Abstract

Economic and social performances are the two strong pillars of sustainable corporate growth. The companies in India are now showing a genuine interest in the upliftment of the stakeholders they serve. They have started giving Corporate Social Responsibility (CSR) a place in their overall strategies of growth. This paper studies the extent of CSR disclosure made by leading companies constituting BSE SENSEX in India. The disclosure practices of 25 of these companies have been studied for the year 2009–2010 by preparing a CSR Index. Content Analysis has been used. Company-wise score and item-wise score has been calculated. The results show that the CSR disclosure by the leading companies in India is low. The company-wise mean disclosure is just 31 per cent while the category-wise mean disclosure is 40.32 per cent. The category of ‘Others’ followed by ‘Environment’ and then ‘Community Involvement’ are the most well-disclosed areas.

Introduction

Corporate Social Responsibility (CSR) is a concept that links corporate sector with social sector. In fact it suggests a contract between the business and the society (Wood, 1991); the only difference being that this contract is a hypothetical one with implied quid pro quo. Since many decades CSR is a part of Indian cultural heritage because the concept of CSR has its origin in the concept of ‘trusteeship’ given by Mahatma Gandhi (Singh, Manmohan, Prime Minister, India, 2007). Gandhiji felt that a non-violent approach will be to treat the capitalists as the trustees of the assets vested with them (Narayan, 1966). This demanded that they managed the assets in the best possible manner; take a part of profit to sustain them and dedicate the remaining profit for the uplift of the society (Masani, 1956; Pachauri, 2004; Renold, 1994). But with the development of company form of organization, shareholders dominated the corporate scene and Shareholder’s model of CSR gained momentum (Friedman, 1970). According to Friedman, business’s sole purpose was to generate profits for the shareholder. He believed that, ‘there is one and only one social responsibility of business: to use its resources to engage in activities designed to increase its profits so long as is stays within the rules of the game’.

But gradually the Shareholder’s model got replaced with a comprehensive approach of ‘Stakeholder’s Theory’ (Freeman, 1984). Stakeholders include all the groups towards whom business holds responsibility. The view based on stakeholder theory, holds that companies have a social responsibility that requires them to consider the interests of all parties affected by their actions (Frederick, et al., 1992; Carroll, 1996; Steiner and Steiner, 2000 and Wilson, 2001). Then, with the ever widening horizons of CSR, the concept of CSR was embraced by ‘Legitimacy Theory’ that suggests the existence of an implicit social contract in which business is accountable to society’s expectations or demands (Patten, 1991; Lindblom, 1994). It ensures that the actions of an entity are desirable, proper, or appropriate within some socially constructed system of norms, values, beliefs and definitions’ (Suchman, 1995, p. 573). CSR can also be viewed from ‘Social Contract Theory’ (Hobbes, 1651; Locke, 1620; Rousseau, 1762) that describes society as ‘a series of social contracts between members of society and society itself’. In the context of CSR, an alternative possibility is not that business might act in a responsible manner because it is in its commercial interest, but because it is part of how society implicitly expects business to operate (Donaldson and Dunfee, 1999; Gray, et al., 1996).

However, today CSR is practiced not only as charity, but has also become an integral part of the corporate strategies (Berad, 2011; Fátima Guadamillas-Gómez, et al., 2010; Kiran and Sharma, 2011). These days the companies follow the theory of ‘Enlightened Self Interest’ (Alexs de Tocqueville, 2000) that states the development of business along with development of society. Companies seem to follow the principle given by Mahatma Gandhi in a modified and strategic manner by balancing between the twin objectives of commercial success along with welfare of the society. Thus, very rightly said by N.R. Murthy, then Chairman Infosys (2008), ‘CSR is ensuring that the company can grow on a sustainable basis while ensuring fairness to all stakeholders’. It is the continuing commitment of a business to behave ethically and contribute to economic development while improving the quality of life of the workforce and their families as well of the local community and society at large (World Business Council for Sustainable Development, 2009).

Globalization of business is one of the key factors for the development of disclosure relating to issues of CSR (Kiran and Sharma, 2011; Krishnan and Balachandran, 2004). Also the corporate governance movements have picked momentum over the past many years incorporating CSR as a main theme (Strandberg, 2005; Wise and Ali, 2009). Customer in today’s world is more powerful as well as more sensitive towards the CSR issues. There exist more effective actions by non government organizations and activists (Azim, et al., 2011). There is a growing role of media in publicizing company’s image that demonstrate voluntary disclosures as commitment to society (Mathews, 1993). The ever rising ethical dilemmas are also putting pressures with respect to level of commitment of company towards sustainable development (Abbott and Monsen, 1979; McWilliams and Siegal, 2000).

CSR reporting also generates competitive advantages (Fát ima Guadamillas-Gómez, et al., 2010; King, 2002). It offers intangible benefits such as better brand image, (Adams, 2002; Simms, 2002), reduced risk of customer boycotts, reduced turnover costs and maintenance of industrial peace (Deegan and Gordan, 1996). Companies following CSR disclosure practices have better internal controls, producing cost savings and improved products and services (Adams, 2002).

