Abstract

Regional economies are shaped by their economic histories and existing endowments. This paper explores the question: how do a region’s economic history and institutional endowments affect its success and trajectory in an emerging industry? Our case, electric vehicle development and production, is an industry which combines more traditional skilled manufacturing with knowledge-driven innovation activities. We present deep qualitative case studies of two regions, focusing on one firm in each. The case of Tesla in the San Francisco Bay Area examines an electric vehicle firm in a region with a strong tech innovation system, while the case of Maserati in Emilia-Romagna, Italy, examines a firm that builds on a regional history of automotive manufacturing. Across cases, we compare regional skill endowments, institutional coordination, and place-based policymaking. We conclude that, as an emerging industry under a new economic paradigm, electric vehicle manufacturing by Tesla and Maserati represents two different conceptions of the industry and consequently two different location strategies. Yet these two strategies remain rooted in regional contexts, owing both their success to successful exploitations of these, and their struggles to their failure to compensate for regional gaps. This presents a clear opportunity for place-based industrial strategy to evolve and intervene.

Keywords

Introduction

Regional economies are shaped by their institutional endowments and economic histories, and this extends from the regional to the firm level in mutually reinforcing ways. A region’s economic success in a certain cluster depends on its ability to generate, attract, and host firms in a certain sector; likewise, a firm’s success in a region is influenced by the institutions that are present. A region’s economic history shapes the institutions that emerge as well as those that persist.

This is especially the case for regions and firms that rely on innovative activity for their economic success. An extensive literature on regional innovation connects firms’ success to regional institutional contexts. Although there is a rich and sometimes diverging set of theoretical explanations for why regional contexts matter to innovation, conclusions center the importance of knowledge sharing to innovation, and the importance of proximity and institutional facilitators to knowledge sharing (Baptista, 2000; Bell, 2005; Bell and Albu, 1999; Moulaert and Sekia, 2003). The advent of advanced manufacturing, including the incorporation of smart technology, has reinforced the role of regional contexts. Given the challenges of industrial reorganization, advanced manufacturing has disproportionately concentrated in a few regions (Andreoni, 2018; Birkel and Hartmann, 2019; Ciffolilli and Muscio, 2018; Tassey, 2014; Tiraboschi and Seghezzi, 2016).

The powerful influence of regional context creates particular challenges for designing place-based industrial policy at the regional level, the topic of this paper. Attempts to intervene at the regional level—defined based on boundaries of political and administrative control—in economic development policy are growing, and the notion of openly targeting sectors or technologies is coming back into political vogue in both the United States and Europe (Andreoni et al., 2019; Block, 2008; Chang and Andreoni, 2020; Di Tommaso, 2020; Di Tommaso and Schweitzer, 2013; Di Tommaso et al., 2019, 2020a, 2020b; Stiglitz et al., 2013). As increasing disparities among regions threaten political, social, and economic stability, countries see place-based policies as critical to lift up regional economies (Iammarino et al., 2019; Rodríguez-Pose, 2018). Yet it is unclear how effective place-based approaches will be for emerging industries.

Thus, we ask: How much, and in what ways, do a region’s institutional endowments and economic history affect its success in a new industry? How can place-based industrial policy intervene to support the growth of new and emerging industries? We approach these questions by examining electric vehicle (EV) development and production, an emerging industry that combines traditional skilled manufacturing with knowledge-driven innovation activities. Drawing on the methodological approach of studying regional economies through the study of prototypical firms, we compare two contrasting cases of firms focusing primarily on luxury EV production (Markusen, 1994). The case of Tesla Motors is a relatively new and highly innovative EV firm, founded and based in the San Francisco Bay Area, a region with a strong technology-oriented regional innovation system but little auto manufacturing. The case of Maserati, an established auto manufacturer based in the Northern Italy region of Emilia-Romagna, provides an example of a traditional auto firm expanding to EVs in a region with a deep history of auto manufacturing and mechanics, but relatively little innovation capacity in electronics and ITs. The regions differ in both economic history and policy context: Tesla emerged largely in the absence of formal industrial policy (excepting tax credits), while Maserati benefits from Emilia-Romagna’s institutional thickness, generated in part by industrial policy.

We use mixed methods to examine these questions. To describe regional economic competitiveness, we analyze data on firms, occupations, trade flows, and productivity (with variations across the two cases due to data availability). Data on EV manufacturers’ locations came from trade publications and firm websites. Description of the firms comes from archival research, including academic articles and popular press, and interviews. In the Bay Area, we conducted five semi-structured interviews with private and public sector informants familiar with Tesla, its home city of Fremont, and Silicon Valley. For the Emilia-Romagna case, we built upon literature and direct data from automotive companies, and conducted semi-structured interviews with public sector informants from Attractiveness Research Territory, the Emilia-Romagna Joint Stock Consortium.

We begin with a discussion of literature on evolutionary economic development, regional innovation systems, and the role of labor supply in industries’ location decisions. We present an overview of the global automobile industry and how its location patterns reflect this literature’s findings. Our two cases are presented individually, with a discussion of each region’s economic history and endowments, the firm’s history and strategic approach, and the firm’s interaction with their region. We conclude with comparative analysis of the two, focusing on how regional economic histories, the regional skill endowment, and institutional coordination have shaped these firms’ strategic approaches, successes and failures, and their implications for the development of place-based industrial policy.

Path dependence and the automobile industry

Economic history, path dependence, and evolutionary economic development

The concept of path dependence describes how certain events can lead to specific pathways of development through self-reinforcement (David, 1985), and can be applied to regional planning and economic geography (Amin and Thrift, 1995). For example, a region’s historical specialization in a certain industry may lead to public and private investments in infrastructure around that industry, and the development and persistence of political, economic, and social institutions appropriate to that industry and its workers (Hassink, 2005; Martin, 2009). These investments and institutions thus reinforce the region’s existing path.

A new development path might evolve out of an existing one; as an example, Boschma and Wenting (2007) find that a thriving bicycle industry in early 1900s Coventry, UK “laid the foundations” for an eventual concentration and success of the automotive industry in the region. But development paths can also disincentivize or prevent a region from reorienting its economic development along a different path, “locking in” particular approaches. Path dependence can thus be interpreted as a place-dependent process (Martin and Sunley, 2006).

Regional innovation systems and regional embeddedness

The economic benefits to firms of agglomeration have been recognized since Marshall’s observations of localization scale economies in the 1920s, in which he noted that firm co-location in the same industry generated shared positive externalities (Marshall, 1930; Van der Panne, 2004). Regional innovation literature argues that firms in highly innovative industries derive particular benefits from co-locating with other innovative firms and institutions (Cooke et al., 1998; Malmberg and Maskell, 1997). In addition to Marshallian externalities like shared labor pools and knowledge exchange, innovative firms benefit immensely from physical proximity at the regional level because it specifically facilitates the exchange of tacit or non-codifiable knowledge and information (versus explicit knowledge), which is increasingly essential to innovation in knowledge-intensive industries and is a source of competitive advantage in global markets (Asheim and Gertler, 2005; Becattini, 1991; Maskell and Malmberg, 1999; Storper, 1995).

Regional innovation systems literature theorizes that formal and informal institutions, including scientific, political, industrial, and intermediary organizations, make up a dynamic environment at the regional level which significantly influences the innovative success of firms and regions (Cooke et al., 1998; Dei Ottati, 1994; Lundvall, 1988). Regional innovation systems emphasize the embeddedness of these institutions—private finance, universities, laboratories, and vocational-training competencies that have close local ties are all identified as indicators of strong regional innovation systems. The importance of embeddedness also extends to firms themselves, which must integrate themselves within their regional innovative system in order to capture the locational advantages (Kramer and Revilla-Diez, 2012; Mattes, 2013). The extent of a firm’s integration into its regional innovation system has significant effects upon that firm’s innovative success.

Labor and space

With the ascendance of knowledge-based industries, there is increasing focus around the world on the need to train and retain a skilled workforce, even in manufacturing. This focus on human capital in information and communications technology (ICT) has altered the spatial division of labor described by Massey (1984), in which peripheral regions become production zones for industries that are controlled almost entirely from central regions. If human capital is now more important in production work, then location strategies of firms and corresponding regional development will evolve to reflect this, and the spatial division of labor will change.

The automotive industry and its location patterns

The automotive industry has roots in both Europe and the US, with significant inroads made by Japanese automakers into global markets in the 1970s (Holweg and Oliver, 2015). During the 1970s and 1980s, automobile manufacturers began consolidating and decentralizing operations, concentrating their research and development (R&D) activities in central locations, and moving manufacturing and production to peripheral regions with lower labor costs (Bordenave and Lung, 1996; Lechner and Dowling, 2003; Schoenberger, 1987). Foreign producers simultaneously opened production plants overseas to reduce transportation costs for the final product (Klier and McMillen, 2006).

In the US, the automobile industry has historically concentrated in the greater Detroit, Michigan region, aided by local agglomeration economies (Klepper, 2007). Headquarters and R&D have remained there, though production functions have been moved overseas or to peripheral regions of the US. Between the late 1970s and the mid-2000s, Michigan lost over a third of auto industry employment, while southern states’ auto industry employment tripled. Foreign-owned auto firms, particularly Japanese firms, also began opening assembly and production operations in the US South (Klier and McMillen, 2006).

In Europe, the auto industry has traditionally concentrated in certain regions of Germany, the UK, France, and Italy, often referred to as the “Blue Banana,” both for innovation and production. However, the European auto industry experienced a similar transformation at the end of the 20th century due to the saturation of local markets and resulting stagnation, and the emergence of new countries as both production sites and new markets (Berta and Ciravegna, 2006; Lung, 2000; Volpato and Zirpoli, 2011). Auto production consequently decreased in the Blue Banana as original equipment manufacturers shifted their production to Spain and Eastern Europe in search of cost advantages (Bordenave and Lung, 1996; Humphrey and Memedovic, 2003; Pavlínek, 2012). In Italy, traditional manufacturing regions such as Piedmont (Fiat) and the southern areas have generally seen declines. Emilia-Romagna, which specialized in luxury and sports cars and developed a local supplier pool, resisted this shift.

