Abstract

This article examines the influence of cross-country differences on bank loan maturity for small and medium-sized enterprises (SMEs), using a sample of 3366 SMEs from 19 European countries. It analyses a country’s legal and institutional environment while controlling for banking structure, economic situation and firm-specific characteristics. The study finds that SMEs in countries that protect its creditors and enforce existing laws are more likely to obtain long-term bank debt. It also shows evidence that banks seem to rely more on the institutional environment when determining loan maturity for micro-firms than for medium-sized firms. Policymakers should take these findings into consideration when proposing policy changes that are likely to impact the legal or institutional environment. For example, policy changes that affect creditor protection may have a direct impact on SME lending, and thus have economic consequences.

Introduction

Variation in debt maturity across countries has received a great deal of attention in recent empirical research. One line of research shows that a better legal and institutional environment significantly improves the availability of long-term debt for medium-sized and large firms, both listed and unlisted (Fan et al., 2003; Giannetti, 2003; González and González, 2008; La Roca et al., 2010; Demirgüç-Kunt and Maksimovic, 1998, 1999; Qian and Strahan, 2007). In a related line of literature, the evidence indicates that debt financing contracts for smaller firms are more subject to the institutional environment than for larger firms, because small firms are financially more constrained and more dependent on domestic capital markets (mostly bank loans) when outside financing is needed (Beck et al., 2008; Giannetti, 2003; Jõeveer, 2005). One direct implication of these studies is that a better legal and institutional environment might lengthen bank loan maturity for SMEs, and that this association is size-dependent. However, we are not aware of a comprehensive study examining the impact of cross-country heterogeneity on bank loan maturity for European SMEs. This article attempts to specifically address this issue.

We examine how the legal and institutional environment affect SME bank loan maturity by analysing a unique sample of 3366 micro-enterprises and SMEs from 19 European countries. This is important because SMEs across developed European countries account for the largest proportion of firms, jobs and gross domestic product (GDP) (European Commission, 2010) and banks often use short-term loans as a contract tool to control the higher borrower risk associated with small firms, imposing a liquidity risk burden that limits the development of these firms (Diamond, 1991; Rajan, 1992). Hence, understanding the association between SME financing patterns and the institutional environment might help policymakers develop better policies that improve SMEs’ access to finance.

Our results show that cross-country differences significantly explain the bank loan maturity structure of SMEs. First, we provide insight on the effect that a country’s legal origin has on bank loan maturity for SMEs. The loan maturity of SMEs in countries under German civil law and Scandinavian civil law is significantly longer than for firms operating under English common law, while for firms in French civil law countries it is significantly shorter.

Next, we examine the country’s legal and institutional environment while controlling for the banking structure and the economic situation. Our results show that firms in countries with an environment that protects its creditor rights and enforce the existing laws, are more likely to obtain long-term bank debt. In addition, we find that the institutional environment is especially important for micro firms when obtaining long-term loans.

This knowledge seems especially important for European Union (EU) policymakers, such that if country-specific characteristics do influence SME loan structure and hence access to finance, the impact of policy changes could vary significantly for SMEs located in different countries across Europe.

The rest of the article proceeds as follows. The next section discusses the previous literature and provides the motivation for the study, then the data and method are presented. This is followed by the results, discussion and conclusion.

Theory and hypothesis development

Empirical research shows the existence of large variations in loan maturity across European countries. Much of the existing empirical research attempting to explain this variation has focused on firm specific characteristics and therefore, fails to capture the effects of institutional differences on financing decisions.1 The law and finance literature (La Porta et al., 1997, 1998; Levine, 1998) suggests that non-price terms of loan contracts, such as maturity, also may be influenced by differences in the legal system across countries. For example, in a legal system with rules that strongly protect creditor rights and mechanisms that rigorously enforce the law, lenders can control borrower risk more easily and reduce the expected loss in the event of default. The use of short-term loans as an instrument to control borrower risk is less likely in such an environment. This argument is in line with findings that large firms have better access to long-term financing in countries with a good functioning legal system and better institutions (Fan et al., 2003; González and González, 2008 Demirgüç-Kunt and Maksimovic, 1998, 1999; Qian and Strahan, 2007). Conversely, in countries with poor protection of creditor rights and inefficient law enforcement mechanisms, lenders are more likely to utilize contracting tools that do not rely on laws or institutions, such as loan maturity. Short-term loans compel banks to monitor the firm’s performance more frequently and, if necessary, vary the terms of the contracts or renounce the loan before losses have accumulated (Diamond, 1991; Rajan, 1992).

A number of recent studies suggest that contract terms for small firm financing, compared with large firm financing, are more dependent on country-specific determinants, such as the legal and institutional environment. Giannetti (2003) and Jõeveer (2005) report that corporate finance decisions for smaller firms are more subject to institutional constraints imposed by domestic markets, while Beck et al. (2008) find that protection of creditor rights increases bank financing of small firms significantly more than that of large firms. Berry et al.’s (2004) evidence shows that bank lending approaches are not uniform across several European countries, indicating the existence of ‘home country effects’.

Based on the above findings, this article attempts to provide some insight into the relationship between cross-country differences and bank loan maturity for SMEs. It does so by testing two hypotheses.

H1: While keeping constant the banking structure and the economic situation, SMEs in countries with a better legal and institutional environment are more likely to obtain long-term bank loans. This association is size-dependent. H2: The smallest firms in the sample, i.e. micro-firms, benefit the most from improvements in the legal and institutional environment.

We test these hypotheses using a unique sample of 3366 micro-enterprises and SMEs from 19 European countries.

Method

Data collection

The initial sample uses several data sources. First, country-level information was obtained from La Porta et al. (1998), the Conference on Bank Concentration and Competition, the United Nations Statistics Division, Heritage Foundation and the World Bank.

Second, firm-specific variables were obtained from the 2002 European Network for SME Research Survey on Small and Medium-Sized Enterprises, Observatory of European SMEs, provided by the EIM Business and Policy Research in the Netherlands.2 From the 7669 checked and approved interviews that are available in the ENSR Survey 2002, there are 3366 observations that contain information about the bank loan maturity of individual firms.

