Abstract

Although calls for firms to disclose their political spending have intensified, nonmarket strategy scholars have yet to explain why some firms embrace corporate political transparency (CPT) while others remain opaque. We theorize that CEO political ideology serves as a critical antecedent of CPT. We argue that liberal CEOs, valuing stakeholder accountability, favor CPT, whereas conservative CEOs, prioritizing shareholder primacy and reputational control, resist it. We further argue that the effect of CEO ideology on CPT depends on contextual factors that shape the discretion CEOs retain in navigating CPT trade-offs. Using a sample of publicly traded firms covered by the Zicklin CPT Index, we find that CEO liberalism increases CPT, but this effect weakens when firm-specific political uncertainty is high, when industry-level transparency norms are strong, and when industry concentration is high. Our study recasts CPT as a value-infused choice contingent on boundary conditions that influence managerial discretion, extends upper echelons theory into the political arena, and advances political activity research.

Keywords

Introduction

On November 9, 2021, The New York Times reported that Mercedes-Benz and Volvo, among other automakers, had committed to ending the production of gasoline and diesel vehicles by 2040 (Plumer & Tabuchi, 2021). However, behind the scenes, the Truck and Engine Manufacturers Association, a lobbying group representing these firms, was working to weaken legislation aimed at curbing emissions (Phillips, 2022). This discrepancy between the firms’ public commitments and private actions underscores a critical tension in corporate political activity (CPA): firms often engage in covert influence efforts while outwardly signaling support for progressive policies. These actions are enabled by the structure of U.S. politics, which permits covert, or “dark money,” expenditures and indirect lobbying to go undisclosed to the public (Jia, Markus, & Werner, 2023; Minefee, McDonnell, & Werner, 2021; Werner, 2017).

Because covert CPA is largely legal but opaque, it has triggered mounting demands for companies to voluntarily disclose how they attempt to influence government through political donations, lobbying, and third-party associations (Lyon et al., 2018; Mithani, 2019). These calls, which originated from investors and policy advocates, among others, reflect a growing concern over the misalignment between firms’ stated values and hidden political behavior (Lynes, Treadwell, & Bavin, 2024; Zingales, 2017). Although corporate political transparency (CPT) can be beneficial to the firm, as firms may gain legitimacy, stakeholder trust, and support, firms face a transparency paradox. While political transparency can yield benefits, it may also expose the firm to criticism and risk, especially when political activities conflict with stakeholder values (Kamasak, Yavuz, & Akin, 2019; Shanor, McDonnell, & Werner, 2021). Indeed, disclosure of controversial contributions can lead to backlash and reputational damage if stakeholders perceive those actions as misaligned with the company’s espoused values (Albu & Flyverbom, 2019; Preuss & Wielhouwer, 2024).

Despite these stakes, research on what drives firms to voluntarily disclose their political activity remains limited. Indeed, while some firms adopt formal policies regulating political activity and voluntarily disclose those activities, others remain silent, suggesting that this is a strategic decision about which we know very little and that is likely influenced by executive values and biases (Hambrick, 2007; Hambrick & Mason, 1984). Recently, the upper echelons (UET) literature has turned its attention to how values, as evidenced through political ideology, influence strategic decision making (Chin, Hambrick, & Treviño, 2013; Chin & Semadeni, 2017; Gupta, Briscoe, & Hambrick, 2018). CEO political ideology, defined as a stable set of values regarding governance, regulation, and the role of business in society, may shape how executives navigate ethically and politically sensitive decisions (Chin et al., 2013; Hibbing, Smith, & Alford, 2014; Jost, 2006). Yet whether, and how, CEO ideology affects CPT remains an open empirical question.

Thus, in this paper, we posit that firms helmed by more liberal CEOs will engage in greater CPT because their value system is more strongly aligned with institutional accountability and societal norms (Chin et al., 2013; Jost, Federico, & Napier, 2009). Conversely, more conservative CEOs, attuned to shareholder primacy and concerned about the potential reputational costs of disclosure, will be less inclined to voluntarily disclose politically sensitive activities, as such disclosures might invite media scrutiny or external interference (Jia et al., 2023; Werner, 2017).

Further, drawing on and extending the managerial discretion perspective (Hambrick, 2007; Hambrick & Finkelstein, 1987), we argue that the extent to which CEO ideology shapes CPT depends on the latitude of action available. Specifically, we argue that the strength of the CEO ideology–CPT link is contingent on three contextual contingencies that shape managerial discretion. First, firm-level political uncertainty limits discretion by magnifying the risks of political engagement. Second, industry political transparency norms can either constrain discretion by imposing institutional pressures or expand it by permitting ideological expression. Third, industry concentration influences the CEO’s level of discretion and engagement in transparency. Together, these contextual contingencies clarify when CEO liberalism is most likely to translate into greater transparency.

To test our theory, we collected a longitudinal dataset of major U.S. publicly traded firms from 2012 to 2021, using disclosure and policy commitment data from the Zicklin Center to measure CPT, as these elements are most likely to be influenced by CEOs. Our results suggest that the effect of CEO ideology on CPT is far from uniform and is instead shaped by relevant contextual factors. Specifically, we find that liberal CEOs increase CPT in stable political environments and industries with low-transparency norms, but in settings marked by political uncertainty, strong normative pressures, or high industry concentration, the relationship is weaker. This suggests that while CPT is directly influenced by CEO liberalism, it is also a strategic behavior shaped by discretion, emanating from context and perceived reputational stakes. Finally, we also find evidence from CEO succession events that a change toward a more liberal CEO leads to increased transparency, and thus succession can influence the firm’s transparency.

Our study makes two contributions that span the CPT, UET, and nonmarket strategy literature. First, we advance the CPT literature by introducing a behavioral perspective that explains variation in voluntary disclosure decisions. Existing research emphasizes how external pressures like stakeholder activism, regulations, and investor demands drive transparency (Goh, Liu, & Tsang, 2020; Lyon et al., 2018; Walker, 2023), but does not explain substantial within-industry variation among similar firms. By examining CEO political ideology, we demonstrate that transparency decisions reflect normative beliefs about the appropriate role of corporate political influence. Liberal CEOs view transparency as accountability that legitimates engagement, while conservative CEOs view it as a potential strategic vulnerability. This suggests that transparency embodies deeper ideological tensions about corporate power and democratic accountability, not merely instrumental stakeholder management. Second, we extend UET by identifying three boundary conditions under which CEO ideology shapes nonmarket strategy. We demonstrate that ideology’s influence on CPT depends on political uncertainty, industry transparency norms, and industry concentration. Overall, these moderating mechanisms suggest that values matter most when executives possess discretion (Hambrick, 2007; Hambrick & Finkelstein, 1987), but different contextual factors asymmetrically moderate liberal versus conservative CEOs through distinct mechanisms.

Literature Review

“Dark money” refers to expenditures intended to influence political outcomes that are often channeled through nonprofit organizations that are not legally required to disclose their donors (Werner, 2017). This redirection of expenditures is one way organizations avoid legally required public disclosure of political activity. In practice, this often occurs when firms direct political spending through trade associations and business coalitions. Prominent associations such as the U.S. Chamber of Commerce and the Business Roundtable engage in policy advocacy while shielding the identities and agendas of their corporate backers. Following the Citizens United decision, the use of such indirect political mechanisms has surged (Hadani & Schuler, 2013), with one study documenting a 38-fold increase in dark money spending in certain U.S. states between 2006 and 2014 (Brickner, 2016). These developments have enabled firms to engage in political influence while avoiding legally required accountability. In response to this situation, external stakeholders such as public interest groups, institutional investors, and regulatory advocates have begun calling for greater levels of CPT (Ali, Adegbite, & Nguyen, 2023; Goh et al., 2020; Lyon et al., 2018; Polman, 2021). Moreover, in its 2023 Transparency and Integrity Report, Altria recognized this increasing CPT expectation, noting that “shareholders and the public want greater access to information about a company’s lobbying and political activities” (p. 2). This increase in calls stems from a host of potential benefits that political transparency offers. However, although there are potential benefits to political transparency (see Mithani, 2019, for a full review), firms face a pervasive “transparency paradox” whereby political transparency can potentially lead to benefits yet also harm.

The Benefits of Corporate Political Transparency

When firms engage in political transparency, they can materialize several interrelated benefits. First, CPT enhances legitimacy and stakeholder trust by demonstrating corporate accountability and ethical behavior (Gao & Hafsi, 2019; Masud, Bae, Manzanares, & Kim, 2019; Okhmatovskiy, 2010). By making political activities visible, firms signal alignment with stakeholders and societal values, fostering stronger relationships with key constituents. This reputational capital is particularly valuable during periods of public scrutiny or crisis, when transparency can buffer firms against criticism and enhance their standing with both political actors and the public (Gagalyuk, Chatalova, Kalyuzhnyy, & Ostapchuk, 2021; McDonnell & Werner, 2016; Smith, 2016). Indeed, politicians prefer to engage with reputable firms, making transparency a potential avenue for maintaining productive political relationships (McDonnell & Werner, 2016).

Second, CPT can generate financial and governance benefits. Transparency reduces information asymmetry between managers and stakeholders regarding political expenditures, thereby lowering agency costs and increasing investor confidence (Ingram, Ridge, & Abdurakhmonov, 2025). When investors view disclosed political activities as strategically sound and aligned with firm interests, transparency enhances firm value and can improve access to capital (DeBoskey, Li, Lobo, & Luo, 2017; Favotto & Kollman, 2021). In this sense, voluntary disclosure functions as a credible signal of managerial accountability and strategic coherence.

The Costs of Corporate Political Transparency

Although CPT offers potential benefits, it also carries downsides, as transparency exposes firms to potential reputational and strategic risks. When disclosure reveals political activities that stakeholders perceive as misaligned with corporate values or contrary to stakeholder interests, transparency can trigger substantial backlash (Albu & Flyverbom, 2019; Preuss & Wielhouwer, 2024). The visibility created by disclosure subjects firms to heightened scrutiny from activists, media, and partisan constituencies, any of whom may mobilize opposition against revealed political positions. This is particularly problematic when firms engage in “corporate political posturing,” or supporting political objectives disconnected from core business interests because such activities may invite accusations of hypocrisy or opportunism (Mithani, 2019).

Moreover, transparency creates competitive and strategic vulnerabilities. Disclosed political contributions and lobbying positions reveal firms’ strategic intentions to competitors, potentially undermining the effectiveness of political investments (Jia et al., 2023). In polarized political environments, transparency can alienate portions of the stakeholder base regardless of the positions disclosed, as revealing support for either partisan coalition invites opposition from the other. The costs of transparency are thus not merely reputational but also strategic, as disclosure constrains firms’ ability to maintain flexibility in their political positioning.

Boundary Conditions: When Does Transparency Help Versus Harm?

