Abstract

How should the grid evolve to accommodate growing demand and the increasingly competitive economics of renewable energy? Who should be responsible for making these decisions? This paper draws on lessons from electricity sector restructuring to examine how institutional frameworks influence investment decisions, contract negotiations, and power production. When regulated utilities are allowed to earn returns on capital investments that exceed their costs, they often overspend compared to scenarios where they bear the financial risk themselves. Additionally, they exert less effort in securing competitive contracts when they do not directly benefit from the savings. These inefficiencies are particularly pronounced when regulators face challenges in determining optimal actions. Evidence from the adoption of wholesale electricity markets highlights that traditional regulatory frameworks are poorly suited to capture the inter-regional efficiencies of renewable energy generation. Strategies to address these issues include implementing yardstick competition for local distribution utilities and expanding the use of competitive bidding for infrastructure projects.

Keywords

1. Introduction

Electricity sector regulators face both a challenge and an opportunity to innovate as the industry transitions to a more electrified economy, powered by renewable energy. This paper draws critical lessons from past electricity sector restructuring efforts to inform how we should approach grid evolution in the face of growing demand and increasingly competitive renewable energy economics.

There is a consensus that enormous investments are needed to accommodate a more electrified economy, especially if it is to be powered by carbon-free resources (Denholm et al. 2022; Jenkins et al. 2021). If only the task were so simple as to calculate the least cost pathway, and then just build it! Instead, regulators must grapple with an inherently unknowable solution, tossed between waves of technological change and shocks to demand. In the midst of this, the most knowledgeable sources of information are utilities or other interested parties who have a vested interest in the outcome (Laffont and Tirole 1985). Even honest information from these parties may quickly become stale. Do we not expect today’s estimates for long-lived capital requirements to look as absurd in twenty-five years as those from the turn of the century look today? As a result, the question of how best to regulate the energy transition is less about the sophistication of grid expansion models than about creating a flexible regulatory framework that can incentivize economical behavior and adapt to changing circumstances.

While investments in the grid will drive up the price of electricity, higher prices work at cross purposes to the goal of deeper electrification. Businesses and consumers have choices of which fuels to use: electrified heating and transportation will depend crucially on individuals’ decisions. These decisions are largely guided by relative prices (Davis 2025). Borenstein and Bushnell (2022) find that the wedge between marginal and social costs in electricity markets is already substantial in many parts of the country. These dynamics make cost containment all the more important: both gold-plating and treating the energy transition as a jobs program are similarly detrimental to the goals of electrification and decarbonization.

This paper reviews evidence that suggests traditional regulatory frameworks have proven poorly suited to two key tasks that are central to the energy transition: local cost containment, and inter-regional coordination. It concludes with a discussion of potential regulatory reforms that could help meet these challenges.

2. Struggles with Local Cost Containment

Cicala (2015) studies how power plant divestiture in the late 1990s and early 2000s affected the fuel costs and abatement decisions of power plants in the US. A naive analysis comparing regulated plants with merchant plants runs the risk of confounding the effects of divestiture with other cost drivers (i.e., distance from potential fuel sources, and the cost of transportation) because the states that chose to divest their plants were not randomly selected.

Cicala (2015) addresses this issue using what economists call a ‘natural experiment’: state legislatures decided to require all plants to be sold off, so there is no risk of cream-skimming. And plants on the other side of state boundaries (the Mississippi River separating Illinois and Iowa, for example), would have similar procurement opportunities. This makes nearby plants in states that retained their traditional regulatory structures an appropriate counterfactual for what would have happened in the absence of restructuring.

Looking at coal-fired power plants, Cicala (2015) finds that power plants managed to reduce their fuel costs by about 12 percent on average after divestiture, led by Commonwealth Edison, who had been paying vastly above market price for years before divestiture. Why had regulators not induced this cost-minimizing behavior among regulated plants? Cicala (2015) suggests an answer can be found in examining the same outcomes among gas-fired plants. These plants were owned by the same utilities, and responded to the same state regulators. It was essentially the same natural experiment, except the fuel involved was homogeneous and traded on an open market. This made it easier for regulators to discipline costs, because they could simply compare gas expenditures with the Henry Hub price. For coal, on the other hand, the fuel is traded bilaterally, with contracts determining characteristics to which plants tune their operations. This gives utilities an information advantage in defending their costs, which are more difficult for regulators to challenge. So while divestiture led to a 12 percent reduction in coal costs, it did not meaningfully reduce gas costs on average.

