Abstract

Purpose

This systematic scoping review synthesizes empirical evidence on human–AI team decision-making in banking and financial services, a domain characterized by rapid AI adoption but limited documentation of how that adoption shapes collaborative decision processes.

Methods

Following the Arksey and O’Malley framework and PRISMA-ScR guidelines, three databases (Scopus, Web of Science, PsycINFO) were searched, along with snowball sampling. Thirteen empirical studies met eligibility criteria.

Results

Three collaborative architectures were identified: human-as-final-decision-maker, human-as-supervisor, and iterative co-construction with AI consistently operating as the initial analytic agent. Trust dynamics ranged from calibrated reliance to algorithm aversion and commitment bias. Explainable AI supported sensemaking, but only when it was designed interactively. Organizational incentive alignment and AI literacy emerged as decisive moderators.

Conclusions

In the included studies, performance gains from human–AI teaming in finance were evident but depended on collaboration architecture, trust calibration, and sociotechnical design. Human-centered outcomes and task performance were partially independent dimensions of effectiveness. Empirical documentation of AI deployment in banking remains thin and geographically concentrated, warranting longitudinal field research and empirically grounded governance standards.

Keywords

Introduction

Artificial intelligence is increasingly embedded across banking and financial services, supporting functions such as credit risk assessment, fraud detection, portfolio optimization, and customer advisory.1,2 In some institutions, AI has moved beyond peripheral applications toward integration in core decision workflows, though the extent and form of this integration vary considerably across contexts.3,4 The organizational and human conditions required for effective deployment, however, remain poorly understood relative to the pace of technical adoption,5,6 and empirical documentation of how human–AI teaming unfolds in financial decision workflows remains scarce, methodologically fragmented, and geographically concentrated. 7

Financial decisions carry legal accountability, and their consequences extend across clients, institutions, and markets. Governance frameworks increasingly require human oversight of AI systems in high-stakes domains, 8 yet evidence suggests that the formal presence of a human decision-maker does not automatically produce meaningful engagement, trust miscalibration, algorithm aversion, and commitment bias can each undermine collaborative quality in ways that existing frameworks may not adequately address.9,10 These considerations suggest that understanding what effective human–AI teaming requires in financial contexts is both a scientific and a governance priority, though the evidence base needed to inform that understanding remains limited.

Existing reviews have addressed human–AI teaming and trust across domains,11–13 with evidence from healthcare suggesting that collaborative gains depend on task structure and implementation context. 14 This review focuses specifically on how these dimensions interact within banking and financial services, a domain whose accountability demands, regulatory constraints, and professional norms warrant dedicated examination. We therefore prioritize theoretically grounded mechanisms likely to shape human–AI teaming across technological generations, rather than cataloguing the effects of any system. 15 Guided by the Arksey and O'Malley 16 approach, we pursue four objectives: (1) map the financial decision contexts and AI system characteristics present in empirical human–AI teaming research; (2) analyze task allocation and decision authority structures; (3) synthesize task-level performance and human-centered outcomes; and (4) identify recurrent implementation barriers and governance gaps warranting future research and regulatory attention.

Literature review and theoretical background

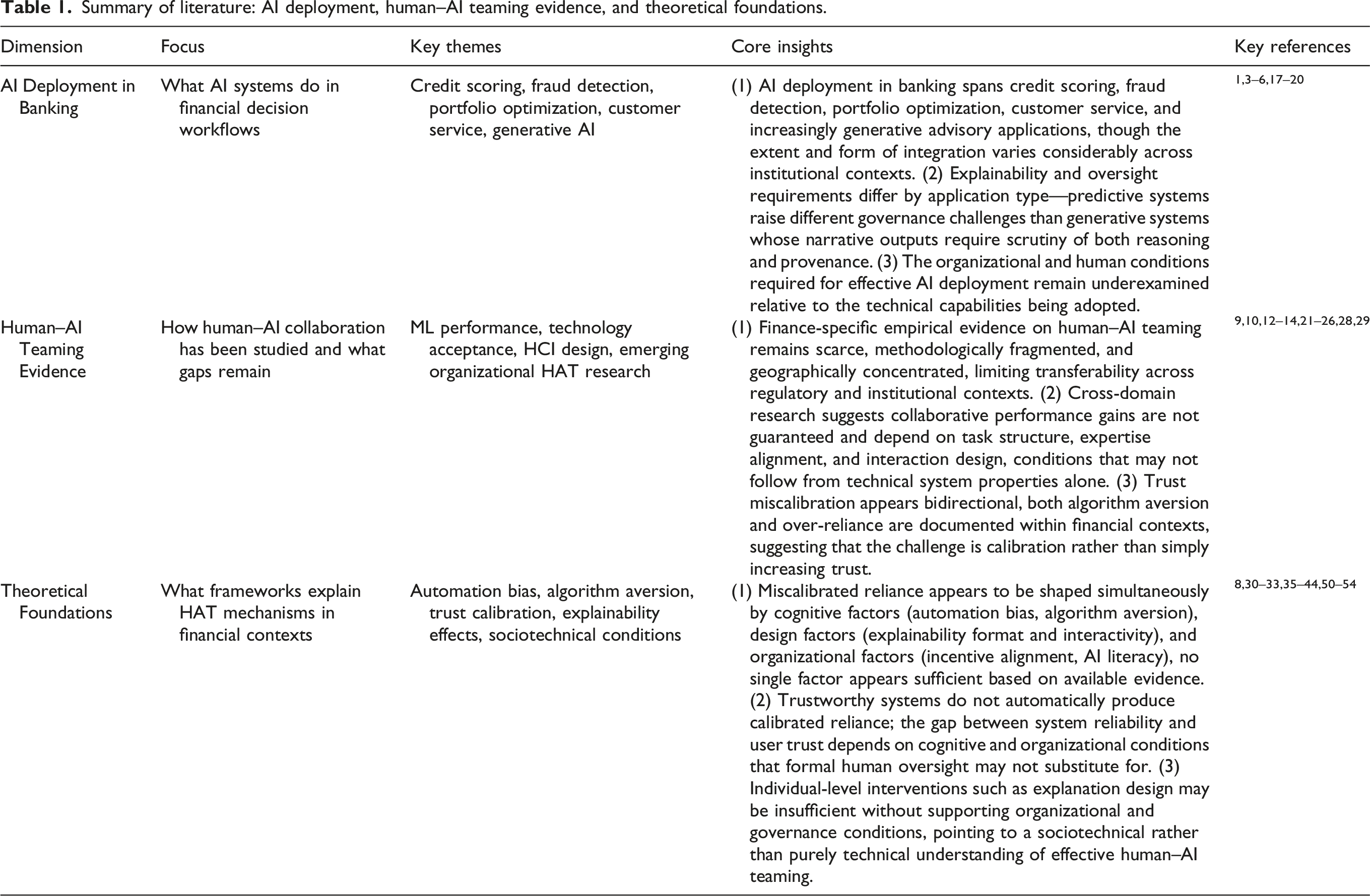

AI deployment in banking and financial services

Credit scoring and loan evaluation are the most studied domains, with machine learning models using borrower characteristics, transaction histories, and alternative data to achieve performance comparable to traditional scorecards.3,4 Such models have also identified risk patterns associated with the 2008 crisis, illustrating the potential of algorithmic credit assessment. 17 Fraud detection systems use anomaly detection to identify suspicious transactions at scales beyond manual review, 4 while portfolio optimization systems apply reinforcement learning and multi-objective algorithms to generate allocation recommendations under varying constraints. 18 Customer service applications range from rule-based chatbots to large language model-based advisory systems. 1

