Abstract

We study the effect of supply and demand-induced oil price uncertainty on the cost of debt for a sample of US loans credited during the 1990 to 2019 period. We estimate oil price uncertainty following Jurado et al.’s study, whereby oil price uncertainty is captured by forecasting the unpredictable fluctuations of oil prices. Interestingly, our findings reveal that oil price uncertainty induced by supply shocks increases cost of credit, while oil price uncertainty driven by demand shocks decreases the cost of bank loans. In further analysis, the positive association between supply induced oil price uncertainty and interest loan spread is more pronounced for major users of oil, while the negative effect of demand driven oil price uncertainty on the cost of bank loans is stronger for firms that belong to industries that produce oil. Overall, our findings feed into the emerging discussion of the differentiating effects of oil price uncertainty on micro-level outcomes and provide useful implications for both bankers and borrowing firms.

1. Introduction

What is the impact of oil price uncertainty induced by demand shocks vis-vis supply shocks on the way banks set interest rate loan spreads? More recently, there is an emerging literature that looks at the relationship between oil price uncertainty and firm-level outcomes focusing on heterogeneous effects of oil price fluctuations depending on the type of shock, that is, demand or supply shock (Amin et al. 2023; Hasan et al. 2022; Kang et al. 2017). This literature embarks on the well-established view regarding the different relationship between oil demand shocks compared to oil supply shocks with the macroeconomy. Oil price fluctuations driven by demand shocks are associated with higher oil production, volume of industrial activities, and better economic conditions (Baumeister et al. 2022; Kilian 2009; Ready 2018; Uddin et al. 2018; Zheng et al. 2021). On the other hand, oil price changes caused by supply shocks are related to decreases in disposable income and consumer spending (Edelstein and Kilian 2009), resulting in lower real output (Baumeister and Peersman 2013; Kilian 2008). Despite the well documented view on the differentiating effects of supply and demand oil fluctuations, there is no study to this date to examine these effects on the interest loan spread charged by banks to corporations. Hence, in this study we aim to fill this gap in the literature by focusing on disentangling the supply-driven and demand-driven oil price uncertainty on the cost of bank loans.

In the banking literature, most of the existing studies examine types of uncertainty other than oil price uncertainty, such as political uncertainty, tax uncertainty, economic policy uncertainty, and macroeconomic uncertainty (Francis et al. 2014; Fuller et al. 2024; Huang et al. 2021; Juelsrud and Larsen 2023; Raunig et al. 2017). All in all, these previous studies point to the negative effects of ‘uncertainty’ for borrowers, which is translated into reduced lending and higher interest loan spread. Hence, in this study our aim is twofold. The first is to shed some light on the potential effect of oil price uncertainty on the cost of bank debt, expanding our understanding on an additional ‘uncertainty’ factor that could affect the cost of banks. The second is to uncover whether oil price uncertainty could have a heterogeneous effect on the interest loan spread depending on the cause of uncertainty, that is, supply shocks vis-à-vis demand shock. To this end, we develop two main hypotheses. If oil price uncertainty is induced by a shock in supply which causes oil shortages, this in turn would increase oil prices resulting in rising costs from the production side. This coupled with the inability of firms to transfer costs to customers due to the lack of alternatives could lead to a deterioration in performance due to lower revenues. Moreover, according to the theory of ‘real option value of waiting’ to invest under uncertainty (Bernanke 1983; Bloom 2009), oil price uncertainty increases due to oil shortages may refrain firms from undertaking future investments as a way of minimizing losses. The response of investment in oil price uncertainty is not symmetrical and could depend on the type of shock (Maghyereh and Abdoh 2020). A supply shock in oil is associated with an increase in the marginal production costs and reduction of expected cash flows and NPV of a future investment. To the extent that NPV decreases due to high expected costs, the gap between the value option to wait and the reward from the new investment is larger, suggesting postponement of the investment. Several studies highlight the positive effect of investment on the performance of firms (Chan et al. 2001; Eberhart et al. 2004; Yen 2013). Hence, taking all the above together, we could conjecture that if banks lend to a firm in periods of high oil price uncertainty induced by supply shocks, we expect that they would be more concerned in terms of firms’ loan repayment charging higher costs on the debt as compensation for the risk they carry (

On the other hand, oil price uncertainty driven by demand shocks is associated with higher economic activity and output (Ready 2018; Uddin et al. 2018; Zheng et al. 2021) in accordance with the ‘option to grow’ channel (Bloom 2014). Under these conditions, firms would have higher expectations on their future investment opportunities, prompting them to take advantage of them and increase their investment (Wong and Hasan 2021). Recent empirical work indicates that oil shocks triggered by demand fluctuations result in increased stock returns and cash flows, higher executive compensation, and enhanced corporate transparency (Hasan et al. 2022; Kang et al. 2017; Wong and Hasan 2021). Hence, the above arguments point to the notion that oil price uncertainty caused by demand shocks could improve the financial performance of corporations, thereby improving their lending terms imposed by banks. Therefore, our second hypothesis suggests a negative association between oil price uncertainty and the cost of bank loans if uncertainty of oil prices is driven by demand shocks (

We focus on bank loans of the US syndicated loan market as it represents the most important source of external funding for US corporations (Bharath et al. 2008). Bank financing could spur firms’ investment and could have a pivotal role in their long-term performance. Therefore, from a firms’ perspective it is helpful to examine the impact of oil price uncertainty on the cost of bank loans. Also, we choose to focus on the US as it represents one of the world’s leading consumers and producers of crude oil and hence sudden changes in the global price of oil could affect significantly the economy. 1 Several previous papers find the negative effects of sudden changes in oil prices for the US (Baumeister and Kilian 2016; Hamilton 1983, 2003; Kilian and Vigfusson 2017; among others). Also, Hamilton (2003) and Kilian and Vigfusson (2017) show that unexpected increases in the price of oil depress the US investment. Moreover, the recent oil macroeconomics literature shows the contractionary effect of oil price uncertainty shocks on the US economic activity (Elder and Serletis 2010; Serletis and Xu 2019; Triantafyllou et al. 2024). Therefore, rising uncertainty about oil prices could increase the vulnerability of the US economy. Lastly, our motivation to study the differentiating effects of oil price uncertainty lies in the real option theory of postponing and expanding investment, and recent empirical papers focusing on the positive impact of oil price uncertainty on firm outcomes. The research so far in the loan syndicate market points to the negative effects of ‘uncertainty’ for borrowing firms, resulting in rising loan spreads for borrowing firms. Hence, by examining the effects of supply vis-à-vis demand induced oil price uncertainty on the cost of bank loans, we are eager to provide new empirical evidence and add to the discussion of the positive or/and negative effects of oil price uncertainty from a banking perspective.

We source data on loans from Dealscan, which provides comprehensive information for loans in the syndicate market, including the cost of loans, loan-level characteristics, and borrowing firms’ identity. Next, we use borrowers’ identity from Dealscan to match with financial and accounting data from Compustat Database. Following this matching process, we have a final sample of 18,465 loan facilities extended to 3,231 unique borrowing firms for the 1990 to 2019 period. For the measurement of oil price uncertainty, we follow a novel approach inspired by the approach of Jurado et al. (2015) and implemented by Triantafyllou et al. (2024) to forecast oil price uncertainty. The main advantage of this method is that we estimate oil price uncertainty as the purely unforecastable component of oil price fluctuations over the same forecast horizon. On the contrary, other methods of estimating oil price uncertainty, such as oil price volatility, rely on observable fluctuations of oil prices (i.e., the realized volatility of crude oil prices). In our estimation, we filter out any predictable fluctuations of oil prices, which, by definition, are not related to oil price uncertainty (for a more thorough discussion of the advantages of this approach for uncertainty please see Jurado et al. 2015), and we thus focus on the ‘real’ uncertainty caused by unpredictable changes of oil prices. Moreover, we follow a Bayesian Dynamic Model Averaging (DMA) approach introduced by Raftery et al. (2010) and Koop and Korobilis (2012), whereby we use a static factor-augmented VAR method to forecast the US macroeconomic fluctuations. This methodology allows for the forecasting model and the model parameters to vary across time, thereby increasing the weight to the most successful predictions for each quarterly period. In this way, we have a more refined and as accurate as possible estimate of the unforecastable component of oil price fluctuations compared with various types of oil price forecasting models.

Our baseline estimations show that oil price uncertainty induced by supply-side shocks increases the cost of bank loans, which confirms our

We perform several tests to ensure that our results are not driven by omitted variable issues. Firstly, we run additional estimates whereby we augment our specification by controlling for oil prices, oil inventories, global economic activity, and general macroeconomic conditions (Baumeister and Hamilton 2019; Kilian 2009, 2019). Secondly, we also run specifications whereby we account for geopolitical, macroeconomic, financial and world uncertainty (Ahir et al. 2022; Caldara and Iacoviello 2022; Jurado et al. 2015). Thirdly, we also employ additional fixed effects, including industry, state-level fixed effects and time fixed effects. To further deal with issues related to trend effects of macroeconomic factors we perform estimations whereby we include time trend. To remedy any bias stemming from multicollinearity issues between the two variables of oil price uncertainty constructed by demand and supply induced shocks, we proceed by estimating mutually orthogonal oil demand, supply and risk structural shocks using a three-factor SVAR model in line with the methodologies developed by Ready (2018) and Clements et al. (2019). In this way, we estimate mutually orthogonal (uncorrelated) series that capture demand-driven and supply-driven oil price uncertainty. To ensure that our estimates are not correlated with financial uncertainty, we also include in our decomposition estimates the volatility implied index (VIX) indicator. In this way, we rule out the possibility that financial uncertainty could be a confounding factor in the relationship between oil price uncertainty proxies and the cost of bank credit. Lastly, we employ alternative measures of demand-induced and supply-induced oil price uncertainty. Results from all our robustness analysis continue to confirm our two main hypotheses.

Our study contributes in several ways to existing literature. Firstly, we examine the effect of oil price uncertainty on the cost of bank loans, and therefore we contribute to the broader literature that observes sources of uncertainty as determinants of the cost of credit (Francis et al. 2014; Huang et al. 2021; Juelsrud and Larsen 2023; Raunig et al. 2017). Notably, most of this literature highlights that uncertainty increases the cost of bank loans, while in our study we are the first to document the beneficial effect of demand-induced oil price uncertainty on the banking sector and particularly for firms that belong to demand sensitive industries.

Secondly, we contribute to the growing literature that observes the differentiating effects of oil price shocks (demand and supply) on firm-level characteristics (Hasan et al. 2022; Kang et al. 2017; Wong and Hasan 2021). Our focus is on the cost of bank loans for corporations in the US, which constitute the major source of financing for US corporations.

Thirdly, by finding evidence on the negative effect of oil price uncertainty on the cost of bank loans, we contribute to the scarce literature that provides evidence of the beneficial effects of oil price uncertainty for corporations (Amin et al. 2023). We, thus, add to the discussion and provide robust evidence that demand-driven oil price uncertainty could be an opportunity for firms to increase their investment and revenues, which is recognized by banks, and which would prone lenders to charge lower interest rates.

