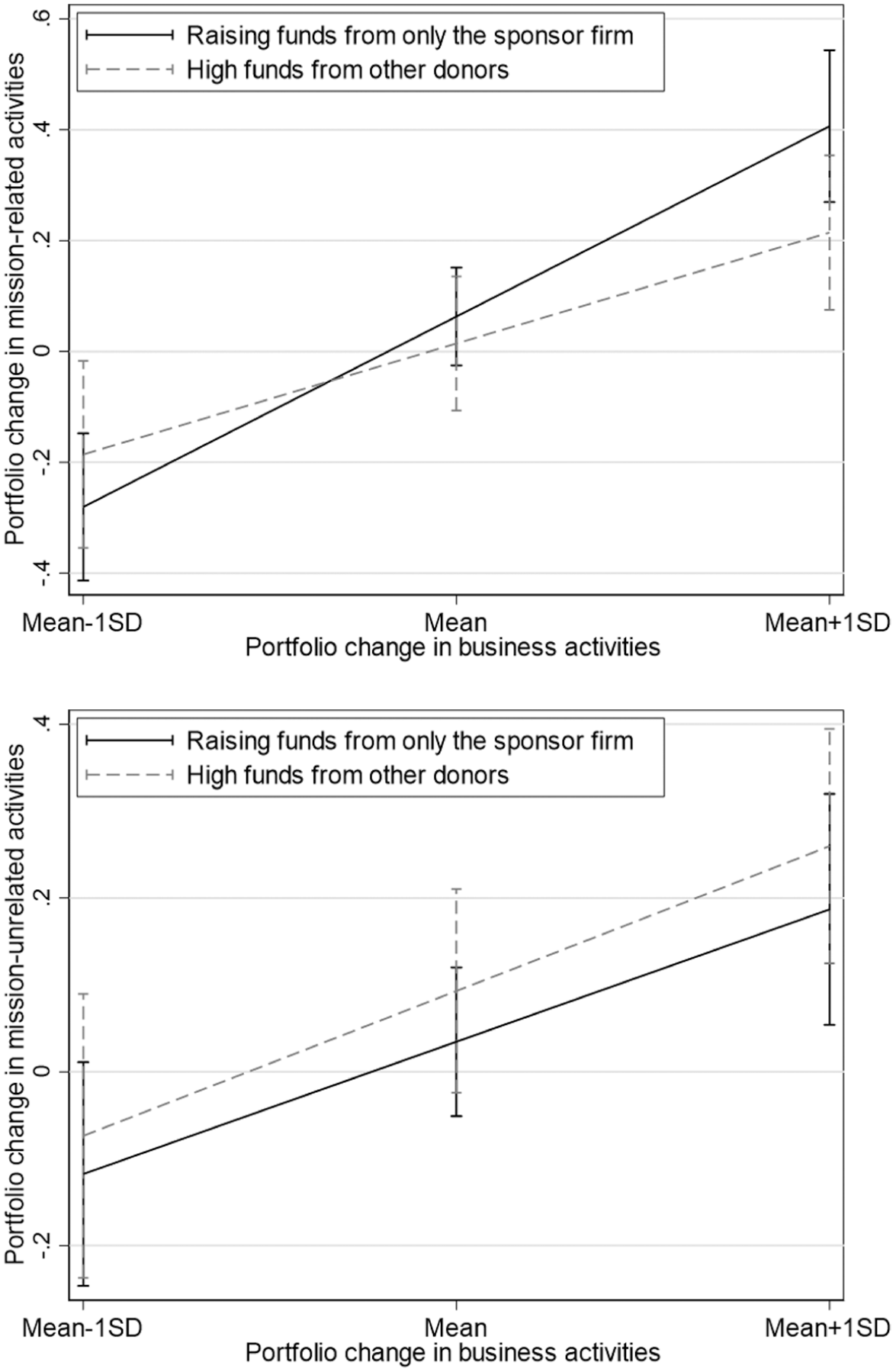

Models 9 and 10 evaluate Hypothesis 3b. The interaction between business change and funds from other donors is negative and significant when predicting portfolio change in mission-related activities (β = −1.50, p = .004), but not significant when predicting portfolio change in mission-unrelated activities (β = 0.15, p > .1). Again, the Wald test confirms that the difference between these interaction terms is significant (∆ = −1.65, χ2 = 4.96, p = .026), supporting Hypothesis 3b. Figures 3 and 4 illustrate these differential effects across mission-related and mission-unrelated activity domains.