Analysis

To assess the impact of country-specific characteristics on bank loan maturity we estimate logistic regressions in the following form:

Where i represents the ith firm in the sample; BLMi is bank loan maturity for firm i; LEi is a vector of legal environment variables; IEi represents the institutional environment variable economic freedom; CSCi is a vector of country-specific control variables; FSCi represents the set of firm-specific control variables and ϵ i is the residual.

Dependent variables

To create the dependent variable we utilize the ENSR Survey, in which managers are asked about the maturity of the largest loan that the firm has received from any bank during the last three years. The answers are categorized as follows: (1) less than one month; (2) one to six months; (3) six months to one year; (4) one to three years; (5) three to five years; and (6) five years or longer. Using these answers we built a dummy variable, bank loan maturity, which is given a value of one when maturity is longer than one year and zero otherwise.3

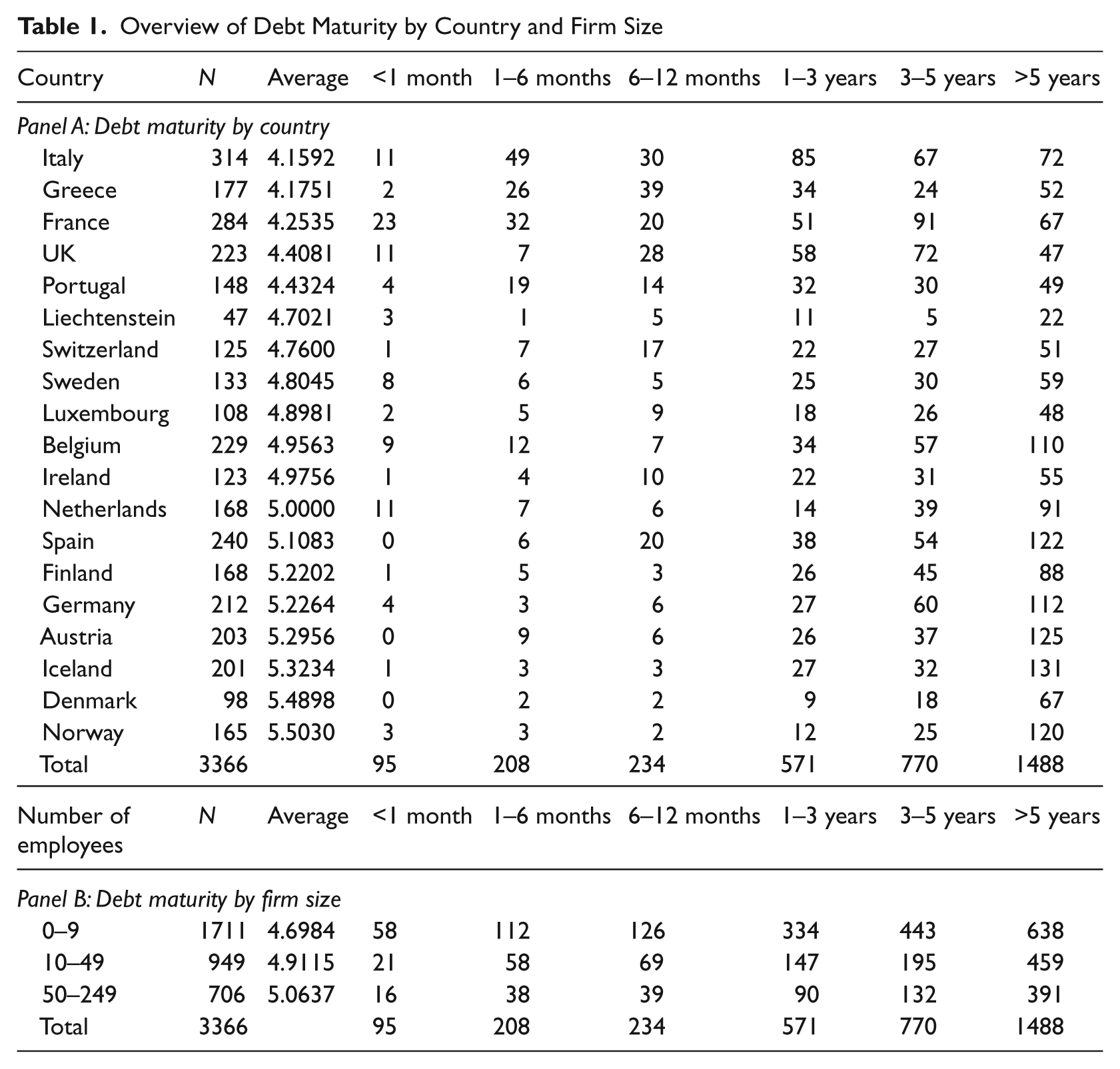

Table 1, panel A gives an overview of bank loan maturity by country ranked in ascending order. The average ranks from 4.16 (Italy), the shortest average maturity, to 5.50 (Norway), the longest. In panel B bank loan maturity is shown by firm size. On average, small firms have shorter bank loan maturity (4.70) than large firms (5.10).

