Abstract

How, if at all, does financialisation affect small firms that have no direct exposure to capital markets? This article argues the need to address this lacuna empirically, conceptually and politically drawing on research from a qualitative longitudinal analysis of UK small businesses in bio-business and film and media sectors. We identify three potential conduits through which financialising principles and practices may be perceived, translated and resisted for owners, managers and staff. More broadly, the article argues that financial relations should figure more prominently and move from their relatively marginal location into the heart of socio-economic analysis of small firms. As such, the research connects with and extends an important social science tradition of research on managerial control in small firms to include issues of financialisation and financial governance.

Introduction

The concept of financialisation has become a significant feature of recent political, economic and cultural debate in contemporary capitalism, most especially in its Anglo-US constitution and manifestations. Much of the literature on financialisation has focused on its macroeconomic dimensions, while relatively less attention has been paid to its meso- and micro-achievement and repercussions (for exceptions, see Orhangazi, 2008; Tori and Onaran, 2015). Financialisation literatures have been developed, quite understandably, in the context of large capital-market-facing corporations (Baud and Durand, 2012; Froud et al., 2006; Lazonic and O’Sullivan, 2000). Extending this growing interest, we ask whether and how such financialising principles and practices are significant for some small 1 privately held firms that have no direct exposure to capital markets.

In what follows, we argue that extending financialisation literatures to consider small firms is important empirically, conceptually and politically. Empirically, the article investigates a selection of small firms and identifies three conduits through which small firm owners and employees may be indirectly exposed to, and affected by, financialising principles and practices. Moreover, the comparative research presented illustrates how contrasting sectoral contexts mediate how financialising principles and practices may be perceived, translated and resisted for owners, managers and staff (see Lapavitsas, 2011; Thompson, 2013), suggesting the need for more grounded, contextual understandings of financialising principles and practices that are sensitised to the heterogeneity of small firms.

Beyond this empirical novelty, however, there are wider conceptual stakes involved in thinking about financialisation and its effects on small firms. Debates about small firm relations with finance (debt and equity) have largely been framed by concerns about ‘funding gaps’ that may constrain the development of new firms. In such readings, finance is conceived in narrowly economic terms as an input to production. Yet, as Fraser et al. (2015) argue, a plethora of policy initiatives in the United Kingdom exist. These range from Small Firms Loan Guarantee (SFLG) to commissions on a lack of competition in the banking services for small- and medium-sized enterprises (SMEs; Cruikshank, 2000; Independent Commission on Banking, 2011) and, more recently, the provision of non-bank sources of finance since the financial crisis (Breedon, 2012). All have struggled with the sheer complexity of both the supply-side and, much less studied, cognitive elements of such funding gaps. Debates about financialisation have, arguably, served a useful purpose in galvanising scholars across the social sciences to interrogate the significance of finance in different domains of contemporary life (see Van der Zwan, 2014). More specifically within this article, attention to the macroeconomic, institutional and cultural elements of financialisation encourage small firm finance debates to engage with more holistic political–economic analyses that conceptualise firm finances as a set of social relations with repercussions that extend beyond supply-side/market failure issues (Coe et al., 2014; Dannreuther and Perren, 2013b; Fraser et al., 2015) to affect all areas of the firm. We deploy small firms as ‘a more diverse politico-intellectual terrain’ (Beck et al., 2016: 216) of financialisation and argue that a more holistic treatment of finance should become more prominent in socio-economic analyses of small firms. As such, the research connects with and extends an important social science tradition of research on managerial control in small firms (Barrett and Rainnie, 2002; Curran, 1990; Ram and Edwards, 2003; Thompson and Van den Broek, 2010) to include issues of financial governance (Fraser et al., 2015). Some of the political implications of such a holistic treatment of small firm finances are pursued in the conclusion.

The article is structured as follows. The section ‘Financialisation and small firms’ considers the intersection between small firm finance and financialisation literatures. The section ‘The research project and methodology’ explains the design of our qualitative, longitudinal research and the section ‘The financial(ising) contexts of small firms’ details how financial principles and practices are shaping small firm behaviour in the bio-business and then film and media sectors. The conclusion distils the key contributions for literatures on financialisation, small business finance and policy.

Financialisation and small firms

Finance is fundamental to how all organisations function. As Sayer (2001) commented,

However good the networking, however strong the reliance on information, economic survival for capitalist firms depends on costs and cash, though extraordinarily the socioeconomics literature says remarkably little about these things. (p. 699)

This state of affairs is remarkable, given that it has long been understood that firm size complicates the provision of finance (Kalecki, 1937). In the UK context, there are long-standing structural problems in the provision of debt and equity to support small firms (Bank of England, 2002; Bolton Committee, 1971; Cruikshank, 2000; Fraser et al., 2015; Macmillan Committee, 1931). Added to ‘an often un-questioned, positive ideological stance towards entrepreneurship and small business’ (Blackburn and Kovalainen, 2009: 129), the under-explored complexities of the finance: production interface are all the more curious.

The insights of heterodox economic sociology, anthropology and geography regarding the social and cultural embeddedness of economic behaviour and institutions have made only patchy incursions into analyses of the flows of money that support small firms (Pollard, 2003). Where such literatures do consider small firm finances, they have often focused narrowly on finance as an economic ‘input’ to production (Lee and Drever, 2014; Lee et al., 2015; Martin et al., 2002; Mina et al., 2013) and relatedly on how ethnicity, class and gender mediate access to credit (Blanchflower et al., 2003; Fraser, 2009; Wilson et al., 2007). In the wake of the 2008 financial crisis, such ‘finance gap’ concerns understandably endure, with further evidence of a slowdown in SME funding (Mason and Harrison, 2015) and associated negative effects on SME growth (Cowling et al., 2012; Fraser, 2012). In addition to the complexity of understanding finance gaps, however, these literatures have often neglected the complexity of financial relationships more broadly when conceptualising small firm dynamics (Gilman and Edwards, 2008). With few exceptions (see Becattini, 1990; Boustani, 2015; Clark and Wrigley, 1995; Coe et al., 2014; Pollard, 2007), analyses of production networks proceed from the assumption that a firm’s means of financial reproduction are in place and relatively unproblematic. In what follows, we argue that diverse literatures on financialisation – usually considered in the context of large corporate entities – can contribute to widening the focus to understand a wider range of relations at the finance: small firm interface.

