Abstract

We document the gender wealth gap among single individuals aged 50 or more, an age group where wealth differences might be particularly pronounced and relevant for economic well-being. We investigate to what extent differences in partnership histories can explain the gender gap in household wealth among singles in four countries using data from SHARE. Whereas we do not find a gender gap in wealth of singles in the Czech Republic, we find that single men live in wealthier households in Austria and Sweden than single women. In Spain, we observe a gender gap favoring women which is partly explained by the high rates of widowhood among single women as well as high home ownership rates. Our results underline the importance of understanding selection into singlehood for interpreting gender gaps in household wealth.

Introduction

Wealth is increasingly being studied as part of individuals’ economic well-being. Wealth provides households with financial resources and can function as a safety net during economically difficult times (Pfeffer & Schoeni, 2016). Individuals tend to accumulate wealth as they age and start consuming wealth at older ages. This makes old age a period of life where individuals rely more heavily on their wealth as income usually decreases after retirement (Gornick et al., 2009). Hence, wealth differences are a particularly important determinant of economic inequalities during old age (Delfani et al., 2015). In this paper, we study to what extent there are gender differences in household wealth among the single population above 50 years of age. Our main research question is: Do single men live in wealthier households than single women after age 50?

Documenting the gender gap in wealth is not straightforward because wealth is in most cases measured at the household level. This implies that any within-household inequalities in wealth are not visible, but likely do exist as women generally have less control over household wealth (Tisch & Lersch, 2020). In a few contexts, most notably Germany, individual data on wealth is available and gender gaps in individual wealth have been found there (Grabka et al., 2015; Kapelle & Lersch, 2020; Kapelle & Vidal, 2022; Meriküll et al., 2021; Sierminska et al., 2010). For other contexts, studies have to rely on household wealth and, therefore, often concentrate on the gender gap in wealth among single individuals. Studying only single individuals is interesting in itself, even though one cannot provide a picture of gender differences in the entire population. The proportion of singles is increasing steadily in more and more European countries and especially among the elderly population, this makes the (potential negative) consequences of singlehood for wealth an important topic of study (Addo & Lichter, 2013; Bonnet et al., 2023; Nutz & Lersch, 2021; Ulker, 2009; Zissimopoulos et al., 2015).

Studies on the gender gap in wealth among single individuals mostly find insignificant differences at the median or mean, but gaps favoring men at the top of the wealth distribution (Austen et al., 2014; Schneebaum et al., 2018; but see Anglade et al., 2017; Schmidt & Sevak, 2006). This conclusion does not hold universally across countries. For instance, the comparative study of Ravazzini and Chesters (2018) does not report a clear gender gap in Australia, but a strong gender gap in Switzerland. In Australia, housing wealth compensates for women’s lower financial wealth at the bottom part of the wealth distribution, whereas in Switzerland households at the bottom part of the distribution are unlikely to have housing wealth.

One of the issues that complicates the interpretation of gender wealth gaps among singles is that singlehood is not randomly distributed across individuals. For instance, resourceful women are prone to remain single or divorce in more traditional contexts (Bellani et al., 2017; Härkönen & Dronkers, 2006). An understanding of gender gaps in wealth among single individuals should therefore start with an understanding of who is single and how selection into singlehood relates to the gender gap in wealth. In this paper, we aim to do this by documenting the importance of partnership histories for the gender gap in wealth among older individuals (50+) in four countries. We ask three main research questions:

First, is there a gender gap in household wealth between single men and single women above age 50? And, second, does this gap vary across countries? Despite the importance of wealth in older age, existing research on the gender gap in wealth has mostly focused on the population overall or on the working age population (for exceptions, see Addo & Lichter, 2013; Bonnet et al., 2023; Nutz & Lersch, 2021; Ulker, 2009; Zissimopoulos et al., 2015).

Third, we ask: Can differences in the prevalence and returns from partnership histories explain the gender gap in wealth among single persons aged 50 or more? We believe that looking at partnership histories (whether having been in a union, divorced, separated, or widowed) becomes particularly important at older ages. Previous research has shown how women’s relationship trajectories are more consequential for their wealth than for men’s (Bonnet et al., 2023; Ulker, 2009; Zissimopoulos et al., 2015), but it remains unclear to what extent these differences could explain the gender gap in wealth. An exception is the study of Kapelle and Rowold (2025) who find an enduring disadvantage of divorce for wealth accumulation for women and for mothers in particular in Germany.

To answer our research questions, we use data on household wealth from SHARE on individuals aged 50 or more from four countries. We selected four countries that differ in terms of levels of divorce and separation, marital property regimes, and (gender) welfare regimes: Austria, Czech Republic, Spain and Sweden covering the years 2004–2017.

Partnership Histories and Gender Differences in Household Wealth During Older Ages

In this literature review, we will discuss how different partnership histories relate to wealth and how this differs between men and women. We first focus on gender differences in the prevalence of each considered category of partnership histories and then on how their association with wealth accumulation could differ between men and women.

Never Partnered Individuals

Because partnering is positively related to wealth accumulation (Bonnet et al., 2023; Kapelle and Rowold, 2025; Zissimopoulos et al., 2015), people who never partner are likely to have relatively low levels of wealth. Even though gender differences in the lifetime likelihood of never having a partner are not often explicitly studied, men appear more likely to have never cohabited or married by late adulthood than women (Bellani et al., 2017; Wiik & Dommermuth, 2014). There are, however, two reasons why this might not directly translate into higher wealth among women as compared to men.

First, there are important differences in the amount of wealth single men and women accumulate. Due to the gender gap in earnings, never partnered women will have less possibilities to accumulate wealth than never partnered men (Sierminska et al., 2010). Gender differences among the never married can also arise due to the reception of transfers and inheritances. Even though there is no clear evidence that men receive more inheritances than women in high-income countries (Black et al., 2022; Edlund & Kopczuk, 2009), men more often inherit family businesses (Crowther & Roos, 2025). Qualitative research shows how the valuation of assets in inheritance processes often benefits the person who inherits the family business (Bessière & Gollac, 2023). Hence, single men are likely to accumulate more wealth than single women.

Second, selection into partnering has been very different for men and women. Studies on partnering have shown how higher educated women are more likely to remain single in more traditional contexts, but that this changes when gender egalitarianism becomes more widespread (Van Bavel et al., 2018). Lower educated men are more likely to remain single across contexts, regardless of levels of egalitarianism. The selection of resourceful women into singlehood can also be interpreted the other way around: staying single might make it easier for women to accumulate wealth. Never partnered women are less directly affected by gendered obstacles to accumulate wealth within relationships, as men’s careers are often prioritized in relationships, especially after the arrival of children (Cooke, 2014).

In line with this argument, Kapelle and Vidal (2022) find the lowest gender differences in individual wealth among the never married in Germany, while Kapelle and Rowold (2025) find similar results for the age group 50–59. In addition, using SHARE data on the older population, De Wilde et al. (2011) found an insignificant gender difference for the never married in 13 EU countries. Hence, if resourceful women and less resourceful men select into singlehood, gender differences in wealth could be less visible among single persons, or even favor women, if selection into singlehood outweighs the impact of gender differences in earnings or inheritances.

Widowed Individuals

Compared to never partnered individuals, widowed persons are likely to have relatively high levels of wealth. Widowed individuals have benefited from the higher wealth accumulation within couples over the life course, and can receive (part of) their partner’s wealth after their partner passes away. At the same time, widowed individuals are at a high risk of poverty as they lose access to their partner’s income and it will depend on the generosity and coverage of widow pensions to what extent this loss of income is compensated for (Ahn & Felgueroso, 2007).

Gender differences in wealth could be small among widowed individuals as both men and women inherit (part of) their former partners’ wealth. In line with this assertion, Sierminska and colleagues (2010) did not find gender differences in wealth among widowed persons in Germany, whereas De Wilde et al. (2011) did so for the 50+ population of SHARE countries. Streeter (2020) found that American men lose wealth after becoming a widower, but only in the short run, while for American women the drop in wealth after widowhood is more enduring. It is possible that some gender differences exist in access to inheritances. Even though both men and women inherit wealth from their former partners, biases within the legal system in inheritance processes can still lead to more favorable inheritances for men (Bessière & Gollac, 2023). In addition, women in general have less earnings or pensions than men and therefore lose more partner income after their partner deceases (Wilmoth & Koso, 2002) which can lead to rapidly declining levels of wealth with time since entrance into widowhood.