Overview of Debt Maturity by Country and Firm Size

Independent variables

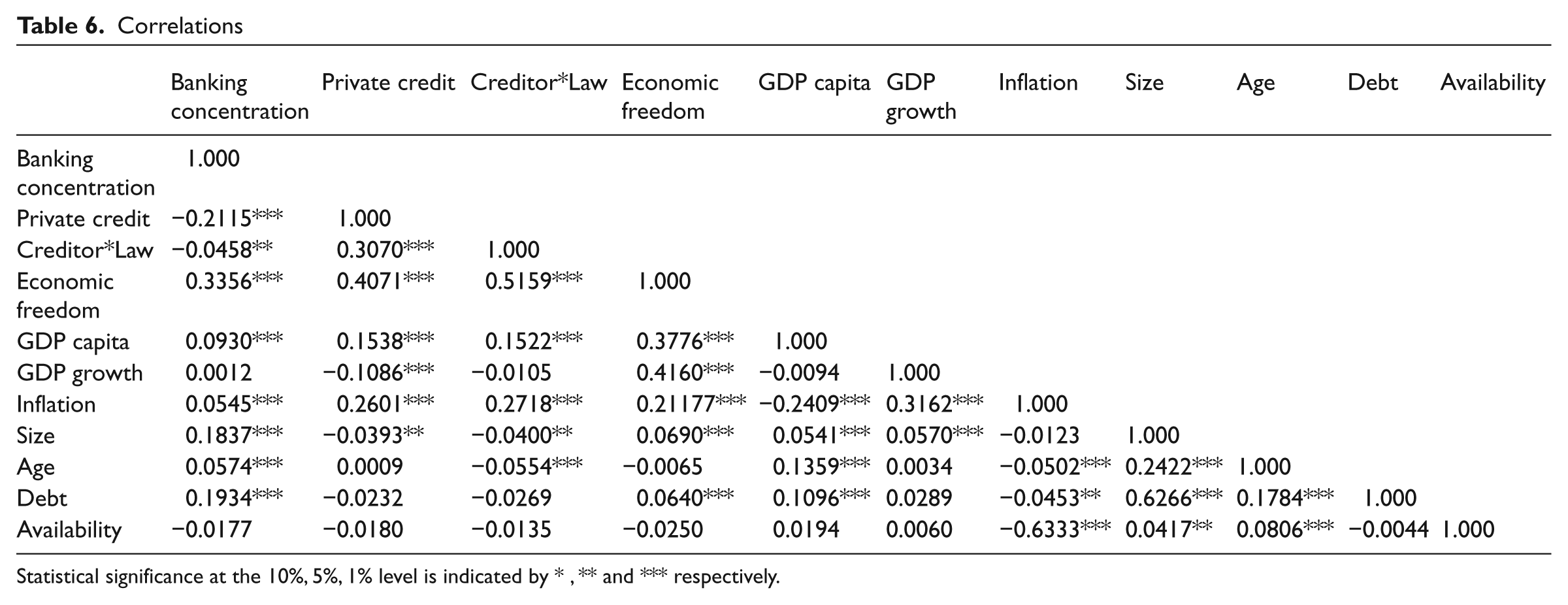

Below we describe the explanatory variables utilized in our analysis. Table 2 provides detailed definitions of all the variables, while Table 5 shows the correlations.

Variables, Descriptions and Data Sources

Data sources:

2002 ENSR Survey on SMEs

La Porta, López-De Silanes, Schleifer and Vishny (1998)

The World Bank

Conference on Bank Concentration and Competition: http://www.worldbank.org/research/interest/confs/042003/data.htm

United Nations Statistics Division

Economic Freedom Index of the Heritage Foundation

Country-specific characteristics

The variables in this section represent the country-specific characteristics that influence the supply and terms of credit that lenders are willing to provide to borrowers. We included the variables legal origin, creditor rights and law & order to account for the differences across countries in the legal environment. To proxy for a country’s institutional environment we included the variable economic freedom. Although these variables are the main focus of our study, we also included banking sector structure variables and several proxies for the economic situation, in order to control for unmeasured variation in credit supply.

A country’s legal origin determines its commercial laws. Commercial law basically comes from two broad traditions: common law, which is English in origin, and civil law, which derives from Roman law. Within the civil law tradition, commercial law originates from three major families: French, German and Scandinavian. La Porta et al. (1998) show that variation in creditor protection across countries can be explained in terms of country differences in legal origin. They find that creditor rights are the least emphasized in French civil law countries, and that their legal systems are the weakest in enforcing contracts. They also show that common law countries enhance creditor rights the most, while countries with German and Scandinavian legal traditions have the most efficient enforcing mechanisms. We expect that the likelihood of issuing long-term debt will be the lowest for banks operating under French legal heritage, where protection of creditor rights is the weakest.

La Porta et al. (1998) find that high quality of legal system enforcement could substitute for weak rules, since active and well-functioning courts can step in and rescue investors abused by firm management. Similar to Ongena and Smith (2000) we create an interaction variable creditor rights*rule of law to take into account that real creditor protection not only depends on laws, but also on their enforcement. The variable creditor rights tabulates scores using two default strategies, being reorganization and liquidation. The index ranges from 0–4, with higher values indicating the existence of more creditor rights (see La Porta et al., 1998). The variable law & order is an assessment of the law and order tradition in a country and provided by the World Bank. This index ranges from 1–100. Low levels of the score denote less reliance on the legal system to mediate disputes. The predicted sign of the legal environment variable is positive, because for a bank the benefits of shorter loan maturity as a mechanism to control for borrower risk reduces when the efficiency of the legal system and the protection of creditor rights become stronger.

To proxy for a country’s overall institutional environment we included the variable economic freedom. This variable is a composite index of 10 institutional factors determining a country’s economic freedom, and comes from the Heritage Foundation’s Economic Freedom Index. This index ranges from 1–100, with large values implying greater protection of economic freedom. It is highest in Luxembourg (79.40) and lowest in France (58). The expected sign on the coefficient is ambiguous. Bianco et al. (2002) show that improvements in the institutional environment increase the value of collateral for bank loans, thus reducing the risk for existing borrowers. A positive relation between these variables and bank loan maturity is then expected. However, such improvements can extend the credit market to low-grade borrowers, therefore raising the average risk of bank loans. Banks may reduce this risk by shortening loan maturity, and the expected sign on the coefficients would be negative.

To control for the banking sector structure we used the variables private credit and banking concentration. Private credit is measured by claims on the private sector by the deposit money banks to GDP. This is a measure of development of the financial intermediaries that isolate credit issued to the private sector, as opposed to governments and public enterprises. Banking concentration equals the fraction of bank assets held by the three largest commercial banks in each country. We expect a positive sign on the coefficients of the banking structure variables. More developed and concentrated banking systems are more efficient in controlling borrower risk, and therefore can facilitate more long-term debt.