On the other hand, there are certain constraints in CSR disclosures. CSR involves increased costs in terms of purchase of environmentally friendly equipment, change of management structure, implementation of stricter quality controls etc. (Azim, et al., 2011). Also the benefits of CSR disclosures are not immediate as compared to the costs involved (McWilliams and Siegal, 2000). The quantification of the costs of CSR disclosure is easy but its benefits that are intangibles are difficult to quantify (Evans, 2003). Also, there is a non-availability of widely acceptable tool to measure CSR parameters (Abbott and Monsen, 1979). Perhaps, that is why CSR related activities are considered as unwelcome and unnecessary deviations from the company’s core affairs. Nevertheless, in the present times companies are conscious about the intangible benefits of synergizing their financial performance with corporate social performance that would help them to sustain themselves in future.

Review of Literature

As suggested by the review of literature the scenario of CSR disclosure differs between developing and developed countries.

Developed countries had high extent of disclosures even around four decades ago as suggested by Ernst and Ernst, 1978 and Abbott and Monsen, 1979. Their studies reveal a disclosure percentage of as high as 85 per cent and 78 per cent respectively in a sample of Fortune 500 firms. However, literature as old as this was not available for developing nations, thereby suggesting that CSR parameters were not considered much important in developing nations during those times. As the decades progressed, the extent of disclosure improved tremendously in the developed countries. As revealed by the studies, the USA had a disclosure extent of 98 per cent (Guthrie and Parker, 1990); the UK had a disclosure percentage of 85 (Guthrie and Parker, 1990); Belgium stood at 81 per cent (Thom and Decoutere, 2009) and Australia at 56 per cent (Guthrie and Parker, 1990). Similarly, in the recent decade the review of leading companies in the developed countries reveal that there has been 37 per cent compound annual growth in the number of companies disclosing CSR issues from 2 companies in 1991 to 154 companies in 2001 and 203 companies in 2006 (Cecil and Mahoney, 2010). Currently the extent of disclosure of leading companies of Global Fortune 500 is touching 88 per cent (Lungu, et al., 2011).

On the other hand, review of literature of developing countries suggests low levels of CSR disclosure. As in countries such as Singapore, Malaysia, Bangladesh, South Africa and even India, the extent of CSR disclosure in their annual reports is low. The disclosure percentages are as low as 26 per cent in Malaysia (Ahmed, et al., 2003; Andrew, et al., 1989; Kin, 1990; Teoh and Thong, 1984); 41 per cent in Bangladesh (Azim, et al., 2011; Belal, 2001; Imam, 2000); 26 per cent in Singapore (Andrew et al., 1989; Tsang, 1998); 50 per cent in South Africa (Savage, 1994); and 46 per cent in India (Aggarwal, 2001; Ghosh, 2002; Kumar, 1996; Lattemann, et al., 2009; Murthy, 2008; Porwal and Sharma, 1991).

The category of ‘environmental disclosures’ has been the most favoured category of companies in developed nations in the past (Abbott and Monsen, 1979; Ernst and Ernst, 1978); as well as in the current times (Lungu, et al., 2011; Thom and Decoutere, 2009). However, developing countries seem to patronize their employees more even in their CSR intent as perhaps they are the major contributors of revenue generation to them. Hence, disclosures related to ‘Human Resource’ Category are the most favoured ones in case of developing nations (Andrew et al., 1989; Baker and Naser, 2000; Kin, 1990; Murthy, 2008; Teoh and Thong, 1984; Tsang, 1998).

Amongst developed nations disclosure of quantitative parameters are of considerable importance along with qualitative aspects (Cecil and Mahoney, 2010; Guthrie and Parker, 1990; Thom and Decoutere, 2009). But, in developing nations more of qualitative CSR disclosures have been reported (Aggarwal, 2001; Azim, et al., 2011; Belal, 2001; Murthy, 2008). CSR disclosures are followed voluntarily by developed nations (Lungu, et al., 2011; Thom and Decoutere, 2009) as against developing countries where mandatory issues alone are focused upon (Ghosh, 2002; Kumar, 1996). Also, reporting the favourable effects of CSR activities in terms of ‘good news’ have been the focus of companies in developing nations and they tend to conceal the unfavourable effects of these activities (Ahmed, et al., 2003; Belal, 2001). However, no such conclusion has been reviewed for developed nations.

In spite of these differences in developed and developing countries the review of literature suggests that researchers from both the groups of countries have followed a common methodology of Content Analysis and have reviewed the annual reports of various companies to study the extent of disclosure amongst developing (Aggarwal, 2001; Ahmed, et al., 2003; Belal, 2001; Kin, 1990; Kumar, 1996; Murthy, 2008; Porwal and Sharma, 1991; Savage, 1994) and developed countries (Cecil and Mahoney, 2010; Ernst and Ernst, 1978; Guthrie and Parket, 1990; Lungu, et al., 2011; Thom and Decoutere, 2009).

Thus, the review of literature definitely suggests a wide gap between the CSR practices as well as CSR disclosures of developed countries and developing countries.

Need of the Study

Corporate Social Reporting practices are affected by the stage of economic development of a country. As suggested by the review of past research carried out in developed and developing countries, extent of disclosure seems to be better in developed countries as the USA, the UK, Australia and Belgium (Cecil and Mahoney, 2010; Guthrie and Parker, 1990; Thom and Decoutere, 2009) as against developing countries such as Singapore, Thailand, Malaysia, Bangladesh and even India (Andrew, et al., 1989; Azim, et al., 2011; Belal, 2001; Kumar, 1996). But in the era of globalization, liberalization and privatization where national boundaries are losing their significance, developing countries need to keep pace with the other developed nations. As per review of literature, Indian companies have less disclosure levels, though India has been given rank IV by CSR Asia’s Asian Sustainability Ranking (October, 2009) among the Asian countries. Moreover, India is one of the ‘Big Four’ countries of BRIC nations, which have been labelled as major polluters (The Hindu Business Line, 3 April 2012, ‘BRICS that make a difference’). Hence, a need to study commitment of Indian Corporate sector towards the society it serves requires a review and thus, the present study.

