Abstract

This article explores the role of calculative technologies, such as taxation, accounting and actuarial practices, in constructing ‘age’ in contemporary society. It argues that retirement income programs built on these technologies attempt to construct specific relations not just between the individual and other generations, but between the individual and herself at other stages of life. Retracing the series of Canadian attempts to secure income for the elderly over the course of the 20th century, the paper shows how calculative technologies have been used to connect responsibility for the elderly to the political rationalities of the day. This genealogy allows us to recognize how the present Canadian retirement income system, with its public and private programs addressing different subsets of the population, is contingent on neoliberal rationalities of governance. These demand the alignment of the individual with the goals of the capital markets, and seek to achieve this through a distributed agency that encourages the investment of individual savings in retirement income products. The paper argues that this distributed agency is perpetually incomplete, and that uncertainty is necessary in order that the individual be constantly remade as an investor.

Introduction

This paper proceeds from the premise that age is relational. We understand ourselves as individuals of a certain age in relation to others our age, and in relation to those who are different ages, like neighbours or grandparents. We also understand ourselves reflexively, in relation to who we were and who we will become. Given this premise, the paper looks at how these relationships are structured by institutions and practices related to age and aging, particularly those pertaining to the provision of income for the elderly. Using the example of the retirement income system in Canada, the paper documents how calculative practices have participated, over the course of the past century, in the changing social construction of the ‘elderly person.’ It argues that accounting and other calculative practices have been instrumental during the past century in connecting responsibility for this ‘elderly person’ to the political rationalities of the day.

The analysis shows how the notion of the elderly as a target of governance has changed over the years. When the elderly were first recognized as a population group to be governed, they were first construed in binary terms as either self-sufficient or destitute. Later, following World War I, they were construed as having failed to secure their elderly years and became the recipients of invasive financial aid programs. Following World War II, they were positioned as part of a larger social contract, where everyone set aside money for old age, and shared it across generations. Finally, in the late 20th century, the elderly were idealized as receiving the reward of a lifetime of personal financial discipline, via individual retirement income products, albeit buttressed by the collective decision making of the finance industry. Concurrent with these shifts in the construction of the elderly, our capacity to act to provide for the elderly shifted from the family and local community to the state and the employer, and from there to the network of finance companies, financial advisors, institutions and regulators that now make up the Canadian system. The paper argues that the present system, ostensibly centred on the decision making of the individual investor, masks a distributed agency (Callon, 2008; Callon & Muniesa, 2005; Langley & Leaver, 2012) that enmeshes the individual in routine calculative practices designed to limit nonconformity and to ensure the supply of capital to the financial markets. The paper explores the internal contradictions and tensions of the system that ensure this form of government over age-appropriate savings and investment decisions remains perpetually incomplete.

The paper’s focus on the Canadian system of public and private pension plans is useful because Canada’s system is relatively comprehensive and diverse, and has a lengthy history. It therefore serves as a rich illustration of how calculative technologies construct our notions of age. Other countries have different retirement income systems, of course, so the focus here is not on specific features that make the Canadian system distinctive, but on the way that the underlying technologies structure Canadians’ approach to old age. These technologies—accounting, actuarial calculations, mutual funds, tax incentives, and so on—are common to retirement income systems from New Zealand to the USA, from Chile to Great Britain; which can be explained at least in part by institutional isomorphism, through common training of bureaucrats and economists, political mimesis, and the structural interventions of the International Monetary Fund and World Bank (Orenstein, 2008: 409; Himick, 2009).

Prior organization research on aging and retirement has examined the practice of compulsory retirement (Gelb, 1977), the implications of new public management (Underwood, 1984), changing retirement practices and the weakening notion of retirement as complete withdrawal from the workforce (Dychtwald, Erickson, & Morison, 2004; Kim & Feldman, 2000; Jacoby, 1999), and the implications of the expected retirement wave of baby-boom workers (Loch, Sting, Bauer, & Mauermann, 2010). Organization research on age has examined the impact of aging on worker performance (Backes-Gellner, Schneider, & Veen, 2011), the meaning of work and how people cope with losing it (Gabriel, Gray, & Goregaokar, 2010), and the notion of career (Inkson, Gunz, Ganesh, & Roper, 2012). The present paper contributes to this literature by examining how age itself is constructed in our society. It argues that the experience of age through our adult years is shaped by technologies that attempt to put us in a specific relationship across time to other stages of our lives, and contemporaneously to other generations. It further argues that the characteristics of this relationship depend upon the political rationalities that pertain in any given period.

The paper contributes to organizational literature on governmentality (e.g. Brown & Lewis, 2011; Chan, 2000; Ezzamel, 1994; Leclercq-Vandelannoitte, 2011; Marsden, 1993; Newton, 1998), and more specifically to Foucauldian research on pensions and retirement income (e.g. Langley & Leaver, 2012; Ring, 2010). It does this by developing a temporal perspective on subjectivity, showing how modern government—understood as much more than just the state—demands self-governing citizens who anticipate their own future in ways that serve the needs of the capital markets. The structure of the Canadian system suggests that normalizing power/knowledge mechanisms are a key to the development of a system that addresses several different economic classes simultaneously and attempts to encourage specific age-appropriate behaviours regarding savings and consumption. However, the highly variable success of tax incentives in the system suggests that the disciplinary technologies are only loosely effective and require a networked distribution of agency in order to achieve even minimal effectiveness. The paper looks at the implications for individual agency and resistance within this calculative, financialized network of aging.

The paper proceeds by theorizing pensions as a social technology and then giving an overview of the data sources and research methods that underpin this study. Next, it reviews the history of the present Canadian retirement income system, from the first attempts at retirement income provision through to the end of the 20th century. This chronology is periodized into four moments: prior to World War I, between the World Wars, from World War II until the 1980s, and since the 1980s. For each moment, the paper shows how the corresponding programs and calculative practices have structured the notion of the ‘elderly person,’ and assigned responsibility for this person’s welfare, according to the political rationalities of the day. This establishes the contingency of the present retirement income system, permitting a critical examination of the financialization of aging in Canada today. This is followed by a discussion of the implications of the Canadian example for our understanding of how aging is organized socially and politically. The paper concludes with a summary of its contributions and limitations.

Theorizing Pensions as a Social Technology

This paper approaches the topic of age from a governmentality perspective (Foucault, 1979; 1980a; 1991). That is, it seeks to understand how particular calculative practices related to aging shape and are shaped by political rationalities, and how they connect those rationalities to the conduct of individual lives (Miller, 1990; 2001; Miller & Rose, 1990). Governmentality research has been described as a rediscovery of the role of calculative practices in society, where they play a mediating role in government that allows both the representation of distant things and intervention at a distance (Miller & Rose, 2010). Recognizing that government is discursive, governmentality research attends to the interrelationship between calculative practices and the ideas and discourses of government. This approach is appropriate for this paper because it enables us to study how mechanisms and assemblages of calculation become widely adopted, at least for a time, and how they shape and are shaped by contemporaneous discursive constructs such as ‘old age.’

This paper looks at certain calculative technologies and practices in their historical contexts. By constructing a genealogy (Foucault, 1984) of present technologies and practices surrounding retirement and aging, the paper permits us to see how they enact changing political rationalities, and thus to question the seeming necessity of present arrangements. Observing historical discontinuities helps reveal the contingent relations that produce particular notions of age, work, saving and retirement. However, we recognize that these discontinuities are never complete ruptures. Rather, practices and attitudes and the social codes by which the individual navigates her way through life ‘are likely to coexist and intermingle across time’ (Newton, 2004, p. 1378).

The discursive and calculative technologies of the Canadian retirement income system, created and revised over the course of the 20th century, represent attempts to ensure certain socially desirable outcomes for the elderly. The sequence of these attempts can be examined as a series of exercises of power, sometimes mandating certain behaviours but more often relying on a degree of voluntary participation by the individual. Chan (2000), drawing on Miller (1987) and Foucault (1980a), reminds us that power operates by engendering in the individual certain intentions, such that the individual becomes the appropriate kind of citizen, choosing behaviours conducive to the overall governance of society. The individual is thus both the product of power and the means by which power operates. The individual exists in a profound, agonistic relationship with the technologies and structures of power, neither mindlessly obeying nor openly confronting them.

Despite the focus on the individual in governmentality studies, it is important to note the rise of actuarial practices in governance, by which the population is mapped into demographic groups to which programs can be tailored, as opposed to requiring the individual to conform to broad norms for conduct. These practices should not be understood as replacing disciplinary mechanisms of power that operate on the individual, but as a tool for the operation of power, alongside disciplinary and sovereign power, articulating with them according to changing political rationalities (O’Malley, 1996).

