Abstract

While existing studies have examined the separate effects of local governments’ internal conditions and external environment on local innovation, few have paid attention to their interactive effects. This study examines whether state-level rules regarding local discretion moderate the effects of city governments’ slack resources and learning, using local sustainability innovation as an example. We distinguish two types of discretion (fiscal and statutory) granted by state governments. Applying a difference-in-differences (DDD) approach with a longitudinal dataset of 238 U.S. cities, we find that fiscal discretion strengthens the positive effect of fiscal slack while statutory discretion enhances the positive effect of learning. The findings uncover the complex interactions between multilevel institutional arrangements and local innovation mechanisms.

Introduction

Sustainability emphasizes the balance between human needs and ecological well-being and consists of three pillars—environmental, economic, and social. Sustainability innovation is often defined as any sustainability policy or program that is new to the government adopting it (Krause, 2011). According to the United Nations General Assembly's sustainable development goals (SDGs), cities should be inclusive, safe, resilient, and sustainable. Local governments are uniquely positioned in this process (Armstrong & Kamieniecki, 2019). Through designing, adopting, and implementing various innovative sustainability programs and services (Krause, 2011), they have played an increasingly salient role in this area (Yi et al., 2017a). Nevertheless, not all city governments take such innovative actions (Svara, 2011); among those that do, many are doing it in a piecemeal, ad hoc manner (Saha & Paterson, 2008). What can explain the variations of sustainability innovation among city governments?

Studies have examined the impact of political and civic participation (Portney & Berry, 2010), resources (Lubell et al., 2009), residents’ education level (O’Connell & McCoach, 2008), government structure (Feiock et al., 2008), capacity building (Wang et al., 2012a), and urban governance regimes (Gibbs & Jonas, 2000; O’Connell, 2009) on local governments’ sustainability policy adoption. An emerging line of inquiry approaches this issue in its multi-level governance context, highlighting how urban sustainability is constructed and contested by multiple tiers of government and spheres of governance (Betsill & Bulkeley, 2006; Bulkeley & Betsill, 2005; Feiock et al., 2017). These studies have examined the effects of state mandates (Tang et al., 2010), intergovernmental grants (Lim & Bowen, 2018; Tang & Hill, 2018), and interlocal collaboration (Deslatte & Feiock, 2019; Hawkins et al., 2018; Yi et al., 2017a). For example, Homsy and Warner (2015) show that a conducive policy and political atmosphere from the state government encourages local sustainability innovation.

Discretion, the institutional space that higher-level institutions give to lower-level institutions, is one of the most important aspects of the multi-level governance arrangements (Bulkeley & Betsill, 2005; Hooghe & Marks, 2001) and has received tremendous attention in the public administration literature (Holzer & Yang, 2005; Meier & Bohte, 2001). 1 Local government discretion has not always been defined carefully or consistently. Many studies use Dillon's Rule or home rule as a proxy (Krane et al., 2001; Weeks & Hardy, 1984). 2 Zimmerman (1995) differentiates four types of local discretion: (1) structural—changing organizational structures, (2) functional—adding, eliminating, or altering functions, (3) personnel—making personnel decisions, and (4) fiscal—levying and raising taxes. Krane et al. (2001) propose four discretion categories, including legal, structural, functional, and fiscal. While these conceptualizations provide valuable insights, the measurements are subjective—based on perceptions of state officials and experts on state–local relations, and the data are not updated.

Building on the literature, we focus on fiscal discretion and statutory discretion. Fiscal discretion is the assignment of revenue and expenditure responsibilities from a higher-level government to lower-level governments (Oyun, 2017). It captures the amount of power local governments have in collecting and expending financial resources. It is similar to Zimmerman (1995)'s and Krane et al. (2001)'s fiscal discretion and corresponds to the concept of fiscal decentralization. Statutory discretion means the extent to which legislatures give flexibilities to local governments regarding their decision-making power (e.g., not limiting their policy choices) or administrative processes. It is determined or at least strongly influenced by specific enabling statutes (Epstein & O’Halloran, 1999). Statutory discretion corresponds to administrative decentralization, which concerns the level of power subnational governments have in turning policy decisions into allocative (and distributive) outcomes through regulatory actions (Pollitt, 2007).

Scholars have had sustained interests in the relationship between discretion and innovation. New Public Management scholars advocate we should “let public managers manage” and give them enough autonomy to develop new ways of processing and handling their business (Wynen et al., 2014). Verhoest et al. (2007) argue that enlarging managerial autonomy can increase public organization innovation. van Thiel and van der Wal (2010) find that agencies with more managerial autonomy exhibit more innovations. In local government literature, since Brandeis (1932), it has long posited that local governments serve as “laboratories of democracy” with each one independently pursuing different experiments. Empirically, scholars have shown that decentralization induces more policy innovations if multiple experimental policies are available (Strumpf, 2002). In the sustainability field particularly, Youm and Feiock (2019) find that while municipal autonomy negatively affects interlocal collaboration on climate change protection, local governments’ fiscal constraints from the state are not a significant predictor. These studies have found inconsistent results regarding the direct effects of discretion. We submit that various types of discretion may interact with other variables differently to influence innovation.

In this study, we examined how discretion moderates the effects of two most important local innovation mechanisms—slack resources (Berry & Berry, 1990; Geiger & Cashen, 2002; Walker, 1969) and learning (Gray, 1973; Rashman et al., 2009; Walker, 2014). Applying a difference-in-difference-in-difference (DDD) approach with a longitudinal dataset of 238 U.S. cities, we examine how the treatment effects of granting two types of local discretion are contingent on a city's fiscal slack and learning behavior.

Framework and Hypotheses

Integrating the local innovation literature and the discretion literature, we adopt an interactionist view of local government innovation, considering it an outcome from continuous and multifaceted interactions between a jurisdiction's internal characteristics and the institutional space where it is situated. We posit local decision-makers are rational strategists acting within a rule-structured situation. They make decisions based on their beliefs about the opportunities and constraints in fulfilling their missions and satisfying their constituents (Bryson, 2003; Ostrom, 2005; Vinzant & Vinzant, 1996).

Local Innovation Factors: Slack Resources and Learning

Slack resources

Organizational slack appears in different kinds of resources, such as financial, material, or human resources, and the slack in financial resources has received extensive scholarly attention (Meyer & Leitner, 2018). While existing studies have highlighted the importance of slack resources on organizational innovation, the empirical findings are equivocal (Geiger & Cashen, 2002; Herold et al., 2006). Some studies show slack resources provide extra capacity to support organizations to innovate or a buffer to bear the potential costs stemming from innovation (Berry & Berry, 1990; Damanpour, 1987, 1991; Fernandez & Wise, 2010). However, others find resources shortage encourages organizations to focus more on marketization and organizational innovation (Nohria & Gulati, 1996; Walker, 2008). The discrepancy suggests the effect of slack resources may depend on policy areas and external influences (Fan et al., 2020).

