Abstract

Due to the high perceived risk and low switching cost, it is critical to building users' initial trust in mobile payment in order to facilitate their adoption and usage. The purpose of this research is to examine the effect of initial trust on user adoption of mobile payment. We conducted data analysis with structural equation modeling. The results indicated that perceived security, perceived ubiquity and perceived ease of use have significant effects on initial trust, which in turn determines perceived usefulness and usage intention. We also found that perceived cost is a significant determinant of usage intention.

Mobile service providers need to offer secure, easy-to-use and reliable payment services to users.

Introduction

Mobile Internet has been developing rapidly around the world. According to a report issued by China Internet Network Information Center (CNNIC) in July 2011, the number of mobile Internet users in China has exceeded 318 million, accounting for 66 percent of the Internet population (485 million) (China Internet Network Information Center 2011). This shows the great mobile user base in China. Especially, the introduction of third generation (3G) communication technologies will trigger mobile Internet development. A few traditional electronic commerce applications and services such as instant messaging (IM), online games and online search have been successfully migrated to mobile platforms. As a basic service supporting mobile transaction, mobile payment has been attached great importance by enterprises. For example, Alipay, which is the largest online payment service provider in China, has released its mobile payment product: Shouji Zhifubao.

Mobile payment means that users adopt mobile terminals to conduct payment at anytime from anywhere. With the help of mobile networks, users have been freed from the temporal and spatial restrictions and they can enjoy the great convenience brought by mobile payment. However, due to the virtuality and lack of control, mobile commerce involves great uncertainty and risk (Siau and Shen 2003, Li and Yeh 2010). To some extent, compared to online payment, mobile payment involves greater risk. For example, wireless networks are vulnerable to hacker attack and information interception. Mobile encryption systems are not as intact and robust as online encryption systems (Misra and Wickamasinghe 2004). These security problems will increase users' perceived risk and decrease their usage intention of mobile payment. Thus, establishing users' trust and mitigating their perceived risk is critical for mobile payment service providers.

As an emerging service, mobile payment has not been widely adopted by users (Dahlberg et al. 2008). The CNNIC (2011) report indicates that only 7.3 percent of mobile Internet users in China have ever used mobile payment. This highlights the necessity to establish users' initial trust in mobile payment to encourage their usage behavior. Initial trust develops when users interact with mobile payment service providers for the first time. On the one hand, due to the lack of previous usage experience, users' perceived uncertainty and risk are very high (McKnight et al. 2002a). Thus they need to build initial trust to mitigate perceived risk. On the other hand, switching cost is low (McKnight et al. 2002b). If users cannot build their initial trust, they may switch to other mobile payment service providers or online payment. Thus, it is imperative to identify the factors affecting users' initial trust in mobile payment. Then mobile service providers can adopt effective measures to engender users' initial trust and facilitate their adoption of mobile payment.

Literature review

Initial trust

Due to its significance, initial trust has received considerable attention in the electronic commerce context. Various factors are identified to affect online initial trust. The first category of factors is associated with website characteristics. Website represents the interaction interface between online vendors and consumers. It is similar to a traditional store’s sales representative. Consumers may rely on their perceptions of websites to form their initial trust in online vendors. Website quality has been found to significantly affect initial trust (McKnight et al. 2002b, Wakefield et al. 2004, Lowry et al. 2008). Information quality also has a significant effect on initial trust (Nicolaou and McKnight 2006, Yang et al. 2006). In addition, two factors of the technology acceptance model (TAM), which include perceived usefulness and perceived ease of use, are often suggested as the determinants of online initial trust (Koufaris and Hampton-Sosa 2004, Wang and Benbasat 2005, Benamati et al. 2010). Other possible factors affecting initial trust include perceived security, perceived privacy (Chen and Barnes 2007), and usability (Hampton-Sosa and Koufaris 2005). The second category is associated with consumer characteristics. Trust propensity, which reflects a consumer’s natural trust tendency, has a direct (McKnight et al. 2002a) and moderation effect (Chen and Barnes 2007) on initial trust. The third category is associated with online vendors. Among them, reputation as a trust signal is a salient factor affecting initial trust (McKnight et al. 2002b, Fuller et al. 2007). Other factors include company size, willingness to customize (Koufaris and Hampton-Sosa 2004, Chen and Barnes 2007), and brand image (Lowry et al. 2008). The fourth category is associated with third parties. When websites build linkages with credible third parties, users may transfer their trust in the third parties to websites (Stewart 2003). These factors affecting initial trust include trust seals (McKnight et al. 2004, Hu et al. 2010), portal affiliations (Lim et al. 2006), brand association (Delgado-Ballester and Hernandez-Espallardo 2008), and structural assurances (McKnight et al. 2002b, Kim and Prabhakar 2004). Culture has been also found to moderate the effect of portal affiliation on initial trust (Sia et al. 2009).