The panoply of state programs and corporate plans by which savings and retirement are governed depends on a normalization and collectivization of risk that is central to the aims of liberal government (Knights & Vurdubakis, 1993). However, this strategy of collectivization has in some ways been occluded by the neoliberal shift that has placed the individual at centre stage in the ‘drama’ of retirement savings (Ring, 2010, p. 538). The individual desired by this policy agenda is regarded in technical terms as rational and capable of appropriate decisions, and in moral terms as responsible (Ring, 2010, p. 542). Programs for retirement savings and income have, as a result of this shift, moved from broad inclusive social forms to more individualized discretionary savings plans characterized by incentives to desired savings and consumption behaviours. This is consistent with the neoliberal view that risk, in this case the risk of insufficient retirement income, is not a pathology to be eliminated from society but ‘a source or condition of opportunity, an avenue for enterprise and the creation of wealth … and a crucial condition for generating [individual] responsibility’ (O’Malley, 1996, p. 204).

The new model citizen has failed to live up to expectations, however, and as a result, discretionary savings technologies have not been as effective as either policy or the markets require. As Langley and Leaver (2012) point out, voluntary corporate pension plans have seen low enrolment among employees, limited voluntary contributions by those who do join, and poor allocation decisions by plan members, despite education programs aimed at fostering ‘better’ decision making by potential and actual plan members. To understand these outcomes, Langley and Leaver examine the assemblage of technologies and rationalities in a discretionary-savings pension plan as an example of distributed agency (Callon, 2008; Callon & Muniesa, 2005). Decisions about retirement savings are distributed over a network of experts and functionaries, connected by calculative routines and procedures. Attempts to encourage desired voluntary savings decisions by the individual worker have in some cases been replaced, through the decisions of employers and financial engineers and regulators, by automatic enrolment, automatic increases in payroll deductions, and automatic shifts in investment allocation as the worker ages (see also Ring, 2010). The individual remains nonetheless mired in uncertainty. This is due, say Langley and Leaver, to structural shifts in the capital markets, imperfect allocation decisions by expert fund managers, and the fragile nature of the individual’s own employment and family circumstances. They argue that the ‘paternalistic’ savings mechanisms of contemporary voluntary pension plans, which are deemed by some to have redressed the failures of the worker as a financial decision maker, mask the function of these plans as a security apparatus.

But what does this security apparatus secure? By focusing on Foucault’s definition of ‘despositif’ as a technology for controlling the population, Langley and Leaver (2012, pp. 477–478) skip over the question of why corporations and financial institutions should bother participating in this paternalism. For the same cost, why not just pay higher salaries and leave the employee to decide whether to save for retirement? This paper argues that it is not simply the retirement of the employee, but the flow of capital into the financial markets, that is being secured. As Hardin (2014, p. 113) suggests, the underfunding of individualized pensions threatens not just the employee’s retirement but those who profit from individual investments in the financial markets. Finance companies profit by aggregating and managing these investments, and corporations benefit by gaining access to new capital, in addition to any benefits they may gain in areas like employee relations.

In securing individual retirement and capital flows into financial markets, pension systems rely extensively on accounting and actuarial calculations. Tracking flows of cash, recording deductions from payroll, disclosing pension assets and obligations, and auditing the records of organizations are all examples of accounting technologies embedded in pension systems. Actuarial calculations, styled as ‘actuarial science,’ play an equally important role, with small changes in actuarial parameters producing enormous changes in a company’s obligation to employees (Graham, 2008). Despite referring to their practice as science, actuaries are subject to management influence when estimating organizational parameters like projected increases in wages, not least because managers have hidden knowledge about their organizations.

Actuaries use statistical methods to assess the likelihood of certain future events within a group of people. Actuarial calculations are central to the normalization and collectivization of risk by which the aging population is governed (Knights & Vurdubakis, 1993). Since actuarial calculations are relatively impenetrable to the average person, they form a ‘black box’ that has the appearance of accuracy, correctness and objectivity, despite relying on estimates. Similarly, the perceived accuracy of accounting calculations and the presumed efficacy of auditing practices create a verisimilitude that encourages users of accounting information to see it as objective and reliable.

This enables a retirement savings scheme to function as both a dividing practice and a disciplinary practice. A dividing practice (Foucault, 2003a, p. 126) is simultaneously social and individual in its effects. Through the processes of observation, measurement and aggregation by which calculative government technologies operate, knowledge about the population is constructed and used to divide it into governable subsets, to which specific social programs can be tailored. At the same time, the individual is divided against herself through this observation and representation. She sees a particular objectivized image of herself and comes to understand herself accordingly.

A disciplinary practice involves what Foucault calls ‘technologies of the self,’ which are technologies for the production of truth about an individual (Foucault, 2003a). It is not enough that an observation of an individual’s behaviour be made by an agent of government. Rather, the individual must participate in the observation through ritual self-examination and disclosure to someone in authority. This has roots in monasticism, and implies asceticism and renunciation (Foucault, 2003b; Graham, 2010); resonance with the practice of saving for retirement instead of spending one’s income is obvious.

The following examination of the Canadian pension system illustrates how such dividing and disciplinary practices interact in the governance of society, structuring our understanding and experience of age.

Data and Methodology

This paper proceeds by constructing a brief genealogy of the Canadian retirement income system. Consistent with other genealogical studies (e.g. Newton, 2004), this paper tries to avoid the continuous causal explanations of present institutional arrangements and the unitary narratives of the past that Jacques (2006) cautions against. Rather, it seeks to document certain discontinuities, certain complex interactions of discourses and technologies, that have led to the way things are today. This approach to history derives from Nietzsche (1967 [1887], p. 77) and was taken up influentially by Foucault (1979, p. 31; 1980b, p. 49; 1984). Through genealogy, we can problematize assumptions about the inevitability of present pension arrangements and question the stated purposes of technologies.

To explain the approach to historical data used here, we draw on Rowlinson, Hassard and Decker (2014), who used a series of dualisms to describe various approaches to historical research. In preparing this paper, the author sought to understand singular events, namely the establishment and extension of specific calculative technologies that have shaped the preparation for old age, and old age itself, in Canada. Rather than attempting to derive universal laws from the data, the author sought to situate events within their historical contexts. The study thus seeks to show that present technologies related to aging are not inevitable, but derive from a discontinuous series of historical decisions and events. In terms of evidence, the study recognizes the data sources available as the product of institutionalized relations of power that very much shape which versions of events have survived. The author looked, therefore, for contradictions and gaps, and for indications of alternative perspectives from the past that have survived despite the ‘official’ version of what happened. The author considered both primary and secondary sources, noting that secondary sources in particular represent a narrative that must be critically appraised. The author recognized that positioning any historical document as ‘data’ is an interpretive act in itself, and therefore remained open to other possible interpretations by noting silences in the historical record and by contrasting various sources to ensure multiple perspectives were respected. In terms of temporality, the author explicitly imposed a periodization on events, rather than assuming a continuous, abstract chronology. In other words, the study regards time as an historically situated reality. The selected periods have been chosen to suit the research objective of understanding calculative technologies as historically contingent.

The selection of periods has been based on a working hypothesis that certain major events during the 20th century created the significant social upheaval necessary to open institutions to political reform. Cowen (2008) argues especially that war efforts in Canada have periodically reorganized the country around the provision of social welfare to the soldier. This helps explain the fluidity of the system of social programs after World War I and World War II. However, the forms adopted at each point of reorganization were influenced heavily by political and economic reforms in other western countries. For this reason, the adoption of neoliberal modes of governance in the USA and the UK, which heavily influenced Canadian government policies beginning in the 1980s, were a more significant inflection point than, say, the Korean War of the 1950s or the Gulf War of the 1990s, both of which involved Canadian soldiers. Hence our four periods are the early part of the century, the period following World War I, the period following World War II, and the period following the advent of neoliberal reform in the West during the 1980s.

Historical data for each period have been drawn from government records and archives, as well as secondary sources. Government sources include the records of federal parliamentary debates, annual reports for government departments and programs, government white papers, and committee proceedings. Archival sources include material from the National Library and Archives in Ottawa and the Ontario Provincial Archives in Toronto. Secondary sources include academic histories covering Canadian pension programs, as well as contemporaneous media coverage of specific events and programs.

