Abstract

Individuals frequently face financial constraints, which can significantly influence their cognitive and consumption decisions. Prior research has mainly investigated how financial constraints influence personal consumption decisions about buying alone and using alone (i.e., solo consumption), but less on consumption decisions with others about buying together and using together (i.e., joint consumption). This research addresses this gap by examining the effect of financial constraints on consumption decisions (joint consumption vs. solo consumption). Across three formal and three supplemental studies (N = 2186), we found that financial constraints significantly increased individuals’ preferences for joint consumption over solo consumption, with this effect being mediated by self-esteem. Furthermore, perceived economic mobility moderates the effect of financial constraints on preferences for consumption decisions (joint consumption vs. solo consumption). Specifically, for individuals with low perceived economic mobility, financial constraints lead to a preference for joint consumption (vs. solo consumption), whereas for individuals with high perceived economic mobility, financial constraints lead to a preference for solo consumption (vs. joint consumption). Our findings extend research on financial constraints, self-esteem, and consumption decisions.

Keywords

Introduction

Financial constraints are a prevalent aspect of daily life, shaping behaviors and limiting spending (Tully et al., 2015). Globally, many individuals experience financial constraints (Paley et al., 2019). In China, the 2024 Chinese Household Wealth Change Trends report reveals that financial stress affects numerous households, with the Total Household Debt Index reaching 103.7, reflecting elevated debt levels (Finance, 2025). Similarly, in the United States, the 2024 Planning and Progress Study finds that one-third of surveyed adults feel financially insecure, marking the highest rate since 2012 (Adamczyk, 2024). Notably, even high-income earners can experience subjective financial constraints, as only 13% of millionaires consider themselves wealthy (Fan et al., 2020). These findings highlight the ubiquity of financial constraints across income levels.

Previous research indicates that financial constraints influence consumption behaviors, such as a preference for scarce products (Sharma & Alter, 2012) or items associated with luck (Wang et al., 2021). Financially constrained individuals also tend to favor high-calorie foods (Briers & Laporte, 2013) and material possessions (Tully et al., 2015). However, these studies predominantly focus on solo consumption, with limited attention to joint consumption. This research investigates how financial constraints shape preferences for joint consumption versus solo consumption, positing that financially constrained individuals engage in compensatory behaviors to restore self-esteem by fostering social support and group identity. Furthermore, perceived economic mobility moderates these effects: individuals with low perceived economic mobility are more likely to favor joint consumption, while those with high perceived economic mobility are more likely to favor solo consumption. These findings offer new theoretical insights into consumer behavior and practical implications for businesses to design products and services that address the social needs of financially constrained consumers.

Theoretical framework

Financial constraints

Financial constraints refer to a subjective psychological state in which individuals perceive their financial situation as limiting their desired consumption, even when their objective financial resources may be substantial (Malika et al., 2022; Tully et al., 2015). This perception emerges when anticipated consumption exceeds affordability, highlighting a disconnect between financial resources and consumption expectations (Fan et al., 2020). For example, one in four millionaires in the United States does not feel wealthy and often experiences financial constraints (Malika et al., 2022). In addition, financial constraints impose significant psychological burdens, influencing emotions, cognition, and behaviors. Financial constraints can trigger negative emotions (Paley et al., 2019; Xiao, Tang, et al., 2011), insecurity (Fan et al., 2020), heightened uncertainty (Vander Elst et al., 2014), diminishing well-being, and eroding a sense of control (Dias et al., 2022). This highlights the psychological burden that financial constraints impose, irrespective of objective financial status.

In response to financial constraints, individuals often adapt their consumption behaviors in line with compensatory theories (Xiao, Ford, & Kim, 2011; Malika et al., 2022; see Online Appendix A: “Positioning of Present Research in the Financial Constraints Literature” for more details). For example, constrained individuals may seek scarce products to alleviate negative emotions (Sharma & Alter, 2012), purchase lottery tickets or items associated with good fortune (Haisley et al., 2008; Wang et al., 2021), and prefer high-calorie foods or material possessions that restore feelings of security (Briers & Laporte, 2013; Tully et al., 2015). Moreover, financial constraints heighten attention to social connections, with working-class individuals, in particular, exhibiting stronger interdependence and prioritizing social goals over solo consumption (Cavanaugh, 2016; Li et al., 2019; Malika et al., 2022). While prior research has predominantly examined compensatory consumption and the pursuit of belonging in solo consumption contexts, the role of financial constraints in shaping preferences for joint consumption has received relatively little attention. To address this gap, this research investigates how financial constraints influence preferences for joint versus solo consumption.

Joint consumption versus solo consumption

Joint consumption refers to multiple consumers sharing the consumption process, encompassing two dimensions: “buying together” and “using together” (Etkin, 2016; Kim et al., 2023; Liu & Min, 2020). “Buying together” involves shared contributions toward the monetary and non-monetary costs of purchasing goods or services. These include splitting the financial expense (e.g., the cost of a product or service) and sharing non-monetary efforts (e.g., collaboratively making decisions, investing time, and expending energy to select the appropriate goods; Kim et al., 2023). Meanwhile, “using together” entails shared ownership or joint utilization of the purchased goods or services. For instance, in the context of restaurant consumption, multiple individuals may collectively decide on a restaurant and share the cost (i.e., buying together) before jointly enjoying the food and services provided (i.e., using together). In contrast, solo consumption refers to individual decision-making and independent use of goods or services (Khoa & Chan, 2024). For example, a person dining alone in a restaurant independently makes the decision, consumes the meal, and bears the entire cost (Ran et al., 2018).

Prior research has explored the factors that influence consumption decisions (joint vs. solo) from two perspectives (see Online Appendix B: “Positioning of Present Research in Solo and Joint Consumption Literature” for more details). On the one hand, individual traits influence preferences. For example, women (Ran et al., 2018), individuals with interdependent self-construal (Malika et al., 2022; Markus & Kitayama, 1991), and those with lower self-esteem (Shin et al., 2018) exhibit stronger preferences for joint consumption, driven by a need for belonging. On the other hand, social relationships play a critical role. For example, familiarity, loyalty (Cavanaugh, 2016; Etkin, 2016), and group identity (Liu et al., 2019) significantly drive joint consumption (Belk, 2010; Cavanaugh, 2016; Liu et al., 2019). However, while existing studies have primarily focused on individual traits and social relationships, the role of financial constraints in shaping consumption decisions remains underexplored. This research aims to address this gap by investigating the impact of financial constraints on joint versus solo consumption decisions.