In short, because widowed individuals are likely to have relatively high wealth compared to never partnered individuals, a high share of widows among single women in a given country could lead to a relatively high level of wealth for single women as compared to single men, and in turn, a smaller gender gap in wealth.

Separated and Divorced Individuals

Separation and divorce can be costly events that drive down individuals’ wealth through direct legal and moving costs, loss of access to partner wealth and the elimination of scale advantages of living in a larger household (McManus & DiPrete, 2001; Zagorsky, 2005). Hence, divorced and separated individuals are likely to have relatively low wealth as compared to partnered, widowed and possibly also never partnered individuals. Bernardi and colleagues (2019) find that divorced or separated individuals have lower wealth than widowed individuals in the US and similar wealth to the never partnered.

The consequences of separation and divorce differ between men and women. Gender differences in wealth among separated persons can directly arise if household wealth is split unequally after separation between men and women. The scope for such gender differences will depend on the legal context and the applicable marital property regime. Boertien and Lersch (2021) did not find evidence for gender differences in how household wealth was divided after divorce in Germany, a context where only wealth accumulated after marriage is divided. However, they did find that women receive a smaller share of household wealth than men after separation from cohabitation, where property regimes are not applicable.

A second reason gender differences in wealth can arise after separation is because earnings and employment rates after separation are lower for women (Andreβ et al., 2006). Lower levels of post-separation income will prevent wealth accumulation and separated women might have to consume accumulated wealth. Lersch (2017) found slightly lower wealth among women following separation as compared to men, using individual wealth data, in line with what Kapelle and Rowold (2025) found for mothers.

In short, gender differences in wealth among single persons can be greater in contexts with high separation rates as women are less likely to re-partner Di Nallo (2019) and Ivanova et al. (2013) and because women lose more economic resources after separation.

Household Structure

The previous discussion has focused on partnership experience and its connection to wealth accumulation. However, given our focus on household wealth, not only partners but also other household members will matter for the estimated gender gap in household wealth. Older individuals can move back in with their children due to economic need or health reasons. Such economic need might arise particularly among divorced and widowed individuals. Given the higher economic need among older single women, they might be more likely to live with other adults as compared with single men. A study on Spain, for instance, found widowed women to be slightly more likely to live with other people than widowed men (Ahn & Felgueroso, 2007). Hence, older women who live alone in more traditional contexts, such as Spain, may be relatively wealthy as the unwealthy co-reside with other adults. We will see that this selection into singlehood of wealthy widows plays a role in explaining the gender difference in wealth in Spain.

Cross-National Variation in the Gender Gap in Household Wealth

In our study, we look at gender differences in household wealth in four countries: Austria, Czech Republic, Spain and Sweden. We selected these countries based on two criteria. First, we selected countries that differ on contextual characteristics relevant for gender differences in wealth: separation rates, marital property regimes, home ownership, and the extent to which welfare regimes support women’s paid work and careers (Gauthier & Koops, 2018). Second, we selected countries for which large samples were available in the SHARE data. Ireland was the only country available in the SHARE data from a market-oriented regime, but its sample appeared too small to obtain robust results. In this section, we discuss the different countries of our study and the characteristics based on which they were selected.

Austria has been classified as having a conservative welfare regime where social security aims to maintain family resources once faced with adversities, especially male breadwinners who have been active for a long period on the labor market (Esping-Andersen, 1990). Policies often do not incentivize women’s employment and the traditional family is strongly entrenched in family policies (Korpi et al., 2013). Levels of separation and divorce are higher than in Southern European countries but lower than in Scandinavian countries or the US (Andersson & Philipov, 2002). The default marital property regime in Austria is one labeled as deferred community of property (Rešetar, 2008), where assets accumulated during marriage are shared upon divorce or widowhood. In the latter case, assets are shared with any children or parents of the former spouse. Divorce law does not apply to cohabiting couples who break up (Perelli‐Harris & Sánchez-Gassen, 2012, p. 450).

The Czech Republic is a former socialist country that is difficult to place in the “classic” welfare regime typology (e.g., Kangas, 1999). Former socialist countries have specific features that include historical support for women’s employment and careers, but have gone against the general trend towards defamilialization since the collapse of socialist regimes (Saxonberg & Szelewa, 2007). For instance, access to childcare decreased in coverage in Czech Republic. Separation and divorce were and still are high (Andersson & Philipov, 2002). Marital property regimes do not cover cohabitations and assets accumulated during the marriage belong in equal shares to both partners except for inheritances and some other forms of “personal” assets (Králíčková, 2021). Widowed spouses share inheritances with children and parents of deceased persons.

Spain has been classified as a traditional country (at least for the older cohorts that we are studying here) that has some similarities to conservative countries but with much more limited social security provisions (Ferrera, 1996). The landscape for families and women has changed rapidly over the last decades, but, for the cohorts under study here, careers were not yet available to many women, cohabitation was still rare, and divorce rates were low (Andersson & Philipov, 2002; Dominguez-Folgueras & Castro‐Martin, 2013). Marital property regimes vary across regions but most regions have a community property regime. In Catalonia and the Balearic Islands, separation of property is the default regime (Rešetar, 2008). When a married person passes away, spouses generally share the inheritance with any living children or parents, but spouses receive all wealth if there are no descendants in some regions. A feature that is specific to the Spanish context is that many widowed persons do not live alone (Ahn & Felgueroso, 2007).

Sweden has been an example of a social-democratic welfare regime, where social risks are to a large extent assumed by the state (Esping-Andersen, 1990). In terms of family policy, policies have aimed at defamilialization by supporting the dual breadwinner model (Gauthier & Koops, 2018). Sweden is often considered a forerunner in terms of demographic change, as divorce and cohabitation spread among the population relatively early, and are also relevant for the sample of older individuals studied here (Andersson & Philipov, 2002). The marital property regime differs from that of the other countries because all assets of the couple are to be divided upon divorce, even though courts can adjust this division when considered unfair, such as after very short marriages (Rešetar, 2008). There are some provisions for the division of property among cohabiting couples but these are less comprehensive than for marriages (Perelli‐Harris & Sánchez-Gassen, 2012). After a person’s death, property is divided between spouse, children and parents, but the latter two groups only access these assets after both spouses passed away. What is more is that the economic exit costs for women are lower in Sweden compared to other countries due to the generous welfare state and the ample labor market participation of women (van Damme & Kalmijn, 2014), reducing the gender differences in economic well-being (including wealth) after separation.

Overall, these differences in separation rates, family policy regimes and legal contexts are likely to lead to cross-national variation in the gender gap in wealth. We can construct two opposing sets of expectations. On the one hand, we might expect a larger gender gap in household wealth in contexts where cohabitation is common and separation and divorce rates are high. Women suffer more economic consequences from separation and divorce, particularly after cohabitation, and women are less likely to re-partner after separation. This would lead to a particularly high gender gap in Sweden, and a low gender gap in Spain where most gender differences in wealth are likely to exist within households and not between singles.

This expectation would also hold if selection into partnerships determines gender wealth gaps. Because resourceful women are more likely to remain single in more traditional contexts, this might translate into a relatively smaller gender gap in household wealth in Spain, Austria, and the Czech Republic, respectively, as compared to Sweden. Hence, once considering partnership histories and selection into singlehood we would expect a large gender gap in household wealth in Sweden with high levels of separation and negative selection into singlehood, followed by Czech Republic, Austria, and a smaller gender gap in household wealth in Spain where few people separate and selection into singlehood is most likely to be positive.

On the other hand, when considering the stronger position of women in the labor market and the marital property regime of Sweden, which covers all marital assets, the opposite could be expected. Women in Sweden might accumulate more individual wealth and might also receive more assets after divorce than in Austria, Czech Republic, and Spain where default property regimes only cover assets accumulated during marriage (or none in some regions of Spain). Hence, if the labor market position of women and welfare state support following separation are more important for the gender gap in wealth we would expect a small gender gap in wealth in Sweden, and a larger gap in the other three countries.

Data and Method

We perform a comparative analysis of the gender gap in household wealth, using the Survey of Health, Aging, and Retirement in Europe waves 1–2 and waves 4–6 (SHARE 2004–2015) (Börsch-Supan et al., 2013 for methodological details). The advantage of SHARE data is that it has detailed information on wealth, household composition, as well as partnership histories (for important parts of the sample). Because partnership histories are a main focus, this puts SHARE at an advantage over other internationally comparable datasets like the Luxembourg Wealth Studies (LWS). Note that we do cross-check our estimates of gender gaps in wealth with LWS data where possible. SHARE has information on partnership histories in SHARELIFE waves 3 and 7, which we will use to partly construct a partnership history variable (see below).

