Abstract

This study examined the financial management practices of 62 participants in Smart Steps stepfamily education courses 1 year following their course completion. Qualitative interviews revealed 29 participants changed their financial practices as a result of the course, 29 did not change, and 4 provided unclear responses. Common reasons for no change included having functional practices that predated the relationship education course or financial difficulties remaining, despite course participation. Common reasons for change included working together as a couple and implementing budget or saving practices. Latino participants were more likely to report change than were European Americans. Findings and implications highlight both the opportunities and challenges associated with teaching financial education as part of a relationship education program.

Financial disagreements are common in marriages and are associated with increased conflict, difficulties in couple interaction, and increases in marital instability (Dew, 2009; Gudmunson, Beutler, Israelsen, McCoy, & Hill, 2007; Papp, Cummings, & Goeke-Morey, 2009). Leading relationship education (RE) experts have noted that finances are a common source of disagreement in marriage (Stanley, Markman, & Whitton, 2002) and have suggested financial education be included in RE courses (Adler-Baeder & Higginbotham, 2004; Hawkins, Carroll, Doherty, & Willoughby, 2004). However, there have been no analyses of the effectiveness of addressing financial issues in RE programming.

Similar to first marriages, couples in stepfamilies commonly argue about finances and can have wants and needs that exceed resources (Ganong & Coleman, 2004; Lown & Dolan, 1988). The complexity of managing finances in stepfamilies is well documented (Coleman & Ganong, 1992; Ganong & Coleman, 2004; Higginbotham, Anderson, & Lown, 2007); yet relatively little is known about how RE can help couples in stepfamilies navigate and negotiate their financial practices. The purpose of this study is to examine perceived changes to financial practices stemming from participation in Smart Steps, a researched-based stepfamily RE course.

Stepfamily formation brings together individuals from two different backgrounds, which often includes different earning and spending practices (Goetting, 1982; Higginbotham et al., 2007). Lown and Dolan (1988) suggested family life educators should assist remarried couples in recognizing differences, learning decision-making skills, as well as implementing financial practices such as budgeting and saving. This may be particularly helpful when considering few remarrying couples discuss finances, let alone plan their management strategies, prior to remarriage (Burgoyne & Morison, 1997; Coleman & Ganong, 1989; Ganong & Coleman, 2004).

Historically, research examining stepfamily finances has focused on how or if couples pool their funds. For example, Fishman (1983) discussed a dichotomous management system with either “two pots” or a “common pot” (cf. Coleman & Ganong, 1989; Pasley, Sandras, & Edmondson, 1994). Over time, scholars noted how examining finances from the lens of two or three categorizations was ineffective because it failed to capture the complexities of financial challenges and behaviors in stepfamilies (Ganong & Coleman, 2004; Higginbotham et al., 2007).

Couples in stepfamilies tend to have more conflictual financial challenges than first-married couples because financial obligations and decisions are often subject to external influences, such as courts and ex-spouses (Burgoyne & Morison, 1997; Coleman & Ganong, 1992; Ganong & Coleman, 2004). Even when there is court ordered child support, it may not come consistently or predictably (Lown & Dolan, 1988). Furthermore, couples must consider payments to and for family members outside of the immediate household, fairness within and across children and households, and integrating two different sets of expectations and financial histories (Ganong & Coleman, 2004; Higginbotham et al., 2007; Jacobson, 1993).

One recommended theoretical lens to examine stepfamily financial practices is Family Stress Theory (Crosbie-Burnett, 1989). Resources, which include tangible goods as well as skills and knowledge, are available to families from both inside and outside the family unit (McCubbin & Patterson, 1983). In the formation of a stepfamily, money is a resource that must be analyzed and then redistributed (Crosbie-Burnett, 1989), and financial arrangements are one of the most commonly reported difficulties stepfamilies face (Coleman, Ganong, & Weaver, 2001; Ganong & Coleman, 2004). Stepfamily members who successfully adapt (e.g., bonadaptation) to challenges tend to employ multiple resources including open communication, realistic expectations, and power sharing (Crosbie-Burnett, 1989). All these resources, or relationship skills, are taught in RE (Hawkins et al., 2004). Stepfamily education has been advocated for years as a way to educate and empower stepfamily members (Ganong & Coleman, 1989; Higginbotham, Miller, & Niehuis, 2009). Owing to financial complexities, it has been recommended that money management be covered in RE programs for stepfamilies (Adler-Baeder & Higginbotham, 2004; Lown, McFadden, & Crossman, 1989). Although several curricula include modules on finances, there has not been research specifically evaluating perceived helpfulness to participants.

