Abstract

This study synthesises research on mortgage financing (MF) and housing affordability (HA). Systematically reviewing 254 Scopus articles (2015–2025) via PRISMA, it combines Scientometric and qualitative analysis. Using a fishbone concept, it details systemic cause-and-effect challenges. Findings show housing deficits and affordability crises are most acute in the Global South, yet scholarly and policy discourse remains dominated by Western nations like the USA, Australia, and the UK. While MF can theoretically improve HA, its current adoption often exacerbates financial and social exclusion and fails to ease access. The analysis establishes a clear nexus between housing-induced financial stress, deteriorating mental health, and social inequities. It concludes that a fundamental reorientation of MF is required. Achieving sustainable HA necessitates robust, inclusive systems characterised by lower mortgage costs and targeted subsidies. Such reforms are imperative for progress toward UN Sustainable Development Goals, particularly SDG 11 (Sustainable Cities) and SDG 8 (Economic Growth).

Keywords

Introduction: The global housing conundrum

Background and problem statement

The closing decades of the 20th century and the opening of the 21st century have been characterised by unprecedented demographic shifts, including massive population growth and relentless urbanisation (Savić et al., 2022; Tambe and Tambe, 2025). This urban transition, while a hallmark of economic development, has precipitated a profound and persistent crisis in housing provision (Anokye et al., 2025; Czischke and Ayala, 2021). Governments worldwide are grappling with the constraint to supply adequate, decent, accessible, and, above all, affordable housing for their burgeoning urban populations (Galster and Lee, 2021; Gazzeh, 2025). Despite concerted efforts and policy declarations, the gap between housing need and effective supply continues to widen, presenting a multifaceted challenge that intersects economics, social welfare, urban planning, and public health (Kilonzo and Iwara, 2025).

The core of this challenge lies in the dual deficit of both housing quantity and housing quality, leading to the provision and supply of ill-decent accommodation globally. In this study, “decent accommodation” is conceptualised as housing that not only provides shelter but also incorporates all necessary internal and external facilities and amenities to ensure safe, healthy, and comfortable habitation (Kurebwa, 2020; Ofori, 2020). This encompasses adequate sanitation (lavatories, wastewater disposal), food preparation spaces (kitchens), sufficient natural and artificial ventilation, reliable electrification, physical security, and adherence to standardised room occupancy ratios, such as the 1:2 ratio advocated by UN-Habitat (Akinwande and Hui, 2024; Aziz et al., 2025). From an economic standpoint, decency is intrinsically linked to affordability. A dwelling cannot be deemed decent if its cost imposes an excessive burden on household finances, thereby compromising the ability to meet other basic needs like nutrition, healthcare, and education (Akinwande and Hui, 2024; Colburn et al., 2025). This intersection of cost and quality brings us to the central concept of Housing Affordability (HA). HA is fundamentally about the relationship between housing costs and household income, reflecting the capacity to secure and sustain appropriate housing without suffering undue financial hardship (Kleshcheva, 2021; Mia and Zull, 2020). It is a multidimensional metric that encompasses both the initial purchase (or entry into rental markets) and the ongoing costs of occupancy. The most widely adopted benchmark, used by institutions like the Australian Institute of Health and Welfare, according to their 2023 report, reiterates that housing is “affordable” when it consumes no more than 30% of a household’s gross income.

Expenditure beyond this threshold is categorised as “housing stress,” a condition associated with a range of negative socio-economic outcomes (Arundel et al., 2024; Baas et al., 2020). Crucially, as scholars like Haffner and Hulse (2019) emphasise, affordability is not a neutral market observation but a normative standard reflecting a societal judgement on the acceptable proportion of income devoted to shelter.

The role of mortgage financing: Promise and paradox

Confronted with the affordability crisis, many governments have turned to financial market solutions, with Mortgage Financing (MF) positioned as a primary engine for expanding homeownership (Agnello et al., 2020; Nakiwala et al., 2023). MF refers to the provision of loans secured by real property, where the borrower (mortgagor) pledges a property as collateral to the lender (mortgagee) and repays the principal plus interest over an extended period (Lehtimäki, 2025; Rim, 2024). By spreading the high upfront cost of housing over time, MF theoretically enhances accessibility for middle-income households.

In advanced economies such as the United States, the United Kingdom, Canada, Germany, Hong Kong, and Singapore, MF has become the backbone of the housing system, deeply interwoven with national capital markets through instruments like Mortgage-Backed Securities (MBS) (Hochstenbach and Aalbers, 2024). However, the efficacy of MF as a tool for promoting genuine, widespread HA remains deeply contested. Evidence suggests that in many circumstances, the expansion of mortgage credit has fuelled asset price inflation more effectively than it has expanded access, embedding affordability problems deeper into the economic structure (Long and Zhuang, 2025).

The indicators of this failure are global. In Australia, soaring rents contribute significantly to a national cost-of-living crisis, straining household budgets even for those in otherwise adequate housing (August and St-Hilaire, 2025). In the United Kingdom, high housing costs force many citizens into a cycle where a disproportionate share of income is absorbed by rent or mortgage payments, limiting capacity for savings and investment and exacerbating wealth inequality (Miles, 2020; Ye et al., 2024). Across Europe, from Belgium and Sweden to Germany, high fees, stringent credit requirements, and rising prices persistently challenge the promise of affordable homeownership (Licchetta et al., 2025). Even in the United States, the birthplace of modern mass mortgage markets, a significant portion of households continues to spend over the 30% affordability benchmark, indicating systemic stress (Breen et al., 2024).

The consequences of unaffordable housing extend far beyond economics. HA challenges are directly linked to increased homelessness, deepening social divisions, and spatial segregation. Perhaps more insidiously, housing stress is a well-documented social determinant of poor mental health, contributing to anxiety, depression, and reduced overall well-being (Bentley et al., 2025). Therefore, addressing the MF-HA nexus is not merely a technical financial issue but a critical imperative for public health, social cohesion, and sustainable urban development as envisioned in the UN Sustainable Development Goals, particularly SDG 11.