Financialisation is a contested, slippery concept (Lee et al., 2009) whose theoretical and political novelty is debatable (Christophers, 2015). Yet, literatures from divergent theoretical antecedents – and operating at different levels of abstraction (Davis and Walsh, 2016; French et al., 2011; Krippner, 2012; Lapavitsas, 2011; Pollard, 2013; Van der Zwan, 2014) – argue that financial principles and practices are increasingly influential in economic, political and cultural life. Epstein (2005) uses the term to mark ‘the increasing role of financial motives, financial markets, financial actors and financial institutions in the operation of the domestic and international economies’ (p. 3). Interior to this broadest definition, however, are three suites of approaches that warrant some further delineation. In its most systemic reading, financialisation is a regime of accumulation ‘in which profits accrue primarily through financial channels rather than through trade and commodity production’ (Krippner, 2005: 174), as value creation is no longer exclusive to the sphere of production. Financialisation represents a period in which financial institutions increase their share of profits vis-à-vis other fractions of capital (Duménil and Lévy, 2001; Stockhammer, 2004). This redistribution takes the form of non-financial corporations (NFCs) increasingly diverting money to financial intermediaries through interest and dividend payments and share buybacks (Van der Zwan, 2014).

A second, meso-analytic reading of financialisation argues that it has taken hold in particular institutional contexts such as the United States and United Kingdom whose Anglo-Saxon varieties of capitalism (Hall and Soskice, 2001), house regulatory and legal structures that privilege the rights of shareholders over corporate and state entities (Davis and Walsh, 2016; Froud et al., 2006). Scholars have noted the growing influence of capital market actors, institutions and discourses of shareholder value in shaping norms and expectations of corporate behaviour (Froud et al., 2006; Montalban and Sakinç, 2013; Orhangazi, 2008; Van der Zwan, 2014). Again, financialisation is viewed here as a redistributive project, privileging investment in financial assets at the expense of building long(er) term productive capacities of NFCs (Baud and Durand, 2012; Orhangazi, 2008). These literatures, however, place greater emphasis on the normative elements of financialisation (Van der Zwan, 2014), exploring how – in the context of NFCs – financialising pressures impinge via the role of institutional investors (Fligstein, 1990) and strategies concerned to appease investors, including squeezing labour costs, downsizing, outsourcing productive activities, disinvestment and the use of stock options (Thompson and Harley, 2012).

A third, more culturally oriented reading of financialisation explores the expanding reach of financial logics and practices beyond the corporation and firm and into everyday life (Martin, 2002). Part of this refers to the cultural, qualitative aspects of financialisation (Sawyer, 2013), for example, the normalisation of credit and debt, most especially in the US and UK contexts, as middle and lower income households are incorporated into mortgage markets, pension plans and other mass marketed financial products (Martin, 2002; Montgomerie, 2009). More than this, however, and relevant to the formation of attitudes to work, risk, identity and life style and life cycle choices, these literatures explore cognitive and discursive processes of subjectification, drawing on Foucauldian ideas of governmentality and ‘technologies of the self’ that are increasingly aligned with financial discourses and technologies. As the state withdraws from welfare provision, individuals are encouraged to become financially literate, self-interested, investor subjects (Langley, 2006), responsible for their own welfare (Watson, 2009). Risk is recast as an investment opportunity (Hall, 2011) and ‘the motivating force to enter financial markets for protection against possible unemployment, poor health or retirement’ (van der Zwan, 2014: 112).

These literatures, albeit from divergent theoretical antecedents, argue that financial intermediaries, principles and practices at a societal, organisational and everyday personal level are increasingly ‘masters’ rather than ‘servants’ of production, regulating firm behaviour and intent on subordinating firm strategies to support financial interests (Engelen, 2003; Montalban and Sakinç, 2013). So, what is the relevance of such literatures for small firms not exposed to capital markets? In asking this question, it is important to reiterate the heterogeneity of small firms in terms of their financing needs and their varied aspirations and objectives for growth. Many small firms, most especially those run by the self-employed, or those who do not require any external finance (other than trade credit), may be relatively unaffected by such financialising logics and practices. In what follows, however, we argue that in some contexts, some small firms can be, and are being, affected by financialising principles and practices. Where they are it is imperative to acknowledge these socio-economic realities because they are affecting decision-making about investment, product development and staffing. Moreover, in undertaking this exercise, we respond to Van der Zwan’s (2014: 118) call to explicate ‘the possibilities for agency by local actors, when financial imperatives are gradually becoming more important’. The research identifies three interrelated conduits through which such financialising principles may make their presence felt for those working in small firms: inter-firm relations, relations with external financial intermediaries and a neoliberal socio-economic context.

The first potential conduit for financialising principles and practices to be transmitted to small firms develops from an appreciation of economic, geographical and institutionalist literatures on small firms. These literatures remind us that small firms are not islands; they are relationally embedded in specific spatial, temporal and competitive contexts (Dicken and Malmberg, 2001; Pollard, 2003). Regional, sectoral and institutional milieux mediate small firm experiences of and responses to competitive pressures. Of vital importance for small firms are their relations with other, and often larger, firms (Rainnie, 1989). While small firms may be privately held and not directly exposed to the financial principles, metrics and practices of publicly listed firms, they may, nevertheless, find themselves working in, or around the edges of, wider global production networks (GPNs) that expose them to the financial networks and performance metrics of their larger corporate clients and customers (Coe et al., 2014). Thus, small firms might, through their relations with larger suppliers and customers, find themselves exposed to financialising principles and practices.

Second, and related, small firms may not – at least in the early stages of their development – be directly exposed to institutional investors and shareholders. Nevertheless, unless they finance entirely through retained earnings, they will have to negotiate other sources of finance and, varying with that, navigate asymmetrical power relations with financial intermediaries such as banks, grant awarding bodies, venture capitalists and business angels. Such intermediaries, in turn, may be under pressure to deliver returns to shareholders, trustees, family and so on that affects their lending behaviour. Beyond this, however, even in cases where small firms do not need bank finance, they may still be caught up in changing bank protocols regarding, for example, the extension (or withdrawal) of overdraft facilities. By way of example, and notable for the timing of this research, the 2008 financial crisis eroded the balance sheets of major banks and prompted a significant credit tightening to small firms in the United Kingdom. In the ensuing credit crunch, the funding landscape for small firms deteriorated, whether they were reliant on family funds (often tied to housing asset values), bank loans or angel finance (Cowling et al., 2012; Degryse et al., 2015; Mason and Harrison, 2015). Most controversial, and testimony to the asymmetry of relations of small firms with banks, were complaints that banks forced viable small firms into default to then seize their assets at a discount (Fedor, 2016).

