Abstract

This article highlights some of Sraffa’s main contributions to the methodology of economics. It argues that Sraffa rejected counterfactual reasoning and hence the ‘marginal method’ of analysis. Sraffa’s theory is built solely on factual and objective information and hence it removes psychology from economics as well. Sraffa’s theory shows that considerations of demand and the condition of equilibrium of demand and supply are irrelevant to a logical theory of prices. The article goes on to show how Sraffa’s novel approach to economic theory was able to expose the logical errors of ‘marginal method’ in the Austrian and Neo-classical theories of distribution. Finally, it also raises some questions for Sraffa’s theory that need to be resolved.

Introduction

In this article I try to delineate and highlight some of Piero Sraffa’s methodological innovations in economic theory, particularly in the area of value and distribution. I shall argue that among his main contributions to economic theory are: (a) a complete removal of psychology from economics and (b) a rejection of counterfactual reasoning. 2 The hallmark of the method of orthodox economics is its reasoning on the basis of counterfactuals, that is, the notional changes at the ‘margin’ of a system in equilibrium. Sraffa’s theory, on the other hand, is built on purely factual and objective information that completely refrains from counterfactual reasoning. In some sense Sraffa’s theory is geometrical in nature as opposed to the mechanical nature of the orthodox theory.

In the following section, I present my interpretation of Sraffa’s basic theoretical model. Further, its methodological aspects are highlighted. After that its critical implications for the orthodox ‘demand and supply’ theory of value and distribution is noted. The last section discusses the generality of Sraffa’s results and some possible direction of its future development.

Sraffa’s Theoretical Model

Let us suppose we observe a simple three commodity economy after a cycle of production (a ‘harvest’ or an annual cycle with equal rotation time for all the industries), which is given by:

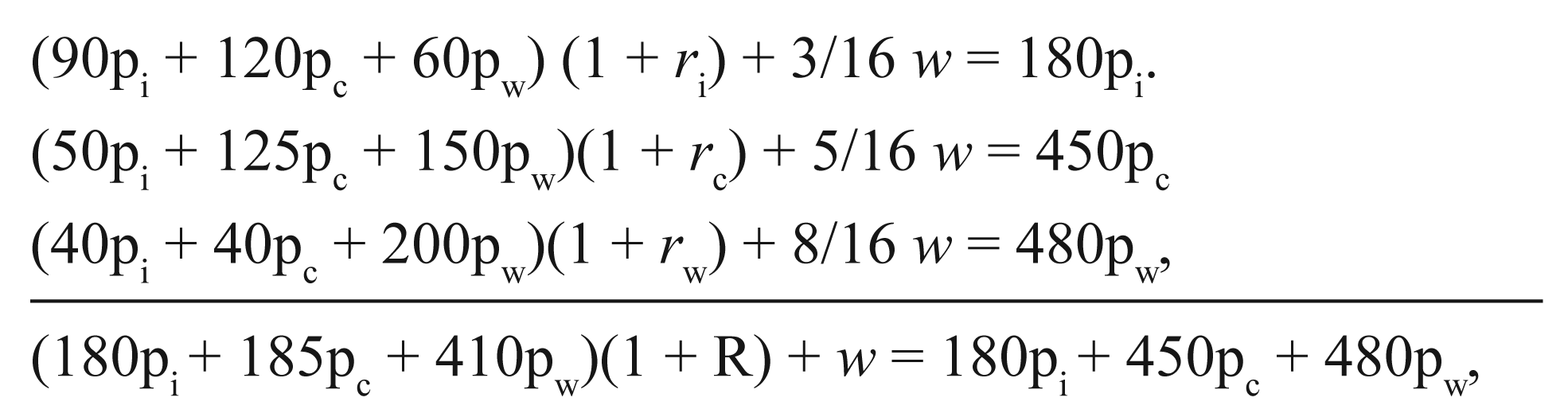

90t. iron + 120t. coal + 60qr. wheat + 3/16 labour → 180t. iron, 50t. iron + 125t. coal + 150qr. wheat + 5/16 labour → 450t. coal, and 40t. iron + 40t. coal + 200qr. wheat + 8/16 labour → 480qr. wheat.

