Abstract

This paper outlines how value can be measured across four elements of the firm/stakeholder relationship beyond standard economic measures. It takes into account the perception of financial value along with non-financial benefits provided and received by the firm and its stakeholders. Focusing only upon the economic or financial outcomes of such relationships can lead to erroneous results as the money spent may not create value for the receiver, and could even do significant harm. The aggregation of views across different firms together with the perceptions of various stakeholders will allow for comparisons between firms and stakeholders. Applying this conceptual model will also reveal what is important to the firm versus what is important to the stakeholder. This paper proposes an improved approach to conceptualizing and measuring net value in which businesses can see if the value they provide exceeds the value they receive from stakeholders and vice versa.

Introduction

Value is contextual, heterogeneous and phenomenological. In line with this, Mazzucato (2022) has argued that economic measurement misses the essence of value and its outcomes. In business, value is created and destroyed in an ongoing complex relationship and interaction between a firm and its various stakeholders. Because of these factors, consistent value measurements across a firm's entire spectrum of stakeholders have continued to elude researchers and practitioners alike. Attempts have been made to look at value from possible economic factors, but are inadequate. But as the world now faces the stark realities of the results of ignoring these relationships and their impacts such as climate change, pollution, human rights abuses, social inequalities, income inequalities, the loss of vibrant local communities, amongst others, it is clear that a new focus on value interaction between a firm and its stakeholders is vital to all of us collectively.

Since its inception, the Journal of Macromarketing has argued that stakeholder relationships beyond shareholders are vital (Hunt 1981), that a systems view of these relationships is tantamount to our understanding of what marketing is (Wooliscroft 2021), and that Socially Responsible Marketing (SRM) is an important concept for modern practitioners and researchers to comprehend and apply (Laczniak and Shultz 2021). While this larger systems view of marketing and its social responsibilities continue to flourish, the counter arguments against such a focus remain equally cogent. From Milton Friedman's (1970) foundational viewpoint, Gaski (2022) has argued that any such stakeholder focus remains flawed and in direct opposition to responsible fiscal management of a company.

Milton Friedman eloquently argued that the only social responsibility of a business was to make profits, and he reached this conclusion by demonstrating that those focused on the larger social impacts that companies make did not have an objective nor rigorous approach to measuring these. And while Laczniak and Shultz have moved the discussion of SRM forward with their work, while eloquently discussing marketing's larger social role and corporate citizenship responsibilities, avoid directly answering Friedman's original arguments against such a stakeholder focus that Gaski has now amplified. Specifically, Friedman's point that all of our talk about social responsibilities are “notable for their analytical looseness and lack of rigor” (Friedman 1970, p. 33) continue to go unaddressed.

Service Dominant Logic (Vargo and Lusch 2016), Stakeholder theory (Freeman 1984), value co-creation (Prahalad and Ramaswamy 2004a, 2004b) and relationship marketing (Berry 1995) each argue that relationships between firms and their stakeholders are (1) 2-way, and (2) that each actor in this relationship (firm or stakeholder) experiences value in their own unique way from the interactions within this relationship. However, the science of measuring value created or destroyed within such relationships remains in its early stages of development due to two important and interrelated issues.