The third conduit relates to how, if at all, the ‘financialisation of everyday life’ (Martin, 2002) affects diverse small businesses, be they run by self-employed individuals or whether they employ staff. Small firms are conceived by, and staffed with, individuals who have been socialised in a socio-economic environment in which finance is ascendant after 30 years of neoliberal deregulation (Davis and Walsh, 2016). Small firms occupy an important place in this context, championed as ideological and political symbols of neoliberalism, replete with ideals of entrepreneurial individuals controlling their own destinies, beyond barriers of class, gender or race (Dannreuther and Perren, 2013a, 2013b). Drawing on Van der Zwan’s (2014) call to interrogate the possibilities of local actors exerting agency, one of the important contributions of financialisation literatures has been to indicate how diverse actors – not just managers and shareholders but also wage earners and home owners – are being drawn into financial markets. Small firms may be key sites where entrepreneurs and employees alike try to achieve their financial objectives, be it just ‘making ends meet’ through self-employment or forging a career path designed to support wider kin networks. Although financialisation literatures typically emphasise the reassertion of the power of capital over labour (van der Zwan, 2014), it is also important to acknowledge a more complex picture in which capital’s lack of commitment and short termism can be reciprocated in kind through declining levels of employee trust and attachment (Cushen and Thompson, 2016: 36) or, indeed, where employees can be beneficiaries of value-maximising behaviour through asset sales, membership of pension schemes and so on. In this sense, the wider macroeconomy of financialising principles and practices can exert their influence directly and indirectly through a whole range of social, political and economic institutions (Pollard, 2013), be they house prices, market expectations or bank credit scoring protocols. In what follows, we explore these three conduits in UK small firms in two contrasting sectors, bio-business and film and media.

The research project and methodology

Our philosophical approach, research design, data collection and analysis protocols are situated in an interpretivist social constructionist tradition. The project 2 involved longitudinal, qualitative research on the processes by which small firms in the United Kingdom understand and respond to regulation. The interpretivist philosophical perspective has significant implications for how claims to knowledge are made and justified (Leitch et al., 2010). Watson (1994) has argued that detailed interpretivist micro-sociological research (in his case, the study of managers) ‘is a means of generalizing about processes managers get involved in … rather than “all managers” … It is a matter of generalizing theoretically rather than empirically’ (p. 7). In our case, our theoretical interest is in how, if at all, financialising principles and practices are perceived, translated and resisted for small firm owners, managers and staff. Thus, human agents in the small firms studied are involved in processes where we have observed, noted and analysed regularities and patterns, such that we can clarify, extend and interpret the meanings and functions of their actions. Moreover, because interpretivist approaches focus on understanding meaning and interpretation, as opposed to more deterministic forms of explanation requiring the establishment of causal associations between variables (Johnson et al., 2006), concerns of cause and effect are less relevant than an interest in how people acting on their interpretations create their reality.

In designing the overall project, we were cognisant that validity is a process, not an outcome (Leitch et al., 2010). At the outset, our choice of sectors responded to calls from previous research (Edwards et al., 2003); we selected both manufacturing and service businesses to avoid over-researched sectors such as restaurants and clothing manufacture. Our sectoral rationale was based on the suggestion by Edwards et al. (2003: 21) that relatively ‘tightly defined’ sector choice can strengthen research because ‘contrasts between sectors can reveal the effects of different external conditions while contrasts within a sector can show how common conditions are mediated differently within the firm’. Variable orientation to growth between sectors also shaped our thinking, in that, for instance, we expected the bio-business sector to be highly growth-oriented and the film and media sector less so. Thus, our strategy reflects a theoretical sampling approach aimed at uncovering differences of process and context.