Research rationale, aim, and questions

Given the critical global importance and complex interplay of MF and HA, there is a pressing need for a comprehensive, systematic synthesis of the extant academic literature. Previous reviews have often focused narrowly on either housing affordability metrics or mortgage market mechanics (Duan and Li, 2024; Mia and Zull, 2020; Ofori, 2021), leaving a gap in integrated analysis that explicitly examines how mortgage financing structures and flows impact affordability outcomes across different contexts. This study aims to fill this gap by conducting a rigorous bibliometric-qualitative review to map the intellectual landscape, analyse prevailing themes, identify barriers, and propose future directions.

To guide this inquiry, the study is structured around the following research questions (RQs):

Research methodology

Overview of the mixed-methods bibliometric-qualitative approach

This study employs a mixed-methods research design, integrating quantitative bibliometric analysis with systematic qualitative synthesis. This approach is increasingly recognised as robust for conducting comprehensive literature reviews in the built environment and policy studies, as it leverages the strengths of both methods while mitigating their individual limitations (Debrah et al., 2023; Bazeley, 2024). Bibliometrics provides an objective, macro-level mapping of the field, identifying publication trends, influential works, key journals, author networks, and thematic clusters through statistical analysis of publication data (Donthu et al., 2021; Hoang, 2025; Mukherjee et al., 2022; Öztürk et al., 2024). The qualitative systematic review then allows for an in-depth, critical examination of the content, arguments, and contextual nuances within the selected literature, facilitating theory building and gap identification (Makateng and Mokala, 2025).

To ensure the rigour and trustworthiness of the qualitative synthesis, inter-rater reliability was established. Specifically, two independent reviewers collaboratively coded a random sample of 20% of the included articles (n ≈ 51), discussing and resolving any discrepancies in thematic interpretation through consensus meetings. This process, consistent with best practices for systematic qualitative reviews, enhanced the consistency, accuracy, and reproducibility of the thematic analysis (Ahmed et al., 2025). To ensure transparency, reproducibility, and rigour, the review process was guided by the Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) framework (Page et al., 2021; Seidu, et al., 2025). PRISMA provides a standardised protocol involving four key stages: identification, screening, eligibility, and inclusion. The methodological workflow is visualised in Figure 1 and described in detail in the subsequent sections. Review framework.

Figure 1 shows the various stages of the review: stage 1, stage 2, and stage 3. Accordingly, the initial stage of this study comprises the search for publications using various search platforms and strategies. A set of data collection strategies from extant literature is required to retrieve relevant data, since it defines the knowledge framework based on which research deduction, idea inception, and conclusions are made. To increase data validity, quality, and reliability, it is significantly important to include all the available research terms based on previous research. The subsequent paragraphs detail the various stages of the review.

Data retrieval strategy and search parameters

Search data parameters for document retrieval.

Inclusion and exclusion criteria

A multi-stage screening process was applied to refine the initial dataset by categorising it into document type, language, publication date and relevant screening. The search was initially limited to peer-reviewed journal articles, as articles undergoing rigorous peer review ensure a baseline of academic quality and are considered the most authoritative source for knowledge synthesis (Darko et al., 2020), a step which removed books, book chapters, conference papers, and editorials to reduce the count to 473. Subsequently, the study was restricted to articles published in English; while this introduces a potential bias towards Anglophone research, it was necessary for practical reasons of comprehension and analysis by the authorial team and ensures accessibility for the intended international audience (Raitskaya and Tikhonova, 2020), a filter that removed 23 articles to leave 450. Furthermore, a 10-year publication date window from 2015 to 2025 was imposed to capture the evolving dynamics of post-Global Financial Crisis housing markets, the rise of financialization (Çelik, Ö. 2024). and contemporary policy debates (Gusenbauer and Haddaway, 2020), acknowledging that technological and financial innovations significantly reshape housing markets within such a timeframe (Al-haimi et al., 2025), which yielded 269 articles. Finally, these 269 articles underwent a manual relevance screening of titles and abstracts, where articles focusing on tangential issues, such as pure real estate valuation, architectural design of public housing without a financing component, or macroeconomic studies of housing prices without linking to mortgage mechanisms, were excluded, resulting in the core dataset of 254 articles for analysis.

Data analysis techniques

The analysis proceeded in two interconnected phases. Phase 1 consisted of a Bibliometric Analysis, for which the bibliographic data of the 254 articles were exported from Scopus and analysed using VOSviewer software (version 1.6.20), a powerful tool for constructing and visualising bibliometric networks based on co-occurrence data (Bukar et al., 2023) To answer RQ1, a Performance Analysis was conducted, extracting and visualising metrics such as annual publication output, leading source journals, most productive countries/regions, and highly cited documents. To understand the intellectual structure (RQ1), Science Mapping was performed through a keyword co-occurrence analysis, which identifies the main concepts within the field and clusters them thematically, thereby revealing the relationships between topics like “financialization,” “homeownership,” and “housing policy.” Phase 2 involved a Qualitative Systematic Analysis, where a systematic, in-depth content analysis of the full texts was conducted to address RQ2, RQ3, and RQ4. Following established practices for qualitative systematic reviews (Haffner and Hulse, 2019), this analysis involved thematic coding using both inductive and deductive approaches to identify recurring themes, arguments, empirical findings, and policy recommendations. Furthermore, the Fishbone (Ishikawa) Diagram was adopted as an analytical framework to synthesise and categorise the root causes (bones) and effects (head) of the HA crisis in the context of MF, a tool ideal for organising complex, multi-causal problems (Kumah et al., 2024). Finally, a synthesis and gap analysis were performed to elaborate on the interconnected drivers, critique existing strategies, and clearly delineate areas where the literature is silent or underdeveloped.

Scientometric analysis and research landscape

Publication trends and growth

The annual publication trend (Figure 2) serves as a barometer of academic and policy interest in the MF-HA nexus. A clear upward trajectory has been observed over the past decade, interspersed with significant peaks. Publication volumes remained relatively modest from 2015 to 2018 but began a marked ascent thereafter. The year 2020 (30 articles) shows a notable spike, likely reflecting intensified scrutiny of housing markets and household vulnerability during the COVID-19 pandemic. The trend reaches its zenith in 2024 (37 articles), with 2025 (36 articles) projected to maintain this high level of engagement. This consistent growth, particularly in recent years, underscores the escalating global recognition of housing affordability as a critical, unresolved socio-economic challenge and the contentious role of finance within it. The increasing scholarly output signals a vibrant and evolving field, responding to real-world crises such as rising interest rates, post-pandemic housing inflation, and growing inequality. Annual trend of publications in MF-HA issues.