Financial constraints and joint consumption

Financial constraints, primarily stemming from the scarcity of financial resources, can diminish an individual’s self-esteem. On the one hand, individuals facing financial constraints may perceive themselves as being at a relative disadvantage, which can lead to negative emotions and diminished self-esteem (Sharma & Alter, 2012). Similarly, individuals with lower income levels may develop stronger materialistic aspirations, and when these aspirations are unmet, they may experience further reductions in self-esteem (Chaplin et al., 2014). On the other hand, in modern society, an individual’s social status is often linked to their financial resources, with financial resources serving as a key indicator of social standing (Hamilton et al., 2019). Thus, perceived decreases in social status due to financial constraints can also lead to diminished self-esteem. Self-esteem, referring to an individual’s self-evaluation (e.g., “Right now, I am satisfied with myself.”), is a multifaceted construct influenced by various factors, including financial status (Jami et al., 2021; Jiang et al., 2024).

To mitigate the negative effects of declining self-esteem, individuals may restore self-esteem through consumer behavior. On the one hand, Self-Consistency Theory suggests that individuals strive for consistency between their behavior and self-concept, aiming to maintain a positive self-concept (Stone, 2003). When self-esteem declines, this positive self-concept is threatened (Liu et al., 2013), prompting individuals to seek ways to restore it. For instance, individuals facing setbacks may pursue recognition from others by acquiring new skills (Thulien et al., 2021; Van der Veken et al., 2020). On the other hand, the Hierarchical Theory of Needs suggests that when self-esteem decreases, individuals seek emotional support and social recognition (Lonnqvist et al., 2009). For example, individuals who experience social exclusion may take steps to restore harmony within their relationships (Lee & Shrum, 2012; Thulien et al., 2021). Thus, individuals with low self-esteem may strengthen social connections and fulfil emotional needs to restore self-esteem. Given that individual often use consumption behavior to enhance self-esteem (Stuppy et al., 2020) and that financial constraints can diminish self-esteem, financially constrained individuals may engage in compensatory consumption to restore their sense of self-esteem.

Compared to solo consumption, financially constrained individuals may prefer joint consumption to enhance self-esteem. On the one hand, joint consumption allows individuals to actively participate in consumption decisions (Wortman & Brehm, 1975), thus providing them with a sense of agency and control, which in turn boosts self-esteem (Su et al., 2017). On the other hand, joint consumption fulfils individuals’ social and practical needs, such as companionship and enjoyment, which can evoke positive emotions (Hart & Dale, 2014). For example, talking to friends during joint consumption can positively affect an individual’s emotions (Borges et al., 2010). These positive emotions, arising from spending time with peers during consumption, can further enhance self-esteem (Kernis et al., 1993). Additionally, individuals with low self-esteem may prefer to participate in joint consumption with multiple people, as this can foster a sense of belonging to a collective and enhance their self-esteem (Bradshaw, 1998; Shin et al., 2018; Stinson et al., 2015). In contrast, solo consumption, which lacks social interaction, does not provide emotional support. Individuals engaging in solo consumption may feel isolated or excluded (Courtet & Olie, 2019), which can reduce their self-esteem (Thulien et al., 2021). Therefore, for individuals facing financial constraints, solo consumption may fail to meet the need to restore self-esteem, whereas joint consumption may fulfil these needs more effectively. In other words, financially constrained individuals may be more likely to choose joint consumption rather than solo consumption to restore self-esteem.

In summary, financial constraints may diminish individuals’ self-esteem. In response to this, financially constrained individuals, driven by the desire to restore their self-esteem, are likely to prefer joint consumption over solo consumption. Therefore, we propose the following hypothesis:

Compared to non-financially constrained individuals, financially constrained individuals prefer joint consumption (vs. solo consumption).

Self-esteem mediates the effect of financial constraints on joint consumption (vs. solo consumption).

Perceived economic mobility

Perceived economic mobility refers to the belief that societal structures facilitate individuals’ efforts to improve their economic status (Yoon & Kim, 2016; Zhao et al., 2023). This belief plays a significant role in shaping individuals' psychological states, cognition, and consumer behavior (Heiserman et al., 2020; Yoon & Kim, 2016, 2018). Based on opportunities for advancement through effort, skill, or education, perceived economic mobility can be categorized as high or low (Yoon & Kim, 2016). Individuals with high perceived economic mobility believe that they can improve their financial situation and secure economic benefits (Kwon & Yi, 2019). For instance, individuals with high perceived economic mobility may anticipate achieving adequate future financial benefits through diverse avenues, increasing their likelihood of engaging in charitable activities (Zhao et al., 2023). In contrast, individuals with low perceived economic mobility believe that changing an undesirable financial situation is difficult (Kwon & Yi, 2019). They tend to be pessimistic about future financial improvements, which influences their spending patterns (Lee & Chen, 2022). Thus, perceived economic mobility plays an important role in shaping individuals’ attitudes and behaviors toward financial problems.

For individuals with low perceived economic mobility, financial constraints may diminish their self-esteem, leading to a preference for joint consumption. Individuals with low perceived economic mobility may believe that financial status is inherent and that individual effort will not improve their financial standing (Fan et al., 2020; Vander Elst et al., 2014). In addition, they may lack confidence in their future financial situation and believe that financial distress will persist (Kwon & Yi, 2019; Martín & García-Perez, 2023). In other words, they remain pessimistic about their financial future. Thus, individuals with low perceived economic mobility may experience diminished self-esteem due to financial constraints and may seek emotional satisfaction and social support through joint consumption. Individuals with low self-esteem are more likely to engage in social activities with multiple people (Shin et al., 2018), as these interactions help restore self-esteem through social support (Liu et al., 2019). Joint consumption can provide these individuals with a sense of importance and belonging in social relationships, which enhances their self-esteem (Liu et al., 2019), thus increasing self-esteem. In contrast, solo consumption, lacking opportunities for interaction, does not fulfil the need for social connection or self-esteem restoration (Shin et al., 2018). Thus, financially constrained individuals with low perceived economic mobility are more likely to prefer joint consumption to restore their self-esteem.