In the past two decades, these shifts have been complicated by the growth of new markets and the emergence of new producers in Asia, with China and India in particular joining Japan as new sources of supply and demand.

The decline of manufacturing in the US and parts of Europe has been the dominant narrative, as the economic paradigm has shifted from Fordist/mass production organization to one based on ICT and automation. However, this has been a decline in terms of employment, rather than in productivity. While the number of jobs in manufacturing has dropped in the U.S. and Western Europe, the productivity of the manufacturing sector has increased (Kowalski, 2014). The types of jobs and the skills demanded in manufacturing have changed to reflect this technological and organizational shift, with literature identifying and investigating “advanced manufacturing,” or manufacturing in which computer and automation technology, flexibility, and integration with services play a significant role (Muro et al., 2015; NSTC, 2012; Tassey, 2014). This evolution blurs the lines between some forms of manufacturing and other industries. For example, Schulze et al. (2015) argue that the technologies used in mobility industries and consumer electronics industries are increasingly convergent. Such changes in the skill content of production would then shift spatial divisions of labor that traditionally separated production functions from research and control functions (Massey, 1984).

Furthermore, it is increasingly theorized that the current economic paradigm, characterized by a shift from manufacturing to services and the increased prominence of ICT, is giving way to a new one. In the new paradigm, the development and implementation of networked technologies that learn, communicate, and self-monitor defines economic growth and organization, and manufacturing processes continue to shift in form. Although these definitions are not interchangeable, the literature, theory and policy on “Industry 4.0,” the industrial “Internet of Things,” and “smart factories” all pertain to new or anticipated changes in how, where, to what extent, and with what characteristics manufacturing will take place. However, in contrast to the proliferation of studies on the integration of innovation and production in industries like life sciences and nanotechnology, attempts to empirically study these changes to manufacturing and their implications for spatial, social, and economic policy are only just emerging (Ciffolilli and Muscio, 2018).

Place-based industrial policy

Interest in place-based industrial policy stems in part from the regional economic divergence of the early 21st century (Rodríguez-Pose, 2018). As an example, the European Union’s emphasis on “smart specialization” strategies in RIS3 incentivizes regions to specialize in industries in which they can, in theory, develop a unique and distinctive advantage that builds on their existing strengths and capabilities (Crespo et al., 2017). Smart specialization assumes that path dependence plays an important role and that regional context matters immensely to both firms’ outcomes and policy effectiveness (Barbieri et al., 2019; Boschma, 2015; McCann and Ortega-Argilés, 2015; Monga, 2013). Despite the lack of comparable industrial policy in the U.S., the EV industry has benefited extensively from federal and state tax credits incentivizing consumers to buy new vehicles. Though these are not explicitly place-based, they do have specific impacts on the places where EV production is concentrated.

Despite the interest in regional place-based policies, there remains a lack of research and theory that can inform how, why, and what interventions will succeed (Bailey et al., 2015; Barbieri et al., 2020; Barca et al., 2012; Di Tommaso et al., 2017, 2020a; Foray et al., 2011). This is particularly the case for emerging industries that reflect the continued transformation of the economy.

The EV industry as a case

The EV industry has emerged only recently, growing from 50,000 total plug-in light EVs sold globally in 2011 to 2 million sold in 2018 (IEA, 2019; US OEE: United States Office of Energy Efficiency and Renewable Energy, 2016). EV development and manufacturing have been undertaken both by new firms focusing primarily upon EVs, such as Tesla, and large automotive firms looking to pivot in the face of rising concerns about global climate change and growing market interest in electric options, such as Chevrolet, Fiat-Chrysler, or BMW.

