Abstract

In wake of the global economic crisis, there is a growing pressure on cities to engage in new entrepreneurial strategies for development. Financialised development mechanisms, such as Tax Increment Financing, could enable cities to re-ignite growth and stimulate development. This article highlights the opportunities of engaging in the process of financialisation, as well as the risky nature of financialised funding mechanisms. Using Newcastle upon Tyne as an example, it is argued that the opportunities and risks of adopting Tax Increment Financing vary geographically. The dilemma for policy makers – embrace a high-risk development strategy or become less competitive – is more apparent in underperforming and peripheral urban areas. In response to these geographically uneven tendencies, this article presents some policy recommendations for mitigating risk and maximising Tax Increment Financing's potential for successful urban development.

Introduction

Tax Increment Financing (TIF) is a tool for tapping into the wealth generation capacity of cities. It offers cities the prospect of successful economic development even in the context of state retrenchment and austerity. TIF is a mechanism that could enable a city authority to borrow against – and capture – tax revenues resulting from increases in the rental value of commercial property within a specific area.

At the heart of the mechanism is the potential to generate new revenue streams (in the form of business rates) that are reinvested into the urban landscape. Revenues are generated by stimulating an increase in the rental value of properties, which is achieved by investing in development projects within the targeted area. Crucially, the revenue streams are used in advance of their receipt in order to secure the debt that is used to invest in the development project. When the actual revenues arrive, the debt begins to be repaid.

Such a scheme also has the potential to stimulate economic development by generating opportunities for private sector investment and by creating jobs across a number of different industries and sectors. As such, TIF presents a viable and potentially groundbreaking solution to the challenge of funding urban development and regeneration in the UK. As well as providing much needed funds for urban development projects at the local government level, the emergence of TIF in the UK can also be understood in the context of the ‘localism’ agenda that has been a core strategy for the current coalition government.

Importantly, TIF involves the accumulation of high levels of debt for a government authority. Indeed, the processes of ‘asset creation, valuation and securitization’, which underpin the mechanism of TIF, make it an innately risky and unpredictable mechanism (Weber, 2010: 270). In order to service its debt, a TIF scheme is dependent on an increase in the rental value of commercial property within the TIF district.

TIF can be regarded as a financialised funding instrument for a number of reasons. First, it relies on the appreciation of rental values, a process which can be easily impacted by movements in the financial markets. Second, and as a result, TIF entails a degree of speculation. Third, TIF can generate large amounts of debt for the public sector, which over time can lead to a downward spiral into over-indebtedness. Fourth, although the funds for TIF schemes in the UK are usually borrowed from the Public Works Loan Board (PWLB), there is nevertheless a clear connection between the price at which Treasury Gilts trade on the financial markets, and the cost for local authorities of borrowing from the PWLB. Finally, the ability of private developers to generate finance for their investments in the TIF district is heavily dependent on the willingness of financial institutions to invest and the price at which they are prepared to lend.

Although TIF can genuinely be considered as an opportunity for economic development and growth, its emergence, along with the emergence of other financialised funding mechanisms, could have uneven implications. That is, cities with weaker economies could face more risk when using TIF. Because of its debt-based nature, TIF directly positions the potential to generate economic growth, realise profits, create employment and stimulate regeneration against the potential to cause jobs losses, over-indebtedness and increases in council tax. Arguably, this dilemma is more pronounced in underperforming areas due to their lower growth rates and their potentially volatile economies.

This article clarifies how financialised mechanisms can function in the UK, through a geographical analysis of TIF in Newcastle. It argues that local government authorities can create opportunities for development through TIF, but also face the most risk when engaging in TIF schemes that require the adoption of high levels of debt. As such, the article highlights an alternative form of TIF scheme that could potentially be adopted in the future, a ‘pay-as-you-go’ model, which passes the risk onto the private sector. This model, however, is not likely to create the same level of opportunity as the debt-based version, and could be viewed as too risky for developers, particularly in peripheral economies.

First, the article explores the concept of financialisation and the impacts that the economic crisis has had for the ability of local authorities to stimulate economic growth through development. Second, the financialised mechanism of TIF is broken down and explained. Third, the article examines the dilemmas of using TIF in Newcastle upon Tyne. The risks of engaging in two types of TIF scheme are discussed; the public sector debt model and the pay-as-you-go model. It is argued that the risks are necessarily higher in underperforming economies if the same level of opportunity is to be generated. The article then makes recommendations which could increase the feasibility of TIF and reduce its uneven impact. These include reducing the level of debt, shortening the repayment profile and increasing the duration of a scheme. Finally, some brief conclusions are offered.

Financialised development tools: Examining the context

A new landscape of urban development

The ‘growing influence of capital markets, their intermediaries, and processes in contemporary economic and political life’, known as the process of ‘financialization’ (Pike and Pollard, 2010: 29), has been a driving force in changing urban development policy. Although the process of financialisation is creating new opportunities for profit, it is also intensifying the crisis-prone tendencies of capitalism (Leyshon, 2004). Indeed, the intensification of capitalist accumulation has rendered the global economic system more unstable and unpredictable.