The potential divergent outcomes explained above reveal that CPT’s implications are highly contingent rather than uniformly positive or negative. A critical boundary condition is the alignment between disclosed activities and stakeholder expectations. When transparency reveals political engagement that stakeholders view as consistent with corporate values and legitimate business interests, it enhances legitimacy and trust (Gao & Hafsi, 2019). Transparency in such cases functions as intended, reducing information asymmetry, signaling accountability, and generating the governance and performance benefits documented in prior research (Ingram et al., 2025). Conversely, when disclosure exposes political activities that stakeholders perceive as misaligned, whether ideologically incongruent with corporate values or strategically disconnected from business operations, the same transparency triggers reputational damage and stakeholder opposition (Albu & Flyverbom, 2019; Preuss & Wielhouwer, 2024). In these cases, transparency transforms from a legitimacy-building mechanism into a liability-creating one, as it provides activists and critics with concrete information to mobilize against the firm.

Beyond alignment, two other factors influence whether transparency is helpful or harmful. First, sensitivity to political context matters. In highly polarized or volatile political environments, even well-justified political engagements carry elevated risks when disclosed, because partisan scrutiny intensifies regardless of alignment. Second, the firm’s ability to credibly justify its political engagement shapes stakeholder reactions. Firms that can articulate clear connections between political activities and legitimate business interests face less backlash than those whose political engagement appears opportunistic or value inconsistent.

This dual-edged nature of transparency explains why executives face genuine strategic uncertainty when considering political disclosure. The same disclosure that could build trust and reduce agency costs might instead trigger backlash and competitive exposure, depending on stakeholder perceptions of political activity alignment. For executives, the transparency decision thus hinges on their beliefs about whether their firms’ political activities will be viewed favorably under external scrutiny. This judgment is shaped by their own values and assumptions about stakeholder expectations. We address this by investigating CEO political ideology as a key antecedent to political transparency and argue that CEO liberalism shapes how CEOs interpret the reputational, strategic, and normative trade-offs associated with disclosure.

CEO political ideology

Recent work in the strategic leadership literature has provided evidence of the importance of values, as reflected in political ideology, in organizational strategy and decision making (Chin et al., 2013; Jost, 2006). Political ideology is a stable and socially meaningful belief system that captures fundamental differences in cognitive style, risk tolerance, and moral reasoning (Graham, Haidt, & Nosek, 2009; Poole & Rosenthal, 1984). Broadly, liberals and conservatives differ across three relevant domains that influence strategic decision making: (1) Market orientation: liberals are more likely to concern themselves with market imperfections, while conservatives favor market autonomy; (2) Attentional focus: liberals adopt a broader stakeholder perspective, whereas conservatives emphasize the primacy of shareholders in publicly traded organizations; and (3) Decision making style: more liberal individuals tend to be more open to innovation and change, whereas their more conservative counterparts favor tradition and the status quo (Weng & Yang, 2023). In line with these broad domains, individuals higher in liberalism have also been shown to exhibit higher tolerance for ambiguity, openness to new experiences, and greater risk taking, whereas conservatives display a preference for order, stability, and conventional norms (Christensen, Dhaliwal, Boivie, & Graffin, 2015; Jost et al., 2009; Jost, Glaser, Kruglanski, & Sulloway, 2003).

Moreover, and key to our context, research suggests that conservative CEOs view CPA as both legitimate and necessary (Unsal, Hassan, & Zirek, 2016) because they perceive CPA as an appropriate exercise of corporate rights consistent with shareholder primacy (Friedman, 2007), and they see no obligation to subject it to external scrutiny. Transparency would only invite interference in what they view as a legitimate business activity. In contrast, liberal CEOs are more attuned to normative concerns in the broader institutional environment about disproportionate corporate influence in democratic processes (Lund & Strine, Jr., 2022). Their ideological orientation toward institutional accountability and checks on concentrated power (Jost et al., 2009) makes them more receptive to calls for transparency as a preemptive accountability mechanism. By making political activities visible, transparency enables external monitoring that can constrain potential corporate political influence from operating unchecked, thereby aligning the firm with democratic accountability norms.

Thus, ironically, the fact that conservatives are more comfortable with corporate political involvement does not make them “pro-transparency”; rather, because they see such involvement as correct, they are not compelled to justify to external outsiders via transparency. These ideological commitments provide a theoretically and practically grounded lens for examining executive behavior in CPA, particularly when decisions involve reputational ambiguity or public scrutiny.

Research in the upper echelons tradition provides evidence that CEO ideology has measurable effects on a range of firm behaviors and outcomes. For instance, liberal CEOs tend to helm firms with greater pay equity in their top management teams (Chin & Semadeni, 2017), have a broader internal resource distribution (Gupta et al., 2018), and engage in more socially responsible actions (Chin et al., 2013). Alternatively, research suggests that conservative CEOs favor risk-averse or fiscally restrained strategies, including lower R&D investment, reduced debt levels, and fewer mergers and acquisitions (Elnahas & Kim, 2017; Hutton, Jiang, & Kumar, 2014). Moreover, Christensen et al. (2015) found that conservative CEOs are less likely to engage in aggressive tax avoidance, reflecting their greater sensitivity to regulatory and reputational risks.

Theory and Hypotheses

CEO Values and CPT

Prior research suggests that liberal CEOs are more likely to prioritize external stakeholders and the broader environment (Chin et al., 2013; Gupta & Briscoe, 2020). Indeed, more liberal CEOs tend to view firm legitimacy and performance as contingent upon stakeholder engagement and responsiveness to societal needs (Briscoe, Chin, & Hambrick, 2014; Gupta, Briscoe, & Hambrick, 2017). Supporting this view, recent research further documents ideological asymmetries in beliefs about the purpose of business, showing that liberals are more likely than conservatives to scrutinize a firm’s broader societal impact and to expect businesses to go beyond core profit-generating activities (Nair & Mooijman, 2025). Generally, these values are consistent with a broader stakeholder management approach, in which transparency and accountability are viewed as essential to cultivating legitimacy in the eyes of external constituents (Jost et al., 2003).

This is typically argued to be because more liberal individuals are more receptive to social change, more tolerant of uncertainty, and more inclined to support market regulations that advance justice and equity, according to political psychology research (Carroll, Perkowitz, Lurigio, & Weaver, 1987; Jost et al., 2009; Skitka & Tetlock, 1993). These ideological inclinations increase concern for how corporate behavior impacts democratic institutions and public trust, encouraging a more comprehensive understanding of firm-society interconnectedness (Kong, Radhakrishnan, & Tsang, 2017; Lyon et al., 2018). Thus, liberal CEOs are more likely to support political transparency as a way to demonstrate conformity to public expectations and reaffirm the company’s dedication to open governance (Lund & Strine, Jr., 2022; Polman, 2021).

Alternatively, because conservative CEOs view the firm as primarily accountable to its owners (Bizjak, Kalpathy, Mihov, & Ren, 2022), they tend to prioritize shareholder interests and resist external interference in firm decision making (Chin et al., 2013; Skitka & Tetlock, 1993; Tetlock, 2000; Weiner, Osborne, & Rudolph, 2011). More simply, conservative CEOs may see little value in political transparency unless it directly supports efficiency or protects the firm from reputational harm. This perspective leads to a lower likelihood of voluntary CPT, particularly if doing so could increase scrutiny or expose the firm to criticism.

These contrasting ideological commitments shape how CEOs interpret the need for disclosure. Conservatives tend to believe that their actions are appropriate and therefore see little need to draw attention by disclosing information, whereas liberals view corporate political spending as potentially problematic and favor transparency to ensure accountability.

We apply these ideological differences to the CPA domain and contend that liberal CEOs are more receptive to the normative demand for firms to disclose their political positions, as well as the growing societal concern over covert political influence (Lund & Strine, Jr., 2022; Lyon et al., 2018). In this area, transparency is a gesture of corporate accountability that liberal CEOs are more ideologically inclined to support, while more conservative CEOs are likely to oppose this kind of openness because they see corporate political activity as a strategic tool that should be used out of the public eye, at least to the degree legally permitted. Specifically, transparency creates accountability by enabling three forms of external monitoring: media scrutiny that can expose problematic activities (Lyon et al., 2018), stakeholder oversight that can challenge misaligned expenditures (Bebchuk & Jackson, 2010), and public information that regulators and voters can use to evaluate corporate political influence (Lund & Strine, Jr., 2022). Liberal CEOs view these monitoring mechanisms as legitimate checks on corporate power, while conservative CEOs see them as more of an interference with managerial discretion (Friedman, 2007; Tetlock, 2000). Furthermore, research has found that liberals have a stronger preference for transparency, but conservatives tend to be more opposed to it, especially when it creates reputational uncertainty (Piotrowski & Van Ryzin, 2007).

Importantly, this ideological disposition toward transparency operates independently of the content being disclosed. Liberal CEOs do not pursue transparency because their firms engage in less political activity overall or in more stakeholder-friendly political activities that they are confident about revealing. Rather, they view transparency as intrinsically valuable for ensuring accountability of corporate political influence, regardless of what specific activities are being disclosed. This distinguishes transparency as a value-driven governance choice from a strategic calculation about whether disclosure content will yield reputational benefits. Even when political activities might invite criticism, liberal CEOs’ ideological commitment to accountability mechanisms makes them more willing to subject those activities to external scrutiny. Thus, we expect that liberal CEOs will demonstrate a greater proclivity for political transparency compared to their conservative counterparts, not because disclosure is inherently beneficial, but because liberal CEOs are more likely to believe that transparency aligns with stakeholder norms and reinforces their ideological beliefs, even when it entails reputational risk. In contrast, conservative CEOs may view CPT as exposing the firm to unnecessary reputational risk and thus prefer opacity as a form of control and insulation.

Hypothesis 1: Firms led by liberal CEOs will exhibit higher levels of political transparency than firms led by conservative CEOs.

While we expect CEO liberalism to increase political transparency, the managerial discretion perspective suggests that this effect materializes only when the CEO retains sufficient latitude of action (Crossland & Hambrick, 2007; Hambrick, 2007; Hambrick & Finkelstein, 1987). We therefore examine three boundary conditions—firm-specific political uncertainty, industry transparency norms, and industry concentration—that shape the contextual conditions under which CEO ideology can influence transparency decisions.

Firm-Level Political Uncertainty

Firm-level political uncertainty refers to the unpredictability of political and regulatory shifts as they specifically impact the firm (Hassan, Hollander, Van Lent, & Tahoun, 2019). Such uncertainty heightens the risk of policy reversal, expropriation, or sudden compliance costs, thereby eroding the expected returns from political investments (Delios & Henisz, 2003; Henisz & Zelner, 2005). When political uncertainty is high, firms are more inclined to increase their behind-the-scenes political activity as a protective measure (Hadani, Bonardi, & Dahan, 2017). However, this very context makes them less willing to disclose those activities because the stakes and unpredictability are so high.

At the same time, under high political uncertainty at the firm level, the risks associated with political transparency increase. Disclosing CPA may reveal vulnerabilities that expose the firm to backlash from newly empowered political coalitions or signal dependence on political outcomes. This occurs because the disclosures might provide competitors with insight into the firm’s operations, strategic objectives, and lobbying investments. In addition, transparency may signal misalignment with whichever policy coalition ultimately prevails, creating the risk of reputational blowback or regulatory retaliation if the political winds shift (Bonardi, Hillman, & Keim, 2005; Dorobantu, Kaul, & Zelner, 2017). Indeed, scholars posit that in volatile environments, firms are tasked with strategically balancing the benefits and risks of transparency (Lawrence & Suddaby, 2006). Upper echelons theory likewise predicts that strong situational threats constrain the expression of managerial values, because survival concerns may override value expression (Crossland & Hambrick, 2011; Hambrick & Finkelstein, 1987). As such, even ideologically motivated CEOs must account for the possibility that transparency may be misinterpreted or weaponized by political actors when political uncertainty is high (Dorobantu et al., 2017).

