Abstract

With this article, we contribute to the recent debate regarding the role of transaction cost economics in IT outsourcing and software development outsourcing research. Our focus is on the contract-type choice for short-term software development outsourcing. For this purpose, we critically examine transaction cost economics and the extant IT outsourcing/software development outsourcing literature and propose a framework which classifies software development outsourcing transactions according to transaction frequency and transaction investment characteristics. The framework identifies short-term software development outsourcing as an occasional, idiosyncratic transaction. Based on this groundwork, we clarify the concept of short-term contract and put forward that such a transaction is governed by a short-term contract. Following transaction cost economics and control theory, our resulting theoretical considerations infer that for short-term software development outsourcing, the vendor’s high human asset specificity and the resulting behaviour-based outcome control, the monitoring of the developer staff, are the triggers for contract-type decisions. Accordingly, staff monitoring by the client should result in Time & Material contracts, whereas staff monitoring by the vendor should result in Fixed Price contracts. We develop corresponding hypotheses which we test with 468 specific contract records for short-term software development outsourcing. The results confirm the transaction cost economics–based recommendations for contract-type choice. We therefore conclude that the advice of the transaction cost economics to use certain governance structures according to transaction attributes is also applicable to IT outsourcing/software development outsourcing transactions. We suggest further exploration of specific contract records to substantiate our results.

Introduction

IT Outsourcing (ITO) includes the procurement of previously internally provided services as well as the subcontracting of another firm to fulfil a special need (Gurbaxani, 2007; Lacity and Hirschheim, 1993; Richmond and Seidmann, 1999). To reach the desired outcome of ITO, the mitigation of contract performance problems through contract choice is widely recognised (Anderson and Dekker, 2005; Eckhard and Mellewigt, 2006; Gefen et al., 2008; Poppo and Zenger, 2002; Richmond et al., 1992). The transaction cost economics (TCE) and its attributes asset specificity, frequency and uncertainty (Williamson, 1985) have been acknowledged as an appropriate, albeit general, framework for contract choice (Lacity et al., 2011). However, TCE and its application have also been critiqued in the strategic information systems literature (Schermann et al., 2016) for not being applied with the necessary precision (Karimi-Alaghehband et al., 2011), and in the context of ITO as merely a basic foundation with ITO being considered a peculiar phenomenon which needs an own and specific theory (Lacity et al., 2011).

Furthermore, unfortunately the existing ITO/software development outsourcing (SDO) literature is ambiguous regarding the transaction type and uses the accompanying terms of short-term contract and long-term contract with different and sometimes contradictory meanings. For instance, the outsourcing of a software development department – where the end of the contract has not been determined and thus is not in sight – might contractually establish a long-term relationship between the client and the vendor. In contrast, in a single outsourced Software Development Project (SDP) that aims to provide a particular software solution and no further cooperation between the client and the vendor is foreseen in the contract, the end of the associated contract has been agreed and thus is in sight. For instance, a client might hire a supplier to develop specific calculation software but sees no need for subsequent maintenance or maintains the software independently or a separate maintenance contract will be negotiated later. For many reasons that are hidden from the supplier, no further collaboration is sought immediately. The contract appropriate for this scenario might be considered a short-term buy-in contract for short-term Software Development Outsourcing (stSDO), but the literature does not provide a unanimous definition of the concepts short- and long-term contract.

We want to contribute to the discussion of contract-type choice. Our focus is in particular on contract choice of stSDO. As a starting point for our research, we argue that research needs to explicitly state and clarify the conceptualisation of efficiently managing transactions and provide clear definitions of the key concepts based on the attributes of a transaction to reduce ‘mixed and unexpected results in terms of the effects of transaction attributes on outsourcing decisions and outcomes’ (Karimi-Alaghehband et al., 2011: 125).

In line with Savolainen et al. (2012), we also contend that TCE-based research on contract choice has to spell out whether it focuses on long-term relations or short-term contracts or both (Savolainen et al. 2012). Long-term relations are built to mitigate lock-in risks (Williamson, 2008). In contrast, short-term contracts tend to cause problems when executed (Banerjee and Duflo, 2000); thus, the concept of short-term contract deserves specific attention. After such clarifications, TCE can be applied more precisely and its benefits for ITO/SDO research can be examined.

For this purpose, we integrate the seminal works of Williamson (1985) on TCE and Macneil (1974, 1978) on contract variants and propose a framework for the classification of SDO transactions in line with the attributes of the transaction which underpins our understanding of stSDO. The framework identifies stSDO as an occasional, idiosyncratic transaction which is governed by a short-term contract. We clarify that a short-term contract is not only defined by its duration, but also by its end that is in sight throughout the contract’s whole runtime because a termination date is agreed and specified in the contract by a client and a vendor.

Following TCE and control theory (CT) (Cardinal et al., 2017; Kirsch, 1996; Ouchi, 1979; Rustagi et al., 2008), our resulting theoretical considerations infer that for stSDO, the vendor’s high human asset specificity and the resulting behaviour-based formal outcome control, the monitoring of task completion by the developer staff, are the triggers for contract-type choice and decisions. Accordingly, staff monitoring by the client should result in Time & Material contracts, whereas staff monitoring by the vendor should result in Fixed Price (FP) contracts. We develop corresponding hypotheses which we test with 468 specific contract records for stSDO.

Our analysis shows that for stSDO, it is crucial for the contract-type choice who actually monitors the vendor’s staff. The results confirm the TCE-based recommendations for contract-type choice to optimise the desired outcome by compensating the vendor at cost of time and material or by a fixed price (Banerjee and Duflo, 2000; Kalnins and Mayer, 2004). We therefore conclude that the advice of the TCE to use certain governance structures according to transaction attributes is also applicable to ITO/SDO transactions. We also determine that in our research based on a precisely defined context and application of TCE, the use of the theory has been beneficial.

This article is organised as follows. In the second section, we position our work with regard to related research and provide the theoretical background. In the third section, we develop our research hypotheses. The fourth section presents our empirical study, including our data set and its analysis. The fifth section concludes with a discussion of our findings, the limits of our research and open issues for further research.

Theoretical background

Outsourcing is a strategic decision of a firm (Lee et al., 2004). The focus of our research is on stSDO, more specifically on the choice of contract type for stSDO for the outsourcing effort to reach the desired outcome. In this section, we provide the theoretical explanation and argument that when a company has decided to occasionally place a one-off, idiosyncratic order as a client with a vendor, stSDO takes place. We further contend that such a transaction is governed by a short-term contract. We also explain that a short-term contract is not characterised by its duration only, but also by its defined end that is in sight throughout its whole runtime because the termination date is agreed and specified in the contract by a client and a vendor.

For this purpose, we first develop a framework for the classification of SDO transactions based on seminal works of Williamson (1985) on TCE and Macneil (1974, 1978) on contract variants that underpins our definition of the key concepts stSDO and short-term contract. On this background, we then critically assess TCE and its impact on the extant ITO/SDO literature with regard to its treatment of the concepts short- and long-term contract. To conclude our theoretical considerations, we subsequently identify and clarify the transaction attributes and transaction costs in the context of stSDO.