See Bergmann et al. (2019) on response and retention rates of SHARE. To address issues of attrition, we weight our descriptive results by using cross-sectional design weights provided by SHARE that make each wave representative for the sex, age, and regional distributions of each country. Pooling all these waves (wave 3 is a retrospective SHARELIFE survey and does not contain similar questions on wealth), our sample size consists of 6,752 single men and 18,196 single women across four countries (Austria, Sweden, Spain, and the Czech Republic). A few cases are dropped due to missing values on employment situation. Our final analytical sample entails 5,085 single men and 13,607 single women. Single individuals living with other adults are not included in this sample as household wealth can be driven by other household members.

Wealth is measured as net household worth, which is the sum of net financial and net real assets. Net financial assets are the sum of bank accounts; bonds, stocks and mutual funds; and savings for long-term investments minus liabilities. Net real assets cover the share of the value of the home that is owned, the share of the value of own businesses owned, the value of car(s), and the value of other real assets minus mortgages or outstanding loans on these assets. Unfortunately, SHARE doesn’t have data on individual wealth and therefore we focus on household wealth. Note that we would have liked to take pension wealth into account, but (as also previous research has shown) this is not straightforward to do as pension wealth usually is not accessible until the time of pension (and its [latent] amount is difficult to estimate) and then it is paid out in the form of pension income. Instead, we discuss the role of pension income and its relationship to wealth later in the article and do robustness analyses controlling for pension income. See appendix, Tables A6a and A6b and the section robustness checks.

To account for the highly skewed wealth distributions and outliers, we use percentile rank scores (relative within each country). Previous research has shown that this is a good solution, as for instance income-wealth correlations turned out to be highly similar whether using rank scores, 99-percentile top-coded, or logarithmic transformations (Killewald et al., 2017). Due to missing values on specific wealth components, SHARE provides five imputations that we use in our decomposition analyses. We estimate our decomposition models five times and these five sets of results are combined into one set of coefficients (the arithmetic mean of the five sets of coefficients of each of the five decomposition results) and one set of standard errors, taking into account the variability between imputations according to the combination rules by Rubin (1987). The fully conditional specification (FCS) imputation method used by SHARE can be found in Christelis (2011).

Our focal explanatory variable is partnership history, which is based on a combination of current relationship status and information on any previous relationships. For ever-married single individuals, current marital status gives information on the route into the current spell of singlehood (i.e., never married, separation, or widowhood), and therewith captures broad categories of partnership histories (acknowledging that these include a possibly larger variety of histories). However, for never married individuals this is less clear as they could have cohabited in the past. Therefore, we used retrospective information from individual partner histories on cohabitation, separation, and widowhood (from SHARELIFE waves 3 and 7) to determine the partnership experience for never married individuals (recoding 19.5% of never married singles’ partnership history). We did not do this for all individuals due to the relatively large number of cases we lose (about 30%) once combining relationship histories with wealth information (from waves 1, 2, 4, 5, 6). To avoid dropping these cases, we created a separate category of never married persons with missing information on retrospective histories.

This leads us to the following categorization of partnership histories: (1) Never married or cohabited; (2) Separated from cohabitation; (3) Still legally married (but possibly already separated as respondents state they are single) or LAT; (4) Divorced or separated from marriage; (5) Widowed; (6) Never married, history information not available. We did a sensitivity check by using the SHARELIFE data as indicative of partner history and filled in all missing histories with current marital status (see Tables A4 and A5a and A5b in the appendix and section robustness checks).

Control variables that we consider are: age, education, and wave. Age is important because wealth usually declines after a certain age. Age at the time of interview is measured in four categories: 50–59, 60–69, 70–79, 80+; education at the time of interview is measured by ISCED categories: (1) Low (ISCED01-2), (2) Mid (ISCED3-4), (3) High (ISCED5-6). In additional models (see Appendix A6a and b), we also consider possible mediators between partnership history and wealth: employment status at the time of interview (Retired, Self-Employed, Salaried Employee, and Non-Employed), total household income (in quartiles; the sum of net earnings from (self)employment, regular payments of public and private benefits and transfers, income from rent and interest/dividend), and number of living children (including natural children, fostered, adopted, and stepchildren).1

We employ a Kitagawa-Oaxaca-Blinder decomposition approach (Blinder, 1973; Jann, 2008; Kitagawa, 1955; Oaxaca, 1973). This method allows us to understand the contribution of observed differences in composition to the gender gap in wealth, as well as the contribution of different effects that these observed characteristics have on wealth for men and women. In other words, it allows us to quantify whether gender differences in the prevalence of partnership histories and gender differences in the returns to these partnership histories contribute to the gender gap in household wealth.

The method relies on running OLS regression models separately for men and women where wealth rank is explained by partnership histories and other covariates. Subsequently, these coefficients can be used to simulate how high the wealth rank of men would be if (1) they had the same prevalence of partnership histories as women; or (2) if the effects of partnership histories were the same as observed for women. The intuition behind this method is as follows. To calculate the effect of compositional differences we apply the distribution across characteristics as observed for group 1 to group 2, while keeping the effects of these characteristics on wealth constant for group 2. To calculate the contribution of differences in coefficients, the effects estimated in the OLS regression models for group 1 are applied to group 2 while keeping the distribution of characteristics for group 2 constant 2 . For more details, see Jann (2008).

Results

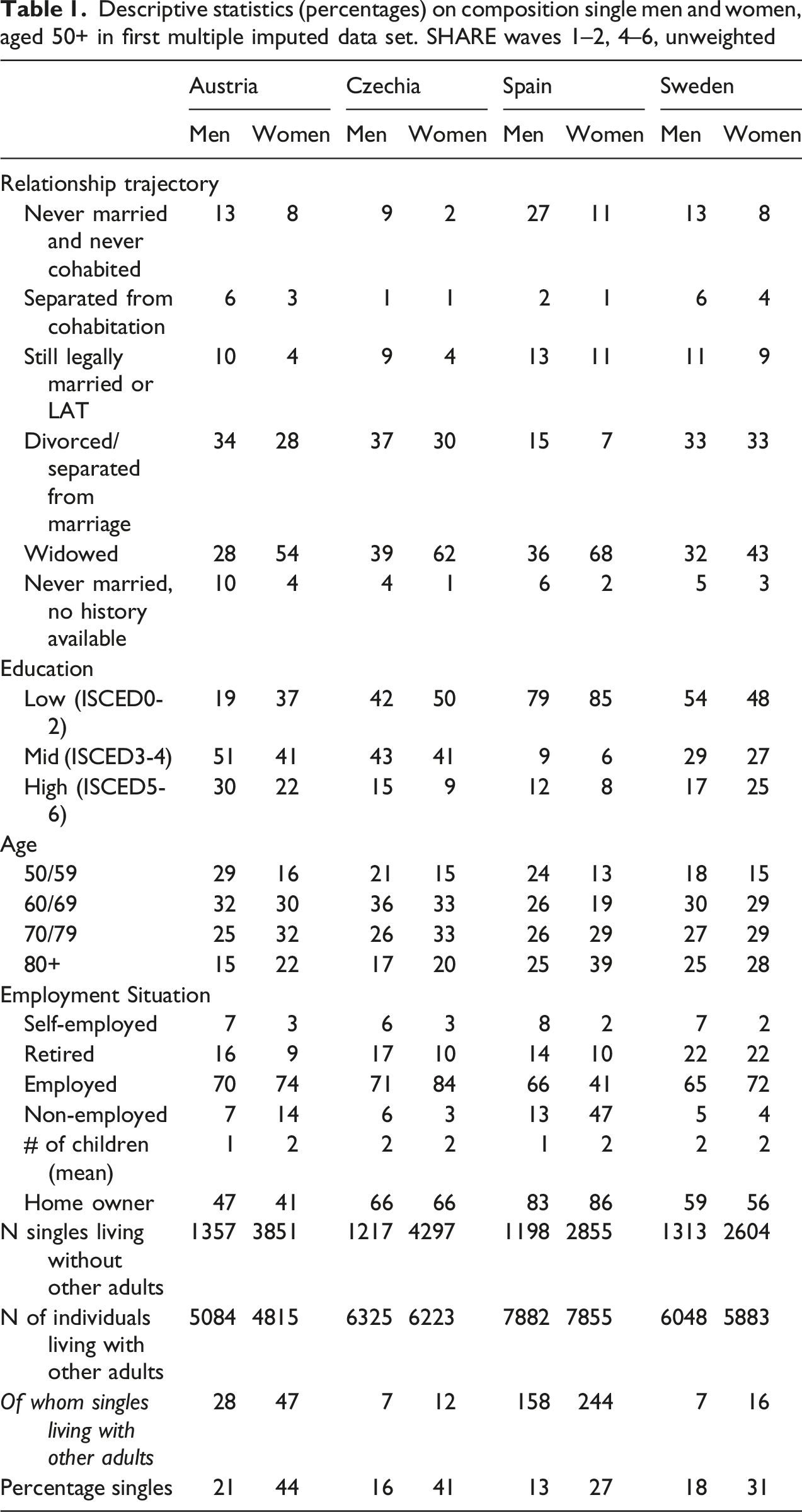

Descriptive statistics (percentages) on composition single men and women, aged 50+ in first multiple imputed data set. SHARE waves 1–2, 4–6, unweighted