Comparing the Moderating Effect of Executives’ Nonprofit Backgrounds When Predicting Portfolio Change in Mission-Related Versus Mission-Unrelated Activities

Comparing the Moderating Effect of Funds From Other Donors When Predicting Portfolio Change in Mission-Related Versus Mission-Unrelated Activities

Note that the sample size decreased from 865 observations in the full sample to 559 observations in Table 6, as the dependent variables for this analysis can only be measured among CFs with clear missions. CFs without clearly articulated mission statements were excluded. To rule out selection bias, we applied a Heckman correction, and results confirm that this sample reduction does not significantly affect our findings (see online Appendix B).

Supplemental Analyses and Robustness Checks

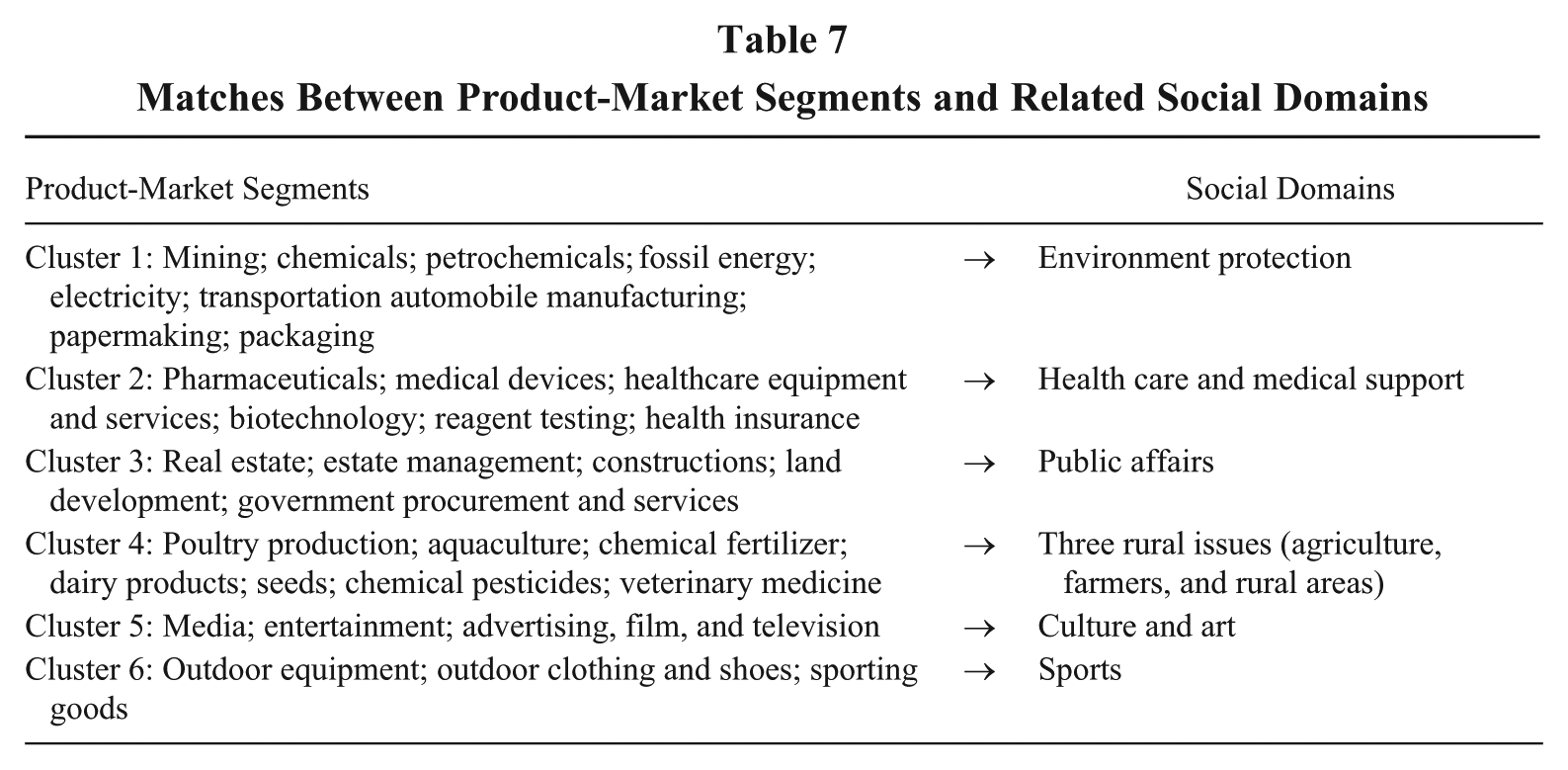

To further examine whether shifts in business portfolios are directionally aligned with changes in philanthropic domains, we constructed matched product-market and social domain clusters. In particular, we identified six clusters linking product-market segments with relevant social domains based on prior literature and industry practices (see Table 7). For example, firms in high emission industries often support environment causes for reputational repair (Luo, Kaul, & Seo, 2018); pharmaceutical or medical businesses frequently fund public health initiatives (Brown et al., 2006); and real estate companies actively donate to improve public services and facilities in local communities where they run construction projects.