Economic crisis has caused a reduction in the inward flow of public sector funds, particularly in peripheral cities, which had previously acted as a vital supporting mechanism for their economies, causing stunted business growth and a rise in unemployment (Dawley et al., 2011), compounding the disproportionate impacts of the crisis (Martin, 2011). The programme of deficit reduction and the wave of austerity in the UK's public sector mean that traditional funding mechanisms for infrastructure projects and urban developments are no longer viable, and that alternative mechanisms need to be found.

Newcastle City Council, for instance, has identified £30 m of savings to be made during 2012–2013 (Newcastle City Council, 2011: 5). At the same time, 24.6% of employed people in the North East of England work in the public sector, which is more than any other region (Office for National Statistics, 2012). As a result, in order to preserve and create jobs, and to stimulate economic growth, Newcastle City Council has been forced to become more entrepreneurial and move beyond the default position of looking to central government for resources. Newcastle's Accelerated Development Zone (ADZ) project (Newcastle Gateshead, 2011), which incorporates TIF, is a key example of such a response.

It is not just local authorities that have suffered in wake of the financial crisis. The central government too has initiated a harsh programme of spending cuts in order to pursue deficit reduction. As part of this strategy, the UK's central government is distributing increasing levels of financial responsibility to local levels of government. Although the devolution of financial power, which is presented as part of the ‘localism agenda’, remains largely rhetorical, instruments like TIF provide genuine opportunities for increased financial autonomy for local authorities and reduced dependence on the centre. One of the primary mechanisms for the devolution of financial power in the UK, for instance, which is of particular importance to TIF, has been the localisation of business rates. This phase of devolution, however, should also be recognised as part of the broader, long-term and ‘multi-dimensional process of state restructuring and re-scaling whereby state functions are being re-organised and re-located between national, supra-national and sub-national levels’, and transferred to private and quasi-public organisations (MacKinnon, 2000: 294). These processes have driven the increasing participation of private actors and international investors in the development of cities, and have necessitated more innovative and entrepreneurial modes of infrastructure provision (O'Neill, 2010). In the UK, emerging mechanisms for funding urban development include municipal bonds, public-private partnerships, local asset backed vehicles, accelerated development zones and TIF (Symons, 2011).

The geographies of risk and the risks of financialisation

Financial risk is geographical in nature; it varies depending on the size and scale of financial markets, is shaped by the type of financial mechanisms and products involved, and is uniquely influenced by place (Clark et al., 2009). The way that risk is constructed, perceived, evaluated and managed is also crucial, and equally variable (Randalls, 2009). Because of the economic climate and the geographical characteristics of a city like Newcastle upon Tyne, the concern is that the opportunities of using new financialised mechanisms exist alongside a number of potentially harmful risks.

Key factors creating more risk for urban development in Newcastle upon Tyne, and other cities outside of England's economic core, include an historically low resilience to economic crises and shocks, and historically low levels of economic recovery (Martin, 2012); low levels of inward investment from both domestic and international sources (BIS, 2012); low gross value added in comparison with the UK's core (BIS, 2012); and, crucially, low non-domestic rateable values, which also increase at comparatively low rates (DCLG, 2009; Valuation Office Agency, 2011).

Financial risk is heightened in cities which have weaker economies, but also those which have engaged in financialised modes of development: for instance, those which have financed landmark urban developments and basic services by entering an uncontrollable borrowing cycle, necessitated by ever increasing debt obligations and repayment demands. In the wake of the global financial crisis, some of the United States’ most financialised municipalities have been forced to declare bankruptcy, such as Vallejo in San Francisco (Dickerson, 2009), while others have suffered ‘declining credit ratings’, ‘restricted access to financial markets’ (Kirkpatrick and Smith, 2011: 477), ‘decreasing revenues’ and ‘increasing costs of borrowing’ (Weinstein, 2009: 271).

Most of the problems suffered by municipalities in the US are not directly related to TIF, as it is common for TIF schemes in the US to operate within some form of bankruptcy-remote entity, to represent a small proportion of a municipality’s overall debt, or for municipalities to be able to levy taxes from other sources to service the TIF debt (O'Toole, 2011). That is not to say that defaults on TIF bond repayments are unheard of (see Devitt, 2012, on Troy Downtown Development Authority). Instead, underpinning instances of severe fiscal distress in US municipalities, are the deep-rooted contradictions in financing development through debt. These contradictions, also exposed under different macroeconomic conditions (see Baldassare, 1998), indicate that financialised development tools pose a significant risk to the economic stability of cities and, as a result, that local authorities contemplating TIF should consider precautions to avoid and deal with fiscal stress and crisis. This is perhaps more important in the UK, given the large scale of some proposed TIF schemes, the limited ability of local authorities to levy taxes from other sources, and the direct linkage between a TIF scheme and the balance sheet of a local authority.

Despite the potential hazards, financialised development mechanisms remain a credible policy option because of their ability to stimulate increased wealth, productivity and economic growth. That is, ‘the ability to create and monetise new asset classes’ (Weber, 2010: 253), through the use of instruments such as TIF, can be a competitive way of funding basic services or pursuing groundbreaking development projects.