Federal government records were searched exhaustively going back to 1900, looking for the first indications of concern about the income needs of the elderly. This cut-off date was chosen because, according to the authoritative history of Canadian pension by Myles (1984), the first government program related to pensions was created in 1908. All parliamentary debates in Canada are collected in what is referred to as the Hansard. This is well indexed, which permitted an exhaustive review of all mentions of topics such as ‘pensions,’ ‘retirement’ and ‘elderly.’

In addition, all debate about specific government programs related to retirement income was exhaustively reviewed. These included the two earliest retirement income programs that are no longer in force, namely the 1908 annuities program and the 1927 Old Age Pension program, and the three programs that are still in force, namely the Old Age Security (OAS) program of 1951, the corporate Registered Pension Plans (RPPs) and individual Registered Retirement Savings Plans (RRSPs) that were given tax status in 1957, and the 1965 Canada Pension Plan (CPP). In addition to parliamentary debate, all departmental reports, committee documents and legislation—both the initial acts and all subsequent amendments—were reviewed relative to these programs.

All annual accounting reports for the programs were entered into comprehensive spreadsheets in order to explore how the accounting numbers related to each other, and in order to uncover all extraordinary revenue and expense entries. These anomalous entries indicate such things as changes to funding assumptions, or allocations to or from the pension plan to balance the accounts when actual experience diverged from prior projections.

This paper also draws on archival material from the National Library and Archives in Ottawa and the Ontario Provincial Archives in Toronto. These archives contain official correspondence of government bureaucrats as well as various forms, notes and reports related to their data gathering efforts. This material illustrates how age and retirement were construed at various points in the past century, and helps us see how the various pension programs operated. These archives were explored with as much thoroughness as possible, given the limitations of the reference indices: these indices frequently name a given fonds (collection of documents from a given source) by the donor, making an orderly, indexed search impossible. The reference staff in these archives were invaluable in pointing out files that might contain information about the pensions programs being researched.

To document public discourse on retirement savings, a wide range of commentaries by academics, interest groups and other members of civil society was consulted. This search deliberately sought perspectives different from mainstream economic arguments about pensions; an example is the 1981 conference on pensions organized by the Canadian Centre for Policy Alternatives. These data were searched by following references and citations from one source to another until a broad range of perspectives was represented and further searches failed to include new relevant information or distinctive interpretations of the retirement income system.

To illustrate popular conceptions of retirement in public discourse, electronically indexed news databases were used. From this search, only the Toronto Globe and Mail has been cited. Although many other examples were available, one of the purposes of including news coverage was to illustrate how strongly financial discourse pervades our notions of age and retirement. Restricting the citations to one national newspaper, when many more examples could be given, emphasizes this dramatically.

Calculative Practices and the Construction of Aging in 20th-Century Canada

In Canada, programs and policies related to old age have been elaborated, adapted, revamped and diversified over the course of more than 100 years. As noted above, we examine four periods, separated by the World Wars and the advent of neoliberal reforms in the 1980s.

Pre-World War I

In the early 20th century, central Canada—that is, Ontario and Quebec—became industrialized. This had a profound effect on the largely rural population of the time, as people of working age left their parents in search of wage labour, either in the commercial activities of cities or in remote resource industries such as mining and forestry (Bellemare, 1982). The elderly, who had previously been integrated into extended families, became more and more vulnerable, particularly as the increasing adoption of ‘scientific management principles’ and hourly wages made it hard for older workers to compete for jobs, and indeed led to Canada’s first mandatory retirement policies (Myles, 1984). This was the beginning of the perception that old age is a time when income ceases; in other words, age as an economic condition.

Political responses to this perception were shaped by moral positions on individual responsibility. Members of the opposition parties in Canada’s Parliament called for something to be done to care for the impoverished elderly (Canada. Parliament., 1907–1908, pp. 3381–3384), but the government instead introduced a retirement savings plan that would enable those who were currently working to set aside money safely for retirement through the purchase of government annuities. This program took effect in 1908. Generally consistent with the liberal notions of government prevalent at that time in Canada, it placed responsibility for retirement income on the individual. It did, however, provide those individuals with a government-backed and government-run savings vehicle, in the absence of suitable savings vehicles from the banks and insurance companies. Naturally, the program did nothing for those who were already elderly unless they were wealthy enough to make a lump-sum payment for an annuity, nor for any younger individuals who were too poor to save anything. Government annuities were chiefly subscribed to by salaried employees and professionals, such as teachers and clergy (Carman, 1915, p. 445).

The government annuities program ran from 1908 until the mid-1970s, although active sales ceased in the 1960s. It segmented age into two phases, one in which one earned and saved—either on one’s own or by investing regularly in deferred annuities—and another in which one consumed one’s savings. Responsibility for saving rested entirely with the individual.

For seniors who were less well off, charitable institutions run by local municipalities and churches offered care. These institutions proliferated to address all sorts of social needs, not just old age. The names of these institutions provide us with a lesson in how social categories have changed over time: the Parkwood Home for Incurables, the Widows’ Home, Mountainview Sanitarium, the County House of Refuge, the House of Providence, the Orphans’ Home, and even the Home for the Friendless (Archives of Ontario, 1928a). It is important to recognize that social categories shift as our technical capacity and our political will to address them change.

Old age prior to World War I was construed by government programs as a time of either self-sufficiency or destitution. Those who did not buy annuities and did not end up in institutions were the unknowable majority, unaddressed by any program.

The inter-war years

The return of veterans following World War I created a demand for new social contracts involving both employers and the state. While many veterans were disabled and unable to work, the rest flooded the labour market looking for jobs. These conditions led to a period of labour unrest, highlighted by the Winnipeg general strike in 1919. Industrialization in central Canada and the embedding of payroll accounting systems in manufacturing corporations provided the necessary technical conditions for corporate pension plans. Previously available only to senior managers, these plans became tools for labour relations between the two world wars. McCallum (1990) argues that pension plans, along with assistance in purchasing homes and systems to encourage savings and thrift among employees, were part of a corporate welfare agenda at this time intended to secure management control over production and to ward off government regulation of industries. The earliest plans varied widely from simple wage-deduction savings plans with interest paid by the company, to stock purchase and profit sharing plans. They began to be standardized in the 1920s and 1930s, in parallel with the gradual standardization of early forms of worker representation into formal trade unions. This led to corporate pensions being associated in Canada with unionized labour (McCallum, 1990).

For workers who were not unionized, the continuing program of government annuities provided a retirement income option. The needs of the elderly poor, however, were not addressed directly until 1927, when a federally funded, provincially administered program of means-tested pensions was created for those who could demonstrate their poverty. Lacking any a priori mechanism for telling who was in need and who was not, the provincial governments instituted invasive processes for assessing the financial means of people applying for benefits. Applicants had to allow a government inspector into their home, to whom they disclosed their income and assets. All assets were deemed to provide an income equivalent to whatever their value would earn if invested. Thus, owning a home reduced the amount of pension a person was entitled to receive. If a pension was required in excess of this entitlement, the provincial government would grant the pension but place a lien on the property, allowing it to recover some of the money upon the death of the pensioner. In addition, adult children were expected to provide for their parents, further reducing the potential pension. In fact, one province insisted that elderly parents who claimed that their children could not support them must sue those children for support before they could qualify for a pension (Vancouver Sun, 1941). The program thus propagated a view of old age as a time of dependency on the younger generation, while in some cases creating intense and personal intergenerational conflict.

