Abstract

The COVID-19 epidemic has hastened the growth of Virtual Communities and is affecting virtually every part of work in the public and business sectors. Virtual communities, popular forums for communication and entertainment, increasingly affected the users’ decisions. Though many technology adoption models/theories are available, a distinctive model for decision-making in a virtual environment is scarce. This research developed the virtual communities’ decision model and empirically tested its performance. This study examined 16 well-established theories/models of information technology, social science, marketing, and behavioral finance and extracted nine constructs from 58 identified constructs considering theoretical cohesiveness along with the three-stage method proposed by Moore and Benbasat. A unified model for virtual communities’ decisions (VCDM) is developed and validated using the data collected from individual capital market investors in Bangladesh. The structural equation modeling technique is used to analyze the data. The upshot implies that VCDM performs adequately and explains the maximum variances in intention to decision and investment. VCDM also outperforms the majority of the related theoretical models. The acceptance levels of fit indices and all significant relationships among different constructs are also empirically validated. The moderating effect of the virtual group use experience is also confirmed. Future research can use VCDM in marketing, behavioral finance, ecommerce, information systems and social science context. VCDM thus facilitates a beneficial tool for managers, service providers, and other users to assess the likelihood of effectiveness for decisions in a virtual environment.

Introduction

The COVID-19 epidemic has hastened the Virtual Communities’ Forum's growth, affecting virtually every part of public and corporate sector activities. One of the strategies to combat the global coronavirus is to exercise social distancing, and the internet forum facilitates this process (Bacon et al., 2020). The COVID-19 epidemic has drastically altered our way of life, work, and contact. People are increasingly joining a virtual forum to express their feelings, learn and listen from one another, and make various decisions even though they are not physically there (Association of Corporate Counsel, 2020). Businesses worldwide, particularly in low- and middle-income nations, are forced to make difficult decisions to deal with the crisis (Nextbillion, 2020). People can use a virtual forum to discuss knowledge and ideas that help them become more assertive and wiser (Durso, 2020).

The rapid evolution of virtual community platforms, popular forums for communication and entertainment, is accelerated by the emergence of online social networks (OSNs), and users’ word-of-mouth (WOM) behaviors are increasingly influencing the decision (Chih et al., 2017).

Users of OSNs make virtual forums an increasingly significant part of their daily activities and decision-making process, where consumers utilize the recommendation and brand page information to define their purchasing habits (Humphries, 2019). Many people crossing geographical and political boundaries interact in a virtual community that is developed potentially based on online social networks platform. Ridings et al. (2002, p. 273) propose an inclusive definition of the word "virtual community" that includes the characteristics of the above definition also: "groups of people with common interests and practices that communicate regularly and for some duration in an organized way over the Internet through a common location or mechanism." Members of the virtual communities can share their interests, develop fantasies, conduct transactions and create a relationship in the virtual environment. The Internet is the precondition to developing these communities and fulfilling users’ communication, entertainment, and information needs (Lin, 2006). This platform provides unexpected facilities to share and interact information among its members (Bagozzi and Dholakia, 2002; Butler, 2001). It plays a vibrant role in economic, social, and political interactions (Park et al., 2013). When individuals perceive the community environment as friendlier, they will perceive the benefits because of usefulness and easiness (Galston, 1999; Kim, 2000). It is said that the members of virtual communities use the system and reside in it, and academics and practitioners have explored online social media in recent years (Olanrewaju et al., 2020).

From a behavioral finance perspective, most studies recognized the online forum as critical because investors and the securities market are significantly influenced by the information disseminated and circulated on this forum (O'Connor, 2013). Participants in investment communities are continuing to grow every day. Some virtual investment communities (e.g., Yahoo! Finance, MSN Money, and AOL Money & Finance) attracted over 60 million unique visitors each month (April 2019, Nielsen). As new technologies have entered the market, a financial debate has grown more common on social media (Greenfield, 2014). The emergence of message boards and virtual investment communities are considered a blessing for investors (Park et al., 2013). Information on virtual communities (VCs) is more authentic than analysts (Bagnoli et al., 1999; Clarkson et al., 2006; Park et al., 2013). Moreover, Antweiller and Frank (2004) and Regnier (1999) explored that stock price movement is significantly affected by the information disseminated on online forums. Given the importance of social media to people and society, academics have become more interested in this area in recent years (Khang et al., 2012). In addition, from a marketing perspective, blogs, online brand communities (OBC), and wikis are emerged due to web 2.0 technology that facilitates the dissemination of user-generated content. It was thought that communication would be initiated and controlled by the firms, but now customers are engaged in this process and create content on different sites (France et al., 2015; Kietzmann et al., 2011; Tiruwa et al., 2018). Social network-based online brand communities help marketers by providing two-way communications and frequently engaging their customers (Sashi, 2012; Thackeray et al., 2008; Tiruwa et al., 2018).

Some contemporary scholars have examined how different factors moderate the user intention to use online brand communities (Tiruwa et al., 2018), virtual community members relationships (Chih et al., 2017), investors homophiles in social media-based virtual communities (Gu et al., 2014), dissemination of investment information on virtual communities (O'Connor, 2013), and purchase behavior in a virtual world (Guo and Barnes, 2011).

Due to the significant emergence and involvement in a virtual platform, developing a model for decisions in a virtual environment is necessary. Moreover, some studies have used already established models, e.g., Lin (2006) applied TAM to understand the behavioral intention to participate in virtual communities, Lin (2007, 2008) used TAM and IS success model for antecedents identification of satisfaction in virtual communities participation and sustaining features of virtual communities respectively, Lin (2009) combine TAM with other constructs (e.g., cognitive absorption) in order to examine the cognitive factors affecting the virtual community usage intention, Wang et al. (2012) used TAM and other constructs(e.g., internet self-efficacy, community environment) in order to understand online community participation, Chang et al. (2016) integrate UTAUT with innovation diffusion theory to explore virtual shopping behavior, and other developed new models regarding the virtual people behavioral intention (e.g., Huang and Farn, 2009). However, only a few studies have addressed how the people in virtual communities will decide on their virtual activities, such as purchasing financial and physical products.

Due to limited proficiency among the existing model or theories and the scarcity of appropriate models to explore the decision in virtual communities, it is imperative to build a model for virtual communities’ decisions, reviewing existing IS/ IT, marketing, and behavioral finance theories/models and concepts (Dwivedi et al., 2017; Rana et al., 2016). Our research objective is to develop a virtual community's decision model and test its performance while carefully considering the investors’ investment context because several studies (e.g., Tiruwa et al., 2018; Chang et al., 2016; Lin, 2009 and Chih et al., 2017) have highlighted the theoretical fragmentation or lack of theoretical progress and rigor in the virtual communities decision research. Based on the objective, the study will address the question:

Does the virtual communities’ decision model appropriately explain the virtual decision aspect?

The study tries to achieve this by scrutinizing the eleven adoption models/theories and five theories from behavioral finance, social science, and marketing. It is grounded on this, framing the VCDM and checking its performance. These theories/models are mainly selected based on their theoretical cohesiveness and frequent use in inspecting virtual community decision contexts. This paper is designed in the following way: Section two presents a review of existing user acceptance models and behavioral finance and marketing theories. Section three discusses the justification regarding the inclusion of different construct of this model. After that, the research method follows a discussion on the proposed research model and developed hypotheses for VCDM. Afterward, the empirical findings section is followed by a discussion. Finally, the paper concludes after mentioning the limitation, future research, and implications to knowledge and policymakers.

Theoretical foundation

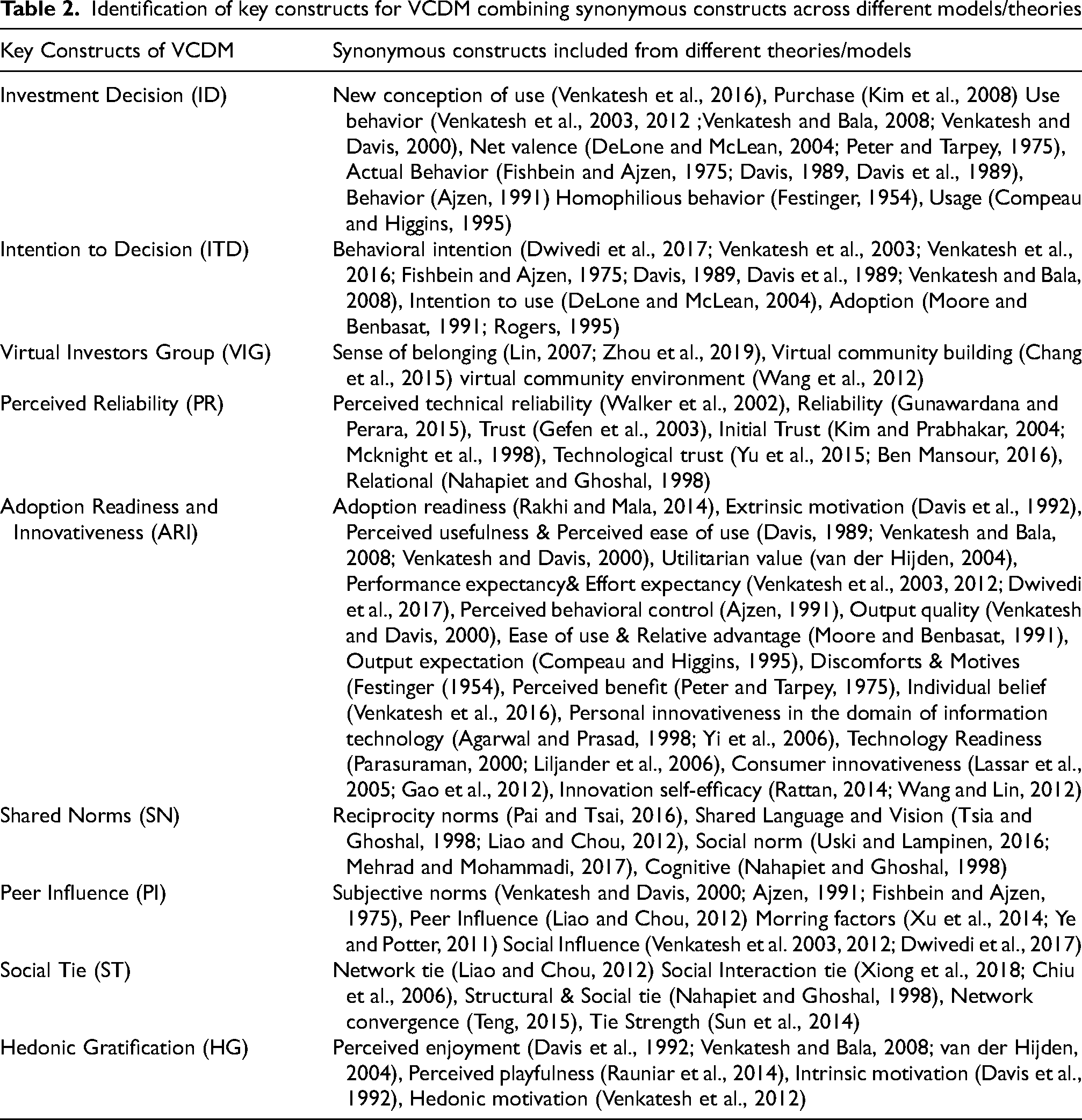

Information systems research tried to determine why and how individuals accept new information technologies (Dwivedi et al., 2017). Several research streams have evolved to investigate the IS/IT adoption in a wide area (Venkatesh et al., 2003). For example, Venkatesh et al. (2003), Compeau and Higgins (1995), and Davis et al. (1989) used intention or usage as the dependent variable on individual acceptance of technology, and Delone and McLean (1992, 2003) used net benefit or satisfaction to measure the success of an IS at the enterprise level (Leonard- Barton and Deschamps, 1988) as well as (Goodhue, 1995; Goodhue and Thompson, 1995) measure task–technology fit. Moreover, Venkatesh et al. (2016) developed a multilevel framework and suggested that attributes be modified and used in different contexts. Although most of the streams, as mentioned earlier, significantly contribute to our understanding of IT user acceptability, the suggested theoretical model includes investment decision as a dependent variable, significantly expanding the literature. The virtual community's decision model (VCDM) was created in response to the need for a decision model in a virtual setting. Table 1 presents core and endogenous components related to 16 theories/models of IT adoption, marketing, social science, and behavioral finance. The table also exhibits the corresponding models’ context, outcomes, and definitions of core constructs. Around 58 constructs are identified from these existing theories and models. This study aimed to review each theory or model and identify persuasive constructs (Table 2) to formulate the VCDM and empirically test its performance.