Stepfamily Education in Utah

Beginning in 2007, the Utah Stepfamily Education Initiative supported approximately 30, free, 6-week, stepfamily RE courses throughout the state each year (Higginbotham, n.d.). With federal and state funding, courses were offered via a partnership between the land-grant University and community family-service providers (i.e., Head Start, Family Support Centers, etc.). Smart Steps: Embrace the Journey (Adler-Baeder, 2007), a 12-hour research-based curriculum, was used in all courses. Approximately half of Lesson 2 addressed financial issues. The content was not designed to be prescriptive and states “there is no definitive answer from research” regarding the “best way” to manage funds in a stepfamily (Adler-Baeder, 2007, Lesson 2, p. 5). Rather, the objective of the curriculum was to facilitate discussions between and within participating couples regarding their financial expectations, assumptions, habits, and traditions. Couples discussed creating monthly or annual budgets, who would handle the budget, comfort levels with debt, how financial emergencies would be addressed, and so on. The curriculum also provided financial worksheets and taught negotiating skills. In addition, throughout the curriculum, couples were taught and engaged in activities that reinforced effective communication and conflict resolution skills. Details and a review of the curriculum have been published elsewhere (see www.stepfamilies.info/smart-steps.php and Adler-Baeder & Higginbotham, 2004).

Objective

Data from the Utah Stepfamily Education Initiative have previously been used to evaluate various components of stepfamily RE including facilitation, recruitment, and retention (e.g., Higginbotham & Myler, 2010; Skogrand, Reck, Higginbotham, Adler-Baeder, & Dansie, 2010; Skogrand, Torres, & Higginbotham, 2010) as well as specific outcomes (e.g., Higginbotham & Skogrand, 2010; Higginbotham, Skogrand, & Torres, 2010). The objective of the present study was to focus on and evaluate perceived changes in financial management practices that occurred because of participation in the course. Consistent with Family Stress Theory, educational experiences and any associated increases in knowledge and skills can be resources that moderate and buffer common stresses, such as stepfamily finances. To explore this possibility, semistructured interviews were conducted with Smart Steps participants 1 year after program completion. Specifically, researchers explored what, if anything, participants had done differently about finances as a result of taking the course.

The reports from Latino participants were of special interest owing to the dearth of published literature on Latino stepfamilies in RE, in general, and their financial practices, in particular. In the Utah Stepfamily Education Initiative, approximately one third of courses were offered in Spanish. Latinos accounted for approximately 30% of those served. The extant literature provides some basis for our supposition that Latino stepfamilies may differ from other RE participants in several ways pertaining to finances. Past research suggests Latino’s financial behaviors, in general, tend to differ from those in other ethnic groups (Watchravesringkan, 2008). For example, Latinos are less likely to take risks with investments than are African and European Americans (Yao, Gutter, & Hanna, 2005). Mexican Americans as well as other Latino households have less wealth than do European American households, even when controlling for various factors (Campbell & Kaufman, 2006). Latino households tend to budget more toward shelter and clothing and are less likely to budget for entertainment, education, or health care (Fan & Zuiker, 1998). They have also been found to worry more about their present situations and are less likely to plan or prepare financially for the future compared with European Americans (Median, Saegert, & Greshman, 1996). More recently, 76% of Latinos reported their financial situations were in fair or poor shape compared with 61% of the general U.S. population (Lopez, Livingston, & Kochhar, 2009).

Method

Methodological Approach

The evaluation of the Utah Stepfamily Education Initiative, by nature of its scope and external requirements, was guided by “action research” precepts (Cassell & Johnson, 2006; Small, 1995). “Action research aims to contribute both to the practical concerns of people in an immediate problematic situation and to the goals of social science by joint collaboration within a mutually acceptable ethical framework” (Rapoport, 1970, p. 499). Consistent with action research postpositivist tenets, the present evaluation sought to more deeply understand the stepfamily education experience by collaborating with nonresearcher participants who “bring practical knowledge and experience about the situations that are being studied” (Small, 1995, p. 942). This was facilitated, as recommended in the recent decade review, through qualitative interviews designed to “enhance our understanding . . . provide much needed insight into mechanisms underlying observed associations . . . and shed light on the considerable diversity in remarried-family and stepfamily experiences” (Sweeney, 2010, p. 678).

Sample

During the first three programmatic years of the Utah Stepfamily Education Initiative, a total of 596 couples were served. Per federal reporting guidelines, only couples who attended four or more of the six lessons were counted as “served.” As part of the qualitative evaluation, 122 participants were interviewed at the conclusion of the course and 62 were interviewed for a second time 1 year later. Because of geographical and budget constraints, interviewed participants were not a random sample. Rather, consistent with action research, a convenience sample was drawn of participants who were willing and able to be interviewed during the time periods and at the locations available to researchers (see Small, 1995). As a sample, interviewed participants were comparable to the total population of participants on measures of age, relationship status, and income. Owing to the large sample of participants in the initiative, some of the comparisons were statistically significant but had little practical significance. For example, the average age of interviewees was 34.03 years compared with 33.54 for noninterviewed participants—a difference of only 6 months.