Compared to the abundant research on online initial trust, there exists less research on mobile users' initial trust. Siau and Shen (2003) proposed a theoretical framework, suggesting that initial trust is affected by the factors related to mobile technology and vendor. The former category includes feasibility, whereas the latter includes familiarity, reputation, information quality, third-party recognition and attractive rewards. Kim et al. (2009) examined initial trust in mobile banking. They found that structural assurance is a main determinant of initial trust. Luo et al. (2010) found that initial trust affects performance expectancy and perceived risk, both of which further determine usage intention of mobile banking.

Mobile payment adoption

User adoption of mobile payment, which represents an emerging service, has received attention from researchers. TAM is often used as the theoretical base. Kim et al. (2010) noted that individual differences and mobile payment system characteristics affect mobile payment usage intention through perceived usefulness and ease of use. Individual differences include innovativeness and knowledge on mobile payment, whereas mobile payment system characteristics include mobility, reachability, compatibility and convenience. Chandra et al. (2010) argues that trust affects user adoption of mobile payment through perceived usefulness and perceived ease of use. Shin (2010) proposes that besides both factors of TAM, perceived risk and trust also affect consumer acceptance of mobile payment systems.

In addition to TAM, the innovation diffusion theory (IDT) has also been used to explain mobile payment user behavior. For example, with a qualitative study, Mallat (2007) found that relative advantage, complexity, pricing and perceived risk have significant effects on user adoption of mobile payment. Schierz et al. (2010) reported that perceived compatibility has a strong effect on the intention to use mobile payment.