Financialised development tools: A geographical dilemma

The need to respond to the negative impacts of the financial crisis on local economies, coupled with the movement towards the devolution of financial power and responsibility to the local level, is forcing local governments to engage in a more entrepreneurial form of policy (Harvey, 1989). New mechanisms for funding development, such as TIF, fit this mould. Financialised development mechanisms, however, are innately speculative and risky (Weber, 2010). Despite the risks, there appears to be no option but for governing authorities to engage in these mechanisms, primarily due to a lack of viable alternatives. Thus, a tension for policy makers is created. For places in underperforming regions this tension is amplified; the heightened need for growth, employment, renewal and competitiveness exists in contrast to the higher risk of scheme failure, bankruptcy, instability and disempowerment.

Tax Increment Financing: A financialised development tool

Making sense of Tax Increment Financing

TIF has the potential to be an effective tool to fund infrastructure in UK cities. This section argues that although TIF can ignite economic growth, it might also act to reinforce the UK's geographies of uneven development.

The proposed TIF model for use in the UK is largely based on the original US concept: A territorial district is created within a city, and the assessed valuation of the property within the district – known as the base value – is determined. Property taxes continue to be levied, and the revenues generated by applying the tax rate to the base value continue to be paid … But revenues generated from applying the property tax to any increased property value within the district are, for the life of the district, set aside and paid to the municipality … to be used for public improvements and other economic development programs within the district. (Briffault, 2010: 67).

After a TIF zone has been established, an investment in public improvements takes place – usually in a piece of physical infrastructure. This public investment is followed by a number of investments by private sector actors, which have become feasible as a consequence of the initial public investment. In the US, the main purpose of the public investment is to increase economic activity within the TIF zone and, as such, to trigger an increase in the value of commercial properties within the zone (Smith, 2006). The increase in property value is vital to the scheme's success, because it increases the level of property tax payable within the zone (although the tax rate remains the same) (Byrne, 2006). The increase in tax revenue – ‘the tax increment’ – underpins the whole TIF project, because it is used to cover the costs of the initial public improvements made in the district (Mason and Thomas, 2010: 169). In the UK, although commercial property taxes are based on rental value, the objective is essentially the same.

The tax increment can either be used to pay for infrastructure as additional revenues come in – on a ‘pay-as-you-go’ basis (Briffault, 2010: 68), or they can be borrowed against in advance (Weber, 2010), allowing a large initial investment in infrastructure to take place, which is then paid off over the duration of the scheme as the incremental revenues arrive. That is, through TIF, public improvements can be ‘built now and paid for later out of borrowed funds secured by the anticipated tax increment’ (Lefcoe, 2011: 7).

Specifically, the tax increment is used to repay the scheme's financiers and any interest that had accumulated on the debt package. In short, the TIF administrator is able to ‘transform promises of future tax revenues into securities’ which can be traded on the global financial markets and borrowed against by the TIF administrator (Weber, 2010: 254). This is what makes TIF a unique and truly financialised development tool. Crucially, the proliferation of TIF is a demonstration of how the pursuit of financially innovative strategies is becoming one of the ‘principal features of contemporary local government’ (Briffault, 2010: 66).

Exporting Tax Increment Financing to the UK

In the UK, TIF is emerging at the same time that there is a scarcity of public sector funds across the board. It is no coincidence that a serious discussion about the local retention of business rates and their use in funding development projects has only emerged since the start of the current financial crisis, even though there have been proposals to use TIF in the UK from as early as 1999 (Urban Task Force, 1999). Because of its timely emergence, there is a danger that TIF could be perceived as a tool for propping up the balance sheet of public sector organisations and for maintaining service provision, rather than being used for its primary purpose of stimulating investment in infrastructure. That being said, these issues are clearly interlinked to a certain extent. Furthermore, even though TIF is designed to be an isolated mechanism for instigating a specific development project, its evolution in the UK context cannot be explained without reference to the economic environment after the fallout of the financial crisis and the broader policies of localism and devolution being pursued by central government.

Indeed, TIF is defined by its characteristics as a tool which enables local authorities to benefit from the local retention of non-domestic rates (or ‘business rates’) (Core Cities Group and PricewaterhouseCoopers, 2008). Business rates are taxes payable on non-domestic properties and are calculated according to the annual rental value of the property (HM Government, 2009; Valuation Office Agency, 2012). Although the degree of genuine devolution incorporated into the Localism Act (HM Government, 2011a) is contested (Jones and Stewart, 2012), the local retention of business rates represents a foundation from which local authorities can begin to harness power and autonomy for themselves, by using schemes like TIF to improve their economies and to reinstate their independence.

Local authorities in the UK have been presented with two opportunities to engage in TIF schemes by central government. First, they can engage in ‘option one’, which would enable them to borrow against future business rate revenues, but which subjects the available business rate revenues to the standard levy and reset regulations that apply more broadly to the local retention of business rates (DCLG, 2011: 35). Second, local authorities can engage in ‘option two’, which bypasses the levy and reset regulations (DCLG, 2011: 35), and which can be viewed as a similar mechanism to the traditional American model of TIF.

