Abstract

Microfinance institutions (MFIs) operate in diverse institutional contexts and serve as the backbone for microenterprises typically excluded from traditional financial markets. At the same time, MFIs and the microenterprises they support solve tangible social problems, such as alleviating hunger, lifting people out of poverty and creating more sustainable communities. When appealing for resources, MFIs work with microenterprises to create rhetoric that communicates both the financial needs and the social good that supporting them can do. Building on previous research concerning the hybrid rhetoric of microenterprises and the literature rooted in organisational legitimacy, we take a multi-level approach and assess whether country stability and MFI financial performance influence the hybrid rhetoric of microenterprises.

Introduction

Microfinance institutions (MFIs) serve as intermediaries for microenterprises excluded from mainstream finance (Khavul, 2010) and fill institutional voids in their home countries (Mair et al., 2012). MFIs, and the microenterprises they support, must traverse both economic and social goals, commonly defined as organisational hybridity (Shepherd et al., 2019), as they attempt to demonstrate legitimacy to different stakeholders (Fisher et al., 2017). Many microenterprises, with the support of their affiliated MFIs, appeal for resources through prosocial crowdfunding platforms. This allows microenterprises to tell their stories to a large pool of potential lenders who offer small-dollar pledges (Allison et al., 2015). Notably, a growing body of research suggests that the rhetorical style of these stories can entice or dissuade lenders (Anglin et al., 2022; Jancenelle and Javalgi, 2018). While previous research identifies that hybrid rhetoric – language simultaneously communicating economic and social goals – is an important explanatory variable to potential microenterprise supporters (Moss et al., 2018), its antecedents remain largely unknown. These antecedents are intriguing for two primary reasons. First, microfinance occurs in diverse institutional contexts with varying degrees of stability. While many organisations have hybrid goals, embracing them is rife with complications (Pache and Santos, 2010). Institutional stability, or lack thereof, could be an important factor in the degree of hybridity that a microenterprise presents to external stakeholders. Next, MFIs must also contend with the legitimacy pressures associated with financial performance (Anglin et al., 2020; Kent and Dacin, 2013), which in turn, influences their lending strategies (Ault, 2016; Zhao and Wry, 2016). Thus, there is some likelihood that macro- and meso-levels have consequences for whether a microenterprise utilises hybrid rhetoric, or opts for a more straightforward narrative approach where they emphasise economic or social goals more exclusively.

To unpack this relationship, we take a multi-level perspective, drawing on the legitimacy literature (Fisher et al., 2017; Suddaby et al., 2016) and seek to answer the following question – is there a legitimacy spillover from macro- and meso-level institutions that influences the hybrid rhetoric of the microenterprises nested within them? In line with previous theory concerning legitimacy spillovers from parent-affiliated organisations (Kostova and Zaheer, 1999), we theorise a multi-level legitimacy spillover effect, where the legitimacy of both the parent hybrid organisation (MFI) and country institutions are related to the degree to which affiliated microenterprises communicate their own hybridity. In other words, if an MFI is legitimate and operates within a supportive country, the microenterprise will have more degrees of freedom to present more complex and robust hybrid goals. Conversely, if the MFI is struggling financially and operates in an unstable country, microenterprises are likely to avoid hybrid rhetoric and instead, keep their stories less rhetorically complex. As such, our conceptualisation of legitimacy spillover expands this construct from multi-national enterprises (MNEs) spilling legitimacy over to their affiliated subsidiaries (Kostova and Zaheer, 1999), and from stakeholders judging an organisation’s legitimacy based on other similar organisations (Jonsson et al., 2009; Li et al., 2022; Shi et al., 2022). We illustrate that legitimacy spillovers from macro- and meso-levels afford microenterprises the freedom to pursue a traditionally illegitimate blending of simultaneous social and commercial goals. To test our theory, we created a three-level dataset of over 370,000 loans to ventures facilitated by 99 MFIs operating in 38 countries. To grapple with the large text corpus, we employ computer-aided text analysis (CATA) to assess the textual narratives provided by microenterprises as they seek resources with their respective MFIs through prosocial crowdfunding (Galak et al., 2011). The nested structure of the data offers a global assessment of the relationships unfolding at the micro-meso-macro levels. Further, rhetoric is an observable facet of organisational life through which tensions might be manifest (Suddaby and Greenwood, 2005), in much the same way that workforce composition and organisational activities are observable facets.

This study offers the following contributions. First, there is increasing recognition of the nuances in microfinance, where scholars are not only questioning whether microfinance is itself effective (Singh et al., 2022), but also how globalisation (Sun and Liang, 2021), biases (Davis et al., 2021), and rhetoric (Anglin et al., 2022) influence outcomes across different levels of analysis. We build on these insights by taking a step back and identifying an important subset of associated mechanisms that point to the origins of hybrid rhetoric. Studies that capture the interplay between the macro-meso-micro institutions and organisations are quite rare (Johnson and Schaltegger, 2020), suggesting that the theoretical puzzles of microfinance are inherently incomplete.

Given the influence of rhetoric in crowdfunding settings (Allison et al., 2017; Anglin et al., 2018; McSweeney et al., 2022; Steigenberger and Wilhelm, 2018), identifying antecedents, or why microenterprises choose to leverage rhetoric as they do, offers theoretical and pragmatic value. Thus, this study, through the theorised legitimacy spillover effect, offers a novel path towards illuminating this further. Further, our multi-level approach extends and integrates prior studies that offer insights into the role of the MFI (Anglin et al., 2020) and the greater institutional context in which the MFI and microenterprise operate (Ault, 2016). We find that MFI financial performance, a critical marker of organisational legitimacy (Fisher, 2020), is associated with hybrid rhetoric for the affiliated microenterprises and can even buffer the effects of country-level instability. Thus, we take an important step to uncover a more complete picture of the microfinance landscape. Finally, we approach the social-economic hybridity tension as a continuum, acknowledging that most entrepreneurs carry some degree of social and economic motives (Shepherd et al., 2019). We thus, account for the variance in hybridity between organisations using quantitative approaches in an area that, to date, has often been characterised by qualitative methods (Battilana et al., 2017). While this study does not claim to identify causality, our large-scale global dataset offers novel insights into our research question.

Theoretical foundations

Legitimacy and hybridity

The legitimacy construct has its roots in institutional theory (DiMaggio and Powell, 1983), wherein legitimacy is described as a social judgement of desirability, appropriateness, or acceptance. This judgement implies a congruency between the values and norms of society and the activities and outcomes of organisations operating in that society (Ashforth and Gibbs, 1990). Suchman (1995: 574) defines legitimacy as ‘a generalised perception or assumption that the actions of an entity are desirable, proper, or appropriate within some socially constructed system of norms, values, beliefs, and definitions’. Legitimacy is a relationship between a social system and the organisations within that system (Zimmerman and Zeitz, 2002). Further, legitimacy is a socially constructed judgement, and consequently, the judgement criteria will differ based on different audiences (Thornton et al., 2015). Noting that audiences (e.g. angel investors, venture capitalists, and crowdfunding backers) differ in their legitimacy evaluations of ventures, Fisher et al. (2017) propose that ventures employ a strategic process of emphasis framing. In other words, ventures will adjust key elements of their message to align with the expectations of a specific audience.

Given the challenges of appearing to ‘fit in’ (De Clercq and Voronov, 2009), one area where audience legitimacy expectations often collide is in the fit between category- and local-level legitimacy (Tracey et al., 2018). A venture possesses category-level legitimacy when it is considered desirable or appropriate within a given category, such as autonomous vehicle firms in the technology sector. In other words, these firms meet stakeholder’s ‘institutionalised expectations for how they should look and act’ (Zuckerman, 1999: 1399) within a specific category. In contrast, a venture possesses local-level legitimacy when it is judged to be desirable or appropriate in the local institutional context in which that venture was created, such as autonomous vehicle firms in Silicon Valley. Yet, when category-level stakeholders are located in a different institutional context from the venture itself, institutional misalignment occurs between the local context and the category context (Tracey et al., 2018). Critically, the venture must decide which group will serve as its primary inspiration, ultimately shaping the way it frames its message as the venture seeks to legitimise itself to different audiences.

