Abstract

Online reviews have become a significant factor in determining prices, complementing the intrinsic qualities of goods. In the art market, these reviews elevate the interaction between artists and connoisseurs, but the diverse levels of expertise and influence among participants demand a more detailed approach. This study investigates the impact of expert opinions and public sentiment on painting prices, using a hedonic regression model with artist-specific fixed effects. Given the common practice of buying art for investment in the secondary market, we also analyze the relationship between review sentiment and investment intentions. Based on a dataset of 18,100 sold paintings, we find that negative sentiment from all sources and positive public sentiment significantly influence prices. Moderation analysis shows heightened sensitivity to negative opinions from experts and media reports. This research contributes to understanding the interaction between social media and the art market, as well as key price determinants for artworks.

Introduction

Media exposure is the key to establishing a sale’s credibility. Before the sale, a media plan is drawn up to enhance the value of the collections or single works and excite the desire of would-be buyers. After the sale, the media serves to amplify the impact of the most impressive prices (only, of course, when those prices and that impact are positive).

— Judith Benhamou-Huet, The Worth of Art

Over the past two decades the diffusion of social-media platforms has transformed the circulation of information about art. Instagram and Twitter now function as always-on galleries, allowing collectors, critics, and casual viewers to comment in real time on exhibitions, record-breaking sales, or even the work in an artist’s studio. This development has “flattened” what was once a vertically organized market, replacing the tight brokerage of a few dealers and critics with densely connected horizontal networks of opinion. Empirical studies of Instagram art accounts, for example, document large-scale peer-to-peer interaction and its measurable effect on visibility and market attention (Kang et al., 2019). Sociological analyses likewise show that contemporary art prices are embedded in these networks of aesthetic judgment and reputation rather than being set by cost or scarcity alone (Beckert & Rössel, 2013).

The public auction room amplifies those social signals. Economic experiments and field data confirm that open, ascending-price auctions generate “auction fever”: bids rise more steeply when participants can observe the competition, and herding behavior is common even when comparable, lower-priced lots are available (Ashenfelter & Graddy, 2006). A celebrated illustration is the sale of Andy Warhol’s Green Car Crash (Green Burning Car I), which realised US$71.7 million at Christie’s New York in May 2007 after a frantic exchange of telephone and floor bids (Renneboog & Spaenjers, 2013). Such headline results are quickly relayed across mainstream and social media, shaping collectors’ perceptions of an artist’s financial and cultural standing.

Conversely, negative publicity can depress prices or even jeopardize a sale. Museum deaccession controversies—such as the decision by the Albright-Knox Art Gallery in Buffalo to sell Artemis and the Stag in 2007—triggered critical scrutiny of both the work and the seller, raising questions about provenance, public stewardship, and long-run resale value (Paterson, 2013). In markets where authenticity, reputation, and future liquidity are difficult to verify, adverse signals carry particular weight.

Taken together, these observations suggest that the economic value of an artwork is tightly coupled to the sentiment environment that precedes a transaction. Yet existing quantitative research still treats expert opinion, journalistic coverage, and public commentary as interchangeable sources of “buzz”. Building on sociological theory and auction economics, we distinguish among these voices and test their separate and joint effects on prices in the secondary market. Our analysis therefore asks:

How do sentiments expressed by experts, professional media, and the broader public differentially affect auction outcomes? Does the impact of those sentiments intensify when a purchase is undertaken as a financial investment rather than for aesthetic consumption?

By integrating textual sentiment measures with a hedonic price model that controls for artist fixed effects and detailed object characteristics, we provide fresh empirical evidence on how layered information flows—from blue-chip critics to anonymous social-media users—enter the price-formation process.

Public

Art, from its earliest origins, has been intimately intertwined with communal belief systems. In antiquity and through the medieval period, artworks were predominantly housed in temples and churches, where they functioned as integral components of sacred ritual. The advent of the public museum in the late eighteenth and early nineteenth centuries—institutions deliberately modelled on classical temples—marked a decisive desecularization of art. This art historical period also witnessed the emergence of a new aesthetic ideal: the cultivation of refined taste by a privileged few who could devote themselves to the contemplation of beauty. Yet by the twentieth century, many artists began to reject this elitist vision, seeking instead to desacralize art and transform spectators from passive observers into active participants.