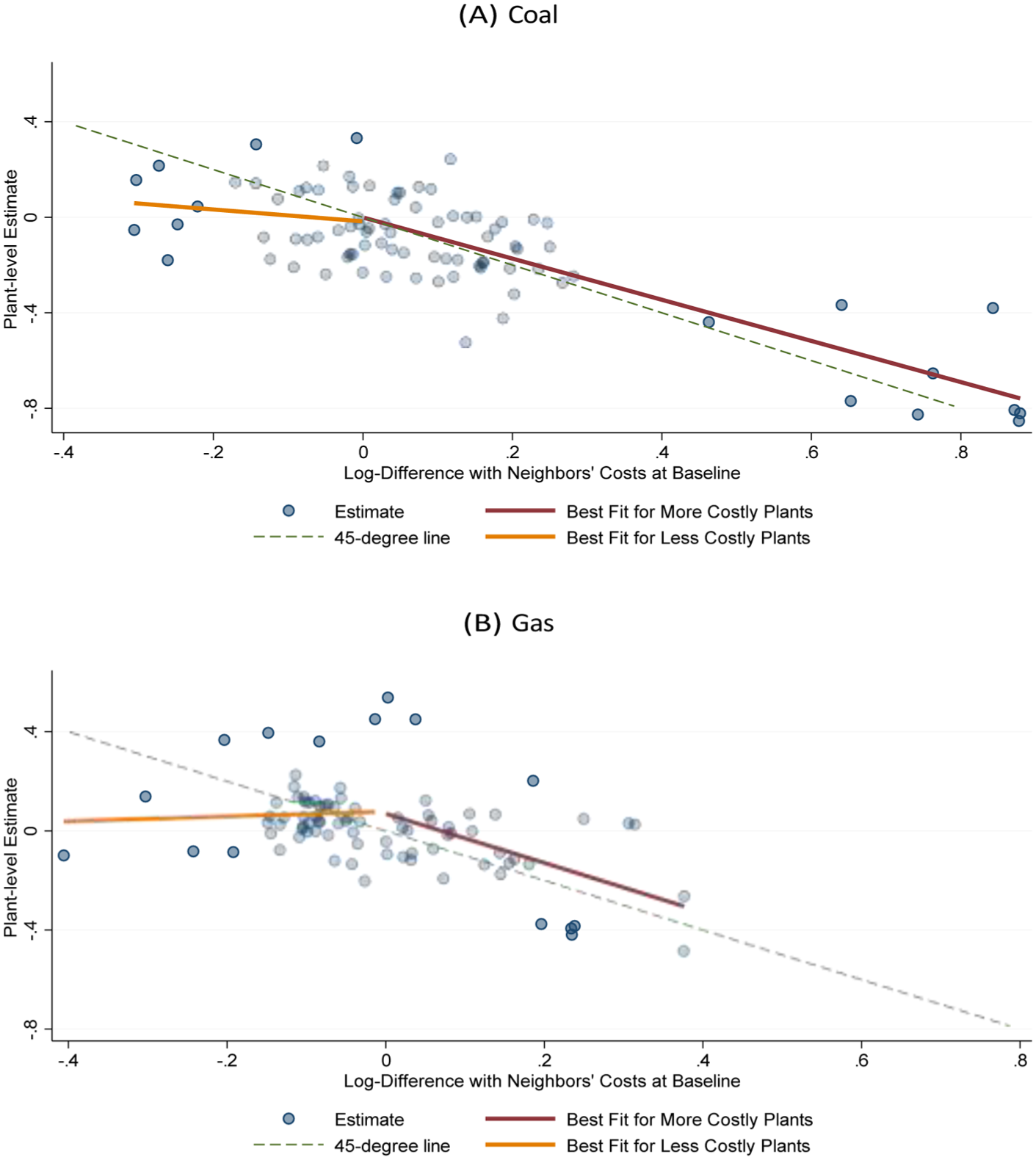

Cicala (2021b) takes this analysis one step further by comparing plant-level estimates of fuel cost changes against the baseline difference in costs compared to the nearby regulated plants, burning the same fuel. These results are presented in Figure 1. To the left of zero on the x-axis are plants that were paying lower prices than their always-regulated neighbors before divestiture began. Plants to the right of zero were paying higher prices. First, note that there is greater dispersion for coal-fired plants (panel A) in how much eventually-deregulated plants were paying at baseline. There are more plants paying substantially higher fuel prices than their neighbors.

Plant-level estimates of divestiture impacts against baseline competitiveness. (A) Coal and (B) Gas.

In both panels, the orange best fit line to the left of zero shows no relationship between the impact of divestiture and how much less plants were paying than their neighbors. This gives some confidence that prices were not simply mean-reverting, with initially low prices rising, and high prices falling in later years. In contrast, the burgundy line to the right of zero shows that fuel prices fell nearly one-for-one (along the 45 degree line) for plants that were paying more than their neighbors before divestiture.