Reviews of existing users technology acceptance frameworks, marketing, social science and behavioral finance theories

Reviews of existing users technology acceptance frameworks, marketing, social science and behavioral finance theories

Identification of key constructs for VCDM combining synonymous constructs across different models/theories

Since introducing information systems into society, users’ participation in virtual communities, also known as e-world, has received significant attention. Various theories on technology adoption proposed a set of variables to predict technology adoption, and another added additional variables to describe continued use (Kim and Crowston, 2011; Setterstrom et al., 2013). However, models are scarce to describe people's decision constructs in the virtual world. Therefore, the study used a theoretical unification approach (Venkatesh et al., 2003) to develop this model (Fig. 1). This allows for both current work and empirical support that can improve our understanding of virtual community decision-making. However, more than merging existing theories are required to expand our knowledge and introduce some novelty (Shaw et al., 2018). Hence, we intended to review competing theories to identify persuasive constructs of VCDM and its impact on the virtual communities. In addition, we incorporate behavioral finance and virtual community-related constructs that are missing in existing technology acceptance models. The selection of these models is based mainly on their frequent use in various virtual communities’ contexts. Researchers are confronted with the option to choose and use the specific model with some additional variables because the existing original model/ theories do not adequately specify the constructs for the virtual community's decision (Venkatesh et al., 2003; Dwevdi et al., 2017). Besides, only a few studies have attempted to explore people's behavior in the virtual world. However, these studies have used the existing adoption model with additional constructs.

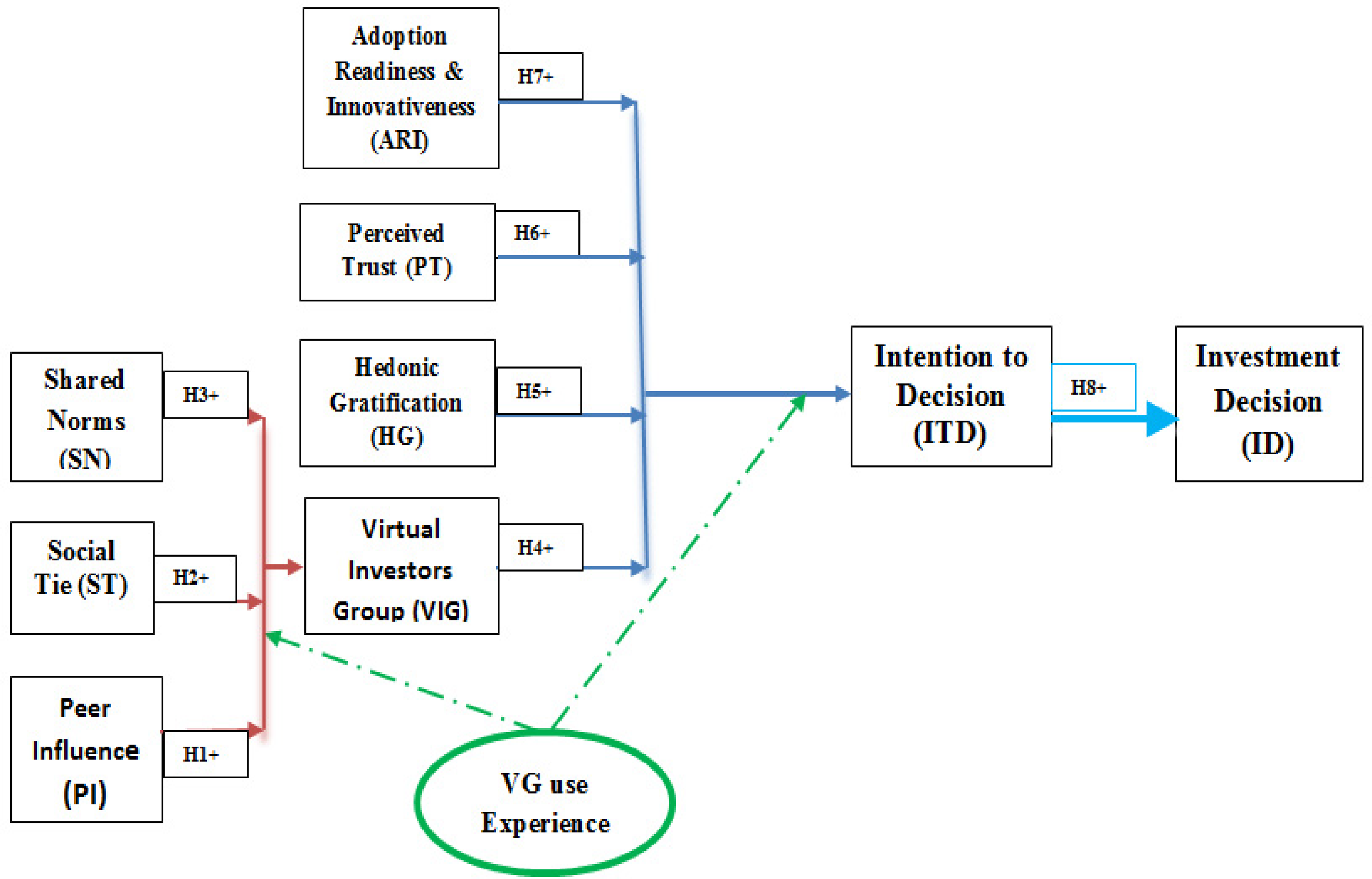

Virtual communities decision model.

This approach differentiates the current research from previous studies, including the TAM (Davis et al., 1989), UTAUT (Venkatesh et al., 2003), UTAUT2 (Venkatesh et al., 2012), and the Multilevel Framework of Technology Acceptance and Use (Venkatesh et al., 2016). This approach makes this model parsimony and focuses on the decision in a virtual environment and the presence of innovative intuitions, which explain the impact of innovative constructs on people's decisions in the virtual community.

In order to develop a model for decision-making in virtual communities, we reviewed 11 technology acceptance and five behavioral finance, marketing, and social science model/ theories in section 2 and Table 1 based on theoretical cohesiveness and frequent use in inspecting virtual community decision contexts. Venkatesh et al. (2003) previously developed the Unified Theory of Acceptance and Use of Technology (UTAUT) after examining eight known theories/models and proposing that four constructs have a crucial role in determining user acceptance and user behavior. Because of the combination of eight theories, UTAUT is regarded as a complete and valuable theory for predicting IS/IT adoption (Qingfei et al., 2008). Venkatesh et al. (2016) later proposed a multilayered framework for technology usage and acceptability due to the wide application of UTAUT. They didnot specify definite constructs; instead, they mentioned some domains, and researchers could use them in different IT/IS adoption contexts. Due to the vast area of IT/IS, different models are also required in different contexts to understand the acceptance and use of users’ perceptions. After reviewing nine theories/models used in technology adoption research, Dwivedi et al. (2017) introduced a unified model for electronic government adoption mainly based on the UTAUT model. They tested the different constructs of those models empirically and extracted five core constructs to develop the model for electronic government adoption. Due to the emergence of web 2.0 technologies, IS/IT has got another attention, and online social media are becoming an inseparable part of today's life. People participate in this virtual world and make decisions such as purchasing their daily necessary physical and financial products. Under these circumstances, it is necessary to develop a model to understand the decision-making antecedents of virtual people, especially in the capital market. To develop this model, numerous constructs from existing models/theories are recognized that influence technology adoption. Some constructs/variables across different models/theories are more or less similar theoretically. Those variables can be grouped into a single construct for consistent testing. This allows the generation of key constructs. We followed the three-stage method proposed by Moore and Benbasat (1991) to develop the constructs for VCDM: The researchers reviewed 16 models/theories and identified the core and endogenous constructs associated with them. The researchers used their judgment to pool the constructs from the first stage based on the theoretical cohesiveness and differences among the constructs. The field test was conducted to check pooled items. Shaw et al. (2018) developed constructs for the technology integration model (TIM), considering only theoretical similarities of different constructs across different models to predict technology use. Succeeding the above techniques, we developed nine constructs for this model by drawing the manifest variables from different constructs used in different models/ theories to predict the virtual people's investment decisions (Table 2).

In order to understand the participation behavior in a virtual group, we used the social capital theory as the foundation for the development of different constructs because this theory explains social behavior. Social ties develop a sound affiliation and subsequently direct people to involve in intense interpersonal actions (Nahapiet & Ghoshal, 1998). Social ties among social groups might help find a better job, innovate new products and services and give information and knowledge regarding participation in a social circle (Granovetter, 1973; Burt, 2001; Lin, 1999). Shared norms imply some rules, such as "one of us" and "out of the circle" (Graeff and Svendsen, 2013). A dense relationship network facilitates interpersonal trust essential for economic cooperation and benefits the entire group (Coleman, 1990). Trust is an influential turn for economic prosperity. When there is high interpersonal trust, people spend less money defending themselves from being deceived in economic transactions (Whiteley, 2000; Sankowska, 2015). Subjective norms are influenced by a peer group that is a source of interpersonal behavior (Ma et al., 2002). Table 2 also shows the different constructs that are combined in peer influence. Deriving from the enhanced performance of the social tie, peer influence, shared norm, and perceived trust, we recommended social ties, shared norms, peer influence as a direct determinant of virtual investors groups, and perceived trust as a direct determinant of intention to decisions in virtual communities.

The virtual investor group is important in a virtual community to the extent that no involvement or participation would be forthcoming from users if it were lacking in them (Roberts, 1998). From a social perspective, studies on virtual communities emphasize supportive social behavior (e.g., shared norms, peer influence) and social relations (e.g., social ties) that encourage forming a virtual group (Lin, 2007). Moreover, Roberts (1998) argued that subjects with higher participation in the virtual group put more time and effort into their virtual communities. Therefore, strong participation in a virtual group (equivalent to a perceived sense of belonging by Lin, 2007) is expected to lead to a strong intention to be further involved in the virtual community. Hence, in this model, the virtual investor's group is a mediator between social ties, shared norms, peer influence, and intention to make decisions. When the user participates in a virtual group, they will form an intention to decide to purchase/sell the financial or physical goods (Kim et al., 2008).