Fourthly, we contribute to the literature that measures oil price uncertainty by constructing a more refined measure of oil price uncertainty estimated as the unpredictable variation of oil price changes. Thus far, the oil-macroeconomics literature has widely used observable measures of oil price uncertainty such as the oil price volatility (Ferderer 1996), conditional GARCH-type volatility models (Elder and Serletis 2010) and stochastic volatility models for the oil market (Jo 2014). The above-mentioned models rely on observable fluctuations in the oil market. However, Triantafyllou et al. (2024) show that the oil price uncertainty measure as estimated in our study has a more pronounced effect on the US investment and production compared to these alternative (observable) proxies of oil price uncertainty. Hence, with our study, we contribute to empirical identification research whereby we use a novel measure of oil price uncertainty as the main independent variable.

The rest of the paper is organized as follows. Section 2 develops the hypotheses. Section 3 describes the data and methodology. Section 4 provides empirical results. Section 5 concludes the findings and discusses implications.

2. Hypotheses Development

In this section, we develop two independent hypotheses which emerge from the well-established view in the literature that the effect of oil price fluctuations could be different depending on the cause of the uncertainty, that is, supply shock as opposed to demand shock (Amin et al. 2023; Baumeister and Peersman 2013; Baumeister et al. 2022; Hasan et al. 2022; Kang et al. 2017; Kilian 2008, 2009; Ready 2018; Uddin et al. 2018; Zheng et al. 2021). We, therefore, treat supply driven and demand driven uncertainty as two independent factors that could have heterogeneous impact on the cost of credit.

2.1. Oil Price Uncertainty Supply Driven and Cost of Bank Loans

Oil price uncertainty could affect the cost of credit through the supply side, that is, the uncertainty of oil prices driven by shocks on the supply of oil. Previous studies provide important theoretical and empirical evidence that oil price uncertainty could influence the cost of bank loans through the supply side channel.

There is empirical evidence to suggest that oil price uncertainty affects negatively financial performance (Phan et al. 2020; Song and Yang 2022). There are two channels that could explain this association. Firstly, uncertainty caused by oil shortages could affect firms’ profitability through the cost side. Oil price uncertainty, which stems from increases of oil prices due to oil shortages may increase the firm’s production costs (Phan et al. 2019). This increase in costs applies to both consumers and non-consumers of crude oil, as most firms use products such as gas, heating oil, and others, which their prices move in line with oil price. Therefore, there could be an important rise in marginal costs due to oil price uncertainty driven by supply shocks. In addition to this, the increase in production costs combined with the incapacity in transferring on the costs to customers due to the lack of alternatives could lead to an important deterioration of revenues for firms. In support of the cost channel, ElFayoumi (2018) finds that oil shortages increase US firms’ costs and decrease their profits.

The second channel through which oil price uncertainty caused by oil shortages could affect firms’ performance is through the option value of delaying investments (Pindyck 1993). Sudden increases in oil prices due to oil shortages may refrain firms from undertaking future investments. The reason being that under increasing uncertainty the option value of waiting may be higher than the net present value (NPV) of a new investment opportunity (Bernanke 1983). There are several empirical studies to confirm the negative relationship between different types of uncertainty including economic policy uncertainty (Kang et al. 2014) political uncertainty (An et al. 2016; Jens 2017; Julio and Yook 2012), stock returns uncertainty (Bulan 2005), inflation uncertainty (Huizinga 1993), climate policy uncertainty (Huang and Sun 2024) and firm investment. In the crude oil literature, there are also studies to show that high oil price uncertainty results in lower investment (Phan et al. 2019; Wang et al. 2017). However, the reaction of investment to oil price uncertainty is not symmetrical and could depend on the type of oil change, that is, positive or negative. Maghyereh and Abdoh (2020) show that positive oil price changes have a more significant negative effect on investment compared to negative oil price changes. In the context of our study, if oil price uncertainty is caused by supply fluctuations this would lead to an increase in oil prices. Rising oil prices increases marginal production costs, which would lead to lower expected cash flow and NPV of future investments. Consequently, the gap between the value of the option to wait and the reward from new investments is larger, leading to the postponement of the investment. Amin et al. (2023) find that oil price uncertainty driven by supply shocks prompts firms to scale down their investments and innovation activities, while demand driven oil price uncertainty is not found to have a significant effect. However, reducing investment could decrease firm performance due to the loss of profitable opportunities. There are numerous studies which show that investment has a positive association with firm value and performance (Chan et al. 2001; Eberhart et al. 2004; Yen 2013) which could be seen as a positive signal by lenders. To the extent that firms withhold profitable investment opportunities and banks expect that underinvestment could have a negative effect on firms’ long-term performance, lenders would be less willing in imposing favoring lending terms. 2

Therefore, from the above discussion we conclude that oil price uncertainty driven by oil supply shocks could decrease firm performance through the cost and the option value of delaying investments channels. As a result, this deterioration of firms’ balance sheet would decrease their capacity to pay back their loan obligations which would prone banks to increase the cost of borrowing to compensate for the higher risk of non-loan repayment. Therefore, our first hypothesis could be formulated in what it follows:

2.2. Oil Price Uncertainty Demand Driven and Cost of Bank Loans

Oil price uncertainty could influence the cost of bank loans through the demand side, that is, the uncertainty caused by surprises on the demand for oil. Oil price uncertainty caused by demand fluctuations could have a positive effect on firms’ performance through the growth channel.

According to the real option of expanding investment or ‘growth’ option theory (Bloom 2014), uncertainty could boost investment in the long run. The positive effect of uncertainty could be explained by a positive shock of aggregate demand for all commodities including oil, signaling increased expectations about long run economic outcomes. There is empirical evidence to verify that oil demand shocks are associated with a positive long-lasting effect on economic growth and output (Alquist et al. 2020; He et al. 2010). In similar terms, rising oil price uncertainty due to increased oil demand could enhance firms’ expectations regarding future investment opportunities (Wong and Hasan 2021). This in turn would prompt firms to increase their investment, which may have a positive effect on firm’s performance. Numerous recent empirical studies find that oil price changes driven by demand shocks increase stock returns, cash holdings, corporate payouts, and corporate transparency (Hasan et al. 2022; Kang et al. 2017; Wong and Hasan 2021).

Hence, from the preceding discussion, we believe that when oil price uncertainty is driven by demand fluctuations firms’ performance and creditworthiness will improve. To the extent that firms improve their financial profile due to oil increased price uncertainty induced by demand fluctuations, we would expect that banks will carry lower loan-repayment risk which would then be translated into lower financing costs. Therefore, our second hypothesis could be stated in what follows:

3. Data and Methods

3.1. Loan Sample

We source our loan-level dataset from the Loan Pricing Corporation (LPC)/Dealscan database for all syndicated loans in the US between 1990 and 2019. This source offers a large and comprehensive coverage on syndicated loans including pricing and non-pricing characteristics. In loan syndication, it is very common that numerous loan facilities are granted to the same borrower firm in the same year. Despite that these loans may be part of the same credit agreement, they may have different loan characteristics, such as the size, maturity, and/or purpose of the loan. Therefore, we treat each loan facility as a unique loan observation as in previous studies (Bermpei et al. 2024; Hasan et al. 2014, 2017).

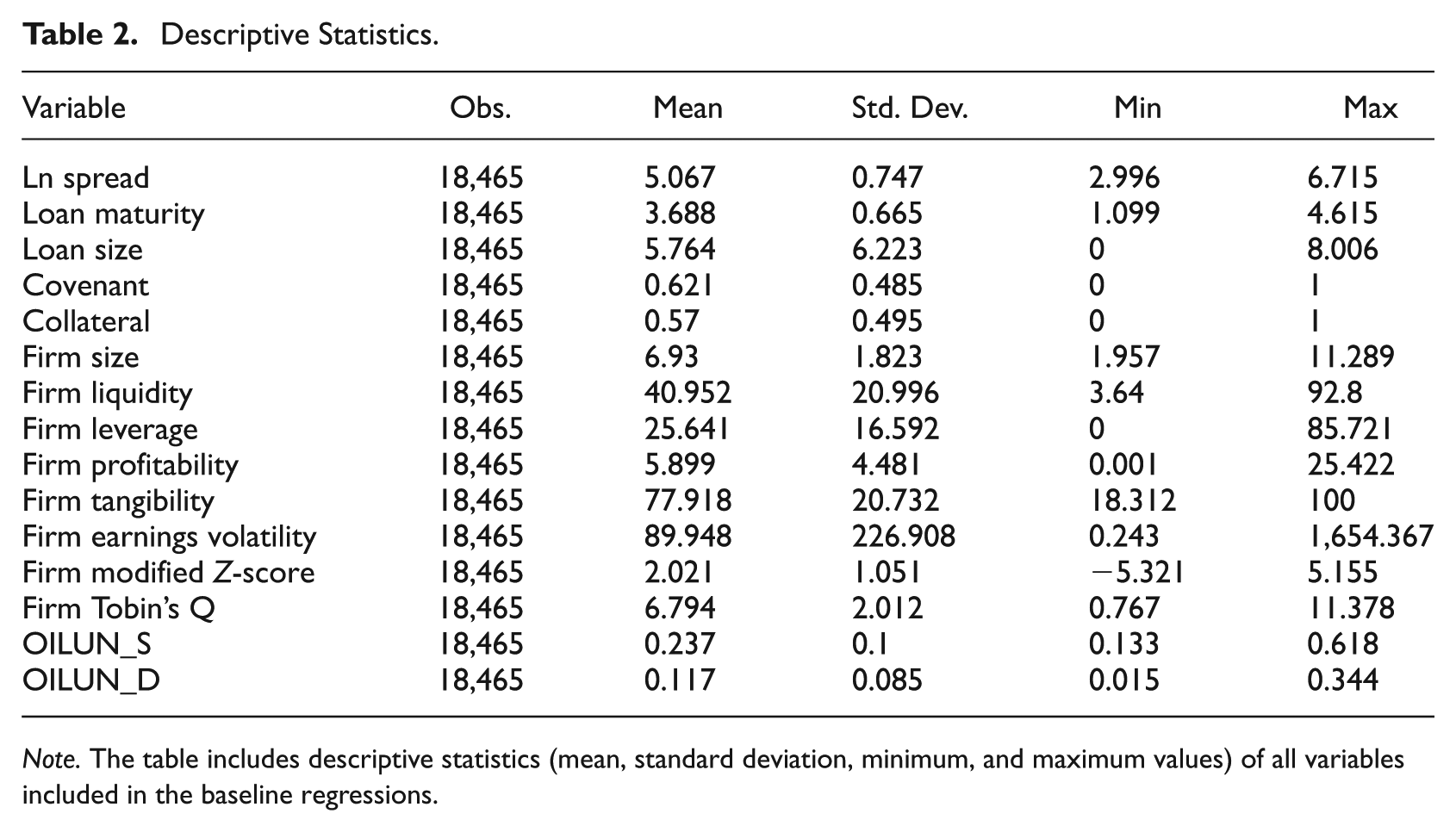

We also match the loan-level data with financial information of borrowers. For the matching process, we use the unique identifiers on the name of the borrowers provided in the Dealscan and link them with the financial data from Compustat database. We exclude from our sample financial and utility firms (with SIC codes 6000-6999 and 4900-4949), as they are subject to substantially different regulatory frameworks which put them under different borrowing conditions compared to other firms. The above process returns in 18,465 loan facilities granted to 3,231 borrowing firms for the 1990 to 2019 period. In Table 1, we provide measurement details of the loan-level and firm-level variables used in the main empirical analysis. In Table 2, we present descriptive statistics of all variables included in the baseline estimations. In our sample, on average the cost of the loan is 159.69 basis points, size of the loan is $318 million, and the maturity of the loan is 3.68 years. These summary statistics are in line with these of previous studies (Francis et al. 2012; Graham et al. 2008; Hasan et al. 2014).