Keyword Co-Occurrence and thematic clusters

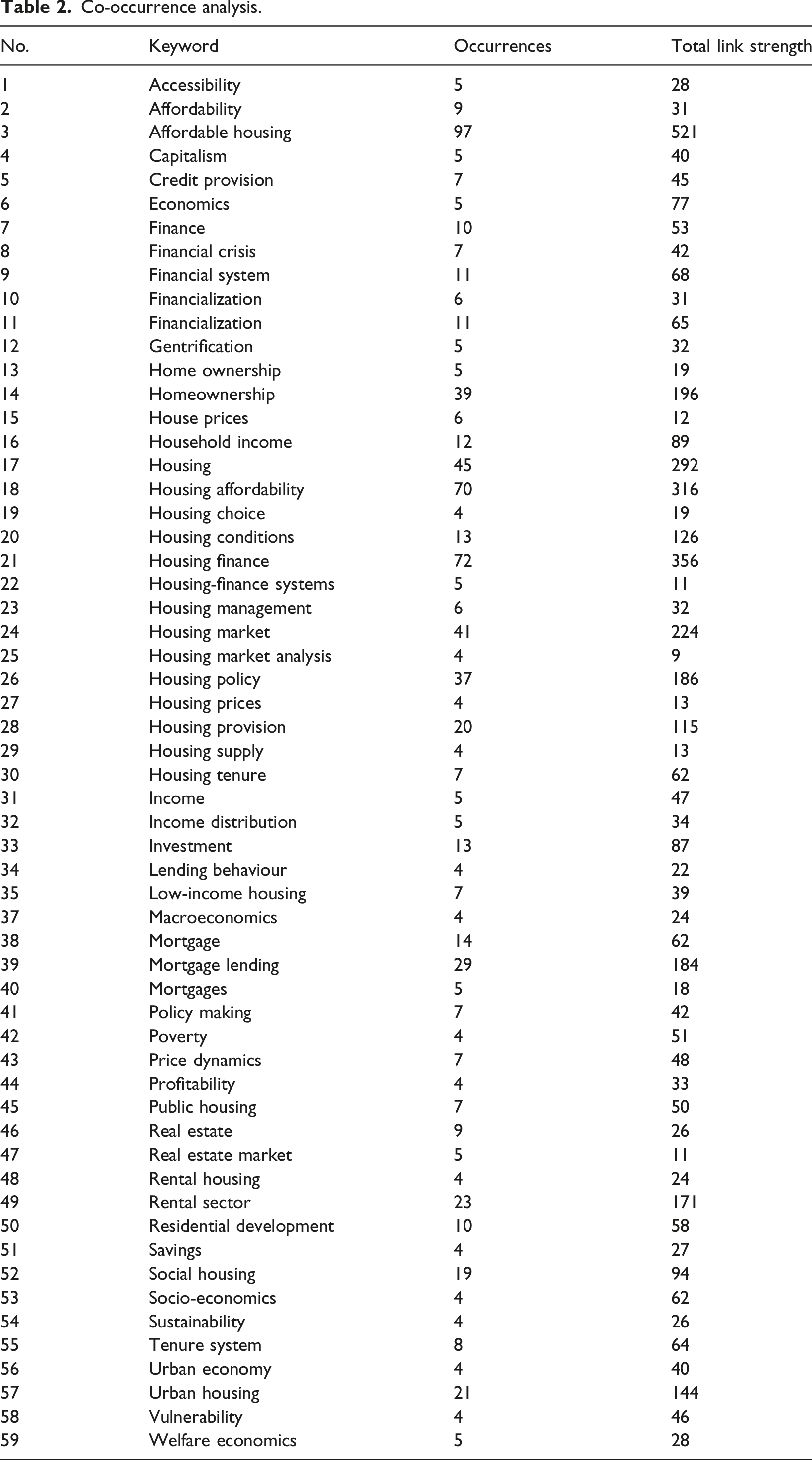

Co-occurrence analysis.

Keyword Co-occurrence cluster.

