Abstract

This paper examines household decisions over long-term care insurance (LTCI) purchases through a bargaining lens. Long-term care insurance purchase is a discrete decision around which spouses’ interests may diverge substantially. The cost of buying LTCI is typically borne by both spouses, but the benefits of LTCI go disproportionately to women, who are more likely to need long-term care for themselves, and to benefit from the asset protection and other support LTCI offers in the event their husband needs care. Using panel data on married couples ages 50–75 from the US Health and Retirement Study (HRS), we test and find support for the hypothesis that spouses’ relative bargaining power is related to LTCI purchase decisions. In particular, when husbands have final say in household decisions, LTCI coverage is less likely. The findings suggest that spouse’s relative bargaining power matters for health care choices and, therefore, for the welfare of older men and women.

Keywords

Introduction

Long-term care (LTC) involves the provision of personal care and other related services on an extended basis to people who need assistance with activities of daily living (ADL), such as dressing, bathing, and toileting.1, 2 The costs of LTC services are extremely high: in the United States (US), the median annual charge for skilled nursing home care in 2018 was just over $100,000 and that for in-home health assistance was $50,000. 2 Private health insurance and Medicare in the US 3 do not pay for LTC services, which means that insurance coverage must be purchased in the private market or obtained through Medicaid. Medicaid eligibility, however, requires very limited assets and income. Non-poor older adults without private insurance for LTC face significant out-of-pocket expenditures for these services. Yet despite the potentially large cost of care, demand for long-term care insurance (LTCI) is very limited (Lambregts & Schut, 2020).

Lack of LTCI coverage is a particularly acute issue for women. In the U.S. and elsewhere, women are more likely to need LTC services at some point than are men, 4 and if they need nursing home care, they need it for longer (Moore et al., 2019). The U.S. Centers for Disease Control (CDC) reports that women make up a large majority of recipients of all forms of LTC services (National Center for Health Statistics, 2019). These outcomes can be attributed to both health and social factors: women have longer average life expectancies than men and have a greater risk for a number of chronic illnesses (Beam et al., 2018; World Health Organization, 2015). Moreover, as women often marry men older than themselves, they are less likely to have a spouse who could care for them at home.

Despite women’s greater likelihood of needing paid care, the LTCI pricing structure was, until 2013, gender-neutral (Brown & Finkelstein, 2007; National Women’s Law Center, 2014). During this gender-neutral pricing period, we would have expected to see more women than men purchasing LTCI insurance, and a significant number of couples purchasing LTCI only for the wife. Yet this predicted pattern was not observed in the market. Brown and Finkelstein (2007, 2008) found that women and men over age 50 were about equally likely to have LTCI coverage. 5 In the national household survey data we use in this paper, it was relatively rare for a couple to purchase LTCI for the wife only, although gender-neutral pricing and women’s higher risk of needing care would seem to make this strategy appealing.

The facts discussed so far present us with two puzzles. The first is the well-known (see, for example, Ameriks et al., 2015) LTCI under-insurance puzzle: given that LTC is such a large and unpredictable expense, why do relatively few people insure against it? The second is what we call the LTCI gender gap: why did relatively few couples take advantage of the option to buy insurance for women at what was, in the absence of gender-rated premiums, a relatively attractive rate? Or, put another way, why do so many couples opt for gender parity in LTCI coverage when women are more likely to need formal LTC than are men?

In this paper, we argue that understanding the LTCI purchase decision as the outcome of bargaining between partners in marriage sheds light on both of these puzzles. We are, as far as we are aware, the first to analyze LTCI purchases as the outcome of bargaining between spouses. A bargaining model explicitly recognizes that family members’ interests can, and do diverge, and provides a framework for understanding how conflicts between family members are resolved. Conflict over LTCI purchase decisions can arise because women are more likely to be the healthy spouse in a situation when one partner needs care, and in that position they value LTCI for their spouse’s well-being, to ease their own caregiving responsibilities, and for asset protection. Women are also more likely to be a surviving sick spouse, hence valuing their own LTCI in the absence of a spousal caregiver. To the extent that LTCI benefits women more than men, we would expect—all else being equal—to see an increase in LTCI purchases when women’s influence over household decisions, or bargaining power, increases.

Our empirical analysis uses multiple waves of the US Health and Retirement Survey (HRS) from 1996 to 2014, when gender-neutral pricing for new LTCI policies was largely ended. One advantage of the HRS for this study is that it surveys couples in the age ranges when LTCI decisions are most likely to be made. Another advantage is the richness of the survey. It contains data on spouses’ decision-making roles, notably perceptions of who has the “final say” in major household decisions; data on other commonly used indicators of partner’s relative bargaining power such as age and education differences, and wife’s share of income; data on well-established determinants of LTCI purchases, such as household income and wealth, family structure, health, and retirement status; and, of course, data on LTCI coverage. With the HRS data, we are able to estimate traditional empirical models of the determinants of LTCI purchase augmented with measures of household decision-making processes. Our estimates confirm that bargaining power matters in married couples’ LTCI decisions, and supplementary estimates demonstrate that potentially confounding factors do not change our main findings.

Our study is situated at the intersection of three literatures: the LTCI literature, the literature on intra-household decision-making, and the somewhat smaller literature that considers LTCI purchase decisions in a household context. The first part of the paper surveys these literatures and establishes a theoretical context for the paper, and sets out the paper’s contribution: it provides a novel explanation of the LTCI under-insurance paradox, it shows that household bargaining considerations influence LTCI purchases, and it contributes to the larger literature investigating the impact of household bargaining on family financial decisions. We go on to describe our research design and data and results of estimating LTCI coverage using data from the HRS. The final section of the paper presents conclusions and implications of the research.

Understanding LTCI Purchase in a Family Bargaining Context

Although there is a large literature on how couples make decisions and the factors that influence how conflicts between partners are resolved, LTCI has rarely been considered in this light. There are a number of scholars who have attempted to understand the intra-family dynamics that inform LTCI purchases, such as Ko (2020) and Tennyson and Yang (2014). However, the literature has focused primarily on the caregiving dynamics between parents and children (see, for example, Barczyk and Kredler (2018); Courbage and Roudaut (2008); Klimaviciute (2017); Lockwood (2018)) or considered children’s influence on LTCI purchases (Sperber et al., (2017); Zhou-Richter et al., (2010)). Some papers have considered spousal caregiving (Mommaerts & Truskinovsky, 2020) or family structure more generally (Van Houtven et al., 2015). However, the possibility that spouses may have conflicting interests over the purchase of LTCI has rarely been acknowledged or discussed. In this section we review standard economic approaches to modeling LTCI purchase decisions, and explain why spouses can have conflicting interests over the purchase of LTCI. We argue that understanding these conflicts and how they are resolved provides novel insights into the LTCI purchase decision and can help explain why relatively few people choose to buy LTCI.

Economic models of the LTCI purchase decision generally use some variation of the framework developed by Pauly (1990) and Zweifel and Strüwe (1998), in which an individual chooses consumption and insurance purchases to maximize expected utility in the face of uncertainty about future health states. In the simplest version of this model (Pauly, 1990), the individual has a fixed amount of wealth to be consumed over two stages of life. In stage 1, the individual is healthy; in stage 2, the individual either becomes sick and needs LTC or remains healthy and then dies without a lingering illness. In this model, the individual’s problem is to choose the combination of stage 1 consumption, savings, and LTCI purchases that maximizes expected lifetime well-being. If risk averse, a person will prefer to smooth consumption over various states of the world. Hence, if actuarially fair LTCI is available, people would rationally choose to purchase the insurance to achieve maximal consumption smoothing.

