Abstract

In this article, a conceptual framework and research propositions are developed to explain how microfinance provision can translate into new venture creation and existing venture growth in an emerging economy context by engendering higher levels of psychological and social capital in clients. In doing this, the extent to which microfinance institutions provide business support and opportunities for social interaction are identified as factors which may strengthen the impact of microfinance provision on psychological and social capital, especially for poor entrepreneurs in resource-constrained settings. The conceptual framework and research propositions developed will be of use to academics in designing an agenda for future empirical research. In addition, they will help policymakers and microfinance providers to better design microfinance initiatives that enhance the well-being of clients and maximise their entrepreneurial outcomes.

Keywords

Introduction

Microfinance refers to the provision of financial services, including small business loans, to lower-income clients, generally in poor communities, with the aim of supporting economic development through the growth of entrepreneurial activity (Bruton et al., 2011; Khavul et al., 2013). Microcredit loans aim to help alleviate poverty by empowering the poor to participate in markets, generate income and become more self-sufficient (Siwale and Ritchie, 2012). The extent to which microfinance supports poverty alleviation in emerging market economies has been the focus of a growing body of research in the field of development economics (Cassar et al., 2007; Feigenburg et al., 2010; Gine and Karlan, 2008; Karlan, 2007; Zeller, 1998). By conducting randomised experiments, researchers have sought to identify factors which may affect the success of microfinance initiatives in terms of facilitating loan repayment and poverty alleviation. These factors include the extent to which the microfinance institution facilitates social interaction and personal trust among its clients (Cassar et al., 2007; Feigenburg et al., 2010; Karlan, 2007), and the level of practical business support afforded by the microfinance provider throughout the lending process (Karlan and Valdivia, 2011).

Compared to the extensive body of work examining the impact of microfinance schemes on loan repayment and poverty alleviation, there is a dearth of literature as to whether microfinance provision influences the creation of new businesses and growth of existing businesses. Although development economists have begun to investigate such issues through empirical work (Banerjee et al., 2010; Crepon et al., 2011; Karlan and Zinman, 2011) the findings of such research are inconclusive, and there has been limited focus on the underlying mechanisms which may explain how microfinance influences entrepreneurial activity. Given controversy as to whether microfinance contributes to entrepreneurial activity, management scholars have called for an increased focus on how and why some microcredit clients create successful enterprises while others do not (Ahlstrom et al., 2011; Bruton et al., 2010).

The present study seeks to address this gap and make a distinct contribution to the entrepreneurship literature through developing a theoretical model which identifies psychological and social capital as mechanisms by which microfinance may lead to higher levels of entrepreneurial activity and improved entrepreneurial outcomes among clients. Although original microfinance models, such as the Grameen Bank in Bangladesh, were based on the premise that the poor primarily lacked money, access to financial capital alone cannot ensure successful entrepreneurship (Berge et al., 2011; De Mel et al., 2008). As with other forms of entrepreneurship, the success of microcredit may depend also on individual entrepreneurs’ skills, mindset and social ties, including their level of social capital and psychological capital to pursue business development. The combined force of different forms of capital may allow even the smallest firms to develop a competitive advantage, consistent with the resource-based view of the firm (Luthans and Youssef, 2004). To this end, many microfinance institutions are exploring integrated ‘credit plus’ programmes that provide various types of practical and social support to clients, in addition to providing financial capital.