Organisational hybridity, where the firm attempts to fuse economic and social goals, serves as an intriguing example of these challenges. MFIs, in particular, have drawn significant scholarly interest as they serve as quintessential hybrid organisations (Battilana and Dorado, 2010; Cobb et al., 2016; Khavul, 2010), rife with challenges and opportunities. For example, Kent and Dacin (2013) noted that the drive to gain category-level market legitimacy pressured MFIs to focus on sound banking at the cost of the social mission. The findings in Ault (2016) added another layer of complexity: MFIs also shift their lending behaviour based on the stability of the institutions within which they operate, at the local level. In other words, the MFI’s primary purpose is to loan money to borrowers that other financial institutions have previously deemed unattractive, and to do so in challenging institutional environments. Given that legitimacy is often coupled with financial performance (Aldrich and Fiol, 1994; Soublière and Gehman, 2020; Tracey et al., 2018), this poses a distinct challenge; the social mission is paramount, but so is convincing stakeholders that the financials are sound. For example, Anglin et al. (2020) found that microenterprises associated with underperforming MFIs were slower to raise capital through prosocial crowdfunding, suggesting that even in an environment with social expectations, financial performance matters. Gama et al. (2023), focusing on refugee-led microenterprises, identified a similar effect. Taken together, the findings of this area of research offer a glimpse of the potential interactions between microenterprise, MFI, and their institutional environment.

The legitimacy spillover effect

The legitimacy (or lack thereof) of one organisation can ‘spill over’ to affiliated organisations (Kostova and Zaheer, 1999; Shi et al., 2022). For example, using the context of rewards-based crowdfunding, Soublière and Gehman (2020) found that when an organisation had outlier-level success, other organisations in the same category were also more successful. They reason that the outlier’s success increases the legitimacy of a category, which increases the crowd’s general interest in the said category. In other words, the success of one organisation broadens the market and increases opportunities for others. Kostova and Zaheer (1999), who focused on MNEs, theorised a similar effect, but focused on the challenges of maintaining legitimacy when higher-ordered organisations falter. More specifically, they point out that MNE subsidiaries, as lower-level organisations, must maintain legitimacy with lower-level stakeholders, such as local communities and employees. As with MNEs and their subsidiaries, we expect there to be legitimacy spillovers from the MFI to the affiliated microenterprises. An MFI perceived as legitimate in a given institutional context is likely to offer benefits to affiliated microenterprises. Given that many microenterprises raise funds through prosocial crowdfunding platforms, it follows that one of the freedoms that a microenterprise can gain from affiliating with a legitimate MFI is the freedom to articulate its own hybrid goals. We conceptualise this as a multilevel legitimacy spillover effect. Moss et al. (2018) noted heterogeneity in the ways microenterprises presented their hybridity and how that ultimately affected their fundraising capability, but their study did not offer insights into the antecedents that shape their hybrid framing. Overall, we already know that hybridity of social and commercial emphasis has implications for fundraising by entrepreneurs, but our understanding is limited when it comes to the origins of such hybridity and related rhetoric (Lee et al., 2020). Before presenting our hypotheses, we briefly review the relevance of hybrid rhetoric.

Hybrid rhetoric as evidence of the legitimacy spillover effect

The literature on hybrid organising provides some insights into how communication broadly serves to alleviate complexities specific to the tension between the competing economic and social goals found in hybrids. Internal communication, such as discourse in training programmes (Zilber, 2002) or recurring organisational meetings (Ashforth and Reingen, 2014), are key mechanisms to limit the impact of the commercial versus social tension on immediate organisational members (e.g. employees). Additionally, external communications such as mission statements (Smith and Besharov, 2019), mass media (Tracey et al., 2011), and online pitch narratives (Moss et al., 2018) provide a basis for hybrid communication to important external stakeholder groups.

Rhetoric is a means to persuade an audience, and can be used strategically by organisations to build legitimacy (Suddaby et al., 2016). Further, institutional vocabularies are developed and deployed to craft consistent organisational messages (Suddaby and Greenwood, 2005). These two points have implications for the rhetoric used by hybrid organisations and subsequent legitimacy in the eyes of external stakeholders. For example, institutional vocabularies for hybrids might include references to the ‘triple bottom line’, ‘community first’ and ‘people over profits’. The way these vocabularies are presented to external stakeholders provides the basis for narrative framing and influences the extent to which outside stakeholders accept these accounts (Harmon et al., 2015; Steigenberger and Wilhelm, 2018). Given the legitimacy spillovers between an MFI and its microenterprise subsidiary, the rhetoric used by the microenterprise in its online crowdfunding narrative is a manifestation of the MFI’s ability to take advantage of its hybrid nature via the MFI’s tangible characteristics, for example, financial performance.

In summary, the literature has demonstrated that misalignment may exist between stakeholders at the local level and at the category level when different stakeholder audiences at these levels have competing demands of an organisation. Legitimacy spillovers occur when the legitimacy of a parent organisation is transferred to a subsidiary organisation, with implications at the local level and the category level. In the context of hybrid organisations in the microfinance industry, the legitimacy pressures facing MFIs promote the transfer of hybridity characteristics to the affiliated microenterprises through policies, practices, and procedures of the MFI through spillovers. These spillovers have implications for MFIs and microenterprises that operate on prosocial crowdfunding platforms because conflicting stakeholder pressures at the local level and the category level are likely to exist. Further, these legitimacy spillovers will be manifest in the rhetoric employed by microenterprises on prosocial crowdfunding platforms in an effort to engage stakeholder audiences. However, questions remain regarding the antecedent role of macro-level factors on organisational hybridity. MFIs operate in a variety of macro environments worldwide, and these environments are likely to influence their behaviours (Zhao and Wry, 2016), with resulting spillovers to the affiliated microenterprises. Further complicating the matter is that the characteristics of the MFIs themselves may mitigate the effects of a difficult macro environment. Next, we unpack and theorise the legitimacy spillover effect in which the macro-level instability constraints placed on organisations, and meso-level factors that moderate this effect, are associated with the rhetoric expressed by these organisations.

Hypothesis development

State fragility

One of the most pressing challenges associated with the microfinance industry is that it operates across a variety of adverse institutional environments (Sun and Liang, 2021). While some countries offer strong and stable institutions, many do not. This is often referred to as ‘state fragility’, which captures a country’s ability (or willingness) to provide essential services to its citizens (Fund For Peace, 2017). State fragility is a high-level indicator of legitimacy as the question of whether businesses and investors can rely on institutions drives that state’s attractiveness. Research notes that fragile states have more difficulty attracting foreign investment (Dimitrova and Triki, 2018); consequently, fragile states are more reliant on alternative financing mechanisms like the microfinance ecosystem. However, despite the many advantages of microfinance, it cannot escape macro-level institutional effects. The global unravelling of key democratic and economic institutions is increasingly directing attention to the fragility and stability of such institutions. More specifically, state fragility captures adversity at the macro (country) level, where the citizen’s social disadvantage can be a result of war, inequality (income, class, ethnic, racial, gender), conflict, poverty, displacement of people, poor state legitimacy and the rule of law, or deficiencies in access to healthcare, education, sanitation, power, infrastructure, human rights and judicial fairness. Fragile institutions can have devastating consequences for businesses, such as firm failure and decreasing benefits of long-term planning (Hiatt and Sine, 2014), ultimately adding another layer of difficulty in their quest for legitimacy.