Definitions and Measurements.

Note. The table includes all variables, definitions, and sources of the variables included in the baseline regressions.

Descriptive Statistics.

Note. The table includes descriptive statistics (mean, standard deviation, minimum, and maximum values) of all variables included in the baseline regressions.

3.2. Measuring Oil Price Uncertainty

Several previous macro-economic studies estimate oil price uncertainty using the conditional variance of the monthly returns of crude oil prices (Chang and Serletis 2018; Elder and Serletis 2010; among others), a stochastic volatility model on crude oil price returns (Jo 2014; Xu et al. 2022), or the realized volatility of crude oil returns (Ferderer 1996; among others). In this study, we employ an alternative method of estimating oil price uncertainty. This approach is based upon the pioneering work of Jurado et al. (2015) and recognizes that uncertainty may not be adequately captured by using oil price volatility or the degree of predictable oil price changes, and that it rather requires an estimate of the unpredictable component of oil price fluctuations which better reflects the ‘real’ uncertainty of oil prices.

Hence, our measure of oil price uncertainty OILUN(h) quantifies the unpredictable component of oil price changes:

where OILRET is the log difference of the WTI crude oil price series.

3

For equation (1) it is evident that h represents the forecast horizon of uncertainty, hence

In more detail, our oil price return forecast is derived by estimating the maximum possible combination of oil price forecasting models with our predetermined set of predictors (Baumeister and Kilian 2015; Koop and Korobilis 2012). The Bayesian Dynamic Model Averaging (DMA) approach constructs recursive real-time out-of-sample forecasts for the crude oil price changes by averaging in each period across K oil price return forecasting models, each containing a different combination of the set of predictors

In equation (2), K is the number of our predictors (in our case we utilize a maximum of thirteen well-established oil price predictors hence K = 13), and

Where INVENT is the quarterly log-difference of US crude oil inventories, BASIS is the price difference between near maturity and three-month maturity crude oil futures, PROD is the growth rate of global crude oil production, SPECUL is the log-difference of the speculation index defined as the percentage of non-commercial traders (speculators) in the crude oil futures market (see Büyükşahin and Robe 2014), VOL is the log-difference of the volume of three-month maturity crude oil futures contracts, GEOP is the geopolitical risk index of Caldara and Iacoviello (2022). SPREAD is the difference between the ten-year government bond yield and the three-month US-Treasury Bill (see Estrella and Hardouvelis 1991), GIPI is the growth rate of the global Industrial Production Index (Baumeister and Hamilton 2019), FFR is the first-difference in the US Fed Funds Rate, OILFUT is the growth rate of the three-month maturity crude oil futures prices, GACT is the real Global Economic Activity index (Kilian 2009, 2019), and INFL is the US inflation rate defined as the quarterly growth rate of the US Consumer Price Index (all items). The crude oil specific series and the macroeconomic series are downloaded from Refinitiv and FRED databases respectively.

After obtaining our oil price forecasts for h = 1 and h = 4 quarters forecast horizon, we use equation (1) to estimate the h-quarter ahead oil price uncertainty as the conditional volatility of the forecast errors (observed minus expected oil price changes) of the forecasting models. 4 Hence, by OILUN1 and OILUN4 we denote the one- and four-quarter horizon oil price uncertainty.

3.3. Demand and Supply Driven Oil Price Uncertainty

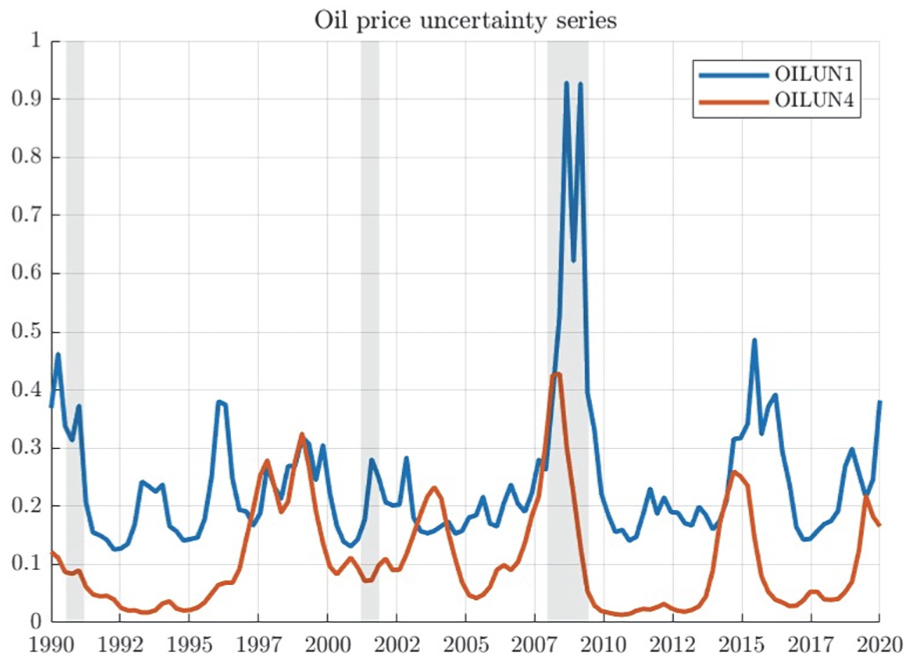

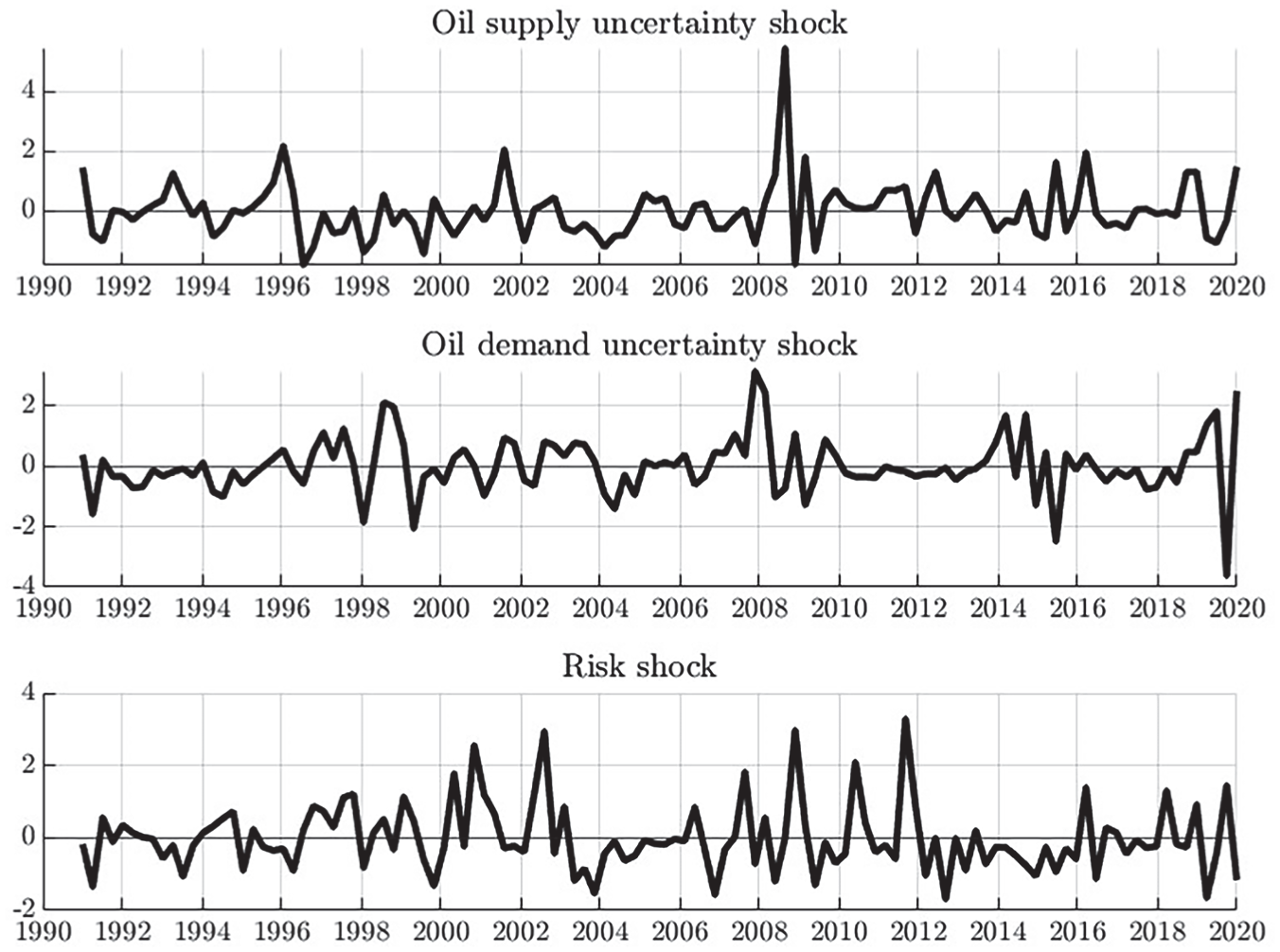

Using a quarterly dataset for the predictions of the above equation, we estimate oil price uncertainty one-quarter ahead (OILUN1), which is our proxy for supply-induced oil price uncertainty. (OILUN_S) and oil price uncertainty four-quarter ahead (OILUN4), which captures the demand-driven oil price uncertainty (OILUN_D). In what follows we provide theoretical and anecdotal evidence to explain the reasons behind using these two factors as our main proxies. Next, we also proceed with empirical estimations to further support theoretical predictions. Figure 1 illustrates the time series of our estimated OILUN1 and OILUN4 factors.

Time series of supply driven (short-run) and demand-driven (long-run) oil price uncertainty.