The sample for the present study was the 62 participants interviewed 1-year after program completion (34 females and 28 males). Their ages ranged from 22 to 48 years, with an average age of 34 years. Consistent with the overall initiative proportions, 43 (69%) of the interviewed participants were married and 19 (31%) were in an unmarried stepfamily relationship. Married participants had been married 3 months to 13 years (M = 4.8 years married). Those who were not married had been together for an average of 5 years. Consistent with the targeted population of low-income stepfamilies, the median income for the participants was in the $15,001 to $20,000 range.

Those interviewed 1-year after program completion were 32 Latino participants, 27 European American participants, 1 Native American, and 2 who self-identified as other. The proportion of Latino participants interviewed (52%) represented a purposefully oversampling inasmuch as they consisted of only 30% of participants in the overall initiative. The Latino and European American participants did not differ statistically on any of the demographic variables.

Procedure

Approximately 1 year from being interviewed after their respective courses, and using contact information provided at enrollment, efforts were made to contact the sample of 122 postprogram interviewees. Those who were tracked down were extended an invitation to be reinterviewed and offered a $20 cash incentive for their time. Interviews lasted between 30 and 45 minutes. The goal was not to just identify “if”, rather “how,” “why,” “in what ways,” and “for how long” the stepfamily education course made a difference. The interview questions asked participants to reflect back on their time in the course and the year that ensued. Consistent with the formative purposes of action research, questions focused on what aspects of the course had been useful and what had not.

Examples of questions in the approved interview schedule included the following: “Are there issues that have come up in your stepfamily since the course that you wish you had learned about?” and “Are there things that you used from the course that worked well for a period of time, but were difficult to maintain? What were the obstacles in maintaining the changes?” Findings, not related to finances, from these interviews have been previously reported (Skogrand, Dansie, Higginbotham, Davis, & Barrios-Bell, 2011; Skogrand, Davis, & Higginbotham, 2011). This study focuses exclusively on the responses given to the question: “Are there things you have done differently because of what you learned about finances in this course? Please explain.” Trained research assistants conducted all interviews. Native Spanish speakers conducted the interviews with Spanish-speaking participants. A team of native Spanish speakers also transcribed, translated, and validated translations.

Spanish and English interviews were analyzed using the procedures described by Bogdan and Biklen (2003). One researcher read through all 62 transcripts and pasted into a separate file any data that were related to money and/or changes in financial practices. Two researchers then independently read all relevant data and identified possible coding categories based on the common themes described by respondents. Two clear and reoccurring themes emerged and were subsequently agreed on by both researchers: (a) Yes, there were positive changes and (b) No, there were no changes since taking the course. Using the coding categories, each researcher then independently coded all the data. Codings were compared and were consistent for 59 of the 62 cases (95%). For the three cases in which there was not initial agreement, the two researchers reviewed and discussed the data together until there was consensus.