In contrast, individuals with high perceived economic mobility generally maintain higher self-esteem and are less affected by financial constraints. These individuals believe that they can achieve considerable future financial gains through their efforts (Kwon & Yi, 2019), which fosters a more optimistic outlook on the future (Jabbari et al., 2024). Individuals with a positive outlook on the future tend to believe that financial constraints can be overcome and have confidence in their financial prospects (Garbinsky et al., 2021). This optimism and confidence can enhance their self-esteem (Bosson et al., 2003). Thus, individuals with high perceived economic mobility are less likely to lose hope when facing financial constraints, and they generally maintain higher levels of self-esteem. Moreover, individuals with high self-esteem are more inclined to maintain an independent and autonomous lifestyle, preferring to consume alone (Shin et al., 2018), and may be reluctant to share resources with others (Philp et al., 2018). Additionally, high-power individuals may have positive experiences dining alone (Hwang et al., 2018). Therefore, individuals with high perceived economic mobility are likely to maintain their self-esteem despite financial constraints and may prefer solo consumption as a reflection of their independence.

In summary, individuals with low perceived economic mobility may experience diminished self-esteem due to financial constraints, leading them to prefer joint consumption for social support and belonging. In contrast, individuals with high perceived economic mobility generally maintain higher self-esteem and are less affected by financial constraints, leading them to prefer solo consumption. Therefore, we hypothesize:

Perceived economic mobility moderates the effect of financial constraints on preferences for joint consumption (vs. solo consumption).

For individuals with low perceived economic mobility, financial constraints lead to a preference for joint consumption (vs. solo consumption).

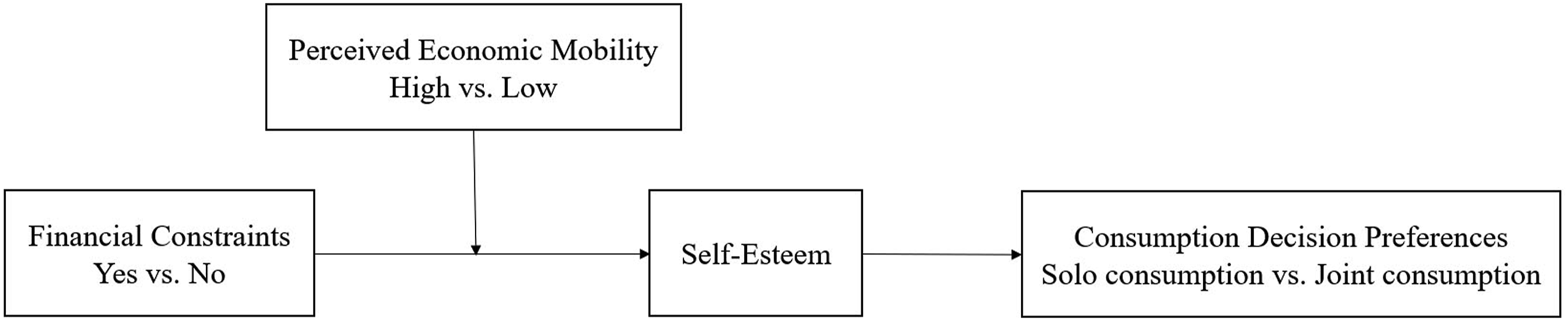

For individuals with high perceived economic mobility, financial constraints lead to a preference for solo consumption (vs. joint consumption). The conceptual model for the hypotheses is shown below (see Figure 1):

Theoretical model.

Study 1

Study 1 aimed to verify that financial constraints lead individuals to prefer joint consumption (vs. solo consumption). Study 1 manipulated financial constraints to explore their causal effect on consumption decision preferences. Previous research has suggested that financial constraints may reduce an individual’s sense of control (Zhang et al., 2023), influence individuals’ perceived price for consumption (Lamberton & Rose, 2012), and their emotions (Dias et al., 2022), Study 1 included direct measures of these variables to rule out these alternative explanations.

Design and participants

Study 1 lasted 20 days and was conducted from 1 to 20 February 2024. To earn course credit, 250 students (Mage = 21.34 years, SD = 2.31; 62.00% female; see Online Table F1 in Appendix F) from a university in Southern China participated in this study. All participants completed the attention testing questions. Thus, no participants were excluded from Study 1. They were randomly assigned to one of two conditions (financial constraint: yes vs. no).

Procedure

First, referring to Dias et al. (2022), we instructed all participants to write down an item they had purchased in the past few weeks costing between $50 and $1,000. This preliminary step aimed to standardize the purchases described across experimental conditions, minimizing systematic variation. In addition, we selected this price range to ensure comparability of purchases and to encourage participants to document meaningful purchases. Subsequently, participants were randomly allocated to one of two conditions. In the financial constraints condition, participants wrote about factors contributing to their financial constraints. In the non-financial constraints condition, participants listed three verifiable facts they knew to be true. Then, referring to Paley et al. (2019), participants completed a manipulation check (“To what extent do you feel financially constrained?”; 1 = not at all, 7 = very much).

Next, participants imagined they were going to a fast-food restaurant (e.g., Online Figure C1 in Appendix C) near their school for lunch and wrote down the name of the fast-food restaurant. Participants then indicated whether they preferred to go alone or with a classmate (0 = go alone, 1 = go with a classmate).

Finally, according to Li (2019), participants also completed the sense of control scale (1 = not at all likely, 7 = very likely; see Online Appendix L). In addition, according to Cutright et al. (2011), participants rated their mood on a four-item scale (see Online Appendix L), with higher scores indicating more positive mood. Participants also indicated the perceived price of the two consumption decisions using a three-point scale: (a) “solo consumption is cheaper (1)”. (b) “both are similar in price (2)”. and (c) “joint consumption is cheaper (3)”. Participants also completed demographic questions.

Results

Manipulation checks

Participants in the financial constraint condition indicated feeling more financially constrained than did participants in the non-financial constraint condition (Mfinancial constraint = 5.22, SD = 1.05 vs. Mnon-financial constraint = 4.32, SD = 1.60; F (1, 248) = 27.82, p < .001), which confirmed that the financial constraint manipulation was successful.