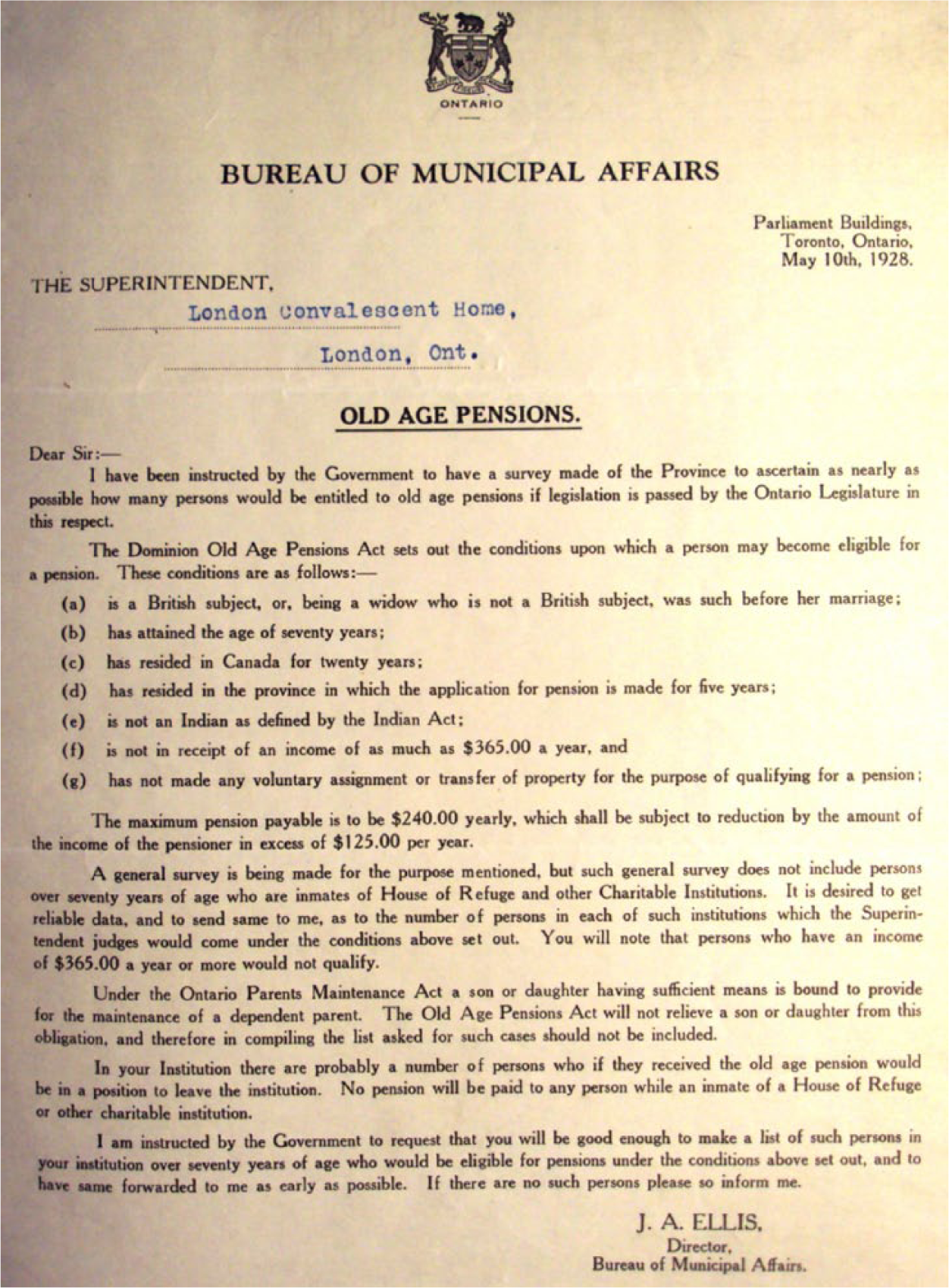

To further understand how this program shaped the social construction of age, we can look at how it transformed other social categories. One of the first activities of the provincial government of Ontario, once the program was announced in the late 1920s, was to assess the population of inhabitants of the province’s various charitable institutions, to see how many might leave institutional care if they qualified for a pension. In 1928, the provincial Director of Old Age Pensions sent form-letter inquiries to each ‘house of refuge’ in the province. The letter (see Figure 1) noted that the government needed ‘reliable data.’

Letter dated May 10th, 1928 from Bureau of Municipal Affairs to London Convalescent Home.

As a dividing practice, this initiative depended on data distributed widely among various institutions; there was no central database, no centre of calculation to drive government policy decisions. Even the distributed data might be inadequate: ‘Without a tedious questioning of each of the thirty or so patients listed I could not answer all the questions asked,’ replied the head of one local institution in a letter dated 28 September 1928 (Archives of Ontario, 1928c). Thus, the effectiveness of diagnostic and programmatic efforts was limited by available technologies, and also limited politically, not just at the level of policy makers who debated what to do but also at the level of individual practitioners and administrators, who resisted the attempt to remove wards from their care.

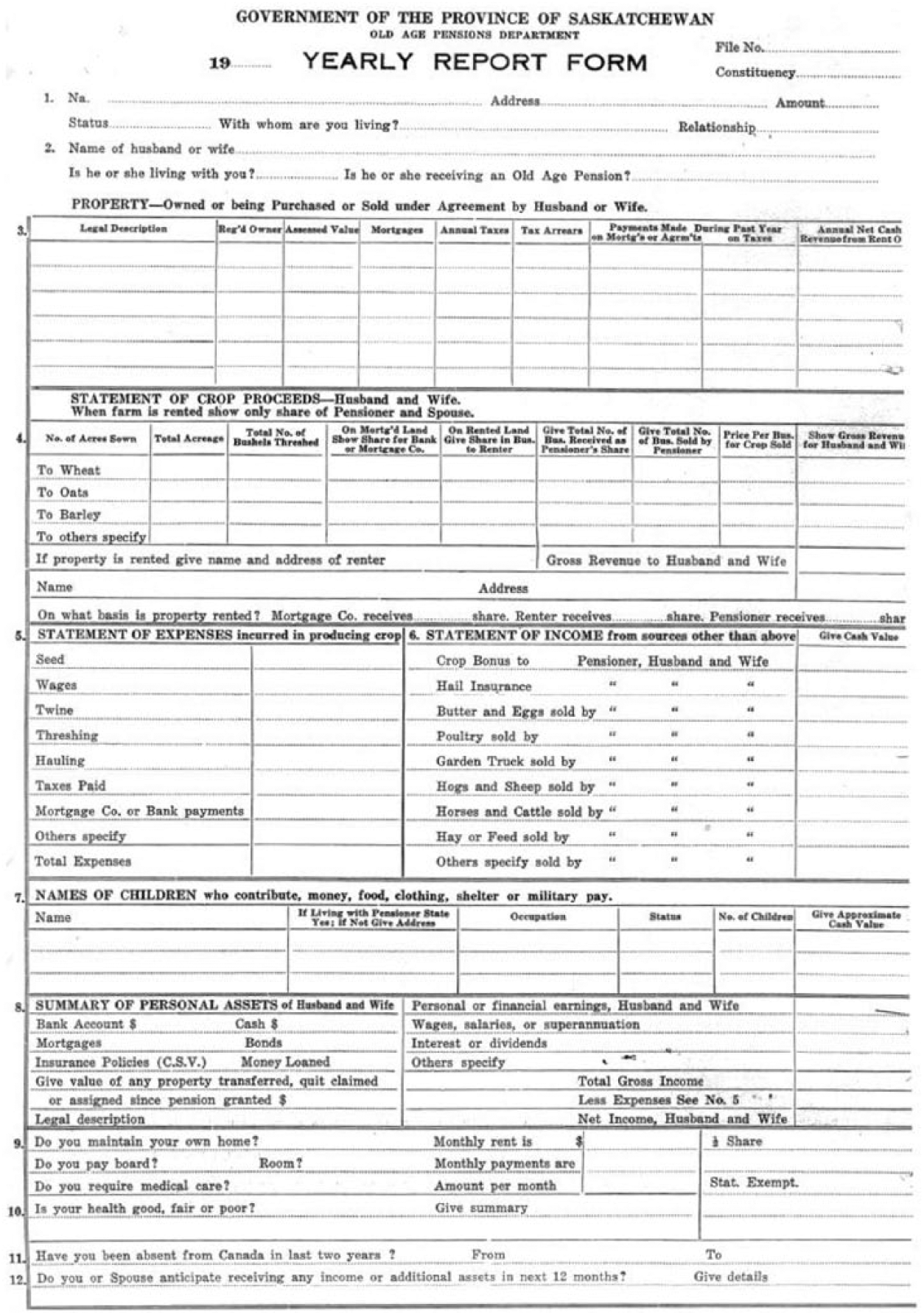

What we see in this program is a crude form of governmentality: there was no mechanism for knowing the population until individuals self-identified by applying for the pension. Once they did—or more to the point, if they did—then they were subjected to a visit from an inspector who entered their home to assess their income and wealth, recording everything on a form they had to sign. The form (see Figure 2, from Saskatchewan and quite clearly tailored to farming), once completed, reflected back to them an image of themselves as economic entities, based on information pried out of them by the inspector.

Yearly report form of Old Age Pensions Department of the Government of Saskatchewan for the year 1941.

According to Foucault, technologies of the self are successful because they involve the individual in self-description (Foucault, 2003b). Having originated in monastic practices of confession to a religious superior, these technologies were transformed into routine bureaucratic practices befitting the secular state. Yet the assembling of this calculative narrative by a pension inspector was anything but routine for the applicants. It was invasive and extraordinary. It constructed age as adversarial, pitting adult children against elderly parents and the individual against the state. What was intended as a means of providing for the elderly poor instead isolated them. This was a dividing practice that cut through families. It also cut clumsily through the demographic of elderly persons, identifying some of them as needy and leaving the rest unknown and unknowable.