In addition, we controlled for the influence of the state of the economy on bank debt maturity by creating the variables GDP capita, GDP growth and inflation. GDP capita is measured as real GDP per capita, averaged over the period 1990–2000 and expressed in 1990 US dollars. GDP growth equals the average rate of real GDP growth, averaged over the same period as before, and inflation equals the log difference of the GDP deflator over 1990–2000. The state of the economy could influence the bank debt maturity structure in two ways. On the one hand, the firm’s need for long-term financing may depends on its growth opportunities which, in turn, may be driven by the overall economic development. On the other hand, a low level of inflation may facilitate the issuance of longer-term contracts. We expect a positive relation between economic development and the maturity of bank loans: i.e. a positive sign on the coefficients of GDP capita and GDP growth, and a negative relation between the level of inflation and bank debt maturity.

Firm-specific characteristics

To account for sample heterogeneity we included several firm- specific control variables in our models. Firm size is one of the known determinants of debt maturity. To proxy for firm size we defined three dummy variables using the number of employees working in the firm: size1 = 1 when the firm has fewer than nine employees and zero otherwise; size2 = 1 when the number of employees is between 10 and 49 and zero otherwise; and size3 = 1 when the number of employees is between 50 and 250 and zero otherwise – or what we respectively call micro- and SME firms.4 We also defined three dummy variables to reflect the number of years that the firm has been in operation: age1 = 1 when the firm has been in operation for fewer than two years and zero otherwise; age2 = 1 when it has been between two and 10 years and zero otherwise; and age3 = 1 when it has been more than 10 years and zero otherwise. To proxy for firm leverage we defined three dummy variables using the firm’s total amount of liabilities to all its banks: debt1 = 1 when the total liabilities amount to less than US$894,846 and zero otherwise; debt2 = 1 when they are between US$894,847 and US$4,474,232 and zero otherwise; and debt3 = 1 when the liabilities are above US$4,474,233 and zero otherwise. Finally, to proxy the firm’s financial access we included the variable availability = 1 when the firm received all the loans requested from its bank(s) in the last three years and zero otherwise.5

Results

Descriptive and univariate statistics

In Table 1, first we analysed the existence of cross-country differences in the use of long- term debt. The average ranks indicate the existence of significant cross-country differences in bank loan maturity, appearing to be divided into two groups of countries. On one side of the spectrum, we found low values for France, Greece and Italy, indicating that SMEs in those countries obtain loans of shorter maturity. On the other side, SMEs in Austria, Denmark, Iceland and Norway have access to loans of longest average maturity. It seems that legal origin elucidates the differences in the use of short-term debt between these countries. Although all of them are civil law countries, they belong to different families. Those with shorter-term debt – France, Greece and Italy – are classified as French civil law countries, whereas the others are either German civil law or Scandinavian civil law countries. According to La Porta et al. (1998), German civil law and Scandinavian countries give creditors stronger protection and have higher quality of law enforcement than French civil law countries. Stronger creditor protection reduces borrower risk for lending institutions and may increase their willingness to lengthen loan maturity.6