A framework for the classification of SDO transactions

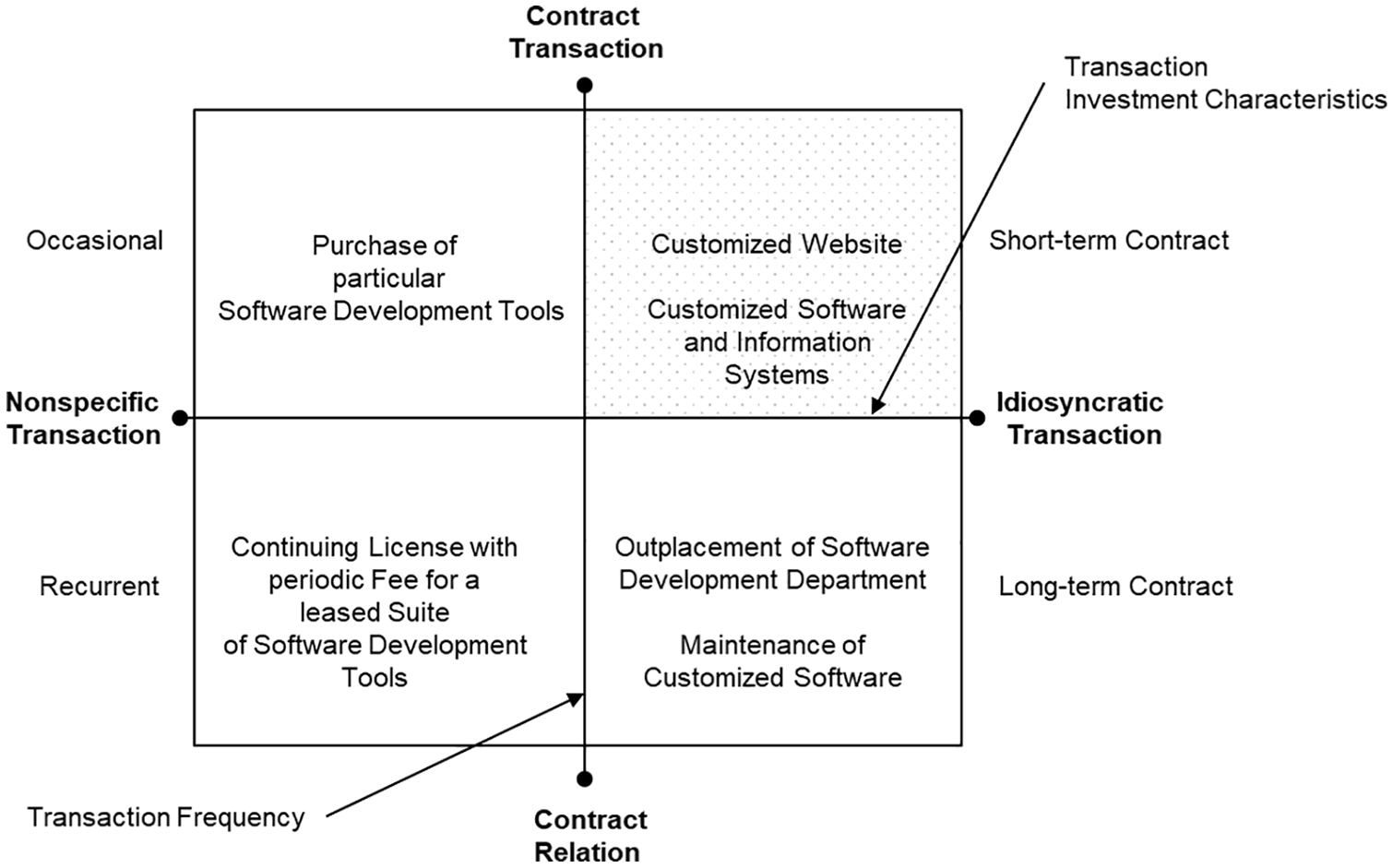

We summarise our proposed framework for the classification of SDO transactions in Figure 1 below.

A framework for the classification of SDO transactions.

We follow Williamson (1985), who referring to the nature of a vendor’s investment, distinguishes between transactional investments in nonspecific transactions and investments in highly specific, that is, idiosyncratic transactions. Specificity here means the alignment of a good or a service to the individual needs of a concrete client. Instances for nonspecific transactions in SDO are, for example, the purchase of particular software development tools or the continuing licence with periodic fee for a leased off the shelf suite of software development tools (depicted in the left half in Figure 1). Instances for idiosyncratic transactions in SDO are, for example, investments in outsourced development of customised websites; of customised software and information systems, as well as the maintenance of such systems; or the operation of an entirely or in parts outsourced software development department (depicted in the right half in Figure 1).

Williamson (1985) also distinguished as transaction frequency the frequency of clients’ activities in the market which varies from occasional to recurrent. Recurrent activities in the market between the same client and vendor lead to long-term relationships which are governed according to Macneil (1974, 1978) by contract relations (lower half in Figure 1), while occasional activity is governed by a contract transaction (upper half in Figure 1).

For investments in nonspecific transactions, Lyons et al. (2009) identified two different contract and payment models: a regular payment for, for example, a leased suite of software development tools, or a fixed price for, for example, the purchase of a particular software development tool. Macneil (1974, 1978) explains that termination is required in the first case, which is usually clearly defined in the contract. In the second case, the contract ends automatically with the payment of the delivered good. According to Macneil (1974, 1978), the former corresponds to a long-term contract relation where a long-term contract wraps around recurrent transactions respective payments. The latter corresponds to a short-term contract transaction with a short-term contract.

Following Macneil (1974, 1978) for the investment in idiosyncratic transactions, the same distinction can be made: Idiosyncratic contract relations are governed by long-term contracts, and idiosyncratic contract transactions are governed by short-term contracts. In the above example of a client outsourcing, an entire software development department or parts of it, it is usually the case that the client regularly pays a fee for an initially indefinite period of time, and the contract relation must be explicitly terminated by one of the two parties (lower right corner in Figure 1). When a client needs and orders the development of some customised software, as a matter of fact the customised software does not exist and cannot be ready for immediate deployment and use. It is in this situation an idiosyncratic contract transaction takes place and stSDO is performed under the governance of a short-term contract (upper right corner in Figure 1).

This reasoning and clarification of the term short-term contract is based on Macneil’s (1978) reflections on the two paradigmatic contract variants: contract relations and contract transactions. These reflections imply that duration and end are concepts that need to be considered together and as a unit. A transaction and the accompanying contract are short term in the sense that, and that is crucial, an end has been agreed and is therefore in sight; no long-term commitment or promise is made that must be expressly terminated by either party. Thus, in demarcation to a long-term relation, we therefore define stSDO conceptually as a short-term contract transaction.

We focus in this research on stSDO as idiosyncratic contract transactions as these, as stated earlier, tend to cause problems when executed (Banerjee and Duflo, 2000). CT proposes in this context behaviour-based and outcome-based contracts (Kirsch, 1996) to control the development process. Behaviour-based contracts reward on the vendor’s behaviour, and outcome-based contracts reward on the consequences of the vendor’s behaviour. In any case, at latest at the end, the client pays the fee for the agreed good or service and the contract is fulfilled and over.

However, the client and the vendor have different goals. The client’s primary goal is to realise their strategic objectives with the customised software (Ika, 2009), of which reducing costs usually is a subordinate goal. Simultaneously, the vendor’s primary goal is the client’s satisfaction as a prerequisite for their own business success (Savolainen et al., 2012). However, the structure of the customised software industry is prone to holdups (Banerjee and Duflo, 2000). A literature review by Gupta et al. (2019), with a focus on project management, confirms that the failure of projects in terms of conflicts during their execution regarding quality characteristics such as to scope, on time, to budget, ultimately leading to their premature termination, is still a very topical issue (see also Baghizadeh et al., 2020). We do not focus on project management but look at the contract between client and vendor. In accordance with the strategic goals of these actors, a dispute in court is a sure sign that at least one actor has not achieved their desired outcome.

While, for a contract relation, problems are anticipated as normal part of the relation to be dealt with in cooperation, for a contract transaction, problems among the parties are expected to be governed by specific rights (Macneil, 1978). In other words, stSDO per se pose a higher risk of conflict. Here, the choice of contract type for a project becomes important. There is consensus among scholars that this choice mitigates contract performance problems (Anderson and Dekker, 2005; Eckhard and Mellewigt, 2006; Gefen et al., 2008; Poppo and Zenger, 2002; Richmond et al., 1992). The contract types for SDO projects are Time and Material (T&M), FP and a hybrid type that consists of a T&M with a Cap (CAP) (Banerjee and Duflo, 2000; Kalnins and Mayer, 2004). With FP and CAP contracts, the scope is usually clearly defined, and the price limit is fixed; for T&M contracts, the actual effort of the vendor defines the price for the project.

TCE and the concept of contract in SDO research

TCE is a key theoretical foundation for investigating and explaining problems with contracts in SDO research (see Benaroch et al., 2016; Chen et al., 2017; Gefen and Carmel, 2008; Gefen et al., 2008; Rai et al., 2009; Walden, 2005).

However, recent SDO research publishes mixed and unexpected results in using TCE (see Karimi-Alaghehband et al., 2011; Lacity et al., 2010; Schermann et al., 2016) and CT researcher queries whether TCE is still a theory (Cardinal et al., 2017) that is suitable for investigating and explaining contemporary organisational and economic challenges. Karimi-Alaghehband et al. (2011), in their review of the use of TCE in SDO, have identified a vagueness in the application of TCE as a possible explanation for the varied and unforeseen outcomes. Transaction frequency and transaction investment characteristics in the context of the concepts of contract and transaction as we have clarified them (see Figure 1) are not explicitly spelled out and studies remain imprecise with regard to what instances of SDO they are investigating. Similarly, Savolainen et al. (2012) have noted in their literature review regarding studies of success and failure of SDP that it was difficult to determine whether the reviewed studies that used TCE were actually about SDO projects because they do not classify their data appropriately.