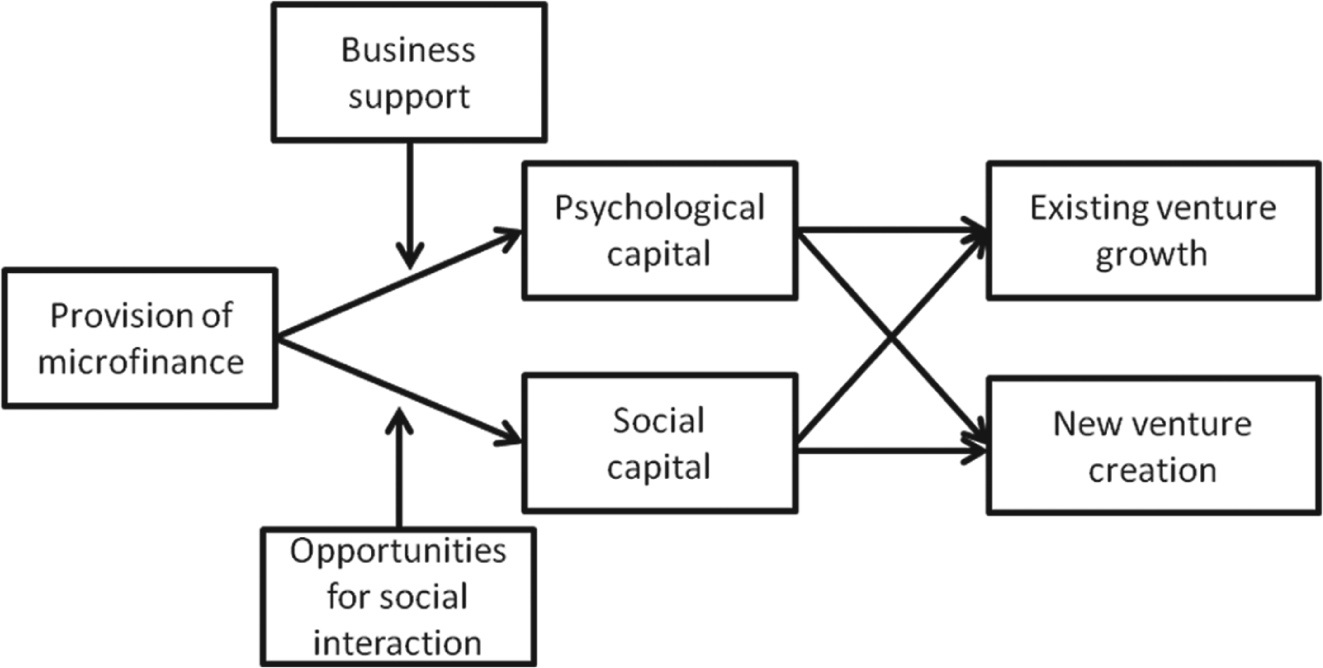

Drawing on previous literature, we argue that microfinance provision, along with the support and opportunities for interaction afforded to clients throughout the lending process, can create positive conditions for psychological and social capital to flourish. This, in turn, can stimulate new venture creation and contribute to the growth of existing ventures, especially for poor entrepreneurs who may have less access to all forms of capital (financial, social and psychological). Specifically, we propose that the extent to which microfinance provision will enhance psychological and social capital is contingent on the business support given to the client by the microfinance institution, and the extent to which it facilitates social interaction among clients throughout the lending process. The theoretical framework for this study is presented in Figure 1.

Theoretical framework.

The conceptual framework and research propositions developed in this study should be useful to both policymakers and microfinance providers, by helping them to understand the mechanisms by which microfinance provision can promote new venture creation and accelerate existing venture growth. It will provide them with a reference to consider when designing microfinance initiatives to enhance the well-being of clients and maximise entrepreneurial outcomes. It is also hoped that the theoretical framework will prove to be a useful guide for future research by linking the domains of entrepreneurship and organisational psychology.

Microfinance in emerging economies

Despite rapid growth in the global economy over the last three decades, as much as one-third of the world’s population is still estimated to live in poverty, earning less than US$2 per day (Chen and Ravallion, 2008). A significant percentage of these individuals are located in large economies such as China and India, which have been the key drivers of growth in emerging markets. There is some debate in the literature about what constitutes an emerging economy. This study follows Hoskisson et al. by defining emerging economies as ‘low income, rapid growth countries using economic liberalization as their primary engine of growth’ (2000: 249). They include those economies that have undertaken economic reform aimed at addressing poverty and recorded sustained economic growth (Tracey and Phillips, 2011), as well as numerous transition economies adopting greater market liberalisation. 1

Within emerging economies, microfinance seeks to connect more people to market opportunities by providing small-scale financial services to low-income clients who otherwise may lack access to formal banking services (Bruton et al., 2011). This discussion refers to microfinance in the sense of unsecured microcredit loans used to foster small business development, typically among poor entrepreneurs lacking significant business management experience. Historically, this group has lacked sufficient collateral to obtain small business loans. In addition, the high cost of screening and monitoring small loans for geographically dispersed, poor clients reduces profitability, thus constraining lending activity by financial institutions. As an alternative to bank lending, the microfinance industry has grown across the globe over the past 10 years, improving access to capital for millions of poor citizens in emerging economies (Midgley, 2008). As microfinance has expanded, services have grown to include loans for consumption (such as food, tuition, mortgage and weddings), insurance, savings deposits, remittances and mobile banking services, which are not specifically dealt with here.

The macro environment also affects our operating definition of microfinance. As discussed in greater detail in the section on social capital, this study focuses on settings that are underdeveloped or semi-developed in terms of commercialisation and access to economic opportunity. 2 It then constructs a model that is applicable to a range of emerging and transition economies, as long as other criteria regarding microfinance are met. These criteria include a loan level at below 1 to 1.5 times a client’s annual income, limited business experience of the entrepreneur, and low levels of institutional development in the area in which the entrepreneur is based.

While provision of microfinance capital seems to make sense in impoverished environments, no conclusive evidence exists as yet to establish that microfinance is a successful development strategy (Armendáriz and Morduch, 2010; Odell, 2010). Existing studies, primarily randomised controlled trials, have been criticised for faulty or incomplete research design (Duvendack et al., 2011; Roodman, 2012). In addition to lack of proven impact, microcredit – particularly in India, Bangladesh and Mexico – has been criticised for high interest rates, the use of loans for personal consumption, the creation of debt traps for the poor and sometimes, the tragic effects of intense pressure for repayment from loan officers or loan groups (Roodman, 2012).

Given this conflicting evidence, the model proposed in this article explores the processes by which microcredit loans may lead to entrepreneurial success under certain conditions, with the lack of these conditions suggesting why the findings from previous studies do not provide conclusive evidence of the impact of microfinance on entrepreneurial outcomes. A testable model is useful to unravel the conditions under which microfinance might have the greatest possible impact.

The role of microfinance in promoting entrepreneurial activity

Microfinance is a new and relatively under-researched domain in the entrepreneurship literature. As a result, entrepreneurship scholars have called for deeper exploration of the role played by microfinance in terms of stimulating entrepreneurial activity and new venture creation (Bruton et al., 2011; Khavul, 2010). Recent empirical studies have begun to identify the factors that influence the success of microfinance schemes through qualitative research (Bruton et al., 2011; Siwale and Ritchie, 2012). For example, Bruton et al. (2011) propose that the success of microfinance provision in terms of creating high-performing businesses will depend on the behaviour and outlook of clients, including their future orientation, decision-making discretion and ability to manage relationships with others in their social network. Taking a different perspective, Siwale and Ritchie (2012) examine the role of the loan officer in microfinance development in terms of facilitating the participation and empowerment of clients. However, these studies have yet to develop an overarching framework to examine the factors that link microfinance provision to entrepreneurial outcomes, and test the framework via quantitative work. Although development economists have begun to examine the impact of microfinance provision using randomised experiments, the findings of prior empirical work are inconclusive (Banerjee et al., 2010; Crepon et al., 2011; Karlan and Zinman, 2011). For example, although Crepon et al. (2011) and Banerjee et al. (2010) find a positive impact of microfinance provision on the business income and profits of Moroccan and Indian entrepreneurs, Karlan and Zinman (2011) find that expanded access to microfinance credit in the Philippines led to a reduction in the number of businesses run by entrepreneurs and the number of people employed. Other work examining the impact of one-off financial grants on entrepreneurial outcomes also reveals inconclusive results (De Mel et al., 2009, 2012b; Fafchamps et al., 2011). For example, De Mel et al. (2009, 2012b) find that the provision of one-off financial grants to Sri Lankan micro-enterprise owners has a bigger impact on the profitability of male rather than female-owned businesses. Similarly, Fafchamps et al. (2011) find that one-off grants, especially in-kind rather than cash grants, have a bigger impact on male-owned rather than female-owned businesses. In addition to inconclusive empirical findings, the extant empirical work by development economists has not sought to identify the mechanisms by which microfinance provision influences entrepreneurial outcomes.