Sustainability policy actions often require local governments to change their infrastructure from traditional energy operating systems to new ones (e.g., retrofitting existing buildings, using energy-efficient devices or renewable energy) or modify internal procedures to go green (e.g., procuring green products/programs, developing inventories of greenhouse gas emission). Such transformation entails costs (Brown et al., 2009; Kwon et al., 2014). For instance, the Renewable Portfolio Standards (RPS) mandates the use of technologies that will be more expensive (Rabe, 2008). Local decision-makers must consider whether they have sufficient financial resources to support these policy actions and whether the constituents will be patient enough to wait for long-term benefits (Wang et al., 2012a). When a local government has more slack resources, local leaders perceive a low “degree of difficulty” in their task environment and feel more confident in their capacity to bear the costs, leading to more sustainability innovation adoption (Andrews, 2009).

Learning

Learning is a process of updating beliefs about key policy components (e.g., problem definition, strategies, and results achieved at home or abroad) through dialogue and interactions among individuals in group, organizational, and network settings (Borins, 2001; Newman et al., 2001; Radaelli, 2009). It emphasizes the decisive role of models in enhancing governments’ innovation capacity (Deutsch, 1966). Models convey knowledge, skills, and strategies for managing task demands. Especially in a highly uncertain environment, learning can be readily activated by looking for models from others. “When technologies are poorly understood, when goals are ambiguous, or when the environment creates symbolic uncertainty” (DiMaggio & Powell, 1983, p. 151), local decision-makers are more likely to model successful policy practices from other regions.

The policy innovation and diffusion literature emphasize the role of learning (Berry & Berry, 1999; Glick & Hays, 1991; Gray, 1973; Mooney & Lee, 1995; Walker, 1969). The social learning model assumes political officials are risk-averse and constantly searching for “satisficing” solutions by looking to neighboring jurisdictions (Berry & Berry, 1990; Walker, 1969) and through political networking (Mintrom & Vergari, 1998). Volden (2006), for example, finds states learn from other states to avoid policy failures. Sustainability policy is a highly uncertain area that demands learning. Through learning, local officials can understand policy options better, decide whether to adopt an innovation, and learn how to apply an initiative in their local context.

The Interaction Between Discretion and Local Innovation Factors

Local fiscal discretion manifests in different ways, such as the diversity of revenue sources, revenue/expenditure limits, and the proportion of local–state expenditures (Garcia-Milà et al., 2018; Mullins, 2004). Diverse revenue sources enable local governments to spread their financial burden across different types of economic activities. With higher debt limits, local governments can borrow more money. Increasing the proportion of local expenditures means local governments are given more freedom in spending money. Overall, fiscal discretion helps improve local governments’ fiscal health and fiscal slacks (Hendrick, 2004; Lubell et al., 2009), which enable local governments to invest in programs that require resource commitments (Hendrick, 2006) and to innovate (Fernandez & Wise, 2010; Walker, 2014). In the sustainability policy area, existing studies show cities with more slack resources can better adopt and implement environmental policies that require extra staff and resources (Kahn, 2006; Kwon et al., 2009; Wang et al., 2012a).

Fiscal discretion can alter local officials’ decision calculus of existing resources (Kalafatis, 2018). For example, Krueger and Bernick (2010) indicate that when states impose property tax revenue limits, cities worry about exceeding the revenue cap and find other alternatives to provide services. With more fiscal discretion, local officials tend to have more flexibility in using financial resources. When considering new sustainability programs, they may face less constraint in adjusting their local spending to facilitate program adoption and implementation. The favorable assessment of future financial conditions will likely strengthen the positive relationship between fiscal slack and sustainability policy innovation.

Hypothesis 1: In cities with more fiscal discretion, the positive effect of fiscal slack on sustainability policy adoption is stronger.

With higher levels of flexibility, local officials are more likely to apply what they have learned from other jurisdictions in terms of new policies and programs, including their design features, implementation procedures, and policy outcomes. Wynen and Verhoest (2016) argue that administrative discretion frees up agencies and encourages them to look for the best ways to steer their organizations, leading to more adoption of performance management techniques. Cities that learn are more aware of successful policy practices and more vulnerable to peer and public pressures (Brass et al., 2004; O’Toole & Meier, 2004). Cities with fewer legal and procedural constraints are more likely to convert the learned knowledge and pressure into new projects that fit local contexts, leading to more sustainability innovation adoption. For example, Salge (2011) shows that public service organizations face potential threats of direct intervention from regulatory bodies or governmental departments. When regulatory agency allows less autonomy, public service organizations tend to focus more on survival and risk minimization and are less inclined to engage in innovative search; conversely, when regulatory agency grants more autonomy, they will engage in risky and costly innovative search processes. Therefore, the effect of learning on innovation is strengthened by statutory discretion.

Hypothesis 2: In cities with more statutory discretion, the positive effect of learning on sustainability policy adoption is stronger.

Data and Model

Data Sources

Several data sources are used in the study. The first is a national survey of cities with populations over 20,000 residents conducted by the Local Governance Lab at Florida State University in 2011. The sample frame of 1,180 municipalities included all cities with populations over 50,000 and a random sample of 500 cities with populations between 20,000 and 50,000. City managers and Chief Administrative Officers (CAOs) were the initial contacts for the survey. A 57.5 percent response rate was obtained, with 679 returned surveys. The second data source is the 2015 International City/County Management Association (ICMA) Local Government Sustainability Practices Survey, which was administered in paper format via direct mail. The survey was sent to 8,562 local governments’ city managers and CAOs and achieved a response rate of 22.2%, with 1,899 local governments responding.

Both questionnaires are about local government sustainability practices, such as policy adoption, internal operations, intergovernmental collaboration, and external environment; some questions were asked in the same way. We extracted the same questions from the two surveys and matched them by cities to build a 2-year panel dataset, which renders a sample of 238 cities in two time points. 3 The dataset includes indicators of local governments’ concrete sustainability innovation actions instead of ceremonial commitments. It is the most updated dataset available on local government sustainability innovation. Local governments may be facing additional pressure in response to the challenge of environmental problems in recent years, and new policies and programs may have emerged. However, we are not focusing on the specific type of innovation programs but the pattern of adoption and the underlying innovation mechanisms, which can be relatively stable.