The last rows of the table show what parts of the sample are single by gender and country, as well as the ratio of single women to single men. In Austria, 44% of female respondents in SHARE are single, against only 21% of men. The Czech Republic has a similarly high share of single women. Note that only a few single individuals live in households with other adults in Austria, Czech Republic, and Sweden. In Spain, 12% of single men and 8% of single women live with other adults in the household. Because the wealth of these other adults contributes to household wealth, singles co-residing with other adults are not part of the remainder of the analysis. For descriptive differences between single and non-single men and women per country, see Tables A2a–A2d in the appendix.

The descriptive statistics of Table 1 confirm that Spain stands out in terms of a low prevalence of divorce and separation and, therefore, a high relative share of never partnered men and widowed women among singles. In all countries, single men are more likely to be never married, divorced, or separated than single women, who are more likely to be widowed. One exception is the prevalence of divorce in Sweden, which is similar between men and women. Home ownership rates are low in Austria, followed by Czech Republic, Sweden and highest in Spain.

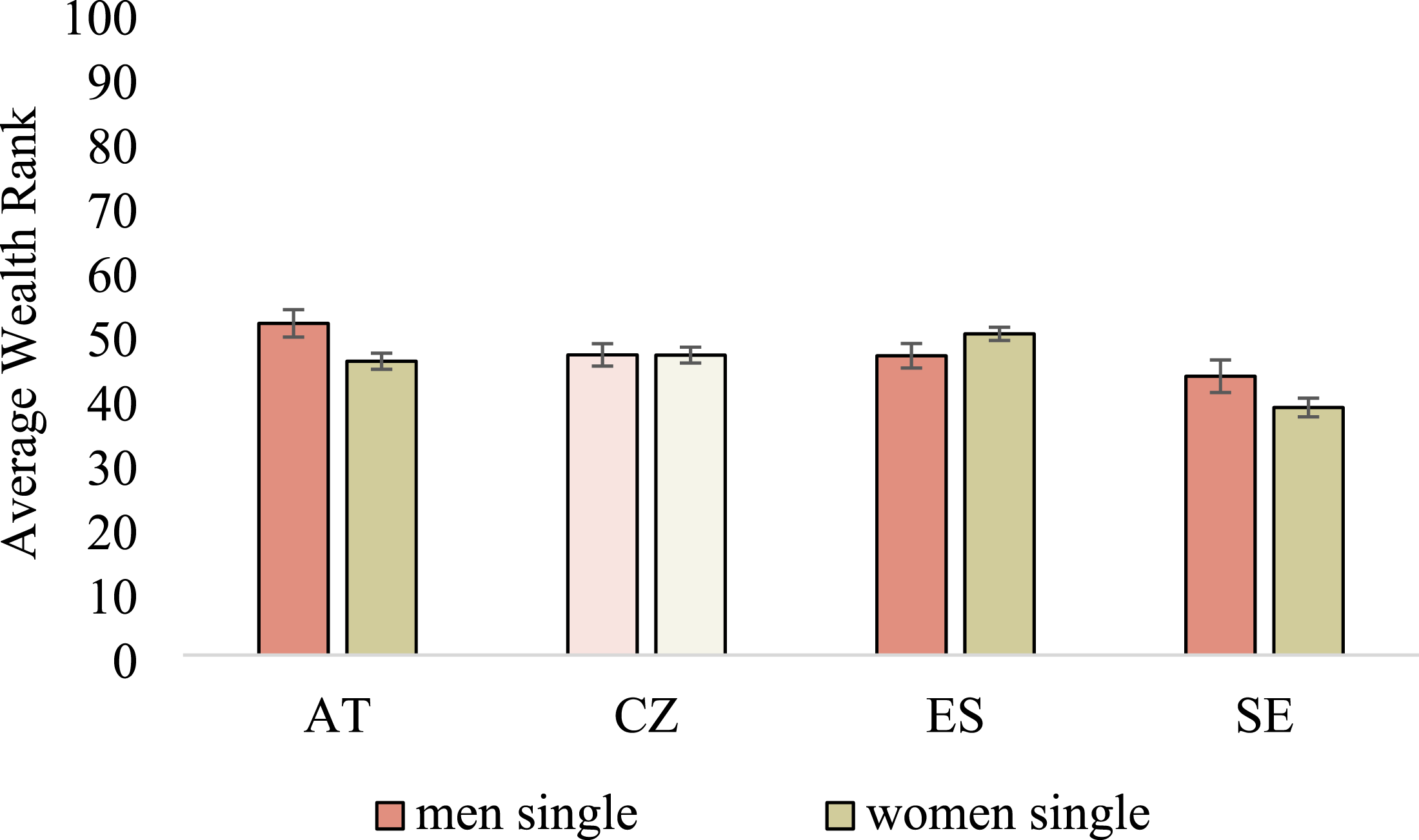

The Raw Gender Gap in Household Wealth

We start our analysis by showing the raw gender gap in rank wealth for each of the four countries in Figure 1. We find clear gender gaps favoring men in Austria and Sweden, whereas we find a small and statistically insignificant gap in Czech Republic, and even a gender gap favoring single women in Spain. Wealth rank by gender and sample (singles only). SHARE waves 1–2; 4–6, controlled for wave, weighted. Lighter colored bars indicate insignificant gender difference. Whiskers indicate 95% confidence intervals

Before trying to explain the gender gap among singles, we checked whether the same gender gaps are observed in other representative datasets. For three countries, Austria, Spain, and Sweden, we used the data as harmonized by the Luxembourg Wealth Studies (LWS) for comparison purposes for the years that were available (see Table A1 in appendix). In general, a similar picture emerges with the strongest gender gap in wealth among singles in Austria, a consistent but modest gender gap favoring men in Sweden, and a gender gap favoring women in Spain. The gender gap at the median appears to be smaller in the LWS as compared to SHARE for Austria, so ours might be an overestimation.

