Abstract

Background

This study examines how Islamic financial principles have influenced human resource management [HRM] practices from 2010 to 2024. Focusing on concepts like Riba [interest], Mudarabah [profit-sharing], and Takaful [Islamic insurance], the research explores their impact on HRM strategies and organizational sustainability.

Objective

The study aims to understand how these principles reshape contemporary HRM practices by identifying research trends, influential scholars, and major publications, and analyzing their effects on HRM strategies and organizational performance.

Methodology

A three-stage approach analyzed 402 articles using RStudio for data analysis, VOSviewer for citation and network analysis, and Excel for visualization. This method highlighted emerging trends and key research areas.

Key findings

Five research clusters were identified: 1] HRM and employee engagement in sustainable organizations; 2] environmental and sustainability practices in HRM; 3] ethical and social dimensions in HRM and finance; 4] corporate Islamic finance’s HRM implications; and 5] strategic management and financial performance.

Implications

The findings suggest a need for organizations to integrate Islamic finance principles into HRM practices and call for further research on emerging trends, cultural impacts, and long-term effects on organizational performance.

Keywords

Introduction

The 21st century has witnessed a number of developments within human resource management and corporate Islamic finance, both important for the attainment of sustainable organizational growth. Human resource management has a significant impact on talent management, employee engagement, and adherence to ethical standards, especially in Islamic finance.1,2 On the other hand, corporate Islamic finance operates under the Sharia framework, which focuses on ethical investment, sharing of risks, and the prohibition of interest (Riba), toward the realization of social justice and equality.

The focus of this study is the emerging connection between HRM practices and corporate Islamic finance, exploring the key processes driving both fields. 4 In this regard, the paper aims to understand the benefits and challenges of integrating HRM methods with Islamic finance principles.5,6 It thus tends to present practical implications for policy makers, scholars, and business leaders in applying HRM and Islamic financing towards gaining sustainable organizational outcomes.1,7 In the modern global context, HRM develops into an ethical leadership promoting the talent development of employees while strictly adhering to Islamic ethical standards. HR practices in the Islamic finance institutions significantly help attain organizational success.8,9 Correspondingly, corporate Islamic finance redefines the way financial operations are executed in a manner that ensures their conduct in accordance with Sharia and the promotion of social responsibility while equitably developing economic participation. 10 Therefore, an understanding of the intersection of HR and Islamic finance is required to enable their full potential in ensuring organizational growth. 11

To that effect, a systematic review methodology has been used for this study since it involves a rigorous yet unbiased analysis of existing literature about HRM and corporate Islamic finance. 12 This offers a holistic comprehension of the ways in which HR practices and Islamic finance influence the success of organizations.13,14 Systematic reviews allow the identification of trends and gaps in the literature, enabling a comprehensive synthesis of perspectives across disciplines. 15 The method also highlights key contributors and offers a roadmap for future research.16,17 Despite the progress, some of the challenges are non-standardized HR practices that integrate Islamic values, which causes variability in talent management and ethical behavior.7,18 In addition, Islamic finance is at the evolution stage, which poses a challenge in terms of risk management and Sharia compliance of financial products 3. All these challenges require an in-depth analysis to provide viable strategies for the development of inclusive and ethical development in both HRM and Islamic finance. 19

More critically, research gaps still exist in exploring how Islamic financial principles relate to leadership, employee motivation, and ethical decision-making processes.1,5 The few available studies have generally relied on quantitative aspects of Islamic finance at the expense of discussing the role of HR strategies toward organizational culture and employee engagement.20,21 It is expected that addressing such gaps will contribute to the attainment of sustainable growth for organizations that abide by Islamic principles. 22 This paper presents a bibliometric review based on 402 academic articles, sourced between 2010 and 2024 from the Web of Science Core Collection. 3 With RStudio and VOSviewer, the study maps major themes, identifies gaps, and provides insights into future directions.1,17 By contributing to various academic and policy discussions, this research offers useful guidance both for HRM and Islamic finance practices.5,23

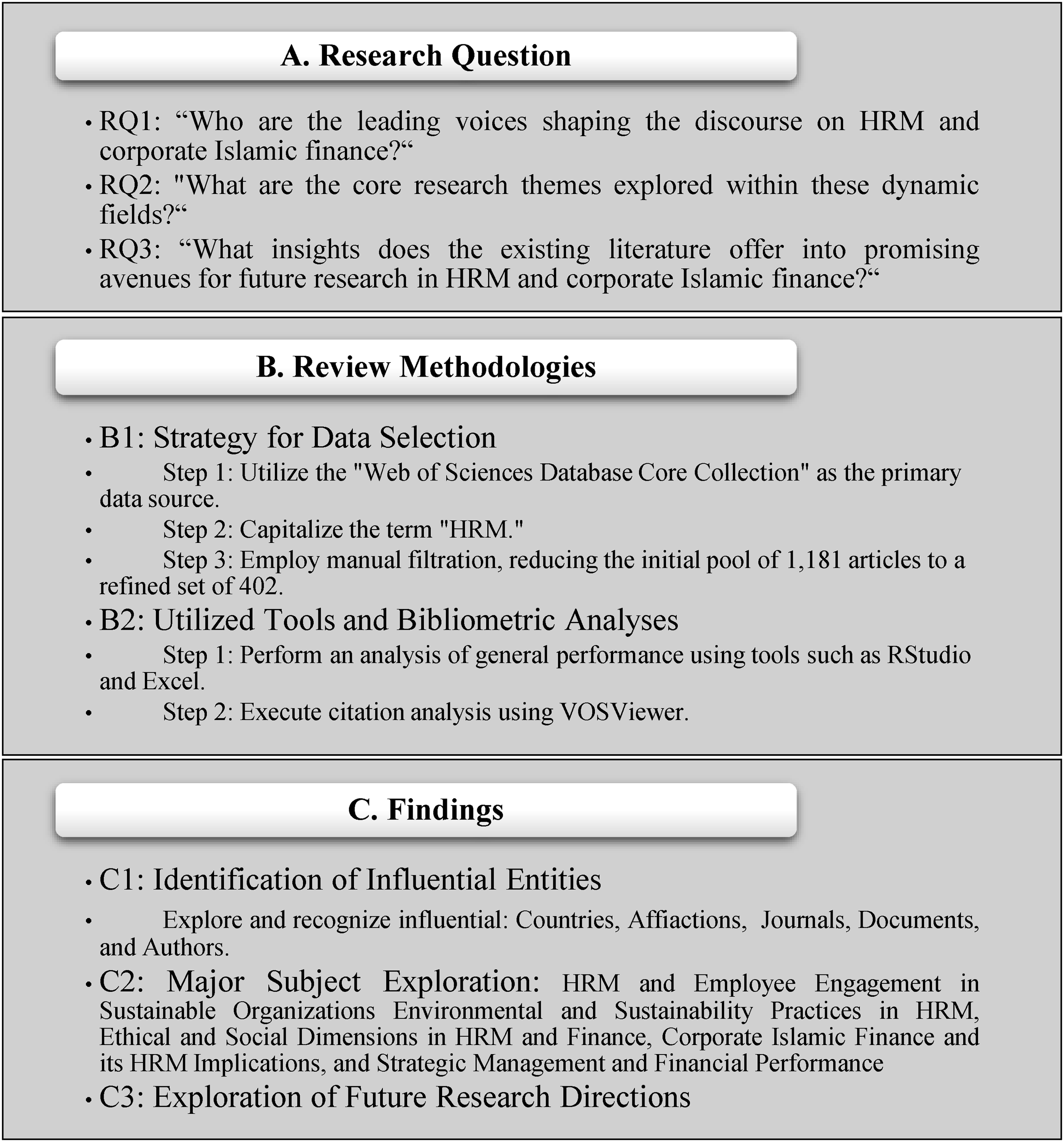

The research dwells on three important questions to tease out the complexity of HRM and corporate Islamic finance

5

: • Who are the influential players articulating the discourse of HRM and corporate Islamic finance? • What are the core research themes that have been addressed within these dynamic fields? • What does the extant literature tell us about the most promising avenues for future research in HRM and corporate Islamic finance?

Our review makes various unique contributions that light the way to further investigation and development in these important areas.3,25 By undertaking an in-depth analysis of key writers, identifying regional patterns of research, making links between academia and policy, and outlining a roadmap for future research, we seek to offer an informed and comprehensive overview of existing knowledge.1,17 This approach paves the way for a deeper understanding of the complex interplay between HRM and Islamic finance, ultimately leading to further exploration and advancement in these crucial fields. 5

In the subsequent sections, we delve deeper into our exploration of HRM and corporate Islamic finance. The Methodology section meticulously details the methodology employed in our research. The Findings section discusses in detail the results of both the bibliometric and content analyses of the selected research works. The Research Streams section elaborates on the research streams identified through the bibliometric evaluation. Lastly, the Conclusion section concludes the study by highlighting promising areas for future research within the domain of HRM and corporate Islamic finance. It provides a full-fledged informative analysis to shed light on the contemporary state of knowledge, thereby acting as a means toward further exploratory research in these dynamic fields.

Method

Following the case of Qudah et al., 26 the combined use of bibliometric analysis and content analysis became particularly common nowadays among scholars. In turn, during the bibliometric review stage, previous research is categorized into five distinct classes: descriptive, integrative, systematic, and meta-analysis reviews, as found by Hallinger, 27 Paul et al., 28 and Khan. 29 This multi-faceted approach allows for more profound insight into existing studies, their impact, and where the future lies. 30 Several studies in the chronology of time have indeed focused on the linkages between human resource management approaches and corporate Islamic finance that range from developing HR strategies in line with Islamic values and principles.31,32 Most importantly, during the 2010s, there has been increased interest in how Islamic finance principles affect HRM practices in aligning human resources policies with the Shariah principles and the influence this can have on organizational culture. 33

In this respect, it needs to be highlighted that the emphases on Green HRM and Environmental Performance in certain studies are actually a reflection of the evolving trend of integrating sustainability into HRM practices and increasingly is seen to conform to Islamic finance’s emphasis on ethical and sustainable practices. Islamic finance principles, anchored on social responsibility and ethical conduct, are thus a natural basis on which to extend the debate of how HRM can support environmental sustainability and greening in organizations. A growing literature focusing on Green HRM in Islamic financial institutions points to increased awareness of the need to align HRM with both Islamic ethical principles and environmental stewardship. 34 This extension of focus into Green HRM is not only relevant within the context of contemporary HR practices but also needed to explore how Islamic finance principles can support wider goals on sustainability.35,36

For example, Alqudah et al. 34 go on, in the 2020s, to explore in more detail how HRM practices might be used within Islamic financial institutions to motivate employees and manage performance, ensuring that any ethical issues were aligned with those of Islamic finance. This paper, together with bibliometric analyses that document the evolution of HRM practices within Islamic finance, maps trends and identifies emerging themes. Content analysis, in particular, shows how integrating HRM practices with Islamic finance principles comes into reality in practice, such as green and ethical HRM practices. 37 In general, this integrated approach shows significant advances and continuing challenges in aligning HR practices with Islamic financial principles that open avenues for future research and practical applications in these fields, specifically those focused on environmental performance and sustainability.36,37

Methodological framework

Figure 1 shows how our research uses the framework suggested by Paltrinieri et al.,

38

but it is tailored for the areas of human resource management and corporate Islamic finance. This approach unfolds in three distinct stages, each critical to achieving a thorough and insightful analysis. We develop the research questions in the first stage that are relevant to the scope, and thus, this forms the bedrock of the entire investigation into the HRM practices within the Islamic finance institutions.

26

This process ensures that the questions are well-aligned with the specificities of integrating HR strategies with Islamic principles.30,39 Research model.