In the 1920s, Bertolt Brecht (1898–1956) pioneered what he termed the “Verfremdungseffekt” or “alienation effect,” interrupting performances so that actors would directly engage the audience in a critical dialogue about their roles (Majumdar et al., 2021). Brecht’s intervention underscored the notion that the only truly authentic response to art is the judgment of its public.

This democratic conception of art deepened in the postwar decades. From the mid-1960s onward, Carl Andre (Pinotti et al., 2018) (b. 1935) and Richard Serra (Liberti et al., 2018) (b. 1938) eschewed traditional pedestals, installing large-scale industrial sculptures at ground level to invite physical and social interaction. In the 1970s, Dennis Oppenheim (1938–2011) (Slifkin, 2019) further extended this participatory ethos through kinetic works activated by viewer-controlled triggers.

More recently, the Tate Modern instituted a “People’s Glossary,” soliciting interpretations from non-experts and elevating them as a valid commentary on exhibited works (Curd, 2020). Similarly, at recent Turner Prize exhibitions (Cunningham, 2022), dedicated “commentary rooms” have given the general public direct input into curatorial narratives.

In the twenty-first century, then, public opinion has emerged as a primary driver of how artworks are valued and understood. This raises two crucial questions: Who shapes collective taste, and by what mechanisms do they do so? In addressing these questions, we turn to two intertwined practices—art journalism and art criticism—as the principal mediators between artists and audiences.

Journalists

According to the Artsy Gallery Insights 2021 Report, “the ranking of the top sales channels shuffled considerably this year, with online sales, social media, and gallery websites taking the place of art fairs and walk-ins” (Artsy, 2021). To stimulate sales, dealers actively use stories, advertising posts and even personal messages to the potential buyers. However, is this an exceptionally modern business technique?

Since the end of the 19th century, the informational function of art has become increasingly important. To promote the Impressionists, the legendary merchants Paul Durand-Ruel (1831–1922), Georges Petit (1856–1920), and Ambroise Vollard (1866–1939) began to collaborate actively with the press. Durand-Ruel engaged famous writers and art theorists, including Emile Zola (1840–1902), to create loyal notes (Nayeri, 2023); he published two international art magazines, La Revue internationale de l’art et de la curiosite (Lambert, 2015) (1869) and L’art dans le deux mondes (Dickie & Bordonaba, 2016) (1890–1891), in which he produced social popularity of the Impressionists. Vollard had his own publishing house and attracted artists, in particular one of the most influential modernist artists Marc Chagall (1887–1985), to create color lithographs (Christies, 2022): the reproduction of paintings played a significant role in art popularization.

Since the emergence of mass media, artists themselves have used it to attract attention to their creativity. Dadaist and Surrealist exhibitions gained fame by their performances, flamboyant and frequently shocking actions (Floyd, 2017). All this was done in order to attract wide public and media attention, to achieve mass fame. Dadaist and Surrealist art was brought into fashion in the literal and figurative sense.

Charles Saatchi (b. 1943) was one of the first mega art collectors, who used media technology to promote artists. The international success of the Young British Artists was partly due to the active support of the local press (While, 2003).

Critics

George Dickie’s institutional theory reconceptualises art as a social artifact: an object only becomes “art” when it is presented to an audience under the designation “this is art” and then evaluated by a community capable of understanding its intent and qualities. In Dickie’s view, without critical appraisal—and the legitimating role of evaluative institutions—an object cannot fully attain the status of a work of art (Van Maanen, 2009).

The figure of the art critic first emerged in the late eighteenth century, concomitant with the artist’s emancipation from purely ecclesiastical or aristocratic patronage. As painters ceased to work exclusively on commission and began to serve an anonymous public market, critics stepped in as mediators, representing the tastes of cultured sectors of society and providing authoritative judgments on artistic quality. This “connoisseur” function persisted until the early twentieth century, when avant-garde creators started to challenge prevailing public tastes. In response, a new breed of critic arose—not as a mouthpiece for existing preferences, but as an ally of artists in their critique of dominant aesthetic norms. Harrison and Cynthia White famously chronicled this “dealer–critic system,” in which commercial galleries secured sales while critics furnished ideological validation (Saint-Raymond, 2019; White & White, 1993).

Today, art criticism remains indispensable for the legitimisation of contemporary practice, which often eschews traditional criteria of representation and craft. Without critical frameworks to articulate conceptual underpinnings, much contemporary work risks losing both intelligibility and perceived value.