In reality, the majority of people do not have LTCI coverage—the so-called “under-insurance puzzle”. Reasons why LTCI coverage is relatively sparse have been explored by, for example, Brown and Finkelstein (2008) and Ameriks et al. (2015). Brown and Finkelstein (2011) and Lambregts and Schut (2020) provide comprehensive literature surveys, while Eaton, 2016 provides an industry perspective. There are numerous explanations for the under-insurance puzzle. Long-term care insurance can be relatively expensive: adverse selection and administrative costs may cause an individual’s LTCI premiums to rise above an actuarially fair level. When premiums exceed what is actuarially fair, a person will weigh the degree of mark-up against the perceived risk of needing care, availability of family caregivers, and ability to self-finance care. Availability of government financing may be another important consideration. In the U.S., payments received through a LTCI policy reduce the amount of Medicaid that an individual can receive, creating an implicit tax on the benefits provided from the policy. Since eligibility for Medicaid is income and asset-tested, the implicit tax rate on LTCI payouts can range from zero, for a person who would never be eligible for Medicaid, to 100 percent. The implicit tax on LTCI created by Medicaid may lead people in certain income and asset ranges to rationally choose not to insure against the need for LTC (Brown & Finkelstein, 2008). Lack of financial literacy, and the difficulty of planning for large and uncertain risks, may also constrain (or, if it leads to people buy over-priced policies, inflate) LTCI demand (Brown & Finkelstein, 2011; Lambregts & Schut, 2020). Alternatively, Lockwood (2018) suggests that bequest motives may induce people to accumulate sufficient savings to self-insure against LTC needs, reducing demand for LTCI.

A final explanation given for the low level of LTCI coverage is summarized by Lambregts and Schut (2020) as follows: “if people prefer informal care they may strategically decide not to buy LTCI in order to increase informal caregiving.” This passage paradoxically both recognizes and ignores the complex intra-household dynamics around caregiving. It recognizes intra-household dynamics by acknowledging that people might think strategically about other family members’ responses, and in particular other family members’ willingness to provide care, when buying LTCI insurance. Indeed, the suggestion that the amount of care people wish to receive might be greater than the amount of care others wish to give implicitly acknowledges that family members have conflicting interests over the provision of care and the purchase of LTCI.

Lambregts and Schut (2020), like Pauly (1990), Zweifel and Strüwe (1998), Courbage and Roudaut (2008), Klimaviciute (2017) and most others who have analyzed this “intra-family moral hazard” focus on parent–child relationships, and the possibility of children shirking their caregiving obligations. In these moral hazard models, parents make LTCI purchase decisions unilaterally based upon their expectations about their children’s future behavior. While parents may care about their children, the children in these models do not have a say in the parents’ LTCI purchase decisions. (In reality, however, children may influence parents’ LTCI purchase decisions (Sperber et al., 2017) or even buy LTCI coverage for parents (Zhou-Richter et al., 2010).) 6

Yet intra-family moral hazard is a potential issue between spouses, as well as between parents and children. Some people in marital relationships may well “strategically decide not to buy LTCI in order to increase informal caregiving”, as Lambregts and Schut (2020) put it. Indeed, this reasoning motivates the title of our paper: “my wife is my long-term care insurance policy”. Yet potential caregivers have an equally strong strategic motive to decide to buy LTCI in order to decrease informal caregiving. Moreover, a caregiving spouse, unlike a child, typically does have a say in the couple’s LTCI purchase decisions. The contributions of this paper are to point out the conflict between spouses who have a strategic incentive not to buy insurance and spouses who have a strategic incentive to buy insurance, and to show that this conflict can partially explain the under-insurance puzzle.

The large economic and sociological literature on intra-household decision-making and resource allocation (e.g., Bittman et al., 2003; Horne et al., 2018; Jianakoplos & Bernasek, 2008; Lundberg et al., 1997; Lundberg et al., 2003; McElroy & Horney, 1981; Romm, 2015; for a survey, see Eswaran, 2014) suggests that, generally speaking, conflicts within families tend to be resolved in favor of family members with greater bargaining power. This insight, when applied to the specific case of LTCI purchases, suggests that if the husband has greater bargaining power, the household’s LTCI purchase decisions will be closer to those he prefers. However, if the wife gains bargaining power she will be able to influence LTCI purchase decisions in her preferred direction.

But what determines how much bargaining power each family member has? Economists emphasize family members’ relative access to resources, such as income, occupation, education or potential earnings, as determinants of bargaining power (Horne et al., 2018; Jianakoplos & Bernasek, 2008; Lundberg et al., 1997; Lundberg et al., 2003; Romm, 2015). However, for retired households employment and occupation is no longer observable. Income is not as important as wealth and retirement assets. Yet because few data sets contain individual-level data on wealth holdings, intra-household inequality in wealth or access to capital income is hard to measure. Thus, in this paper, we employ a different approach: we measure bargaining power directly using information on which partner has the most say over family decisions, gathered in the HRS by asking respondents “When it comes to making major family decisions, who has the final say…?”

Our analysis contributes to the emerging literature investigating the impact of “final say” on family financial decision-making. For example, (Friedberg & Webb, 2006) and Yilmazer and Lich (2015) use self-reported measures of “final say” to study the impact of bargaining power on household investments in risky assets. Phipps and Woolley (2008) and Gibson et al. (2006) use such measures to study the effect of bargaining power on household savings; other papers have used this to test household bargaining models of life insurance purchases (Babiarz et al., 2012; Wong, 2015).

Using “final say” as a measure of bargaining power assumes that the person with final say has greater influence, and is able to sway outcomes in his or her preferred direction. Support for this assumption is given by research finding that measures of say line up with other indicators of bargaining power. For example, Dobbelsteen and Kooreman (1997) argue that “financial management”, that is, who has greater say in household decisions, “is primarily determined by bargaining considerations.” Bertocchi et al. (2014) find that measures of decision-making responsibility are associated with other measures of power and influence, such as income. Likewise, Mazzotta et al. (2019) find as the income (and education) of women increases relative to their partners’, they are less likely to have responsibility for time-consuming decisions and more likely to be responsible for making less frequent, higher-stakes decisions. Thus, “final say” is a measure of bargaining power, but one with a crucial advantage: it can be observed even after individuals have withdrawn from the labor force. Use of this measure also avoids some of the endogeneity issues that come with relying on resource-based measures such as income and wealth (Friedberg & Webb 2006).

It could be argued that answers to questions about “final say” reflect respondents’ gender norms, as gender roles and relations limit how much women are expected to exert autonomy in decision-making (Osamor & Grady, 2018). Yet gender norms do predict how resources are allocated within households (Bittman et al., 2003). Mabsout and van Staveren (2010) term this “institutional bargaining power” or “the bargaining power one party freely derives from unequal social norms.” The fact that “final say” captures this institutional bargaining power, as well as resource-based sources of bargaining power, is a strength of the measure.

Drawing from the analysis so far, we can predict that in households where the wife (husband) has final say, the households’ resources are more likely to be used in ways that she (he) prefers. But what does this mean with respect to LTCI purchases? To answer this question, we begin with a thought experiment: how would men’s and women’s incentives to buy LTCI differ if men’s and women’s differential risks of needing care were priced into LTCI premiums? For example, imagine that both male and female policy holders could expect to receive, on average, $0.98 in benefits (say) was for every $1 paid in LTCI premiums, making LTCI an extremely attractive purchase. We argue that, even in this case, partnered men and partnered women have different incentives to buy insurance, for a number of reasons.

First, women tend to be more risk averse than men (Eckel & Grossman, 2008). People who purchase LTCI have been found to be more risk averse than people who do not (Ameriks et al., 2015), which would tend to lead to greater demand for LTCI among women. Second, men are more likely than women to have a spouse available to act as a caregiver in the event of debilitating illness. Men who reason as strategic, rational economic agents have an incentive to forgo purchasing LTCI in order to encourage the provision of informal care in this situation, as described by Lambregts and Schut (2020). Men who think less strategically may simply assume their wife will be available to care for them. As Cash et al. (2019, p. E19) note “normative roles of women as caregivers are embedded across the life course”—even though in reality a non-trivial number of men are caregivers to their spouses. Third, because men on average predecease their partners, they are less likely to benefit directly from any asset protection or choice in care provided by having LTCI for their wives.

Women, on the other hand, are more likely to be the surviving spouse. They need their spouse to have LTCI coverage for asset protection purposes and need LTCI coverage themselves to pay for their own care. Finally, women are statistically more likely be the caregiving spouse. In this role, they have a strategic incentive to encourage their partners to buy LTCI, because they benefit from the relief that insurance offers them in terms of choice of care options. For example, Coe et al. (2015a, 2015b) find that an exogenous increase in the availability of LTCI decreases the amount of informal caregiving provided by family, suggesting that the presence of LTCI coverage can offer real relief from the stressful work of caregiving. Similarly, van den Broek and Grundy (2020) find that availability of formal LTC improved caregivers’ life quality.