Gender Differences in the Effects of Partnership Histories

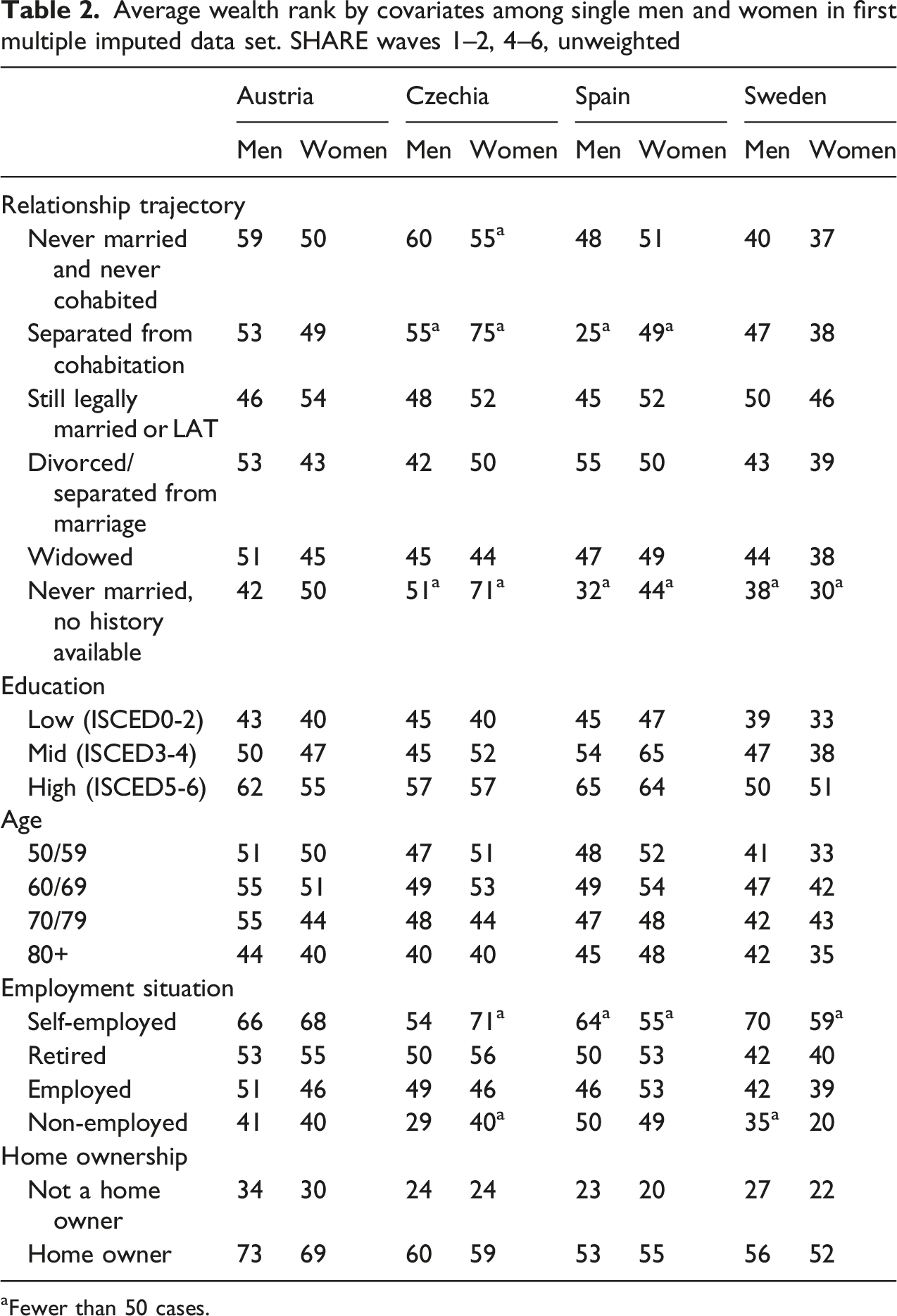

Average wealth rank by covariates among single men and women in first multiple imputed data set. SHARE waves 1–2, 4–6, unweighted

aFewer than 50 cases.

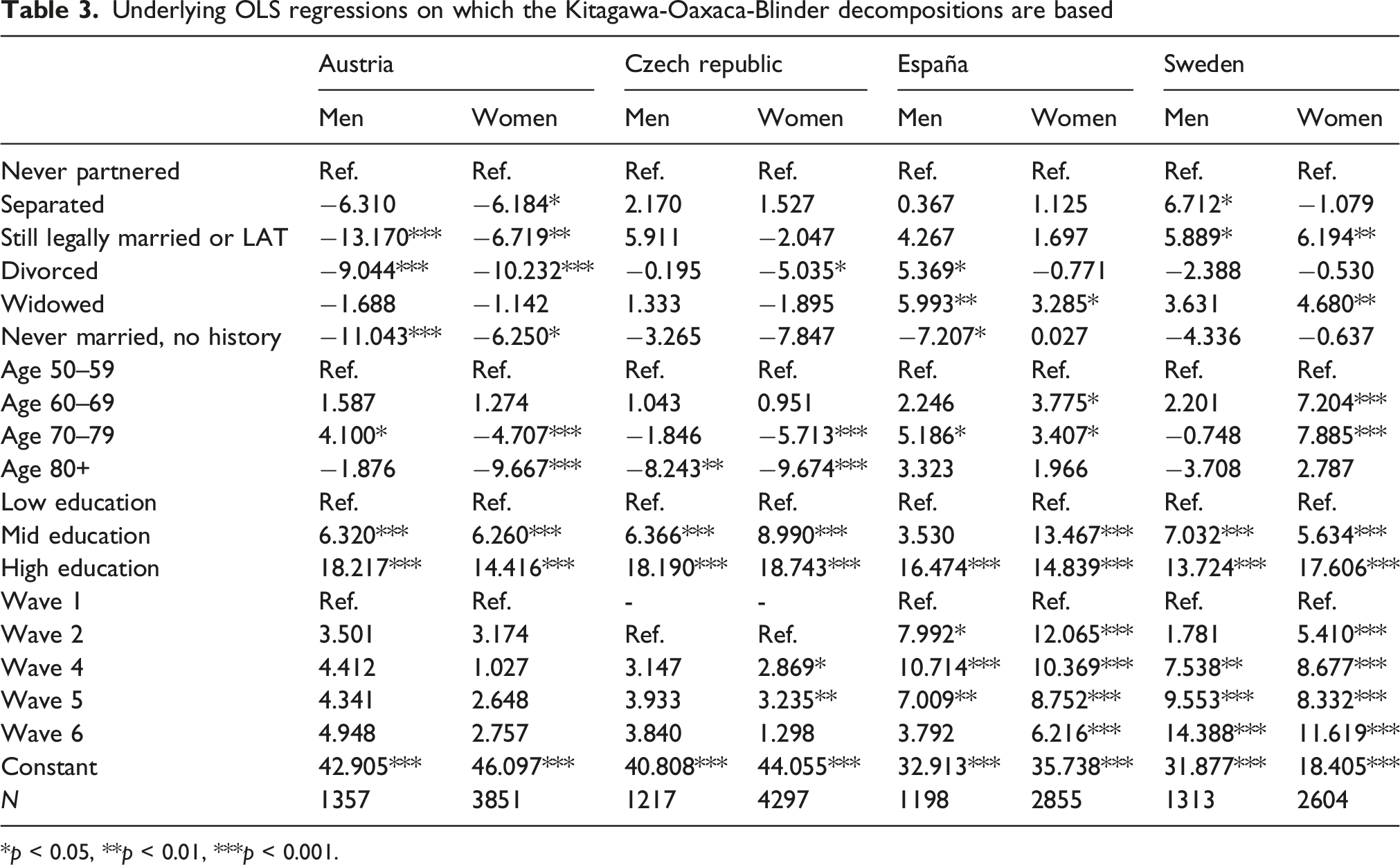

Underlying OLS regressions on which the Kitagawa-Oaxaca-Blinder decompositions are based

*p < 0.05, **p < 0.01, ***p < 0.001.

We expected never partnered women to have relatively high wealth in more traditional contexts because resourceful women might select into singlehood when there are major obstacles toward combining work and family life. This might explain why we observe high levels of wealth for never partnered women in Austria, and the Czech Republic, but low levels of wealth in Sweden. In addition, contrary to expectation, we observe similar cross-national differences for men, with relatively high levels of wealth for never partnered men in Austria and Czech Republic.

We expected widowed individuals to be relatively wealthy as they benefited the most of all unpartnered individuals from wealth accumulation within couples. A clear wealth advantage is indeed observed for widowed individuals in Spain and Sweden, and widowed individuals have relatively high wealth compared to separated or divorced individuals in Austria. In line with expectations, gender differences in the effects of widowhood are limited, with the possible exception of the Czech Republic. This might explain why gender gaps in household wealth are limited in Spain, a context where two-thirds of older single women are widowed and large in contexts with lower levels of widowhood, like Sweden.

Beforehand, we stated that separated and divorced individuals are likely to have relatively low wealth, something we clearly observe in Austria and among divorced women in the Czech Republic. In Sweden this holds once compared to widowed individuals. The most salient exception to this observation is Spain where divorced men have more wealth than never married individuals. This could indicate that selection into divorce plays a role there, and is in line with studies showing that the correlation between education and divorce is positive in contexts where divorce is less common (Härkönen & Dronkers, 2006). It is among the divorced where we observe the clearest gender differences in effects. The effect of divorce is considerably more negative among women in Czech Republic and Spain than among men in those countries. This result is also observed in Austria and Sweden, but to a smaller extent. In Sweden, this relatively small gender difference in effects might have to do with the default marital property regime prescribing the division of all of couples’ assets after divorce in Sweden, whereas only part of couples’ assets is covered by default regimes in the other countries. In addition, Sweden’s generous welfare state and high labor market participation impact positively on the economic well-being of separated women.

