Abstract

The study examines how premiums ceded to a reinsurer affect the profitability of non-life insurance companies in Ghana. Secondary data on reinsurance ceded, combined ratio, assets, liabilities and return on assets for 20 non-life insurance companies over the period 2008–2018 were sourced from National Insurance Commission whilst interest and exchange rates variables were obtained from the Bank of Ghana. Panel regression model was employed for the analysis of the data collected.

The results show that purchasing high levels of reinsurance alone does not affect the profitability of non-life insurance companies, but the combined effect of reinsurance and solvency ratio significantly impact their profitability. Managers of non-life insurance companies in Ghana should increase their ability to repay all financial obligations in the short, medium and long term in combination with reinsurance. This will enable insurers to stabilize growth, earn profits and meet their obligations to policyholders in a timely fashion.

Introduction

Reinsurance is simply insurance for insurance companies. Just as individuals, companies or businesses seek protection for their loss exposures, insurance companies also need similar protection for losses that exceed their retention limit or are unexpected and catastrophic. Reinsurance can boost the underwriting capacity of an insurer and reduce its financial exposure (Hall, 2010). Insurers buy reinsurance cover because it enables them to better adjust the capital they actually or potentially have available to the risks they retain (Group of Thirty, 2019). According to Shah et al. (2015), when insurance companies are faced with high losses such as those from the severity of hurricanes, reinsurance helps to maintain the solvency of the primary insurer, that is, the company that cedes its risk by paying a fee. The primary insurer can avoid those risks capable of depleting their financial resource by reinsuring all risks beyond their retention limit. Moreover, to manage and prepare for any potential financial crisis as well as create value for insurance companies, a better reinsurance decision is required.

The concept of reinsurance dates back to the middle ages around 1370. The first known reinsurance contract was established in Genoa and it was purchased to manage marine risks. Later on, Cologne Re, the first specialized reinsurer, was founded in 1846 in Cologne. The economic and political crises, world wars and the world economic cycle contributed to the development of the reinsurance industry in the twentieth century (Group of Thirty, 2019; Holland, 2009). According to Webb et al. (2002), six functions performed by reinsurance for insurance companies include underwriting assistance, financing (surplus relief), stabilization of loss experience, catastrophe protection, large-line capacity and withdrawal from territory or class of business. Group of Thirty (2019) asserts that the risk exposures of insurance companies are efficiently and economically diversified by reinsurance. They also posited that reinsurance helps in covering the financial risks of individuals and corporations. Moreover, reinsurance sustains the stability of the primary insurance market by reducing income volatility as a result of adverse impact on the financial positions of primary insurers.

Insurance companies accept various types of risk expecting to generate an adequate return on capital from the premiums charged and indemnify the policyholder in case of any eventuality of loss (Bony & Moniruzzaman, 2017; Soye & Adeyemo, 2017). The financial performance of insurance companies is also relevant within the macroeconomic context since insurance companies have important functions and contribute to the development of an economy and financial system. It is a major ingredient for an organization’s survival and existence and vital for efficient, fair, safe and stable insurance markets for the benefit and protection of policyholders (Kramaric et al., 2017; Soye & Adeyemo, 2017). According to Calandro and Scott (2001), reinsurance influences insurer’s performance in two ways. Reinsurance expands capacity, stabilizes loss experience and reduces bankruptcy risk. Thus, when the price of reinsurance falls, reinsurance becomes more affordable for insurance companies and this will be reflected in more capacity and price competition (Meier & Outreville, 2006). On the other hand, purchasing reinsurance may increase cost, causing prices to increase and/or decrease profits. Therefore, reinsurance transactions affect ceding insurers’ performance and conduct since they are related to underwriting risk and capacity. Moreover, Iqbal et al. (2014) posited that risk averse insurers use reinsurance to diversify and to decrease their risk, but risk neutral insurers use reinsurance to increase their firm value.

