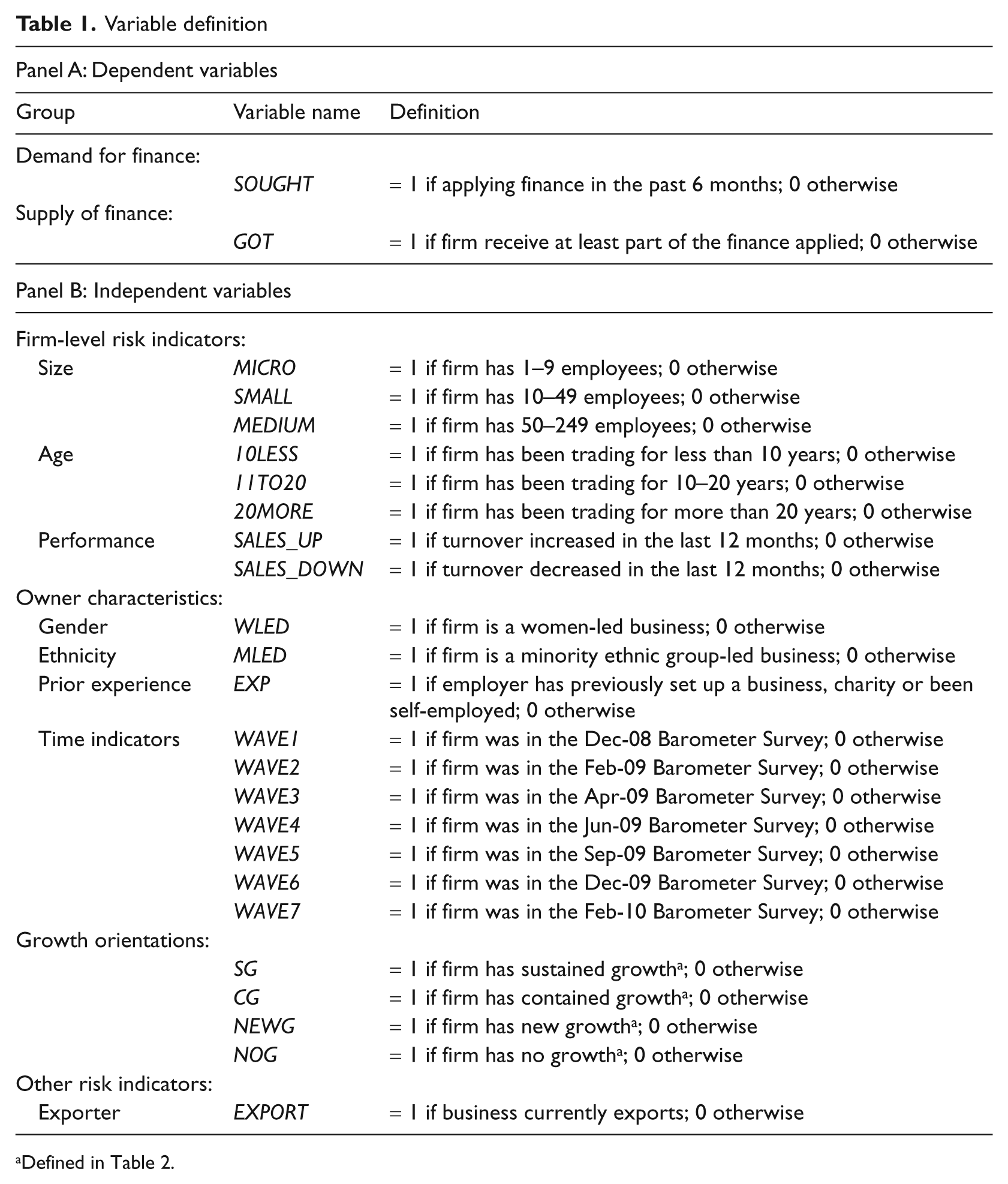

Abstract

This article uses empirical evidence from the UK to consider how demand for external finance changed as the economy entered recession and whether external finance became more difficult for entrepreneurs to access as the recession progressed. It finds that larger firms and those experiencing declines in sales were more likely to maintain or increase their demand for external finance. The opposite was true for women-led businesses. Generally, finance was more readily available to larger and older firms throughout the recession. At its peak 119,000 (10% of the total stock) smaller firms were denied credit in a three-month period.

Introduction

The financial crisis, which began in September 2008, contributed to a fall of 6.4 percent in UK gross domestic product (GDP) in the subsequent six quarters that constituted the official recession. This represents around three years of trend-level economic growth for the UK economy. As the crisis had its roots in the banking sector, retail banks and credit institutions became increasingly unwilling to lend to the personal and business sector particularly, those financial institutions that were overexposed in riskier lending products and markets. Bank of England figures show that net monthly flows of business lending fell from £7.4bn in 2007 to an overall net repayment of £3.9bn in 2009 (Bank of England, 2011). Loan-to-value rates declined considerably, even when financial institutions were prepared to advance credit, and the cost of small firm credit increased to a median of 4 percent even when base (interest) rates fell rapidly to 0.5 percent, where they have remained to date.

With some justification, banks have been accused of not lending to small businesses by the popular press – but this is probably only half the story. Even if we accept the general truth that lending volumes to the small business sector have fallen considerably, there is a gap in our knowledge about precisely the types of small businesses and entrepreneurs to which banks are unwilling to lend. Equally important is the nature of demand for credit and lending from small businesses. It is naive to expect that demand for credit from small businesses remains constant in the face of a global financial crisis – and even if it did, the types of small businesses that demand credit may be quite different.

It is the intention of this article to use a unique longitudinal dataset for the UK, which spans the period leading up to the financial crisis in September 2008 and all through the subsequent recession, in order to address three key research questions.

RQ1: Has the demand for credit from the small business sector fundamentally changed in the current recession? RQ2: Has the supply of credit to the small business sector fundamentally changed in the current recession? RQ3: How many smaller firms have been denied credit in the recession?

In doing so, we hope to add to the general understanding of what really happens in the market for small business financing in an economic downturn, from both a demand and supply perspective. This will enable us to speculate about the potential impacts of credit rationing on the small business sector, and to identify areas where government action might be appropriate. Further, we provide insights into what state the small business sector might be in as the economy climbs slowly out of recession. This is of great importance given the political onus placed on the small business sector to provide new jobs and economic prosperity in the future.