Prior to the dramatic industrialization of Canada during World War II, it was not possible for the government to know much about the population, apart from the national census conducted every decade. It was certainly infeasible to create a pension program integrated with employers’ payroll systems. As the head public servant responsible for the government annuities program put it in an internal memo to the Prime Minister in 1931: The large proportion of the population engaged in agriculture makes assessment upon wages impracticable. The mobility of labour in the employed occupations also imposes a difficulty. (Superintendent of Insurance, 1931)

Canada was simply not as industrialized as other countries, such as Great Britain, which introduced more comprehensive socialized pension programs ahead of Canada. However, the Canadian system now contained three separate methods of providing retirement income, with three separate ways of constructing age. Government annuities continued to be available for moderately successful people who were disciplined and thrifty. For them, advanced age was a time of individual self-sufficiency backed by the security of the state. The second method, the means-tested program, constructed age as a time of need and failure—and not just personal failure but the failure of the family. During the 1940s, Canadian employers began to purchase group annuities from the government for employees, consistent with the corporate welfarism behind the third method, corporate pension plans. For these employees, age was a time to reap the benefits of a collective, contractual relationship to industry.

The three elements of this system suggest differing notions of old age as a target of governance. Revising previous conceptions of the elderly as either self-sufficient or destitute, the destitute elderly were now construed not as recipients of charity but as having failed morally to secure their elderly years. Retired union workers, in contrast, were positioned as members of a collective who received the earned benefits of a specific contract with their employer, resulting from their lifetime contribution to the firm.

The three elements of the system also illustrate variations on agency. Those who involved themselves in the annuities program did so by choice, electing to turn over their savings to the state in exchange for a secure income stream. The means-tested program was a site of defiant resistance for some elderly people in need who refused to apply, refused to be subjected to its invasive assessment and pitted against their children for financial support. Corporate pensions for workers were born in a crucible of active resistance and conflict between collectivized workers and corporate management.

Corporate pension plans were embedded in existing organizational routines, taking advantage of wage deductions at the source. Neither government program did this. As a dividing practice, corporate pensions relied first on hiring decisions and then on unionization, while government pensions relied on self-identification by individuals, both in the purchase of government annuities and in the application for a means-tested pension. As a disciplinary practice, the corporate pension relied on narratives related to collectivization. Government annuities did little to discipline the individual to savings behaviours, while means-tested pensions relied on invasive, quasi-confessional assessments to enforce self-examination after the individual had already reached old age.

Both government programs continued to rely on self-identification to enroll individuals. Income taxation provided the state with a way to identify individual workers and collect information about them over their lifetime, but of course it did not identify non-taxpayers, and so excluded many women and the poor. It was not until the creation of the Social Insurance Number in the 1960s that the state acquired the means of identifying and tracking virtually all adult Canadians. We see this broad surveillance at work in the next phase of programs.

Post-World War II

In the 1950s and 1960s, consistent with a growing acceptance of social welfarism in Canada, a trio of retirement income programs was established that leveraged the Social Insurance Number and the income tax system to address overlapping segments of the population. The individual as a card-carrying member of society—the white ‘SIN’ card became ubiquitous—was plugged into these programs according to his or her tax status. Meanwhile, the means-tested pension program was cancelled and the government annuities program gradually phased out.

The first of the three new programs to replace them was Old Age Security (OAS), in 1951. It offered all Canadians a small, fixed pension upon reaching the age of 70, preventing destitution in old age but not permitting luxury. The simplicity of this program belies its importance to the overall system. As the only truly universal program, it permitted the government to assert equality in its policies. As a program funded by specific new surtaxes, it permitted the government to make explicit the cost of this equality.

The surtaxes at a rate of 2% were applied to corporate income tax, individual income tax, and manufactured and imported goods. This meant that the program relied on the ability of organizations to account for their income and expenses, and on the ability of the state to acquire this information reliably. It similarly relied on the reporting of personal income, which could be verified in the case of wages by comparison to corporate payroll information. Finally, it relied on corporate inventory and sales information for manufacturing and importing. All of these sources of information required systematic, routine compliance by the individuals and firms, as opposed to the sort of extraordinary investigation by inspectors seen in the means-tested program. Routine accounting procedures and voluntary compliance, albeit with the threat of legal penalties for non-compliance, made Old Age Security an interesting example of governmentality. Operating entirely through organizational bureaucratic routines, it did not involve the individual in the production of truth about herself, save for the ancillary calculation of the income tax surtax. Even this would disappear in later modifications to this program, detailed below.

The second program was the Registered Retirement Savings Plan (RRSP) of 1957. This was a tax-deferral system designed to extend to individuals the same tax advantages as those enjoyed by members of corporate pension plans. With corporate plans, individual members did not pay tax on their pension benefits until they received them. This makes perfect sense: the corporate pension plan was effectively a way for the company to defer paying wages, so the worker was not charged income tax on those wages until she was paid them under the pension plan. With an RRSP, individuals could make voluntary contributions to their own savings plan out of the wages they had received, and, just like corporate plan members, defer paying tax on the contributed money until it was withdrawn again after retirement. Because of progressive taxation rates, that is, low income tax rates on the first portion of annual income and progressively higher rates on additional portions, the overall tax rate paid by the individual could thus be reduced, in addition to deferring the actual payment of the tax.

The third program was the Canada Pension Plan (CPP) of 1965. Like OAS, the CPP was considered universal. However, unlike OAS benefits, CPP benefits varied with one’s income level. Within limits, the more one earned, the more one paid in CPP contributions while working and the more one received in CPP benefits upon retirement. This was similar to registered pension plans, such as the RRSP. The chief differences between the CPP and the RRSP were that CPP contributions were mandatory, the employee’s CPP contribution was matched by an equal contribution from her employer, and CPP contributions made were not actually set aside for the worker’s own retirement. Rather, they were used to pay current CPP benefits to others who had already retired, with only a minimal two- or three-year buffer of accumulated funds. The CPP was, therefore, largely an intergenerational wealth transfer. The demographic reality of the baby boomers, Canadians born in the decade after World War II, meant that this intergenerational transfer was quite effective for many years. Large numbers of workers supported a relatively small number of pensioners. However, as this boom levelled off and moved closer to its own retirement, this would eventually cause a funding problem.

Alongside these three public components of the Canadian pension system, corporate pension plans continued to play a prominent role. By the middle of the 20th century, companies began to use corporate pensions for unionized employees, not just to secure their access to labour and their control over the organization, but as a way of deferring some of the increasing costs of worker compensation. This led to the development of the defined benefit (DB) pension plan, that is, a plan that specifies the amount of pension the company is obliged to pay a given worker upon retirement.

The risks associated with meeting this obligation were contractually placed on the shoulders of the employer, which was required by government regulation to set aside funds and invest them conservatively in order to pay future benefits. These plans reached their peak membership towards the end of this phase of our study, coinciding with a peak in union membership around 1980 (Visser, 2006). As long as labour forces grew, DB pension plans remained healthy, in Ponzi-like fashion: there were always enough new contributions coming in to meet the demand for benefits. This would have been verified by the professional calculations of actuaries. The appearance of robust financial health was reinforced by nearly monotonic growth in the plans’ invested assets, due to the health of the overall economy. Many DB plans grew to the point where they rivaled or even dwarfed the corporation’s own balance sheet. Minor fluctuations in the huge asset and obligation values would have swamped the financial performance of the company, good or bad, were it not for intricate smoothing calculations permitted by accrual accounting regulations (Graham, 2008, pp. 779–780). The legal separation between the trust that owned the plan and the corporation that had made contractual pension obligations to its workers was a one-way barrier. The corporation would always have to make up shortfalls, but could not benefit from surpluses, apart from being relieved for a time of the burden of making cash contributions to the plan.

Together, the programs and technologies of this period constructed a comprehensively different notion of who is responsible for the elderly, compared to the earlier period of government annuities, means-tested pensions and primitive corporate pensions. In mid-century, the state played a major role in redistributing income from the wealthy to the needy, from the working to the retired. It is worth noting that the earliest recipients of CPP benefits did so without contributing much, if anything, to the plan. As noted above, the CPP was run almost on a pay-as-you-go basis. The OAS and CPP therefore involved little actual saving. Corporate DB pension plans were ostensibly savings mechanisms, but investment of funds in the financial markets meant that sometimes, when investments did well, contributions were not required. The RRSP thus stood alone as a clear savings plan, as well as the most individualized program in the system. Provision for old age was thus mainly a collective responsibility during this period. Age was explicitly constructed in relation to others through social wealth transfers, and in relation to one’s membership in collective plans.

