Abstract

As states move toward offering defined contribution retirement plans as an alternative or addition to traditional defined benefit pensions, they need to consider the preferences and long-term consequences for different groups of employees. This study looks at which plan employees choose when given the option of either a defined contribution or defined benefit plan. The strongest driver of that choice is education level where the most educated prefer defined contribution plans and the least educated stay in defined benefit plans. A unique contribution of this study is that we include region of origin as a study and determine that cultural differences influence plan selection. The study also explores the role of sex, age, and tenure. Challenging other studies on financial planning, these findings indicate that sex and age are not significant factors. This research was conducted using data from more than 4,000 employees from Florida International University and an interview with HR professionals. By understanding retirement preferences in a more nuanced way, we can better craft our approaches to retirement security and financial literacy training in public sector organizations.

Keywords

Introduction

Why might some public employees have defined benefit (DB) retirement plans as their primary pensions, while others have defined contribution (DC) plans 1 as theirs? Thirty years ago, when Herman Leonard (1986) sounded an alarm regarding chronic underfunding of many public pensions, that question was of limited relevance. Two generations later, the question is not only relevant, but of primary concern in an age when the DC option is an increasingly common choice for public employees (Sanford & Franzel, 2012). 2 The trillion dollar or higher unfunded liabilities facing state and local pensions (Amenson, Slobaugh, & Lahey, 2014; Burns, 2011; Holland, Goodman, & Stich, 2008; Novy-Marx & Rauh, 2009; Zelinsky, 2004) have obligated governments to consider pension plans that shift cost burdens from taxpayers to participants (Frank, Gianakis, & Neshkova, 2012). Jonathan Forman (1999) succinctly notes that “The debate over whether or not to shift away from defined benefit plans and toward defined contribution plans is now also squarely before state and local policymakers” (p. 188). Recent changes in governmental accounting (Munnell, Aubry, Hurwitz, & Quigby, 2012) assure that Leonard’s “quiet” underfunding of public pensions formerly given short shrift in accounting footnotes is now acutely transparent to citizens, elected officials, and employees, adding impetus to myriad pension reforms that reduce current and future pension obligations (Amenson, Slobaugh, & Lahey, 2014; Fletcher, 2011). The movement toward offering or requiring DC retirement plans is becoming more and more widespread. As of 2011, 18 states offered at least some form of a DC plan and that number continues to grow (Snell, 2012). In fact, as of 2019, Pennsylvania will no longer offer a pure DB plan to new employees; instead they will offer either DC or DB/DC hybrid approaches (Murphy & Thompson, 2017).

There are also signals that given a choice, employees are increasingly moving toward DC plans. For employees of the State of Florida, participation in DC options is growing. According to the Florida State Board of Administrator’s (2004, 2006, 2016, 2017) Annual Investment Reports, participation in the DC option has increased from 40,000 participants in 2004 to more than 177,000 in 2017. In the 10-year period from 2006 to 2016, new employees opting for a DC plan nearly doubled as 12% of new employees elected the DC option in 2006 compared with 23% in 2016. Given the increasing prevalence and participation in DC plans, it is important to understand the factors that drive the choice between DB and DC plans. This study explores whether and how education, region where someone is born, sex, age when they are hired, and length of service influence the decision between a DC and DB plan.

The question of drivers of the choice between DB and DC retirement plans is indicative of key employment and demographic changes that the public sector needs to embrace in developing recruitment and retention plans, and in supporting public sector employees in long-term security and financial stability. As public sector employees show more mobility than previous generations, governments need to think of employee supports such as retirement benefits as places to compete for the best employees. Public organizations need to also be cognizant of how differences in benefit choices can institutionalize differences among various demographic groups. Recognizing the importance of these differences calls for a more nuanced approach to demographics than our traditional minority/nonminority distinctions. Inherent in all demographic variables, be they traditional variables or alternatives offered here, are cultural and ideological/political belief systems. The term demographic variables is broadly defined in this context to capture underlying political and cultural differences. This study seeks to identify which differences correspond with employee’s preferences for a traditional DB pension versus a more market-based DC option. Developing a more sophisticated understanding of demographic differences is an opportunity for public organizations to act as a leader in creating dynamic benefits that attract and keep employees without exacerbating hidden disparities.

If there are underlying differences in who chooses DB versus DC plans, there is also a risk of adverse selection that could further exacerbate the actuarial shortfalls experienced by many DB plans. Adverse selection tells us that those with better information about their actuarial futures and about the future solvency of plans will make different decisions than those with less information. DB plans rely on continued contributions from current employees. If those with the highest earnings (often correlated with education, gender, and mobility) prefer DC plans, DB plans could become increasingly underfunded. Essentially, States often provide DC options to relieve current and future financial obligations related to operating a DB plan, but this option may give the most valuable contributors a way out of a traditional plan leaving the plan more fiscally vulnerable (for further discussion of adverse selection, see Brown & Weisbenner, 2007; Investment Company Institute, 2000; National Association of Insurance Commissioners, 2011).

Shifts in demographics and the relationship between employers and employees captured here are indicators of broader questions for public administration scholars. They signal underlying movements that are quietly altering public sector employment. Gaus called upon the field in 1947 to recognize that the ecological changes in people, place, technology, public philosophy, and crises explain changes in government itself. Here, we see that public sector changes reflect an overall workforce movement that is decades old in the private sector and the country as a whole. More recent calls to public administration come from Roberts (2013) and Durant (2014). Roberts (2013) asserts that public administration is missing “ . . . a recognition of the relevance of large forces as variables in explaining the path of administrative development: why governments adopt and abandon functions, and why they use certain structures or techniques to execute those functions” (p. 48). Likewise, Durant (2014) offers a six-component framework for considering these large forces in society and public administration that includes “recapitalizing personnel assets” and “reengaging financial resources.” This study seeks to explore these large-scale variables in terms of the financial and human capital questions related to retirement planning movements in public organizations.

Retirement Planning With Changing Workforce–Employer Relationships

In an increasingly white-collar service economy, it is important to note that we are shifting to a more mobile workforce and organizations with less of a long-term commitment to employees. In addition to facing the same balance-sheet challenges to sustaining a DB plan that the private sector faced 40 years ago, public organizations offer less institutional loyalty as many states move to right-to-work models where traditional worker protections restricting the ability of public organizations to fire employees and eliminate positions are disappearing. In an age where the public sector is pressured to cutback, pensions and retirement plans pose critical questions for the financial security of both employees and organizations. In theoretical terms, social exchange theory posits that human relationships are based on cost-benefit decisions that support interdependence. The concept is first proposed by Homans (1961) and continued by Emerson, Thibout, and Kelley (see Emerson, 1976, for an overview of their work). In the context of employment, there is an implicit contract between employees and employers where employers offer economic and emotional supports for employees in exchange for employee engagement and commitment. When the long-term benefits that employers provide to employees shift, that relationship changes. Whereas two generations ago employees entered into government with the expectation that they would stay with their organization for their full career and receive a comfortable pension upon retirement, newer employees expect less of a commitment between organizations and employees. For employees in DC retirement plans, the organization does not have the leverage of requiring many years of work for employees to be “vested” in their retirement plan. The vesting period for DC plans is only on matching funds supplied by the employer and is often as little as 1 year. Instead of encouraging retention through vesting, employers can use tools like generous matching programs to foster the commitment once gained through traditional DB pension requirements.

Financial sustainability aside, changes in the workforce augur for DC adoption. Younger workers, particularly millennials, may not abide by the multiyear vesting and decades-long tenure associated with the traditional public pension (Cong, Neshkova, & Frank, 2013). Kelly and Shreetama (2015) note that younger workers seek financial services that align with shorter expected tenure in any given job. This reflects, in part, the Great Recession’s impact on younger workers and their employment opportunities. Attenuated public sector motivation among younger workers may also shorten tenure (Chetkovich, 2003; Ertas, 2016). The upshot is that younger government employees may embrace the portability associated with the DC model and bring greater turnover to the public workplace as a result (Lewis & Stoycheva, 2016).

While younger employees may favor portability, there are mixed findings as to the implications for organizations. The traditional conceptualization of turnover says that it is expensive and damaging to organizations (e.g., see Abbasi & Hollman, 2000; Cascio, 2006). However, there is also recent research from the private sector that considers turnover as having a curvilinear relationship where higher turnover can benefit an organization (Park & Shaw, 2013; Shaw, Gupta, & Delery, 2005).