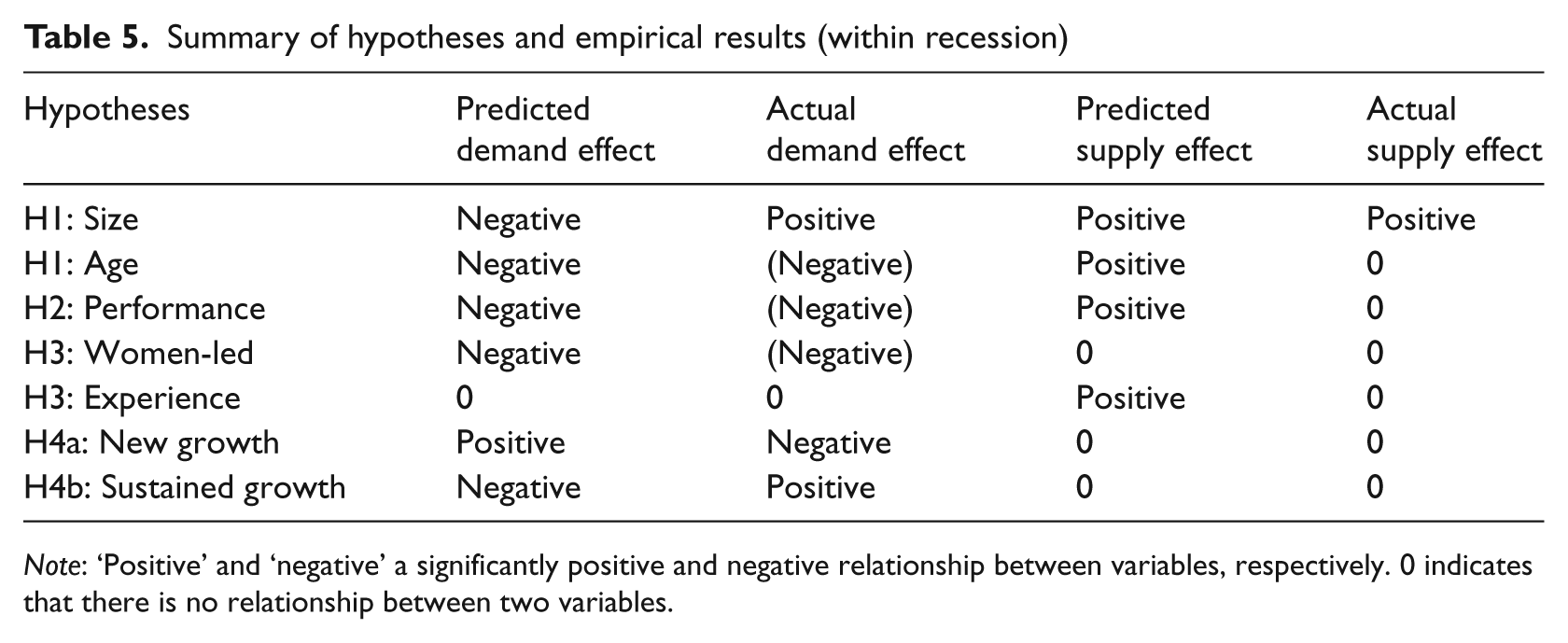

Generally, we find that it is easier to predict changes in demand for external finance than it is to predict changes in the supply of external funds during a recession. What is apparent is that in periods of economic stability or growth, financial institutions use a richer set of factors to make their lending decisions. During a recession, lending institutions appear to use firm size as their primary lending criterion, with micro-business in particular being restricted in their access to capital. We also find that women-led firms have a lower general demand for external finance, and this is maintained in recessionary periods despite lenders being equally willing (or unwilling) to advance funds to them. Experienced entrepreneurs had a higher demand prior to the recession, but similar levels of demand to relatively inexperienced entrepreneurs during the recession. These results suggest that in periods of relative economic prosperity the opportunity for investment differs across types of entrepreneurs, and hence, their demand for capital is different. However, in recessionary environments with falling general demand across the economy, these opportunities disappear. On growth, we find that firms that have achieved growth in the past, and expect to grow in the future still sustain their demand for external capital, but lenders appear not to take this information into account when making their funding decisions. Thus, growth potential and static firms are effectively treated the same by lenders in recessions. The overall patterns in demand and supply for external finance as the recession unfolded suggests that there was a decline in demand as the recession progressed, but a U-shaped pattern to supply as lending approval rates recovered within 12 months. In absolute terms, the total number of credit rationed firms in the UK economy peaked in February 2009, six months after the start of the financial crisis, when 119,000 smaller businesses (10% of the total stock) which applied for finance were rejected. Ten months later in December 2009, this number had fallen to 56,000 smaller firms.

The remainder of the article proceeds as follows. The next section reviews the relevant literature on small business finance, based on which we develop our main hypotheses for empirical investigation. The following section describes the data source for this study and the survey method from which the data are derived, followed by a discussion on the variables used in the empirical analysis. This is followed by reports of sample descriptives and the results of multivariate regression analyses. The article concludes with the policy implications of this study.

Literature review and hypotheses development

It is widely recognised that entrepreneurial activity and the growth of small businesses can be constrained by limited access to financial resources arising from imperfections in capital market allocations (Auerswald and Branscomb, 2003; Cressy, 2002; Revest and Sapio, 2010; Westhead and Storey, 1997). The reasons for these difficulties in access to finance can be traced back to the economic literature on asymmetric information and imperfect markets (Bester and Hellwig, 1989; Binks et al., 1992; Hillier and Ibrahimo, 1993). As a result, lenders charge higher prices (risk premiums) to compensate for the higher uncertainty and risk associated with investing in small businesses. However, empirical evidence suggests that in the normal course of bank lending, banks simply refuse to provide any finance to small some firms (absolute rationing), rather than engage in quantity (volume) rationing (Centre for Business Research, 1996; Cowling, 1999; Storey, 1997). The seminal credit rationing paper by Stiglitz and Weiss (1981) provides a theoretical framework in which the interest rate or collateral is excluded as a rationing device due to information asymmetries in the small firm–bank relationship, and ‘credit rationing’ is used to define the situation in which ‘there exists an excess demand for loans because quoted loan rates are below the Walrasian market clearing level’ (Jaffee and Stiglitz, 1990: 847).

The subject of financial constraints or credit rationing has been the focus of a considerable body of theoretical work, and the existence of credit rationing has been examined extensively (Berger and Udell, 1992; Cowling, 2010; Goldfeld, 1966; Jaffee, 1971; King, 1986; Slovin and Slushka, 1983; Sofianos et al., 1990); however, the extent of ‘true’ credit rationing remains limited (Levenson and Willard, 2000). In this section we review some of the key literature on the relationship between the firm, entrepreneur characteristics, the general state of the economy and access to finance with a view to developing testable hypotheses which can be empirically examined with our unique data.

However, before we begin the detailed review on literature, it is worthwhile to note that information asymmetry between lenders and borrowers may not necessarily lead to under-investment. Particularly under certain assumptions, the unobservable quality of entrepreneurs may indeed result in investment exceeding the optimal level (De Meza and Webb, 1987, 2000). The term ‘funding gap’ has been excessively used to justify government intervention to increase lending, regardless of the creditworthiness of borrowers (De Meza and Webb, 2000; Nightingale et al., 2009). Moreover, credit rationing should count for businesses with potentially good investment opportunities and need for finance, but these are discouraged from applying for external funding as they fear rejection (Han et al., 2009; Kon and Storey, 2003). These issues have significant policy implications, and thus, deserve further investigation in future research.