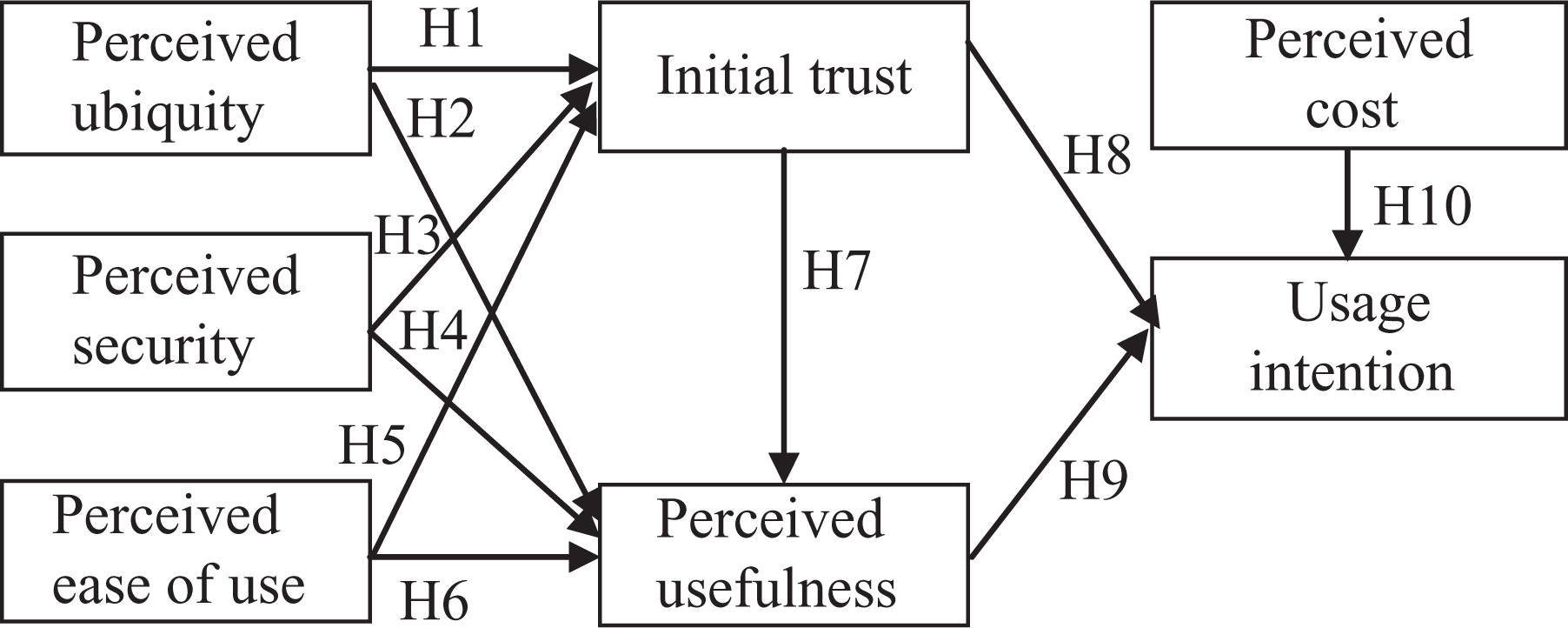

Research model and hypotheses

Perceived ubiquity

A main advantage of mobile payment is ubiquity, which means that users can access mobile payment services at anytime from anywhere (Varshney and Vetter 2002). Compared to traditional and online payment, mobile payment has freed users from temporal and spatial restrictions (Dahlberg et al. 2008). Users can conveniently conduct payment in real time, which improves their living and working performance and efficiency. However, it means a challenge for mobile service providers to offer ubiquitous payment services because users are always on movement. They need to invest great effort and resource to ensure the reliability and availability of mobile payment. This may enhance users' initial trust. If mobile payment services are always unavailable and unreachable, users may feel that service providers have not enough ability and integrity to provide quality services. This will decrease their trust. Prior research has revealed the effect of ubiquity on user trust and perceived usefulness. For example, Lee (2005) found that ubiquitous connections affect mobile user trust. Kim et al. (2010) suggested that mobility (similar to ubiquity) influences perceived usefulness of mobile payment. Thus, we propose,

H1: Perceived ubiquity positively affects initial trust.

H2: Perceived ubiquity positively affects perceived usefulness.

Perceived security

As mobile payment deals with financial information, it involves great uncertainty and risk for users. Users may doubt whether mobile service providers can ensure their payment security, such as account and password confidentiality. To some extent, security is the cornerstone of mobile payment (Mallat 2007). If mobile payment is insecure, users may feel that mobile service providers have not enough ability and benevolence to protect them from potential problems. This will affect their initial trust. In addition, mobile payment lacking security cannot be deemed useful by users. Much research has reported the effect of perceived security on online consumer trust. Kim (2008) noted that security protection as a self-perception based factor strongly affects user trust in online vendors. Koufaris and Hampton-Sosa (2004) found that perceived security has a direct effect on online consumers' initial trust. Kim et al. (2008) reported that perceived security protection as a cognition-based factor affects online consumers' trust.

H3: Perceived security positively affects initial trust.

H4: Perceived security positively affects perceived usefulness.

Perceived ease of use

Perceived ease of use reflects the difficulty of using mobile payment. Compared to desktop computers, mobile terminals such as mobile phones have some constraints, such as smaller screens, lower resolution and inconvenient input. This highlights the need to present users with an easy-to-use interface (Lee and Benbasat 2004). If mobile interfaces do not have clear layout and effective navigation, users may feel difficult to use mobile payment. They may also doubt mobile service providers' ability and benevolence to provide quality services. This will affect their initial trust. A few mobile payment services require users to download and configure the software based on the type of their mobile phones. If the configuration process is complex, users cannot perceive the utility of mobile payment. Previous research has pointed out the effect of perceived ease of use on user trust (Li and Yeh 2010) and perceived usefulness (Kim et al. 2010, Shin et al. 2010).

H5: Perceived ease of use positively affects initial trust.

H6: Perceived ease of use positively affects perceived usefulness.

Initial trust and perceived usefulness

Trust reflects a willingness to be in vulnerability based on the positive expectation towards another party’s future behavior (Mayer et al. 1995). Trust includes three beliefs: ability, integrity and benevolence (Kim et al. 2008, Palvia 2009). Ability means that mobile service providers have enough skills and knowledge to fulfill their tasks. Integrity means that mobile service providers keep their promises and do not deceive users. Benevolence means that mobile service providers are concerned with users' interests, not just their own interests. Perceived usefulness reflects that users obtain their expected utility associated with using mobile payment. Trust provides a guarantee that users will acquire their expected utility (Gefen et al. 2003). If users do not trust mobile service providers, they may feel that mobile service providers lack the ability, integrity or benevolence to provide quality mobile payment services. This will decrease their perceived usefulness. The effect of trust on perceived usefulness has been validated in a variety of contexts, including online shopping (Gefen et al. 2003, Pavlou 2003), electronic voting (Gefen et al. 2005) and online recommendation agents (Wang and Benbasat 2005). Thus, we posit,

H7: Initial trust positively affects perceived usefulness.