In information systems and social networking research, hedonic pleasure (conceptualized as perceived enjoyment/reported playfulness) has been established as a direct predictor of technology adoption and use (e.g., Venkatesh et al., 2012; van der Heijden, 2004; Turel and Serenko, 2012; Thong et al., 2006; Chen et al., 2017; Rauniar et al., 2014; Ernst, 2015). As a result, we included hedonic gratification as a predictor of decision intention in online communities. Potential users should have a certain level of adoption readiness and innovativeness with a view to the intention to use/decide on any new IS/IT. Considering the features of virtual communities, this study reviewed some literature on factors affecting the users’ readiness and innovativeness for new technology adoption. Examining the literature of Davis (1989), Venkatesh et al. (2003), and Rakhi and Mala (2014), it is found that novel constructs, namely adoption readiness and innovativeness, which encompass the utilitarian and personal characteristics, can be derived from perceived usefulness, perceived use of use and personal innovativeness in IT. Davis (1989) presented the perceived usefulness and perceived ease of use constructs to predict new technology adoption intention in TAM, where perceived usefulness reflects utilitarian value (van der Heijden, 2004; Moqbel, 2012; Ernst, 2015). Agarwal and Prasad (1998) introduced personal innovativeness in IT (PIIT), which is restricted to the area of technology and may be described as "an individual's readiness to try out any new information technology." A substantial number of studies discovered a strong degree of correlation between various UTAUT factors (e.g., performance expectancy equivalent to perceived usefulness, effort expectancy equivalent to perceived ease of use, and perceived facilitating condition) in different technology acceptance around the world (Rakhi and Mala, 2014). Sharma et al. (2009) found a strong relationship between perceived usefulness and perceived ease of use when determining the influence of common method variation using TAM. A meta-analysis of 26 significant publications utilizing TAM by Qingxiong Ma and Liu (2004) revealed a significant association between perceived usefulness and perceived ease of use. In research on internet adoption as a distribution channel, Izquierdo-Yusta and Calderon-Monge (2011) discovered a high relationship between perceived usefulness and perceived ease of use. In a Chinese mobile instant messaging study, Jiang and Deng (2011) discovered a positive association between perceived usefulness and perceived ease of use. In research on m-banking, Wessels and Drennan (2010) showed a significant association between perceived usefulness and perceived ease of use. Giovanis et al. (2018) and Fagan et al. (2012) discovered that personal innovativeness in IT is a major predictor of engagement in virtual reality. However, Rakhi and Mala (2014) found a positive relationship between adoption readiness and personal innovativeness in mobile payment service adoption studies.

Even though various scholars proposed and investigated directional associations between perceived usefulness, perceived ease of use, and personal innovativeness, these constructs remain the most frequently used and validated constructs in influencing the usage intention of novel technologies. Besides, most studies have pointed out a strong association among these constructs though they proposed these relationships in different contexts. Consequently, the existing research leads us to believe that these components are not genuinely distinct constructs influencing one another but rather aspects of a single construct called "ARI" in this study. As a result, this study offers "ARI" as a second-order construct containing six manifest items derived from previous studies, which would capture the utilitarian and personal qualities of users’ intention to make decisions in VCDM. Original TAM, including TRA (Davis, 1989), indicates that the intention to achieve a specific action is a direct cause of actual behavior since individuals have a general propensity to behave as they anticipate to do within the current time and context (Moon and Kim, 2001). Therefore, this model used intention to the decision (considering different constructs of previous models) as a mediator between investment decisions and other constructs. Most models or theories showed the use of behavior or usage or net valence as the outcome variable. In their study, Kim et al. (2008) showed decision to purchase as a dependent variable. Finally, reviewing the final dependent variables of a different model, this model proposed a new variable called investment decision as a final dependent variable, which suggested the forecasting investment decision of people in virtual communities.

Moreover, although VC has become increasingly popular, not all investors are equally experienced with them. We anticipate that investors’ experience with virtual groups will moderate the degree of their decision-making and engagement in VCs. Investors with less (vs. greater) experience with VCs are more inclined to participate and make decisions in virtual communities in various ways.

Research model and development of hypothesis for VCDM

Peer influence (pi)  virtual investors group (VIG)

virtual investors group (VIG)

Peer influence can be defined as an apparent signal where investors’ decisions are influenced by peers’ actions (Garg et al., 2011). PI affects one person's decision to another by providing motivation during learning and accepting a new technology (Benbunan-Fich, 2001; Eastman and Swift, 2001). Virtual groups such as Blogs (Jackson et al., 2007) and message boards (Bickart and Schindler, 2001) can influence consumers’ intention to purchase more effectively than direct marketing channels. Cheung et al. (2012) found that argument quality, peer influence, and source are critical antecedents for assessing decision credibility in consumer review websites. Ma (2013) explored that peer reviews successfully fight against biased reviews on online reviews. Kapoor et al. (2018) identify the consumer's interest and peer influence guides the users to pick the best value product or services. Garg et al. (2011) explored the influence of peers in the diffusion of new-fangled information on social network sites. Liao and Chou (2012) defined virtual communities as cyberspace and explored that peers highly influence knowledge adoption through virtual communities. Moreover, individuals are inclined to share more information in virtual groups when they are influenced extensively by their peers (Bock et al., 2005; Liao and Chou, 2012).In line with these arguments, we postulate the following hypothesis

Social tie (st) virtual investors group (VIG)

Social Tie can be defined as a neutral association among members in a social network where they are connected with each other's (Chiu et al., 2006). Furthermore, virtual community members engage with one another through online interactions. The social interaction bond is the foundation for establishing relational and cognitive elements of social capital (Chiu et al., 2006). Strong ties proceed to local cohesiveness among members and develop social networks, whereas weak ties create opportunities for individuals to integrate into communities (Granovetter, 1973). Most of the time, members of virtual communities exchange and decide without meeting personally. A stronger association motivates the users to maintain the relationship and communication extensively with others through virtual groups, which leads to the intention to use social networking sites (He et al., 2009; Levin and Cross, 2004). Strong relationships actively enhance information flow more than weak links (Brown and Reingen, 1987), and the strength of social ties in a virtual community is a significant element in the use of social networking sites (SNSs) (Tsai and Ghoshal, 1998; Wasko and Faraj, 2005). This is also consistent with Hsiao and Chiou (2012), Teng (2015), and Xiong et al. (2018), who reveal that social ties encourage the formation of virtual communities (VC).

Shared norms (sn) virtual investors group (VIG)

Shared norms describe the degree of agreement in the social system and commonality across internet users (Coleman, 1990). Participants of Facebook and Lastfm, had to adapt their behavior to comply with the shared norms of that platforms (Uski and Lampinen, 2016). Shared norms significantly influence mobile banking uptake research (Aboelmaged and Gebba, 2013; Chitungo and Munongo, 2013). McLaughlin and Vitak (2012) explored different close relationships when the norms are violated on Facebook. People with strong norms can contribute to an online group if the group provides members with additional chances to trade resources (Pai and Tsai, 2016). Though the norm is primarily invisible, it has immense power to control human behavior (Ivaturi and Chua, 2018). Kapoor et al. (2018) review 132 papers on social media research and find that SNSs motivate employees about their shared language and trust in a workspace. A considerable number of studies (e.g., Chang and Chuang, 2011; Chiu et al., 2006; Schumann et al. (2014) assert that shared norms have constructive impacts on members "information-sharing" behaviour in a virtual setting. Pai and Tsai (2016) discovered the virtual community's moderating function in facilitating the effect of reciprocity norms on the intention to use virtual networking platforms.

Furthermore, shared norms impact group performance (Mayo, 2003). As a result, shared norms produce propositional attitudes that favorably impact investors’ intention to utilize virtual communities in decision-making and mediate the link between investor intentions to use virtual communities in decision-making. These lead to propose the following hypothesis

Virtual investors’ group (VIG) intention to decision (ITD)

An online community offers a platform that can foster information, share knowledge, and support users in performing their necessary activities (Bart et al., 2005). An investors’ group or page offers more knowledge about the stock market. By collecting more valuable information about the stock market, VIG becomes a more helpful platform for investors. A virtual group provides an environment that accelerates communication and enables investors to understand other investors’ preferences. Because such platforms exist, investors no longer have to wait for sluggish or otherwise unequal responses from other systems because they can engage with other investors and gain a better knowledge of the stock market. The virtual community positively influences product familiarity, which mediates purchase intention (Chang et al., 2015; Tiruwa et al., 2018). Moreover, the Community environment positively encourages the online community participant to actual use through perceived usefulness and perceived ease of use (Wang et al., 2012). Since investors get information and other investors’ opinions regarding the market through the virtual group, that will encourage them to decide on investment. Therefore, this study presents the following hypothesis

Hedonic gratification (hg) intention to decision (ITD)

Hedonic gratification is associated with the fulfillment of hedonic anticipation (Hirschman and Holbrook, 1982). Virtual community users are likely to find the decision more effective if they enjoy it. Recent research has focused on perceived playfulness/perceived enjoyment, which captures hedonic gratification as a predictor of intention to use. Hedonic gratification is frequently regarded as a primary/strong predictor of intention to use online social networking sites in hedonic information technologies, such as online social networks(Ernst et al., 2013; Moqbel, 2012; Pillai and Mukherjee, 2011; Sledgianowski and Kulviwat, 2009; Rauniar et al., 2014). In addition, Gan (2017) suggests that hedonic gratification strongly determines WeChat liking behavior. By examining the empirical study and clearly understanding the importance of hedonic gratification in the virtual environment, the authors can infer that hedonic gratification can be a strong antecedent in virtual users’ intuition to decisions. Considering the empirical evidence of previous studies in online social networks, we propose that hedonic gratification is a strong determinant of intention to make decisions in VCDM. Therefore, we hypothesize that.

Perceived trust (pt) intention to decision (ITD)

Trust is the preparedness to rely on others, making oneself susceptible to another person (Currall and Judge, 1995; Mayer et al., 1995). In technology, trust is defined as beliefs about the performance of technology and a person's readiness to depend on it (Thatcher et al., 2007). In online social networking research, some studies explored trust as a primary/significant determinant of intention to use online social media (Rauniar et al., 2014; Lorenzo-Romero et al., 2011; Alarcon-del-Amo et al., 2012). In online communities, users create their profiles and share information in communities. When users feel their privacy is protected, they will trust the site and be interested in making decisions for any purchase. Perceived trust and intellectual capital transfer are crucial antecedents of information exchange in virtual communities (Inkpen and Tsang, 2005; Nahapiet and Ghoshal, 1998). Individuals’ confidence level in others may motivate them to participate in virtual community initiatives (Chiu et al., 2006). Furthermore, Ridings et al. (2002) highlighted trust as a critical component in virtual communities because the lack of effective norms increases reliance on others and aids in socially acceptable behavior. The following hypothesis is claimed based on prior literature

Adoption readiness and innovativeness (ARI) intention to decision (ITD)

In this study, ARI is defined as a user's belief that he or she is ready and inventive to accept new technology. According to Rakhi and Mala (2014), perceived usefulness encapsulating utilitarian value, ease of use, and perceived facilitating condition are aspects of adoption readiness that influence the relationship between these sub-constructs and the desire to use mobile payments. Other researchers back their findings, and they investigated a positive relationship between usefulness and ease of use as rated by respondents in Brazil, Kuwait, India, and Hong Kong (Koenig-Lewis et al., 2010; Laukkanen and Kiviniemi, 2010; Riquelme and Rios, 2010; Venkatesh et al., 2012). Rakhi and Mala (2014) investigated adoption readiness as a distinct construct and described adoption as an embryonic multi-dimensional construct evidenced by four sub-constructs. They asserted the four constructs as theoretically relevant and meaningful. They also explored personal innovativeness significantly and positively correlated with adoption readiness in adopting mobile banking services. Considering the utilitarian and individual characteristics of users and their non-compensatory rule of decision-making in a virtual world, we also infer that combined constructs, namely adoption readiness and innovativeness (ARI), will be a strong positive determinant of intention to make decisions in a virtual community

Intention to decision (ITD) investment decision (id)

Several well-recognized IS/IT and social psychology theories recommended that behavioral intent is a significant causal forecaster of behavior, and it mediates the various external constructs (e.g., individual features, system features, etc.) and beliefs on actual behavior (decision) (Davis et al., 1989). Considering the different technological and cognitive models (e.g., TAM (Davis, 1989); TPB (Ajzen, 1991); TRA (Fishbein and Ajzen, 1975) and Valence framework (Peter and Tarpey, 1975)), many IS/IT researchers have examined that participants intent to partake in online dealings is an essential forecaster of participants actual involvement in dealings (Pavlou and Fygenson, 2006). This relationship is also supported by other IS/IT academics (Al-Maghrabi and Dennis, 2011; Venkatesh et al., 2012). Moreover, Kim et al. (2009) developed an extended valence framework based on TRA and empirically validated that individuals’ Intention to use leads to purchase decisions. This study developed VCDM for making a decision in e-World. Considering the previous studies on the relationship between Intention–behavior, we believe that the Intention to make decisions from communities directly predicts actual user decisions, particularly investment decisions. Therefore the following hypothesis is proposed.