Then, it is necessary to select literature for inclusion into the review with due carefulness to ensure the completeness of the sample and to reflect main ideas and variances of HRM and corporate Islamic finance in the research topic.31,32 This step becomes relevant within the understanding of how the principles of Islamic finance influence HRM practices regarding the motivation and performance management of employees. 33 Finally, we analyze selected literature to identify trends and insights that help in a greater understanding of the practical approach towards HRM practices followed in Islamic financial institutions based on the works of many scholars.34,40 This structured methodology, reflecting the framework given by Paltrinieri et al., 38 provides a robust basis on which to examine and make further advancements in this body of knowledge.

Methods of sampling

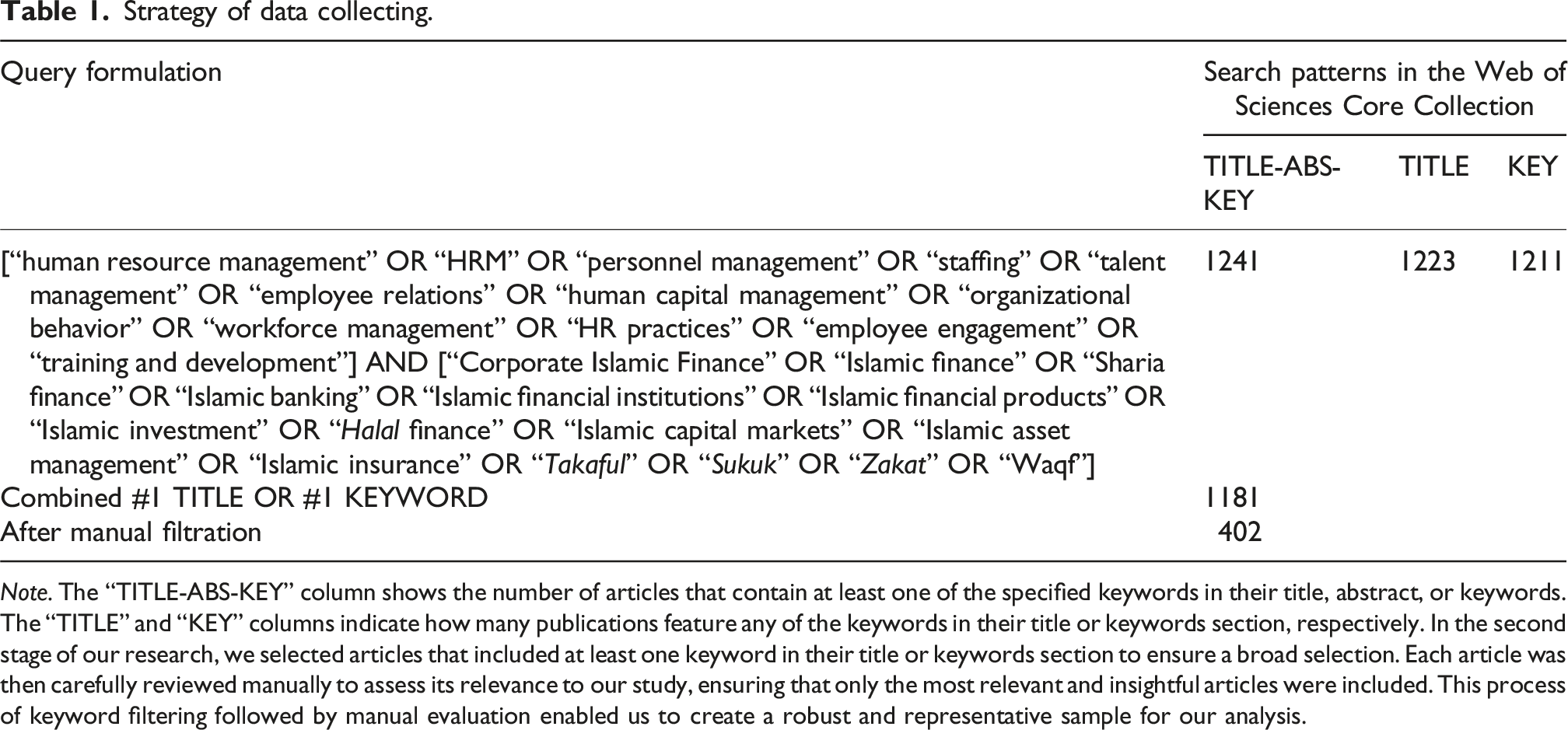

Strategy of data collecting.

Note. The “TITLE-ABS-KEY” column shows the number of articles that contain at least one of the specified keywords in their title, abstract, or keywords. The “TITLE” and “KEY” columns indicate how many publications feature any of the keywords in their title or keywords section, respectively. In the second stage of our research, we selected articles that included at least one keyword in their title or keywords section to ensure a broad selection. Each article was then carefully reviewed manually to assess its relevance to our study, ensuring that only the most relevant and insightful articles were included. This process of keyword filtering followed by manual evaluation enabled us to create a robust and representative sample for our analysis.

Following careful consideration, we chose the Web of Science Database Core Collection for our research, opting against other popular databases. The significant difference in the number of publications relevant to HRM and corporate Islamic finance drove this decision. 34 Compared to Scopus, which offers a limited 241 articles, the Web of Science Core Collection provides access to a vast 1181 publications, an undeniable advantage for our research. 42 Moreover, although Google Scholar has the largest collection, its inclusion of 798 unreviewed and poor-quality articles that lack scientific scrutiny made us suspicious, and we decided to exclude it from our choice.43,44 In order to identify the relevant publications in the selected database, we performed a careful analysis of keywords. Table 1 shows in detail the specific keywords, queries, and resulting search outputs before their further refinement by human intervention. 35 This multi-faceted approach allowed the creation of a comprehensive, representative sample for our review.

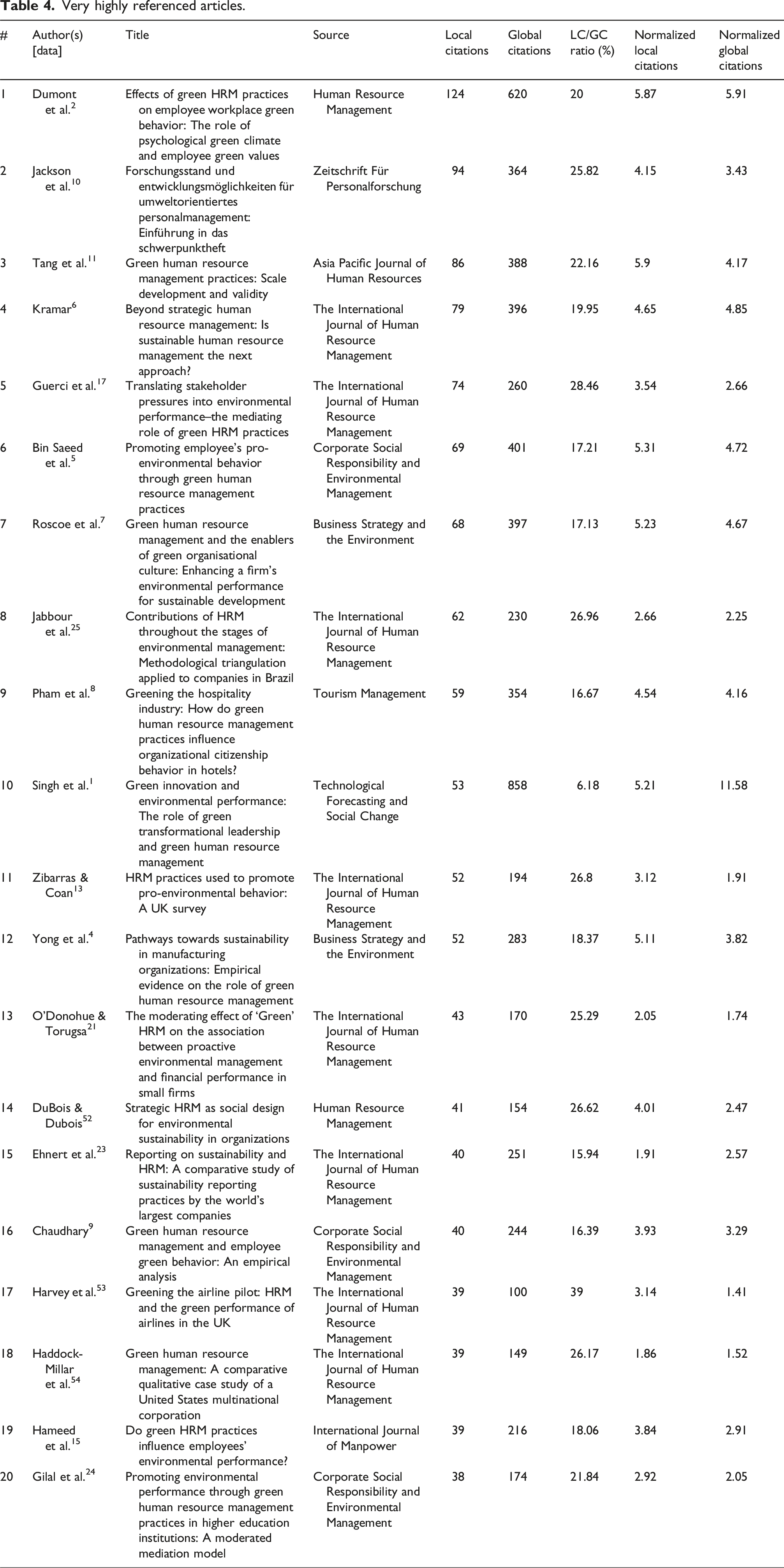

We have identified 1181 publications for bibliometric analysis in HRM and corporate Islamic finance for the period from 2010 to 2024. This period encompasses most of the critical changes that have taken place since the global financial crisis and reflects changing trends in globalization, digitization, and regulatory requirements that have affected these industries. Including 2024, this ensures the most recent trends and emerging insights are included. Table 4 highlights the 20 most cited articles that form the basis of insight into influential works in the field of HRM and corporate Islamic finance. These can be used to explore significant themes, trends, and future directions in these exciting fields and form a strategic foundation for further research and policy development.

Research instruments

To analyze the complexity of HRM and corporate Islamic finance, we utilize several powerful software tools that enhance our capability for analysis and answer our research questions with precision and depth. First, RStudio—an integrated development environment or IDE designed for R—is our main statistical analysis platform. Strong programming capabilities in R enable us to perform complex calculations, informative visualizations, and repetitive tasks efficiently and accurately during our research process in RStudio. Furthermore, VOSviewer extends this by allowing us to create and visualize bibliometric networks or “maps.” These interactive maps visually represent the intricate relationships between authors, sources, nations, and keywords within HRM and Islamic finance research. Recent studies by Qudah et al. 26 and Alqudah et al. 30 have explained in detail that with the help of algorithms made by Van Eck and Waltman45–48 and improved by Waltman et al., 49 one may analyze collaboration patterns, emerging keywords, and influential publications, which is very helpful and important for identifying the major contributors and showing hidden patterns in the corporate Islamic finance and HRM fields.30,32

Moreover, Excel—the generic spreadsheet software—finds great importance in arranging and manipulating numerical data in sets. We utilize advanced formulas and functions offered by Excel to systematically organize and analyze the data, execute calculations, and produce editable graphs and charts. This tool will support the clear and concise presentation of our findings, enhancing the accessibility and impact of our research [Microsoft, 2024]. An example of the use of Excel in structuring data in order to analyze it deeply is shown in references 40,41. Based on these combined uses, by the application of RStudio, VOSviewer, and Excel, we feel highly empowered to give a State-of-the-Art Analysis of HRM and Islamic Finance. It is expected, therefore, that the insights to be gained within this study would go toward underpinning future research and policy decisions in related areas, thereby helping to further the knowledge of these rapidly evolving fields.