Results

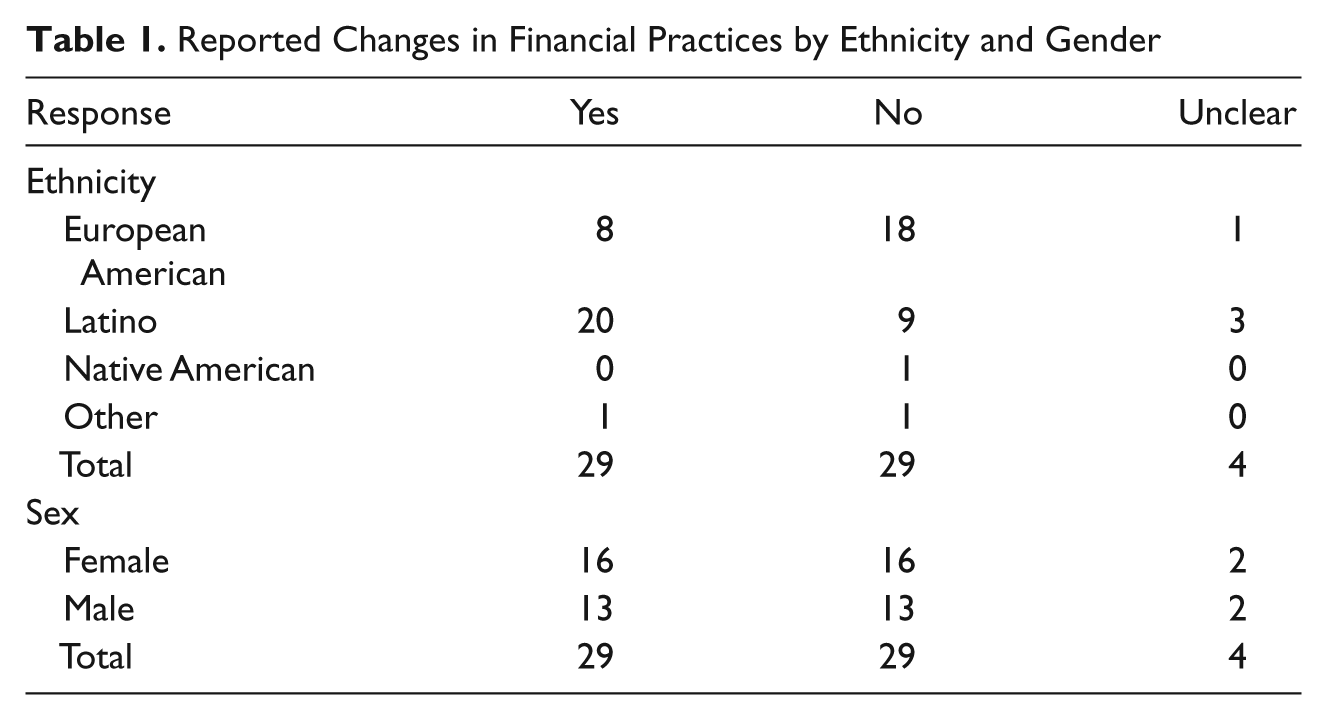

Of the 62 participant interviews, 29 participants reported they learned or changed something in their financial practices as a result of the course, 29 participants reported they did not change their practices, and 4 participants were unclear in their response. Quotes in this section are followed parenthetically by the participants’ gender, ethnicity, and age. Table 1 depicts the proportion of responses by ethnicity and gender.

Reported Changes in Financial Practices by Ethnicity and Gender

Positive Changes as a Result of the Course

Twenty-nine participants indicated they experienced and implemented positive changes in their financial practices. The majority of the participants who experienced positive changes indicated that they learned how to use a budget and/or learned to save (n = 13). Other participants learned to work together (n = 10). There were several other, less descriptive, comments also suggesting positive change (n = 6). For example, one participant simply reported “Yes” there was an improvement in financial practices without further explanation.

Budgeting and savings practices

Thirteen participants identified how learning to use financial practices, including budgeting and saving, was the primary catalyst for positive change. Participants began to take closer notice of what they were spending, they felt more organized, were cognizant of saving money, and were exposed to new financial management strategies.

Several participants commented that the course helped them notice what they were spending. One participant said, “We watch what we do with the money instead of being somewhere and saying ‘Oh, we’re hungry,’ and spending $60 to eat for everybody. We’ve been watching that” (Male, European American, 29). Another said, “I try not to spend too much. Before, even when we didn’t have money, we would go to the store and buy things we didn’t need” (Male, Latino, 31).

Other participants discussed feeling more organized or being better informed about their financial situations as a result of the course. One participant commented, “We’re not going to say, ‘Well, you’ve got to wait until payday.’ We’re organized better” (Female, Latina, 31). Another reported the thing she implemented to change her financial practices was, “Just trying to keep a budget, knowing that my husband has to pay child-support and stuff, and mortgage payments and everything” (Female, Latina, 23).

For three of these participants, learning to save for an emergency was very important. One said, “Before, when I would get paid I would spend my money on stupid little things, but now I try to save for important things that may happen” (Male, Latino, 43). Another participant stated, “My husband is the one who works and we try to pay the bills and if we have money left over then we save it for an emergency, for our kids or a family member” (Female, Latina, 36). Another discussed the current economic condition and how the course taught him, “To save money, not to splurge, now that the economy is in crisis, save in the bank” (Male, Latino, 31).

One participant spoke about building a new system, one in which his wife was more involved and she knew more about what was going on with their finances. He said,

We started to have a new system, agendas with dates and budgets. Then she began to ask for advice as to how I managed it. It’s less work for me, less stressful. And the best of all is that she does not demand to know any more. I mean, I should have done this earlier. (Male, Latino, 32)

Working together

Ten participants who reported positive changes talked about working with their partner. As one participant said, “We had problems with finances because sometimes I felt like I was spending too much money and she wasn’t at all or vice versa. But talking in the course, they made us see that we have to work together” (Male, Latino, 29).

Participants reported learning skills and strategies that enabled them to effectively work on their financial management collaboratively. A male participant said, “We work together on finances. We sit down and talk together” (European American, 35). Another similarly stated, “It’s like we learned how to put our money together and used it that way, instead of just having our own money” (Male, European American, 22). Another spoke about their decision as a couple to consciously apply what they had learned in the course:

The thing we’ve done differently is try to get out of debt and build our credit. And we did that just by sitting down and saying, “Okay, let’s take what we’ve learned here and try to apply it so that later we can get a house.” And we were able to do that. (Female, European American, 32)

One participant spoke about sharing expenses and coming to an agreement together. “I work and he works. Both of us now share expenses, not everything but I help him with some things and he takes care of other things, but we are in agreement” (Female, Latina, 40). Another participant talked about her financial situation before the course, when she felt like she was solely responsible for her son and his needs. Since the course, she and her partner subsequently decided as a couple they would both contribute to purchasing items for her son. She said, “Now we share the money, and I think it’s because of the course we took” (Female, Latina, 25).