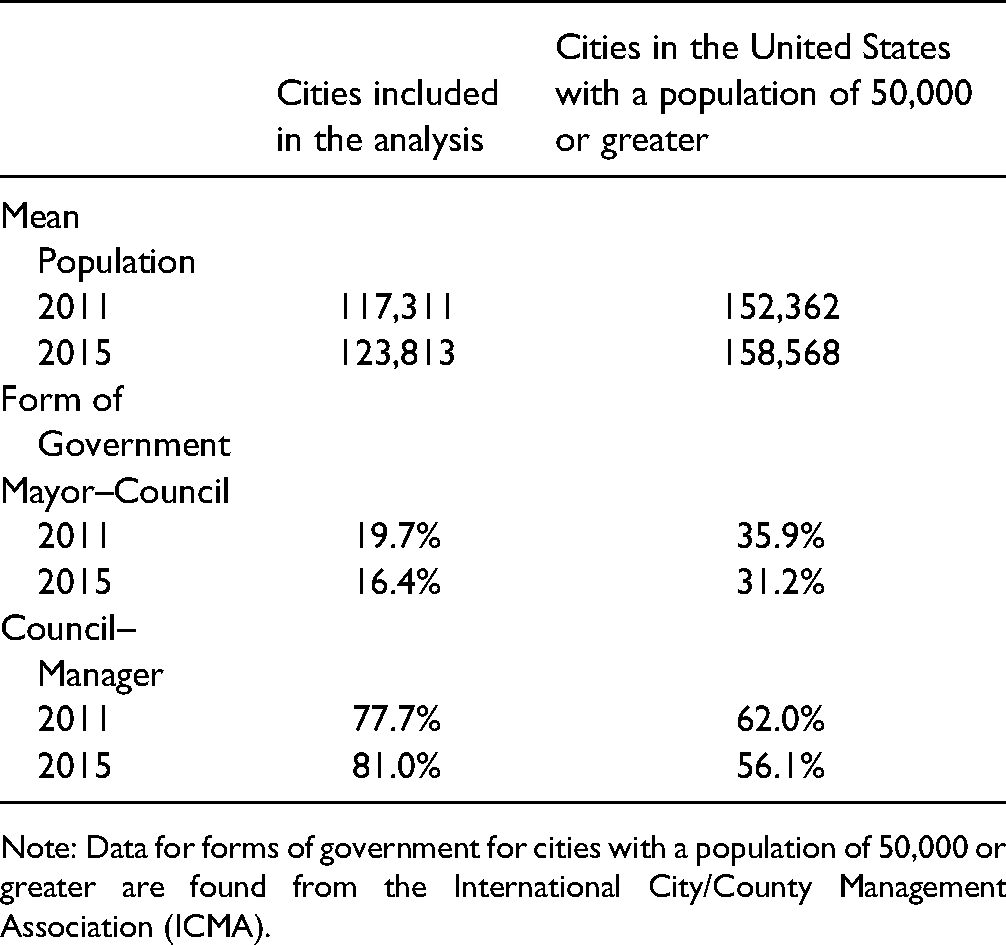

The cities included in the empirical analysis, for example, those for which data are available at two periods, are similar to the total population of cities in the United States with a population of 50,000 or greater (Table 1). The council–manager and mayor–council forms of government were present in 77.7% and 19.7% of responding cities in 2011, and 81% and 16.4% of responding cities in 2015. Compared with national statistics of forms of government, cities with a council–manager form of government are slightly overrepresented in our sample.

Comparison of Cities in the Analysis with Cities in the United States.

Note: Data for forms of government for cities with a population of 50,000 or greater are found from the International City/County Management Association (ICMA).

Additional data were collected from the following sources. National Conference of State Legislatures (NCSL)'s 50-State Searchable Bill Tracking Databases provide the most comprehensive and complete 50-state bill information across a variety of policy issues. The League of Conservation Voters’ (LCV) environmental scorecard provides information about all the members of the first session of the Congress's votes on the most important issues of the year, including energy, global warming, public health, public lands, and wildlife conservation, and spending for environmental programs. The scorecard is the nationally accepted yardstick used to rate members of Congress on environmental, public health, and energy issues. Urban Institute's State and Local Finance Initiative provides fiscal information (various sources of revenues and expenditures) about state and local governments. Population data is derived from the U.S. Census.

Dependent Variable

Sustainability innovation is new to the government adopting it but is not necessarily an altogether new idea (Berry & Berry, 1999). Many prior studies measure a city's sustainability policy adoption by counting the number of programs or policies the city has adopted. For example, Kwon et al. (2014) use the number of cities’ environmental conservation actions to measure policy adoption. Yi et al. (2017b) develop an additive index of local governments’ adoption based on policy actions that promote different aspects of energy and climate sustainability. Following this approach, our dependent variable measures the extent to which a city adopts sustainability (energy/climate-related) policies and programs, including retrofitting existing buildings for energy efficiency, green procurement, energy-efficient devices (appliances, lighting, etc.), inventory of greenhouse gas emissions, and renewable energy. The five items are shared across the two surveys and exemplify the common sustainability practices adopted by local government. If the city answers yes to one item, then the item is coded 1 (0 otherwise). The dependent variable is thus an aggregated index, ranging from 0 to 5.

Treatment

This study uses the DDD analysis to investigate how discretion moderates the effects of local characteristics on cities’ adoption of sustainability policies (Wooldridge, 2010). We focus on two treatments—fiscal and statutory—at the state level. In general, local governments look to the past few years for indicators for fiscal health, in which fiscal discretion is a critical component. The trend of states’ total local government own-source revenue/expenditure ratio in several consecutive years reveals meaningful information about whether fiscal discretion broadens or narrows in that state (Turley et al., 2015). Similarly, they will examine the external legislative environment within their state. Local budget planning and election cycles are approximately 4 years. Therefore, we use 2014 as the treatment year and use correlation of year and fiscal/statutory information at the state level to determine whether treatments exist in different states.

Scholars use different ways to differentiate the treatment group from the control group in a DID analysis. Some argue that treatment should be determined by nature, such as the occurrence of a natural disaster, the passing of new laws and regulations, or the implementation of a new program (Ma, 2016; Wang et al., 2012b). Others seek to capture policy change by identifying the patterns in the data and inferring from practices. For example, Flammer (2015) uses sharp changes in import tariff rates to determine treatment groups. When investigating the relationship between female executive leadership and corporate social responsibility, Hyun et al. (2022) used whether the percentage of females in the top executive team increases to differentiate treatment and control groups.

Fiscal discretion

It is measured by the proportion of local own-source revenue over local general expenditure. Existing studies mostly use either revenue- or expenditure-side indicators to measure fiscal discretion. Revenue indicators show the level of authority local governments have over their own revenues. Expenditure indicators (decentralized expenditures) mean access to additional resources and stronger financial health (Oyun, 2017; Singla & Stone, 2018). Our measure considers both revenue and expenditure sides. As Tatsos (1999) notes, when local government mainly uses their revenues, such as local taxes, fees, and revenues from local property, to finance their expenditure responsibilities, they are more fiscally independent and can make long-term financial planning. Data for each state's total local general expenditures and total local own-source revenue from 2011 to 2014 were found from State and Local Financial Query System by Urban Institute.

The share of total local government own-source revenue over total local general expenditures was calculated for each state and each year, and the trends (increasing or decreasing) of the proportions were identified by examining the correlation between year and proportion. Maintaining a local government's fiscal health is an ongoing process, including regular assessment of its finances (Honadle, 2003). An increasing trend from 2011 to 2014 indicates more discretion was given to local governments, and vice versa. States with more discretion were selected as the treatment group.