Size, age and performance

Firm size and age are two of the most common risk indicators used by financial institutions to evaluate small business financing propositions. More established and larger firms are more likely to achieve economies of scale by reducing information asymmetries (Berger and Udell, 1998; Cassar, 2004). Further, investing in small businesses introduces significant transaction costs which, in most cases, are higher for smaller and less established firms due to the fixed cost element of the due diligence process (Titman and Wessels, 1988; Wald, 1999). It follows that smaller and younger firms are likely to be charged higher loan rates, if they are not absolutely rationed for any external finance (Cassar, 2004; Cosh and Hughes, 1994; Scherr et al., 1993; Van Caneghem and Van Campenhout, 2010).

While it might be true that young and small firms find it more difficult to access external finance, in a sufficiently efficient market it could be the case that these firms are rejected as a result of investors rationally assessing their quality and deciding that they are not worth investment given the levels of risk incurred (Nightingale et al., 2009). Therefore, many empirical studies have assessed whether financing constraints on small businesses are the rational outcome of the application of lenders’ credit risk measures, or discrimination based on prior criteria such as size and age (Becchetti et al., 2010; Cowling, 2010; Riding, 1997).

On the demand side of the market, the same firm-level characteristics that lenders typically associate with risk when evaluating lending propositions (age and size) also play a key role in determining the need (demand) for external finance. For example, younger and smaller firms are more likely to require outside financing as their internal resources (owner’s wealth, retained profits and cashflow) are unable to finance new investment and growth opportunities fully. These general problems can be exacerbated in periods of low demand when cash flows tighten and profits decline, and business survival requires an injection of capital to maintain liquidity until demand grows again. Taken together, we propose two hypotheses relating to firm size and age: H1a (demand): Younger and smaller firms will have a higher demand for external finance in a recessionary environment. H1b (demand): Younger and smaller firms will have a lower demand for external finance in a recessionary environment due to borrower discouragement. H1 (supply): Younger and smaller firms will be more likely to be refused finance in a recessionary environment.

While the size and age of a firm are important and easily verifiable proxies for firm-level risk, lenders also use historical and behavioural information relating to firm performance in order to capture important elements of potential downside risk: the probability that a firm’s performance may not be able to cover capital and interest repayments (Cowling, 2010). Banks call this ‘serviceability’, which simply reflects their judgement on whether the funding proposal appears capable of generating the scale of revenues required to repay the debt. However, it also might be the case that firms with superior historical performance have been able to build up capital reserves within their business, which will reduce their subsequent level of demand for external finance. With this in mind, we propose two further firm-level hypotheses relating to the demand and supply sides of the market: H2 (demand): Firms that have performed well going into the recession are less likely to require external funding in a recessionary environment. H2 (supply): Firms that have performed well going into the recession are more likely to receive funding in a recessionary environment.

Owner characteristics

The characteristics of business owners capture important aspects of the entrepreneur human capital and therefore, the creditworthiness of the enterprise. This is especially true for small businesses at early stages of firm development, when owners are usually the major (and probably the only) decision-makers (Cassar, 2004).

Characteristics such as gender and ethnicity may reflect the relative risk aversion of business owners and accordingly, the choice of capital structure and demand for finance, which in turn may influence the relative probability of accessing finance. For example, research has found that women are less likely to seek external finance (Carter and Shaw, 2006; Coleman and Cohn, 2000) and ethnic minority (especially black) owners are significantly more likely to encounter financing problems (Bank of England, 1999; Biggs et al., 2002; Fraser, 2009; Smallbone et al., 2003; Storey, 2004). However, this should not be automatically taken as evidence of discrimination against certain ethnic groups, as they may indeed have a different borrowing patterns or other non-ethnic risk factors (Bank of England, 1999; Fraser, 2009; Kon and Storey, 2003; Raturi and Swamy, 1999; Sena et al., 2010; Storey, 2004; Storey and Strange, 1994). While earlier studies typically found that women are more likely to be rejected when applying for bank loans (Bates, 1990; Blanchflower et al., 2003; Cavalluzzo and Cavalluzzo, 1998), again the empirical evidence becomes less clear when the exogeneity of borrowing patterns by female business owners is controlled for in more recent and sophisticated research (Coleman and Cohn, 2000; Sena et al., 2010; Storey, 2004).

In addition, studies on owner characteristics and access to finance tend to build on human capital theories, using the owner’s age, education and experience as signals for better human capital and therefore lower credit risks. These studies usually find a negative relationship between owner experience and difficulties in accessing external finance (e.g. Blumberg, 2007; Cassar, 2004; del-Palacio et al., 2010; Storey, 2004), which leads to our third hypotheses: H3 (demand): Women-led businesses are less likely to seek external finance per se, and this effect will strengthen in a recessionary environment. H3 (supply): Experienced small business employers are more likely to be granted finance per se, and this effect will strengthen in a recessionary environment.

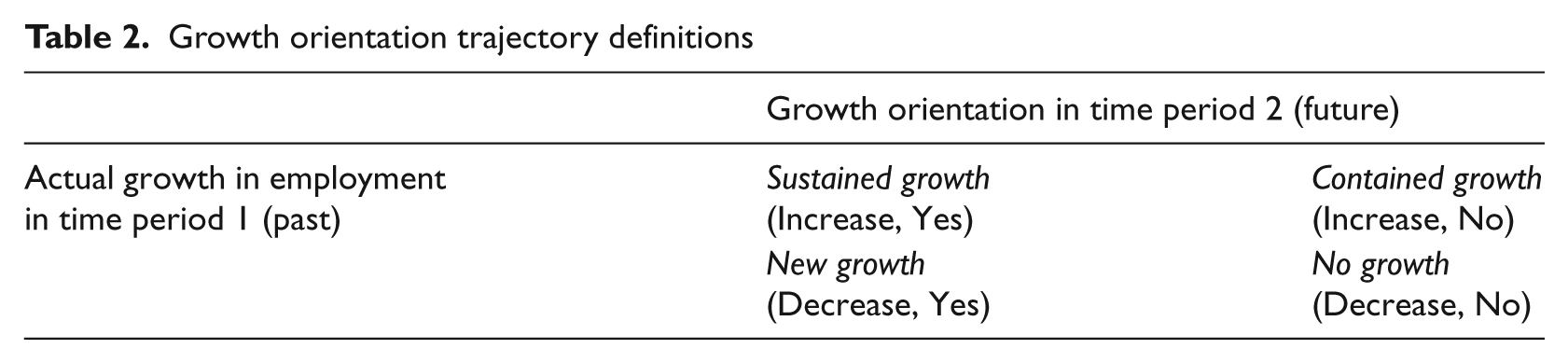

Growth orientations

Myers (1984) shows that information asymmetries between firms and outside investors result in the financing of investments by a firm undertaken by first using internal resources, then debt and, as a final resort, equity (the ‘pecking order theory’). This theory predicts that firms with better growth opportunities and therefore, a greater need for finance resources are more likely to turn to debt finance after internal funds have been exhausted (Michaelas et al., 1999; Psillaki and Daskalakis, 2008). However, the conflicts of interest between debt and equity-holders, especially with the presence of associated bankruptcy risks, imply that even with significant growth opportunities, highly levered firms tend to under-invest due to the debt overhang (Myers, 1977). Therefore, the effect of growth opportunities on the costs of finance and consequently difficulties in accessing external finance should be viewed in conjunction with internal firm resources (e.g. cashflow) and the cost of financial distress (López-Gracia and Sogorb-Mira, 2008; Myers, 1984).