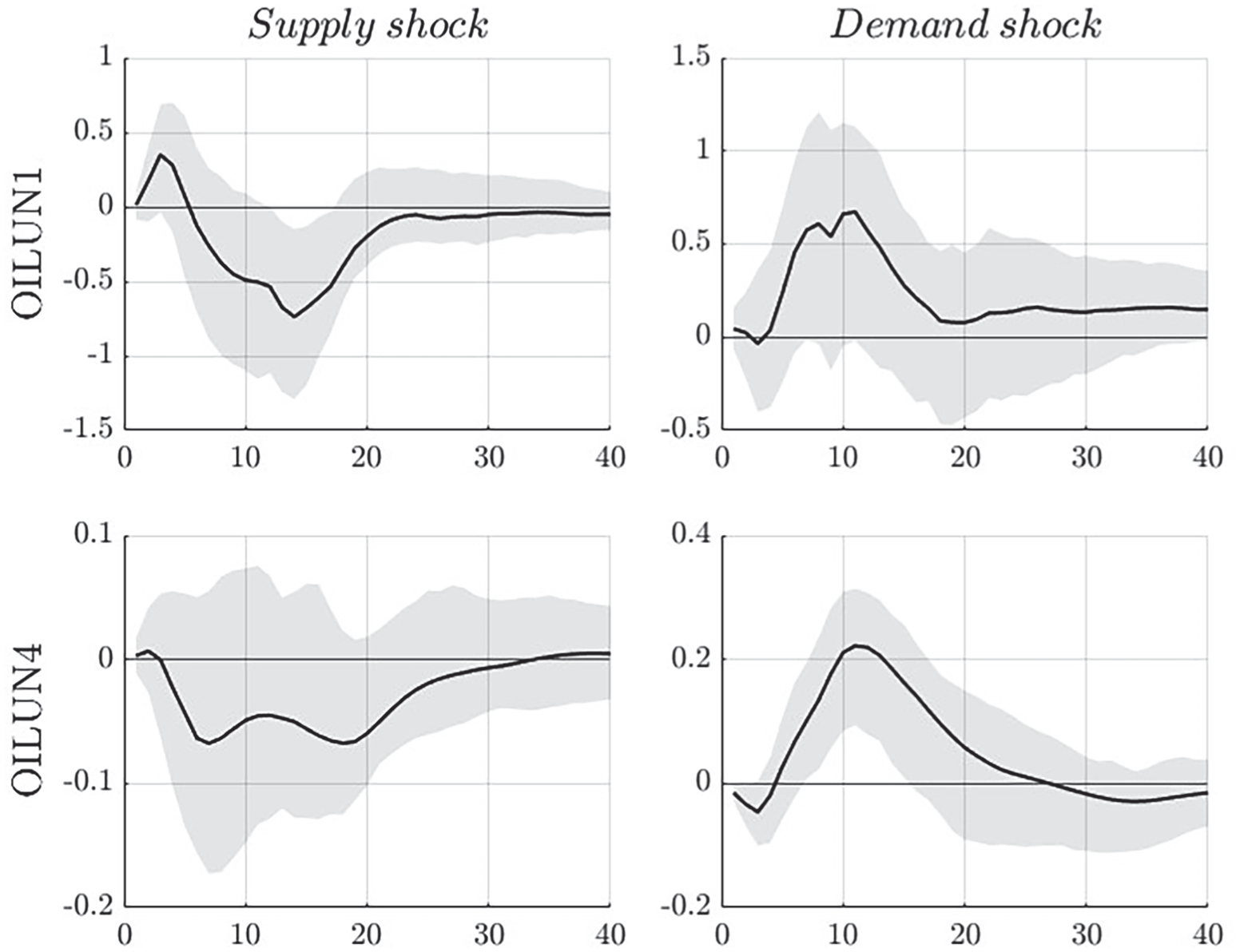

As it is evident from Figure 1, OILUN1, which is our proxy for supply-driven oil price uncertainty (OILUN_S) is more volatile compared to OILUN4, the demand-driven oil price uncertainty proxy (OILUN_D). Also, we can observe more frequent spikes for OILUN1 which are related to oil supply disruptions. For instance, the large price spike of the OILUN1 series in the fourth quarter of 1990 coincides with the oil supply disruption caused by the Iraq invasion to the state of Kuwait. On the contrary, we do not observe a spike in the OILUN4 series during the 1990 to 1991 period. To demonstrate further that the short-term (first quarter ahead) and the long-term (fourth quarter ahead) of oil price uncertainty series are driven by supply and demand oil price shocks respectively, we proceed by estimating a version of the Kilian’s (2009) SVAR model augmented with oil price uncertainty shocks. We follow Kilian (2009) and fit a monthly-frequency SVAR, whereby we use monthly oil price uncertainty series (having a three-month and twelve-month horizon respectively). Further, we decompose oil shocks to oil supply, aggregate demand, oil-specific demand, and oil price uncertainty, with the following VAR ordering:

In equation (4), the OILPROD is the monthly growth rate of global crude oil production, GACT is the global economic activity index as employed by Kilian (2019), OILPRICE is the natural logarithm of the real WTI crude oil price (defined as the nominal WTI oil price deflated with the US Consumer Price Index) and OILUN(h) represents the oil price uncertainty factor with horizon h (h = 3, twelve months). For consistency purposes, we chose to present the results of our SVAR model when using OILUN1 (first quarter (three-months) ahead oil price uncertainty) and OILUN4 (fourth- quarter (twelve months) ahead oil price uncertainty) to be comparable with our respective first quarter and fourth quarter ahead oil price uncertainty factors employed in our study.

The SVAR model representation is given in (5) below:

In equation (5)εt is the vector with orthogonal structural innovations. Following, Hamilton (2003) and Elder and Serletis (2010) and Kilian (2009), we allow for one year of lags (h = 12) to allow for sufficient dynamics in the oil-macroeconomy interactions, as shown in equation (5). 5 The recursive structure of matrix A0 in (5) and is given in (6):

We estimate the SVAR model using

Estimated impulse response functions (IRFs) of short and long-run oil price uncertainty (OILUN1 and OILUN4) to demand and supply shocks.

Our estimated IRFs show that the response of one quarter ahead oil price uncertainty (OILUN1) to aggregate demand shocks is insignificant, while a positive supply shock has a transitory negative effect on OILUN1, remaining significant for fifteen months following the initial supply shock. Therefore, according to our results, an unexpected oil supply shortfall (a negative oil supply shock) will result in rising uncertainty in the crude oil market in the first quarter. There is evidence in the oil-macroeconomics literature which shows that unforeseen oil supply shocks have a temporary impact on oil prices (Baumeister and Kilian 2016; Kilian 2009; Prest 2018). For instance, Kilian (2009) shows that an unexpected oil supply shock has a temporary positive effect on the crude oil price which vanishes and turns to negative six months after the shock. One explanation of the transitory impact of oil supply shortfalls on the crude oil price is that an oil supply disruption in some regions, that is, Middle East, could be (at least partially) offset by an expansion in crude oil production in some other regions (Kilian 2008, 2009).

On the other hand, the fourth quarter (twelve-months) ahead component of oil price uncertainty (OILUN4) is found to be driven by aggregate demand shocks. According to our SVAR model estimates, a one standard deviation shock in demand results to a long-lasting positive response of OILUN4, with the effect remaining positive and statistically significant between the eighth and the eighteenth month following the demand shock. Moreover, based on this analysis, the fourth quarter ahead of oil price uncertainty is not driven by unexpected innovations in oil supply. Based on our findings, uncertainty about the future level of oil prices having a long-run (fourth quarter) horizon is primarily driven by changes in global demand. In line with these results, the oil macroeconomics literature shows that an unexpected global demand shock has a long-run and persistent effect on the crude oil price (Kilian 2009; Kilian and Hicks 2013; Prest 2018). An illustrative example of the impact of the unexpected aggregate demand shock on oil prices is the unanticipated growth of emerging Asian economies occurring between mid-2003 and mid-2008. This unexpected growth and the aggregate demand (for all industrial commodities) shocks surrounding this period are the key source of the oil price boom occurring during the same period (Kilian and Hicks 2013).

Our SVAR analysis demonstrates further and provides robust empirical support to our conjecture that our estimated OILUN1 (first quarter ahead uncertainty) is a supply driven uncertainty, while the OILUN4 (fourth quarter ahead uncertainty) is a demand driven uncertainty. In the next sections which include the regression model and the discussion of the main analysis (Section 3.3 and Section 4), we denote as the supply-induced oil price uncertainty, OILUN_S, and the demand-driven oil price uncertainty as OILUN_D for consistency reasons.

3.4. Regression Specification

To test our

where

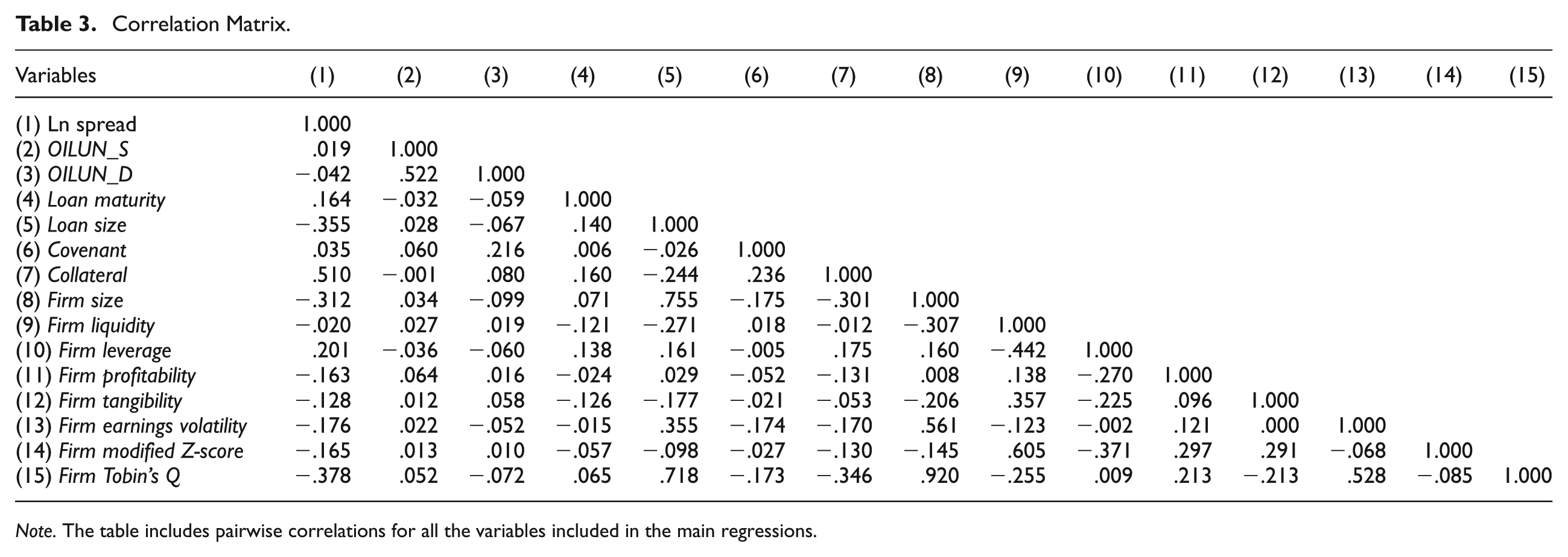

Correlation Matrix.

Note. The table includes pairwise correlations for all the variables included in the main regressions.