Decomposition of the Gender Wealth Gap Among Single Individuals

Using a Kitagawa-Oaxaca-Blinder decomposition analysis, we will now formally test to what extent gender differences in composition and effects can explain the gender wealth gap among singles in each country. In additional analyses, we also included employment status, income, and number of children. As we consider these variables to be mediators between relationship trajectories and wealth, we only present them in the online appendix (Table A6a and A6b); any changes in results in these additional models are discussed in the text.

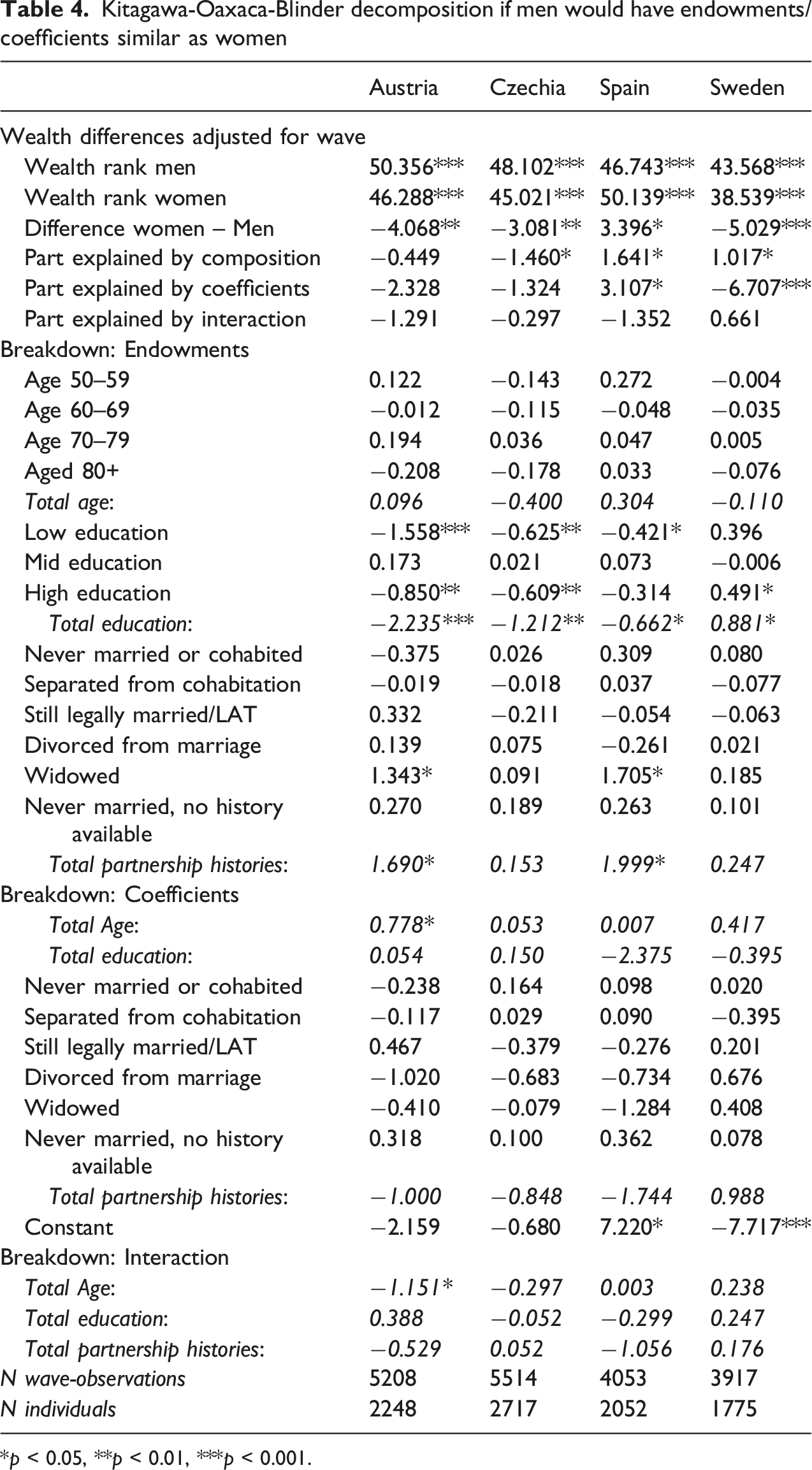

Kitagawa-Oaxaca-Blinder decomposition if men would have endowments/coefficients similar as women

*p < 0.05, **p < 0.01, ***p < 0.001.

The subsequent parts of the table consist of (1) endowments, the part of the gender gap that can be attributed to gender differences in compositions of characteristics; (2) coefficients, the part of the gender gap that can be attributed to gender differences in the effects of these characteristics; and (3) interactions, an additional part that gets explained by endowments and coefficients jointly, in other words, any additional changes in wealth rank if both endowments and coefficients would be as observed for the other group. This component does not have a straightforward interpretation as it cannot be readily attributed to either endowments or coefficients, and is therefore not discussed further.

Note that we estimated the decomposition table from the perspective of men: if men would have the characteristics of women, how high would their rank wealth be? In the appendix in Table A3, we provide the same estimation from the perspective of women. This opposite perspective does not change our decomposition conclusions, although the estimations of the composition and coefficient effects are slightly different.

Gender Differences Explained by Compositional Effects

In Austria, Czech Republic, and Spain, compositional differences explain 11%, 47%, and 48% of the gender gap in rank wealth, respectively. In Sweden, gender equality in compositional characteristic would have enlarged the gender gap instead of reducing it. These overall contributions of compositional differences are a combination of partnership histories, age, and education.

Once looking only at the contribution of partnership histories, we see that men would have less wealth if their partnership histories were as observed for women (i.e., all overall coefficients are negative). These effects are significant only in Austria and Spain (nearing 2 points in the wealth rank distribution), and primarily produced by the higher likelihood of being widowed among women. In Spain, the higher prevalence of widowhood among women is an important reason why single older women have more wealth than single older men, and accounts for roughly half of the gender gap in wealth favoring women.

Other variables also play explain the gender gap: If single men had the levels of education as single women, men would have less wealth in Austria, Spain and Czech Republic. Because women in Sweden were already higher educated than men in the cohorts studied here, we see the opposite result there.

Gender Differences Explained by Coefficient Effects

The coefficients part of the table quantifies how much the wealth rank of men would change if the effects on wealth of characteristics would be as observed for women. The overall contribution of coefficients also includes a constant which makes it hard to interpret directly, we therefore focus on considering the specific groups of variables directly. Overall, we do not see statistically significant contributions of differences in effects (except for age for Austria). There is a general tendency of the higher effects of divorce on women’s wealth explaining part of the gender gap favoring men (in Austria, Czech Republic, and Spain), but these are not significant.

In Spain, we observe a relatively large but insignificant contribution of differential effects of widowhood. Men would have 1.3 points less of wealth if widowhood had the same effects for them as observed for women. However, because we observed a gender gap favoring women overall, this is a factor that does not help explaining the gender gap in Spain.

Overall, these results suggest that relationship trajectories can explain parts of the gender gap in terms of composition, but we do not find statistically significant contributions of gender differences in effects of relationship trajectories on wealth.

Robustness Checks

We did various robustness checks: First of all, we checked what the results would be if we would have used the partner history information maximally (by imputing missing histories with current marital status). In appendix Tables A4 and A5a and b we show that the patterns of our main analyses roughly hold.

Second, we consider number of children, employment status, and income of the respondent as additional covariates in the decomposition models (Tables A6a and b). Men would have less wealth if their income and employment were as observed for women, and in Spain there is also such an effect observed for number of children. The effects of partnership histories persist, even though these characteristics explain part of the compositional effect of widowhood in Spain. Including pension income does not explain much of the gender gap in the four countries (Tables A7a and A7b).