Perceived cost and usage intention

Trust has been found to mitigate perceived risk and encourage user behavior (Gefen et al. 2008, Kim et al. 2008). Perceived usefulness as a positive expectation also encourages user behavior (Venkatesh et al. 2003). In fact, perceived usefulness has been found to be a significant determinant of both initial and continuance usage intention (Venkatesh and Davis 2000). Numerous studies have revealed the effects of trust and perceived usefulness on behavioral intention (Kim et al. 2009, Li et al. 2010, Lu et al. 2010). Compared to the positive effects of both initial trust and perceived usefulness, perceived cost may have a negative effect on usage intention. Users need to bear some costs such as communication fees and transaction fees when using mobile payment services. These costs may inhibit user adoption of mobile payment services. Previous research has found the effect of perceived cost on user adoption of 3G services (Kuo and Yen 2009), digital multimedia broadcasting (DMB) (Shin 2009), mobile Internet (Shin et al. 2010) and mobile games (Ha et al. 2007).

H8: Initial trust positively affects usage intention.

H9: Perceived usefulness positively affects usage intention.

H10: Perceived cost negatively affects usage intention.

Data collection

Research model

To validate the proposed model, we conducted an empirical study, which is common in information systems and user behavioral research (Straub et al. 2004). We first developed the measurement items for each factor, which represents a latent variable. Then we collected data through a survey and examined these data with structural equation modeling (SEM), which is widely used to conduct multiple-variable statistical analysis. SEM includes two types: covariance-based such as LISREL and component-based such as PLS. Compared to PLS, LISREL can provide more fit indices to measure the research model. In addition, LISREL is often used in confirmative research, whereas PLS is used in explorative research. Considering that our research is confirmative and has strong theoretical support, we adopted LISREL to conduct data analysis.

The research model includes seven factors and each factor was measured with multiple items. All items were adapted from existing literature to improve content validity (Straub et al. 2004). These items were first translated into Chinese by a researcher. Then another researcher translated them back into English to ensure consistency. When the instrument was developed, it was tested among ten users that had mobile payment usage experience. Then according to their comments, we revised some items to improve the clarity and understandability. The final items and their sources are listed in Appendix A.

Items of perceived ubiquity were adapted from Lee (2005) to reflect that users can use mobile payment services at anytime from anywhere. Both perceived security and initial trust were measured with items from Koufaris and Hampton-Sosa (2004). Items of perceived security reflect that mobile service providers adopt security measures such as identity verification to ensure payment security. Items of initial trust reflect a user’s beliefs towards mobile service providers' ability, integrity and benevolence. Items of perceived cost were adapted from Luarn and Lin (2005) to measure the access and transaction costs associated with using mobile payment. Items of perceived ease of use, perceived usefulness and usage intention were adapted from Kim et al. (2010). Items of perceived ease of use reflect the difficulty of learning to use and skillfully using mobile payment. Items of perceived usefulness reflect the transaction and payment efficiency improvement by using mobile payment. Items of usage intention reflect the intention to use mobile payment in future.

Data were collected at the service halls of China Mobile and China Unicom, which represent two main telecommunication operators in China. There are plenty of mobile users at these places and this expedited our data collection process. We randomly contacted users and inquired whether they had mobile payment usage experience. Then we invited those without previous experience to access mobile payment services via the mobile phones provided by us. We had installed simulated mobile payment software in these mobile phones in advance. Then they were asked to fill the questionnaires based on this first usage experience. We scrutinized all questionnaires and dropped those with too many missing values. As a result, we obtained 277 valid responses. Among all respondents, 62.8 percent were male and 37.2 percent were female. In terms of age, 32.1 percent were between 20 and 25 years old.

We conducted two tests to examine the common method variance (CMV). First, we performed a Harman’s single-factor test (Podsakoff et al. 2003). The results show that the largest variance explained by individual factor is 13.923 percent. This indicates that none of the factors can explain the majority of the variance. Second, we modeled all items as the indicators of a factor representing the method effect (Malhotra et al. 2006). The results show a poor fitness. For example, the goodness of fit index (GFI) is 0.462 (<0.90), and the root mean square error of approximation (RMSEA) is 0.247 (>0.08). With both tests, we feel that CMV is not a significant problem in our research.

Data analysis and results

Following the two-step approach recommended by Anderson and Gerbing (1988), we first examined the measurement model to test reliability and validity. Then we examined the structural model to test research hypotheses and model fitness.