4. Empirical Findings

4.1. Testing H1 and H2 Hypotheses

4.1.1. Baseline Estimations (H1 and H2)

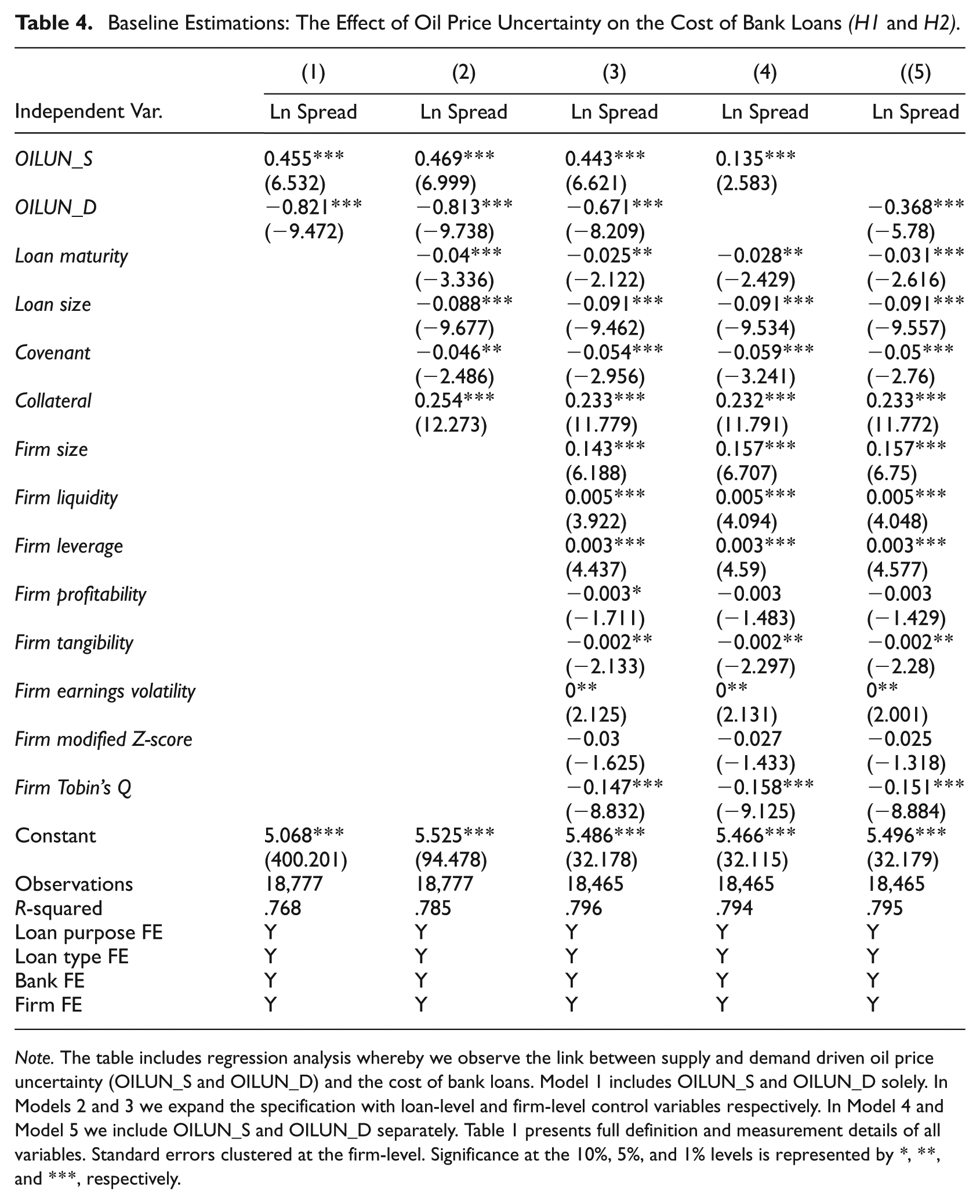

Table 4 shows the baseline regressions of our two main hypotheses: (i) the relationship between oil price uncertainty and the cost of syndicate bank loans, if oil price uncertainty is caused by supply fluctuations (

Baseline Estimations: The Effect of Oil Price Uncertainty on the Cost of Bank Loans (H1 and H2).

Note. The table includes regression analysis whereby we observe the link between supply and demand driven oil price uncertainty (OILUN_S and OILUN_D) and the cost of bank loans. Model 1 includes OILUN_S and OILUN_D solely. In Models 2 and 3 we expand the specification with loan-level and firm-level control variables respectively. In Model 4 and Model 5 we include OILUN_S and OILUN_D separately. Table 1 presents full definition and measurement details of all variables. Standard errors clustered at the firm-level. Significance at the 10%, 5%, and 1% levels is represented by *, **, and ***, respectively.

These findings lend support to our H1 and H2 hypothesis. The results suggest that rising oil price uncertainty driven by supply shocks increases firms’ borrowing costs (H1), while oil price uncertainty caused by demand fluctuations decreases the bank loan cost (H2). The first result could be explained by the cost channel, whereby variation in oil prices caused by oil shortage could increase the production cost of firms. This in turn could hamper firms’ revenues and loan repayment capacity, leading banks to charge higher loan spreads to compensate for the higher risk they carry under rising oil price uncertainty caused by supply shocks. The second result could be justified through the positive effect that oil price uncertainty driven by demand fluctuations could have on economic activity. This, in turn, would improve the firm’s expectations regarding future investments and prompt them to seize profitable opportunities that would boost their sales and improve firms’ creditworthiness. Therefore, banks would face lower loan loss risks which would prompt them to decrease the cost of bank loans under periods of high oil price uncertainty caused by demand shocks. Additionally, our results regarding the loan-level and firm-level control characteristics are in line with these of earlier studies (Bharath et al. 2011; Graham et al. 2008).

4.1.2. Alternative Measures of Oil Price Uncertainty (H1 and H2)

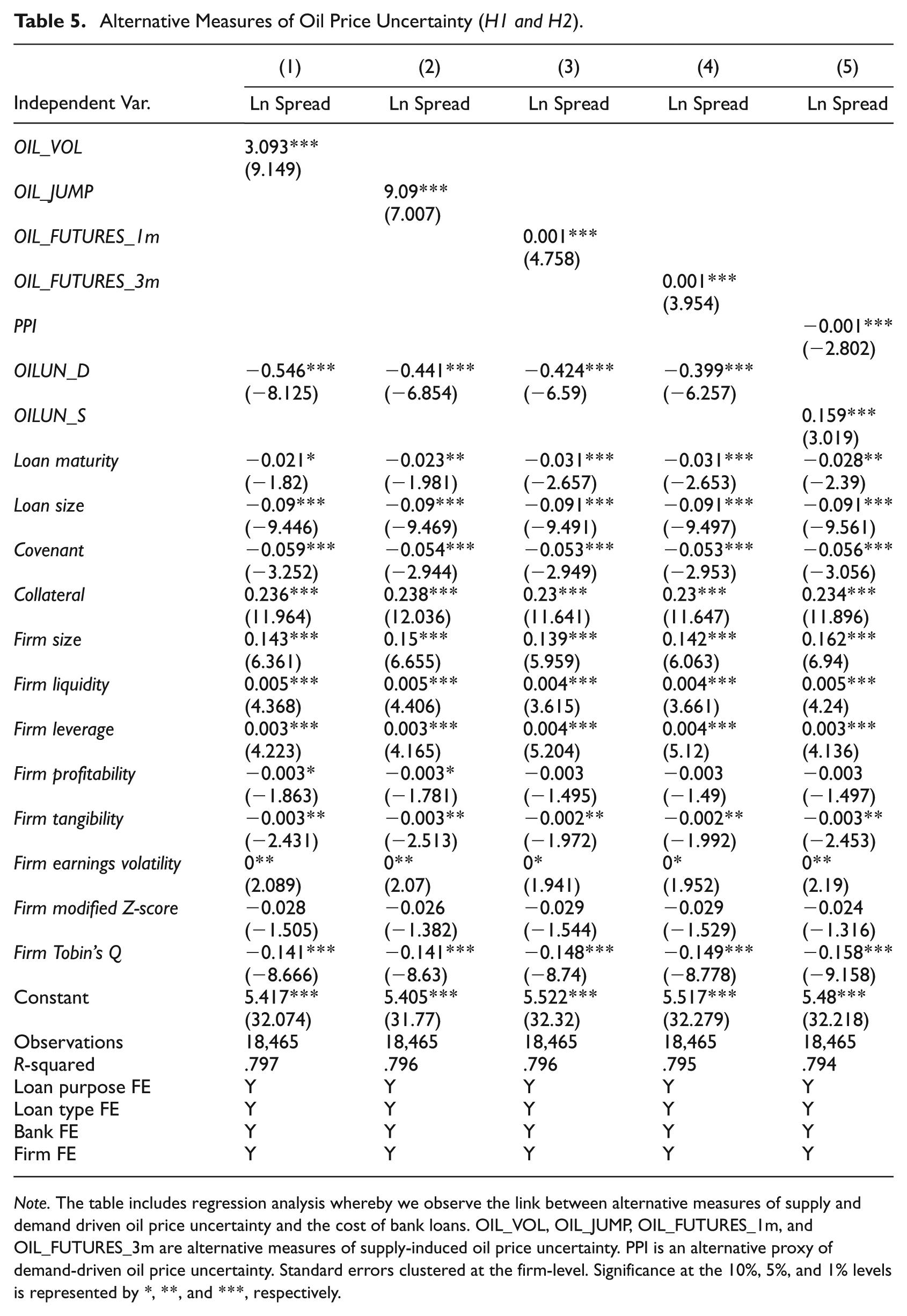

In this section, we replace our main proxy of oil price uncertainty caused by supply shocks (OILUN_S) with alternative measures to further test the validity of our baseline findings presented in the previous section (Section 4.1). These measures have been used in previous studies to capture this effect on macroeconomic and microeconomic, that is, firm, outcomes. Results from this exercise are available in Table 5.

Alternative Measures of Oil Price Uncertainty (H1 and H2).

Note. The table includes regression analysis whereby we observe the link between alternative measures of supply and demand driven oil price uncertainty and the cost of bank loans. OIL_VOL, OIL_JUMP, OIL_FUTURES_1m, and OIL_FUTURES_3m are alternative measures of supply-induced oil price uncertainty. PPI is an alternative proxy of demand-driven oil price uncertainty. Standard errors clustered at the firm-level. Significance at the 10%, 5%, and 1% levels is represented by *, **, and ***, respectively.

In model 1 of Table 5, we employ oil price volatility (OIL_VOL) as an alternative measure of oil price uncertainty driven by supply shocks. In line with the theoretical explanation introduced by the ‘theory of storage’, the rising volatility in crude oil markets is associated with increasing convenience yields for holding commodity inventories. This in turn rises fears of commodity producers and consumers regarding future inventory stock-outs ultimately leading in decreases in production (Geman and Ohana 2009; Pindyck 2004; Symeonidis et al. 2012). In model 2 of the same Table, we use oil price jump (OIL_JUMP) as another measure that could capture the oil price uncertainty induced by supply changes (Elder et al. 2013; Gundersen 2020; Kumar and Mallick 2024). Commodity markets are more vulnerable to price spikes in times where the global commodity inventory levels are low. For this reason, commodity price jump tail risk could act as another market-based (real time) proxy for future inventory stock-outs and commodity supply shortfalls (Bobenrieth et al. 2013; Geman and Ohana 2009; Triantafyllou et al. 2020). Lastly, in model 3 and model 4 of Table 5, we use the one-month (OIL_FUTURES_1m) and the three-month oil futures (OIL_FUTURES_3m) respectively as alternative proxy for oil-supply driven uncertainty shocks (Alquist and Kilian 2010; Geman and Ohana 2009; Pindyck 2004; Ready 2018). According to the theory of storage (Brennan 1958), the variation in the oil futures spread is associated with changes in global crude oil inventories and oil supply shortfalls (Alquist and Kilian 2010; Pindyck 2004). In all these four specifications, we find that the alternative measures exert a positive and significant at the 1% level, effect on the cost of borrowing. We also use an alternative proxy for demand-driven oil price uncertainty. In model 5 of Table 5, we use the producer price index for the oil and gas extraction sector (PPI) in line with Amin et al. (2023). We find that PPI has a negative and significant at the 1% level effect on the cost of credit. Altogether, the above findings provide additional support to our main estimations and further confirm our