Methodologies of analysis

Our analysis proceeds in three stages, each of which sheds light on important aspects of HRM and corporate Islamic finance research: overall performance, citations, and networks and content. The overall performance analysis provides an overview of the growth of the literature over time. First, this stage identifies key authors, countries, and institutions contributing to the field of HRM and Islamic finance. 26 It will, therefore, help us trace the development in research emphasis and the dominant players driving the field forward. The citation analysis delves deeper into the influential papers, authors, and journals. By identifying highly cited works, we gain substantial insights into the core knowledge and major themes shaping research in HRM and corporate Islamic finance. This process highlights how citation patterns reflect the priorities of emerging research trends. 30 Thus, citation analysis not only pinpoints influential studies but also helps trace the origins of current research directions.

On the other hand, network and content analysis use advanced techniques such as bibliographic coupling, co-citation, and co-occurrence to uncover hidden relationships and identify clusters of interconnected research. For instance, Al Karabsheh et al. 40 utilized similar methods to quantify the evolution of HRM and corporate Islamic finance practices, thereby enriching our understanding of the intellectual structure within HRM and Islamic finance research. The integration of these three phases will enable our study to provide a comprehensive, systematic understanding of the contemporary state of research in HRM and corporate Islamic finance. As a result, we develop salient insights, pinpoint significant contributors and emerging trends, and inform future research effort. Ultimately, this supports the development of better knowledge and the building up of sustainable and equitable practices for these critical areas.

Findings

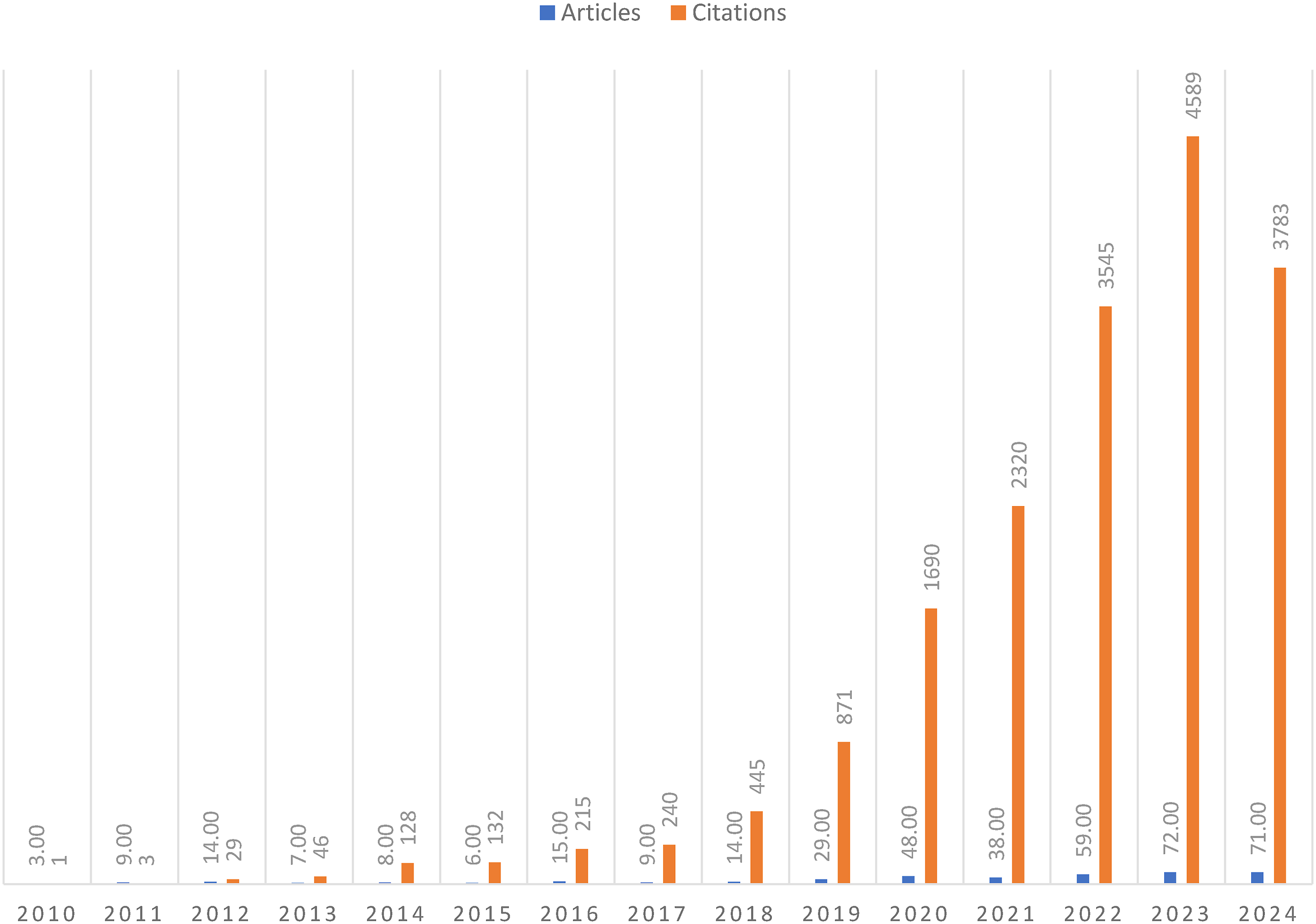

Figure 2 shows the annual trends in HRM and corporate Islamic finance literature between 2010 and 2024, with some turning points. In 2010, the area started with a small number of publications, with 6.80 citations per year, which means that the scientific interest was at its very beginning. While moving to the next years, there is an obvious upward trend in the number of publications and citation counts. This growth becomes more pronounced by 2014, with a total of 128 citations. Continuing this upward trend, from 2015 to 2018, the pace of research really picked up. In 2018, the series reached its peak at 445 citations, reflecting heightened academic engagement. However, from 2019 onwards, and even while the total number of citations has increased, the mean citations per article have slowly begun to decline. The total citations in 2020 reached 1,690, while the mean per article fell to 74.12, reflecting not only a broader publication base but less impact per article. This trend continued throughout 2021 and 2022 when the figures retreated to 38.39 and 31.24, respectively. For this same period, notwithstanding, the total citations grew higher and peaked at 3545 in 2022—a high-volume publication trait that underlined a growth characteristic. Corporate Islamic finance and HRM annual evolution of literature.

In 2023, the field reached an overall citation of 4,589, while the average citations per publication declined to 10.94. This reflects a movement toward higher numbers of publications whose impact is diluted. In the year 2024, the mean citations per article fell dramatically to 3.06, though the total citations were high at 3783. This ultimate decline suggests that saturation has reached the significant publications, thus underlining the nature of research in HRM and corporate Islamic finance with evolving focuses, varied influences, and shifting over time.

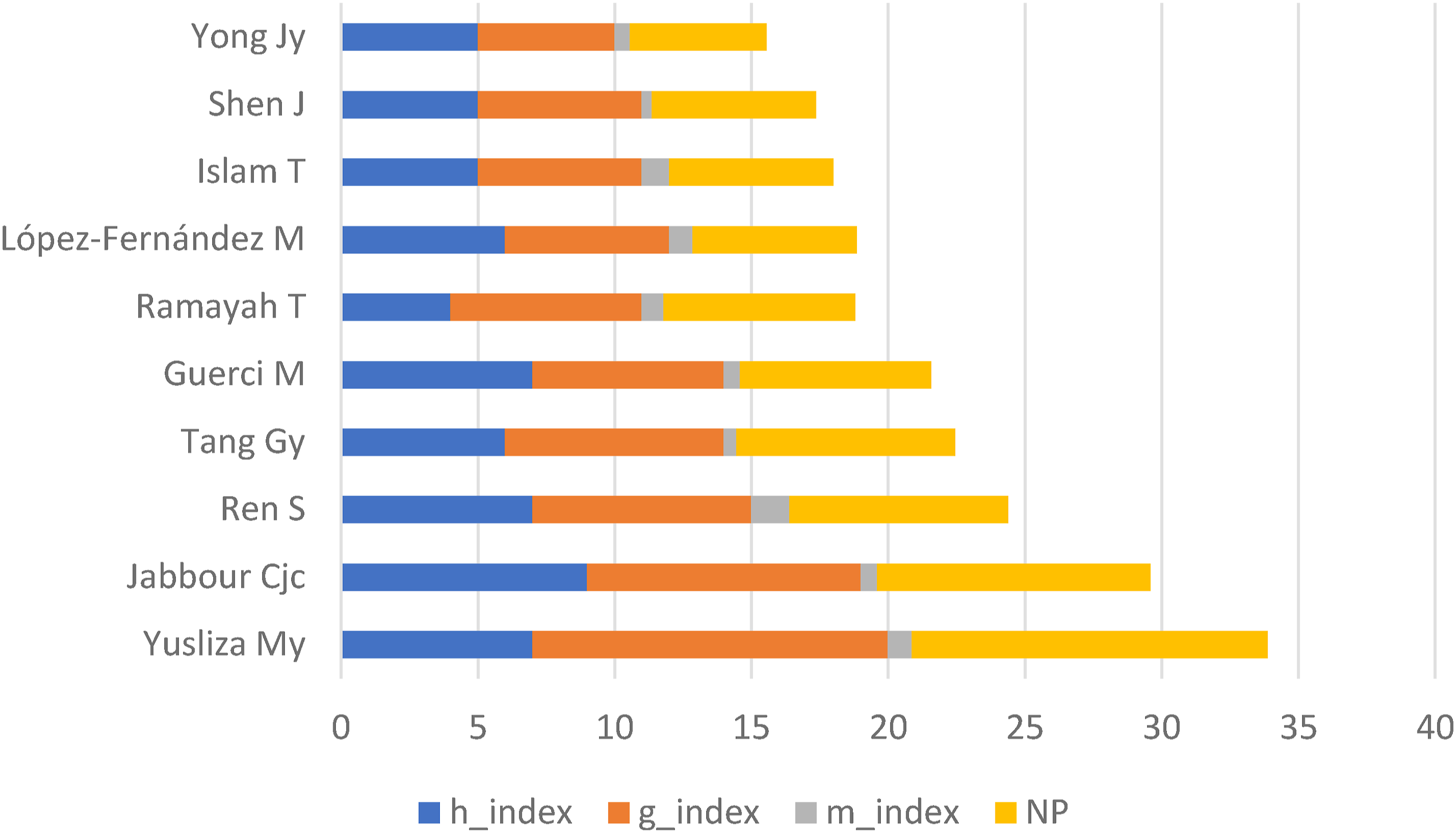

Figure 3 presents the detailed analysis of author productivity in HRM and corporate Islamic finance, using some key bibliometric indicators that have pointed to influential researchers. The first is Jabbour CJC, who has a very high productivity with an h-index of 9 and a g-index of 10. This author has acquired an impressive overall total of 1925 citations from 10 publications, having started his research in 2010. The long list of citations proves the continuous impact and superiority of the Journal over time. On the other hand, Yusliza My, with an h-index of 7, compensates with a better g-index of 13, showing an upward trend. Since 2017, I have accumulated 740 citations from 13 papers, reflecting a recent but significant contribution. Ren S., with an h-index of 7 and a g-index of 8, has accrued 305 citations for 8 works published since 2020. This relatively recent start supposes a promising trajectory in the field. With an h-index of 6 and a g-index of 8, Tang Gy has been cited 593 times from 8 papers he started working on in 2012, proof of Tang’s continued relevance and productivity. HRM and corporate Islamic finance top author productivity index.