In this sense, political uncertainty introduces both competitive and interpretive risk, raising the cost of expressing ideological preferences through CPT (Edelman & Suchman, 1997; Lawrence & Suddaby, 2006). Under such conditions, even ideologically liberal CEOs are likely more cautious about pursuing openness. High political uncertainty creates situational pressures that force CEOs to prioritize risk-minimizing strategies, dampening the distinctive imprint that a CEO’s liberal values would otherwise leave on disclosure practices (Hambrick, 2007; Hambrick & Finkelstein, 1987).

For conservative CEOs, transparency is already viewed as unnecessary external scrutiny (Friedman, 2007; Tetlock, 2000), and political uncertainty reinforces that perspective rather than altering this stance. When uncertainty is low, conservative CEOs might marginally increase disclosure to meet stakeholder expectations or regulatory pressure. As uncertainty rises, their baseline preference for opacity aligns perfectly with strategic caution. Thus, while high political uncertainty suppresses liberal CEOs’ transparency tendencies, it simply maintains conservative CEOs at their already low disclosure baseline.

Hypothesis 2: Firm-level political uncertainty will weaken the positive relationship between CEO liberalism and corporate political transparency.

Normative Political Transparency

Industry-level CPT norms may set the outer limits of managerial discretion, conditioning the extent to which CEO ideology can shape CPT. Such norms are shaped by peer behavior, stakeholder pressure, and broader institutional forces, and thus we expect them to influence firm CPT decisions (DiMaggio & Powell, 1983; Kennedy & Fiss, 2009; Marquis & Tilcsik, 2013). As political transparency becomes institutionalized in an industry, CEOs’ strategic discretion over disclosure diminishes because firms must meet rising transparency expectations to maintain legitimacy (DiMaggio & Powell, 1983). Thus, political transparency becomes less of a value-based choice and more of a legitimacy-seeking response to external pressures and reputational risk. Strong industry transparency norms (i.e., where most peer firms engage in high levels of transparency) constrain CEO discretion, whereas weak norms in more opaque industries allow greater latitude for a value-driven CEO to make a difference.

Indeed, as industry norms solidify, voluntary political transparency decisions converge across firms as legitimacy benchmarks define acceptable behavior (Deephouse, 1999; Zuckerman, 1999). In effect, strong norms establish a disclosure “floor,” while practical costs and information overload create a de facto “ceiling,” further constraining variance (Oliver, 1991).

For liberal CEOs, this normative level of political transparency constrains the ability to express their ideological preference for transparency because institutional conformity pressures reduce the distinctiveness of additional transparency rather than simply limiting discretion. Conversely, in industries where political transparency is uncommon or weakly institutionalized, liberal CEOs have greater room to act on their values and implement transparency as an intentional, value-driven strategy. When industry norms are low, disclosure is more discretionary and thus more likely to serve as an ideology-driven act because contextual pressures are minimal (Gupta, Nadkarni, & Mariam, 2019). In such contexts, liberal CEOs have greater latitude to act on their values (Chin et al., 2013). Consequently, the effect of liberal ideology on CPT is more pronounced because disclosure is not normatively required and thus reflects an authentic expression of executive values.

For conservative CEOs, when industry transparency is low, they face minimal institutional pressure to disclose, and their ideological preference for opacity goes unchallenged. In this environment, they maintain low disclosure levels without consequence. However, when industry transparency norms become strong, conservative CEOs face legitimacy costs for remaining opaque that may override their ideological resistance to disclosure (DiMaggio & Powell, 1983). Thus, strong industry transparency norms compress ideological variance by simultaneously limiting liberal CEOs’ ability to differentiate through greater openness and raising conservative CEO’s minimum transparency threshold. A vivid illustration is the U.S. utilities sector, where most large firms have adopted strong voluntary political disclosure practices through industrywide transparency norms that emerged from peer pressure and stakeholder advocacy, according to the Zicklin Index. As a result, a liberal CEO has limited room for ideological distinctiveness beyond this industrywide benchmark, while conservative CEOs face elevated legitimacy costs for maintaining opacity below that benchmark. Thus, we hypothesize:

Hypothesis 3: Firm industry transparency norms will weaken the positive relationship between CEO liberalism and corporate political transparency.

Firm Industry Concentration

Industry concentration, which is the extent to which an industry is dominated by a few large firms versus being fragmented with multiple competitors (Hoberg & Phillips, 2016), shapes the competitive context within which CEOs make transparency decisions, creating structural constraints that influence managerial discretion (Hambrick & Finkelstein, 1987; Porter, 1980). This constraint operates through oligopolistic interdependence unique to concentrated markets. In such industries, dominant firms often maintain tacit coordination around political strategies to preserve collective influence while avoiding regulatory attention (Porter, 1980). Transparency by a single firm can disrupt this balance by potentially exposing industrywide political strategies, creating what amounts to a collective action problem (Olson, 1965): while transparency might benefit the industry if all firms adopted it simultaneously, the first mover faces potential retaliation through market mechanisms. For instance, disclosing political contributions might reveal to competitors and stakeholders the firm’s strategic intentions, creating competitive vulnerabilities in markets where dominant firms closely monitor each other’s strategic moves. Thus, even a liberal CEO who personally values transparency faces structural disincentives to break from the industry’s established opacity norms. Importantly, these constraints operate regardless of whether industry leaders themselves are transparent, as any deviation from coordinated behavior threatens tacit cooperation and exposes sensitive information.

This logic aligns with institutional theory, which suggests that in concentrated markets, leading firms create powerful normative pressures that shape acceptable strategic behavior (DiMaggio & Powell, 1983). Upper echelons theory further suggests that CEO effects are strongest when environmental constraints are minimal (Gupta et al., 2019; Hambrick & Finkelstein, 1987). In highly concentrated industries, strategic interdependence among dominant firms creates heightened visibility and mutual monitoring, effectively constraining CEO latitude to pursue ideologically driven strategies that deviate from industry norms. This constraint operates through both competitive and reputational channels. Competitively, transparency in concentrated markets risks revealing strategic information to a small number of powerful rivals.

Conservative CEOs in concentrated industries face similar structural pressures but for different reasons. Their baseline resistance to transparency means they prefer opacity even without concentration pressures. In concentrated markets, if a conservative CEO were to ignore industry norms by increasing transparency (perhaps due to external pressure), they would face the same competitive vulnerabilities as liberal CEOs and encounter resistance from peer firms that prefer the status quo. Therefore, concentration locks in the existing low-transparency equilibrium. In less concentrated markets, conservative CEOs still prefer opacity, but the competitive dynamics differ. With many players, no single firm’s disclosure significantly threatens industrywide political strategies. Moreover, if some competitors begin disclosing (perhaps led by liberal CEOs seeking differentiation), conservative CEOs may face stakeholder pressure to follow suit without the same level of coordination risk. Thus, fragmentation creates opportunities for gradual norm shifts that can elevate baseline disclosure levels even among ideologically resistant CEOs. Therefore, we hypothesize:

Hypothesis 4: Firm industry concentration will weaken the positive relationship between CEO liberalism and corporate political transparency.

Methods

Sample

Our sample consists of all publicly traded firms from 2012 to 2021, which are also included in the Zicklin Index of Corporate Political Disclosure and Accountability—an index measuring political transparency and accountability (https://www.politicalaccountability.net). The Zicklin Index was established in 2012 by the Center for Political Accountability—a nonpartisan, nonprofit advocacy group dedicated to “achieving corporate political disclosure and accountability” in partnership with the Zicklin Center for Business Ethics Research at the Wharton School of the University of Pennsylvania (Goh et al., 2020). The Index covers a sample of major U.S. public firms, with selection based on firm characteristics such as size and public visibility as determined by the Center for Political Accountability.

Consistent with prior research, information on CEO political ideology is collected from the Federal Election Commission database (Chin et al., 2013). We obtained data on firm-level political uncertainty using the validated text-based index developed by Hassan et al. (2019), which analyzes quarterly earnings conference call transcripts to capture firm-level political risk exposure. We use the Center for Responsive Politics for information on firm political activities (Abdurakhmonov, Ridge, & Hill, 2021; Ridge, Ingram, & Hill, 2017), and data on firm, CEO, and board characteristics obtained from Compustat, Execucomp, and BoardEx, respectively. We also obtained the board ideological diversity measure from the dataset developed by Mannor and Busenbark (2025).

We measure independent variables in time t and dependent variables in time t + 1. Our hand-collected dataset was able to identify 638 unique publicly traded firms from the Zicklin Index of Corporate Political Disclosure and Accountability. Accounting for missing data due to data availability limitations in Compustat, Execucomp, BoardEx, and firm-level risk measures, our final sample consists of 1,662 firm-year observations that span 341 firms. Finally, consistent with the disclosure requirements of the Journal of Management, we acknowledge that we employed ChatGPT 5.2 for editing the preceding sections and the discussion for clarity of writing.

Dependent variable

Our dependent variable of corporate political transparency (CPT) is measured using 16 metrics that assess “disclosure practices and spending and accountability policies for spending with corporate or treasury funds to influence elections” (Center for Political Accountability, 2021). Broadly, Zicklin uses 24 metrics to capture CPT and accountability that focus on three broad areas: disclosure, political spending decision making policies, and board oversight and accountability policies. Appendices A and B provide the specific indicators, descriptive statistics, and a link to details about the indicator scoring rubric.

To isolate a firm’s commitment to transparent disclosure and policy, we focus on the 16 indicators related to (1) the public disclosure of political expenditures (items 1-9) and (2) formal policy statements governing such activity (items 10-16). These items were summed to capture whether a firm reports its contributions to candidates, PACs, trade associations, 501(c)(4)s, and ballot initiatives; discloses decision making authority; maintains an archive of reports; and adopts formal policies defining permitted contributions, oversight processes, and alignment with corporate interests. Hence, we exclude oversight-specific items (indicators 17-24), which reflect implementation structures rather than disclosure or policy commitments. 1

Independent variables

To measure CEO liberalism, we collected data on the individual campaign contributions made by each CEO in the ten years leading up to their appointment as CEO. This approach is consistent with prior research on CEO political ideology (Chin & Semadeni, 2017; Chin et al., 2013; Gupta et al., 2018). As such, the CEO’s political ideology is defined by an average of four indicators related to the CEO’s campaign contributions. These indicators include: (1) the ratio of donations made to Democrats compared to donations made to recipients from both parties, 2 (2) the ratio of the dollar amount donated to Democrats compared to the total amount donated to both parties, (3) the ratio of the number of years the executive made donations to Democrats over a 10-year period compared to the total number of years donations were made to either party, and (4) the ratio of the number of distinct Democratic recipients to whom the executive made donations compared to the total number of distinct recipients from both parties. 3

We operationalize firm-level political uncertainty using the validated text-based index of political risk developed by Hassan et al. (2019). This measure captures the share of earnings call discussion devoted to government-related risks and uncertainties and thus reflects managers’ perceptions of political uncertainty specific to the firm (Gad, Nikolaev, Tahoun, & van Lent, 2024; Shi, Gao, & Aguilera, 2021). 4 While prior literature often distinguishes between uncertainty (macro-level unpredictability) and risk (firm-level exposure), our measure is designed to capture the firm-specific salience of political uncertainty as perceived by management. We therefore label it “firm political uncertainty” and interpret higher values as indicating greater firm-level exposure to unpredictable policy or regulatory shifts.