Human involvement remains integral due to regulatory requirements and risks such as bias and fairness in AI-supported decisions. 19 Employee skills, data reliability, and management alignment have been identified as decisive organizational conditions for effective human–AI collaboration in financial services firms. 6 Generative systems add oversight challenges because narrative outputs require scrutiny of reasoning and provenance,1,20 raising governance questions that remain underdeveloped in current frameworks.

Evidence on human–AI teaming and research gap

Empirical research on human–AI teaming in banking has developed across three streams: machine learning studies focused on model performance, technology acceptance research examining adoption, and human–computer interaction studies addressing interface design.21–25 Cross-domain research suggests that collaborative gains depend on task structure, expertise alignment, and interaction design,12,14 with conceptual frameworks for human–AI teaming emerging across service domains including healthcare 14 and tourism. 26 In banking specifically, longitudinal evidence suggests that value creation through human–AI teaming depends on interaction quality and dynamic organizational capabilities rather than algorithmic performance alone. 5

Trust in AI is shaped not only by accuracy but also by transparency and perceived fairness. 13 In financial contexts, trust dynamics are sensitive to AI performance disruptions and error exposure, with recovery depending on explanation quality and interaction history.9,10 Recent work further identifies teamwork frameworks, engagement, transparency, process control, and the substitution or supplementation of knowledge components as relevant to understanding employee-AI co-production and domain expertise in financial service contexts.27–29

Theoretical foundations of human–AI teaming

We draw on three interconnected theoretical traditions: human factors and automation theory, judgment and decision-making research, and sociotechnical systems theory, each addressing a distinct dimension of human–AI teaming.

Human factors and automation theory helps explain task structure and authority allocation. The levels-of-automation taxonomy30,31 distinguishes functional stages of decision-making and provides a basis for identifying where miscalibrated reliance may emerge. In financial AI deployments, where systems typically support early-stage analysis while humans retain decision authority, this configuration may create risks related to automation bias, over-reliance, and vigilance. 31 Automation bias varies with task complexity, time pressure, and prior experience. 30 Effective human–AI teaming might require alignment of AI purpose, value commitments, and system properties, increasingly reflected in regulatory expectations for high-risk AI systems.8,32,33 Early studies 34 identified coordination and communication demands in AI-agent integration, suggesting that human–AI teaming challenges are fundamentally relational and organizational rather than purely technical.

Judgment and decision-making research helps explain the cognitive processes through which humans engage with AI outputs. Under time pressure or cognitive load, individuals may accept AI outputs with insufficient scrutiny. 31 Algorithm aversion, the tendency to discount AI advice after seeing it make errors, is a separate but related problem that often appears alongside other trust failures. 35 These patterns can coexist within the same populations,36,37 indicating that miscalibrated reliance is not unidirectional. Algorithm aversion may happen even when objective performance favors the algorithm, 35 and domain expertise can moderate these effects, although findings remain context dependent. 38

The literature on trust provides a conceptual bridge between task structure and organizational context. Across disciplines, AI reliance depends on actual performance, perceived transparency, contextual risk, social norms, and the broader organizational environment.39,40 This carries governance implications: effective human oversight cannot be reduced to the formal presence of a human decision-maker, as evidence suggests it depends on the cognitive and organizational conditions that enable calibrated trust. 38 Evidence across human factors, HCI, and interpretability research41–43 suggests that explanation quality shapes how users integrate AI outputs with domain knowledge, though its relationship with decision quality is not consistently positive. Surface-level transparency can increase confidence without improving accuracy, 42 and the effectiveness of explanation design depends on format, user expertise, and task structure.23,25,44 Rigorous evaluation of interpretability therefore requires task-specific measures. 42 Recent evidence from financial contexts suggests that end-users and technical stakeholders diverge substantially in their explanation format preferences 45.

Summary of literature: AI deployment, human–AI teaming evidence, and theoretical foundations.

Method

A systematic scoping review was conducted following the five-stage framework proposed by Arksey and O'Malley, 16 appropriate for heterogeneous and emerging bodies of literature where studies vary widely in design, context, and reported outcomes. To enhance transparency and reproducibility, the review was reported in accordance with PRISMA-ScR guidelines, 55 which informed the reporting of study identification, screening, eligibility, and data charting. The review protocol is documented in an Open Science Framework (OSF) registration. The registration is currently embargoed for peer review and will be made publicly accessible upon publication. Database searches were conducted in December 2025; background references were updated during revision and did not affect corpus composition.

Step 1: Identification of the research question

The study focused on situations in which humans and AI systems jointly contribute to decision-making, rather than fully automated systems. Extracted dimensions included AI system type and purpose, task allocation, and outcomes covering trust, reliance, sensemaking, perceived control, and autonomy. By systematically mapping these dimensions, we discuss empirical patterns and gaps in the literature, regarding decision contexts, methodological limitations, and emerging AI technologies.