Consumption decision choice

The results of the Chi-Square analysis indicate that financial constraints have a significant effect on participants’ consumption decision choices (χ2 (1, 248) = 11.51, p = .002). In the financial constraint condition, participants were more likely to choose joint consumption (63.49%), while in the non-financial constraint condition, participants were more likely to choose solo consumption (56.45%), which supported H1.

Alternative explanations

An analysis of variance (ANOVA) showed that financial constraints had no significant effects on participants’ sense of control (Mfinancial constraint = 4.91, SD = 1.10 vs. Mnon-financial constraint = 5.15, SD = 1.06; F (1,248) = 2.91, p = .089), mood (Mfinancial constraint = 5.03, SD = 1.24 vs. Mnon-financial constraint = 5.20, SD = 1.23; F (1,248) = 1.10, p = .295), and perceived price (Mfinancial constraint = 2.65, SD = 0.65 vs. Mnon-financial constraint = 2.66, SD = 0.62; F (1,248) = 0.02, p = .896). In addition, to rule out alternative explanations for the influence of a sense of control, emotions, and perceived value in the effect of financial constraints on consumption decision, we conducted a mediation analysis (5,000 bootstraps; PROCESS Model 4; Hayes, 2017). The analysis revealed that the mediating effect of sense of control (Indirect effect = 0.0188, SE = 0.0354, 95% CI = [−0.0409, 0.1048]), mood (Indirect effect = 0.0158, SE = 0.0293, 95% CI = [−0.0266, 0.0916]), and perceived price (Indirect effect = 0.0026, SE = 0.0263, 95% CI = [−0.0523, 0.0653]) were not significant.

Discussion

Study 1 demonstrated a causal relationship between financial constraints and joint consumption (vs. solo consumption), showing that financial constraints increased consumers’ intention to engage in joint consumption rather than solo consumption, thus supporting H1 (In Study A of Online Appendix I, we explored the correlation between financial constraints and joint consumption.). Additionally, Study 1 ruled out mood, perceived price, and sense of control as alternative explanations. Study 1 still had some limitations. Study 1 used functional dietary consumption decision as stimuli for joint consumption. Thus, Study 2 used entertainment consumption decision (i.e., film) as a stimulus to enhance the external validity of the findings. In addition, Study 1 used a consumption scenario in which costs could be shared (i.e. restaurant consumption), and Study 2 used a consumption scenario in which costs could not be shared (i.e. film) to exclude the price factor.

Study 2

Study 2 aimed to verify the mediating role of self-esteem in the effect of financial constraints on consumption decision preferences (joint consumption vs. solo consumption). This study differed from Study 1 in four ways. First, Study 1 asked participants to recall past purchases to activate financial constraints, whereas Study 2 asked participants to think about future purchases. Second, to enhance the external validity of the studies, we used film (entertainment consumption) as stimuli rather than the dietary consumption decisions of Study 1. Third, to rule out the possibility that financially constrained individuals in Study 1 could choose joint consumption that can be cost-shared because they are seeking a cheaper product, we chose film consumption that cannot be cost-shared. Fourth, we measured communal norms to exclude potential interference.

Design and participants

Study 2 lasted 21 days and was conducted between 25 March and 14 April 2024. We recruited 337 participants from Credamo from Southeast China to complete this survey in exchange for a small monetary reward. Five participants did not complete the attention test. Thus, the final sample comprised 332 participants (Mage = 28.66 years, SD = 8.10; 56.27% female; see Online Table F2 in Appendix F). They were randomly assigned to one of four conditions: 2 (financial constraints: yes vs. no) × 2 (consumption decision: joint consumption vs. solo consumption).

Procedure

Drawing on Paley et al. (2019), participants first named a discretionary item costing between $50 and $1000 that they planned to purchase in the next few weeks. Similar to Study 1, participants in the financial constraints condition wrote about factors contributing to their financial constraints, while those in the control condition listed three verifiable facts, they knew to be true. Afterwards, participants completed the same financial constraints manipulation checks as in Study 1.

Next, participants imagined browsing social media platforms on their mobile phones and encountering a film of interest that was about to be released (see Online Figure D1 in Appendix D). In the joint consumption condition, participants indicated how likely they were to “Go to the cinema with friends to see this film” (1 = very unlikely, 7 = very likely; see Online Figure D2 in Appendix D). In the solo consumption condition, participants indicated how likely they were to “Go to the cinema alone to watch this film” (1 = very unlikely, 7 = very likely; see Online Figure D3 in Appendix D).

Finally, referring to Stets and Burke (2014), participants completed measures of self-esteem, reporting the extent to which they agreed with statements such as “I feel that I have a number of good qualities” and “l usually feel good about myself” (1 = not at all, 7 = very much; see Online Appendix L). Participants also reported their favorability (1 = very unfavorable, 7 = very favorable) and familiarity (1 = very unfamiliar, 7 = very familiar) with the film. Additionally, participants completed measures of communal norms (Malika et al., 2022), reporting the extent to which they agreed with statements (1 = not at all, 7 = very much; see Online Appendix L). Participants also provided demographic information.

Results

Manipulation check

Participants in the financial constraints condition reported higher levels of financial constraints compared to those in the non-financial constraints condition (Mfinancial constraint = 5.08, SD = 1.25 vs. Mnon-financial constraints = 4.59, SD = 1.38; F (1, 330) = 11.62, p = .001), indicating that the financial constraints manipulation was effective.