Statutory discretion

Huber and Shipan (2002) measure statutory discretion by assessing statutes’ length (# of words) in a jurisdiction. While it is a relatively simple measure to construct, it is statute-specific. We aim to capture statutory discretion in a given policy area (e.g., sustainability policy), which may have many statutes covering various policy aspects. We first collected the summary information for 3,028 bills (including both adopted and enacted) in the energy field between 2011 and 2014 from the 50-State Searchable Bill Tracking Databases by the NCSL. We then conducted sentiment analysis on these bills using Opinion Lexicon, a dictionary for mining sentiments, opinions, and emotions

4

(Liu, 2015). Each bill was assigned a sentiment score, based on which we can determine whether it is restricting or enabling. As such, 1,407 restricting bills were identified. Below is an example of a restricting bill summary. Here, the bill asks that the governor has the power to suspend certain requirements, which is considered direct intervention from the higher-level government. The bill also seeks to restrict local government authority to regulate overweight vehicles on the state highway system. The summary clearly shows that the bill attempts to reduce local governments’ discretionary power. TX H 2741 Regulation of Motor Vehicles Enacted - Act No. 113506/14/2013: Relates to regulation of motor vehicles by counties and the Texas Department of Motor Vehicles, authorizes a fee, creates an offense, allows the governor to suspend certain requirements in response to an emergency declaration of another jurisdiction, relates to electronic funds transfer, relates to issuing specialty license plates, relates to restriction on local government authority to regulate overweight vehicles and loads on state highway system.

We count the number of restricting bills in each state legislature from 2011 to 2014. The trends (increasing or decreasing) of the number of bills were identified by examining the correlation between year and number of bills. An increasing trend from 2011 to 2014 indicates less discretion was given to local governments, and vice versa. States with more discretion were selected as the treatment group.

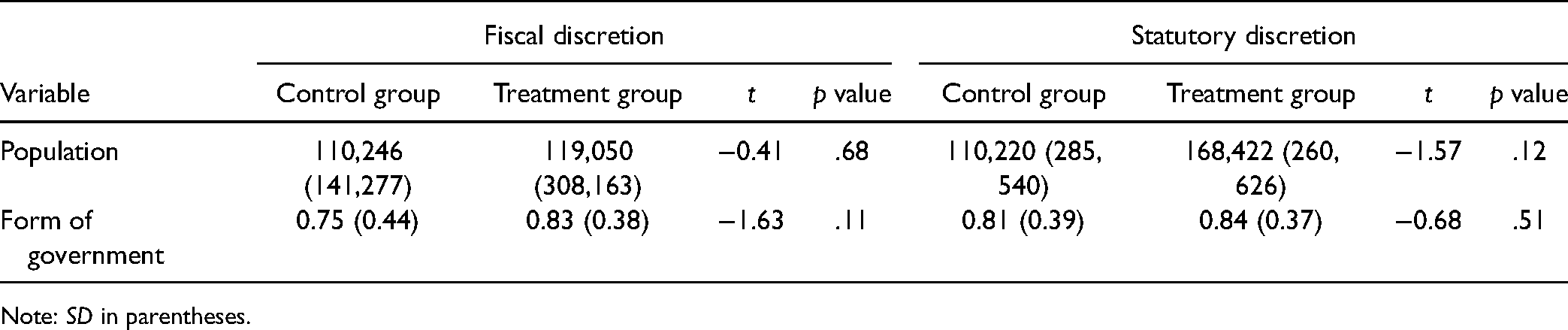

Table 2 compares cities’ characteristics in population sizes and government forms in the control and treatment groups. Student’s t-test results indicate that these groups are not statistically significant (p > .05) in terms of population and form of government, meaning that the two sets of control and treatment groups do not substantially differ concerning key city characteristics.

Comparison of Cities in the Control and Treatment Groups.

Note: SD in parentheses.

Fiscal slack

It is measured by the ratio of each local government's total revenue over total expenditures. Fund balance is a common measure of fiscal slack in public organizations (Marlowe, 2011). A ratio that is greater than one means that a local government has more fiscal slack; and vice versa. The fiscal data for each local government come from the Annual Survey of State and Local Government Finances (2011 and 2015), U.S. Census.

Learning

This index consists of four items, examining whether a local government examines policies of other governments in (a) their region, (b) their state, (c) other states when developing energy and climate policies, and (d) whether the local government is a member of International Council for Local Environmental Initiatives (ICLEI) U.S. Cities for Climate Protection, a network that provides technical advice, forums for information exchange, training, and software for local governments to engage in sustainability innovation (Betsill & Bulkeley, 2004, 2007; Krause, 2012; Yi et al., 2017b).

Control Variables

Based on existing studies on sustainability innovation, we include several control variables at both city and state levels. At the city level, we include three variables. The first one is city population (Hawkins et al., 2018), which is log-transformed. The second one is goal setting (Kanie & Biermann, 2017), which is measured by whether the greenhouse gas reduction goal has been formally adopted by the city (No = 0, Yes = 1). The third one is sustainability plan (Conroy & Berke, 2004), which measures whether the city has adopted planning goals relating to climate protection or energy efficiency in its general plan (No = 0, Yes = 1). At the state level, we capture if a state's governing body is oriented toward pro-environmental legislation. It is measured by the annual average pro-environmental vote for all members of the Congress in 2011 and 2015 (Carley, 2009; League of Conservation Voters, 2020).