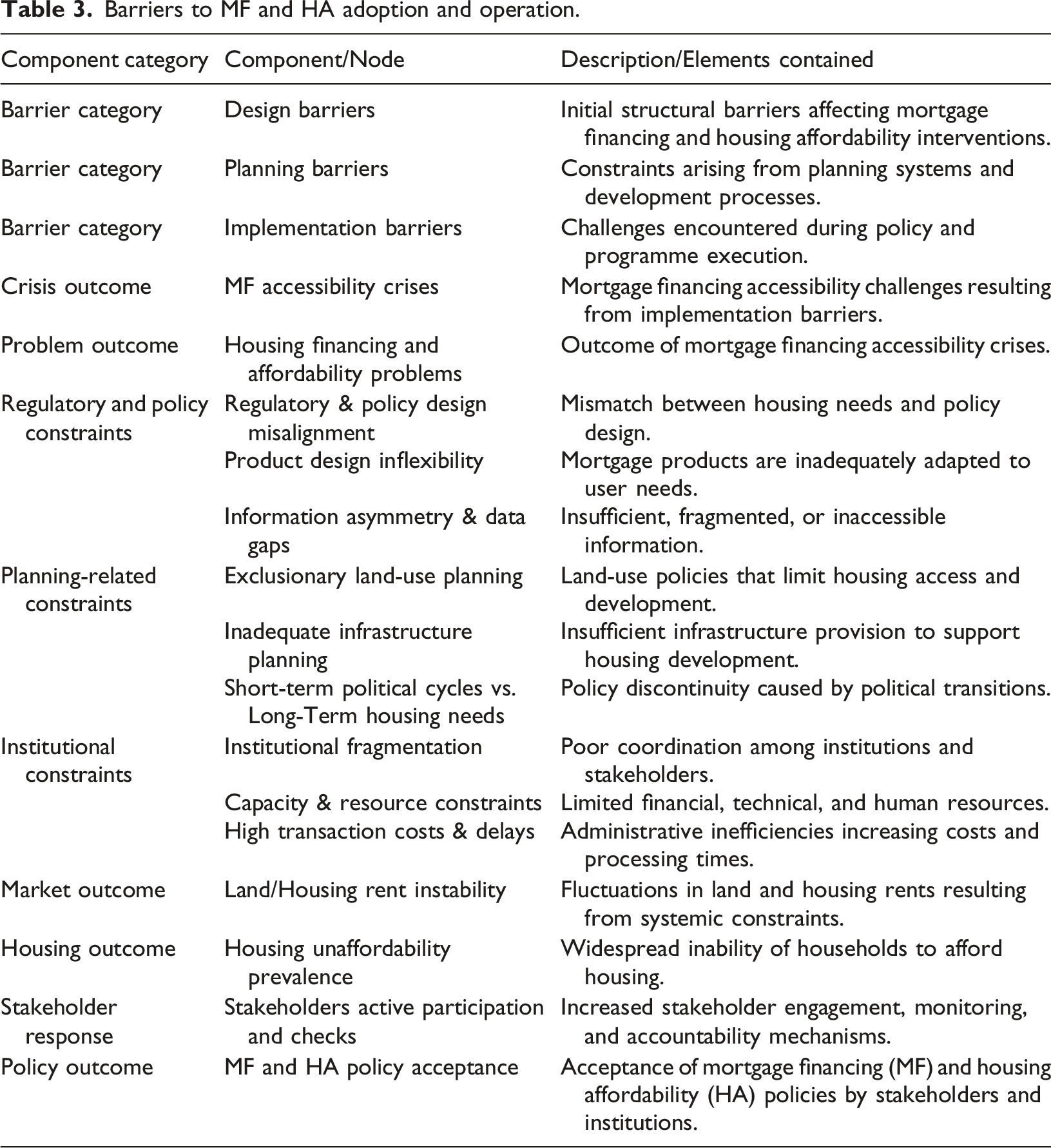

Barriers to MF and HA adoption and operation.

The visual network map in Figure 3 illustrates that nodes represent keywords and links represent co-occurrence. Larger nodes indicate higher frequency. Distinct colour clusters emerge, for example, a red cluster around “affordable housing,” “housing policy,” “public housing”; a green cluster around “housing finance,” “financialization,” “homeownership”; a blue cluster around “housing market,” “house prices,” “rental housing”.

The analysis, as shown in Figure 3 reveal three core interconnected thematic pillars with reference to literature on housing studies. The first is the Policy and Supply Pillar, centred on concepts such as affordable housing, housing policy, public housing, and social housing. This domain focuses primarily on state intervention, subsidy mechanisms, and the direct provision of below-market housing. The second, the Financial Systems Pillar, is anchored by key terms such as housing finance, financialization, homeownership, and mortgage lending. It interrogates the role of credit markets, securitisation, and the transformation of housing into a financial asset. Third is the Market Dynamics Pillar, which revolves around the housing market, including house prices, rental housing, and housing market analysis, focusing on price determinants, supply-demand imbalances, and rental affordability. Critically, the high link strength between keywords such as “affordable housing” and “housing finance” or between “housing affordability” and “homeownership” visually and quantitatively confirms that the literature itself is fundamentally grappling with the intersections between these pillars, the very focus of this review.

Influential publications and citation impact

Citation analysis helps identify seminal works that have shaped the discourse. The most cited articles often provide foundational theories or compelling empirical evidence. Key among them is the work of (Wijburg and Aalbers, 2017), which introduced the concept of “alternative financialization” in the German housing market, highlighting how even non-anglophone models are increasingly shaped by global financial logic. Ryan-Collins (2021) is highly influential for its analysis of the “housing-finance cycle,” arguing that feedback loops between bank credit and land/house prices inherently drive inequality and unaffordability. Fainstein (2016) and Kosīte et al. (2025) are also pivotal, linking financialization to urban justice and housing tenure to mental health outcomes, respectively. These highly cited works underscore the field’s engagement with critical political economy perspectives and its concern with the social consequences of housing financialization.