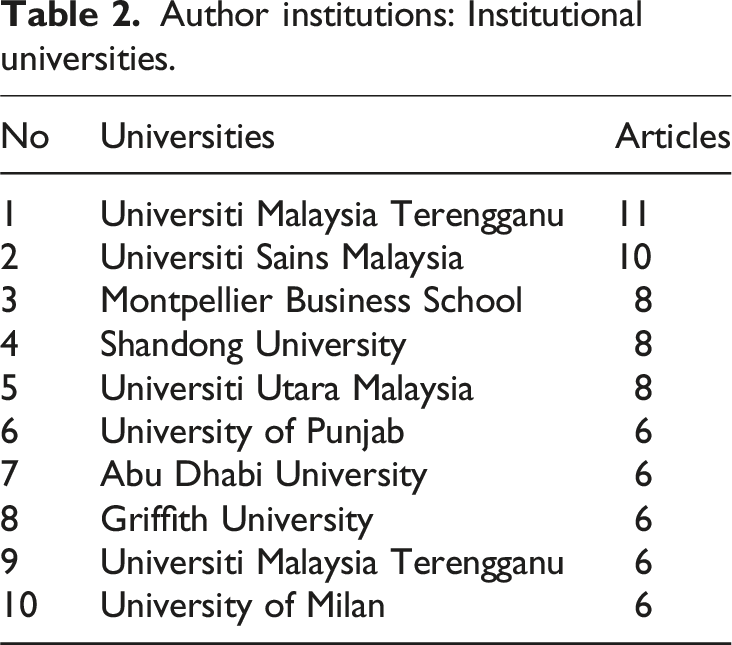

Author institutions: Institutional universities.

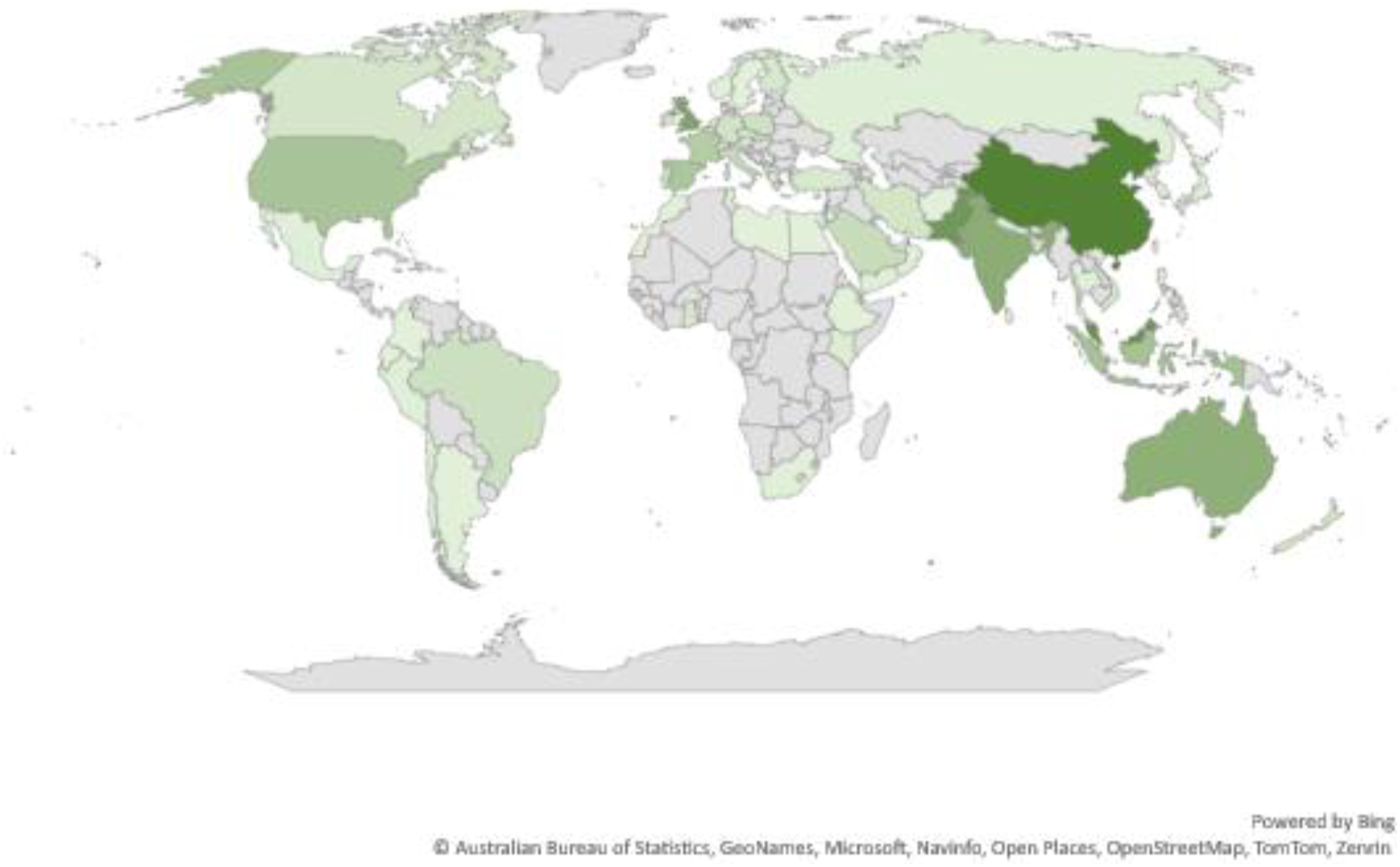

Figure 4 shows the world representation of research in the area of HRM and Islamic corporate finance. China maintains the lead in contributions: 112 articles, against Malaysia, which comes next with 96, and then Pakistan with 90 contributions. The United Kingdom is quite prominent, with 78; then India, 69; and Australia, 67. Other contributors like Indonesia contributed 48; the United States, 46; Spain, 43; and France had 36. In terms of citation impact, China is dominant with 2749 total citations, averaging 57.3 citations per article. Pakistan has a total of 1839 citations, averaging 51.1 citations per paper, whereas China had a higher number of articles published. Australia has the highest citation average per article [60.3 out of 1809 citations]. The United Kingdom is also doing well with regard to citations, with 1517 total citations and 63.2 citations per article. Global HRM and corporate Islamic finance research presence.

It can be observed that the United Arab Emirates, in the Middle East, has a great average of 195 citations, although it contributes only a small number of publications. Other countries, like Saudi Arabia and Lebanon, also had fewer articles but had impressive citation averages of 20.4 and 108, respectively. Collaboration trends of Chinese articles have a middle level internationally; there are 28 papers with multiple countries involved, and the multiple-country publication ratio is 0.583. Malaysia and Pakistan have MCP ratios of 0.567 and 0.528, respectively, reflecting high levels of cross-border research collaborations. This global distribution underlines a growing international interest in HRM and corporate Islamic finance research, with China, Malaysia, Pakistan, and a number of Western nations leading both in output and impact. In addition, regional research hubs, especially in the Middle East and Southeast Asia, also contribute to the development of the field.

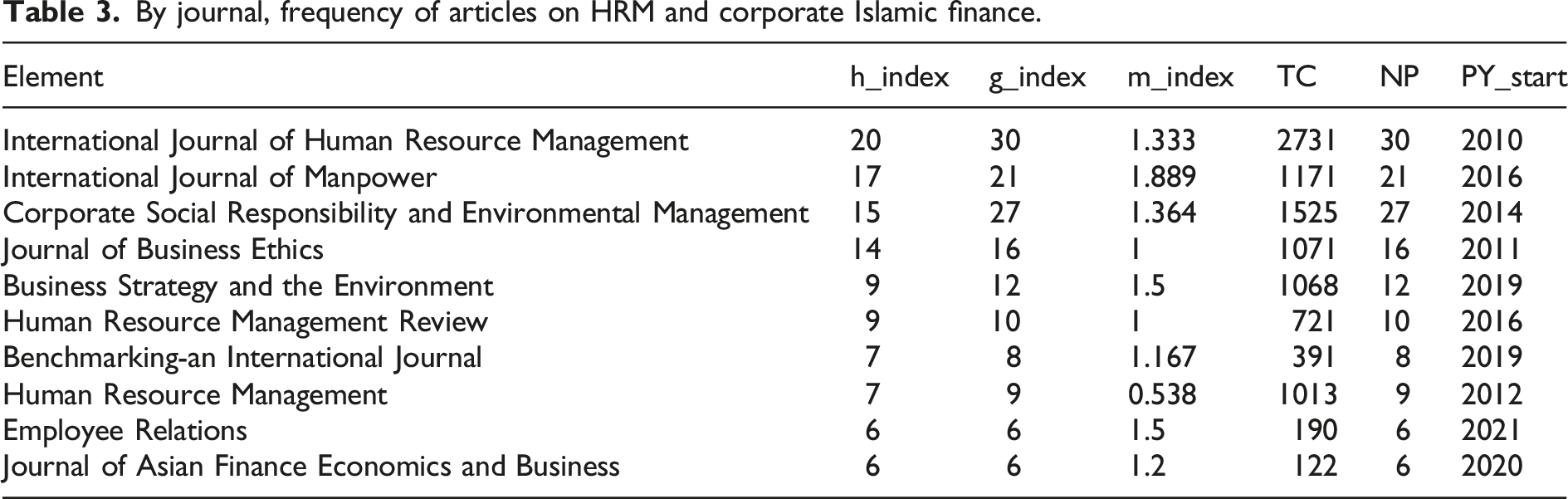

By journal, frequency of articles on HRM and corporate Islamic finance.

Citations’ analysis

Citation analysis is a technique for the analysis of bibliographic references 50. It established connections between scholarly works in the fields of human resource management [HRM] and corporate Islamic finance. Although its accuracy in assessing the quality of research articles has been debated, citation analysis remains an important tool in understanding the diffusion of influence of academic contributions in these disciplines. These concerns of potential bias come from the inclusion of negative citations, which refer to flawed research for critique, self-citations, and outdated references 51. Regardless of these criticisms, citation analysis is still a vital tool in assessing the research impact in HRM and corporate Islamic finance. It identifies key publications and provides insight into the status of knowledge concerning Islamic financial systems, the relevant Sharia-compliant HRM practices, and their links to corporate governance. It is thus, while realizing the limitation inherent in this analytical technique, an important tool to scholars in these fields in that it gives an insight into how their work contributes to Islamic corporate finance and management of human capital in line with Islamic principles.

Very highly referenced articles.

Jackson et al. 10 make a very valuable contribution to environmental HRM research, with 364 global and 94 local citations, hence giving an excellent LC/GC ratio of 25.82%, thus having a strong regional and scholarly influence. The International Journal of Human Resource Management is an important disseminator in green HRM research, such as Kramar, 6 Jabbour et al., 25 and Guerci et al., 17 whose works have generated significant citation impacts. Harvey et al., 53 with a 39% LC/GC ratio, present the high local impact of their work in greening airline pilots. The table indicates an increasing international awareness of green HRM research. High LC/GC ratios indicate that the works have impacts both locally and internationally that further the cause of sustainable HRM practices.

Content and network mapping tools

This section presents the research landscape in the field of HRM and corporate Islamic finance. By applying co-authorship patterns, citation relationships, bibliographical coupling, co-citation relationships, keywords, theme evolution, and hierarchical clustering methods, five different research streams have been identified. Such in-depth analysis provides much-needed insight into the existing status of research but at the same time pinpoints avenues for further research.

Cooperation in authorship analysis

Co-authorship in a research publication refers to the collaboration of multiple authors or organizations.