These patterns reveal two striking facts. First, the savings from divestiture depended on how much plants were paying in excess of their neighbors. In other words, divestiture helped reduce costs where there was fat to cut, but otherwise did not lead to fuel price savings. Second, though the overall average effect for gas plants is zero (the mean of the y-axis in panel B), the pattern between the two fuels is similar. In the gas versus coal comparison, the transparency of gas markets meant there was less fat to cut overall, but divestiture still disciplined the prices at high-cost plants.

Cicala (2015) also evaluated how divestiture affected plant owners’ decisions to comply with environmental regulations. The Clean Air Act Amendments of 1990 introduced a cap-and-trade system for sulfur dioxide emissions, which gave plants compliance flexibility. They could either invest in scrubbers, which are capital-intensive pieces of equipment that remove sulfur dioxide from the flue gas. They could switch to low-sulfur coal, which was less capital intensive, or they could simply buy allowances to cover their emissions.

As with the fuel price analysis, the natural experiment comes from comparing two regulated plants burning high-sulfur coal, in close proximity (and thus with the same procurement opportunities), but one of which becomes divested. The generation units in question were of similar size and age. But the divested units were substantially less likely to invest in scrubbers, and instead largely switched to low-sulfur coal. This is consistent with the Averch and Johnson (1962) hypothesis, which posits that regulated utilities have an incentive to over-invest in capital-intensive projects, such as scrubbers, because they are allowed to earn a return that exceeds the cost of capital. Similar results have been found by Fowlie (2010), and recent works by Dunkle Werner and Jarvis (2024) and Rode and Fischbeck (2019) show that utilities broadly earn rates of return that are higher than their cost of capital, distorting investment decisions.

Cicala (2025) shows that these forces continue to affect the transmission and distribution (T&D) utilities whose generation operations were sold off during restructuring. Using similar methods as those described above (comparing nearby utilities of similar size), it finds that the new wires-only utilities born of restructuring expanded their capital investments relative to their vertically-integrated peers. Nine years after divestiture, the average T&D utility whose generation plants had been sold off increased its (largely distribution system) capital investments by $450 million relative to nearby utilities with no regulatory changes. The hypothesized reason for this change is that restructuring led to generation cost savings. Faced with the choice of either lowering retail rates (by passing on the savings), or keeping retail rates constant (by investing the savings in T&D capital), utilities chose the latter. These investments allowed the utilities to capitalize the savings from divestiture into a stream of payments reaped from the enlarged rate base.

Overall, the evidence supports two important channels of cost distortion that raises electricity prices for consumers. The Averch-Johnson effect leads regulated utilities to over-invest in capital-intensive projects because the return they earn on each dollar invested exceeds the cost of capital. The second issue is emphasized in the theoretical literature on asymmetric information. The utilities have much better information on their procurement and construction options than regulators. This makes it difficult for regulators to discipline costs, especially when the products being procured are complex and bespoke.

3. Struggles with Inter-regional Coordination

The US’ balkanized grid owes its existence to both its regulatory patchwork and the historical economics of fossil fuels and transportation. The major population centers were largely fixed in place at the dawn of the electric age. The deposits of coal, oil, and gas that would fuel the power plants were fixed even farther back in time, and their locations were largely undiscovered at the time of settlement. The solution to the geographic mismatch was to build rail and pipeline networks to connect the two. It was only later that technological advances in transmission lines would make it possible for the bulk transmission of energy over long distances by wire. By that time, a regulatory framework had already enshrined the domination of local utilities to exclusively serve their customers. For these companies, who earned money by owning capital, it was far preferable to build (and own) local generation plants and pay for fuel transportation, than to simply own local transmission and distribution lines to connect to far away power plants close to the resources.

One fundamental difference between fossil and renewable resources is that the latter cannot be put on a rail car or in a pipeline. An economical generation industry must relocate to meet the resources, when and where they are available. The geographic mismatch between resources and demand requires high-capacity transmission lines, so that energy-rich areas become exporters, and demand-rich areas become importers.

This interconnection is also important for aggregating shocks to renewable supply. Individual plants, or even regions may be volatile with their production, but these shocks cancel out and yield smooth (and more predictable) generation patterns when considered over larger areas. This approach contrasts quite starkly with the prevailing framework, which requires sufficient local generation, and generally treats the grid’s primary purpose to facilitate reliability between utility service areas.