At the time of observation, all the gross outputs of iron, coal and wheat are concentrated in separate hands. It is clear that the industries must exchange their commodities with each other before they could renew another cycle of production. The question is: what would be the exchange rates among these three commodities? To find the answer to our question, we must convert our description of production into equations of costs and income, which is given by:

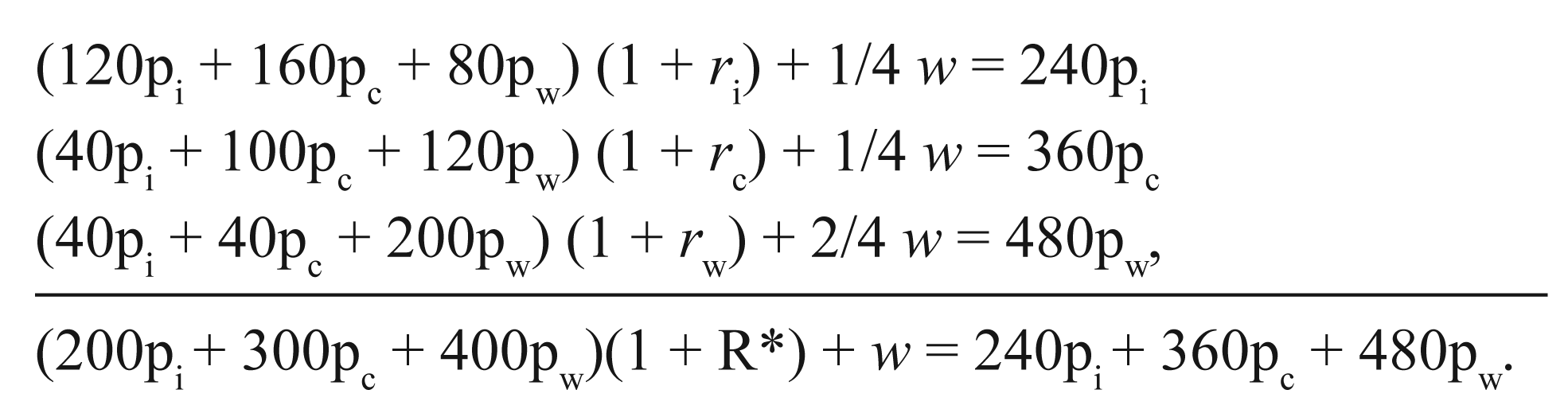

where pi, pc and pw represent prices or exchange ratios of the respective commodities, ri, rc and rw represent the rates of profits in the three industries respectively, R represents the average rate of profits of the system and w represents the remuneration of the workers or wages per unit of their labour. Clearly, the equation system (I) cannot be solved for p’s as it has more unknowns than independent equations. Let us now multiply the second equation of the system by 3/5 and the third equation of the system by 3/4 and then rescale all the equations such that the total labour used by the system remains equal to 1. This gives us an equation system (II), which is equivalent to equation system (I):

In this case, if we put the value of w = 0, then the value of R* is known since (40pi+ 60pc + 80pw)/(200pi+ 300pc + 400pw) = 1/5 or 20 per cent irrespective of what r’s and p’s happen to be. This is not a statistical average but an ‘algebraic result’ derived from the equation system (I). Before going any further, I must point out that the equation system (II), which is Sraffa’s ‘Standard system’, is unique to equation system (I), if all p’s must be positive (see Sraffa, 1960, ch. V). Hence, an algebraic solution of equation system (I) that guarantees all p’s to be positive must result in a unique R = R*. It should also be noted that the derivation of equation system (II) from equation system (I) does not assume that the actual system (I) can in reality be converted to equation system (II). The equation system (II) is simply an imaginary system, algebraically derived from equation system (I). No real change in the actual system (I) is contemplated and hence no question of returns to scale, constant or otherwise, arises.