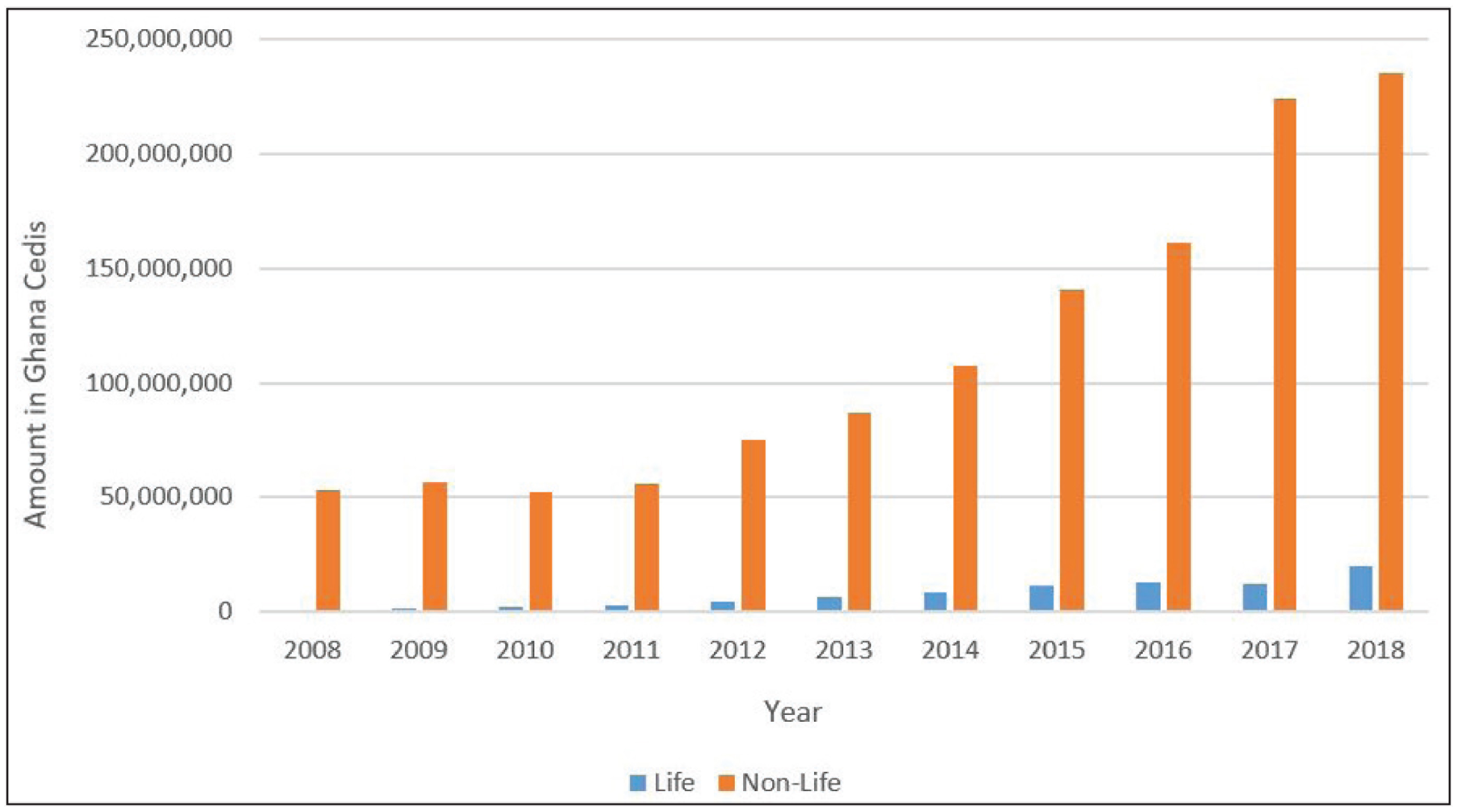

In Ghana, there are three main reinsurance companies, namely the Ghana Reinsurance Company, Mainstream Reinsurance Company and GN Reinsurance Company. Ghana Reinsurance was the first reinsurance company in Ghana. In 1972, it was initially set up as a reinsurance department of SIC Insurance Company. Then in 1984, it gained autonomy as a reinsurance company. It was incorporated as a limited liability company with 100% government shareholding in 1995. Mainstream Reinsurance Company was the first private reinsurance company to start its operations in 1994. This was followed by the establishment of GN Reinsurance Company in 2014. GN Reinsurance is the second privately owned reinsurance company and the third reinsurance company in Ghana (Oxford Business Group, 2020). With the presence of 29 non-life insurance and 24 life insurance companies operating as of 2018, the Ghanaian insurance market can be characterized as a competitive one. However, the lack of confidence in the insurance market and delays in claim payments are two key factors that continue to affect the growth of the insurance industry. Though reinsurance provides capacity for insurers and helps to smoothen out irregular performance thus enhancing innovation, competition and efficiency in the marketplace, the reinsurance sector in Ghana is not fully utilized by insurers. To ensure the growth of the reinsurance industry as well as its full utilization, reinsurance guidelines have been developed and made available to insurers to ensure that they cede majority of their businesses to the local reinsurance companies before any consideration to reinsurance outside the country so as to minimize premium flight (NIC, 2018). The non-life sector is the major contributor of the reinsurance market premium in the Ghanaian insurance market as seen in Figure 1. The low contribution of premiums by life business of the reinsurance sectors income is mainly due to the high retention of life insurers who generally sell investment saving linked products (NIC, 2016).