Yet while the benefits of LTCI differ, on average, between men and women, if couples share expenses, then the costs of insurance will be borne by both of them. Long-term care insurance insurance premiums are substantial. Premiums averaged nearly $4675 per couple per year in 2018 for buyers of stand-alone LTCI coverage at age 65. 7 Even the most loving of spouses might hesitate before investing many thousands of dollars annually into an insurance policy that provided him with relatively little direct benefits. In sum, even when men’s and women’s differential risks of needing care are fully priced into LTCI, women would typically be expected to value LTCI coverage, both for themselves and for their spouses, more highly than men.

So far, we have been working through a thought experiment that assumed men’s and women’s differential risks of care were priced into LTCI—that the ratio of expected benefits to premiums was the same for both male and female policy holders. However, our study covers a period when, according to Brown and Finkelstein (2007), gender-neutral insurance pricing meant that the expected benefits of insurance were substantially higher for women than men. Indeed, Brown and Finkelstein estimated, using 2002 data, that for women a typical LTCI policy held until death paid out, on average, $1.04 for every dollar in premiums, whereas men’s policies only paid out $0.56. These differences in load factors made LTCI for women a particularly attractive investment. Indeed, the hypothesis advanced in this paper is one of the few ways to explain why an informed, non-Medicaid-eligible household would not buy LTCI for women given these load factors: LTCI purchase decisions are the outcome of household bargaining, and they reflect each spouse’s bargaining power. Men tend not to value LTCI for a variety of reasons, and they are typically the ones with greater influence in family decision-making. The unique contribution of this paper to the literature is to recognize the possibility of spousal conflicts over LTCI purchases and to use insights from bargaining theory to explain the gender gap in LTCI purchases. We suspect at least for the married couple, the dynamics between husbands and wives matters more than the dynamics with children in LTCI decisions.

There are other real world complexities that affect LTCI purchases. Specific household characteristics including age, financial resources, health trajectories, risk preferences, Medicaid eligibility, and availability of children who could act as caregivers will affect valuation patterns for individual households. Not everyone who applies for LTCI is accepted. The LTCI marketplace has evolved over time (Eaton, 2016), and premium levels have risen, particularly in the period immediately after the 2008 financial crisis. In the next section, we describe how we control for these complexities in our empirical research design. The point of this section has simply been to argue that, within a marriage, LTCI coverage benefits men and women differently. Therefore, we would expect the degree of bargaining power each person has in the relationship to influence the amount of LTCI coverage purchased for each family member.

Empirical Research Design

Using data on both husbands and wives from a sample of married individuals in the HRS, we estimate empirical models to measure the effects of household decision-making on the probability of LTCI coverage. Our measure of relative bargaining power is based on couples’ self-reported “final say” on major household decisions. All married or cohabiting respondents are asked about this in the first wave that they appear in the HRS survey. Because the “final say” variable is measured only once per couple, we interpret it as an indicator of an underlying relational constant that reflects relative bargaining power. 8

We employ two approaches to estimating the effects of household bargaining on the probability of LTCI coverage. The first approach provides linear probability estimates 9 (Generalized Least Squares estimators, GLS, henceforth) of LTCI coverage for each married individual in our sample. We estimate models for husbands and wives separately. We first include only the individual respondent’s characteristics as controls and then compare estimates that add spousal characteristics. Finally, we add measures of relative bargaining power to the models. This analysis replicates and adds to the traditional empirical models employed in the LTCI literature. The second approach estimates multinomial logit models (MNL) of the composition of household LTCI coverage within each household. For each married couple in the sample, we estimate the composition of household LTCI coverage in each year—whether neither spouse, only the husband, only the wife, or both spouses—is covered by LTCI. These estimates include characteristics of both spouses and measures of relative bargaining power. This analysis provides a clearer look at LTCI decisions at the household level. Both the individual and couples’ estimates incorporate extensive individual and household control variables, individual random-effects 10 and survey year fixed-effects. Standard errors are clustered at the household level.

Data and Sample

The HRS collects information on income, work, assets, health insurance, physical health and functioning, cognitive functioning, and health care from a representative sample of individuals over age 50 (Institute for Social Research, 2017). The HRS additionally reports information on demographic, economic, education, family, and health characteristics of surveyed individuals and their spouses. We use 10 waves of HRS data from 1996 to 2014 in this study; 1992 and 1994 waves are excluded because the survey question asking whether one has LTCI changed significantly in 1996. 11 Post-2014 waves are excluded because the switch to gender-rated insurance premiums changed men’s and women’s relative incentives to buy insurance after this point in time. Our sample includes couples from all HRS cohorts. 12 We use the RAND-HRS data in our study (Rand Corporation, 2017) because it is formatted in a manner better suited to panel data analysis and includes in each observation the responses from both the respondent and their spouse (if married/partnered).

Since we are interested in couples’ bargaining, we limit the sample to those couples who are married or partnered. 13 To focus our analysis on active LTCI decision-making, we eliminate respondents in which anyone in the household is covered by Medicaid. We further limit the sample to those ages 50 to 75, since most LTCI purchases occur after age 50 and the majority of purchases occur before age 70, and comparatively few individuals over age 70 are healthy enough to successfully apply for LTCI (American Association for Long-term care Insurance [AALTCI], 2017).

We drop respondents when changes in marital partners create ambiguity about the identity of spouses who bargained over LTCI purchase. If a respondent did not have LTCI when they entered the HRS and remained married to the same individual throughout our study period, no such concerns arise. However, for those who reported already owning LTCI in their first HRS interview, we include in our sample only those who were married to the same individual since at least age 50. For those who did not have LTCI when they entered into HRS but married again within the study period, we keep them in the sample only if the “final say” question was asked after the remarriage.

Finally, to reduce concern that responses to household decision-making questions may be subject to social response bias, we omit respondents and their spouses if either partner refused to answer or responded “don’t know” to the question about which spouse has “final say”. Applying these criteria results in a sample of 51,308 observations on 12,396 individuals who are married/partnered, and both spouses report data on LTCI coverage and household decision-making. 14

LTCI Coverage

We obtain LTCI coverage information from the following question in HRS: “not including government programs, do you now have any insurance which specifically pays any part of LTC, such as personal or medical care in your home or in a nursing home?” This question is general enough to include all forms of insurance policies that cover LTC, whether stand-alone coverage or coverage bundled with life insurance or annuities. The question has been asked of both husbands and wives in all waves in our study period.

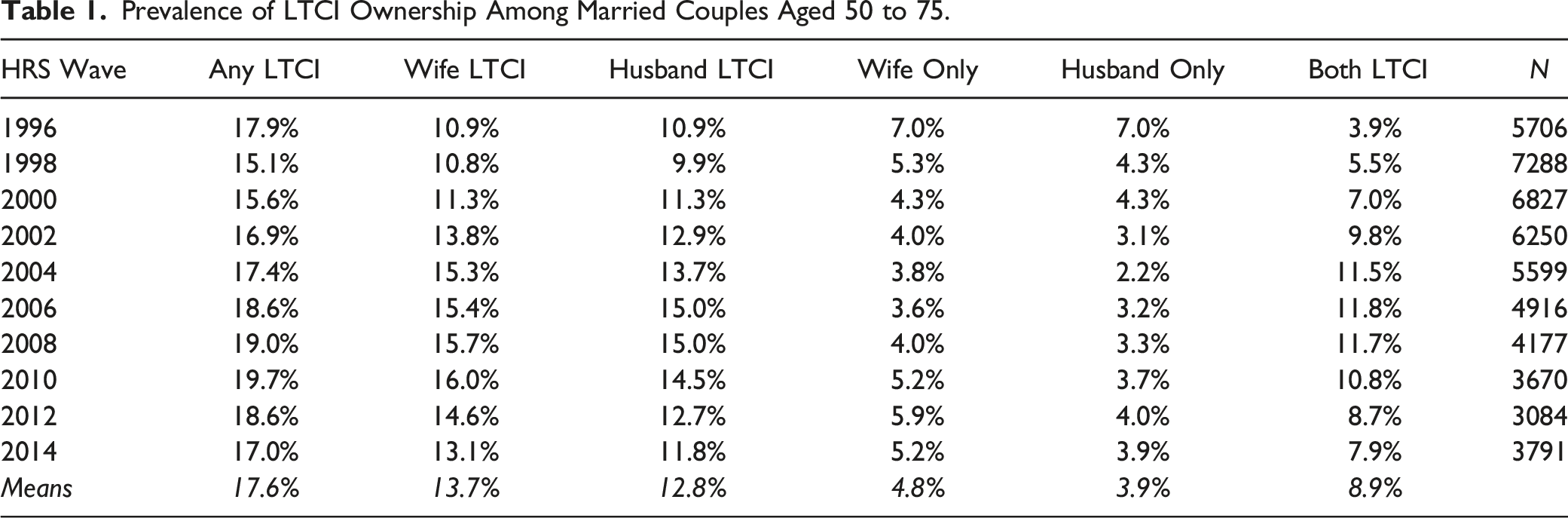

Prevalence of LTCI Ownership Among Married Couples Aged 50 to 75.