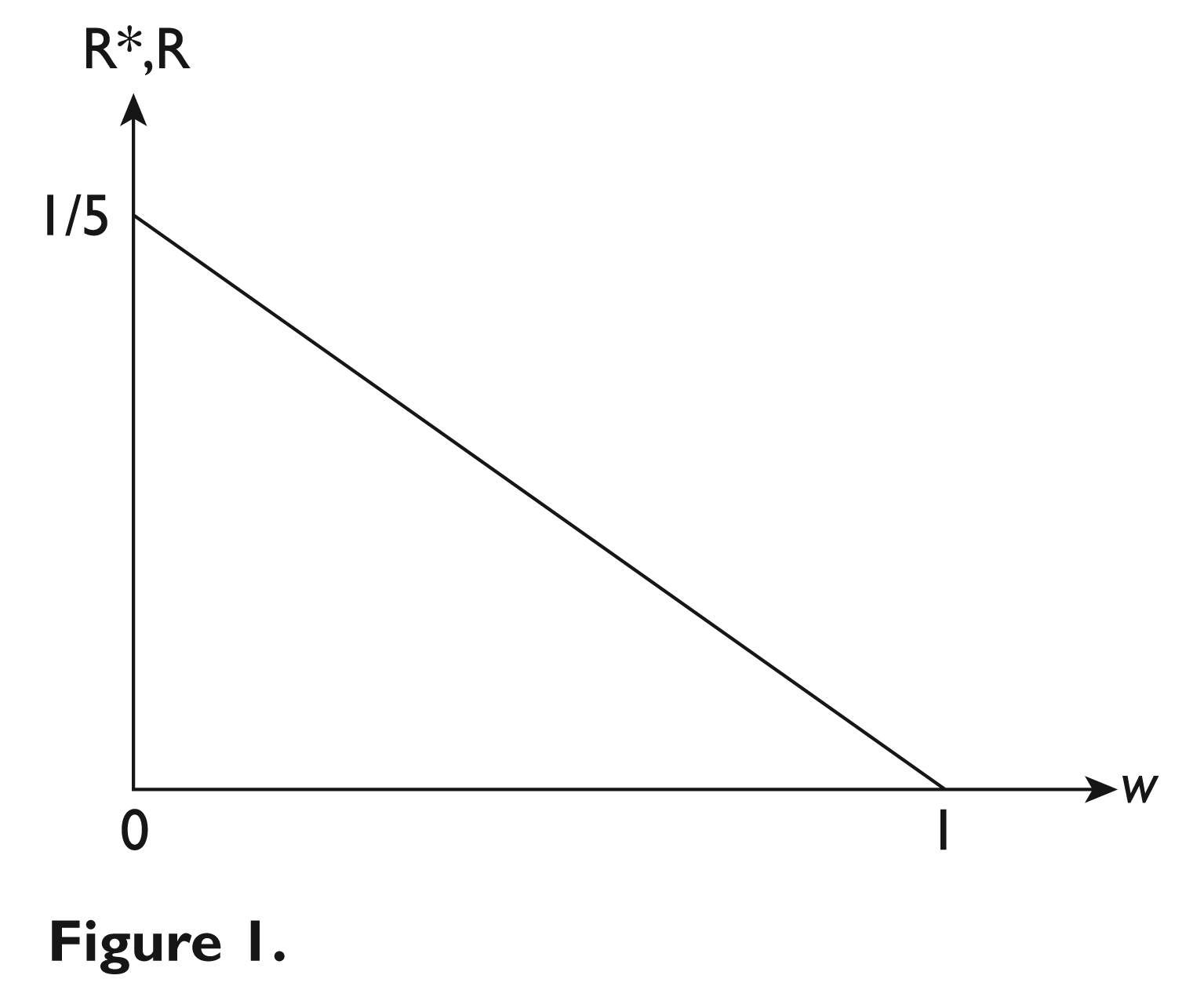

Let us put (40pi+ 60pc + 80pw) = 1; that is, make the Standard net output to be the money-commodity by which the price ratios and wages are measured. Now, wages can move from 0 to 1. We assume that wages are given from outside of the equation system. For any level of wages given in the Standard net product, we can derive the average rate of profits R* in the system without the knowledge of prices, since it does not disturb the proportionality of the commodity mix of aggregate inputs and total profits. Hence, we can derive a straight line negative relationship between R* and w without any knowledge of p’s, and if the Standard net output is used for measuring wages and prices in the observed system (I) as well then the identical relationship must also hold for R and w. This relationship is given by: R = Rmax(1 − w), where Rmax is the value of R when w is zero. In other words, given the industry wise physical data of inputs and outputs, if one distributive variable is fixed from outside then the other is fixed too.

Given that R* is the algebraic average of the equation system (I), it follows that R* must be the algebraic average of all the rescaled systems derived from system (I or II), which is possible if and only if all the r’s are equal. Given this result, for any given value of w we can now solve for the uniform rate of profits r and the three p’s of the system (I) by adding the normalization equation (40pi+ 60pc + 80pw) = 1. The result can be generalized to n commodities.