Another factor at play in the DB–DC choice is inertia. Employees may opt for one or the other with little or no concern for long-term financial well-being (Carroll, Choi, Laibson, Madrian, & Metrick, 2005; Madrian & Shea, 2001). Participants given a DB–DC choice at hire or subsequently may effectively throw up their hands and choose a plan suggested by peers (Duflo & Saez, 2002). This behavior is attributable to widespread financial illiteracy 3 (Lusardi & Mitchell, 2005; Munnell, 2012). Viewed through this prism, the DB–DC choice may overwhelm employees by requiring complex decisions about expected length of tenure and anticipated rates of investment return. Most public organizations do not provide low- or no-cost third party financial advisors to assist with these decisions (Cong et al., 2013; Holland et al., 2008). This suggests the DB–DC decision may have elements of randomness as opposed to rational, long-term financial planning.

Demographics play a critical role in the DB–DC choice. Gender, age, education, and race are generally viewed as predictors of public pension preference (Frank, Condon, Dunlop, & Rothman, 2000). Literature suggests that younger, better educated males prefer the DC model, whereas women and minorities prefer the DB model, controlling for education (Frank et al., 2012). These preferences may reflect a number of factors, including risk tolerance and overarching belief in the fairness of the economic system. They may also reflect America’s inequity of wealth; minorities have fewer assets than White counterparts with commensurately lower propensity to acquire the basics of asset management required under the DC model (Choudhury, 2001). Demographics include cultural factors that are often multigenerational as well. Payne, Yorgason, and Dew (2014) found that family socialization of children regarding financial decision-making had long-term influence on retirement planning.

Another possible predictor of pension choice is region of origin. The International Monetary Fund (2011) notes considerable difference in retirement asset allocation by nation. In general, North America has greater stock participation in retirement accounts than Europe, with the exception of the United Kingdom, where stocks are a higher proportion of retirement assets than the United States. These differences reflect cultural and economic preferences related to risk, political stability, and economic growth. Hence the choice between a DB and DC approach may be influenced by the role of the state in securing old age benefits in addition to political and market stability that furthers long-term wealth creation.

Region of origin may also affect the DC-DB decision as a result of macroeconomic performance, property right security, and financial reporting transparency. Individuals from countries where financial markets are stable and investment approaches are familiar may be more likely to opt for a DC model. G. L. Clark, Strauss, and Knox-Hayes (2012) summarize the impact of national origin by stating that recent research on the costs of deep, long-standing decisions, including those that involve retirement savings, suggests that where we begin from in time and space can make a profound difference to both the path of asset accumulation

People from countries where markets are either unstable or underperforming, or subject to uncertain property rights, may view the DB versus DC choice differently than plan participants from developed countries with transparent markets and more secure property rights.

In the U.S. context, retirement savings are obtained in multiple ways: employer sponsored plans, social security through the government, and individual planning and savings independent from either employers or government. In European systems, the proper role for government-provided pensions and privatization has been a key debate in recent decades. These debates in Europe and across the globe are often centered on cultural values as well as technocratic analyses of policy options (e.g., see Hyde, Dixon, & Drover, 2003; Orenstein, 2011; Whiteside, 2006). This line of literature points to the need to factor cultural differences into our understanding of employee decisions.

Another theoretical basis for regional differences is Hofstede’s (2011) concept of cultural differences based on six dimensions: power distance or tolerance of power inequity, individualism versus collectivism, desire to avoid uncertainty, masculinity, long-term orientation, and indulgence versus restraint. These cultural norms influence individual decision-making including attitudes toward finance and retirement. Those who are culturally oriented toward individualism may prefer the market-based DC approach over a more collectively focused DB. Capturing the individual versus collective orientation is an important component of regional differences as the collective orientation corresponds with more left-leaning preferences for social supports. The desire to avoid uncertainty corresponds with a preference for the predictable payment stream of a DB model. Long-term orientation refers to the propensity to attach more value to the future. Similarly, those who prefer restraint may emphasize saving over spending. In both of these cases, a long-term saving orientation may correspond with a DC model that allows for more variation in contributions and greater personal investment in the future.

Other factors at the organization level relate to what might be termed the informational climate related to investment choice. Evidence suggests that employees recognize the fine line that exists between sales and financial advising (Frank et al., 2000; Holland et al., 2008; Lusardi & Mitchell, 2005). Thus, “best practices” in the financial planning realm suggest independent advising that is separated from direct sales (Sanford & Franzel, 2012). At a more granular level, recent U.S. Department of Labor regulations (Siegel, 2016) regarding retirement accounts and increased competition among major mutual fund providers (Jaffe, 2013; Waggoner, 2016) may have the salutary effect of lowering lifetime costs of asset accumulation. Nonetheless, lower costs will shrink commissions to the point where clients with smaller accounts may receive online “robo-advising” model portfolio decision guidance with little attention to personal circumstances (Leary, 2016). 4

The upshot is that the DB–DC choice is likely to entail an array of factors. Organizational drivers “set the table” in terms of DB versus DC options. They also include availability of training in basics of financial planning as well as the compensation of financial representatives responsible for distributing financial services. At the individual level, past research suggests that pension choice is also determined by sociological and economic characteristics that reflect risk preference, financial literacy, cultural patterns, and market dynamics that influence savings patterns from childhood (Rodriquez & Saavedra, 2016).

Research Hypotheses

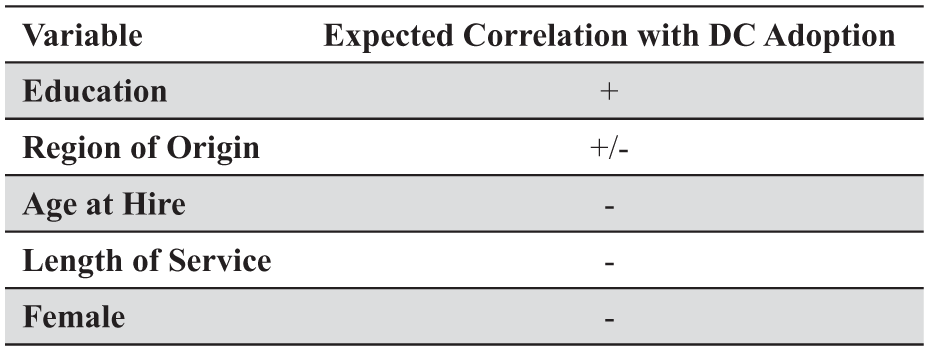

Figure 1 sets forth the independent variables in our model. It is a shorthand representation of the factors expected to play a role in the DB versus DC choice made by employees within 60 days of hire at the institution being studied.

Independent variable and expected correlation with DC adoption.

Education is the strongest predictor of financial literacy (Behrman, Mitchell, Soo, & Bravo, 2010; Lusardi, 2008). Literacy drives willingness and ability to manage personal finances. This makes the DC model, which requires participants to make investment choices and select a financial provider, less foreboding than it would to those in lower education brackets, typically defined as below a baccalaureate. Better educated participants have longer time horizons due to sounder financial footing, with concomitant acceptance of short-term financial market shocks en route to long-term gains (Behrman et al., 2010), making the DC model’s market volatility less challenging.

A key factor in the choice between a DB and a DC approach is portability. Better educated participants may envision careers spanning multiple employers—a realistic assumption in light of the average tenure being 4.2 years for all workers and 7.9 years for workers 45 to 54 years old (U.S. Bureau of Labor Statistics, 2016). This turnover negatively affects DB pensions. According to Alicia Munnell (2012), most public employees benefit from DB benefit accrual if tenure is longer than 15 years. Prior research (Jacobs & Watkins, 1984) suggests that a job change after 10 years diminishes DB pension wealth relative to the DC alternative. In this more mobile workforce, the traditional conceptualization of a DB pension as “golden handcuffs” that keep employees in their jobs by holding them to a larger future pension gives way. Thus, better educated employees may opt for the DC model to match their higher levels of financial literacy and expected career mobility and to maximize postretirement income.

A unique contribution of this research is our ability to explore whether region of origin affects one’s understanding of and comfort with private market investment strategies versus state-provided retirement benefits. Empirical evidence suggests significant cultural differences in consumption and saving patterns across nations (Jain & Joy, 1997). This may reflect any number of factors, including the value placed on human capital development relative to broader consumption. It may also reflect life expectancy and the extent of the social safety net (Doshi, 1994). Regional differences also capture other elements of cultural differences and preferences including those included in Hofstede’s (2011) six dimensions of culture.

