Abstract

We explore the interdependence between stakeholder controversies and shareholder engagement on environmental and social issues and how it affects corporate financial performance. Viewing shareholder impact as a distributed and dynamic process, we theorize that shareholder dialogue can affect investors’ risk perceptions. As an ambivalent signal, its impact may be negative or positive, contingent on media-covered stakeholder controversies. In the absence of those controversies, shareholder dialogue may highlight the existence of environmental and social liabilities in targeted companies. In the presence of stakeholder controversies, however, shareholder dialogue may reassure the investment community about shareholders’ commitment to and confidence about improving environmental and social policies and practices. We test our hypotheses on a proprietary dataset of 771 S&P 500 companies between 2007 and 2019 that covers 176 environmental and social shareholder dialogues. We find that, in the wake of stakeholder controversies, shareholder dialogue moderates the negative effects of controversies on targeted companies’ financial performance, consistent with our theory that shareholder dialogue may mitigate investors’ perceptions of risk. Our findings contribute to the understanding of shareholder engagement and, more broadly, of stakeholder–shareholder dynamics.

Introduction

As sustainable investing has become mainstream, whether it has a significant impact on environmental and social (E&S) issues—in both driving actual change and affecting the financial performance of portfolio companies—has become a central question (Chuah et al., 2024). Sometimes called active ownership or stewardship, the practice of shareholder engagement is core to sustainable investing and designates the process by which investors seek to influence companies’ environmental, social, and governance (ESG) policies and practices through various strategies, such as sending letters, casting proxy votes, filing shareholder resolutions, and initiating private dialogue with portfolio companies (Logsdon & Van Buren, 2009).

While the literature has begun to explain the mechanisms of shareholder engagement and the different types of impact it may have (Chuah et al., 2024), the dominant focus so far on the direct effects of engagement has also given rise to ‘heroic’ narratives (Marti et al., 2024, p. 2202) whereby individual shareholders, by themselves, appear to successfully influence companies and whereby change results from their isolated actions. Yet a more ‘distributed’ account of shareholder impact as a ‘process that emerges gradually as different shareholders build on each other’s efforts’ (Marti et al., 2024, p. 2183) may better explain—both theoretically and empirically—the indirect impact of shareholder engagement and its interaction with other stakeholders’ actions.

Vasi and King (2012) made a first step in this direction by studying the indirect impact of shareholder resolutions (the most traditional and adversarial form of engagement) on corporate financial performance through their ability to shape security analysts’ and other shareholders’ perceptions of environmental risk. Building on this work, we seek to advance the literature on shareholder engagement and its impact by focusing on non-adversarial, behind-the-scenes private dialogue that has so far remained largely underexplored (Chuah et al., 2024). Complementing previous studies on private dialogue’s direct impact in allowing shareholders and managers to reach workable agreements and translate them into policy or operational changes (Beccarini et al., 2023; Ferraro & Beunza, 2018), which in turn affect the accounting, operational, and financial performance of engaged companies (Barko et al., 2022; Dimson et al., 2015), we argue that dialogue with some shareholders can also help other shareholders make sense of E&S controversies and mitigate their negative effect on long-term financial performance.

Thus far, studies have addressed how stakeholder controversies on E&S issues—especially when broadcasted and amplified by the media—affect target companies’ reputational (King, 2008, 2011; McDonnell & King, 2013) and financial risk (Durand & Vergne, 2015; Kölbel et al., 2017). These controversies may reduce stock prices (Capelle-Blancard & Petit, 2019; King & Soule, 2007; Kothari et al., 2009; Serafeim & Yoon, 2023; Wong & Zhang, 2022) and change target companies’ opportunity structures (Briscoe & Gupta, 2016) by making them more open to address stakeholder demands following E&S controversies (McDonnell et al., 2015; Slager et al., 2023). Additionally, stakeholder controversies on E&S issues may attract further activism from shareholders. Shareholders—made more aware of specific ESG issues in their portfolio companies—may be more likely to target companies exposed by the media (Dimson et al., 2015; Semenova, 2023) through dialogue to both (a) mitigate risk (Solomon et al., 2011) and (b) scale the overall ESG impact by legitimizing the claims of activists who may otherwise be seen as peripheral to the company’s core business (Vasi & King, 2012).

We theorize that shareholders continually monitor each other’s engagement activities with companies through several channels. We further suggest that shareholder dialogue, by itself, is an ambivalent signal in that its significance could be negative or positive. Which of these signals becomes dominant for the investment community may depend on whether the company has been exposed to a media-covered stakeholder controversy. In the absence of one, dialogue may simply make investors aware of potential E&S liabilities at the company, increasing their perception of risk and thereby potentially leading to a negative impact on corporate financial performance. However, during a controversy, because media coverage has already made the investment community aware of the existence of an E&S issue, the presence of shareholder dialogue may bring novel information that comes from knowing that shareholders are committed to and confident about improving target companies’ controversial E&S policies and practices. In the wake of stakeholder controversies, then, the positive signal may become more salient, and shareholder dialogue may act as ‘soothing whispers’ by reassuring the investment community about the potential for change at the targeted company and shareholders’ efforts to resolve the issues or to mitigate the risks associated with them (Eesley et al., 2016). As such, we argue that shareholder dialogue may eventually mitigate the negative effect of stakeholder controversies on corporate financial performance.

To test our hypotheses, we utilize a unique proprietary dataset on the shareholder dialogues of Federated Hermes Engagement Ownership Services (EOS), a world leader in providing engagement services to other shareholders that collectively represent more than US$1.4 trillion under management. Our sample covers the years from 2007 to 2019 and includes 771 S&P 500 companies and 176 E&S dialogues. Our study contributes to the debate on whether and how shareholder activism impacts companies (Marti et al., 2024). While the shareholder activism literature has explored adversarial forms of engagement—shareholder resolutions—and their indirect impact on other shareholders by increasing their perception of companies’ exposure to risk (Vasi & King, 2012), we explore an understudied and non-adversarial form of engagement—shareholder dialogue (Eesley et al., 2016; Ferraro & Beunza, 2018)—and raise an opposite indirect impact mechanism: the potential of shareholder dialogue to mitigate investors’ perceptions of company risk following stakeholder controversies.

Theoretical Background

Shareholder dialogue in the wake of stakeholder controversies

Social movement and stakeholder theory have established that the actions of social movements, NGOs, and other stakeholders, and the public controversies they generate, may negatively impact targeted companies. Stakeholder activism can affect competitive dynamics by creating opportunities for competitors to enter a market (Yue et al., 2013) and can lead to an increase in board member turnover at companies whose corporate social responsibility has been questioned (McDonnell & Cobb, 2020) or to the dismissal of CEOs in the wake of negative ESG news (Burke, 2022).

By signaling dissatisfaction among stakeholders, negative ESG media coverage may increase a targeted company’s reputational risk (Fombrun & Shanley, 1990; King, 2011; Zavyalova et al., 2016), decrease its legitimacy (King, 2008; McDonnell & King, 2013), and cause a variety of actors—employees (Bhattacharya et al., 2008; Y. Chen et al., 2021), consumers (Elfenbein & McManus, 2010), suppliers (Dyer & Singh, 1998), investors (Durand & Vergne, 2015; Mackey et al., 2007), and politicians (McDonnell & Werner, 2016)—to distance themselves from the targeted company, eventually impacting its labor, production, and capital costs (Madsen & Rogers, 2015). Media coverage of stakeholder discontent may further affect targeted companies’ financial performance by causing negative market reactions (Capelle-Blancard & Petit, 2019; Davidson et al., 1995; King & Soule, 2007; Kothari et al., 2009), increased financial risk (Kölbel et al., 2017), and lower firm valuation and higher probability of exit by more environmentally and socially conscious investors (Gantchev et al., 2022).

By broadcasting the concerns of different stakeholders, the media may trigger subsequent waves of activism from other stakeholders whose perceptions they have influenced and shaped (Bundy et al., 2021; Hawn et al., 2026; Marti et al., 2024). By increasing the salience of specific contested ESG issues (Bednar et al., 2013; Bundy et al., 2013), negative ESG media coverage may increase shareholders’ perception of E&S and financial risk and lead them to directly engage with the target companies to mitigate those risks (Solomon et al., 2011) and to scale the overall ESG impact by legitimizing the claims of activists who may otherwise be seen as peripheral (Vasi & King, 2012). By making the contested issues more salient also for managers (Bundy et al., 2013; Odziemkowska & Henisz, 2021), stakeholder controversies may further affect target companies’ opportunity structures (Briscoe & Gupta, 2016; McDonnell et al., 2015; Slager et al., 2023) and make them more receptive to collaboration with shareholders that are seen as more moderate as compared to their peers in the ‘radical flank’ (Baron et al., 2016, p. 106; Schifeling & Hoffman, 2019).

Unlike secondary stakeholders, shareholders enjoy privileged access to institutional channels to raise their concerns and thus do not need to generate media attention to controversies to inflict reputational and financial damage on targeted companies but can, instead, engage companies directly via shareholder resolutions and private dialogue (McCahery et al., 2016; Slager et al., 2023). Because shareholder resolutions are public and therefore data on them is more available, both finance and organizational scholars have traditionally focused primarily on them, leading to a large literature on resolutions (Bauer et al., 2022; Busch et al., 2025; T. Chen et al., 2020; Chuah et al., 2025; Fich & Xu, 2025; Flammer et al., 2021; He et al., 2023; McCahery et al., 2016; Proffitt & Spicer, 2006). And yet shareholder dialogues (i.e., private discussions with boards and managers) are an increasingly impactful channel of engagement.