To capture industry CPT, for each firm-year, we calculated the average CPT score of all other firms operating in the same 4-digit SIC industry, which is the most granular and strategically relevant peer environment (Delmas & Toffel, 2008; Zuckerman, 1999). Specifically, we summed CPT scores across firms within each SIC-year group and subtracted the focal firm’s score from the total, dividing the remainder by the number of peer firms. In instances where a firm was the only member of its SIC-year group, we retained its own score to maintain sample continuity. 5

We measure industry concentration using the validated Herfindahl-Hirschman Index (Hoberg & Phillips, 2010, 2016) based on the Text-Based Network Industry Classifications (TNIC) from Hoberg and Phillips (hobergphillips.tuck.dartmouth.edu/tnic_competition.html). The TNIC approach provides a more precise measure of competitive industry structure by using product similarity derived from 10–K business-description text analysis, rather than relying on traditional SIC codes that may not accurately capture actual competitive relationships. The HHI is calculated as the sum of squared market shares within each TNIC industry, with higher values indicating greater industry concentration.

Control variables

We control for three categories of factors that the literature has identified as important determinants of political transparency: (1) institutional and governance factors, (2) resource-based factors, and (3) firm political activity characteristics. Prior research suggests that institutional pressures and governance structures shape CPT practices (Bebchuk & Jackson, 2010; DiMaggio & Powell, 1983; Lund & Strine, Jr., 2022). We control for board independence, measured as the share of independent directors to the total number of directors, because stronger board monitoring may increase transparency demands (Goh et al., 2020). We control for the number of directors because larger boards may have more diverse stakeholder perspectives that favor disclosure. We control for board ideological diversity (Mannor & Busenbark, 2025), which captures the heterogeneity of political orientations within the board of directors, as heterogeneous boards may influence transparency through governance mechanisms. We include industry regulation, using a dummy variable (regulation), coded “1” for firms in regulated industries and “0” otherwise, as firms in regulated industries face heightened institutional pressures for transparency (Coates IV, 2012; Werner, 2017). Finally, we control for dynamism of industry CPT, operationalized as the percentage of change in industry CPT relative to the prior year, to capture evolving institutional expectations.

The resource-based view of the firm suggests that CPT decisions depend on firm capacity and strategic resources (Barney, 1991). We control for firm size, operationalized as the logged value of total number of employees, because larger firms have greater capacity to develop transparency infrastructure. We control for firm slack, measured as selling, general, and administrative expenses divided by total sales revenue, capturing discretionary resources that can be allocated to transparency initiatives (Shi, Zhang, & Hoskisson, 2017). We control for firm accounting performance, operationalized as return on sales, and shareholder returns, measured as the annual stock price appreciation plus dividends, scaled by the beginning-of-year stock price, as better-performing firms may have more latitude to pursue transparency or face greater stakeholder scrutiny. We control for debt intensity, operationalized as the debt-to-equity ratio, because it signals the resources available to support firm operations (Gibbs, 1993). We control for capital intensity, measured as firm capital expenditures divided by firm total assets, and inventory intensity, operationalized as firm inventory value divided by total sales, to account for operational differences that may affect transparency capacity. We also control for CEO ownership, operationalized as the percentage of firm stock owned by the CEO, as CEO equity stakes may align transparency incentives with shareholder interests and affect resource allocation priorities (Carpenter, Geletkanycz, & Sanders, 2004). Finally, we control for firm vertical integration, which captures the degree to which a firm’s operations are integrated across the supply chain (Hoberg & Phillips, 2016), as more vertically integrated firms may have greater organizational complexity that affects both political strategy sophistication and transparency capacity.

Lastly, because political transparency may be influenced by the scale and nature of political engagement, we control for lobbying activity, measured as the logged value of total expenditures devoted to lobbying in a year (Ridge et al., 2017) and for firm political activity contributions (PAC), measured as the logged value of total expenditures for campaign contributions by a firm PAC, as firms more active in politics may face greater pressure to disclose. Additionally, to account for the political context in which firms are embedded, we control for the state partisan orientation of the firm’s headquarters, which shapes local political norms, media attention, and stakeholder expectations regarding corporate political engagement. Following prior work (Gupta & Wowak, 2017), we operationalized state political leaning using presidential election outcomes. Specifically, we identified the percentage of votes cast for the Democratic Party in the firm’s headquarters state in the most recent presidential election and coded the state as Democratic-leaning (1) if a majority of votes (≥50%) were cast for the Democratic candidate, and zero otherwise. This measure captures the dominant political environment surrounding the firm and allows us to account for geographic variation in political norms that may independently influence transparency decisions. Lastly, we also control for the CPA ideological orientation, PAC liberalism. Using firm-affiliated PAC contribution data obtained from the Center for Responsive Politics (www.opensecrets.org), we identified PAC contributions explicitly labeled as supporting the Democratic Party (“D”) or the Republican Party (“R”). We then constructed a continuous measure capturing the share of PAC spending directed toward Democratic committees, calculated as the total dollar amount contributed to Democratic Party committees divided by total PAC contributions made to both Democratic and Republican Party committees.

Analysis and Results

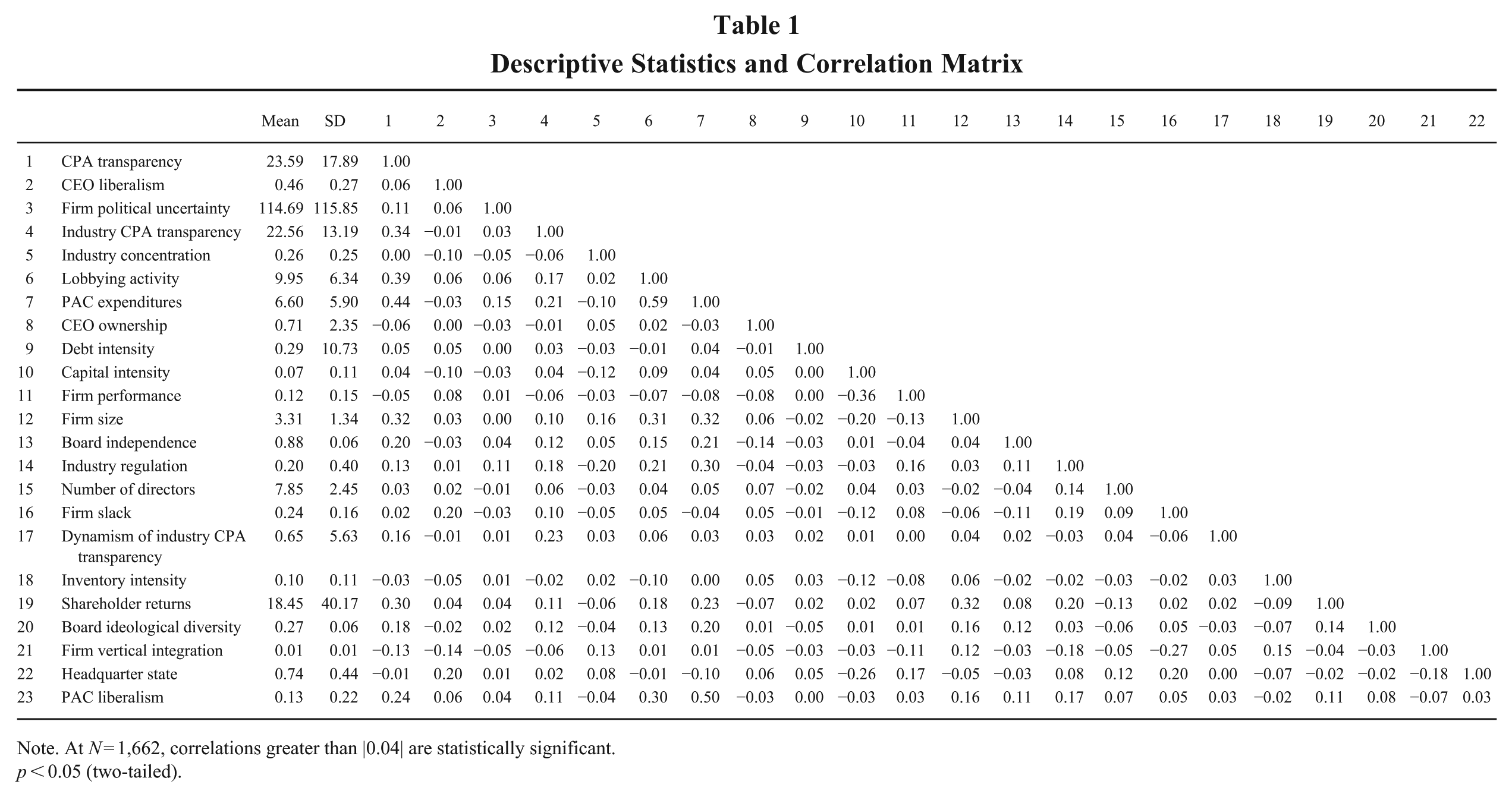

We present descriptive statistics and correlations in Table 1 and the results in Table 2. To examine whether multicollinearity poses a statistical concern, we computed variance inflation factor (VIF) values and found that the mean VIF values were 2.81, suggesting that multicollinearity was not a statistical concern (Allison, 1999).

Descriptive Statistics and Correlation Matrix

Note. At N = 1,662, correlations greater than |0.04| are statistically significant.

p < 0.05 (two-tailed).