55

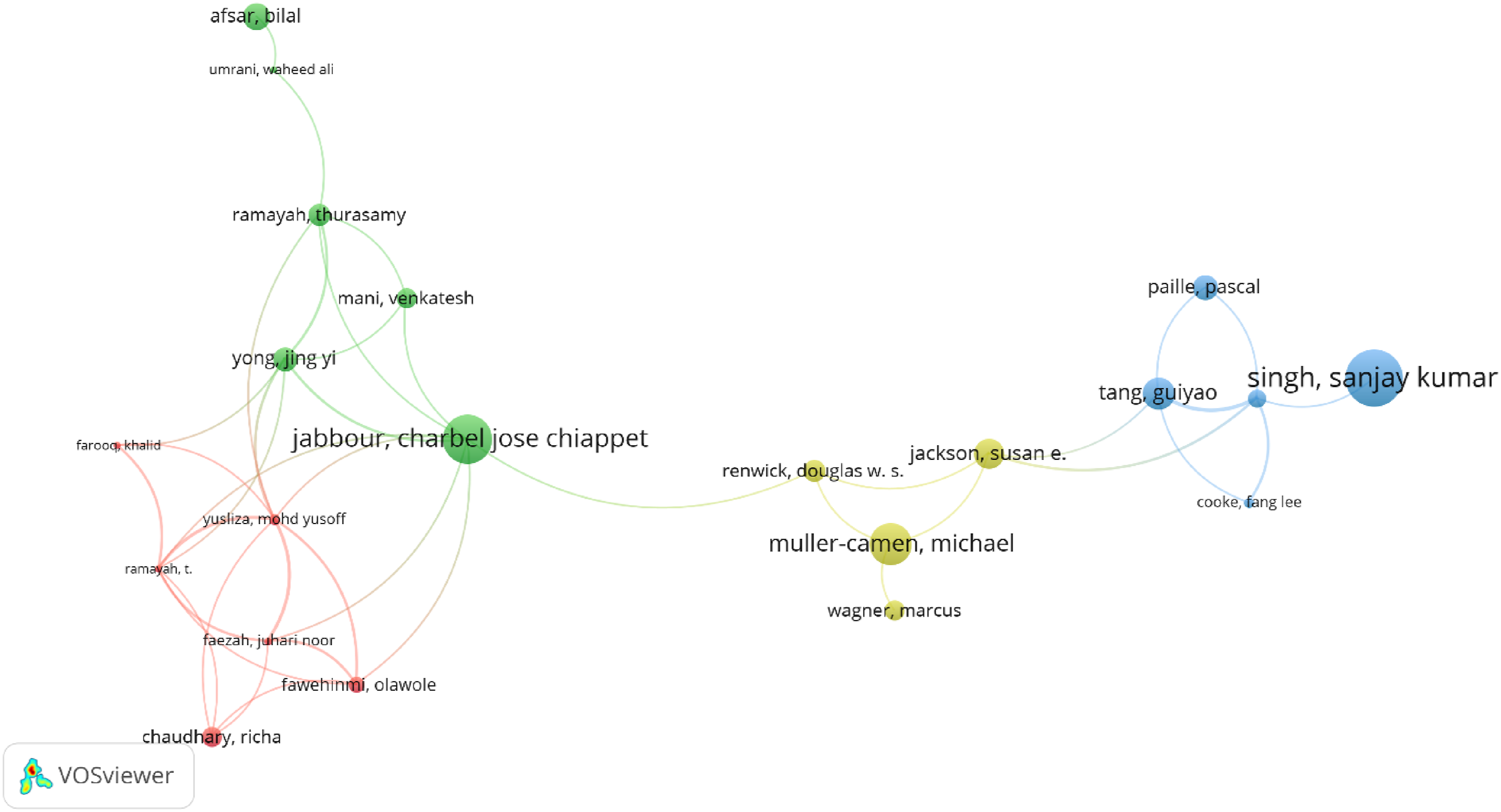

Co-authorships are important in developing and speeding up scientific progress. In our study, taking at least 3 citations, 16 source papers had combined connection strength of 35, indicating a moderate connection among them. The higher the connection strength of publications, the stronger is the relationship between the publication. Figure 5 depicts four clear co-authorship clusters as obtained from VOSviewer software, where each cluster is assigned a different color for easier visualization. The red cluster is dominated by Chaudhary and Richa and assumes an asterisk-like formation, which indicates that these authors are in high agreement and collaboration with one another. This cluster is very consistent, with average citations ranging between 154 and 1126. The rest of the co-authorship links outside this cluster are of average strength, which reflects a collaborative effort of authors from different geographical regions exploring various aspects of HRM and Corporate Islamic Finance. Co-authorship analysis.

Co-citation analysis

Using VOSviewer software, we performed a co-citation analysis to explore key themes within the HRM and Corporate Islamic Finance literature.

56

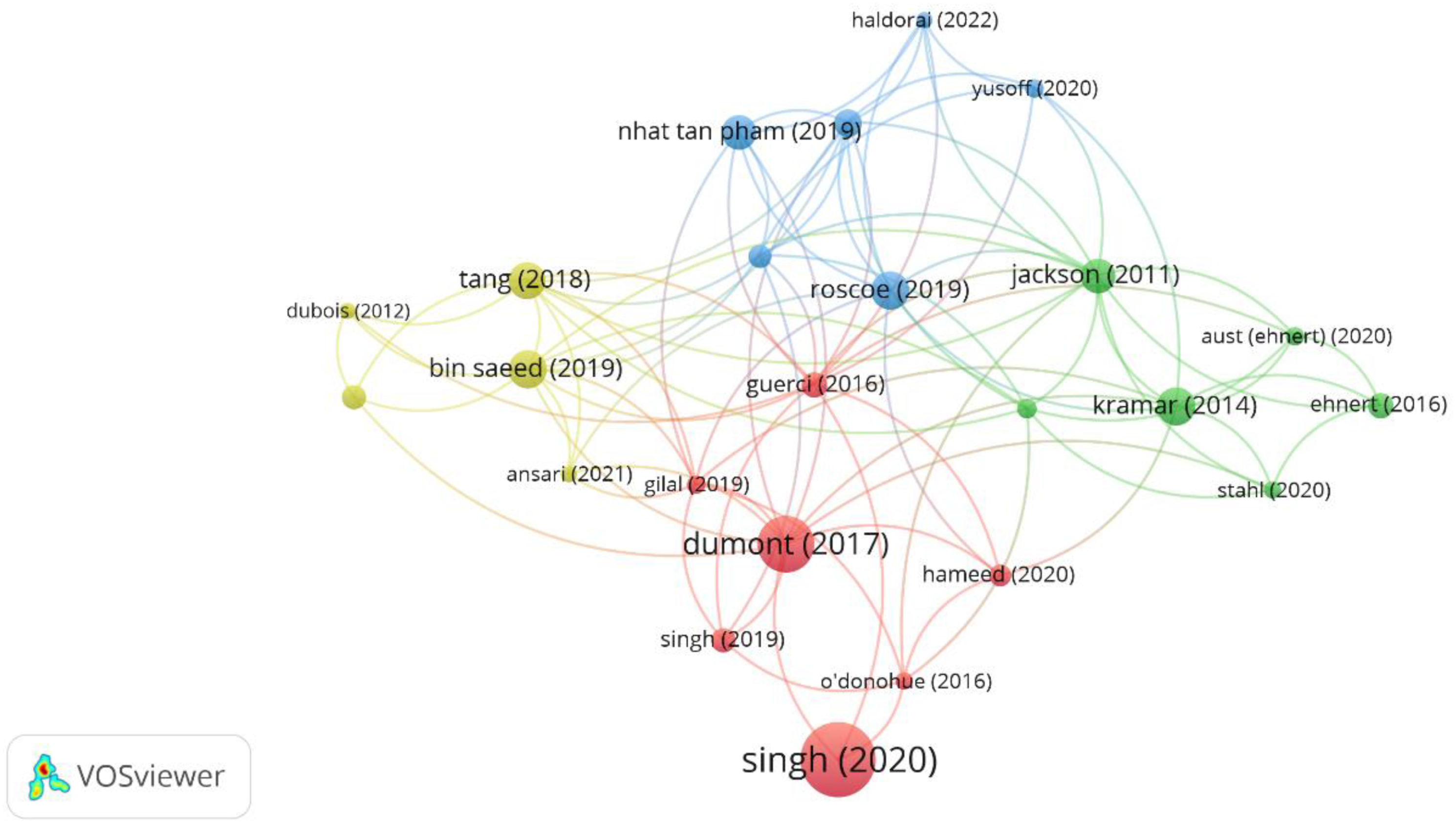

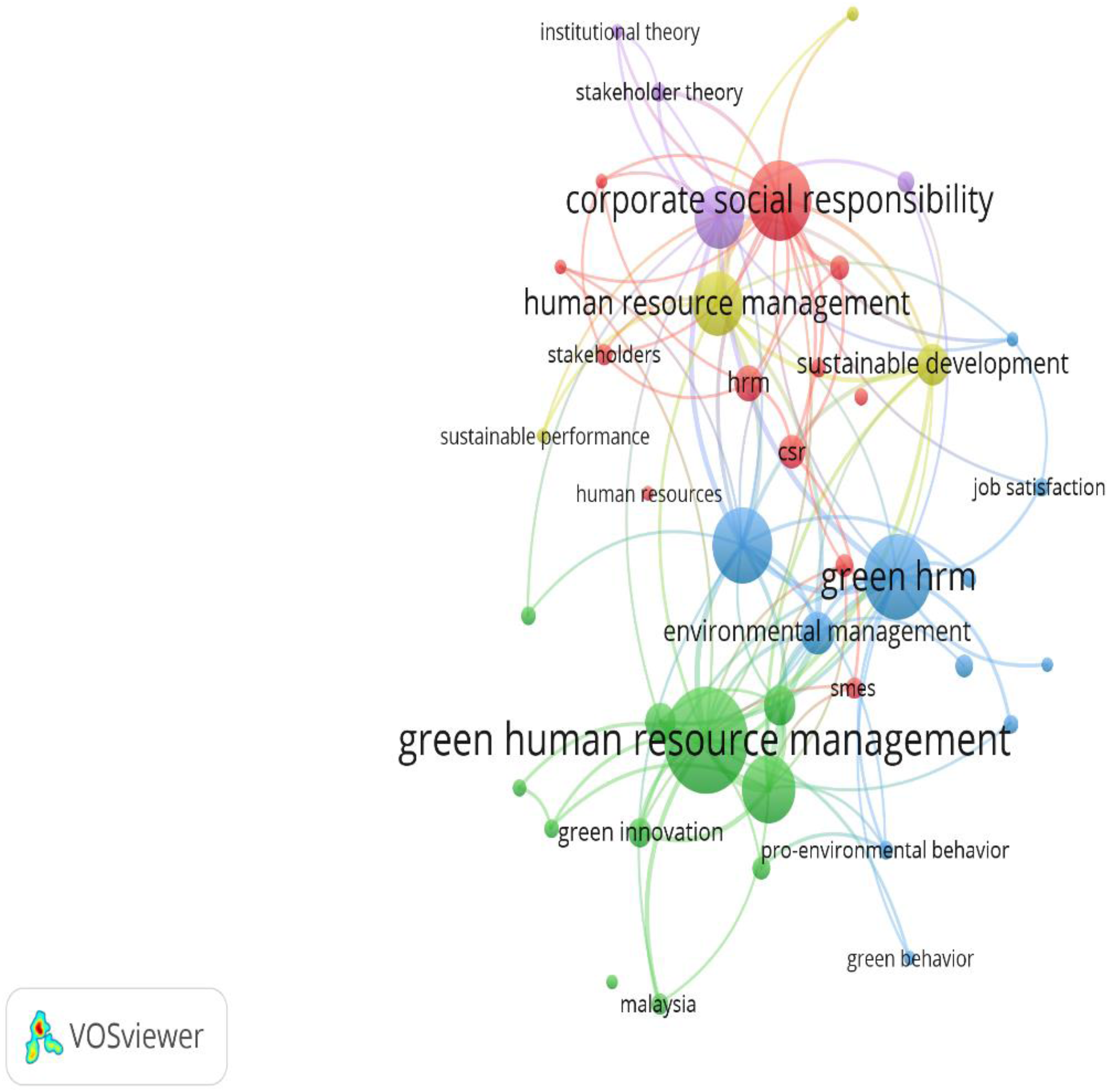

Co-citation analysis, a common method for clustering in large bibliographic datasets, identifies relationships between publications based on their shared citations to common sources. This approach enabled us to visualize the interconnections among research papers and delineate four distinct research clusters [see Figure 6]. Co-citation of documents.