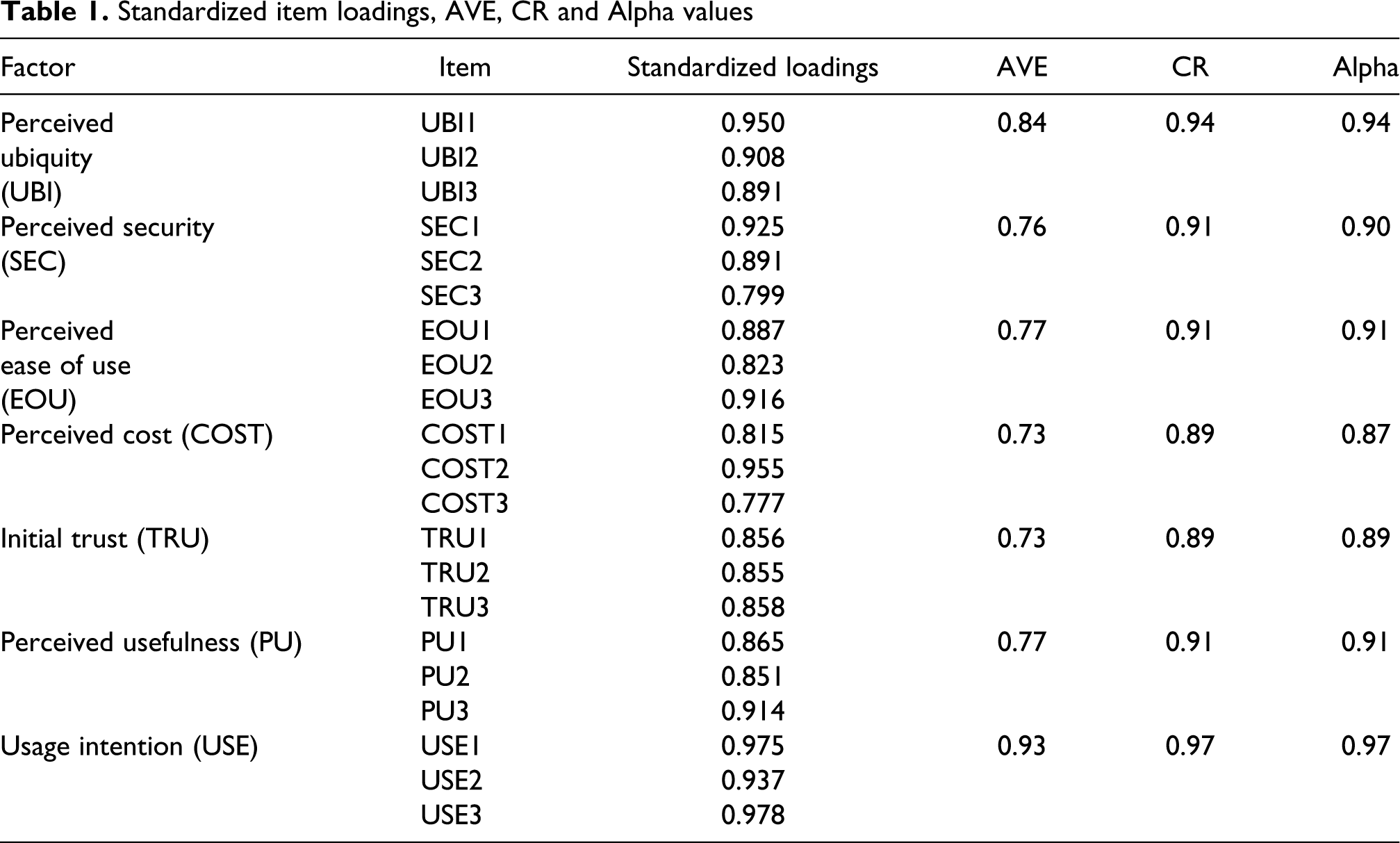

First, we conducted a confirmatory factor analysis (CFA) to examine the reliability and validity. Validity includes convergent validity and discriminant validity. Convergent validity measures whether items can effectively reflect their corresponding factor, whereas discriminant validity measures whether two factors are statistically different. Table 1 lists the standardized item loadings, average variance extracted (AVE), composite reliability (CR) and Cronbach Alpha values. As shown in the table, all item loadings are larger than 0.7 and T values indicate that they are significant at 0.001. All AVEs, CRs and Alpha values exceed 0.5, 0.7 and 0.7, respectively. Thus the scale has a good reliability and convergent validity (Bagozzi and Yi 1988, Gefen et al. 2000).