Model Specification

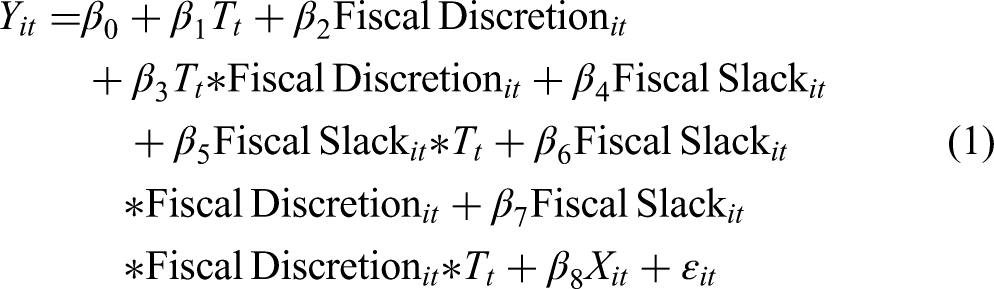

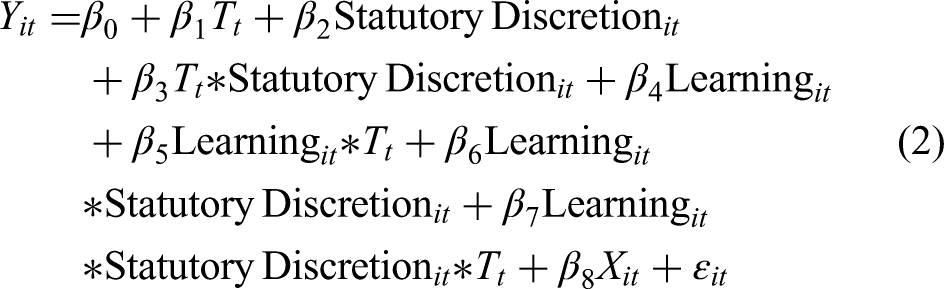

To examine the direct effects of discretion on cities’ adoption of sustainability innovation, one should use the DID analysis to estimate the effects of discretion on the cities as a whole by comparing the situation before and after the discretion changes (some cities were given more discretion while others were not). Due to data availability, we applied the simplest form of the DID design to compare two groups in two time periods. While used in some studies (e.g., Grosso & Van Ryzin, 2012), such design may be questionable because there is some time-varying confounder that changes differentially across the states that make up the study design. One way to strengthen the research design is to add an additional comparison group and estimate treatment effects using a DDD design (Wing et al., 2018). Thus, we incorporated a third comparison group into the DID framework: cities with higher or lower levels of fiscal slack or cities that engaged in proactive learning versus those that did not. The equations are as follows:

Take equation 1 as an example, conceptually,

Warranted by the skewed distribution of the dependent variables, Poisson regressions were conducted for all measures of quality, and goodness-of-fit statistics were examined. The deviance goodness of fit test shows that the assumption of equality of the mean and the variance of the dependent variable imposed by the Poisson model is not violated (Gardner et al., 1995). The nested nature of the data poses a unique challenge: Cities cannot be treated as independent as they are clustered within states. We cluster standard errors at the treatment level (the state), which limits biases caused by the correlation of errors within a unit.

Results

Table 3 includes the descriptive statistics and measurements for all the variables. On average, a city adopts approximately three sustainability-related policies. 5 While 80% of 476 cities are assigned to the treatment group of more fiscal discretion, only 12% are assigned to the treatment group of more statutory discretion. The mean for learning is 2.51, and 60% of cities have engaged in at least 2 learning-related activities. The mean for fiscal slack is 0.75, and approximately 29% of cities have more fiscal slack.

Descriptive Statistics and Measurements.

Note: LCV = League of Conservation Voters.

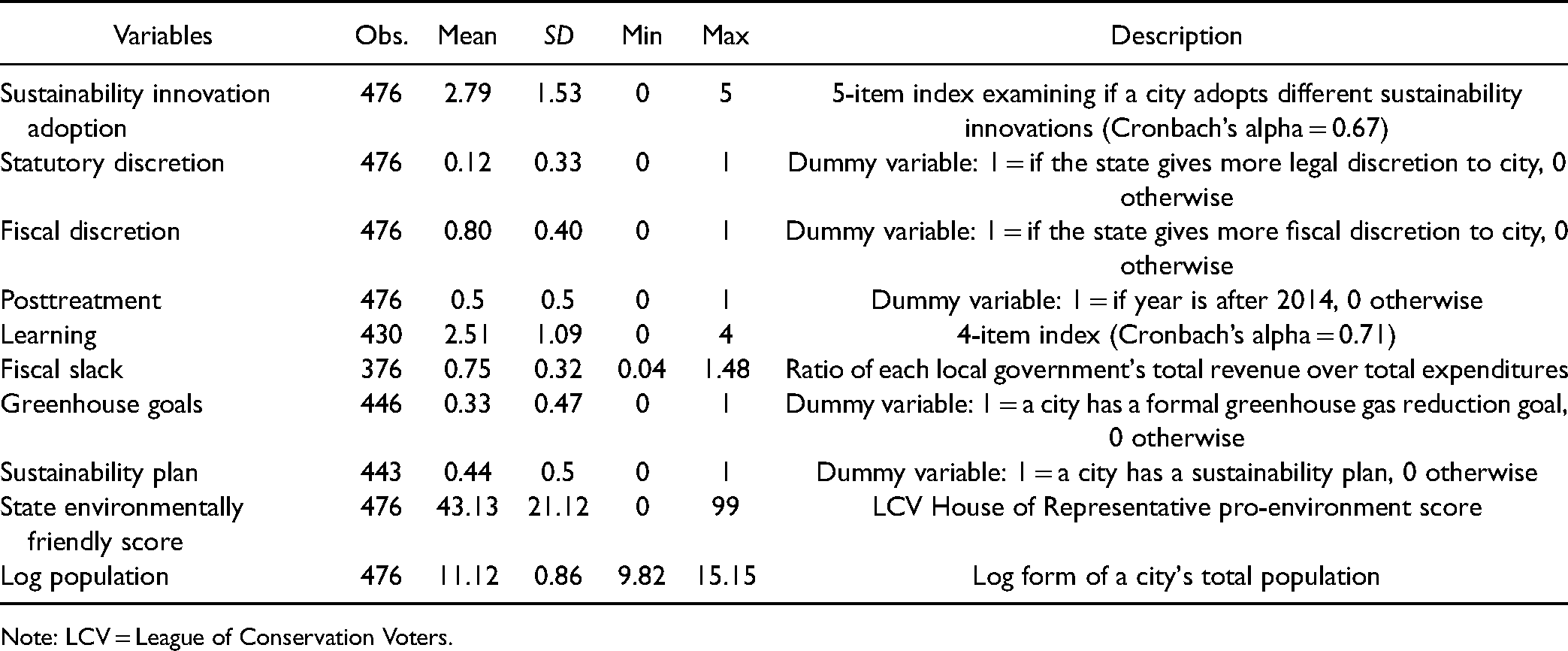

In Table 4, we estimate how fiscal discretion moderates the effects of local characteristics on sustainability innovation. Model 1 is the DID estimation, which explains 50% of the variance in sustainability innovation adoption. In Model 2, we examine cities’ adoption of sustainability innovation after 2014 in cities with higher fiscal slack when developing sustainability policies. Overall, the model explains 52% of the variance in sustainability innovation adoption. The last interaction term represents the DDD estimate. We find that among cities granted more fiscal discretion after 2014, those with a higher fiscal slack are more likely to adopt sustainability innovations than those with lower fiscal slack (β = 2.182, p < .01). Figure 1 shows the effect of fiscal slack on sustainability policy adoption before versus after the treatment. The dotted line indicates the effect of fiscal slack before treatment, and the solid line after the treatment. The graph shows that the positive effect of fiscal slack on sustainability innovation is stronger after treatment than before treatment, supporting Hypothesis 1.

The moderating effect of fiscal discretion on the relationship between fiscal slack and sustainability innovation.

Fiscal Discretion and Local Sustainability Innovation.

Note: N = 376; Numbers in parentheses are SEs and are clustered by states.