Consumption intentions

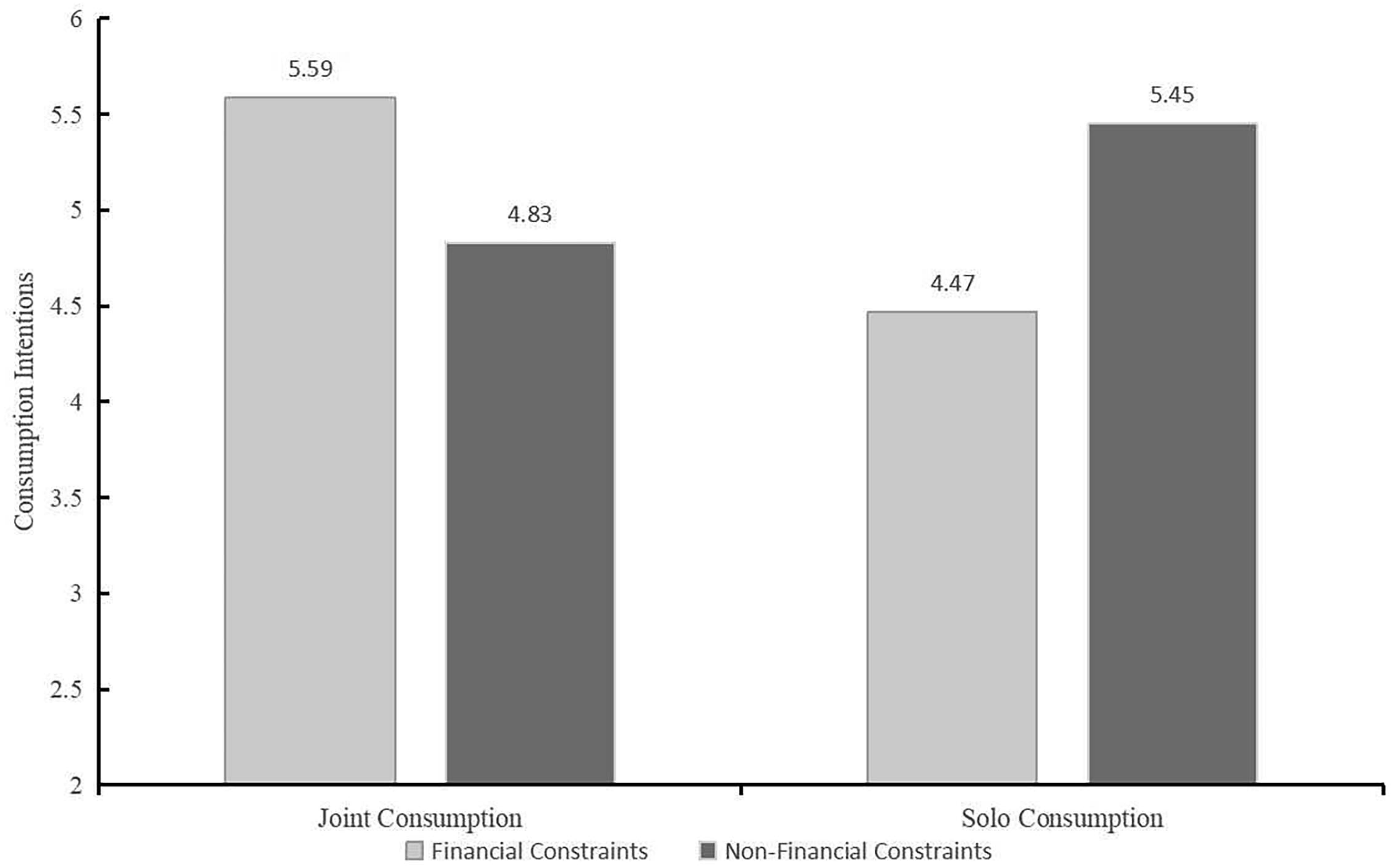

A two-way analysis of variance (ANOVA) revealed a significant interaction between financial constraints and consumption intentions (F (1, 328) = 26.23, p < .001; see Figure 2). Specifically, for joint consumption, participants in the financial constraints condition exhibited higher consumption intentions compared to participants in the non-financial constraints condition (Mfinancial constraints = 5.59, SD = 1.37 vs. Mnon-financial constraints = 4.83, SD = 1.78; F (1, 161) = 9.52, p = .02). In contrast, for solo consumption, participants in the non-financial constraints condition exhibited higher consumption intentions compared to participants in the financial constraints condition (Mfinancial constraints = 4.47, SD = 1.74 vs. Mnon-financial constraints = 5.45, SD = 1.26; F (1, 167) = 17.53, p < .001), which supported H1. Effect of financial constraints on consumption intentions.

Mediation analysis

A one-way analysis of variance (ANOVA) showed that financial constraints significantly reduced participants’ self-esteem (Mfinancial constraints = 4.07, SD = 1.34 vs. Mnon-financial constraints = 4.64, SD = 1.11; F (1, 330) = 18.05, p < .001). Subsequently, to test whether financial constraints affected participants’ preference for joint consumption through self-esteem, we conducted a mediation analysis (5000 bootstraps; PROCESS model 4; Hayes, 2017) with financial constraints as the independent variable, joint consumption intentions as the dependent variable, and self-esteem as the mediator variable. The analysis found that self-esteem had a significant mediating effect (Indirect effect = 0.3074, SE = 0.1197, 95% CI = [0.0922, 0.5643]), supporting H2.

Alternative explanations

We conducted a one-way analysis of variance (ANOVA) with financial constraints as the independent variable and communal norms as the dependent variable. The results showed that the effect of financial constraints on communal norms was not significant (Mfinancial constraints = 5.55, SD = 0.97 vs. Mnon-financial constraints = 5.44, SD = 1.02; F (1, 330) = 0.95, p = .329). Furthermore, when conducting a mediation analysis (5000 bootstraps; PROCESS model 4; Hayes, 2017) with financial constraints as the independent variable, joint consumption intentions as the dependent variable, and communal norms as the mediator variable, the results showed a non-significant mediation effect for communal norms (Indirect effect = 0.1208, SE = 0.0933, 95% CI = [-0.0329, 0.3329]). Moreover, we observed no significant differences in familiarity (Mfinancial constraints = 4.85, SD = 1.41 vs. Mnon-financial constraints = 4.67, SD = 1.84; F (1, 330) = 1.01, p = .317) and favorability (Mfinancial constraints = 5.15, SD = 1.66 vs. Mnon-financial constraints = 4.98, SD = 1.75; F (1, 330) = 0.86, p = .355), which did not affect the results.

Discussion

Study 2 found that financial constraints caused participants to prefer joint consumption (vs. solo consumption), supporting H1. Furthermore, the results showed that self-esteem mediates the effect of financial constraints on joint consumption (vs. solo consumption), supporting H2. Study 2 also ruled out communal norms, familiarity, and favorability as alternative explanations. In addition, we also excluded alternative explanations such as price sensitivity and loss aversion (see Study B in Online Appendix H for details). We replicated the results of Study 2 in a supplemental study using a moderated approach to validate the mediating effect (see Study C in Online Appendix K for details).