Propositions

The following sections develop a series of research propositions to be tested in the future, examining how microfinance provision may engender positive entrepreneurial outcomes in emerging economies through eliciting higher levels of psychological and social capital, and the situations in which it will have the biggest impact. An overall framework utilising social capital and psychological capital is particularly relevant in an emerging economy context, given that poor entrepreneurs operating in these settings are generally resource-constrained, lacking financial and other forms of capital required to foster economic opportunity. For example, scholars have pointed to the value of social capital or network ties in facilitating micro-lending relationships (Adekunle, 2011), especially when there is no material collateral (Ito, 2003; Ledgerwood, 1999). Social capital is relevant for entrepreneurs involved in either lending or applying for individual loans, (Attanasio et al., 2011). Guo and Miller (2010) note that network ties help entrepreneurs to overcome resource deficiencies, while research on venture capital in emerging economies highlights the value of social capital and informal ties in environments where institutions are weak or ineffective (Bruton et al., 2010).

In addition, in emerging economy settings, psychological capital may be threatened by high levels of risk, uncertainty and anxiety (Hmieleski and Carr, 2008; Welter and Smallbone, 2011), economic stress such as unemployment (Cole et al., 2009a) and the lack of a supportive operating climate exacerbated by the longstanding economic vulnerability of potential microfinance clients. The literature points to the need for a positive, supportive environment and interventional training to reinforce business performance through enhancing psychological capital (Luthans et al., 2006, 2008, 2010). Moreover, Luthans and Youssef (2007) have proposed that psychological capital has the greatest potential for producing positive outcomes, such as enhanced performance when conditions are less favourable.

Given these findings, the model presented in this article is most applicable for poor entrepreneurs with limited capital, experience and connections, who may be forced into entrepreneurship due to a lack of other economic opportunities in the immediate vicinity. Understanding the role of these other forms of capital in the entrepreneurial process would contribute to resolving the debate over whether microfinance actually works, and under what conditions.

Microfinance and psychological capital

Microfinance offers the poor a chance to address poverty, generate income and seize entrepreneurial opportunities. We argue that the provision of loans will not only have a direct effect on entrepreneurial activity by increasing financial capital, but also will have a positive impact on entrepreneurial outcomes by engendering greater psychological capital in clients. This is particularly likely in markets where true credit demand exists. While over-supply is an issue in some markets where clients suffer from over-indebtedness, globally the industry is considered to have a supply gap (Schicks, 2011) in which a significant number of potential clients are not receiving microfinance loans (Armendáriz and Labie, 2011). A case in point is China, where demand for financial capital generally outstrips supply in rural areas (Tang, 2011). Indeed, one study notes that ‘the rural market is begging for more credit’ (Wharton Business School, 2007: 1), as supply in these regions is constrained by government caps on interest rates and institutional challenges. In such cases, meeting the need for credit at the bottom of pyramid is likely to have a positive impact on both psychological capital and entrepreneurial outcomes.

Psychological capital refers to a positive psychological state that an individual develops over time. It consists of four main dimensions, describing the extent to which an individual:

has confidence (self-efficacy) to work towards success in challenging tasks;

exhibits a positive attitude (optimism) about succeeding at present and in the future;

exhibits persistence towards achieving goals and when necessary, redirects paths to goals (hope) in order to have a greater chance of success; and

shows the ability (resilience) to bounce back and achieve success when faced with challenges and adversity (Luthans et al., 2007).

Luthans (2002) initially developed the theory of psychological capital to capture an individual’s psychological capacities which can be measured, developed and exploited for individual or organisational effectiveness. For a construct to be included as a dimension of psychological capital, Luthans and his co-authors provide a set of inclusion criteria; it needs to be grounded in theory or research, have valid measures and must be state-like (as opposed to trait-like) therefore, having the potential to be developed through training and intentional practice (Luthans et al., 2008).

Despite some explorations of the construct of psychological capital within an organisational setting (Avey et al., 2010) relatively little attention has been afforded to the factors which may elicit psychological capital among entrepreneurs, especially in the nascent stages of the entrepreneurial process. Given the stressful and uncertain institutional environment that often exists in emerging economies (Welter and Smallbone, 2011), in which entrepreneurs find it difficult to leverage financial resources outside their immediate family network, microfinance provision should strengthen psychological capital and reduce the levels of stress and anxiety arising from limited access to financial resources. Poor entrepreneurs within impoverished settings in particular may be lacking in the forms of capital needed to succeed in business and may be driven to entrepreneurship not by opportunity, but necessity (Bradley et al., 2012; McMullen et al., 2008), given few options in the immediate environment for education, social connections or formal employment (Bhola et al., 2006; Minniti and Bygrave, 2005). Having access to greater financial security and resources should help to make entrepreneurs more resilient in the face of challenging situations, more optimistic and hopeful about the future, and more confident in their ability to overcome difficulties (Crabb, 2008). Of course, loan provision may raise anxiety levels simultaneously, as poor entrepreneurs face tight repayment schedules enforced by microfinance institution officers acting as debt collectors (as highlighted by Siwale and Ritchie, 2012). However, Siwale and Ritchie also find that the client–loan officer relationship positively influences client empowerment and outcomes. In particular, where credit demand is high and a supply gap exists (Schicks, 2011; Tang, 2011), we argue that the net effect of lending on psychological capital is positive.