Additional Analyses: Wealth Composition

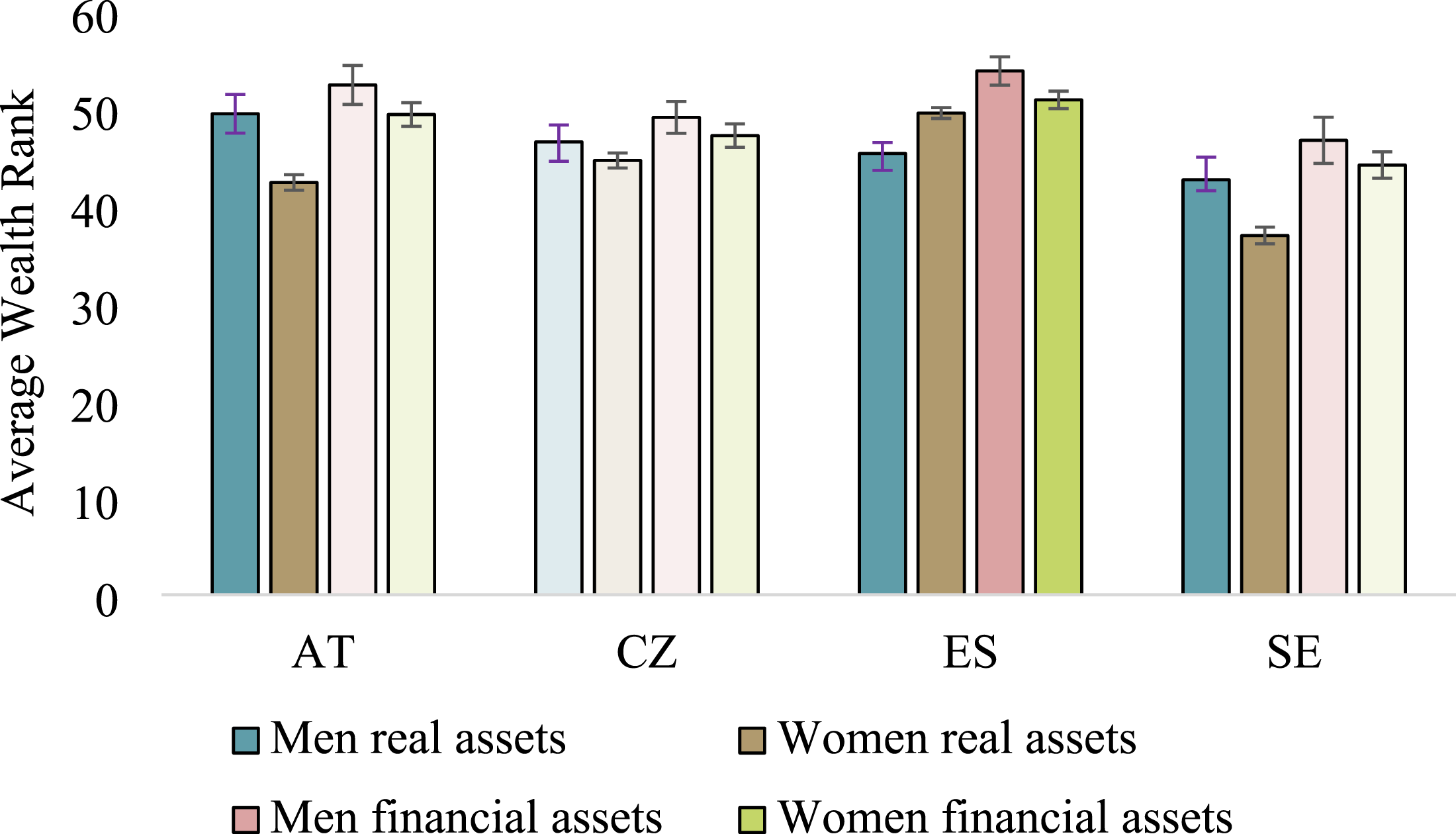

So far, we have focused on all wealth, but previous research has highlighted that a more equal distribution of housing wealth is related to lower wealth inequality in general and some studies suggested that lower gender gaps in wealth exist when home ownership rates are high (Kukk et al., 2022; Pfeffer & Waitkus, 2021; Ravazzini & Chesters, 2018). To examine this issue, Figure 2 shows gender differences in financial and housing wealth. We observe that the gender gap in housing wealth is similar to what we observe for wealth overall: a gender gap favoring men in Austria and Sweden, but a gender gap favoring women in Spain. For financial wealth we see that men always have more than women (even though differences are not significant in all countries). Raw gender gap in rank real assets and financial assets, singles, men and women. SHARE waves 1–2; 4–6, controlled for wave, weighted. Transparent bars indicate insignificant gender difference. Whiskers indicate 95% confidence intervals

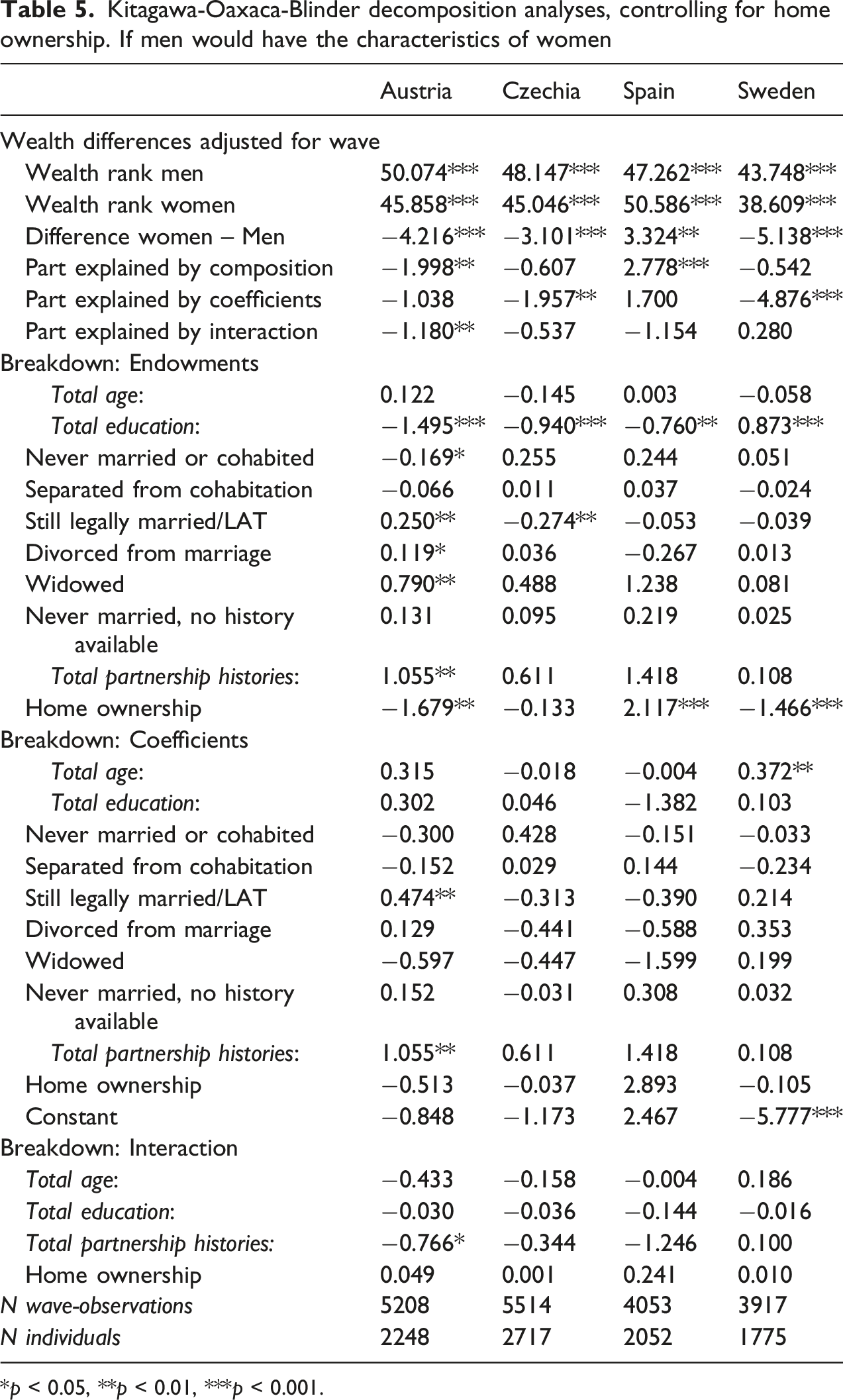

To what extent could gender differences in home ownership rates explain the gender gap in wealth? Table 1 showed home ownership rates by gender and country, and indeed both rates of home ownership and gender differences in home ownership align with gender differences in wealth: older single men are more likely to own a home than older single women in Austria and Sweden, countries with low home ownership rates. In contrast, women are more likely to own a home in Czech Republic and especially Spain, the country with a very high home ownership rate in comparison to the other three.

Kitagawa-Oaxaca-Blinder decomposition analyses, controlling for home ownership. If men would have the characteristics of women

*p < 0.05, **p < 0.01, ***p < 0.001.