Step 2: Identification of relevant studies

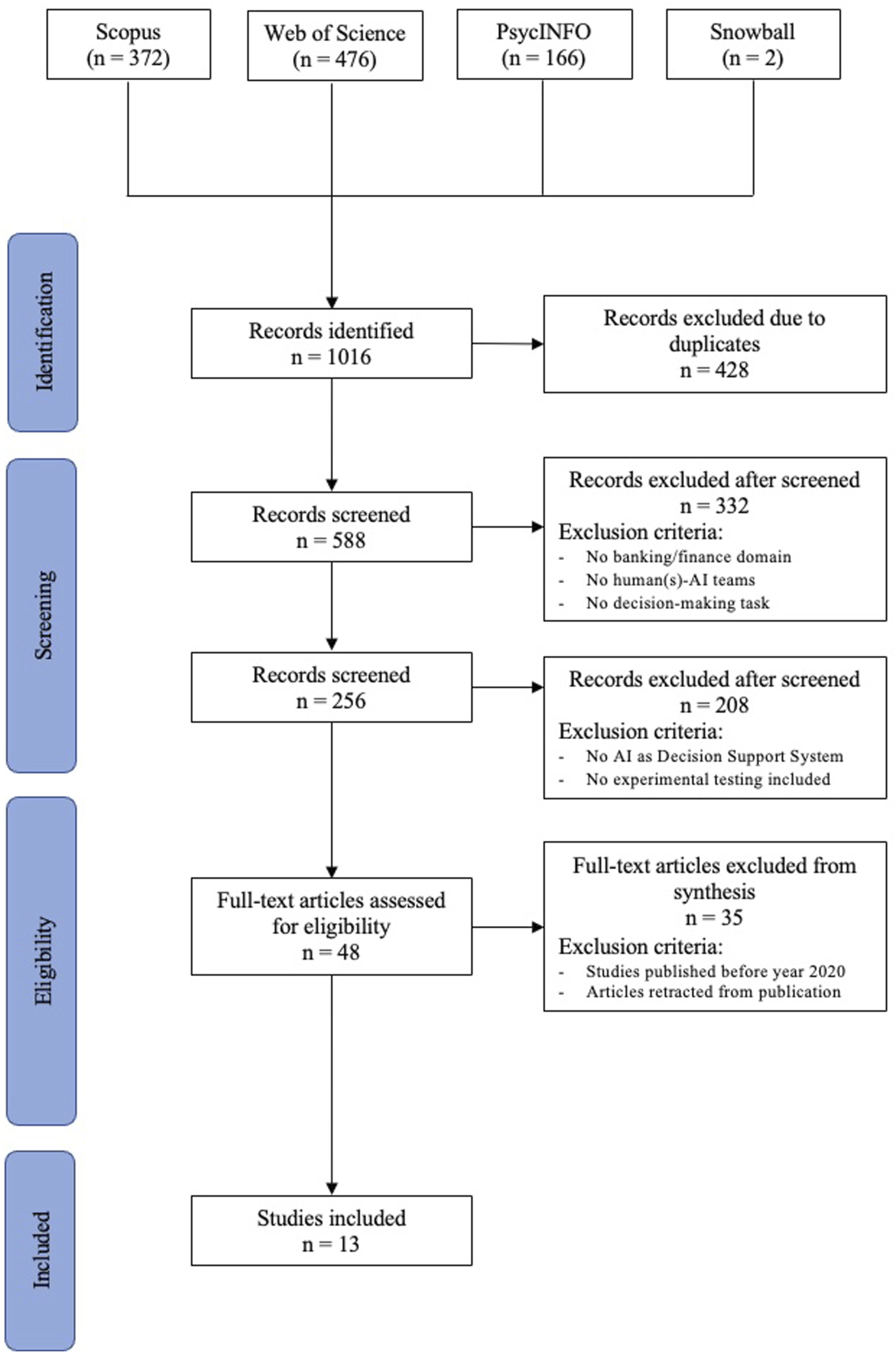

Searches were conducted in December 2025 across three databases (Scopus, Web of Science, and PsycInfo). Snowballing techniques complemented database searches following established guidelines, 56 through backward citation searching and forward citation tracking applied to the full set of included studies as the seed corpus following completion of database screening. One round of snowballing was conducted, with candidate references screened against the same eligibility criteria applied to database records. The low yield of snowball sampling (n = 2) may reflect the comprehensiveness of the primary database search, although it also indicates that snowballing contributed only minimally to the final corpus. Full search strings for all databases, database-specific adaptations, and procedural documentation are reported in the OSF-registered protocol, which is currently embargoed for peer review and will be made publicly accessible upon publication. Boolean operators and wildcard symbols were applied to refine retrieval. The search syntax for Scopus was as follows: (“AI” OR “Artificial intelligence” OR “decision support system*” OR “DSS*” OR “human-AI team*” OR “human AI team*” OR “human-agent team*” OR “hybrid team*” OR “AI team*” OR “AI collab*” OR “human-AI agent collab*”) AND (“bank*” OR “banking” OR “finance*” OR “financial”) AND (“decision*” OR “decision-making” OR “decision support”).

Equivalent search strategies were adapted for the other databases, considering their specific indexing conventions and search fields, while maintaining the same conceptual scope. The initial search yielded 1016 records (Scopus: n = 372; Web of Science: n = 476; PsycInfo: n = 166; Snowball: n = 2). After removing duplicates (n = 428), 588 articles remained for screening.

Step 3: Study selection

In the first stage, 332 records were excluded for absence of a banking or financial domain, human–AI teaming, or decision-making task, leaving 256 articles. In the second stage, 208 records were excluded for lacking AI as a decision-support system or for being non-empirical, yielding 48 full-text articles assessed for eligibility. Eligible studies were empirical, published in peer-reviewed journals or conference proceedings in English since 2020, and situated within a banking or financial decision-making context involving explicit human–AI teaming. Conceptual papers, literature reviews, industry reports, and studies of fully automated systems were excluded. Following full-text review, 35 articles were excluded, leaving 13 studies in the final synthesis. One study meeting all other criteria was published in late 2019 and was retained given its direct relevance to the review’s decision-making focus. Disagreements were resolved through discussion. The study selection process is summarized in the PRISMA flow diagram (Figure 1). PRISMA flowchart summarizing the study selection process.