The ‘institutional freedom’ of hybridity can only be leveraged by those whose legitimacy is secure in the first place (Pache and Santos, 2013). This means that local legitimacy is paramount (Tracey et al., 2018) yet, institutions that grant legitimacy in fragile states are weak and uncertain, making it difficult for businesses to understand and follow the rules of the game. For example, operating in failed states is related to higher MFI operating costs due to factors like bribery and corruption (Ault and Spicer, 2014). At the same time, Ault and Spicer (2014) found that MFIs had difficulty serving the demand for their services in fragile states. Further, Ault (2016) notes that MFIs alter the strategy when state fragility is heightened and emphasise financial performance rather than public good. Accordingly, pursuing the hybrid ideal (Battilana and Lee, 2014) by the MFI will be increasingly challenging in fragile institutional contexts; melding the economic and social elements of the organisation is less likely to be balanced. The same applies to microenterprises served by MFIs; it is harder for them to pursue and communicate hybridity, which will be evident in their narratives and rhetoric.

Legitimacy concerns related to hybridity lead us to expect that a microenterprise articulating its economic and social goals in tandem is not a common organisational form in fragile states (cf. Pache and Santos, 2013). The majority of organisations have hybrid goals, albeit to different degrees (Shepherd et al., 2019). Whereas the social (Allison et al., 2015) and financial (Anglin et al., 2020) aspects are critical to microfinance, attempts to fuse them together might be risky (Moss et al., 2018). Given the evidence suggesting that state fragility influences the behaviours of the MFI (Ault, 2016; Ault and Spicer, 2014; Sun and Liang, 2021), it follows that there will be a negative legitimacy spillover effect down to the microenterprise as well, where microenterprises avoid the complications of using hybrid rhetoric (that is, language simultaneously communicating economic and social goals) when state fragility is high.

Hypothesis 1: Higher state fragility is associated with lower microenterprise hybrid rhetoric.

Financial performance

An MFI’s path to legitimacy is challenging due to the newness of the organisational form (Khavul, 2010) coupled with the tensions of conflicting missions (Battilana and Dorado, 2010). On the one hand, there is an expectation of sound financial principles to ensure economic sustainability. On the other hand, they are formed with the express intent to improve local society through improving the livelihoods of the entrepreneurs. Yet, despite their hybrid goals, MFI intermediaries are not charities – they administer loans that must be repaid. Financial performance is no less important in the prosocial crowdfunding context where misalignment between local- and category-level stakeholder legitimacy demands is evident. At the local level, stakeholders such as investors/owners of the MFI expect a financial return, and high financial performance is necessary to ensure the longevity of the MFI. At the category level, stakeholders such as prosocial crowdfunding lenders worldwide expect that their capital will improve the lives of entrepreneurs. Indeed, recent scholarship has shown that microenterprises that pitch themselves on prosocial crowdfunding platforms receive funding more quickly when they emphasise social themes (Moss et al., 2018). Prior research has shown that this misalignment between local- and category-level stakeholders is problematic for organisations (Tracey et al., 2011), as one audience is usually prioritised over another (Fisher et al., 2017).

In a prosocial crowdfunding context however, legitimacy spillovers from MFIs to affiliated microenterprises are a mechanism that explains why the financial performance of the MFI is related to the hybrid rhetoric within the microenterprise pitches on those platforms. The affiliated microenterprises presented on prosocial crowdfunding platforms are purposefully chosen by the MFIs, as they represent only a subset of an MFI’s total loan portfolio. Additionally, most online pitches are written in the third person, suggesting that the MFIs play an important role in creating the online pitch narrative, albeit with input from the entrepreneur before the MFI posts the pitch narrative on the crowdfunding platform. This suggests the potential of the hybridity afforded to microenterprises is predicated on the MFI’s ability to show sound financial performance. MFIs, like many other startups, take time to make a profit. In fact, a large number of MFIs lose money (Cobb et al., 2016). Moreover, new evidence suggests that MFI performance is an important factor in the decision to support a microenterprise (Anglin et al., 2020). MFIs that establish themselves as financially self-sustaining are likely to enjoy more freedom in the way their affiliated ventures present themselves, as there is inherited legitimacy. In turn, they can embrace the complexity of both economic and social logics without impairing stakeholder perceptions. In other words, MFIs with poor financial performance are incentivised to push their affiliated ventures to focus on prevailing economic issues as it allows for more straightforward rhetorical signalling to an audience.

Therefore, we argue an important link will be manifest in the financial performance of the ‘parent’ MFI and the institutional vocabularies deployed by affiliated ventures via the spillover effect:

Hypothesis 2: Higher MFI financial performance is associated with greater microenterprise hybrid rhetoric.

MFI financial performance and state fragility

By and large, the previous hypotheses extend the domain of legitimacy spillovers by demonstrating that such spillovers not only take place between organisations in a certain category, as established in previous research (Shi et al., 2022), but also between affiliated organisations across categories and levels. It is important however, to note that where local institutions in any one country might be fragile in terms of laws, norms and conventions, there may still be MFIs operating in those countries that succeed financially. For example, Coopec Cahi, an MFI in Congo Democratic Republic, one of the most fragile states in the world in 2018, 1 maintained a profit margin percentage of over 20% throughout 2015–2018 (based on MIX Market data set, provided by the World Bank, which tracks the performance of MFIs). In another highly fragile country, Syria, an MFI – UNRWA – had a profit margin of 48% in 2018, even though at that time, Syria was ranked the fourth most fragile country in the world. Clearly, the institutionally legitimising forces at MFI (meso) and country (macro) levels can coexist in various combinations of high and low. While we expect to find significant relationships between the hybridity of microenterprises and both levels of institutional forces, we do not believe that the two levels of legitimacy spillovers operate in isolation from each other. The surrounding society influences what is appropriate in terms of microenterprise roles and behaviours, which pervades the decision-making of microentrepreneurs and extends to decisions relating to the accepted balance between social and commercial missions in a microenterprise. Yet the country-level institutional environment is exogenous to individual entrepreneurs, creating boundaries for what is – and is not – legitimate.

The importance of legitimacy spillovers from MFIs becomes particularly clear when considered in the context of macro-level institutions and their failures. When uncertainty in the local institutional environment increases, and the entrepreneur cannot be sure what the expectations of various local stakeholders are, it becomes particularly important that they can benefit from the strength of an MFI that serves them. Financially strong MFIs act as buffers, allowing affiliated microenterprises to draw on their legitimacy, so that those microenterprises can fully embrace both the social and commercial benefits they create. Legitimacy spillovers from the macro-level can then be thought of as the more distant influence on microenterprise hybridity, while the legitimacy of MFI at the meso level has the more immediate spillover effect on microenterprise hybridity. Despite the deleterious effects of state fragility previously hypothesised, the MFIs that achieve high financial performance should be able to convey the hybrid ideal to the microenterprises with which they work. Such MFIs draw from both high levels of local- and category-level legitimacy to lend some of it to the affiliated microenterprises, which are highly vulnerable because of their small size and typically precarious financial position. Thus, only high-performing MFIs will be able to offset, or mitigate the impact of state fragility to their microenterprise clients.

Hypothesis 3: Stronger MFI financial performance positively moderates the relationship between state fragility and the microenterprise’s hybrid rhetoric.

Methods

Data

MFIs typically operate within emerging economies supporting several special purposes, each facing unique challenges in their home countries. For these reasons, research on hybrid organising has frequently examined samples in the microfinance industry (Battilana and Dorado, 2010; Cobb et al., 2016; Pache and Santos, 2013). MFIs fill a critical funding gap for small-scale entrepreneurs starting or expanding their businesses. Given the multi-level nature of our theorising, we constructed a methodologically appropriate three-level hierarchical data set to capture microenterprises (level 1) nested within MFIs (level 2) operating within their respective countries (level 3).