Some Methodological Aspects of Sraffa’s Theory

Can the statistical average rate of profits of system (I) be different from its ‘algebraic average’? In other words, can prices be such that the industrial rates of profits turn out to be unequal, and therefore, the average rate of profits turns out to be different from R? Let us suppose, we begin with an equilibrium situation with uniform rate of profits in all industries, which is equal to zero. We also assume that the demand functions of all the capitalists and the workers are identical. Now, suppose a capitalist government wins the election and orders that half of all the wages must be transferred to the capitalists. If this transfer takes place within every firm then industry-wise the capitalists of the industries that use relatively more ‘capital’ (indirect labour) per worker would receive relatively lower rates of profits compared to the capitalists of the industries that use relatively less ‘capital’ per worker. Now, let us assume that prices are determined by the conditions of demand and supply in the market and not by the solution of our equation system (I). Since we have assumed that the demand functions of the capitalists are the same as the workers, this transfer of income would not affect the demand and supply conditions in the market for the three commodities and therefore not affect the prices. Let us say this set of prices is given by

Now, if prices must be determined on the basis of given distribution of income from outside then the set of prices must change such that it is compatible with equal rate of profits given by R, which in this case is 10 per cent. Let us say, this set of prices is given by

This brings two important facts to light: (a) if prices are determined by demand and supply conditions in the market then the distribution of income cannot be taken from outside the system of price determination or independently of prices; (b) if the distribution of income is given from outside the system of price determination then prices can be determined irrespective of the condition of equilibrium of demand and supply in the market.

In our example, the set of prices given by

This argument, however, implicitly assumes that constant returns to scale prevail in all the industries, otherwise the changes in supplies would change the equations along with it; and that the rescaling of the industries during the adjustment process does not change the total demand for labour in the system, otherwise its effect on wages and consequently the rate of profits and prices cannot be ignored. Furthermore, the argument also implicitly assumes that there are no substitutes to the given techniques of production, otherwise if substitutes to the given techniques existed then switches in techniques by industries due to changes in their rates of profits and therefore changes in the equations cannot be ruled out.

Given all these restrictions, is the classical proposition valid? When one thinks of it in terms of a single commodity then the proposition appears to be highly persuasive. However, in a system of large number of interconnected industries, the matter turns out to be quite complicated. Recently, Dupertuis and Sinha (2009a) have shown that in a system of three or more basic goods, that is, goods that are directly or indirectly used as inputs in the production of all goods, the mathematical probability of the system converging to the centre of gravitation from its neighbourhood by following the classical gravitation mechanism is zero. One important reason why one should not expect classical gravitation mechanism to converge to the price set

Now, if our interpretation of Sraffa’s main contribution is accepted then the problem of convergence to the point of equilibrium becomes irrelevant. There is no need to make any assumption regarding returns to scale or any kind of movement of the given system. The condition of equal rate of profits in the equation system is simply a consequence of the assumption that the distribution of income between the two classes is given from outside the system of price determination. It rejects the idea that prices carry signals that cause agents to behave in such a manner that the market adjusts to an equilibrium. In Sraffa’s case, prices have only one job to do and that is to account for the given distribution of income. In other words, there is no causal mechanism (as in mechanics) of price determination; the relationship of prices with the given wages and the algebraic average rate of profits is logical (as in geometry) such as a relationship of one angle with the other two angles of a triangle—in some sense Sraffa’s proposition is similar to Einstein’s theory of gravitation, which is geometrical, as opposed to Newton’s theory of gravitation, which is mechanical. 3 The irrelevancy of the condition of equilibrium of demand and supply also makes any consideration of demand or psychological or subjective motives of agents irrelevant to the determination of prices in Sraffa’s theory. The theory is based solely on the objective data.

This appears to be counter-intuitive. Don’t we consistently observe that a sudden rise in demand for certain things raises their prices? Since Sraffa did not answer such questions, I will here try to think aloud on this issue. First of all, we should keep in mind that in our equation system the industries directly exchange with each other at one point of time. In real world there exists a class of traders, particularly for consumer’s goods, who buy from the industries and supplies these goods over the year to the consumers. In this case when demand for a particular commodity suddenly rises prompting the traders to increase its price then that represents a transfer of income from wages of the workers and/or profits of the capitalists to the traders. This sort of pricing would be akin to pricing of goods that are fixed in supply. But the important point to keep in mind is that here we are dealing with transfer of already produced income and not the generation of new income through price mechanism. Second, let us take our example of system (I) with R = 10 per cent. Clearly, in our case the demands and supplies are in disequilibrium, however, exchange between the industries must take place at the set of prices given by

A Critique of the Post-classical Theory of Distribution

Until now we have emphasized that Sraffa’s results are valid in the case when either wages (or alternatively the rate of profits) is taken from outside the system of price determination. On the other hand, the Post-classical (Austrian and Neo-classical) demand and supply theory of price determination maintains that the distribution of income is an outcome of pricing of commodities and hence cannot be taken as given from outside the system of price determination. One of the contributions of Sraffa’s theory is to show that the Post-classical theory of income distribution is logically flawed. Sraffa concentrated his critique on their theories of returns to capital or the determination of the rate of interest/profit.