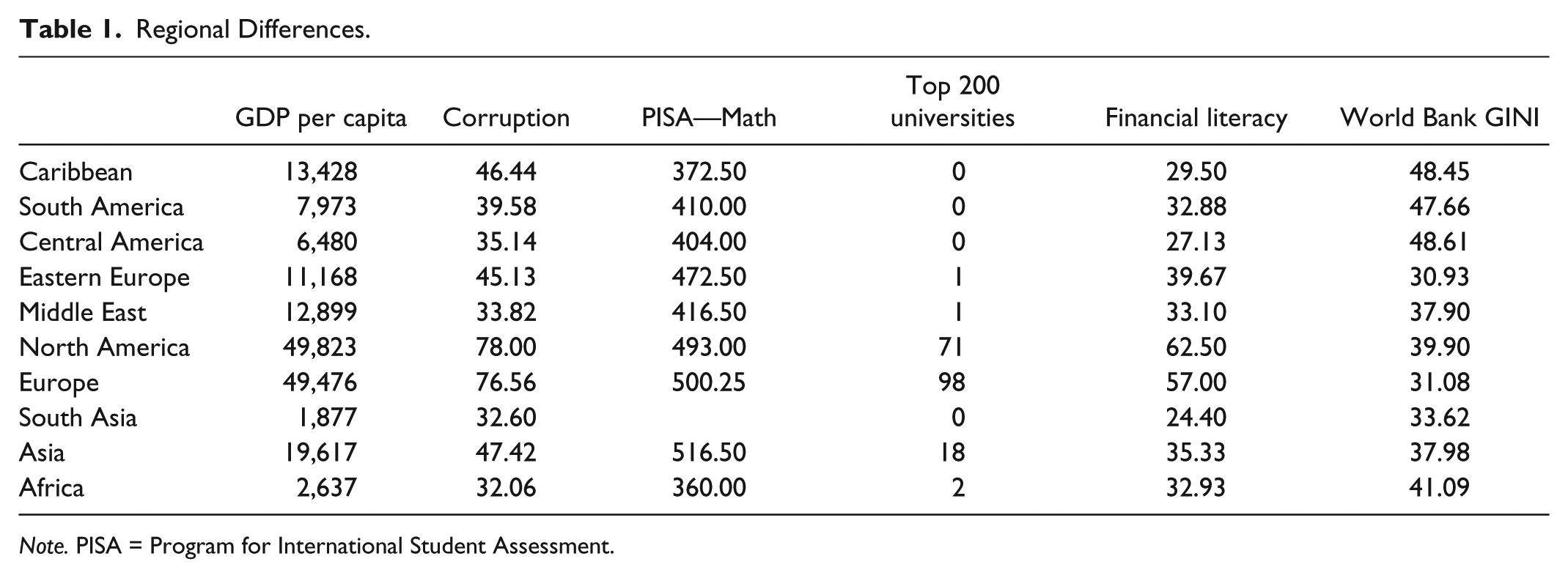

Thus, we compare people from various regions, including the Caribbean, South America, Central America, East Asia, South Asia, Western Europe, Eastern Europe, the Middle East, and Africa to the preferences of North American natives and test for region of origin as a driver of pension choice. For informational purposes, Table 1 gives regional data including per capita gross domestic product; corruption perception scores; Program for International Student Assessment (PISA) math scores; the number of top 200 universities in the Times Higher Education rankings; financial literacy scores from Klapper, Lusardi, and van Oudheusen (2015); and World Bank GINI scores. Corruption Perception Index scores are published by Transparency International and are on a scale from 0 (highly corrupt) to 100 (minimal corruption). PISA scores evaluate achievement by 15-year-olds in reading, math, and science where higher scores are better. A limitation of PISA scores is that they are only available for Organisation for Economic Co-Operation and Development (OECD) countries meaning that the countries that are most likely to be underachieving are excluded from this assessment. The GINI index measures wealth disparities in a community where a zero represents complete income equality and one represents maximum inequality (e.g., in a community of two people, one has all of the wealth and the other has nothing. These regional averages are based on countries within each region that are included in our sample. The information is limited because the measures are not consistently available for every country in the sample. Despite these limitations, the table indicates there are notable differences among the regions on critical variables relating to education, income, corruption, and inequality.

Regional Differences.

Note. PISA = Program for International Student Assessment.

Finally, another way that region is important is that people look to their social circles for advice. Peers, who may be of similar background, may reinforce individual preferences (Duflo & Saez, 2002). Individuals reduce their information costs by asking peers about retirement planning when given limited information and have limited time to make a choice about their retirement options. In our data set, employees have only 60 days from their hire date to commit to a retirement plan. Hence we expect that people heavily weigh the advice of those in their immediate community.

Given the exploratory nature of the use of region as a variable, we do not offer directional hypotheses for specific regions. Our discussion includes possible directions based on Hofstede’s cultural dimensions and other factors, but we do not find a sufficient history of application of these factors in the context of financial decision-making to confidently make assertions. Rather, the results of this study are a building block for future studies that can delve into specific components of societal differences that translate into variables influencing individual choices.

Immigrants from the Caribbean, Central America, and South America are less likely to prefer a DC plan for numerous reasons. Under Hofstede’s (2011) cultural dimensions, his research finds that the countries in these regions tend to prefer collectivism, avoiding uncertainty; focus on tradition and the present over the future; and emphasize indulgence over restraint. In addition, Latin American countries display high inequity as measured by the GINI index, and less political and economic stability than their North American counterparts possibly undermining trust in market-based approaches. All these factors point toward a preference for DB models over the DC option.

Countries in Eastern Europe tend to score high on individualism and restraint under Hofstede’s (2011) dimensions. These countries also have lower levels of inequality as measured by the GINI index. Movement away from Communist political systems may also contribute to distrust of collective approaches and favoring market-based options.

Western Europe appears very similar to North America for most indicators of regional differences including Hofstede’s dimensions, political stability, education, wealth, and inequality. Because of the commonalities in indicators and strong historical cultural ties between the regions, we do not expect to see differences between immigrants from Western Europe and North Americans.

Countries in South Asia show high levels of inequality in both GINI scores and in Hofstede’s (2011) dimensions. These countries also tend to favor collectivism over individualism. This paired with a history of lower participation in stock markets for most of the population leads us to believe that we may find a greater preference for DB plans.

East Asian societies show a greater orientation toward the long-term orientation in attitudes toward investment and favor restraint over indulgence (Hofstede, 2011). East Asia also shows levels of educational achievement and university systems that either exceed or compete with North American and Western European counterparts. These factors, paired with political stability and relatively heavy participation in stock markets argues for a greater trust in DC plans.

Countries in the Middle East and Africa both display high inequality, and preferences for collectivist values and low long-term orientation (Hofstede, 2011). This, combined with regional political instability, may encourage DB choices over more volatile market-based DC options. We are cautious about any findings for these regions as our sample size is low for people from these parts of the world.

Prior work (R. L. Clark & Pitts, 1999; Frank et al., 2000; Jacobs & Watkins, 1984) finds that older workers prefer the DB option. This may reflect the belief their “wandering days” are over and it is actuarially rational to vest and stay the course to normal retirement age. Conversely, younger workers who view their careers in relatively short stints may prefer the flexibility of the DC model (J.P. Morgan Asset Management, 2016; Lusardi, Mitchell, & Curto, 2010). For these workers, portability of pension benefits may be a significant plus.

This hypothesis is a modified version of its predecessor. But instead of examining chronological age, we test for recency of hire. This posits a belief in a post–Great Recession reality wherein hires of all ages view the DC model as more appropriate. From this vantage, new participants may prefer immediate vesting as a property right in addition to portability, if rightsizing and cost reduction are viewed as constants. Hence, “portability” may be seen as roughly synonymous with “survivability” in an economy characterized by generational lows in labor force participation (Kwok, Daly, & Hobijn, 2010).

Women invest differently than men (Bajtelsmit, Bernasek, & Jianakoplos, 1999). They tend to eschew stocks due to significantly higher risk aversion (Powell & Ansic, 1997). Other factors include lower income, poorer health, and longer lifespan relative to males in the same age cohort (Fisher, 2010). Women score lower than males on financial literacy, leaving them less capable and willing to engage in financial planning (Lusardi & Mitchell, 2008). On face, this makes the “self-management” of the DC model more challenging to women. Prior empirical testing (R. L. Clark & Pitts, 1999; Frank et al., 2000; Jacobs & Watkins, 1984) shows significantly lower preference for the DC model among women, controlling for education, tenure, and race. Hence we expect lower preference for the DC model in this study.