Drawing on these theories, intentions to grow are predicted to be associated with a demand for external finance. Moreover, Cassar (2004) suggests that firms are better off establishing credit relationships with outside financiers as early as possible in their life cycles in order to benefit from easier access and lower cost of future outside financing. Therefore, it is expected that firms with ongoing (sustained) growth orientations are likely to fulfil their external financing requirements at an earlier stage than firms with shorter-term financing relationships.

Empirical studies on growth prospects and access to finance yield inconclusive results. While Chittenden et al. (1996), Jordan et al. (1998) and Scherr and Hulburt (2001) find that growth options have little effect on leverage, other studies find a positive relationship between leverage and growth (Cassar, 2004; Esperanca et al., 2003; Lopez-Gracia and Sogorb-Mira, 2008; Michaelas et al., 1999; Van Caneghem and Van Campenhout, 2010). It should be noted that many of the previous studies use ex-post measures of growth (e.g. actual growth in employment or sales), and only a few recent studies (e.g. Cassar, 2004) use growth intentions by business owners, possibly due to the difficulties in accessing such information. This gives rise to the following hypotheses: H4a (demand): Firms with newly-formed growth orientations are more likely to seek external finance in a recessionary environment. H4b (demand): Firms with sustained growth orientations are likely to have secured higher levels of external financing prior to the recession, and their subsequent demand for external finance will decrease during a recessionary environment.

Macroeconomic conditions

Undoubtedly, economic downturn and unfavourable financial market conditions affect the operation and survival of firms. Given the economic importance and vulnerability of small businesses, a better understanding of how adverse macroeconomic conditions influence entrepreneurial activities is crucial to effective crisis management by small businesses (Herbane, 2010). Several studies have focused on business survival or operation during economic downturn. For example, Requena-Silvente (2005) find that small and medium-sized enterprises (SMEs) base their export decisions on ‘typical’ export behaviour, which is not affected by economic recessions. Fotopoulos and Louri (2000) show that survival becomes more difficult for firms established closer to recessions. Grilli (2011) finds that established start-up firms with more experienced entrepreneurs are actually less likely to survive during negative industrial shocks, and suggests that this result reflects voluntary exit by experienced entrepreneurs to minimise potential losses.

Nevertheless, there is limited research on the financial constraints faced by small businesses during recessionary periods. Acharya and Viswanathan (2011) suggest that following the sudden drying-up of liquidity in adverse economic shocks, greater credit rationing and de-leveraging in the economy are expected to be observed. Empirical evidence shows that small businesses rely more on external finance in hard times (Bank of England, 1993; Binks et al., 1992; Cowling et al., 1991). However, the ease of getting the required finance is likely to be negatively affected by economic environments such as tight monetary conditions (Bougheas et al., 2006). This gives rise to the following two hypotheses: H5 (demand): Firms are more likely to seek finance in a recessionary period as cashflow tightens, retained profits decline and survival becomes a more prominent concern for entrepreneurs. H5 (supply): Firms are less likely to secure external finance in a recessionary period as lending institutions tighten their lending criteria.

Method

Sample and data collection

This study is intended to analyse existing data from two previous survey sources which cover information on small businesses in the pre-recession and recessionary periods, respectively.

The pre-recession data is derived from the Annual Small Business Survey in 2007/08. The Survey has been conducted on an annual basis 1 since 2003 and the 2007/08 survey involved a large-scale telephone survey conducted by IFF Research Ltd between November 2007 and March 2008, in order to monitor key trends in the characteristics and perceptions of small business owners and managers. The main purpose of the survey is to gauge the needs and concerns of small businesses and identify the barriers that prevent them from fulfilling their potential. A total of 9362 SMEs (businesses with fewer than 250 employees) were interviewed using a stratified random sample selection method evenly across 13 regions in the UK, and the sample was randomly drawn across all commercial sectors of the economy.

A sample of the SMEs entering the 2007/08 Annual Small Business Survey were re-contacted in a series of Business Barometer surveys to determine how well or badly they had performed in the previous year, and to assess their levels of business confidence going forward. On average, 500 SMEs were re-surveyed using questions similar to the 2007/08 Annual Small Business Survey in each of the seven Business Barometer waves, starting from December 2008 to February 2010 with intervals of two to three months. The survey period coincides with the latest financial crisis, therefore giving us the opportunity to investigate how business attitudes and access to finance by UK SMEs change pre- and post-recession. The ‘matching’ of 2007/08 Annual Small Business Survey and Business Barometer surveys yield a dataset of 3506 SMEs, which means that there is no loss of data from the Barometer surveys. Excluding missing values only reduces the sample size by a very small amount. It is also possible that a firm was defined as an SME in earlier surveys but grew to a larger firm with more than 250 employees, and so we have removed these firms to restrict our analysis to SMEs only.

Dependent variables

Panel A of Table 1 shows the definition of dependent variables, which capture small businesses’ demand for, and supply of, external finance. Both variables are binary variables and static in nature. Demand for finance is defined as whether firm owners reported having sought/applied for finance for their businesses in the previous 12 months. Supply of finance is defined as whether the firm obtained (all or part of) the finance required.

Variable definition

Defined in Table 2.

Over 80 percent of businesses have chosen to apply for debt finance, in the form of loans, leasing or hire purchase or bank overdrafts. This is consistent with the financing pattern predicted by the pecking order theory (Myers and Majluf, 1984), in which firms requiring external finance prefer debt to equities, given the information asymmetries between the firm and its potential financiers. In addition, this choice of capital structure reflects the general belief that the unique characteristics of small businesses, such as small-scale and low expected return or high risk, may lead to limited use of equity-type finance (Berger and Udell, 1998; Scholtens, 1999).

Explanatory variables

The independent variables in this study can be classified into four groups: firm-level risk indicators, owner characteristics, growth orientations and time indicators. Panel B of Table 1 defines the explanatory variables by these four groups.

The main firm-level risk indicators include size, age, sector, region and performance. Firm size is measured by employee numbers. This can either be a continuous variable or as discrete size bands, namely micro (1–9 employees), small (10–49 employees) and medium-sized (50–249 employees) firms. Age is given by both the Annual Small Business Survey and Business Barometer surveys as banded variables (up to 10 years, 11–20 years and more than 20 years). Measuring small business performance is problematic due to the lack of accurate accounting data and the variety of different objectives of those running a small business (Storey, 2004). Here we use a relatively subjective measure of whether owners reported increased, stable or decreased turnover. In addition, other variables related to firms’ business activities may influence the demand for finance and/or lenders perception of business risk, such as whether a firm exports, but such information is not available across all survey respondents.

Owner characteristics or human capital measures consist of gender, ethnicity and prior experiences. We are not able to specify the exact ethnic origins of business owners, but are only provided with information on whether a business is a minority ethnic group-led business. An experienced employer is defined as having previously set up a business, charity or been self-employed.