Matches Between Product-Market Segments and Related Social Domains

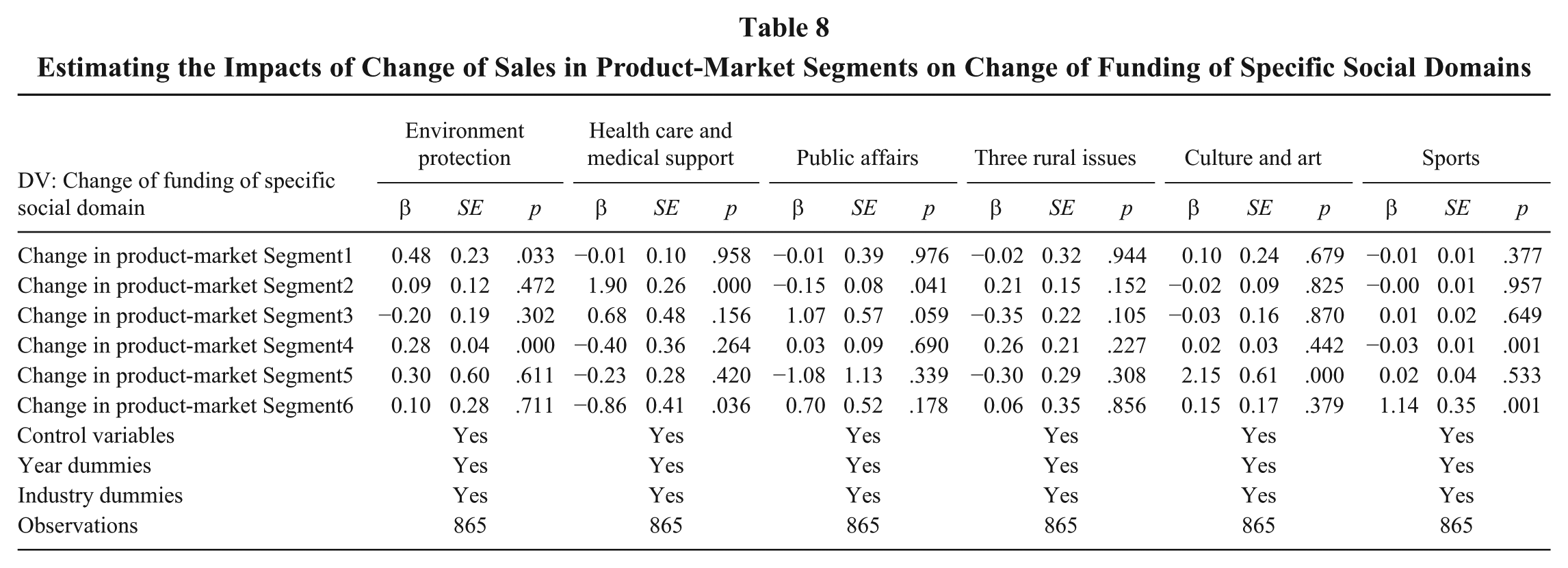

We constructed six explanatory variables—change in product-market segment 1/2/3/4/5/6—to capture the extent of firms’ business shift towards specific product-market segments. For each cluster of product-market segments, we first calculated the segments’ sales proportion among firms’ total annual sales, and then measured the year-to-year change of this proportion. Dependent variables captured proportional change in CFs’ funding of corresponding social domains. Table 8 presents the results based on random-effects models, which confirm directional alignment between business change and shifts in philanthropic focus: CFs tend to change philanthropic activities in directions that align with firms’ business. For example, increased sales in high-emission sectors (Cluster 1 including mining, chemicals, petrochemicals, fossil energy) are positively associated with CFs’ increased donations to the social domain of environment protection (β = 0.48, p = .033). Growth in pharmaceutical segments (Cluster 2 including pharmaceuticals, medical devices, biotechnology) predicts greater donations to social domains of health care and medical support (β = 1.90, p = .000). Expansion in real estate and construction (Cluster 3 including real estate, constructions, land development) aligns with increased support for social domains of public affairs (β = 1.07, p = .059). Other results are similarly consistent with theorized matches, including significant effects for culture and arts (β = 2.15, p = .000) and sports (β = 1.14, p = .001). The result for rural development (Cluster 4) is not statistically significant (β = 0.26, p > .1).

Estimating the Impacts of Change of Sales in Product-Market Segments on Change of Funding of Specific Social Domains