Psychological capital and business support

This study proposes that the extent to which microfinance leads to higher psychological capital among clients is dependent on the extent to which business training or support is provided to the client by the microfinance institution during the lending process. The need to support the development of business skills for low-income entrepreneurs is well established in the literature. Berge et al. (2011) find that human capital, in terms of a lack of business knowledge and skills, is a greater constraint to entrepreneurial success than financial capital. Similarly, Odell (2010) finds that micro-entrepreneurs’ lack of knowledge and experience in launching and managing profitable small business can hamper business development. For example, residents in India and Indonesia have demonstrated very low financial literacy which impacts on business success rates (Cole et al., 2009b). Developing entrepreneurial skills is vital to success for business at the base of the pyramid (Afrin et al., 2010). For inexperienced entrepreneurs operating at the lowest socioeconomic levels, often in remote rural settings, external organisations such as microfinance institutions may be a critical source of business knowledge, practical tools and strategies, in addition to providing basic financial services. Indeed, a review of microfinance programme results conducted by the Asian Development Bank calls for microfinance providers to adopt a more integrated approach to economic development by offering more vocational and technical training and market information services (Zhuang et al., 2009). Zhuang and colleagues argue that microfinance programmes should be accompanied by the provision of training and capacity building and assistance in accessing markets and technologies. Similarly, Datar et al. (2008) encourage a greater focus on supporting client enterprises, rather than focusing primarily on loan repayment; they argue that this should be through the provision of a wider range of services than is offered at traditional financial institutions, such as financial education, management training, value chain support and social services.

In response to this established need, microfinance providers worldwide are experimenting with training and support services for nascent entrepreneurs, an idea that is being increasingly examined in the literature (Afrin et al., 2010; Goldmark, 2006; Karlan and Valdivia, 2011; Sebstad and Cohen, 2001). Training can take many forms, from one consultation to a year-long programme, individual or group-based, and may focus on financial literacy, business administration, marketing, accounting or vocational and sector-specific skills. As noted by one international non-governmental organisation (CARE International, 2012), such programmes have the potential to increase productivity, income and diversification, and to help clients overcome non-financial constraints to business development.

In addition to reducing stress and feelings of uncertainty, we argue that microfinance programmes that provide business support will not only enhance the knowledge and skills of entrepreneurs but also make them more confident, optimistic, hopeful and resilient in the face of challenging conditions. The value added by such support is likely to be greater for poor entrepreneurs operating in resource-constrained emerging economy settings, who may be lacking in psychological capital from the start. However, microfinance providers face some risks in establishing such integrated programmes (also called ‘credit plus’ to distinguish from the more minimalist ‘credit only’ models). These include the cost of provider and client time and resources invested in business support activities, as well as the real or perceived liability for client business outcomes when the microfinance provider forwards business advice.

The integration of business support services with microfinance loans naturally raises a question about the efficacy of such services. In this regard, there is growing agreement in the literature that the provision of business training might impact positively on the entrepreneurial outcomes of micro-entrepreneurs in emerging economies, and accentuate the impact of microfinance provision in terms of increasing loan repayment rates and improving entrepreneurial outcomes (Bruhn et al., 2010; McKenzie and Woodruff, 2012). For example, Marconi and Mosley (2006) found that community-based microfinance institutions that took a ‘credit plus’ approach in Bolivia experienced lower default rates in a financial crisis than those that provided credit only. Field et al. (2010) found positive income effects for female clients invited to a two-day training programme with an Indian microfinance institution. Similarly, Biosca et al. (2011) found that the business development services offered to microfinance clients in Mexico increased their income. Studying the impact of a business and financial literacy training programme on young entrepreneurs in Bosnia and Herzegovina, Bruhn and Zia (2011) found that although it did not increase business survival, training led to improvements in business practices, business performance and sales. Gine and Masuri (2011) found that business training led to increased business knowledge and better business practices among Pakistani entrepreneurs. Finally, Klinger and Schündeln (2011) found that the provision of business training in three Central American countries increased the probability that a participant would start a new business or expand an existing business.

However, other studies suggest that the provision of business training might not have a positive impact in all situations. For example, Cole et al. (2009b) found minimal benefits from a small-scale financial literacy programme in Indonesia. Berge et al. (2011) found mixed effects for an ambitious business training programme in Tanzania: men’s financial practices improved, as did their business results, while women’s remained the same. Karlan and Valdivia (2011) conducted a large-scale, randomised evaluation of microfinance clients in Peru, in which the lender used a third-party agency to incorporate training into client meetings over the course of several months. They found greater knowledge and improved business practices, yet mixed results for sales and revenue. Examining the impact of business training on female entrepreneurs in Sri Lanka, De Mel et al. (2012a) found that it had an impact on the business practices of existing entrepreneurs, but did not lead to increased sales, profits and capital stock. However, when combined with a grant of money, it led to increased business profitability for a period of eight months. In addition, they found that for women interested in starting a business, provision of business training sped up the process of opening a business and led to higher profitability and improved business practices for those starting up. Conducting randomised field experiments in the Dominican Republic, Drexler et al. (2010) found that although the provision of simplified, rules-based financial training led to improvements in business practices and increased sales among micro-entrepreneurs, the provision of fundamentals-based accounting training did not.