Study Context: Organization and Plan

This study was conducted at Florida International University (FIU). FIU is located in University Park, Florida, in the Greater Miami (Miami-Dade County) region. Founded in 1965, it belongs to the 12-campus State University of Florida System. FIU has grown from being an upper-division only institution with a handful of MA-level programs to a Carnegie Classification “Very High Research” University with a law and medical school. FIU is the fourth largest university in the United States, with 54,099 students as of the 2014-2015 academic year. The university employed 6,963 people including 1,208 full-time faculty/instructors, and 3,658 full-time noninstructional staff (FIU, 2015). FIU is a Hispanic Serving Institution. The student body is 59.5% Hispanic (of any race) while 20.2% is African American, 13.0% is White, 2.9% is Asian, and 4.0% identify as either two or more races, or do not report. The full-time faculty is also diverse: 53.5% White, 18.5% Latino, 5.9% Black, and 14.0% Asian, with 7.9% not reporting or claiming two or more races. Gender is also a factor of faculty diversity as women represent 43.4% of the faculty. The composition of the full-time staff more closely mirrors that of the students and the South Florida community with 52.5% Hispanic, 17.7% White, 11.1% Black, 3.0% Asian, and 15.6% either categorizing themselves as having two or more races, or not reporting. Women constitute 61.0% of the full-time staff (FIU, 2017).

FIU employees participate in retirement plans offered through the State of Florida. This means that FIU employees can carry their plan with them to any other state employer including all of public universities in Florida, the 67 county governments, and school districts. There are more than 100,000 employees in this system. The implication is that the DB retirement plan does not limit mobility within the state system where there are many job alternatives but does factor in to the ability to move outside of state employment.

In the State of Florida, all employees hired after 2001 have a choice between a DB and a DC plan. During the years of this study, employees are automatically placed in the DB plan unless they actively choose a DC plan within the first 60 days of hire. It is important to note that beginning in 2018, the State of Florida reversed the default option so that new employees will automatically be placed in the DC plan unless they opt-in to the DB plan (see Florida Enrolled SB 7022, 1st Eng. Approved, Chapter No. 2017-88).

After the initial decision or default placement, employees can change their retirement plan choice one time meaning that employees have little flexibility to move between plans. The DB plan requires employees to stay for at least 8 years before they are vested in the plan. If they leave before that date, they are reimbursed for their contributions with none of the employer contributions. If employees opt for the state’s DC plan, they are vested after 1 year. If they choose the private alternatives (Voya, VALIC, TIAA-CREF, or Metropolitan), they are vested immediately. The principal differences between the state and private DC option are cost and investment options; the state option is lower cost, but with few investment options, whereas the private providers are approximately 30 basis points higher in annual expense, but offer a wider range of investment, including overseas and alternative options. According to HR staff, very few opt for the state’s option given the delay in vesting and limited investment alternatives. It is important to emphasize that all those who are in DC plans have actively opted in or chosen them. In contrast, it is unclear whether those in DB plans are there because they chose them, or because they did not select a plan and thus landed in a DB plan by default.

If employees elect a DC plan, they are then faced with a second set of decisions about which provider to use and which funds to invest in with more than 20 options. In addition, providers also offer add-on products for employees to consider such as life insurance. While people do not have much flexibility in going between DB and DC plans (generally, only once during their careers), they can move among DC providers. However, surrender fees of some companies may curtail inter-provider switching.

Understanding the implications of these decisions and fee structures requires some financial literacy on the part of employees. Human resources professionals can provide the basic information to new employees, but do not offer recommendations or advice about options. While they do make efforts to offer general financial literacy trainings, there is no guarantee that employees will have access to additional training within the window where they can choose their retirement plan.

It is also worth noting that in August 2015, the private DC providers were obligated to lower the cost of their offerings. Most actively managed fund alternatives had reductions of 0.5% or more in expense ratios, reducing their average expense ratios to 0.5% to 0.8%, closer to Exchange-Traded Funds or Index Funds. Perhaps more importantly, the 1.0% “Mortality and Expense” charge on 403(b) plans was eliminated, even on existing accounts. While most of the revenue collected from these “M&E” charges cover the insurance component of variable annuity operations (i.e., returning principal to survivors in case of participant death during the accumulation period), a portion also goes to commissions, selling, and general expense. Reducing this expense is a plus for the consumer in terms of lifetime cash buildup. However, interviews with University HR staff suggest these cuts have dented the already limited advising financial representatives offered by the four above-referenced firms.

Another important consideration is that many people who work for the university are not eligible to participate in any of the retirement plans. Part-time employees, temporary employees, student workers, and those who work for contractors do not have access to plans. However, there are still many full-time employees of the university who serve in lower skill roles and participate in retirement plans. This is consistent with other organizations in both the public and private sectors. Exclusion of part-time and lower skilled workers means that people in many low-wage and service positions do not have any employer-based retirement planning available and are thus at greater risk for long-term financial insecurity.

Data, Variables, and Methods

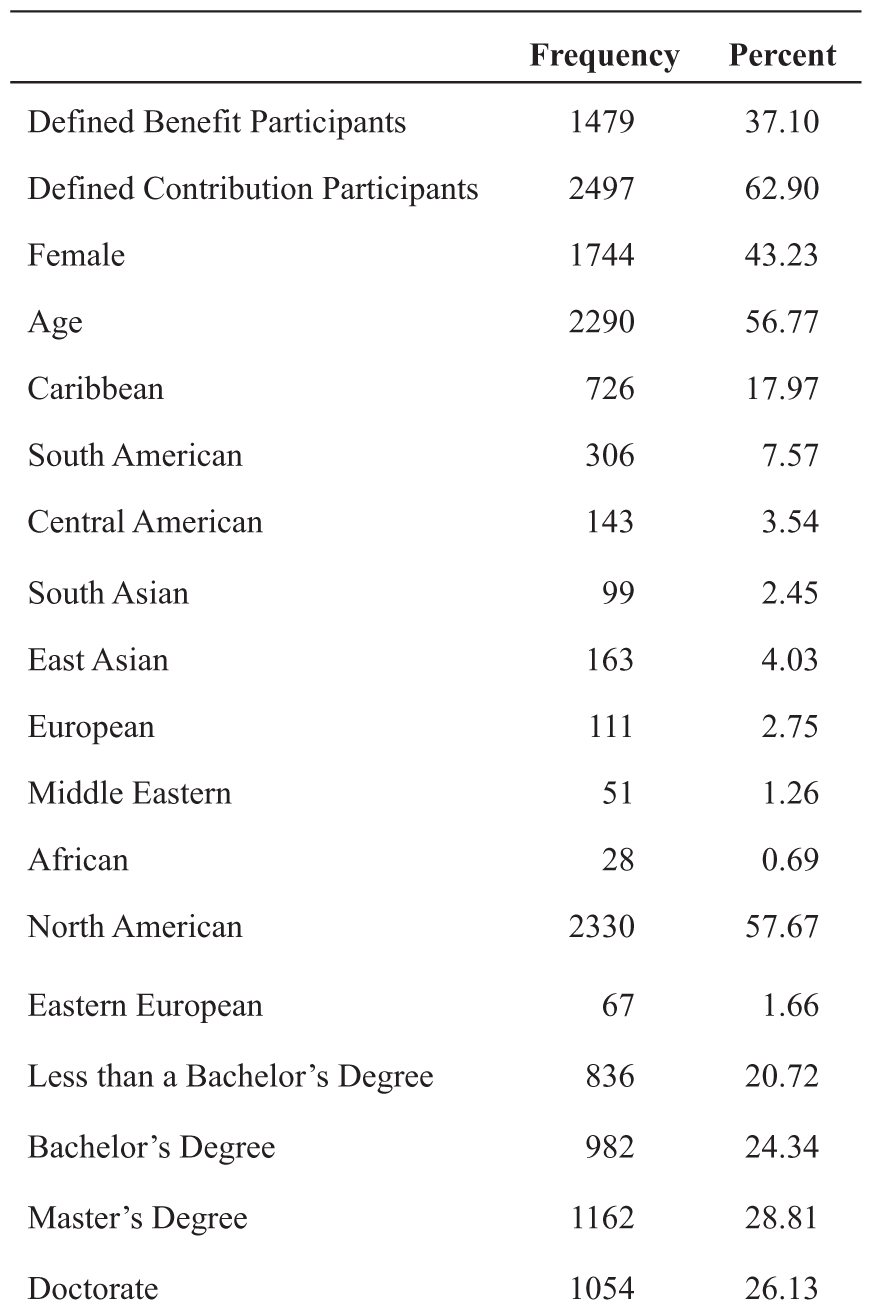

The data set includes information on all the 4,249 full-time employees at FIU who are eligible for either DB or DC plans as of March 2015. However, we limited the data set to employees who were hired after 2001 so that all the employees in the study had the option to choose between a DB and a DC retirement plan reducing our sample to 4,040 employees. The data include information on the date of hire, age, sex, marital status, education, retirement plan, and region of origin. The dependent variable is the binary choice between a DB pension plan and a DC investment plan. In the data set, 38.7% of respondents chose a traditional DB pension plan, and 61.3% opted for a DC approach.