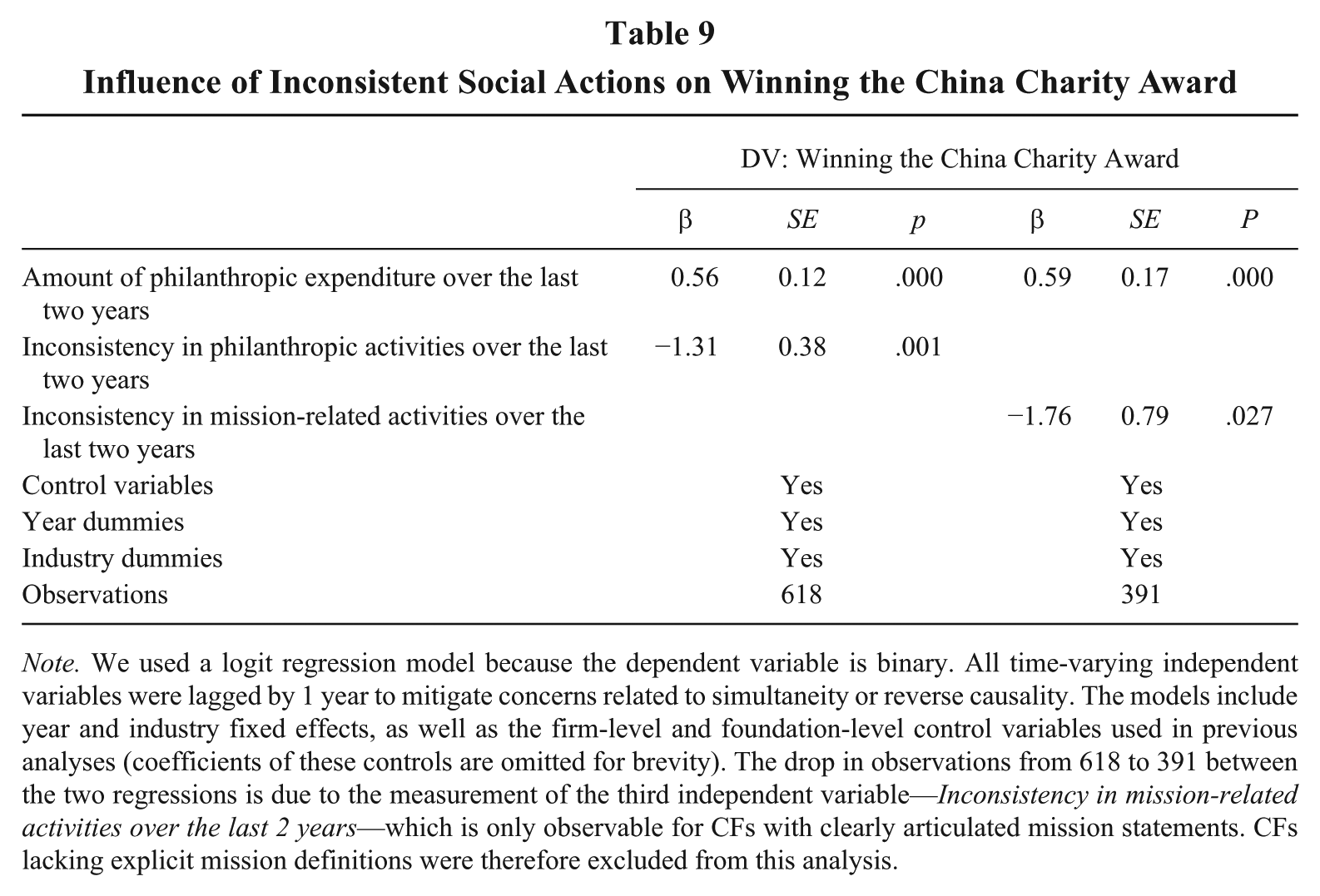

We also examined the social cost of inconsistent social actions by analyzing CFs’ receipt of China Charity Award—the nation’s most prestigious recognition for innovative social practices and outstanding social impact. This biennial award is granted by the Ministry of Civil Affairs and the China Charity Federation and provides a valuable context for examining how the patterns of CFs’ philanthropic activities over 2-year periods influence their social evaluations. Table 9 shows that the total amount (logged) of CFs’ philanthropic expenditure in the prior 2 years is positively associated with the probability of receiving the Award, as expected. However, after controlling for philanthropic spending, inconsistency in philanthropic activities significantly reduces the likelihood of winning (β = −1.31, p = .001). Among CFs with specified social missions, inconsistency in mission-related activities also predicts a lower chance of receiving the award (β = −1.76, p = .027). These results suggest that CFs’ inconsistent social actions carry reputational and symbolic costs, potentially undermining the social legitimacy of CFs.

Influence of Inconsistent Social Actions on Winning the China Charity Award

Note. We used a logit regression model because the dependent variable is binary. All time-varying independent variables were lagged by 1 year to mitigate concerns related to simultaneity or reverse causality. The models include year and industry fixed effects, as well as the firm-level and foundation-level control variables used in previous analyses (coefficients of these controls are omitted for brevity). The drop in observations from 618 to 391 between the two regressions is due to the measurement of the third independent variable—Inconsistency in mission-related activities over the last 2 years—which is only observable for CFs with clearly articulated mission statements. CFs lacking explicit mission definitions were therefore excluded from this analysis.

Our theory suggests that the asymmetric pattern—wherein mitigating associations are more pronounced for mission-related activities than for mission-unrelated activities—depends on the presence of nonprofit-oriented forces and the buffering structures they enable. In other words, this asymmetry is not expected to arise mechanically from business change alone. To examine this premise more directly, we estimated baseline models regressing sponsor firms’ business portfolio changes on both mission-related and mission-unrelated philanthropic portfolio changes without including the moderating variables. The results (see Table C1 in online Appendix C) indicate that the asymmetric effects do not arise automatically in the baseline predictions but instead emerge only under specific enabling conditions articulated in our moderating hypotheses.

To assess the robustness of our findings to alternative estimation strategies, we re-estimated the main models using foundation fixed-effects specifications. Because fixed-effects models absorb time-invariant characteristics, variables such as state-owned and industry dummies are omitted in these estimations. Despite this stricter specification—which relies solely on within-foundation variation over time—the core patterns remain substantively similar (see Table D1 in online Appendix D). The coefficients for all baseline effects and moderating effects remain statistically significant.