Since Kodak outsourced the majority of its IT function to IBM in 1989, the efficient continuation of the relationship between a client and its vendor, that is, contract relations, has dominated the research (Chen and Bharadwaj, 2009; Heiskanen et al., 2008; Lacity and Willcocks, 1998). However, as stated above, the existing ITO/SDO literature is not clear regarding the transaction type based on transaction frequency and transaction investment characteristics or uses the terms short-term contract and long-term contract with different and sometimes contradictory meanings. In the following paragraph, we illustrate the treatment of the concepts short-term and long-term contract which corroborate these inaccuracies before further specifying the transaction attributes and costs of an stSDO transaction with some examples.

Wang et al. (1997) investigate differences in uncertainties regarding internal development or outsourcing, among others in terms of different contract structures. The authors state, ‘a long-term contract can always be structured to mimic a series of short-term contracts’ (Wang et al., 1997: 1728). As such, they eliminate any clear properties of the wrapping long-term contract.

Lacity and Willcocks (1998) investigate the outsourcing of IT functions ‘such as applications development, telecommunications, or applications support’ (Lacity and Willcocks, 1998: 407). The authors use the phrases ‘Contract duration: short-term contracts versus long-term contracts’ (Lacity and Willcocks, 1998: 367) and classify contracts ‘into three categories: “less than four years”, “between four and seven years”, and “more than seven years”’ (Lacity and Willcocks, 1998: 377). They use the expressions short term and long term literally, bearing in mind that the outsourcing of IT functions is more of a contractual relationship.

Gopal et al. (2003) describe ‘different contractual arrangements, ranging from individual contracts for individual projects to long-term (10-year) contracts for dedicated offshore centers’ (Gopal et al., 2003: 1761) and ‘long-term multiproject contractual arrangements’ (Gopal et al., 2003: 1681). However, in their data set, they place different transaction types, such as recurrent maintenance and occasional one-off development, in the same category when investigating single contracts (see Figure 1).

Gefen et al. (2008) investigate 238 SDO contracts they had access to, excluding, for instance, maintenance as a recurrent transaction. However, their central measure ‘number of previous contracts’ was ‘calculated based on all the 424 SDO contracts’ (Gefen et al., 2008: 541) the client had signed within a period of time. The authors have therefore not consistently retained their own classification.

Lioliou and Willcocks (2019), summarising 30 years of ITO research, consider system development, system support and maintenance as different types of transactions. However, in their case study, they put all three into the same category. The authors state that each has its own frequency, but for simplification, they nevertheless ‘classify the transaction as “mixed recurrent”’ (Lioliou and Willcocks, 2019: 187). This indicates that these authors also do not take their own classification into account; as in earlier work, they use the expressions short term and long term literally.

However, our theoretical considerations based on Williamson’s (1985) and Macneil’s (1974, 1978) work suggest mapping the concept of long-term contract on the concept of contract relation, and the concept of short-term contract on the concept of contract transaction. Lee et al. (2004), who focus on strategic outsourcing decisions, support this perspective. The authors combine the term short-term with buy-in contracts and comprehensive partnerships with long-term relationships. We also see our perspective as a reasonable reaction to Savolainen et al.’s (2012) observation regarding a lack of categorization of data sets in previous research as the proposed framework for classification of SDO transactions allows for a clear classification of any used data set in contract choice research. We here focus on stSDO contract transactions. To develop our research hypotheses, we now further clarify the transaction attributes and transaction costs of stSDO.

Transaction attributes of stSDO transactions

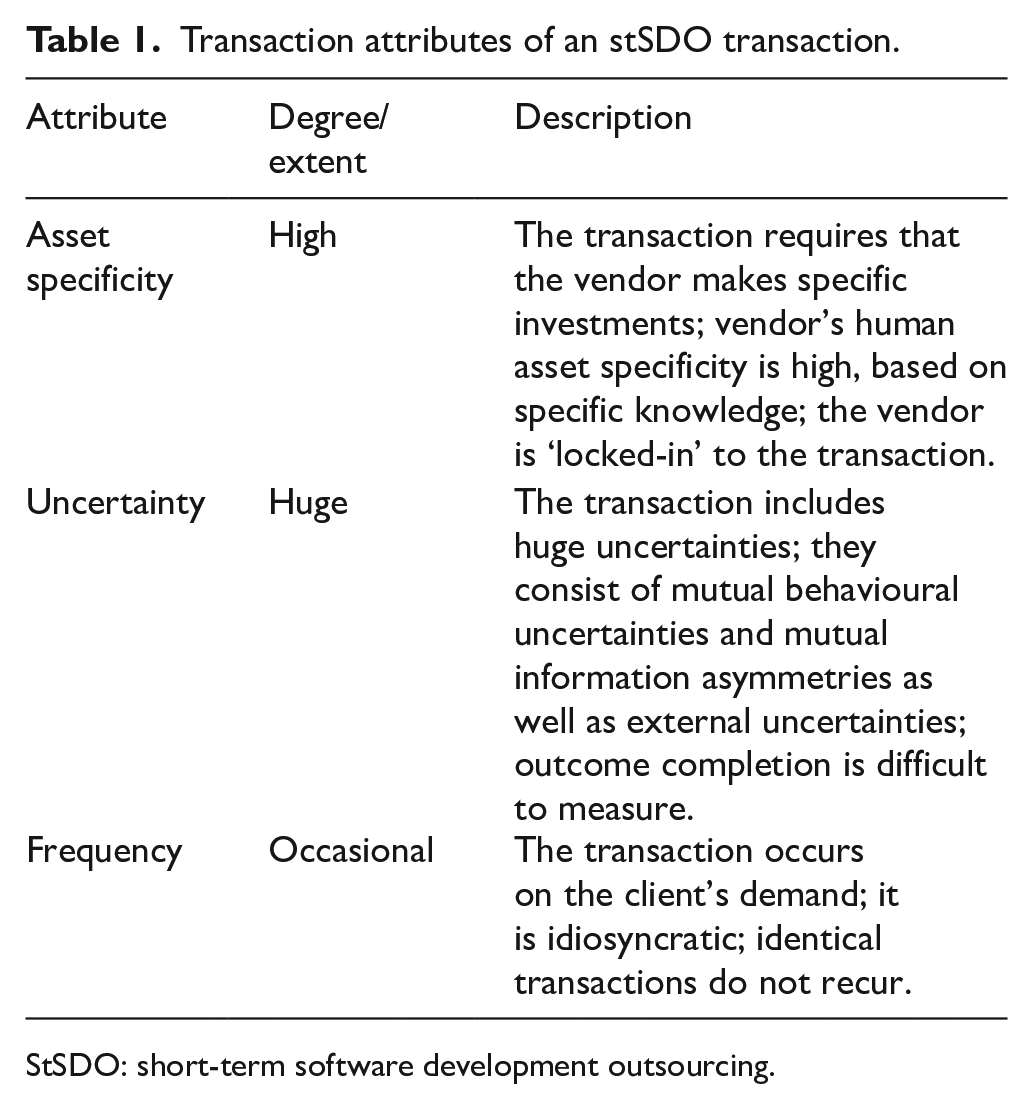

We return to Williamson’s (1985) work regarding TCE. The basic unit of analysis in TCE is the single transaction between a client and a vendor. In TCE, a transaction that is characterised by asset specificity in conjunction with uncertainty is regarded as critical. The frequency of the transaction recurrence affects both issues. These ex-post analytical considerations are based on the assumption that the client and the vendor act with bounded rationality and opportunism (Simon, 1955; Williamson, 1985). In this context, bounded rationality means that the contractual parties act as intended but are limited by cognitive competence, even if all necessary information would be available. The concept of opportunism culminates in seeking self-interest; the contractual parties may act with guile (Williamson, 1981). Necessarily, in the following, we review asset specificity, uncertainty and frequency as dimensions of an stSDO transaction according to TCE. Table 1 summarises this review.

Transaction attributes of an stSDO transaction.

StSDO: short-term software development outsourcing.