The profitability of the non-life companies in Ghana that we proxy by return on assets (ROA indicates how profitable a company is relative to its total assets) has been fluctuating over the years though reinsurance demand has been increasing steadily. Between 2008 and 2018, ROA of non-life insurance companies were 9%, 6%, 2%, 4%, 5%, 6%, 4%, 3%, 4%, 4% and 6%, respectively. It can be observed from Figure 1 that though reinsurance patronage for non-life insurance companies has generally been increasing within the study period, ROA has been quite erratic over the period. What role does reinsurance have in this trend of ROA?

A number of studies such as Choi (2010), Choi and Elyasiani (2011), Lee and Lee (2012), Kramaric and Galetic (2013) and Soye and Adeyemo (2017) have been conducted on the impact of reinsurance on insurers’ profitability in different countries. However, most of these studies were conducted in developed countries where the insurance market is developed. Furthermore, no significant work has been done on reinsurance and its impact on insurance companies’ profitability in Ghana. Moreover, reinsurance is not a widely investigated subject in the Ghanaian insurance space, hence the interest to examine the impact of the premiums ceded to reinsurance on the profitability of non-life insurance companies.

With the many benefits associated with reinsurance and the cost involved with it, the study seeks to find out how reinsurance affects the non-life insurance companies where the industry is still in its growing stage. Specifically, the study seeks to determine the effect of reinsurance on the performance of non-life Ghanaian insurers. This article makes some contributions to existing literature and practice. First, it provides some insights about the interdependence of the financial performance of insurance companies and reinsurance. Moreover, the study enhances the insurance literature regarding the effect of reinsurance on financial performance. The article further explores the interaction effect of reinsurance and solvency ratio and shows how these variables work together to impact the financial performance of non-life insurers. Another contribution of the article is the addition of macroeconomic variables such as exchange rate and interest rate to other firm-specific variables in analysing the effect of reinsurance on insurance performance which the other researchers did not explore. This will assist managers of insurance companies to formulate strategies and policies that can protect shareholders’ capital and at the same time ensure efficiency in financial operations.

To achieve the desired objective of this study, 20 non-life insurance companies in Ghana were sampled over a period of 11 years (2008–2018). This period was chosen because in 2006, a law was passed where composite companies which were underwriting both life and non-life policies were mandated to separate both the life and non-life insurance activities by December 2007 so that companies could specialize in one area, that is, gaining the expertise necessary for the industry to expand. Hence, the separation of life and non-life insurance companies took full effect in 2008 (Boadu et al., 2014). The 20 non-life companies sampled were those in operation since the separation. The secondary data collected from the annual reports and financial statements of these insurance companies and bank of Ghana were analysed using a panel regression model. Panel data analysis was used to address the problem of insufficient information and data as a result of using expo and multiple linear regression analysis. Panel data contain information on both the intertemporal dynamics and the individuality of the entities may allow one to control the effects of missing or unobserved variables. It provides a greater sample size and a higher degree of freedom generating more accurate predictions for individual outcomes, whereas ex post facto design does not provide adequate reliable information; therefore, less evidence exists to infer a causal relationship (Ary et al., 2010; Hsiao, 2007).

The rest of the article is organized as follows: the next section presents the review of relevant literature on the concept and theory of reinsurance, followed by the methodology employed for the study. Results and discussion of findings can be found in the fourth section. The fifth section contains the conclusion whereas the sixth section provides recommendations for further studies.

Literature Review

According to Iqbal et al. (2014), one major theory that explains the desire to purchase reinsurance by an insurer to cover the risks being assumed is corporate demand theory. The corporate demand theory is of the view that companies purchase insurance to protect stockholders against the risk of loss. Moreover, Kader et al. (2010) and Mayers and Smith (1990) were of the view that purchasing reinsurance may be motivated by underinvestment problem and the expected cost of bankruptcy hypothesis. Underinvestment problem occurs when firms have to reduce investment spending during times when internally generated cash flows are not sufficient to finance growth opportunities because external financing is sufficiently expensive (Gay & Nam, 1998). Hence, these managers sometimes purchase reinsurance in order to take on excessively risky investment policies that take away value from debtholders and maximize equity value and this could damage the firm’s possibility to survive (Myers, 1977). Bankruptcy cost is the loss in value that occurs when ownership of a firm is transferred from equity holders to debt holders. This cost can be direct (lawyers’, accountants’ and other professional fees) or indirect (lost sales and profits, the possible inability of the firm to obtain credit and/or to issue securities) (Warner, 1977). As the probability of incurring these costs of bankruptcy rises, the value of the firm decreases and hence the desire of managers and shareholders to purchase reinsurance in order to avoid these costs (Masulis, 1980).