Growth orientation variables combine measures of both actual growth and ambition for future growth. Actual growth is defined as whether a business had more, fewer or the same number of employees compared to 12 months ago. Growth ambition is measured by the intention of businesses to increase staff numbers in the next year. Therefore, we could attribute firms’ growth orientation dynamics into four categories, as shown in Table 2. We use seven time dummies, each representing one of the seven Business Barometer surveys, in order to examine the effect of market conditions on SME access to finance.

Growth orientation trajectory definitions

Results

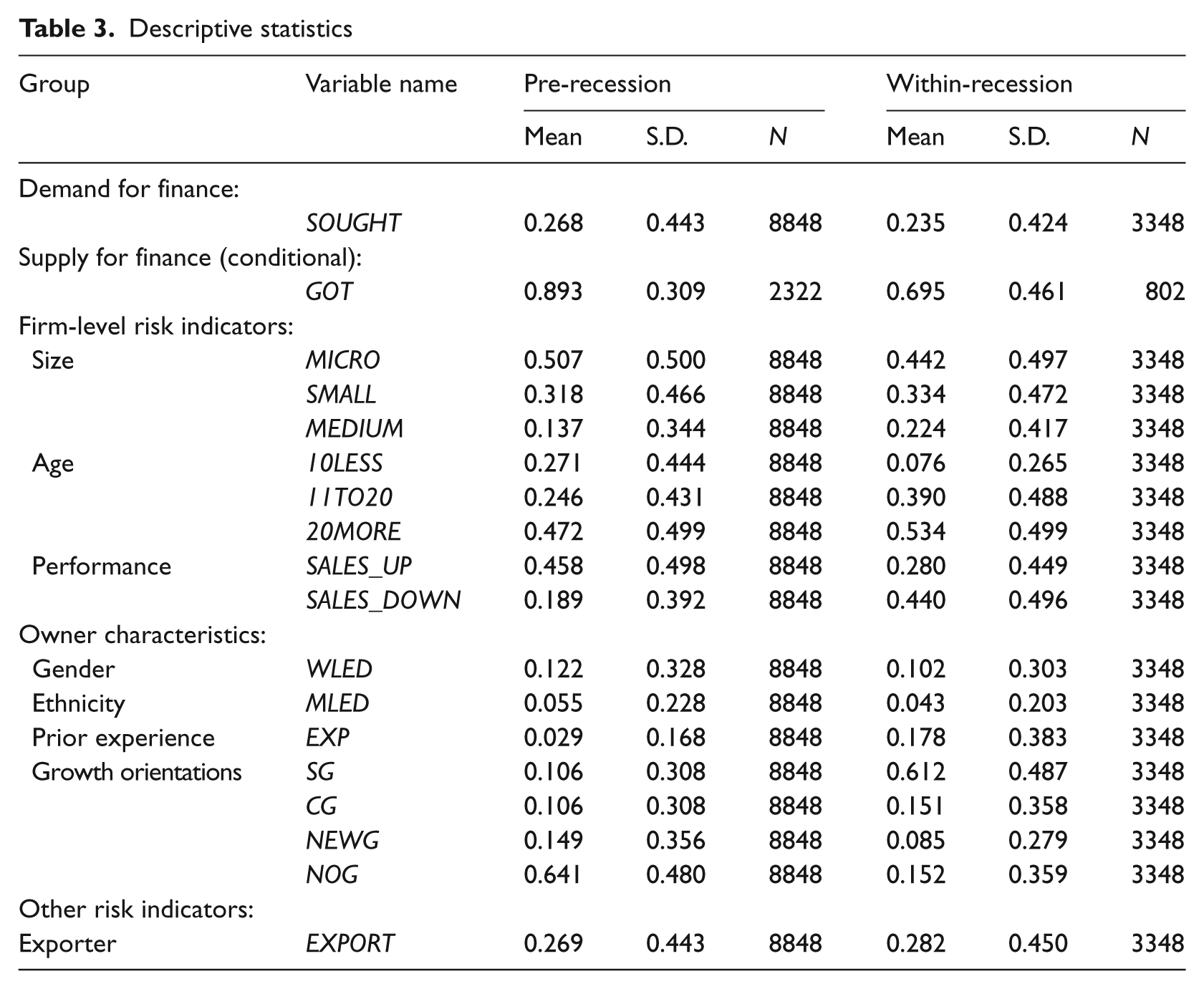

Descriptive statistics

Table 3 reports the descriptive statistics of dependent and independent variables. Using the sample validation criteria results in 3348 firm-level observations for the analysis of SME access to finance during the recession. As comparison we have retrieved firm-level data from the 2007/08 Annual Small Business Survey, and this gives us 8848 observations. Since most of the variables are dummies, it is worth noting that the mean of each dummy is equivalent to the percentage of observations where the variable takes a value of 1. Note that the sample selection is inevitably influenced by possible survivorship bias, as by construction only active firms are eligible for the later barometer surveys; however, it is reasonable to believe that such bias is lowered to a large extent due to the small time lag between the two sets of surveys. Looking across the seven waves of Barometer surveys, we note that 8.4 percent of the total sample in Wave 1 (December 2008) and 7 percent of the sample in Wave 7 (February 2010) are young firms, but the distribution of age is independent from Barometer survey waves. Equally, 43 percent of the total sample in Wave 1 are micro firms compared to 41.9 percent in Wave 7. Thus there is a small selection effect across the surveys, but the scale does not appear to be likely to unduly influence the results.