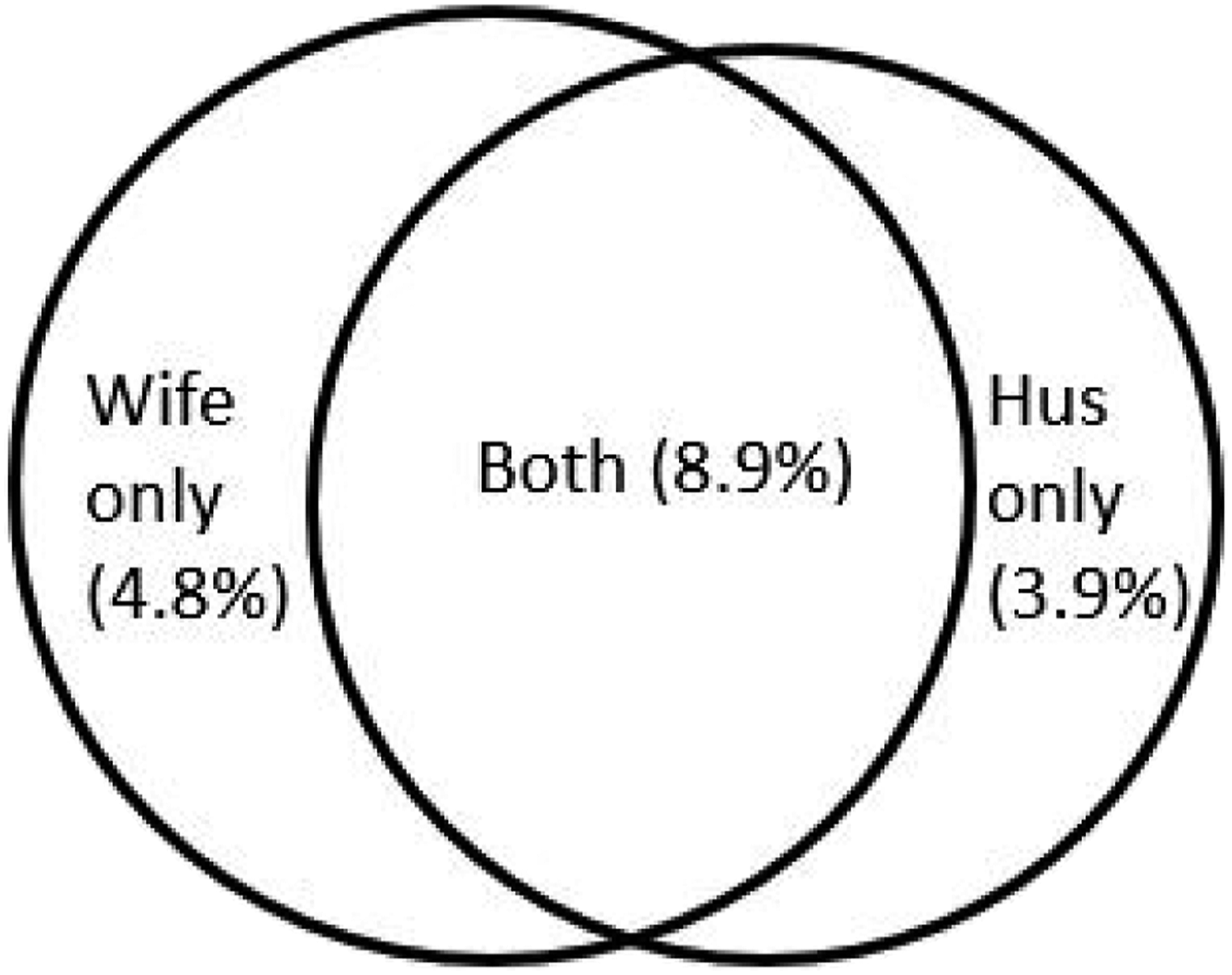

Diagram of Long-Term Care Insurance ownership of a couple.

The data show that only a minority of older couples have any LTCI coverage and that coverage rates vary over time. 15 Averaging over all waves of the sample, in 17.7 percent of households at least one spouse is covered by LTCI. Coverage rates for wives are slightly higher than for husbands, but differences are relatively small (13.7 percent vs. 12.8 percent when averaged over all waves). Within households, it is again slightly more likely that only the wife has LTCI coverage (4.8 percent all-wave average) compared with only the husband having it (3.9 percent all-wave average), and the proportion of couples with both spouses having LTCI increases over time. In 1996, only 4.0 percent of couples reported both spouses having LTCI coverage; this increased sharply to 11.9 percent in 2006, before falling gradually to 11.0 percent in 2010 and then more sharply to 8.1 percent by 2014. The declines in LTCI coverage beginning in 2010 may reflect changes in the LTCI market and/or entry of new HRS cohorts that change the age-mix of respondents in our dataset.

Relative Bargaining Power

A key contribution of this paper is to add measures of spouses’ relative influence on household decision-making, as captured by say over decision-making, to the standard determinants of LTCI coverage. We obtain household measures of “final say” from the HRS questions asked of each partner in a married or cohabiting couple in the first wave that they appear in the study: “When it comes to making major family decisions, who has the final say—you or your spouse? By ‘major family decisions’ we mean things like when to retire, where to live, or how much money to spend on a major purchase.” All married or cohabiting respondents were asked this question in the 1992 HRS and again in 1994. In subsequent HRS waves, only new entrants or those with new spouses/partners were asked the question. Thus, for our sample period we include couples’ 1994 responses for those who entered the survey in 1992 or 1994 and the entry wave responses for those who entered the survey in subsequent waves. We use this response throughout the sample period unless/until a new response is gathered due to a change of partner.

Distribution of Views on Household Decision-Making Among Couples Aged 50 to 75.

Because husbands and wives do not always agree on who has more say over major decisions, our main specifications employ three “say” measures to indicate substantially more decision-making power for the husband. In the first set of specifications, we include a variable indicating that according to the respondent (who may be either the husband or the wife) the husband has final say. In the second set of specifications, we include a variable indicating that both spouses agree that the husband has final say. In the final set of specifications, we include three indicators of final say—a variable indicating that only the wife says that the husband has final say, a variable indicating that only the husband says that he has final say, and a variable indicating that both spouses agree that the husband has final say. In this specification, the omitted category of responses includes all responses indicating that the wife has final say and those indicating that the spouses have equal say. Due to the low prevalence of responses indicating that the wife has final say, we group these together since both represent a household perception of less decision power for the husband than the included category. A fourth specification includes (only) a variable indicating that both spouses agree that each spouse has equal say, to confirm whether households in which wives have greater bargaining power are more likely to have LTCI coverage.

Control Variables

Demographic characteristics may affect the demand for insurance through their reflection of differences in life expectancies or health trajectories, risk-aversion, information sets or costs of obtaining information; hence, our models control for individual characteristics including age, years of education, gender, and race.

We control for retirement status with the expectation that retired individuals will be more likely to own LTCI, since research has shown that LTCI purchase often occurs as part of retirement planning (Stum, 2006). We control for total household income and household net worth using data taken directly from the RAND dataset; we aggregate net worth into quintiles and include income in log form. These measures include retirement income and pension assets, respectively. Individuals with higher income or wealth are expected to be more likely to own LTCI.

We include a dummy variable set equal to 1 if the respondent receives health insurance from a (current or former) employer. Because traditional health insurance does not pay for LTC, this variable does not reflect the availability of an insurance substitute. Rather, we hypothesize that it may indicate greater awareness or ease of purchasing LTCI if the employer makes it available through the workplace.