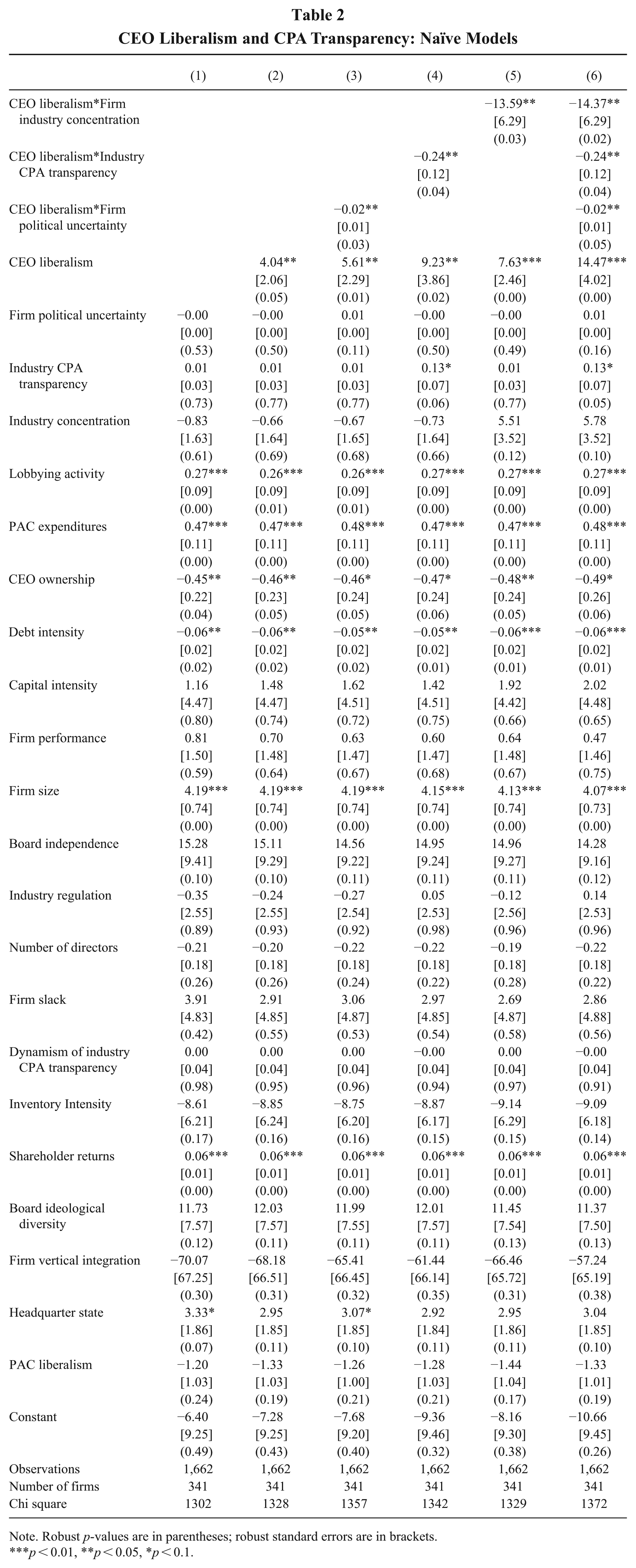

CEO Liberalism and CPA Transparency: Naïve Models

Note. Robust p-values are in parentheses; robust standard errors are in brackets.

p < 0.01, **p < 0.05, *p < 0.1.

We follow prior CEO political ideology research by employing generalized estimating equations (GEE) with robust standard errors (Chin & Semadeni, 2017; Chin et al., 2013) because of this model’s appropriateness when including time-invariant variables such as CEO liberalism (Chatterjee & Hambrick, 2007; Quigley & Hambrick, 2012). For all models, we specified an autoregressive (AR1) working correlation structure, with the firm set as the panel unit, since it allows for the possibility that unobserved factors influencing CPT may be correlated across adjacent years within the same firm (Wowak, Mannor, Arrfelt, & McNamara, 2016). To account for temporal and industry-specific effects, we included year and industry fixed effects in all analyses.

Model 1 includes only the control variables and establishes the baseline relationships. Several predictors are significantly associated with CPT. Specifically, PAC expenditures (β = 0.47, p < 0.01) and lobbying activity (β = 0.27, p < 0.01) are positively related to CPT, suggesting that firms more engaged in political spending are also more likely to disclose such activities. Additionally, firm size (β = 4.19, p < 0.01) and shareholder returns (β = 0.06, p < 0.01) are positively associated with CPT, indicating that larger and more resource-rich firms may be more capable of sustaining transparent political strategies.

Model 2 introduces the main independent variable, CEO liberalism, and provides support for Hypothesis 1. The coefficient is positive and statistically significant (β = 4.04, p < 0.05), indicating that firms led by more liberal CEOs exhibit higher levels of CPT. This finding suggests that CEO political ideology meaningfully shapes corporate approaches to disclosure in the political domain. In practical terms, moving a publicly traded company from a fully conservative CEO to a fully liberal CEO is associated with an 11% increase in firm CPT.

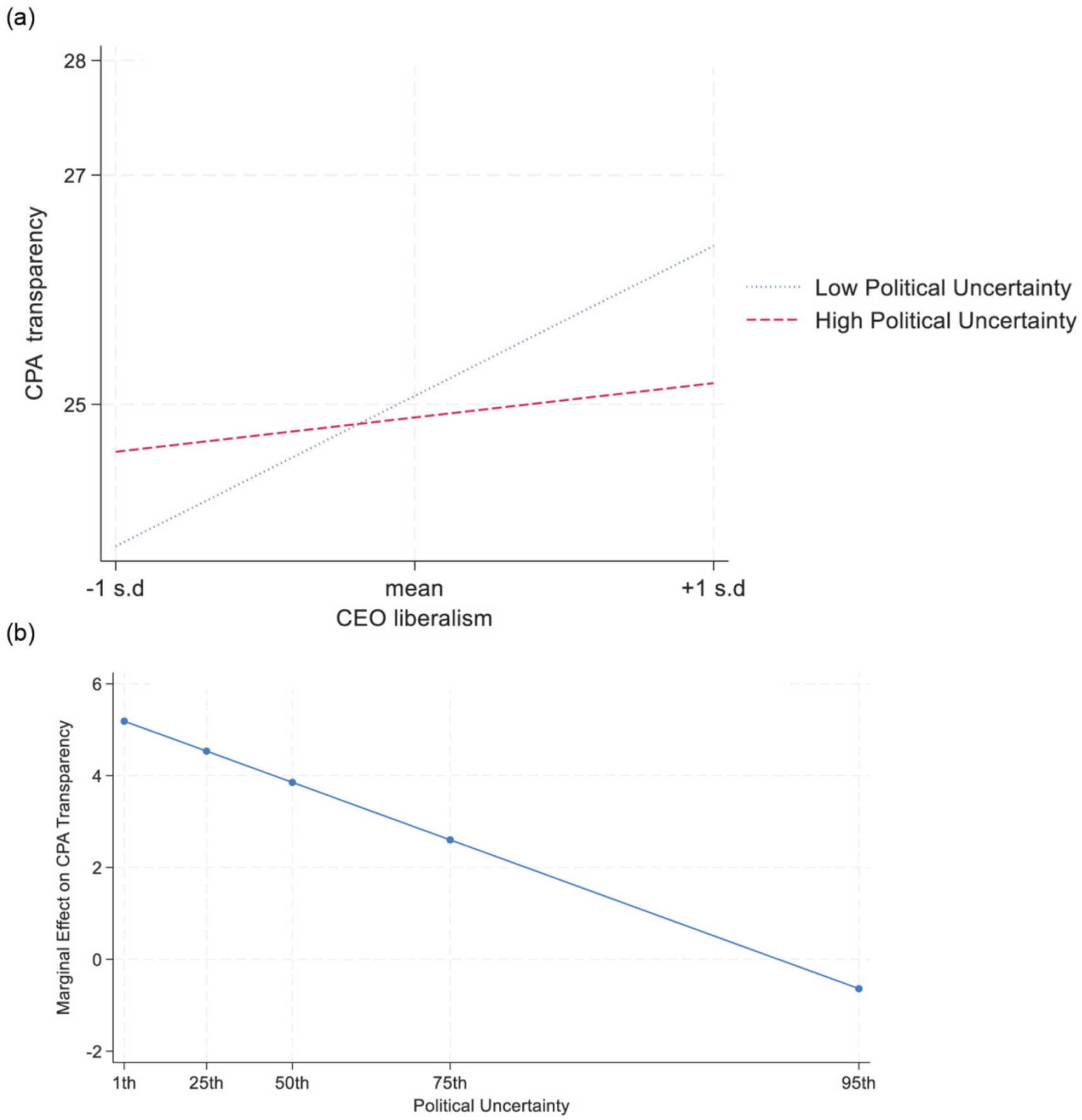

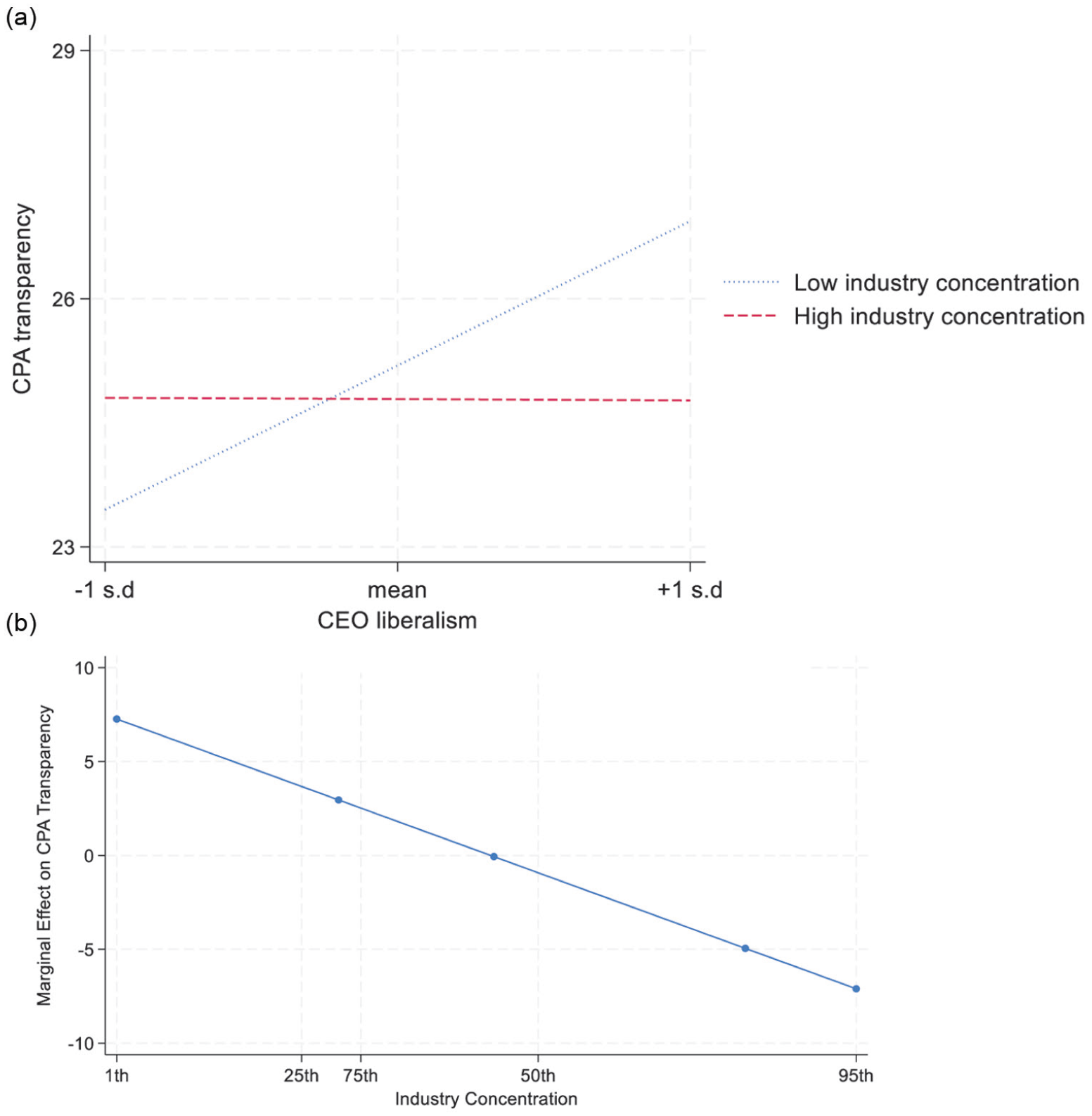

We introduce interaction terms in Models 3 through 5 as partial models, while Model 6 incorporates all three interaction terms to test our Hypotheses 2 through 4. Hypothesis 2 posits that firm political uncertainty weakens the effect of CEO liberalism on CPT. The interaction term is negative and significant in Model 3 (β = –0.02, p < 0.05), indicating that when firms face higher levels of political uncertainty, the positive relationship between CEO liberalism and CPT diminishes. In practical terms, as displayed in Figure 1a, when political uncertainty is low, increasing CEO liberalism from one standard deviation below to above the mean leads to a 10.7% increase in CPT, but when political uncertainty is high, the same increase in liberalism yields only a 1.1% increase. Figure 1b further visualizes this moderation by showing that the marginal effect of CEO liberalism decreases steadily across percentiles of political uncertainty, falling from strongly positive at the 1st percentile to near zero or slightly negative at the 95th percentile.