The ability of shareholder dialogue to foster the creation of collaborative relationships with corporate managers and the development and implementation of shared solutions is highly varied (Beccarini et al., 2023; Ferraro & Beunza, 2018; Gond & Piani, 2013; Goodman & Arenas, 2015; Goodman et al., 2014). Successful dialogues, by changing policies and practices to address the root causes of E&S problems, may ultimately resolve controversies, reduce operational risk at engaged companies and portfolio risk for investors (Hoepner et al., 2024), and have a direct impact on operational and financial performance (Barko et al., 2022; Dimson et al., 2015). Yet companies have no obligation to enter into a shareholder dialogue. Even when they do so, the dialogue may last several years and its outcomes may be uncertain.

As such, in this study, to capture the full extent of the impact that shareholder dialogue can have on financial performance, we move beyond dialogue’s direct effects to focus on its indirect ones (i.e., those produced by other shareholders’ reactions to it). We suggest that ongoing shareholder dialogue sends two opposing signals to the investment community and that the respective salience of those signals depends on whether the company is embroiled in stakeholder controversies. Thus, we hypothesize that (a) shareholder dialogue may have a negative main effect on corporate financial performance, yet (b) in the wake of stakeholder controversies, it may mitigate their negative consequences on targeted companies’ long-term financial performance.

Hypotheses Development

Shareholder dialogue and financial performance

What are the effects of shareholder dialogue on target companies? While finance scholars have studied this question, results have been mixed. On the one hand, researchers have found that dialogue may improve ESG and accounting performance (Barko et al., 2022), increase stock prices and abnormal returns (Becht et al., 2008; Dimson et al., 2015), and deliver profitable trading opportunities (Becht et al., 2025). On the other hand, Bauer et al. (2023) have found that only companies engaged in dialogues on material governance issues experience higher stock returns than their peers, as well as higher post-dialogue profitability and lower expense ratios. By being more financially material, governance issues have a clearer link to company performance, thus making it easier for shareholders to argue that companies should address controversial practices in this domain (Bauer et al., 2023).

To explain these mixed empirical results, there may be different mechanisms by which shareholder dialogue affects corporate performance and market value that need to be theorized and tested. Most prior research emphasizes the direct effect of successful dialogue (e.g., its ability to generate changes in companies’ ESG practices) (Chuah et al., 2024; Marti et al., 2024). By contrast, we seek to explore how shareholder dialogue can trigger reactions from other shareholders and stakeholders to have an indirect impact on companies. It is quite common, in fact, for institutional investors to monitor each other (Sias, 2004) to reduce risk and generate ESG impact (Gond & Piani, 2013; Solomon et al., 2011), which leads, for example, to correlated trading patterns (Sias, 2004) and herding behavior (Brown et al., 2014; Rao et al., 2000, 2001). Investors and analysts increasingly pay attention to E&S issues and ratings in their forecasts (Ioannou & Serafeim, 2015; Park et al., 2024; Roger, 2024; Schiemann & Tietmeyer, 2022), and sell-side security analysts often integrate information on companies’ engagement practices in their earnings estimates (Z. Li, Bilinski, & Jung, 2024).

While shareholder dialogue is a private process, some information about it is publicly divulged in the quarterly and annual reports of both engagement specialists, as well as shared by companies as part of their communication and reporting. Engagement professionals may become aware of shareholder dialogue with companies through several channels, both formal and informal. Among the formal ones, they may meet at companies’ annual general meetings (AGMs), at specialized conferences organized by the Principles for Responsible Investing (e.g., ‘PRI in Person’ events), and, more broadly, at governance-focused venues and events such as the ones organized by the International Corporate Governance Network (ICGN). They may also meet through collaborative engagement initiatives such as the ones long organized by the Interfaith Center on Corporate Responsibility (ICCR; Ferraro & Beunza, 2018; Proffitt & Spicer, 2006) and more recently by the PRI (Dimson et al., 2023; Gond & Piani, 2013; Slager et al., 2023) and Climate Action 100+ (Chuah et al., 2025). In these collaborative engagement initiatives, shareholders pool their ownership positions to initiate dialogue with companies, and even if usually only one investor leads the coalition, all members may maintain regular contact to coordinate their activity on specific corporate targets. Although shareholders tend to avoid any exchange or one-way disclosure of nonpublic and sensitive information which might result in a breach of corporate or competition law (Becht et al., 2025), they may learn through their collaboration with other investors about public information shared through dialogues, even the ones individually conducted by other shareholders.

Such exchanges are essential for engagement professionals to learn from their peers and share information with their portfolio managers and other engagement professionals. Given this mutual monitoring of shareholders, we expect the knowledge that investors and portfolio managers acquire about a focal shareholder’s ongoing E&S dialogues to affect their perceptions of target companies’ risk and valuation. Nevertheless, shareholder dialogue may be an ambivalent signal as its implications can be either negative or positive. On the one hand, it may indicate the existence of E&S issues at target companies, while on the other hand, it may signal that shareholders are committed to addressing them.

Despite being initiated to mitigate risk, shareholder dialogue, similar to shareholder resolutions (Vasi & King, 2012), may increase other shareholders’ perceptions of targeted companies’ exposure to risk by highlighting the existence of potential liabilities in their E&S domains (Bauer et al., 2023; Monks & Minow, 2011; Van Buren, 2007). This, in turn, may lead investors to reduce the valuation of targeted companies that are perceived to be more involved in social crises, environmental disasters, and scandals, ultimately resulting in financial losses and weaker long-term corporate financial performance. Accordingly, we posit the following hypothesis:

H1: Shareholder dialogue has a negative effect on targeted companies’ long-term financial performance.

Shareholder dialogue and risk mitigation in the wake of stakeholder controversies

While, as a negative signal, shareholder dialogue suggests the existence of potential liabilities at a company, unlike shareholder resolutions, it can also imply that a group of shareholders is committed to addressing the company’s E&S issues. We argue that, when companies’ E&S issues have already been exposed by a media-covered stakeholder controversy, the positive interpretation of shareholder dialogue may become more salient for investors because it delivers new information. While stakeholder controversies increase target companies’ reputational and financial risk (Durand & Vergne, 2015; King, 2008; Kölbel et al., 2017; McDonnell & King, 2013), shareholder dialogue may assuage investors’ concerns by signaling shareholders’ commitment to and confidence about improving target companies’ E&S policies and practices.

We start from the premise that, given the continual monitoring among shareholders, even relatively small shareholder actions might have important consequences for corporate valuation. For instance, in the case of divestments, while it is often argued that divestments by one or few shareholders may not move the needle in terms of companies’ cost of capital (Edmans, 2023), a recent study suggests that, following E&S stakeholder controversies, companies may react even to a small divestment, given the threat that other shareholders may revise their assessment of the ESG practices of the company, and leave en masse—even if E&S conscious investors rarely do so (Gantchev et al., 2022).

Following a reputational threat to a company, investors may monitor each other more intensely and may be especially reassured by observing that other shareholders are dialoguing and collaborating with the targeted company. In the wake of a stakeholder controversy, targeted companies themselves may disclose their ongoing engagements to manage criticism by showing the restorative actions they are already undertaking in response to activists’ demands (Godfrey et al., 2009). Shareholders may also publish statements of support for a company experiencing stakeholder controversies, as Union Investment did after the publication of Volkswagen’s Xinjiang audit (Mayer-Kuckuk, 2023).

Knowledge that reputable shareholders are actively engaged in private dialogue with a company about its contested E&S practices may instill confidence in the investment community more broadly that the associated risks are being scrutinized, considered, and discussed in an effort to mitigate their consequences (Eesley et al., 2016). In general, because much of the information needed to evaluate the E&S risk of a company is noisy (Connelly et al., 2011; Makarius et al., 2017; Sanders & Boivie, 2004), investors tend to place more weight on signals from highly credible sources (Gomulya & Mishina, 2017). Some stakeholders may be perceived as more credible if they interact more frequently with the company and thus have first-hand information about the company’s exposure to risk and its ability to secure cash flow and sustain market value (Eesley et al., 2016; King & Soule, 2007). Among stakeholders, fellow investors may be perceived as more credible because of their shared concern for financial performance and their privileged access to information about the company due to their ownership rights (McCahery et al., 2016; Vasi & King, 2012).

Building on these mechanisms, we argue for several reasons that, by entering a dialogue with a company, shareholders send a strong signal to the market. First, instead of divesting their holdings after a reputational crisis (Gantchev et al., 2022; McCahery et al., 2016), they have not only remained invested in the company but started a dialogue that can last several years. This signals (a) their continued commitment to the company and to the improvement of its corporate E&S policies and practices and (b) their confidence in the company’s goodwill and potential for change. Even if dialogue is not always successful and its outcomes are uncertain, the demonstrated commitment of these shareholders is likely to shape the expectations of fellow investors and increase their willingness to continue granting their support to the targeted company (Dorobantu et al., 2017; Rao et al., 2000). In turn, financial analysts (Z. Li et al., 2024) and portfolio managers (Becht et al., 2025) may be more optimistic in their assessment of the investment prospects of engaged companies, which may mitigate the negative effect of stakeholder controversies on long-term corporate financial performance. Accordingly, we posit the following hypothesis:

H2: Shareholder dialogue positively moderates the negative effects of stakeholder controversies on targeted companies’ long-term financial performance.