4.2. Firms in Supply-driven and Demand-driven Industries

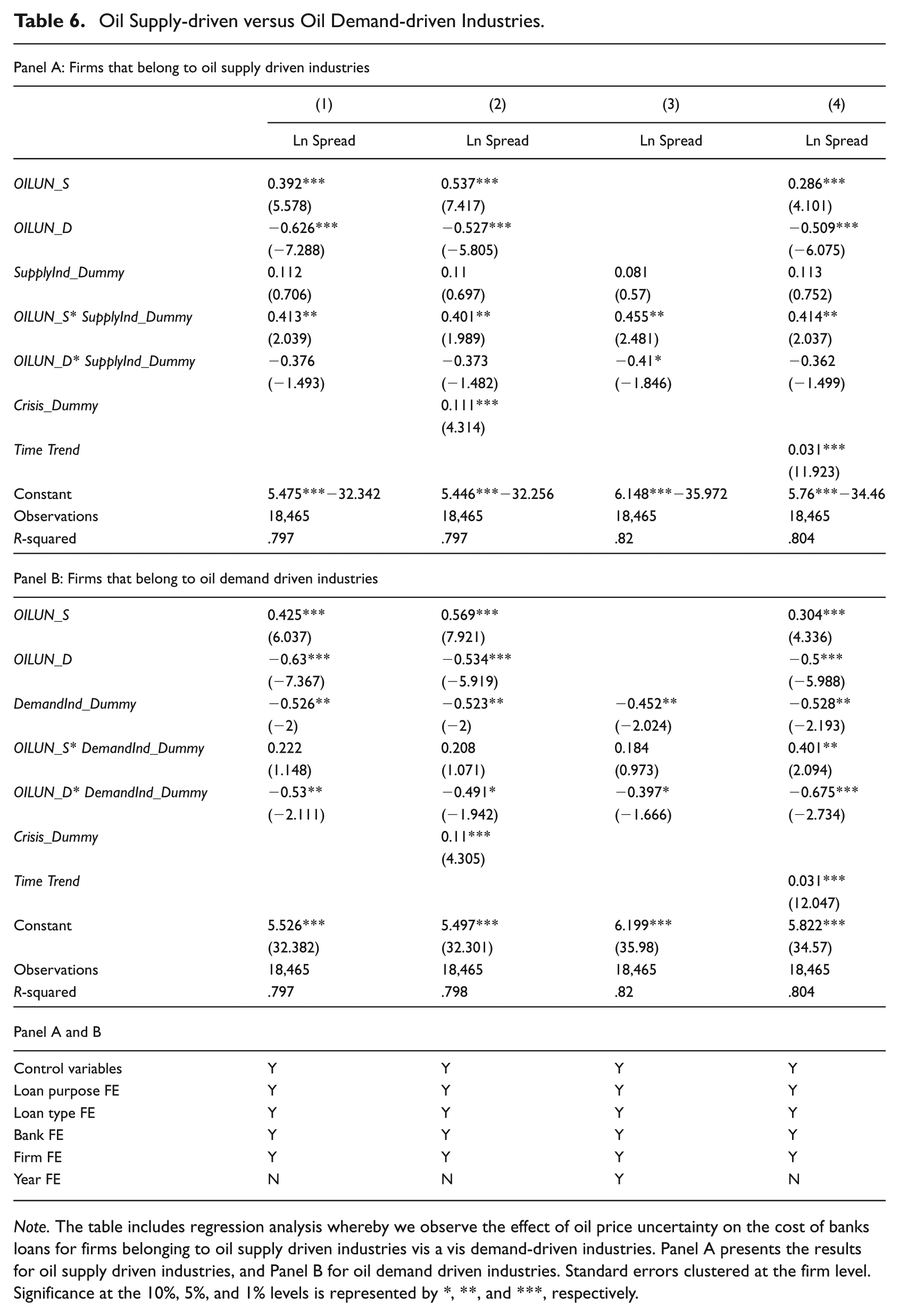

We take a step further and investigate the effect of oil price uncertainty on the cost of bank loans for firms that belong to industries that are major oil consumers vis a vis firms that belong to oil producer industries and of similar products such as petroleum and coal. On the one hand, to the extent that oil price uncertainty is driven by supply shocks, we would expect that the effect of OILUN_S would be more pronounced to firms that are more dependent on supply shortages, that is, users of oil. On the other hand, increased demand-driven oil price uncertainty, OILUN_D, would have a stronger impact on firms that belong to industries that would be more significantly affected by the demand for oil, that is, oil producers and producers of other similar products.To test the above predictions, we create two dichotomous variables. SupplyInd_Dummy would take the value of 1 if the firm is in one of the following industries, buildings (sic 15), tires, rubbers, and plastic products (sic 30) transportation equipment (sic 37), and air transportation (sic 45). The second variable, DemandInd_Dummy stands for a variable that takes the value of 1 if the firm is in one of the following two producing industries, oil and gas extraction (sic13) and petroleum and coal products (sic 29). Next, we interact our two oil price uncertainty variables (OILUN_S and OILUN_D) with SupplyInd_Dummy and DemandInd_Dummy respectively. The results from this exercise are available in model Panel A and Panel B of Table 6.

Oil Supply-driven versus Oil Demand-driven Industries.

Note. The table includes regression analysis whereby we observe the effect of oil price uncertainty on the cost of banks loans for firms belonging to oil supply driven industries vis a vis demand-driven industries. Panel A presents the results for oil supply driven industries, and Panel B for oil demand driven industries. Standard errors clustered at the firm level. Significance at the 10%, 5%, and 1% levels is represented by *, **, and ***, respectively.

In Panel A of Table 6, we present the results from the interaction between the SupplyInd_Dummy and oil price uncertainty variables. In model 1 of Table 6, we run the baseline model and see that the interaction between supply-driven oil price uncertainty (OILUN_S) and SupplyInd_Dummy is positive and significant at the 5% level. In the same model we also find that demand-driven oil price uncertainty (OILUN_D) and SupplyInd_Dummy has a negative effect, albeit weak, on the cost of bank loans.

To capture any effects that could potentially affect the pricing terms of credit during the period of financial crisis, in model 2 of Table 6, we also include a financial crisis variable (Crisis_Dummy) that takes a value of 1 for years 2007 to 2009 and 0 otherwise. We find that the interaction between supply driven oil price uncertainty (OILUN_S) and SupplyInd_Dummy enters the regression positive and significant at the 5% level and that the interaction between demand induced oil price uncertainty (OILUN_D) and SupplyInd_Dummy is negative but statistically not significant. In model 3 of Table 6 we include year fixed effects, as the interactions will still be identified. This estimation allows us to capture for any time variant characteristics that could confound our analysis. Finally, model 4 of Table 6 includes a time trend variable to control for potential trend effects related to macroeconomic conditions. Results from the above estimations remain the same. In Panel B of Table 6, we repeat the similar empirical strategy as in Panel A. All in all, findings from Panel B show that firms that belong to industries on the production of oil (DemandInd_Dummy) are more strongly affected by the demand-driven oil price uncertainty (OILUN_D) compared to supply-driven oil price uncertainty (OILUN_S). Hence, our findings in Panel A and Panel B of Table 6 confirm our expectations on the heterogeneous effects of OILUN_S and OILUN_D on the cost of bank loans for firms that belong to supply sensitive industries as opposed to the cost of credit of firms that belong demand driven industries.

4.3. Robustness

4.3.1. Controlling for Macroeconomic Conditions, Supply and Demand in the Crude Oil Market

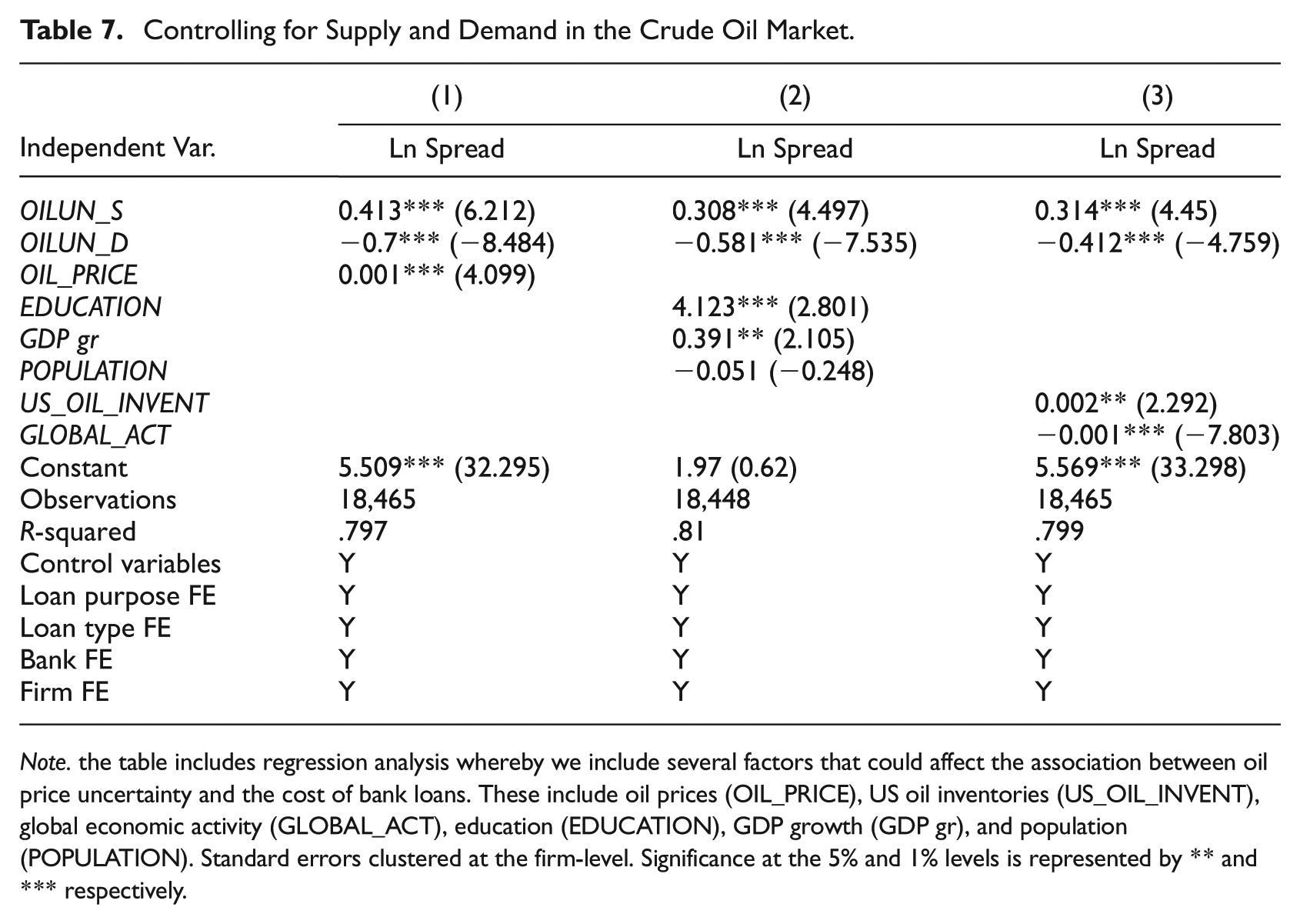

In our baseline estimations, we have included several loan-level and firm-level characteristics to control for possible estimation bias stemming from omitted variables. We have also included several fixed effects, including lead bank, borrower, loan purpose, and loan type fixed effects. Hence, as robustness test, we include several macroeconomic variables and supply and demand proxies that could potentially affect the cost of bank borrowing. The results from this test are in Table 7.