By investigating the most frequently cited articles in our dataset, a number of key studies emerged. Of particular note are Singh’s 11 work on “Green Innovation and Environmental Performance: The Role of Green Transformational Leadership and Green Human Resource Management” and Dumont’s [2017] study on “Effects of Green HRM Practices on Employee Workplace Green Behavior: The Role of Psychological Green Climate and Employee Green Values.” Singh’s, with 858 citations, is outstanding, highlighting the effect of green HRM practices and leadership on environmental performance. Equally, Dumont’s work, with 620 citations, also puts a strong case for the role of green HRM practices in improving employee’s sustainability-related behaviors. These two studies are thus highly cited, showing the focused attention of the literature to the interlinkages that exist between green HRM practices and corporate environmental performance, which indicates a rising need for integrating sustainability into human resource management practices and which leadership can ensure by giving a lead for green organization culture. Co-citation patterns reflect that much of the research in HRM and corporate Islamic finance revolves around these themes, demonstrating a strong scholarly interest in the nexus between HRM practices and environmental sustainability.

Bibliographic coupling analysis

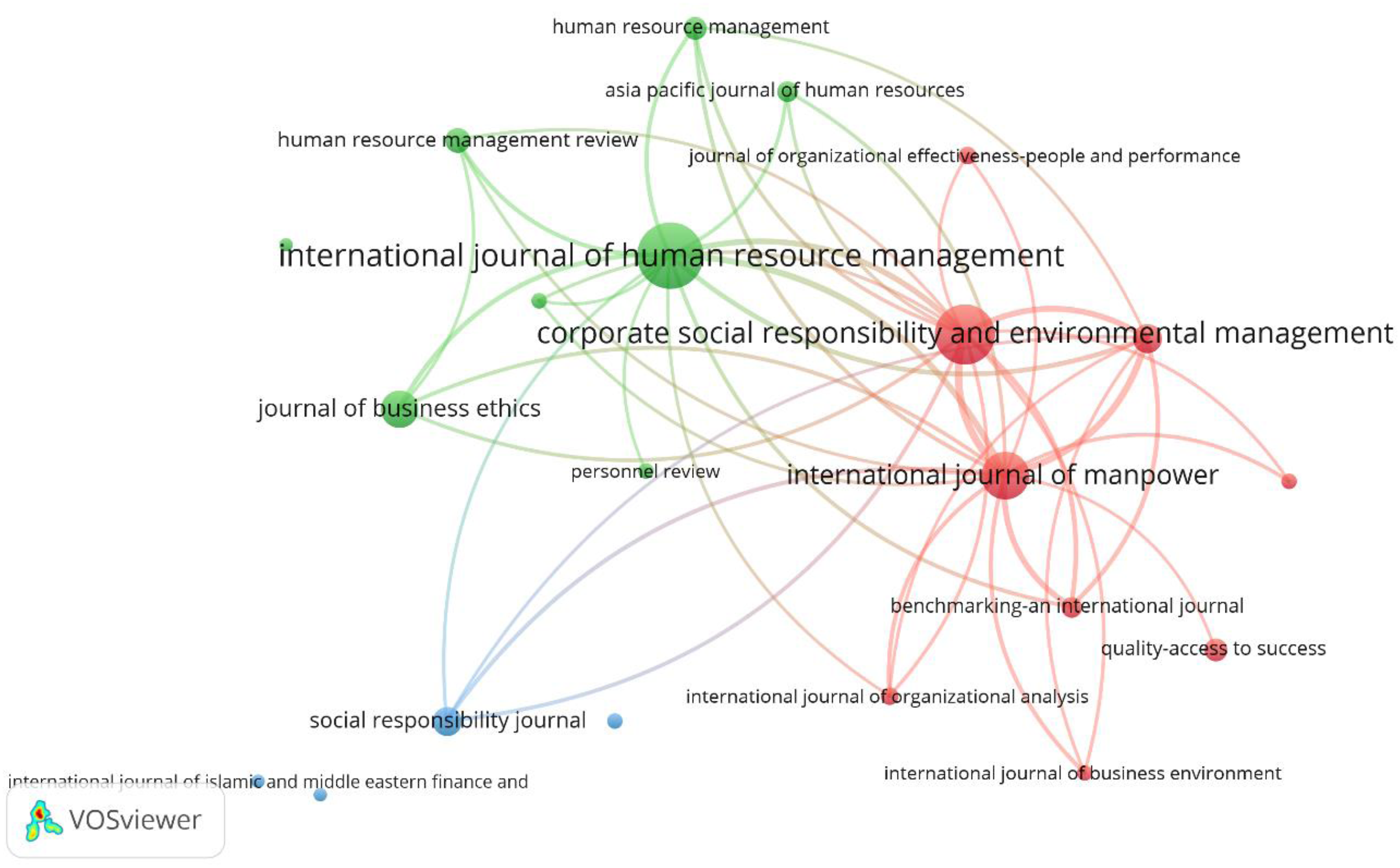

Figure 7 shows clusters of journals in which Corporate Islamic Finance and HRM are interested. The groups have been identified using the VOSviewer software and the criteria set by Paltrinieri et al.

38

Limiting the number of citations per source to five this method ensures that within such a visualization, robust clusters will form. The International Journal of Human Resource Management is the most representative of the green cluster, having strong links with the Journal of Business Ethics and the Human Resource Management Review. Large links in this cluster indicate that these journals are very important in the HRM arena. Bibliographical relationship of journals.

The Business Strategy and Environment journal occupies the central position in the red cluster, while it is also closely connected with the International Journal of Islamic and Middle Eastern Finance and Management. This would show strong thematic coherence between HRM and corporate Islamic finance, underlining their junction with environmental and strategic business considerations. The blue cluster, containing both the Journal of Islamic Marketing and the Journal of Organizational Effectiveness: People and Performance, demonstrates strong relatedness with articles on Islamic finance practices. However, connections with other clusters remain fairly weak, which testifies to a rather more specialist agenda within this cluster around integrating Islamic principles into HRM practices. What Figure 7 shows, finally, is the powerful role played by key journals in the development of discourse within HRM and corporate Islamic finance. From this analysis, one is able to identify strong links and thematic connections between a variety of publications, gaining insight into the major academic outlets and possible avenues for future research and collaboration within these fields.

Co-citation analysis

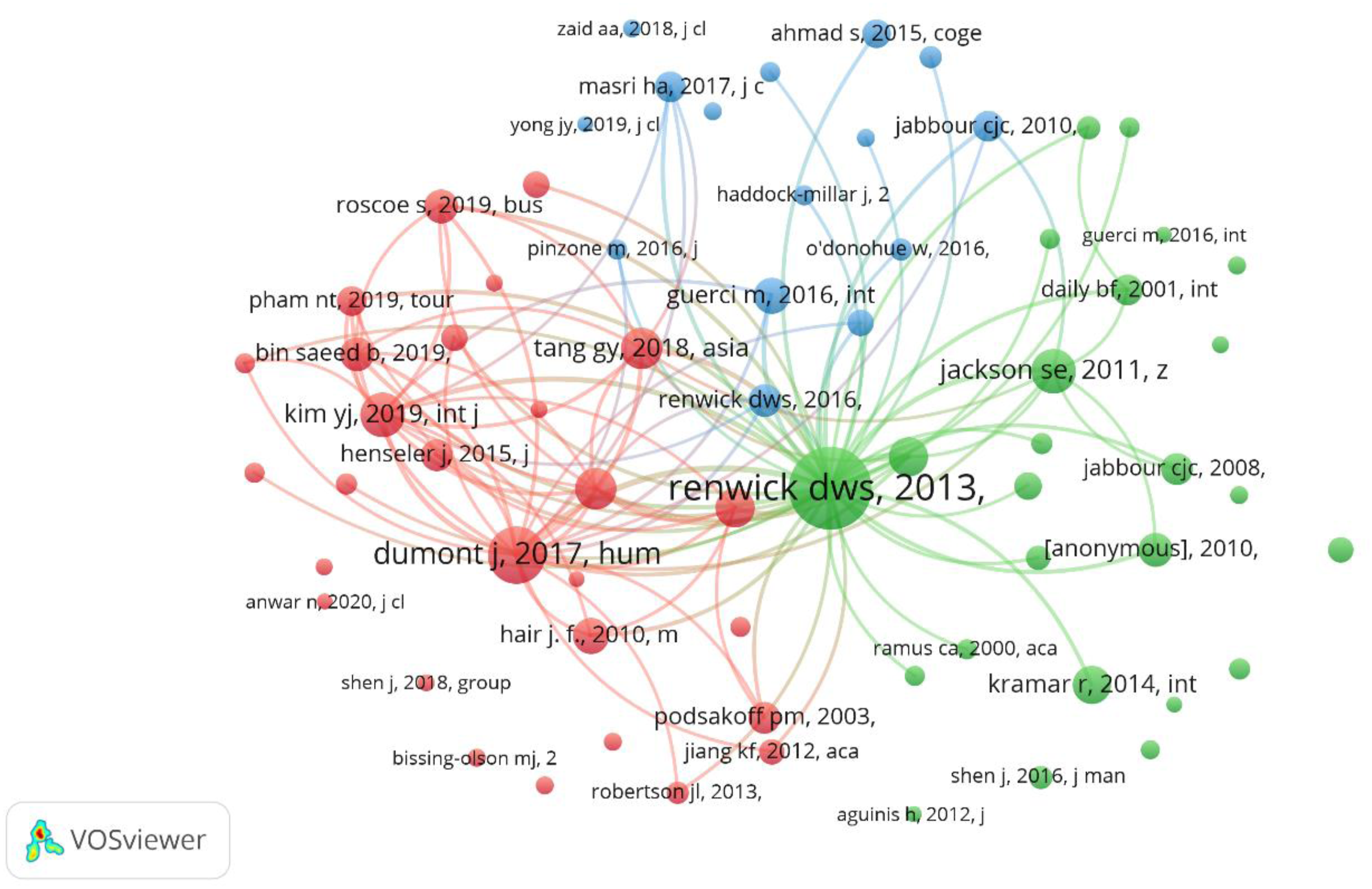

Co-citation analysis, a technique detailed by Boyack and Klavans, 51 involves examining pairs of papers cited together to uncover research streams and assess their connections. Applying a citation threshold of three, we identified four distinct clusters within a network of 45 publications focusing on human resource management [HRM] and corporate Islamic finance.

Figure 8 shows that the red cluster, although works such as reference 2 show weak relations with both the blue and green clusters, the latter two are strongly correlated. The blue cluster shows influential studies in HRM such as those by Guerci et al.

17

and Renwick et al.,

57

intersects significantly with the green cluster. This overlap indicates a strong convergence of themes, which represents a new line of research that seeks ways to inculcate sustainability into the HRM strategies of Islamic finance institutions. Such an understanding highlights the links in current research trends and thus helps direct future investigations into impactful areas at the crossroads of HRM and corporate Islamic finance. Reference co-citation.