Despite a growing focus on the impact of training on the success of microfinance schemes in the recent literature, previous work has not examined whether microfinance provision, coupled with client support and training, directly impacts on the psychological capital of clients. However, there is growing evidence that psychological capital can be developed through training interventions for employees (Luthans et al., 2006, 2010), and that a supportive organisational environment can influence psychological capital development and employee performance in an organisational setting (Luthans et al., 2008).

Given these findings, it is reasonable to conclude that provision of both financial capital and business support programmes would help to create such a positive climate for entrepreneurs as well as employees, and lead to higher levels of psychological capital. Based on the above literature, the following research propositions are developed:

P1: Microfinance provision can lead to higher levels of psychological capital (self-efficacy, optimism, hope and resilience) among clients. P2: The extent to which microfinance provision impacts on the psychological capital of clients is dependent upon the level of business support afforded to them during the lending process.

Psychological capital and entrepreneurial outcomes

By fostering higher levels of psychological capital among clients, microfinance schemes should positively affect new venture creation and the performance of existing ventures. Psychological capital has been shown to endow individuals with the resources needed to deal with the emotional challenges that are part and parcel of the entrepreneurial process, especially in dynamic environments characterised by high levels of risk and uncertainty, such as those faced by nascent entrepreneurs in emerging economies (Hmieleski and Carr, 2008). Prior research has established that those high in psychological capital tend to create strong emotional connections with others in their social networks (Fredrickson, 2001). These supportive relationships should assist in the entrepreneurial process and allow individuals to succeed in situations that others might find overwhelming (Corey et al., 2003).

Although there has been limited examination of the factors which may engender the development of psychological capital in entrepreneurs, a small number of studies have begun to examine its impact on new venture performance (Hmieleski and Carr, 2008) and the growth aspirations of entrepreneurs (Kauko-Valli et al., 2009). For example, Hmieleski and Carr (2008) found that psychological capital was positively related to new venture performance and that it explained a significant amount of the variance in performance above and beyond traditional forms of human and financial capital. This was especially true for entrepreneurs operating in dynamic industrial environments. Kauko-Valli et al. (2009) found that two dimensions of psychological capital, self-efficacy and hope, have a positive effect on the growth aspirations of entrepreneurs. Other studies have begun to uncover relationships between the four sub-dimensions of psychological capital and entrepreneurial outcomes. For example, Adekunle (2011) used personal agency belief to measure business performance and found that aspects such as self-efficacy among Nigerian entrepreneurs predicts growth in savings, employees, profits and sales. The following sections review each of the dimensions of psychological capital, and examine how they might influence the growth of existing ventures and new venture creation in an emerging economy setting.

Self-efficacy is based on Bandura’s (1997) social cognitive theory, and refers to an individual’s belief in their ability to mobilise motivation, cognitive resources and courses of action in order to achieve high levels of performance in the tasks that they undertake (Stajkovic and Luthans, 1998). Individuals with low self-efficacy generally believe that they will not succeed in addressing difficult challenges whereas, those with high self-efficacy generally believe that difficult challenges are surmountable and generally persist towards the achievement of goals in the face of adversity. Similar to other psychological dimensions, self-efficacy is considered to be a ‘state-like’ characteristic which can be developed over time. A number of studies have found a positive relationship between entrepreneurial self-efficacy and both new venture growth and performance (Adekunle, 2011; Baum and Locke, 2003; Baum et al., 2001; Chandler and Jansen, 1992; Hmieleski and Corbett, 2008; Segal et al., 2005). These findings indicate that entrepreneurs ranking highly in self-efficacy are more likely to set challenging growth targets and persevere towards achieving the goals that they set for themselves. Given the high levels of risk and uncertainty in emerging economies, one might expect the self-efficacy of entrepreneurs to be beneficial in allowing them to persevere in the entrepreneurial process in the face of great odds.

Optimism pertains to an individual’s expectancy of positive outcomes (Carver and Scheier, 2002). Individuals high in optimism build positive expectancies that motivate them to pursue their goals and cope with challenging situations, whereas pessimists are hindered by negative expectancies and self-doubt. Compared to self-efficacy, optimism tends to be more stable in individuals across time and context. However, it can vary within individuals as a result of positive experiences, and has been shown to be amenable to development up to a certain limit (Seligman, 1990). Previous research highlights that optimists are more able to persist towards the achievement of goals when faced by challenges than pessimists, who tend to give up in the face of adversity (Scheier et al., 2001). Existing evidence suggests that optimism might have only a positive effect on the performance of individuals up to a certain level, after which negative returns might set in (Brown and Marshall, 2001). For example, Hmieleski and Baron (2009) find a negative relationship between entrepreneur optimism and new venture performance. They argue that this may occur because entrepreneurs typically rank higher than the general population on the optimism dimension, and highly optimistic entrepreneurs are likely to undervalue new information and learn less from previous experience than moderately optimistic entrepreneurs. However, in an emerging economy context, where there are significant life challenges and limited institutional support for entrepreneurs, especially in poor settings, one might expect there to be lower levels of optimism among entrepreneurs. As a result, optimism is expected to have a greater positive impact on existing venture performance, and to stimulate more new venture creation than in the context of mature economies, where there is greater institutional support.

Hope has been defined as ‘a positive emotional state that is based on an interactively derived sense of successful (a) agency (goal-directed energy) and (b) pathways (planning to meet goals)’ (Snyder et al., 1991: 287; Snyder et al., 1996). Agency refers to the willpower or motivation to succeed at a given task in a specific context, and pathways refer to the way or means by which to accomplish a given task. For an individual to possess hope, they need the will to succeed in a given task (agency) as well as a viable means (pathway) to achieve it (Luthans et al., 2008). Although hope has been linked to employee performance in previous studies (Luthans et al., 2005; Youssef and Luthans, 2007), limited research has investigated its impact in an entrepreneurial setting. Hope might be expected to influence entrepreneurial outcomes, as previous work on entrepreneurial improvisational behaviour and entrepreneurial bricolage indicates that setting goals and envisioning multiple pathways to achieve those goals are factors influencing entrepreneurs’ success (Baker and Nelson, 2005; Hmieleski and Corbett, 2008). Given that emerging economies are characterised typically by resource-poor environments, where entrepreneurs are forced to overcome institutional deficits and span institutional voids by engaging in high levels of improvisational behaviour and bricolage activity (Mair and Marti, 2009), hope should be expected to influence venture performance positively and sustain new venture growth to a greater extent than in mature economies.