Asset specificity becomes important because ‘specialized assets cannot be redeployed without sacrifice of productive value if contracts should be interrupted or prematurely terminated’ (Williamson, 1985: 54). In particular, Williamson (1981: 564) describes human asset specificity in ‘terms of (1) the degree to which they are firm-specific and (2) the ease with which productivity can be metered’. For stSDO, the vendor’s human asset specificity is high as it is based on highly specific knowledge about appropriate software – this knowledge is not easy to transfer.

However, here not only the measurability of productivity of a transaction based on specific knowledge but also the measurement of the degree of the vendor’s client-specific investments creates serious problems for at least three reasons. First, the degree of the vendor’s client-specific knowledge is difficult to measure. In addition, ‘one cannot “unlearn” and recuperate the time spent’ (Aubert et al., 2004: 922). Second, project-specific teams arise, and if the client interrupts or prematurely terminates the contract, these teams are scattered and the vendor’s employees are not easily assigned to other teams (Williamson, 1981) Third, both parties of an SDP have relevant information that must be integrated during the project (Dibbern et al., 2008; Gemünden, 1981; Tiwana, 2003, 2004). For mixed teams consisting of employees from the client and the vendor, productivity is difficult to assign to one side or the other (‘King Salomon Problem’, Williamson, 1985: 82). Ultimately, with asset specificity, ‘the vendor is effectively “locked into” the transaction to a significant degree’ (Williamson, 1981: 555).

Against this backdrop, measuring the value of physical assets or site-specificity in the context of stSDO appears secondary to the measurability of human assets, and with this, the uncertainties related to human assets become huge. Furthermore, the existing mutual information asymmetries in conjunction with bounded rationality and opportunism generate mutual behavioural uncertainties. Consequently, mutual behavioural uncertainties of clients and vendors characterise stSDO. Moreover, external influences may lead to further uncertainties inside the transaction as many contingencies are unforeseeable, and foreseen completion of a transaction may be mistaken, ‘possibly because the parties acquire deeper knowledge of production and demand during contract execution than they possessed at the outset’ (Williamson, 1984: 53). Thus, the client may gain knowledge that will make the project obsolete and will look for an exit scenario to achieve their desired outcome.

Furthermore, for stSDO projects, identical transactions do not recur and cannot generate economies of scale and scope (Williamson, 1985). An agreement on a certain frequency of a transaction may support the decision for specific investments. However, the repetition of a transaction does not occur in stSDO. Accordingly, frequency does not apply to stSDO because there is no secure future promise in the form of a long-term contract (see Aubert et al., 2004).

However, we suspect that due to the stated lack of clarity regarding the transaction type based on transaction frequency, the literature on ITO/SDO does not differentiate between the lock-in situation caused by asset specificity in a contract transaction and in a contract relation. Bahli and Rivard (2003: 214), for example, argued earlier that ‘a client cannot get out of a relationship except by incurring a loss or sacrificing part or all of its assets to the supplier’. Nonetheless, the authors in their work reflect on the fact that the vendor’s assets specificity ‘creates bilateral dependency and poses added contracting hazards’ (Williamson, 1991: 282) which is valid for recurrent transactions, but less so for occasional ones. Unfortunately, they do not make this distinction explicit. Others such as Tebboune and Urquhart (2016: 34) who, in their work on netsourcing strategies for vendors which they explicitly base on TCE, argue that if ‘a firm . . . possesses highly specific assets, then outsourcing an activity . . .becomes a source of major problems, mainly contractual problems’ do not clarify their understanding of the concept asset specificity. Finally, Schneider and Sunyaev (2016: 13) in their reflections on the ITO literature show similar ambiguities in the understanding of asset specificity when they put forward that ‘the risk of the expropriation of valuable (high strategic importance) firm-specific (high human asset specificity) knowledge resulting from the opportunistic behavior of vendors has a negative influence on sourcing decisions’.

We suggest that this also has contributed to the earlier identified inconclusive and possibly misleading research results with regard to the impact of transaction attributes on ITO/SDO contract choice and results (Karimi-Alaghehband et al., 2011). Williamson (1991: 281) himself was rather unspecific when he defined asset specificity as ‘degree to which an asset can be redeployed to alternative uses and by alternative users without sacrifice of productive value.’ This definition does not clearly distinguish the asset-specificity-induced interdependencies within a contract transaction or a contract relation. It is therefore not surprising that Lacity et al. (2010) when referring to this definition in their review of empirical ITO research lament inconsistent results relating to the concept based on Williamson’s work.

We contend that our clarification of transaction attributes in particular of the concept of asset specificity will help to avoid the identified research inaccuracies and mixed results based on Williamson’s (1991) unspecific definition as part of the application of TCE in ITO/SDO research (Karimi-Alaghehband et al., 2011). On this background, we finalise our theoretical considerations with an analysis of the effect of the transaction attributes on the transaction costs.

Transaction costs of stSDO

Transaction costs are the ‘costs of planning, adapting, and monitoring task completion under alternative governance structures’ (Williamson, 1981: 552). For stSDO, planning and adaptation lies inside the client’s company. According to CT, monitoring is viewed as part of formal control (Kirsch, 1996). ‘[M]arkets deal with the control problem through their ability to precisely measure and reward individual contributions’ (Ouchi, 1979: 833). Rustagi et al. (2008: 128) emphasise ‘prevalence, importance, and utility of formal controls . . . in outsourcing’. ‘[O]utcome control is a function of the extent to which behaviors are monitored and outcomes are measurable’ (Kirsch, 1996: 1).

In particular, asset specificity and the control of the vendor’s performance generate transaction costs (Argyres and Mayer, 2007; Dibbern et al., 2008; Reuer and Ariño, 2007). As explained above, stSDO is characterised by high human asset specificity and mutual information asymmetries. Therefore, the transaction costs can be high (Poppo and Zenger, 2002; Williamson, 1985). For stSDO, a deliberate contract-type decision in conjunction with the ‘assignment of someone to oversee the work [,] may be needed’ (Williamson, 1985: 83). Both the client and the vendor are faced with a trade-off between providing incentives through a contract-type decision and ex-post transaction costs for monitoring task completion.

There is a broad consensus about the incentives of the different contract types (Banerjee and Duflo, 2000; Benaroch et al., 2016; Kalnins and Mayer, 2004; Kautz, 2009; Schermann et al., 2016). With an FP contract, the vendor bears all risks for cost overrun, whereas with a T&M contract, the client takes this risk. The CAP contract looks like a flexible contract type between an FP and a T&M contract, but in this case, the vendor bears all risks above the cap and loses profit opportunities. Therefore, when ‘good risks can offer hostages’ concerning premature termination (Williamson, 1985: 177), the vendor offers a hostage with the FP contract, whereas the client offers a hostage with the T&M contract. With the CAP contract, both the client through payment at cost and the vendor through the CAP offer a hostage.

Nevertheless, due to the transaction costs from monitoring task completion for stSDO, mutual behavioural uncertainties require further arrangements (Alchian and Demsetz, 1972; Williamson, 1985). Monitoring task completion can be performed through outcome-based control by measuring the quality of the result of the SDP or through behaviour-based control by respective monitoring of the vendor’s staff during the SDP. Poppo and Zenger (2002) propose to facilitate the monitoring of staff behaviour when the performance is difficult to measure. However, monitoring the vendor’s staff is an undisputed part of project management tasks, and this applies especially to SDPs (Atkinson, 1999). Therefore, we attribute these costs to the production costs. Consequently, if the client takes over the monitoring of the vendor’s staff, the client assumes production costs. However, if the client avoids or does not have the ability to monitor of the vendor’s staff, the client expects that the vendor’s project manager actively striving and monitoring their staff for the delivery of good results by monitoring their staff. This leaves the client with the responsibility to measure the quality of the result. The client’s costs for this activity are transaction costs.

We have now established the necessary concepts for our investigation. Next, we proceed to the development of our hypotheses concerning the role of monitoring of developer staff as a form of behaviour-based outcome control for contract-type choice for stSDO.