Objectives of the Paper

The paper focuses on analyzing the company-wise and item-wise CSR disclosures by the SENSEX companies. The following are the specific objectives:

To study the extent of corporate social disclosure made by the companies, To identify the companies with high and low levels of CSR disclosure, To analyze the category-wise CSR disclosure by the selected companies.

Database and Methodology

CSR index has been prepared after analyzing the annual reports of the companies and studying the previous literature available. Only those variables have been taken that represent voluntary disclosure by the companies, not compulsorily covered under any statute. The index consists of five major heads, further consisting of 50 items in all as, (i) Community Involvement, (ii) Customer and Product, (iii) Human Resources, (iv) Environment and (v) Others. Content analysis has been used. It is a technique of gathering data that consists of codifying qualitative information in anecdotal and literary form, into categories in order to derive quantitative scales of varying levels of complexity (Abbott and Monsen, 1979). As per content analysis scoring is done on dichotomous basis, that is, assigning 0 as the score when no disclosure has been made, assigning 1 as the score if only qualitative disclosure has been made and assigning 2 as the score if quantitative disclosure has been made. However, 1 score has been assigned in case of items where quantitative disclosure is not possible. The total score that a company could obtain came to be 84.

Company-wise score has been calculated to identify the high and low disclosure companies, as: Score obtained by a company/Maximum obtainable score. Also, item-wise score has been calculated to identify the most popular category of disclosure among Indian companies, as: Number of companies disclosing a particular item/total number of companies in the sample. Means of the scores of each category have been calculated to rank the preferences of categories on average basis.

Results and Discussion

Company-wise CSR Disclosure

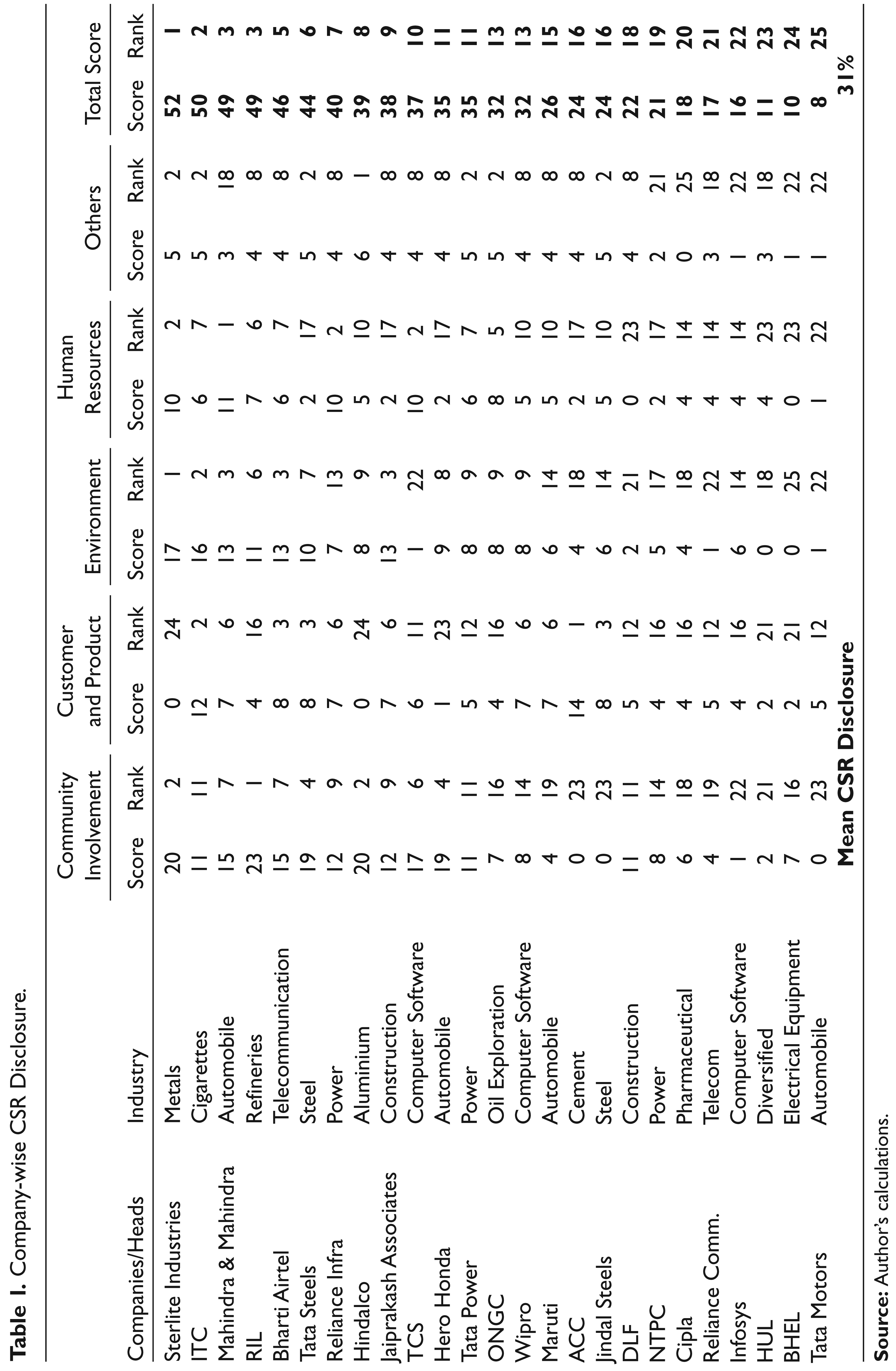

The results of company-wise disclosure have been summarized and presented in Table 1.