Moderating role of virtual group use experience

Previous research (e.g., Kim and Malhotra, 2005; Venkatesh et al., 2003) operationalized experiences that echoed a chance to use specific technology and were often viewed as the passage of time from users’ initial usage of technology. UTAUT's approach emphasizes the crucial importance of human variables (such as age, gender, and experience) as drivers of usage intentions or moderators affecting behavioral intention (Venkatesh et al., 2012; Slade et al., 2013). Some studies (e.g., Meuter et al., 2005; McKechnie et al., 2006; Heidenreich and Handrich, 2015; Blut et al., 2016) use the experience as an antecedent of TAM's salient beliefs. However, the influence is either restricted or poor. As a result, Blut et al. (2016) suggested considering demographics as moderator variables. Previous research, which has used UTAUT and its modifications to analyze adoption intentions, has hypothesized that the correlations between technological, social, and/or channel characteristics and behavioral intentions are mediated by experience (Slade et al., 2013). According to Venkatesh et al. (2003), improved experience may considerably impact potential customers’ adoption intention compared to performance expectancy, effort expectancy, and social influence.

On the other hand, experienced potential users seek more value in new technologies, and thus their belief in the technology's performance expectancy might have a more substantial effect on adoption intentions than those with limited experience (Tsourela and Roumeliotis, 2015). In other words, non-conscious and powerful reasons are more likely to affect investors’ participation and desire to make a decision. Experienced investors can protect themselves from homophile behavior and can make sound investment decisions (Gu et al., 2014). Furthermore, an affect-laden feature is more likely to encourage homophily in more experienced (rather than less experienced) investors. Online forums’ trolling and flaming activities may elicit strong emotions (Alonzo and Aiken, 2004; Johnson, 2009). These negative sentiments can stimulate an inexperienced investor to comply with these homophiles since the findings show that when people feel negative, they are likely to demonstrate homophiles (Gray et al., 2011). An experienced investor, on the other hand, is less likely to be swayed by these feelings. However, no study has looked at the moderating effects of virtual group usage experience on any model's first and second-order components in a virtual community environment. Therefore, considering the theoretical spat and sensible necessity, we expect that virtual group use experience will moderate the relationships for participation in virtual communities and the relationships for forming decision intention in VCDM. Hence we propose

Research method and data

Research setting and data collection

To test the proposed VCDM and interrelationship among different constructs, we selected capital market individual investors of Bangladesh as the research settings for some causes. OSNs are a new technology in Bangladesh, and the number of users has exploded (Shams, 2017). Therefore, the sampling frame for this study is the list of individual investors who constitute a significant portion of investors in Bangladesh. The research questionnaire was scattered into three parts (A, B, and C). Part A contains basic questions about the internet and OSNs use. Part C contains the demographic information, and all the questions regarding the various constructs of proposed VCDM were included in part B. 7-point Likert scale ranging from (1) "strongly disagree" to (7) "strongly agree" was used for all non-demographic items.

In order to ensure the content validity of the questionnaire's items, a pre-test of the questionnaires was performed. This test was conducted among friends and family members with a BO account. After developing the questionnaire and writing the pre-final version, three academics who were knowledgeable in instrument development in the field of technology adoption reviewed the questionnaire. Before the final survey, a pilot study was conducted among 20 known investors to get feedback. The final questionnaire was designed after incorporating pilot testing results and academic opinions. The study employed convenience and snowball sampling techniques as survey tools. Convenience sampling is "a type of nonprobability sampling, which involves the sample being drawn from that part of the population which is close to hand" (Ritchie et al., 2003). Besides, it is broadly used in IS (Information Systems) research due to cost-effectiveness (Eze et al., 2011).

Additionally, it is discovered from demographic statistics that our data accurately represent the bulk of demographic differences. Between January and March 2020, the research collected data. In order to ensure the participation rate, a personally administered face-to-face active recruitment strategy was followed. Besides, to take benefit of the "friends" characteristics of SNSs, an emerging snowballing technique was applied to find prospective participants and detect subsequent respondents. Previous IS research has used the snowball sampling strategy effectively (Lapointe and Rivard, 2005; Yin et al., 2013; Wells et al., 2011). The study circulated 550 questionnaires physically and got back 420. This reflects the response rate is around 76.9 percent. Twenty incomplete questionnaires were discarded from the analysis. In addition, by using the snowball technique, we collected 110 responses. As a result, 510 questionnaires were eventually submitted for further analysis. For statistical analysis, e.g., structural equation modeling (SEM), a sample size of 200, is considered fair and 300 as good (Kline, 2005). To test structural equation modeling (SEM), a sample size of 200 is also optimum (Hair et al., 1995). Roscoe (1975) recommended that in the case of multivariate studies such as multiple regression analysis, the sample size should be equal to or above ten times the number of items in the research. This study's sample size represents more than ten times the number of items (31) examined in the research and is adequate for structural equation modeling (Roscoe, 1975).

Scale development

Several latent construct measures from previous research were used to collect empirical data and operationalize the VCDM. Most of them were selected from earlier research because of their theoretical cohesion. The measures are modified to adjust virtual community users, particularly capital market investors in Bangladesh. Three items are drawn from Liao and Chou (2012) and Xu et al. (2014) to measure peer influence. Three items developed by Liao and Chou (2012) and Pai and Tsai (2016) were taken to measure the shared norms. The social tie was measured by three items validated by Liao and Chou (2012) and Xiong et al. (2018). Measurement scales for hedonic gratification were adopted from Davis et al. (1992) and van der Heijden (2004). Scales for perceived trust are adopted from Sun et al. (2014), Liao and Chou (2012) & Rauniar et al. (2014). Six items were drawn from Rauniar et al. (2014), van der Heijden (2004) & Yi et al. (2006) to measure the adaption readiness and innovativeness. Measures for Intention to Decision (ITD) were taken from Davis et al. (1989) and Venkatesh et al. (2012). Three measures scales were developed for the virtual investors’ group by partly adapting the scale of Chang et al. (2015). In the end, three partially modified items from Kim et al. (2008, 2009) are used to evaluate investment decisions. Appendix A contains the specifics on each of the constructs, items, and sources listed above.

Data analysis

To empirically check and confirm the VCDM and the relations among the theorized constructs, we used statistical analysis techniques, namely Structural Equation Modeling (SEM) (partial least squares (PLS)/variance-based method and AMOS/covariance method. To check the fitness of the research model, Smart PLS generates significantly fewer indices than CB-based AMOS (Garson, 2016). To overcome this limitation and check other requirements (e.g., CMB, Sobel test, and moderating effect), the study used SPSS 21.0 and Amos 20.0. First, the offline data were captured into Microsoft Excel, and an excel sheet was also generated from Google form data. Then the combined data file was imported to SmartPLS 3.0, SPSS, and AMOS graphics software for statistical analysis.

Empirical findings

Demographic characteristics of sample

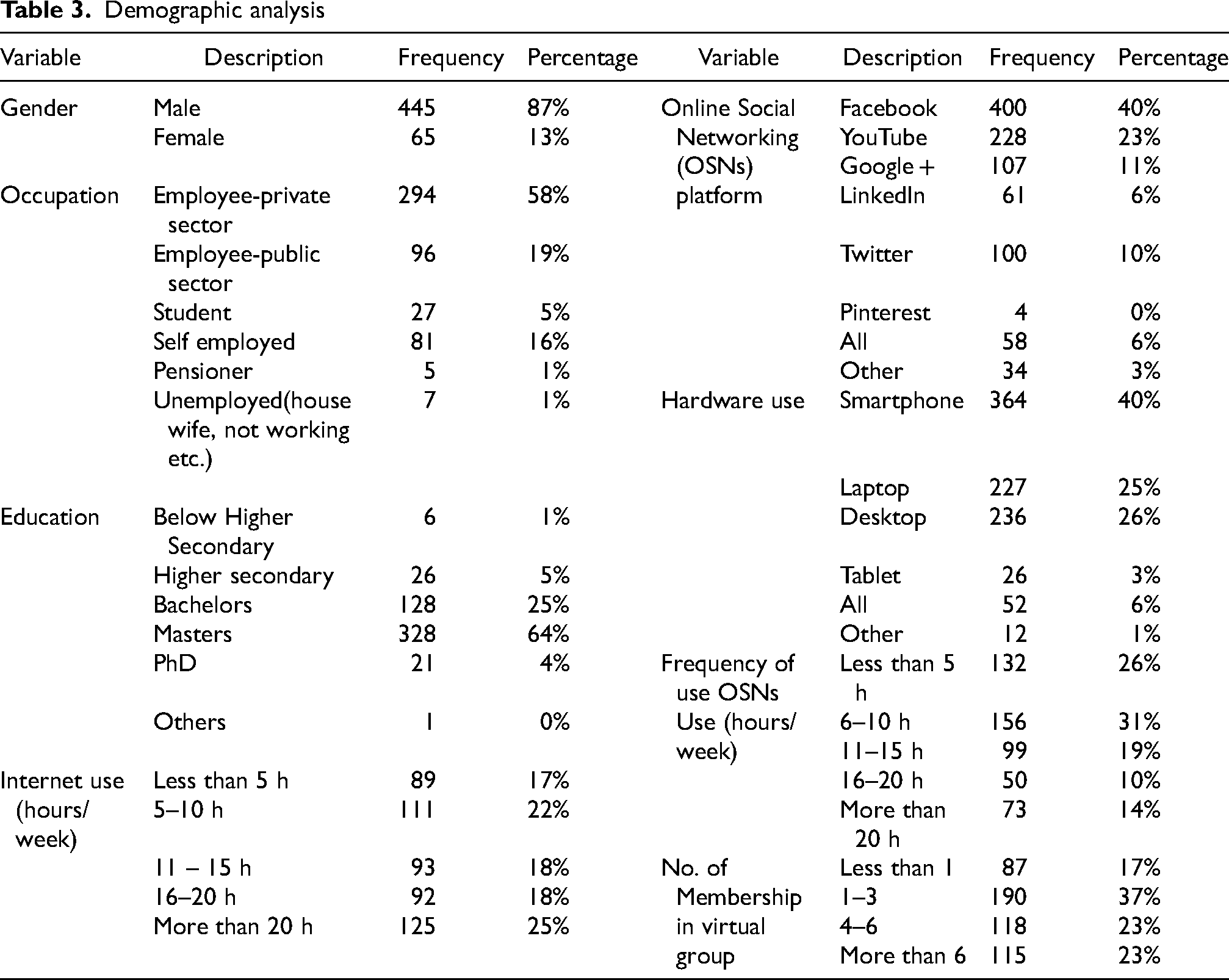

87% of males and 13% of females who participated in the study indicate that females are not so much engaged in capital market investment consistent with the beneficiary account (BO) holders data in Bangladesh (CDBL, 2019). The highest numbers of respondents (58%) are private-sector employees, 19% are government employees, and the remaining are students, self-employed, pensioners, etc. Most participants (64%) have attained master's degree education, indicating educated people are using virtual communities to share stock market information. In the case of virtual platforms and hardware use, each respondent can use one or more virtual platforms and hardware. Most respondents (40%) use Facebook, and (40%) use smartphones to make investment decisions in the capital market through virtual platforms in Bangladesh. Most respondents (54%) joined the Facebook group for less than or equal to three years for capital market investment.

On the other hand, 61% of respondents use the internet at least 11 h per week, and the bulk of the participants (57%) use virtual communities less than or equal to ten hours per week (Table 3). In data analysis, all the demographic factors were taken as control variables.