Descriptive statistics

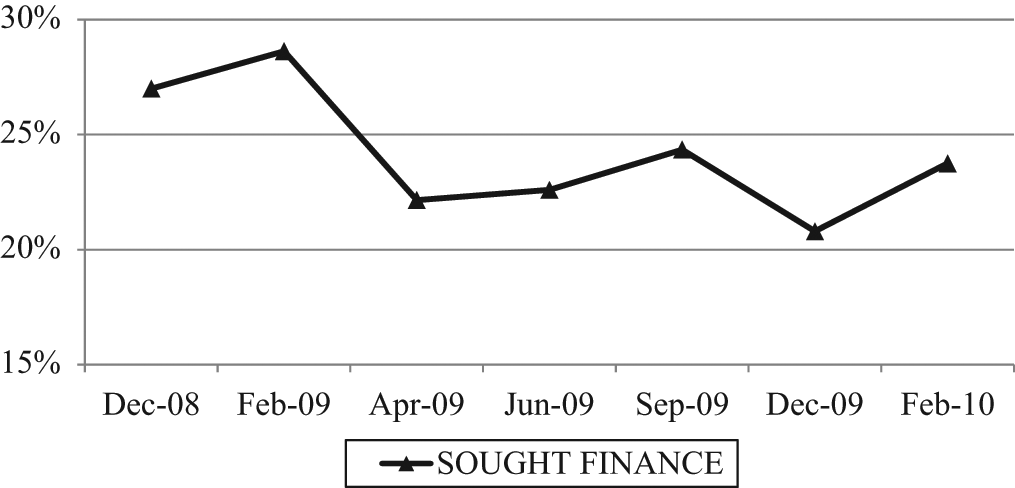

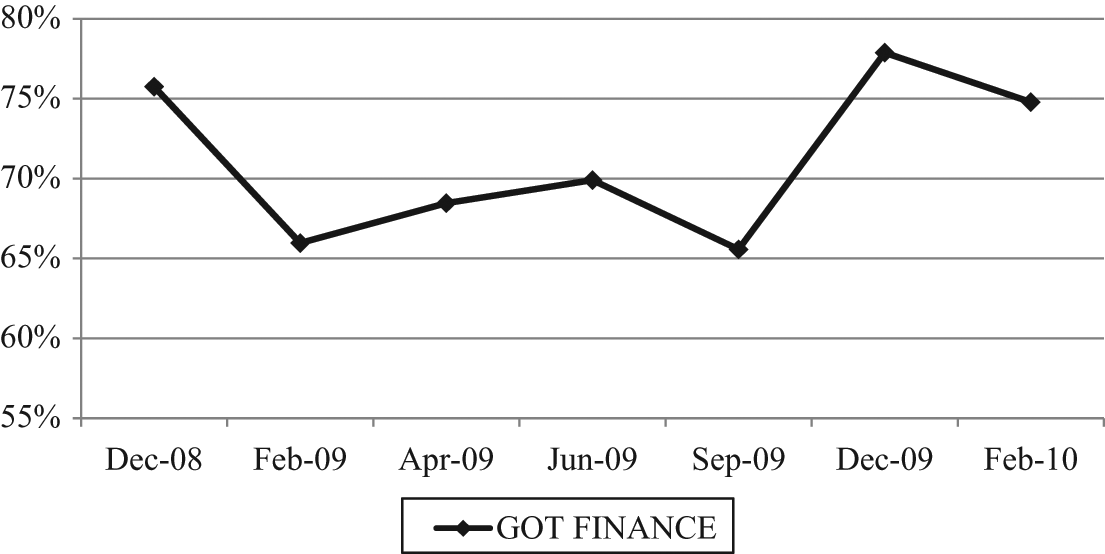

As reviewed from the 2007/08 Annual Small Business Survey data, 27 percent of business owners have sought external finance before the recession and among those requiring finance, and almost 90 percent have obtained (at least part of) the finance needed. During the latest financial crisis and between December 2008 and February 2010, just under one-quarter (24 percent) of SME employers had tried to obtain finance for their business in the previous 12 months (16 percent had tried to obtain finance once, and 8 percent tried more than once). The supply of finance during the recession has dropped even more dramatically than demand, with fewer than 70 percent of applicants receiving the finance they had sought. Figures 1 and2 illustrate the change of fund demand and supply during the recession (between December 2008 and February 2010), as reviewed by the Business Barometer surveys. Drawing on the discouraged borrower theory to develop H1b, which predicted that younger and smaller firms were more likely to be discouraged from applying for external funding during recessions, we note that, using a broad definition, actual levels of discouragement were only 2.5 percent of the total stock of firms. On this evidence, we did not pursue this line of investigation here.

Proportion of business seeking external finance over time

Proportion of business securing external finance over time

This reduction from the 2007/08 figures suggests that both the demand for, and supply of, finance has decreased during the financial crisis. In particular, fewer than two-thirds (or 15% of the barometer-surveyed firms) of the firms seeking finance during the recessionary periods also sought finance before the recession, with the rest of the firms (9%) growing demand only recently. Around one-quarter of the businesses stopped seeking finance during the recession, and it remains an interesting question as to whether this is a result of firms voluntarily reducing demands, given that they had already fulfilled their financing needs at earlier stages (Cassar, 2004), or as a result of firms being rationed by lenders in adverse economic conditions.

The rest of Table 3 shows the summary statistics for independent variables for both pre- and within-recession periods. A striking difference between the pre- and within-recession sample is the performance and the subsequent survival of small businesses: 46 percent of the firms reported increased sales before the recession, and fewer than 20 percent report decreased sales. The situation is virtually reversed afterwards during the recession, with 28 and 44 percent of employers reporting increased and decreased sales, respectively. As a result of the economic downturn, older and larger firms (with more experienced employers) are more likely to survive. Here the percentage of micro (up to 10 employees) and youngest (up to 10 years old) businesses before the recession is 7 and 10 percent more than within-recession, respectively. Interestingly, businesses’ growth orientation trajectories have not changed significantly over time, except that employers appear to have become more pessimistic during the recession even though they have achieved actual growth over the past year.

Multivariate regression results

The starting point was to model econometrically the demand for and supply of external finance both before and during the period of economic recession. The demand-side variable is named SOUGHT, coded 1 if a business sought external finance, and 0 otherwise. The supply-side variable is named GOT, coded 1 if the business who sought external finance was successful in securing that finance, and 0 if it was unsuccessful. By definition, the outcome of a finance application is only recorded if a firm actually sought finance. As both of the dependent variables are binary variables by construction, a probit model with selection 2 was used and the maximum likelihood coefficient estimates are shown in Table 4. 3 We used this econometric method to test for sample selection effects that which might occur, as only those firms with a high probability of securing external actually apply. Those firms that perceive their chances of securing external are low are reluctant to incur the costs of applying. As we are particularly interested in how demand and supply changes when the economy moves into recession, we estimate separate pre-recession and within-recession models. Ideally, we would have liked to incorporate a cost of lending measure (loan interest rates) into our analysis, but the available Bank of England Trends in Lending time series, from which average lending margins are derived, did not cover the full sample period. A further complexity is that Bank of England base rates have been stable at 0.5 percent since March 2009. While our time dummy variables are a noisy proxy for lending costs as they also capture other exogenous factors, they will capture some of this variation in demand for loans.

Probit regressions with sample selection for SMEs demanding finance

Note: This table reports the probit regression results first for the probability of businesses seeking external finance and then the probability of successfully accessing finance conditional on the firm seeking finance. The first set of regressions uses all available firms from the 2007/08 Survey and the last two sets of regressions use only businesses interviewed in the Business Barometer surveys. Some dummy variables are excluded as appropriate to avoid collinearity. Constant terms and region dummies are included in the regressions but results are not reported. Marginal effects of the coefficient estimates for the conditional supply equations are also reported to illustrate the direct effect of explanatory variables on the dependent variables. This does not alter the statistical inference or the estimation method of the model. Model diagnostics include the log likelihood and chi-squared statistic of the regression. * = 10%, ** = 5%, *** = 1% significance levels.

Table 4 reports the maximum likelihood estimates for both demand and supply equations. For ease of interpretation, marginal values of coefficient estimates are reported for the supply equation, which show the change in probability as the independent variable switches its value from 0 to 1. Models (1), (3) and (5) of Table 4 relate to the demand-side of the market (SOUGHT) and models (2), (4) and (6) relate to the supply-side (GOT) of the market. Models (1) to (4) relate to the pre-recession period, and models (5) to (6) relate to the within-recession period.