Company-wise CSR Disclosure.

As can be seen from Table 1, the company-wise CSR disclosure score varies from 8 per cent to 52 per cent. The top five companies with respect to CSR disclosure scores are Sterlite Industries (52 per cent), ITC (50 per cent), Mahindra & Mahindra (49 per cent), RIL (49 per cent), Bharti Airtel (46 per cent) and Tata Steel (44 per cent). For Sterlite Industries out of total score of 52 per cent, 20 per cent disclosure is with respect to ‘Community Involvement’, followed by 17 per cent for ‘Environment’, 10 per cent for ‘Human Resource’ category, 5 per cent in the category of ‘Others’ and 0 per cent for ‘Customer and Products’. Similarly, for ITC out of total score of 50 per cent, 16 per cent for ‘Environment’, 11 per cent is for ‘Community Involvement’, 12 per cent for ‘Customer and Product’, 6 per cent for ‘Human Resource’ and 5 per cent for ‘Others’. For Mahindra & Mahindra out of 49 per cent, 23 per cent is for ‘Community Involvement’, 13 per cent for ‘Environment’, 11 per cent for ‘Human Resources’, 4 per cent for ‘Customer and Product’ and 4 per cent for ‘Others’. The total score of Reliance Industries Ltd. of 49 per cent is contributed by 23 per cent from ‘Community Involvement’, 11 per cent from ‘Environment’, 7 per cent from ‘Human Resources’, 4 per cent from ‘Customer and Product’ and ‘Others’. Bharti Airtel has 15 per cent disclosure score from ‘Community Involvement’, 13 per cent from ‘Environment’, 8 per cent from ‘Customer and Product’, 6 per cent from ‘Human Resources’ and 4 per cent from ‘Others’. The 44 per cent score of Tata Steels is constituted by 19 per cent from ‘Community Involvement’, 10 per cent from ‘Environment’, 8 per cent from ‘Customer and Product’, 5 per cent from ‘Others’ and 2 per cent from ‘Human Resources’. It can be observed that maximum disclosure score of the top five companies is with respect to ‘Community Involvement’, followed by ‘Environment’, then ‘Human Resources’, then ‘Customer and Products’ and at the end from ‘Others’.

It can be observed from Table 1, Sterlite Industries has rank 1 in totality. It also stands at rank 1 with respect to ‘Environment’. The company stands at rank 2 for ‘Community Involvement’, ‘Human resources’ and ‘Others’. However, Sterlite Industries has last rank of 24 for ‘Customer and Product’ with 0 per cent disclosure. ITC Ltd at rank 2 in totality also has rank 2 for ‘Environment’, ‘Customer and Products’ and ‘Others’, rank 7 for ‘Human resources’ and rank 11 for ‘Community Involvement’. However, Mahindra & Mahindra stands at rank 1 for ‘Human Resources’, rank 3 for ‘Environment’, rank 6 for ‘Customers and Products’, rank 7 for ‘Community Involvement’ and at 18th rank for ‘Others’. Though the company stands at rank 1 in the category of ‘Human Resource’s but the percentage disclosure score is only 13 per cent. Similarly RIL has rank 1 for ‘Community Involvement’, rank 6 for ‘Human Resources’ and ‘Environment’, 8 for ‘Others’ and 16 for ‘Customer and Product’. Bharti Airtel has 3 rank for both ‘Customer and Product’ and ‘Environment’, rank 7 for ‘Community Involvement’ and ‘Human Resources’ and rank 8 for ‘Others’. Tata Steels stand at rank 2 for ‘Others’, rank 3 for ‘Customers and Products’, rank 4 for ‘Community Involvement’, rank 7 for ‘Environment’ and rank 17 for ‘Human Resources’. A noticeable observation is that these top most five companies have good ranks for various categories of disclosures but the extent of disclosure for each category is very low as revealed by their CSR disclosure scores that varies between 23 per cent (RIL for Community involvement) to 0 per cent (Sterlite Industries for Customer & Products). This is also because much of the information in the annual reports of the companies is qualitative in nature, thereby reducing the total obtained score of the top companies from the total obtainable score. Indian companies ought to realize that quantitative and precise information is more useful and enhances management’s reputation and credibility (Botosan, 2007). Qualitative disclosures alone are subjective. These are not sufficient to form concrete judgments in reaching significant conclusions. The results also indicate that even the top most companies of India are reluctant to disclose CSR initiatives which are non mandatory in nature. Moreover, while preparing the CSR Index, only the voluntarily reported issues have been focused upon in this paper; as a result of which the CSR disclosure score of companies are coming low because companies in India are still sticking to reporting of mandatory disclosures only.