Demographic analysis

Demographic analysis

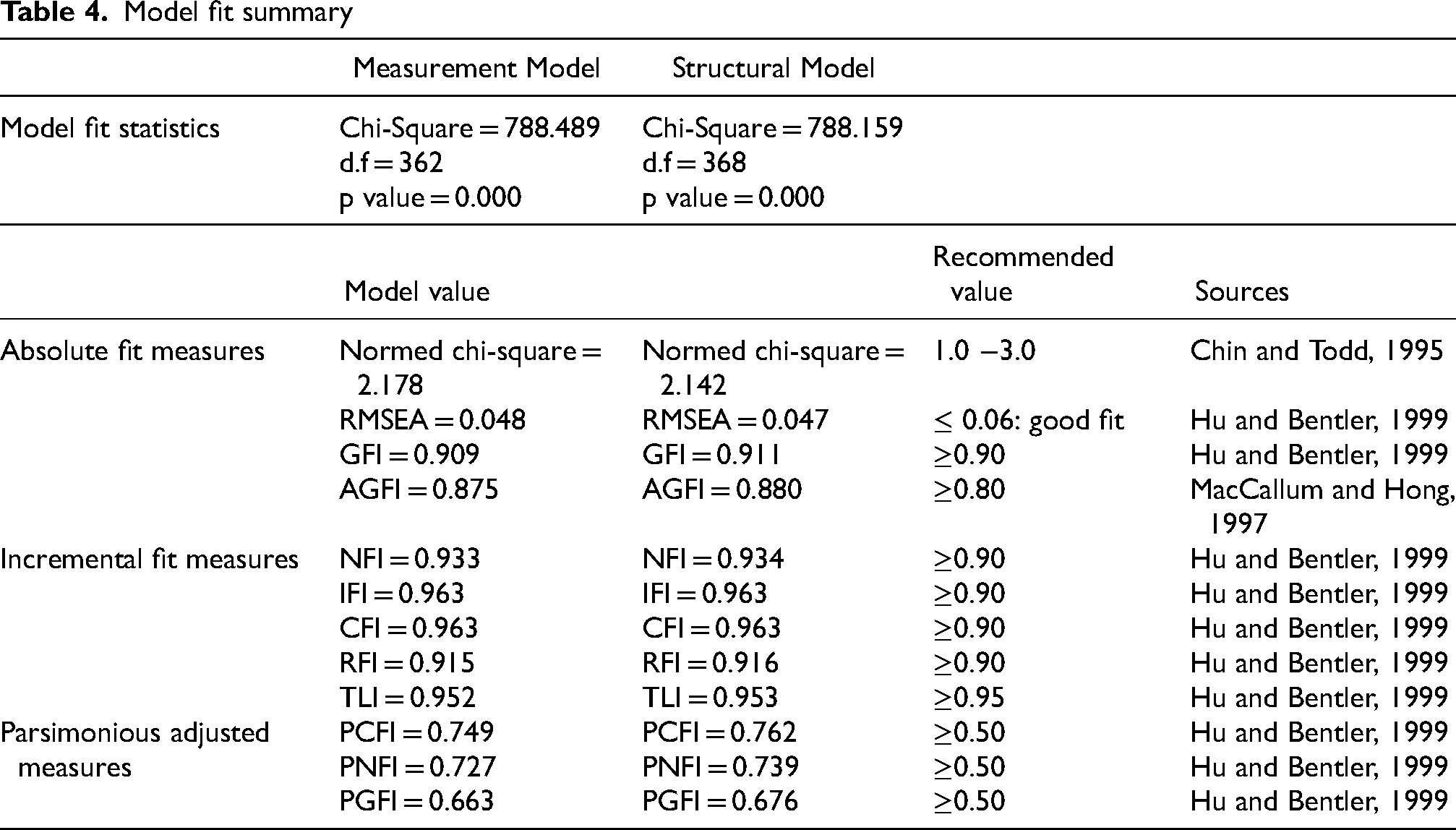

Intending to check the measurement and structural model fitness, we used AMOS 20.0 version estimation indices and followed the recommended classification of Hooper et al. (2008). They recommended and classified the goodness of fit indexes into three categories: absolute fit measures, incremental fit measures, and parsimonious adjusted measures. We used Schreiber's (2008) suggested measures to check the GFI (Goodness-of- Fit).

We used four indexes to test the absolute fit measure of our model. i. χ2 (Chi-Square) over df (degree of freedom) ii. RMSEA iii. GFI and iv. AGFI. The measurement model exhibits values 2.178, 0.048, 0.909, 0.875, and the structural model shows 2.142, 0.047, 0.911, 0.880 for χ2/df, RMSEA, GFI, and AGFI, respectively, which indicates the proposed model fits the absolute measures fitness criteria (see Table 4). In order to check the incremental fit measures, we used NFI (Normed Fit Index), CFI (Comparative Fit Index), IFI (Incremental Fit Index), RFI (Relative Fit Index), and TLI (Tucker-Lewis Index). Our model fit summary generated from AMOS shows the value NFI = 0.933, IFI = 0.963, CFI = 0.963, RFI = 0.915, TLI = 0.952, and NFI = 0.934, IFI = 0.963, CFI = 0.963, RFI = 0.916, TLI = 0.953 for measurement and structural model respectively (see Table 3). It indicates that our proposed model fits the incremental measures fitness criteria well. Finally, to check the parsimonious adjusted measures, we used PCFI (Parsimonious Comparative Fit Index), PNFI (Parsimonious Normed Fit Index), and PGFI (Parsimonious Goodness of Fit Index). The measurement model exhibits values of 0.749, 0.727, and 0.663, and the structural model displays values of 0.762, 0.739, and 0.676 for PCFI, PNFI, and PGFI, respectively (see Table 4). It suggests our proposed model is well fitted with parsimonious adjusted measures criteria. The result of absolute fit, incremental, and parsimonious fit measures suggests that the proposed VCDM is well-fitted regarding measurement and structural criteria. Hereafter, we could advance to check the path coefficient of the structural model.

Model fit summary

Model fit summary

SmartPLS 3.0 was utilized to test the measurement model in the study. We used Anderson and Gerbings’ (1988) two-step statistical analysis procedure to measure the measurement model in SEM. First, the measures’ validity and reliability should be checked before examining the hypothesis (Bagozzi et al., 1991).

Evaluation of reliability and convergent validity

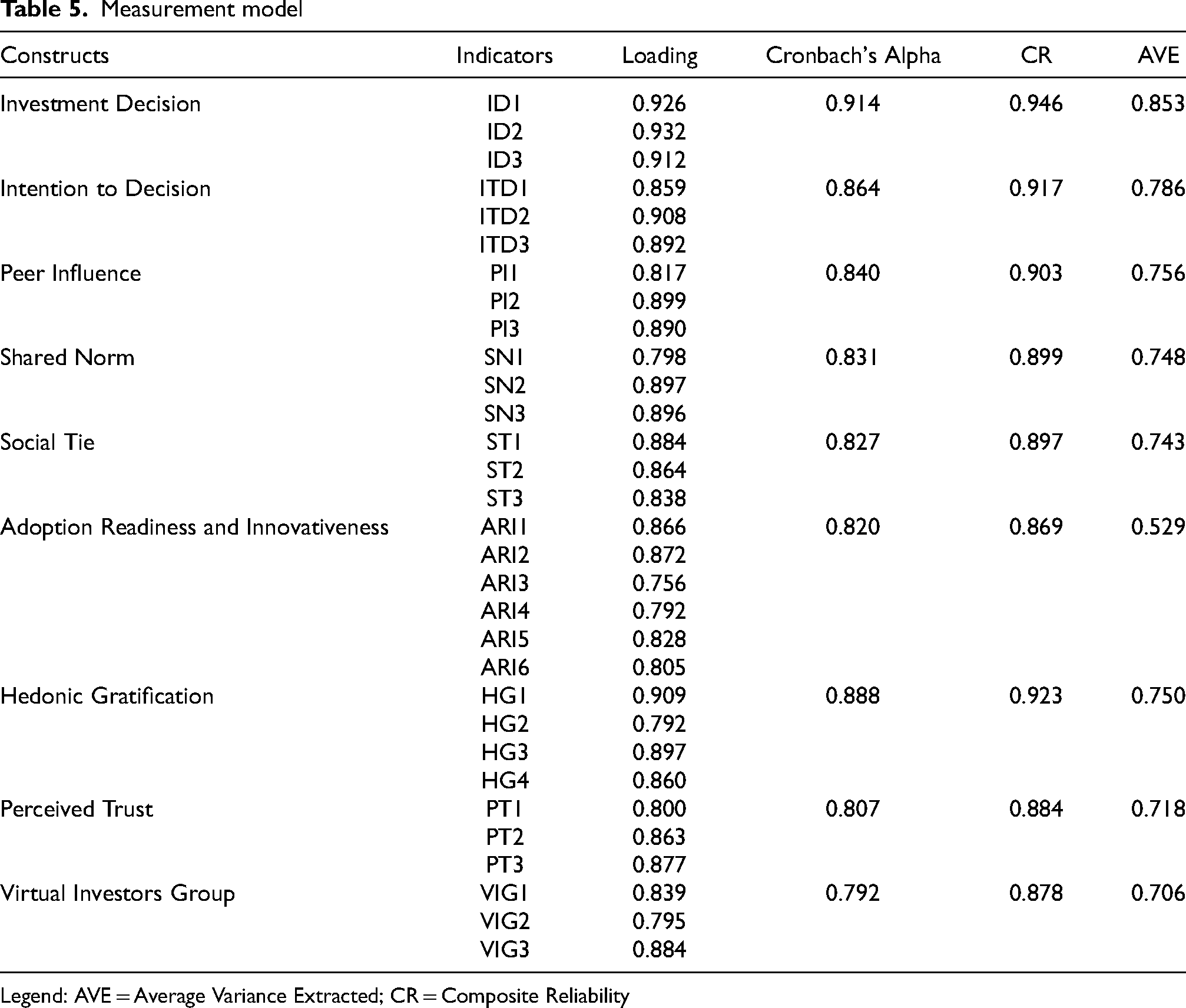

Internal consistency and reliability are assured when Cronbach's alpha and composite reliability are equal and less than 0.70 (Hair et al., 1995). Table 5 shows that the values varied from 0.792 to 0.914 for Cronbach's alpha (α) and 0.869 to 0.946 for composite reliability. The study shows significant internal reliability as the values exceed the cutoff value of 0.70. We used two standards recommended by Fornell and Larcker (1981) to test Convergent validity. First, the value of each item loading should be ≥ 0.70, and second, the value of AVE should be equal to or more than 0.50. Table 5 exhibits that all item loadings were substantial and more than 0.70, and AVE values surpassed 0.50. As a result, the research confirms the suggested measurement model's convergent validity (Fornell & Larcker, 1981; Hair et al., 2011).