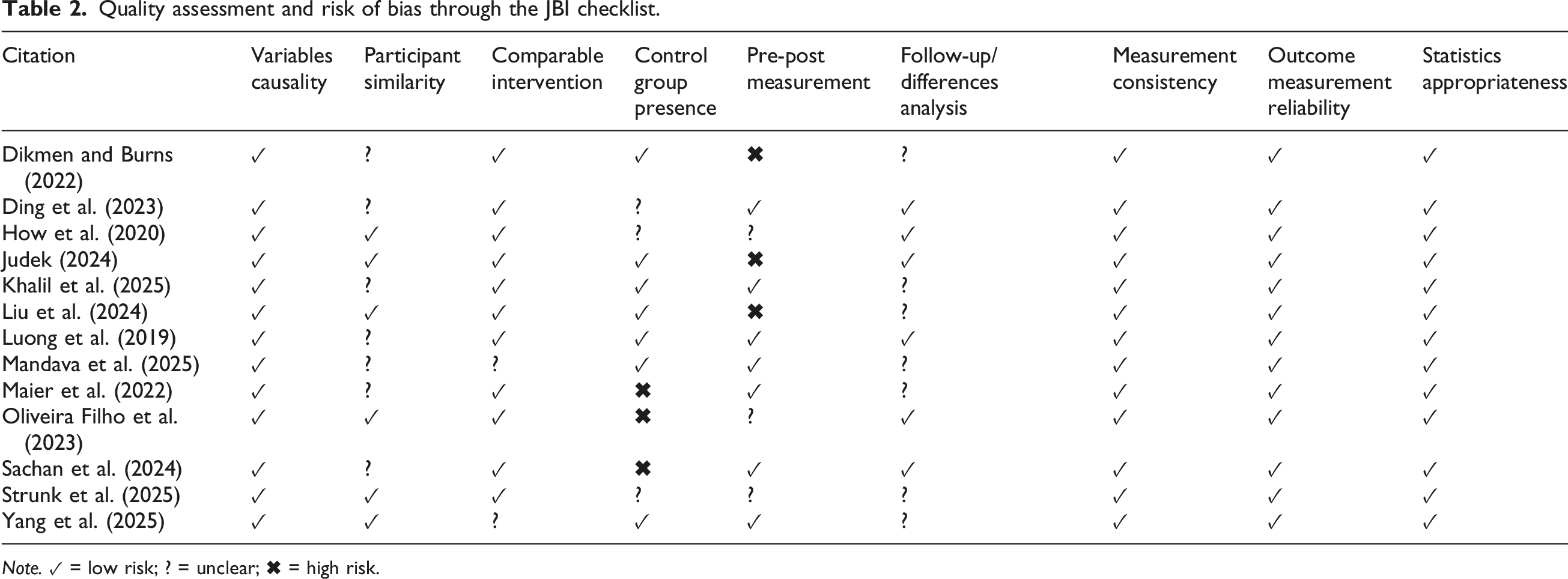

Step 4: Quality assessment of studies

Quality assessment and risk of bias through the JBI checklist.

Note. ✓ = low risk; ? = unclear; ✖ = high risk.

Step 5: Charting the data and reporting the results

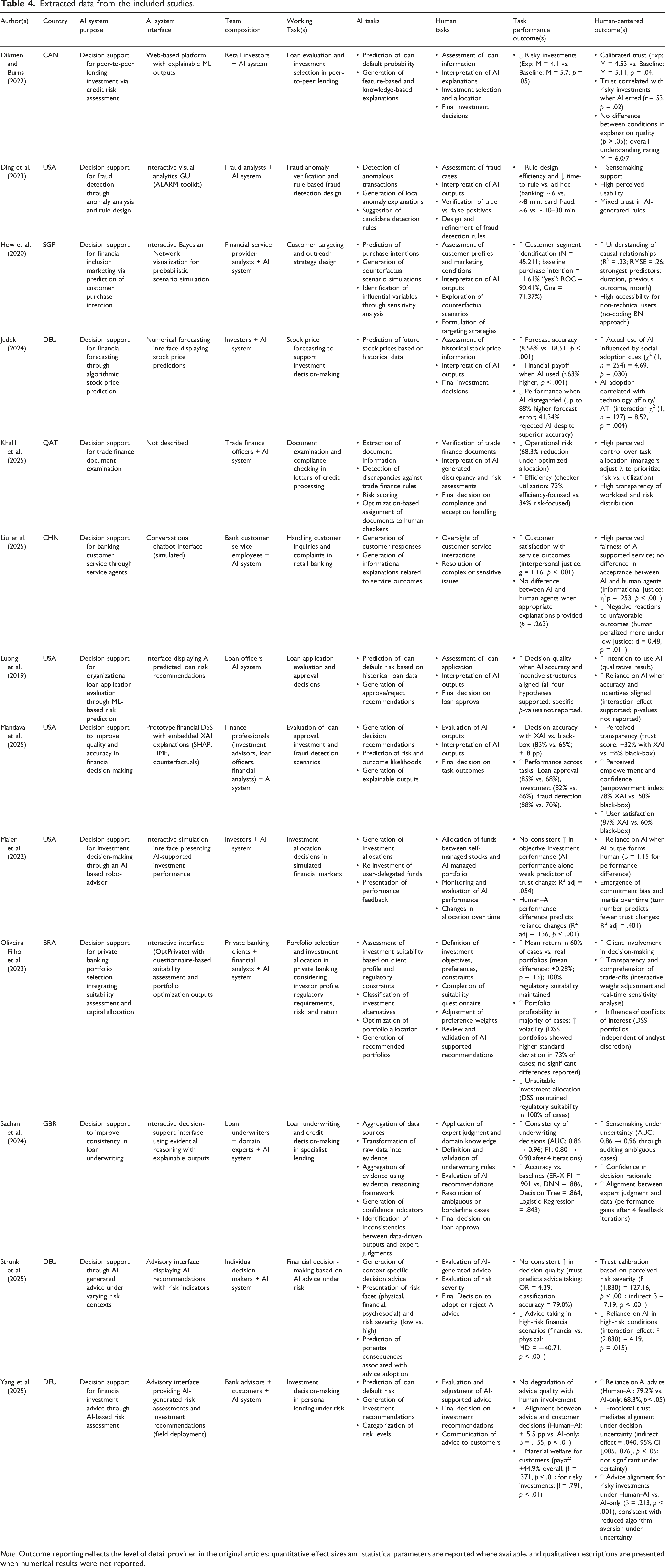

Data were extracted using a predefined, iteratively refined data charting framework, designed to create consistency across studies while accommodating methodological diversity to reveal patterns among organizations or contexts. Extracted information included author and year, country, AI system model and purpose, AI interface, human–AI team composition, working task, AI tasks, human tasks, performance outcomes, and human-centered outcomes.

Results

Risk of bias and quality of studies

Of the 13 studies, 7 (53.8%) received no high-risk ratings across evaluated domains,57–63 while 6 (46.2%) presented at least one high-risk rating on a specific criterion. No study was classified as high risk across all criteria. All studies presented a sufficiently clear causal or comparative structure for the purposes of the JBI appraisal and received low-risk ratings for measurement consistency, outcome reliability, and statistical appropriateness. Three studies did not employ pre-post measurements,64–66 and three lacked a defined control group.67–69 Follow-up and difference analysis received unclear ratings in seven studies, reflecting a common design feature of this literature rather than a systematic quality concern. Where inferential statistics were reported, effect sizes and p-values are included in the synthesis.