Resilience refers to an individual’s capacity to bounce back from adversity, uncertainty, risk or failure (Masten and Reed, 2002). Individuals high in resilience show the ability to adapt and cope in the face of negative experiences, as they are typically open to new things, flexible to changing demands and emotionally stable (Tugade and Fredrickson, 2004). As with the other psychological capital dimensions, there is growing evidence that resilience is state-like and open to development (Coutu, 2002). Previous research has shown resilience to be an important factor in enabling individuals to navigate turbulent and demanding workplaces successfully (Tugade and Fredrickson, 2004), and has been found to influence employee performance in the workplace (Luthans et al., 2005). Given the fact that the ability to persevere in the face of adversity is critical to all entrepreneurs who are faced with significant resource constraints (Markman et al., 2005), resilience should be expected to have a positive influence on the growth of existing ventures and new venture creation. This is especially true for micro-entrepreneurs within an emerging economy, where resources are severely constrained and entrepreneurship may be the only choice, whereas already-resilient individuals in developed settings will be more likely to self-select entrepreneurship. The above literature leads to the following proposition:

P3: Psychological capital (self-efficacy, optimism, hope and resilience) will impact positively on new venture creation and existing venture growth.

Microfinance and the social capital of entrepreneurs

In addition to engendering higher levels of psychological capital among clients, microfinance schemes, in particular those based on group-lending methods or encouraging participation, should elicit greater social capital, given that they typically facilitate social interaction between clients (Phan, 2009). Social capital refers to the sum of actual and potential resources embedded in social networks that are crucial to the functioning of individuals (Burt, 1992; Coleman, 1988; Nahapiet and Ghoshal, 1998). It includes both the structure of the network and the assets that may be leveraged from the network (Burt, 1992). The social capital inherent in an entrepreneur’s networks with other economic actors facilitates access to information in a timely manner thus, promoting opportunity identification and exploitation (Tang, 2010).

Drawing upon Nahapiet and Ghoshal’s (1998) work, we highlight two dimensions of social capital that may be fostered through microfinance provision; structural capital and relational capital. These dimensions of social capital have been widely investigated in prior studies, and have been shown to facilitate the sharing of knowledge and resources between individuals (Li et al., 2007; Liao and Welsch, 2005). Structural capital refers to the pattern of connections between actors within a network (Burt, 1992). Network ties between actors facilitate timely access to relevant resources and information which are critical to the identification and exploitation of entrepreneurial opportunities (Adler and Kwon, 2002; De Carolis et al., 2009; Shane and Venkataraman, 2000). The resources and information made available by an entrepreneur’s networks have been shown to enhance greatly the survival and performance of new ventures in both developed and emerging economies (Bruderl and Preisendorfer, 1998; Honig, 1998). In contrast, relational capital refers to connections which have been developed through an individual’s interactions with other actors in their social network over an extended period of time (Granovetter, 1992). While structural capital refers to the presence of network ties that enhance access to resources and information and the position of the individual within the network, relational capital focuses on the nature of relationships that people have in terms of respect, trust and emotional support: that is, the quality of network ties (Liao and Welsch, 2005). Although entrepreneurs might hold similar positions in a network, the strength of their ties with other members of the network might differ, which in turn will affect their ability to obtain access to external information and resources.

Microfinance schemes, in particular those with a group-based lending methodology or training programmes encouraging participation and involvement, should lead to greater structural and relational social capital between clients. Clients who participate in lending groups that meet on a regular basis have opportunities to enhance both the number and quality of network ties that they possess with other entrepreneurs and the wider community: that is, their structural and relational capital. Included in such microfinance schemes are not only non-governmental organisations practising traditional group lending, but also other microfinance institutions such as rural credit cooperatives and village banks that operate through a principle of cooperative financing and self-help. Increasingly, a range of institutions are embedding some form of management or business training and peer-group interaction into the lending process as part of a more integrated approach to microcredit (Karlan and Valdivia, 2011; Sebstad and Cohen, 2001). Indeed, the link between microfinance provision and social capital has obtained some degree of support from recent studies (Feigenburg et al., 2010; Mosley et al., 2004; Sanyal, 2009). Using data from microfinance clients in Peru, Feigenburg et al. (2010) demonstrated the positive impact of group-based lending on the social capital of clients. They find that weekly group meetings of microfinance clients, in which loan repayments are made, led to regular social interaction between individuals within the client group outside of these meetings, and subsequently to higher levels of social capital. After five months of membership within a weekly lending group, clients were 90 percent more likely to have met other group members in their homes, and 40 percent more likely to meet each other outside of meetings, compared to clients in monthly lending groups. The groups meeting more frequently had lower loan default rates and greater informal risk-sharing. Mosley et al. (2004) found similar results from work conducted in Russia, Romania and Slovakia. They demonstrated that microfinance provision leads to higher levels of social capital between members of the lending group, whether or not they are in receipt of group loans. In addition, membership in the microfinance association was found to influence the extent to which individuals engaged in informal political participation: it assisted them in extending their social capital beyond members of the immediate lending group. Sanyal (2009) found that microfinance programmes based on group lending in West Bengal, India, had higher levels of structural and relational social capital between individuals of the lending group, which positively influenced their collective social behaviour.