Kiva

At level 1, we draw our sample of entrepreneurs from Kiva, arguably the most well-known prosocial crowdfunding platform and has been previously studied in the entrepreneurship literature (Jancenelle and Javalgi, 2018; Moss et al., 2018). Kiva is a non-profit organisation, and relies on donations to sustain its operations. It operates a lending-based crowdfunding model in which groups of individuals (the ‘crowd’) lend small amounts of money via Kiva’s online platform, which is then transferred to a local MFI which administers the loan. While Kiva’s lenders only receive their principal back, MFIs tend to charge interest or fees to cover their operational expenses. This approach differs from the rewards-based or equity-based crowdfunding models where backers receive a product or some type of ownership in the organisation, respectively, for their investment. As detailed on their website (www.kiva.org), a micro entrepreneur’s Kiva online profile includes their photograph, a textual narrative, country, industry sector, and information about the local MFI partner. Like venture pitches, the narratives from the microenterprises are crafted to entice the broader online ‘crowd’ into supporting the venture. These communications are vital to the lending process because there are significant information asymmetries between the micro entrepreneur and the lender (Ahlers et al., 2015); they are one of the few pieces of information the crowdfunding lender has to make a lending decision. The micro entrepreneur narratives are typically written in the third person and aided by the MFI. As such, the construction of these communications occurs within a specific institutional context that influences the information presented in the communications. A small portion of Kiva loans are used for non-business purposes, notably in the education and housing category. Thus, those categories were filtered out of our sample.

Microfinance information exchange

On the meso-level (level 2), we draw on data from the Microfinance Information Exchange (MIX), the largest and most comprehensive source of global microfinance institution-level financial and operational data available. The World Bank created MIX to provide additional transparency to the microfinance industry, and it has been used in previous studies that explore MFIs (Cobb et al., 2016; Zhao and Wry, 2016). As noted above, MFIs typically charge interest fees to sustain their operations. Further, while many MFIs operate as non-profits, there is also a subset of for-profit entities. As highlighted below, we account for this in our control variables. We merged the MIX data with Kiva microenterprise data based on the microfinance partner entity’s name, listed on each micro entrepreneur’s Kiva profile. We removed from the sample one MFI due to its large size, and ten countries with less than 1,000 loans in the sample.

Fragile states index

At level 3, we use the Fragile States Index to capture macro-level influence. This index is published by The Fund for Peace and contains country-level institutional data commonly used in economic and conflict studies (Dimitrova and Triki, 2018). In addition, we included country-level data from the World Bank, which we leverage to build control variables. In sum, the merged three-level dataset yielded 374,277 loans nested within 99 MFIs, with an average of 3780 entrepreneurs in each MFI, operating in 38 countries, with an average of 9849 loans per country. The years covered include 2011 through 2017, and we lag the meso- and macro-level variables one year (cf. Cobb et al., 2016). We also describe multiple measures for relevant variables below to provide more robust conclusions, including an exploratory post hoc analysis (Anderson et al., 2019).

Measures

Dependent variable

Our central research question concerns whether legitimacy spills over from higher-level institutions and influences the hybrid rhetoric employed by microenterprises. By definition, a hybrid organisation attempts to achieve economic and social goals simultaneously, which will be reflected through using multiple vocabularies simultaneously. Scholarly interest in hybrids balancing social and economic orientations is shifting towards the question of ‘how much’ of each dimension rather than a dichotomous view of ‘whether or not’. Importantly, this new research direction acknowledges that firms manifest varying degrees of hybridity (Shepherd et al., 2019). Very few for-profit firms have entirely economic goals, nor will nonprofits exhibit purely social motives, as these would alienate their key stakeholder groups. The tensions associated with ‘how much’ are likely to be reflected in the institutional vocabularies deployed by the venture, illustrating the degree to which economic and social goals are emphasised and integrated.

Text narratives are an effective way to communicate prevailing organisational emphases through the use of institutional vocabularies (Suddaby and Greenwood, 2005). Given the large number of narratives to be analysed, algorithmic approaches are often the most consistent and efficient. Thus, to measure the hybrid balance, we leverage CATA, deriving the measure from the online pitch narratives of micro entrepreneurs on the Kiva crowdfunding platform. We utilise validated word dictionaries for economic value orientation (EVO) and social value orientation (SVO), developed by Moss et al. (2018), who follow best practices outlined by McKenny et al. (2018) to determine the emphasis placed on economic value and social value in each narrative. These dictionaries were then processed in Linguistics Inquiry and Word Count (LIWC; Pennebaker et al., 2017) software to analyse the loan narratives to generate quantifiable data operationalised as the dictionary word frequency per one hundred words of text. The LIWC formatted dictionaries used by Moss et al. (2018) and illustrative examples are provided in Supplemental Appendix S.1 for convenience.

Hybrid balance is derived by the formula highlighted below. First, the LIWC scores for EVO and for SVO are standardised (e.g. z-scores) and shifted so that the minimum value is zero. Next, we take the absolute value of the difference between the scores, where a value of zero indicates a perfect balance between the two logics. Last, the value is reverse scored to simplify interpretation, meaning that more negative values suggest further distance from hybridity. In contrast, less negative values suggest balance, an approach consistent with Moss et al. (2018). This variable was then winsorised at the 0.001 level to reduce the outlier effects. The results of the non-winsorised variable are consistent, albeit with non-normal residual plots. We also constructed an alternative measure, EVO-SVO Skew, capturing the direction of imbalance, which we discuss in our post hoc analysis.

Independent variables

We draw meso-level independent variables from the MIX dataset (Ault, 2016; Cobb et al., 2016). First, MFI ROA captures the microfinance institution’s return on assets, a standard measure to gauge organisational financial performance. A second variable, MFI OSS, captures whether the microfinance institution was financially self-sustaining, offering a secondary dichotomous operationalisation of performance for robustness. We use the overall Fragility Index the Fund For Peace (2017) provides at the macro-level. This measure is based on an assessment of a country’s conflict and has been used for over a decade (Carlsen and Bruggemann, 2017). The index relies on qualitative and quantitative indicators from public source data, producing quantifiable results. The index changes year-over-year based on updated information and is reported as country-year observations. The index is a summed continuous measure of the 12 indicators for 178 countries, in which a lower score indicates a better, less fragile environment. In 2018, the countries with the highest scores (most fragile) were South Sudan (113.4) and Somalia (113.2). The countries with the lowest scores are Finland (17.9) and Norway (18.3).

Control variables

We include several control variables in our models, which could reasonably be expected to affect the results. We account for the scope and size of the microfinance institution by capturing MFI Loan Count, MFI Assets in USD, and the MFI Age measured in years, as older or larger MFIs might have routines in place that may affect communicated hybridity. In addition, we account for the organisation’s recognised status as MFI For Profit, the MFI Board Size, and the MFI Quality Rating.

At the venture (micro) level, we draw from the Kiva data to account for gender as Gender (F) for female entrepreneurs, whether a Group made the loan, and finally, the Group Size. We also include loan significance, measured as the loan amount as a percentage of the GDP Per Capita (via World Bank), indicating the significance of the loan relative to the country where the entrepreneur resides. Larger loans might reasonably be expected to affect the emphasis on economic or social value creation. Following Moss et al. (2018), we include a measure of tangible and intangible assets. These measures were created based on custom text analysis dictionaries described in their article and were made available by the authors. Tangible assets measure fixed and current assets, while intangible assets measure nonphysical assets and skills. A greater emphasis on assets should affect a micro entrepreneur’s emphasis on EVO and SVO.