Models (1) and (2) report the results for pre-recessionary demand and supply of finance using all available data from the 2007/08 Annual Small Business Survey. It can be seen that the demand for finance is positively associated with firm size (number of employees) and negatively related to firm age. Prior performance is found to have no effect on the demand for finance. Consistent with earlier research (Carter and Shaw, 2006; Coleman and Cohn, 2000), female entrepreneurs are less likely to seek external finance than male entrepreneurs. This suggests that risk aversion-based theories might help explain why women appear more reluctant to borrow than men. After controlling for non-ethnic risk factors, the odds of minority ethnic group-led businesses demanding finance are just the same as other firms. Businesses with experienced owners are more likely to require external finance, as are firms that export goods outside the UK. Firms with negative growth in the past, whether they intend to grow in the future or not, have lower demand for finance.

At the industry sector level, there is a remarkable degree of consistency between the two models in terms of firms in particular industry sectors being less likely to apply for finance, and less likely to secure finance even if they do apply. In order of magnitude the industry sectors that were least likely to apply for finance were transport and communications, construction, non-metals manufacturing and other manufacturing. Again in order of magnitude, the industry sectors least likely to secure finance even after applying were transport and communications, construction, other manufacturing and non-metals manufacturing. By contrast, firms in different geographic regions were equally likely to apply for finance, and equally likely to receive it if they did apply.

Financiers tend to supply finance to small businesses according to common firm-level risk indicators. Measured in marginal terms, medium-sized and small-sized businesses are 19 and 12 percent more likely to be offered the finance required, respectively compared to micro-businesses. More established firms find it easier to obtain the finance needed. Prior performance is an important criterion used by providers of finance, who are 2 percent more likely to grant finance to firms with increased sales. However, the fact that prior performance is only marginally positively related to the supply of finance indicates that lenders may have realised that better access to finance could indeed enhance the firm’s future performance (Storey, 2004). Women-led businesses are 5 percent less likely to be successful in finance applications, indicating possible gender discrimination during the sample period. Human capital plays an important role in the supply of finance. Here, experienced employers are 10 percent more likely to have their financing needs met. Lenders are more likely to provide finance to borrowers with actual growth than those with downsized or stable employment numbers. However, a higher denial rate is seen in businesses with neither actual nor intended growth, which are 10 percent more likely to be rejected than those with sustained growth.

As a robustness check, the same regression was run using only firms that were interviewed in the Business Barometer surveys in Models (3) and (4). The fact that the results are fairly similar (but weaker in some cases) indicates that selection bias is not a major concern in the pre-recession results. The only difference between the whole and matched sample pre-recession results is that minority ethnic group-led businesses have a higher demand for finance. However, once they apply for finance with other firms, there is still no sign that they are discriminated against by lenders.

The last two models show smaller firm demand for and supply of finance during the latest financial crisis. It appears that small businesses make financing decisions based on similar factors as in pre-recession times. An interesting feature of recessionary-time demand for finance is that businesses are more likely to seek external finance to compensate for the loss of revenue from sales. This is consistent with pecking order theories, where entrepreneurs prefer to self-finance investments before seeking external bank loans. Further, growth orientation plays an even more important role in determining the need for finance during the recession. Business owners seem to have become more prudent when applying for external finance in the sense that only those with both actual growth and future growth ambitions are most likely to turn to costly external sources of finance during a recession. This is especially true when growth orientation is hampered by limited internal funds due to decreased sales. 4 Finally, demand for finance is lower in the middle and towards the end of the recession. Firms in April, June and December 2009 are less likely to have sought finance than firms in other periods.

In terms of industry sector, which was an important factor in both the demand for and supply of finance in the pre-recession period, we also find that its relative importance in the determination of demand and supply diminished during the recession. However, what was interesting is that firms in business services were the least likely to apply for finance, and those in other manufacturing and transport and communications also had a relatively low demand; but on the supply side, only firms in other manufacturing were more likely to have their loan requests turned down. Again, we found that no regional effects were apparent for either demand or supply during the recession. This evidence as a whole is consistent with credit rationing theories that emphasise the randomness of loan denial, which is not based on borrower quality. Thus, credit rationing theories appear to have greater traction and empirical support in recessionary environments.

Financiers have obviously become more cautious when making lending decisions. This is evident as lenders have shifted away from human capital criteria (e.g. experience) towards more direct measures of credit risk, especially firm size. Here, small businesses were 12 percent more likely to receive the finance they sought and medium-sized businesses 19 percent more likely. The insignificant effects of age and performance are likely to be due to size as a better proxy for the collateral that a firm can provide, which acts as a sorting device for business risk and found to alleviate credit rationing by banks (Cowling, 2010). This is consistent with the collateral being used by banks when information asymmetries are heightened during a recessionary period.

Growth orientation is no longer a significant driver for the supply of finance. This has an important implication, as during periods of severe economic downturn financiers tend not to take into consideration the more subjective measure of business prospects (growth ambition) while making lending decisions. Financial constraints are evident during the recession, but they are not observed consistently across all periods. April and September 2009 were the periods when the probability of being unsuccessful in a fund application was at its highest (with 16 percent and 14 percent more likely to be rejected, respectively), indicating that smaller firms are most likely to be rationed for credit during these periods. It is also clear that business cycle theories of investment and financing have a great deal of empirical support and traction in recessionary environments.

Summary of hypotheses and empirical results (within recession)

Note: ‘Positive’ and ‘negative’ a significantly positive and negative relationship between variables, respectively. 0 indicates that there is no relationship between two variables.

Conclusion

Our general finding indicates that it is easier to predict changes in demand for external finance than it is to predict changes in the supply of external funds during a recession. What is apparent is that in periods of economic stability or growth, financial institutions use a richer set of factors to make their lending decisions. During a recession lending institutions appear to use firm size as their primary lending criterion, with micro-business in particular being restricted in its access to capital. Interestingly, in recessionary periods lenders seem to ignore growth orientations; this might suggest that the subset of small businesses most capable of creating new jobs and stimulating economic growth as the economy emerges from recession may be prevented from doing so by limited access to investment capital.

In terms of answering the three broad research questions, our evidence is as follows.

RQ1: Has the demand for credit from the small business sector fundamentally changed in the current recession?

Our results suggest that demand for credit does fall in general in a recession, but the effect is far from immediate. In terms of scale of the reduction in demand we estimate it to be a maximum of 21 percent. In terms of timing, it appears that it was only when the economy had been in recession for a full nine months that demand dropped off significantly and sharply. It was also the case that demand for credit is more equally spread across the smaller business population in recession.

RQ2: Has the supply of credit to the small business sector fundamentally changed in the current recession?

In contrast with demand, the supply of credit to the small business sector dropped off from December 2008 onwards and only recovered 12 months later. The scale of the fall in supply of credit was approximately 13 percent. We also note that supply of credit is more targeted in recession at larger firms.

RQ3: How many smaller firms have been denied credit in the recession?

Scaling up our findings to the small business population in the UK suggests that credit rationing peaked in February 2009 (six months into the recession), when an estimated 119,000 firms (10% of the total stock of smaller firms) were denied credit. A year later, only an estimated 56,000 (4.8% of the total stock of smaller firms) were denied credit.