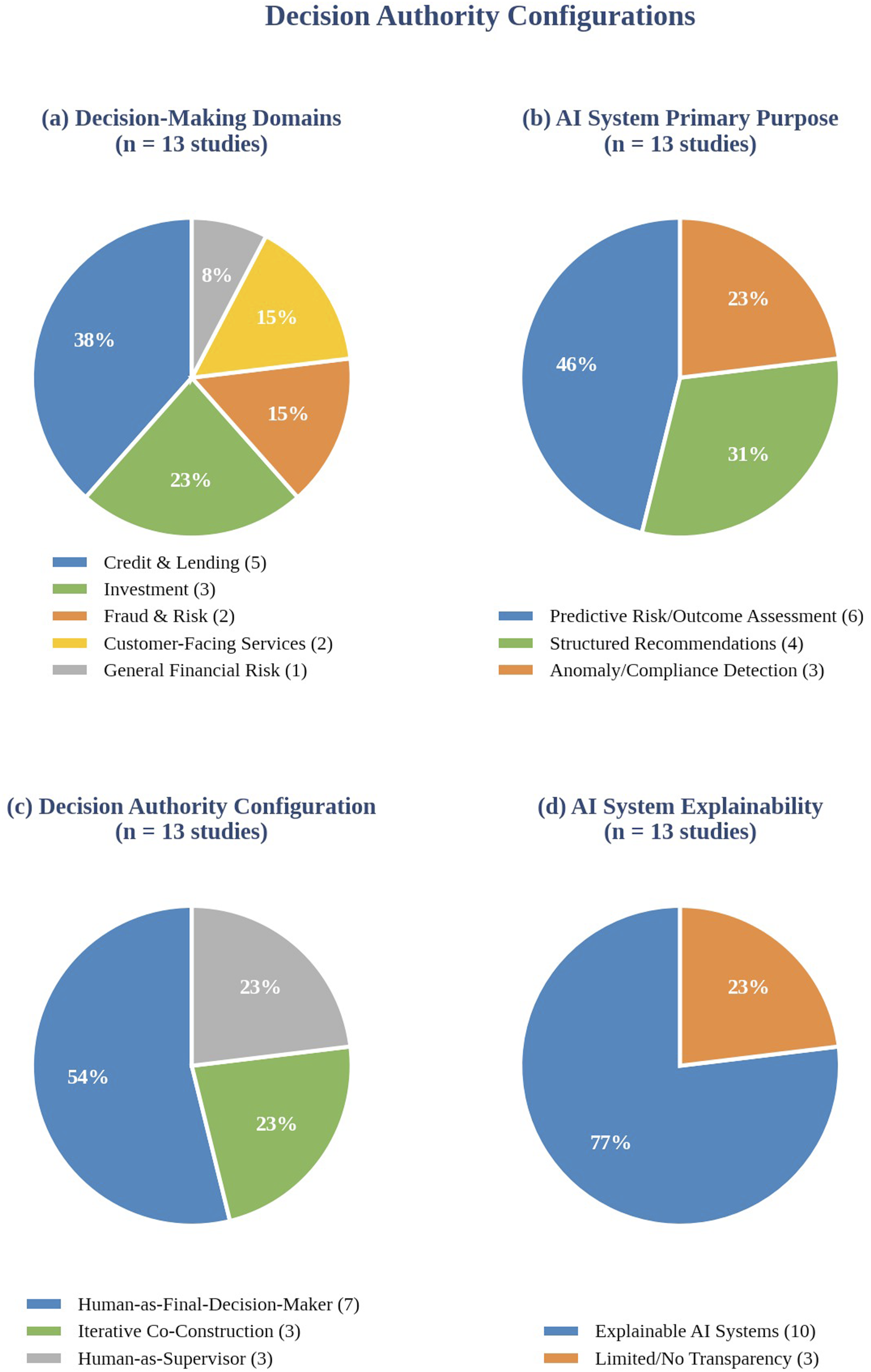

Decision contexts and AI system characteristics

The 13 studies covered diverse financial decision-making contexts. Credit, lending, and trade finance decisions were the most frequent domain, examined in five studies.59,60,63,64,68 These studies addressed loan application screening, peer-to-peer lending investment selection, trade finance document verification, and specialist loan underwriting. AI systems typically generated predictive risk assessments, discrepancy flags, or structured compliance outputs to support human evaluation and final decisions.

A second cluster focused on investment-related decision-making, including stock price forecasting, portfolio allocation optimization, and investment suitability assessment.65,69 Here, AI systems provided probabilistic predictions, portfolio recommendations, or optimization outputs for interpretation by investors or financial advisors. A third group addressed fraud detection and broader risk assessment, where AI systems performed anomaly detection, generated fraud risk indicators, or produced explainable risk classifications to support analysts working under uncertainty.57,61

The remaining studies examined customer-facing financial services, including AI-supported retail banking interactions 66 and predictive targeting for financial inclusion marketing. 58 One study examined financial decision-making under risk more generally, without anchoring the task in a specific operational banking process. 62

Across contexts, AI systems functioned as decision-support tools, with humans retaining evaluative, supervisory, or final decision roles. Their main functions included predicting outcome probabilities, generating recommendations, and detecting anomalies or compliance discrepancies in financial data.

A key source of variation concerned explainability. Most studies used transparency or interpretability mechanisms, including feature-based and knowledge-based explanations, 64 SHAP, LIME, and counterfactual explanations, 61 local anomaly explanations, 57 Bayesian network visualizations, 58 and evidential reasoning frameworks. 68 In contrast, some studies implemented systems with limited or no explicit transparency regarding internal decision logic.62,65,67 These systems typically presented numerical forecasts, risk indicators, or recommendation signals without detailed explanation of feature contributions or reasoning pathways. This distinction appeared, in several studies, to be associated with patterns of trust, reliance, and advice-taking.

Interfaces included visual analytics dashboards,

57

Bayesian visualization tools,

58

prototype explainable AI systems,61,68 conversational chatbots,

66

portfolio optimization interfaces,

69

and numerical forecasting displays.

65

One study did not report interface details.

59

This diversity suggests that standardized interaction patterns have not yet emerged in financial decision-making. Figure 2 summarizes these distributions. Decision-making domains (a). AI system’s primary purpose (b). Decision authority configuration (c). AI system explainability (d).