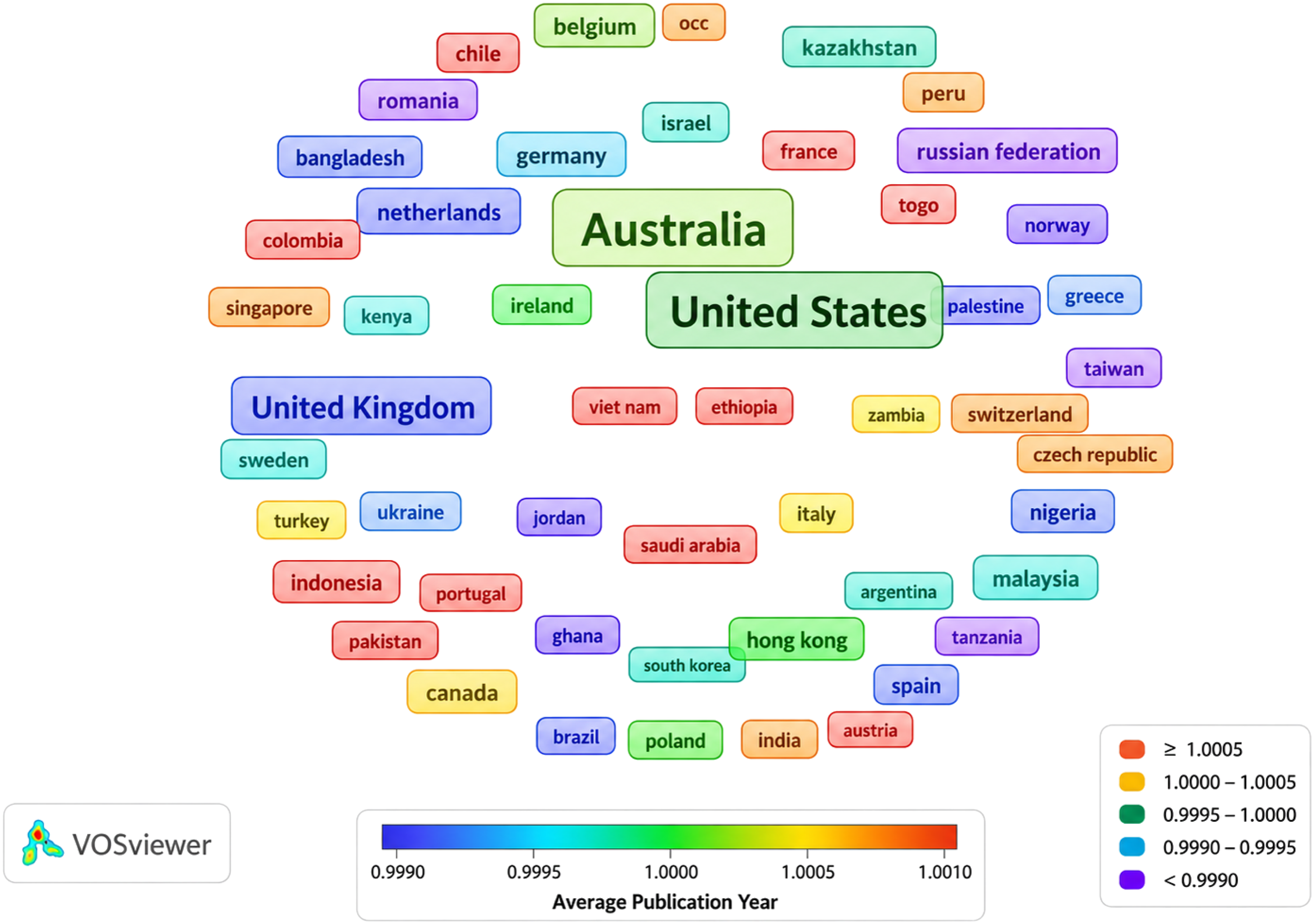

Geographical distribution of research output

The geographical analysis (Figure 4) reveals a significant concentration of research output. The United States (USA) is the dominant contributor, followed by Australia and the United Kingdom (UK). This triad accounts for a disproportionate share of publications. Other European nations (e.g. Germany, Sweden, and Spain), Canada, and China also feature prominently, but with lower volumes. Geographical distribution of publications on MF and HA.

It illustrates a world map overlay with colour intensity indicating publication volume. The USA, Australia, and the UK are the brightest hotspots. Western Europe and East Asia (China) show moderate activity. Africa, South Asia, and large parts of South America appear with minimal or no intensity.) This distribution points to a critical geographical paradox: while the most severe quantitative housing deficits and affordability crises are often felt in the rapidly urbanising nations of the Global South (Africa, South Asia, Latin America), the academic and policy discourse remains largely framed and dominated by scholars and evidence from the Global North. This indicates a substantial gap in context-specific research from the regions where innovative, scalable solutions are most urgently needed. The dominance of Anglo-Saxon countries also reflects their historical experience with mortgage-led housing models and their central role in the 2008 Global Financial Crisis, which triggered a wave of critical scholarship on mortgage markets.

Qualitative synthesis: Drivers, barriers, and the systemic crisis

The fishbone analysis: Deconstructing the systemic failure

To synthesise the complex, multi-causal nature of the housing affordability crisis within the context of mortgage financing, a Fishbone (Ishikawa) diagram was constructed (Figure 5). This framework organises the root causes identified across the literature into six interconnected categories (“bones”) that collectively lead to the central problem (“head”), thus Systemic Housing Insecurity and Unaffordability, as shown in the subsequent paragraphs. The fishbone diagram.

The analysis of the thematic categories demonstrates that the relationship between mortgage finance and housing affordability (MF-HA) is highly systemic, multidimensional, and interconnected. Financial systems emerged as the central mechanism through which mortgage finance is expected to improve housing affordability; however, the literature shows that this mechanism frequently produces unintended consequences. The pro-cyclical nature of mortgage finance expands credit availability during periods of economic growth, thereby inflating housing prices, while contractions during economic downturns intensify market instability and exclude vulnerable households from homeownership opportunities (Brueckner, 2013). This challenge is further reinforced by the financialization of housing, a process through which homes are transformed into tradable financial assets rather than social necessities. Consequently, speculative investment diverts financial resources away from owner-occupiers and pushes housing prices beyond local income levels, thereby worsening affordability conditions (Hochstenbach and Aalbers, 2024; Wijburg and Aalbers, 2017). In addition, easy access to mortgage credit can generate excessive household indebtedness, leaving borrowers vulnerable to income shocks and interest rate increases, thus transforming mortgage finance into a source of financial fragility rather than affordability (Cheng and Chiu, 2020; Liu, 2023).

These financial pressures are strongly influenced by policy and governance structures, which operate either as enabling or constraining frameworks within housing systems. The literature indicates that inconsistent, ideologically driven, and short-term housing policies frequently fail to create stable conditions capable of supporting affordable housing supply (August & St-Hilaire, 2025). Moreover, excessive dependence on market-oriented approaches and Public-Private Partnerships (PPPs) often prioritises investor profitability over broader social welfare objectives. The absence of policies promoting decommodification further allows market forces to dominate housing systems unchecked, thereby undermining the treatment of housing as a social right rather than a commercial commodity (Kumnig and Litschauer, 2025).

These governance failures are directly reflected in market dynamics, which represent the visible manifestation of the affordability crisis. Rapidly increasing land and housing prices, market volatility, and unaffordable rents continue to intensify affordability pressures across urban areas. Existing studies identify land scarcity, often reinforced through restrictive zoning systems, as a major structural driver of rising housing costs (Chen et al. 2025). Consequently, the rental sector increasingly mirrors ownership unaffordability, with rent burden becoming a persistent condition for many low-income households (Sharma and Samarin, 2021).

The affordability crisis also generates profound social and equity implications that disproportionately affect vulnerable populations. Low-income households, young first-time buyers, and historically marginalised groups frequently experience structural discrimination in lending practices and zoning systems, thereby limiting equitable access to housing opportunities (Haycox et al., 2024). Such exclusion contributes to displacement, gentrification, social fragmentation, and declining community cohesion, while simultaneously producing severe mental and emotional stress among affected populations.