Methods

Data and dependent variables

To test our hypotheses on the effect of shareholder dialogue and its interaction with stakeholder controversies on corporate financial performance, we followed previous studies that have focused on large, publicly traded companies—the ones most targeted by both activists and shareholders (Barko et al., 2022; Dimson et al., 2015; King, 2008; King & McDonnell, 2015; McDonnell, 2016; Vasi & King, 2012)—by gathering a sample of 771 US Standard & Poor’s 500 (S&P 500) companies comprising 9,630 observations from January 2007 to September 2019.

To operationalize our dependent variable, we chose Tobin’s Q, a market-based proxy for financial performance that measures companies’ value over their assets (Servaes & Tamayo, 2013). A measure of market valuation (Andrei et al., 2019), Tobin’s Q is increasingly used in management and strategy research as a proxy for long-term financial performance (Arts et al., 2023; Cho et al., 2025; Flammer, 2015; Langan & Deuschel, 2025; McDonnell et al., 2015; Servaes & Tamayo, 2013; Vasi & King, 2012). Because Tobin’s Q captures the present value of all the future expected cash flows (Servaes & Tamayo, 2013), it is a better measure of performance than profit-based ratios such as return on assets (Miller et al., 2015) for several reasons. First, in considering future cash flow, Tobin’s Q is a long-term, forward-looking measure, whereas return on assets considers only performance in the previous accounting year. Second, since investors tend to discount future cash flows, Tobin’s Q is also a risk-adjusted measure. Finally, it is not as easily manipulated by company leaders engaging in earnings management as profit-based ratios (Healy & Wahlen, 1999). As our theory hinges on the risk perception of market actors, Tobin’s Q is an appropriate choice for capturing the consequences of changes in these perceptions.

To avoid simultaneity bias, we considered financial performance in the year following shareholder and stakeholder activism as collected from the Compustat North America database. Tobin’s Q is measured as the company’s market value divided by the replacement costs of assets. In line with recent management and CSR studies (e.g. Sauerwald et al., 2018), we used Chung and Pruitt’s (1994) method to calculate Q.

Where:

MVE = (Closing price of share at the end of the financial year) * (Number of common shares outstanding);

PS = Liquidation value of the company’s outstanding preferred stock;

DEBT = (Current liabilities - Current assets) + (Book value of inventories) + (Long-term debt); and

TA = Book value of total assets.

Independent variables

To capture stakeholder controversies, we used the RepRisk database. While stakeholder activism—in the form of boycotts and public protests—is traditionally studied in the literature with hand collected and coded data from select major newspapers (Earl et al., 2004; King, 2008; McDonnell, 2016; McDonnell & King, 2013; McDonnell et al., 2015; Wang & Soule, 2012), RepRisk is more suitable for capturing E&S stakeholder controversies, such as major environmental and social incidents and scandals, due to its methodology. RepRisk uses artificial intelligence to collect negative news on ESG issues in 23 languages from over 100,000 different sources, such as major newspapers, news websites, and social media. It additionally categorizes news into 28 issues that fall into the three categories of ESG. Finally, it employs a team of trained analysts to verify and analyze the data to code for additional variables (Kölbel et al., 2017), such as the severity, reach, and novelty of the incident. 1 Given the consistency, reliability, and extensiveness of the RepRisk database, recent studies in management, finance, and accounting increasingly rely on it to measure reputational risk (DesJardine et al., 2023), negative ESG media coverage (Burke, 2022; Gantchev et al., 2022; Kölbel et al., 2017; Wong & Zhang, 2022), ESG incidents (J. Li & Wu, 2020), ESG criticism (Breitinger & Bonardi, 2019), and stakeholder pressure (Hawn et al., 2026).

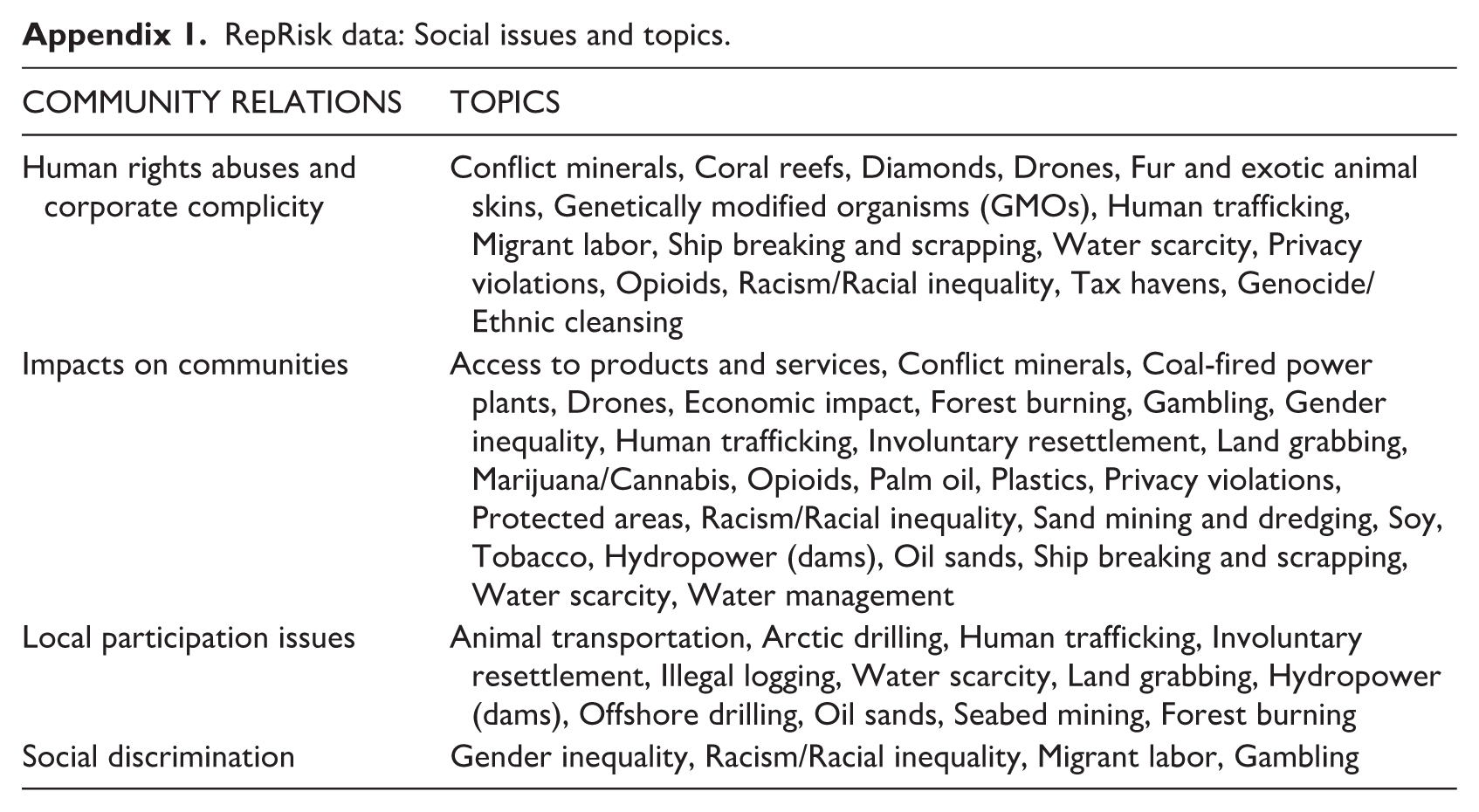

To create our variable for stakeholder controversies, we focused on RepRisk E&S topics that affect multiple stakeholders, i.e., those listed in RepRisk’s community relations (CR) sub-category of social issues. In the RepRisk database, one issue category (whether environmental, social, or governance) can be linked to multiple topics that belong to the other two categories. For example, all the environmental issues that affect multiple stakeholders appear also in the community relations sub-category. (See Appendix 1 for all the topics covered in CR.) We also dropped the employee relations sub-category, as it covered topics specific to labor issues, which affect only one stakeholder group. We then constructed a count measure of the number of CR incidents per company and year (J. Li & Wu, 2020) and scaled each event by its severity—low, medium, and high—as measured by RepRisk, following the formula:

To capture shareholder dialogue on E&S issues, we used a proprietary database of ESG dialogues with US public companies over the period 2007–2019. We obtained full access to the engagement database of Federated Hermes EOS, a large institutional investor that has more than US$1.4 trillion under advice and is a world leader in providing engagement services to global asset owners. This investment manager directly engages about 3,500 companies around the world through private, nonpublic letter-writing campaigns, phone calls, emails, and face-to-face meetings with directors and top managers and is one of the most influential asset managers when it comes to promoting the adoption of better ESG policies at portfolio companies. EOS engages companies in its own holdings and in those of the other large institutional investors that it represents (Hoepner et al., 2024). For each engagement, EOS’s database reports a description; the themes and subthemes; the start, milestones, and completion dates; the participants and the topics of all incoming and outgoing emails, letters, telephone calls, conversations, and meetings with executives.