Conclusion

As said by Ruel and Hauser (2013) there is no tidy gender wealth gap story. We slightly contributed to this state of affairs by finding variation in the gender gap across countries among older single individuals. We aimed to answer three research questions in this paper: (1) Is there a gender gap in household wealth between single men and women above age 50? (2) Does this gender gap vary across countries? (3) Can differences in the prevalence and returns from partnership histories explain the gender gap in wealth among persons aged 50 or more?

With respect to the first two questions we found, using SHARE data, that single men live in wealthier households than single women after age 50 in Austria, Czech Republic, and Sweden, but that single women live in wealthier households in Spain.

Our third question related to understanding the role of partnership history, as selection into singlehood is an essential factor to understand when starting to interpret gender gaps in household wealth among single people. In measuring partnership history, we used information from the SHARELIFE waves 3 and 7, in case individuals were never married. We also performed sensitivity checks using the full partnership history information from the SHARELIFE waves, but these did not alter our conclusions.

We found that divorced and separated individuals, and in particular women, generally had relatively low levels of wealth. We found that widowed individuals had relatively high levels of wealth across countries. In Spain, this could explain to an important extent why single older women have more wealth than single older men. The role of this mechanism was particularly pronounced there as the majority of older single women was widowed in Spain, a context where separation and divorce were still relatively uncommon for the cohorts studied here (born before the mid-1960s).

Some results aligned with the expectations formulated beforehand about why gender gaps could vary across countries. For instance, Sweden was one of the two countries with a clear gender gap in wealth favoring single men. We expected the gender gap to be small there if women’s labor market position were of determining importance. However, we expected a large gender gap in Sweden if many disadvantaged women select into singlehood, either because they never partner or because they are more likely to separate and divorce. Previous research has shown how resourceful women tend to select into singlehood in more traditional contexts, but that they are more likely to partner in more egalitarian contexts (Van Bavel et al., 2018). Similarly, in contexts with high levels of separation and divorce, the correlation between resources and divorce generally becomes negative as legal, economic, and social barriers to divorce decline with its increasing acceptance (Härkönen & Dronkers, 2006). We indeed found relatively low levels of wealth among the never partnered in Sweden (and not clearly so in the other contexts), which could explain why we did not find that partnership histories significantly affected the gender gap in wealth there (as we did observe in Spain and Austria). In addition, many older singles in Sweden are separated or divorced, and separated or divorced women have similarly low levels of wealth as never partnered women in Sweden. We found a contribution of gender differences in the effects of separation and divorce to the gender gap in wealth, but this was not statistically significant.

Even though several results aligned with expectations based on selection into singlehood, this was not the case for several other results. Never partnered individuals in Austria have relatively high wealth, but we observed a gender gap in wealth favoring men that is similar to Sweden. Even though the high levels of separation and divorce could explain part of these results, a closer look at the decomposition results of Table 4 suggests that educational differences between men and women form a clearer explanation for the gender gap in wealth in Austria. This is also the case in Czech Republic. In other words, the results seem to reflect more clearly women’s socioeconomic disadvantages in those two contexts.

Finally, the gender wealth gap in favor of women in Spain was explained by about half due to the gender differences in the likelihood of being widowed. This, in combination with the apparently strong selection into singlehood of wealthy individuals and the high homeownership rates, provides an explanation for the seemingly better situation of Spanish single women compared to men. Future research using individual level wealth data should corroborate to what extent this finding can be generalized to the entire population of 50+ individuals in Spain, taking into account within-household wealth differences.

One interpretation of our findings is that gender differences in wealth switch from existing primarily within households in traditional contexts (as observed in Spain) to gender differences in wealth between households in contexts with high rates of individualization (as observed in Sweden). Within traditional contexts, this would make within-household differences in (access to) wealth extra important. Within more individualized contexts, however, an important question becomes to what extent the state is able to minimize the impact of gender inequality in the labor market and society in general on gender differences in wealth during older ages.

There are also limitations that we could not deal with in our paper due to the lack of data on pension wealth. We have taken into account the potential impact of pension income on the gender gap in wealth. Comparing pension systems and making estimations of individuals’ pension wealth still remains a challenge, however, considering the large distribution of pension rights in the population depending upon contribution periods and differences in reference wages, leading to a difficult estimation of individual pension wealth at a certain age during life.

In conclusion, there are important gender differences in wealth between men and women at older ages. We found significant differences in wealth between single men and women in Austria, Sweden, and, in some specifications, in the Czech Republic. This stands in contrast with previous research on the working age population or population overall, which mostly finds insignificant differences among singles at the median or mean (Austen et al., 2014; Schneebaum et al., 2018; but see Anglade et al., 2017; Schmidt & Sevak, 2006). Hence, gender differences in wealth might become more visible with age as fewer individuals live in couples. However, it appears to depend on the context whether gender gaps in wealth among older singles reflect women’s disadvantages or differential selection into singlehood.

This conclusion underlines that an understanding of selection into singlehood is an important first step before interpreting gender gaps in wealth. As younger cohorts become older who are more likely to do so being single (because separation and divorce are more common), and for whom wealth is likely to become increasingly important (because of the increasing wealth-to-income ratios and pressures on public pensions), gender differences in wealth among older people are likely to become increasingly visible and relevant.

Supplemental Material

Supplemental Material - Partnership Histories and the Gender Gap in Wealth Among Older Singles: A Study Across Four European Countries

Supplemental Material for Partnership Histories and the Gender Gap in Wealth Among Older Singles: A Study Across Four European Countries by Maike van Damme, Diederik Boertien in Journal of Family Issues.

Footnotes

Ethical Considerations

The SHARE study is subject to continuous ethics review. During Waves 1 to 4, SHARE was reviewed and approved by the Ethics Committee of the University of Mannheim. Wave 4 and the continuation of the project were reviewed and approved by the Ethics Council of the Max Planck Society. In addition, the country implementations of SHARE were reviewed and approved by the respective ethics committees or institutional review boards whenever this was required. The numerous reviews covered all aspects of the SHARE study, including sub-projects and confirmed the project to be compliant with the relevant legal norms and that the project and its procedures agree with international ethical standards.

Consent to Participate

Not applicable, as this is a secondary data source.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the “La Caixa” Social Research Call 2019 [LCF/PR/SR19/52540010]; the Spanish Ministry of Science, Innovation and Universities [RYC2019-026510-I; PID2021-124267OB-I00], and the European Research Council [ERC-2020-STG-948557-MINEQ]. This paper uses data from SHARE Waves 1, 2, 3, 4, 5, 6, 7, 8 and 9 (DOIs: 10.6103/SHARE.w1.800, 10.6103/SHARE.w2.800, 10.6103/SHARE.w3.800, 10.6103/SHARE.w4.800, 10.6103/SHARE.w5.800, 10.6103/SHARE.w6.800, 10.6103/SHARE.w7.800, 10.6103/SHARE.w8.800, 10.6103/SHARE.w8ca.800, 10.6103/SHARE.w9ca800). The SHARE data collection has been funded by the European Commission, DG RTD through FP5 (QLK6-CT-2001-00360), FP6 (SHARE-I3: RII-CT-2006-062193, COMPARE: CIT5-CT-2005-028857, SHARELIFE: CIT4-CT-2006-028812), FP7 (SHARE-PREP: GA N°211909, SHARE-LEAP: GA N°227822, SHARE M4: GA N°261982, DASISH: GA N°283646) and Horizon 2020 (SHARE-DEV3: GA N°676536, SHARE-COHESION: GA N°870628, SERISS: GA N°654221, SSHOC: GA N°823782, SHARE-COVID19: GA N°101015924) and by DG Employment, Social Affairs & Inclusion through VS 2015/0195, VS 2016/0135, VS 2018/0285, VS 2019/0332, and VS 2020/0313. Additional funding from the German Ministry of Education and Research, the Max Planck Society for the Advancement of Science, the U.S. National Institute on Aging (U01_AG09740-13S2, P01_AG005842, P01_AG08291, P30_AG12815, R21_AG025169, Y1-AG-4553-01, IAG_BSR06-11, OGHA_04-064, HHSN271201300071C, RAG052527A) and from various national funding sources is gratefully acknowledged (see ![]() ).

).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The SHARE data are distributed by SHARE-ERIC to registered users via the SHARE Research Data Center, which is operated by Centerdata at Tilburg University in the Netherlands in cooperation with the Central SHARE Coordination Team at the SHARE BERLIN Institute (SBI) in Germany on behalf of SHARE-ERIC.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.