At the same time, supply and development constraints represent critical physical bottlenecks within the housing system. A chronic undersupply of adequate housing, particularly within high-demand urban centres, continues to drive affordability challenges globally (Kholodilin, 2024). As a result, many households resort to informal and incremental housing solutions that remain excluded from formal mortgage systems and institutional financing structures (Amoako and Boamah, 2017; Achumie et al., 2024). External shocks further intensify these systemic weaknesses by acting as stress tests on the entire housing system. Events such as the 2008 Global Financial Crisis and the COVID-19 pandemic exposed and amplified existing structural vulnerabilities, triggered evictions, altered housing demand patterns, and tested the resilience of housing safety nets (Dunga, 2023).

Overall, the Fishbone analysis clearly demonstrates that the MF-HA problem is systemic, implying that isolated interventions targeting only one dimension are unlikely to produce sustainable affordability outcomes and may even worsen existing market distortions.

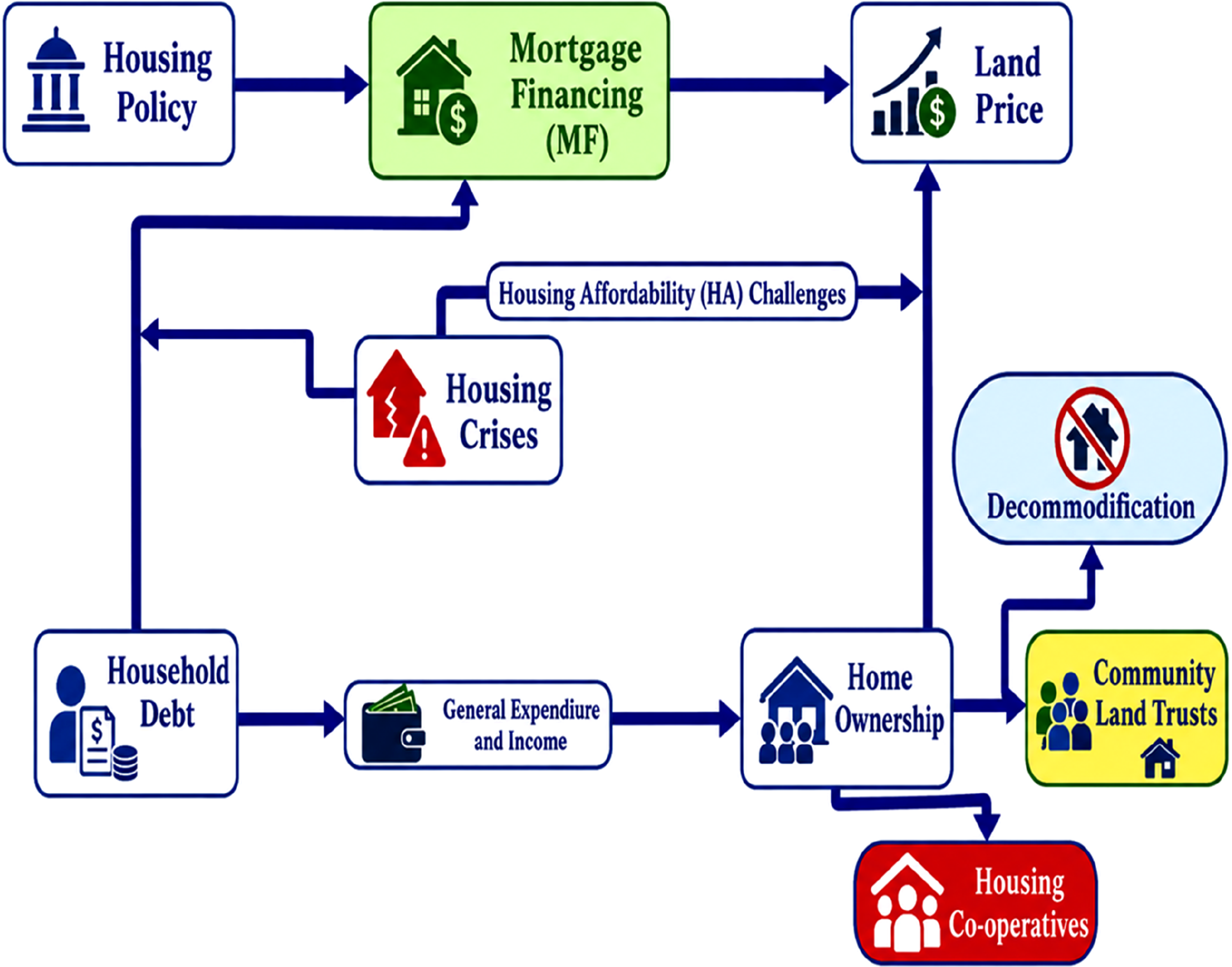

The vicious cycle of mortgage financing and affordability

Building on the systemic view, the review identifies a self-reinforcing vicious cycle (Figure 6) that often characterises the MF-HA nexus, particularly in liberal market economies. This cycle typically begins with the policy goal of expanded homeownership, where governments promote it as a means of wealth-building and stability. Through policies that incentivise banks to lend, such as government guarantees or securitisation, an expansion of mortgage credit follows. Synergistic vicious cycle of MF and HA.

Consequently, this easier credit increases effective demand from buyers; however, when housing supply is inelastic due to planning restrictions or slow construction, the primary result is the bidding up of prices. This leads to reduced real affordability, as house prices rise faster than incomes and the purchasing power of mortgages decreases, causing the homeownership goal to recede for new entrants. In response, political calls for more credit or intervention typically emerge, often doubling down with “affordable” loan schemes, shared ownership, or first-time buyer subsidies.

These measures then re-inject subsidised demand into the same supply-constrained market, which frequently raises the price floor and benefits existing owners or developers, thereby restarting the cycle. This cycle explains why, in many contexts, MF has become part of the affordability problem rather than its solution, and it highlights the critical importance of simultaneously addressing supply constraints (Bone 5) to break the cycle.