To match the topics captured in the stakeholder controversies variable, we focused on EOS dialogues on E&S issues—covering topics such as coal-fired plants, carbon emissions, water management, and methane emissions (in the environmental domain), and human rights, conduct and culture, and diversity (in the social). EOS conducted 182 dialogues from 2007 to 2019, of which 118 were on environmental issues, and 64 on social ones. Shareholder dialogue typically unfolds over several stages, broken into four ‘milestones’ by EOS. The first milestone is raising a specific issue at the company. Companies faced with the complaint may deny, postpone addressing, or acknowledge the issue. A company acknowledges an issue—milestone 2—when it recognizes that shareholders might be right about the need to take action on a specific environmental or social concern. Milestone 3 is reached when the target company develops a solution strategy, and milestone 4 when the solution is implemented and deemed satisfactory by EOS. The variable shareholder dialogue is then measured as the sum of all the dialogues on E&S issues per company and year that have reached at least milestone two, i.e., the ones in which the company has acknowledged that there is an issue.

Control variables

To analyze the effect of stakeholder controversies and shareholder dialogue on corporate financial performance, we first controlled for shareholder resolutions. We used the ISS ESG Voting Analytics database and measured the variable shareholder resolutions as the count of shareholder resolutions directed at the company (Vasi & King, 2012). We then included a measure of company reputation (King, 2008), a dummy variable equal to 1 if the company was listed among the Fortune’s 50 Most Admired Companies in the observation year and 0 otherwise.

We further controlled for companies’ actual E&S performance, since it may (a) make targeting more likely (Barko et al., 2022), (b) predispose companies to respond positively to both stakeholders and shareholders (McDonnell et al., 2015; Rehbein et al., 2013), and (c) generate more favorable valuations by analysts and investors (Godfrey, 2005; Ioannou & Serafeim, 2015). We constructed a composite E&S performance variable using the London Stock Exchange (LSEG, formerly Refinitiv) Environmental and Social Pillar scores, which are percentile scores ranging from 0 to 100 that measure companies’ commitment to resources use, emissions, and environmental innovation (Environmental Pillar) and their capacity to build trust across stakeholders and consider their needs (Social Pillar). We collected the data at year end and calculated the average of the Environmental and Social Pillars. Then, we grouped companies into performance deciles.

Since institutional ownership may influence both the targeting and outcomes of dialogue (Dimson et al., 2015; Rehbein et al., 2013), we controlled for it as the percentage of total shares issued by the company that are owned by institutional investors. We calculated institutional ownership at year end using the 13F and mutual funds reports provided by FactSet. As a proxy for analysts’ and investors’ attention (Barko et al., 2022), we controlled for analyst coverage as the total number of analysts following the company, as reported by the I/B/E/S database.

Lastly, we included a set of firm-level controls from the Compustat database. First is firm size. Although large and visible companies tend to be more targeted (Rehbein et al., 2004), smaller ones are more likely to respond positively to stakeholder requests for change (Eesley & Lenox, 2006). We measured firm size as the natural logarithm of a company’s total assets, and the level of debt with the variable leverage ratio, calculated as the ratio of total debt to total assets. We then included research and development (R&D) and advertising expenses. In addition to being positively associated with companies’ short- and long-term financial performance, R&D, and advertising expenses may influence both targeting and outcomes of dialogue (Aguinis & Glavas, 2012; Barko al., 2022; Dimson et al., 2015). We measured R&D expenses as Compustat R&D expenditures divided by average total assets, and advertising expenses as Compustat advertising expenditures divided by average total assets. We then included intangible assets, calculated as Compustat intangible assets divided by average total assets, and cash flow to account for a company’s financial health, calculated as the company’s operating income plus depreciation and amortization divided by the company’s average total assets. This variable indicates the excess resources a company can use to eventually accommodate activists’ requests.

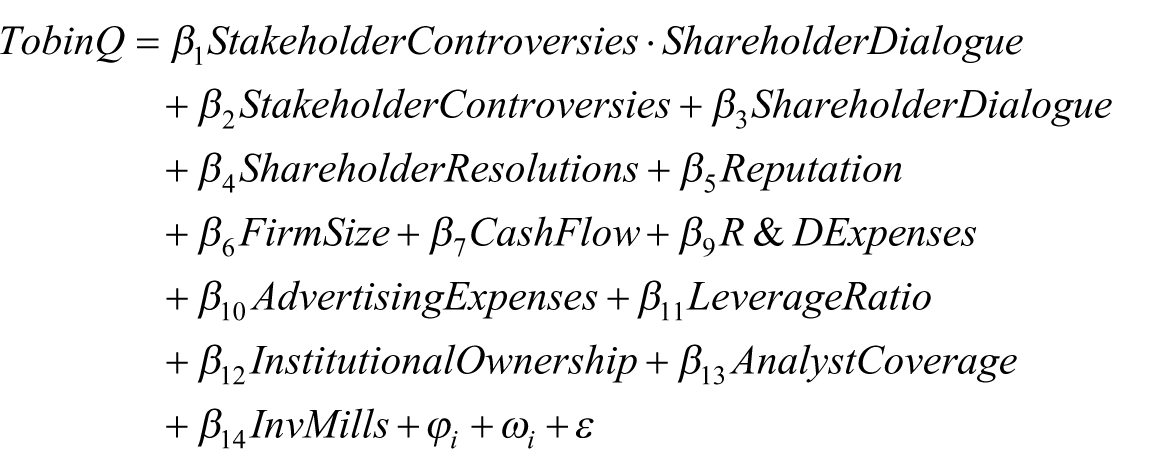

Empirical specification

Since the sample of companies engaged through dialogue by shareholders is not a random one, we used a two-stage Heckman model (Heckman, 1979), a common technique in management studies to account for sample selection bias (Leiblein et al., 2002). The first stage of the Heckman model uses a probit specification to estimate the selection-effect coefficient, λ (the inverse Mills ratio), which reflects the probability that a company will not be selected for shareholder dialogue. This coefficient is then included as a control in the second stage to correct for selection bias. To estimate the first-stage probit model, given the difficulty of finding adequate exclusion restrictions (i.e., exogenous variables that are associated with the dependent variable in the first-stage model but uncorrelated with the error term associated with the dependent variable in the second stage) (Certo et al., 2016), we implemented the Lewbel’s (2012) latent instrumental variable approach. Lewbel’s (2012) approach has become increasingly popular in management research for dealing with endogeneity concerns when exogenous instrumental variables are weak or unavailable (Y. Chen et al., 2021; Hasan et al., 2022; see also Andries & Hünermund, 2020). The method relies on generating instruments by exploiting the heteroskedasticity in the error term of an auxiliary regression with the endogenous regressors. In our case, the auxiliary regression is a linear model whose predictors include stakeholder controversies, shareholder resolutions, and company reputation, size, and leverage ratio, all lagged by one year to avoid simultaneity bias. For each observation, following Lewbel (2012), we multiplied the residual from this regression by the difference of each variable with its own mean (residual*(X - mean(X)), yielding five latent instruments (LIs) that are uncorrelated with the second-stage regression error term, thereby addressing potential bias from unobserved factors that may influence selection into an EOS dialogue.

To use the Heckman model correctly, we then included in the first stage the five latent instruments, along with the variables that may predict targeting, i.e., stakeholder controversies, and shareholder dialogue in industry, operationalized as the number of dialogues that companies in the same industry had with shareholders in an observation year. 2 We grouped firms by industry using the four-digit Global Industrial Classification Standard (GICS) codes (Bhojraj et al., 2003; Hrazdil et al., 2013). We further included shareholder resolutions, analyst coverage, institutional ownership, company reputation, firm size, and the leverage ratio. We lagged all variables by one year and added industry and year fixed effects. We then included the selection coefficient returned by the first-stage Heckman to the second-stage model to control for the selection effect, or the different likelihood companies have of being targeted by shareholder dialogue.