Some participants discussed the benefits of learning and trying, as a couple, new money management strategies. One participant felt their arguments had decreased once they learned how to put their money together. She said, “We would argue because he makes more money, ‘You don’t buy me anything or give me anything.’ But now everything is together” (Female, Latina, 28). Another participant said it was helpful to “know how to distribute the money of both. I think that was helpful for me and for my wife” (Male, Latino, 30). In the curriculum and class discussion, several techniques were shared. Of this dynamic, one participant reported:

In the course, it was okay to hear about techniques to know how to work out finances, to understand each other, and how we should be cautious. But the time came when we had to do it, and it’s been successful for us to take a technique they gave us. We have our income, we have a joint account, we distribute our expenses, but we also have a separate account to deposit an amount for emergencies. (Female, Latina, 40)

For some participants, working together was captured in how they discussed their communication about finances. For example,

There have been a couple of times where he’s made major decisions financially without talking to me at all, and I tried to get him to understand that if I had done the same thing he would have freaked out. I’ve noticed that it hasn’t happened since I talked to him about it. If there is any major decision that needs to be made, then we need to make sure we realize that we are a partnership and talk, and find out how the other person thinks about it, before we move forward. (Female, European American, 36)

Other reasons for improved practices

The remainder of the coded “yes” responses varied in content and detail. For example, one participant felt the financial portion of the course was helpful because it provided useful “hints” (Female, European American, 29). Two participants identified the course as being empowering. One said, “I felt like what I got out of it was more of a ‘Yes! You can do it!’ kind of thing” (Male, European American, 32). The other recognized she now had the ability to examine their financial situation from her husband’s perspective. One husband came to recognize that his partner was better with finances. Consequently, they changed who managed the money. He said,

I used to think that being the man of the house, I controlled the money, paying the bills, but I was always short on cash. Now, I give my check to my wife and she controls it and things are looking better. (Male, Latino, 36)

No Changes as a Result of the Course

Twenty-nine participants did not report changing their financial practices as a result of the course. Several succinctly answered the question with a straightforward “no” providing no further explanation (n = 4). The majority coded as “NOs” reported functional financial management practices that dated back to the beginning of their relationship (n = 13). Although the RE course may have reinforced their strategies and practices, the individuals did not report changing anything because of Smart Steps participation. Others had experienced financial difficulties during their relationship but had come to agreement prior to participation in Smart Steps (n = 5). Consequently, RE was not viewed as particularly helpful in terms of finances. Others reported ongoing financial difficulties (n = 7). One of these participants reported that instead of learning to handle their own finances, the course led to a decision to outsource them. She said, “We took the easy way out, instead of learning we just hired someone to do it” (Female, European American, 26).

Set practices from the beginning

Thirteen of the participants who reported no change in their financial practices discussed how their financial management system had already been in place since the beginning of their relationship. One participant said, “We don’t have any problems, we are both savers. We are not spenders” (Female, Other, 40). Several participants reported a smooth financial transition from the very start of their stepfamily. One participant said, “We were always kind of a unit from the finance end, we’d sit down together to do bills . . . we’re in it together” (Male, European American, 34). Another said, “Everything is ours and nothing is mine and nothing is his. Everything is ours. And we’ve done that from the beginning” (Female, European American, 31). One participant spoke about experiencing difficult financial situations prior to her current relationship, which contributed to their approach to manage finances from the beginning on their marriage. She said,

I had to do my best to try to support me and the kids. I was on food stamps and so I had to be tight and I couldn’t give in to things. And my husband, he’s basically the same way. When he got divorced . . . he had to support himself and so that’s what helped us in our relationship from the beginning was that we were on the same page as far as finances go and we discussed things with each other. (Female, European American, 37)

Because what they were already doing was working, several participants did not see a need to change. One said, “I am the one who handles finances, so I do the accounting. So it hasn’t been different” (Female, Latina, 41). Another said, “You know, my wife does all the finances. I’m okay with money, but she’s a wiz with money” (Male, European American, 24).

Resolved previous difficulties

Five participants noted prior financial difficulties, but discussed how they had come to a resolution prior to the Smart Steps course. One participant said, “My finances are just as tight as they were. I’d just as soon go with my budget, so I feel we didn’t learn anything that was new for us” (Female, European American, 41). Another participant felt the financial content may have been helpful for other people in the program but not for her. She said, “It wasn’t really an issue for us because we always had just one little tiny pool of money” (Female, European American, 31). A male participant made a similar observation, “There wasn’t really anything about finances in the class that really helped me on that because I pretty much already knew what I had to do” (Male, European American, 34).

Continuation of difficulties

Seven participants reported continued financial difficulties, as exampled by the participant who said, “No, we’re still bad at our finances. It’s worse now” (Male, European American, 35). Some participants blamed long-standing habits. As one participant reported, “No, I’m just an impulse spender and that is something we fight with a lot. We really struggle to get me over that impulse spending” (Female, European American, 29). Another participant said, “We’ve gotten more debt this year. The goal was paying off the credit card and we had too much fun in the summer” (Female, European American, 37).