Table 1 further reveals that the bottom five companies with respect to CSR disclosure are Tata Motors (8 per cent), BHEL (10 per cent), HUL (11 per cent), Infosys (16 per cent) and Reliance Communication (17 per cent). Tata Motors is at lowest level of disclosure. Also, Tata Motors has the lowest rank for ‘Community Involvement’ (0 per cent). The company has the second lowest ranking for ‘Environment’ (1 per cent), ‘Human Resources’ (1 per cent) and ‘Others’ (1 per cent); thus standing at 25th rank in the sample size. Leading company of Indian like BHEL is at 24th rank (10 per cent), with 0 per cent CSR disclosure score in ‘Environment’ and ‘Human Resources’ and 1 per cent in ‘Others’, thus standing at 25, 23 and 22 ranks in the respective categories. HUL too has made just 2 per cent disclosure for ‘Community Involvement’ and ‘Customers and Products’ standing at 16 and 21 ranks in each of the heads. Also, HUL has 0 per cent disclosure score for ‘Environment’ and 4 per cent and 3 per cent each for ‘Human Resources’ and ‘Others’, getting 23 and 18 rank respectively. Infosys too has poor disclosure scores on account of which it has a rank of 22 among the sample of 25 companies. The company has made just 1 per cent disclosure both for Community Involvement as well as for ‘Others’, getting rank 22 for both categories. Reliance Communications too stands at 21st rank with disclosure varying between just 1 per cent and 5 per cent in the categories taken. It is also observed that the top five companies are those that have high percentage disclosures in the categories of ‘Community Involvement’ and ‘Environment’ as against their counterparts in the bottom five of the list that have low percentage disclosures in these two categories.

Table 1 also shows the CSR disclosure score of the remaining middle companies which are neither top disclosure companies and nor the bottom ones. Here the disclosure percentage varies from 18 per cent to 40 per cent with ranks from 7 to 20. Amongst these companies also, some noticeable findings are that Hindalco Industries that is at rank 8th, stands at rank 2 with respect to ‘Community Involvement’, sharing its position with Sterlite Industries. Also TCS is at rank 2 for ‘Human Resources’ though has 10th rank overall. ACC at rank 1 for ‘Customer and Products’ though it is at rank 16 in totality. Second rank in the category of ‘Others’ is shared by six companies, Sterlite Industries, Tata Steels, ITC, ONGC, Tata Power, Jindal Steels, though the disclosure percentage is very low.

The mean CSR disclosure score for the entire sample is 31 per cent which is very low in comparison to the results reported by past research (Guthrie and Parker, 1990; Kim, 1990; Lungu, et al., 2011; Porwal and Sharma, 1991; Thom and Decoutere, 2009). Further the sample companies constitute the SENSEX of Bombay Stock Exchange and are characterized by their high market capitalization with most actively traded stocks. These companies have financial soundness and good operating results. So much so, that these companies are representatives of the various industries of the economy. But, their commitment and disclosure of CSR issues is not very appreciable as represented by their respective disclosure scores. It was expected that these companies would have higher voluntary CSR disclosure scores.

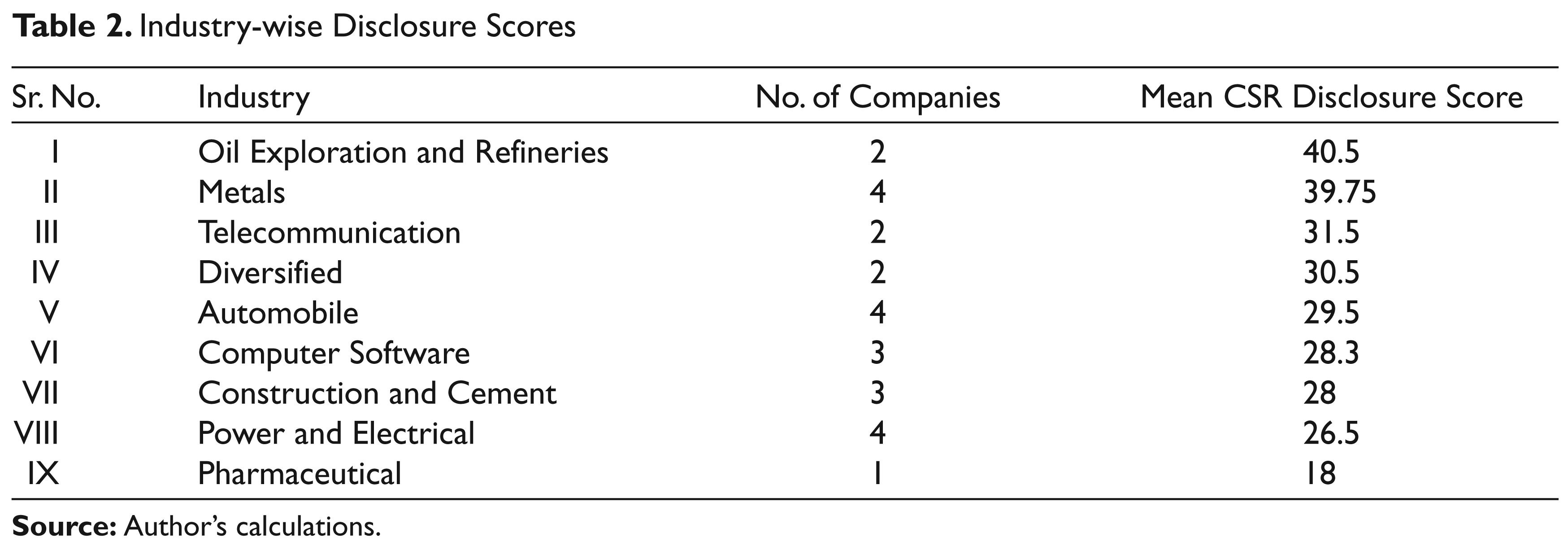

In order to analyze whether the CSR disclosures vary according to nature of industries, the selected companies were divided into nine categories. The mean CSR disclosure scores for each of these industries are shown in Table 2.