To capture changes in future cash flows and, therefore, financial performance, we measured firm-level changes in Tobin’s Q in the second-stage of the Heckman regression model through a two-way (firm, year) fixed effects model that fits the operationalization of the dependent variable, Tobin’s Q, as a continuous variable, and is specified as follows: 3

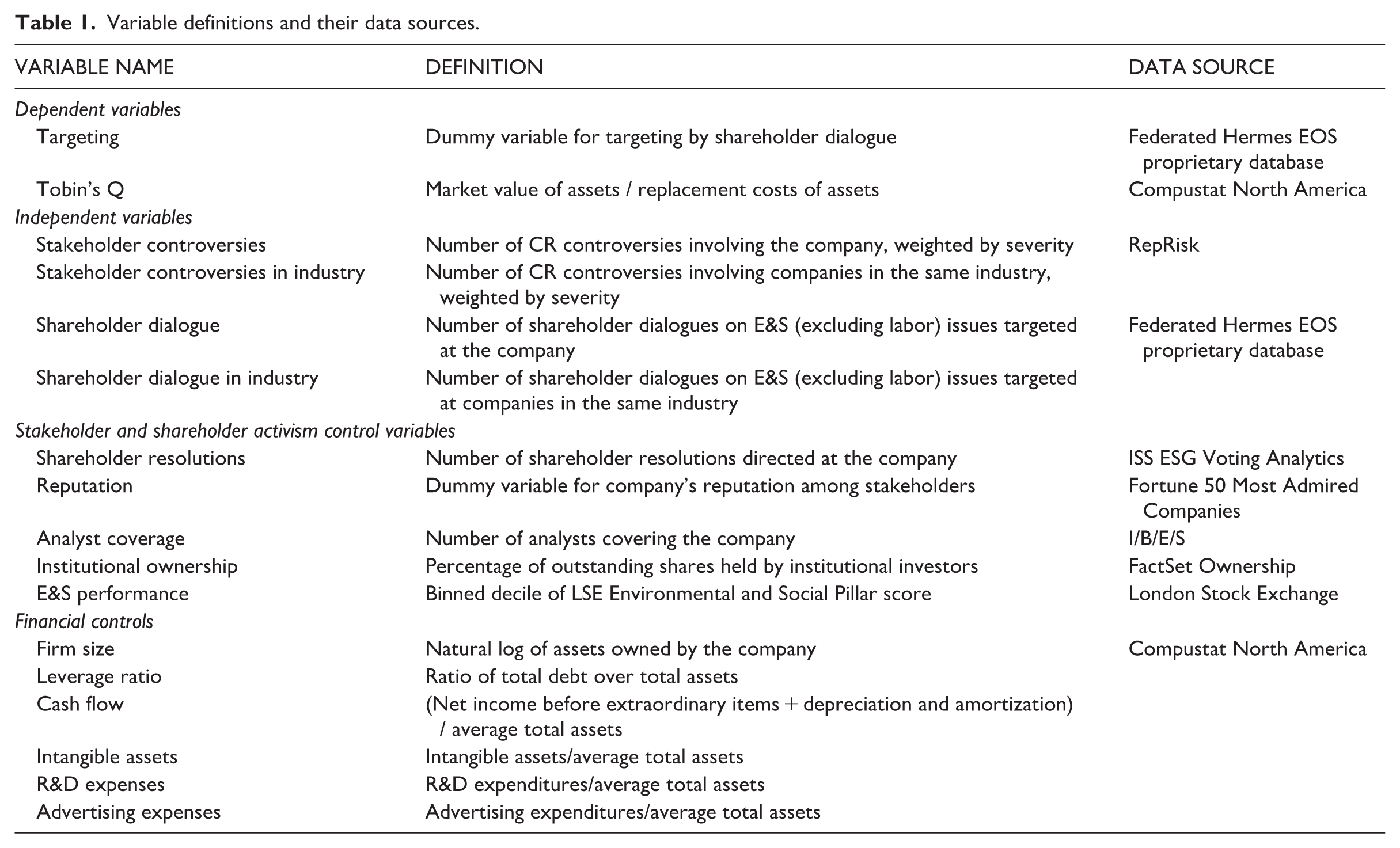

Lastly, to obtain robust standard errors and consistent, unbiased regression estimates, we clustered the observations by firm to account for within-firm heteroskedasticity and autocorrelation in the error term. Table 1 describes all variables by data source and model.

Variable definitions and their data sources.

Results

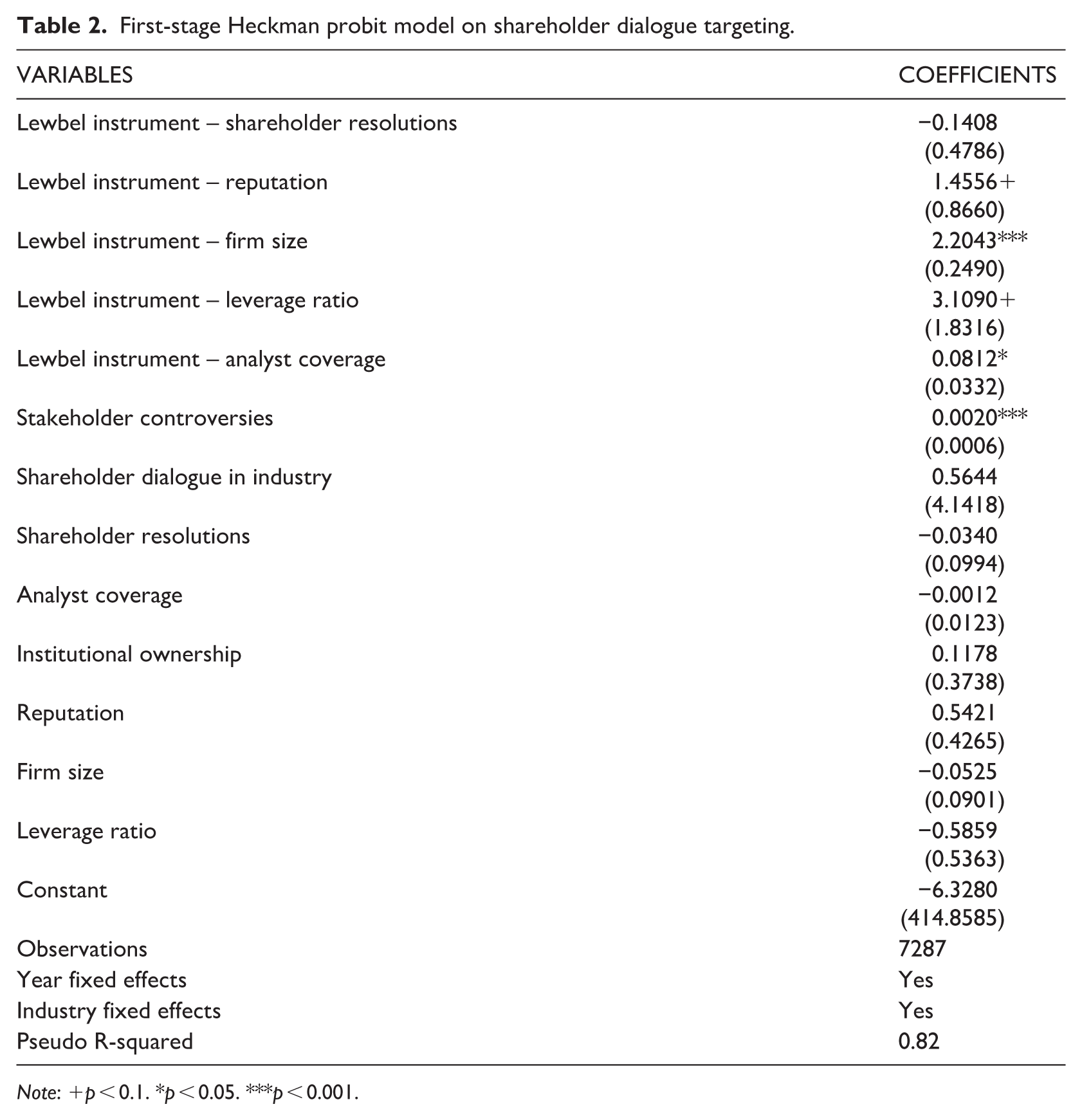

Table 2 reports the estimates from the first-stage Heckman (probit) selection equation. Following Certo et al. (2016), we assessed the fit of the model by analyzing the pseudo R-squared value associated with the first stage and the correlation between our independent variable shareholder dialogue and λ (the inverse Mills ratio). The correlation (.38) for the instrumental variable was above the value (.31) that indicated a strong exclusion restriction in Certo et al.’s (2016) simulation. Notably, when the exclusion restrictions are weak in a model, λ will correlate too highly with the main independent variable, thus introducing multicollinearity problems in the second stage of the model (Certo et al., 2016). The McFadden pseudo R-squared (.82)—much higher than the pseudo R-squared of the Heckman selection without the Lewbel instruments (.39)—further confirms the strength of the model.

First-stage Heckman probit model on shareholder dialogue targeting.

Note: +p < 0.1. *p < 0.05. ***p < 0.001.