The ability of local authorities to actually commence a TIF scheme, however, is limited and requires a considerable amount dialogue between a local authority and central government, which is codified in the form of a ‘City Deal’ (HM Government, 2011b). As a result of the somewhat laborious and occasionally one-sided conversation between central and local government, which could even be likened to a traditional bidding process, the cities of Newcastle, Sheffield and Nottingham have developed plans for TIF schemes and are in the initial stages of implementation (Newcastle City Council, 2012; Nottingham City Council, 2012; Sheffield City Region, 2012).

Although the model of TIF in the UK is not an exact replica of the traditional American version, is far less dependent on investment from financial institutions and private investors, and is underwritten (albeit implicitly) by the weight of the British government, TIF in the UK is highly connected to the logic of financialised capitalism. As a consequence, the uneven geographies of investment, development and economic growth are reinforced through the introduction of TIF to the UK.

TIF can be considered as a financialised development tool for several key reasons. Primarily, TIF depends on a considerable increase in the average rental value within the TIF district. In some respects, increasing rental values are an inevitable consequence of the development of new infrastructure and commercial property, particularly when the original base level of the rental value within the district is negligible. However, the recent subprime crisis has demonstrated that even when increases in asset and rental values seem inevitable, they can prove to be illusive. Furthermore, local authorities are required to adopt a substantial amount of debt in order to invest sufficiently in the initial stages of the TIF project. High levels of debt mean that the failure of a TIF scheme could be more damaging to the local economy.

Even though local authorities are unlikely to borrow directly from the markets to fund a TIF scheme, and instead would typically look to borrow from the PWLB, there is a connection between the cost of borrowing for local authorities and the ebbs and flows of global financial markets. This is because the rate at which local authorities borrow from the PWLB is directly linked to the price of Treasury Gilts (Debt Management Office, 2012). Thus, in a TIF scheme, it is crucial to account for variable borrowing costs, as well as variable levels of business rate revenue. Similarly, private developers are dependent on the availability of affordable funds in order to make necessary investments in the development project. If the markets are unwilling to lend or will only lend at a particular rate, the TIF scheme, regardless of success of the public sector investment, is likely to fail.

Tax Increment Financing's prerequisites: A ‘blighted’ area, or a strong economy?

Because a TIF project requires a significant investment to come from the private sector before incremental revenues can arrive, it is essential that there is a high level of economic potential in a particular area, simply waiting to be unlocked by the initial public intervention. Indeed, TIF does not have the ability to create new markets. As such, it is arguable that only a handful of cities have the capacity to implement a TIF project in the UK. Not only does an investment have to be profitable for private enterprise, but it must also result in increases in broader economic activity and rental value, creating an additional layer of risk. The inclination to implement TIF in places that are more likely to achieve these requirements contrasts with the notion that TIF should target a ‘blighted’ area (Smith, 2009: 210).

The case of Newcastle upon Tyne serves to illustrate some of these potential issues. One the one hand, it has a reasonably strong economic base, which prior to 2007 experienced particularly high levels of employment growth when compared to other English cities outside of London. On the other hand, it faces some key challenges, particularly in the development of commercial property (Newcastle City Council, 2011: 6).

Although it can be used for stimulating development in truly blighted areas, TIF would appear to be geographically selective, favouring more economically productive areas. As such, rather than addressing the need for investment in infrastructure and development in weaker economies, the legacy of TIF could be to reinforce the peripherality of some cities and localities with already underperforming economies. The increasing economic pressure on cities, however, could mean that TIF is introduced in cases where its ability to succeed is marginal and where the risks of this financialised mechanism are higher, with potentially hazardous results.

Assessing the risks: Is Tax Increment Financing a suitable tool for Newcastle upon Tyne?

This section analyses whether Tax Increment Financing (TIF) could be used as a tool for development in Newcastle upon Tyne. It is important to note that Newcastle City Council, in partnership with Gateshead City Council, is currently in the process of developing an ADZ, which uses TIF to fund development activities. Whilst this section does not seek to provide a case for or against the implementation of Newcastle's ADZ, it identifies some key issues, dilemmas and opportunities that will necessarily be at the centre of the Council's strategy.

Taxation, completion and valuation risk

TIF has the potential to increase competitiveness and accelerate economic development. Indeed, avoiding such a strategy could be damaging for the competitiveness of a city like Newcastle. The risks at the heart of TIF, however, make it a potentially hazardous tool, particularly in peripheral and underperforming places. The primary risk in a TIF scheme is that the incremental value will not be high enough to repay the initial borrowing for the scheme. Weber (2010: 260) highlights ‘completion risk’, ‘valuation risk’ and ‘taxation risk’ as three categories underpinning this risk.

Taxation risk is more pronounced in the US, but could apply to the UK, for instance, if the Government decided to change any of the legislation around the retention of business rates, such as the hotly debated reset period (DCLG, 2011).