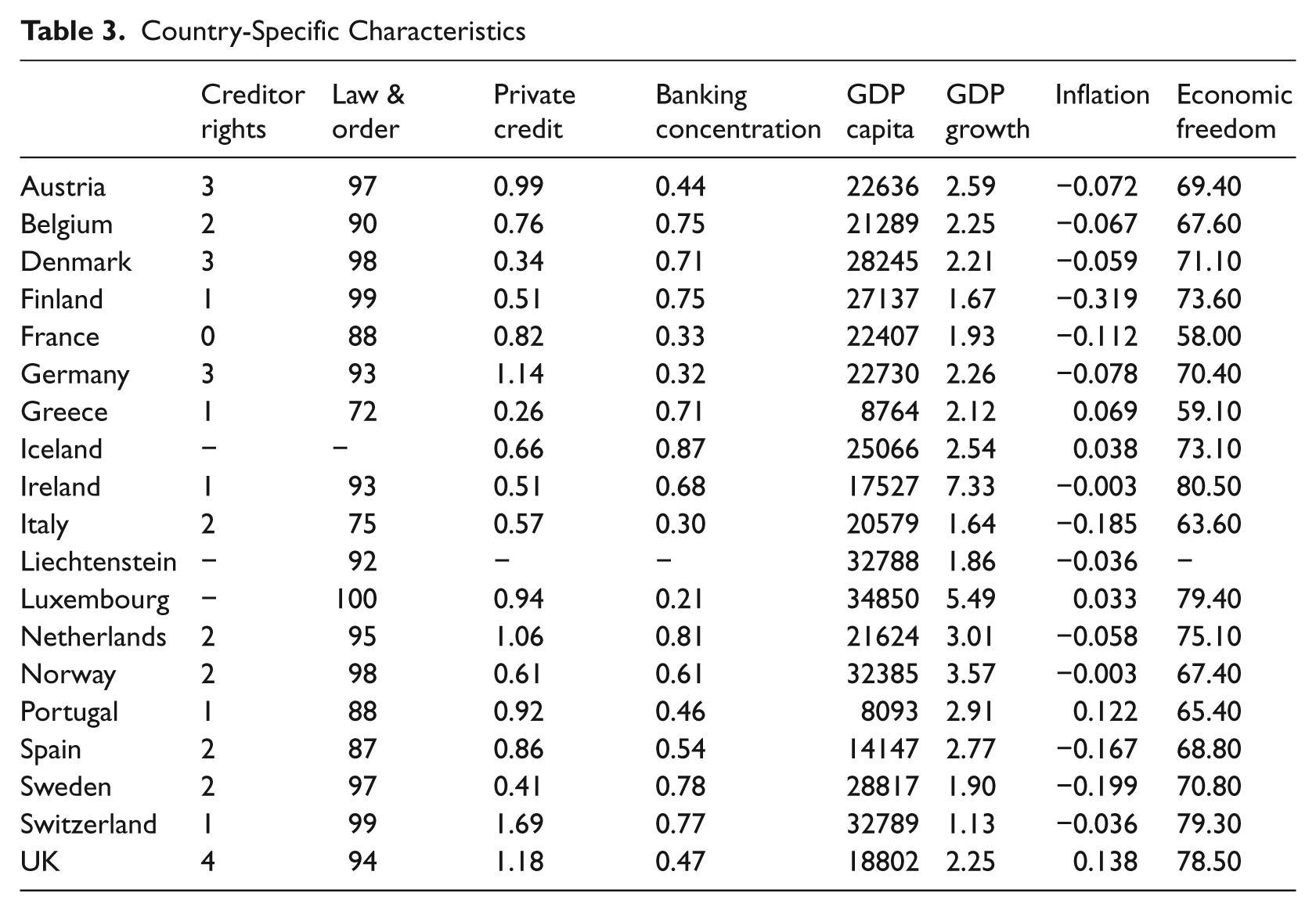

Table 3 reports the mean scores of the country-specific variables by country. There seems to be considerable cross-country variation in the sample. For example, Denmark, Germany and the UK have strong protection laws in place, while creditors in France, Finland, Greece, Ireland, Portugal and Switzerland are hardly protected by law. The quality of legal enforcement is weakest in the majority of the French civil law countries, which are France, Greece, Italy, Portugal and Spain, whereas the Scandinavian civil law countries demonstrate the highest quality of law enforcement. Economic freedom scores high in the common law countries, which are Ireland and the UK, while the lowest values are in most of the French civil law countries.

Country-Specific Characteristics

The ratio of the deposit money banks to GDP ranges from 1.69 (Switzerland) to 0.26 (Greece). As for the percentage of assets held by the three largest banks, we found the higher rates in Iceland, the Netherlands and Sweden − 87 percent, 81 percent and 78 percent respectively − whereas lower levels of concentration correspond to Luxembourg, Italy, Germany and France − 21 percent, 30 percent, 32 percent and 33 percent respectively.

The most developed countries in the sample in terms of GDP per capita are Luxembourg, Switzerland and Liechtenstein, whereas Portugal and Greece are on the other side of the spectrum. The GDP growth is highest in Ireland (7.3%) and lowest in Switzerland (1.13%). As for the level of inflation, it ranges from −0.32 in Finland to 0.14 in the UK.

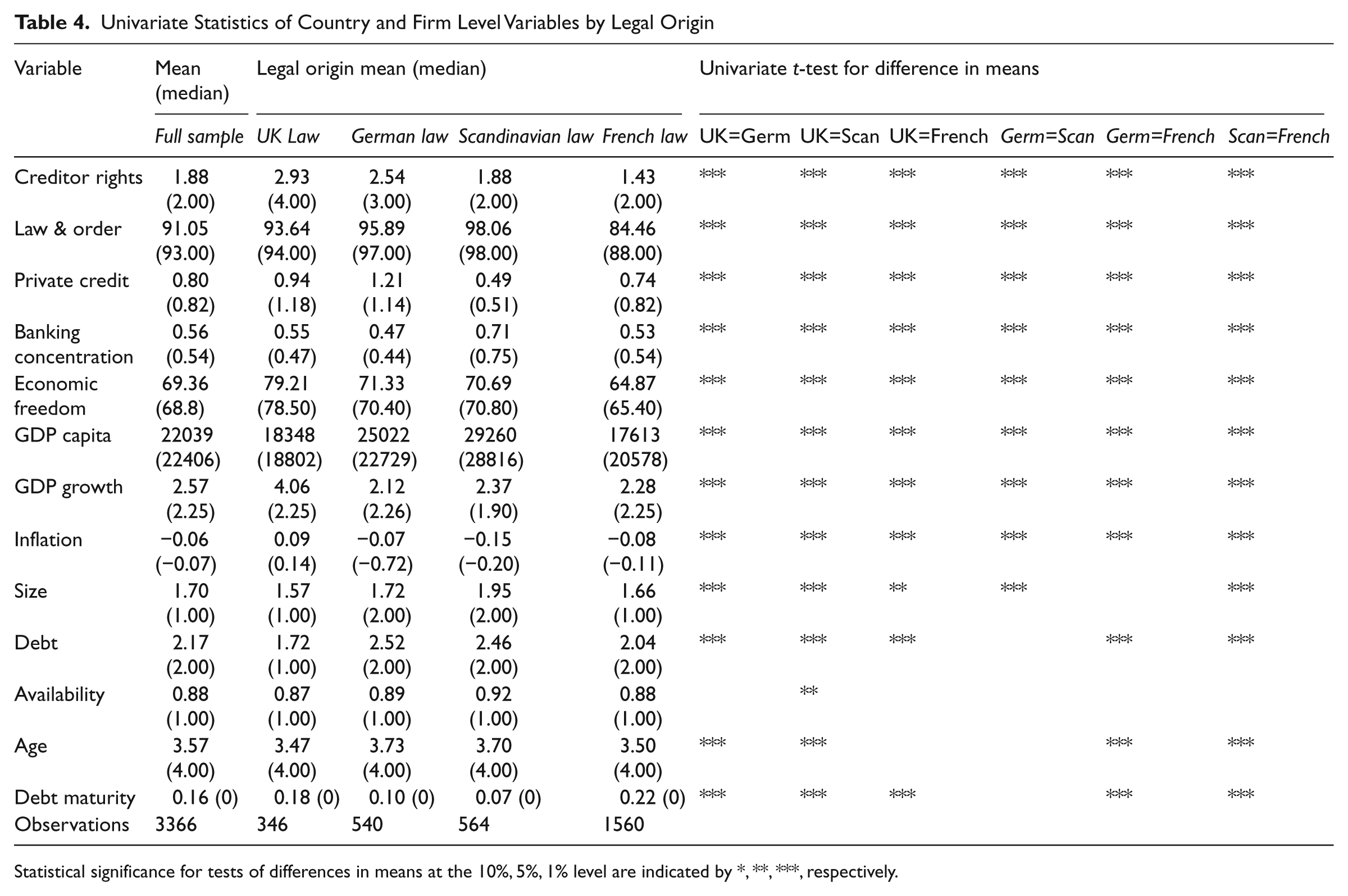

Table 4 shows the mean (median) scores of the country and firm-specific variables for the full sample and subsamples based on legal origin.7 We tested whether the means of the subsamples were significantly different from each other. They differ significantly (α = 0.01) for almost all of the country-specific variables, indicating that the legal, economic and institutional environment variables vary among countries with different legal origin. French law countries score lowest on the legal environment and institutional variables. Creditors in common law countries enjoy the strongest protection, and legal efficiency is highest in the Scandinavian law countries.