Standardized item loadings, AVE, CR and Alpha values

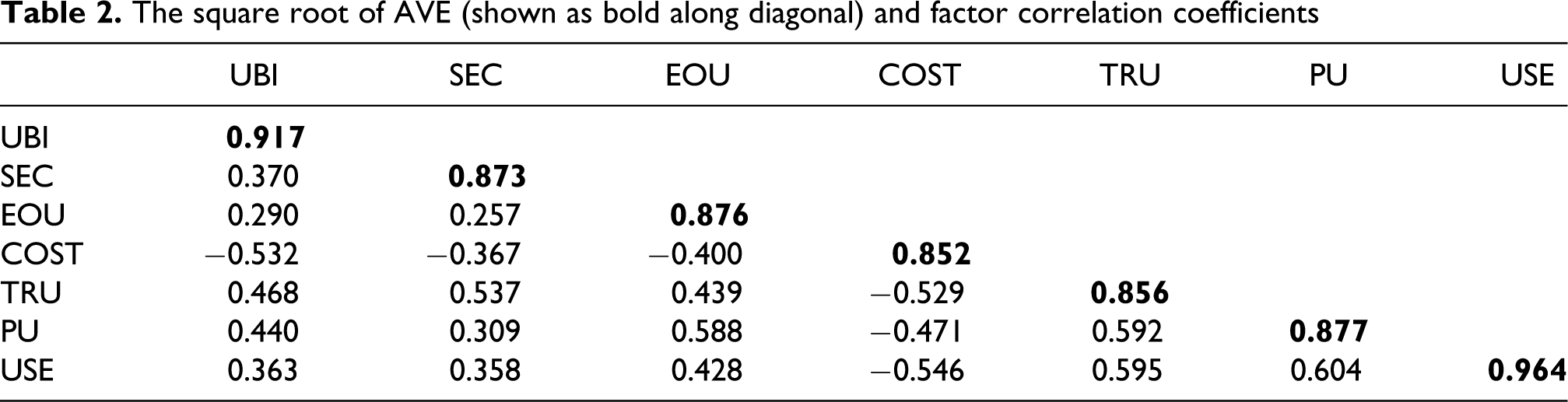

To examine the discriminant validity, we compared the square root of the AVE and factor correlation coefficients. As listed in Table 2, for each factor, the square root of AVE is significantly larger than its correlation coefficients with other factors. This shows that the correlation among an individual factor and its items is larger than the correlation among the factor and other factors. Thus the scale has a good discriminant validity (Fornell and Larcker 1981).

The square root of AVE (shown as bold along diagonal) and factor correlation coefficients