Study 1 used dietary consumption decisions, and Study 2 used an entertainment consumption decision. Study 3 used a leisure consumption decision as a stimulus to further enhance the external validity of the findings. In Study 3, we refined our experiment by further validating the moderating role of perceived economic mobility.

Study 3

The purpose of Study 3 is to demonstrate that perceived economic mobility moderates the effect of financial constraints on consumption decision preferences (joint consumption vs. solo consumption). Specifically, for individuals with low perceived economic mobility, financial constraints increase their preferences for joint consumption. In contrast, for individuals with high perceived economic mobility, financial constraints increase their preferences for solo consumption. In addition, in Study 5, we chose the leisure consumption decision (tourism) as the stimulus to further enhance the external validity of the studies.

Design and participants

Study 3 lasted 30 days and took place between 1 and 30 June 2024. We recruited 790 participants through Credamo to complete the study with a small monetary reward. Three participants failed the attention testing questions. Thus, the final sample consisted of 758 participants (Mage = 29.22 years, SD = 7.46; 63.72% female; see Online Table F3 in Appendix F). They were randomly assigned to one of eight conditions: 2 (financial constraints: yes vs. no) × 2 (perceived economic mobility: high vs. low) × 2 (consumption decision: joint consumption vs. solo consumption).

Procedure

First, following Yoon and Kim (2016), all participants were informed about the opportunity to improve their economic situation. They were then randomly assigned to two conditions and completed respective writing tasks. Participants in the high perceived economic mobility condition wrote three reasons supporting the idea, while those in the low perceived economic mobility condition wrote three reasons opposing it. Then, participants completed the question items measuring perceived economic mobility: “It is possible for anyone, regardless of the conditions of his/her birth, to acquire great wealth.” “Society provides enough opportunities for those who are motivated to advance.”, and “Everyone has a fair chance to move up the economic ladder.” (1 = not at all, 7 = very much; see Online Appendix L).

Next, participants completed the same financial constraints manipulation and measurement of financial constraints questions as in Study 1. Afterwards, according to Malika et al. (2022), participants were asked to complete a task that required them to indicate their incentive-compatible consumption intentions. Specifically, they were asked to choose a consumption option that they could actually receive. They were told that all participants would enter a lottery, and two of the winners would receive the gift card that they had selected. In the joint consumption condition, participants saw $30 worth of gift cards, including two tickets. In the solo consumption condition, participants were presented with a gift card worth $30, which included one ticket and a lunch. These gift cards were chosen based on pre-tests indicating that the two gift cards were comparable in terms of good feelings and expected happiness (see Online Appendix H). Finally, consumers indicated consumption intentions (1 = very unwilling, 7 = very willing) and provided demographic information.

Results

Manipulation check

Participants in the financial constraints (vs. non-financial constraints) condition reported higher levels of financial constraints (Mfinancial constraint = 5.01, SD = 1.26 vs. Mnon-financial constraints = 4.70, SD = 1.43; F (1, 756) = 9.93, p = .002), confirming the success of financial constraints manipulation. In addition, participants in the high (vs. low) perceived economic mobility condition reported higher levels of perceived economic mobility (Mhigh perceived economic mobility = 5.15, SD = 1.11 vs. Mlow perceived economic mobility = 3.83, SD = 1.41; F (1, 756) = 202.68, p < .001), indicating the success of perceived economic mobility manipulation.