The purpose of this article is to answer the following research questions:

Intrinsic characteristics: size, medium (acrylic, gouache, oil, etc.), genre or theme, date, signature, and other physical attributes (Garay, 2021; Renneboog & Spaenjers, 2013). Sales characteristics: auction house, sale location, sale date, and a dummy for whether the artist was living at the time of sale. Acquired characteristics: prior exhibition record, mentions in catalogues or monographs, and other proxies for recognisability and fame.

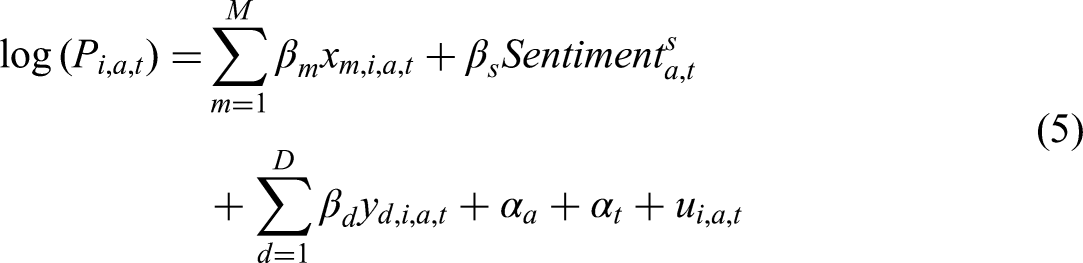

To investigate these questions, we employ a hedonic pricing model that regresses log prices on three sets of explanatory variables (Pimenov et al., 2025; Stepanova, 2019):

In addition, we include an investment-value proxy—whether the work was later resold—to capture buyers’ resale expectations (Foka, 2018). Renneboog and Spaenjers (2013) suggest that the aggregate sales volume at high-profile Impressionist and Modern auctions can serve as a leading indicator of market sentiment.

With this framework, we measure three distinct sentiment streams—expert tweets, journalistic articles, and public posts—and estimate their separate and joint effects on prices. Our empirical sample comprises 18,100 paintings sold at Sotheby’s, Christie’s, and Phillips from 2012 through 2021. We then conduct a moderation analysis to assess how repeat-sale intention amplifies or attenuates sensitivity to each sentiment source.

Our findings reveal that negative sentiment from all three groups significantly depresses prices, whereas positive public sentiment has a discernible price-boosting effect. Moreover, investment-oriented buyers exhibit heightened responsiveness to negative expert and journalistic sentiment. These results deepen our understanding of how layered information flows—from credentialled connoisseurs to anonymous social-media users—shape value formation in the art market.

This paper is structured as follows. Section “Related Work” reviews the relevant literature; Section “Conceptual Model and Hypotheses” develops our theoretical model and hypotheses; Section “Data” describes the dataset; Section “Method” outlines the econometric approach; Section “Results” presents the empirical findings; and Section “Conclusion” concludes with implications and avenues for future research.

Related Work

A growing body of literature examines how professional and public opinions shape prices, demand, and other market outcomes across diverse industries. Depending on the nature of the product under review, expert judgments may be captured via structured ranking systems—common in sectors such as film (Peng et al., 2013) and wine (Ashton, 2016; Cardebat et al., 2014)—or through free-text commentary annotated with star ratings or numerical scores. When lay consumers adopt similar ranking schemes, it becomes feasible to compare expert versus crowd evaluations directly. Beyond dedicated review platforms, social-media posts have emerged as a rich source of both professional and public sentiment; their high volume and rapid cadence have been leveraged to forecast asset returns in financial markets (Fraiberger et al., 2021; Jiao et al., 2020; Ullah et al., 2022) and to study consumer behavior in other contexts (Barhorst et al., 2020c; Upadhyaya et al., 2023). However, such unstructured data require careful filtering to isolate relevant messages and rigorous sentiment-analysis techniques to quantify their valence.

Certain markets demand a stringent definition of “expert.” In the case of experience goods—whose quality can only be assessed post-purchase—buyers frequently rely on certified ratings or professional evaluations. For example, in oenology, multiple scoring systems maintained by accredited critics guide investment in fine wines (Ashton, 2016). In the art world, expertise is more diffuse: gatekeepers may include museum curators, gallery directors, critics, collectors, and even artists themselves (Ginsburgh, 2003). These intermediaries not only shape an artwork’s cultural legitimacy but also influence its economic performance: negative critical reviews can dampen short-term sales and erode long-run symbolic value (Debenedetti, 2006). Assessing the intrinsic and acquired worth of an artwork requires substantial cultural capital (Angelini & Castellani, 2019; Seaman, 2006), and experienced dealers and professional critics exert a great deal of influence over market sentiment. Becker and Johnson (1982) note that critics and gallery owners often discover and promote the same emerging talents, underscoring the pivotal role of expert networks in artist reputation formation.