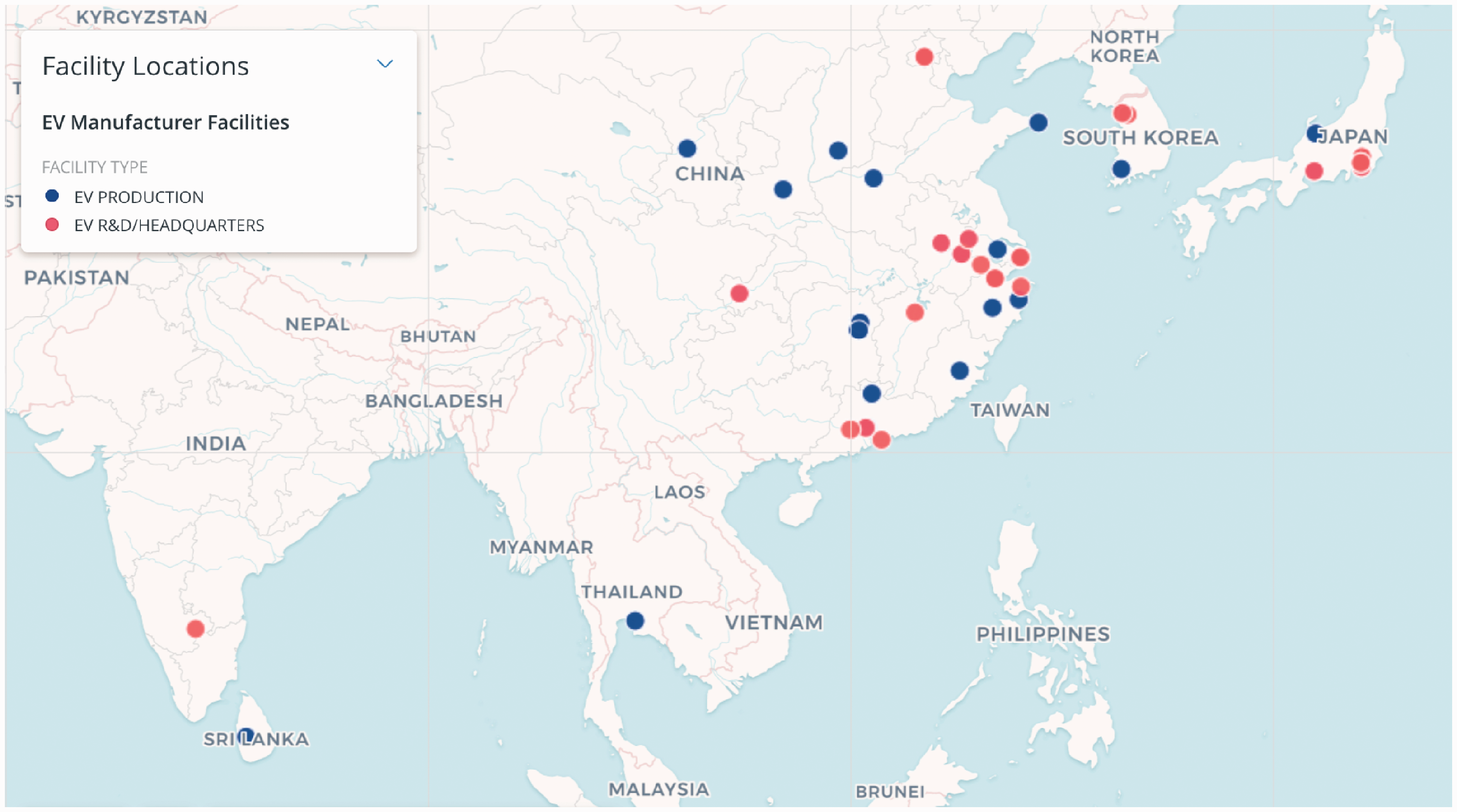

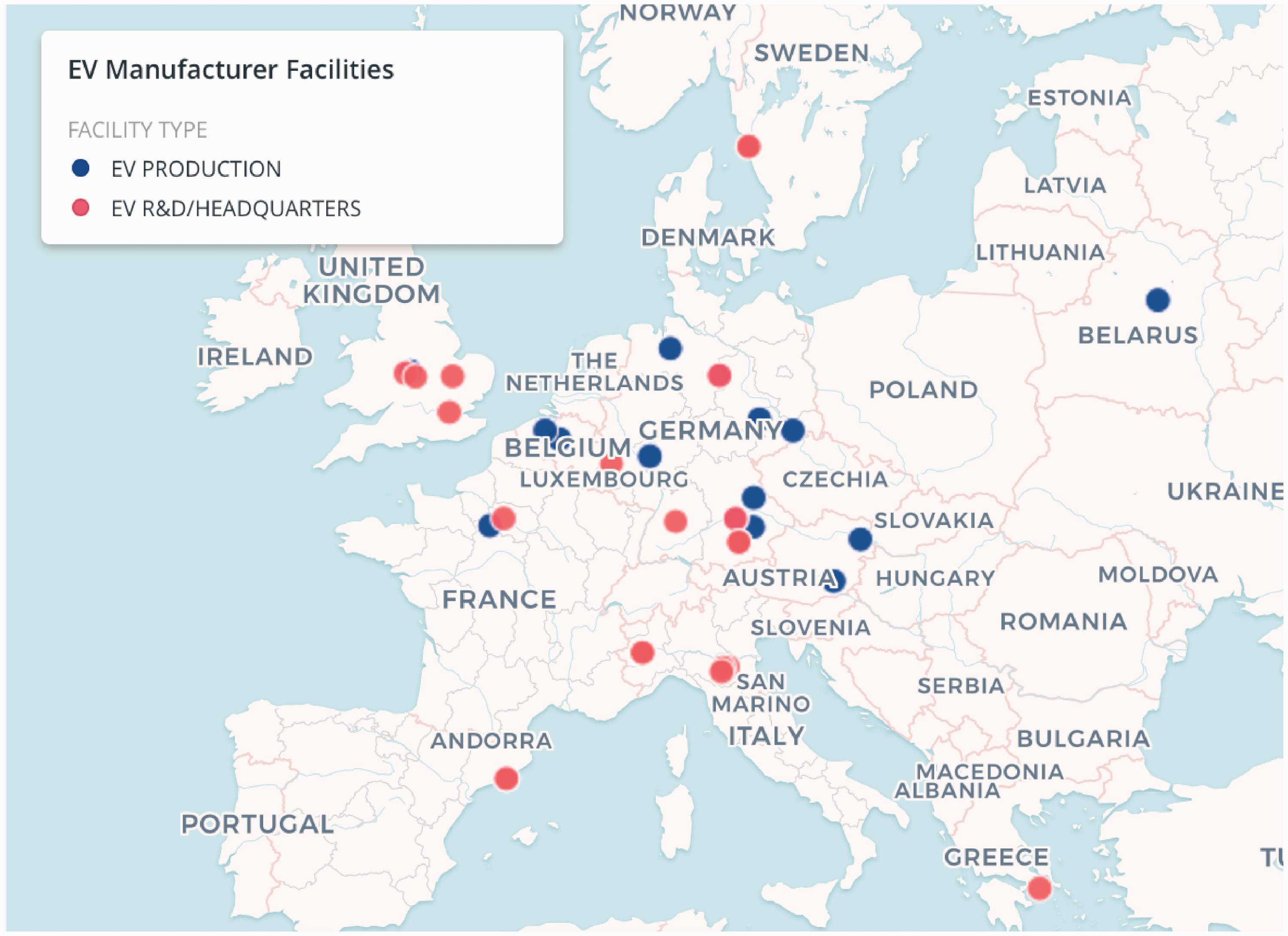

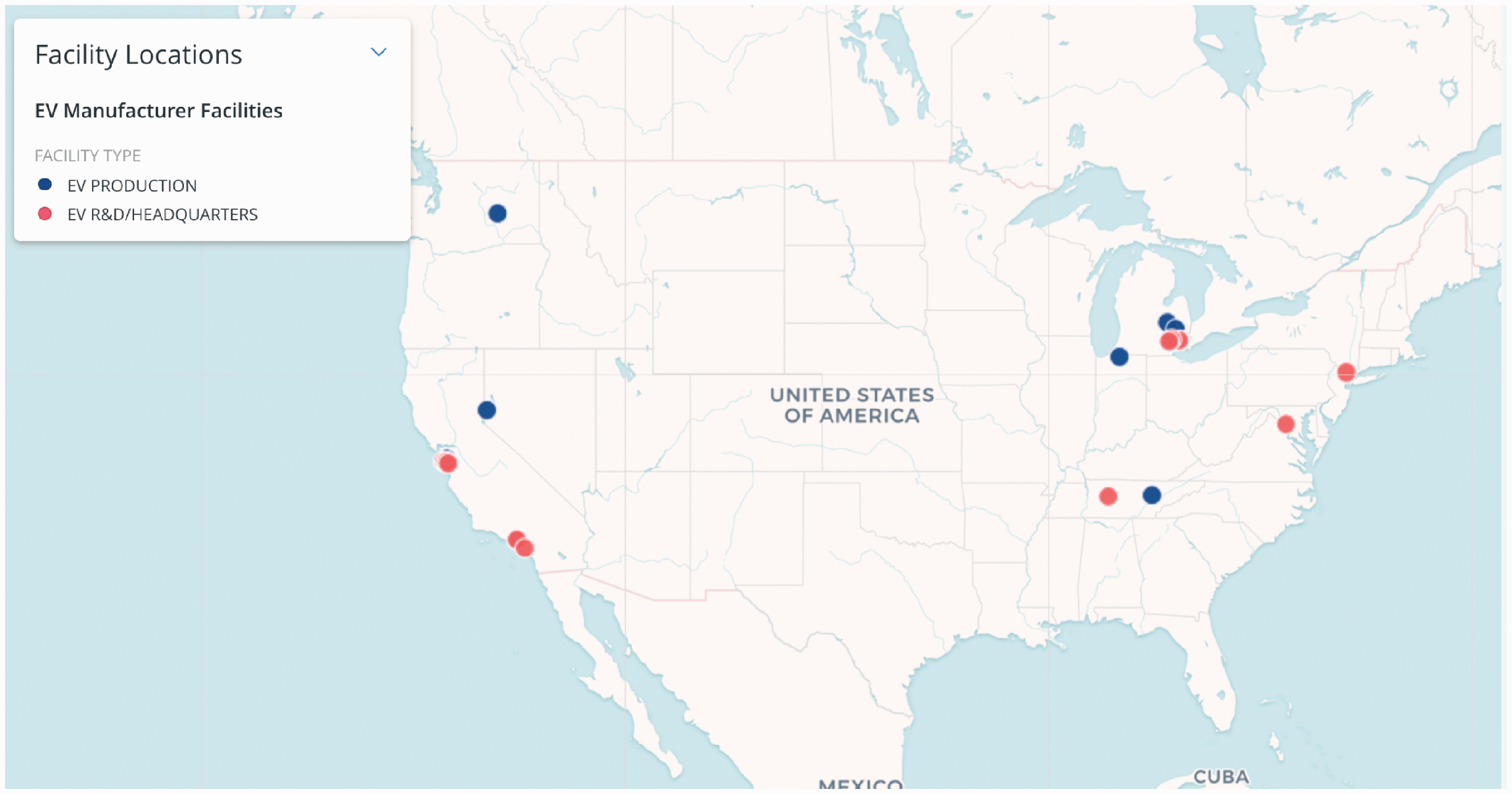

Auto manufacturers providing EVs are headquartered in North America, Europe, and Asia. Location choices for these firms largely follow the patterns of the traditional auto manufacturing industry. As seen in Figures 1 to 3, R&D activities are located near firm headquarters or in central regions with significant endowments of skilled labor, and production facilities tend to be located in more peripheral areas, though firms make efforts to open production plants in different continental markets.

EV manufacturers in North America. EV: electric vehicle.

EV manufacturers in Europe. EV: electric vehicle.

EV manufacturers in Asia. EV: electric vehicle.

Map of Silicon Valley (R. Schten).

Tesla locations with job postings, 2018. Source: Data scraped from www.tesla.com/careers on 9 October 2018.

The following case studies examine two regions: the San Francisco Bay Area in the US, and Emilia-Romagna in Italy. Both regions host manufacturing activities for EV producers, but differ significantly in their institutional and skill endowments, and in the nature of their regional innovation systems.

Tesla and the San Francisco Bay Area

The economic history of the San Francisco Bay Area

The San Francisco Bay Area has long been a global leader in the development of innovative technology, particularly in high-tech sectors. From the 1970s to the early 2000s, most of the region’s high-tech innovation was concentrated in the two counties of “Silicon Valley” (San Mateo and Santa Clara), although activity has since spilled over into Alameda County and San Francisco County (Figure 4). The Bay Area is one of, if not the, most characteristic examples of a regional innovation system, with knowledge generating and knowledge exploiting institutions linked to one another and to national and global systems (Cooke, 2001).

Federal investments in defense in Santa Clara County during and following the Second World War helped spur the transformation of Silicon Valley from a predominately agricultural region to a hub for technology. Stanford University received extensive federal R&D funding for projects like ARPANET and for education and research in engineering and computer science. Local firms expanded significantly due to wartime and postwar defense contracts (Mazzucato, 2015; Saxenian, 1996). Capitalizing on local institutions like the Stanford Research Institute and the Stanford Industrial Park, an open culture of business development between university and private entities emerged (O’Mara, 2005).

By the early 1970s, two major shifts were reshaping the region’s economy: the shift to semiconductor manufacturing as the major industry in the Valley, and the shift from federal defense contracting to consumer electronics development and production (Collaborative Economics, 2001). Following increased international cost competition for manufacturing, Silicon Valley’s manufacturing sector diversified into other products like printers, business services, disc drives, PCs, and customized chips, reorganized into a flexible production system (Saxenian, 1996). The personal computer revolution then laid the groundwork for the IT and internet revolution of the 1990s, fueled by venture capital (Castells, 1997; Saxenian, 1996). Despite the dot-com bust in 2001, firms like Apple and Google matured into giant corporations, while a new generation of software development, artificial intelligence, and other startups emerged in the 2010s.