***p < .001, ** p < .01, * p < .05, † p < .1.

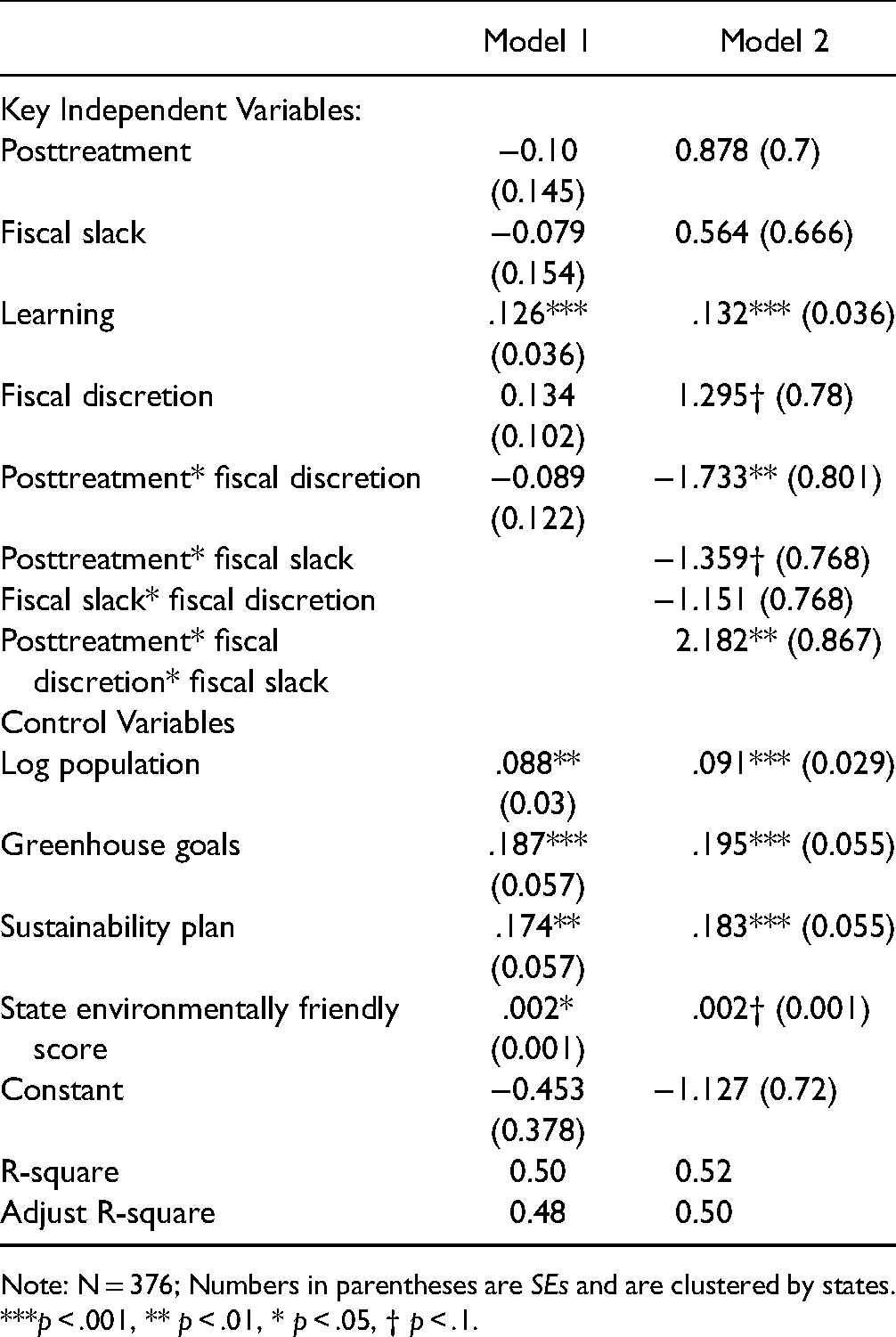

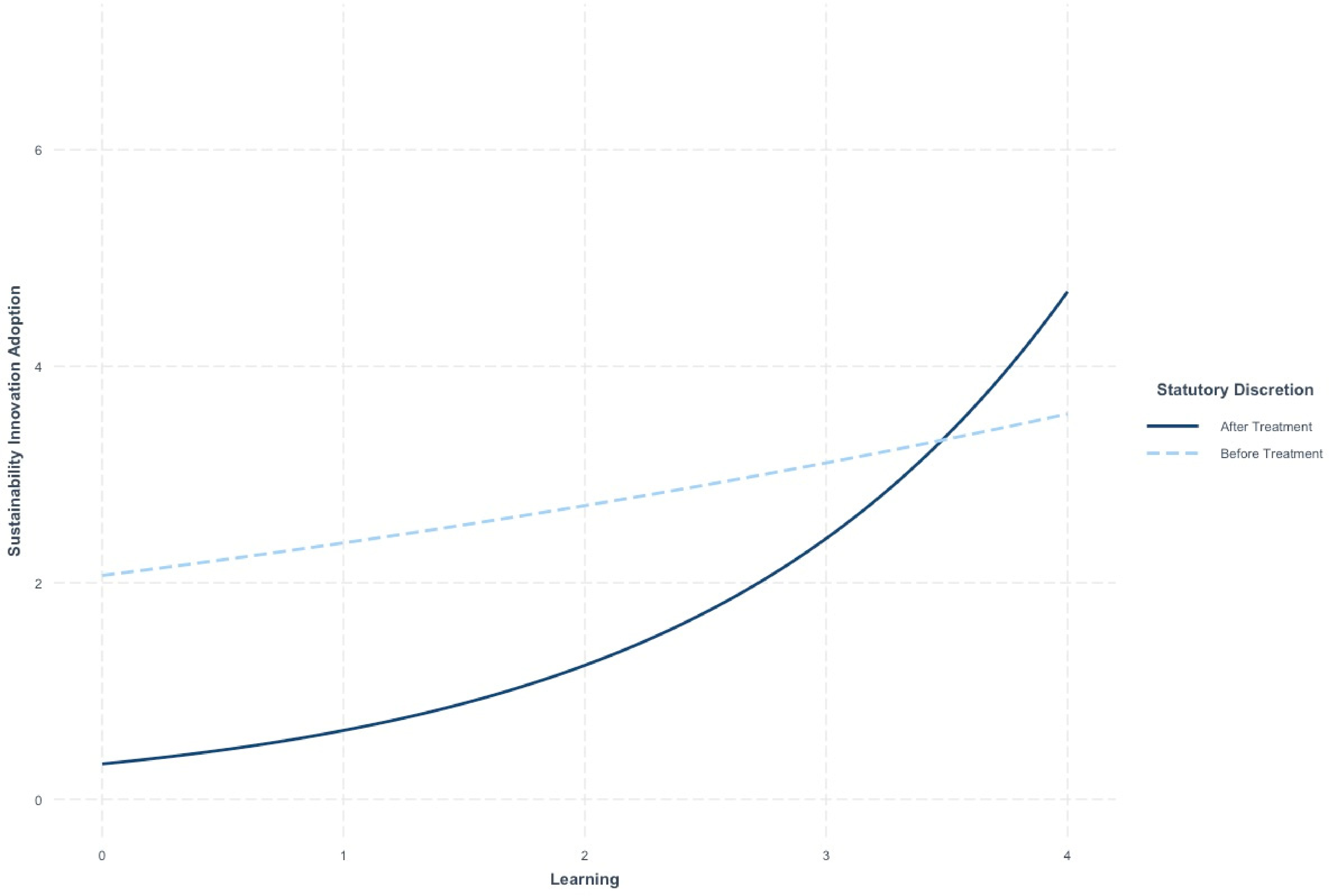

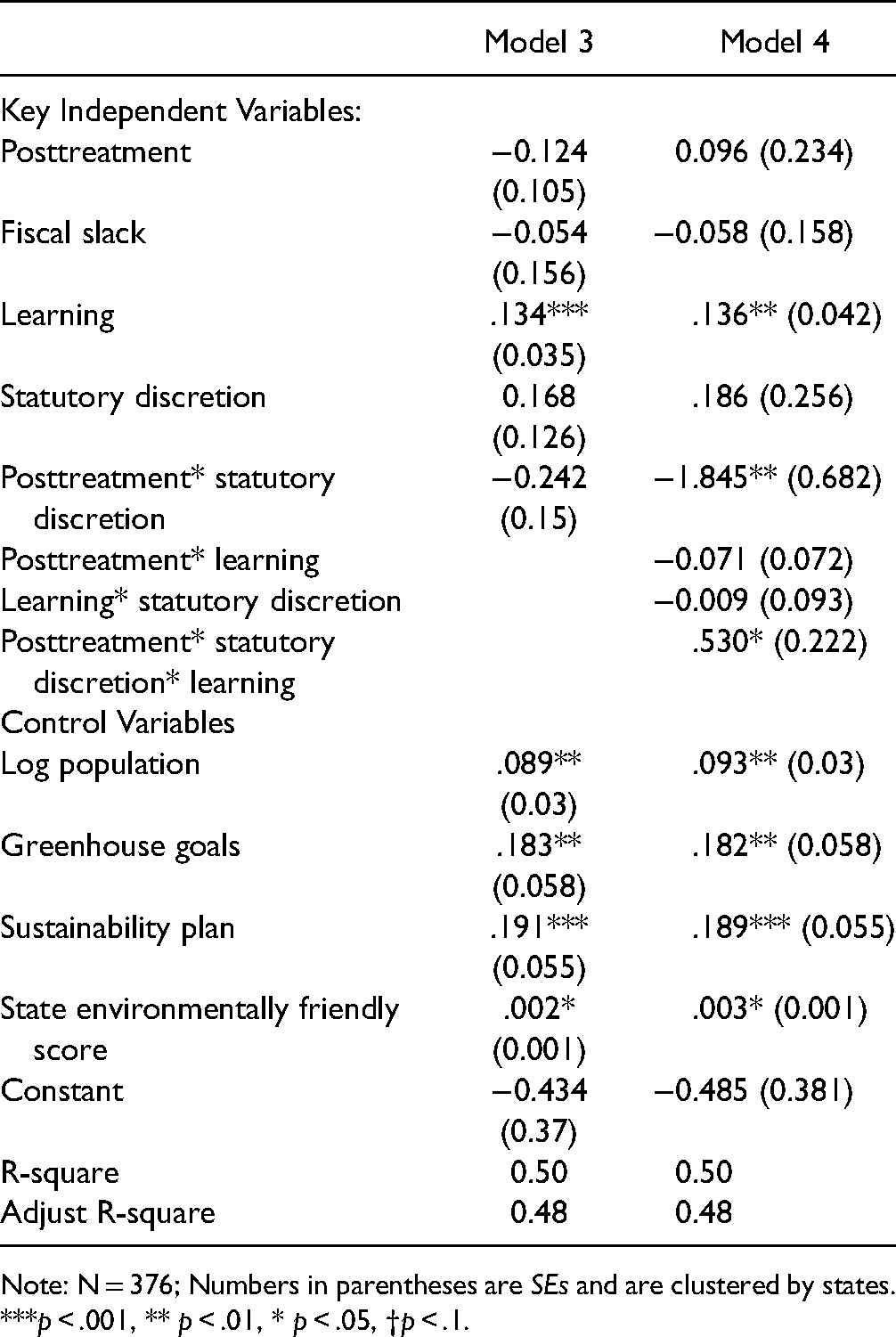

Table 5 examines the effects of statutory discretion. The DID estimates in Model 3 show no significant effects from statutory discretion on sustainability innovation. Model 4 is the DDD estimation model examining cities’ adoption of sustainability innovation after 2014 in cities with more learning when developing sustainability policies. The last interaction term represents the DDD estimate. We find that among cities granted more statutory discretion after 2014, those that learn more from others adopted significantly more sustainability innovation than those with less learning (β = 0.53, p < .05). Figure 2 shows the effect of learning on sustainability innovation adoption before versus after the treatment. The graph shows that the positive effect of learning on sustainability innovation is stronger after treatment than before treatment, supporting Hypothesis 2.

The moderating effect of statutory discretion on the relationship between learning and sustainability innovation.

Statutory Discretion and Local Sustainability Innovation.

Note: N = 376; Numbers in parentheses are SEs and are clustered by states.

***p < .001, ** p < .01, * p < .05, †p < .1.

Across models, the effects of fiscal slack and learning are both positive, and they are stronger when discretion is higher. The results for the control variables are consistent across the four models and are consistent with prior research on sustainability innovation adoption, which buttresses the validity of our research. Specifically, cities with a larger population, a greenhouse goal, a sustainability plan, or states with higher environmental-friendly scores, adopt more sustainability innovations (O’Leary, 1999; Wang et al., 2014).

Inference and Robustness