Keywords analysis

The first keyword analysis that we conducted was at the threshold of 6 occurrences, and the outcome provided very little insight. So, we adjusted the threshold to 6 to give a better insight into pattern disclosure. Figure 9 shows the more distinct clusters obtained from this method that uncovered five research fields from HRM and Corporate Islamic Finance. Co-occurrence.

This comprehensive review thus has both keyword review and the identification of clusters, and it indeed offers an overview of the main trends of research in this area. From a thematic standpoint, research on HRM and corporate Islamic finance falls into five main categories, namely, HRM and Employee Engagement in Sustainable Organization; Environmental and Sustainability Practices in HRM, Ethical and Social Dimensions in HRM and Finance; Corporate Islamic Finance and its Implications for HRM; and Strategic Management and Financial Performance.

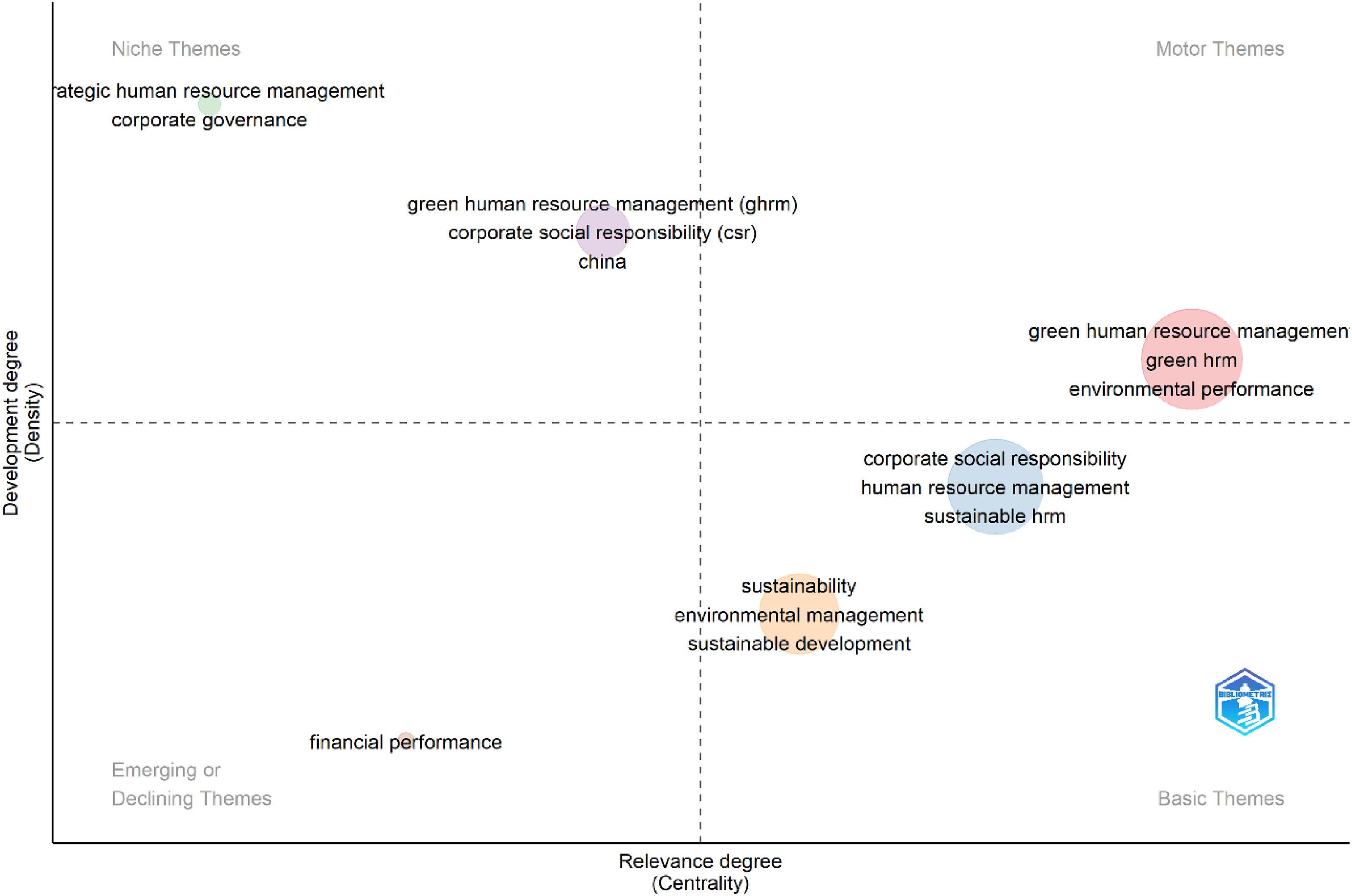

Thematic evolution

Figure 10, on the thematic evolution of literature on human resource management-HRM and corporate Islamic finance, is an interlinked web of emerging themes with established areas in the field. The figure depicts a granular breakdown of clusters based on keyword occurrences and centrality metrics that point to dynamic evolution in research topics. The cluster named “Green Human Resource Management” [HRM] brings into focus such critical issues as “Green HRM,” “Environmental Performance,” and “Green Innovation,” thus showing the increasing emphasis on integrating environmental sustainability into HR processes. Key keywords were “environmental sustainability” and “green human resource management practices,” focusing on eco-friendly behavior and sustainable practices inside enterprises. The high betweenness centrality scores for concepts like “environmental performance” and “green HRM” suggest that these concepts act as important bridges within the larger HRM literature. Thematic evolution.

The cluster “Corporate Social Responsibility” reflects an emphasis on CSR, which has been identified as playing a major role in enhancing organizational performance and stakeholder relationships. The emergence of such keywords as “corporate social responsibility,” “sustainable HRM,” and “stakeholder theory” attests to the significant relation between CSR practices and strategic HR management. This cluster highlights the growing integration of CSR practices in the context of HR strategies for sustainable development and ethics. The last cluster, “Sustainability,” reflects the broader debate on sustainability in both HRM and corporate Islamic finance. Terms such as “sustainable development,” “environmental management,” and “innovation” are part of this cluster. The high frequency and centrality of these terms indicate an increasing awareness of sustainability as an integral element of organizational strategy and performance. Figure 10 sums up that the thematic evolution in human resource management and corporate Islamic finance reflects a shift of integrating sustainability and CSR in core organizational practices.

Research domains and anticipated research questions

Domain 1: HRM and employee engagement in sustainable organizations

In the framework of human resource management and employee engagement in sustainable organizations, the integration of Islamic finance principles gives a new light to HR practices. The prohibition of [Riba] and [Gharar] indicates the core principles of fairness and transparency within HR practices. The same principle gives support for compensation systems that are clearly and equitably framed in a way to minimize conflict and increase mutual trust.1,2,58,59 The principles of Mudarabah (profit-sharing) and Musharakah (partnership) encourage a team-oriented work environment, as employee interests are combined with organizational objectives through sharing profits and risks, leading to increased commitment and loyalty 5; 7. Also, Murabahah (cost-plus financing) and Ijarah (leasing) practices, where the terms and conditions are fixed, contribute to sustainable HRM by providing clarity in the employment contract and benefits, hence minimizing the potential for conflict 6; 11; 60; 61. Instruments like [Sukuk] (Islamic bonds) and [Takaful] (Islamic insurance) play a role in providing financial stability and effective risk management within organizations, enabling the development of strong HR policies that support long-term employee engagement and welfare.8,10,63

The principle of [Zakat] or charitable giving, on the other hand, motivates an organization to invest in employees’ welfare and community development initiatives, thus creating a culture of corporate social responsibility and ethics within the workplace.4,17 Avoiding [Haram] or prohibited practices ensures that HRM strategies remain aligned with ethical standards and cultural values, reinforcing employee trust and organizational loyalty.3,23,64 In a nutshell, the integration of Islamic finance principles into HRM practices is not only congenial with ethical and religious values but also ensures the sustainability of a work environment that is engaging. This concept enhances transparency, cooperation, and social responsibility, each of which plays a major role in developing appropriate and effective sustainable HRM strategies for modern organizations.9,14,25

Domain 2: Environmental and sustainability practices in HRM

The integration of Islamic finance principles into the practices of HRM, especially on sustainability, exposes a complex interrelationship between financial ethics and environmental stewardship. First, Islamic finance disallows Riba-usury and Gharar-excessive uncertainty and thus puts much emphasis on fairness and transparency in human resource management practices that ensure environmental sustainability.1,64 For example, Mudarabah represent equity and shared benefit principles that can be coupled with green HRM initiatives toward improved environmental performance and employee commitment.2,5,65 Organizations can embed the concept of mutual benefit and fairness into their culture through such principles, which might inspire employee involvement in any green-related initiative. Besides, Murabahah cost-plus financing and Ijarah leasing set a frame in which financial transactions occur in a transparent and honest way. These principles can be incorporated into the HRM strategies to support green human resource management, such as green training programs and environmentally friendly recruitment processes. 7 In this case, HRM practices will not only be in compliance with Sharia but will also contribute to the organizational sustainability by encouraging employees towards environmentally responsible behavior.11,66 The use of Sukuk—Islamic bonds—further indicates this commitment by providing the opportunity for organizations to fund green projects while remaining within the guidelines of Sharia, thus improving their environmental performance. 6

Also, Takaful and Zakat show the Islamic concern for social responsibility and the care of one’s brothers. An organization can capitalize on such principles in order to enrich corporate social responsibility and institute a culture of sustainability.4,8 With Takaful and Zakat, an organization might give support to green initiatives or community welfare, thus managing to bring its operational strategies in line with ethical and religious values. This will allow the company to conform to the standpoints of Halal not only but also improve the commitment for environmental and social responsibilities.3,17,67 In other words, human resource practices combined with Islamic finance principles, avoiding activities of Hara’m, and strict adherence to the requirements provided by Sharia have a bearing on increased organizational sustainability and ensuring employee integrations. This is very significant in formulating a broad green HRM strategy that would be supportive of environmental performance and ethical business considerations.20,23 This would mean the combination of such principles, establishing a sustainable and ethically sound HRM framework for long-term success and impact.68,69

Domain 3: Ethical and social dimensions in HRM and finance

Islamic finance principles profoundly influence the ethical and social dimensions of human resource management [HRM], shaping sustainable HRM practices in distinctive ways. For example, the ban on Riba [interest] and Gharar [too much uncertainty] means that HR practices must be open and fair, pay systems must be fair, and conflicts must be kept to a minimum.1,70,71 The transparency extends to the employment contract itself, whereby concepts like Mudarabah and Musharakah create a partnership between employees and employers, giving employees a mutual interest in the success of the organization, hence improving employee engagement.2,9,72 Besides, Murabahah and Ijarah highlight clear terms and conditions, which are critical for creating well-defined and mutually agreed-upon employment terms. These practices support sustainable HRM by ensuring that the employment agreements are transparent, hence reducing friction and improving job satisfaction while supporting sustainable HRM.5,11 Sukuk [Islamic bonds] and Takaful [Islamic insurance] provide financial stability and risk management, which is important to developing HR policies that support long-term welfare and engagement of employees.8,10

Moreover, Zakat [almsgiving] enhances organizational responsibility to invest in employee welfare as well as community development. This concept concurs with the greater objectives of CSR in cultivating a trend of social responsibility and ethics in the workplace.4,17,73 Similarly, obedience to the concept of Halal practices also guarantees that human resource strategies will be implemented ethically in a culturally correct manner in order to develop trust and loyalty among the employees themselves.3,23 In all, the integration of Islamic finance principles into HRM not only makes human resource practices ethical and in line with religious values but also helps to develop a sustainable and engaging working environment. Fairness and transparency are focused on by Riba and Gharar; Mudarabah and Musharakah develop collaboration, while Murabaha and Ijarah develop transparent agreements. Sukuk and Takaful give stability, while Zakat arouses social responsibility. Following Halal, abstaining from Haram, also ensures that the HRM strategies will be ethical and culturally sensitive.9,14,25