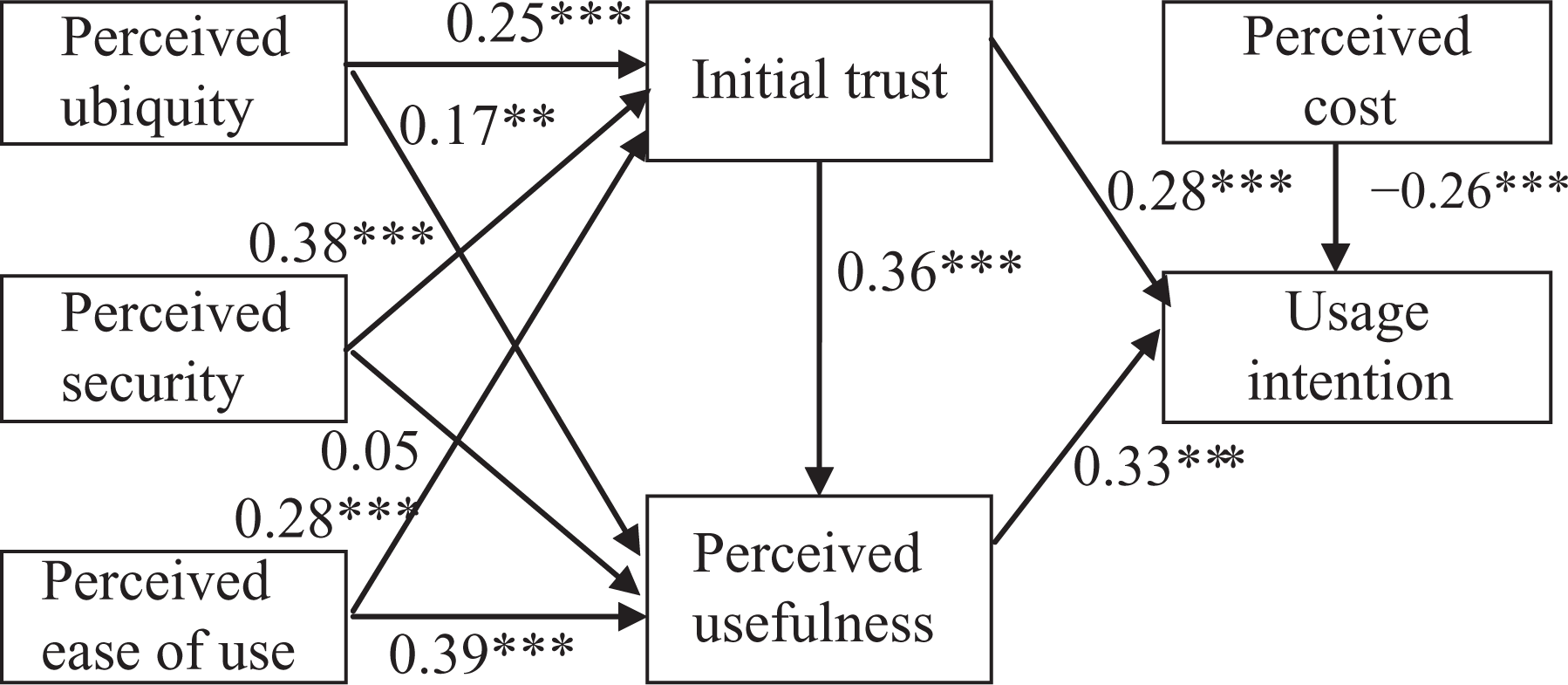

Second, we adopted SEM software LISREL 8.72 to estimate the structural model. Figure 2 presents the results. Table 3 lists the recommended and actual values of some fit indices. Except GFI, the actual values of other fit indices are better than the recommended values, showing a good fitness (Gefen et al. 2000). The explained variance of initial trust, perceived usefulness and usage intention is 44.9 percent, 50.9 percent and 47.9 percent, respectively.

Path coefficients and their significance Note: ** p < 0.01; *** p < 0.001

The recommended and actual values of fit indices

Note: chi2/df is the ratio between Chi-square and degrees of freedom, GFI is goodness of fit index, AGFI is the adjusted goodness of fit index, CFI is the comparative fit index, NFI is the normed fit index, NNFI is the non-normed fit index, RMSEA is the root mean square error of approximation.

We conducted a post-hoc analysis to examine the mediation effects of initial trust and perceived usefulness on usage intention. We added three direct paths from perceived ubiquity, perceived security and perceived ease of use to usage intention and re-estimated the model. The results indicate that none of the three paths is significant. In addition, the chi-square difference test showed an insignificant difference (Δχ2 (3) = 3.43, p = 0.33) between the original model and the new model. Thus both initial trust and perceived usefulness fully mediate the effects of perceived ubiquity, perceived security, and perceived ease of use on usage intention (Baron and Kenny 1986).

Discussion

The results indicate that both perceived ease of use and perceived ubiquity have significant effects on initial trust and perceived usefulness. While perceived security significantly affects initial trust, it does not affect perceived usefulness. Initial trust affects perceived usefulness and both factors together with perceived cost predict usage intention.

Among the factors affecting initial trust, perceived security has a relatively larger effect (γ = 0.38). This result is consistent with previous findings (Mallat 2007, Kim et al. 2009), highlighting the significant role of perceived security in building users' trust in mobile payment. Compared to traditional e-commerce, mobile commerce built on wireless networks is more vulnerable to hacker attack and information interception. In addition, viruses and Trojan horses may also exist in mobile terminals. These security problems increase users' perceived risk of using mobile payment. They may worry about the leakage of payment passwords and loss of money. Mobile service providers can use advanced encryption and certification such as secure socket layer (SSL) to improve users' perceived security and mitigate their perceived risk. The effect of perceived ease of use on initial trust is also significant. An easy-to-use mobile payment system demonstrates that service providers have spent effort and resources on providing quality services. This will build user trust. We also found the significant effect of perceived ubiquity on initial trust. Users expect to conduct payment at anytime from anywhere. If mobile payment service is always unavailable or has a slow response, users cannot build their trust. Thus mobile service providers need to optimize their back-end systems such as databases and servers, and provide reliable and ubiquitous payment services to users.