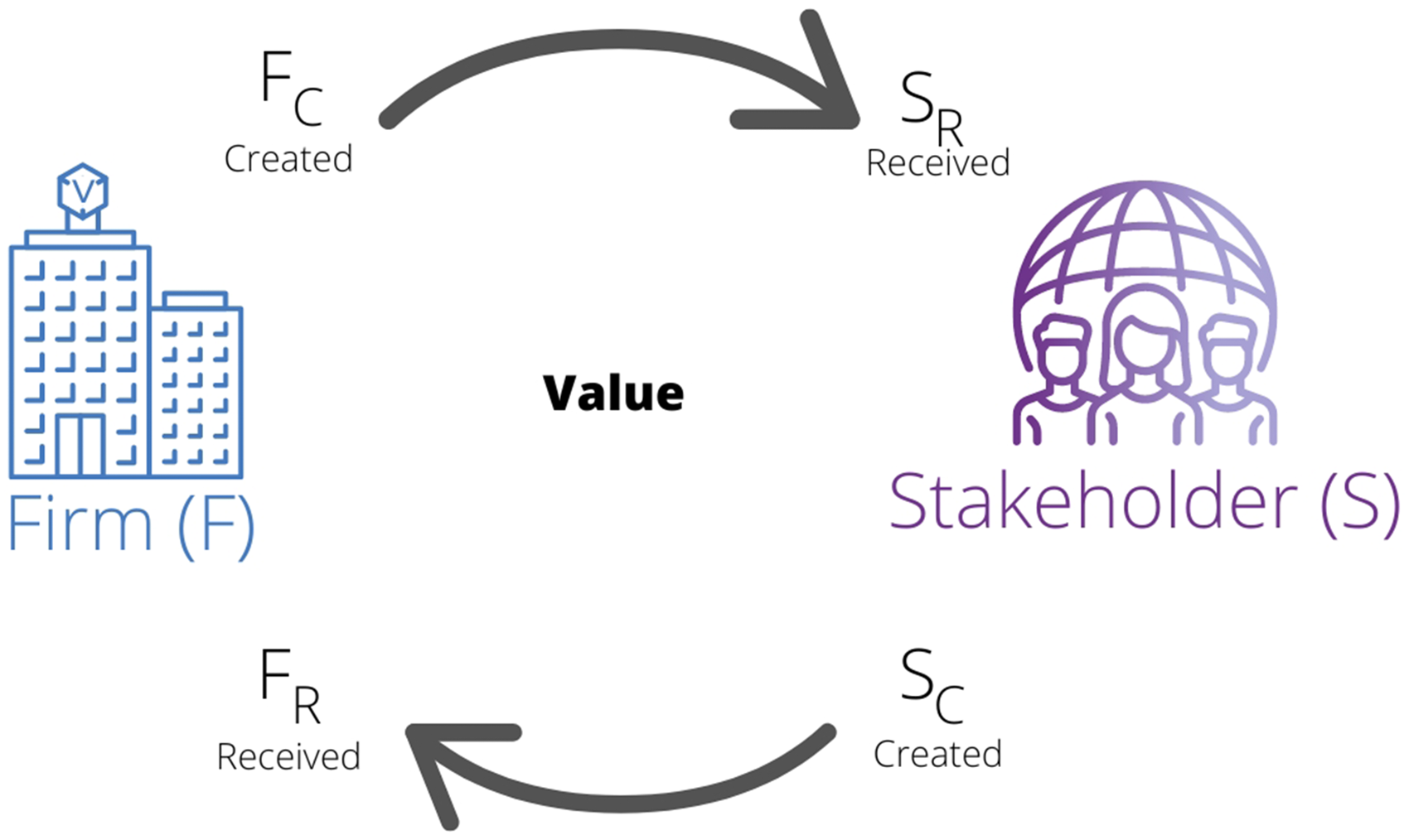

Problem #1 – Perspective

As outlined in Figure 1, a relationship between a firm and any one of its stakeholders can be separated into four unique elements including (1) FC, (2) SR, (3) SC and (4) FR, where “F” refers to the firm as one actor in the relationship and “S” refers to the stakeholder as the other actor. In such relationships, “C” refers to value created by one of these actors, and “R” refers to the value received by one of the actors, or:

FR = the value received by a firm from the stakeholder FC = the value created by the firm for the stakeholder SR = the value received by a stakeholder from the firm SC = the value created by the stakeholder for the firm

Four value flows between firm and shareholder.

In traditional ways of accounting for value, the spending by a firm is considered to create value but a check and balance with the stakeholder that the value provided is actually received or perceived is not included. In reality then, while value may have been conjured into a spreadsheet as an economic value for reporting purposes, it is quite possible that the stakeholder who experienced the intended benefits of such an investment does not value them highly, or at all. Even worse, that stakeholder may feel that such investments have caused them harm, generating negative value instead.

To further highlight the essence of the problem, we find then that two different perspectives of value measurement related to a stakeholder exist depending on whose perspective is taken. For example, if we define the stakeholder as a customer, then customer value can either mean (A) the value the firm receives from that customer (SC→FR), or (B) the value the customer receives from the firm (FC→SR). Each perspective has an extensive body of research related to it. For example, regarding (A) above, lifetime value of a customer research has a long history and continues today (c.f. Jain and Singh 2002; Venkatesan and Kumar 2004). While at the same time there is similarly extensive research from the perspective of the customer and the value received from the firm in line with (B) above (c.f. Kordupleski 2015; Mahajan 2011; Reichheld 2003). Each perspective shows ways of measuring value, offers data for how they have been applied partnered together with real company examples of value measurements and their efficacy and the usefulness of these, but neither imagines value to comprise all four aspects shown in Figure 1 above.

In fact, the exploration of justice related to interpersonal relationships, and relationships between actors within a society are a core element of philosophical thought (Rawls 1971; Sandel 2009). Marketing scholars have built upon this foundation to focus on issues related to the fairness of business relationships and the justice that arises from them. Studies of Distributive Justice (Laczniak and Murphy 2011) highlight the net results of such relationships between actors, and serve as the foundation for some of our thinking here. However, there is scant research on how to settle the balance between these two perspectives either theoretically or practically, leading us to five fundamental questions related to value and its measurement today.

What is the firm's perception of FR, FC, SR and SC? What is the stakeholder's perspective of FR, FC, SR and SC? What is the difference between these views? What behaviours or outcomes result from these views? Can a relationship between these be surmised to show if net value is positive or negative?