This was not an undifferentiated collectivization, however, as each part of the system was relevant to different classes. The system rested on a panoply of dividing practices, segmenting the population along employment and wealth lines. For all wage earners, the CPP represented a broad social contract around old age. For unionized labour, corporate pensions continued to frame old age as a time of financial security earned in solidarity with fellow workers. For those with minimal incomes during their working lives, Old Age Security framed old age as a time of solidarity with the rest of society, thanks to universal income security. For RRSP contributors alone, financial security in old ages was a result of one’s individual savings habits.

The system as a whole rested on assumptions about the elderly as participants in the social contract between citizens, between one generation and another, as well as between the individual and either the state or the employer. The role of disciplinary technologies was weak, with most of the calculation being done behind the scenes by unknown accountants and actuaries, resulting in a pension benefit upon retirement, the total amount of which may or may not have come into the consideration of the individual until retirement loomed.

Since the 1980s

This complex, layered and largely collectivized version of age persisted until the 1980s, when the Canadian retirement income system began to be impacted by neoliberal reforms. Associated with Thatcher in the UK and Reagan in the US, these reforms swept many western countries, Canada included. Coupled with the advance of the baby boom generation through the workforce, and the spectre of large numbers of them retiring in a few decades, the reforms touched every part of the system.

Old Age Security was the least affected, but even it was changed from a fundamentally universal program when its flat-rate benefits became taxable in 1989, for Canadians in high income tax brackets. The Canada Pension Plan, also universal but with variable benefits that depended on lifetime earnings, was much more dramatically altered. In 1996, concerns about the long-term cost of the CPP led to major changes in its funding model. Contribution rates were raised to create a surplus in the plan. This surplus was invested in the capital markets through an independent board, the CPP Investment Board, created for the purpose. These changes paralleled those in other countries, as public pension plans were subjected to neoliberal transformations that attempted to individualize and marketize social benefits programs (Himick, 2009). As with the RRSP program, the new arrangement aligned the interests of Canadian workers with the capital markets, albeit at arm’s length and without the immediacy of a personal monthly statement connecting one to rising and falling stock prices. The arrangement increased considerably the funds available to the capital markets. The CPP Investment Board has since become one of the largest institutional investors in Canada.

Registered retirement savings plans also went through big changes. They had originally been restricted by law to conservative fixed-income investment instruments. In the 1980s, RRSP owners were allowed to invest their funds more directly in the capital markets through mutual funds. This seemingly banal change was a marked shift in governance, for it attempted to align the interests of the average working Canadian directly with the capital markets. Prior to this point, few working Canadians owned stocks. Afterwards, ownership of stocks became extremely popular, especially indirect ownership through mutual funds. Financial innovation of this sort was crucial to the success of this program. Mutual funds were popularized by books such as The Wealthy Barber (Chilton, 1989), which demonstrated with a folksy narrative the benefits of regularly investing relatively small amounts of money early in one’s career. Personal involvement in the savings process and in the capital markets was heightened by the receipt of monthly statements documenting one’s transactions and indicating the (usually increasing) balance in one’s savings plan. For the first time, large numbers of individual Canadians could see and measure the personal impact of fluctuations in the stock markets. The effect was heady, given the pronounced rise in those markets through the last two decades of the millennium.

Corporate pensions also changed significantly during this time period. Defined benefit (DB) plans began to be replaced by defined contribution (DC) plans, which stipulate the contribution the employer must make to the employee’s pension account. This contribution is heavily influenced by actuarial calculations, to try to ensure that it is sufficient for retirement income requirements. However, once that contribution is made, the employer is largely absolved of responsibility. The funds are invested and whatever they are worth upon retirement is what the worker gets.

DC plans do less to bind the employee to the employer, compared to DB plans, but like the RRSP, they explicitly serve to align the worker’s economic interest with the performance of investments in the financial market. Importantly, they also individualize the connection between the employee and the pension arrangement, shifting the power relations between employer and employee dramatically and reducing the influence of the union by removing the collective pension fund from the field of struggle; however, items like coverage of part-time workers and the size of the DC contribution remain open to union negotiation. As noted above, DC plans have largely failed to entice workers to make voluntary contributions, resulting in various mechanisms to automatically increase employee contributions and automatically adjust portfolios for risk as retirement approaches (Langley & Leaver, 2012).

Retirement income programs in Canada had taken a collective turn from the state to the markets, with a greater emphasis on individualized outcomes. OAS benefits were now taxable for high income earners, CPP reserves were now invested in the financial markets, RRSPs could also be invested in the financial markets, and corporate pension plans now connected to the individual instead of the union. The retirement income system now hinged on the performance of the financial markets and, both practically and ideologically, on the savings and investment decisions of individuals.

The impact of all these retirement savings changes on age discourse was transformative. Initially under neoliberal reforms, old age began to be portrayed as a promised land of financial independence, particularly in advertisements for finance companies. One example was the ‘Freedom 55’ campaign mounted by the London Life Insurance Company, launched during the 1980s, which encouraged workers to set aside more than they needed for retirement at age 65 in order to enjoy a life of luxury sooner. Middle age was turned, at least in these advertisements, into a time of fantasizing about the future. Old age became a phase of life to be managed and enhanced by prudent economic planning, a time to reap the rewards one had sown earlier in life. Later, during the 1990s, concerns about the viability of corporate and social pension programs led to old age being portrayed as a time of financial crisis, a future crippled by pension expenses we could not afford. This message came from every direction, including the World Bank (1994), the news media (e.g. Robson, 1996; Turner, 1995), corporations pleading poor to their unions (e.g. Sudbury Star, 2001; Watson, 2001), and the federal government itself (Department of Finance, 1996).

The Financialization of Aging in Canada Today

These portrayals seem contradictory, but they are entirely consistent. Both images serve the needs of the capital markets. The positive image enlists the savings of individuals, enticing them with a promise of wealth through ownership of stocks and mutual funds, suggesting that they can break out of the working class if they invest their savings in the stock markets. The negative image enlists the savings of the state by portraying socialized retirement income programs as bankrupt, demanding increased state contributions to these programs, and insisting that the funds be turned over to the markets. This was done with the CPP in 1996 and with similar programs in other countries (Graham, 2010; Himick, 2009).

While restructuring public pension programs to enlist them in the service of the markets has met with success in country after country (see Orenstein, 2005, p. 187 for a list), the enlisting of private savings and the encouraging of desired savings and investment decisions has in many respects fallen short. The individual wage earner has been offered substantial tax incentives, yet aggregate RRSP savings under post-1980s regulations have never kept pace with the permissible amount of savings. Unused ‘room’ in RRSP accounts exceeding $250 trillion by the end of the 20th century (Li, 2002).

This has occurred despite the enormous advertising efforts of mutual fund companies and financial advisors. Like most advertisements, the ones for financial products are ‘airbrushed’ to remove the warts. The people shown in the advertisements (see Figure 3), whom we understand to be better versions of ourselves (Ekerdt & Clark, 2001, p. 58), are successful. They do not appear to have any worries, not even about the instability of the financial markets that investors can read about on a daily basis. Mutual fund advertisements rarely discuss risk (Jones and Smythe, 2003, p. 38). The image of financial security in investment advertisements is thus just as heavily distorted as the image of beauty in fashion advertisements.

A stock picture taken from a London Life ‘Freedom 55’ advertisement.

It should not be surprising that a savings regime predicated on the consumption of financial products would be filled with contradictions and achieve ambiguous results. Yet advertising is only a small part of the effort that has achieved such mixed results in constructing the individual as investor. Newspapers abound with advice from personal finance gurus who almost always convey the message that Canadians are not saving enough for retirement: ‘One-third of young Canadians have no retirement savings’ (Luciw, 2012a), ‘Are you saving enough?’ (Dalglish, 2012), ‘Do I have enough money?’ (Investopedia.com, 2012). Young adults are urged to contribute to RRSPs as early as possible (e.g., Luciw, 2012b).

A burgeoning industry of financial advisors and experts also attempts to shape savings and investment behaviours. In 2006, there were 288,000 Canadians employed in the financial advice industry (Investment Funds Institute of Canada, 2010). In meetings with their financial advisors, Canadians can recapitulate the monastic rituals of confession and penance from which modern technologies of the self are derived. Individuals can open up private areas of their lives for examination to an expert who prescribes the correct rituals of investment practice for their particular stage in life. They can also refuse to buy into this ritual, however. It can be treated as merely an obligatory point of passage, no more important to one’s notion of age than renewing a driver’s license.