Wholesale electricity markets are helping understand the insufficiency of the local regulatory framework, and the value of inter-regional coordination. This is evaluated in a comprehensive manner in Cicala (2022). It studies the history of wholesale electricity market initiations in the US, from 1999 to 2012. During this time the share of US electricity dispatched by markets went from about 10 percent to over 60 percent in a series of discrete events (i.e., the initiation of MISO market dispatch, or the expansions of PJM to new territories).

By collecting hourly generation data from nearly every power plant in the country, as well as hourly load from the ninety-eight historical local power control areas (PCAs), Cicala (2022) is able to construct a series of real time supply curves, and observe which units were called on to actually generate power. The paper considers two key components of total generation costs: how closely PCAs followed the merit order within their own areas, and the volumes and values of power traded between areas. While there are surely substantial long-term changes due to generation investment and exit, the paper focuses on the two years around the start of the markets. This allows one to focus on the value of the institutional changes in how the grid was run, as power plants began to bid into the market rather than simply being dispatched by the local utility. The changes in outcomes for the PCAs that adopted markets are compared to those that did not within the narrow windows of market initiation.

The paper finds that wholesale electricity markets inject strong forces for cost reduction, in spite of the usual concerns about market power. The volume of power traded across areas increased by 25 percent, and the costs of out of merit generation fell by 16 percent as price signals guided operational decisions. Overall, this single administrative change in who ran the grid and how led to a 5 percent reduction in total generation costs. In short, wholesale markets facilitate the improved utilization of capital. This is extremely important for the energy transition, as generation resources are geographically tied to the places where the sun shines and the wind blows. Remembering the importance of keeping electricity prices low, wholesale markets provide clear signals about where the best resources are located. The difference in prices between resource-rich and demand-rich areas signal the need for investment in transmission. In the absence of wholesale markets, it is too easy for local regulators (and utilities) to focus on building within their respective service areas, unaware that the lowest cost solution may come from elsewhere.

4. Implications for the Energy Transition

The energy transition will require enormous investments in generation, transmission, and distribution. Wholesale electricity markets now cover over two thirds of the US, and control both access to the grid and output pricing. Strategies to stymie entry now move into more obscure corners, like decisions on interconnection queues, or the siting of new transmission lines. This is at least an improvement over utility behavior in areas without markets, where incumbents are effectively the sole decision makers. This is not to say that the transmission problem is solved (Davis et al. 2023)!

Key issues of government jurisdiction and issues with NIMBYism are discussed at greater length in Cicala (2021a). One notable new addition to this discussion is the work of Hausman (2024), which highlights the role of incumbent utilities, even in market areas. Though they no longer ‘control’ the grid as they once did, they remain ‘stakeholders’ who hold sway over market policies, including what resources are devoted to staffing interconnection studies and transmission build-out. What has long been an electricity market problem is looking more like a good old-fashioned market power problem in the wheelhouse of government agencies tasked with policing anti-competitive behavior. Someone should tell them.

Distribution systems remain universally regulated in the same manner as they were at the dawn of state public utility commissions. The growth of rooftop solar as well as electrifying transportation and heating will require significant upgrades to these local distribution systems. Though we are really only at the beginning of this transition, residential ratepayers are already spending more on T&D than they are on generation (Energy Information Administration 2021). If we have been unable to contain distribution costs when simply treading water, how will we be able to do so when the real upgrades are due?

Here is where the lessons from Cicala (2015) are most salient. For as difficult as it may have been for regulators to know what coal contract would minimize costs, this is surely less complex than the question of upgrading distribution systems. The asymmetric information problem is extreme, and we know this creates problems for keeping costs down. If local distribution systems continue to be understood as natural monopolies, what can be done to incentivize utilities to behave more economically?

A classic regulatory design for handling local monopolies is presented by Shleifer (1985) as ‘yardstick competition’. The idea is to set the price for a local monopolist based on the average costs of similar firms. Firms that behave economically can keep the savings for themselves, while firms that struggle may have to sell off their business to a superior provider. This is a way to avoid the problem of asymmetric information, as it does not require regulators to know the optimal investment decisions. Instead, they can simply look at what other firms are doing, and set prices accordingly.

While this may seem far-fetched for electricity rate setting, regulators often use a perverse version of this when setting rates of return: rather than considering the cost of capital for comparable utilities and setting a rate of return that reflects that cost, PUCs will find a rate of return reasonable if it is comparable to the rates of return allowed for other utilities (Ellis 2025). All utilities therefore have rates of return set by each other’s rates of return, and no one has rates that are set by costs. In other words, regulators are allowing a utility to earn 12 percent not because that is what is required to attract investment, but because other utilities are also earning 12 percent. Generations of parents have cut through this logic with a question about peers jumping off the Brooklyn Bridge. Dunkle Werner and Jarvis (2024) and Rode and Fischbeck (2019) show that this has led to rates of return that are substantially higher than the cost of capital, distorting investment decisions.