Industry-wise Disclosure Scores

Table 2 also shows that there are differences in CSR disclosure scores among industries. The range of the mean CSR disclosure varies from 18 (Pharmaceutical industry) to 40.5 (Oil exploration and energy). The industries performing better on CSR front are the ones that include companies belonging to leading business groups such as Reliance (Reliance Industries Ltd.) and TATA (TATA Steels) which have created their niche in CSR initiatives in the Indian corporate sector over a period of time. TATA Steel was the first company in India to conduct voluntary social audit way back in 1981. Similarly, according to reports by Hong Kong based brokerage and investment firm CLSA; RIL has been ranked as the topmost company involved in CSR initiatives in whole Asia (The Indian Express, 2010).

Table 2 also reveals that the mean CSR Disclosure Score not only differs across industries, but is also very low. The oil exploration industry has high damaging effects on environment (Dudley, 1996; Ismail, 1994), but the mean CSR disclosure of 40.5 is rather disappointing when compared to the nature of activities this industry undertakes. Similarly, metal industry which is responsible for emissions of organic water pollutants (Hettige, et al., 1998) has a mean of 39.75. A lot of hazardous waste is generated from steel industries (State of Environment Report, 2003) and other metal industries and considering the nature of their manufacturing processes this industry should strive for betterment. Similarly, Pharmaceutical industry with the lowest mean CSR Disclosure score of 18 needs to boost up as it is responsible for generating organic pollutants in air (State of Environment Report, 2003). There is always a room for improvement. The manufacturing processes of these industries lead to pollution of environment through hazardous wastes (The Ethical Consumer Research Association, 1994). These industries might be satisfying other parameters of CSR activities as ‘Community Involvement’, ‘Human Resources’ and even ‘Customer and Product’, but they especially need to check the impact of their production processes on the environment. Indian companies in various industries need to make efforts in the direction of sustainable living as there still seems to be a long journey ahead.

Item-wise Disclosure

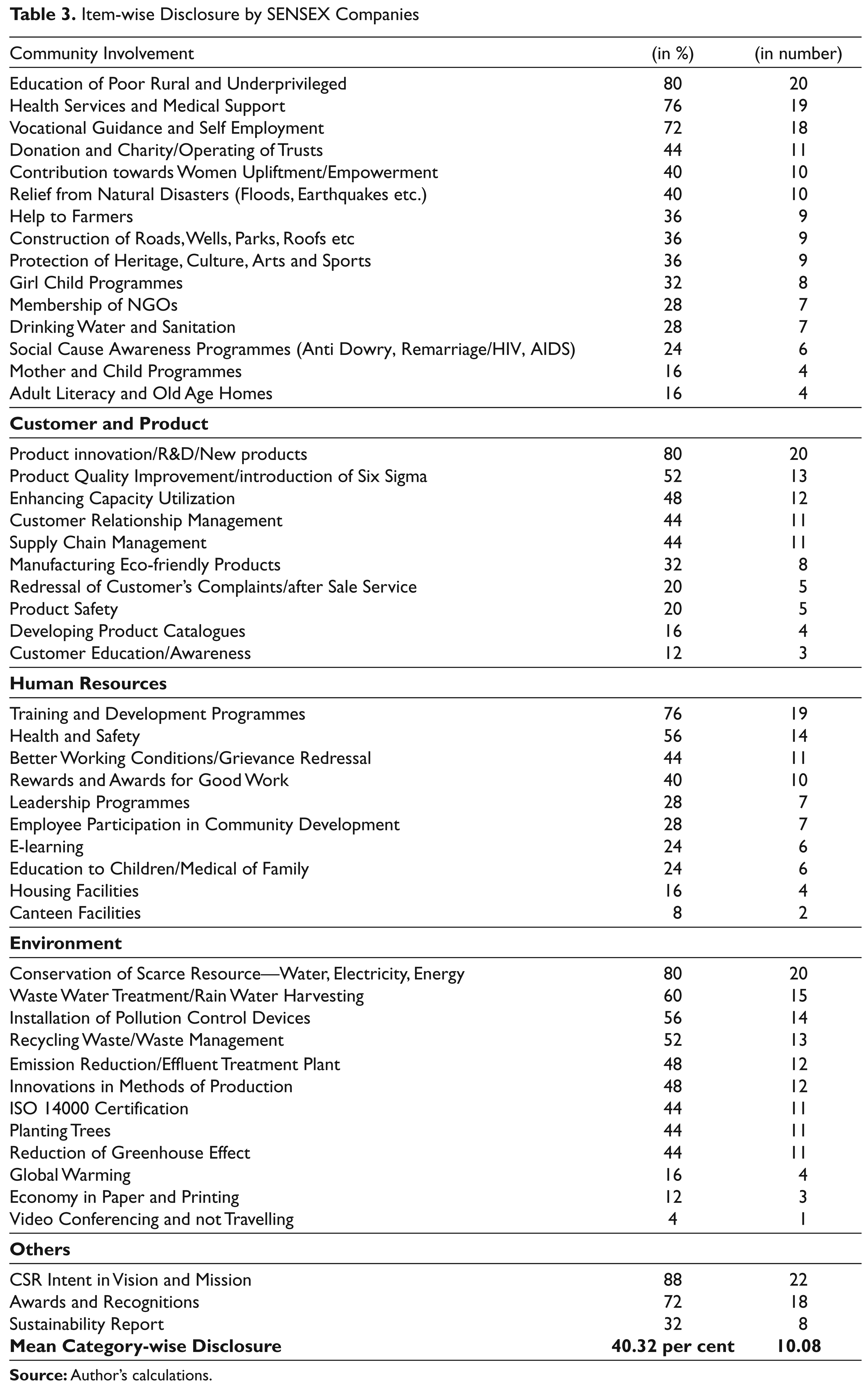

Table 3 shows the item-wise CSR disclosure by the SENSEX companies. The disclosure of all the 50 items has been shown under 5 categories—Community Involvement, Customer and Product, Human Resources, Environment and Others.