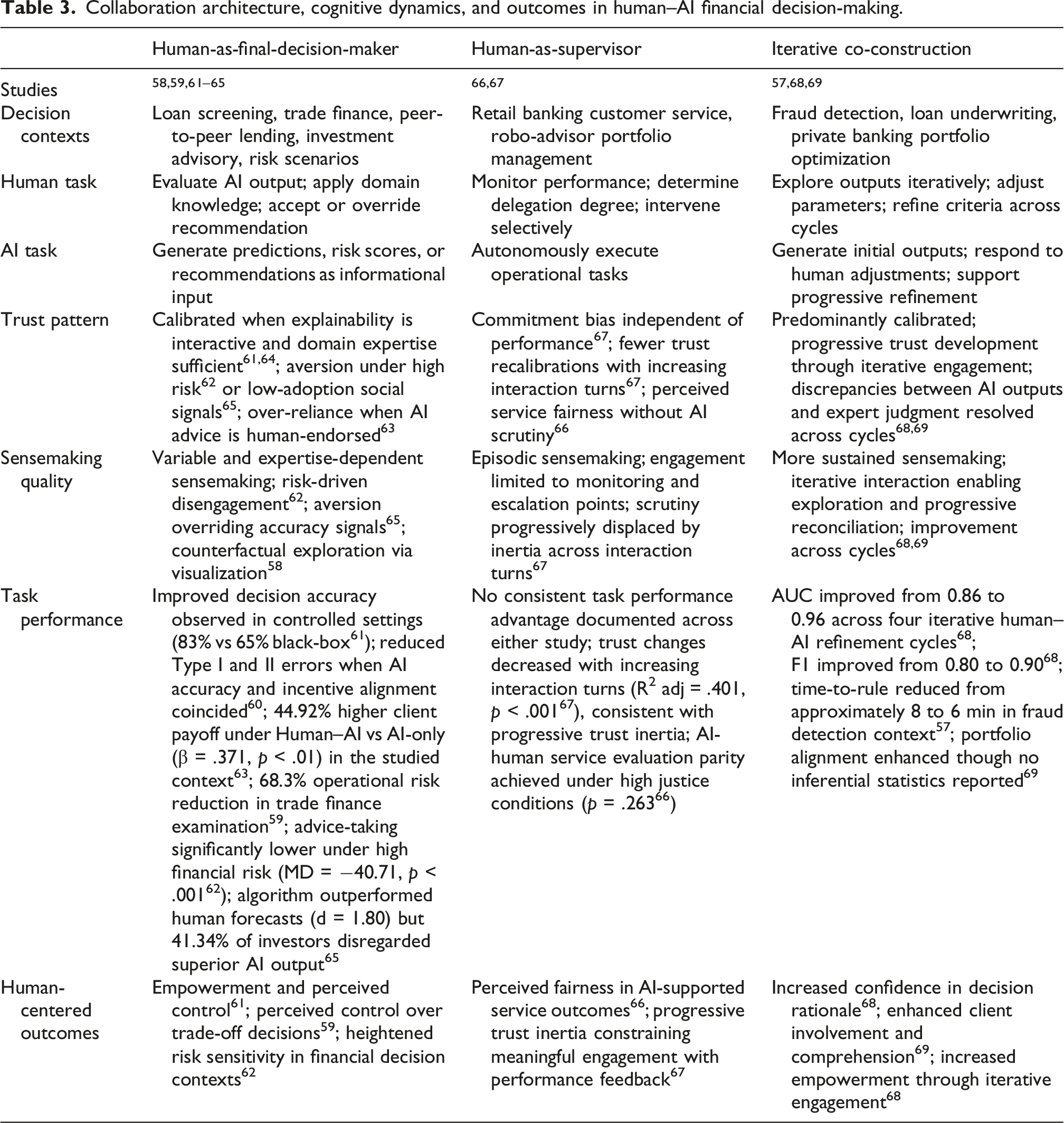

Task allocation and decision authority distribution

Across the studies, AI systems consistently acted as the initial analytic component in the decision flow. They aggregated data, detected patterns, modeled predictions, identified anomalies, and generated recommendations or risk scores. Human actors then interpreted these outputs, evaluated contextual information, and made or supervised final decisions. This sequential configuration, AI generation followed by human adjudication, was the dominant model.

Decision authority varied across three configurations. The most common was the human-as-final-decision-maker model, observed in seven studies.59–65 In this arrangement, AI systems provided predictions, recommendations, or risk scores, while humans retained authority to accept, modify, or reject the output. AI shaped the informational context but did not override human judgment. Human tasks involved evaluating AI-generated information against contextual knowledge, professional standards, or strategic objectives.

A second configuration, human-as-supervisor, appeared in two studies.66,67 Here, AI systems played a more operational role, autonomously generating customer responses or managing investment portfolio segments. Human actors monitored performance, determined delegation levels, and intervened selectively. Authority was partially shared, with human influence exercised through oversight and escalation rather than evaluation of each discrete output.

A third configuration, iterative co-construction, characterized studies in which human and AI contributions were integrated through repeated interaction rather than a single handoff.57,64,68 Analysts explored AI-generated outputs, examined explanations, adjusted parameters or preference weights, and refined decision criteria through interaction with the system. Authority was distributed across multiple stages, with both human and AI contributions shaping the final decision.

Collaboration architecture, cognitive dynamics, and outcomes in human–AI financial decision-making.

Cognitive and relational dynamics in human–AI joint decision-making

Three interrelated mechanisms shaped human interaction with AI systems across the reviewed studies: trust and reliance calibration, sensemaking, and the moderating role of risk perception and organizational context.

Trust calibration and reliance

Trust in AI was the most frequently examined human-centered construct, with studies documenting calibrated, under-reliant, and over-reliant patterns.

Several studies reported calibrated trust dynamics, where users differentiated between credible AI outputs and situations requiring skepticism. Dikmen and Burns 64 found that explainable AI enabled retail investors to rely selectively on AI predictions when explanations aligned with domain cues, while maintaining skepticism when discrepancies arose. Participants in the explainability condition made fewer risky investments (M = 4.1 vs 5.7, Mann-Whitney U = 271.5, p = .05) and fewer investments when the AI was incorrect (M = 2.9 vs 3.8, U = 283.5, p = .02). They also reported lower trust scores (M = 4.53 vs 5.11, t (38) = 2.1, p = .04), consistent with calibrated, skepticism-informed reliance rather than blind acceptance. Similarly, Mandava et al. 61 found that SHAP, LIME, and counterfactual explanations increased perceived transparency and confidence among participants with finance backgrounds, suggesting a possible pathway toward comprehension-based trust.

Algorithm aversion and under-reliance appeared in other contexts. Judek 65 found that 41.34% of investors disregarded accurate AI forecasts despite superior algorithmic performance. AI forecasts showed lower error than human forecasts (8.56% vs 18.51%, t (252) = 14.19, p < .001, d = 1.80), and AI use yielded approximately 63% higher financial payoff (t (252) = 17.47, p < .001). Adoption was influenced by social adoption cues (χ2 (n = 254) = 4.69, p = .030) and technology affinity, although participants with lower ATI scores were more likely to use the algorithm (χ2 (n = 127) = 8.52, p = .004). Strunk et al. 62 further showed that trust shaped advice-taking under varying financial risk conditions. These findings suggest that trust may depend not only on system performance but also on perceived risk and individual differences.

A third pattern involved over-reliance or inertia. Maier et al. 67 found commitment bias among robo-advisor users: participants were less likely than random to decrease trust after having increased it and often maintained their allocation regardless of previous performance. Turn number predicted fewer trust changes over time (adjusted R2 = .401, p < .001), indicating increasing reliance inertia. Yang et al. 63 found that embedding AI-generated advice within a human advisory context increased client reliance, suggesting that social framing may influence adoption independently of technical accuracy in advisory settings.