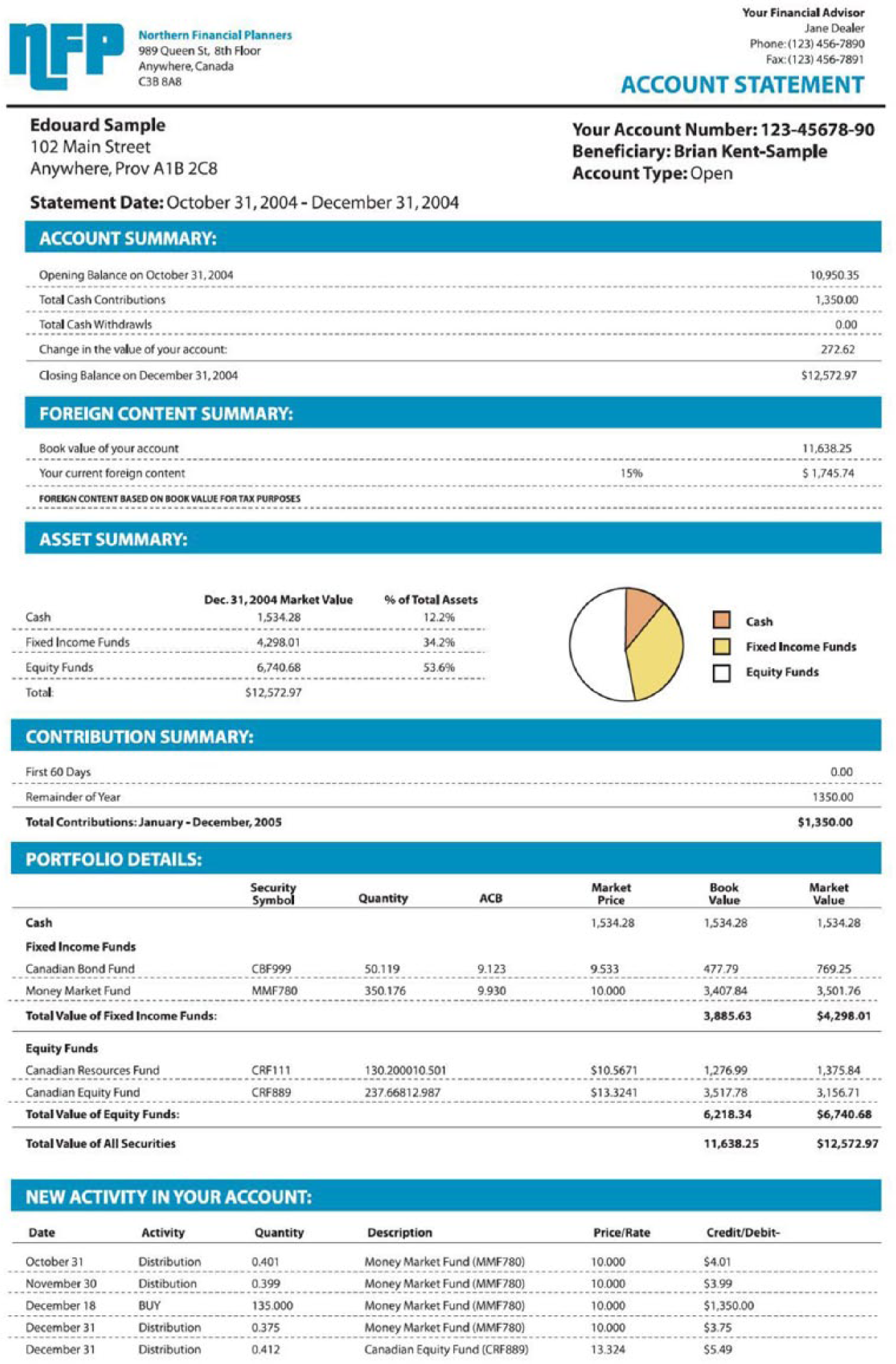

Despite, or perhaps because of, this ambiguous relationship between advisor and client, finance companies expend considerable effort to craft the images they present to their customers. This extends especially to their carefully prepared monthly statements. Statements of investors’ assets reflect their past choices and behaviours, even as they convey the professionalism and clarity of the finance firm itself and even though the choices may have been automated. These statements purport to narrate the investors’ financial lives, a narrative they have co-authored with their expert advisor. A typical monthly statement (see Figure 4) contains a section identifying the account holder and the beneficiary who will inherit the funds if the account holder dies; a summary section describing the changes in the account value over the past month; an asset breakdown, stating in numbers and sometimes graphs how much of the account is held in foreign investments, in cash, in equity funds, and so on; a summary of tax-deductible contributions; and details of every investment held and every transaction that occurred in the account.

An example of an individual retirement fund statement.

These statements are about the production of trust and the production of the individual as an investor. They assure us, as readers, of the validity of our investments. The carefully tallied numbers and the formality of the prose accompanying the numbers convey an image of correctness and impeccable record keeping. The statements say, ‘Your money is in safe hands.’ The layers of assurance, from the regulations of the federal government and the capital markets to the mundane daily routines of the financial firms and the assiduous checking of their auditors, all combine to tell us that what we have done with our money—setting it aside for old age—is prudent and appropriate. At the same time, the statements describe us as owners of a growing portfolio of wealth. Considerable effort goes into educating the consumer to comprehend this, both in public schools where practical financial skills are now part of the curriculum, and in private educational efforts. For instance, the Investor Education Fund, a nonprofit organization, has been created to teach consumers about investing, including how to understand an investment statement. It was established by the main financial market regulator in Canada, the Ontario Securities Commission, to provide ‘unbiased and independent financial tools to help you make better money decisions’ (Investor Education Fund, 2012). ‘Unbiased’ means not biased towards any particular financial company. It does not mean unbiased about the finance industry or the best way to provide for the elderly.

It is worth pausing to note that a securities regulator believes that the formation of educated consumers is part of its mandate. The construction of the financial markets and the construction of the individual go hand in hand. The system needs both trustees and trusters. The investment firms must be able and willing to produce suitable images of the investor, and the individual investor must be able to make sense of the image.

The objectified image of the prudent investor in financial advertisements forms the ideal against which we evaluate the objectivized image of ourselves in the investment statements. We evaluate the performance of our investments and, by extension, our own imputed performance as economic decision makers: we come to know ourselves through these externalized images. We can see if we are participating in the retirement income system in age-appropriate ways.

The finance industry is aggressively working to open up new markets for its services by shaping the notion of old age. The kind of people we need to be depends on our expectations for the future, and we are now being told that our future is not about retirement but about caregiving. ‘Longevity’ seminars (e.g. HollisWealth, 2013) have been launched to convince us to set even more money aside for retirement so we can give our aging parents and our future senescent selves the financial means to avoid socialized elder care. When investment is constructed as a moral responsibility (Ring, 2010), one simple way to increase the amount we invest is to add new responsibilities.

The notion that we will live longer than previous generations has therefore been seized upon by finance companies and their latest promotional tool, the elder care consultant. These tell us that old age now has three phases, not one: early, middle and late old age, with corresponding levels of mobility and zest for adventure; that frailty and dementia are the top categories of risk; that 40% of spousal Alzheimer caregivers will die of stress; that caregivers have a 63% higher death rate than others their age; and that women spend 17 years caring for a child and 18 caring for a parent (Randall, 2007). This goes hand in hand with the recognition by the pension industry that increasing longevity is the newest risk to pension funds, with major industry conferences organized to address it (Pensions Institute, 2012).

The redefinition of old age as a time to receive expensive care instead of a time of independent leisure, and adulthood as a time to prepare for this new responsibility, brings us almost full circle back to the liberal assumptions of the early 20th century, when caring for the elderly was a family affair. The difference now, under neoliberalism, is that these responsibilities have been mediated by the finance industry and its legions of expert advisors. This is paralleled by a transfer of physical caregiving duties from family members to professional caregivers, at least for those who can afford to do so. Decisions about how to manage care and how to fund it are now integrated into decisions about how to save for retirement.