The effects of reinsurance on the financial performance of insurance may differ for each insurance market. Kramaric and Galetic (2013) suggested that smaller or undeveloped insurance markets with activities limited to national boundaries and not exposed to the impact of severe losses may perform worse when using reinsurance since they are, in that way, losing part of their income by purchasing reinsurance. However, developed insurance markets with companies that are conducting insurance business across many countries, especially in the regions with high risk accumulation see reinsurance as a tool for better risk mitigating and thus may have a better financial performance. A study by Choi (2010) on firm growth and size in the US property and liability insurance industry pointed out that insurers using more reinsurance grow slower than those who ceded less. This is supported by a study by Lee and Lee (2012) who investigated the relationship between reinsurance and firm performance of the property-liability insurance industry in Taiwan between the period 1999 and 2009. They found that insurers with higher dependence on reinsurance have a lower level of performance than insurers who purchase less reinsurance. Furthermore, Adams et al. (2008) posited that life insurance companies with higher profitability are likely to use less reinsurance than less profitable ones. This is because expected underwriting risks are easily covered by life insurance companies which are more profitable than companies which are less profitable.

However, Berger et al. (1992) argued that the ceding company’s profit is affected by reinsurance activities. The findings of Soye and Adeyemo (2017) who evaluated the impact of reinsurance mechanism on insurance companies’ sustainability in Nigeria for the period 2009–2015 supported this argument. Using expo-facto research design and inferential statistical analysis, the study revealed that ceded reinsurance has a significant positive impact on the profitability of insurance companies. Kramaric and Galetic (2013) examined the effect of reinsurance on the profitability of insurance companies in Austria, Croatia and Romania between 2007 and 2011. The results using panel analysis revealed that in Croatia, insurance companies with lower profitability cede higher percentage of their premiums to reinsurance. However, in Austria, companies which ceded more business to reinsurers reported higher levels of profitability. In Romania, reinsurance had no significant impact on insurance companies’ profitability. This is also supported by Kramaric et al. (2017) who analysed the influence of insurance company-specific, insurance industry-specific and macroeconomic variables on performance of insurance markets in selected Central and Eastern European countries during the period 2010–2014. They found an insignificant influence of reinsurance on insurers’ performance. Choi and Weiss (2005) also investigated market structure, efficiency and performance in the US property-liability insurance industry and found that the relationship between profit and reinsurance is unclear; hence, no firm conclusions were drawn from this study.

Mwangi and Murigu (2015) examined the determinants of the profitability of non-life insurance companies in Kenya. Employing multiple linear regression for the period 2009–2012, they found that leverage, equity capital and management competence index positively affected profitability whilst size and ownership structure negatively affected profitability. Ullah et al. (2016) analysed the determinants of non-life insurance firms’ profitability in Bangladesh using a panel data of eight different insurance companies between 2004 and 2014. They found that underwriting risk and size had a significant inverse relationship with profitability whilst a significant positive relationship was found between expense ratio, solvency margin and growth. Burca and Batrînca (2014) analysed the determinants of the financial performance in the Romanian insurance market during the period 2008–2012. The results from the study showed that financial leverage in insurance, company size, growth of gross written premiums, underwriting risk, risk retention ratio and solvency margin significantly affected profitability. Boadi, Antwi and Lartey (2013) examined the determinants of the profitability of insurance firms in Ghana. The article used 16 insurance firms for the period 2005–2010 and found that tangibility had a negative significant relationship with profitability. However, leverage, liquidity, growth, size and risk did not have any significant influence on profitability. Alhassan et al. (2015) examined the impact of the regulatory-driven market structure on firm pricing behaviour on insurance markets in Ghana. They identified underwriting risk, leverage and inflation as major factors influencing the profitability of both life and non-life markets.

Data and Methodology

Sample and Data

The sample comprised 20 out of the 29 non-life insurance companies due to the availability of data and the number of years in operation. Secondary data on firm specific variables were obtained from the annual reports and financial statements of insurance companies from National Insurance Commission (NIC). The data collected covered the period 2008–2018. Data on interest rate and exchange rate were obtained from the Bank of Ghana.

Empirical Model

To ascertain the effect of reinsurance on the performance of insurance companies, a panel regression model of the form

was employed. Here, βj, j = 0, 1, …,6 are the regression coefficients, i denotes an insurance company with i = 1, …, 20 and t, the time period where t = 2008, …, 2018. In addition,

ROA: return on asset Reins: reinsurance ceded Size: company size SR: solvency ratio CR: combined ratio ER: exchange rate IR: interest rate

Moreover, εit is decomposed as

where δi denotes the insurer’s fixed effect for company i, γt denotes the time-specific effect at time t and ϵit denotes the error term for insurance company i at time t.

Description of Variables Used

The model used had ROA as the dependent variable with reinsurance along with five other independent variables that are expected to affect the profitability of non-life insurance companies. These variables were chosen based on relevant theory and literature.

Dependent Variable

Profitability: It is one of the most important determinants of insurers’ performance and healthiness (Dorofti & Jakubik, 2015). There are many ways of measuring insurers’ profitability. Some of these methods include technical profitability ratio, return on equity (ROE), return on investment (ROI), sales profitability ratio and return on assets (ROA). ROA and ROE are normally used to measure profitability because they are readily accessible, rely on public data and are calculated in accordance with strict, prudent accounting rules (Dorofti & Jakubik, 2015).