According to Bertrand et al. (2004), the estimation of DID is in practice subject to a possible serial correlation problem, which may create large mismeasurement in the standard errors. To address this concern, we clustered standard errors by state, which adjusts standard errors by accounting for within-cluster correlation (Cameron & Miller, 2015). As a robustness check, we applied different measures of learning and fiscal slack to calculate DDD estimates. For learning, we excluded one item from the learning index and reran the analysis. For fiscal slack, we replaced the original measure with a measure that examines a city’s surplus over total expenditures and reran the models. The results are overall robust (see Appendices A and B).

Discussion

Findings

This study aims to examine the relationship between local characteristics, discretion, and sustainability policy innovation. Discretion, as an institutional condition, defines or shapes the choices available to local governments. As a critical dimension of power dynamics between different levels of governments, discretion shapes the institutional space in which local governments make innovation decisions independently. Existing studies have highlighted the multidimensional nature of discretion (Verhoest et al., 2004). We distinguish two types of discretion: fiscal and statutory, capturing two ways state governments use to shape local government behaviors. Since measures of municipal discretion in the literature are either subjective or lack updated data, we propose objective measures by examining local–state revenue and expenditure data and bills enacted or adopted by state legislatures, respectively. Our results show that discretion strengthens the effects of local innovation mechanisms. They are consistent with the observation that state-level rules interact with the local environment to alter the decision calculus of local leaders (Krueger & Bernick, 2010). They also echo Walker’s (2014) suggestion that one must examine the joint effects of organizational environments and internal capacities on innovation.