As a simple alternative to benchmarking return on equity, regulators could instead set a rate of return equal to the cost of capital for comparable firms, allowing the utility to reap rewards for lining up lower cost financing. Doing so would put downward pressure on other utilities subject to the same mechanism, yet also be flexible enough to rise when capital costs are indeed higher.

This mechanism could be implemented in an essentially automatic way at any time frequency when it comes to setting rates of return. If comparable utilities are securing loans at a 7 percent interest rate (or analogous CAPM value), that is the rate of return the local utility is permitted. If they can instead secure loans at 6 percent, they reap the difference for their shareholders. If they cannot attract capital at a 7 percent rate, there are demonstrably a set of credible operators who can take over.

The question of what investments are actually prudent is a separate question from the question of what rate of return is reasonable. Here regulators face the difficult task of honestly assessing their competence to determine optimal investment decisions. Does a line require two transformers or three? Are there producers offering comparable products at lower cost? Could the same task be accomplished in a completely different manner? What is the cost of delaying the project another year, or what maintenance could be done instead? More to the point, what is the value of a regulator who takes a profit-maximizing utility’s proposals at face value?

Without the expertise to challenge utility proposals, it is only the fig leaf of a rate case that separates electricity distribution regulation from that of broadband. Ultimately the service companies make unfettered decisions in their own interest. To change this status quo, regulators must decide whether to invest in the expertise to make these decisions, or to adopt a regulatory framework that will induce utilities to behave more economically without the regulator knowing exactly what economical behavior is.

One approach that would reduce the regulatory burden would require utilities to put projects out to bid rather than allow them to just present receipts for projects of their own design and construction. This is similar to FERC Order 1000, which requires competitive bidding for inter-regional projects rather than defaulting to incumbent utilities. 1

A straightforward application of this approach would close the ‘regulatory gap’ created by FERC formula rates for projects not approved by state regulators (Joskow 2024; Macey and van Emmerick 2025). Under current rules, a FERC presumption of prudence allows local utilities effectively bypass oversight. With the framework of competitive bidding in place under Order 1000, FERC could restrict eligibility for formula rates to only those projects whose costs have been disciplined by a competitive bidding process. Demonstrating the efficacy of this approach for local transmission projects could pave the way for its broader application by state regulators to distribution projects as well.

Yet working within the utility’s proposed design and simply bidding out construction limits the scope for more innovative cost savings. More broadly defined projects would allow for the possibility of solutions that may be more efficient than the utility’s proposal. For example, rather than a contract to replace an existing transformer substation, the contract could be for the services such a station would provide over a specified period of time. Whether that requires replacing the substation or something different can be left to the bidders, who assume the obligations of the contract.

Taken to the extreme, the role of the local utility would be more of an auctioneer and payments processor than a local juggernaut who leverages its expertise over regulators to extract rents from the public. This approach might be combined with yardstick competition on distribution rates, so the utility would become the residual claimant when choosing between alternative bids—a more expensive bid that it deems necessary to do the job requires them to trade off rewards for reliability against the rewards of selecting cheaper contracts. This complements calls for more performance-based regulation (Joskow 2024), which focuses on outcomes rather than inputs.

How far one should pursue this approach requires balancing the returns from competition-induced cost reduction against the complexity of designing and enforcing such contracts (as well as monitoring the risks of market power). This is ultimately a question of regulatory capacity. When a regulatory agency is dominated by lawyers and accountants, their expertise favors monitoring contracts rather than blueprints. Such an agency is well-suited to overseeing competitive bidding processes, but poorly suited to evaluating the technical merits of utility proposals. It need not be at the local utility’s mercy when it comes to cost containment.

5. Conclusion

As technologies for generating renewable power, powering electric vehicles, and pumping heat have matured, it is clear that an energy transition is well-underway. Yet these forces are pushing inexorably on transmission and distribution systems that were designed for a different era. The regulatory framework that built those systems is similarly ill-suited for the task ahead. By studying the impacts of restructuring in the electricity sector, we can learn about the vulnerabilities of the current regulatory framework, and begin to think about how it needs to evolve to meet the challenges of the energy transition.

Footnotes

Acknowledgements

I am grateful for helpful comments and feedback from Lynne Kiesling, Josh Macey, Dave Rapson, two anonymous referees, and participants from the IRLE Workshop on Resources for Practitioners. All errors remain my own.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

1

At present no projects have been built under this order, as incumbent utilities have simply turned their attention to local projects that are exempt.