Health status should also affect LTCI ownership, both through health-related demand effects and health-related underwriting by insurers. Based on the literature on LTCI demand, 16 our models include the number of limitations on activities of daily living (ADL) and past health status as control variables. Past health status is measured by the count of chronic health conditions ever diagnosed among hypertension, diabetes, cancer, pulmonary disease, heart disease, and stroke, since these types of diseases may affect LTC risk. A higher value of the variable means the individual has suffered from more chronic illnesses. 17

Family structure can influence the demand for LTCI due to the desire to leave bequests, which may increase or decrease demand; or to the availability of informal care, which may decrease demand. Thus, we include the total number of children that a couple has, along with a dummy variable set equal to 1 if any of the children live within 10 miles of the couple. The evidence from previous studies has been mixed—some studies found little evidence of bequest motives in LTCI purchase decisions (Mellor, 2000; Sloan & Norton, 1997), while others such as Lockwood (2018) claim that bequest motives can decrease the demand for insurance by reducing the opportunity cost of precautionary saving. Based on the previous studies, we expect that children—and especially children living nearby—primarily reflect availability of informal care and will be negatively related to LTCI purchases.

Lastly, LTCI purchase decisions can be affected by an individual’s life experiences. Previous studies report that an individual’s experience providing informal LTC to family members, and whether parents have used LTC, are significantly related to an individual’s LTCI demand (Coe et al., 2015a, 2015b; Courbage & Roudaut, 2008; Tennyson & Yang, 2014). Thus, our models control for whether an individual has ever provided informal care to their parents, and whether their parents ever stayed in a nursing home.

In preliminary estimates, we included a larger set of covariates comprising additional health status variables, longevity expectations, a direct measure of risk-aversion, and self-reported probability of moving to a nursing home. Expanded health measures included limitations on instrumental activities (IADL) and self-rated general health status (ranging from poor to excellent). Longevity expectations were constructed from HRS questions regarding the respondent’s estimated probability of living about another 10 years. Greater longevity expectations may increase demand for LTCI, due to the associated likelihood of physical or mental frailty at older ages. The measure of risk-aversion was based on the set of income gamble questions in the HRS. 18 These additional health, longevity, and risk-preference variables had a large number of missing values, however, and their inclusion did not significantly affect our estimates. Therefore, we report estimation results without these additional control variables. 19

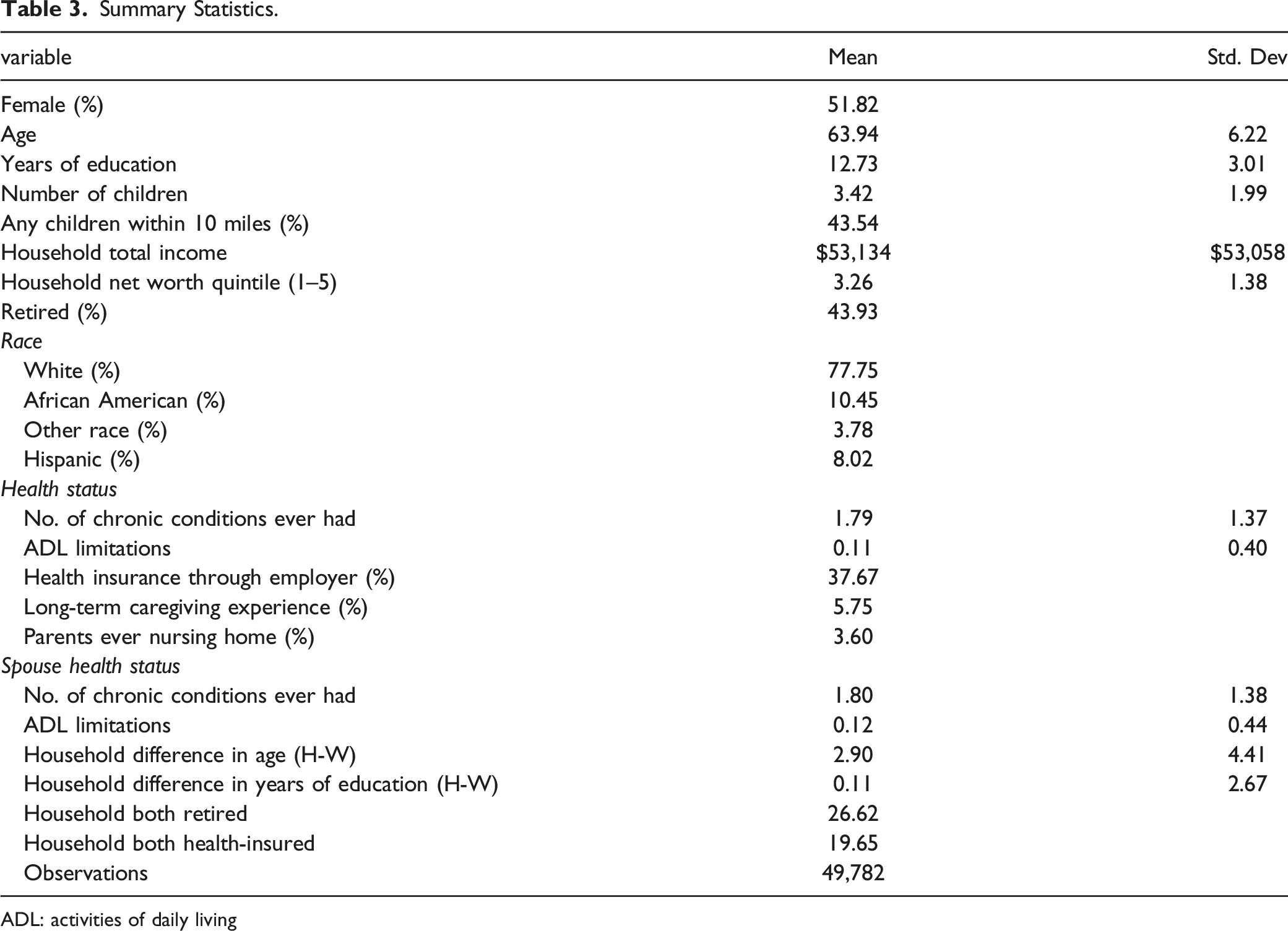

Summary Statistics.