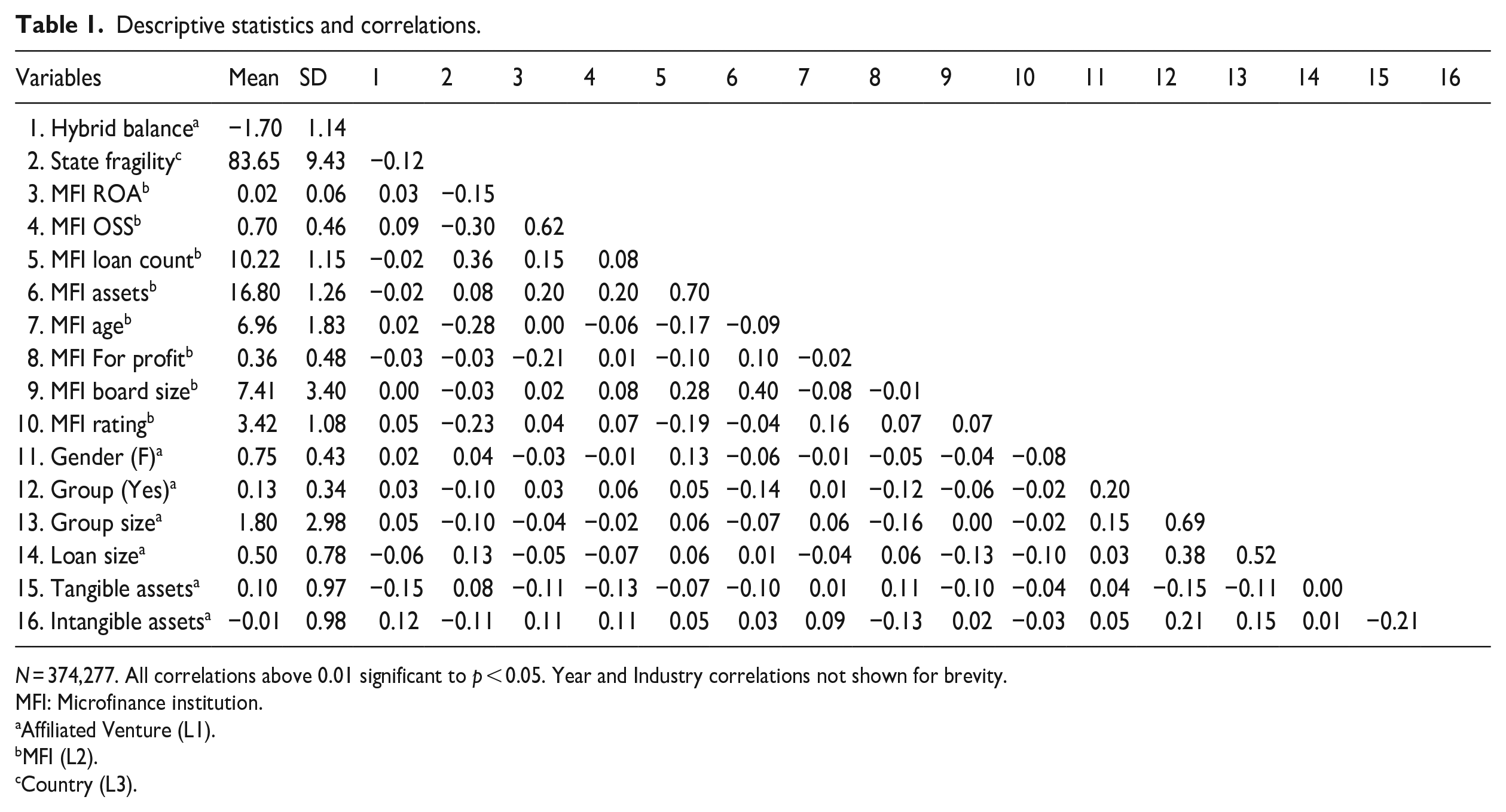

Finally, we also include controls for the year in which the loan was posted on the Kiva website to account for any year effects and for the industry sectors in which Kiva classifies its loans: Agriculture, Arts, Clothing, Construction, Entertainment, Food, Health, Manufacturing, Retail, Services, Transportation and Wholesale. Table 1 displays correlations and Table 2 provides an overview of the variables.

Descriptive statistics and correlations.

N = 374,277. All correlations above 0.01 significant to p < 0.05. Year and Industry correlations not shown for brevity.

MFI: Microfinance institution.

Affiliated Venture (L1).

MFI (L2).

Country (L3).

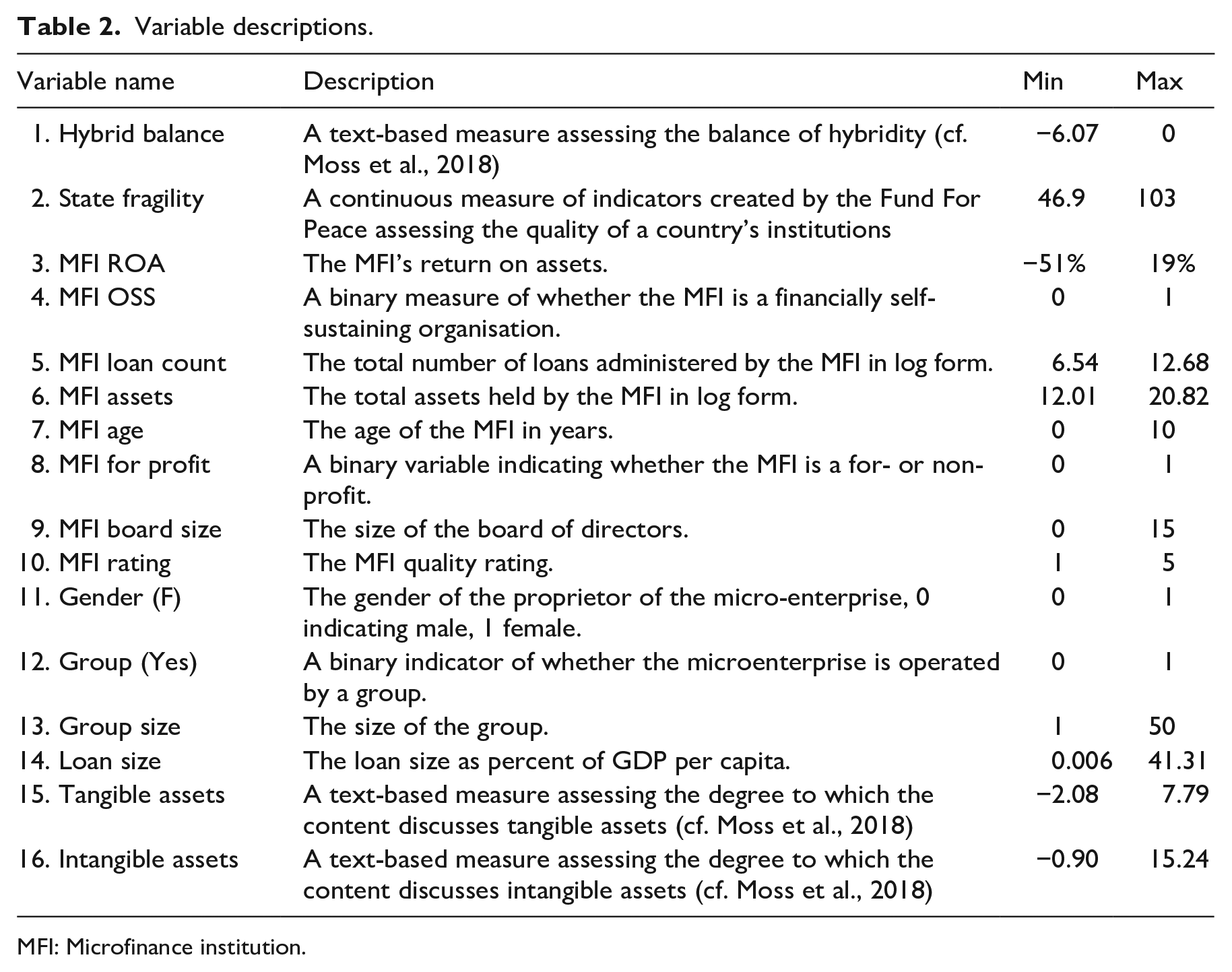

Variable descriptions.

MFI: Microfinance institution.

Analysis and results

To test our hypotheses and to address robustness concerns, we use mixed-level modelling (MLM; also called hierarchical linear modelling or random coefficient modelling). MLM is useful when observations are nested and are thus not independent. This technique accounts for the non-independence of nested observations by concurrently estimating regression models at specific levels of analysis. Our null models indicated an ICC1 of 0.30 at the second level (entrepreneurs nested within MFIs) and 0.08 at the third level (MFIs nested within countries), suggesting the appropriateness of MLM (cf. Bliese et al., 2018). In our case, each interaction variable has a meaningful value for zero and therefore, is not mean-centred (cf. Aguinis et al., 2013). State fragility is standardised at the country level to ease the interpretation of the overall effect size.