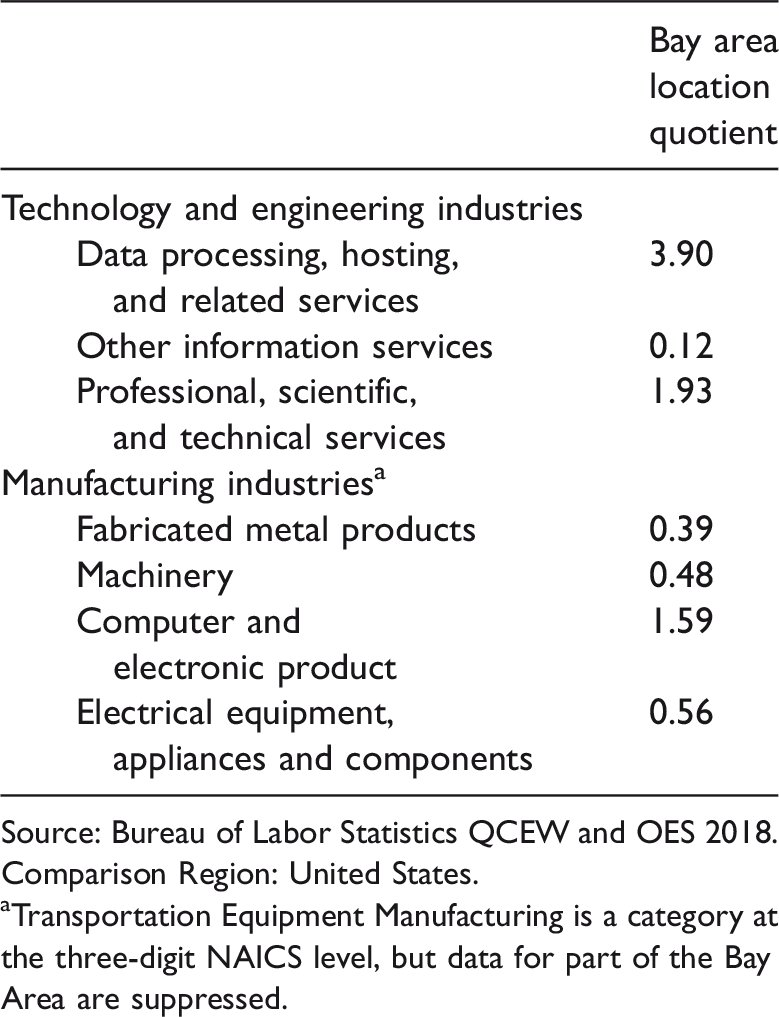

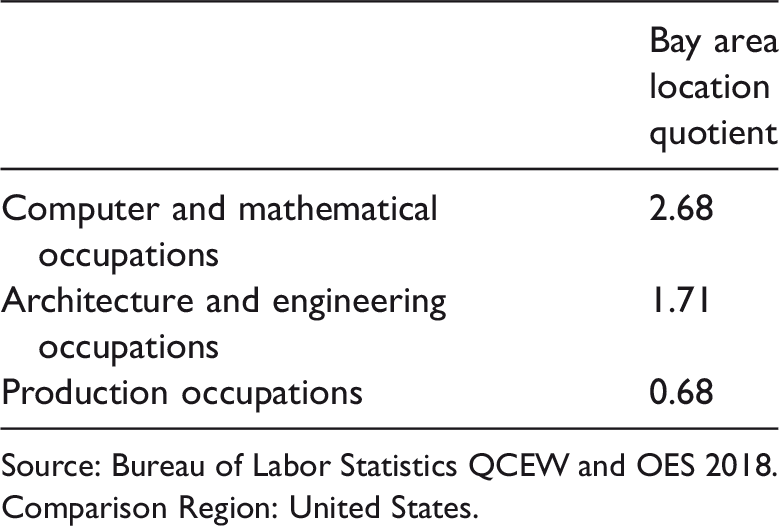

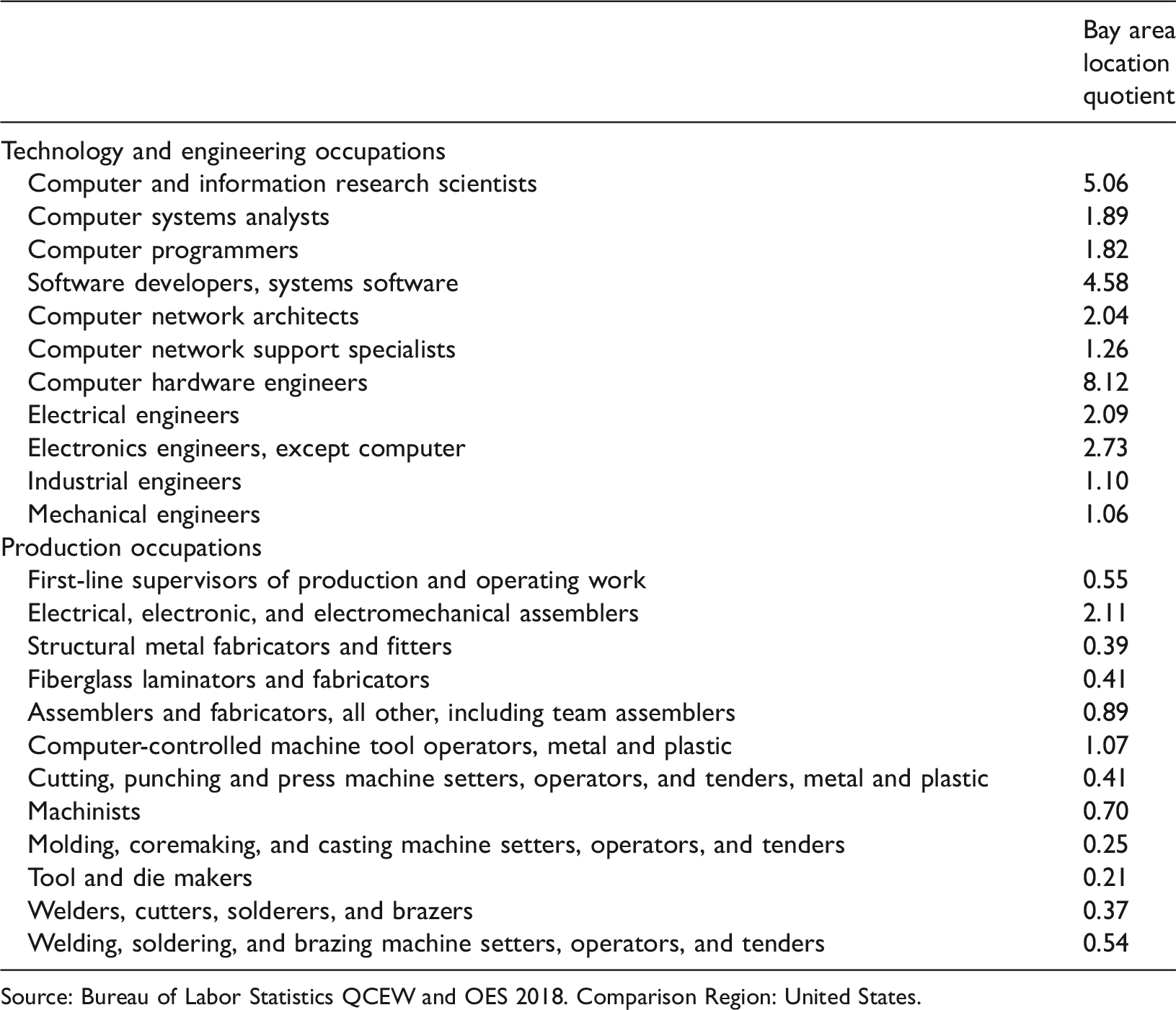

Location quotients for industry and occupations at the two-digit and three-digit NAICS code level (Tables 1 to 3) show a relative concentration of high-tech employment in the Bay Area, consisting here of the San Francisco–Oakland–Hayward and the San Jose–Santa Clara metropolitan statistical areas. While the region hosts a competitive concentration of high-tech occupations, it is weaker in concentration of production workers, with the exception of electrical, electronic, and electro-mechanical assemblers, suggesting that a shift to knowledge-based manufacturing is taking hold.

Bay area industrial location quotients 2018.

Source: Bureau of Labor Statistics QCEW and OES 2018. Comparison Region: United States.

aTransportation Equipment Manufacturing is a category at the three-digit NAICS level, but data for part of the Bay Area are suppressed.

Bay area occupational location quotients 2018, major occupational categories.

Source: Bureau of Labor Statistics QCEW and OES 2018. Comparison Region: United States.

Bay area occupational location quotients 2018, detailed occupational categories.

Source: Bureau of Labor Statistics QCEW and OES 2018. Comparison Region: United States.

Skill requirements from Tesla job postings in manufacturing department, Fremont, CA.

Source: Data scraped from www.tesla.com/careers on 9 October 2018.

aThe majority of jobs requested MS Office skills; these were not included.

Institutional coordination in the bay area

The Silicon Valley model has diverged from high-tech regions in other parts of the US and other countries, which are organizing place-based industrial policies to support the emergence of entrepreneurial ecosystems anchored by local institutions. Despite Silicon Valley’s roots in government and university collaborations with the private sector, there are few formal initiatives to shape cross-fertilization between researchers and industry. Instead, a specialized business ecosystem, consisting of a plethora of firms—lawyers, accountants, management consultants, etc.—providing support services to entrepreneurs, has emerged organically and is heavily subsidized by local venture capital. For example, in the past three years, Silicon Valley firms received $139 billion in venture funding, 40–50% of the US total each year (PricewaterhouseCoopers, 2020).

Driving the success of the model in Silicon Valley is human capital, consisting of education and work experience as well as tacit knowledge (Gertler, 1995, 2003). Exchange of tacit knowledge in the Bay Area is facilitated by worker mobility and immigrant entrepreneurship (Saxenian, 1996, 2005). Over one-fourth of Bay Area residents are foreign-born, compared with 14% of U.S. residents (Johnson and Sanchez, 2019).

Place-based (industrial) policy in the bay area

Despite the region’s many assets for entrepreneurship, it faces challenges related to land use and infrastructure, especially housing shortages, transportation bottlenecks, rising income inequality, and unequal access to social services and education for residents. Though the State of California offers business support programs, including tax credits for equipment purchases and workforce retraining, these are generally not targeted by either industry or region. Absent an explicit industrial policy at the federal and state level, several regional organizations, including the Bay Area Council, and the Silicon Valley Leadership Group, dominate the regional economic development dialogue (Storper et al., 2015). Given the region’s livability crisis, these actors have largely shifted their focus to planning issues. Thus, to the extent that there is a place-based industrial policy in the region, it focuses on residential quality of life rather than creating and retaining jobs.

Tesla

Tesla was founded in Palo Alto in 2003 by four entrepreneurs and a software developer (Voigt et al., 2017). At the time, the other commercially available EVs were produced by established auto manufacturing firms who also produced conventional and hybrid vehicles. Tesla was awarded an early stage loan from the US Department of Energy in 2010 under the Advanced Technology Vehicles Manufacturing program, which the firm repaid nine years ahead of schedule (Tesla, Inc., 2013b; US DOE: United States Department of Energy Loan Programs Office, 2013). Tesla also benefited from a California state tax credit of $15 million in 2016 (Baker, 2016).

Although established as an EV production firm, Tesla’s strategy differs from other manufacturers of EVs, targeting the niche market of luxury sports cars. The firm envisioned first creating a demand for “high-performance electric vehicles,” then subsequently producing a mass market line (Hettich and Müller-Stewens, 2014). Tesla has consequently attempted to compete on technology and design rather than on price, and hasn’t pursued the economies of scale that make auto manufacturing profitable for traditional firms. Tesla invested significantly in R&D and in specific technologies, first through partnerships with existing firms and then in-house (Hettich and Müller-Stewens, 2014). Human capital is essential to this strategy, with intellectual property and talent constituting a significant part of the firm’s value (Voigt et al., 2017).

Tesla is arguably a prototypical example of the emerging economic paradigm, reflecting characteristics of “Industry 4.0” or the industrial IoT in its production and maintenance processes (Cheng et al., 2016; Valentin, 2019). A recall issued by the company in 2014 was implemented entirely remotely, with consumers receiving updates to faulty software on their vehicles without physically bringing them to a dealership (Brisbourne, 2014; Rayes and Salam, 2017).