Three of the participants felt they did not retain what was discussed. One participant said, “I’m horrible at finances. If there was something I learned in that course about finance, I obviously didn’t retain it or use it, because I’m still a mess. My finances are still a mess” (Male, European American, 36). Another participant said, “I don’t remember us talking a lot about that in class. If we did, I don’t know where my mind was because that’s something we struggle with, keeping the budget good and getting the credit card paid off” (Female, European American, 37).

Unclear Responses

There were four participants whose comments were coded as “unclear.” Two simply felt they could not say whether the course was the cause of change in their financial practices. For example, “We’re changing our finances based off of our family, and I don’t know if that’s necessarily off of the course, but it’s based off of goals that we have” (Female, European American, 31). Another participant gave a conflicting report, saying at one point in the interview, “It’s all the same. What is his is his, and what’s mine is both of ours” but then later saying, “I have learned to try to save” (Female, Latina, 31). The final participant felt he could not honestly answer that question since his wife was in charge of the finances.

Discussion

Theoretically, stepfamilies who successfully adapt to stressors do so by employing resources, which can include relationship skills such as communication, negotiation, and conflict management (Crosbie-Burnett, 1989). Courses in RE can foster new and expand existing resources—even in low-income families—by teaching and reinforcing effective relationship skills (Adler-Baeder, Robertson, & Schramm, 2010; Hawkins & Fackrell, 2010). In addition to the specific stepfamily-related content, the general relationship skills and the group nature of RE are believed to help couples deal with common stepfamilies problems (Messinger, Walker, & Freeman, 1978; Skogrand, Torres, et al., 2010).

One of the targeted objectives of Smart Steps is to “Identify financial issues and improve communication over financial issues” (Adler-Baeder, 2007; Lesson 2, p. 1). This objective is strategic considering financial issues are often associated with increased arguments regarding finances as well as other issues (Dew, 2009). To facilitate the targeted outcomes, the associated activities include group discussions, individual worksheets, and couple talk around expectations, assumptions, habits, traditions, and financial goals. This approach and our findings are consistent with conclusions from other scholars: “Instead of a prescription for managing complex financial relationships . . . it appears that most important for healthy stepfamily couple functioning is agreement (Adler-Baeder et al., 2010, pp. 309-310; see also Coleman et al., 2001).

In the Smart Steps group discussions, class members identified unique money challenges in stepfamilies. From that list, they derived questions and topics that should be talked about, negotiated, and decided on by each couple. From personal experience, they shared pros and cons of different types of money management strategies (e.g., one-pot, two-pot, mixed). Using worksheets, individuals and couples then considered the hows, whys, and whats of their particular financial histories, practices, and goals. Questions, provided in the curriculum, helped guide their discussion, such as: How will unexpected expenses be handled? What will you do if another parent is not meeting their child support obligation? What is the limit for spending without asking the other?

The objectives and activities of Smart Step were informed by extant stepfamily research and best practices for family life education (Adler-Baeder, 2007; Adler-Baeder & Higginbotham, 2004). The opportunities to discuss finances, as a group and as a couple, are important for several reasons. First, there is evidence that remarried couples tend to have more autonomous views toward finances; yet few couples discuss finances in-depth before remarriage (Allen, Baucom, Burnett, Epstein, & Rankin-Esquer, 2001; Burgoyne & Morison, 1997; Coleman & Ganong, 1989; Ganong & Coleman, 2004). Second, the process of hearing other couples discuss common issues normalizes problems and facilitates social support (Skogrand, Torres, et al., 2010). Scholars have suggested support and validation from fellow program participants can enhance the effectiveness of the resources offered and may lead to more positive programmatic impacts on marital and family functioning (Adler-Baeder et al., 2010). Third, couples may not know what they do not know. Group discussion and brainstorming can bring forward new concepts and previously unconsidered strategies (Messinger et al., 1978; Skogrand, Torres, et al., 2010).

In the present study, consistent with Family Stress Theory (McCubbin & Patterson, 1983), participants varied in their financial stressors, perceptions, and existing resources (e.g., relationship skills, and knowledge and use of financial management practices). Approximately one third of those interviewed had functional strategies that predated their Smart Steps participation, and consequently, no change was reported as a result of the course. On the other hand, about one half of interviewed participants reported adopting or using new relationship patterns such as working together, communicating more, budgeting, and saving.

Of the 29 individuals in this study who experienced positive changes regarding finances, 13 interviewees talked about learning practices such as budgeting and saving. In the interviews, it was common to hear changes in perception and behavior as exemplified by the participant who said, “Before, when I would get paid I would spend my money on stupid little things, but now I try to save for important things that may happen.” Prioritizing, budgeting, and saving are skills commonly developed under the guidance of financial counselors and are not necessarily dependent on couple dynamics or relationship skills. However, 10 of the participants described how the RE course helped them to communicate, work together, and agree on financial issues. This supports the family stress theoretical assertion that communication is an important component of stepfamily bonadaptation (see Crosbie-Burnett 1989).