In the tradition of Jevons, Menger, Böhm-Bawerk and Wicksell, ‘capital’ could be measured by the ‘period of production’ and given a system in stationary state a marginal stretching of the period of production implies increase in the demand for labour and thus a rise in wages and a fall in the rate of interest. Wicksell had shown that the production function with constant returns to scale is a logical necessity of marginal productivity theory of distribution, otherwise income distribution determined by the marginal productivity will not be able to exhaust total income in the system. In the Clarkian tradition (Clark, [1899] 1965), on the other hand, ‘capital’ is measured by monetary-value of capital goods—‘capital’, however, is supposed to be an abstract entity that changes its form with every change in its size to suit appropriately the given size of labour. Again in this case as well, given the stationary state, a marginal rise in the size of capital implies less labour per unit of capital, that is, increase in the intensity of capital; therefore, capital’s average and hence marginal productivity falls and simultaneously marginal productivity of labour rises for the same reason. Thus, in both the cases a rise in capital/output ratio must be associated with a rise in wages and a fall in the rate of interest/profit.

Now, imagine that either our equation system (I) or (II) is in a stationary state. The constancy of R*max or Rmax with respect to changes in w clearly shows that in a stationary state output/capital ratio remains constant with respect to changes in wages and the rate of profits, which contradicts the prediction of the marginal productivity theory. There are several reasons why the marginal productivity theory turns out to be wrong. In Jevons–Wicksell tradition ‘capital’ is measured by ‘period of production’, this assumes that all the capital-goods can be ultimately reduced to wages in a long chain of dated labour. Sraffa’s example shows that as long as there are material capital goods used in production there always will remain some commodity residue no matter how far back in time we go; and the problem cannot be solved by going back and back till the commodity residue becomes ‘negligible’, since at what stage the commodity residue becomes negligible depends upon the rate of interest itself. For example, if the rate of interest is at its maximum value, that is, R = Rmax, then the commodity residue will never become negligible and it will become negligible with shorter and shorter periods with the fall in R.

In this context, Sraffa (1960, ch. VI) showed that when we reduce price of a commodity to its dated quantity of labour such as: Law + La1w(1 + r) + … + Lanw(1 + r) n + … = Apa, where symbols have their usual meaning [Sraffa uses r for our R, given all r’s are equal, our R is always equal to r. Sraffa reserves the symbol R for our Rmax], A is the total quantity of good ‘a’ produced and 1 to n are the dates going back in production cycles, then for any labour term of the period n a rise in the rate of profits would pull its value in two directions. This can be seen by replacing w with w = 1 – r/R [given, r = R(1 – w), where R is the maximum rate of profits and r is the uniform industrial rate of profits] in the nth term of the equation: Lan(1 − r/R)(1 + r) n . Clearly with the rise in r, the term in the first parenthesis falls whereas the term in the second parenthesis rises. In an example, Sraffa showed that if two commodities ‘a’ and ‘b’ are produced by equal amount of labour but dispersed at different dates, for example, they differ in three of their labour terms while identical in all the others: ‘a’ has 20 units of labour in excess of ‘b’ for n = 8 whereas ‘b’ has 19 units of labour in excess for n = 0 and 1 unit of labour in excess for n = 25. Now the difference between their prices in terms of the Standard commodity is given by: pa – pb = 20w(1 + r)8 – {19w + w(1 + r)25}. The price of ‘a’ rises relatively to ‘b’ with a rise of r from 0 to 9 per cent, then it falls between 9 per cent and 22 per cent and then again rises from 22 per cent to 25 per cent, for R = 25 per cent. Such movements in prices clearly show that no measure of capital independently of the rate of profits is possible.

This shows that the conceptualization of the economic problem as a linear narrative, that is, that the final purpose of any production is consumption, which defines the end point, and that production of any consumption good can be traced back to a point where labouring activity is unassisted by any produced means of production, which identifies a well-defined beginning, is false. Sraffa’s system, on the other hand, has a circular narrative, it begins with what exists and ask the question: what conditions are required for its reproduction.

Both in the Jevonsonian as well as the Clarkian traditions the marginal productivity of capital, which is supposed to determine the equilibrium interest rate, is associated with the condition of stationary state. In other words, the idea of change is inextricably associated with the idea of no-change, which introduces the fundamental contradiction in their argument. All that the ‘marginal method’ does is to dodge the problem rather than solve it. In the Jevonsonian tradition the marginal change in capital is measured on the continuous scale of time, which ignores its relation to physical techniques of production, but it still has to further ignore the effect of the changes in the rates of interest and wages on prices to ensure its result—this was noticed by Wicksell himself (1901 [1934]).