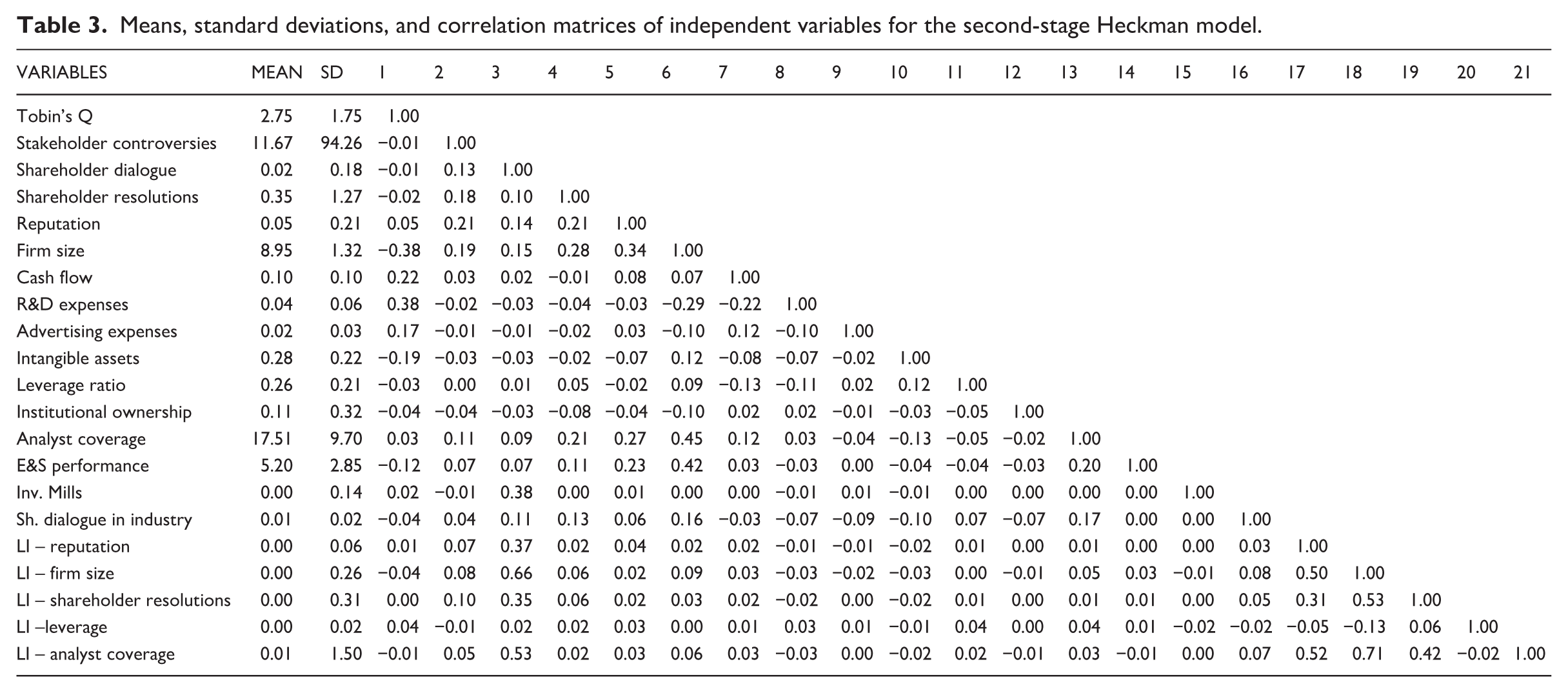

Table 3 presents descriptive statistics and correlations between numerical variables for the first and second-stage Heckman model. Inspecting the cross-correlations between our dependent and independent variables, we observe no concerning high correlations for our dependent variables or one of our two key independent variables, stakeholder controversies and shareholder dialogue.

Means, standard deviations, and correlation matrices of independent variables for the second-stage Heckman model.

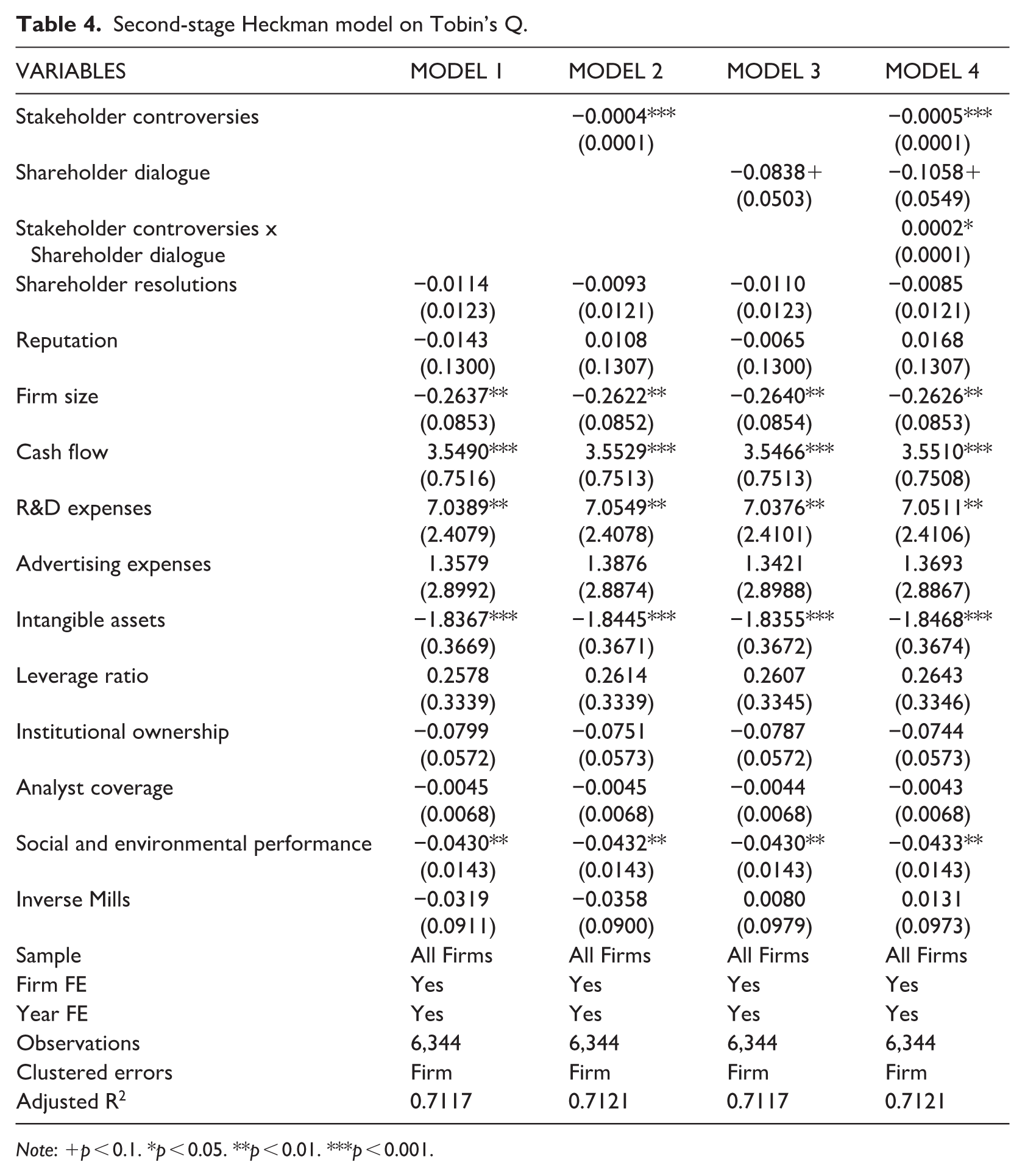

Table 4 reports the results of the second-stage Heckman two-way fixed effects panel model in which the dependent variable is financial performance as indicated by Tobin’s Q. The first column reports the baseline model, Model 1, which includes only the control variables. While most control variables have no significant relationship with financial performance, larger companies, companies with higher levels of debt and intangible assets, and companies that are more committed to their environmental performance have lower Tobin’s Q, while companies with higher R&D expenses and cash flow have better financial performance.

Second-stage Heckman model on Tobin’s Q.

Note: +p < 0.1. *p < 0.05. **p < 0.01. ***p < 0.001.

Model 2 adds the variable for stakeholder controversies, while Models 3 and 4, respectively, test our hypotheses on the effect of shareholder dialogue and its interaction with stakeholder controversies. In contrast with previous literature that did not find a significant effect of stakeholder activism (protests, demonstrations, boycotts, and lawsuits) on long-term financial performance (Vasi & King, 2012), our results show, in both Model 2 (β = −0.0004, p < .001) and Model 4 (β = −0.0005, p < .001), a negative and strongly significant estimated coefficient of stakeholder controversies. These results might suggest a difference between social movement activism in the form of boycotts and protests, which leads to a temporary decline in financial performance (no longer than 90 days on average; King & Soule, 2007), and E&S controversies, such as environmental disasters and social scandals, which might have a different media cycle and weaken long-term financial performance.