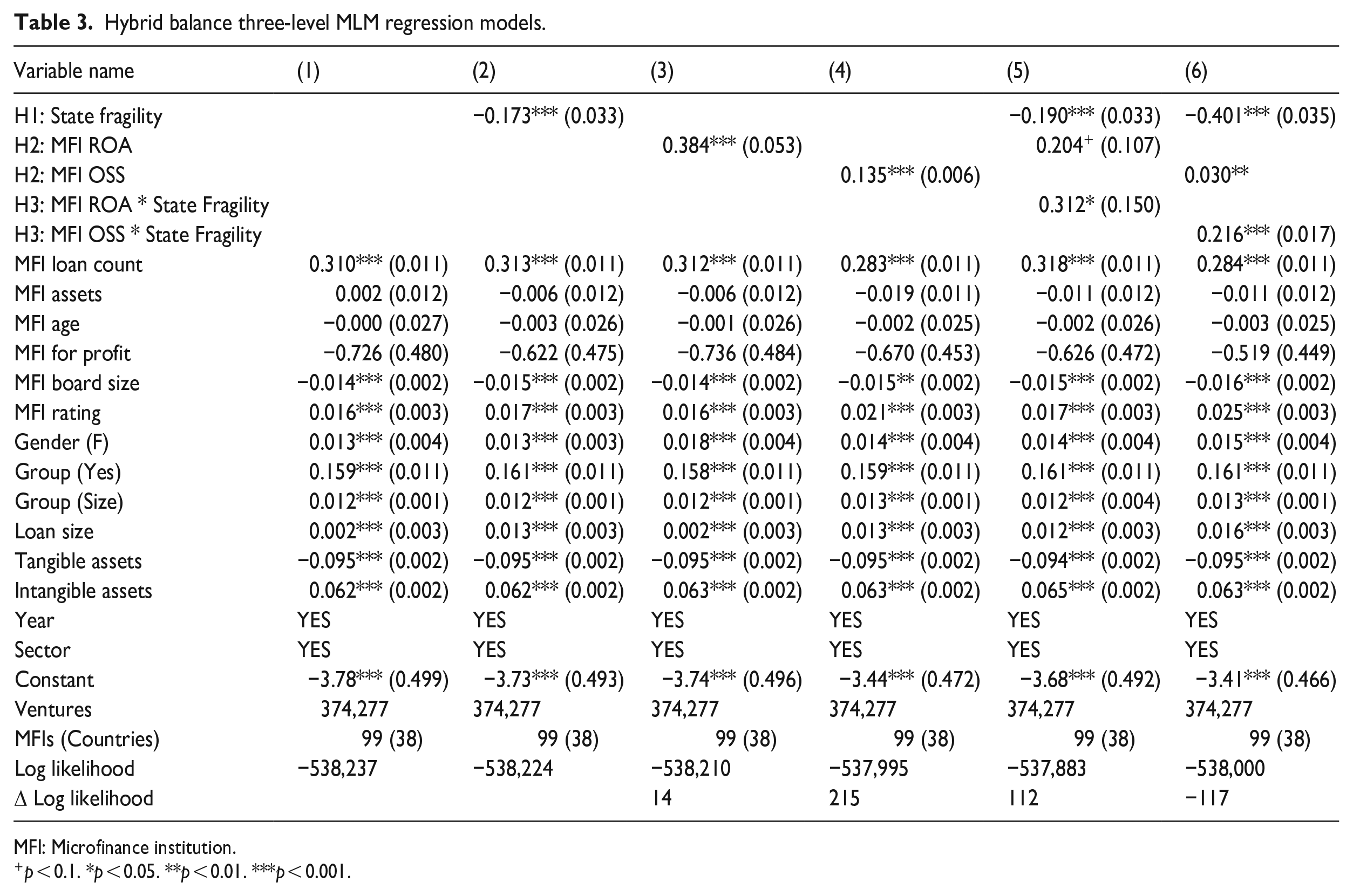

Hypothesis tests

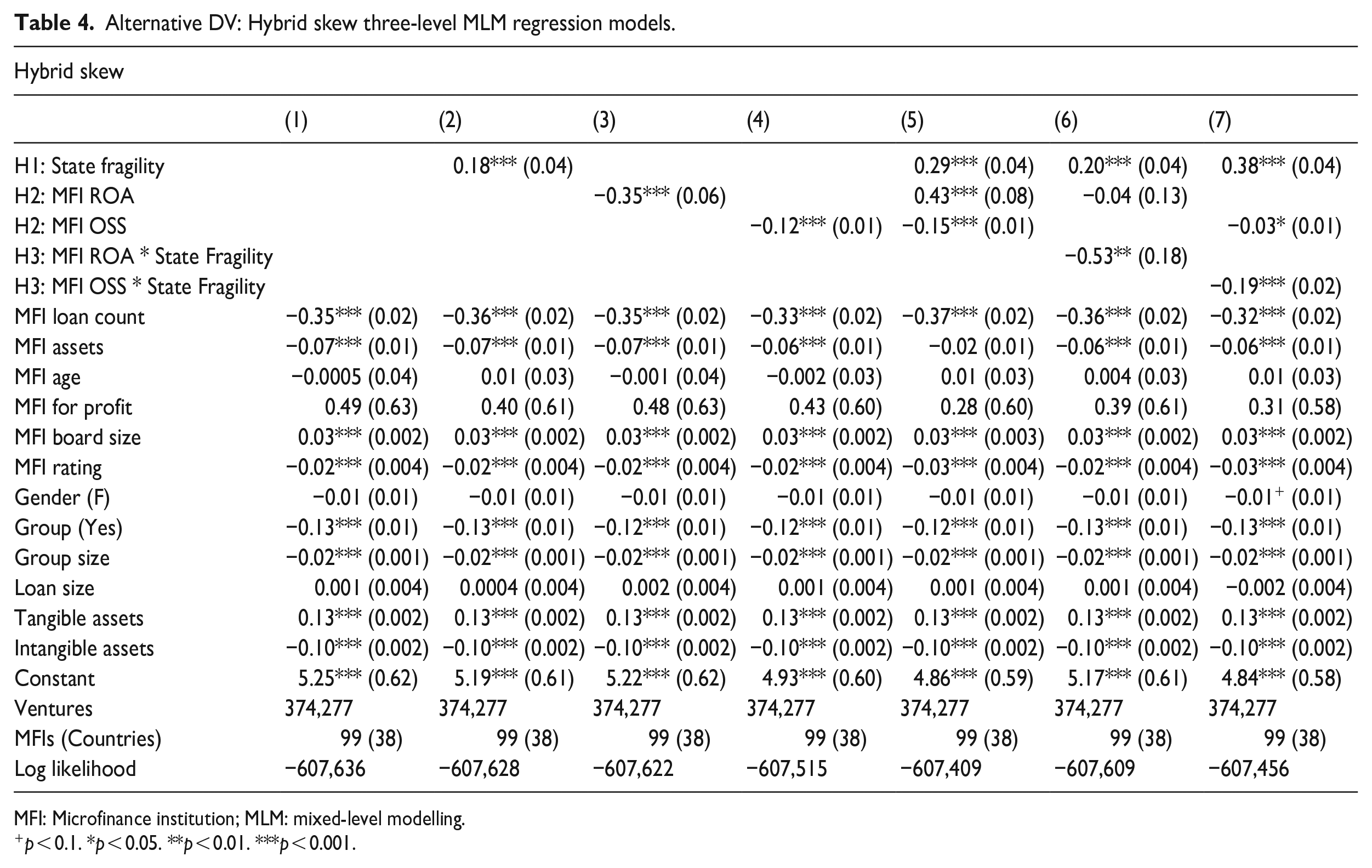

Table 3 presents the MLM regression results for the main effects tests. Model 1 tests the effects of the control variables in isolation. Model 2 tests our first hypothesis, suggesting that state fragility impairs hybrid balance (γ = −0.18, p < 0.001), and H1 is thus supported. Models 3 and 4 provide tests for our second hypothesis, where we speculated that MFI performance would increase the hybrid balance of the affiliated ventures. We find support for H2 with both of our performance measurements, MFI ROA (γ = 0.384, p < 0.001) and MFI OSS (γ = 0.135, p < 0.001). Model 7 includes all independent variables simultaneously.