Independent Variables

For independent variables, we look at education, region of origin, age, hire date, gender, and marital status (see Figures 2 and 3). Our first independent variable, education, has four categories: those with less than a bachelor’s degree (20.7%), a bachelor’s degree (24.3%), a master’s degree (28.8%), or a doctorate (26.1%). In the context of a university setting, there is a high representation of people with advanced degrees. It is also important to note that many of those with doctorate degrees are tenure-seeking faculty where portability is particularly important. However, many also serve in administrative roles, as instructors, or enter as tenured faculty members who do not operate under the same concerns about future employment. Overall, 24.8% of full-time employees are faculty members, and only a portion of those enter as tenure seeking.

Descriptive statistics: Plan choice, sex, age region of origin, and education.

Descriptive statistics: Year hired.

When we look at the education and retirement plan preferences, there appears to be a strong relationship where 23.3% of people with no college or some college, 59.3% of those with a bachelor’s degree, 73.8% of those with a master’s degree, and 85.4% of people with a doctorate choose a DC plan. While the choice of plan is made at the onset of employment, it is important to remember that employees can change their plan once. This is critical if our hypothesis that education is an important determinant of the DC versus DB preference is correct. In the case where increased education correlates with changing preferences, employees can switch plans.

The data set includes country of origin for the full sample. However, as the sample included people from 119 countries, we could not include controls for each individual country. Instead, we generated regional variables based on the United Nations (UN) geopolitical regions and subregions where the sample permitted. These regions are designed to balance representation of geographic, political, and cultural perspective in UN proceedings. Basing our regional variables on the UN standard similarly groups nations with similarities together. While some nuance from individual countries within regions is absorbed, UN regions serve as a proxy for these cultural, geographic, and political differences. As a uniquely diverse organization, we had sufficient representation to include North America including the United States and Canada (57.7%), the Caribbean (18.0%), South America (7.6%), East Asia (4.0%), Central America (3.5%), Europe (2.8%), South Asia (2.5%), Eastern Europe (1.7%), the Middle East (1.3%), and Africa (0.7%). We excluded Oceania because there were only two employees from these countries.

We include age in our model as over time, we have seen a shift in both the private and public sectors away from DB programs toward DC programs. We expect that age may factor into the choice between programs as older employees may view a DB program as more of the norm than DCs. The average age in our sample is 41.0 years old with a standard deviation of 12.1. The youngest person in our data set is 19 years old and the oldest is 88.

We also included hire date in our model to test for the same shifts from preferences for DC plans over DB plans over time. Our data set spans from January 2002 to March 2015. The mean hire date was the beginning of 2010 with a standard deviation of 3.5. When we tested for correlation between age and hire date, we found that there is a low correlation of –.301 indicating that it is appropriate to include both variables.

Our population includes 43.2% males and 56.8% females. Finally, we include marital status as a control because decisions about the future are often influenced by one’s spouse and in the case of two-income households, married couples may decide retirement options based on perceptions of combined approaches rather than as individuals. Single people represented 53.1% of those in our data set, while 46.9% were married.

Two important variables that are missing from our data are income and race. Neither was available to us due to privacy concerns. Income is captured to some degree through our education variable and the two are often used as proxies for each other. While limited racial differences are captured in our region of origin variables, our ideal study would include race/ethnicity as an independent variable. The Pew Foundation (Kochhar & Fry, 2014) reported that the gap between White, Black, and Hispanic wealth has reached 30 year highs. In 2007, the White-to-Black median wealth ratio was 10.0; in 2013 it was 12.9. For Hispanics, the respective ratios were 8.2 and 10.3. While “The Great Recession” reduced all family wealth from US$135,700 to US$82,300, the drops for Blacks and Hispanics were even more dramatic. Why? The post–Great Recession recovery has had a differential impact on various asset classes and their ownership pattern.

Financial assets, such as stocks, have recovered in value more quickly since the recession ended. White households are much more likely . . . than minority households to own stocks directly or indirectly through retirement accounts. Thus, they were in better position to benefit from the recovery in financial markets. (Kochhar & Fry, 2014, p. 3)

The pattern of asset ownership noted by Pew not only relates to a number of factors (income, education, discrimination) but it also correlates to financial literacy. Like women, minorities rank low in financial literacy. Many do not have checking or savings accounts—a springboard for asset accumulation (Lusardi & Mitchell, 2005, pp. 3-4). Controlling for education and incomes, minorities own far fewer “risk assets” and are far less likely to open Independent Retirement Accounts (IRAs) or apply for mortgages. Unsurprisingly, and as the case with women, we expect results here to follow on prior work (R. L. Clark & Pitts, 1999; Frank et al., 2000; Jacobs & Watkins, 1984) with minorities showing lower predisposition to the DC model.

Although differences among races are an interesting variable, there is current debate about the validity of traditional race classifications and binary minority/nonminority variables. There is a significant societal change in the percentage of people who identify themselves as multiracial. In 2000, 2.4% of people reported to the U.S. Census that they were two or more races. That number increased by 32% in the 2010 Census to 2.9% of the population (Jones & Bullock, 2012). This trend toward an increasingly multiracial society presents an important challenge for social scientists. The U.S. Census Bureau is currently testing multiple methods of categorizing race and ethnicity using region of origin as a building block. For example, one test model includes “Middle Eastern or North African” instead of the tradition pushing of these populations into either White or Black categories (Cohn, 2015). Hence we are deploying a regional approach that may be used in the 2020 Census in the absence of more traditional racial categories.