(a) Political Uncertainty and CEO Liberalism in CPA Disclosure and (b) CEO Liberalism Across Percentiles of Political Uncertainty

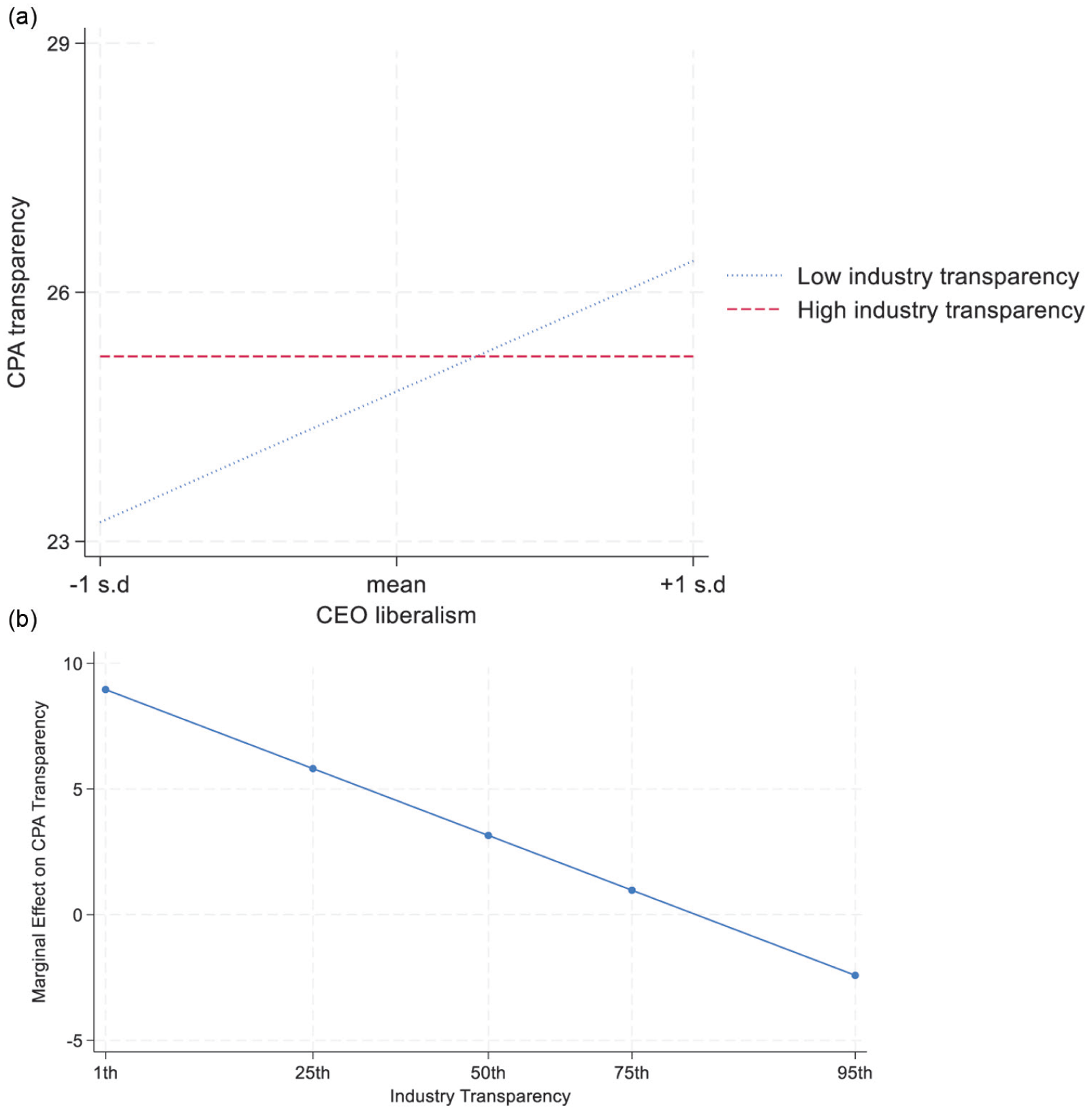

Hypothesis 3 argues that the effect of CEO liberalism on CPT is weakened by industry CPT. The interaction term is negative and statistically significant in Model 4 (β = −0.24, p < 0.05), suggesting that the ideological influence of liberal CEOs weakens in industries where CPT is already widespread. In practical terms, as shown in Figure 2, increasing CEO liberalism from one standard deviation below to one above the mean leads to a 12.6% increase in CPT when industry transparency is low, but has virtually no effect when industry transparency is high. Figure 2 further illustrates this pattern by plotting the marginal effect of CEO liberalism across percentiles of industry transparency. The relationship is strongly negative and linear, and thus, liberal CEOs have the strongest positive impact on CPT in low-transparency industries, but their influence diminishes steadily and turns slightly negative as industry transparency approaches the 95th percentile.

(a) Industry Transparency and CEO Liberalism in CPA Disclosure and (b) CEO Liberalism Across Percentiles of Industry Transparency

Hypothesis 4 posits that industry concentration weakens the effect of CEO liberalism on CPT. The interaction term is negative and statistically significant (β = −13.59, p < 0.05) in Model 5, indicating that when firms operate in more concentrated industries, the positive relationship between CEO liberalism and CPT diminishes. In practical terms, as displayed in Figure 3, when industry concentration is low, increasing CEO liberalism from one standard deviation below to one above the mean leads to a 12.4% increase in CPT. However, when industry concentration is high, the increase is only 0.7%. Figure 3 further illustrates this pattern by plotting the marginal effect of CEO liberalism across percentiles of industry concentration. The relationship is strongly negative and linear, and thus, liberal CEOs have the strongest positive impact on CPT in low-concentration industries, but their influence diminishes steadily and turns slightly negative as industry concentration approaches the 95th percentile.

(a) Industry Concentration and CEO Liberalism in CPA disclosure and (b) CEO Liberalism Across Percentiles of Industry Concentration

Taken together, the results from both the partial and full models provide consistent support for our hypotheses, demonstrating that CEO liberalism’s effect on transparency is contingent on political uncertainty, industry CPT norms, and competitive structure.

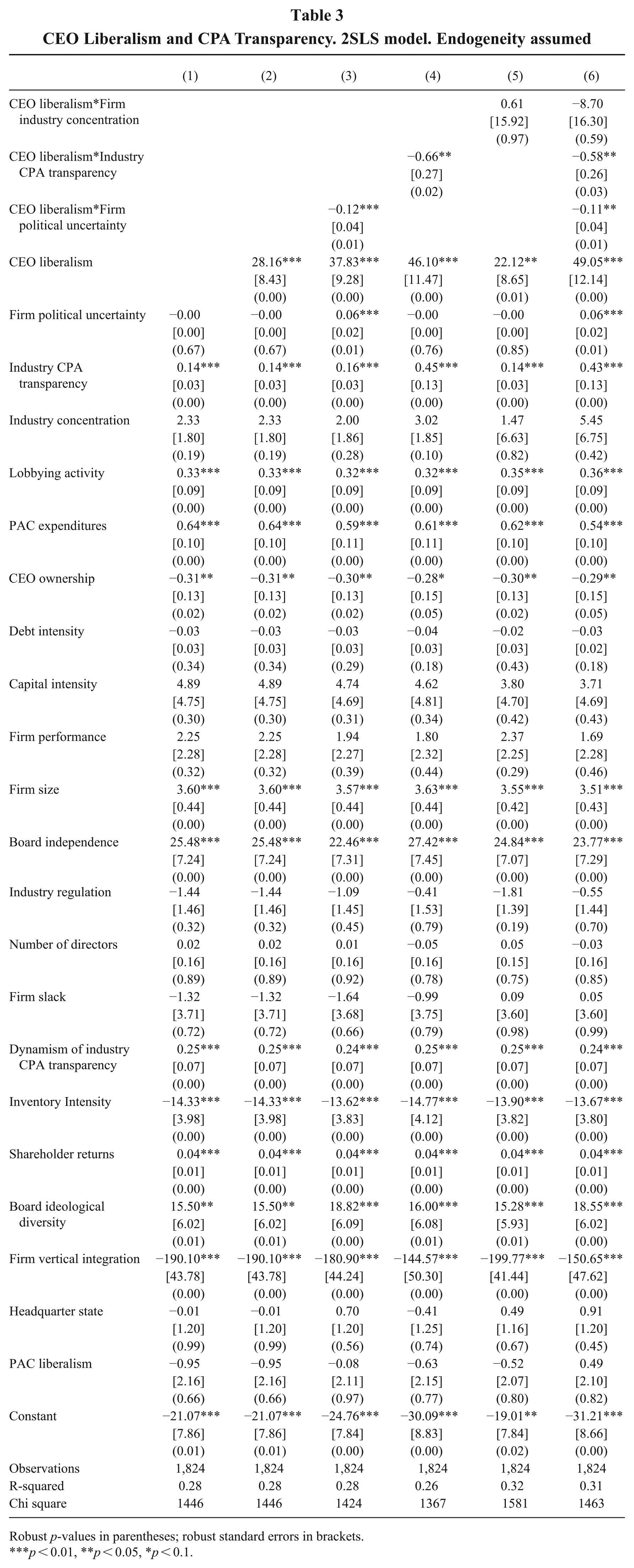

Addressing Potential Endogeneity

Prior research has considered CEO political ideology as a stable, dispositional attribute that precedes and shapes firm strategic choices (Chin & Semadeni, 2017; Chin et al., 2013; Gupta et al., 2017, 2018). To mitigate concerns about reverse causality or simultaneity, we lagged the dependent variable (CPT) by one year (t + 1). Furthermore, given its dispositional nature, political ideology is unlikely to be influenced by short-term firm-level dynamics such as annual shifts in transparency or regulatory activity (Chin et al., 2013; Tetlock, 2000).