ADL: activities of daily living

LTCI Coverage for Married Individuals

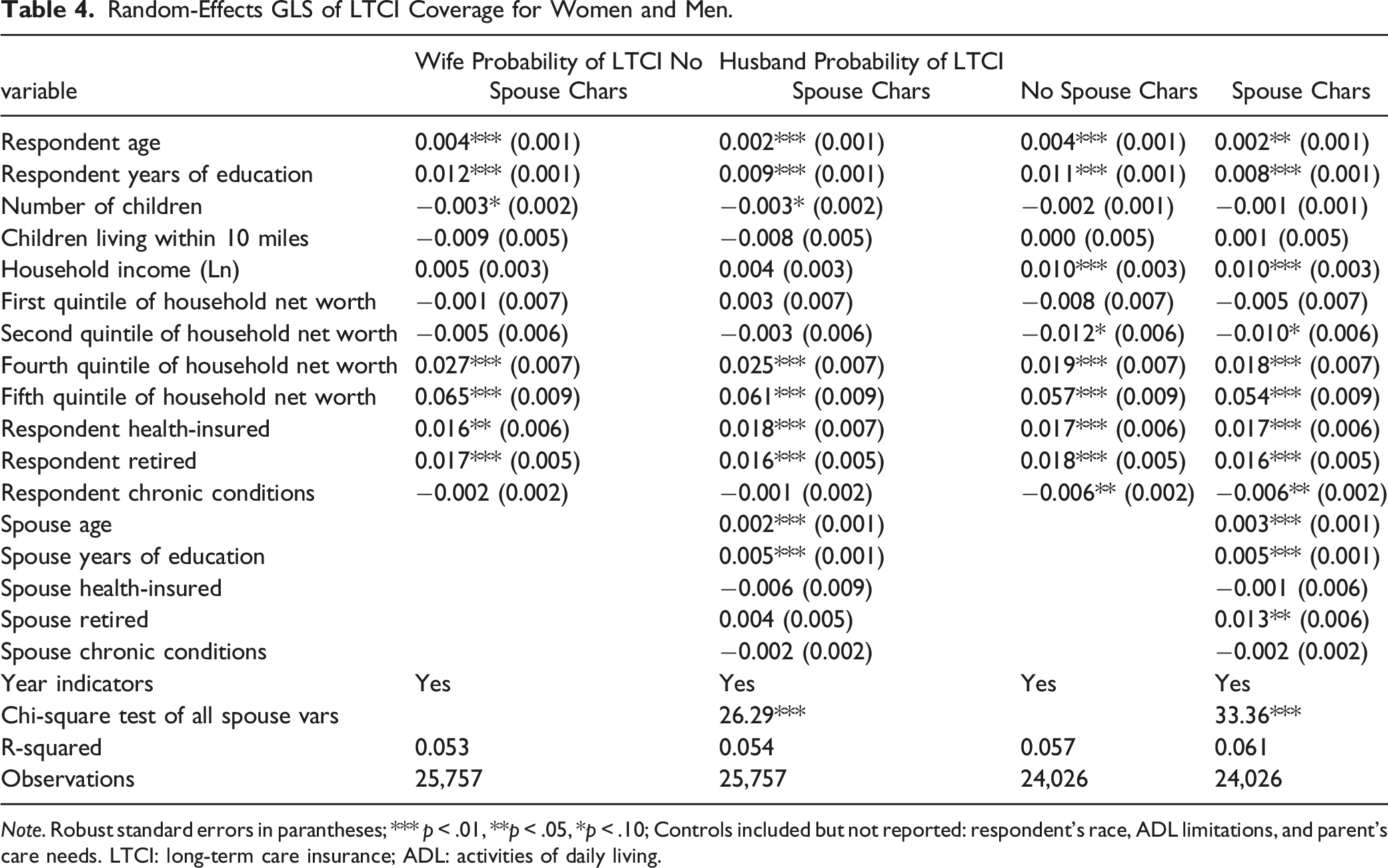

Random-Effects GLS of LTCI Coverage for Women and Men.

Note. Robust standard errors in parantheses; *** p < .01, **p < .05, *p < .10; Controls included but not reported: respondent’s race, ADL limitations, and parent’s care needs. LTCI: long-term care insurance; ADL: activities of daily living.

Across all model specifications, the estimated impacts of independent variables are generally consistent with expectations, when statistically significant. Among both men and women, respondents are significantly more likely to have LTCI coverage if they are older, more educated, and in the top two quintiles of the net wealth distribution. Household income is positive and significantly related to LTCI coverage only for men. Both men and women who are retired and who have health insurance through their employer are significantly more likely to have LTCI. Minority racial or ethnic status is associated with a significantly lower likelihood of LTCI coverage, especially for men.

Estimates that include spouse characteristics (columns 2 and 4) reveal that the only spouse characteristics consistently associated with LTCI coverage are age and education, which are statistically significant and positive in all model specifications for both men and women respondents. Having a retired spouse with health insurance is a positive and statistically significant predictor of LTCI for married men. Chi-square tests of joint statistical significance demonstrate that when considered together a spouse’s characteristics are statistically significant determinants of LTCI for both men and women.

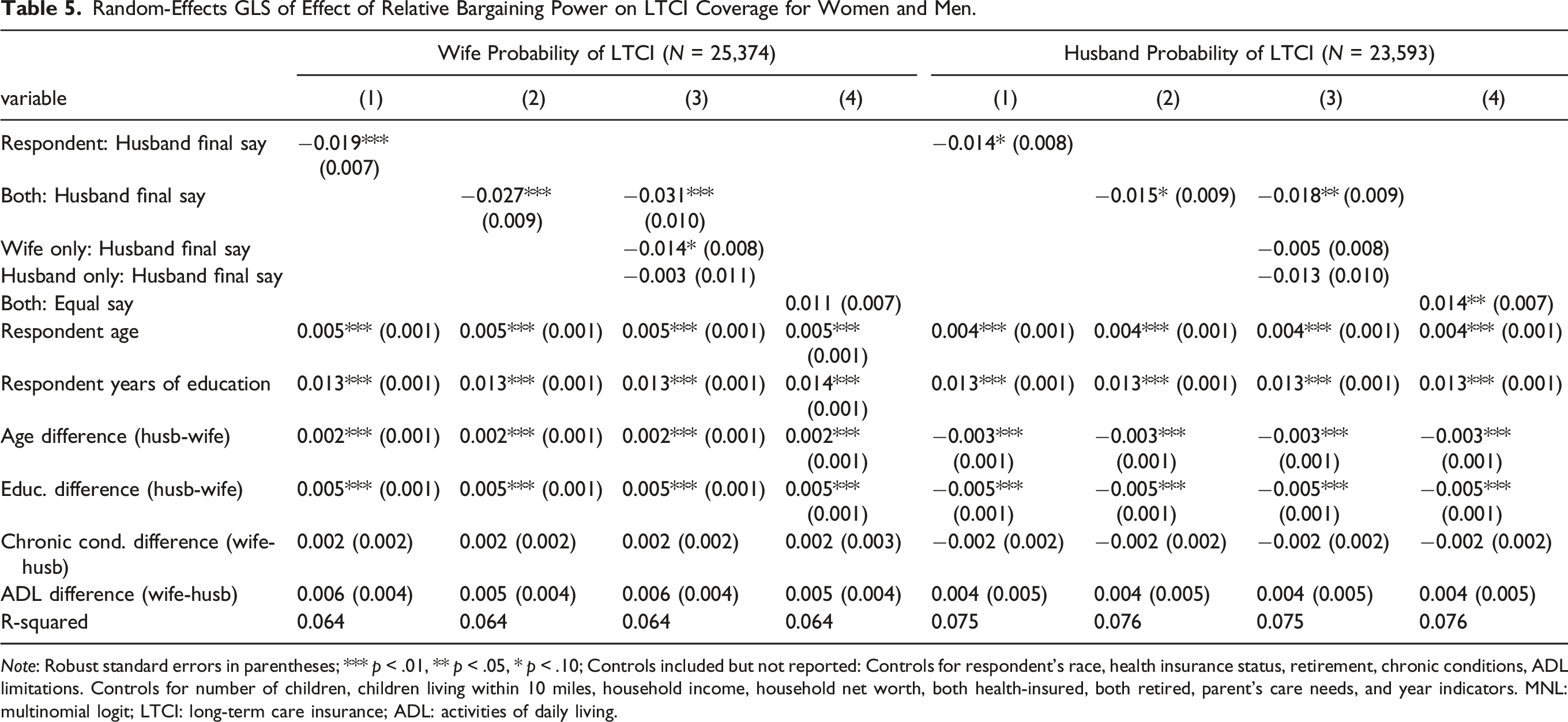

Random-Effects GLS of Effect of Relative Bargaining Power on LTCI Coverage for Women and Men.

Note: Robust standard errors in parentheses; *** p < .01, ** p < .05, * p < .10; Controls included but not reported: Controls for respondent’s race, health insurance status, retirement, chronic conditions, ADL limitations. Controls for number of children, children living within 10 miles, household income, household net worth, both health-insured, both retired, parent’s care needs, and year indicators. MNL: multinomial logit; LTCI: long-term care insurance; ADL: activities of daily living.

Estimation results support the hypothesis that relative bargaining power is related to the likelihood of having LTCI coverage. Variables indicating whether the husband has final say in major household decisions are always negative and often statistically significant, consistent with the hypothesis that husbands are less likely to demand LTCI insurance. Estimates that include the “equal say” indicator are also consistent with this hypothesis. These specifications show that when wives have equal say in major household decisions there is a higher probability of LTCI coverage, and this relationship is statistically significant for husbands’ ownership of LTCI.

More specifically, the first three columns of Table 5 show that the predicted probability of a female respondent (wife) having LTCI is lower by 1.4–1.9 percentage points for wives who report their husband has final say and is lower by 2.7–3.1 percentage points for wives when both spouses agree that the husband has final say. To put these numbers into perspective, a 2.7 percentage point reduction in the probability of purchasing LTCI is similar in magnitude to the impact of reducing the woman’s education by 2 years, or reducing the age gap between the spouses by 13 years. In estimates that use the sample of men respondents (husbands), the man reporting that he has final say is associated with a 1.4 percentage point drop in the probability that he has LTCI coverage, and both spouses agreeing that the man has final say is associated with a 1.5–1.8 percentage point lower predicted probability of him having LTCI. A 1.5 percentage point reduction in the probability that the husband has LTCI is an effect similar in magnitude to a decrease in his education level by 1.1 years.