Completion risk and valuation risk are pivotal in the adoption of a TIF scheme in a city like Newcastle. Completion risk is the possibility that the planned developments are never built or are completed late and thus the anticipated revenues, needed to service the debt, are not generated.

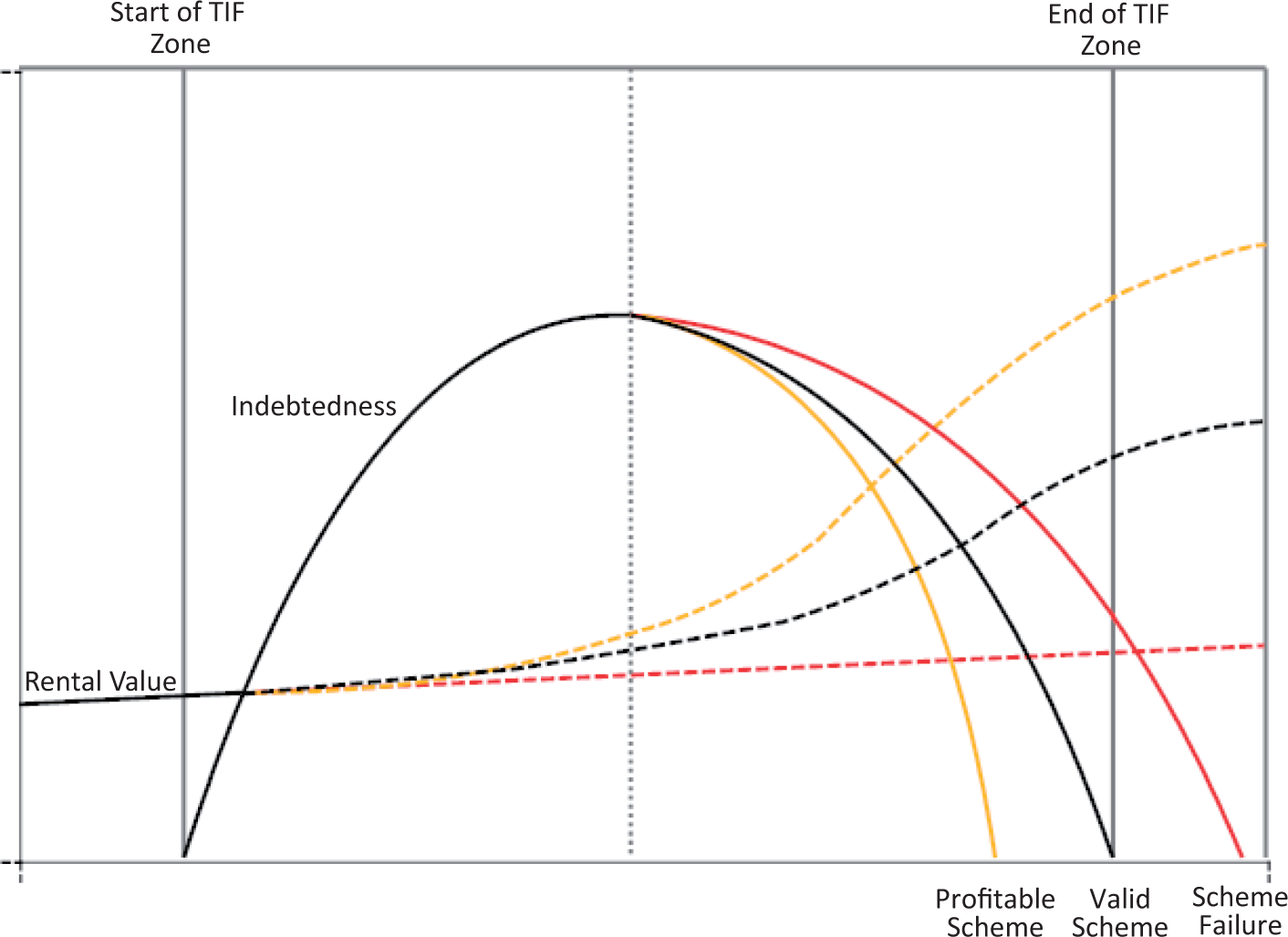

Valuation risk is the potential failure to generate sufficient revenues to repay the scheme's financiers, due errors in calculating the ‘base value’ of the TIF zone, failing to accurately predict the ‘incremental value’, and failing to stay on budget. These risks are illustrated by Figure 1. Because business rate income, the source of the incremental value, depends on the rental value of commercial property, insufficient growth in commercial property value would leave the local authority in a position where it could not service its debt. Ultimately, unless every aspect of the project can be linked with every penny of revenue, the level of risk becomes extremely high.

An illustration of the relationship between property value growth and the success of a Tax Increment Financing Scheme.