Of the factors affecting perceived usefulness, perceived ease of use and initial trust have strong effects (γ = 0.39 and β = 0.36, respectively). Due to the constraints of mobile terminals such as inconvenient input and small screens, it is necessary to provide an easy-to-use interface to users (Lee and Benbasat 2004, Li and Yeh 2010). Without previous experience, initial users are very concerned with the ease of use of mobile payment. When users have more usage experience, the effect of perceived ease of use may gradually diminish (Venkatesh and Davis 2000). In addition, some mobile payment services entail users to download and configure the software based on the type of their mobile terminals. This may mean a difficulty for mobile users. Thus mobile service providers need to simplify the operation process and improve users' perceived ease of use. The results also indicate that initial trust affects perceived usefulness. Trust ensures that users will acquire the expected utility in future (Gefen et al. 2003). If users do not trust mobile service providers, they may feel that mobile service providers lack necessary ability to provide quality services to them. They may also feel that mobile service providers will deceive them, or only care their own benefits. This leads to their suspicion of mobile payment utility. The effect of ubiquity on perceived usefulness is relatively lower, but still significant, suggesting that ubiquity also affects user evaluation of mobile payment utility. We did not find the direct effect of perceived security on perceived usefulness. However, perceived security has a significant effect on initial trust. This shows that initial trust mediates the effect of perceived security on perceived usefulness.

The results indicate that perceived usefulness, initial trust and perceived cost have significant effects on usage intention. Among them, perceived usefulness and initial trust act as enablers, whereas perceived cost acts as inhibitor. The results also show that initial trust and perceived usefulness fully mediate the effects of perceived ubiquity, perceived security and perceived ease of use on users' behavioral intention. This highlights the necessity to enhance users' trust and their perceived usefulness of mobile payment. The negative effect of perceived cost also deserves further attention from mobile service providers. Users need to bear communication and transaction fees when they use mobile payment. This means a high cost burden for many users. Thus mobile service providers need to lower the usage cost. For example, in the early stage, many service providers have used free or discount strategies to encourage user adoption of mobile payment. On the other hand, they also need to improve charge transparency and cannot charge users without their knowledge. Otherwise, users may give up using mobile payment. For example, Chinese government has issued a policy named “second confirmation” to protect consumers' interests. This policy demands that mobile service providers charge users only when they have confirmed their payment willingness twice.

Theoretical and managerial implications

From a theoretical perspective, this research identified the significant effect of initial trust on user adoption of mobile payment. Although initial trust has received considerable attention in the online commerce context such as online shopping (Gefen et al. 2008), it has seldom been examined in the mobile commerce context, especially in the context of mobile payment which involves great uncertainty and risk. Thus it is necessary to take initial trust into consideration when facilitating mobile payment usage. On the other hand, extant research has mainly used information technology adoption theories such as TAM and IDT to examine mobile payment user behavior. Factors such as perceived usefulness and compatibility have been identified to affect user adoption of mobile payment. We found that in addition to perceived usefulness, initial trust also has a significant effect on usage intention. This enriches extant findings and advances our understanding of mobile payment user behavior. The results indicate that perceived security, perceived ease of use and perceived ubiquity affect users' initial trust in mobile payment. These factors are mainly related to payment system characteristics. As noted earlier, there exist a variety of factors possibly affecting initial trust, such as trust propensity, reputation and institutional trust mechanisms. Future research can explore their effects on initial trust.

From a managerial perspective, our results imply that mobile service providers should not only deliver a positive utility to users, but also build users' initial trust in order to facilitate their adoption and usage of mobile payment. We found that perceived security has a strong effect on initial trust. Mobile service providers can take measures such as encryption, certification and third-party assurance mechanisms to enhance users' perceived security and alleviate their perceived risk. The results also show that perceived ease of use and perceived ubiquity significantly affect initial trust. Mobile service providers need to optimize the operation process and provide an easy-to-use interface to users. They can also adopt education and training to equip users with relevant knowledge, thus improving their perceived ease-of-use. Further, they should improve the reliability and response speed of payment systems and enable users to conduct ubiquitous payment.

Conclusion

Due to the high perceived risk and low switching costs, it is critical to building users' initial trust to facilitate their usage of mobile payment. Our results show that perceived security, perceived ease of use and perceived ubiquity significantly affect initial trust, which in turn determines perceived usefulness. Both initial trust and perceived usefulness affect usage intention. Thus, mobile service providers need to offer secure, easy-to-use and reliable payment services to users. Then they can build users' initial trust and promote their usage intention.

This research has some limitations. First, the explained variance of initial trust is about 50 percent. Thus there exist other factors possibly affecting initial trust, such as reputation and service quality. Future research can examine their effects on initial trust. Second, we collected data in China, where mobile commerce is developing rapidly but still in its infancy. Thus our results need to be generalized to other countries that had developed mobile commerce. Third, we conducted a cross-sectional study. However, user trust is dynamic. A longitudinal research may provide more insights on user trust development.

Footnotes

Acknowledgement

This work was partially supported by a grant from the National Natural Science Foundation of China (71001030), a grant from Zhijiang Social Science Young Scholar Plan (G94), and a grant from Hangzhou Soft Science Project (20110934M41).