However, the potentially negative effects of group lending must be acknowledged. There is debate as to whether lending groups are a true source of social and business support, given the complex nature of social capital and the transactional nature of lending groups (Armendáriz and Morduch, 2010; Bruton et al., 2011). Group members may be linked to each other only in a transactional way in order to gain access to loans, rather than generating true social ties. In addition, lending groups can be a source of negative peer pressure to repay loans, as members seek to avoid liability for failed members (Montgomery, 1996). Nonetheless, based on findings to date, the overall influence of group lending appears to be more positive than negative, to a degree that is worthwhile testing further within this model. It is useful also to look at individual lending models that foster participation in other ways, such as via business training and support programmes.

Based on the above findings, we argue that the extent to which the microfinance provider affords regular opportunities for clients to interact with one another will positively affect the social capital of clients. This leads to the following research propositions:

P4: Microfinance provision can lead to higher levels of social capital (structural and relational) among clients. P5: The extent to which microfinance provision affects the social capital (structural and relational) of clients is dependent upon the extent to which the microfinance provider facilitates social interaction among clients.

Social capital and entrepreneurial outcomes

Microfinance schemes, especially those involving group lending or other participatory activities, should have a positive impact on new venture creation and the performance of existing ventures by fostering higher levels of social capital among clients (Midgley, 1998; Phan, 2009). Arguably, social capital facilitates the sharing of knowledge and resources between clients (Cope et al., 2007; Maclean, 2010; Roomi, 2013), and leads to an improvement in business practices, identification of new opportunities and improved risk management strategies (De Carolis et al., 2009; Gomez and Santor, 2001; Phan, 2009). Work by Gomez and Santor (2001) supports the applicability of such assertions in the microfinance arena. They found that both the quantity of social ties (structural capital) and quality of social ties (relational capital) of microfinance clients enhanced entrepreneurial performance in terms of self-employment incomes. However, other studies have revealed mixed results. Maclean (2010) found that social capital had a positive impact on income generation for certain groups of microfinance clients yet, had no effect on other groups, suggesting that group characteristics are important. A study by Bradley et al. (2012) of Kenyan clients revealed contrasting findings. Although structural social capital, as measured by the quantity of network ties between the microfinance client and other members of the lending group, was found to lead to higher levels of innovation, it did not influence firm performance. The lack of a positive impact of structural capital on firm performance in this study might result from the fact that its effectiveness depends upon the position that the individual maintains in the social network, and the diversity of people with whom the client is able to build network ties as a result of membership in the lending group. This study also failed to examine the strength of the ties (relational capital) between the client and members of the lending group.

A positive relationship between structural social capital and entrepreneurial outcomes might be expected, given that network ties between the entrepreneur and a diverse range of actors within their social network exposes them to different ideas and wider sources of information, which should be useful when making decisions regarding the future direction of their business (Birley, 1985; Cope et al., 2007; Ramos-Rodriguez et at., 2010). Given a lower level of social capital to begin with, poor entrepreneurs in emerging economies with limited knowledge of, or experience in, a particular industry especially should benefit from accessing a wide range of information and advice through their network ties (Roomi, 2013). Relationships with others in their social network, especially entrepreneurs who have good connections with government authorities, should heighten their ability to obtain relevant and timely knowledge and help to overcome institutional constraints.

Relational social capital engendered through group-based lending should influence the creation and subsequent performance of new ventures, particularly within the weak institutional contexts typical of emerging economies, for two main reasons. First, relational capital facilitates the exchange of information between individuals due to the fact that it embodies trust, cooperation, reciprocity and obligation between individuals (Granovetter, 1985; Uzzi, 1996). The greater the level of interaction with others in the social network, the easier it is for an entrepreneur to develop trust and gain access to information and resources from the entrepreneurial network (Tang, 2010). Second, relational capital improves access to external information and resources by enabling entrepreneurs to learn appropriate business behaviour, and by enhancing the legitimacy of new ventures via association with individuals and organisations with a positive reputation. Legitimacy refers to the ‘generalized perception or assumption that the actions of an entity are desirable, proper or appropriate within some socially constructed system of norms, values, beliefs and definitions’ (Suchman, 1995: 574). It should enable the entrepreneur to access the necessary resources to survive and develop, and provide a means to overcome the liability of newness that contributes to new venture failure (Tang, 2010). Relational capital plays a particularly important role in emerging economies due to scarcity of resources and the lack of developed market institutions to direct and govern economic exchange (Le and Nguyen, 2009). Recent empirical research highlights the importance of relational capital to overcoming deficient institutional environments that exist in emerging economies (Ren et al., 2009).

It should be noted that the setting matters in terms of access to social capital. For this reason, the model presented in this article applies most closely to ‘semi-developed’ locations in rural locations or urban settings which have not been fully commercialised in terms of economic infrastructure and access to opportunity. Even at the lowest levels, entrepreneurs operating in highly developed urban areas often have significant access to social capital that is lacking in less developed regions. The above literature leads to the final proposition:

P6: Social capital (structural and relational) will impact positively on new venture creation and existing venture growth.

Structure of future research

Given the adoption of various models of microfinance in emerging economies, this study proposes a set of testable propositions in order to understand better whether and how microfinance actually works, and in which contexts it may have the biggest impact on entrepreneurial outcomes. Despite an otherwise rich literature from developmental economists, there continues to be no clear empirical evidence that microcredit loans reliably promote business development and expansion. While management scholars have begun to examine the factors which may influence the success of microfinance schemes, only a handful of studies exist which apply management theory to microfinance, and thus management scholars have called for greater attention to the topic (Khavul, 2010; Phan, 2009).