Measurement model

Measurement model

Legend: AVE = Average Variance Extracted; CR = Composite Reliability

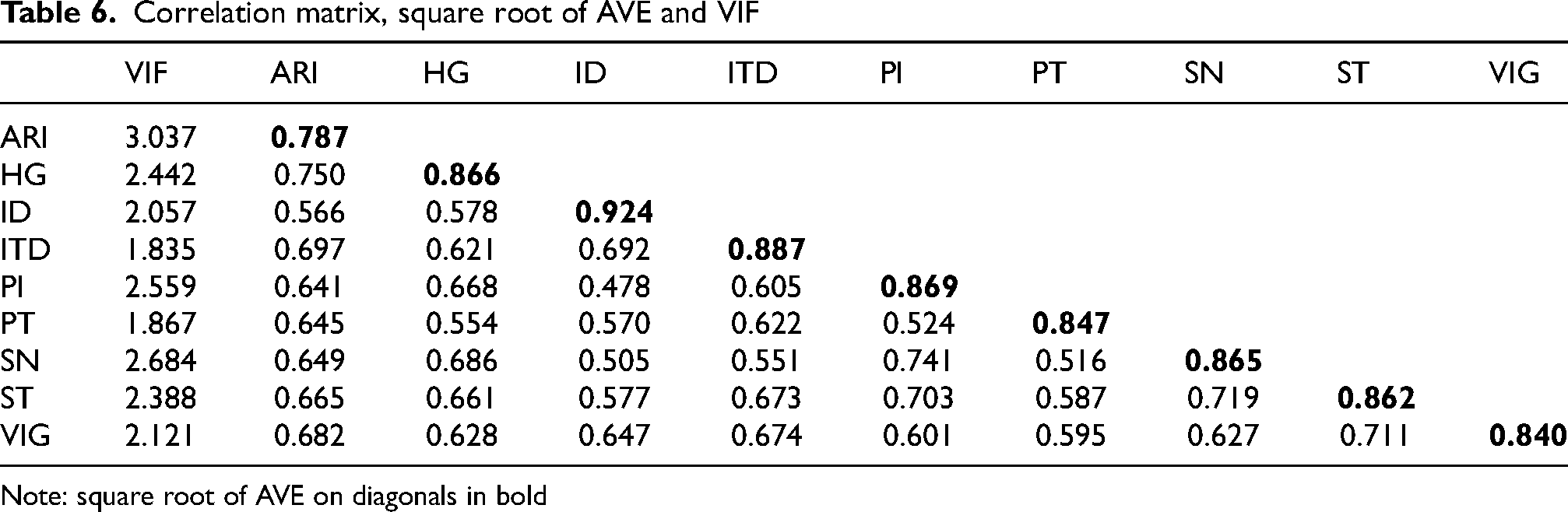

Discriminant validity was assessed based on the two tests (1) the value of correlations among constructs should be within a recommended range of less than 0.850 (Kline, 2005). In addition, (2) the value of correlations of each constructs with other latent constructs should be exceeded by the square root of AVE in the measurement model (Fornell and Larcker, 1981; Henseler et al., 2009). The measurement model results shown in Table 6 reveal that all constructs satisfy both criteria, and the discriminant validity of the data is also confirmed.

Correlation matrix, square root of AVE and VIF

Correlation matrix, square root of AVE and VIF

Note: square root of AVE on diagonals in bold

Due to cross-sectional data, we checked common method Bias (CMB) estimations using Harman's single-factor test (Podsakoff et al., 2003) and (iii) variance inflation factors (VIF) (Kock, 2015). First, using SPSS 21.00 version, we checked Harmon's single-factor test to assess the probability of CMB. Podsakoff et al. (2003) suggested that there may be unfavorable CMB when one item emerged from unrotated exploratory factor analysis and one general item explain more than 50 percent variance among the construct. We also checked for CMB estimations using the variance inflation factor (VIF). “When all VIFs values are equal to or lower than 3.3 from a full collinearity test, then the research model will be treated as free from CMB” (Kock, 2015). Table 6 shows that all variables have a variance inflation factor (VIF) of less than 3.30. These two tests provide evidence that the model is free from CMB.

Interrelationship among model constructs

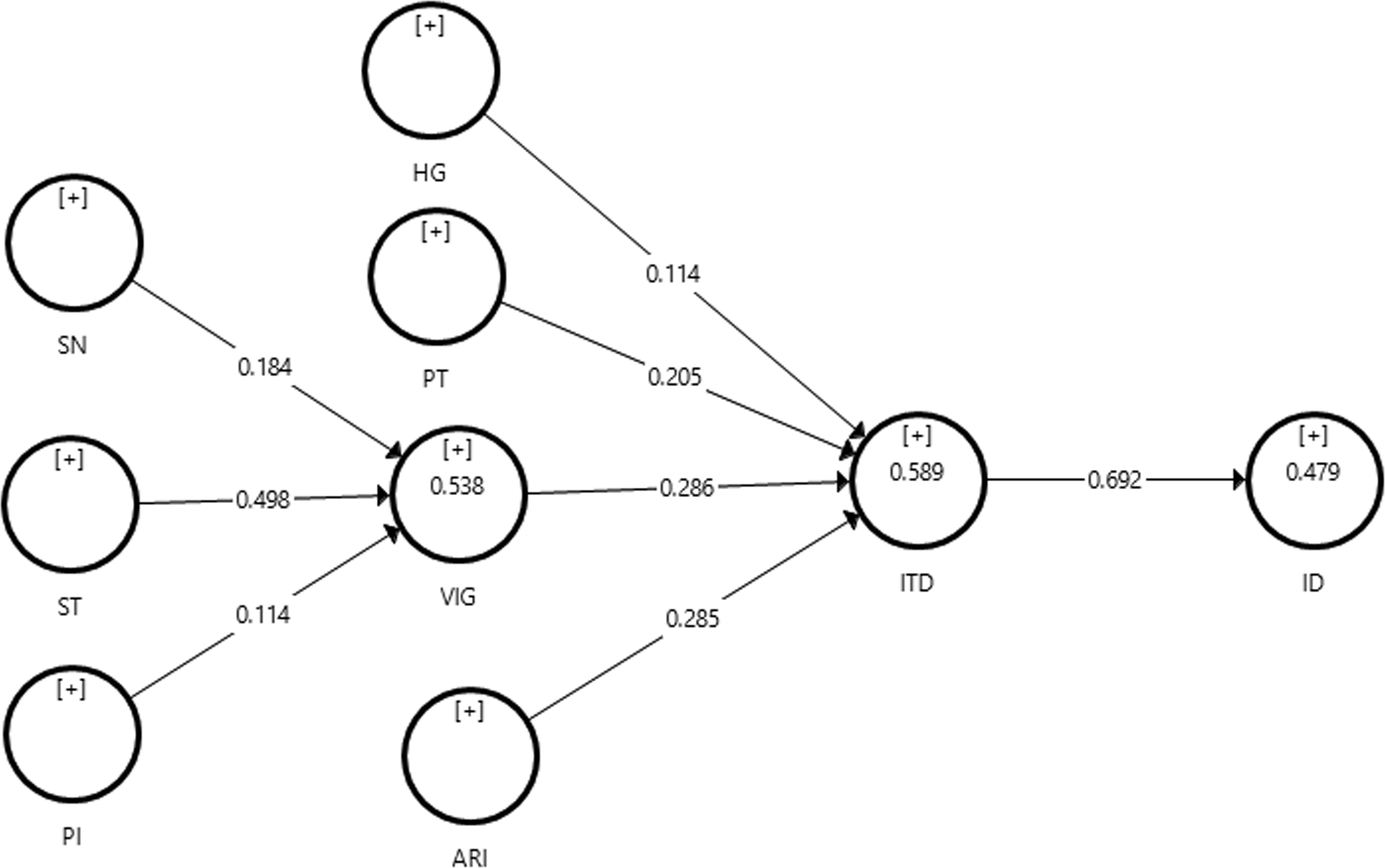

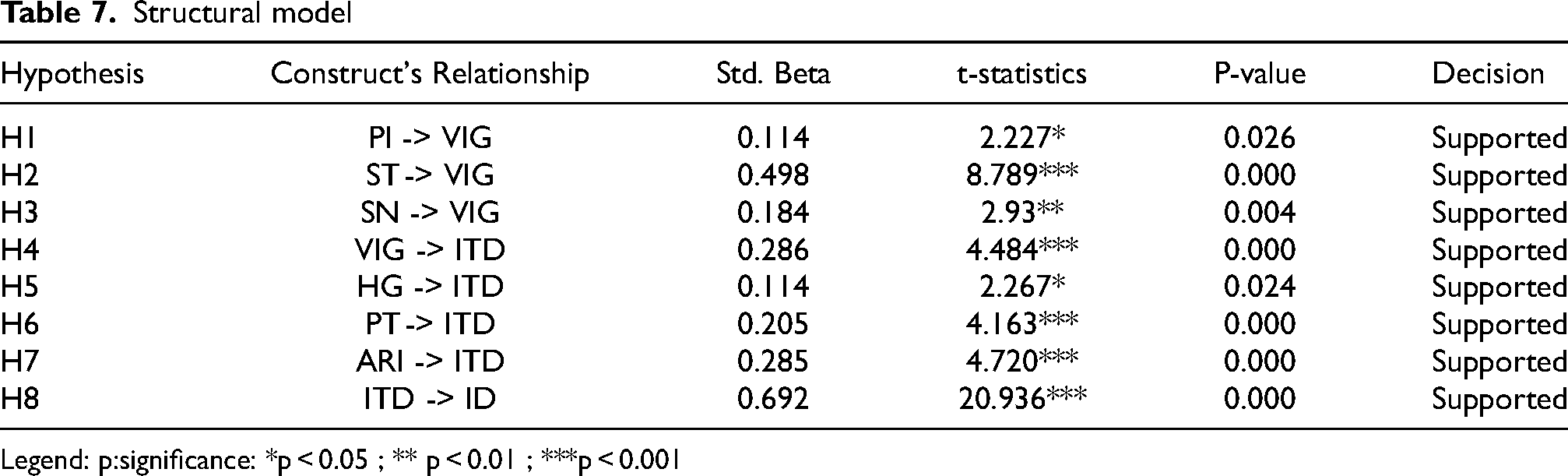

The hypothesized relationships among different constructs of VCDM were checked through the bootstrap significance test of SmartPLS 3.0. Figure 2 displays all path coefficients and standardized betas of a structural model that indicate the intensity of the causal relationships between constructs (Wixom and Watson, 2001). Structural multicollinearity may have in the reflective or formative model when the coefficients of inner VIF or of structural VIF would be greater than 4.0 or 5.0 preferably (Garson, 2016). The output generated from the software specifies that multicollinearity was not an issue in this research since the inner VIF values ranged from 1.835 to 3.0375 (see Table 7). The result from the software indicates that we cannot reject H1, H2, and H3, which implies that all first-order constructs significantly influence the virtual investors’ group. In addition, the empirical outcome indicates that all second-order constructs also substantially impact the intention to make decisions. Therefore, we support H4, H5, H6, and H7. Finally, because it has a statistically significant value (p 0.001, = 0.692, t = 20.936), we validated the H8 hypothesis that the intention to decide on a virtual environment considerably influences capital market investment decisions (see Table 6 for details). The study's most noteworthy discovery is that all offered hypotheses are validated by empirical evidence, indicating model goodness.

Validated VCDM.

Structural model

Legend: p:significance: *p < 0.05 ; ** p < 0.01 ; ***p < 0.001

Figure 2 also shows the explanatory power for each dependent construct. The investor group accounts for 53.8%, intention to decision 58.9%, and investment decision 47.9% of the variance of the proposed VCDM. All the values supersede Hair et al. (2017) recommended 20% threshold (R2) value. We looked at the effect size (f2) to see if the research model was significantly affected. According to Cohen (1988), a "little" impact size is 0.02, a "mid" effect size is 0.15, and a "high" effect size is 0.35. So far, our model reveals that the intention of the decision (f2 = 0. 227) and virtual investors group (f2 = 0.263) have a medium impact size, while the investment decision (f2 = 0.918) has a significant effect size. Furthermore, the study examined the substantive effect of the research model using non-parametric Q2 Stone-value (Geisser, 1974). The predictive relevance (Q2) was further investigated using Cohen's (1988) statistical methods (Garson, 2016). As a result, the model reveals that the investment decision (Q2 = 0.385), intention to the decision (Q2 = 0.436), and virtual investors group (Q2 = 0.356) all had a significant impact. The results also validated the model's predicted accuracy.