In his review of Dr Gustaf Akerman’s Realkapital und Kapitalzins written in 1923, Wicksell (1934) realized that the proposition that marginal productivity of capital is positive can be proved only on the assumption that an increase in wages always brings an increase in the period of production, given all the functions are continuous. Now, this is the consequence of marginal productivity theory. But Wicksell (1934, Appendix 2, pp. 293–296) shows that to prove the presupposition of the theory one needs to assume the consequence of the presupposition. In other words, the whole argument goes in a circle. Wicksell shows that if this assumption is not maintained then it cannot a priori be ruled out that changes in wages and changes in the ‘period of production’ can have opposite sings. Let us suppose that output ‘p’ is a function of capital ‘t’, that is, period of production, and the number of current labour, ‘h’, that is, p = f(t, h). Moreover, p = w + t(dp/dt); where w is the total wage bill given h and dp/dt is the marginal productivity of capital, which must be equal to the rate of interest in equilibrium. Taking h to be fixed, we can write the production function as p = f(t), where f’(t) > 0 and f”(t) < 0. Now, d(w/p)/dt = p(dw/dt) – w(dp/dt). Since w = p – t(dp/dt), we have dw/dt = −t(d2p/dt2). Therefore, d(w/p)/dt = −pt(d2p/dt2) + t(dp/dt)2 – p(dp/dt). Clearly the first two terms on the RHS of the equation are positive but the last term is negative. Hence the sign of d(w/p)/dt cannot be determined a priori unless more information about the production function is available. In other words, a logical possibility of d(w/p)/dt < 0 cannot be ruled out. From this it follows that wages and the period of production are not uniquely determined by each other and that wages may have two or more values for the same value of capital and vice versa. Although Wicksell’s original argument was made in the context of Akerman’s case of fixed capital and its life-time, Uhr (1962) translated it into the case of pure circulating capital and called this result the ‘Wicksell effect’.