There is no reason to expect that this increased demand for savings will be met by individual decision makers, any more than was the demand for basic retirement savings. The limitations of the disciplinary approach to savings, based on tax incentives, training and intensive advertising, has necessitated the construction of automated savings, investment and even disinvestment mechanisms throughout the system. Financial products such as reverse mortgages now exist to smooth the consumption phase of retirement. In fact, the consumption of wealth during retirement has become mandatory in Canada. Tax laws require that one’s RRSP funds be moved into a Registered Retirement Income Fund (RRIF) by the age of 71. RRIFs can continue to grow through dividends, interest and increases in market value, but a minimum amount, determined by actuarial formulae, must be withdrawn each year. This prosthetic or paternalistic approach to distributed agency is the neoliberal equivalent to the ‘nanny state.’ It is far removed from the espoused ideal of free markets. The gap between the ideal and the reality of neoliberal governance is partly the result of basic contradictions described above: the predication of a savings regime on the consumption of savings products, and the marketing of old age as a time of luxury while social programs for retirement income are dismantled because they are deemed too costly.

This gap will not be closed. It is necessary. It is linked to fundamental uncertainty about how different investment classes perform, which drives both investment and financial innovation for the insatiable capital markets. The individual must be kept in a state of permanent uncertainty, so that she or he can be constantly remade (Langley & Leaver, 2012, pp. 481–482). This is why the responsibilities of people of working age and the requirements of people of old age are constantly being redefined. The network of financial technologies and experts that create retirement savings and income are indeed a security apparatus, as Langley and Leaver point out, but the profound integration of the finance industry and the state means that the security needs of the capital markets cannot be separated from the security needs of the state. Hence, the security needs of the capital markets depend on the insecurity of the individual. The government of aging is therefore necessarily focused on the construction and reconstruction of financial subjectivity, backed up by the distributed network of expert agents and automated technologies to reinforce required behaviours. These behaviours are not guaranteed, however, because the individual’s uncertainty might result in an indefinite postponement of her investment decision.

The retirement income system, though highly technical, is driven by discursive moves that attempt simultaneously to reshape individual expectations concerning age and reconfigure political interest groups. For example, in 1985, the Canadian government proposed de-indexing OAS benefits to save money, but backed down under stern opposition from seniors. This was one of the first signs in Canada that the elderly were becoming a significant political force. The next attempt to reduce OAS costs, when OAS benefits were made taxable in 1989, was successful. The key to success was setting the threshold for the ‘claw back’ fairly high. They are now set at almost $70,000, an income level that means only 6% of OAS recipients pay tax on their benefits, and only 2.3% have all their benefits taxed back entirely (Jackson, 2012).

Then, in 2012, the federal government raised the age of eligibility for OAS from 65 to 67. This was again justified on the basis that OAS was too costly (Flaherty, 2012; Grant, 2012). This particular change was interesting because a simple alternative would have been to freeze the income levels at which OAS became taxable. If these levels were frozen instead of being indexed to inflation, gradually the proportion of OAS benefits taxed back from wealthier individuals would have increased. The decision instead to raise the age of eligibility indicates that the federal government, which at the time was a fiscally conservative party, wanted the cost reduction to be very visible, perhaps even provocative.

The change from 65 to 67 was an implicit decision to change part of the definition of when ‘old age’ begins. This demonstrates that our notions of age are caught up in other social constructions, such as the cost of government. Framing a program in terms of financial cost, as opposed to social benefit, means that the program is experienced as divisive rather than unifying: OAS benefits are universal but the cost is borne unequally, since not everyone pays taxes.

It is no coincidence that these changes were enacted, not as part of a bill on Old Age Security, but as part of the government’s routine budget process. This positioned the change as a matter of fiscal constraint and sound financial management, something the governing Conservative party claimed as its strength. But because the change centred on the very visible change in age limit rather than incremental taxation rates or other technical variables, it was sure to attract attention. This suggests that the effort of ‘reining in’ the apparently burgeoning cost of the elderly to society is as much symbolic as it is substantive. Critics and political foes even suggested that the financial ‘crisis’ in the Old Age Security program had been manufactured by the Prime Minister (Curry, 2012). Whether or not this was true, the linkages between age and cost are clearly crucial to contemporary political discourse, which accepts and reinforces the financialization of age.

Discussion and Implications

This examination of the Canadian retirement income system has important implications for our understanding of how age is constructed in society. From the earliest examples, we have seen how political responses to issues of aging have been driven by normative positions on individual responsibility, as well as by technical capabilities that have enabled the reshaping of old age. The creation of new social programs based on financial technologies, such as pension accounting and tax returns, transforms our social categories, changing a person from a ‘widow’ who belongs in a house of refuge to a ‘pensioner’ who belongs in her own home. We have seen how changes in economic beliefs about what should be done by the public sector, the non-profit sector and the corporate sector are connected with changes in the sometimes negative labels used to describe the objects of social policy, be they the ‘insane,’ the ‘friendless’ or the ‘elderly.’ We have seen how major upheavals like the world wars have provided the opportunities for change, while major shifts in political economy from liberalism to welfarism to neoliberalism have provided the discursive tools to reshape the system.

While the features of individual programs in Canada may now differ from those of other western countries, and while the overall system of programs may be more or less comprehensive than in other countries, the Canadian example demonstrates a number of important aspects of the construction of age and the government of aging in western societies. The use of overlapping programs allows policies to be tailored to different income groups and age brackets. Reliance on demographic information, obtained through census taking and income tax returns, allows the impact of policy to be measured and the programs to be refined. The information flowing through the system depends on the implementation by employers of routine standard practices, such as biweekly payroll and the withholding of income tax. It also depends on financial firms producing monthly investment statements that feed back to individuals their status as savers and investors.

All of this blurs the boundary between the state and the private sector, or at least makes the organizations involved so interconnected in their data systems that the boundary is complex and permeable. Responsibility for the specification of certain aspects of these systems, such as the substantive content of data feeds, may rest officially with the state, but the technical capability to design and administer the systems is distributed among both public sector and private sector employees, through practices such as management consulting and outsourcing. It cannot be said that even such a clear policy decision as raising the age of eligibility for Old Age Security is purely a ‘government’ decision, because such changes involve considerable consultation with and lobbying by finance companies, major unions and nongovernmental organizations.

The programs that result from these inter-organizational collaborations and contestations affect the self-formation of the individual to varying degrees. Certain programs, the contributory ones especially, can involve direct participation by the individual in the construction of narratives of the self. This process attempts to shape the individual into a self-governing person suited to the pertinent programs. The reflection of the self in the mirror of these systems is reinforced by the normative images used by these companies in their advertising. The relevant behaviours of the individual are measured and laid out for reflexive analysis, thanks to the data-processing capabilities of corporate and governmental accounting systems, which support the whole edifice of financial management from the level of the individual to the level of the financial markets and the state. Thus the dividing practices and the technologies of the self are integrated into a totalizing and transformative tool of governance. Power operates through this production of knowledge. Retirement becomes thinkable. The individual, it is hoped, is prepared for retirement. Yet, the preparation is incomplete, so decision making must be redistributed through automated savings and investment technologies for the young, and automated consumption technologies for the elderly. Age and aging are rendered administrable thanks to financial prostheses.

Even so, many choose not to wear their prosthetics, some because they would rather spend and others because they are simply too poor to save. Only the former category can be said to actively resist programs of government related to retirement income. When the individual is posited as a consumer of retirement income products, the decision to buy something else always remains a possibility. Yet resistance, just like the savings decision, is also distributed. Employers can resist increases to pension benefits that they will have to partly or fully fund. Investment advisors may counsel a client to pay down a mortgage rather than save for retirement, and union negotiators may demand more current wages or health benefits instead of increases to pension benefits. These contemporary sources of resistance echo resistance in the prior programs, like the refusal of individuals to submit to invasive means testing, or the lack of cooperation shown by those who managed ‘houses of refuge’ in 1928. The opportunities for resistance thus vary with the roles one plays in the system.

The limited success of administrative routines, policies and technologies in shaping age-appropriate behaviour matches incomplete governance observed in other settings. Brown and Lewis (2011), for instance, examined the routines of lawyers throughout the working day, and found that individuals were not completely taken over by the technologies of power/knowledge embedded in the routines. They were ‘able to liberate themselves from the normalizing and totalizing tendencies’ of these discursive practices (Brown and Lewis, 2011, p. 885). Given how the technologies of retirement savings and income operate in the background, with the individual only periodically being called to account, limited subjectivization of the individual with respect to age is unsurprising. Payroll systems calculate the earnings of the worker, banks track the flows of remittances for payroll deductions, pension plans track contributions to funds: the moments when the individual is brought into relationship with these calculations and is asked to hold himself to account are few, and even these can be highly routine and indeed passive. In addition, the calculative system is only a part, albeit an important part, of the cultural production of age and aging. The influences of literature and music, and of personal family stories, still play a vital part in helping us understand ourselves as aging people.