In this study, profitability has been measured using ROA because it captures the fundamentals of business performance in a holistic way, looking at both income statement performance and the assets required to run a business (Malik, 2011). It indicates how efficient a company is using its assets to generate profit for the various stakeholders. It is calculated as net financial result/total assets (NIC, 2018).

Independent Variables

Results and Discussion

Descriptive Statistics

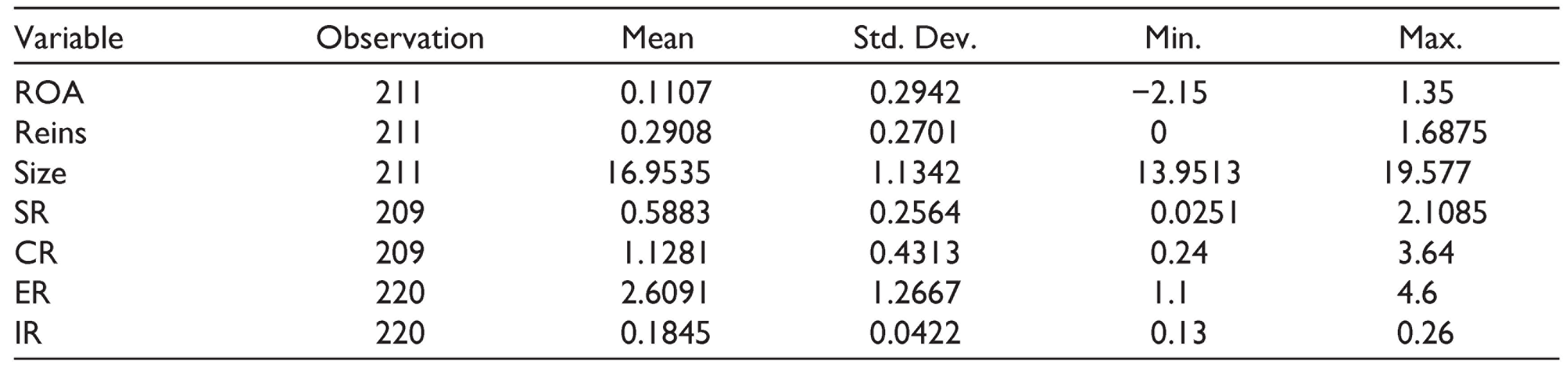

The summary statistics for all variables used in the study are presented in Table 1.

From Table 1, it can be observed that the reinsurance ratio varies from 0% to about 169% with an average of about 29% which is very low. This means that on average, non-life insurance companies do not cede most of their businesses to reinsurance companies. It could be inferred from the data that three insurance companies ceded more than their retention limit to reinsurance. The combined ratio recorded an average of about 113% meaning that non-life insurance companies on average incur underwriting losses. The exchange rate of the dollar to the cedi over the 11 years on an average is around 2.6, with the highest exchange rate recorded in 2018 and the lowest in 2008. This shows that the worth of the US dollar in terms of Ghana cedi keeps rising over the years. On average, the interest rate is around 18.45%. The highest rate was recorded in 2015 and the lowest in 2011.