‘Pay-as-you-go’: Risk aversion comes at a price

It is possible for local authorities to transfer risk by encouraging private sector organisations to play a larger role in TIF. Private developers could engage in the majority of borrowing needed to fund the infrastructure in the TIF scheme, and then be paid at a premium rate by the local authority for doing so, using a portion of the future incremental revenues. In such a case, even on the complete failure of the scheme, the local authority would have no debt obligations. Once again, when defining the role of the private sector, it is important to distinguish between the US case, where developers can sometimes obtain direct access to TIF revenues providing that they fulfil particular criteria, and the UK case, where it would be politically unpalatable to channel tax revenues directly towards private enterprises. The primary role for a pay-as-you-go approach in the UK, then, would be to transfer risk to the private sector by placing the emphasis on developers to undertake a large proportion of the scheme's borrowing.

In areas with a stagnant economy, however, it is possible that developers would view such a financial burden on themselves as too risky. For Newcastle upon Tyne, a city in a region which, in spite of some very positive recent increases in private sector growth and job creation, has historically suffered from low levels of private investment (Pike, 2006; Wray et al., 2010), this is problematic. The pay-as-you-go model is certainly less attractive for developers than the model in which the local authority pays for the infrastructure through debt finance. In a peripheral economy, such as Newcastle upon Tyne, where there is no market for certain types of development, the pay-as-you-go model would not incentivise a developer to invest, because the developer's revenue streams would be uncertain.

Alternatively, when key infrastructure is paid for through public sector debt, investing in the TIF zone would be more attractive for developers. The developer would still face its regular investment risks, but thereafter, in the public sector debt model, is not dependent on the increase in property value across the TIF zone.

On the one hand, then, Newcastle City Council could pursue a safe strategy, avoiding highly leveraged projects and instead opting for a pay-as-you-go TIF scheme, but risk that there might not be enough private sector demand for the development to be viable. On the other hand, the city authority could pursue a more aggressive strategy, which involves the adoption of high levels of debt, and which has a far greater potential of sparking economic activity and creating a competitive edge. Indeed, according to Newcastle City Council, TIF offers ‘a viable and cost effective solution to address existing barriers to development’ such as ‘[t]he requirement for significant up-front enabling infrastructure investment’, ‘[v]iability gaps’, ‘[c]onstraints in development finance markets’ and a ‘lack of alternative public funding sources’ (NewcastleGateshead, 2011). If this type of scheme failed, however, there would inevitably be significant consequences for the city, such as public sector spending reductions, job cuts and council tax increases.

This tension is particularly evident in the context of Newcastle's peripheral economy. If TIF is going to be used in Newcastle upon Tyne, then it is crucial that measures are taken to reduce the tensions that lie at the mechanism’s heart. It is important to stress that in making TIF part of their ADZ scheme, Newcastle City Council are taking a thorough approach to minimising levels of risk, through the use of prudent assumptions on business rate growth, and by matching – as far as possible – the repayment profile with the likely business rate profile. Their proposed scheme is calculated to return business rate revenues well in excess of the total financial costs of the infrastructure.

Making Tax Increment Financing viable: Policy recommendations

This section highlights a number of ways in which public sector risk can be mitigated, whilst maintaining the economic viability of a TIF scheme for investors and private sector actors. De-risking remains an essential practice because it minimises the possibility of scheme failure and ensures that economic development and growth can take place.