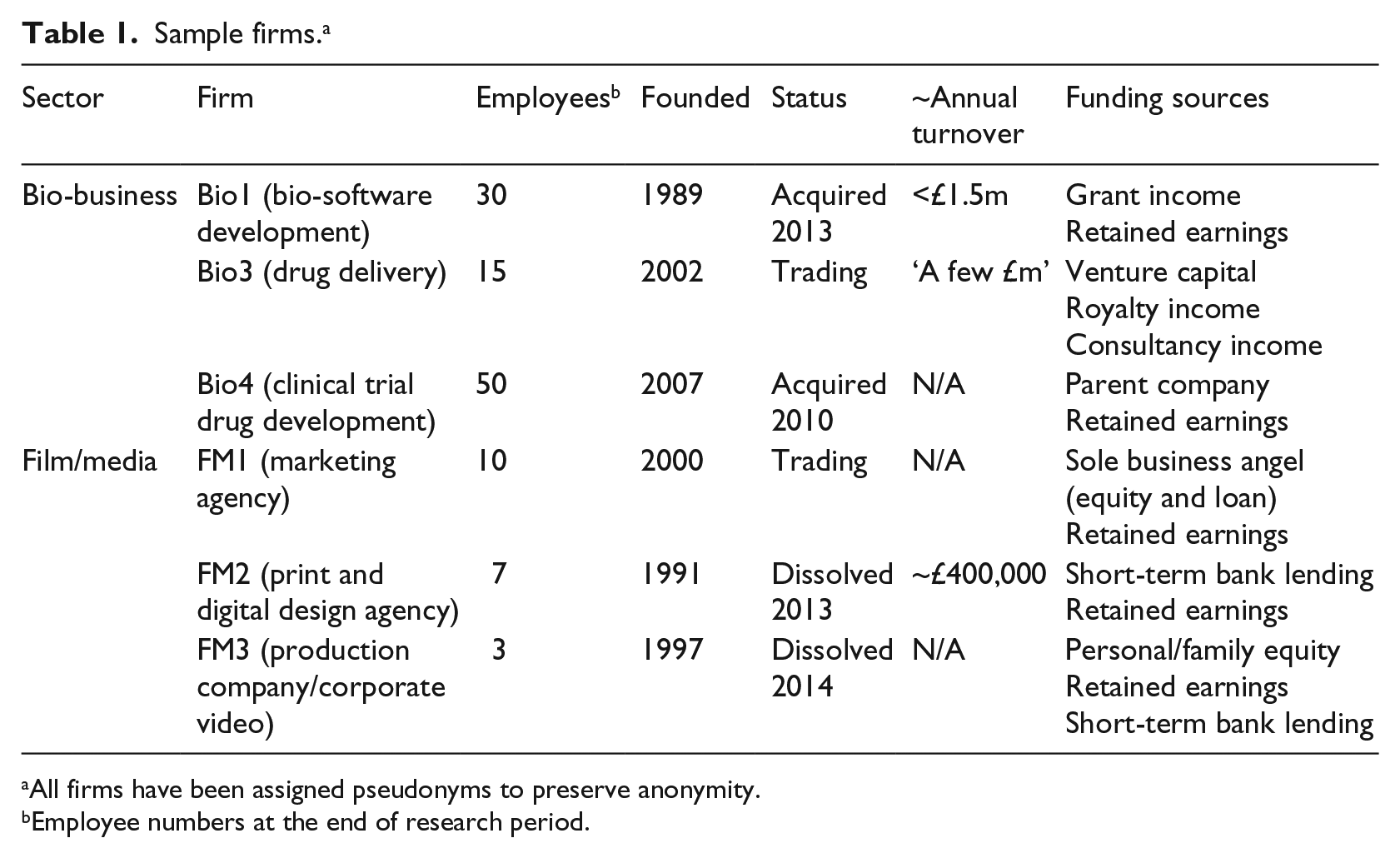

The project comprised 82 interviews in 14 small firms in four sectors, bio-business, security, film and media and environmental services. The following discussion reports on a subsample of six firms in the bio-business and film and media sector (see Table 1). Although interpretivist research philosophy does not aim to achieve generalisability nor seek representativeness of whole populations, we are concerned to show that the theoretical generalisations of process we are describing can be plausibly applied to other small firms in other sectors. Hence, our strategy in selecting a subsample of the broader project’s data encompasses the design principle of ‘maximum variation’ (Flyvbjerg, 2001). That is, we have sought to describe firms at opposite poles of experience in two specific respects. First, this subsample spans the breadth of our data in terms of the capital intensiveness of production; the bio-business and film and media firms researched occupied opposite ends of the spectrum in terms of their financial requirements. Second, these firms span the diversity of ambition regarding growth through the recessionary period when the research was undertaken (2010–2012); the three bio-sector firms sought expansion and external financing, while the film and media companies were intent on survival and less reliant on external finance. In what follows, our purpose is not representativeness or generalisations about all small firms or all firms in these sectors; it is to highlight theoretical generalisations about financialisation processes.

Sample firms. a

All firms have been assigned pseudonyms to preserve anonymity.

Employee numbers at the end of research period.

In addition to collecting secondary material for each firm and sector, the research team undertook non-participant observation and in-depth unstructured interviews of managers, employees and external network relations. To achieve this, it was necessary to incrementally build relationships with owner–managers because we were seeking commitment to the longitudinal and intensive nature of the research. 3 In addition to the observation and everyday casual conversation that typified a significant aspect of the research effort, in this subsample of six firms we undertook 42 semi-structured interviews with staff (at various levels of seniority) in three phases separated by six-month intervals. All interviews were tape recorded and transcribed. Analysis of the interview transcripts was carried out by three of the research team who jointly undertook detailed coding and cross-comparison of coded transcripts across the three phases of research to ensure the stability and accuracy of codes used to draw out key themes, commonalities of experience and sources of difference.