Research hypotheses

We develop our research hypotheses based on our analysis of TCE in the context of stSDO. We have clarified that the transaction costs for ‘planning, adapting, and monitoring task completion’ (Williamson, 1981: 553) differ depending on the chosen governance structure. Accordingly, ‘working out the efficient alignments between transactions and governance’ as Williamson (2008: 5) requested, we argue that one contract type will be more efficient than another in terms of ex-post transaction costs to reach the desired outcome. We also follow Macneil (1974: 773) who put forward that ‘[c]omplete and specific planning at or before the commencement of a pure transaction renders unnecessary, indeed inconsistent and undesirable, further planning or other readjustment after commencement of the transaction and prior to its termination’. Consequently, for stSDO, planning and adaptation lies outside the transaction, and the client commissioned the vendor to perform a self-contained task. Planning and adaption inside a transaction corresponds to project management, ‘[p]rocess planning in transactions is thus always a sideshow, always collateral to the main point of the transaction’ (Macneil, 1974: 759). The remaining task is the monitoring of task completion which is a control activity. It can be done informally or by output-based and/or behaviour-based formal control (Kirsch, 1996; Ouchi, 1979). As formal control dominates in outsourcing situations over informal control (Rustagi et al., 2008), we concentrate on formal control. Because of the identified mutual information asymmetries and mutual behavioural uncertainties that lead to difficulties in the output-based formal control, our further focus is on behaviour-based formal control.

Monitoring as behaviour-based formal control

According to Jensen and Meckling (1976: 308), ‘the term monitoring includes more than just measuring or observing the behaviour of the agent. It includes efforts on the part of the principal to “control” the behaviour of the agent through budget restrictions, compensation policies, operating rules etc’. In other words, monitoring means observation and rules. ‘Monitoring is an integral part of the enforcement apparatus of contracts’ (Chen and Bharadwaj, 2009: 7), whereby the lack of observability is associated with a greater demand for rules (Argyres and Mayer, 2007). This is reflected by the fact that monitoring is adopted by the coordination function of inter-firm contracts in general (Benaroch et al., 2016; Eckhard and Mellewigt, 2006). To name some examples for control, Ryall and Sampson (2009) emphasise the number of employees contributed by each firm and the right to conduct physical audits; Reuer and Ariño (2007) refer to auditing rights; and Chen and Bharadwaj (2009) list reporting and interviews. Finally, Anderson and Dekker (2005) notice a positive effect of joint management control structures on contact performance. Summarising, the literature emphasises rule-based control.

However, although it is known that joint processing of information generally enables involved parties to observe the other side (Paashuis, 1998), the common contract literature is silent on observation. This silence is noteworthy because the continuous observation of the vendor’s developers allows an assessment of disruptions; luck and idleness may have the same result as bad luck and diligence (Spremann, 1990). In addition, on-site collaboration is a known and practised software development technique (Gefen et al., 2008; Holmström et al., 2006).

Therefore, we conducted an examination of stSDO contracts focused on observation as a behaviour-based control. However, institutions for the governance are the contract provisions (terms) of a written contract as well as the oral agreements between the contractual parties (Williamson, 1979). We develop our hypotheses as follows. First, we focus on written contract provisions. To obtain a complete view of written contract provisions for monitoring, we differentiate formal control provisions for behaviour-rules and behaviour-observation. Second, we focus on oral agreements regarding behaviour-based control represented by the established project office during contract performance. Therefore, in analysing oral agreements, we do not differentiate between behaviour-based rules and behaviour-based observation. Finally, we examine the association between both behaviour-based control mechanisms of the contract, the written contract provisions and the oral agreements.

Written contract provisions concerning observation and rules

According to our theoretical considerations, we expect that the terms of the written contract – that is, the contract provisions – mirroring behaviour-observation and behaviour-rules separately (Hypothesis 1a (H1a) and Hypothesis 1b (H1b)) influence the contract-type decision because of two paradigmatic cases. In the first case, the development takes place in the client’s office. However, it is unlikely that the entire project workforce of the vendor shifts their workplace to the client. The managers responsible for the contract are not members of the developer team. The work of the developers is thus beyond the control of the vendor. Therefore, we assume that in this case, the risk shifts between client and vendor; the client, who has the developer team in their office, has an information advantage. In addition, mixed teams and site-specificity arise. Therefore, the vendor needs a hostage from the client side; we assume that the vendor cannot accept FP contracts in this case. Furthermore, increasing behaviour-based control of the vendor’s staff during the SDP decreases the costs for output-based control, and the client can accept a T&M contract. In the second case, the development takes place in the vendor’s office. Due to the relational teams and the information advantage of the vendor in the event that the vendor produces the software under its own control, we assume that the vendor has to offer a hostage. Furthermore, decreasing behaviour-based control of the vendor’s staff during the SDP increases the costs for output-based control. In other words, the client cannot accept T&M contracts if the client cannot measure the vendor’s productivity.

However, the vendor should normally control its own staff. By default, the workplace of the vendor’s staff is on the vendor’s side. Therefore, we assume, separately for observation and rules, contract provisions, in association with the selected contract type. Precisely, we assume that with positive probability, T&M contracts contain provisions concerning explicit observation of the vendor’s staff by the client. Moreover, we expect that FP contracts in particular contain control provisions regarding rules. We hypothesise for written contract provisions regarding behaviour-based formal control the following:

H1a: For stSDO contracts, written contract provisions concerning the observation of the vendor’s staff by the client are positively associated with the T&M contract type.

H1b: For stSDO contracts, written contract provisions concerning rules for the vendor are positively associated with the FP contract type.

Oral agreements concerning monitoring

Due to the silence of the ITO contract research regarding the gap in written contract provisions for observation and the practical software development techniques, we expect to find oral agreements concerning monitoring for stSDO. We assume that the nuanced outsourcing decision concerning on-site software development, the shift (or not) of the vendor’s developer team to the client’s office, is part of the contract negotiation and therefore an influencer of the contract-type decision (Hypothesis 2 (H2)). We further assume that an oral agreement concerning that the client monitors the vendor’s staff is positively associated with T&M contracts. Therefore, we hypothesise for oral agreements regarding behaviour-based formal control:

H2: For stSDO contracts, oral agreements concerning the monitoring of contract performance by the client are positively associated with the T&M contract type.

Written contract provisions and oral agreements

Likewise, due to the silence in ITO contract research regarding the contract provisions for observation, we suppose that oral agreements regarding the monitoring of contract performance prevail over written agreements. However, we expect that written and oral agreements tend to move in the same direction with which they are associated (Hypothesis 3a (H3a) and Hypothesis 3b (H3b)). Therefore, we hypothesise separately for observation and control contract provisions:

H3a: For stSDO contracts, written contract provisions concerning the observation of the vendor’s staff by the vendor are positively associated with oral agreements regarding the monitoring of contract performance by the vendor.

H3b: For stSDO contracts, written contract provisions concerning rules for the vendor are positively associated with oral agreements regarding the monitoring of contract performance by the vendor.

Empirical study

We used the contract database of a German software development company as the empirical basis for our investigation. The clients are banks, insurance companies, public authorities, manufacturers and other types of companies.

In the contract database, we found T&M, FP, or CAP short-term contracts according to our definition. We excluded all long-term contracts, including body leasing, consulting, system maintenance, or software licencing. To this end, the database contained information on 468 SDPs with stSDO contracts.

Data set

The SDPs investigated in our study were carried out by the vendor for 77 different clients. With 35 clients, only a single SDP was realised. The average number of projects realised with the same client was 27; the maximum was 82. The first SDP started in 1996, and the last finished in 2018. Therefore, a period of 20 years was covered. The duration was considered the period between the start date and the end date of the SDP. The revenue of the considered SDPs can be described by the amount paid by the client. Finally, we contacted the respective managers, who encoded the information according to our guideline presented in the following section.

The link between the research model and the measured items

The following items, except two, are nominal categorical items where the possible values are distinct and only a few, for instance (Yes/No), or a maximum of four classes. Therefore, as described below, we used the statistical methods developed for such items (Agresti, 2013). In the following sections, we explain the link between the measured items.

The written contract provisions for behaviour-based formal control

Based on extant literature (e.g. Jensen and Meckling, 1976; Kirsch, 1996; Ouchi, 1979), we earlier clarified that monitoring in our context means rules and observation. Therefore, we had to measure two things. On the one hand, by looking at Rule Provisions (Yes/No) in the written contracts, we measured the provisions regarding obligations for meetings or reports. We found provisions for regular or weekly reporting obligations or workshops concerning the progress of the project.