The qualitative synthesis crystallises the specific barriers that prevent MF from fulfilling its promise of enhancing HA. These barriers operate at multiple levels as depicted in Table 3. Table 3 presents a comprehensive overview of the key barriers influencing MF and housing HA. The findings indicate that affordability challenges arise from interconnected policy, planning, institutional, financial, and market-related constraints rather than a single factor. Regulatory inconsistencies, inflexible mortgage products, and information asymmetry reduce access to housing finance, while weak planning systems, inadequate infrastructure, and land-use constraints limit affordable housing supply. Institutional challenges, including fragmented governance, limited technical capacity, and high transaction costs, further undermine the effectiveness of housing finance systems. These barriers collectively contribute to mortgage accessibility constraints, housing shortages, rising housing costs, and declining affordability. The table also highlights the importance of stakeholder participation, policy coordination, and institutional accountability in improving housing outcomes. Overall, Table 3 supports the study's central argument that addressing housing affordability requires an integrated approach that simultaneously strengthens housing finance, planning, governance, and policy implementation to achieve sustainable and equitable housing delivery.

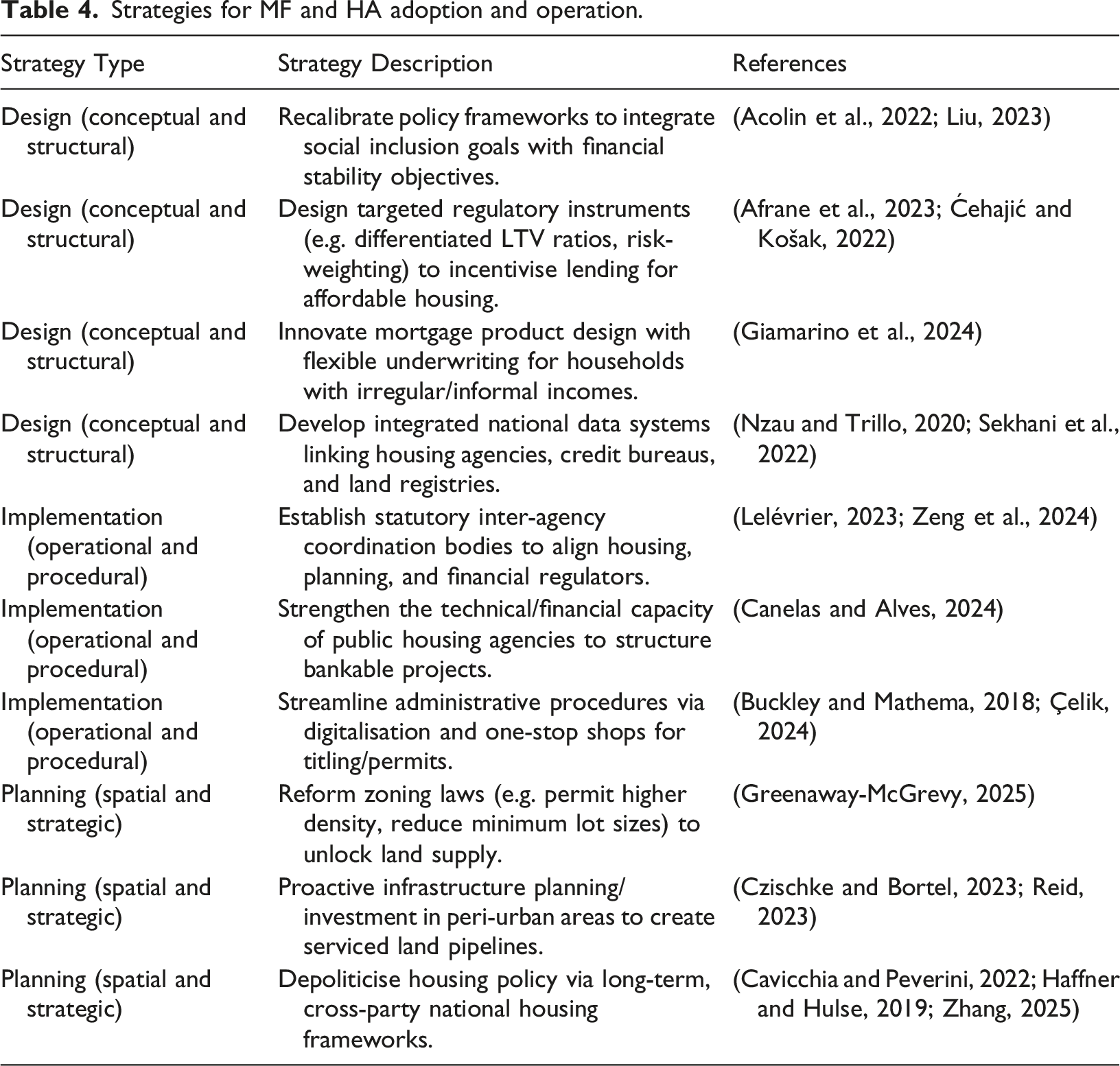

Emerging strategies for adoption and operation

Strategies for MF and HA adoption and operation.

Discussion

Interpreting the bibliometric and thematic landscape

The Scientometric findings paint a picture of a research field in ascent, one that is responsive to global crises. The dominance of keywords like “financialization” alongside “affordable housing” signifies a paradigm shift: housing is no longer analysed solely through the lenses of planning or social policy, but critically through the lens of political economy. The high productivity of the USA, UK, and Australia reflects their status as archetypal “homeownership societies” built on mortgage markets, which have subsequently experienced severe affordability crises and market failures, thus generating critical scholarly reflection. The geographical concentration of research, however, is a major limitation. The relative silence from the Global South in the high-impact journal literature means that context-specific models, such as incremental housing finance, community-led upgrading, or unique rental systems, are underrepresented in the global discourse. This creates a risk of policy transfer where solutions from the Global North are applied inappropriately to the vastly different institutional and economic landscapes of the South.

Reconciling the dual nature of mortgage financing

The core dilemma elucidated by this review is the dual nature of mortgage financing. It is simultaneously a tool for access and a driver of inflation. The determining factor is the elasticity of housing supply. In contexts with responsive planning systems and adequate land supply, an expansion of mortgage credit can increase homeownership rates without excessive price spirals. In supply-constrained markets, which characterise most major global cities, additional credit primarily bids up the price of a relatively fixed asset stock. Therefore, MF cannot be evaluated in isolation. Its impact on HA is contingent on the regulatory and spatial planning regime within which it operates. The most effective policies, as suggested by the literature, are those that couple demand-side financing with aggressive supply-side interventions.