Hybrid balance three-level MLM regression models.

MFI: Microfinance institution.

p < 0.1. *p < 0.05. **p < 0.01. ***p < 0.001.

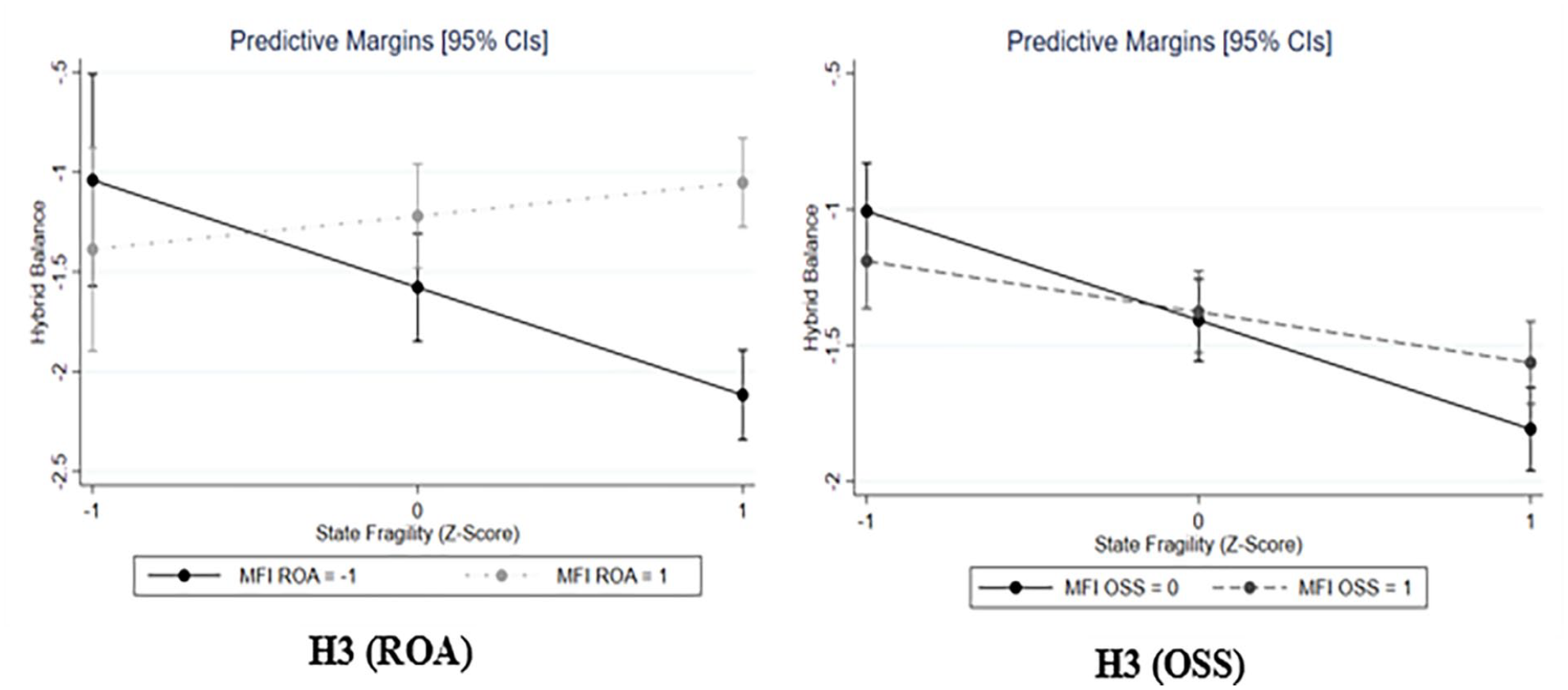

We then predicted that MFI performance would positively moderate the negative relationship between state fragility and hybrid rhetoric by the affiliated microenterprise. Figure 1 displays visual interaction plots. Models 5 and 6 test whether higher MFI Performance would mitigate the negative impact of state fragility on hybrid balance. MFI ROA (γ = 0.352, p = 0.019) and MFI OSS (γ = 0.214, p < 0.001) both had significant interactions, supporting Hypothesis 3. We expand on these results and the size of the effects in the subsequent discussion.

State fragility interaction plots.

Post hoc analysis: Alternative dependent variable

Our hypotheses did not explicitly predict which logics the venture would emphasise, though we believe it is an interesting empirical question and will likely inspire additional theoretical insights. Therefore, we also ran our models using a different operationalisation of our dependent variable where, instead of taking the absolute value of hybridity to determine balance, we tested to see whether economic or social is the prevailing logic. This variable is calculated simply as the standardised EVO measure minus the standardised SVO measure. A positive value emphasises an economic logic, while a negative value indicates a social logic. The mean of this variable is 1.52 and ranges from a minimum value of −4.54 to a maximum value of 5.99. Table 4 displays the results from replicating our hypotheses using this variable.

Alternative DV: Hybrid skew three-level MLM regression models.

MFI: Microfinance institution; MLM: mixed-level modelling.

p < 0.1. *p < 0.05. **p < 0.01. ***p < 0.001.

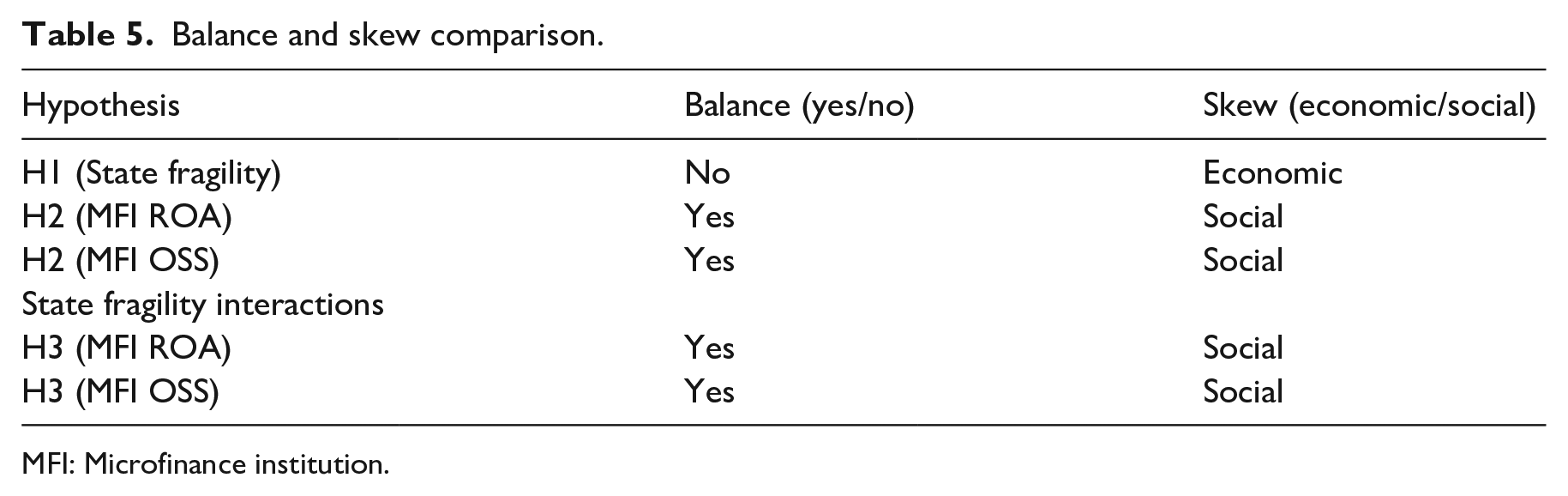

State fragility led to a skew towards economic focus (γ = 0.18, p < 0.001). MFI financial performance is associated with greater emphasis on social logics; ROA (γ = −0.35, p < 0.001), OSS (γ = −0.12, p < 0.001). The interaction between ROA and state fragility led to a social emphasis (γ = −0.53, p = 0.003) and was consistent with OSS (γ = −0.19, p < 0.001). Table 5 illustrates a summary of the balance and skew effects for comparison.