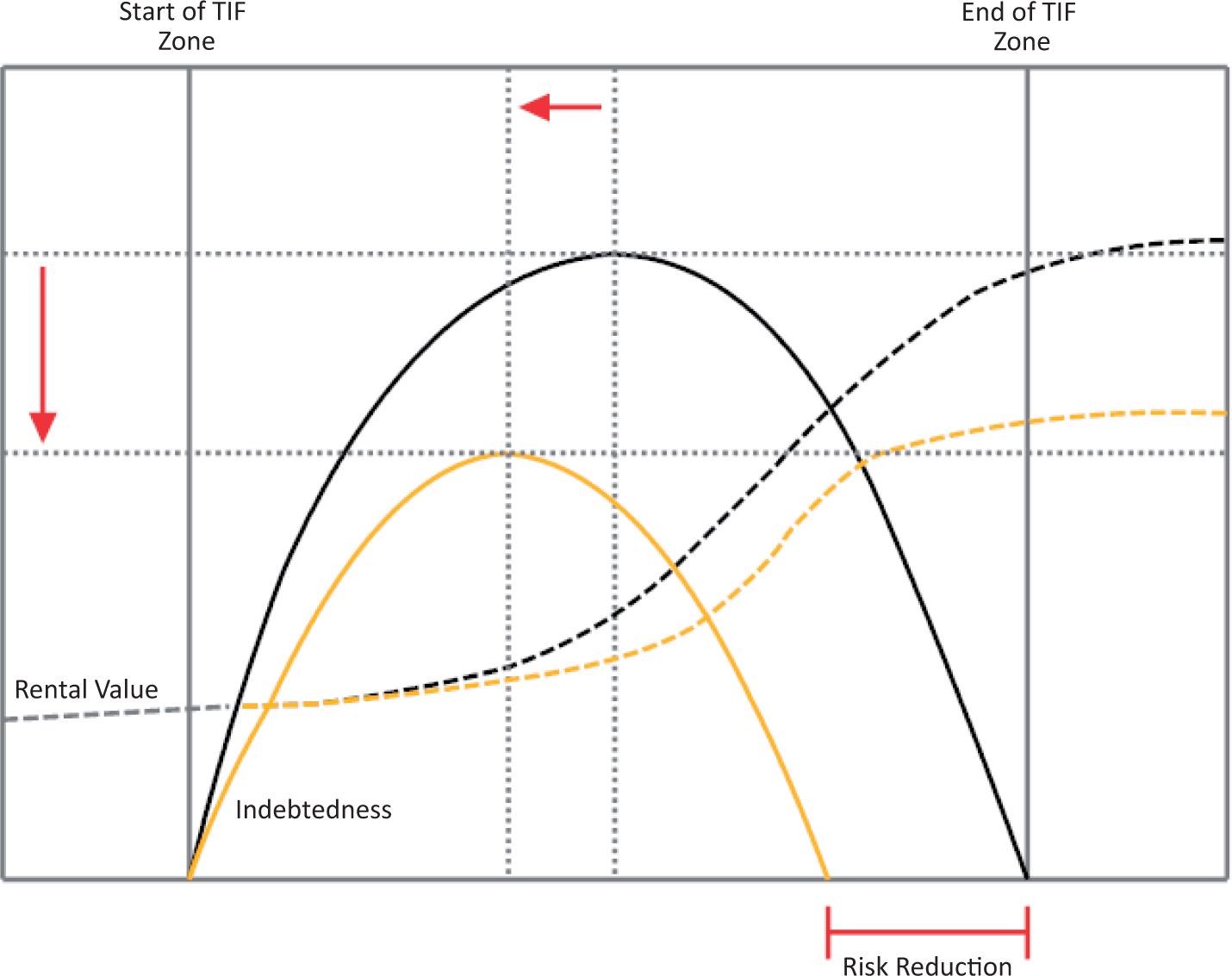

Valuation risk, the possibility that the TIF administrator ‘may overestimate property value growth’ (Weber, 2010: 260), cannot simply be mitigated by improving forecasting accuracy. More practicable solutions are required, such as reducing a scheme’s leverage, shortening the repayment profile and increasing a scheme’s duration. These measures can also mitigate completion risk – the possibility that the infrastructure underpinning the growth in rental value will not get built in time.

It is possible for a TIF administrator to reduce risk by borrowing a significantly lower level of capital than the scheme is anticipated to generate in the form of incremental revenue streams, by reducing the loan-to-value ratio, and by repaying the debt earlier. These measures would ensure that there is a positive net present value in the scheme. Figure 2 shows that by reducing the total level of indebtedness and bringing forward the repayment schedule, a significant risk reduction can be made.

Managing risk by reducing indebtedness and shortening completion period.

Borrowing less money and repaying the debt earlier, however, means that the infrastructure has to be less expensive and on a smaller scale. It is probable, therefore, that the risk mitigation measures would come at the expense of any large profit beyond the revenues required to repay the debt. Nevertheless, schemes that minimise risk would provide a city like Newcastle with the opportunity to engage in a public sector debt model of TIF, whilst still maintaining a degree of certainty that it will not lead to over-indebtedness and default.

Newcastle City Council, for example, has calculated that its ADZ scheme would remain viable even if there is a 40% reduction in business rate revenues generated by the development activities (Newcastle Gateshead, 2011). The Council also aims to transfer as much risk to the private sector as possible, through measures such as agreeing a fixed price for contracts, securing commitments around minimum volumes of floorspace, and negotiating underwriting agreements and clawback arrangements (NewcastleGateshead, 2011).