Item-wise Disclosure by SENSEX Companies

The results of item-wise disclosure, as shown in Table 3 suggest that in totality, CSR item-wise disclosure score is maximum in case of CSR intent as reflected in ‘Vision and Mission’ (22; 88 per cent), thereby suggesting that companies prefer to disclose their CSR intent in their vision and mission statements. Contrary to this, CSR item-wise disclosure score is minimum in case ‘Video Conferencing and not travelling’ (1; 4 per cent). In fact, Mahindra & Mahindra is the only company reporting on this issue.

In each individual category it is observed that, In ‘Community Involvement’ maximum item-wise disclosure score is in the category of ‘Education of poor, rural and underprivileged’ (20; 80 per cent) and minimum in ‘Mother and Child Programmes’ and ‘Adult literacy and Old Age homes’ (4; 16 per cent). In ‘Human Resources’ maximum item-wise disclosure score is in the category of ‘Training and Development Programmes’ (19; 76 per cent) and minimum in housing and canteen facilities (2; 8 per cent). In ‘Customer and Products’ maximum item-wise disclosure score is in the category of ‘Product innovations, R&D and new products’ (20; 80 per cent) and minimum in ‘Customer education and awareness’ (3; 12 per cent). In ‘Environment’ maximum item-wise disclosure score is in the category of ‘Conservation of scarce resources’ (20; 80 per cent) and minimum in ‘Video conferencing and not travelling’ (1; 4 per cent). In ‘Others’ maximum item-wise disclosure score is maximum in the category of ‘Vision and Mission’ (22; 88 per cent) and minimum in ‘Sustainability Report’ (8; 32 per cent).

Thus, Indian companies are disclosing with respect to community involvement and working for education of poor and rural population of the country. Many schools have been opened by Indian companies for the poor and rural (Satya Bharti School programme by Bharti Airtel); vocational centres have been made (Industrial Training Institutes by ACC) and charitable dispensaries opened (DLF Primary Health Centre by DLF). However, it may also be observed that there is very less disclosure with respect to construction of old age homes. But, at least adult education needs to be focused by the Indian companies as literacy definitely contributes to the growth of the economy as a whole.

With respect to environment the companies are trying to conserve their scarce resources and reporting the same. But, the companies seem to be bothered only about their own resources and not the resources of the economy as a whole as they are disclosing very less for video conferencing and seem to prefer travelling. With the skyrocketing prices of an exhaustible resource like petrol, companies should be thinking of conserving this resource as well. Obviously, it would be eco-friendly too.

Indian companies believe in spending a lot on training and development of its employees, but in the era of hi-technology they should make them e-savvy too. High disclosure score for training and development of employees also suggest that companies are willing to spend and make arrangements where it is for their commercial benefit as trained employees definitely mean higher productivity. Perhaps giving canteen facilities and housing facilities to employees would be a bit too costly for them.

Similarly there is high contribution towards product innovations, R&D and new products. It is more beneficial to the company in terms of its turnover and market share, though it also contributes to country’s GDP and elevation in the standard of living of its people. Indian companies still need to realize the benefits of an educated and aware consumer and hence, work more towards the same.

Also, no doubt companies have developed their vision and mission statements in the light of CSR initiatives as for example, Hindalco’s vision statement quotes, ‘To actively contribute to social and economic development of communities in which we operate’; TATA Steels vision statement mentions, ‘Being a global benchmark in value creation and corporate citizenship’; but if seen minutely this type of CSR reporting satisfies more of a strategic objectives and involves less of financial expenditure. Hence, perhaps it is a myopic vision that these companies offer to the society as a whole more through its words than its deeds. At last, though many companies are aware of it, but a lot has to be done for issuing separate sustainability reports by the companies as supplementary to the Annual Reports. The CSR issues are being reported by majority of the companies either in ‘Director’s Report’ or in ‘Management Discussion and Analysis’, which in fact do much of qualitative reporting only.