We know that the purpose of a firm is to receive more value from a stakeholder than the firm creates for it. This is the value the firm can extract if necessary, as “profit”. For example, from the customer's perspective, different value calculations of these four variables will impact their perceptions of relationship, fairness, and in turn, brand value, stakeholder advocacy for the firm, firm values as perceived by stakeholders, and impact a host of other actions (future purchase decisions, word of mouth decisions, etc.). Similarly, from the firm's relationship and fairness calculations, segmentation strategies will be changed as will pricing decisions, advertising messaging, etc. because these measurements tell the firm what is truly important to them.

Problem #2: Complexity

Chandler and Vargo (2011) propose three levels of complexity in service relationships including the micro level (actor to actor dyads, as we’ve outlined above), meso-level (dyads in relationship as triads), and macro-level (triads in relationship as ecosystems), and all of these functioning within an all-inclusive meta-context. Recent empirical research highlights the critical task facing today's marketing executives in orchestrating optimal performance of different service ecosystems (Carida et al. 2022), however the immense complexity of actually measuring value across each of Service Dominant Logic's three relational levels goes far beyond what any researcher or business software solution can manage.

Hartman (2011, 2019) introduced formal axiology as an approach for measuring value using transfinite calculus more than 50 years ago. Under axiology value is infinite and ever evolving, similar to Service Dominant Logic's view of value constantly emerging. In a system of perfect information, within which the value outcomes from all actor to actor relationships could be captured in real time across micro, meso and macro levels, Hartman's formal axiology offers the proper mathematical foundation for calculating such multiple infinite, constantly evolving value ecosystems.

However, as the technology and tools to do this may be considered a lofty goal for future marketers to achieve, regulatory issues related to data privacy, end user security, and ethics may all combine to stop such a future reality from emerging. In light of this, it is possible that a less complex, proxy-based system for value measurement may achieve enough helpful insights into the measurement and management of value that axiology and the multiple infinities of axiologicial value measurement may never be required. However, as even these systems have yet to be designed, marketing researchers and practitioners are left without a clear understanding of how value is created or destroyed across multiple actor-actor dyads at the meso and macro level.

A Model for Value Measurement

Taking into account these two problems, a possible solution would

First recognize value across all four elements of actor-actor relationships as outlined in Figure 1, while simultaneously avoiding the overwhelming complexity that existing conceptualizations of value measurement entail doing so to help develop enough objective data to spark constructive dialogue around fair and just outcomes for all stakeholders, as proposed by Sandel (2009) show the relative importance of each of the factors contributing to the value as perceived by the receiver of the value and create a means of comparing the value creation performance of firms.

With these five aspects of value measurement understood, the work of marketing team shifts to optimizing value between stakeholders at the individual level, as well as overall value generated across the entire value ecosystem. If such results from all companies could be made available for transparent review by all stakeholders, decisions and investments could then be made based on the impacts that these stakeholders feel to be most valuable in aggregate.

Again, in an axiological world coupled with perfect information flows, firms would be able to capture FR, FC, SR and SC across every interaction with every stakeholder. However, at this point neither the technology nor the capability to measure value in this way exists. Because of this, we believe that a critical first step in achieving this end goal of perfect value measurement is to outline an overall framework for such a system, and develop a survey-based approach to measuring FR, FC, SR and SC that can serve as an initial proxy for this more comprehensive system. With the approach we propose, a view of micro-level, meso-level and macro-level value creation outcomes can be obtained at the time of the measurement, and will hold for some time depending on how fast the business environment changes.

In fact, a significant body of research already exists across each of these stakeholder groups, showing specifically how a firm creates value for its stakeholders and how they in turn create value for the firm. However, to our knowledge no research has yet been conducted to compare the value created from each of these four elements nor the overall value created from the overall value system of all these relationships in aggregate. Based on this foundation, this paper aims to proposes a new way of measuring value.

One should note, as a caveat, firms attempt to measure and use economic inflow and outflow of such value from/to each stakeholder. Many firm managers may just have a gut feeling for whether it is economically worthwhile to do something for society or the planet or some other stakeholder without clear evidence to support these. They then state that this is their corporate social responsibility rather than a business need. We feel instead that this is a business need and positive net value can be derived from stakeholders just as much as positive net value can be received by stakeholder in their interactions with businesses. The precise methodology for calculating these net results has yet to be developed, and could be considered one future research initiative from this current paper.

Moving Beyond Traditional Methods of Measuring Value

Economic value is typically the measure of value created or destroyed by stakeholders for the firm ignoring the impacts that this relationship has on the individual stakeholders themselves. However, recently there has been a change in focus in the purpose of a firm, championed both by the Business Roundtable (2019) and World Economic Forum's Davos Manifesto 2020 (Schwab 2019) that argue that the purpose of a corporation extends beyond the simple generation of value for (1) itself and (2) its shareholders, to include its (3) customers, (4) employees, (5) partners, (6) society, and (7) the planet. Both the Business Roundtable and WEF do not adequately define, or prescribe a way of measuring this value.