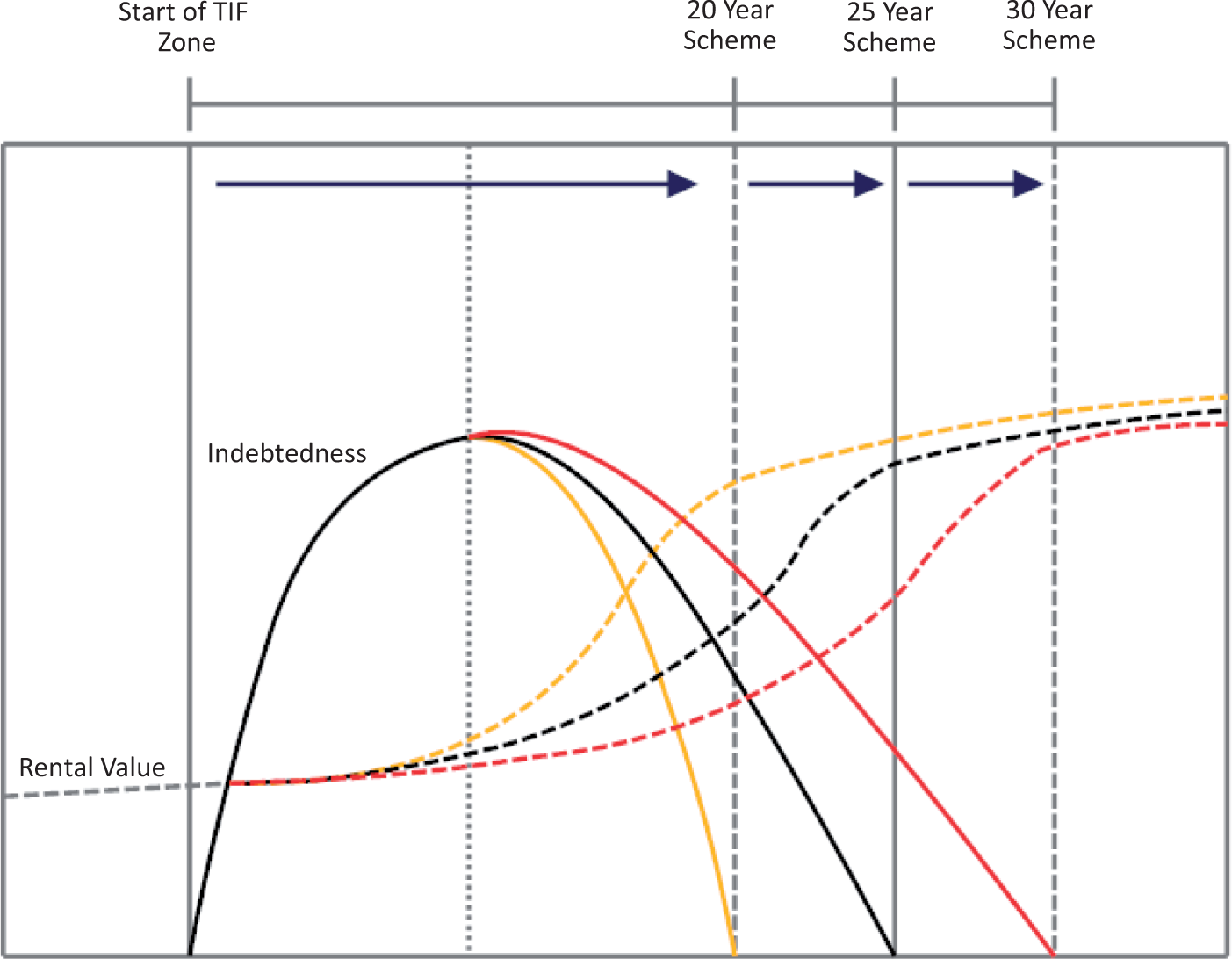

When the infrastructure cost is high and the completion cannot be brought forward, another de-risking strategy is required. In such an instance, TIF could be made viable by increasing the duration of the scheme (see Figure 3). That is, a city authority might consider a 30-year scheme instead of the typical 25-year scheme. In a more dynamic economic environment, the scheme duration could even be reduced. A downside is that the total interest payments on a longer scheme could be higher.

Increasing a scheme’s duration: realising TIF’s full potential while managing risk.

Conclusion

TIF is a ‘financialized’ mechanism which allows local government authorities to borrow against anticipated future revenue streams in order to fund infrastructure (Weber, 2010: 258). Financialised tools for development, however, can be ‘speculative and high-risk’ (Kirkpatrick and Smith, 2011: 489). Local government authorities face a dilemma, therefore, in that they can engage in a TIF scheme and face the risks of default and over-indebtedness, or avoid financialised mechanisms but fall behind in a world characterised by intense inter-urban competition.

Crucially, the risks of engaging in financialised development mechanisms, such as TIF, are geographically uneven. Places with economies that are most in need of an economic stimulus and a new competitive advantage, are also the places where property and rental value growth is uncertain. In contrast, prosperous and growing economies can be more certain of future property value growth, on which the debt repayment programme depends. Financialised mechanisms, such as TIF, therefore, inevitably serve to reinforce the geographies of uneven development.

TIF schemes can be made less risky. A pay-as-you-go model of TIF could reduce substantially the riskiness of TIF for local authorities. In an underperforming city, however, the additional investment risks could affect a TIF scheme’s viability and repel private developers. Pay-as-you-go schemes function best in prosperous and growing cities, and thus underline the geographical unevenness of TIF.

In a city with a weaker economy, adopting the public sector debt model of TIF is arguably more feasible. Problematically, this type of scheme carries more risk for the public sector. However, it can be modified to mitigate some risk, by reducing levels of borrowing and bringing forward the infrastructure completion date, and by increasing the duration of a TIF scheme. Indeed, Newcastle City Council are demonstrating that TIF schemes can be successful even in challenging economic circumstances, through the adoption of a prudent borrowing framework and by targeting a revenue stream that is considerably higher than the financial costs of the urban development project.

Given the increasing financial pressures on all levels of government, there is a danger that local authorities could be forced to engage in financialised tools like TIF, in instances where they are inappropriate. The tension facing some local authorities, particularly in underperforming and peripheral places, is whether to accept the risks of financialised mechanisms and adapt to them accordingly, or to face continued economic underperformance. This also raises broader questions about the role of local authorities moving forward, the power and autonomy they should have, and the extent to which they are becoming more independent and proactive on the one hand, or more confined and isolated on the other.

Footnotes

Funding

This research received no specific grant from any funding agency in the public, commercial or not-for-profit sectors.