Our results offer insights into the effects of slack resources on innovation. Existing studies show that slack resources can have a positive, negative, or nonsignificant effect on innovation (Damanpour, 1987, 1991; Ringquist, 1993; Walker, 2008, 2014). There are also studies that find the role of fiscal slack is contingent on external environment pressures (Fan et al., 2020). Our results demonstrate that the effect of slack resources is stronger when local governments have more fiscal discretion, implying the effects are context-dependent. The extent to which fiscal slack is effective depends on local government officials’ discretion regarding resource allocation. With more fiscal discretion, local leaders have more flexibility in spending money and more confidence for future fiscal health, which affects how they use current slack resources. Moreover, our results show the effects of fiscal slacks are not only moderated by fiscal discretion but also are curvilinear when fiscal discretion is high. This highlights the complexity of the effects of fiscal slacks, which could be extended to explain other dependent variables. For example, Youm and Feiock (2019) find fiscal discretion is not a predictor of interlocal collaboration in sustainability, but it may be productive to examine whether the effects will show under certain institutional conditions and whether they are curvilinear.

Our results extend the research on the effects of learning on innovation. Learning has been consistently shown to be a salient predictor of policy innovation and diffusion (Berry & Berry, 1999; Glick & Hays, 1991; Gray, 1973; Mooney & Lee, 1995). We confirm that learning stemming from professional networks, which are a prime means for information exchange within organizations and governments, helps local governments to innovate (Borins, 2001; Newman et al., 2001). More importantly, we find the effects of learning depend on institutional arrangements regarding local governments’ flexibility in policy and administration. Our results demonstrate statutory discretion strengthens the positive effects of learning on local governments’ sustainability innovation adoption. Among cities with more statutory discretion, the increase of sustainability policy adoption is more notable in cities with more learning. The results are consistent with Yi and Feiock (2014)'s finding that smaller commissions with a lower degree of checks and balances can encourage states’ renewable energy development. Furthermore, our results show the effects of learning are curvilinear when statutory discretion is high, suggesting that future research should consider the possibility of nonlinear effects.

Our results also show interesting differences between the roles played by the two types of discretion in moderating the effects of local innovation mechanisms. We tested the moderation effect of fiscal discretion on the learning-innovation relationship and the moderation effect of statutory discretion on the fiscal slack-innovation relationship. The results show neither is supported by our data, suggesting that the two types of discretion do not have spillover effects. That is, fiscal discretion strengthens only the effects of fiscal slack on innovation adoption, and statutory discretion only strengthens the positive effects of learning. This seems in line with Strumpf (2002) theoretical argument regarding the effects of decentralization. Overall, our results underline the importance of considering multi-level governance structure and distinguishing between different types of discretion when studying local government innovation.

Limitations and Future Research Directions

This study has several limitations, which provide fruitful avenues for future research. First, we adopt a top-down approach and assume that the two types of discretion are designed or granted. In reality, however, there are many principal–agent dynamics, where some are top-down and others are bottom-up or negotiated (Carpenter, 2010). The very nature of repeated interactions and mutual bargaining in the principal–agent dynamics could lead to the ebb and flow of discretion. Future studies should look into if and how reputable innovating local governments negotiate with their political principals and gain more discretion.

Second, our study focuses exclusively on the U.S. case, which has a strong tradition of local autonomy. It is likely that discretion works differently across political and institutional settings. As Pollitt (2007) argues, “decentralization…can mean something different in France than in Sweden…we need to locate studies of specific acts (or rhetorics) of decentralization within the particular institutional patterns and trajectories of the countries concerned” (p. 382). Even within the United States, the willingness for innovation can vary across forms of government, where executive officials in council–manager governments are more likely to adopt innovations than their counterparts in mayor–council governments (Carr, 2015). However, mayor–council governments are underrepresented in our data, and a more representative sample may add nuances to our findings.

Third, the effects of discretion could also vary across policy domains. Sustainability policy innovation requires more initiative from local governments. The adoption of sustainability innovation must be tailored to local characteristics, highlighting the importance of local discretion and choices. However, in other policy areas, the effects of discretion may not be as salient. One should consider the boundary conditions when trying to generalize our findings.

Fourth, to ensure the internal validity of DID design, one must probe the common trend assumption. Our data only have two groups in two time periods, so the assumption is not testable. We sought to strengthen the research design by adding an additional comparison group and estimating treatment effects using a DDD design (Wing et al., 2018). Future studies should include more time points and conduct more robustness checks.

Fifth, one can explore new ways of measuring fiscal and statutory discretion and verify if the results still hold. For example, statutory requirements are legally binding on local governments, it is common for local officials not to know precisely what they are mandated to do or not do (Bryson, 2003). A review of all relevant legislation, ordinances, charters, articles, and contracts is necessary to determine how many mandates exist, the level of their specificity, and the extent to which they prescribe organizational choices. Future studies can refine our measure of statutory discretion by content-analyzing the details of state legislations.

Conclusion

Scholars have paid increasing attention to mechanisms for local governments’ sustainability innovation adoption. An emerging stream of research focuses on how multi-level governance contexts affect innovation. A particular feature of the multi-level governance framework is the local discretion granted by higher-level governments. However, higher-level institutions often ponder over the level of discretion they should delegate, worrying that lower-level institutions may misuse the discretionary power. This article shows that two types of discretion—fiscal and statutory—are beneficial for local sustainability innovation. If other accountability mechanisms can be put in place to ensure local governments’ responsible behavior, state governments should grant more fiscal and statutory discretion to local governments to encourage local innovations.

As one of the few studies that applied the DDD design to study local government innovation, this article highlights the importance of examining innovation in a multi-level governance framework. In particular, attention should be paid to the separate effects of different types of discretion (and its related institutions). Our findings show that fiscal discretion and statutory discretion interact with different local conditions or innovation mechanisms, and we find no spillover effects. Theoretically, this may not be totally new for decentralization literature but could be expanded to other public management topics. For instance, in representative bureaucracy literature, scholars have long been interested in how discretion moderates the effects of passive representation. Would different types of discretion have different moderating roles? Future research should continue this agenda and examine the moderation effects of different types of discretion on various policy and performance outcomes.

Practically, the separate effects of fiscal discretion and statutory discretion suggest that political principals should adopt a contingency-based view of discretion design in multi-level governance. When granting discretion, political principals should tailor institutional designs to the preferences and needs of the agent as well as the political, social, economic, and institutional contexts. It is not necessarily true that giving more discretion would result in more innovation; the success of granting discretion is contingent on careful assessment of lower-level governments’ local conditions, such as fiscal conditions and learning behaviors.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Social Science Foundation of China, (grant number 17VZL003).

Notes

Author Biographies

Appendix A

See Table A1.

Appendix B

See Table B1.