Univariate Statistics of Country and Firm Level Variables by Legal Origin

Statistical significance for tests of differences in means at the 10%, 5%, 1% level are indicated by *, **, ***, respectively.

Regression analyses of bank loan maturity

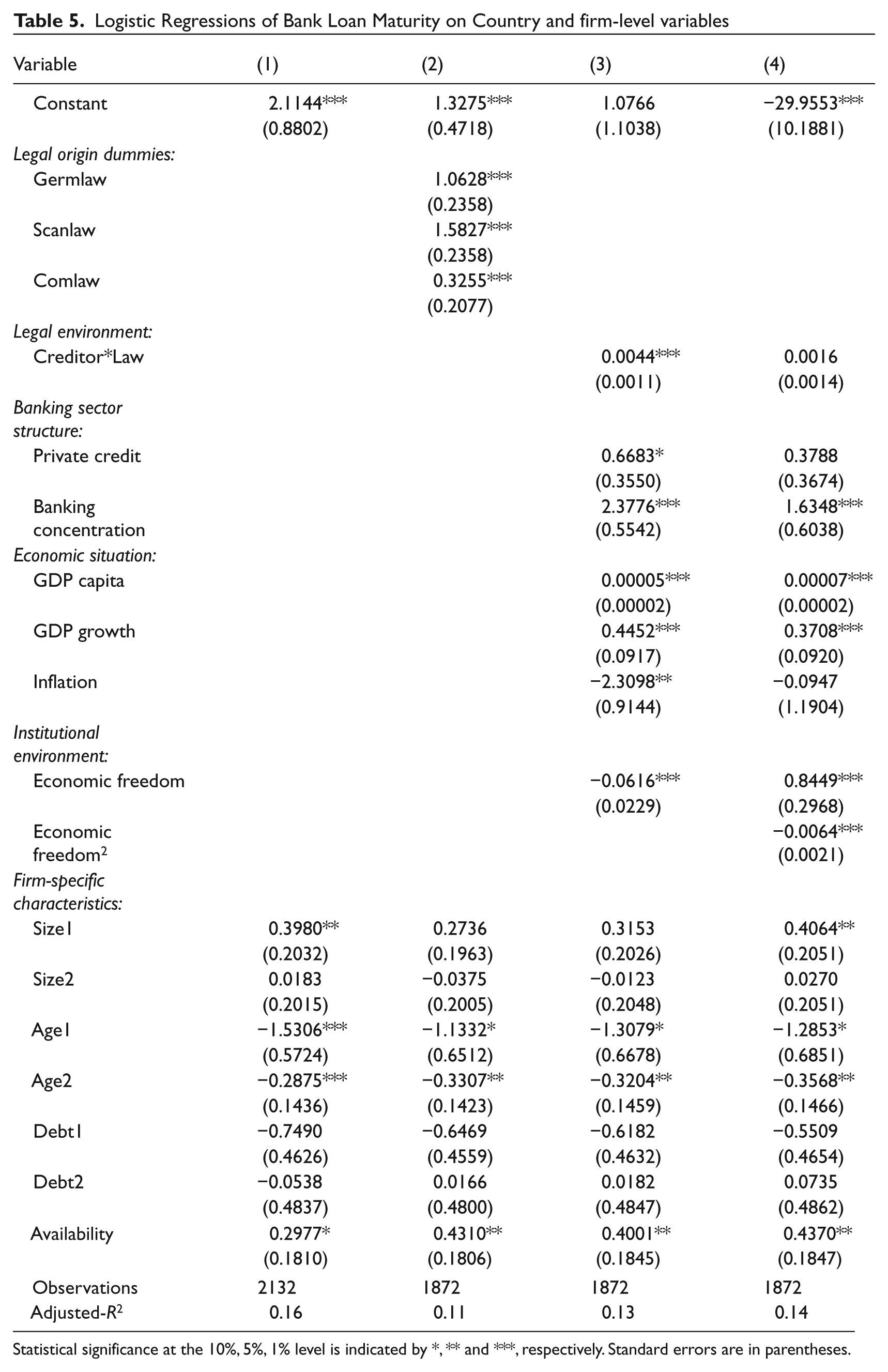

In Table 5, model 1, first we analysed the existence of cross-country differences in the use of long-term debt by regressing the variable bank loan maturity on 18 country dummies – we did not include a dummy for the Netherlands, which is our base category – and firm-specific control variables.8

Logistic Regressions of Bank Loan Maturity on Country and firm-level variables

Statistical significance at the 10%, 5%, 1% level is indicated by *, ** and ***, respectively. Standard errors are in parentheses.

The results show significant cross-country differences in bank debt maturity, confirming the existence of two groups of countries. On one side of the spectrum, we found negative and significant coefficients for France, Greece, Italy and Portugal, indicating that SMEs in those countries obtain loans of shorter maturity than firms in the Netherlands. On the other side, SMEs in Austria, Denmark, Finland, Germany, Iceland and Norway are more likely to obtain longer-term debt.

In addition, most of the firm-specific control variables are statistically significant. Consistent with previous studies by Heyman et al. (2003) and Ortiz-Molina and Penas (2008), we found that better-quality firms – proxied by the availability of credit – are more likely to receive long-term debt.