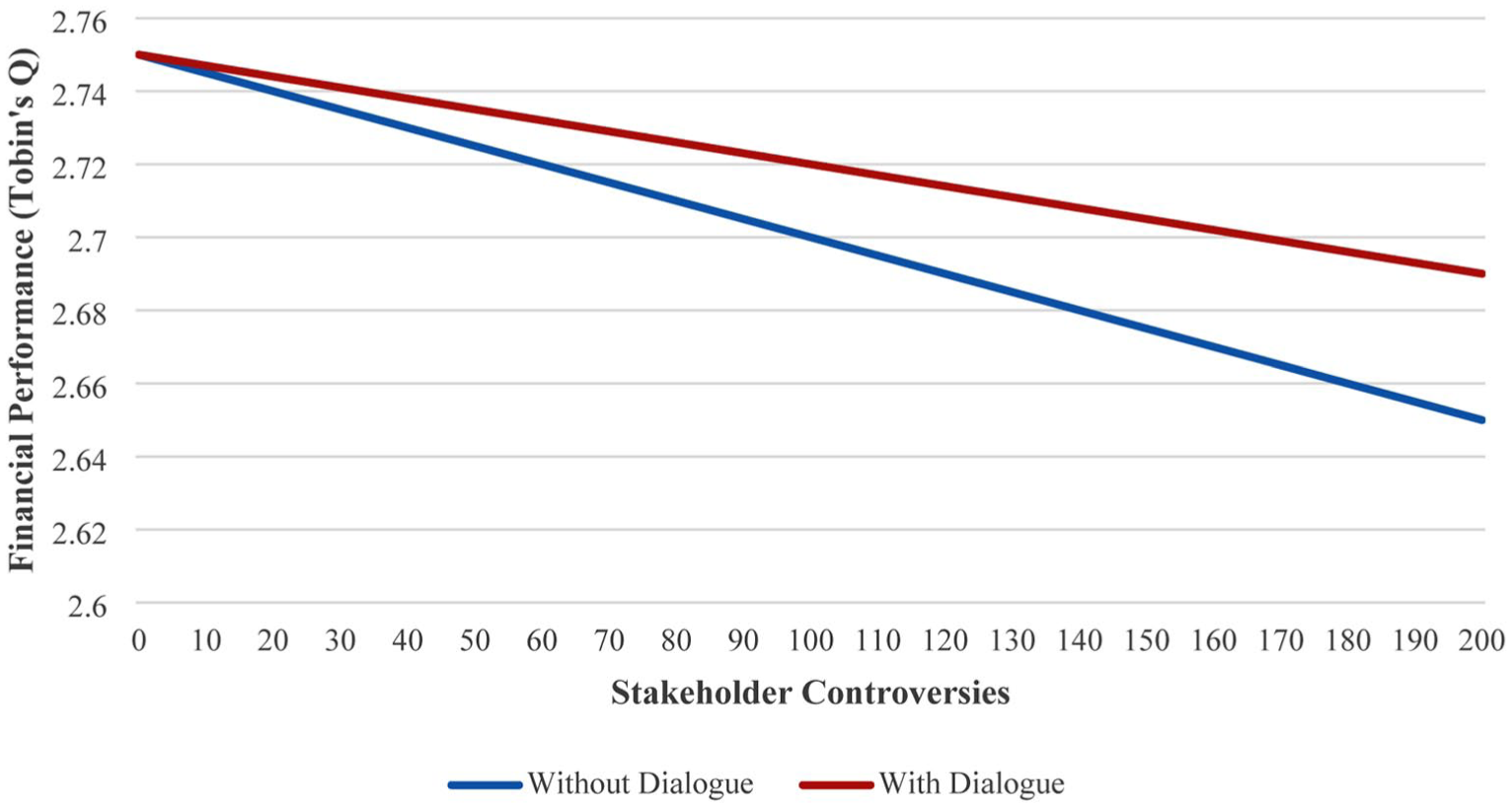

In both Model 3 (β = −0.0838, p < .10) and Model 4 (β = −0.1058, p < .10), shareholder dialogue has a negative but only weakly significant effect on Tobin’s Q, not fully supporting Hypothesis 1. On the contrary, Model 4 supports Hypothesis 2, as the interaction between stakeholder controversies and shareholder dialogue is positive and significant (β = 0.0002, p < .05). The mitigation effect of shareholder dialogue is graphically represented in Figure 1, which shows the effect of (a) stakeholder controversies and (b) stakeholder controversies in the presence of shareholder dialogue on financial performance.

The moderating effect of shareholder dialogue on the negative effect of stakeholder controversies on companies’ long-term financial performance.

To confirm our results, we conducted several robustness checks, which we do not report here but which are available upon request. First, we added two-way clustered standard errors at the firm and year level to our model (Petersen, 2009). We further replaced four-digit GICS codes with two-digit Standard Industry Classification (SIC) codes. The results of these different specifications are consistent with the ones we report in Table 4. To confirm the plausibility of our information exchange mechanism, we further identified the subset of our dialogues that were part of collaborative engagement processes. Given the formalized exchange of information collaborative engagement assumes, we would expect it to have an even stronger effect in influencing investors’ perceptions and valuations (Dimson et al., 2023). Our results do confirm our expectations and therefore support the plausibility of our mechanism.

Finally, to rule out alternative explanations, we tested two possible mechanisms. First, we analyzed whether the effect we observed on Tobin’s Q may be due to companies’ reformative efforts that were induced by the dialogue with shareholders, as captured by EOS milestones 3 and 4, which signal that the targeted company has developed a strategy to address the issue and has implemented it, respectively. Results show a modestly significant and negative independent effect for milestone 2 and 4 dialogues on Tobin’s Q, and a significant and negative interaction effect of the same magnitude for all milestones. The lack of a significant and positive independent effect and a stronger interaction effect for dialogues at milestones 3 and 4 is consistent with our interpretation of the results as driven by signaling rather than reformative efforts. Second, we tested whether the financial materiality of the issue may be driving our results. Specifically, we used the Morgan Stanley Capital International’s (MSCI) framework for materiality (MSCI, 2025) that identifies which issues are material to each sector (Behzadifard, 2023a, 2023b). By linking MSCI issues to EOS engagement descriptions, we created a material dialogue variable that takes the value of 1 if the dialogue on an issue is classified as material for the company’s industry and 0 otherwise. We then re-estimated our main model using this variable. Results did not show any significant moderating effect of material dialogues on the negative relationship between controversies and Tobin’s Q.

Discussion and Conclusion

In this study, we explored how stakeholder controversies and shareholder dialogue can affect the long-term financial performance of companies. While the idea that stakeholders and shareholder actions are interdependent and shape corporate decisions is not new (Crilly, 2013; Ferns et al., 2022), researchers have recently called for stakeholder impact to be approached as a ‘distributed process’ among different stakeholders and for the mechanisms through which ‘stakeholders build on each other’s efforts’ to be further theorized and empirically tested (Marti et al., 2024, p. 2183). In this study, we focused on shareholder dialogue as an ambivalent signal in the wake of media-covered stakeholder controversies and argued that its significance can be negative or positive, contingent on the presence of such controversies. We found that, while shareholder dialogue may signal the existence of liabilities in targeted firms, in the absence of stakeholder controversies it does not significantly influence investors’ perception of companies’ exposure to risk. However, in the presence of stakeholder controversies, shareholder dialogue can help assuage the concerns of other shareholders and significantly mitigate any financial loss that results from the negative press.

The theory we outlined in this article has two boundary conditions. First, given the role that peer monitoring among investors plays in our theory, we would expect dialogue to exert its soothing effect only when it is performed by shareholders that are relatively central in the investors’ network. This does not mean that our theory applies only to the largest asset owners (e.g., NBIM, the Norwegian Pension fund) or asset managers (e.g., BlackRock) but that engagement professionals must be sufficiently high status and high reputation in the investors’ network to shape the perception of other investors. Second, our theory applies only to ESG engagement and may not apply to the activism of investors focused solely on short-term financial gains, such as hedge funds, for instance (DesJardine et al., 2022). Investors engaging on ESG issues have a shared interest in seeking a reduction in their portfolio risk and perhaps even in their systemic risk (as with the case of climate engagement). By contrast, investors motivated by purely financial interests may be more likely to share information only to the extent it improves their financial position. For this reason, while activist hedge funds tend to publicize their actions, professional investors are often suspicious of their motives.

Theoretical and empirical contributions

Our work contributes to two research areas. First, we contribute to the shareholder activism literature by (a) suggesting an indirect impact mechanism for shareholder engagement (i.e., dialogue’s potential to mitigate investors’ perceptions of E&S risk) and (b) identifying the scope conditions for a significant positive impact of dialogue on financial performance (i.e., the presence of stakeholder controversies). Second, we contribute to the broader literature on shareholders-stakeholders dynamics by studying (a) the interplay between stakeholders and shareholders and (b) how the credibility of different signals affects shareholders’ reactions.

Shareholder activism and shareholder engagement

Our study responds to calls for understanding shareholder activism as a ‘complex, dynamic, and adaptive’ system where ‘complex interactions occur between stakeholders, campaigns unfold dynamically over time, and various actors in the system learn and adapt to activism’ (Chuah et al., 2024, p. 105). Following the path opened by Eesley et al. (2016) and Vasi and King (2012), our theory considers both direct and indirect effects of shareholder dialogue (Marti et al., 2024) and emphasizes the role that dialogue plays in shaping the risk evaluations of other shareholders. In building on this literature, we derived novel hypotheses on the effect of dialogue on long-term financial performance and produced results that suggest an indirect impact mechanism. This mechanism contrasts with the one identified by Vasi and King (2012). While they found that engagement in the form of shareholder resolutions increases investors’ perception of target companies’ risk, we found that shareholder dialogue, following a stakeholder controversy, has the potential to mitigate the stakeholder-induced increase in investors’ perceived risk of targeted companies.

Our approach moved beyond ‘the focal activist–firm dyad’ to consider the ‘interactions and responses of other actors and reactors, and the broader institutional environment in which activism campaigns unfold’ (Chuah et al., 2024, p. 88). In doing so, we contribute to recent research analyzing the spillover effects of activism (Cao et al., 2019; Denis et al., 2020; Gantchev et al., 2019; Shi et al., 2020; Zhang, 2022). Our mechanism, focused on investors’ reactions to dialogue, is consistent with studies pointing to the role of boards of directors and board interlocks in diffusing the knowledge acquired through dialogue—as signaled by withdrawn resolutions (Bauer at al., 2022)—at a focal company to peer companies (Chuah et al., 2025).