Sensemaking and comprehension

Sensemaking appeared across several studies as a potential mediator between AI system design and decision quality, although mechanisms and effect sizes varied. In fraud detection, Ding et al. 57 reported that interactive fraud rule authoring reduced analyst time-to-rule to approximately 6 min, compared with around 8 min using ad-hoc tools on the Czech dataset and 10–30 min for domain rules on the Card dataset. Rule quality was broadly comparable across conditions, although coverage advantages varied by dataset. Sachan et al. 68 found that an evidential reasoning framework helped underwriters identify and resolve inconsistencies between data-driven outputs and expert judgments, improving underwriting consistency across four iterations (AUC: 0.86 to 0.96; F1: 0.80 to 0.90).

How et al. 58 showed that Bayesian network visualizations enabled analysts to explore counterfactual scenarios and variables influencing customer purchase intentions, with good model performance (ROC = 90.41%, R2 = .33). De Oliveira Filho et al. 69 reported that interactive portfolio optimization tools enhanced clients’ understanding of risk-return trade-offs. Collectively, these findings suggest that explainability alone may be insufficient; effective sensemaking appeared to depend on interaction designs enabling exploration, comparison, and iterative refinement of AI outputs.

The moderating role of risk perception and organizational context

Contextual factors, especially perceived risk and organizational alignment, moderated trust and reliance. Strunk et al. 62 found that advice-taking was significantly lower in high-severity financial risk scenarios than in physical risk contexts (MD = −40.71, p < .001), with trust mediating the effect of risk severity on advice-taking (indirect effect = 17.19, p < .001). Luong et al. 60 showed that reliance on AI recommendations depended on alignment with organizational incentive structures; when AI outputs were congruent with institutional objectives, decision errors decreased.

Yang et al. 63 found that human delivery of AI-generated investment advice increased client trust and material welfare outcomes in the studied context, with 44.9% higher payoff under Human–AI than AI-only advice (β = .371, p < .01). This points to the relevance of sociotechnical integration in shaping human–AI teaming effectiveness.

Decision outcomes and implementation challenges

Most studies reported positive effects of human–AI teaming on task performance, although mainly in controlled or single-context deployments. Improvements included reduced decision errors in loan evaluation, 60 improved underwriting consistency, 68 reduced operational risk in trade finance document examination, 59 improved mean portfolio returns relative to analyst-selected portfolios despite higher volatility and a DSS Sharpe ratio of 0.13, 69 increased forecast accuracy and payoff when AI outputs were adopted, 65 enhanced efficiency in fraud rule design, 57 and improved decision accuracy with explainable outputs compared with black-box systems (83% vs 65%). 61

However, performance gains were not uniform. Maier et al. 67 found that neither AI nor human performance alone strongly predicted trust change (adjusted R2 = .054 and adjusted R2 = .023, respectively), whereas the difference between human and AI performance was a moderate predictor (adjusted R2 = .136, p < .001). Judek 65 also observed reduced performance among participants who disregarded AI outputs.

Human-centered outcomes included increased perceived transparency and empowerment, 61 enhanced client involvement and comprehension, 69 greater confidence in decision rationale and improved alignment between expert judgment and data-driven evidence, 68 comparable perceived fairness between AI and human agents under high justice conditions (p = .263), 66 and flexibility for managers to adjust risk-utilization trade-offs in task allocation. 60

Importantly, task performance and human-centered outcomes did not always co-occur. In some contexts, reliance persisted without objective performance gains; in others, reduced trust limited advice adoption despite potential accuracy benefits. This pattern suggests that task performance and human-centered outcomes are partially independent dimensions of human–AI teaming effectiveness.

Extracted data from the included studies.

Note. Outcome reporting reflects the level of detail provided in the original articles; quantitative effect sizes and statistical parameters are reported where available, and qualitative descriptions are presented when numerical results were not reported.

Discussion

Key findings

Across the four objectives, the findings suggest that collaborative gains in human–AI financial decision-making depend not only on algorithmic performance, but also on the organizational and cognitive conditions surrounding its use. Evaluating financial AI through predictive metrics alone risks overlooking dimensions of collaborative quality that Schmutz et al. 12 and Chiriatti et al. 70 identify as central to effective human–AI teaming. This concern is supported by the partial independence of task performance and human-centered outcomes observed across several studies. Khalil et al., 59 for example, showed that operational risk reduction and managerial flexibility over risk-utilization trade-offs could co-occur, a pairing that human-centered frameworks position as a design target rather than an incidental outcome. 12

The reviewed studies also show that human professionals function as active cognitive agents rather than passive recipients of AI outputs. 43 They engaged in sensemaking, contextual reasoning, and evaluative judgment grounded in domain knowledge, accountability, and organizational norms. However, this engagement was neither uniform nor consistently effective. When collaboration architecture, explainability design, and organizational incentives were aligned, studies reported gains in task performance or human-centered outcomes, although most evidence came from controlled or single-context deployments. These included reduced risky investments through calibrated reliance on explainable AI, 64 reduced analyst time-to-rule through interactive fraud rule authoring, 57 improved decision quality through transparency design, 61 improved underwriting consistency through iterative refinement, 68 and increased client welfare and trust when AI advice was routed through a human intermediary. 63

In contrast, where these enabling conditions were absent, collaboration produced no consistent advantage and sometimes introduced systematic biases. In experimental and simulated settings with non-expert participants, algorithm aversion, 65 trust inertia, 67 and risk-driven advice rejection 62 suggest that miscalibrated collaboration may produce outcomes no better than unaided judgment. Whether these patterns persist under real accountability structures remains an open empirical question.

Theoretical contributions

The findings offer preliminary grounding for the frameworks outlined in the literature review section by showing how automation bias, reliance, and collaborative outcomes vary across decision architectures. The three collaboration architectures identified in this review map onto distinct vulnerability profiles. Human-as-final-decision-maker configurations concentrate automation bias risk at the evaluation stage, 31 consistent with the commitment bias 67 and risk-driven trust erosion 62 observed in the reviewed studies. Human-as-supervisor configurations shift this risk toward delegation calibration. 12 Iterative co-construction distributes cognitive labor across repeated interaction cycles, allowing expert judgment and data-driven evidence to be progressively reconciled. 68 This configuration may create conditions under which miscalibration is corrected rather than compounded. 31 Domain expertise also appeared important for calibrated reliance, consistent with Hickman and Langer’s 29 proposition that AI may augment performance through the substitution or supplementation of declarative and procedural knowledge.