Regarding the size of the firm, the positive coefficient of the variable size1 indicates that medium-sized firms use more short-term debt than micro-firms.9 Larger firms can use lower-priced, short-term debt due to lower liquidity risk. In this case the relation between size and long-term debt is expected to be negative. The negative signs on the age coefficients indicate that older firms are more likely to obtain loans of longer maturity, which is in line with our expectations, because these firms are usually exposed to fewer asymmetric information problems than younger firms. 10

In Table 5, model 2, we grouped the countries according to their legal origin and regressed bank debt maturity on these four groups, using French common law as our reference group. Consistent with the findings of La Porta et al. (1998) we found that firms in countries under German civil law and Scandinavian civil law obtain significantly more long-term debt (α = 0.01) than firms operating under French civil law. Bank debt maturity for firms in common law countries is significantly longer at the 1 percent level.

Having established the existence of cross-country differences in the use of long-term debt, next we examined the origin of such variations using our set of country-level variables in Table 4, model 3. The interaction variable creditor rights rule of law is significant at the 1 percent level. The expected positive sign attests that firms in countries with stronger protection of creditor rights and more tradition for law and order are more likely to obtain debt of longer maturity. This is consistent with previous evidence for large and medium-sized firms, showing that firms in countries that protect creditors and enforce the law are more likely to acquire long-term debt (Demirgüç-Kunt and Maksimovic, 1999; Gianetti, 2003; Qian and Strahan, 2007). Regarding the institutional environment variables we found that higher economic freedom is negatively associated with bank debt maturity (α = 0.01), indicating that firms in countries with more economic freedom are less likely to obtain long term debt.

For completeness, we also analysed the control variables that proxy for the banking sector structure and economic situation separately. The evidence indicates that these variables also play an important role in determining the use of long-term debt. The coefficient of the variable private credit is positive and significant at the 10 percent level. This is consistent with the result presented by Demirgüç-Kunt and Maksimovic (1999), that a large banking sector enables small firms to extend the maturity of their loans. Consistent with González and González (2008), we also found evidence that a higher concentration of the banking market increases the extent of long-term loan usage. The indicator of the fraction of assets held by the three largest banks in the country is positive and significant at the 1 percent level. This result confirms Petersen and Rajan’s (1995) argument that reduced credit market competition gives banks an incentive to invest in close relationship lending. The risk reduction induced by these relationships enables banks to grant debts of longer maturity to relationship borrowers than to other firms. Model 3 reveals that the economic conditions also explain some of the variation in bank debt maturity. The ratio of GDP to population and the rate of growth in GDP are positively and significantly associated with long-term borrowing. The variable inflation has a negative and significant coefficient. Consistent with the results reported by Fan et al. (2005) and Demirgüç-Kunt and Maksimovic (1999), high levels of inflation seem to negatively affect the use of long-term debt.

In Table 6, model 4 we explore the non-monotonic association between the institutional environment and loan maturity by including the squared value of the economic freedom variable in the model. We found that bank loan maturity is increasing in economic freedom and decreasing in economic freedom-squared. These results indicate that in a relatively weak institutional environment (i.e. low values of economic freedom), an increase in economic freedom increases bank loan maturity. Conversely, in a relatively strong institutional environment (i.e. high value of economic freedom), an increase in economic freedom decreases bank loan maturity. This pattern suggests that for low values of the variable economic freedom (when the institutional environment is relatively weak) improvements in the institutional environment reduce borrower risk, while for higher levels the risk may increase. However, the significance of our legal environment variable Creditor Rights*Rule of Law disappears. Demirgüç-Kunt and Maksimovic (1999) point out that there might be a problem when explaining differences in financial structures across nations by institutional factors, because the development of these institutions are correlated. Indeed, Table 6 shows that the variables Creditor*Law and economic freedom are significantly correlated at (0.5159). 11

Correlations

Statistical significance at the 10%, 5%, 1% level is indicated by * , ** and *** respectively.