Whether Tesla is a “tech company” or an “auto company” has been widely debated, both by mainstream and tech media, and by academics in business and management fields. The former argue that Tesla’s similarities or dissimilarities in executive compensation strategies, valuation, product types, etc. determine the distinction (Aziza, 2019; DeBord, 2019; Smith, 2020). The latter argue over the significance of Tesla’s ability to overcome barriers of entry to the automobile industry, becoming the first new U.S. auto company to do an initial public offering on the New York Stock Exchange since the 1950s (Perkins and Murmann, 2018). Some interpret Tesla’s success as evidence that large tech firms like Google and Apple can easily enter the EV market; others argue that Tesla’s success is neither easily reproducible nor indicative of a fundamental shift in the industrial organization of auto manufacturing.

Tesla’s characteristics, and whether they reflect an orientation as a tech company or an auto company, have significance for industrial policy, regional planning, and economic geography. In planning for an emergent EV industry, how should regions respond? What institutions, labor, and infrastructure will be needed, and how can existing regions adapt their endowments to meet these needs? What spatial patterns of investment might arise and how will they affect local markets for land use and labor?

Tesla has employees at multiple locations on three continents (Figure 5). Both the firm’s headquarters and the largest manufacturing plant are located in the Bay Area, in Palo Alto and Fremont, respectively. Tesla also owns and operates a solar cell factory in Buffalo, NY; a battery factory in Nevada; and two other locations that assemble cars for specific domestic markets: Tilburg, Netherlands, and Shanghai, China, opened in late 2019. The company has announced plans to open a fourth plant that will manufacture batteries, vehicle components, and assemble vehicles in Berlin, Germany (Metzner, 2019; Tesla, Inc., 2013).

Tesla in California

In 2010, Tesla purchased an auto manufacturing plant in Fremont, CA for $42 million, recently vacated by the joint Toyota–GM project of New United Motor Manufacturing, Inc. (NUMMI) (Tesla engineer, personal interview, 27 February 2019). Under GM’s ownership, the plant was plagued by labor disputes and low productivity. The subsequent takeover by NUMMI in 1984 resolved these problems. As a manufacturing firm in a higher-cost region with a unionized workforce and high productivity, NUMMI was widely recognized as a success story of a more innovative, flexible approach during the ongoing disintegration of manufacturing industries in the U.S. Following the 2008 recession, however, Toyota closed the NUMMI plant, moving its vehicle production to lower-cost North American regions.

Tesla’s production approach varied significantly from Toyota’s. When Toyota took over NUMMI, they retained workers, invested in training, and permitted continued union representation. Despite a weak attempt at intervention by the State of California, Tesla rehired only a small portion of former NUMMI workers, successfully and intentionally avoided union representation, and offers lower wages for similar positions (Kowalski, 2014). Much of its workforce comes from the megaregion, living in temporary housing or even RVs (Tesla engineer, personal interview, 27 February 2019).

Tesla describes its operation as vertically integrated: even the car seats are manufactured in-house for quality control (Tesla engineer, personal interview, 27 February 2019). Its plant houses the largest hydraulic press in the world. At the same time, it has largely recreated NUMMI’s specialized pool of suppliers. Though Fremont feared the loss of supplier firms linked to NUMMI, the automotive cluster rebounded a few years after Tesla arrived, providing more jobs than before (Chapple et al., 2017).

Assembly line automation at the Tesla Factory is key to the firm’s strategy. The Fremont plant is noted for the number, size, and capacity of the robots involved in its automated manufacturing process, with robots always on hand to repair those that have broken down (Perkins and Murmann, 2018; Tesla engineer, personal interview). These robots were heavily relied upon when Tesla attempted to dramatically scale-up production of the Model 3 in 2017 and 2018 (Kottenstette, 2019). Struggles in this process, mostly attributed to failures in the automation technology, caused Tesla to miss its production targets in 2018 and 2019 (Boudette, 2019).

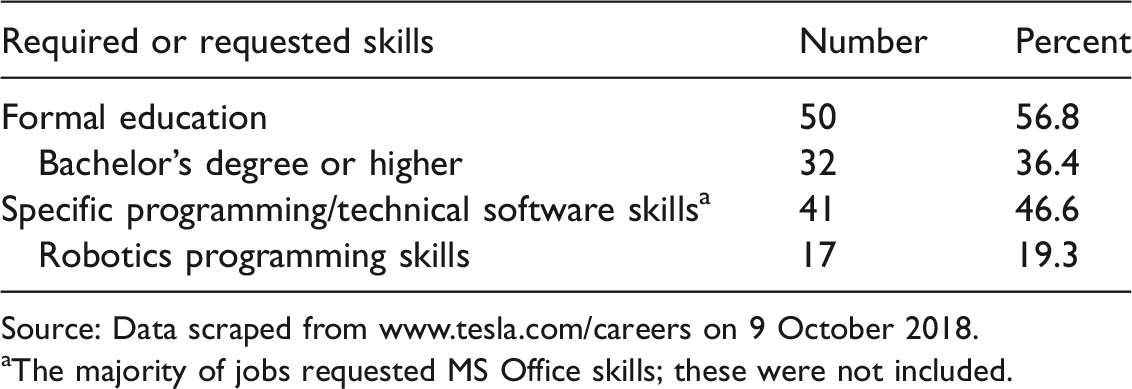

Tesla’s recruitment strategies reflect an emphasis on knowledge-based and formal/semi-formal technical and programming skills. A scraping of the Tesla website’s job postings in October of 2018 found that over half of the 88 manufacturing department job openings at the Fremont factory requested a specific level of formal education. Over a third requested a bachelor’s degree, seven specified an associate’s degree or higher, and six a high school diploma. Of those that didn’t specify formal education, 19 requested specific software or robotics programming skills (Table 4).

Tesla’s strategy in the regional context

Tesla’s successes and failures relate closely to place-based assets in the San Francisco Bay Area. First, much of Tesla’s success is attributed to their technological product. Their battery and powertrain technologies were estimated in 2019 to be “years” ahead of their competitors. Tesla’s incorporation of advanced, networked software, including driver-assistance technologies, contributes significantly to the firm’s success and indicates possible fundamental shifts in the auto industry. Tesla’s ability to compete on a technological basis, particularly as an unusually vertically integrated auto firm, reflects its dependence on intellectual property and human capital. Both are place-based assets entrenched in the Bay Area’s long-time role as an innovative, tech-focused region.

In addition, Tesla’s ability to raise financing during its early years was essential to its survival and success as a startup, and contributed to its position as the second highest-valued car company in the world (Stringham et al., 2015). As noted previously, the vibrant venture capital scene is a widely acknowledged component of the Bay Area’s success as a regional innovation system.

Tesla’s failures are similarly linked to the region. Tesla has been widely criticized for failing to produce its vehicles at anything approximating a mass-market level, failing to meet industry norms for auto production until 2019 (MacDuffie, 2018). A recent “turnaround” in the last half of 2019 led to rising stock prices, but Tesla has continued to suffer from safety issues related to batteries that reflect poorly on the firm’s production quality (Alba, 2019). The Fremont factory has also received significantly more fines for occupational health and safety violations than any other U.S. factory (Adelson and Hull, 2019; Ohnsman, 2019).

Tesla’s recent selection of Berlin, Germany, as the location for their fourth plant, reflects a location choice oriented toward technology development rather than production skills endowments. Europe’s auto manufacturing regions are located elsewhere: in southern Germany, northern Italy, and the UK. Production strategies based on peripheralizing manufacturing in low-cost regions while concentrating R&D elsewhere would suggest lower-cost production sites in Spain, Portugal, or Eastern European countries. Berlin, however, is receiving media coverage deeming it an emerging technology hub, with a possible emphasis on mobility technology (Petzinger, 2019).

Maserati in Emilia-Romagna, Italy

Economic history of Emilia-Romagna

Emilia-Romagna, located in central northern Italy, has followed a path distinct from other highly industrialized Italian regions, emerging as a relatively knowledge-intensive manufacturing region in the past two decades. Emilia-Romagna’s industrial specialization evolved out of military exploitation of its strategic location and agricultural resources, and following the process of mechanization of its large traditional agricultural sector (Montanari et al., 2004; Zamagni, 1993). In both World Wars, the region served as a hub for military transport, logistics, mechanics, and food processing. Following the Second World War, Emilia-Romagna gradually reconstructed itself on the basis of this deep expertise, becoming a center for traditional industries including the processing and packaging of food and pharmaceuticals, machinery manufacturing, and motor industries.

In the 1970s, the transition to post-Fordist modes of production caused an economic crisis for Italy’s most industrialized regions. In other regions, including Emilia-Romagna, a new approach to industrialization emerged, which became widely known as the “Third Italy” (Bagnasco, 1977; Becattini, 1987, 2004; Brusco, 1982; Fuà and Zacchia, 1983). The Third Italy regions were characterized by communities of diverse actors connected by dense social networks, including small and medium enterprises, local institutions, associations, and skilled workers and entrepreneurs. Through flexible specialization and adaptive innovation, these regions were able to respond to the demands of the post-Fordist system (Amin, 1999; Boschma and Lambooy, 2002; Helliwell and Putnam, 1995; Piore and Sabel, 1984). In the 1980s and 1990s, Emilia-Romagna’s economy continued to develop based on this model of industrial organization, which was rooted in the productive history of the region and facilitated by government and civic institutions.

Even as manufacturing regions in Italy have evolved from flexible specialization to a knowledge-based economic paradigm, Emilia-Romagna has retained more manufacturing than its peers. The service sector has grown, and manufacturing has shrunk, but this shift has been slower than in other Italian regions. Manufacturing is relatively concentrated among a few industries, particularly in machinery (21% of manufacturing employment) and in metallurgy and vehicle production (18%), but has diversified at the sub-industrial level (Andreoni, 2018). The regional economy has also become increasingly organized around value chains, linking diverse production, activities, and firms in Emilia-Romagna (Rinaldi, 2005).