Controlling for Supply and Demand in the Crude Oil Market.

Note. the table includes regression analysis whereby we include several factors that could affect the association between oil price uncertainty and the cost of bank loans. These include oil prices (OIL_PRICE), US oil inventories (US_OIL_INVENT), global economic activity (GLOBAL_ACT), education (EDUCATION), GDP growth (GDP gr), and population (POPULATION). Standard errors clustered at the firm-level. Significance at the 5% and 1% levels is represented by ** and *** respectively.

Firstly, in model 1 of Table 7 we include as an additional control variable the natural logarithm of oil prices (OIL_PRICE) as there are previous studies that show that oil prices could affect lending terms. The results from this estimation indicate that oil price uncertainty proxied by the two variables (OILUN_S and OILUN_D) continue to exert statistically similar effects on the cost of credit. Next, in model 2 of Table 7 we control for state macroeconomic and socioeconomic variables that could affect the cost of borrowing. These include GDP growth, population, and education. We still observe that our findings regarding our two proxies of oil price uncertainty (OILUN_S and OILUN_D) are similar to these of our baseline estimations and statistically strong. Lastly, in model 3 of Table 7 we also control for the supply and demand of oil production by using US oil inventories (US_OIL_INVENT) and global economic activity (GLOBAL_ACT) respectively, as suggested by Kilian (2009) and Baumeister and Hamilton (2019) among many others. The reason being that we aim to test if our results are driven by supply and demand of oil production rather from increases of oil price uncertainty. Yet, after we control for these two factors, our results still show that the effect of oil price uncertainty induced by shocks in supply and demand on cost of borrowing remains unchanged.

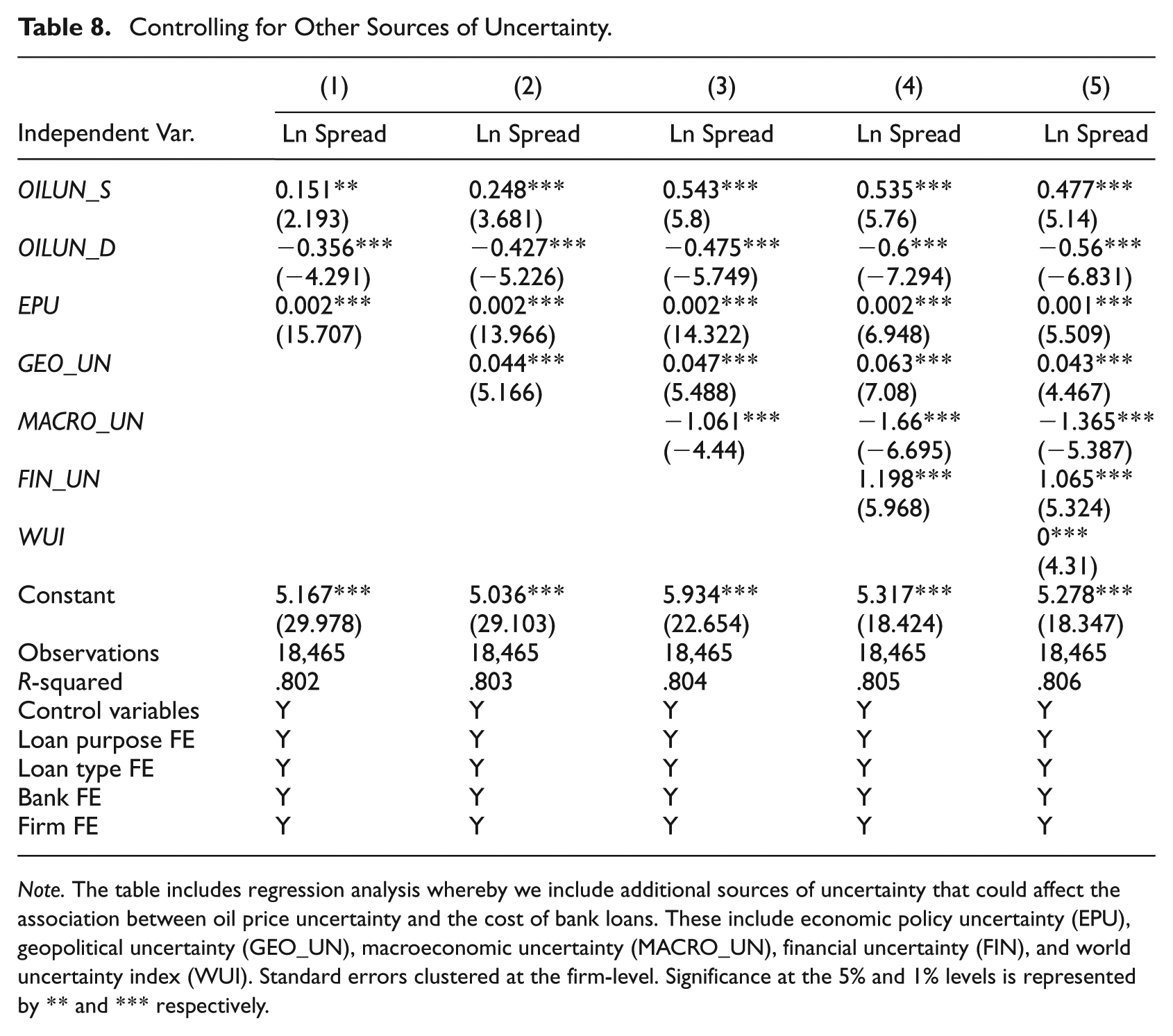

4.3.2. Controlling for Other Sources of Uncertainty

We acknowledge that our results may be driven by other types of uncertainties induced in the general economy. Hence, in this section, we proceed with additional robustness tests whereby we include other types of uncertainties that could affect the cost of credit. The results from this estimation are in Table 8.

Controlling for Other Sources of Uncertainty.

Note. The table includes regression analysis whereby we include additional sources of uncertainty that could affect the association between oil price uncertainty and the cost of bank loans. These include economic policy uncertainty (EPU), geopolitical uncertainty (GEO_UN), macroeconomic uncertainty (MACRO_UN), financial uncertainty (FIN), and world uncertainty index (WUI). Standard errors clustered at the firm-level. Significance at the 5% and 1% levels is represented by ** and *** respectively.

In model 1 of Table 8, we add in our specification the economic policy uncertainty (EPU) variable introduced by Baker et al. (2016) as there is empirical evidence to show that the latter could have an important effect on the cost of bank loans. In model 2 of Table 8, we augment the model by including geopolitical uncertainty (GEO_UN; Caldara and Iacoviello 2022). Further, in model 3 and model 4 of Table 8, we add macroeconomic (MACRO_UN) and financial uncertainty (FIN_UN) respectively (Jurado et al. 2015). Finally, in the last specification of Table 8, we add the world uncertainty index (WUI; Ahir et al. 2022). Across all models of Table 8, the results show that the variables of our main interest (OILUN_S and OILUN_D) continue to exert a significant and similar in terms of sign effect on the cost of borrowing. These results further lend support to the validity of our proxy of oil price uncertainty which is not driven or explained by other types of increased uncertainties present in the US or globally.

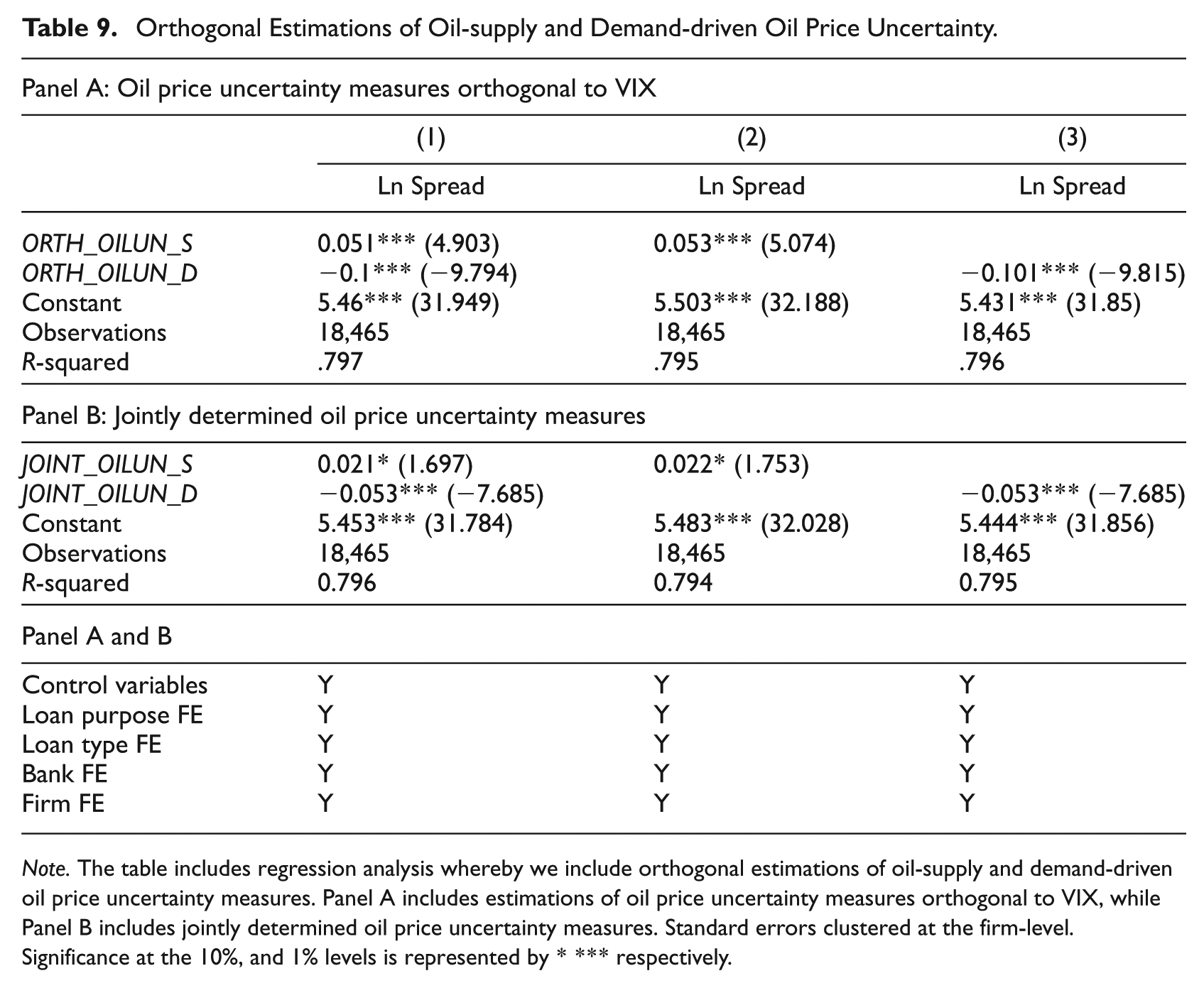

4.3.3. Orthogonal Estimations for Oil-supply and Demand-driven Oil Price Uncertainty

To overcome the issue that our proxies for oil supply (OILUN_S) and demand-driven uncertainty (OILUN_D) might be highly correlated, we follow the modeling approach of Ready (2018) and Clements et al. (2019) by estimating the mutually orthogonal oil demand, supply and risk structural shocks stemming out of a three-factor SVAR model. In more detail, to infer the structural shocks for oil supply and demand-driven uncertainty, we estimate the following SVAR model.