In line with previous research, we also find that women-led firms have a lower general demand for external finance, and this is maintained in recessionary periods despite lenders being equally willing (or unwilling) to advance funds to them. In contrast, ethnic minority group-led firms had a higher demand for external finance in periods of economic stability or growth, but reduced their demand to comparable levels of non-ethnic minority group firms in the recession. A similar pattern was observed for experienced entrepreneurs who had a higher demand prior to the recession, but similar levels of demand to relatively inexperienced entrepreneurs during the recession. These results suggest that in periods of relative economic prosperity the opportunity for investment differs across types of entrepreneurs, and hence their demand for capital is different. However, in recessionary environments with falling general demand across the economy, these opportunities disappear.

On growth, we find that firms that have achieved growth in the past, and expect to grow in the future, sustain their demand for external capital yet, firms that aim to grow in the future exhibited a fall in demand for external finance, as did those with no future growth ambitions. However, lenders appear not to take this information into account when making their funding decisions. Thus, growth potential and static firms are effectively treated the same by lenders.

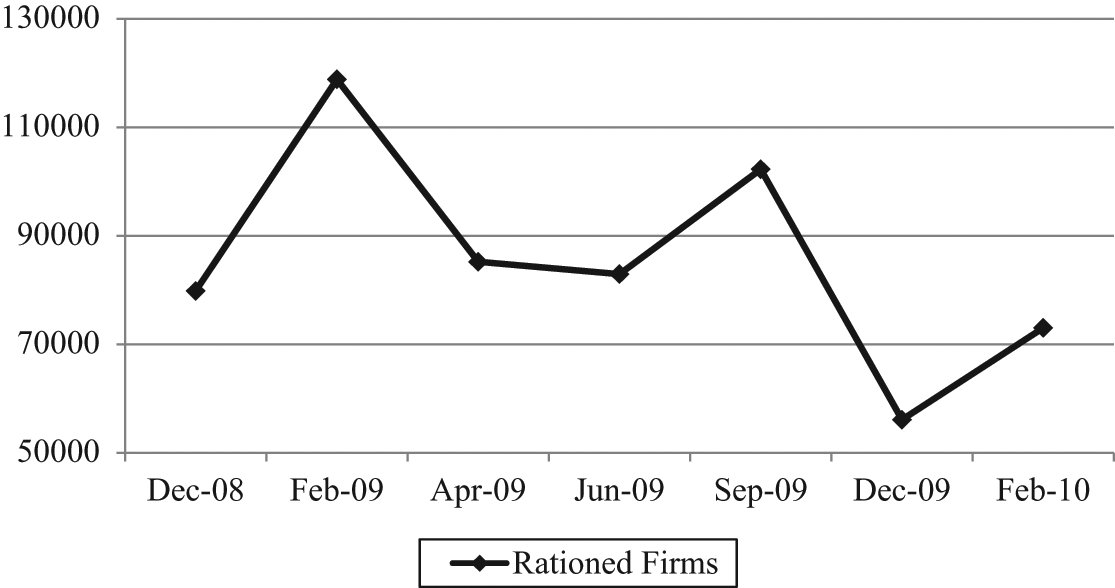

Finally, we observed in Figures 1 and 2 the overall patterns in demand and supply for external finance as the recession unfolded. The general pattern was a decline in demand as the recession progressed, but a U-shaped pattern to supply as lending approval rates recovered within 12 months. Figure 3 shows what these demand and approval rates actually mean in the context of the UK small business sector and its 1.2m firms with employees (UK SME Statistical Bulletin, 2011) by imposing our key results on this total actual business population.

Absolute number of credit rationed small firms in the UK economy

It is clear that in absolute terms, the total number of credit-rationed firms in the UK economy peaked in February 2009, six months after the start of the financial crisis, when 119,000 smaller businesses that applied for finance were rejected. Ten months later in December 2009, this number had fallen to 56,000 smaller firms. As the official recession ended in the first quarter of 2010, the number of credit-rationed firms increased to an estimated 73,000 smaller businesses. We conclude that the recession has led to a significant decrease in the ability of smaller firms to access external credit, and that this may inhibit the potential of the smaller business sector to take advantage of, and contribute to, economic recovery in the UK.

Implications of the study

So, what are the potential implications of the present findings for practitioners and policymakers? For banks and small businesses, the way they react to a recessionary environment is quite different and not synchronised. It appears that banks cut off lending when small businesses still want to borrow early in a recession, then later as banks relax their lending policies, small firms scale back their demand for credit. Thus, throughout an entire recessionary cycle the market for small business lending is in disequilibrium, and this benefits neither banks nor smaller businesses. One potential solution is for firms to react more quickly to the onset of recession by scaling down their lending requirements and, equally, when the economic environment improves, however slowly, by increasing their demand for loans and seeking new growth opportunities. Another potential solution is for the public sector to seek to support early recession lending as a short-term measure to cover the most severe supply constraints, effectively smoothing out the period of disequilibrium between the demand and supply of loans. This policy was actually adopted by the British Government through transitional loan funds and on a broader level by the Enterprise Finance Guarantee.

Suggestions for future research

In terms of potential implications for theory and future avenues of research, the present findings suggest that information-based theories of credit rationing appear to be more valid in recessionary environments, when banks become increasingly unsure about the relative quality of firms and entrepreneurs seeking funding. Aside from a general reduction in the supply of loans, banks seem to target available lending funds to the largest of firms which they perceive as being the most creditworthy. Other signals that allow banks to discriminate between potential borrowers are ignored, particularly human capital measures. The evidence also suggests that pecking order theories are still valid in recessionary environments, when loan denial appears more random than the case in non-recessionary economic environments. The implication here is that some small firms which are denied credit (presumably because they cannot self-fund projects fully) must seek external equity funding or abandon their investment projects. The general findings of this study also show how powerful business cycle effects are in the market for small business lending. This leads us to suggest that an important avenue for future research is to consider how long the scarring effects of the initial credit squeeze last among smaller businesses and entrepreneurs, even when banks have relaxed their lending criteria. In addition, further work could examine why male and female entrepreneurs act so differently in the lending market, even when there is no difference in the probability of securing loans during a recession.

Footnotes

Funding

Initial funding for this study was provided by the UK Department for Business Innovation and Skills.

Notes

Marc Cowling is a professor of entrepreneurship at Exeter Business School, where he leads a group of academics involved in teaching and researching aspects of entrepreneurial business processes and performance. Currently his research focus is on the impact of the global financial crisis on the financing and performance of smaller firms, particularly on how experienced and inexperienced entrepreneurs differ in their ability to access finance and subsequent business outcomes. Prior to his appointment at Exeter, he was chief economist at the Institute for Employment Studies, where he led a team of researchers examining labour market issues.

Weixi Liu is a lecturer in finance at Renmin University, China. Previously he was a research fellow in entrepreneurship at the University of Exeter. His research interests include entrepreneurship, the finance of entrepreneurial firms, especially high-tech young firms, venture capital and government policy on entrepreneurship and entrepreneurial finance. He has been commissioned by both national governments (UK, New Zealand, Australia and China) and international institutions (World Bank) to conduct policy-focused research on entrepreneurship and small business policies.

Andrew Ledger is a statistician at the Department for Business Innovation and Skills in the UK, working in enterprise and economic development analysis. He has a wide range of responsibilities around enterprise analysis and policy and provides statistical support to a number of projects, including the Department’s Small Business Survey and the Business Barometer series.