On the other hand, by looking at Observation Provisions (No/Client/Vendor/If necessary) in the written contracts, we measured the provisions regarding determinations of the workplace of the developer team, the vendor’s staff. The default workplace of the vendor’s staff is on the vendor’s side. We also found cases of the client’s project control when the client provided workplaces for the vendor’s staff on-site at the client’s facilities (Client). Some contracts contain an explicit provision that the development had to be carried out on the vendor’s side (Vendor). Furthermore, we found provisions that the client had to support the development by providing on-site workplaces for the vendor’s staff if necessary (If Necessary).

The oral agreement for behaviour-based formal control

An important part of the agreement between the client and the vendor of an SDP is the oral agreement about which party actually (physically) monitors the progress of the project, that is, actually rules, and observes the vendor’s staff. We do not make the distinction between observation and rules for actual monitoring because we are not able to measure it. Therefore, as a proxy, we chose the location of the project office to map the construct monitoring in terms of both observation and rules. For this oral agreement, we contacted the respective manager and documented the place where the project office was set up for each project. We found three possible cases of Staff Monitoring (Client/Vendor/Jointly). In the first case (Client), the project office was on the client side. The client provided workplaces for the vendor’s staff on-site at the client’s facilities. The client provided the project management. The vendor’s staff reported directly to a project manager of the client, and the client made the necessary decisions. Therefore, the client observed and ruled the project staff. In the second case (Vendor), the project office was on the vendor side. The vendor provided the project management and also observed and ruled the project staff. The project manager of the vendor made all decisions during the project. The client received reports about the results. In the third case (Jointly), there was no precise assignment of the project office and thus of the workplaces for the vendor’s staff; managers of both sides were responsible for the project’s progress. The vendor’s staff worked on-site as well as at the vendor’s office. The project managers of the vendor and the client discussed the project’s progress and made the necessary decisions jointly.

For the sake of completeness, we note that we did not find the two remaining constellations, that is, where the vendor’s staff workplace is on the vendor’s side without a project manager from the vendor or on the client’s side without a project manager from the client.

The contract type

We measured the attribute Contract Type (T&M/FP/CAP) by using the price clause of the contract. In our sample, we found three different price clauses in accordance with the findings in the research literature.

Additional items

For the sake of completeness of our descriptive analysis, we added the additional item Project Size and the number of Previous Projects. We measured the Project Size by the overall amount of euros the client needed to pay to the vendor. We calculated the number of contracts signed with this client in the past, that is, the number of start dates in the period before the actual start date of a project with the same client for each project.

Method of the analysis

Because our empirical description of SDP contracts consists of a set of nominal categorical items, we used contingency tables with Cramer’s V as chi-square-based measures for testing the strength of statistical correlations between the relevant items (Agresti, 2013; Kirk, 2003; Sharpe, 2015). We used the p-value for statistical significance evidence. The p-value is an index measuring the strength of evidence against the default position where there is no relationship between two measured items.

In detail, the chi-square-based measure describes the statistical correlation between two items. Each contract has one value for each item. In an empirical data set, between two items, pairs of values occur with a certain frequency, the observed frequency. The calculated expected frequency represents the value that the observed frequency should match in the case that there is no connection between two items (zero hypothesis). The p-value (between 0 and 1) shows the probability that there is in fact no correlation (p = 1). We require a strict level of confidence with p = 0.005. The Cramer’s V (between 0 and 1) shows the strength of the correlation. As a result, it is possible that the p-value shows a statistically significant correlation between the items (p < 0.005); however, there is only a weak correlation (0.10 ≤ Cramer’s V < 0.20) because of other influencing parameters not considered in the test. Appendix A includes our interpretation of the Cramer’s V of association following Rea and Parker (2014). In addition, for a better understanding of the relation between the two items with a statistically significant correlation, we had to compare the observed values with the statistically expected frequencies.

Moreover, in the case of expected frequencies of fewer than five, we had to employ Fisher’s exact test. However, this computationally more intensive test delivers results that are not normalised. For these tests, we used IBM SPSS Software. In addition, we employed the chi-square test; the results are comparable with those of Fisher’s exact test. However, we refer to Cramer’s V, a normalised chi-square-based test, when interpreting our results.

Furthermore, we calculated the Standardised Residuals for a cross-table cell-by-cell comparison of the observed and the expected frequencies (Haberman, 1973; Sharpe, 2015) (see also Appendix B). A magnitude greater than ±2 in a cell indicates a lack of fit of the zero hypothesis that the items are independent. A magnitude greater than ±3 indicates that something extremely unusual is happening (Agresti, 2013).

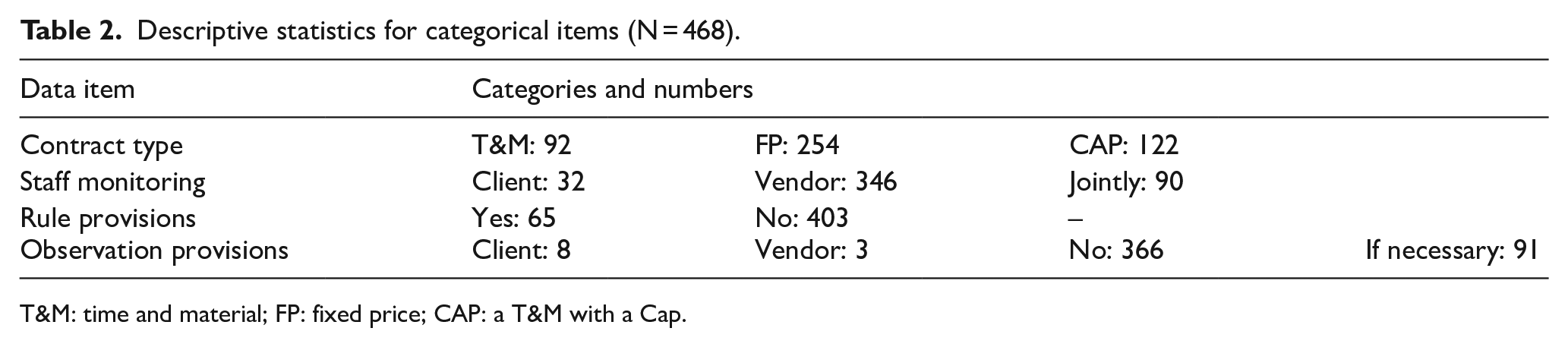

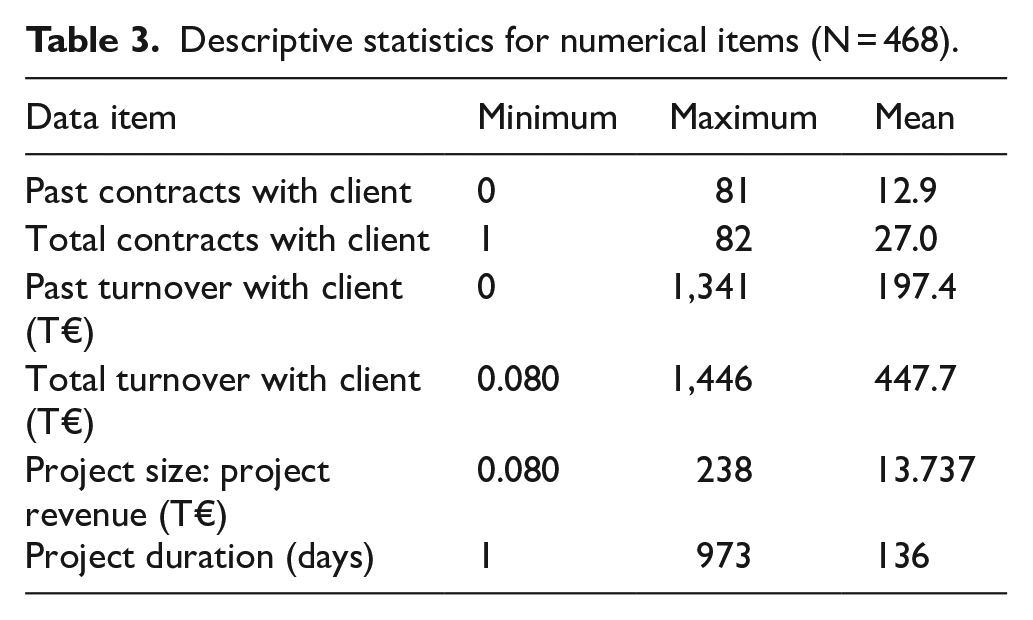

Table 2 shows an overview of the categorical items we collected. Table 3 shows the numerical measured items that we collected. The number of past contracts with a client reflects the number of past contracts for each contract individually, while the total number of contracts relates to the number of contracts with a client overall. We dealt with the turnover in the same way. Project size, project revenue and project duration are measures for each contract in detail.