Summary Statistics

Multicollinearity Test

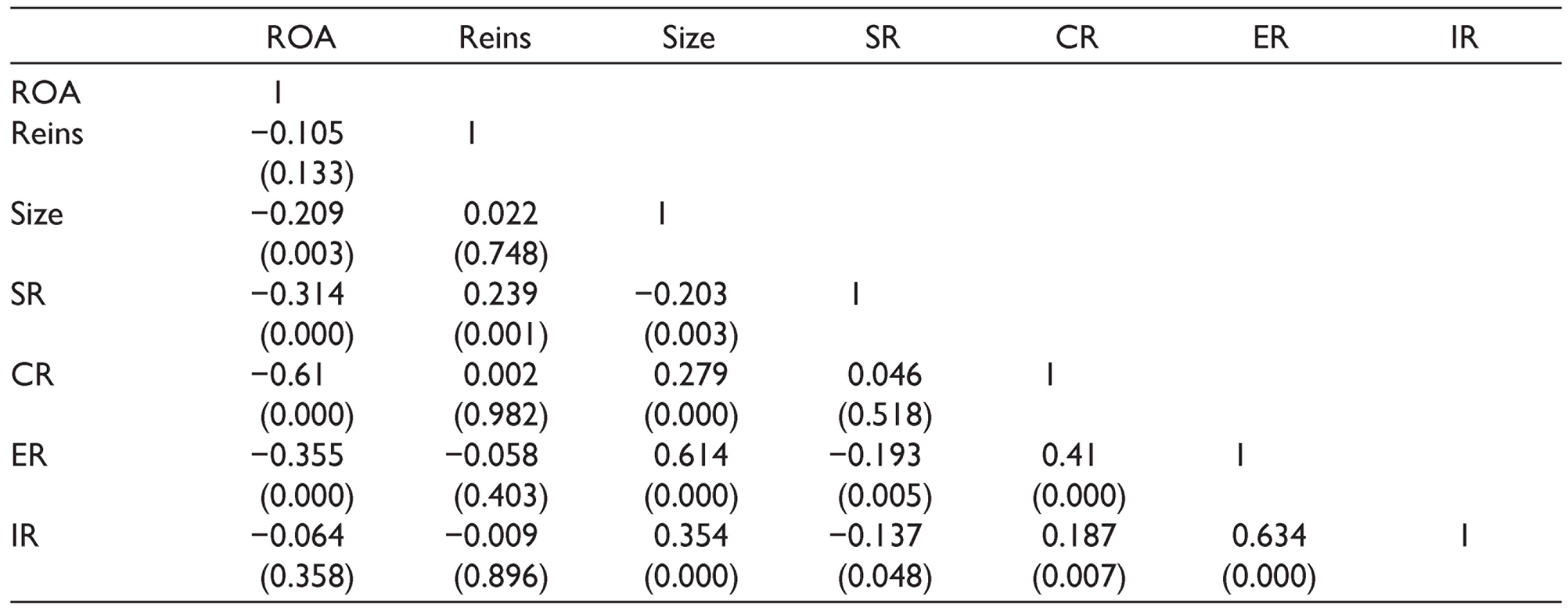

The correlation matrix of the variables used for the study is shown in Table 2. A correlation coefficient more than 0.8 signifies a multicollinearity problem (Kennedy, 1985). From Table 2, no correlation coefficient exceeded 0.8 and so there are no highly correlated independent variables to cause a problem in the regression model. From Table 2, ROA is correlated with size, solvency ratio, combined ratio and exchange rate.

Correlation Matrix

Breusch–Pagan Lagrange multiplier (LM) test was carried out and the results show that there exists a panel effect in the model. The test had a chi-square value of 22.30 and a p-value of 0.0000

Similarly, Hausman test was carried out and the results showed that the random effects model is the best model to be used. The results showed a chi-square value of 49.06 and a p-value of 0.058.

Regression Results

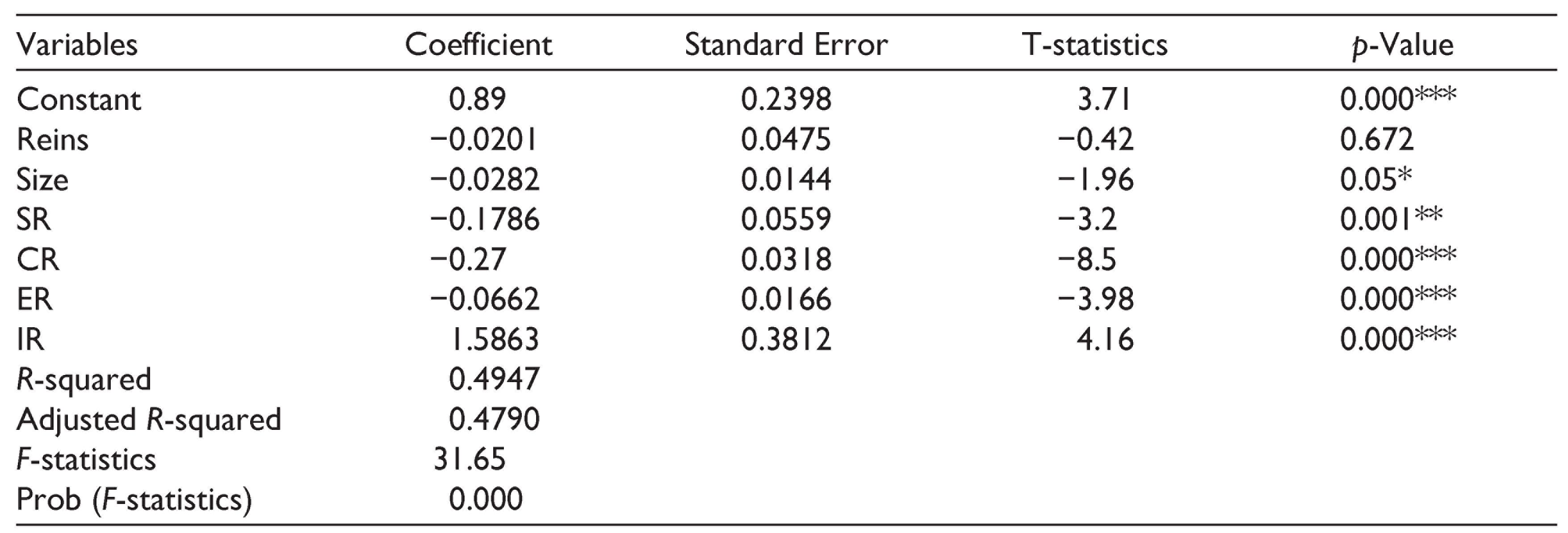

Using a random effects panel regression model, the results of the model are presented in Table 3.