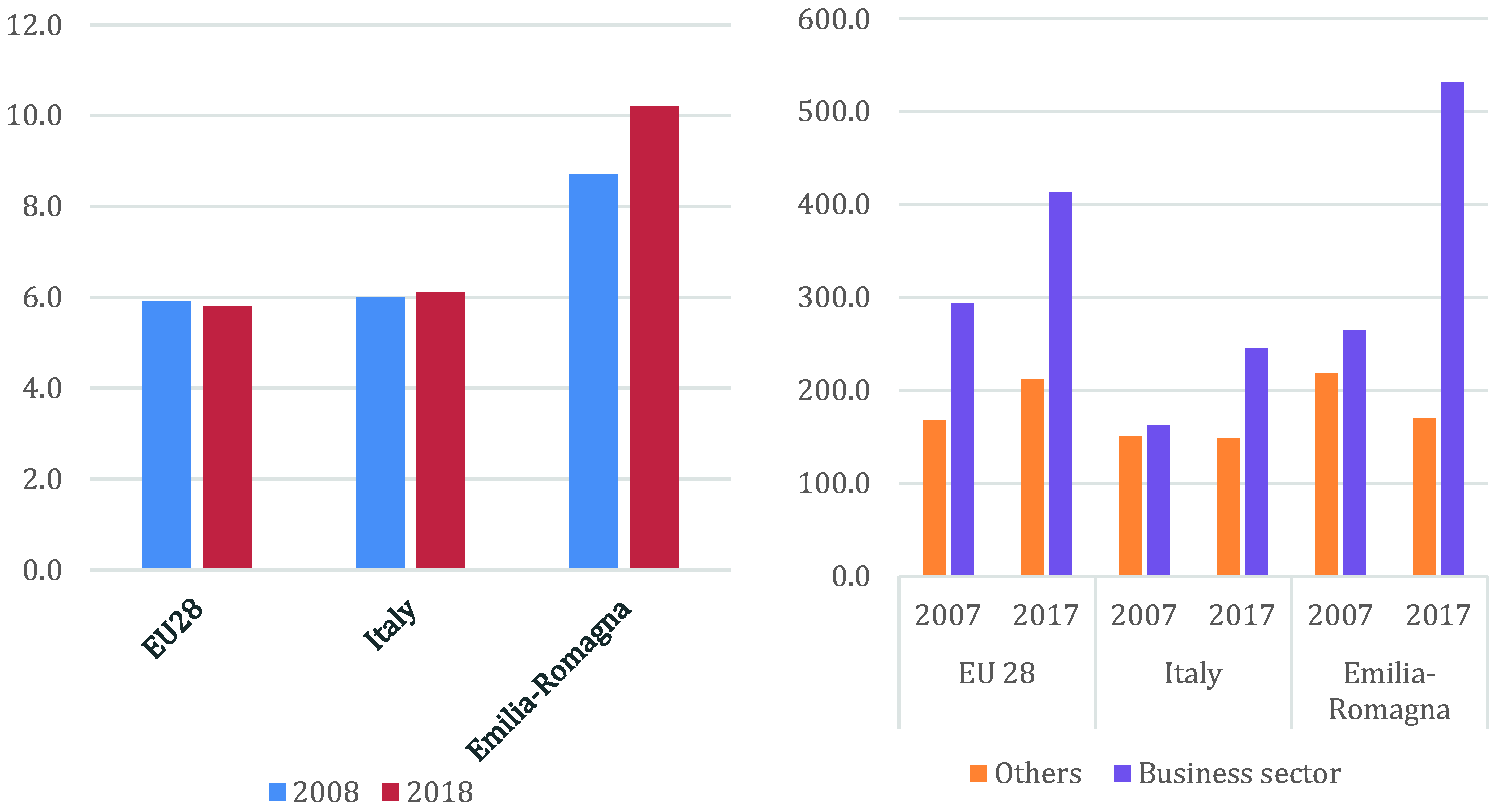

Although Emilia-Romagna has retained a significant manufacturing base, knowledge and technology have become more important components within it. Employment in mid- and high-tech manufacturing has increased from 8.7 to 10.2% of all manufacturing employment in the past 10 years. Private investment in R&D per capita in Emilia-Romagna was over twice the Italian average, and above average for regions in EU28 member states (Figure 6).

Growth in knowledge and technology content of regional manufacturing. Source: Eurostat.

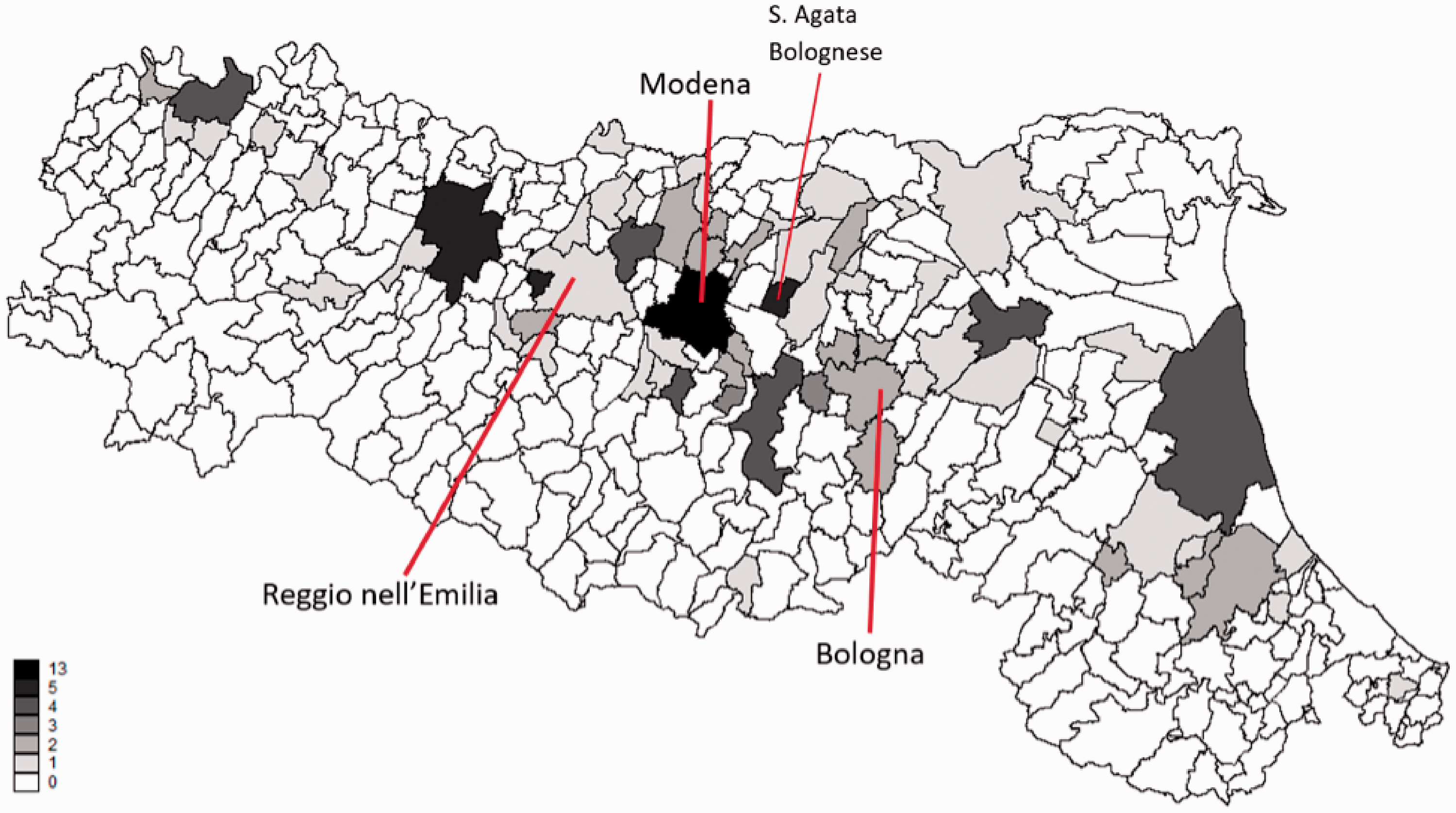

Automotive firm density by town, Emilia-Romagna, 2017. Source: AIDA-Bureau Van Djik database.

The automobile industry contributes approximately 10% of the total value added generated by the Emilia-Romagna manufacturing sector. It is geographically concentrated in three of Emilia-Romagna’s provinces: Modena, Bologna, and Reggio nell’Emilia, though automotive firms are present across the region.

Institutional coordination in Emilia-Romagna

In the last century Emilia-Romagna has hosted a community of firms, people, and institutions specialized in mechanics and motors, which continues to shape the local manufacturing economy (Figure 7). The density and cohesion of this community constitutes a territorial asset and an attracting factor for external actors. Ferrari, Lamborghini, and Maserati are some of the best-known brands, heading up a long list of small and medium firms that make up the “Emilia-Romagna Motor Valley.”

Formal institutions and policies have played an essential role in the region’s transition to knowledge-based advanced manufacturing. Since 2002, when the innovation law was established, regional institutions have built and strengthened networks of existing actors and connected tangible and intangible assets already rooted in regional manufacturing. Emilia-Romagna is home to four public universities providing advanced and a network of technical colleges and post-secondary diploma technical training institutions (Istituti tecnici superiori (ITS)) providing specialized training. Seven public–private foundations offer two-year courses in specific competencies linked to local economic strengths, including mechatronics, logistics, and sustainable mobility. 1

Regional institutions and policies also support networking, collaboration, and knowledge exchange, and provide funding and services. The backbone of the regional innovation system is the High-Technology Network, a group of 96 public and private innovation centers and laboratories, which emerged informally in the 2000s and was later connected by public initiatives into an organized framework including incubators, digital innovation hubs, and enterprise clusters.