Nevertheless, we next assessed the robustness of our inference to potential bias using two diagnostics: the threshold for percent bias required to invalidate our estimates and the impact threshold for a confounding variable ITCV (Busenbark, Yoon, Gamache, & Withers, 2022). Results indicate that 38.70% of the sample would need to be replaced with observations for which the effect of CEO liberalism is null to reduce the estimate to statistical insignificance, suggesting a high degree of robustness to sampling variability. We also compute the ITCV equals 0.0002, implying that an omitted confounder would need to exhibit partial correlations of at least 0.174 with both CEO liberalism and CPT to eliminate the observed effect. In our models, none of the included covariates meet this threshold on both dimensions. Assuming our model captures the key theoretical drivers of both CEO ideology and political transparency, omitted variable bias is unlikely to account for the observed relationship (Hamilton & Nickerson, 2003; Semadeni, Withers, & Trevis Certo, 2014).

We recognize the possibility that our results may be driven by unobserved factors influencing both the hiring of liberal CEOs and the firm’s CPT, and we conducted three additional tests aimed at mitigating potential omitted variable bias 6 (Busenbark et al., 2022; Certo, Busenbark, Woo, & Semadeni, 2016; Semadeni et al., 2014).

First, we focused on CEO succession events to isolate within-firm changes in political ideology. By examining CEO succession events, we leverage within-firm changes in political ideology to better isolate its effect on CPT. This approach reduces the risk that unobserved, time-invariant firm characteristics are confounding the observed relationship. If CPT increases following the appointment of a more liberal CEO within the same firm, this pattern is less likely to reflect selection effects or stable firm attributes and more likely to reflect the influence of the CEO’s personal ideology.

We identified 132 CEO transitions during our sample data period in which the incoming CEO had a different CEO liberalism index than the predecessor. We then re-estimated the impact of this change in political ideology on firm CPT while controlling for the prior CEO’s political ideology using cross-sectional regression. As reported in Appendix D, we find that changes in CEO political ideology at succession (e.g., CEO becoming more liberal compared to the predecessor) are significantly associated with changes in CPT, even after accounting for the political orientation of the outgoing CEO (β = 11.00, p < 0.05). We also reran the models for CPT change two and three years following CEO succession, and the results remained identical. 7 These findings, which incorporate changes in a firm’s CPT across multiple years following CEO succession provide strong evidence that the observed effect is attributable to CEO ideology itself rather than to time-invariant firm characteristics or selection processes.

Second, we also employed 2SLS models under the assumption that our measure of CEO liberalism is potentially endogenous (Semadeni et al., 2014). For instruments, we used (1) CEO early-life political exposure and (2) organizational ideology. The political environment during a CEO’s adolescence is likely to shape their long-term ideological orientation but is less likely to directly influence the firm’s CPT (Jennings & Niemi, 2014; Malmendier & Nagel, 2011). To capture this exogenous variation in formative political exposure, we construct an adolescence ideology index based on the political environment experienced during a CEO’s developmental years, drawing on political socialization theory (Jennings & Niemi, 2014; Malmendier & Nagel, 2011).

Specifically, for each CEO, we calculated the average Democratic political exposure between the ages of 15 and 25—a period widely recognized as critical for the formation of durable political beliefs. We computed the index as the mean of two components: the proportion of Democratic seats in the U.S. House of Representatives and the proportion of years under a Democratic president during this window. This yields a continuous measure of early-life exposure to liberal political conditions, with higher values indicating greater Democratic influence during a CEO’s formative years. Organizational political ideology is also likely to influence the appointment of CEOs whose ideological preferences align with the organization’s existing political orientation. Moreover, prior work has shown that firms often seek ideological alignment between executives and organizational values to maintain stakeholder trust and internal legitimacy (Gupta et al., 2017). Furthermore, organizational ideology is unlikely to directly influence CPT once CEO ideology is accounted for, because firm-level ideology reflects historical political behavior, whereas the decision to disclose political activity is typically situated at the executive level and shaped by the CEO’s preferences, risk tolerance, and personal values 8 (Chin et al., 2013; Christensen et al., 2015).

F-tests based on an ordinary least squares (OLS) regression are well above the threshold suggested by Stock and Yogo (2001), providing evidence of validity. The Sargan test statistic following the second-stage regression also suggests that our variable selection strategy was sound (Semadeni et al., 2014). 9 We present results for 2SLS models, which are qualitatively identical to our main models in Table 3, apart from the interaction term with firm industry concentration. 10

CEO Liberalism and CPA Transparency. 2SLS model. Endogeneity assumed

Robust p-values in parentheses; robust standard errors in brackets.

p < 0.01, **p < 0.05, *p < 0.1.

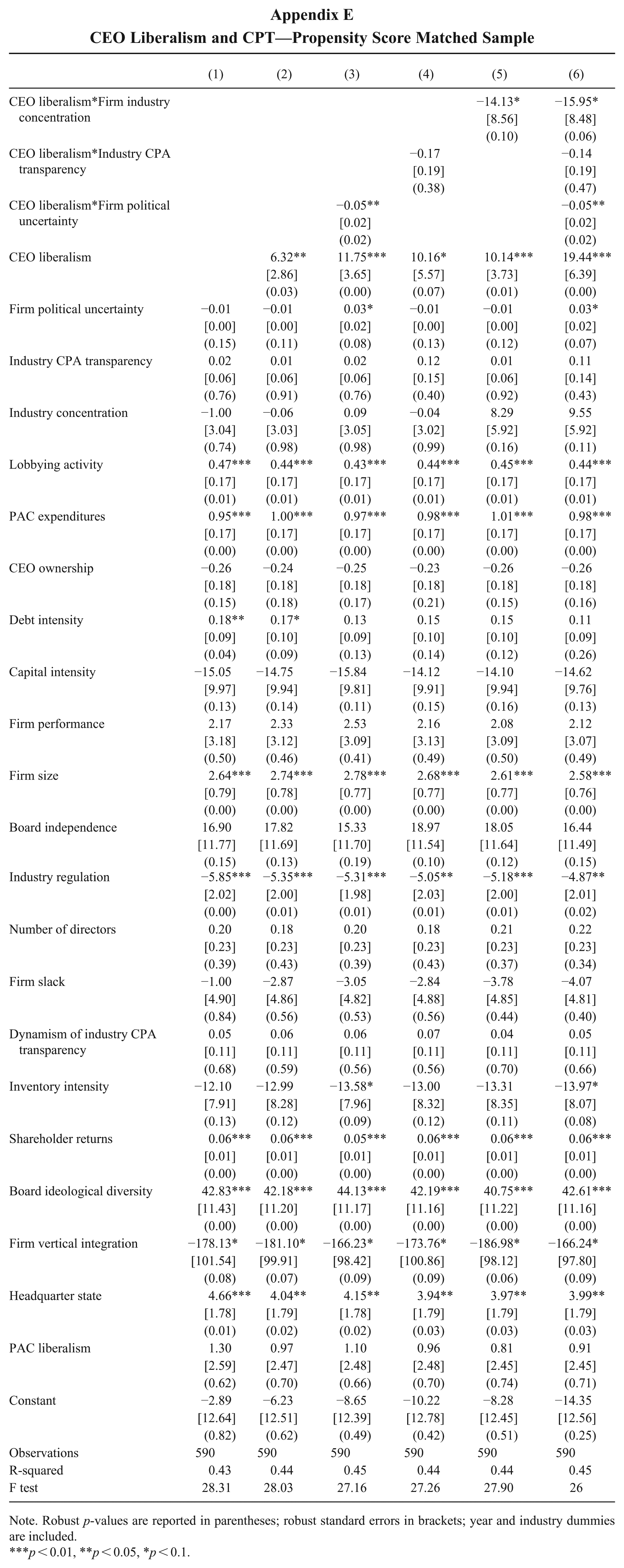

While the use of relevant and exogenous instruments helps address endogeneity concerns in our 2SLS models, we also implement a propensity score matching (PSM) approach as a supplemental robustness test (Chang, Chung, & Moon, 2013; Chang & Shim, 2015; Qian, Lu, & Yu, 2019). Specifically, we construct a binary treatment indicator equal to one if the CEO liberalism score exceeds 0.5, and zero otherwise, thereby distinguishing firms led by liberal versus conservative CEOs. We then match treated firms (CEO liberalism >0.5) to control firms (CEO liberalism <0.5) using nearest-neighbor matching with three neighbors via the psmatch2 command in Stata 17, based on key observable firm characteristics such as firm size, sales, profitability, leverage, and capital intensity. This method resulted in 590 matched observations, reducing the overall sample size (treatment and control groups). We then estimate treatment effects using weighted cross-sectional regressions on the matched sample, including interaction terms between CEO ideology and our moderators, with results reported in Appendix E. In the matched sample analysis reported in Appendix E, the results continue to support Hypotheses 1, 2, and 4; however, Hypothesis 3 is not supported. Overall, the direction and magnitude of the remaining effects are comparable to those observed in the full sample, which increases our confidence in the robustness of the main results.

Discussion

Our study makes two contributions to understanding CPT and the boundary conditions of CEO ideology. First, we advance the CPT literature by explaining within industry variation that external pressure theories cannot address. While prior research emphasizes stakeholder activism, regulations, and investor demand impact transparency (Lyon et al., 2018; Walker, 2023), we show that transparency decisions reflect executives’ normative, ideological beliefs about corporate political influence. Liberal CEOs view transparency as accountability that legitimizes engagement. In contrast, conservative CEOs view it as a vulnerability that invites scrutiny. This suggests that disclosure embodies fundamental tensions around corporate power and democratic accountability, advancing understanding beyond purely instrumental stakeholder management. Second, we extend the upper echelons theory by identifying when CEO ideology shapes nonmarket strategy. Political uncertainty suppresses liberal CEOs’ transparency, specifically through asymmetric constraints. Indeed, strong industry transparency norms constrain ideological variance, by limiting how much more transparent liberal CEOs can be while simultaneously raising the minimum level of disclosure conservative CEOs must adopt. Industry concentration limits liberals through collective action problems. These patterns show that ideology’s influence depends on alignment between preferences and contextual demands, not merely the presence of discretion. Different factors asymmetrically moderate liberal versus conservative CEOs’ behavior, revealing complex disposition-context interactions (Hambrick, 2007; Hambrick & Mason, 1984).

Theoretical Implications

First, our findings recast CPT not merely as a reflection of firm-level resources or institutional pressures (Hillman, Keim, & Schuler, 2004; Hillman, Withers, & Collins, 2009) but as a value-contingent, context-sensitive outcome shaped by the ideological dispositions of the CEO (Chin et al., 2013). In doing so, we extend upper echelons theory into the political arena, highlighting how individual-level belief systems interact with environmental conditions to shape transparency. Rather than predicting a direct association in which greater liberalism uniformly predicts greater disclosure, our results uncover a nuanced risk–reward calculus: liberal CEOs are more likely to champion disclosure when discretion is available and reputational alignment is favorable, yet they retreat when political or normative threats elevate the potential downside of transparency. This contingency perspective responds to and advances recent calls to more precisely specify the boundary conditions under which executive characteristics shape organizational outcomes (Crossland & Hambrick, 2011; Gupta et al., 2019; Hambrick, 2007), offering a more dynamic understanding of how values-based discretion operates within politically sensitive domains. Our findings also clarify that CPT represents both a strategic decision and a value-driven choice, demonstrating that executives’ personal values can shape strategic decisions in domains with reputational ambiguity.