From Table 3, reinsurance has a negative impact on the profitability of non-life insurance companies. Nevertheless, this variable was not significant. This finding is inconsistent with the works of Ma and Elango (2008), Soye and Adeyemo (2017) and Aduloju and Ajemunigbohun (2017).

Regression Results

Size has a negative significant effect on the profitability of insurance companies. According to Adams and Buckle (2003), as insurance companies grow larger and larger, owners or shareholders find it challenging to competently and effectively control deviant behaviour by managers. In addition, the growth in the size of the company may lead to inefficiencies which may reduce insurers’ profitability (Almajali et al., 2012). This is similar to the findings of Ullah et al. (2016), but it differs from the studies of Kaya (2015) and Berhe and Kaur (2017).

Solvency ratio was found to influence insurers’ profitability negatively and significantly. A high ratio indicates that liabilities may be greater than assets and in order to meet the long-term obligations, managers have to borrow from external sources or issue shares and other equities. This may reduce the company’s ability to absorb unexpected shocks and pay claims promptly and thus affect their profitability. Also, companies with higher solvency ratios may find it difficult attracting investors. This is consistent with the findings of Lire and Tegegn (2016), but it differs from the works of Burca and Batrînca (2014) and Ullah et al. (2016).

Combined ratio had a significant negative impact on the profitability of insurance companies. This shows that a lower combined ratio may be due to higher premiums, better cost control and more rigorous management of risks covered. This may cause a positive underwriting result leading to increased profitability (NIC, 2018).

Profitability of non-life insurers was affected negatively and significantly by exchange rate. This is because fluctuations in exchange rates have the potential to affect premiums and claims payment, and hence affecting profitability of non-life insurance companies (Laing, 2008). This is not surprising as many insurers cede portions of business to reinsurers outside Ghana and are affected negatively by the declining value of the cedi to the dollar.

Interest rate positively and significantly affected profitability. A higher interest rate may cause an increase in their investment income such as that on bonds and premiums, and this may increase profitability. This is in line with the findings of Dorofti and Jakubik (2015).

Overall, about 47.9% of the variations in profitability (ROA) can be explained by the independent variables in our regression model. The value of the F-statistic which equals 31.65 is significant at 1% which means the regression model is fit.

Relationship Between Return on Asset and the Interaction of Reinsurance and Solvency Ratio