The financial(ising) contexts of small firms

The bio-business sector

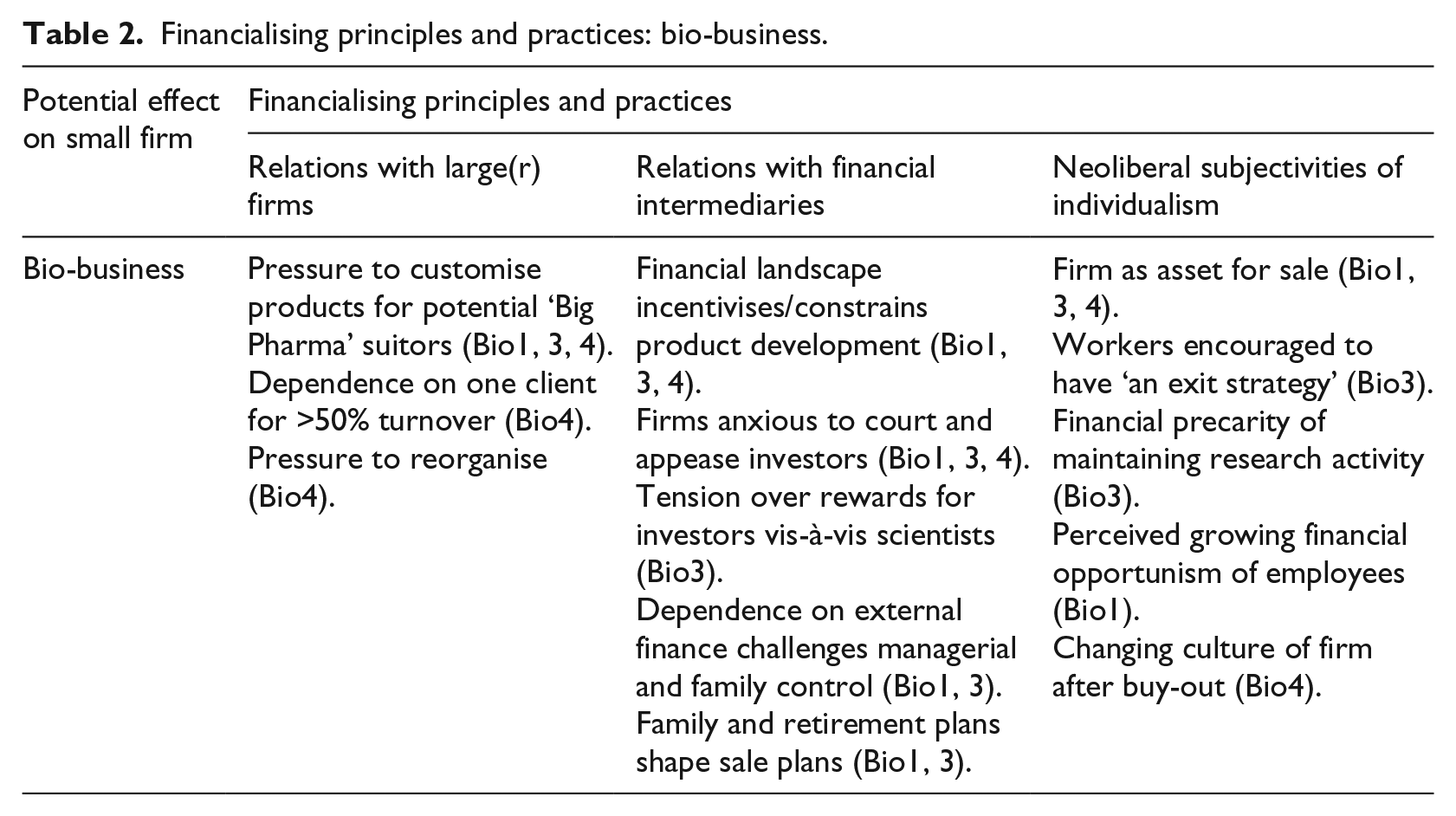

Financialising principles and practices were in evidence in all three of our bio-business firms (see Table 2). The first conduit of financialising principles and practices that we consider is the firms’ relations with large(r) firms; it is difficult to overstate the significance of these relationships in this sectoral context. The UK bio-business sector is dwarfed by what all our firms referred to as ‘big pharma’, most notably GlaxoSmithKline (GSK), Pfizer and Astra-Zeneca. Resonating with other research on the vertical disintegration of big pharma (Gleadle et al., 2014), our interviewees noted that the high costs of R&D coupled with the uncertainty of market returns mean that bioscience innovation has, in essence, been out-sourced to small firms like Bio1, 2 and 4. For such small firms, failure rates are notoriously high:

what the big pharmas will do is they will wait until it [new drug or therapy] goes through its initial phase 1 [clinical trials]… then they’ll either licence it off the biotechs or they’ll buy it … rather than Glaxo having a small division for everything, it’s just best [for Glaxo] to wait until that biotech comes up with this great idea. (Clinical Trials Manager, Bio1, Phase 1)

4

Financialising principles and practices: bio-business.

Success for our three bio-business firms was equated with either licensing their product or being sold to larger firms (Andersson et al., 2010; Montalban and Sakinç, 2013). All three firms were conceived – from their inception – as assets for eventual sale to a larger company. This firm-as-asset principle was operationalised in Bio1 in the form of sales targets:

we’ve got a thing at the moment, it’s a cricket score thing but 135 for six, where what we’ve got to do is, we’ve got to bring in £135,000 grand of sales for the next six months … if we can do those sorts of numbers then we could float … Don’t care if you’re programmers, salesperson, admin bod, CEO or whatever, your job is that line over that line and by a lot until we’re 135 over six. (Chief Executive Officer (CEO), Phase 1)

At Bio3, a strategy to attract larger suitors involved targeting their products and services geographically (in European and North American markets) and strategically fostering working relationships with potential suitors by arranging small collaborative feasibility studies. For Bio3’s CEO (Phase 1), such studies would enable potential suitors to appreciate the value of Bio3’s technology, akin to ‘kicking the tyres’ of Bio3 before making an offer to buy the company. Bio4, formed in 2007, were bought out during the research. Although senior management ‘all did very nicely, thank you’ from the buy-out (Office Manager, Phase 2), eight months later, they were less sanguine about their situation and relations with their new parent company. Managers were conscious of their reliance on one large client for more than 50% of their turnover (Quality Assurance Manager, Phase 2), and there had been no new business leads, and little by way of communication or strategic direction, from their new parent. Instead, rumours were starting to circulate of an impending reorganisation and possible redundancies.

The attractiveness of the bio-business firms to large(r) firms was, in turn, bound up with the second conduit of financialising pressures identified: their relations with financial intermediaries and specifically, their success (or not) in attracting external funding. Small firms in bio-business – often university spin outs with a ‘great idea’ – require significant external finance because R&D and clinical trials are too expensive to be financed through retained earnings. Too high risk for bank financing, these firms were reliant on grant income, venture capital monies, royalties and some consultancy income (see Table 1). Thus, it is critical to explore how, if at all, this dependence on external finance exposes these firms to financialising principles and practices.

One consequence of the need for external financing was an interest in, and concern to improve, how the firm was perceived and evaluated by financial intermediaries. For Bio1, this translated into a decision to modify their accounting practices. During the first phase of our research, they took the ‘onerous’ (Financial Director, Bio1, Phase 1) decision to shift from Generally Accepted Accounting Principles (GAAP) to International Financial Reporting Standards (IFRS), because ‘it’s doubled the size of the accounts … it might be important to someone, an analyst in New York’. Bio4 – bought out over the course of the research – also reported modifying their accounting conventions, making sure that in the year of their acquisition spending was ‘squeezed’ and profit ‘optimised’ (Quality Assurance Manager, Phase 1). The shift in accounting conventions operated as a form of market signalling (Spence, 1974) that made the firm’s accounts larger and more legible for analysts and potential investors.

A second consequence of their dependence on external finance emerging clearly over the three phases of interviews was growing concern regarding how to manage the tension between the need to secure money, on one hand, and the resulting loss of control over some business decisions and need to meet demands of financiers, on the other. Bio1, for all their sales targets designed to enable flotation, were unable to float during the research period due to the macroeconomic uncertainty. Moreover, management at Bio1 and 3 became increasingly pessimistic about the UK economy and, relatedly, the capacity of the National Health Service (NHS) to fund research and clinical trials. In need of funds for clinical trials, Bio1’s CEO (Phase 2) applied for more European grant monies but was reluctant to seek funding from venture capitalists because

they just say ‘right, you know, we want most of your company for it’, and the sad truth is that they all do that … and they think they can run your company better than you can … I just don’t want to go there.

Between Phases 1 and 2 interviews, Bio3’s CEO retired and their Chief Business Officer took over as CEO. Too high risk to secure bank loans and ‘nowhere near profitability’, the new CEO managed to secure another 12 months of working capital, but the form of this capital – a convertible loan – required tortuous negotiations with 30 new shareholders:

The management team believed there was better ways of doing it but the investors wanted it done a different way, so … it’s their company … We disagreed with certain elements of what they wanted us to do and it’s turned much more complicated than it needed to be. And actually some of them have changed their mind about what they wanted to do but it’s too late. (CEO Bio3, Phase 2)

Finally, in terms of the third potential conduit of financialising principles and practices, the financialisation of everyday life, CEOs and employees talked about how their relations with the firm and other employees were being shaped by financial concerns. To give just a few examples (and see Table 2), all three firms were conceived as assets for eventual sale to a larger company; our bio-business CEOs narrated finance not merely as an input that made their R&D possible but rather as a spectral presence shaping the very idea and purpose of the firm. Bio3’s CEO became resigned to the ‘huge distraction’ (Phase 3) of managing relations with new shareholders because she or he felt a responsibility to maintain the financial flows necessary to retain and support Bio3’s scientists and their ability to do cutting edge research. Moreover, these relations were not simply about investment in Bio3 as the new shareholders also had ‘rights over IP [intellectual property] and things like this every time we do a licensing deal or something’ (Bio3 CEO, Phase 3).