As the art market has grown increasingly complex, scholars have advocated for segmenting participants and goods to reveal more precise pricing dynamics (Plotkina & Munzel, 2016; Prieto-Rodriguez & Vecco, 2021). Such segmentation may rest on intrinsic attributes (e.g., artist biography, exhibition history) or on features that are less directly observable, such as buyers’ willingness to pay and sellers’ reservation prices. A particularly salient dimension is investment intent: artworks purchased with the explicit aim of resale may respond differently to sentiment signals than those acquired for personal enjoyment. Indeed, the 2021 Art & Finance Report by Deloitte Private finds that over three-quarters of collectors and art professionals cite investment as a primary motive for acquisition (Deloitte, 2021). Even among those who value art for its emotional resonance, financial considerations remain prominent. Moreover, the Hiscox Online Art Trade Report (Hiscox, 2020) documents a dramatic rise—from 48% in 2016 to 87% in 2020—in the use of social-media channels such as Instagram to discover and evaluate artworks, underscoring the deepening integration of digital sentiment into art-market decision-making.

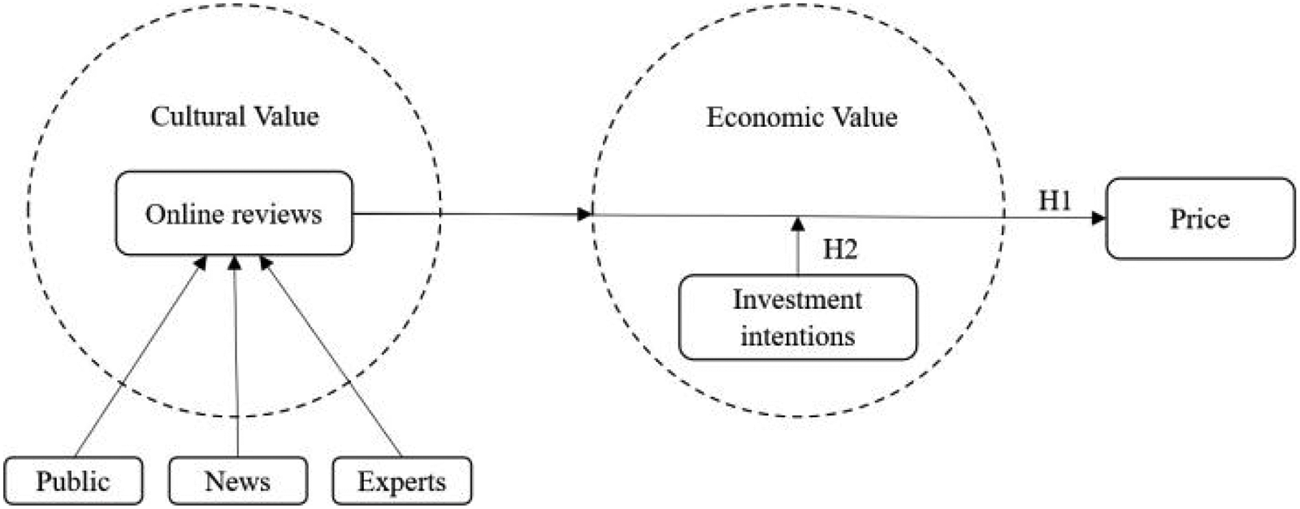

Conceptual Model and Hypotheses

Existing scholarship on cultural goods frequently applies a value-based approach to investigate their pricing, distinguishing principally between economic and cultural values (Angelini & Castellani, 2019; Throsby, 2000). The economic value typically encapsulates the artwork’s price and exchange potential, whereas the cultural value comprises a multifaceted array of attributes, including aesthetic, spiritual, social, historical, symbolic, and authenticity dimensions (Throsby, 2003). Specifically, aesthetic qualities and cultural significance constitute core aspects of cultural value; social value emerges from shared experiences among observers; historical value fosters continuity with past cultural heritage; symbolic value encompasses meanings communicated through the artwork; and authenticity underscores the uniqueness of the artwork. Scholars widely agree that fluctuations in cultural value correlate significantly with shifts in economic value, underscoring their inherent interdependence (Hutter & Frey, 2010; Throsby, 2000).