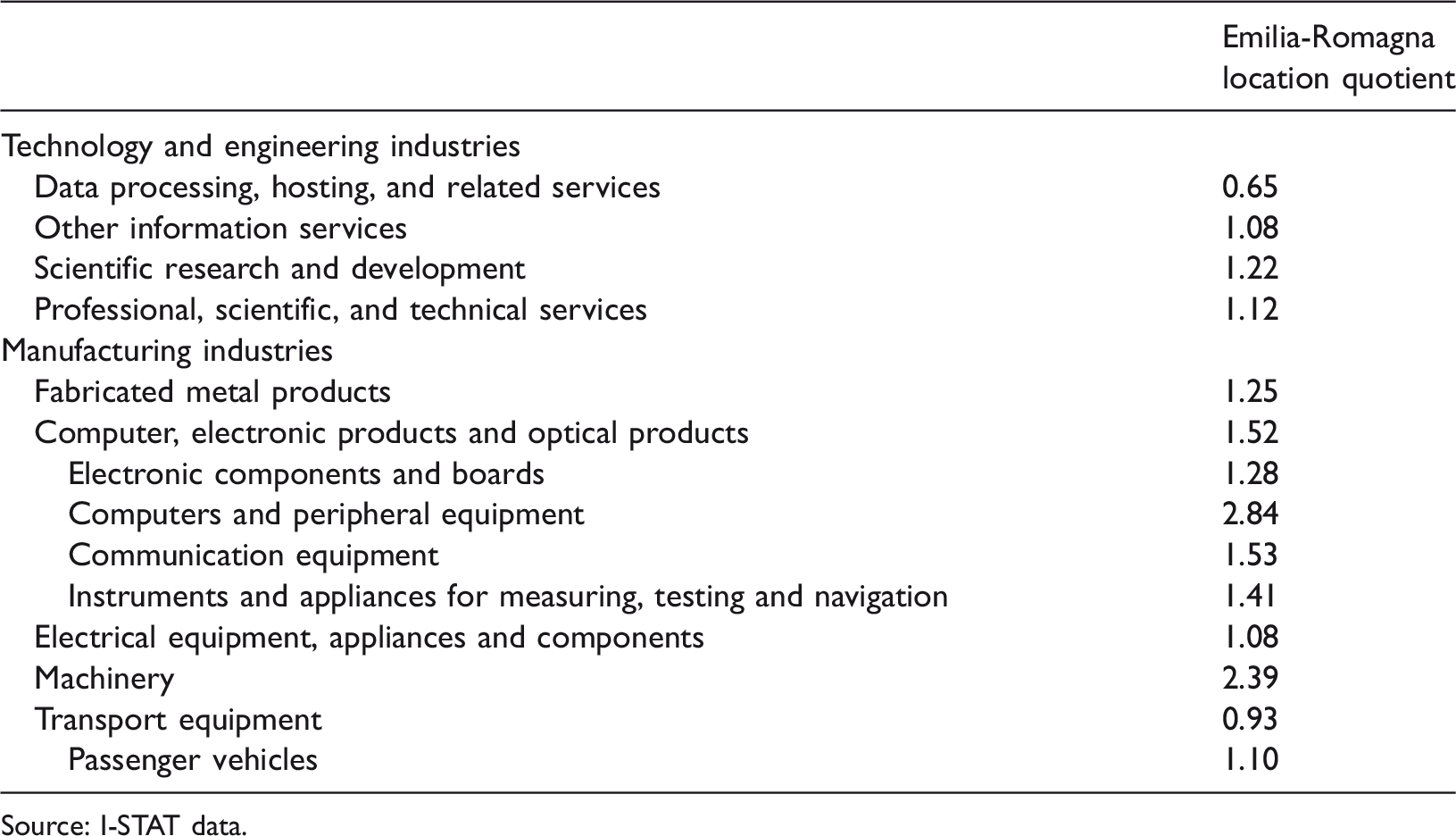

Location quotients for the region confirm that manufacturing industries, especially machinery manufacturing, play a significant role in Emilia-Romagna (Table 5). Knowledge-oriented industries are somewhat concentrated in the region, though to a lesser extent.

Emilia Romagna industrial location quotient 2017.

Source: I-STAT data.

Place-based policy in Emilia-Romagna

The Emilia-Romagna region released a smart specialization strategy in 2012, specifying areas in which the region’s competitive and innovative potential could be augmented through intervention (Regione Emilia-Romagna, 2012). The automotive industry was identified as a specialization area and three strategies were developed to support it. Corresponding policies and initiatives were undertaken to implement each strategy, creating an integrated, dense architecture of institutional, policy, and financial support.

In the first strategy, regional institutions in Emilia-Romagna work to strengthen technological and human capital in the region, providing targeted training through ITS in technology related to mobility, including software applications, automation, and new energy sources. The region also established a university program dedicated to automotive engineering and design, the Motor-vehicle University of Emilia-Romagna (MUNER), which links regional universities and nine large firms representing luxury, sport, and high-range engines brands. 2 Emilia-Romagna also developed a formal innovation platform for tech and knowledge transfer from 26 of the High Technology Network’s research laboratories to producers in the sector.

The second strategy strengthens collective action among firms. Regional policymaking supported and financed the development of formal associations representing different clusters, including one on mechanics (MECH-ER). 3 The MECH-ER cluster, which involves 48 firms, 32 research centers, 6 private innovation centers, and 3 training centers, gathers and integrates actors belonging to different value chains. One of these, MoVES, Motori e Veicoli efficienti, sostenibili e intelligenti, is focused on improving environmental sustainability, energy efficiency, connectivity, and automation of vehicles, and aims to formalize scientific collaborations among and between firms and research institutions. Another association, the Emilia-Romagna Sustainable Electric Mobility association (E-Rmes), gathers 24 firms and 3 research institutions involved in the design and production of automotive components, particularly electric powertrain integration (Ausiello, 2016).

The final regional strategy aims to attract resources to the region by providing financial support to firms that improve innovative, technological, and employment outcomes at the regional level. Suppliers have been increasingly involved in MUNER, contributing to human capital formation. In addition, some foreign actors that have increased their presence in the region are willing to co-develop EV technology with smaller brands to share the cost of development and exploit the advantages of scale economies in such forms of investments. 4

Emilia-Romagna’s automotive industry strategies have interpreted smart specialization policies as an investment in territorially based resources, building off of existing capacities and potential to improve the region’s competitive position in an international economy. The region has increasingly attracted foreign automakers from countries that are emerging as global automotive producers. For example, a Chinese joint venture was recently established between the state-owned enterprise FAW and the regional engineering firm Silk EV.

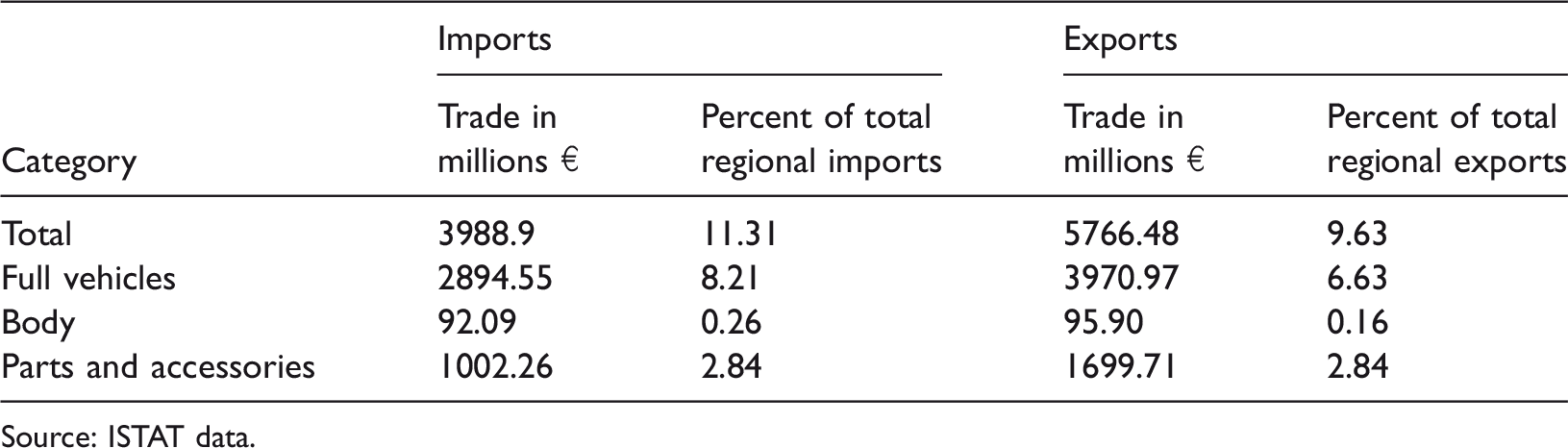

Emilia-Romagna’s auto industry has close trade linkages with other European regions and is a net exporter in each sub-industry of automotive production (Table 6). Production is highly integrated with Germany in particular, which is both the largest trading part for the Emilia-Romagna auto industry and the main country of origin for foreign firms producing passenger vehicles in the region (Pollio, 2018). Full vehicles produced in Emilia-Romagna are exported to a wider range of areas, with the U.S. accounting for the largest share.

Emilia Romagna’s international trade flows, 2017.

Source: ISTAT data.

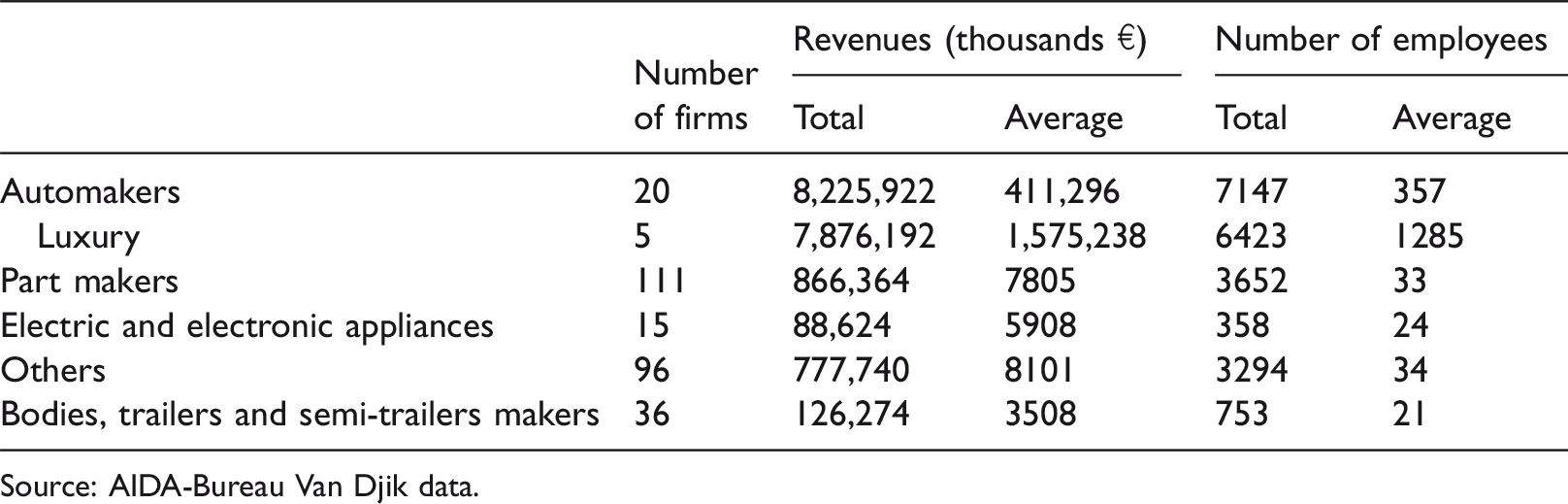

Emilia-Romagna auto industry, firm-level data, 2017.