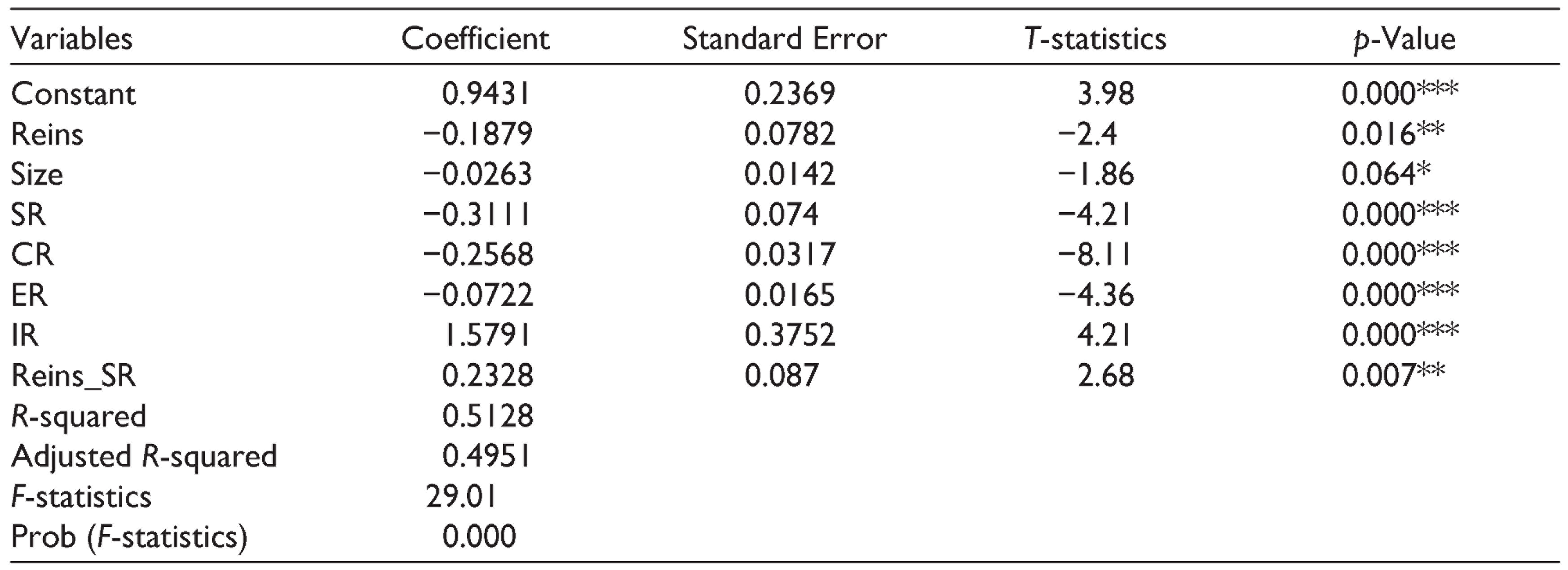

An insurance company’s financial performance and healthiness can be enhanced by the company’s ability to repay all financial obligations in the short, medium and long term and also the amount of reinsurance required to support payments when they fall due. Consequently, reinsurance and solvency were interacted to examine their combined effect on profitability. It can be seen from the regression results in Table 4 that both solvency ratio (SR) and reinsurance (Reins) had a negative influence on the profitability of non-life insurance companies.

From Table 4, it was seen that the combined effect of reinsurance and solvency (Reins_SR) had a significant positive impact on ROA though both reinsurance and solvency ratio variables had a negative effect on ROA. A company’s ability to repay all financial obligations, should all its assets be sold, and be able to continue operations as a viable firm after a financial adversity, coupled with a better reinsurance decision, enables the primary insurance company to spread the risk of loss assumed. The ability to settle financial obligation impacts a company’s ability to obtain loans and broadens its economic capacity to expand their market share and investment (Soye & Adeyemo, 2017).

Regression Results (Incorporating the Interaction Term Reins and SR)

Summary and Conclusion

The study examined the effect of reinsurance on the financial performance of the non-life insurance companies in Ghana. Using a panel regression analysis, 20 companies were sampled over a period of 11 years (2008–2018). The results showed that reinsurance had no effect on the profitability of general insurance companies. However, the combined effect of solvency ratio and reinsurance had a positive effect on profitability. In addition, size, solvency ratio, combined ratio and exchange rate had a negative impact on the profitability of insurers. Moreover, interest rate had a significant positive effect on profitability.

The findings of this study contribute towards a better understanding that purchasing high levels of reinsurance alone does not affect the profitability of non-life insurance companies in Ghana which differed from the findings of Ma and Elango (2008), Soye and Adeyemo (2017) and other researchers. However, when these companies simultaneously increase their ability to repay long-term obligations as well as increase their purchase of reinsurance, it significantly impacts their profitability by enabling them to spread the risk of loss and obtain loans and broadens their economic capacity to expand market share and investment. Moreover, borrowing from external sources or issue of shares and other equities to meet their long-term obligations may reduce the company’s ability to absorb unexpected shocks and pay claims promptly and thus affects their profitability. Again, an insurer’s inefficiency in its underwriting decisions and operations can negatively affect its profitability. Furthermore, when interest rate increases, investment income increases which may increase profitability. Lastly, though insurers with large size can exercise their market power, take advantages of economies of scale and gain access to investment opportunities, the growth in the size of the company may lead to inefficiencies which could reduce insurers’ profitability.

Recommendations

Managers of non-life insurance companies in Ghana should increase their ability to repay all financial obligations in the short, medium and long term in combination with reinsurance. This will enable insurers to stabilize growth, earn profits and meet their obligations to policyholders in a timely fashion.

Other risk management methods such as risk reduction and prevention, coinsurance, insurance securitization and derivatives could be explored by non-life insurers to reduce their financial exposures and boost their underwriting capacity.

National Insurance Commission (NIC) should constantly regulate the capital requirement, assets and reserves of non-life insurers to ensure that they will be capable of paying claims to policyholders and maintain solvency.

Managers of non-life insurance companies should ensure optimal allocation of their capital in assets and other investments that will generate high income and increase their financial value.

The government and other policymakers should put in measures to stabilize the cedi against the dollar to protect the profits of insurance companies. One way of doing this is to ensure continuous education of the citizens to depend on locally produced goods as opposed to foreign made ones which is currently the case.

Future research could consider other relevant variables which might explain the remaining variances of profitability of non-life insurance companies. Moreover, the study focused on the non-life insurance sector. The life insurance sector is a fast-growing sector of the insurance market in Ghana. Consequently, a study that assesses the effect of reinsurance on the life sector and the entire insurance sector will be enriching for insurers and policymakers.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received financial support from the Research and Conferences Committee is highly acknowledged by the lead author.