Due to the complexity inherent in assessing cultural value, researchers have adopted various methodological approaches. Throsby (2000) identifies three principal evaluation methods: mapping (contextual analysis), attitudinal analysis (capturing social and spiritual engagement via individual responses), and expert appraisal (professional assessment of aesthetic, historical, and authenticity dimensions). Within contemporary art markets, expert appraisal methods are increasingly executed through analysis of online reviews, reflecting the rapid proliferation of digital communication platforms and social media channels. Platforms such as Twitter facilitate the aggregation and classification of substantial volumes of relevant evaluations according to author expertise, enabling rigorous empirical analyses of cultural valuation.

In operationalizing expert appraisal, we adopt essential characteristics of art professionals based on criteria outlined in the related literature: experts should possess recognition, influence in defining artwork quality and value, and substantial educational or cultural capital. In digital contexts, these characteristics can be proxied effectively through metrics such as follower counts, reach, and reputation within online communication channels.

Following the existing theoretical framework (Angelini & Castellani, 2019), we formalize our conceptual model as a set of interrelated equations:

Artist fame, a critical determinant of economic value, is influenced not only by intrinsic talent but also significantly by external validation from critics, curators, collectors, and other prominent market participants. Consequently, we specify the formation of artist fame as:

Figure 1 summarizes a four-step causal pathway connecting information flows with realized auction prices. Initially, expert assessments—from critics, curators, and prominent dealers—provide credible signals of quality and authenticity. Empirical evidence based on large-scale data demonstrates that social signals, rather than intrinsic visual attributes, primarily account for variation in contemporary art prices (Lee et al., 2024).

Conceptual Model and Hypotheses.

The second step involves media amplification, wherein specialist publications and mainstream media rapidly disseminate expert evaluations to broader audiences. Financial market research similarly documents that aggregated expert sentiment conveyed through media reduces informational friction and consequently affects asset prices (Fang & Peress, 2009; Tetlock, 2007). This analogous mechanism operates effectively within art markets.

Third, these amplified signals influence public sentiment. Studies analyzing social media indicate that engagement metrics, such as likes, comments, and follower growth on platforms like Instagram, closely mirror shifts in perceived artistic value, originating from influential expert or institutional posts (Kang et al., 2019).

Ultimately, when expert appraisals, media tone, and public sentiment align, they collectively affect auction outcomes. Positive social signals systematically elevate

The vertical arrow labeled H2 in Figure 1 illustrates how investment intentions moderate this causal pathway: investors, who approach art as a financial asset, respond more sensitively to negative amplified signals—a documented phenomenon in both conventional financial markets (Tetlock, 2007) and fine-art market studies (Hernando & Campo, 2017). This integrated framework clarifies the process through which expert commentary diffuses via media, shapes public sentiment, and ultimately influences secondary market pricing. Changes in cultural value informed by these diverse opinions subsequently transform into economic value shifts.

To address our first research question on the impact of online reviews on artwork prices, we propose two initial hypotheses:

Additionally, because experts often serve as reference points for investors (Cameron, 1995; Hernando & Campo, 2017), the economic valuation of artworks may vary depending on whether they are viewed primarily as investments or aesthetic objects. Prior research suggests that artworks acquired explicitly for investment purposes exhibit heightened sensitivity to market signals (Deloitte, 2019). Thus, using repeat sales as a proxy for investment intent, we propose two supplementary hypotheses:

To control for potential heterogeneity due to artistic movements (Hodgson & Hellmanzik, 2019), our moderation analysis specifically focuses on artworks within the Pop Art genre, thereby enhancing empirical comparability.

Integrating evaluations from experts, media, and the public into our value-based conceptual model allows us to comprehensively examine how layered assessments of cultural value ultimately influence the economic valuation of artworks. This framework, as depicted in Figure 1, explicates the information flows underlying price formation in the secondary art market.