Methodology and Model

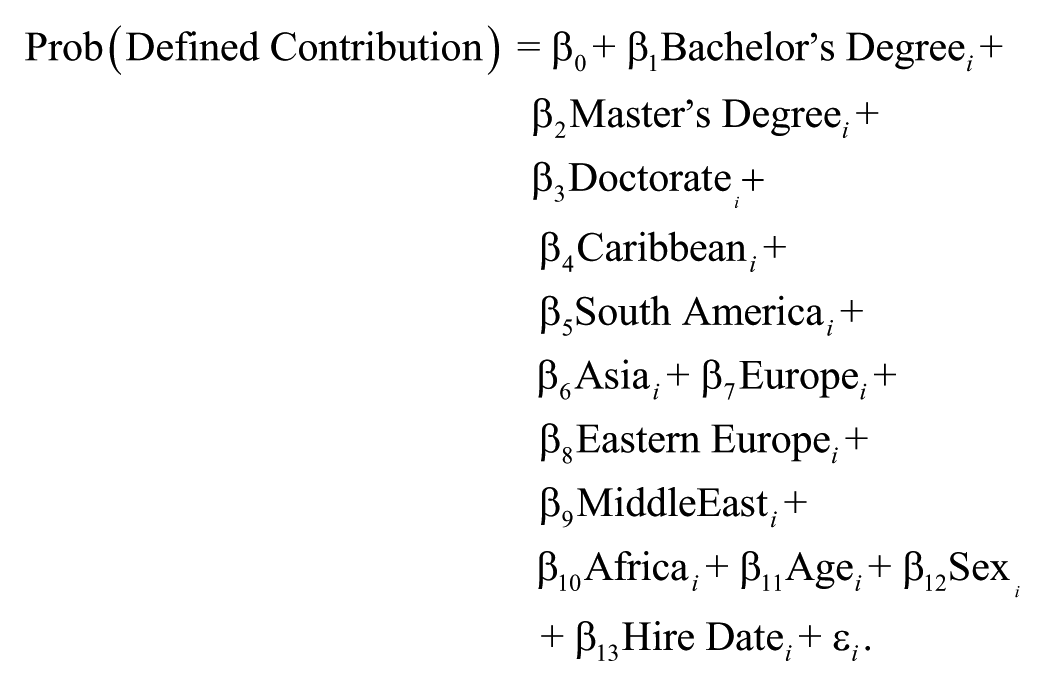

To test our hypotheses, we use a binary logit model to assess the factors that contribute to the choice between a DB and a DC plan. For the first hypothesis, education is broken into four categories (less than a bachelor’s degree, a bachelor’s degree, master’s degree, and doctorate). These categories are then used to create dummy variables where the reference group was those with less than a bachelor’s degree. This approach was used rather than viewing education as an ordinal variable to address concerns that the relationship between plan choice and education is not linear. The second hypothesis uses a series of dummy variables comparing each region’s choices to the choices of people from North America. The third and fourth hypotheses concerning age and hire date are continuous variables. Finally, there is a dummy variable for gender used to test the fifth hypothesis. We examined correlations to test for multicollinearity and all of the relationships were well below the .70 threshold (see Table 3). Our model had a pseudo r2 of .1667 and the Pearson’s chi-square measure of goodness of fit had a probability of .1787 indicating that the model is acceptable. Thus, the model is hypothesized as follows:

To further understand our quantitative findings, we conducted an interview with an Assistant Director of Benefits Administration and two Benefits Specialists at FIU on July 20, 2016. This interview contributed further insights into how the plans operate, patterns of behavior that they observe, and questions that new employees ask about their benefits. The semistructured interview was conducted post data analysis to better understand our quantitative findings. Our goal was to use the interview data as a supplement to our quantitative findings rather than a cornerstone of our research. For a more robust qualitative study that stands independent of quantitative findings, future research should interview employees about why they chose one retirement plan over another. The initial questions for the interview were:

What drives the choice between plans?

We see that education is the biggest determinant. Is that about mobility, knowledge, or income?

Do people who end up in the traditional pension choose that or end up there by default?

Do you observe difference based on where people immigrate from?

What do you do to try to educate people on their options? Do people ask for much information?

Does gender or being married matter?

It also looks like young people are more likely to choose the Optional Retirement Plan system. Is that about faith in markets, mobility, or something else?

Findings

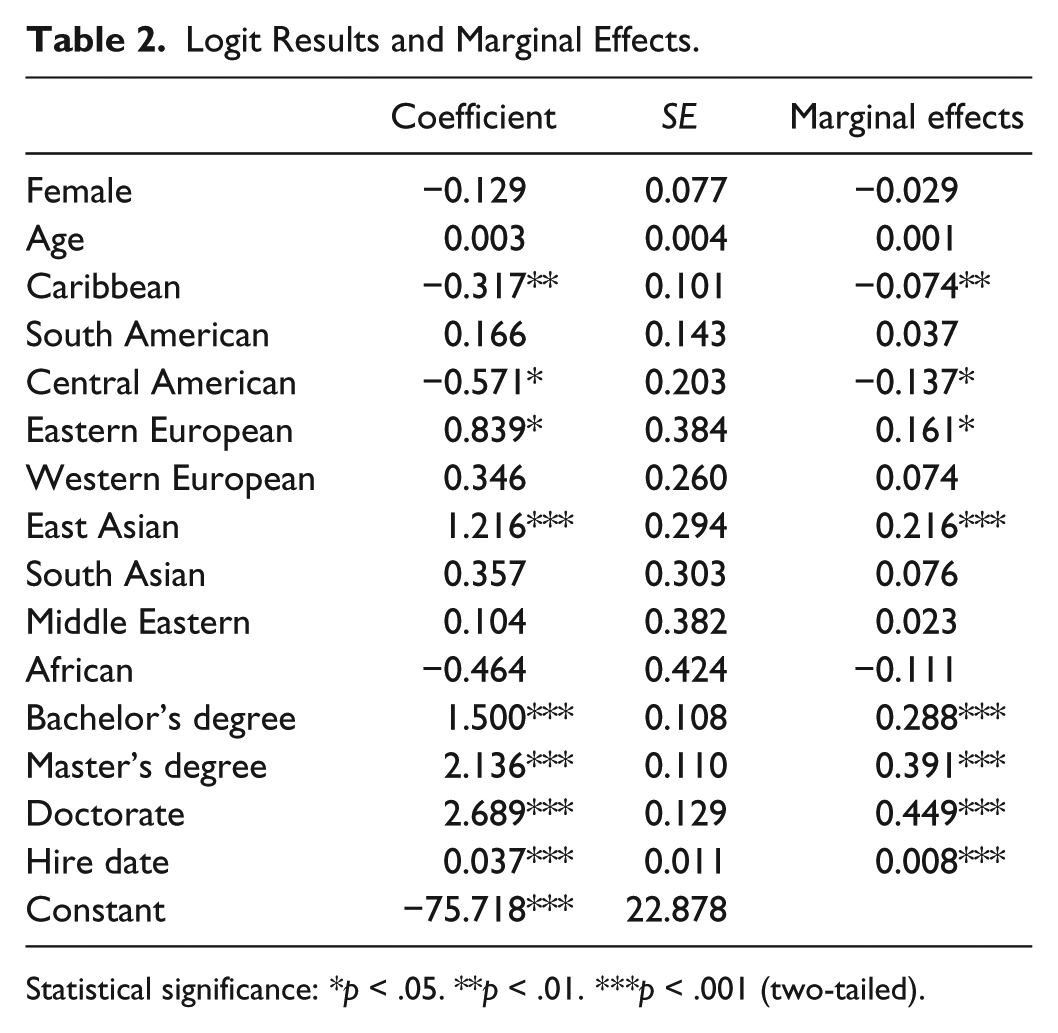

As hypothesized and consistent with other research (Frank et al., 2000; Frank et al., 2012), our results show education is the biggest driver of the DB versus DC choice (see Table 2). The probability of choosing a DC plan increases dramatically as education level increases. Compared with those who have either no college education or less than a bachelor’s degree, the probability of choosing a DC plan is 28.8% higher for those with a bachelor’s degree, 39.1% higher for those with a master’s degree, and 44.9% higher for those with a doctorate.

Logit Results and Marginal Effects.

Statistical significance: *p < .05. **p < .01. ***p < .001 (two-tailed).

Correlations.

We had mixed findings for whether those born in other regions were more or less likely to choose a DC plan than those born in North America. People from the Caribbean and Central America were less likely to choose a DC plan than North Americans. There is support for this hypothesis as people from the Caribbean were 7.4% less likely to choose a DC plan than their North American counterparts. We also find that people from Central America were 13.7% less likely to choose a DC plan than those from North America. However, there was not a statistically significant difference between South American and North American preferences.

Employees from two regions were more likely to opt for a DC plan than their North American counterparts. Immigrants from Eastern Europe were 16.1% more likely to choose a DC plan than their North American peers. Similarly, people from East Asia were 21.6% more likely to choose a DC plan compared with those from North America.

In Western Europe, South Asia, Africa, and the Middle East, there were not significant differences in plan preferences compared with North Americans. In both historical ties and Hofstede’s dimensions, Western Europe and North America have numerous commonalities that may contribute to similar decision-making in retirement planning. However, the lack of support for Hypothesis 2 for South Asia, the Middle East, and Africa cannot be attributed to the same similarities. It is possible that small sample sizes for these regions contributes to the finding of no difference from North Americans.

The model does not support the third hypothesis that older employees are less likely to choose a DC plan than younger employees. This finding is contrary to previous research that finds that younger workers do not expect or prefer long tenure with an organization (Cong et al., 2013; Kelly & Shreetama, 2015; Lewis & Stoycheva, 2016). While age was an insignificant predictor, year of hire was significant and in the expected direction. Newer hires are more likely to choose a DC plan than employees with longer tenure. When all other variables are held at their means, an employee hired in 2015 was 10.4% more likely to choose a DC plan than an employee hired in 2002.

Gender is not a significant predictor of pension type. This is perhaps our most surprising finding. Empirical findings coupled with Weickian “sense-making” suggest that level of education, region of origin, and the pursuit of portability are effectively eliminating gender from the model. This is an intriguing finding given prior research (see Frank et al., 2000; Frank et al., 2012).