Source: AIDA-Bureau Van Djik data.

Luxury vehicle production plays a significant role in Emilia-Romagna’s regional automotive manufacturing industry (Table 7). Firm-level data show that, while only a handful of auto firms are specialized in luxury and sport vehicles, they are responsible for more than 96% of the total revenues and about 90% of employment in the regional auto industry (Pollio, 2018).

Foreign firms also have a strong presence within the production context and are essential actors in the regional value chain. Like luxury firms, they represent a small total number of firms (17 out of 157) but a disproportionate part of revenue (87% of total) and value-added generated by the auto industry (92% of total) in Emilia-Romagna. Many suppliers and luxury automakers are under foreign ownership (for example, Lamborghini is owned by the German Audi-Volkswagen).

Maserati in Emilia-Romagna

Maserati is a key part of Emilia-Romagna’s unique development as an automotive production and innovation region. The firm was founded in 1914 in the city of Bologna, Emilia-Romagna, and the first Maserati was manufactured there in 1926. Maserati initially specialized in racing autos, through which the firm improved its technological capacity and gained international brand recognition. Its first non-racing road car was produced after the end of the Second World War. The firm has changed ownership and management several times during the past century, controlled by the founders Maserati brothers (1914–1939), the Orsi family (1939–1968), Citroen (1968–1974), Italian state-owned enterprise GEPI (1975–1993), Fiat/Ferrari (1993–2010), and now Fiat-Chrysler. 5

Maserati’s strategy in the Emilia-Romagna context

Despite ownership changes, Maserati’s factory in Modena, Emilia-Romagna has been there since 1939, and its headquarters and R&D are also located there. Industry press indicates that the Modena plant is being upgraded to produce Maserati’s first EV, the Alfieri, in 2020 or 2021, and that the firm will partner with Ferrari to produce the powertrains (Kautonen, 2019). The Fiat-Chrysler group has invested significantly in Maserati, targeting EVs and luxury markets. Relative to the other two exporting brands in the region, Maserati has significantly increased the number and percentage of its cars sold abroad in the past five years, drawing on the region’s strong foreign linkages (ANFIA, 2020).

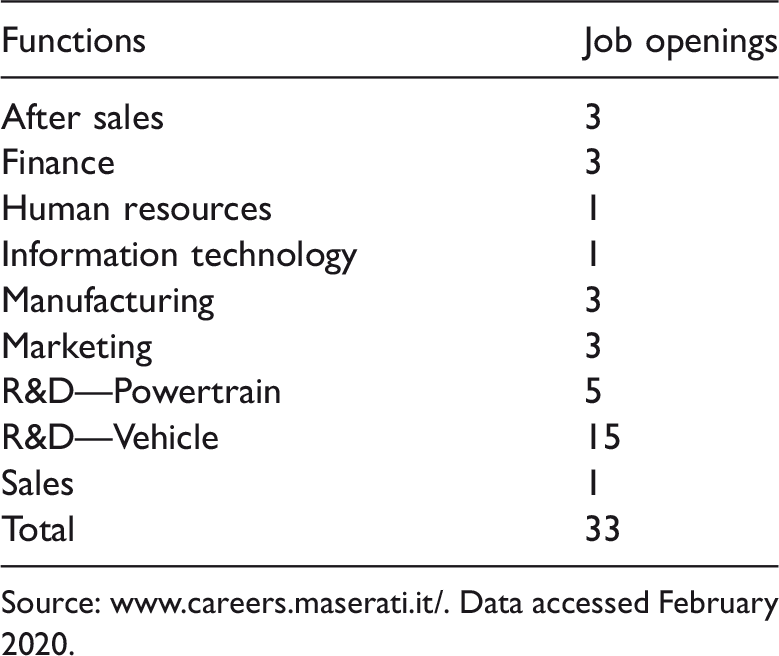

Maserati’s labor demands are shifting to reflect the technological advancement of their program. Their 2019 job listings reflected expanding R&D needs, with demand for workers with engineering degrees and software skills (Table 8). Maserati is active in the Emilia-Romagna auto manufacturing cluster as a partner of the MUNER project.

Labor demand by Maserati, 2019.

Source: www.careers.maserati.it/. Data accessed February 2020.

The future of EV manufacturing in Silicon Valley and Emilia-Romagna: Critical reflections on place-based industrial policy

Effective place-based policy promoting innovative economic development is in demand. Tailoring regional place-based strategies to emerging industries presents a particular challenge, as intervention is demanded even when it isn’t yet clear what kinds of externalities will benefit emerging industries, what kinds of spatial location patterns these industries will adopt, or how the industry could be expected to continue to evolve. The two cases of Tesla and Maserati provide an opportunity to examine these questions via the emerging EV production industry, which involves elements of traditional auto manufacturing and of high-tech innovation and advanced manufacturing. The cases demonstrate a potential role for place-based industrial policy in supporting emerging industries, but also suggest that the interventions needed will vary widely depending on context.

Both Tesla and Maserati draw on their regions’ extensive economic histories and endowments and the industrial paths that they created. Tesla, a firm that emerged from a high-tech regional innovation system, draws heavily on its local high-tech workforce. In an emerging industry that combines elements of both innovative high technology and traditional auto manufacturing, Tesla’s technology has remained at the forefront of the EV industry and enabled it to compete effectively with traditional auto manufacturers. Maserati also draws advantage from Emilia-Romagna’s long-established history as a manufacturing-oriented region. The firm has access to a trained production workforce, production infrastructure, and networks of suppliers with expertise in luxury automobile markets.

Both Tesla and Maserati also benefit from institutional coordination of their regions. Tesla has been able to draw on the Bay Area’s deep venture capital to successfully finance its unorthodox attempt to break into the automobile production sector. It benefited not only from infrastructure and suppliers inherited from the NUMMI plant, but also the broader Silicon Valley ecosystem of tech startups. Maserati has profited from a dense network of regional institutions supporting innovation, and has been able to partner with established auto manufacturers, including global players, that are part of the regional “community of people and firms” (Becattini, 2015).

The embeddedness of the two firms in their home regions seems to support place-based industrial policy; place-based industrial policy appears to benefit Maserati already. The Emilia-Romagna local government has designed, implemented, and funded policy intended to cultivate knowledge-intensive innovation, production, and skill development. This policy builds off of the existing regional strength in automobile manufacturing, and works to develop cross-sector partnerships and diversify beyond traditional production areas. Such policy intervention should help Maserati compensate for potential regional technology shortcomings, while it benefits from regional production expertise, infrastructure, and partnerships.

Conversely, Tesla has developed and implemented cutting-edge technology throughout its existence without the benefit of place-based policy intervention. Although tax credits supported production in the Fremont plant and stimulated EV consumption, there is no industrial policy supporting local knowledge-intensive innovation and skill development. Thus far, the firm’s acquisition of NUMMI has enabled production. However, Tesla’s output remains unreliable due to bottlenecks in the production process and labor performance instability. Despite continual expansion, Tesla is rarely able to meet its production goals. Tesla may also struggle to find and retain production employees and expand production infrastructure in the Bay Area if regional land prices and cost of living continue to rise. Without place-based interventions to help stabilize the workforce, Tesla will likely take advantage of its expansion to other knowledge-intensive regions, like Berlin, to shift production outside of the Bay Area.

Unlike Tesla, Maserati has not yet put its EV on the market, although its partnership and knowledge base are in place. Yet its future is also tenuous, in part because regional policies have focused largely on the risky strategy of attracting foreign capital to the region, as well as relying on foreign actors to support the region’s skill-building. Its EU ranking as a moderate innovator raises questions about its long-term competitiveness vis-à-vis other competitors in Europe (European Commission, 2018).

Literature on regional innovation systems emphasizes the value of environments that encourage informal networking and knowledge exchange, including across sectors, and the importance of embeddedness for firms seeking the advantages of this environment. However, these case studies emphasize that policies intended to support or grow innovation systems will vary based on the types of industries these regions seek to germinate, and the needs of the firms that are embedded in the regional system. Place-based policies appropriate for EVs would need to identify both the specific needs of this emerging industry and the shortcomings of the region in question. In Tesla’s case, this means ensuring that workers can move to and remain in the area. In Maserati’s case, interventions would need to continue to increase local knowledge competencies and access to capital. These are two distinct approaches to place, suggesting that the construction of industrial policy must be locally specific, even for the same industry.

Emerging industries may diverge from existing patterns of the spatial division of labor seen in more established industries. For example, production and research may not be as clearly delineated from one another in more advanced manufacturing contexts. Skill needs are also transformed, requiring a smaller, more agile, and high-skilled workforce. In some cases, knowledge-intensive regions may gain new production activities (viz. Tesla building a new plant in Berlin); yet at the same time, regions with multiple traditional strengths like Emilia-Romagna may also benefit. Existing development paths may support new players in emerging industries, but may also hamstring them, sometimes simultaneously. This is illustrated in Tesla and Maserati’s successes in capitalizing on regional strengths while struggling to make up for regional shortcomings. Thus, whether adopted by a region acting alone or an entire country or federation like the EU, a place-based industrial policy will need to give regions the flexibility to design their own unique approaches.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was conducted within the framework of the project ‘Emilia-Romagna International School of Policy’ (CUP: E45J19000150004) funded by Emilia-Romagna regional government.