A model that measures both economic and non-economic factors to both the firm and its stakeholders can also account for intangible elements. As we will measure value across all six stakeholder categories and, seventh, the firm itself, we can also derive the relative importance of these . We can then determine if there is a mismatch of perception and whether the company could deliver more value for its stakeholders individually or in aggregate by focusing on what is important to the stakeholder rather than what is important to the company.

Specifically, because we are exploring value in terms of actual value perception, measurement and derived impacts (or importance of each factor), the relationship is not necessarily zero sum, with increasing levels of stakeholder value possible to be generated at potentially little or no extra financial expense. There can also be widespread ripple effects from one action across multiple stakeholder groups. For example, by embracing a zero plastic waste policy, a company not only can create incremental value for nature, but simultaneously for customers, employees, partners and society. In turn, this shift away from plastics may not only increase sales (economic value), but additionally brand equity both inside (non-economic employee value) and outside of the company (non-economic customer value, non-economic partner value, economic social value) such as word of mouth recommendations made by customers or society.

In order to measure value across these four unique instances of value creation and reception as outlined in Figure 1, it is essential to first define what we specifically mean by value.

Value, as defined by the Journal of Creating Value (Mahajan 2017) is “executing normal, conscious, inspired, and even imaginative actions that increase the overall good and well-being, and the worth of and for ideas, goods, services, people or institutions including society, and all stakeholders (like employees, customers, partners, shareholders and society), and value waiting to happen”.

For a business to create value based on this definition, we measure an increase in the overall good as the net difference benefits and cost, which can be measured financially (i.e., price) or non-financially (i.e., time, effort, etc.).

How the Measurement is Done

The first step for any measurement of value between a micro-level stakeholder dyad is to define the components of value (such as benefits, cost) specifically and in the context of each individual actor. While future technology advances will allow for the passive collection of such data through either software tools, or other data collection and tracking systems, in this paper we propose the collection of this data through surveys delivered to each actor in the relationship dyad. For example, for employee value calculations, we would survey both the human resources department of the company (i.e., Chief Human Resources Officer) and a representative sample of employees working for that firm and experiencing the results of the decisions that the human resource executives make. Similar dyads for other stakeholder/firm relationships would include a responsible officer from the firm and a stakeholder representative.

As stakeholder representatives are heterogeneous, value measurements should take into account the context of measurement which may be defined as unique geography, business segment or timing, or any other factor that would make the measurement of the same actors within a different context return different perceptions of value. Companies with heterogeneous stakeholder groups may choose to conduct such surveys across multiple segments in order to gain a complete understanding of value creation impacts across and between these.

With the survey sample defined, the next step required to measure value is to build a waterfall of needs (Kordupleski 2003) of stakeholders and the company. This enables executives to look at the entire needs of both the stakeholder and the firm from their own unique perspectives. For example, society may view the benefits of a company trying to enter as potential employers, as investors in society through plant and equipment; then as taxpayers and spenders in the economy, as well as people helping in charity and through corporate social responsibility (CSR) initiatives. Ultimately, the goal of this exercise is to clearly define the unique themes, both financial and non-financial that comprise SC, SR, FC and FR for this relationship dyad.

The second step of this process is to use the information collected in Step 1 to create value attribute trees that show the components of value (SC, SR, FC and FR) in detail. These attribute trees are written down, and then vetted by experts inside and outside the company to confirm their validity. Comments from the subject matter experts can also be used to firm up the contents of these attribute trees. Typically, the main components of value are benefits and costs (or sacrifice). Benefits break up into those items important to a stakeholder. For example, for a customer these could include product, service, image including brand, people, or relationships. The value trees then take on meaning by breaking each component into sub components. Thus, sub components of product can be feel, experience, ease of use, or functionality.