Responses about positive change either highlighted skills traditionally taught by financial counselors (i.e., budgeting and saving) or those traditionally taught by RE facilitators (i.e., working together and communication). In light of these findings, questions which have been raised before should be repeated here (e.g., Skogrand, Johnson, Horrocks, & DeFrain, 2011): Should financial counselors and relationship educators work together to help couples communicate more effectively and develop trust, which provides the foundation to more effectively address financial issues?

The results of this study suggest financial counselors and relationship educators could work collaboratively. It may be that couples struggling with finances are better served by attending both RE and financial counseling rather than just one or the other. After all, how can a couple that does not communicate well and does not trust each other effectively develop a savings plan or a budget together (see Skogrand, Johnson, et al., 2011)? Another implication of these findings is that program developers can merge finance and relationship education, as is the case with Smart Steps. Even though the finance-specific content was relatively brief (one half of Lesson 2 in a six-lesson curriculum), 29 of 62 interviewed participants still reported positive changes in some aspect of their finances as a result of the course. Rather than attributing all the change to the actual financial content, it is more likely that the relationship skills of communication and conflict resolution, taught throughout the curriculum, enabled and empowered participants to address their financial issues.

On the other side of the coin, it is important to note that seven of the interviewed participants with financial problems prior the course still had the same problems after the course. For this group, the limited content on finances and the more general focus on relationship skills were not seen as sufficient to change their financial problems. These participants cited various reasons such as not remembering, not incorporating what was taught, or inability to change habits. Others wanted more information and assistance like the participant who said:

I feel like we really didn’t have enough time to cover everything because finances are a huge stress and burden, you know. I feel like, you know, there were some ideas thrown out there of what we can do, but I feel like maybe we need more practice in working through it with somebody instead of just being told, well, here is A, B, and C. How do we put that into practice?

It is unclear if the lack of positive change for these participants ultimately stemmed from their lack of financial education or relationship skills; however, the implication is that some couples in stepfamilies may need more finance-specific knowledge and skills while others may simply need general relationship education.

The fact that Latinos were more likely to report positive financial changes deserves attention, and we can only speculate about the reasons for this difference. We speculate that many of the Latino participants in this study, by virtue of state demographics, were likely to have an historical understanding of finances from other countries (U.S. Census Bureau, 2009). Although country of origin was not asked of participants, facilitators of the Spanish courses provided anecdotal data on participants indicating predominately Mexican descent. It has been reported that Mexican Americans, compared with European Americans, are more likely to focus on present day financial issues and not be as concerned about longer-term money management behaviors (Median et al., 1996). These same researchers conclude that Mexican Americans are less likely to be concerned with financial planning for the future, which affects budgeting and savings. Some of our participant interviews corroborated these previous research findings; however, others did mention saving and thinking of the future.

One possible explanation for why Latino participants were more likely to see improvement in financial practices could be the novelty of the experience coupled with accessibility of resources. The class discussions and information may have presented novel ways of thinking about and handling money. Related findings have been published on relationship topics such as intimate partner violence. There are fewer community resources for Latino families (Gonzalez-Guarda, Peragallo, Vasquez, Urrutia, & Mitrani, 2009). In Utah, Smart Steps is the first-of-a-kind program to help stepfamilies; and it is one of few programs that specifically target Latino families at all on relationship topics in Spanish. Another explanation stems from research that has found Latinos, particularly of Mexican origin, have lower financial satisfaction than other groups (Coverdill, López, & Petrie, 2011). The results of our study may reflect a greater variability and corresponding range to improve in areas like financial management and practices.

We might also speculate that Latinos in this study were more likely to report changes in financial practices because the information was presented within the context of their family. Because family is so important in Latino culture (Skogrand, Barrios-Bell, & Higginbotham, 2009), the connection made between (step)family well-being and financial practices may have made the financial information more meaningful. For example, one Latina participant indicated that she had learned to save for an emergency “for our kids or a family member.”

Past research has suggested that for Latinos, access to information and education are important factors for planning for the future. Yet Latinos in the United States may have less access to financial information that is trusted, translated, and helpful (Delgadillo, Sorensen, & Coster, 2004). Our findings add to this past research and imply, for Latino stepfamily education, there could be more discussion, more information, and more time devoted to financial management. However, more research needs to be conducted to draw definitive conclusions.

It has been suggested that regardless of the content issue, when teaching RE for stepfamilies, practitioners should be sensitive to heterogeneity within Latino culture and households (Skogrand et al., 2009). For example, although some Latino households may not have a history of saving or planning for the future, others may be very skilled in these areas. Facilitators should also recognize that much of what is included in stepfamily curricula is not based on research with Latinos (Adler-Baeder & Higginbotham, 2004; Adler-Baeder et al., 2010). Consequently, information should be presented in an indirect and nonprescriptive manner. Facilitators should consider using phrases such as “research with some groups has found . . .” or “some families find . . .” According to Skogrand et al. (2009) “this approach can help participants to take the information and apply it in ways that fit their cultural values and traditions” (p. 124).