Descriptive statistics for categorical items (N = 468).

T&M: time and material; FP: fixed price; CAP: a T&M with a Cap.

Descriptive statistics for numerical items (N = 468).

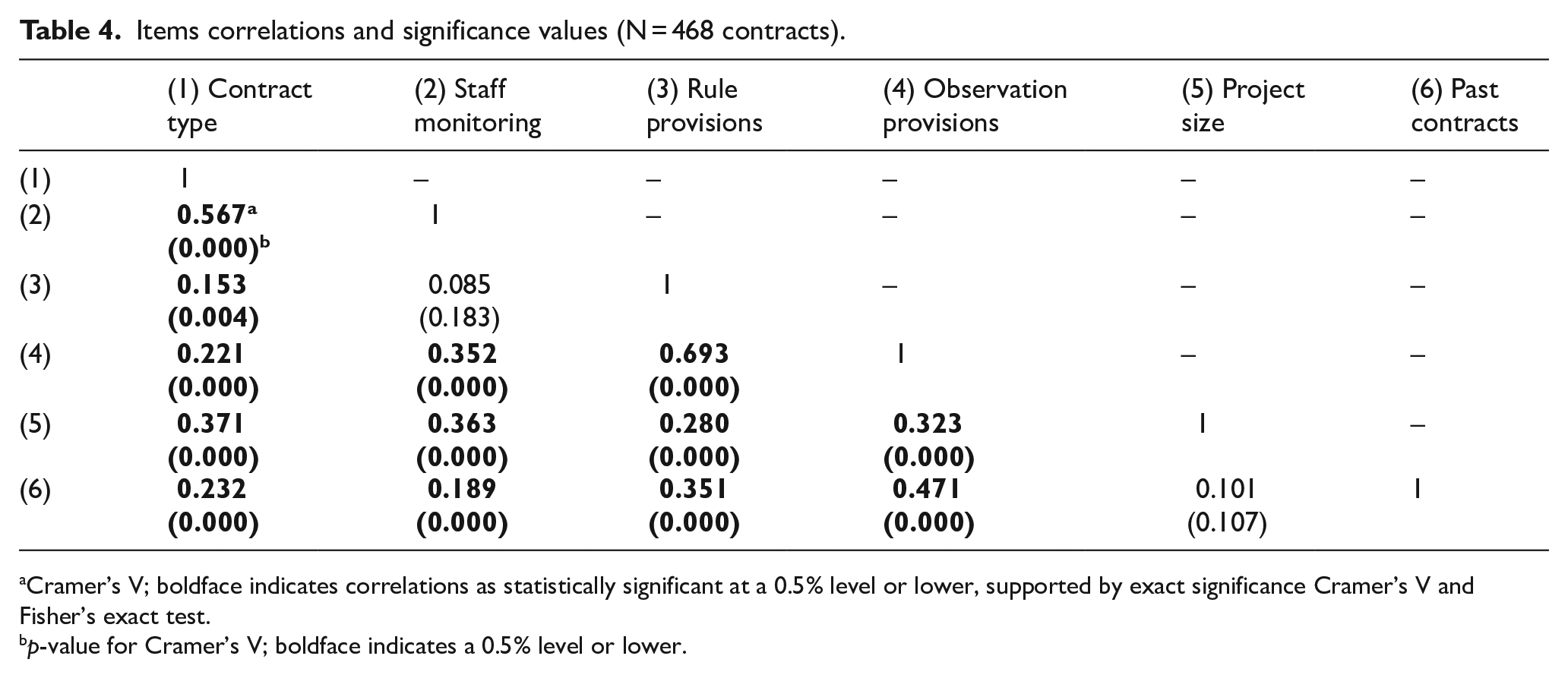

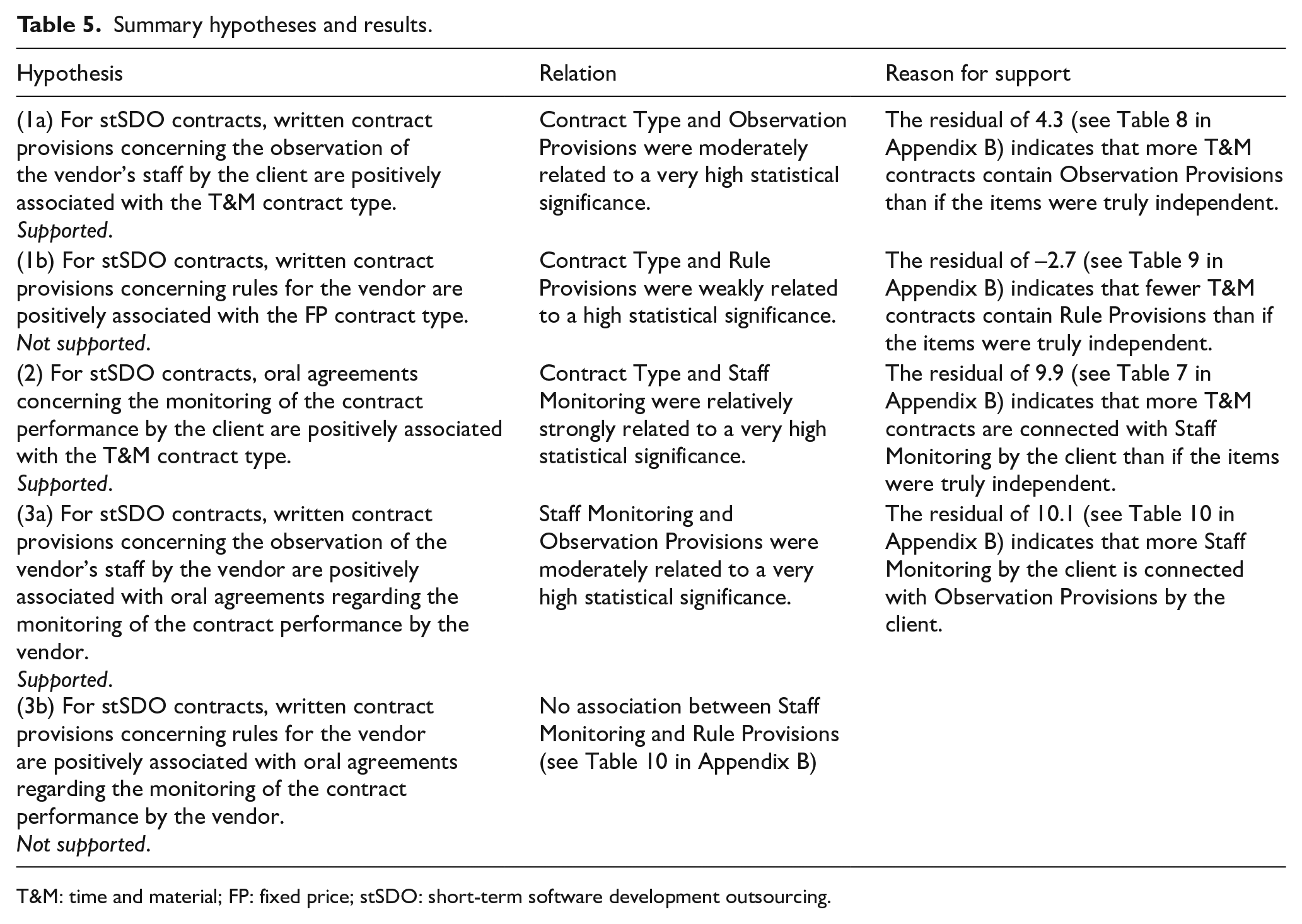

Table 4 contains the correlations by Cramer’s V and associated significance values (p-values). We summarise our results in Table 5 and present their more detailed analysis and interpretation in Appendix B. For our data set, we found that the decisions of the contractual parties are not different from what TCE suggests.

Items correlations and significance values (N = 468 contracts).

Cramer’s V; boldface indicates correlations as statistically significant at a 0.5% level or lower, supported by exact significance Cramer’s V and Fisher’s exact test.

p-value for Cramer’s V; boldface indicates a 0.5% level or lower.

Summary hypotheses and results.

T&M: time and material; FP: fixed price; stSDO: short-term software development outsourcing.