Domain 4: Corporate Islamic finance and its HRM implications

This fact manifests that corporate Islamic finance principles being integrated within HRM do indeed mark a subtle convergence of religious, ethical, and financial concerns. This ban therefore affects how HRM functions by drawing attention to the good morals and social ethics that the financial activity of organizations needs to maintain conformity with 74,75. The effect is even bigger for Murabahah and Ijarah since these products require transparency of transaction and its Sharia compliance. This makes sure that employees know about and follow these financial rules. 5 Fairness and inclusivity HRM strategies can mirror the broader commitment to ethical financial practices and risk-sharing reflected in the use of Sukuk and Takaful.7,76

In addition, the principles of Zakat and Takaful imply social responsibility and community sharing, which is an essential ingredient in work environment development and employee engagement improvement. 6 The prohibition of Gharar, or excessive uncertainty, demands clarity and equity in the HRM policies and practices, which implies transparency and fairness of employment terms and conditions. 11 Additionally, Halal and Haram differentiation guides the ethical boundary in which HRM functions have to be performed within the organization, including recruitment and employee benefits, according to Islamic principles. 10 It aids in nurturing a workplace culture that is respectful of, and inculcates, Islamic values into daily HRM practices.8,77 The infusion of these principles into HRM necessitates a strategic process by which organizational goals are made to align with those of Islamic finance. This involves embedding the ethical practices into HR policies and fostering green and socially responsible behaviors while ensuring compliance to Islamic and secular regulations.14,25 In other words, as a result of religious adherence, the organizations not only follow religious requirements but have enhanced overall sustainability and improved ethical performance. 78

Domain 5: Strategic management and financial performance

It thus considers the impact of strategic management and financial performance on/through the principles of Islamic finance within HRM. The principles of Islamic finance clearly reject Riba, or interest, thereby influencing HRM to shy away from debt-based financing, which can lower financial performance metrics.14,77 Mudarabah and Musharakah, on the other hand, facilitate profit-sharing and joint venture contracts. These can be aligned with strategic HRM objectives, as they encourage integrative business practices and shared financial rewards, which can affect the bottom line of the organization. 2 Murabahah is a cost-plus financing structure. It is a legitimate option to traditional interest-based loans, thus easing investment in such HRM projects that align with Sharia law.7,68 Ijarah, or leasing, and Sukuk, or Islamic bonds, further extend the avenues of financial management in such a way that organizations can finance HRM projects while remaining within the boundaries of Islamic dictates. 6 Takaful, an Islamic model of insurance, supports the HRM through risk-sharing mechanisms that could improve employee benefits and organizational stability.11,72

While zakat necessarily calls for the distribution of wealth and, therefore, may have an impact on organizational strategy and HRM practices as it encourages corporate social responsibility and community support, with an effect on employee morale and organizational reputation. 8 In contrast, Gharar, or excessive uncertainty, and Haram, or prohibited activities, need to be taken into consideration by the HRM strategies to avoid unethical or Sharia-non-compliant practices. 10 Such alignment of HRM practices with Halal principles secures activities within what is permissible under Islamic law, therefore enhancing organizational legitimacy and employee trust.4,69 The strategic practice of such principles will help improve financial performance through compliance and an ethical work environment that fosters the objectives of both organizations and employees alike.17,73 So, combining Sharia-compliant money management with strategic human resource management can help an organization do better and last longer, while also following the moral and legal rules of Islamic finance.3,23

Agenda of future research developments

Set focus on some of the arising areas in which future studies on human resource management and Islamic finance may be focused: the use of new, developing technologies, including artificial intelligence, blockchain, and large amounts of information in practices associated with human resource management and Islamic finance. Understanding how these technologies influence efficiency and effectiveness can help researchers get valuable insights into their potential benefits and challenges.1,74–76 Cross-cultural and regional studies will also be able to show how different cultural contexts shape HRM and Islamic finance practices. This is particularly relevant in comparative studies between Western and Islamic finance systems, which may indicate how different cultural frameworks influence financial practices and HRM strategies. 2 The evolving regulatory environment also provides a critical area of research, given the importance of a focus on how new regulations affect organizational performance and compliance.5,10,70

Furthermore, the increasing focus on sustainability and ethics provides a clear rationale for the examination of the status of adoption and the effects of green HRM and ethical Islamic finance practices on organizational culture and environmental performance.7,68 Longitudinal studies that follow how these practices change over time can provide information on long-term trends and emerging challenges. In this context, interdisciplinary approaches that draw on insights from HRM, Islamic finance, and cognate disciplines such as economics and sociology can offer holistic perspectives. 6 There is a need to study the influence of global events such as economic crises and pandemics on organizational practices and financial performance.11,66 The final research gap is how policy recommendations are translated into actual implementations in HRM and Islamic finance to improve outcomes and reduce challenges.10,60 This, if pursued, would result in better understanding and practices in the future in both areas.

With the continuous change in the landscape of HRM and corporate Islamic finance, there is a dire need for future research to tackle emerging trends and gaps in existing literature. For example, there is a need for studies that will seek to determine how Islamic finance principles are combined with HRM practices. This includes the study of how certain Islamic finance instruments, such as Sukuk and Takaful, can be utilized to improve employee engagement, welfare, and organizational sustainability.8,61 Furthermore, the practical implications of these financial tools on HR policies need to be explored, especially in terms of how financial stability can be combined with ethical practices and employee benefits.4,59 In addition, the study of the impact of Islamic finance on green HRM practices may indicate how the principles of finance support environmental sustainability and corporate social responsibility [CSR].17,62

There is also a need for empirical studies that investigate the performance of Islamic finance-driven HRM strategies at various levels of organizational contexts and, to what extent they affect employees’ satisfaction, retention, and overall organizational performance.3,74 Future research can derive critical lessons to be learnt in areas where such implementations were missing, by assessing gaps in these areas and can significantly contribute to strategic implementations of Islamic finance principles for the advancement of equitable and sustainable HRM practices.23,63–65 Another critical area of future research pertains to developing frameworks that integrate the Islamic finance principles with strategic management and financial performance metrics. How these principles influence strategic decision-making and financial outcomes is of vital importance to understanding their wider effects on organizational success.9,70 Moreover, the studies should focus on how principles such as Mudarabah or Musharakah may inspire cooperation in business activities and improve financial performance accordingly.14,50 In addition, the contribution of Islamic finance to financial risk management and ethical conduct of financial managers will provide an all-round understanding of the impact on organizational stability and growth.25,56

These promising but also challenging dimensions include those concerning Islamic finance and some emerging HRM trends related to the digital revolution and home working. In terms of theorizing at both a conceptual and practical level, such an assessment would be able to determine the degree of adaptability these principles show toward contemporary challenges.15,58 By focusing on such issues, future research could therefore provide practical lessons and strategies that would help organizations seeking to align their HRM practices with the principles of Islamic finance, while adding to a more sustainable and ethical business environment in general.60,61

Conclusions

This paper reviews the complex dynamics that surround HRM in relation to corporate Islamic financing during the last decade. Accordingly, by analyzing a dataset comprising 402 articles from the years 2010 to 2024, we enable further insight into the meaning of adopting and integrating the methods of HRM in such a way that would permit a proper analysis of its economic impact and implications for society. Using RStudio, VOSviewer, and Excel for analytical purposes, the research has been done in three steps: a comprehensive performance analysis, citation analysis, and network and content analysis. This approach will enable us to grasp the current structure of research in the given area, including changing priorities, significant authors and their works, and implicit connections within the body of literature.

In this respect, we also suggest that future research is guided by some of the emergent themes and questions identified from our study, including: • The opportunity to explore the intersection between HRM and Islamic finance presents a series of opportunities and challenges. For example, Islamic principles related to the prohibition on Riba shape the nature of financial transactions that, in turn, affect HRM practices. For example, the HR policies of Islamic finance institutions should be aligned with Sharia compliance, which influences compensation structures, employee benefits, and investment strategies. The study on how Islamic financial principles influence the HRM practices, in integrating elements such as Mudarabah or Musharakah into employee compensation and performance management, calls for further research. • Economic crises are a specific test for employees and organizations alike, and an HRM perspective in the context of Islamic finance can offer valuable insights. For instance, Islamic finance practices such as Ijarah during financial crises may affect how companies support their employees through financial assistance and job security. Understanding the use of Islamic financial instruments in employee welfare, such as Takaful, is key to developing resilient HR strategies that stand on ethical grounds and extend support to employees during the economic slump. • It is very important to integrate Islamic finance principles with modern HRM practices, particularly in developing regions where traditional practices may differ. Research should be focused on aligning Islamic finance concepts such as Sukuk [Islamic bonds] and Zakat [charitable giving] with modern HR practices to create effective, culturally sensitive business models. We need to check the application of these principles in employee development programs, recruitment practices, and performance evaluations, ensuring their Sharia compliance and alignment with global HRM standards. • We need to address gender disparities within the HRM and Islamic finance sectors to foster inclusive growth. We can use some Islamic finance principles that are based on fairness and equity to increase the level of inclusiveness of the gender dimension in HRM practices. Research should be done to identify how Islamic financial principles, such as the prohibition of Haram, influence gender in HRM. This will include a review of equal opportunity, pay equity, and career development policies in Islamic finance institutions. • It is important to understand how Islamic financial models affect HRM practices in ways that are fair and effectively implemented. Islamic finance, based on principles like Mudarabah and Musharakah, offers alternative modes of investment in employees and profit-sharing that may have an impact on HRM policy. Researchers in this area are supposed to look into the social repercussions of these models on employee engagement, culture, and stakeholder relationships to ensure Islamic finance practices support ethical and equitable human resource management practices. • In the future, research should be directed to sustainability in HRM practices within the framework of Islamic finance. It would involve the integration of the principles of sustainability, the circular economy, and ethics in resource management with the Sharia-compliant financial practice. For instance, embedding Zakat in CSR practices and aligning Ijarah with sustainable leasing practice will further enhance sustainability in the HRM strategy. By focusing on the above areas, research can give valuable inputs to develop effective, ethical HRM practices for Islamic finance institutions that satisfy both Islamic finance principles and contemporary sustainability goals.

Although our study offers some insight, there are some limitations that we must acknowledge. Analysis is based on the accuracy and completeness of citation data, which may vary across sources. Additionally, the selected timeframe may not encompass the latest developments in the field. Furthermore, the selected tools and methods of analysis are robust, yet subjective. Consequently, we recommend that the results be interpreted with caution. Further research using a variety of methodologies may confirm and add weight to our conclusions. In this respect, the study has deepened the understanding of the use of HRM in the context of corporate Islamic finance and laid the groundwork for further research in the emergent field. In particular, by focusing on recommended research areas, scholars and practitioners will be able to develop knowledge and policies that create enabling environments for sustainable and equitable HRM practices in the context of Islamic finance.

Statements and declarations

Footnotes

Acknowledgements

The authors would like to express their gratitude to Al-Balqa Applied University and Middle East University for their support throughout this research process. Special thanks are extended to the Web of Science database team for facilitating access to valuable research resources. The authors are also grateful to their colleagues for their insightful feedback and to the administrative staff for their logistical assistance.

Author contributions

Rula Mustafa Airout conceptualized the research topic and led the data collection from the Web of Science database. Mashhour Hathloul Mousa Maharmah contributed to the analysis of the literature and provided critical insights into corporate Islamic finance. Jamileh Ali Mustafa assisted in drafting and revising the manuscript and contributed to the discussion on human resource management in Islamic finance. All authors read and approved the final manuscript.

Conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.