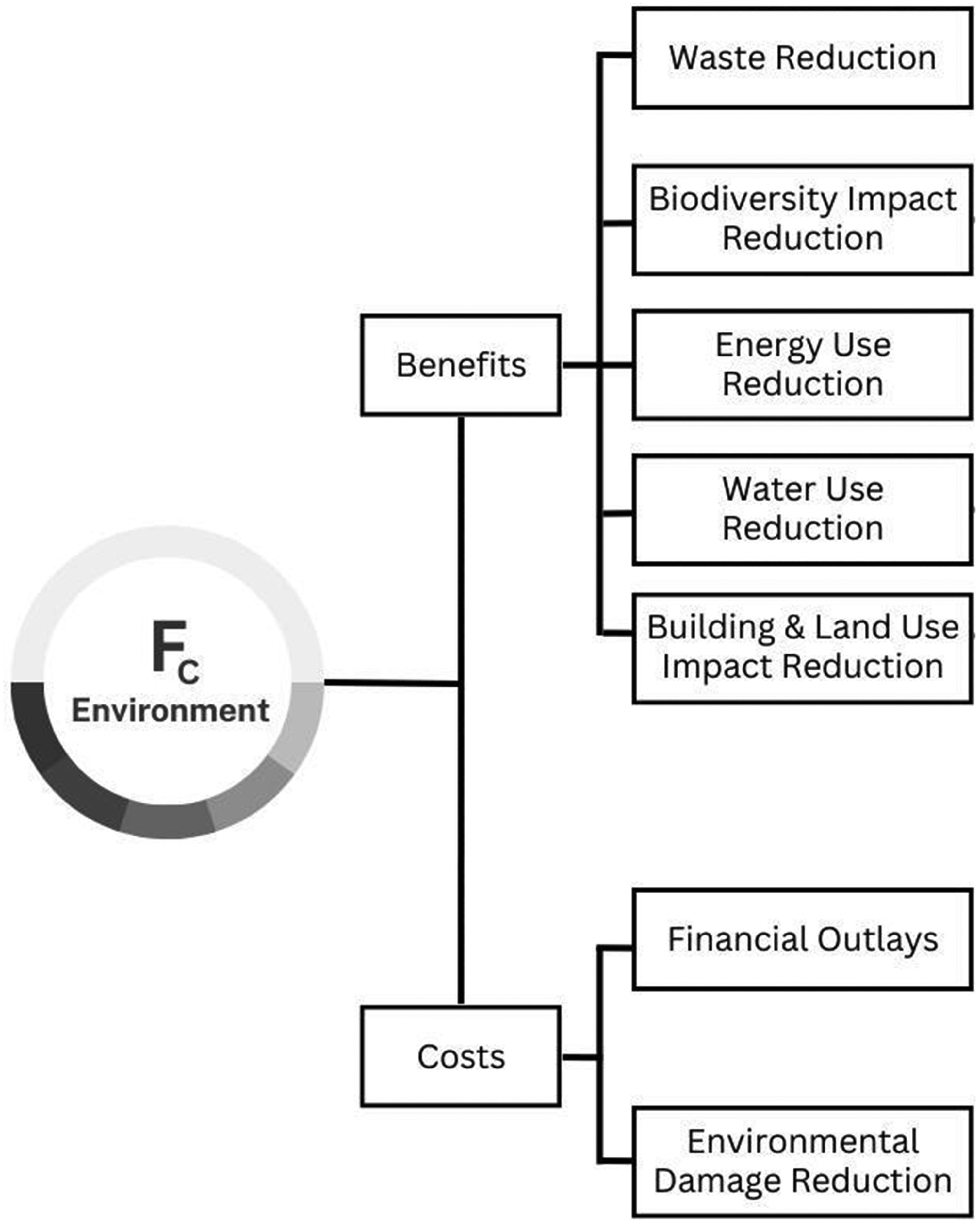

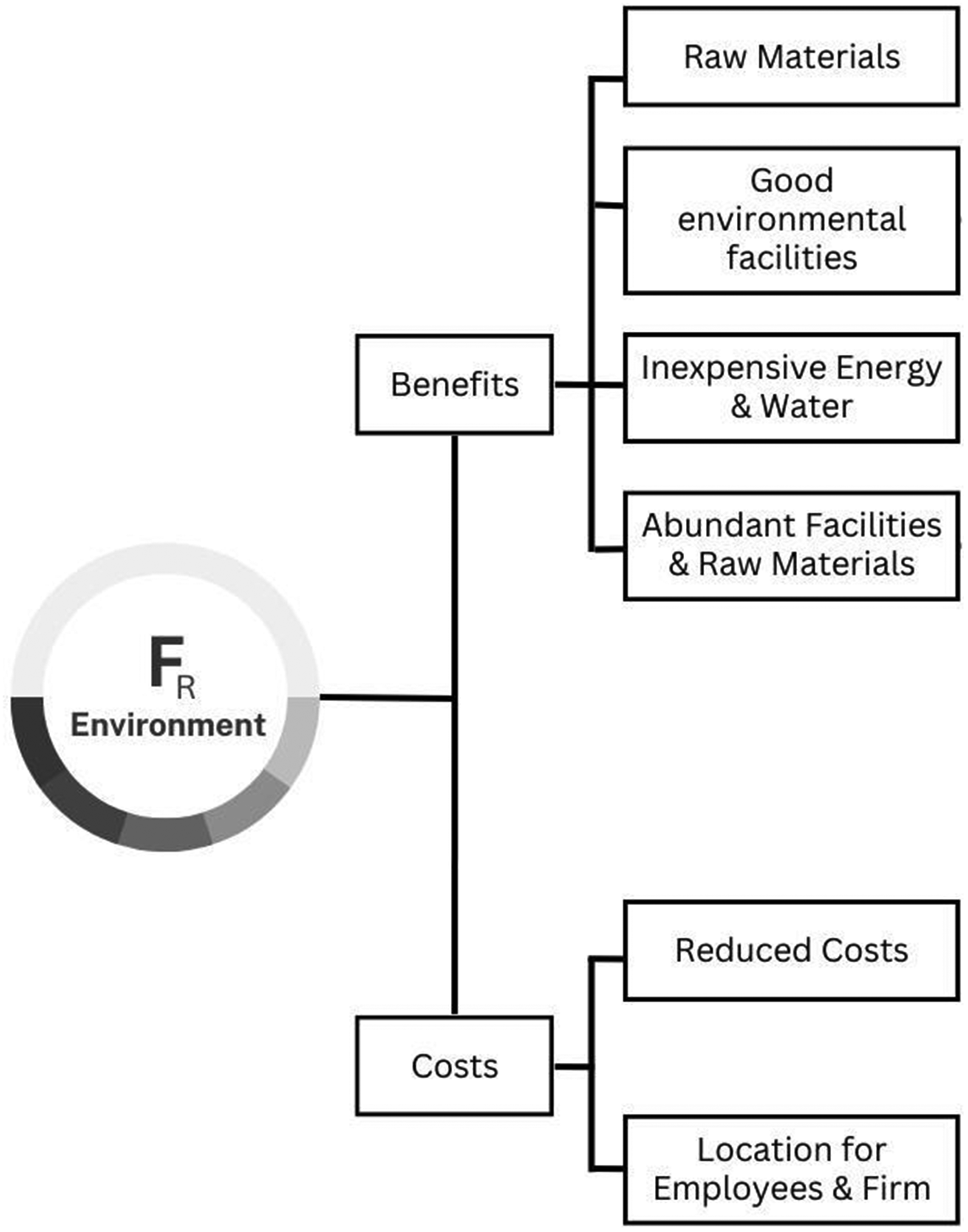

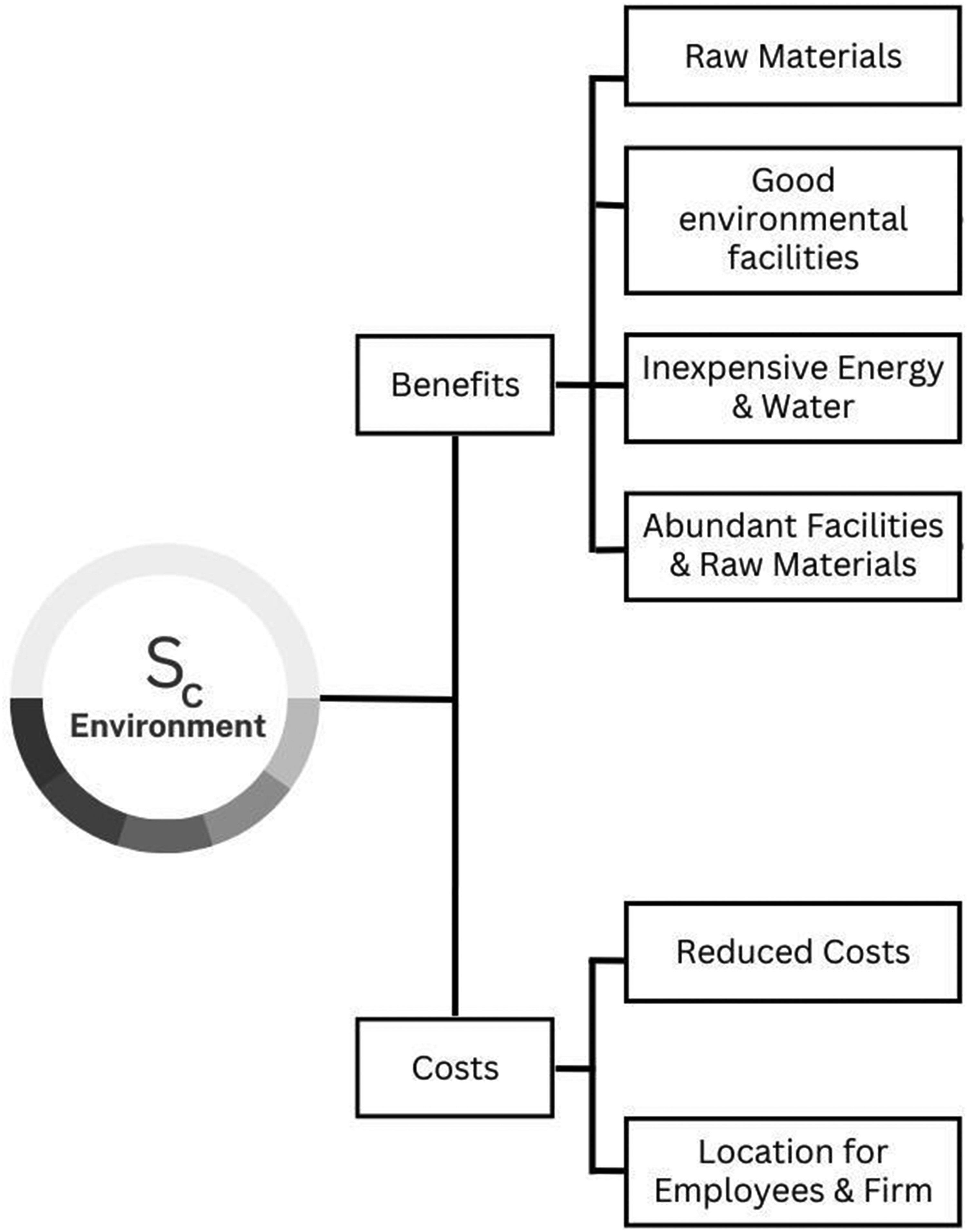

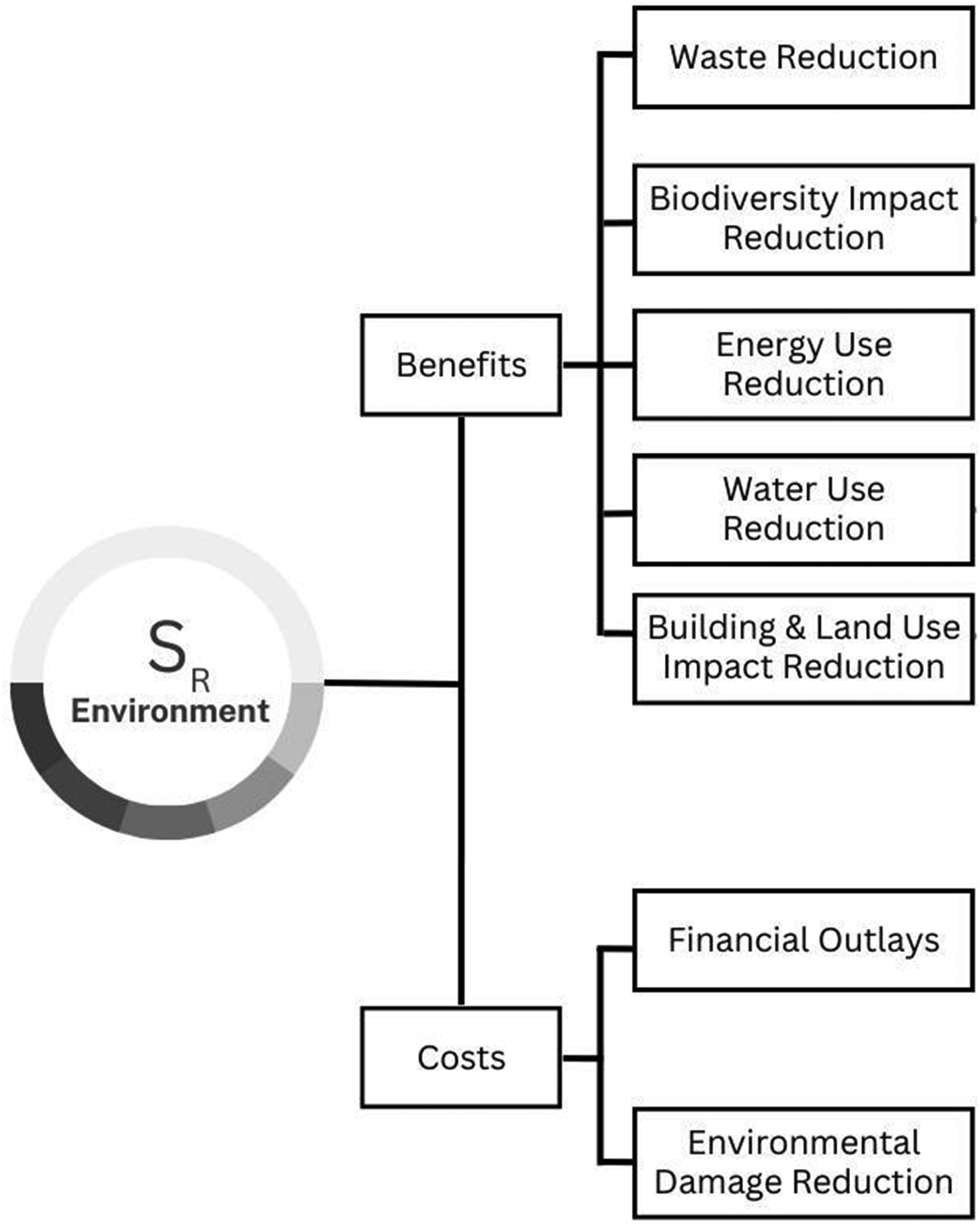

Examples of how such value trees would look from each of the four perspectives within on of the stakeholder-firm dyads (here Firm – Environment) are shown below. (Figures 2–5)

Firm-Environment value tree FC

Firm – environment value tree FR

Firm – environment value tree SC

Firm environment value tree SR

With these Value Trees in place, Step 3 of this process includes the formal specification of the stakeholder group into a population for study and an appropriate, representative research sample. And once each of these samples are defined surveys are developed from the attribute trees, which can be further tested in a pre-market survey, corrected, and ultimately the surveys are fielded, and data is collected.