Discussion and conclusion

To contribute to the recent ITO/SDO research, we offer a framework for the classification of SDO transactions and the corresponding contract variants. Depending on the vendor’s specific investments and the client’s frequency of demand (Macneil, 1974, 1978; Williamson, 1985), the contract variants which we put forward range from nonspecific or idiosyncratic long-term contract relations to nonspecific or idiosyncratic short-term contract transactions (Figure 1).

In detail, we have focused on stSDO, and the decision that concerns choice of the contract type for stSDO. In order to make appropriate recommendations for practice on the choice of contract type, we followed Williamson’s (1985) advice and analysed the distinct properties of the stSDO transactions in terms of asset specificity, uncertainty and frequency. We identified high human asset specificity in conjunction with information asymmetries as essential properties of stSDO transactions. From a TCE point of view, because of measurement difficulties regarding the value of the vendor’s specific investments, high mutual behavioural uncertainties characterise stSDO further. Together, these conditions cause high transaction uncertainty for both the client and the vendor. Furthermore, a short-term contract for a single SDO project will not trigger reputational effects and economies of scale and scope.

For idiosyncratic contract relations, ‘planning, adapting, and monitoring task completion’ (Williamson, 1981: 552) are part of the relation. For idiosyncratic contract transactions, planning and adaptation lie inside the client’s company, and the client commissioned the vendor to perform a self-contained task. The remaining task is the monitoring of task completion. Following the findings of CT, monitoring task completion can be done outcome-based or behaviour-based (Kirsch, 1996). According to our theoretical considerations for stSDO, increasing behaviour-based monitoring of the vendor’s staff by the client during the SDP (production costs) decreases the costs for output-based monitoring task completion (transaction costs) and indicates a T&M contract. Thus, the client bears only the actual production costs. As the client monitors the development process, the client can stop the SDP at any time without having to pay the vendor for efforts and services which have not been provided. The outcome is still acceptable for both parties.

Conversely, decreasing behaviour-based monitoring of the vendor’s staff by the client during the SDP as part of the production costs increases the costs for output-based monitoring task completion as transaction costs and indicates an FP contract. However, the client can refuse to accept and to pay for the result of the SDP in the case of an FP contract. Because of the vendor’s specific investments, the FP contract is very risky for the vendor, and the vendor is ‘locked-in’ to the transaction. In such a case, a dispute has to be expected. For a third party however, it is not apparent whether the client is pursuing fraudulent goals or whether the client rightly criticises the vendor’s performance. In the first case, the client reaches a desired outcome and the vendor pays for it. Williamson calls this a ‘contrived cancellation’ induced by the client (Williamson, 1985: 179). In the second case, both the client and the vendor do not reach their desired outcome but that cannot be cured by the contract. It indicates, following principle-agent theory (see Arrow, 1986; Spence, 1973), that the mutual choice of a contractual partner through client and vendor was not thorough enough.

We reviewed our considerations by means of 468 data records from one vendor with different clients. Emphasising the normative character of TCE, the contract-type choice of these stSDO contracts corresponds to the theoretical considerations and the recommendation we derived from TCE and the CT. Because of the vendor’s high human asset specificity and the client’s one-off demand, the behaviour-based monitoring task completion dominates the contract-type decision for stSDO.

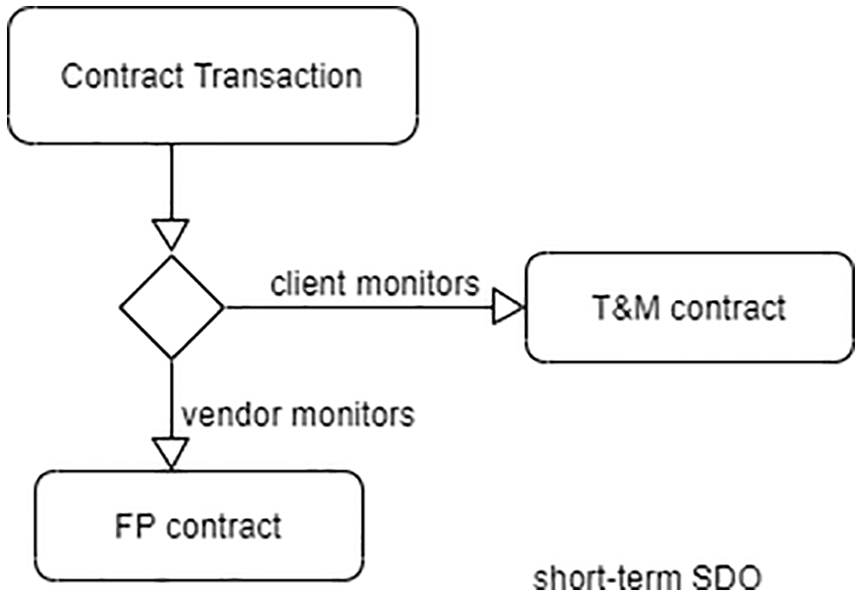

This means that if the SDP was performed under the client’s monitoring at the client’s office, the T&M contract was dominant. When the SDP was executed under the vendor’s monitoring at the vendor’s office, the FP contract was dominant. Our recommendations for contract-type choice for stSDO are in accordance with these.

However, most contracts did not contain written provisions for monitoring. We explain this finding with the fact that monitoring is part of the production of software; the vendor observes their own staff by default. Nonetheless, the written contract provisions regarding the observation of the vendor’s staff were consistent with the oral agreements. However, we found fewer rule provisions in FP contracts than expected. We suspect that this might be the case because the effect of the fixed price is so strong that the client and the vendor see no need to explicitly state what the vendor has to do.

In this context, we recall the contrived cancellation by the client as a vendor’s risk in the case of an FP contract (Williamson, 1985). In our data set, only FP contracts failed in the sense that the parties ended up before a court for a conflict resolution. In total, these were only three of 468 contracts. Two cases clearly indicate a contrived cancellation induced by the client. However, because of the small number of failed FP contracts, we could not extend our statistical research in this direction. In this context, we acknowledge that our research is limited as its use of only one data set and coding scheme naturally involves some subjectivity and further research is required.

From our data set, the CAP contracts did not give any support to the association between written contract provisions and the chosen contract type itself. However, as the number of past contracts increased, we observed a tendency to shift from CAP to FP contracts. We explain this effect with decreasing behavioural uncertainties on both sides through reputational effects from payment history and observed work results. Thus, with the FP contract, the vendor waives the hostage of the CAP contract (payment at cost) and improves their profit opportunity. At the same time, the client withdraws from the observation of the vendor’s staff and reduces production costs. However, in our research, the role of the CAP is not fully explored, and further research is required regarding CAP contracts.

To summarise, our research shows that most of the existing ITO/SDO research cannot be placed in a clearly defined classification of SDO transactions (see Figure 1) and provide recommendations for the subsequent contract-type decision in the case of stSDO such as the ones that we have developed and presented here (Figure 2). Moreover, the unspecific definition of asset specificity by Williamson (1991) has led to research inaccuracies regarding TCE (see also Lacity et al., 2010; Schneider and Sunyaev, 2016). More precisely, it remains unclear who invests specifically and who is dependent (‘lock-in’) on the other contractual partner and when, that is, who needs protection by the contract. We also reveal that TCE introduced in this form by Williamson does not sufficiently take into account the contributions made by Macneil. The contribution of the contract to the success of the short-term SDP is therefore overlooked. With our classification, we are making a suggestion on how this gap can be closed. In our view, the previously reported mixed research results therefore had to be expected.

Recommendation for contract-type decision for stSDO.

In this regard, we have provided a clarification and subsequently shown the usefulness of TCE as an analytical framework for governing ITO/SDO transactions (Karimi-Alaghehband et al., 2011; Lacity et al., 2011; Schermann et al., 2016). Moreover, we demonstrated the usefulness of balancing incentives through contract-type decisions, and ex-post transaction costs for monitoring task completion. We hope that this motivates future CT research to include the incentive effect of the contract in their considerations. We however emphasise that the smallest unit of investigation has to be a defined transaction (Williamson, 1985). We have shown that classifying the transactions and their contracts leads to results that can be explained by TCE. Long-term maintenance is very different from a single software project. Therefore, the contract-type choice and the assessment of ex-post transaction costs for monitoring task completion differ. Consequently, we recommend further exploration of specific contract records with clearly defined subjects of a contract; otherwise, the results of the exploration of unspecific contract records might possibly lead to inaccurate outcomes and mislead practitioners in their governance of outsourcing decisions.

Footnotes

Appendices

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.