Consumption intentions

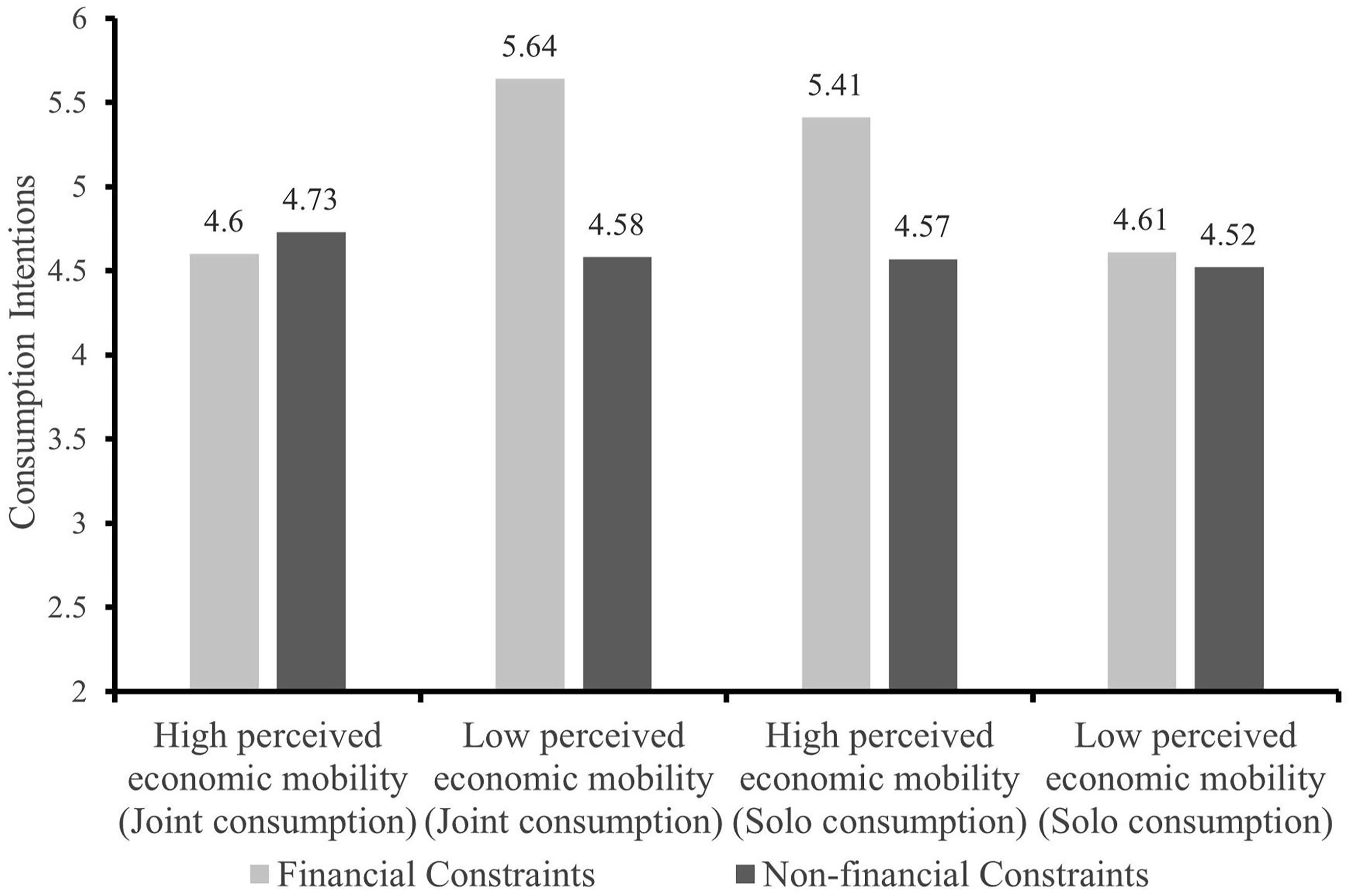

A three-factor analysis of variance in consumption intentions revealed a significant three-way interaction (F (1, 750) = 29.00, p < .001; see Figure 3). In addition, the effects of financial constraints on consumption intentions are significant (F (1, 756) = 25.26, p < .001), whereas none of the other effects were significant. Next, we conducted a series of planned comparisons. In addition, we found that financial constraints and perceived economic mobility significantly affect consumption intentions for joint consumption (F (1, 376) = 13.39, p < .001) and solo consumption (F (1, 374) = 15.79, p < .001). Specifically, for participants in the low perceived economic mobility condition, consumption intentions for joint consumption were significantly higher in the financial constraint condition compared to the non-financial constraints condition (Mfinancial constraint = 5.64, SD = 0.93 vs. Mnon-financial constraints = 4.58, SD = 1.47; F (1, 187) = 35.89, p < .001), whereas consumption intentions for joint consumption were no significant difference between the two conditions (Mfinancial constraint = 4.61, SD = 1.47 vs. Mnon-financial constraints = 4.52, SD = 1.25; F (1, 189) = 0.205, p = .651). In contrast, consumption intentions for solo consumption were significantly higher in the non-financial constraint condition compared to the financial constraints condition (Mfinancial constraint = 5.41, SD = 0.85 vs. Mnon-financial constraints = 4.57, SD = 1.27; F (1, 184) = 30.23, p < .001), whereas consumption intentions for joint consumption were no significant difference between the two conditions (Mfinancial constraint = 4.60, SD = 1.33 vs. Mnon-financial constraints = 4.73, SD = 1.32; F (1, 190) = 0.497, p = .482). Effect of financial constraints and type of consumption decision on consumption intentions.

Discussion

Study 3 found that perceived economic mobility moderates the effect of financial constraints on consumption decision preferences (joint consumption vs. solo consumption), with support for H3. Specifically, for individuals with low economic mobility, financial constraints lead to a preference for joint consumption. In contrast, for individuals with high economic mobility, financial constraints lead to a preference for solo consumption. In addition, Study 3 used leisure consumption (tourism) as a stimulus to test our hypotheses and further improve the external validity of studies.

General discussion

Financial constraints are common in daily life and significantly influence consumption behavior and decisions. While prior research has focused on how financial constraints shape solo consumption, such as preferences for scarce products, lucky products, and high-calorie foods (Haisley et al., 2008; Sharma & Alter, 2012; Wang et al., 2021), this research examines their impact on consumption decisions involving others (i.e., joint consumption). Across three formal studies (Studies 1–3) and three supplemental studies (Studies A-C), we find that financial constraints increase individuals’ preferences for joint consumption (vs. solo consumption), with self-esteem playing a mediating role. In addition, we find that perceived economic mobility moderates the effect of financial constraints on joint consumption (vs. solo consumption). Specifically, for individuals with low perceived economic mobility, financial constraints lead to a preference for joint consumption, whereas for individuals with high perceived economic mobility, financial constraints lead to a preference for solo consumption. To ensure robustness, the studies examine diverse consumption contexts (see Online Appendix M), including hedonic dietary consumption (leisure restaurant, Study A), functional dietary consumption (fast-food, Study 1), entertainment (movies, Study 2), self-improvement (fitness, Study 2), and leisure (tourism, Study 3), across varying relationships such as family members, classmates, friends, and peers. The research uses different dependent measures, such as preferences, actual choices, consumption intentions, and incentive-compatible decisions, while ruling out alternative explanations, including the sense of control, emotions, perceived price, communal norms, price sensitivity, and loss aversion. These findings fill a gap in understanding how financial constraints influence joint versus solo consumption decisions.

Theoretical contributions

This research contributes to the literature in three ways. First, this research presents the effect of financial constraints on preferences for different consumption decisions, which extends research on consumption decisions to the economic dimension. Financial constraints are prevalent across both high-income and low-income groups (Fan et al., 2020). Existing research has mainly focused on the effect of financial constraints on personal consumption decisions. For example, financially constrained individuals purchase scarce products (Sharma & Alter, 2012), lucky products (Wang et al., 2021), and high-calorie foods (Briers & Laporte, 2013) for themselves. However, existing research has less focused on the effect of financial constraints on individuals’ consumption decisions with others. Therefore, this research fills this gap by exploring the effect of financial constraints on consumption decisions (joint consumption vs. solo consumption). By doing so, this research adds an important new dimension to the literature on consumption decisions by demonstrating that financial constraints have an impact on enhancing consumers' intentions to engage in joint consumption (vs. solo consumption). This distinction provides a more nuanced understanding of consumer behavior under financial constraints and highlights the importance of considering the financial context in consumption decision research.

Second, this research enriches the understanding of how financial constraints affect joint consumption. Previous research has mainly examined financial constraints through direct resolution strategies, emphasizing increased financial vigilance (Jones et al., 2015) and consideration of opportunity costs (Carvalho et al., 2016; Guo & Lamberton, 2021). Based on self-consistency theory and Maslow’s hierarchy of needs theory, this research suggests that financial constraints reduce individuals’ self-esteem, which creates a drive to restore self-esteem. This research shows that to mitigate the negative effects of lower self-esteem, individuals are more likely to engage in joint consumption (vs. solo consumption). By proposing and preliminarily validating this mechanism, our findings contribute to a deeper comprehension of consumer decision-making under financial constraints, offering a novel theoretical perspective in the field of consumption behavior research.