In summary, the 1-year postprogram interviews of Smart Steps participants suggest that some experienced positive changes in their financial practices whereas an equal number of participants did not. Although some family life educators might be discouraged by these findings, it should be noted that the time actually spent on finances out of a 12-hour course was relatively short (approximately 1 hour). We might conclude that given the variety of topics covered in the curriculum and the limited time spent specifically on finances, the reported changes were substantial. Components of stepfamily education will ultimately serve some individuals, couples, and families, and not others. Any time family life education is provided, it is likely participants tune in to the issues that are particularly relevant in their lives at that point. One participant summarized this programmatic dynamic in her statement, “Well, some things didn’t pertain to us. Finances weren’t really a concern for our scenario specifically, but I knew they were for other people.”

In light of the heterogeneity in stepfamilies’ needs and issues, program development should not assume that all curriculum content will be, or needs to be, applicable to all participants. Rather, a comprehensive approach may still be the most practical strategy to ensure that there will be at least something for everybody. Some modules may really resonate with particular participants whereas other content may not be applicable. Yet rather than viewing this as a negative programmatic implication, it can be seen as an opportunity to engage “successful” participants to teach and help empower their peers. Furthermore, even the participants in our study who did not feel the course affected their personal financial practices were self-reflective and were able to discuss their skills, often using the language and terms from the course. This raises the possibility that these participants may have learned new skills or reinforced existing skills, even though they did not acknowledge as much in their qualitative interview. Future quantitative evaluations could assess this possibility.

Even though approximately half of the interviewees reported no change in their finances, their experience in Smart Steps was far from negative. Although not analyzed and presented here, many of these same participants reported improved relationships with children, their partner, and increased family unity (Skogrand, Dansie, et al., 2011). Other studies from the Utah Stepfamily Education Initiative suggest that participants appreciated the group format that brought together stepfamilies with very different issues, experiences, and insights (Higginbotham & Skogrand, 2010). So although a participant may have already mastered stepfamily finances and may not personally benefit from the finance portion of curriculum, he or she can share wisdom and experience with fellow class members. This model not only fosters group cohesion but also engages participants in the discussions and provides social support, which repeatedly emerges as a highly rated and important aspect of RE for stepfamilies (Adler-Baeder et al., 2010; Skogrand, Torres, et al., 2010).

Conclusion

Scholars have speculated how exposure to program content in the areas of financial management might result in enhanced general stepfamily functioning (Adler-Baeder et al., 2010). The findings from this study begin to address this possibility, provide preliminary data, and lay a foundation for future inquiry. It appears that for some participants the exposure to financial content may do very little because they already have successful and functional practices. Others may begin to recognize and try new strategies, like working together, that hold the potential for improved financial cooperation and greater relational harmony overall.

This study provides new information about potential benefits, for low-income and Latino participants, of incorporating a financial component into stepfamily RE programs. However, this contribution to the literature is not without its limitations and is intended to spur further research and discussion. The findings presented herein should be considered tentative and the study should be viewed as an initial step into a more robust evaluative effort with regard to conducting financial education with stepfamilies. For example, in what specific ways should stepfamily education, and financial modules in particular, be different for diverse and minority stepfamily audiences? What is the optimal balance of financial education and general relationship education in a RE program? It would also be useful to know more about participants’ knowledge about finances and relationship skills coming into the course, and how baseline knowledge moderates benefits in the short- and long-term following RE participation.

Many of the limitations of this study (e.g., sample and design) are consistent with other programmatic evaluations with budget, time, and data constraints (see Bamberger, Rugh, Church, & Fort, 2004). Yet qualitative action research and its variations (i.e., empowerment, participatory, and feminist approaches) are not necessarily intended to be representative or generalizable. Rather, the intention is to contribute to practice, policy, and social discussions (Small, 1995). To that end, the voices presented in this study offer additional insight and encouragement to those engaged in healthy relationship initiatives, including the Federal Hispanic Healthy Marriage Initiative. And, yet, they also speak to the diversity in RE participants’ needs, experiences, and benefits (cf. Higginbotham et al., 2009; Hawkins et al., 2004). As the field moves forward they challenge us, as scholars, policy makers, program developers, and educators, to be cognizant of the individual while we attempt to serve the masses.

Footnotes

Authors’ Note

Any opinions, findings, and conclusions or recommendations expressed in this material are those of the authors and do not necessarily reflect the views of the U.S. Department of Health and Human Services, Administration for Children and Families, the funding agency.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Funding for this research was provided, in part, by the U.S. Department of Health and Human Services, Administration for Children and Families, Grant No. 90FE0129 and Grant No. 90YD0227.