Balance and skew comparison.

MFI: Microfinance institution.

Discussion

Our study offers three primary contributions. First, we identify a subset of associated mechanisms that point to the origins of hybrid rhetoric. While many studies have identified the influence of rhetoric in crowdfunding settings as an explanatory variable (Allison et al., 2017; Anglin et al., 2018; McSweeney et al., 2022; Steigenberger and Wilhelm, 2018), we have little evidence regarding why microenterprises choose to position themselves as they do. Through the theorised legitimacy spillover effect, this study offers a path towards illuminating possible antecedents of hybrid rhetoric. Second, our multi-level study integrates and extends prior studies that explain the role of the MFI (Anglin et al., 2020) and the larger institutional context in which the MFI and microenterprise operate (Ault, 2016). Studies that capture the interplay between the macro-meso-micro institutions and organisations are quite rare (Johnson and Schaltegger, 2020), suggesting that the theoretical puzzles of microfinance are inherently incomplete. We find that MFI financial performance is associated with hybrid rhetoric for the affiliated microenterprises while also moderating the effects of country-level instability. Thus, we take an important first step to uncover a more complete picture of the microfinance landscape. Finally, our study examined hybridity in degrees rather than absolutes (Shepherd et al., 2019) so as to account for the variance in hybridity between organisations using quantitative methods that account for variance in hybridity, which to date has been characterised by qualitative methods (Battilana et al., 2017). Our methodological approach enabled robust and large-scale hypothesis testing across a variety of institutional settings that are only possible with quantitative methods. These findings from a large sample should be interpreted in light of balancing the statistical significance of the results with the practical importance of the relationships uncovered. To avoid over-reliance on statistical significance, we followed Combs’s (2010) suggestion, drawing our measures from established sources that have already demonstrated construct validity and highlighting the meaningfulness and relevance of our results, as we outline below.

Our analysis suggests that the most substantial effect on hybrid balance is derived from the financial performance of the MFI. Consistent with the literature, performance is an important part of the legitimacy of these hybrid financial organisations (Kent and Dacin, 2013), and thus is prone to legitimacy spillover. ROA in our sample varied from −51% to a positive return of 18%, suggesting that while financial performance is a challenge for an MFI, the impact on its affiliated ventures can be substantial, where the range in our sample accounts for one-third of a standard deviation in hybrid rhetoric balance. The cross-level interactions shed additional light on performance, where the effect of state fragility on hybridity is less extreme for microenterprises affiliated with high-performing MFIs, but quite dramatic for those affiliated with lower-performing MFIs, as visualised in Figure 1. In other words, MFIs with lower performance might be perceived as less legitimate and thus, encourage ventures they support to simply emphasise either economic or social goals, rather than attempting balance. Our alternative dependent variable, which tested the skew towards economic or social emphasis, suggests that an economic emphasis of a microenterprise is more prevalent at lower levels of ‘parent’ MFI performance, offering further evidence of the spillover effect.

Theoretical implications

To date, theories concerning MFIs as hybrid organisations offer insights into various domains of organisational tensions: intra-organisational relationships, culture, organisational design, workforce composition, and organisational activities (Battilana et al., 2017; Battilana and Lee, 2014; Pache and Santos, 2013; Smith and Besharov, 2019). We build on, and extend, these studies by examining how the performance of an MFI relates to hybridity as adopted by those entrepreneurs who depend on the MFI for their financing. Our theory and findings suggest that legitimacy pressures faced by a poorly performing parent organisation (MFI) systematically influence the institutional vocabularies employed by affiliated microenterprises. As such, we show how the concept of legitimacy spillovers (Shi et al., 2022) can help us understand the origins of hybrid communication among some of the world’s most vulnerable entrepreneurs.

A majority of organisations operate along a continuum of hybridity. Given that organisational hybridity is both delicate and important to stakeholders, specifically the MFI-affiliated microenterprises, there is theoretical value in assessing what moves an organisation to signal more or less hybridity (Shepherd et al., 2019). To assess hybridity, we use textual narratives that serve as the primary vehicle to influence potential lenders and are created in collaboration between the microenterprise and the MFI. Thus, our study offers a relatively objective assessment of the hybridity continuum, building on previous studies where hybridity has been often assessed as a simple categorical variable, using more subjective measurements (cf. Fu, 2023). Finally, our global sample and three-level model offers a robust assessment of how hybrid manifestations change as the macro environment changes. Because MFIs operate in a number of countries with a wide variance in institutional stability, it is reasonable to expect that the legitimacy constraints would be influenced by country context. Thus, our theory and data shed light onto MFIs in a variety of geographies, aiding in the generalisability of our findings.

Relevance

Previous research concerning MFIs notes the challenges of grappling with competing institutional logics (Kent and Dacin, 2013). Given the important role MFIs play in emerging economies, it is critical to assess both the internal workings of MFIs as well as their affiliates. Rather than relying exclusively on the benevolence of the wealthy, MFIs offer a path of financial independence to enterprises that would otherwise be excluded from capital markets. However, the complications of the MFI, and their home countries, need to be acknowledged in order to construct a more complete picture. Our study sheds light on these issues, highlighting several factors that relate to the MFI influence over the ventures they finance. For policymakers, our findings suggest that if we want to support microenterprises in pursuing both social and economic goals, we need to ensure that the institutions at the country level are stable and that key organisations supporting microenterprises locally are seen as legitimate. While it may feel that there is sometimes little we can do to prevent country-level institutions from faltering, policymakers and the public can still work to ensure that MFIs, as an organisational form, enjoy legitimacy as valuable institutions supporting economic development.

Limitations and future research

As with any study, there are several limitations that we hope will inspire further theoretical refinement. First, big data samples are attractive for a number of reasons (George et al., 2014), but also have notable challenges (Combs, 2010). One such challenge is that our methodology relies on CATA to assess hybridity, which may fail to capture nuance within textual narratives. For example, words can imply different intensities (e.g. like versus love), and dictionary-based approaches to automated content analysis presently lack the capability to identify these. Thus, future research to determine organisational hybridity would benefit from continued refinement of these methods, perhaps using advanced machine learning algorithms borrowed from the computer science literature (Choudhury et al., 2021). Next, while this study offers a truly global perspective on the influence of MFIs on legitimacy spillovers and captures multiple years of MFI operations, our technique does not capture causality. One fruitful avenue to address this deficiency would be to follow a smaller set of homogeneous MFIs from their inception and track how affiliated hybrid framing changes as the MFI gains legitimacy over time, perhaps supplementing CATA analysis with a subset of interviews from the MFI employees involved in creating the loans. Third, we relied on Kiva for the individual-level portion of our dataset. This decision was pragmatic for several reasons, as outlined in our methods section, but potentially also suggests that the generalisability of the results needs to be carefully considered. Given the size and influence of Kiva in the prosocial crowdfunding space, a comparison between enterprises operating on Kiva, and those who do not, would be a leap forward in this regard. Finally, while the funding performance of the microloan was outside of the scope of this study, there are opportunities to further understand the consequences for the quality of the institutions and how it might influence funding performance (Anglin et al., 2020).

Footnotes

Acknowledgements

The authors gratefully acknowledge the thoughtful feedback of the attendees of the 2018 Annual Social Entrepreneurship Conference.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.