Data

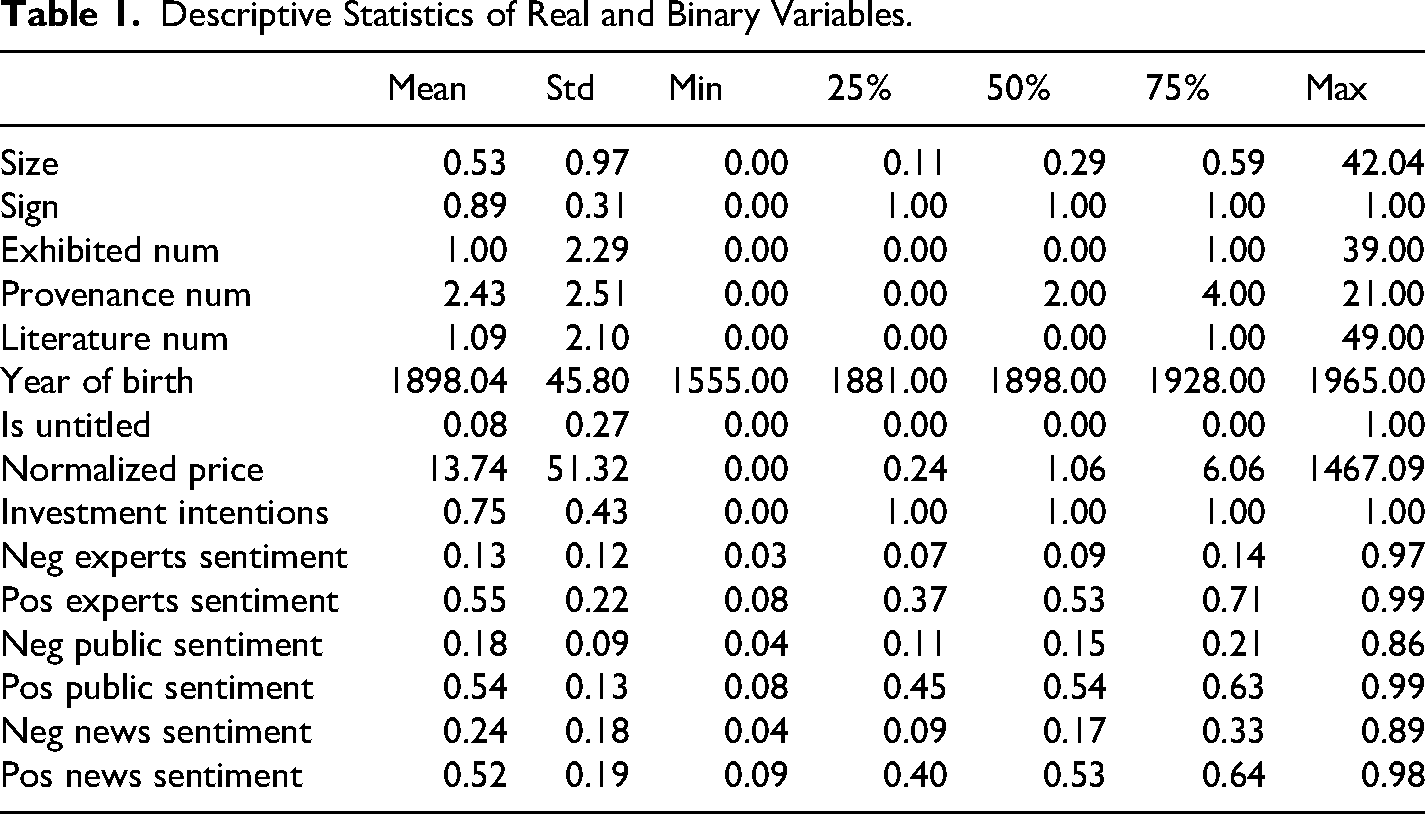

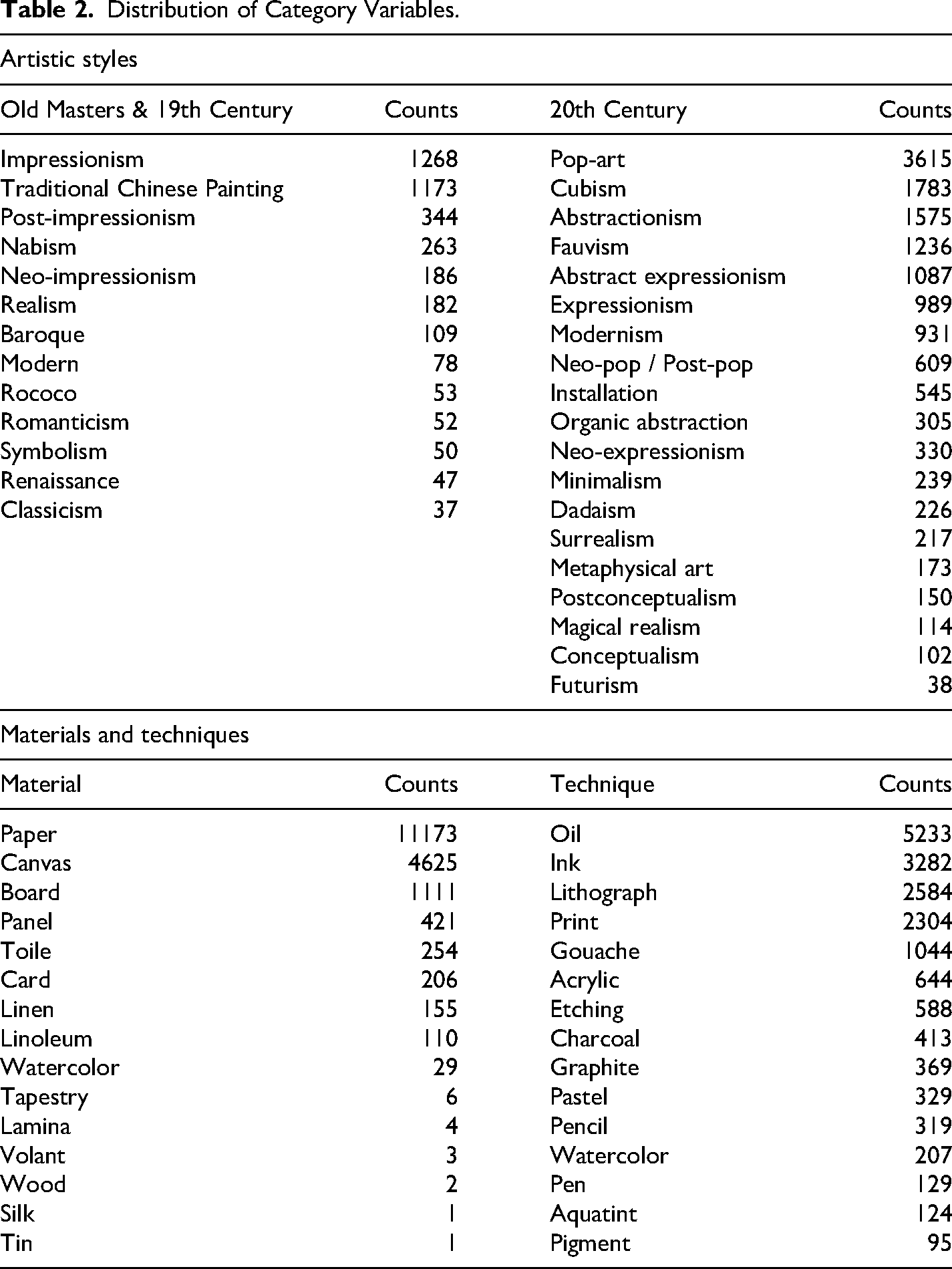

Our empirical analysis draws on a hand-curated dataset of 18,106 paintings auctioned between January 2012 and mid-2021 across three leading houses (Sotheby’s, Christie’s, and Phillips). These works span 32 stylistic categories, with Pop-Art (3,615 lots) and Cubism (1,783 lots) the most prevalent, and include 97 distinct artists (each represented by at least 20 paintings). Seventy-five percent of the objects in our sample have been resold at least once, although repeat-sale records are unevenly distributed owing to our uniform sampling protocol over the decade. In terms of physical attributes, 89 % of the paintings bear the artist’s signature and 72 % were offered framed. By auction house, 8,419 lots sold at Sotheby’s, 5,983 at Christie’s, and 3,704 at Phillips. Detailed summary statistics appear in Table 1 (continuous and binary variables) and Table 2 (categorical breakdowns).

Descriptive Statistics of Real and Binary Variables.

Distribution of Category Variables.

To quantify public sentiment, we harvested approximately 512,000 tweets that mention one of the 97 artists in the 60 days preceding each sale. Sentiment scores were generated by the transformer-based

Tweets have become a rich source for gauging collective attitudes across domains (Trabucchi et al., 2018). We used the Twitter API to filter messages that mention an artist’s name; attempts to further narrow by “artist–painting” pairs yielded insufficient volume for robust inference. Consequently, our sentiment measures capture the prevailing tone toward each artist in the immediate pre-sale window, in line with our conceptual model that positions artist fame as an input into economic value. Following prior work on asset pricing and goods valuation (Oliveira et al., 2017; Ranco et al., 2015), we adopt a 60-day event window for both tweet-based and news-based sentiment aggregation.