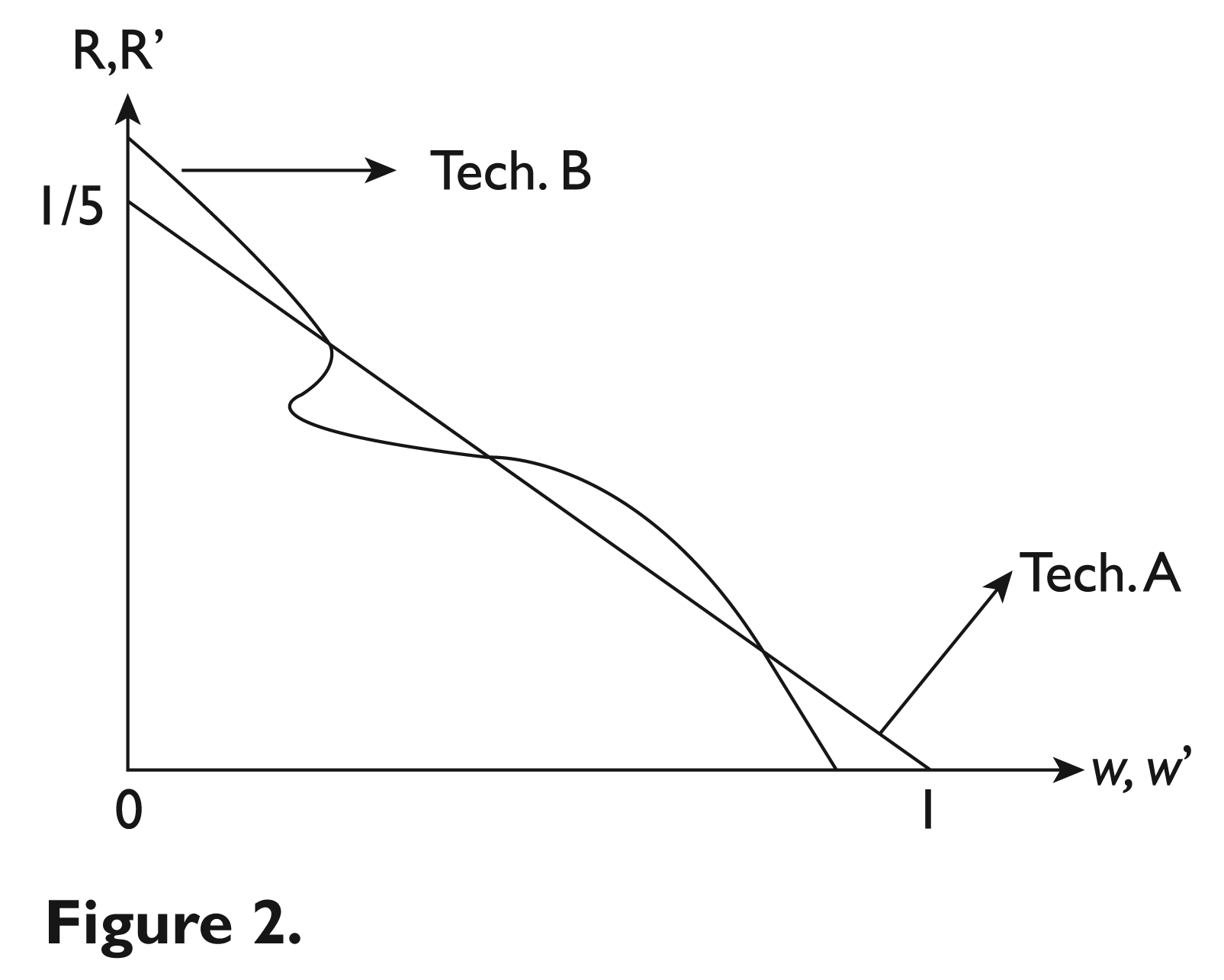

In the Clarkian tradition the marginal change in ‘capital’ is associated with an implicit change in technique of production but here too its impact on prices is ignored. However, once the real change is allowed then the comparison between ‘before’ and ‘after’ the change can only be between two stationary states (leaving aside the dynamic problem of crossing from one stationary state to another) and not within the same stationary state. Thus what it compares is difference between two adjacent stationary states and not change. In this case, Sraffa showed that if a given gross output can be produced by more than one technique then if a rise in wages leads to a switch from technique A to technique B then a further rise in wages may lead to a re-switch from technique B to technique A and there can be several such re-switching, which implies that techniques cannot be defined in terms of ‘capital intensity’ independently of the rate of interest. This is because given our straight line w-R relation for technique A, if we introduce another w’-R’ relation for technique B then this relationship must be non-linear as our measuring unit, the Standard commodity for technique A, is just an arbitrary measuring unit for technique B and there is no a priori reason why the non-linear w’-R’ curve not cut the straight line w-R curve more than once.

The modern Neo-classical theorists have conceded to Sraffa-critique of the marginal productivity theory of capital as an explanation of the rate of interest (see Symposium, 1966). In the inter-temporal general equilibrium version a la Arrow and Debreu (1954) every commodity has its ‘own rate of return’, which depends on the inter-temporal utility functions of the agents and need not be equal for all commodities in the equilibrium condition. Hahn (1982) has made a counteroffensive on this basis that Sraffa’s case is a very special case of stationary state where input prices are assumed to be equal to output prices, implying that all ‘own rates of interest’ are equal. Sinha and Dupertuis (2009) and Sinha (2010) have shown that Sraffa’s equations cannot be translated directly into inter-temporal general equilibrium equations. It can be done only on the assumption that ‘own rates of interest’ are equal. The problem with Hahn’s position becomes clear when we look at Sraffa’s Standard system (equation system II). In this case, for every given w, R* is determined by physical data irrespective of prices. Now, if we take different prices for inputs and outputs then the rate of profits derived on price basis would contradict the physical rate of profits, which shows the inherent contradiction in the attempt to translate Sraffa’s equations into inter-temporal general equilibrium equations.

The fact that the orthodox economic theory does not have a good explanation of distribution of income has been accepted by none other than the two leading lights of orthodox economics of the second half of the twentieth century, Paul Samuelson and Kenneth Arrow:

But I fear that when the economic theorist turns to the general problem of wage determination and labour economics, his voice becomes muted and his speech halting. If he is honest with himself, he must confess to a tremendous amount of uncertainty and self-doubt concerning even the most basic and elementary parts of the subject. (Samuelson 1956, p. 312) In principle, we ask about allocation among individuals or among owners of different factors of production, but it must be recognised that distribut-ional questions are not asked very loudly or answered very well. (Arrow 1991, p. 74)