Other potential measures of bargaining power, such as husband–wife age differences and husband-wife education differences, are also significantly associated with LTCI coverage. Wives who are younger than their husbands are more likely to own LTCI, while husbands who are older than their wives are less likely to own LTCI. The wife’s absolute level of education is positively related to the probability of her having LTCI, but as the wife’s education falls relative to that of the husband, the wife’s likelihood of having LTCI coverage increases. Specifically, an increase in the husband-wife education gap by 1 year is associated with a 0.5 percentage point increase in the probability of the wife having LTCI. However, this impact is less than half the size of the impact of her own education: when a wife’s education level increases by 1 year, her probability of having LTCI coverage increases by 1.3 percentage points. Hence, the overall impact of wife’s education on LTCI is positive.

Composition of LTCI Coverage Among Married Couples

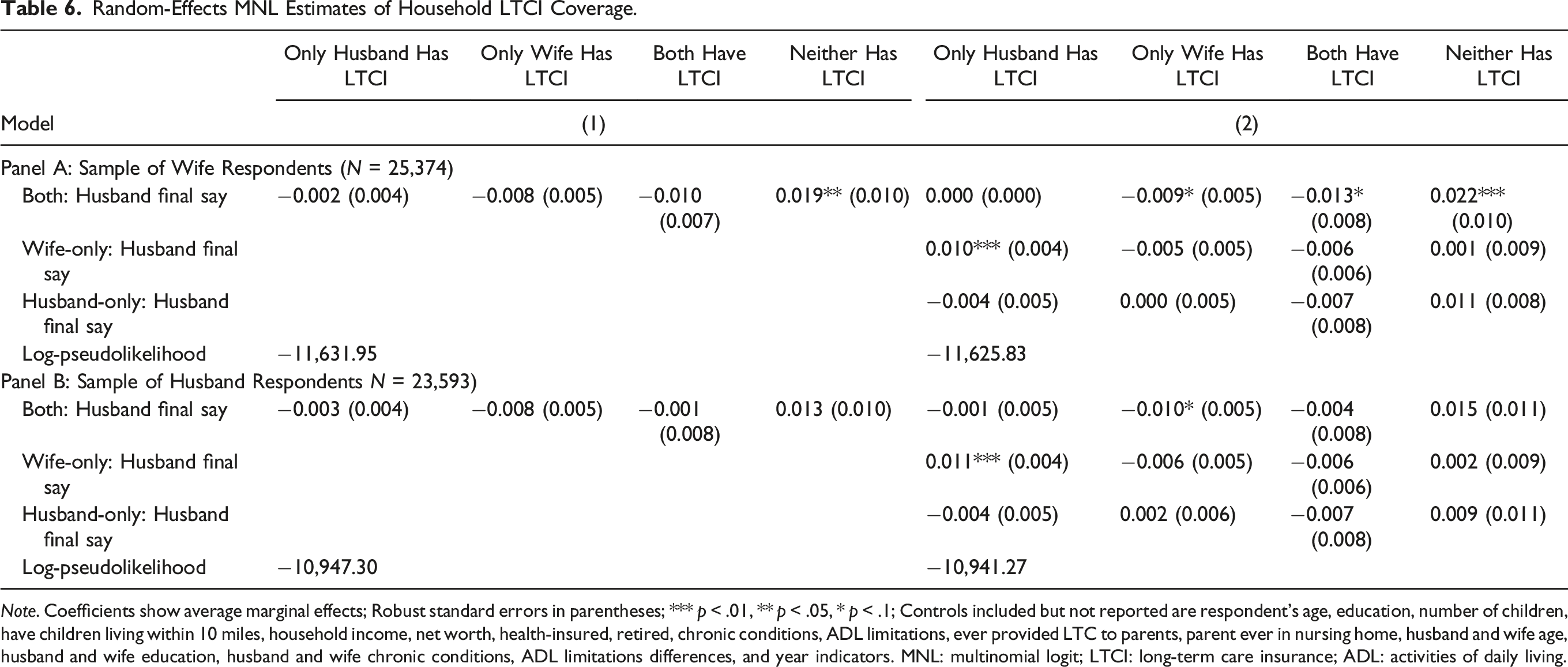

Random-Effects MNL Estimates of Household LTCI Coverage.

Note. Coefficients show average marginal effects; Robust standard errors in parentheses; *** p < .01, ** p < .05, * p < .1; Controls included but not reported are respondent’s age, education, number of children, have children living within 10 miles, household income, net worth, health-insured, retired, chronic conditions, ADL limitations, ever provided LTC to parents, parent ever in nursing home, husband and wife age, husband and wife education, husband and wife chronic conditions, ADL limitations differences, and year indicators. MNL: multinomial logit; LTCI: long-term care insurance; ADL: activities of daily living.

The results are again consistent with household bargaining over LTCI coverage, and with a lower likelihood of insurance purchases in households where husbands have final say. Estimation results using the sample of women (wife) respondents show that in households where husbands and wives agree that the husband has final say it is more likely that neither spouse has LTCI. 21 The point estimates are statistically significant and suggest an associated 1.9–2.2 percentage point higher probability of no LTCI coverage in the households. Given the low rates of LTCI coverage among the sample population, a 1.9 percentage point decline in LTCI ownership represents an 11 percent reduction in any household LTCI coverage (from the sample average of 17.6 percent to 15.7 percent) and is thus a meaningful change in the extent of LTCI coverage.

In both the women (wife) and men (husband) samples, only the wife responding that the husband had final say was associated with a statistically significant 1.0 to 1.1 percentage point increase in the probability that only the husband has LTCI coverage. The explanation for this result can be found by turning back to Table 5, which shows that when only the wife responds that the husband has final say, the probability of her having LTCI decreases substantially (1.4 percentage points), while the probability of the husband having coverage decreases by a smaller, statistically insignificant amount (0.5 percentage points). The combination of a substantial decrease in wife coverage and a much smaller decrease in husband coverage leads to the increase in the number of respondents reporting husband-only LTCI shown in Table 6.

Robustness Checks

We conduct several checks on the robustness of our results. Our first approach is to re-estimate the models using alternative samples and study periods. One sample change we explored is to end the sample period in 2010 because widespread unexpected and retroactive changes in LTCI pricing occurred in 2011. This may have influenced LTCI coverage in the HRS and therefore our findings. Another change we explored is to drop from the sample the oldest (AHEAD cohort) or the youngest (mid-baby-boomer cohort), to test whether potential evolution in couples’ decision-making over cohorts may be influential in our findings. A third sample check is to drop households in which both spouses report that the wife has final say in major household decisions. We conduct this robustness check because analysis of final say patterns reveals that households in which the wife has final say exhibit important differences from other households. 22 In all cases the estimated coefficients on the final say variables are similar in sign, magnitude, and statistical significance to those reported in the paper. 23

Our second set of checks test the robustness of our assumption that the “final say” variable is a fixed characteristic of the spousal relationship. To make this assumption more reasonable, we have limited our sample to the age range of 50–75 so that we are examining the period of active consideration of LTCI purchase and avoiding concerns about health declines in later life that may change bargaining power. We also believe that in this age range changes in bargaining power will not be as likely as they may be in earlier life stages when income shares and child-rearing responsibilities may vary. To check the robustness of our results to this assumption, we undertook supplementary estimates in which we (i) eliminate from the sample couples for whom either spouse experiences a large change in health status, defined as moving three or more categories in self-reported general health (e.g., from excellent to fair or poor, from very good to poor, from poor to very good, or from fair to excellent); (ii) eliminate from the sample couples who experience a change of three or more quintiles in their net worth; and (iii) we restrict our sample to include only four waves beyond the year when the bargaining question was asked, and simultaneously impose the restrictions in (i) and (ii). The sample restrictions in (i) and (ii) eliminate couples for whom major life events may change relative bargaining power, and the additional restriction in (iii) reduces the likelihood of unobservable changes which may occur over the passage of time. Our findings remain unchanged—particularly for wives: husbands having final say is associated with a lower likelihood of wives owning LTCI. 24

Our final check tests the robustness of our findings to relevant features of the LTCI and life insurance markets during our sample period, by testing whether final say variables are significant when we recognize that life insurance ownership is a potential substitute for LTCI ownership. Some life insurance policies that accumulate a cash value can be purchased with a rider permitting the owner to use accumulated values for LTC expenses, or offer accelerated death benefits that can be used for this purpose. In addition, viatical settlements provide owners of life insurance policies the ability to pre-sell life insurance death benefits to investors for a fixed sum of money. This means that ownership of any life insurance policy may indirectly provide LTCI coverage in the event of needing care, and some individuals may anticipate this in their LTC planning.