The SVAR model representation is given in (8) below:

Following Ready (2018) we utilize a full year of lags (h = 4 in our quarterly SVAR shown in (8)). The serially and mutually uncorrelated orthogonal shocks

The equation (9) in analytical form (describing the recursive structure of matrix Bo and of structural and reduced form errors

Consequently, our imposed orthogonality condition on structural shocks imposes the following diagonal form on the variance-covariance matrix of structural shocks is given in (11) below:

Where

Orthogonal shocks in oil supply, demand, and risk (stock market uncertainty).

In models 1 to 3 of Panel A of Table 9, we provide the results from this exercise. We find that the orthogonalized estimates, ORTH_OILUN_S and ORTH_OILUN_D exert a positive and negative at the 1 percent effect respectively on the cost of borrowing. These results further confirm our previous estimations and reject doubts on whether our supply and demand-induced oil price uncertainty variables are sufficiently district.

Orthogonal Estimations of Oil-supply and Demand-driven Oil Price Uncertainty.

Note. The table includes regression analysis whereby we include orthogonal estimations of oil-supply and demand-driven oil price uncertainty measures. Panel A includes estimations of oil price uncertainty measures orthogonal to VIX, while Panel B includes jointly determined oil price uncertainty measures. Standard errors clustered at the firm-level. Significance at the 10%, and 1% levels is represented by **** respectively.

4.3.4. Jointly Identified Demand and Supply Oil Price Uncertainty Shocks

Moreover, in addition to the main SVAR model estimates shown in Figure 3 in which we show that the OILUN1(OILUN4) shocks are main supply (demand) driven we estimate an SVAR model in which we allow for the joint identification of global demand, oil demand, oil supply, OILUN1, and OILUN4 shocks. In this way, we estimate the orthogonal demand and supply driven oil price uncertainty shocks. The SVAR model representation is given in equation (12) below:

As in the previous model, we allow for a full year of lags of our set of endogenous variables. εt represents the vector of orthogonal structural shocks using the Cholesky recursive identification strategy. Following the SVAR modeling approaches of Kilian (2009) and Ready (2018) we estimate a SVAR model with the following VAR ordering:

Results from this exercise are provided in models 1 to 3 of Panel B of Table 9. These results show that the jointly orthogonalized estimate for supply induced oil price uncertainty, JOINT_OILUN_S, has a positive and significant at the 10% level on the cost of bank credit. While JOINT_OILUN_D, which is the equivalent proxy for the demand driven oil price uncertainty, exerts a negative and significant at the 1% level impact on the interest loan spread. These findings lend additional support to our baseline estimations.

4.3.5. Additional Fixed Effects and Alternative Clustering of Standard Errors

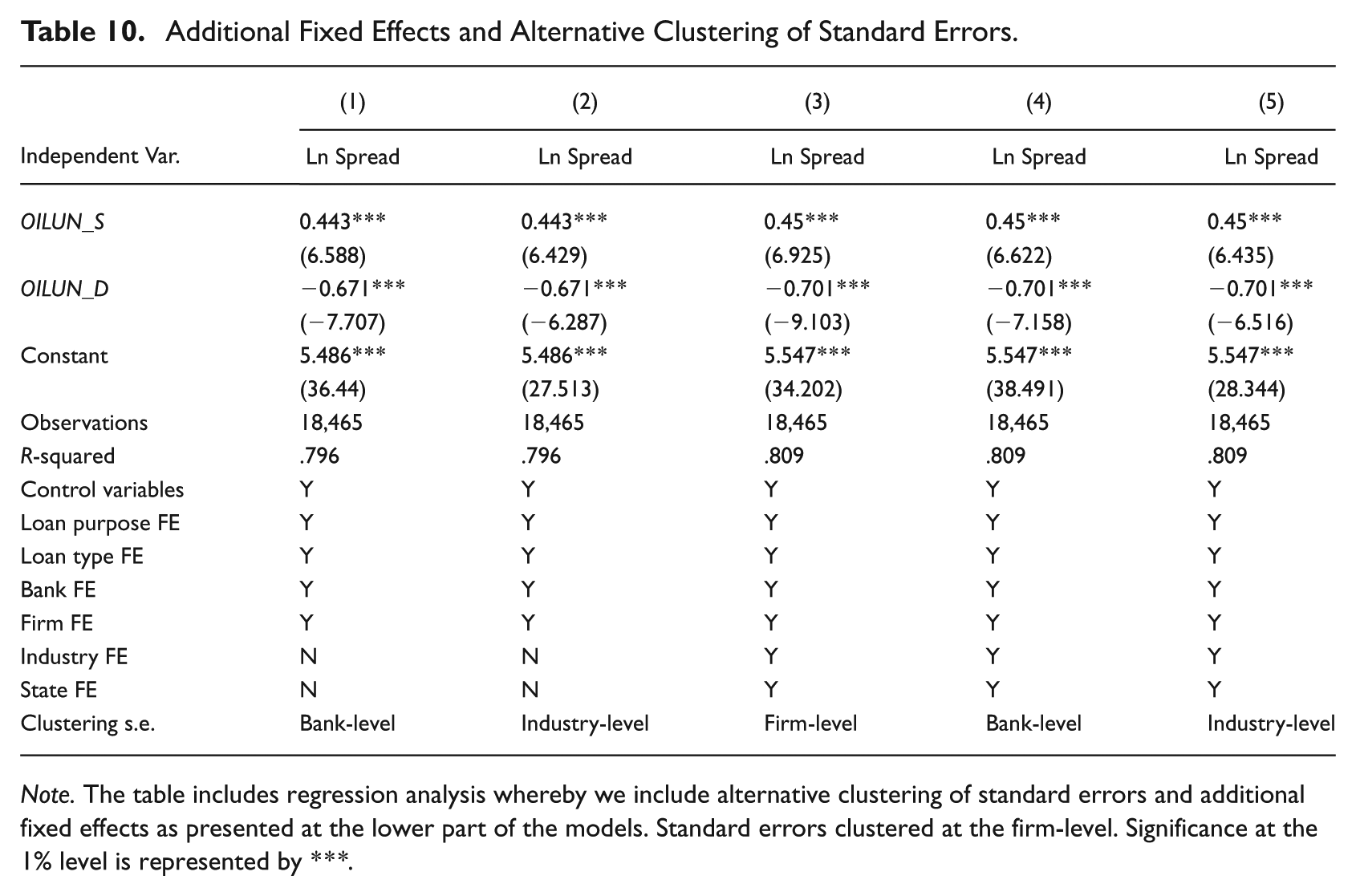

In our baseline estimations, we use firm-level clustering of standard errors in line with several previous studies in the loan syndicate market. As another robustness of our results, we run our baseline model whereby we cluster standard errors by the lead bank and borrower’s industry. The results from these estimations are in model 1 and model 2 of Table 10 respectively. We also run additional estimations whereby we include additional fixed effects, namely industry fixed effects and state fixed effects. Results are in models 3 to 5 of Table 10. Altogether, the findings support our previous estimations.

Additional Fixed Effects and Alternative Clustering of Standard Errors.

Note. The table includes regression analysis whereby we include alternative clustering of standard errors and additional fixed effects as presented at the lower part of the models. Standard errors clustered at the firm-level. Significance at the 1% level is represented by ***.

5. Conclusion

In this paper we study the effect, if any, of oil price uncertainty on the cost of bank loans for US corporations during the 1990 to 2019 period. Our results show that when oil price uncertainty is driven by supply shocks the effect is positive, while it turns negative when oil price uncertainty arises because of demand shocks. We also show that the positive effect on the cost of credit is more pronounced for firms that belong to supply-driven industries, while the negative impact on cost of borrowing is stronger for firms that belong to oil demand sensitive industries respectively.

These findings provide important implications for corporations. Corporations could take advantage of high demand-driven oil price uncertainty and negotiate better lending terms, as banks perceive this uncertainty as a signal for increased cash flows for corporations. On the contrary, firms could pull back during periods of increased supply-driven oil price uncertainty as it is expected to face increased borrowing costs. Moreover, banks could consider the findings of this study useful as they could provide clear evidence on the importance of oil price uncertainty for banking decisions and the presence of two different pricing policies depending on the cause of oil price uncertainty. Overall, our findings open the discussion that uncertainty around the prices of major commodities, such as oil, could be an important factor for banks to consider which has been neglected by literature and warrants for further research.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

1

Despite the importance of changes of oil prices for the local economy, the US holds around 15% of the global demand and supply during the period of our study (https://www.eia.gov/opendata/). This suggests that US-specific oil shocks could not change dramatically the estimates of our global oil price uncertainty measure. Moreover, we measure oil price uncertainty variables as the unpredictable (unexpected) component of oil price fluctuations (see more details in Section 3.2) and hence we do not expect that our proxy for oil price uncertainty could be endogenous to the US economy. Lastly, there is already an abundant amount of literature review focusing on the US that treat global oil shocks as exogenous (Baumeister and Peersman 2013; Elder and Serletis 2010; ![]() ; among others).

; among others).

2

Although investment is found to have long lasting positive impact on firm performance, finance literature also suggests that firms that hold high leverage may decrease investment in their effort to reduce the agency costs of debt that arise from the increased tension in fulfilling debt obligations (![]() ). In that case, banks may view underinvestment positively and thus may be more willing to extend credit.

). In that case, banks may view underinvestment positively and thus may be more willing to extend credit.

3

Thanks to an anonymous Reviewer’s comment on potential price differences between WTI and other proxies of the global crude oil prices during periods of non-availability of storage in Cushing (Oklahoma), we also estimate the oil price uncertainty (OILUN1 and OILUN4) using PADD and Brent crude oil prices to control for the existence of oil price changes (which are specific to the WTI Cushing oil price) that could have an important effect in our findings. Our results are similar to our baseline estimations and are available upon request.

4

5

Following Hamilton (2003) and ![]() , we additionally estimate an identical SVAR model using one full year of lags and our main SVAR estimates remain qualitatively and quantitatively unaltered. Finally, we estimate the SVAR allowing for the optimal lag-length suggested by Akaike and Schwartz information criteria and our main SVAR findings remain unaltered. These additional results can be provided upon request.

, we additionally estimate an identical SVAR model using one full year of lags and our main SVAR estimates remain qualitatively and quantitatively unaltered. Finally, we estimate the SVAR allowing for the optimal lag-length suggested by Akaike and Schwartz information criteria and our main SVAR findings remain unaltered. These additional results can be provided upon request.

6

Several previous studies use the loan spread as the dependent variable (Bermpei et al. 2024; Delis et al. 2020; ![]() ).

).