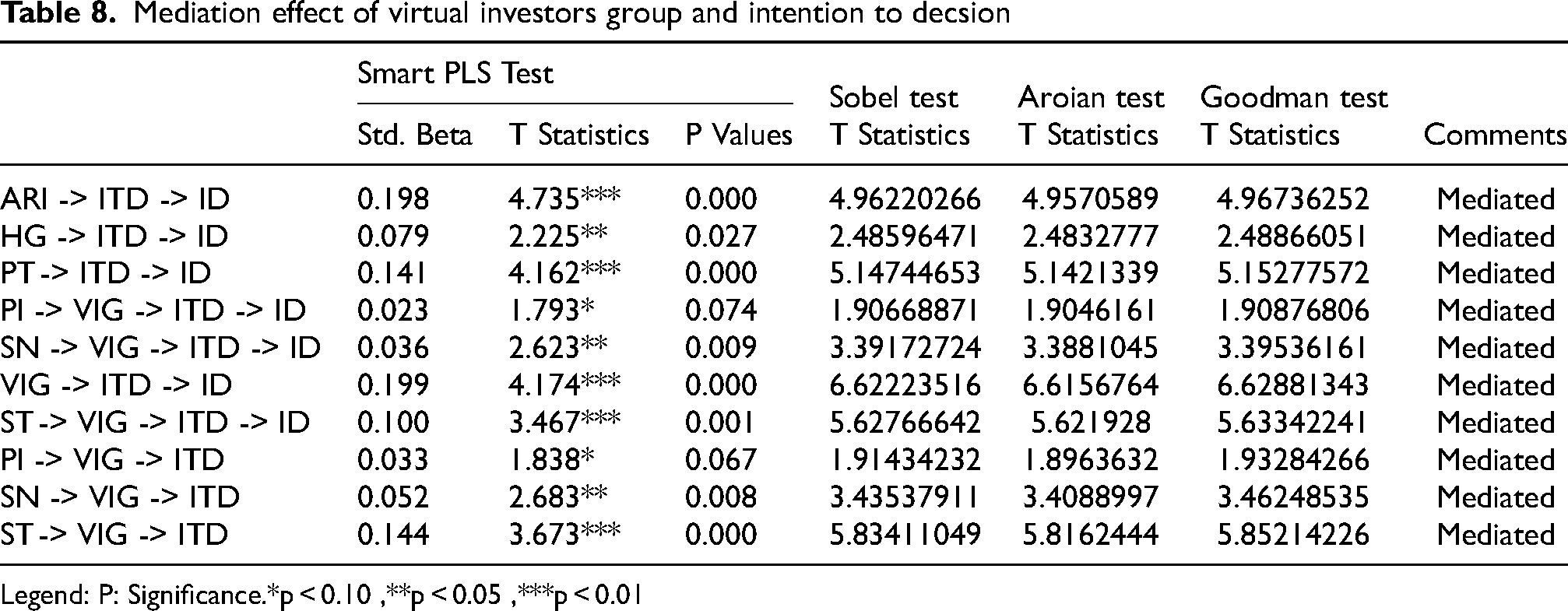

This study developed VCDM to understand the virtual users’ decision status, especially for capital market investments. It used the virtual investor group as a mediator of first-level constructs with the intention to make a decision and the intention to decision as a mediator of second-level constructs with the investment decision. Since it is the first model in the virtual environment decision process, this is the first time anyone has used these constructs. However, these constructs were developed based on some previous research where those constructs are used for different contexts (see Table 2). So it is imperative to know whether these two constructs mediate the different predictors and outcome variables of this model's first-order and second-order constructs, respectively. To analyze the mediation, we followed two approaches: 1) bootstrapping for significance testing (Preacher and Hayes, 2008) and 2) the Sobel test (Sobel, 1982). We utilized SmartPLS bootstrapping to discover the particular indirect impact of the mediator between multiple predictors and the outcome variable for significance testing in bootstrapping. We used SPSS 21.0 for the Sobel test.

To begin, we checked the data for normalcy using the Kolmogorov-Smirnov and Shapiro-Wilk tests. Then we used SPSS regression output in the Sobel test calculator. The significance test revealed that VIG properly mediates between all first-order constructs with the intention to decision, and the intention to decision precisely mediates all second-order constructs with investment decision (see Table 8). Sobel, Goodman, and Aroian test also confirm the bootstrapping result. Thus, both approaches assert that the virtual investors’ Group (VIG) and intention to the decision (ITD) rightly mediate the relationship between first-order and second-order constructs in VCDM.

Mediation effect of virtual investors group and intention to decsion

Mediation effect of virtual investors group and intention to decsion

Legend: P: Significance.*p < 0.10 ,**p < 0.05 ,***p < 0.01

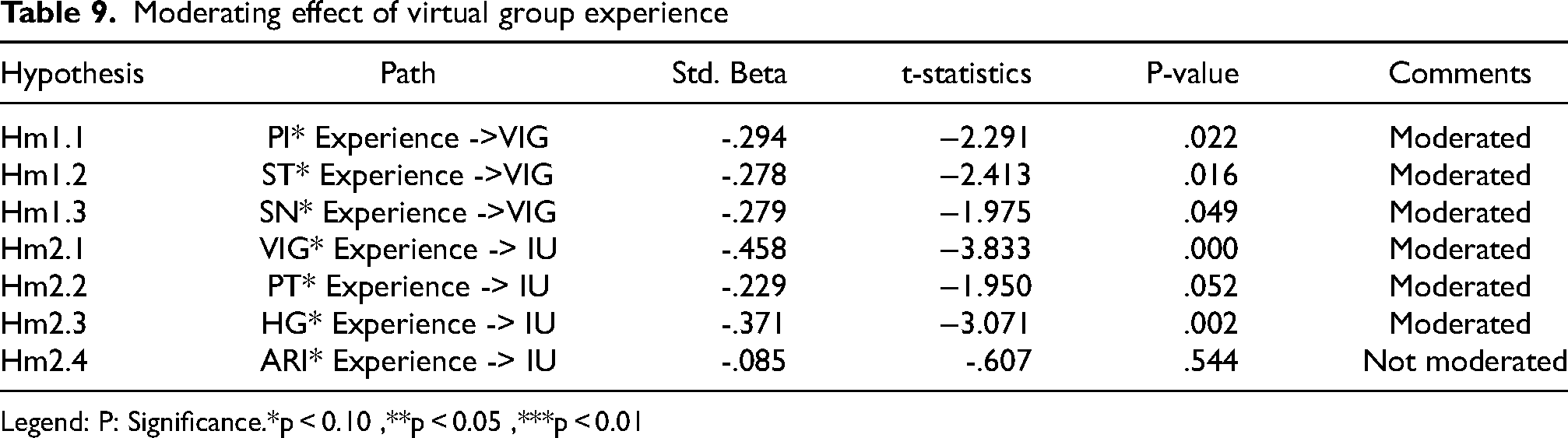

Virtual group use experience, proposed in VCDM, moderated the model's first-order and second-order constructs relationships. By employing SPSS 21.0 version, first, we checked the main effect of a predictor variable on the outcome variable, then the interaction effect of the predictor and moderating variable on the outcome variable. The study executed this process separately for first-order and second-order constructs because virtual group use experience moderated their relationships with outcomes differently. The study explored VG use experience negatively moderated different relationships of the first-order and second-order constructs perfectly. VG use experience does not moderate the relationship between ARI investment intention because people with a high level of adoption readiness and innovation require less experience to make a decision in the virtual world (see Table 9).

Moderating effect of virtual group experience

Moderating effect of virtual group experience

Legend: P: Significance.*p < 0.10 ,**p < 0.05 ,***p < 0.01

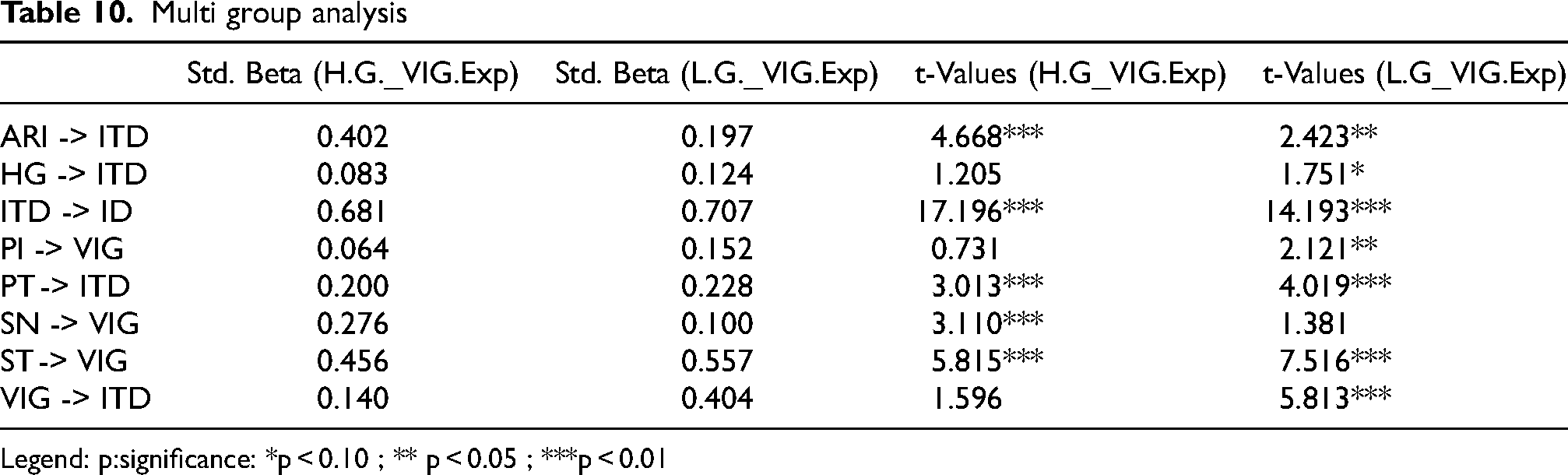

Additionally, the study conducted a multi-group analysis using the PLS-MGA method (Henseler et al., 2009) to comprehend the influence variation among different constructs relationships. The collected data were segregated into two groups based on VG use experience measured by the years used VG. High groups consist of investors who have used virtual groups for more than two years, whereas low groups have experience using virtual groups for two years. In the virtual group use experience, the study uncovered similar and different influences of a different construct to adopt OSNs for investment decisions in the capital market. In respect of peer influence (PI), the hedonic gratification and virtual investors group (VIG) low group exposed more significant factors than the high group (see Table 10). It is indicated that the investors with less experience using virtual groups are more influenced by their peer investors, hedonic satisfaction, and participation in a virtual group. However, for social norms, the high group showed more significant factors than the low group, implying investors with more user experience of the virtual group are concerned about the norms of using the group. Though there is a statistical similarity between the high and low groups in respect of social tie, perceived trust, adoption readiness, and intention to the decision of OSNs, the low group is more concerned about the social tie and perceived trust than the high group and high group is more concerned about the intention to decision adoption readiness and innovativeness.

Multi group analysis

Legend: p:significance: *p < 0.10 ; ** p < 0.05 ; ***p < 0.01

The outcome indicates that high and low-experienced users pointedly influenced the adoption of OSNs for investment in the capital market because it provides the necessary expertise and convenience to use this platform soon.

The study is designed to develop a virtual community decision model (VCDM) from online social networks (OSNs) perspective, considering the pandemic caused by Covid-19. The current study examined the different models and theories of IS/IT adoption, behavioral finance, sociology, and marketing. This study assimilated the disjointed theory and study on the individual involvement and decision into a theoretic model for virtual environment decision that incorporated the vital components of some earlier well-known models (Dwivedi et al., 2017; Venkatesh et al., 2003). First, we recognized and studied eleven models from IS/IT espousal and five theories from behavioral fiancé, marketing, and social science for determining different constructs of VCDM (see Table 1).