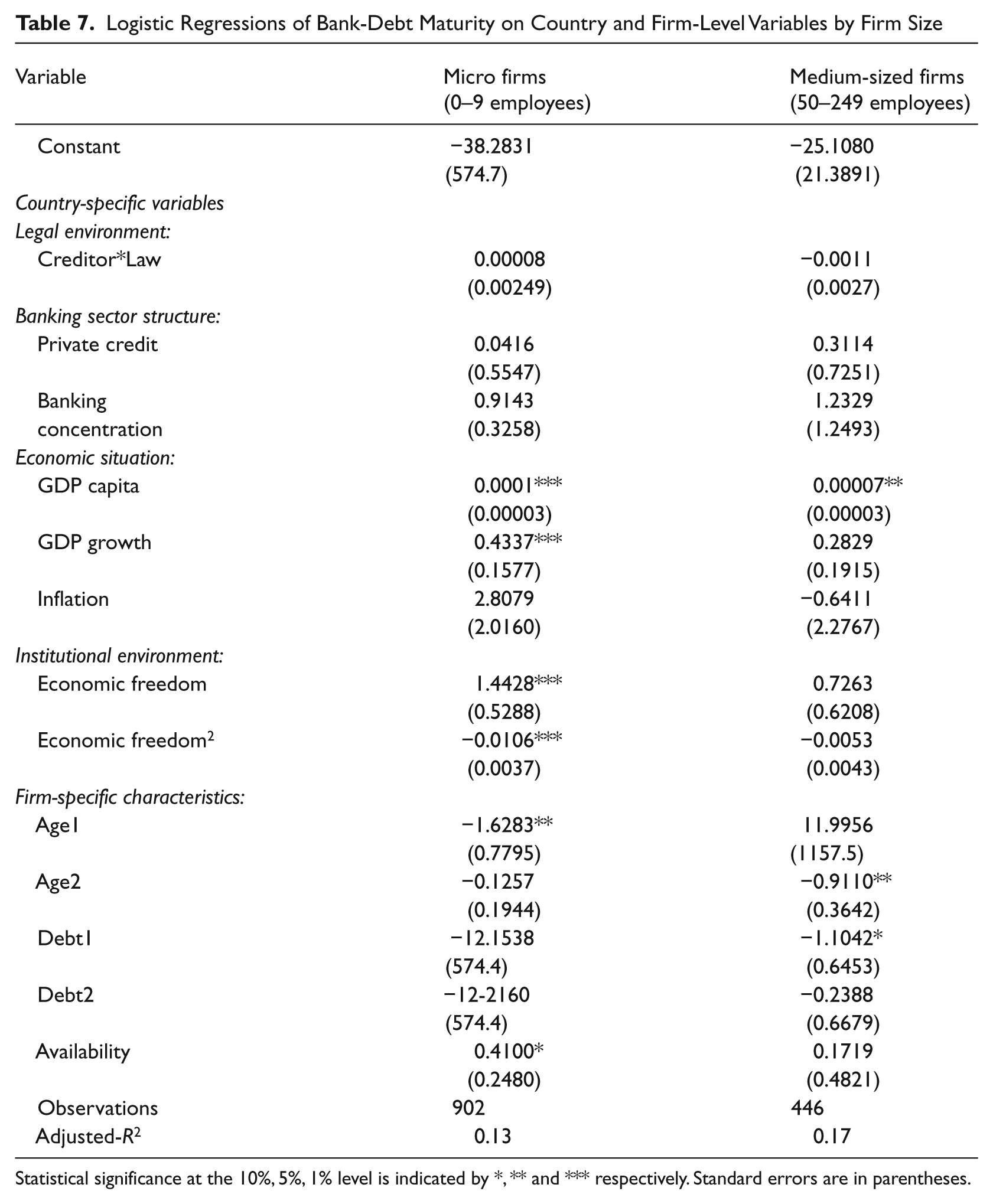

Most models in corporate finance analyse capital structure from the perspective of the borrower, who chooses a debt maturity structure that maximizes the value of the firm. However, Dennis and Sharpe (2005) show that only large firms have the ability to manipulate debt maturity to maximize firm value, whereas small firms have little influence in loan maturity settlement. This suggests that the choice of bank debt maturity for small firms might be more dependent on country-specific characteristics than on borrower specific attributes. To test this conjecture, we bifurcated our sample into the smallest firms, i.e. micro-firms with a maximum of nine employees, and medium-sized firms, i.e. between 50 and 249 employees, and regressed bank loan maturity on the firm and country-level variables. The results are reported in Table 7.

Logistic Regressions of Bank-Debt Maturity on Country and Firm-Level Variables by Firm Size

Statistical significance at the 10%, 5%, 1% level is indicated by *, ** and *** respectively. Standard errors are in parentheses.

Interestingly, the impact of the country-level variables is significantly more important for micro-firms than for the medium-sized firms. More specifically, GDP growth, GDP capita, economic freedom and economic freedom-squared, are strongly statistically significant in our micro-firm sample, whereas for medium-sized firms only GDP capita is significant. 12 Since bank loans to very small firms are deemed to be riskier due to higher asymmetric information problems, it seems logical that banks have to rely more on institutional structure when determining the duration of a loan agreement. This result seems to be in line with the findings of Jõeveer (2005), who shows that country factors are more important for small firms than for large firms when explaining leverage variation.

Discussion and conclusion

Using a unique sample of 3366 SMEs from 19 European countries, we examined the influence of cross-country differences on bank loan maturity for micro-enterprises and SMEs. It is important to know how SME loan maturity is affected by country-specific differences in the legal and the institutional environment, because this allows policymakers to better assess the impact of proposed policy changes designed to improve SME financing. Many studies report on the relationship between country-specific characteristics and debt maturity for publicly traded firms; however, little is known about this relationship for small firms.

We analysed the determinants of bank loan maturity by examining the country’s legal and institutional environment while, in addition to firm-specific characteristics, controlling for the banking structure and the economic situation. A very interesting finding is that even after the inclusion of the firm-specific control variables, country-specific factors remain significantly important in explaining bank loan maturity for SMEs. Our results indicate that, after controlling for standard economic influences, bank loan maturity is a function of the country’s legal and institutional environment. More specifically, firms in countries that protect creditors and enforce existing laws are more likely to obtain long-term bank debt. In addition, when the institutional environment is relatively weak, an increase in economic freedom increases the likelihood for SMEs to obtain loans of longer maturity. These results suggest that policy changes that make insolvency procedures more efficient, accessible, simpler, fairer and transparent (such as the insolvency provisions in the UK Enterprise Act 2002), should improve SMEs’ access to bank finance.

We also provided insight into the effect of the country’s legal origin on bank loan maturity. SME firms in countries under German and Scandinavian civil law and English common law are more likely to obtain bank loans of longer maturity, compared with SMEs in countries under French civil law. Our findings are size-dependent, such that the existence of efficient institutions seems to be even more important for the smallest firms in our sample, i.e. micro-firms. One explanation is that due to lack of specific firm information, banks have to rely more on country-specific characteristics when providing loans to micro-firms. They are more willing to provide longer-term loans to these opaque firms when they operate in countries with a better institutional environment.

There is one note of caution with regard to our results. SMEs are small, privately held companies, and therefore are not required to provide publicly available financial statements. Financial information about SMEs is difficult to obtain and often has to come from survey data, as in our sample. We recognize that survey data might create potential biases and possible measurement problems. However, we believe that our sample is large enough for cautious but valid conclusions to be drawn.

Footnotes

Acknowledgements

The permission of the EIM Business and Policy Research in the Netherlands to use the 2002 ENSR Survey data and to publish findings based on analysis of that data is gratefully acknowledged. We especially like to thank Rob in ‘t Hout, whose continuous support to access the data has made this project possible. Responsibility for interpretation of the findings lies solely with the authors.

This research is part of Project ECO2008-06179/ECON, financed by the Research Agency of the Spanish government.