Finally, this research enriches comprehension of the effect of perceived economic mobility. Perceived economic mobility, rooted in an individual’s belief in achieving superior economic status through personal endeavor (Yoon & Kim, 2018), has been widely acknowledged for its influence on consumer behavior across various contexts. For instance, it has been linked to heightened willingness to donate (Zhao et al., 2023), propensity for aggressive behavior in pursuit of personal gain (Kwon & Yi, 2019), and moderation of impulsive spending among materialistic consumers (Yoon & Kim, 2016). In contrast to the existing literature, our research finds that perceived economic mobility is a key factor in the effect of financial constraints on consumption decisions. Specifically, we find that in a state of financial constraint, individuals with low perceived economic mobility prefer joint consumption (vs. solo consumption). In contrast, individuals with high perceived economic mobility prefer solo consumption (vs. joint consumption). This finding expands the scope of perceived economic mobility research and contributes novel insights to the literature.

Practical contributions

This research provides valuable insights into firm production and marketing. First, we suggest that managers should use different advertising and product supply strategies depending on whether individuals are financially constrained or not. On the one hand, in terms of advertising strategies, we recommend joint consumption with multiple consumers for financially constrained consumers. For example, advertisements that emphasize eating together (Studies 1 and A), going to the cinema together (Study 2), going to the gym together (Study C), and going on a trip together (Study 3) increase the intention of consumers to spend money in joint consumption. Similarly, Starbucks’ global advertising campaign showing how its shops promote relationships (Malika et al., 2022) may be particularly effective with financially constrained consumers. On the other hand, in terms of product supply, firms can develop different product marketing strategies for individuals with different financial situations. Before payday (Seligman et al., 2014), before repayment dates, or during significant events like the COVID-19 pandemic (Goldsmith et al., 2020), consumers may feel financially constrained. During economic downturns, direct price promotions such as price discounts and coupons make products cheaper, such as buy-one-get-one-free or second-half-price, more attractive. For example, Study B showed that in a situation of financial constraints, consumers would prefer a second half-price joint consumption, even if the price is the same for the joint consumption as for the solo consumption. In addition, during boom times, merchants can offer sophisticated and compact products, such as miniature sizes, which can better meet the individual needs of financially well-off consumers.

Second, given that self-esteem guides individual preferences for consumption decisions, it would be useful to incorporate self-esteem into marketing strategies. In terms of advertising strategy, highlight the sense of social identity or self-esteem that consumers gain from using a product or service. For example, promoting products or services that emphasize the social value of joint consumption, such as family and friend gathering scenarios, enhances consumers’ self-esteem through these shared experiences. In terms of promotional strategies, the high value and quality of the product or service are emphasized in pricing and promotional activities so that consumers feel that choosing the product is a recognition of their own value, thus enhancing self-esteem.

Finally, the findings emphasize that perceived economic mobility moderates the effect of financial constraints on joint consumption (vs. solo consumption) preferences. Perceived economic mobility is an actionable factor. Therefore, firms that encourage joint consumption can reduce consumers’ perceived economic mobility by emphasizing in their marketing messages that resources are limited, and competition is fierce and by using imagery such as “empty wallets” to evoke or enhance a sense of financial constraint, thereby effectively guiding consumers to choose products for joint consumption. In addition, firms that promote solo consumption can improve the perceived economic mobility of financially constrained consumers through advertising messages, such as “upwardly mobile people are more likely to succeed” and “everyone has a fair chance to make the class leap”, thus boosting consumers' self-esteem. These messages increase consumers’ self-esteem, which in turn increases their preference for solo consumption.

Limitations and future research

While this research provides theoretical insights and practical implications on the effect of financial constraints on consumers’ preference for joint consumption (vs. solo consumption), it acknowledges some limitations in its scope. The notion of consumer constraint encompasses not only tangible resource scarcities like food constraints and product constraints (Cannon et al., 2025), but also intangible constraints such as time limitations (Liu & Wang, 2011). This research focused exclusively on financial constraints, leaving open the question of whether intangible constraints similarly influence individual preferences for joint consumption. Future research could investigate the effects of various types of constraints on joint consumption.

In addition, our research has not fully addressed the cultural dimension, a key area for further study. Cultural contexts, particularly collectivism versus individualism, shape cognitive patterns and behaviors, with collectivists prioritizing social connections and individualists valuing independence (Hofstede et al., 2010; Minkov et al., 2013). For instance, individuals in collectivist cultures are more likely to prioritize social interactions and interpersonal connections, whereas those in individualist cultures tend to emphasize independence and self-reliance (Hofstede et al., 2010). Future research should explore how culture moderates the relationship between financial constraints and joint consumption to reveal cross-cultural differences. Finally, while the current research’s demographic data were limited to gender and age, key variables such as race, sexual orientation, and socioeconomic status were omitted. Future research should incorporate these factors to enhance the generalizability and transparency of the findings, and to facilitate a more comprehensive understanding of diverse consumer behaviors.

Supplemental Material

Supplemental Material - Being alone or together: How financially constrained individuals restore their self-esteem through consumption decisions

Supplemental Material for Being alone or together: How financially constrained individuals restore their self-esteem through consumption decisions by Shichang Liang, Jingyi Li, Tingting Zhang, Yizheng Zhou, Yanrong Hao, Yanru Lv and Lixiao Geng in Journal of Social and Personal Relationships.

Footnotes

Authors contribution

S.L. Conceptualization, Supervision, Methodology, Funding Acquisition. J.L. Data curation, Writing Original draft preparation. T.Z. Data curation, Investigation, Writing Original draft preparation. Y.Z. Visualization, Software, Validation. Y.H. Investigation, Software, Validation. Y.L. Investigation, Software, Validation. L.G. Project administration, Software, Validation.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study is supported by National Natural Science Foundation of China (Grant No. 72162002); the Natural Science Foundation of Guanxi Province of China (Grant No. 2025GXNSFAA069968); Key Research Base of Humanities and Social Sciences in Guangxi Universities and Guangxi Development Strategy Institute (Grant No. 2022GDSIYB10 and 2024GDSIYB02).

Ethical statement

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.