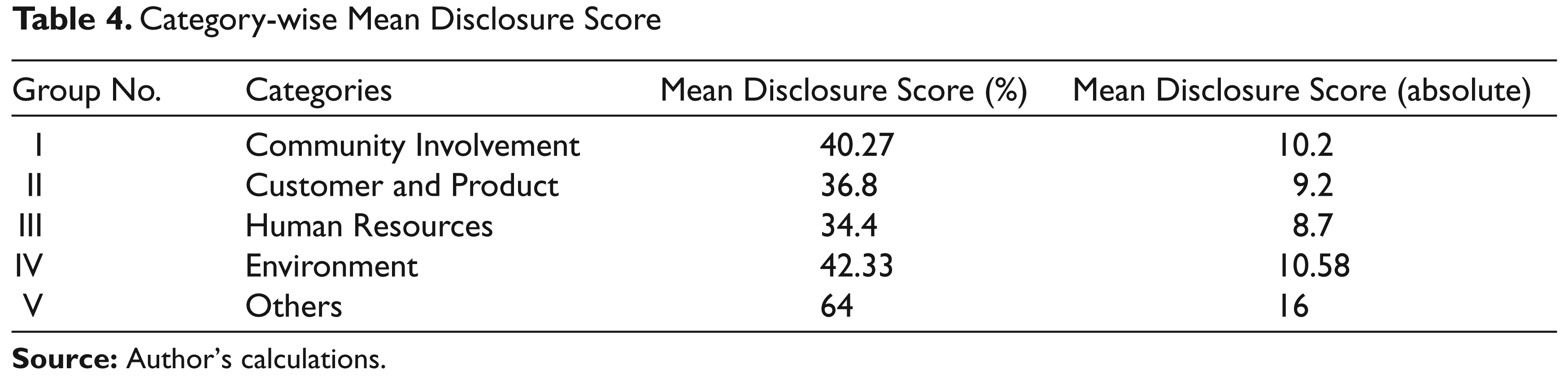

In order to find out that which category of CSR has the maximum reporting, the Mean disclosure score for each category was calculated as shown in Table 4.

Category-wise Mean Disclosure Score

From Table 4, Mean disclosure score for each category shows that ‘Community Involvement issues’ are reported on average by 10.2 (40 per cent) companies, ‘Customer and Product’ by 9.2 (37 per cent), ‘Human Resources’ by 8.7 (34 per cent), ‘Environmental’ issues by 10.58 (42 per cent) and 16 (64 per cent) companies do reporting in the category of ‘Others’. On the basis of mean, maximum disclosure is made by Indian companies in the category of ‘Others’, followed by ‘Environment’, then ‘Community Involvement’, ‘Customer and Product’ and at last in ‘Human Resources’. Thus, it can be said that though the extent of disclosure in Indian companies is low, but the most favoured categories are ‘Others’ (comprising of Vision and Mission, Awards and Sustainability reporting), ‘Environment’ and ‘Community Involvement’. In fact, these categories depict CSR disclosure in real terms. However, the maximum mean by 16 (64 per cent) companies in ‘Others’ also suggests that Indian companies use CSR as a strategic tool and hence, disclose it in their ‘vision and mission statements’ (22; 88 per cent). Also, since 64 per cent companies fall in the category of ‘Others’, this highlights that but for incorporating in their ‘vision and mission statements’ the sample companies believe in issue of separate ‘sustainability reports’ as well (8; 32 per cent), rather than just showing CSR activities as a part of the annual reports alone.

Our results corroborate with the previous literature available on the developing nations of the world, as suggested by Andrew et al. (1989) and Tsang (1998) for Malaysia and Singapore; Belal (2001) and Azim et al. (2011) for Bangladesh; Porwal and Sharma (1991) and Aggarwal (2001) for Indian companies. All these studies corroborate with our study and report low extent of disclosures for CSR.

However, our results differ from the findings of the studies conducted in developed nations as Ernst and Ernst (1978), Guthrie and Parker (1990), Lungu et al. (2011) who showed high CSR disclosure scores in their respective studies. But for the extent even the nature of CSR disclosure for Indian companies is different as compared to the developed nations of the world. They prefer to report both monetary and non monetary information (Thom and Decoutere, 2009) as against our findings where amongst Indian companies the nature of disclosure is more descriptive. These differences are definitely on account of the stage of economic development of a country. These companies tend to achieve their Break Even Points much earlier than the developing nations and thus can contribute to social affairs and sustainability issues.

With respect to the item-wise disclosure our results coincide with Aggarwal (2001) who state comparatively lesser disclosure in HR category as in our results. However, Savage (1994) and Baker and Naser (2000) report Human Resource to be the most disclosed category in companies of South Africa and Jordan respectively, as against our findings where Community Involvement and Environment is the most popular theme of disclosure. Perhaps this difference is again because of the difference in the state of level of development of a country. Porwal and Sharma (1991) and Murthy (2008) also report only 11 per cent and 12.5 per cent disclosure with respect to environment as against our results of 42 per cent item-wise score. In fact, over the years environmental issues have become more important because of cropping problems relating to pollution, global warming, destruction of ozone layer etc. as a result of which the Indian companies have become more sensitive to such issues.

Conclusion

This study has revealed that CSR disclosure is low in case of Indian companies as compared to their counterparts in developed nations. The sample selected consists of the most representative companies of the Indian economy with a very high market capitalization. Still, in spite of being the leading companies of India, the extent of CSR disclosure is low. But, the appreciable aspect is that the most disclosed categories of CSR by the Indian companies are the ‘Community Involvement’ and ‘Environment’, which are in fact the real CSR issues, which should get the attention of the corporate sector.

Further it is very heartening to know from this study that a vast majority of the SENSEX companies mention CSR in their vision and mission statements. This reveals that these companies report their strategic CSR intent through their vision and mission, which pave the way for crafting their business strategies.

Still, it is recommended that Indian managers should rely on the principle of shared value creation which involves creating economic value in a way that also creates value for society by addressing its needs and challenges (Porter and Kramer, 2011). Also, the Company Bill, 2012 has given new mandatory dimensions to CSR reporting amongst Indian companies. Hence, corporate sector in India needs to pull up its socks and drive the next wave of innovation and productivity growth in the global economy, by transforming its business thinking.