Discussion

The first finding of note is the fact that nearly 63% of employees opted for the DC model. Prior research suggests that discussions of the DC alternative in the public sector are often framed in one of two ways. The first is that of a fiscal safety valve that reduces current and future fiscal burdens (Forman, 1999). The second is an ideological statement, in which DC adoption is Thatcherite “deprivileging” of public workers (Campbell, 2011; Hays, 1996). This connotes the predominant DB model, with its guaranteed future income stream, as an anachronism tied to an economic past free of global competition, coupled to lifetime employment.

The Florida Retirement System’s DB alternative available to employees is considered, along with Delaware, a model of actuarial soundness (Munnell, 2012) and ranks in the top 10 state plans in funding status (Florida Retirement Security Coalition, 2013, pp. 2-3). Moreover, at the time of this study, employees defaulted into the DB plan unless they opted out. This suggests employees at FIU are not “running from” an actuarially unsound DB model as they might in Illinois or Kentucky. And they are not under any pressure to opt out of the DB model. But empirical findings suggest the DC model and its portability are preferred, a finding strongly supported by interviews with HR staff.

An important corollary made clear in our interviews is that DC portability trumped other property rights as a driver of choice. The authors wondered if part of the overwhelming DC preference was tied to the fact that DC pension assets could, for example, be borrowed against for medical emergencies or housing, and transferred to heirs upon passing; contrariwise, DB assets are essentially nontransferrable prior to death and only carry value via survivor benefits tied to lifespan of designated beneficiaries (typically a spouse). Human resource staff, all with decades-long experience, stated these considerations were off the radar screen. Their principal “property rights” issue was consistent with the high divorce rates stated earlier—divorce and parsing of assets related to Qualified Domestic Relations Order execution. Statistics show that first, second, and third marriages in the United States have respective failure rates of 50%, 67%, and 73% (Banschick, 2012). Moreover, the commonplace that divorce probability decreases with age has been challenged by recent evidence (Wolfinger, 2015) that it actually increases by 5 percent points a year starting at age 32. Noting this observation from interviews, we tested marriage as a variable in alternative models and found that it was not significant and reduced the goodness of fit measures. This contradiction between observations of HR professionals and statistical findings opens opportunities for future exploration. It is possible that marriage is not a consideration when one first signs up for benefits, but retirement income becomes a key component when pending divorce requires people to consider the division of assets. Hence, people’s initial choice is without regard for marital status (as was captured in this data set), but people seek the advice of HR professionals on retirement plans again when they are entering divorce proceedings to “game the system” or best manage their assets.

From the vantage of HR professionals, employees viewed their careers in relatively short (3-5 years) stints, and portability of assets through that trajectory made more sense than the 8 year vesting and 33-year tenure required of Florida’s DB system. Long-term concerns such as borrowing privileges or bequeathing of pension wealth were not, in their judgment, a rationale for DC adoption. This movement toward a mobile workforce is not unique to universities. The trend toward a workforce that does not expect or desire a commitment of lifelong employment started in private sector organizations and is filtering into public sector organizations as they focus on cost controls and shift responsibilities to contractors, and states adopt right to work policies that remove traditional civil service job protections.

The movement toward DC approaches that we find in this study poses benefits for financially astute participants, but significant risks for uninformed investors. A concern underscored by our findings is that the low-cost DC plan alternatives (exchange traded funds, life cycle funds, index funds, and low-cost actively managed funds) offered by the institution do not generate sufficient expense fees to encourage significant investment advice and financial counseling from investment professionals. Human resources staff believe that after an initial consultation, many account representatives of the four financial services companies offering DC plans are typically unavailable, even for a once-a-year financial checkup. This is unsurprising. The typical American retirement account for those 55 to 64 is valued at just around US$100,000 (Transamerica Center for Retirement Studies, 2016). With overall expense fees pegged at 0.5% or less, commissions for face-to-face advising are limited and it is likely that many new accounts with low accrued value may be relegated to phone centers or robo-advising as a result (Carey, 2016).

Federal regulations that took effect in 2017 effectively codify this low-cost approach. These rules mandate that retirement accounts be managed to a higher “fiduciary” standard rather than a lesser “appropriate” one. According to Ben Levisohn (2016), “The change is a big deal. Now your broker must truly be able to justify why a particular product is in your best interest—and not his. Often that boils down to: ‘Is there a cheaper comparable product’” (p. 15). In the context of the typical DC retirement plans, these rules make index funds, exchange traded funds, and low-cost mutual funds the default option as professionals would need to justify any higher cost alternatives. The salutary impact of these rules is cost-savings: Participants will save thousands of dollars over a lifetime of saving, resulting in larger retirement payments. But these savings will come at a cost in reduced availability of investment advice. It is easier to place everyone in the lowest cost option without need for explanation or regard for anticipated performance than to explain to each client why a higher cost option may benefit them long-term. Investment advisors are thus encouraged to manage large volumes of low-cost, low-maintenance clients over more time-consuming individual consultations. Many public organizations may be hard-pressed to fill this advisory vacuum due to staffing limitations and liability concerns over giving advice in the first place. The adequacy of online or phone alternatives for public employers is conjectural, as it is for private employers. Ludden and Kendra’s (2015) work, suggests robo-advising may be adequate for assisting with branch decisions about allocating contributions to a retirement account, but it is unlikely to help with root decisions such as the trade-offs between saving for children’s college versus saving for retirement. And it cannot alter the reality that online counseling does not work for everyone. The dangers of market trends and regulatory reforms that discourage active account management by investment firms are exacerbated by recent changes that make the DC option the default in Florida. The negative spillover effects of lower commissions and use of passive investment funds such as exchange traded funds or index funds, will be heightened as of January 2018, when the new rules making DC funds the default take effect. These changes will increase the number of investors who are neither actively engaged in financial decisions nor substantively served by investment professionals.

Our next set of findings relates to how America’s changing demographics may affect pension choice and organizational preparation for adoption of DC plans. Our results reflect a dichotomy between noncollege and college-trained participants that correlates education and investment literacy. They may also suggest a reality in Florida and elsewhere that the public sector workforce is comprised of two groups. One effectively “works for its pension” (predominately noncollege trained) and the college-trained, who envision a more varied career path free of the “golden handcuffs” associated with DB pension accrual (Amenson et al., 2014; Cong et al., 2013; Costrell & Podgursky, 2010). The choice between a DB and a DC plan is in many ways the choice between a long-term commitment to an organization and the ability to move among organizations while still building one’s financial future. In this case, we see that more educated employees are opting for the DC plan and therefore, assure their ability to change organizations without repercussions on their long-term financial plans. For organizations, this is a signal that they must consider their more educated employees as a greater flight risk. Choosing a DC option means that retirement benefits do not serve as a retention tool in the same way as a traditional DB pension.

This split may evince a phenomenon seen in the 2016 presidential election (Tyson & Maniam, 2016) and in politics throughout the OECD (Judis, 2016) in which college and noncollege educated citizens are split in their post–Great Recession attitudes to an increasingly globalized economy. Those with college education have seen their earnings hold up, while those without the BA have seen significant earnings decline. The DC-DB preference split by level of academic attainment is suggestive of this earnings pattern wherein lesser educated employees “seek shelter” from global markets via the DB model.

Findings from prior decades pointed to a DB–DC dichotomy: White, male, college-educated employees opted for the DC model, while others went the DB route (Frank et al., 2000; Munnell, 2012). Our findings are more nuanced. Gender may not be as central to the DB–DC choice as it was. Furthermore, in our study, a White–non-White “switch” would be misleading. Pension preferences may reflect the cultural and economic climate related to region of origin. We build on Hofstede’s (2011) approach to cultural differences paired with UN defined regions to explore demographic impacts in a more nuanced way than the literature typically uses with the expectation that exploring region of origin is increasingly important in our diverse society. Trust in financial and political systems, financial literacy, and cultural norms for old age and retirement planning all may vary by region. For example, those immigrating from economically and politically stable regions may feel greater affinity for the DC option and its portability while those from emerging, unstable regions may prefer the relative security of the DB option. Some of these preferences may be moderated by socialization in the United States, but previous literature indicates that the predisposition toward financial literacy is established in childhood and heavily influenced by the wealth and literacy of one’s parents (Lusardi et al., 2010). We also know that financial literacy varies from country-to-country and region-to-region creating an uneven playing field for financial planning (Klapper et al., 2015). Given the early establishment of likely financial literacy and constraints on organizations in providing recommendations or financial literacy training, it is important that future research continues to recognize ways that the financial literacy of people of different backgrounds varies to better inform people in making financial planning decisions.