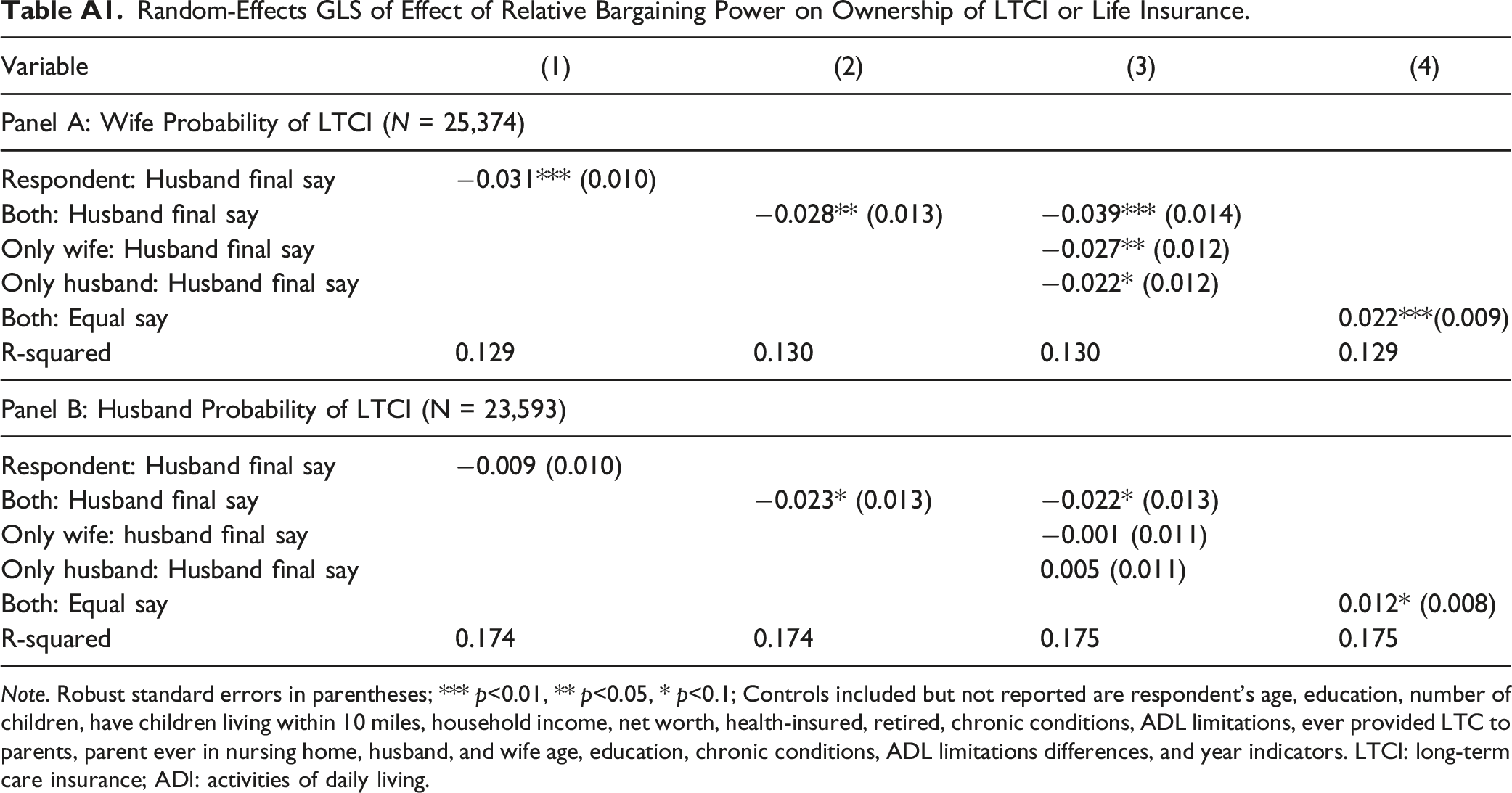

Table A1 reports results of re-estimating the random-effects GLS models of Table 5 using an indicator of ownership of either LTCI or life insurance as the dependent variable. Estimates for women and men respondents are reported separately, and estimated models include the full set of control variables. Only the coefficient estimates for the household say variables are displayed in the table, and the estimates are consistent with husbands having less demand for end-of-life financial planning than wives. Using the sample of women respondents, when both spouses agree that the husband has final say there is a statistically significant 2.7 to 3.9 percentage point lower predicted probability of the wife having either LTCI or life insurance coverage. For men, when both wife and husband agree that the husband has final say, the predicted probability of him having either LTCI or life insurance is lower by 2.2–2.3 percentage points. Results using the “equal say” indicator are also consistent with this interpretation, showing that husbands and wives having equal say in major household decisions is associated with a statistically significant higher probability of both husbands and wives having either LTCI or life insurance.

Conclusion

As the literature on saving and retirement planning increasingly rejects the traditional, rational individual choice model of financial decision-making, an emergent literature has arisen to investigate whether the distribution of bargaining power within a household influences the financial decisions made. This paper adds to that literature by exploring the effects of intra-household bargaining on the decision to purchase insurance coverage for LTC. Long-term care is a particularly good testing ground for this theory, since it is a decision that affects all family members and around which family members’ interests may diverge substantially. Using data on older married couples from the 1996–2014 waves of the HRS, we explore the extent to which estimates based on the outcome of a family bargaining game explain LTCI coverage patterns among married couples.

We find substantial evidence that LTCI purchase is related to household characteristics and situations. In addition to individual characteristics, relative values of spouses’ age and education, and joint situations such as retirement and health insurance ownership are statistically significant correlates of LTCI coverage. Moreover, even after controlling for this wide assortment of characteristics, we find a statistically significant relationship between LTCI ownership and relative bargaining power. Estimates of married individuals’ LTCI coverage reveal that wives in households where the husband has final say over major household decisions are significantly less likely to have LTCI. Estimates exploring within-household LTCI coverage patterns show that when husbands have greater decision-making power, it is significantly less likely that the wife has LTCI, and significantly more likely that neither spouse has LTCI. The effects of greater bargaining power for husbands in reducing LTCI coverage is in keeping with the average husband’s interests, since married men are more likely than married women to have a spouse available to care for them throughout their old age, and LTCI is more likely to benefit a surviving wife.

The immediate significance of our results is a better understanding of how LTCI decisions are made. Their wider significance is a demonstration that household decision-making matters: who has the final say in household decisions has real effects on households’ spending decisions. A considerable body of research in developing countries finds a link between women’s influence on decision-making and health-related choices (Osamor & Grady, 2016). The findings of this paper suggest that intra-household decision-making matters for health care choices and, therefore, for the welfare of older men and women in developed countries as well.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Appendix 1

Random-Effects GLS of Effect of Relative Bargaining Power on Ownership of LTCI or Life Insurance. Note. Robust standard errors in parentheses; *** p<0.01, ** p<0.05, * p<0.1; Controls included but not reported are respondent’s age, education, number of children, have children living within 10 miles, household income, net worth, health-insured, retired, chronic conditions, ADL limitations, ever provided LTC to parents, parent ever in nursing home, husband, and wife age, education, chronic conditions, ADL limitations differences, and year indicators. LTCI: long-term care insurance; ADl: activities of daily living.

Variable

(1)

(2)

(3)

(4)

Panel A: Wife Probability of LTCI (N = 25,374)

Respondent: Husband final say

−0.031*** (0.010)

Both: Husband final say

−0.028** (0.013)

−0.039*** (0.014)

Only wife: Husband final say

−0.027** (0.012)

Only husband: Husband final say

−0.022* (0.012)

Both: Equal say

0.022***(0.009)

R-squared

0.129

0.130

0.130

0.129

Panel B: Husband Probability of LTCI (N = 23,593)

Respondent: Husband final say

−0.009 (0.010)

Both: Husband final say

−0.023* (0.013)

−0.022* (0.013)

Only wife: husband final say

−0.001 (0.011)

Only husband: Husband final say

0.005 (0.011)

Both: Equal say

0.012* (0.008)

R-squared

0.174

0.174

0.175

0.175