The spectral presence of finance and its influence on firm strategy was not only experienced by individuals in senior management or finance-related positions responsible for negotiating with external financial intermediaries. In addition, middle-grade employees in different parts of the firm also came to experience the power of financial logics and practices. For example, an Operations Manager (Bio3, Phase 1) recounted their decision to leave a job in ‘big pharma’ to join Bio3 because they felt that it would provide opportunities to ‘do more innovative science, cutting edge stuff’; they were ‘quite surprised’ to then learn of Bio3’s desire to be sold to a bigger firm. Alongside this news, the employee was advised to revisit their career plans: ‘My boss at the time said, ‘“You should have an exit strategy” … he said “Look, all the investors have an exit strategy”’. In Phase 2 of the interviews, following successful clinical trials, the same manager observed,

the company is going off in a different direction. We’ve now got clinical data on a product which … well it’s definitely added significantly to the value of the company. And I sometimes think that, it’s not just [Bio3], it’s generally, that scientists and engineers don’t get enough of the credit … I get slightly peeved about various people who have got the shares in the company who will probably therefore do better than I would.

At Bio1 (Phase 3), the CEO described what she or he felt was a growing culture of financial opportunism among employees, an ‘entitlement mentality’, that was being exacerbated by the deteriorating economic outlook. Fearing that Bio1 was vulnerable to litigation if there were any health and safety incidents and/or performance issues, she or he hired a lawyer:

He is frankly a bastard … everybody who works here knows that he’s lurking in the wind [laughter]. If you’re a good leaver we’ll be very good and nice to you and all that stuff. If you fuck us around we’ll bite you. And so it’s kind of like an insurance policy.

At Bio4, the founder (Phase 3) reflected on how their buyout had changed their company from the small, passionate start-up founded with a friend to a ‘big faceless organization’ in which staff were less committed:

small companies, I think … you expect each other to operate in kind of extreme circumstances like, ‘This month we’re not going to take any money, okay?’ or, ‘We’ve all got to work over the weekend’ … It’s easier in a big faceless organization to think, ‘Well, I’m away for a week, who gives a stuff?’.

The film and media sector

The film and media firms in our sample articulated a rather different set of sectoral and competitive conditions than those prevalent in our bio-business firms. The sector is characterised by the production of bespoke creative content specified by end-user requirements. Our sample firms were smaller than those in bio-business and did not require finance to trial ‘great ideas’. Instead, they articulated success in terms of a variety of issues. These included: recruiting and retaining passionate and committed staff, staying abreast of a rapidly shifting technological landscape and being able to purchase the specialist equipment and/or technical expertise necessary to enable cost-effective content delivery to tight deadlines.

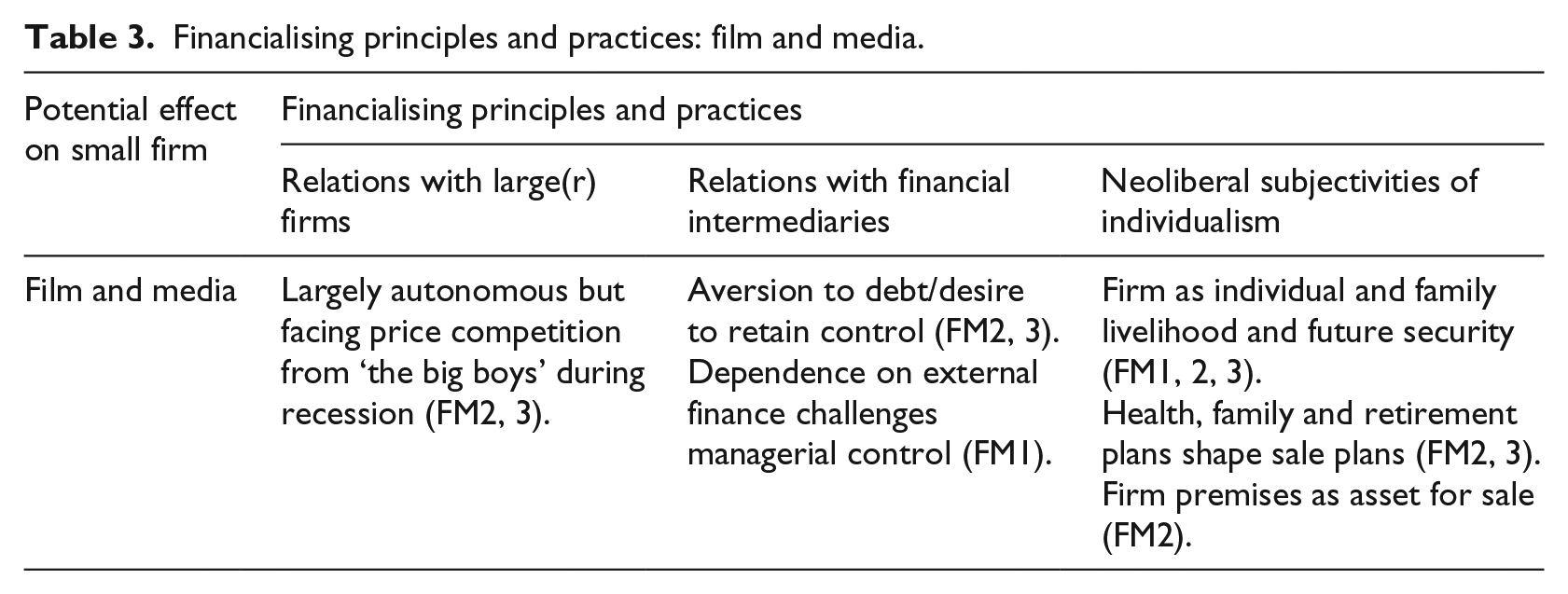

In terms of their exposure to financialising principles and practices courtesy of their relations with larger firms (see Table 3), our film and media firms were not dependent on larger firms for their customer base or for the supply of key inputs. Individuals in all three sample firms commented on the declining volume of work in a deteriorating macroeconomic climate and, to this extent, felt disadvantaged by their larger competitors. FM2 and FM3, for example, described how their sales were being squeezed because of price competition from ‘the big boys’ who, in recession, ‘are cannibalising into our level of work, you know … drifting down into some of the £10,000 and £20,000 jobs’ (FM2 CEO, Phase 2), forcing ‘little companies to the lowest price’ (FM3 CEO, Phase 2). FM1 also reported losing some large public sector contracts as budgets were squeezed. Beyond intensifying price competition in recession, however, their relations with large(r) firms did not appear – in and of themselves – to expose them to financialising principles and practices.