Generality of Sraffa’s Results

How general is Sraffa’s results? (a) In our example, all the three industries are basics, in the sense that they inter directly or indirectly in the production of all the commodities (in our example, all of them enter directly). Does the result hold when we add pure consumption goods that do not enter either directly or indirectly into the production of all the commodities? The answer is: yes. It is because once the ‘algebraic average’ rate of profits of the system is determined then adding any non-basic good does not affect the rate of profits as it only brings one additional equation with one additional unknown, that is, its price. However, in a highly unlikely case when a non-basic uses itself in its production to such a high degree that its rate of profit cannot admit the rate of the basic good system then the rate of profits would not be equalized for this particular commodity; for example, let us suppose the rate of profits of the basic goods system happens to be 15 per cent and there is a non-basic commodity, say ‘beans’, that requires 100 units of beans to produce 110 units of beans then obviously its rate of profits cannot be more than 10 per cent. (b) In our example, the net output of the system is well defined in physical terms but what about the case when an economy is going through technological change such that the industries producing means of production for the old technology is shrinking? In this case, some of these means of production may be in less amount on the RHS of the equation than the LHS, that is, the net output cannot be determined in physical terms. Even in such cases, if the number of equations is large enough then we can always rescale the system by increasing the relative weightage of the shrinking industries to make the system produce physical net output. (c) Our example is a case of industries that produce single commodities and there is no fixed capital, but in reality there are large amounts of fixed capital invested in industries and many of them produce joint-products. Sraffa (1960, chs VII–X) has extended his system to accommodate joint-production. Actually, he views joint-production as the general case where fixed capital is treated as joint-products. An Italian mathematician Carlo Manara (1980 [1968]) had come up with some examples that suggested that in the general case of joint production a Standard commodity might not exist in the realm of real numbers. Recently, Dupertuis and Sinha (2009b) have shown that this problem arose because Sraffa’s system was erroneously interpreted to conform to the equilibrium of demand and supply. If our interpretation of Sraffa is accepted then this problem can be resolved. (d) Can Sraffa’s system take into account rent on the use of fixed natural resources as means of production? The answer is: yes, as Sraffa has shown in Ch. XI of his book. (e) In our example, we have assumed single rotation period and annual production cycle for all the commodities. In general one should expect varying rotation periods for different commodities, for example, industrial cycles are almost continuous compared to agricultural cycles. Introduction of varying rotation periods would definitely complicate the mathematics considerably but there seems to be no reason as to why the results would not hold.

Now we take up some of the problems with Sraffa’s theory that I think need further consideration. In Sraffa’s theory we take the Standard commodity as the money-commodity. But the real world ‘money’ cannot be the Standard commodity because the real world is constantly changing in terms of its equations and total utilization of labour. Hence the Standard commodity must also be changing but we cannot expect money-commodity to keep changing continuously. Thus we need some method of translating given money wages into its equivalent in Standard commodity at any given point of time. But this is not possible. One could, of course, replace the normalization equation given by Standard net product = 1 by simply invoking the logical result, in Sraffa’s symbols, r = R(1 – w) or 1/w = R/(R – r), but still it requires that w must be reckoned in terms of the Standard commodity. This has prompted Sraffa to argue that instead of taking wages as given from outside, one may take the rate of profits, r, as given from outside the equation system. Since r is a percentage, it does not require a Standard commodity for its measure. Thus if we invoke r = R(1 − w) in the system of equations and take r as given from outside, we would determine p’s and w in terms of the Standard commodity without having to know the Standard commodity.

The problem with this way out is that in real world labour is not homogeneous. In the first case, the heterogeneous labour could be homogenized in a simple manner. Let us suppose the total wage bill for the whole economy is US$100 and that industry a uses 5 units of labour and pays US$60 in wages whereas industry b uses 5 units of labour and pays US$40 in wages. If we define wages for homogeneous labour equal to US$8 per unit of labour then all we have to do is to count 5 units of labour of industry a to be equivalent to 7.5 units of homogeneous labour. But this exercise cannot be done if wages are unknown.

Sraffa’s proposition that distribution of income is given independently of prices opens up economic theory to history, sociology and politics. The determination of wages may require us to take into account not only history and culture of a society but also the relative strength of the working class vis-à-vis the capitalist class as well as the political set-up in which the class struggle takes place—demand and supply of labour can only be one element in determining such strength. Similarly, the rate of interest may be determined by the interaction of the central bank, the commercial banks and the stock exchange. At this time, however, we do not have a developed theory that takes account of these elements in a coherent manner. But the greatest challenge would be to integrate the theory of wages and the theory of interest/profits. They cannot be developed independently of each other as Sraffa’s theory requires that if one is fixed from outside then the other is fixed too.

The other major issue that the followers of Sraffa must deal with is, how to understand economic growth in terms of a non-causal theory.