Employees from two regions were less likely to choose a DC approach than their North American peers. The negative coefficient on DC participation for those from the Caribbean and Central America suggests that coming of age in economies plagued by overreliance on tourism and mineral extraction (International Monetary Fund, 2014; Caribbean Development Bank, 2014) may diminish appetites for the DC model. For these participants, the relative surety of the DB model may be preferable to the vicissitudes of market performance that may, from the vantage of upbringing, seem less than desirable.

On the contrary, immigrants from the former Soviet Union and surrounding areas (Eastern Europe) may prefer the DC model for a different reason, that being a fear of expropriation of private assets. From their vantage, the DB model is “statist” and subject to the property rights alteration at the government’s discretion. While the statist model offered under Soviet communist rule offered stability, it did not allow for the accumulation of wealth and substantial change in one’s economic quality of life. Whereas in other economically disadvantaged regions, lack of stability encourages people to seek financial security, in Eastern Europe, stability without opportunity encourages emigrants to seek the “wins” that a market-based system offers. Significant changes to Florida’s DB model in 2011, including cuts to the Deferred Retirement Option Plan (DROP), reductions in benefit multipliers, and increase of vesting from 6 to 8 years lend credence to those concerns. The DC model may not provide a certain benefit, but from this group’s perspective, it is less prone to direct government manipulation.

The higher DC preference among East Asian immigrants is unsurprising given prior research indicating a high predisposition to restricting current spending in favor of investing in the future (Coeurdacier, Guiband, & Jin, 2015; Paige, 1994; Stiglitz, 1996). The DC model provides a tangible personal savings account coupled with a direct reduction in taxable income. The DB model may provide a formula-driven benefit at the end of one’s career but this may be ephemeral to those who look to positive, immediate reinforcement of savings behavior.

Our findings initially suggest that age is not a factor in retirement plan choice. Upon closer examination, we propose that while older employees may be more familiar or comfortable with traditional DB plans, that may be offset by shorter expected tenures and higher financial literacy for people approaching retirement. The HR professionals interviewed felt that employees in their 20s had little understanding of how retirement plans operated, but that those who were older were progressively more knowledgeable about how the various plans function. Our findings indicate that regardless of age, better educated workers prefer the DC model.

Where age was not a significant factor in retirement plan preference, hire date was. Living in a post–Great Recession world may be affecting hires of all ages, with the realization that greater economic uncertainty is shortening job tenure. This makes the DC choice an appropriate one in terms of lifetime pension wealth accrual (Munnell, 2012). This point is reinforced in the state’s factsheet describing the three retirement options, wherein new hires are counseled to choose a DC option if expected tenure is less than the 8-year vesting period pointing out that people “would not be eligible for employer-funded benefits under the Pension Plan.” For those who expect to stay with a participating employer for 9 or more years, employees are told that the best plan for them “depends on a number of factors” and are then referred to a toll-free line where they can get more information (MyFRS Florida Retirement System, 2016).

Limitations and Future Research

Our findings are drawn from one institution; hence generalizability may be limited. Nonetheless, the empirical literature on public sector determinants of pension choice is limited, as the DB model’s predominance (Beshears, Choi, Laibson, & Madrian, 2010) constrains real-world assessment of what motivates choice between the two basic model types. The study of retirement planning choices would also benefit from data on individual financial literacy and how perceptions of longevity and other supports such as Social Security and dependence on children influence preferences. We also note that while ideological experiences are partially captured by regional differences, future research could connect individual ideologies with retirement planning preferences as one’s faith in collective action in general could relate to one’s preferred retirement plan. Those limitations notwithstanding, our findings merit consideration given the fact that employees are indeed given a choice between the two pension models, and the institution’s demographics reflect a diversity the nation will attain by 2050 to 2065, depending on projection method (Pew Research Center, 2015). Thus, findings from this case study may provide important lessons for public sector human resource practice in coming years.

We also see opportunities for future research that explores ethnicity along different dimensions. Our use of regions provides a more nuanced approach than traditionally used ethnicity variables that rely on identification as Hispanic or Black in the U.S. context, but does not capture all of the subtleties possible. We consider region to be a balance between the two extremes of having so much detail that it is impractical for application and such broad terms that they tell us little about underlying causes. For example, the widely used variable of Hispanic does not account for the wide array of cultural distinctions or financial differences within the Hispanic community. We propose that as immigration and emigration continue to be dynamic in our communities, it is critical that we consider the implications and better understand how regional differences drive cultural differences that appear in the workplace. There is also opportunity in future research to connect information from the World Values Survey and Hofstede’s work on differences among regions and countries to the individual choices and preferences of employees.

Finally, our regional variables only capture whether or not someone is an immigrant. They do not capture age of immigration or how long someone has lived in the United States. Nor do the variables explore the regional impacts on second or third generations. Data that captured these nuances could better assess at what point the differences captured in regions diminish and behaviors become consistent with the overall U.S. culture.

Conclusion

Our findings take on heightened significance in light of the January 1, 2018, changes in both Florida

Furthermore, these findings suggest that public sector HR professionals need to plan for a more mobile workforce. Regardless of age, post–Great Recession hires frame their pension choice to account for mobility between employers rather than one lifelong employer; they value portability over the certainty of a revenue stream they may not accrue due to shorter job tenure. Increased utilization of the DC model will require public organizations to compete in recruitment and retention based on other conditions of employment. The finding that more educated employees are more likely to top for DC plans also indicates that the most educated are also the least likely to be committed to long-term employment with a single organization. Organizations need to tailor recruitment and retention plans to address the increased flight risk of the academically best trained employees.

Those responsible for administering the increasingly prevalent DC plans in the public sector will be obligated to tailor investment options with a more complex and differentiated set of participants in mind. These differences present further challenges to HR professionals that may not be well equipped to face a paradigm shift in public employee retirement planning (Cong et al., 2013). This challenge is also critical as HR professionals are constrained in their ability to give employees advice about plans and providers, and employees have limited time to make choices that have profound consequences on their financial future.

Moving forward, this study indicates that public organizations need to view retirement planning benefits in the context of a more mobile and diverse workforce. To effectively recruit and retain the best employees and minimize disparities connected to educational and demographic differences, public sector HR professionals need to consider how to provide financial literacy training, offer benefit packages that encourage organizational commitment, and recognize how differing backgrounds drive benefits decisions. Public sector organizations also need to be cognizant of how cultural differences among employees have deeper roots than traditional demographic variables such as Hispanic versus non-Hispanic, or Black versus non-Black. By integrating a more sophisticated use of demographic variables, public administrators can improve their approach not only to benefits as discussed in this context, but also to employment issues as a whole in a time where the relationship between employees and employers is based on an expectation of greater mobility.

Our findings raise another thorny issue facing any pension and insurance operation; adverse selection. When given a choice of pension model, better educated, higher income, and actuarially longer lived participants are opting for the DC model. Cultural differences may exacerbate this issue, unintentionally creating systematic disparities. Decision makers are taking numerous incremental steps to salvage DB plans through increasing vesting period, lengthening tenure needed for retirement, increasing employee contributions, and decreasing deferred retirement option payments among other techniques (Cong, Neshkova, & Frank, 2017). These actions paired with the trend of increased DC optionality may exacerbate the long-term solvency of DB plans to the extent that economically advantaged participants are choosing DC over DB. The incremental steps to save DB plans may make DB options less attractive to more financially literate participants encouraging them to opt for DC plans.

When looking at regional differences through the lens of Hofstede’s measures of culture, we find that cultural context matters. While not as precise as breaking apart culture into individual components such as political backgrounds, economics, and value systems, this cultural approach does offer a more nuanced approach with greater explanatory value than traditional male/female, Black/White, Hispanic/non-Hispanic demographic variables. These concepts of culture are embraced in other fields, but public administration has limited research that extends beyond these traditional demographic variables. This opens the opportunity to respond to calls from Pollitt & Bouckaert (2017), Roberts (2014), and Durant (2014) to extend the scope of public administration research to capture larger forces and long-term movements and trends. One stream of this is future research on how cultural differences affect workplace and employment decisions in an increasingly diverse public sector.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.