This article contributes to such calls by proposing psychological and social capital as mechanisms by which microcredit loans may foster the creation of new businesses and expansion of existing businesses. Although both psychological and social capital have been examined previously in relation to entrepreneurship, no previous study applies these concepts to poor entrepreneurs, whose forced entrepreneurship and resource-constrained environments ensure they lack multiple forms of capital. We believe that management theory offers a particularly effective approach to explanatory forms of research on microcredit. As discussed by Roodman, an explanatory approach can ‘help us understand the mechanisms that link cause and effect’ (2012: 156). This contrasts with and complements previous studies that address the direct impacts of microfinance on client treatment groups, which may be conducted more appropriately by micro-economists.

Having studied microfinance in emerging economies for several years, we acknowledge the challenges of collecting reliable data among low-income clients in the poor, often remote or chaotic environments highlighted by microfinance scholars (Khavul et al., 2013). This observation is based on our experience primarily in Asia, collecting data from microfinance clients, loan officers, senior managers and directors of microfinance non-governmental organisations, microcredit companies, village township banks and rural credit cooperatives, as well as some commercial microfinance companies that provide loans at the microcredit level.

In terms of research design, options to explore and test the propositions from an explanatory management perspective include qualitative interviews and randomised quantitative survey work. Here, Roodman (2012) points to the limitations of both approaches. Qualitative work offers credibility and depth but faces the danger of subjectivity, and is difficult to extrapolate to other settings. In contrast, randomised surveys provide greater breadth and representation, but may sacrifice depth, precision and nuance.

Weighing these drawbacks and advantages, we recommend an approach combining the benefits of both. First, in-depth qualitative interviews and case studies may be conducted with the purpose of developing and fine-tuning categories and questions that can be developed later into a survey instrument. For example, the nature or type of business and social support may differ depending on the model of microfinance being practised, and the cultural context of the microfinance institution and its clients. Second, survey research may be conducted to test empirically the propositions developed in this theoretical model. Preferably, this should be done by face-to-face administration of the survey in an interview-style format, rather than by self-administration by participants, for two main reasons. First, in certain emerging economy environments where interactions tend to be relational rather than transactional, a relationship must be established in order collect data (Bruton and Ahlstrom, 2003). Moreover, many microfinance clients may not be able to read at a level sufficient to complete a survey independently. Second, survey data collection would ideally be conducted longitudinally. At time one, when microfinance clients receive the loan, researchers may collect demographic data and information about the loan. At time two, the end of the loan period, they may collect data on psychological capital, social capital and business support. Finally at time three, one year later, they may collect data on entrepreneurial outcomes.

Given this overall research design, there are numerous ways to structure an effective study. Selection of appropriate microfinance institutions is critical. In emerging economy settings, access to clients and microfinance institution personnel typically cannot be gained without an inside connection or established relationship with management; yet, these ties also can threaten the collection of accurate, unbiased data. We recommend extensive preliminary field visits to potential research sites to ensure that all criteria are in place: group lending (still widely used in many settings), client participation in meetings or social events, actual provision of business support in a consistent and measurable way, and a social and organisational context amenable to ongoing data collection by outsiders.

After meeting these criteria, sample selection is critical. This model is intended to apply to clients using microcredit for entrepreneurship, not consumption, and interview or survey candidates should be selected with this criterion in mind. In terms of data collection, different approaches have their strengths and weaknesses. First, researchers can visit clients in the field, usually at their place of business or occasionally at their homes. This allows for natural observation and some verification of business status, but can be extremely time and labour-intensive to generate a significant number of participants. In addition, loan officers may accompany researchers to assist the researcher to build trust and credibility with clients. However, this approach may inhibit negative responses. Second, data collection could be conducted at the microfinance headquarters, for example, as clients visit to apply for and repay loans or to attend meetings. This approach works best if data collection can be conducted independently without close monitoring by microfinance institution personnel. Clients not repaying loans or not attending events still need to be sought out, usually in the field, to avoid biasing the sample toward more successful, interactive subjects. Third, research could be conducted primarily through smaller branch offices, which may offer a higher degree of efficiency combined with more honest responses.

Conclusion

Over the past two decades, microfinance has gained increasing traction as a concept and practice to help alleviate poverty worldwide, particularly as a strategic alternative or complement to international development aid. Its proponents argue that microfinance has the potential to deliver the prospect of market participation and free enterprise to billions of people at the base of the economic pyramid. Meanwhile, critics assert that no solid evidence exists as yet that microfinance actually works to generate entrepreneurial activity and alleviate poverty.

In light of this debate, scholars, particularly development economists, continue to evaluate the impact of microfinance programmes. An important contribution for management scholars is to explore the detailed mechanisms of how microfinance schemes may foster success in emerging economy settings. Ultimately, social and economic historians will evaluate the extent to which microfinance has generated economic development. Here, we apply management theory in order to understand better the mechanisms by which microfinance can work and how it might be improved, in particular by bringing together and applying theories in entrepreneurship and organisational psychology.

This study introduces a conceptual framework and develops research propositions to guide future research about the manner and degree to which microfinance impacts on the entrepreneurial outcomes of poor clients in an emerging economy context. In doing this, it highlights the importance of two mechanisms, psychological and social capital, which may explain how microfinance provision affects new venture creation and existing venture growth. It also identifies factors which may contribute to the development of these constructs, such as level of business support and opportunities for client interaction afforded by the microfinance provider. We introduce this model in response to calls by researchers in the management field to investigate the factors which contribute to the success of microfinance initiatives, in terms of the processes by which they foster entrepreneurship (Khavul, 2010; Phan, 2009). We see a substantial opportunity for additional empirical research on the psychological and social mechanisms that might facilitate positive entrepreneurial outcomes among the billions at the bottom of the economic pyramid in emerging economies.

Footnotes

Funding

This research received no specific grant from any funding agency in the public, commercial or not-for-profit sectors.