The centrality of decommodification and alternative models

A significant thread in the qualitative synthesis is the growing scholarly and advocacy interest in decommodification and alternative housing models. The failure of market-mediated mortgage systems to serve low- and moderate-income households has renewed interest in models that remove housing (or the land beneath it) from the speculative market. Community Land Trusts (CLTs), housing cooperatives, and social/public housing represent pathways to “housing as a right” rather than “housing as an asset.” The review suggests that future housing-finance systems may need to be pluralistic, incorporating these non-market, decommodified sectors alongside reformed market mortgage products, with clear channels of public support for each.

The role of technology and data

An emerging theme, though not yet dominant in the keyword analysis, is the role of technology (PropTech, FinTech). Digital platforms can lower transaction costs, enable alternative credit scoring, and improve the efficiency of subsidy targeting and land management. Blockchain, for instance, holds promise for securing land titles in contexts with weak registries, a foundational requirement for mortgage lending. Future research must critically examine how these technologies can be harnessed to promote inclusion rather than further financialization and exclusion.

Research gaps and future directions

Based on a comprehensive synthesis of the literature, this review identifies several critical gaps that chart a clear course for future scholarly inquiry. First and foremost, there is an urgent need for rigorous, empirical research into context-specific housing-finance models for the Global South, particularly mechanisms that function within the unique institutional settings of Sub-Saharan Africa, South Asia, and Latin America; this includes evaluating microfinance for housing, community savings schemes, and the adaptation of Islamic finance. Simultaneously, the field would benefit from more longitudinal and comparative policy analyses, which could track the long-term impacts of specific interventions on affordability and access while comparing outcomes across different welfare state regimes to uncover effective governance structures. Furthermore, the emerging field of climate-resilient finance remains poorly integrated with core affordability concerns, thereby creating a significant gap. Consequently, research is urgently required to understand how to finance the retrofitting of existing affordable housing for energy efficiency without triggering displacement through rising costs, a process often termed “green gentrification.” In addition to these structural factors, more work could explore the behavioural economics underlying housing decisions, specifically how households perceive risk and navigate complex financial products under conditions of uncertainty.

Finally, and crucially, future research must delve deeper into the political economy of housing-finance reform, as understanding the power dynamics and vested interests that resist change is as important as designing technically sound policies. Therefore, addressing these interconnected gaps, from contextual models and policy impacts to climate resilience, behavioural insights, and political feasibility, is essential for advancing both knowledge and equitable practice in housing finance.

Limitations of the study

While this review offers a systematic analysis, it is important to acknowledge several inherent limitations. The reliance on the Scopus database alone, although comprehensive, introduces a potential database bias, as relevant studies indexed in regional or specialised repositories may have been omitted. Furthermore, the imposition of an English-only criterion creates a language bias, which likely excludes valuable research and perspectives published in other languages, particularly from non-Anglophone regions. In terms of scope, the contemporary focus enforced by the 10-year publication window, while providing a timely snapshot, may exclude foundational theoretical works from earlier periods, constituting a temporal bias. Methodologically, although the qualitative synthesis employed a structured Fishbone framework and transparent coding to enhance rigour, the process inherently involves interpretive subjectivity on the part of the researchers. Finally, it is crucial to recognise that, as a synthesis of secondary literature, this review identifies significant associations and critiques but cannot establish primary causal relationships.

Conclusion and policy implications

This bibliometric-qualitative review has systematically mapped and synthesised a decade of research on the complex relationship between mortgage financing and housing affordability, ultimately concluding that mortgage financing is a double-edged sword. While it remains an essential component of modern housing systems and can facilitate access, its current dominant form is deeply implicated in perpetuating and exacerbating affordability crises, particularly in supply-constrained markets. The problem is systemic, rooted in financial systems prone to pro-cyclicality, governance frameworks that prioritise market logic over social need, and planning regimes that restrict supply; therefore, the policy implications are profound. Policymakers must first abandon the notion that tweaking mortgage products alone can solve affordability, moving beyond silver bullets toward integrated strategies that simultaneously address credit access, land supply, planning reform, and direct subsidy.

Furthermore, governments should actively support and scale up alternative, decommodified housing models like Community Land Trusts and social housing, thereby creating a permanent stock of affordable housing insulated from market volatility. Concurrently, the public sector must take a leading role in creating digital land-information systems and in assembling and servicing land for affordable development, which reduces costs and de-risks projects for private actors. Moreover, solutions cannot be copied and pasted, requiring a place-based and context-sensitive approach instead. This is especially critical for policymakers in the Global South, who need to develop and invest in finance models suited to their large informal economies and unique urban growth patterns. Underpinning all these measures, however, is the need for stability and long-term commitment; indeed, the most important policy may be a political one, focused on forging a stable, long-term consensus on housing as essential infrastructure. Such stability is the fundamental prerequisite for attracting the investment needed to build affordable, sustainable, and inclusive cities for the future.

Ultimately, making mortgage financing a genuine tool for housing affordability requires a fundamental reorientation, from viewing housing primarily as a vehicle for wealth accumulation and financial profit to prioritising its function as a foundational pillar of social security, health, and equitable community development.

Footnotes

Acknowledgement

The authors declare their sincere appreciation to the Department of Building and Real Estate, Hong Kong Polytechnic University, for the financial support in the form of a PhD studentship to the corresponding author, including the payment of the Article Publication Charges, to bringing this research to fruition.

Ethical considerations

The study did not conduct experiments involving humans or animals, and therefore, no ethical approval was sought.

Author contributions

All authors contributed to the manuscript; however, the idea inception, drafting of the manuscript, literature search, and data analysis were done by Peres Ofori. Albert Chan and Rotimi Abidoye critically revised the work. Further revision was done by Seidu Sakibu, who also proofread and provided corrections to finalise the paper.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The Authors acknowledge the receipt of funding in the form of a studentship in support of the research from the Department of Building and Real Estate, Hong Kong Polytechnic University (PolyU), Hong Kong (25036872r).

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data will be made available upon request.