We also considered the possibility that the presence of executives with nonprofit backgrounds may be endogenous. Foundations that appoint such executives may differ systematically from others in unobserved ways—for example, in underlying social orientation or sponsor firm values. To address this concern, we implemented propensity score matching (PSM), matching CFs with and without nonprofit-background executives on observable characteristics, including sponsor firm attributes and foundation-level controls (Dehejia & Wahba, 2002). Using the matched samples, we re-estimated Model 4 in Table 5 and Models 7 and 8 in Table 6; results remain consistent (see Tables E1–E2 in online Appendix E). While PSM does not eliminate all endogeneity concerns, these results suggest that observable selection differences are unlikely to account for the moderating patterns we document.

To ensure that our results are not sensitive to the specific operationalization of portfolio change, we employed alternative outcome measures. First, we calculated the portfolio change in philanthropic activities using Euclidean distance rather than the reverse Cosine similarity metric. Second, we constructed a count-based measure capturing the number of social domains in which a foundation altered its funding allocation from one year to the next. Because funding requirements differ across social domains, this count-based measure is less sensitive to differences in expenditure scale. Both alternative operationalizations yield substantively similar results to our primary specifications (see Tables F1 and F2 in online Appendix F).

Lastly, we considered the possibility that certain portfolio shifts reflect responses to urgent social needs rather than to sponsor firms’ business changes. In such cases, discontinuity in project engagement does not necessarily indicate a lack of commitment to the CF’s social missions. Disaster relief projects, in particular, are often episodic and may generate year-to-year discontinuities that do not reflect instability in mission commitment. To address this concern, we recalculated the dependent variable after excluding disaster relief activities from the philanthropic portfolio. The results remain consistent with our main findings (see Table F3 in online Appendix F), suggesting that the documented associations are not driven by short-term humanitarian responses.

Taken together, these supplementary analyses provide convergent evidence that the documented associations are not artifacts of model specification, measurement choice, or episodic philanthropic activity. While our design remains correlational, the consistency of results across multiple robustness checks strengthens confidence in the empirical patterns reported in the main analyses.

Discussion

In this study, we examined how changes in sponsor firms’ business portfolios are associated with instability in the philanthropic portfolios of their affiliated CFs. We find that year-to-year shifts in sponsor firms’ business activities are positively associated with changes in CFs’ philanthropic portfolios, indicating that sponsor firms’ evolving business priorities represent one important source of variation in philanthropic instability. These findings suggest that, despite their legal independence, CFs’ philanthropic engagement is meaningfully shaped by the business dynamics of their sponsor firms.

At the same time, this influence is not uniform across foundations. CFs with a higher proportion of executives with nonprofit backgrounds and those receiving greater funding from non-corporate donors exhibit weaker associations between sponsor firms’ business changes and philanthropic portfolio shifts. Moreover, these moderating associations are asymmetric in mission-related and mission-unrelated domains. When nonprofit-oriented governance and funding structures are present, changes in sponsor firms’ business portfolios are less strongly associated with instability in mission-related activities than in mission-unrelated activities. This asymmetry pattern is consistent with activity compartmentalization within philanthropic portfolios.

Contributions to Research on Social Missions Under Resource Dependence

Our study contributes to ongoing conversations about how organizations pursue social missions while operating under resource dependence. Prior research has emphasized the potential for corporate affiliation to create tensions between commercial priorities and social commitments (Ebrahim et al., 2014), although corporate donations constitute a key source of nonprofit funding (Gautier & Pache, 2015). We extend this literature by identifying a dynamic pathway through which such tensions may manifest: sponsor firms’ business portfolio changes account for part of the observed compositional shifts in affiliated foundations’ philanthropic engagement over time. Such disruptions can be problematic because many social issues require sustained engagement to generate meaningful outcomes (Cranenburgh & Arenas, 2014; Meijs, 2010). By documenting the disruptive influence, we move beyond generalized claims of “mission drift” (Grimes et al., 2019) to document how inconsistency in philanthropic engagement unfolds over time and under what organizational conditions it varies. The finding that such inconsistency is negatively associated with external recognition (China Charity Award) further underscores its potential implications for social legitimacy.

More broadly, our study challenges overly optimistic views of corporate philanthropy as a “win-win” or “shared value” proposition. While these frameworks emphasize alignment between business and social objectives (Aakhus & Bzdak, 2012; Porter & Kramer, 2011), they often understate the trade-offs between short-term strategic responsiveness to shifting corporate priorities and the long-term needs for supporting social beneficiaries and addressing social issues (Wry & Zhao, 2018).