Second, the conceptual resemblances across different theories/models and the formulation process of other models, such as UTAUT, UMEGA, and TIM, were followed to develop VCDM. The items for the constructs of VCDM were consciously collected from similar constructs based on their conceptual and empirical performance in previous research following the three-stage procedures for scale development of Moore and Benbasat (1991) (see Table 2). We empirically tested the VCDM with the dataset of individual investors’ investment decisions in the capital market using online social networks at the beginning of the pandemic. The empirical findings reveal robust support for VCDM, which posits first-order constructs (e.g., peer influence, social ties, and shared norms) are direct determinants of virtual investors group and second-order constructs (e.g., virtual investors group, hedonic gratification, perceived trust, and adoption readiness & innovativeness are direct determinants of intention to a decision that had an impact on the ultimate decision on investors in a virtual environment at the beginning of Covid-19. The research model provides strong support for mediating the role of virtual investors group with the intention to decision and first-order constructs. The study's findings explicitly accentuate the significance of different constructs in a virtual environment through the proposed VCDM.

Moreover, the model was capable of explaining 58.6% of the variance (adjusted R2) in intention to decision, 53.6% of the variance (adjusted R2) of the virtual investor group, and 47.8% of the variance (adjusted R2) of investment decision. Regarding first-order constructs of VCDM, it is explored from empirical findings that peer influence, shared norms and social ties are constructive constructs of VCDM. The findings indicated that participation in a virtual group is influenced by peers, friends, collogues, shared language, shared vision, behavioral manner, and ties among members. These findings support the previous studies of Ma et al. (2002), Lippert and Forman (2005) and Liao and Chou (2012), Pai and Tsai (2016), and Xiong et al. (2018) in a different context. The virtual communities’ service providers should develop a more convenient and flexible interaction channel, language and norms policy, and features for incorporating peer opinion to promote strong relationships and participation among the members in e-communities.

Regarding second-order constructs of VCDM, it is uncovered that hedonic gratification, virtual investors group, perceived trust and adoption readiness, and innovativeness are influential constructs of this model. Consistent with prior studies (e.g., Venkatesh et al., 2012; Ernst, 2015; van der Heijden, 2004), this research found hedonic factor is an essential antecedent for adoption/decision in virtual communities since users emphasis on more on the fun aspect during the use of such a virtual environment. This indicates that virtual communities’ service providers should focus on devising hedonic features (e.g., perceived playfulness/enjoyment) to satisfy the members’ needs during pandemic situations.

Virtual investors group is another significant construct of VCDM as the empirical finding supports its strong impact on intention to the decision. Moreover, VIG also emerged as a potent mediator in VCDM since it has strong predicting power (adjusted R2 is 0.536). This indicates that when members formed individual groups in virtual communities, they decided to purchase financial products (e.g., the decision to purchase/sell/ hold stock or bond in the capital market). This assertion confirms the findings of Lin (2007) and Chang et al. (2015), who find that sense of belonging and a virtual group are strong determinants of forming an intention to purchase. It implies that virtual community service providers should develop some features to create groups and effectively enhance communication. Perceived trust is also explored as an essential antecedent to forming decision intention in a virtual world. This finding is consistent with different researchers in different contexts (e.g., e-health adoption (Hoque et al., 2017), mobile self-service technology adoption (Giovanis et al., 2018)) and social networking sites continuance use (Sun et al., 2014), where they found a positive relationship between trust and continuance intention to use social network sites (SNSs).

Adoption readiness and innovativeness have emerged as influential determinants of VCDM since it has more significant statistical value. It indicates that when people are innovative and aware of the utilitarian value of the virtual environment, they are more inclined to make a decision in that context. This finding is consistent with other findings in different contexts, such as mobile self-service technology adoption (Giovanis et al., 2018), m-Payment adoption (Rakhi and Mala, 2014), self-service technology adoption (Lee et al., 2012), and m-health adoption (Hoque, 2016). Virtual communities’ service providers may develop some rules and regulations to monitor and standardize user activities to maintain the proper privacy of users and ensure the instrumental aspect of users.

Finally, intention to the decision has the most significant effect on the investment decision of the virtual communities’ model, indicating that intention to decision is a strong mediator of VCDM since it has strong predicting power (adjusted R2 is 0.586). This finding is consistent with previous findings of different models (e.g., TAM (Davis et al., 1989), Venkatesh et al. (2003, 2012). Moreover, the study also explored that virtual group uses experience moderates VCDM. This finding has consistency with Venkatesh et al. (2003, 2012), where experience moderated the relationship between UTAUT and UTAUT2. This outcome also confirms the framework of behavioral finance proposed by Gu et al. (2014) for individual interactions and thread choices in virtual communities. They found that when investors are more or less experienced in virtual community use, their decision varied for choice.

Implications

Theoretical implications

VCDM was developed to help decisions in virtual environments considering Covid-19 and explain the technology used for decisions in e-World literature. It will enrich the knowledge of behavioral finance, marketing, information systems, and social media by introducing a new model for decision-making in the e-Environment. The majority of existing models for IS/IT adoption account for technological aspects (e.g., performance expectancy and effort expectancy of UTAUT (Venkatesh et al., 2003), implementation aspects (e.g., social influence and facilitating conditions of UTAUT (Venkatesh et al., 2003), and individual characteristics (e.g., the attitude of UMEGA (Dwivedi et al., 2017). Social structural, relational, and cognitive aspects are not included in those models. This model incorporated the social capital theory's structural, relational, and cognitive aspects to explain the decision intention and virtual environment decision of e-peoples. This provides the uniqueness of the VCDM from existing adoption models or theories.

This research proposed and validated the hypothetical model, namely VCDM, with hedonic, utilitarian, and individual, as well as structural, relational, and cognitive variables. The empirical findings provide significant support for VCDM, and the model exhibits outstanding performance than other models. The possible reason is the selection of better-suited measures from different theories of behavioral finance, marketing, social, and information systems. These will advance the existing knowledge of the concerned areas.

Besides, the anticipated model encompassed the virtual investor group to provide a sense of the virtual environment-related characteristics of VCDM. This construct will enrich existing technology adoption research and behavioral and marketing research since rare researchers have developed models for virtual environment decisions. The VCDM offers other persuasive constructs, namely adoption readiness and innovations. This construct encompasses the utilitarian and personal characteristics of users. This integrated construct will guide the future researcher to incorporate this construct in marketing and technology adoption research.

VCDM also include investment decision as the final dependent variable. This decision variable wills enrich the behavioral finance, marketing, and technology adoption domain. VCDM proposed two levels of constructs. First-level constructs deal with participation in virtual groups, and second-level constructs deal with the intention to make decisions in a virtual environment. So these different constructs will help researchers use this model in a different context by using only first or second-level constructs. The VCDM properly balances complexity and explanative power and becomes a more parsimonious and straightforward model. Though this model reduced many moderators like UTAUT and minimized complexity, its explanatory power (variance in intention to the decision of 59% and investment decision of 48%) has notably enhanced its acceptance.

Above all, due to its simplicity and introduction of significant variables, such types of extensive explanatory power are ensured. VCDM incorporated virtual group use experience as moderators for both levels of constructs. Besides, virtual group use experience is a relatively new term in e-World, and it will add new moderators to existing knowledge.

Implications for practice

Due to splinters of knowledge, the adoption literature needs to be more cohesive, confusing the policymakers regarding the model's suitability in the virtual world. The outcomes of this study specified that VCDM would play a conclusive role in an individual's intention to adopt and use the model in the e-environment, considering the pandemic situation. The findings indicated that adoption readiness and innovativeness played a decisive role in an individual's intention to invest in virtual communities. It was found to be an influential determinant of VCDM, implying that the firm should emphasize this factor when designing virtual environments that allow virtual people to make decisions.

The virtual group has emerged as a crucial factor of VCDM, which implies that e-world people are more concerned about discussion and opinion sharing in the virtual group. This study provides a guideline for policymakers (e.g., government and private) regarding the development of virtual groups for their users, which allow them more discussion and opinion-sharing facilities.

Shared norms, social ties, and peer influence are influential antecedents of virtual group formation. It indicates relational dimension plays a vital role in forming the virtual group. Policymakers should be more concerned about the opinion-sharing policy and bindings among the virtual world people during the design of the virtual group.

Trust is an influential turn for using and making decisions in the virtual world. This research also discovered perceived trust as a vital virtual world element. Managers and designers of virtual environments should care more about their pages’ trustworthiness. They should refrain from the decisive links in their pages. Enjoyment is also identified as an influential component of the virtual world. Designers of the virtual world should develop techniques so that users enjoy using the virtual platform.

Additionally, most firms are developing and maintaining online communities for their customers to accelerate their campaigns and sales. This model will guide the manager of such an organization to formulate appropriate policy considering the nature of the user's decision in a virtual world. It will help the service provider of virtual communities to develop related strategies considering the persuasiveness of different constructs of VCDM.VCDM will provide practical guidelines to different practitioners in the virtual world to develop their firm strategy to attract different users in the virtual environment.

Limitations and future research

Though we methodically developed and confirmed the VCDM based on the data gathered from individual capital market investors in Bangladesh, this research has certain limitations. The VCDM was empirically validated by the individual investors of the capital market at the beginning of Covid-19. Hence, generalizing the findings to all types of investors needs more attention. Further research is recommended to extend and validate the model for institutional investors and other consumers in the marketing arena, considering the Covid-19 situation. In choosing different constructs of VCDM, we used only theoretical cohesiveness and previous empirical findings. The study reviewed 58 constructs to develop the constructs for this model. But every construct was not empirically tested using the data gathered for VCDM development. Thus, the items of each construct for VCDM should be considered as introductory; future research can be conducted and test every construct empirically and then take the constructs considering their higher level loading (Dwivedi et al., 2017). In order to validate the VCDM, we used a mixed sample of students, self-employed, government employees, private employees, and pensioner investors.

Generation Y is curious about using new technology in a virtual world. This generation, “Y,” could be looking for future researchers. One-time cross-sectional data collected from individual investors in the capital city of Bangladesh are used in this study to validate the VCDM. In order to check the pre and post-effect and further performance of VCDM, future researchers can use longitudinal data. VCDM did not consider all the utilitarian measures during the intention to decision. Future researchers can extend the VCDM with other utilitarian and personal characteristics measures (e.g., self-efficacy and anxiety) in diverse situations. Finally, while the VCDM explains a more significant proportion of variance (59 percent for intention to decisions and 48 percent for investment decisions) than other models, additional work should be done to identify and test additional boundary conditions for the model in order to provide a richer understanding of virtual communities.

Conclusion

A comprehensive virtual community decision model was created considering the inception of Covid-19 based on literature that encompasses persuasive constructs from previous theories and models. Sixteen established theoretic models/ theories were examined, and 58 diverse constructs were explored to develop VCDM. VCDM is a new model that predicts decisions in a virtual environment and offers robust explanatory value by upholding the parsimony and expediency of society. Each construct in VCDM represents different characteristics, and these features are necessary for virtual environment decisions. All the proposed and empirically supported hypotheses indicate this model's generalizability and can motivate a multitude of hypothesis-oriented research.

Additionally, the moderating effect of virtual group usage experience on first- and second-order construct connections is empirically evaluated and supported. Due to the generalizability of this model, it can be used in a wide range of virtual contexts, allowing the e-People to decide about the future in a virtual environment. This study will encourage interdisciplinary collaboration and exploration of behavioral finance, marketing, information systems, and social media research. Since it extracted essential constructs from well-known models and theories, it can be used as a prime model by the researcher in the virtual community. By developing new measurement scales, scholars are also recommended to add distinct constructs related to virtual communities, such as anxiety, privacy, security, and self-efficacy. Finally, VCDM can accelerate the decision-making process of e-world users and guide the virtual community's service provider to develop pragmatic strategies for the future, considering the social distance concept caused by Covid-19.