Finally, our study adds nuanced theoretical and empirical contributions to the small but growing shareholder engagement literature that has focused on dialogue rather than resolutions (Barko et al., 2022; Becht et al., 2008; Chuah et al., 2025; Dimson et al., 2015). Theoretically, our focus on the indirect effects of shareholder dialogue furthers the development in organization theory and management of research that suggests that dialogue does not operate as a reputational threat but as a deliberative process that enables more productive discussions of issues of concern (Beccarini et al., 2023; Ferraro & Beunza, 2018). This perspective has started to develop a relational theory of dialogue, primarily focused on explaining dialogue success (Goodman et al., 2014; Ferraro & Beunza, 2018). The limitation of this theory is that it has remained primarily dyadic and has not directly considered the role of relationships between stakeholder and shareholder actions, nor the indirect effect of dialogue.

Empirically, our study offers robust findings on the role that shareholder dialogue plays in mitigating investors’ perceptions of risk and its effect on long-term financial performance. While evidence has been mounting on the consequences of dialogue, the results so far on its operational and financial performance for companies have been mixed, with some studies reporting desirable impacts on valuation (Barko et al., 2022; Dimson et al., 2015) and risk (Hoepner et al., 2024) and others suggesting that these effects are primarily restricted to governance engagement (Bauer et al., 2023). In our study, by theorizing and exploring dialogue’s indirect impact, we introduced an important scope condition that may need to hold for dialogue to exert a significant positive impact on financial performance—the presence of stakeholder controversies—and suggested that shareholder dialogue may mitigate the negative consequences of these controversies.

Shareholders-stakeholders dynamics

Our study also dovetails with and advances Dorobantu et al.’s (2017) contribution to the study of the dynamics of stakeholders’ interactions. Those authors found that companies, during crises, tend to maintain their market value if they have had historically good stakeholder relations and are supported by high-visibility or high-status stakeholders, who are perceived as possessing more relevant firm-related information. Yet, while suggesting that shareholders’ reactions may neutralize the effect of stakeholder-initiated attacks, the authors did not theorize ‘the interplay between [different stakeholders’] movement and countermovement dynamics’ nor assess ‘the extent to which the credibility of different types of signals affects stakeholders and shareholder reactions’ (Dorobantu et al., 2017, p. 590). We took a significant step toward filling this gap by focusing on the interaction between shareholder dialogue and stakeholder controversies. Our study suggests that while stakeholder controversies raise the attention of other stakeholders—including shareholders—on specific E&S issues, shareholder dialogue plays a complementary role by decreasing other shareholders’ risk perceptions in the wake of stakeholder controversies, ultimately shaping the company’s market value and long-term financial performance.

Limitations and future research

Our study has several limitations that present opportunities for future research. While our theory hinges on shareholders’ risk perception and reactions, we do not directly measure these variables. Although our results provide evidence consistent with our theory, future research could explore more in depth the relationship between shareholder dialogue and risk assessment. A recent study in finance leveraged proprietary data from an asset manager to establish a relationship between dialogues’ content and subsequent analysts’ reactions and portfolio managers’ decisions (Becht et al., 2025). Future research could connect dialogue data with social movements and stakeholder activity to further our understanding of these dynamics.

We relied on a unique source of data that allowed us to study shareholder engagement beyond resolutions, the engagement database of EOS, a world leader in stewardship services. Even though EOS is well known in the industry for the quality of its engagement services and acts on behalf of many other asset managers, we could observe only the dialogues led by this asset manager, even as companies could be targeted by different institutional investors. The impact of dialogues from other institutional investors may not be the same as those that we observed for EOS. Future research could bring together different datasets—possibly thanks to the collaboration of different research teams—to explore the interaction among dialogues led by different shareholders.

We limited our analysis to news coded as ‘Community Relations’ in RepRisk to focus on issues that are more local and thus more likely to be targeted by social movement and stakeholder activity. Meanwhile, we excluded ‘Employee Relations,’ as these issues are primarily addressed by labor unions. With regard to other issues, especially given the rising importance of climate change and the increasing focus of the financial sector on the topic, future studies could focus more on climate-related stakeholder activity, and its interaction with shareholder dialogue.

Finally, while we acknowledged the importance of collaborative engagement as a vehicle for sharing the public information obtained via dialogues, we did not directly study these collaborations. One of the few studies that directly investigated collaborative climate engagement, using a fuzzy-set qualitative comparative analysis (fsQCA), concluded that engagement success is the result of a configuration of coalition variables—its size, shareholding stake, experience, and local access—that fit the receptivity of the targeted company (Slager et al., 2023). Our theory proposes a more nuanced approach to understanding shareholder dialogue and its combined effect with stakeholder controversies. Social movement organizations and other stakeholders are often tacit members of these coalitions, and engagement practitioners are aware of the role that attacks from the more radical flanks of social movements (Baron et al., 2016) can play in opening up companies to the dialogue with shareholders (Schifeling & Hoffman, 2019). Future research could explore how shareholders in collaborative engagement coordinate their actions with those of other stakeholders.

Another limitation is our study’s rather limited treatment of dialogues’ relational dynamics. Other studies have suggested that these relational dynamics and their deliberative nature matter for engagement success (Beccarini et al., 2023; Ferraro & Beunza, 2018). It is unclear how engagement professionals can discursively leverage stakeholders’ actions and controversies in the dialogue. Future studies could consider how these relational dynamics affect the indirect impact of dialogue.

Practical implications

Our study also has practical implications for corporations, shareholders, and regulators. When we started this project, we did not realize that only a couple of years later our theory and findings would be highly relevant in the anti-ESG countermovement, which started in 2022, gained traction in 2024, and calls into question whether companies should collaborate with shareholders on ESG issues. Our theory and findings suggest that, rather than being damaging to corporations, shareholder engagement may shield companies in the wake of stakeholder controversies and help preserve their market value.

For corporations, our findings suggest that efforts to get shareholders to back them during stakeholder crisis are, on average, fruitful for preserving long-term financial performance. The observed soothing effect of shareholder dialogue may lead investor relations departments and corporate managers to become proactive in inviting or seeking out dialogue with shareholders concerned about E&S issues, especially in the wake of E&S controversies. For shareholders, our findings imply that acting in the wake of stakeholder activism may be beneficial from both an impact and risk/return perspective. For regulators and policymakers, our findings suggest that there is merit in Stewardship Codes encouraging transparent shareholder dialogue and explicitly acknowledging and permitting collaborative shareholder engagement on ESG issues.

Footnotes

Appendix

RepRisk data: Social issues and topics.

| COMMUNITY RELATIONS | TOPICS |

|---|---|

| Human rights abuses and corporate complicity | Conflict minerals, Coral reefs, Diamonds, Drones, Fur and exotic animal skins, Genetically modified organisms (GMOs), Human trafficking, Migrant labor, Ship breaking and scrapping, Water scarcity, Privacy violations, Opioids, Racism/Racial inequality, Tax havens, Genocide/Ethnic cleansing |

| Impacts on communities | Access to products and services, Conflict minerals, Coal-fired power plants, Drones, Economic impact, Forest burning, Gambling, Gender inequality, Human trafficking, Involuntary resettlement, Land grabbing, Marijuana/Cannabis, Opioids, Palm oil, Plastics, Privacy violations, Protected areas, Racism/Racial inequality, Sand mining and dredging, Soy, Tobacco, Hydropower (dams), Oil sands, Ship breaking and scrapping, Water scarcity, Water management |

| Local participation issues | Animal transportation, Arctic drilling, Human trafficking, Involuntary resettlement, Illegal logging, Water scarcity, Land grabbing, Hydropower (dams), Offshore drilling, Oil sands, Seabed mining, Forest burning |

| Social discrimination | Gender inequality, Racism/Racial inequality, Migrant labor, Gambling |

Acknowledgements

We are grateful to (in alphabetical order) Daniel Beunza, Hans Hirt, Despoina Kentrou, Yanan Lin, Massimo Maoret, Shawn Pope, Matteo Prato, Giovanni Valentini, Michael Viehs, Xioayan Zhou, and participants at the 2015 IESE Finance and Organization Theory Conference, in IESE brownbag seminars, and in the 2018 Final Workshop on Socially Responsible Investments for their thoughtful comments and to Angela Herrera and Lydia Lafoz for research assistance. Our sincere gratitude also goes to our Senior Editor, Santi Furnari, and the anonymous reviewers for their competent and constructive feedback and to Sophia Tzagkaraki for her continuous assistance. All remaining errors are ours. Authors are listed in alphabetical order.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research underlying these findings was funded by the European Research Council under the European Union’s Seventh Framework Programme (FP/2007-2013) / ERC Grant Agreement n. 263604 and Mistra Financial Systems. The views expressed in this manuscript are not necessarily shared by the Technical Expert Group or the Directorate-General for Financial Stability, Financial Services, and Capital Markets Union (DG FISMA).

Declaration of conflicting interests

The authors declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: Beccarini, Ferraro, and Hoepner had personal exchanges with representatives of Hermes Equity Ownership Services (EOS), but neither of them has ever been paid a fee or salary by EOS, nor have any of the authors’ relatives been employed by EOS.