Second, we contribute to the nonmarket strategy literature by bridging micro-level leader ideology with macro-level political risk to explain variation in CPT (Hassan et al., 2019). Whereas prior political activity research has largely conceptualized political uncertainty as an external, structural driver influencing the volume or timing of lobbying and PAC contributions (Hadani et al., 2017; Hillman et al., 2004), our findings reveal that political uncertainty also shapes the visibility of such engagement by moderating ideologically driven disclosure behavior. Specifically, we show that under heightened political uncertainty, even liberal CEOs, who are typically predisposed toward transparency, may withhold disclosure to manage interpretive and reputational risk. This interaction underscores the behavioral consequences of institutional volatility and reveals how risk perceptions filter ideological expression in the political arena. In doing so, we illustrate how individual cognition and preferences interact with political institutions to shape strategic outcomes. By integrating upper echelons theory with macro-political contingencies, our work offers a more nuanced account of how firms navigate ambiguous and politicized environments.

Third, we reframe CPT not as a normative good or compliance obligation, but as a strategic choice embedded in the broader repertoire of CPA. Prior research has often treated transparency as an unproblematic virtue (Lyon et al., 2018) or as an exogenous institutional expectation (DiMaggio & Powell, 1983; Marquis & Qian, 2014), yet our findings underscore that disclosure is both selective and strategically contingent. We show that CEOs do not passively conform to transparency demands. Instead, they weigh the reputational risks, political context, and peer norms to determine whether openness serves or undermines firm objectives. This perspective pushes the nonmarket strategy literature beyond a focus on what firms do in politics (e.g., lobby, donate to political campaigns) to also consider how they reveal or conceal such activities (Jia et al., 2023; Minefee et al., 2021; Werner, 2017). In doing so, our work highlights CPT as a dynamic signaling choice rather than a fixed institutional constraint. Importantly, framing CPT as a strategic decision does not imply the absence of pressure. Rather, industry norms and structural conditions can constrain managerial discretion without converting transparency into a formal compliance obligation.

Implications for Practice

Our findings also carry important implications for boards, investors, and policymakers seeking to navigate and shape firms’ political disclosure practices. Whereas the theoretical implications of our study highlight the conditional nature of values-based discretion, the practical lesson is that such discretion is not equally available across contexts, and therefore, cannot be uniformly expected or incentivized. As such, corporate boards may need to weigh ideological fit against context. That is, appointing a liberal CEO can enhance CPT only when organizational latitude and industry norms provide space for ideological imprinting. In highly institutionalized or politically volatile environments, even value-aligned CEOs may find their discretion constrained by informal normative and competitive pressures, rather than formal disclosure mandates. Thus, boards should not assume that appointing ideologically liberal executives will automatically translate into heightened transparency. Rather, alignment between the CEO’s political ideology and contextual conditions is key. Specifically, proxy advisory firms, which increasingly evaluate nonmarket risks as part of their governance assessments, could incorporate CEO political ideology metrics into their risk models. By doing so, they would provide boards and institutional investors with a tangible tool to assess potential misalignment between executive values and CPA. ESG rating agencies could similarly integrate ideological alignment assessments into their governance scores, creating market incentives for consistency between leadership values and political transparency practices.

Investors and watchdog groups, in turn, should temper expectations for disclosure in high-uncertainty arenas and instead target firms where ideological discretion more strongly shapes by disclosure decisions. Beyond viewing CPT as merely a signal of CEO values, sophisticated investors may attend to ideology–transparency misalignment as an informational cue when assessing governance quality and leadership fit. For instance, an activist shareholder observing that a conservative CEO helms a firm with unusually high political transparency—or, conversely, a liberal CEO leading a politically opaque firm—may interpret this inconsistency as indicative of governance tension, constrained discretion, or misalignment between executive values and organizational practices. Such misalignment could signal either forced compliance that masks underlying resistance or a breakdown in governance that allows CEOs to act contrary to stakeholder expectations. This insight can inform stakeholder engagement strategies as well. For example, activist investors and shareholder advocates might prioritize transparency campaigns in industries where norms are still emergent and CEO discretion is high. They could also use CEO succession events as windows of opportunity, pressing for transparency commitments when incoming CEOs’ ideologies suggest greater openness to disclosure. Our CEO succession analysis provides compelling evidence that within-firm changes in political ideology lead to corresponding changes in transparency, strengthening causal inference.

For policymakers, understanding that disclosure lapses may reflect ideological calculus rather than pure opportunism suggests that stronger baseline mandates—not simply “naming and shaming”—may be required to close transparency gaps. When political uncertainty or reputational threat suppresses even well-intentioned transparency, relying solely on voluntary disclosure is unlikely to ensure accountability. Instead, clearer disclosure rules and consistent enforcement may help level the playing field and reduce the influence of ideological or strategic opacity.

Limitations and Future Research

Like any study, ours has limitations that may motivate future research. First, although our use of the Zicklin Index provides a rare longitudinal window into firm-level political transparency practices, the dataset is limited to publicly traded U.S. firms and excludes privately held and foreign firms. This restriction raises concerns about generalizability. Cross-national extensions—particularly in settings where political disclosure is not voluntary but mandated (e.g., the EU)—would help assess whether ideological effects persist or attenuate under different regulatory regimes. For instance, the United States has a unique regulatory framework for political disclosure. Investigating whether these ideological effects translate to countries with stronger legal disclosure mandates or different political cultures would enhance the generalizability of our findings. Such work could also help disentangle ideology from institutional constraint. For example, in countries with mandatory disclosure laws, does CEO ideology shape the tone, timing, or framing of disclosure, even when content is mandated?

Second, our CEO-centric lens invites further investigation into the ideological composition and dynamics of the broader strategic leadership team. Boards and top management teams (TMTs) may constrain, amplify, or reinterpret the CEO’s ideological imprint depending on their own beliefs and the level of internal alignment. Our theory assumes liberal CEOs engage in political activities that align with their stated values, making transparency beneficial or neutral. However, cases where liberal CEOs’ political actions diverge from their espoused values represent an important boundary condition we could not systematically examine. Does ideological diversity foster strategic balance, or does it generate value conflict in politically sensitive decisions like transparency? Research at the group level could integrate upper echelons with team cognition literature to unpack these dynamics.

Lastly, there are additional avenues of inquiry that are important for understanding the complex relationship between firms and political transparency. Future research should examine whether CPT disclosures accurately reflect firms’ actual political behavior or serve as impression management. Additionally, investigating how the ideological nature of specific political activities (e.g., lobbying for environmental regulations versus tax reductions) interacts with CEO ideology could reveal nuanced patterns in transparency decisions. Moreover, future research could explore whether political transparency is interpreted as instrumental or symbolic when disclosure coincides with public controversy (McDonnell & Werner, 2016). Examining these symbolic versus instrumental interpretations may reveal nuanced implications for firms’ political legitimacy and reputation management strategies. Another important avenue is to assess how symbolic versus instrumental interpretations of CPT interact with other dimensions of nonmarket strategy, such as CSR, lobbying, and campaign contributions—to shape stakeholders’ perceptions and responses. While our theory suggests liberal CEOs would generally avoid or minimize political activities that contradict stakeholder values, exceptional circumstances, such as legally mandated disclosures, preemptive disclosure strategies, or political issues with mixed ideological implications, might create scenarios where transparency persists despite value misalignment.

Conclusion

In an era where firms face mounting scrutiny for their political engagement, understanding the drivers of CPT is important. By demonstrating that CEO political ideology shapes CPT, we offer an ideology-infused perspective on transparency in corporate political behavior. Our boundary-condition findings remind scholars that values matter most where discretion and contextual constraints intersect, an insight that may extend to other opaque strategic arenas. In doing so, we extend the emerging research on CPT while building on the established work in political activity and upper echelons traditions.

Footnotes

Appendix

CEO Liberalism and CPT—Propensity Score Matched Sample

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| CEO liberalism*Firm industry concentration | −14.13* | −15.95* | ||||

| [8.56] | [8.48] | |||||

| (0.10) | (0.06) | |||||

| CEO liberalism*Industry CPA transparency | −0.17 | −0.14 | ||||

| [0.19] | [0.19] | |||||

| (0.38) | (0.47) | |||||

| CEO liberalism*Firm political uncertainty | −0.05** | −0.05** | ||||

| [0.02] | [0.02] | |||||

| (0.02) | (0.02) | |||||

| CEO liberalism | 6.32** | 11.75*** | 10.16* | 10.14*** | 19.44*** | |

| [2.86] | [3.65] | [5.57] | [3.73] | [6.39] | ||

| (0.03) | (0.00) | (0.07) | (0.01) | (0.00) | ||

| Firm political uncertainty | −0.01 | −0.01 | 0.03* | −0.01 | −0.01 | 0.03* |

| [0.00] | [0.00] | [0.02] | [0.00] | [0.00] | [0.02] | |

| (0.15) | (0.11) | (0.08) | (0.13) | (0.12) | (0.07) | |

| Industry CPA transparency | 0.02 | 0.01 | 0.02 | 0.12 | 0.01 | 0.11 |

| [0.06] | [0.06] | [0.06] | [0.15] | [0.06] | [0.14] | |

| (0.76) | (0.91) | (0.76) | (0.40) | (0.92) | (0.43) | |

| Industry concentration | −1.00 | −0.06 | 0.09 | −0.04 | 8.29 | 9.55 |

| [3.04] | [3.03] | [3.05] | [3.02] | [5.92] | [5.92] | |

| (0.74) | (0.98) | (0.98) | (0.99) | (0.16) | (0.11) | |

| Lobbying activity | 0.47*** | 0.44*** | 0.43*** | 0.44*** | 0.45*** | 0.44*** |

| [0.17] | [0.17] | [0.17] | [0.17] | [0.17] | [0.17] | |

| (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | |

| PAC expenditures | 0.95*** | 1.00*** | 0.97*** | 0.98*** | 1.01*** | 0.98*** |

| [0.17] | [0.17] | [0.17] | [0.17] | [0.17] | [0.17] | |

| (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | |

| CEO ownership | −0.26 | −0.24 | −0.25 | −0.23 | −0.26 | −0.26 |

| [0.18] | [0.18] | [0.18] | [0.18] | [0.18] | [0.18] | |

| (0.15) | (0.18) | (0.17) | (0.21) | (0.15) | (0.16) | |

| Debt intensity | 0.18** | 0.17* | 0.13 | 0.15 | 0.15 | 0.11 |

| [0.09] | [0.10] | [0.09] | [0.10] | [0.10] | [0.09] | |

| (0.04) | (0.09) | (0.13) | (0.14) | (0.12) | (0.26) | |

| Capital intensity | −15.05 | −14.75 | −15.84 | −14.12 | −14.10 | −14.62 |

| [9.97] | [9.94] | [9.81] | [9.91] | [9.94] | [9.76] | |

| (0.13) | (0.14) | (0.11) | (0.15) | (0.16) | (0.13) | |

| Firm performance | 2.17 | 2.33 | 2.53 | 2.16 | 2.08 | 2.12 |

| [3.18] | [3.12] | [3.09] | [3.13] | [3.09] | [3.07] | |