Step 4 includes the process of analysis. This approach gives researchers the ability to see the relative importance of each of the inputs to value perceptions for both the stakeholder and the firm using correlation analysis.

Further Details of Survey and Analysis

Using the survey methodology outlined in Step #3 above:

Representatives of the firm rate their perceptions of FR, FC, SR and SC Representatives of the individual stakeholder group rate their perceptions of FR, FC, SR and SC FR <–> SC, or the value the firm feels it receives from the stakeholder vs. the value the stakeholder feels that it has provided to the firm. FC <–> SR, or the value the firm feels it provides to the stakeholder vs. the value the stakeholder feels that it has received from the firm FR <–> FC, or the value the firm it feels it provides to the stakeholder vs. the value the firm feels that it has received from the stakeholder SR <–> SC or the value the stakeholder it feels it provides to the firm vs. the value the stakeholder feels that it has received from the firm

Based on these results, in Step #4, we can then compare:

We can then compare the relative differences between how firms and their stakeholders judge the overall relationship across these four interactions outlined above. In doing so, issues of relationship fairness (or justice) can be highlighted, and the relative strength of these relationships in the past, present or future can also be derived.

There are clear limitations from implementing such a research approach, most specifically that results can only serve as proxies for the actual, infinite and constantly emerging elements of value mentioned by Hartman and within the Service Dominant Logic literature. But until the technology to capture value emerging in real time across micro, meso, and macro-levels of actor-actor, dyad-dyad, and triad-triad interactions is developed, we believe that this is a legitimate proxy for value measurement until then. If such research is done across multiple companies in similar industries, average benchmarks of performance across all four of these variables can be calculated, and more robust comparisons can be conducted. Then every company can compare itself to the industry average, see where they stand, and understand how important each item is to each stakeholder category.

Another important result is that stakeholders can start to understand firms better, Thus, employees, partners, society can understand the firms needs better and devise negotiations and better performance stances.

Analysis of Value Created and Received

As we mentioned earlier no comprehensive methodology yet exists for comparing the value given by a firm and received by a stakeholder or vice-versa which has complete validity. Below, we outline four unique levels of value measurement that can be applied in a research effort to measure relative value.

Level 1: The firm's opinion of FC, SR, SC, and SR Level 2: The firm's and the stakeholder's opinions of FC, SR, SC, and SR Level 3: The firm's and a large and statistically valid group of stakeholders (let us say in this case, society) views of FC, SR, SC, and SR and use these to extrapolate the average thinking of stakeholders within the larger population. Level 4: Each firm in context of its larger industry group Level 5: Each industry in context of its larger overall market

Based on these levels, we can see the importance of standard scores and measures of value and their resulting relative value calculations from such measurements. Doing so will not only help each firm become better at generating the value but simultaneously increase the value each stakeholder receives in aggregate from all competing firms. The firm then becomes far more attuned to the needs and perceptions of its stakeholders as it adjusts its perceptions to better match theirs.

After this in-depth analysis of stakeholder value is developed, a firm's leadership team can then update its overall corporate strategy to better align with stakeholder needs, improve competitive advantage; and competition can shift to increasingly better and more innovative ways of meeting the needs of all stakeholders. Eventually, all this should lead to better efficiency, more focused efforts, improved market share and profitability.

Future Research

Based on this foundation, the next step beyond the actual implementation of these surveys and the publication of their results will be the development of a real-time, updatable value measurement system, potentially using AI to highlight key trends across industries and markets, while also creating individual reports at the firm and stakeholder level. This will in turn lead to the development of better, stakeholder-based business strategies that generate the highest possible value.

We are also left with a series of questions that we hope future researchers will undertake:

Question 1: Assuming that a business is profitable, how can it continue to improve the value it creates and receives from these stakeholders? Question 2: How can companies start to look at stakeholders as potential profit centres rather than as cost centres? Question 3: How can automatic data reception and reporting from each stakeholder be implanted to develop real-time value-focused dashboards? Question 4: How can the results of this approach be used to compare various geographies and industry segments? Question 5: How can these results be used to better align purpose, mission and vision with actual value creation outcomes for stakeholders?

Conclusion

Approaching value in the ways that we have outlined throughout this paper give a clearer indication of the synergy between how companies and their stakeholders view their relationship, and the specific elements that make that empower the relationship to create or destroy value. Economic value, which has been the main view of value implemented throughout western capitalism, offers only an opaque approximation of value, because it is based on several unknowns and offers executives limited tools to handle intangibles. The methodology that we have outlined in this paper offers an improvement on pre-existing economic valuation models and offers a platform to enable firms and their stakeholders to work more closely together to forge a common value mindset.

Footnotes

Associate Editor

M. Joseph Sirgy

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.