Financialising principles and practices: film and media.

In terms of the second conduit for financialising principles and practices – relations with financial intermediaries – the firms again reported a different disposition to external finance than the bio-business firms. Both FM2 and FM3 described themselves as relatively financially independent, relying on short-term bank finance and retained earnings. Moreover, they emphasised the avoidance of external finance as an important organising principle and key to their survival. Both firms were family owned and debt averse. They were distrustful of banks, in general, and their treatment of small firms in particular, most especially in a period of recession when banks, intent on repairing their balance sheets, could suddenly call in loans and end overdraft facilities. By contrast, FM1 were dependent on external funding from one business angel 5 who was also a friend of the CEO. This dependent relationship meant that she or he felt ‘a little bit like a puppet in many respects’ (Phase 1).

The contrasting abilities of the firms to maintain autonomy from financial intermediaries generated operational consequences resonating with classic debates about managerial autonomy and independence (Curran, 1990). For example, the deteriorating macroeconomic environment in the United Kingdom reinforced their financial caution and hardened their aversion to debt. For FM2 and FM3, expenditure on new equipment was their most significant financial outlay beyond wages and salaries. FM3 relied on retained earnings and/or bank loans to renew £50–£75,000 worth of equipment on a three-year redundancy cycle (FM3 Marketing Manager, Phase 2). Their investment needs, and potential returns, were too small to interest venture capital. The key uncertainty in their business was staying current in a rapidly shifting technological terrain and timing their investments to avoid investing in the wrong technological innovation (CEO, FM3, Phase 2). In terms of the timing of new investment in equipment, FM3’s CEO (Phase 2) described a risk-averse strategy:

we tend to lag behind … if you’re a new adopter it costs a bloody fortune. If you wait six months or a year, it’s very do-able at a price you know … essentially our pursuit is of speed, so new work stations that have faster chip sets are always of interest to us.

During the research, both FM2 and FM3 delayed equipment purchases because of the economic uncertainty. FM3 decided not to extend their loan deal from their bank because, once in place, ‘you can’t sack that’ (CEO FM3, Phase 2), whereas they did have the flexibility to make employees redundant (FM3 Financial Director, Phase 3). At FM3, the financial (if not legal) ‘risk aversion’ strategy extended to their staffing decisions: they would not employ any women of child-bearing age because

I put my own money into this business to help it over difficult periods you know and … you do that because you worry about everybody in the company and particularly at times like this, just a little thing like that [maternity leave] can be critical in taking you under.

At FM1, meanwhile, the reliance on one external funder had profound implications for managerial autonomy. FM1’s very existence was precarious during the research; the CEO had closed part of its business to downsize ‘to the bare bones’, reducing from 34 to 18 and then down to 10 staff (CEO, Phase 1). The angel investor was attentive and interventionist, keen to query and/or suggest changes in strategy, personnel and technology: ‘he kind of comes in with his big size 12s and he’ll try and solve a problem with throwing more cash at something or bringing people in who aren’t right’ (CEO, Phase 2). By Phase 3 of the research, the CEO observed,

There’s a period of time when he’ll sit back and you’ll think ‘he’s sitting back and letting me get on with it’, but he’s not really because he’s holding the purse strings.

While not as dependent on securing external finance or needing to negotiate with shareholders or parent companies as their counterparts in the bio-business sector, managing relationships with financial intermediaries was challenging. This included resistance to deeper debt or equity relationships and the managerial interference such arrangements could precipitate. This was a consuming process for all three film and media firms, leading them to cut or delay spending on equipment, staff and salaries.

Finally, what of the third potential conduit of financialising principles and practices related to the financialisation of everyday life? Managers in all three firms, not least through their desires to resist intense and unremitting financial pressures, reflected on the lived professional and personal toll of securing their financial reproduction and future in a very difficult economic climate. The CEO of FM2 (Phase 2) argued,

The reason we’ve survived is because we have no debts. Whatsoever. We’ve taken massive hits ourselves, personally, you know, because the turnover’s dropped by 60% or more now, so we’ve all had to take huge salary cuts.

At both FM2 and FM3, the CEOs articulated concerns about their age, health and the possibilities of selling up and/or retiring; for both firms, battening down the financial hatches and managing shrinkage was the key objective. Between Phases 1 and 2, the CEO at FM2 was hospitalised with high blood pressure and approached with an offer to buy FM2’s premises. The prospective buyer was not interested in film and media but in realising a profit through a different channel, namely, the conversion of their premises into student apartments. At FM3, although the Financial Director (Phase 3) had avoided the ‘financial market and everything like the plague … I’ve never had any faith in pensions or anything’, she or he was planning for the future by investing in holiday homes and in woodland.

At FM1, the professional and personal strains of managing a precarious technological and macroeconomic context combined with financial dependence on a friend were becoming overwhelming. In the early part of 2011, FM1’s CEO (Phase 2) was exhausted and ready to admit defeat. She or he approached the business angel – who had over £800,000 invested in FM1 – to say,

‘I’m not going to be able to turn it around’. And he disagreed with me and said ‘No, it’s your confidence. You’ll be fine’. And he put hundreds of thousands in to give me time … That made me feel even worse.

By Phase 3 of the research, FM1’s CEO observed,

It’s really unsettling because you’re very focused on building the company and focusing on all of the many things that you need to think about in running a business, and then you’ve got this huge … It’s like a side play. It’s like a Shakespearian play running on the sidelines. And it’s hugely complicated, it’s hugely political and emotional … It takes a lot of willpower and a lot of headspace, as I say. He’s put a huge amount of money into this business … I’ve invested huge amounts of my time and energy and life.

At the time of writing, FM1 is still trading. FM2 and FM3 ceased trading in 2013 and 2014, respectively.

Conclusion

This article has explored whether and how financialising principles and practices affect small firms that have no direct exposure to capital markets. In addressing this question, the article has drawn upon longitudinal research in six small firms in the United Kingdom in two contrasting sectors. The article makes three interrelated contributions to theory and future research.