Contributions to Dependency Management and Buffering

We further contribute to research on dependency management by examining how organizational conditions are associated with differential responsiveness under entrenched dependence and close oversight. Much of the RDT literature emphasizes strategies that reduce dependence or rely on symbolic buffering (Oliver, 1991; Pfeffer & Salancik, 1978; Wry et al., 2013). However, such approaches may be structurally constrained in settings where power asymmetries are embedded and transparency requirements are high.

Our findings suggest that variation in governance composition and funding structure is associated with differences in how philanthropic portfolios evolve in response to sponsor firms’ business changes. Specifically, the presence of nonprofit-oriented executives and non-corporate funding partners is associated with weaker alignment between business portfolio shifts and philanthropic instability. While our design does not permit direct observation of internal decision processes, the observed patterns are consistent with the view that nonprofit-oriented actors help preserve organizational autonomy by introducing evaluative criteria and accountability expectations that shape how discretion is exercised once external demands arise. These governance features may also co-occur in practice; for example, nonprofit-oriented executives may facilitate CFs’ access to external funding.

Moreover, we identify a novel form of buffering within prosocial activities—activity compartmentalization based on mission relatedness. Rather than relying on symbolic buffering approaches that conceal or obscure activities (Oliver, 1991; Pfeffer & Salancik, 1978), this mechanism reflects more substantive responsiveness to external demands under conditions of close oversight. When nonprofit-oriented forces are present, mission-related activities exhibit greater stability, whereas mission-unrelated domains display greater flexibility. This asymmetry pattern extends prior research on compartmentalization, which has primarily examined separation among commercial units or between commercial and social units (e.g., Lee & Bansal, 2024; Stål & Corvellec, 2022). We instead document compartmentalization within prosocial activities themselves, uncovering the mechanism through which CFs minimize the tensions inherent in their dependency management—between safeguarding social missions and retaining support from corporate sponsors. Our observation of this form of buffering is consistent with the view that nonprofit-oriented actors shape how discretion over philanthropic operation is exercised in response to external demands, particularly through adaptation that involves lower perceived costs under their evaluative criteria.

More broadly, activity compartmentalization provides mission-driven organizations with a viable means to balance adaptation to changing environmental demands with preserving authenticity in pursuing core missions and long-term payoffs (Grimes et al., 2019; Kouamé et al., 2022).

Contributions to Governance and the Role of Professional Background

Our findings also speak to research on governance boards and executive composition in nonprofit and hybrid organizations. Prior research highlights boards as boundary-spanning structures that link organizations to external resource providers, helping organizations reduce resource uncertainty by absorbing and aligning with external interests (Davis & Cobb, 2010; Pfeffer & Salancik, 1978). Yet, alignment with powerful stakeholders may also constrain autonomy when stakeholder priorities diverge from organizational missions (Wry et al., 2013).

Although executives are often seen as unlikely to resist pressures tied to managing crucial dependencies, we show how the professional backgrounds of CF executives are associated with differential patterns of philanthropic responsiveness. Drawing upon their nonprofit expertise and value orientations, these executives evaluate corporate demands and may negotiate or push back when such pressures create acute conflicts of interest. In our case, CFs with a greater presence of executives socialized in nonprofit settings exhibit weaker associations between sponsor firms’ business changes and philanthropic instability—particularly in mission-related domains. These findings suggest that board composition and executive background shape how organizations navigate competing logics and external pressures, extending scholarship on organizational autonomy amid multiple and competing interests (e.g., Ebrahim et al., 2014; Smith & Besharov, 2019). Importantly, we interpret these patterns as conditional associations rather than as evidence of deliberate resistance or purposive strategy.

Practical Implications

Our findings carry important implications for the governance of CFs. Although CFs benefit from corporate sponsorship, close alignment with shifting business priorities may coincide with inconsistency in philanthropic engagement. Such instability may result in fragmented and opportunistic social engagement, undermining continuity in supporting beneficiaries and weakening commitment to key stakeholder groups.