Trust miscalibration was bidirectional, context-sensitive, and socially mediated. This aligns with HMI scholarship suggesting that trust in AI draws partly on social-cognitive schemas from interpersonal interaction while operating under distinct accountability and epistemic conditions. 71 The coexistence of algorithm aversion62,65 and commitment bias 67 supports the view that the target state is calibration rather than trust per se. Multilevel trust frameworks71,72 are consistent with these patterns, as Yang et al. 63 showed that relational and emotional trust mediated AI adoption through a human intermediary. The distinction between trustworthiness and trust is also visible: Judek 65 found distrust of high-performing algorithms, while Maier et al.’s 67 robo-advisor generated commitment bias without objective warrant. 13

At the organizational level, incentive alignment, knowledge adaptability, and AI literacy appeared as relevant moderators. 73 Luong et al.’s 60 finding that decision errors decreased only when high AI accuracy coincided with organizational incentive alignment is consistent with the argument that AI effectiveness is co-determined by organizational design.12,74 AI-induced technostress may reduce engagement and well-being in banking populations, 75 although no reviewed study directly measured it. Implementation challenges such as misaligned incentives, unmanaged expectations, and cognitive bias effects are consistent with organizational conditions associated with perceived injustice, reduced autonomy, and privacy concerns, 54 and are unlikely to be addressed through individual-level interventions alone.

Practical implications

For financial institutions, three priorities emerge. First, deployment should begin with organizational readiness rather than tool selection alone. Performance and empowerment gains documented across studies61,63,68 depended on institutional conditions such as alignment between human and AI performance goals and ongoing monitoring of reliance calibration. 60

Second, evidence from contrasting trust patterns across explainable and opaque systems suggests that architecturally embedded, interactive explainability may support calibrated reliance more effectively than static post hoc explanations. 41 Interactive tools that allow users to explore outputs, compare alternatives, and interrogate reasoning pathways appear more likely to support meaningful oversight.57,61 Clarity over whether systems are designed to “assist” or “augment” human decision-makers also remains a design-level decision with implications for accountability. 76

Third, individual differences in technology affinity and domain expertise were among the most consistent moderators of reliance calibration across the reviewed studies.64,65 Institutions may therefore consider these characteristics in role assignment, team composition, and onboarding, including training on how AI outputs should be interpreted, challenged, and integrated with domain judgment.

For regulators, three areas for attention emerge. First, existing frameworks that mandate human involvement without specifying meaningful engagement may leave important failure mechanisms unaddressed, including commitment bias, social framing effects, 63 and risk-driven trust erosion. 62 Minimum standards for explanation quality therefore represent a tractable regulatory intervention, provided they support sensemaking rather than merely satisfy transparency requirements. Such standards might require interactive explanation mechanisms, counterfactual exploration, and evaluation against decision quality outcomes rather than user satisfaction alone.57,61,64

Second, the three collaboration architectures identified in this review, human-as-final-decision-maker, human-as-supervisor, and iterative co-construction, may offer regulators a practical taxonomy for specifying oversight requirements proportionate to delegated decision authority. This could help address accountability ambiguities that current frameworks leave unresolved. Third, guidance on AI literacy as an operational condition of deployment would complement technical standards with human capital requirements. The organizational failure conditions identified by Zhou et al., 54 including perceived injustice and reduced autonomy, suggest that explanation standards may support not only transparency, but also calibrated reliance and employee well-being.

Limitations and future research

The small evidence base warrants interpretive caution. Only 13 studies met the inclusion criteria, reflecting the early stage of empirical documentation relative to the scale of AI deployment in banking. Most were conducted in controlled or simulated settings, limiting ecological validity and leaving open whether findings transfer to professional populations operating under real accountability structures. Geographic concentration in North America, Europe, and East Asia further limits transferability across regulatory, institutional, and cultural contexts.

The predominance of cross-sectional designs also leaves unresolved how trust calibration and collaboration quality evolve during sustained deployment, a critical gap given evidence of both temporal inertia 67 and iterative improvement. 68 Several financial decision domains, including trading, anti-money-laundering, insurance underwriting, and regulatory compliance, remain empirically underexamined from a teaming perspective.2,24 Healthcare research has begun to formalize governance frameworks for continuously learning human-in-the-loop systems, highlighting the absence of comparable regulatory clarity in financial decision environments. 77

Future research should prioritize longitudinal field studies of trust calibration and reliance in banking environments, complemented by organizational ethnographies of incentive structures, knowledge dynamics, and workflow adaptations. Cross-country comparative studies would clarify how regulatory frameworks and institutional cultures shape collaboration architectures. Further work should assess both objective performance and human-centered outcomes using validated measures of empowerment, fairness, and well-being. AI literacy also warrants investigation, including whether structured training improves reliance calibration and reduces automation bias among financial professionals. 51 Finally, validated teamwork frameworks have not yet been applied to human–AI teams in financial contexts, 27 and future studies should examine how generative AI capabilities, including autonomous reporting and contextual reasoning, 78 alter authority configurations.

Conclusions

The current evidence suggests a coherent but not definitive account of human–AI teaming in financial decision-making. Across the reviewed studies, AI systems typically operated as the initial analytic component in the decision flow, while humans interpreted, evaluated, and authorized outputs. The human role appears more cognitively demanding and evaluative than “human-in-the-loop” rhetoric often implies, involving sensemaking, calibrated trust, and contextual judgment. However, whether these patterns hold under live conditions with professional populations, across regulatory and cultural contexts beyond the geographically concentrated current evidence base, and over sustained longitudinal deployment remains to be established.

Explainability was more consistently associated with calibrated reliance when architecturally embedded and interactively designed than when delivered as static post hoc output, 41 although the evidence remains too limited for generalization. Organizational conditions, including incentive alignment, governance clarity, AI literacy, and adaptable knowledge structures, appeared at least as consequential as technical AI properties. Effective banking decision-making may therefore depend on preserving and augmenting distinctively human capabilities, including judgment, relational intelligence, and professional accountability, through AI systems designed to support rather than erode them.12,54

For institutions, interactive explanation design and AI literacy may support more calibrated human–AI teaming,51,57,61,64,65,68 although live-deployment evidence remains limited. For regulators, specifying conditions for meaningful engagement, including explanation quality and collaborative process design, may offer stronger governance than mandating human involvement alone.62,63,67 Longitudinal field studies with financial professionals across diverse regulatory and institutional contexts remain a methodological priority.

Footnotes

Ethical considerations

This study is a scoping review of published literature and did not involve primary data collection. Ethical approval was therefore not required.

Consent to participate

Informed consent was therefore not required.

Author contributions

All authors reviewed and approved the final manuscript.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data supporting the findings of this study are derived from publicly available published articles. The data extraction table is available.