First, the article extends literatures on financialisation by focusing on small firms as different potential sites of financialising principles and practices. While some research on financialisation has moved beyond exploring its macroeconomic, systemic effects to focus on firm behaviour (Froud et al., 2006; Orhangazi, 2008; Tori and Onaran, 2015), this work has typically focused on large, capital market facing NFCs. By contrast, this analysis identifies three conduits through which small firms may be indirectly exposed to, and affected by, financialising principles and practices. Three sets of relations – inter-firm relations and divisions of labour, relations with financial intermediaries and the formation of individualising neoliberal subjectivities – were identified as conduits through which financialising principles and practices could be perceived, translated and resisted for owners, managers and staff. As such, the article not only demonstrates the relevance of financialisation to small firms but in so doing, also addresses one of the challenges about the ‘how’ of financialisation (Lapavitsas, 2011).

All the firms – for all their differences in financing and ambitions for growth – were affected by a macroeconomic context in which increased demand for finance gave financial intermediaries superior bargaining power (Mason and Harrison, 2015). The firms devised strategies to manage financial pressures while seeking to preserve their research and creative capabilities. Significantly for our arguments, three phases of longitudinal research provided grounded empirical analysis of these indirect effects in two contrasting sectors with different demands for, and dispositions to, external finance. This comparative element of the research is suggestive of how sectoral contexts can mediate whether and how financialising principles and practices are perceived, translated and resisted (Lapavitsas, 2011; Thompson, 2013). The bio-business firms most especially exemplified an ‘ontological reconfiguration’ for finance, in that their very existence was premised on ‘establishing the power to effectively capitalise on future “earnings”’ (Ouma, 2015: 227). Bio1’s interest in flotation produced unattainable sales targets that reverberated throughout the firm, while Bio3 reconciled itself to a funding regime that brought with it ongoing tensions with managing investor expectations. Firms in the film and media sector were less dependent on external finance than Bio1, 2 and 4. Yet, their financial reproduction also exposed them to pressures from financial intermediaries – themselves trying to manage recessionary conditions – and encouraged a range of decisions designed to resist ceding greater control to financial intermediaries. Sectoral context is, of course, but one marker of variegation for small firms. More grounded, contextual understandings of financialising principles and practices need to be sensitised to other and multiple axes of heterogeneity among small (and other) firms. Particularly important in this respect will be investigations into the geographically variegated economic, institutional and socio-cultural constitution and expression of financial principles and practices (Boustani, 2015; French et al., 2011; Klagge et al., 2017; Pike and Pollard, 2010).

Second and related, the article has deployed literatures on financialisation to contribute to an important and growing literature on small firm finances (Coe et al., 2014; Fraser et al., 2015; Dannreuther and Perren, 2013a, 2013b). This literature is extending intellectual and policy debate beyond concerns with funding gaps, attitudes to risk and business size to develop links to political and socio-economic analyses. Such analyses conceive firm finances as sets of social relations with repercussions for all aspects of the firm, be it purchasing and investment, staffing, governance or managerial control. Literatures elucidating the macroeconomic, corporate and cultural elements of financialisation have been deployed here to open up conceptual and empirical space for more holistic treatments of small firm financial relations. The argument is that financial relations should be moved from the margins into the mainstream of socio-economic analysis of small firms. Froud et al. (2006) argued that literatures on firm strategy share an anachronistic ‘firm in industry problem definition’, a productivist bias that has privileged a firm’s location in product markets, to the neglect of understanding its location in financial markets (p. 28). This productivist bias similarly afflicts analyses of small firms. By way of expanding on this point, this analytical ambition is not simply doing justice to ‘varieties of financialisation’ but also explicating the possibilities for agency by local actors at a time when financial imperatives are becoming more important elements of political economic life in contexts like the United Kingdom (Van der Zwan, 2014). Those working in small firms can participate in financial markets in multiple ways – as owners, shareholders, managers, wage earners, householders and pension fund investors – and benefit or lose from various value-maximising strategies. As such, this research extends a long tradition of research on managerial control in small firms (Barrett and Rainnie, 2002; Curran, 1990; Ram and Edwards, 2003; Thompson and Van den Broek, 2010) and connects small firm finance literatures with more holistic political economic literatures that conceive firms as ‘battlefields’ for different groups of interests (Stockhammer, 2006).

Third and finally, there is a politics to addressing the significance (or not) of financialising principles and practices for small firms not directly exposed to the workings of capital markets. In one of the few UK studies of the microeconomic effects of financialisation, Tori and Onaran’s (2015) analysis of manufacturing NFCs supports other more macroeconomic work which argues that an expanding financial system has negative effects on growth and investment (Epstein, 2005; Orhangazi, 2008; Stockhammer, 2004, 2006). This research presents findings from a longitudinal, qualitative project working with small firms in two very different sectors. Throughout we have stressed the heterogeneity of the small firm population and make no claims for the universality of our findings. What is clear, however, is that in some contexts, small firms, managers and employees are exposed to wider financialising logics and practices, and these have material effects. Alongside a wealth of information from broader quantitative surveys, there is an exciting agenda, here, to take more seriously the sheer complexity of elements affecting a firm’s financing decisions.

Interior to this argument, there are (at least) two key issues specific to small firms. First, Dannreuther and Perren (2013b) argue persuasively that the political construction of ‘small firms’ has long been malleable for different, even competing, purposes, be it pushing back the state, supporting individualised subjects or delivering government agendas. In a period in which financial logics and products have penetrated ever more areas of life, from public debt through to retail products (Montgomerie, 2009), ‘rhetorical support for the small firm offered individualised responses to a wide range of contradictions that emerged from the process of accumulation’, encouraging the self-employed and other budding entrepreneurs to embrace the ideal of the small firm ‘with the portrayal of ever-increasing wealth … taking ever more financial risks and incurring ever more debt’ (Dannreuther and Perren, 2013b: 38). Second, and related, if there is a policy interest in supporting ‘the small firm’, however defined, these findings add to a body of work that suggests the need to (re)consider sites of policy intervention. The United Kingdom houses one of the most centralised and concentrated banking sectors in the Organisation for Economic Cooperation and Development (OECD), an oligopolistic landscape in which four institutions supply over 80% of loans to SMEs (Competition and Markets Authority, 2014). Reduced bank lending and venture capital investing are the ‘new normal’ (Davis, 2011; Mason and Harrison, 2015). In this macroeconomic context of over 30 years of neoliberal deregulation and state supported financialisation (Davis and Walsh, 2016), it is imperative to consider the nature and implications of such financial forms of control for small firms.

Footnotes

Acknowledgements

To all the individuals who generously gave their time to this longitudinal project, we can thank them best by maintaining their anonymity. We would also like to thank the Editor and anonymous referees for their comments and suggestions that have helped us strengthen the paper.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by funding from the UK Economic and Social Research Council (ESRC RES-062-23-1916).