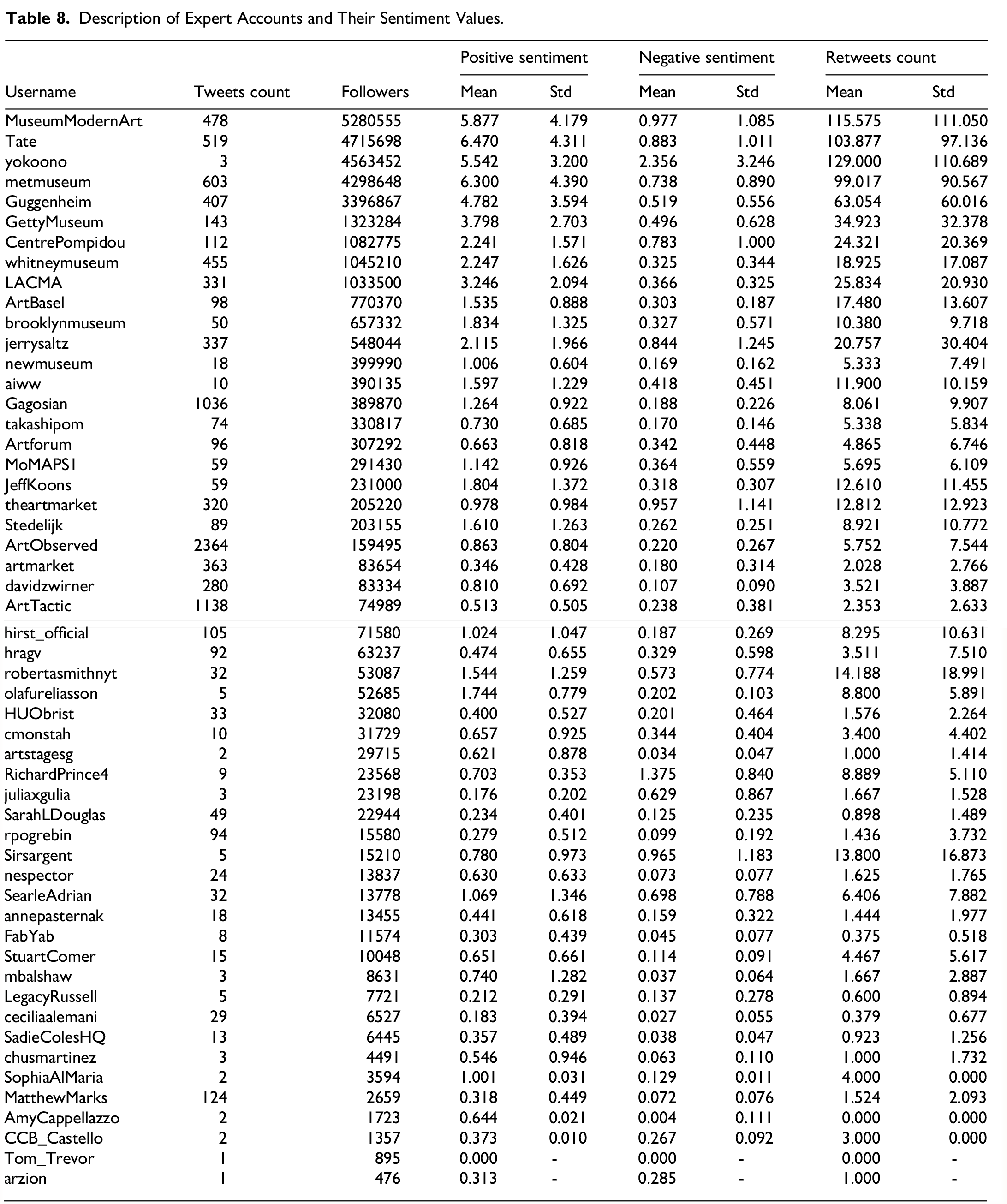

To assemble a corpus of professional opinions, we first identified expert Twitter accounts following the criteria laid out in Section “Related work”. An initial seed list was drawn from the “ArtReview Power 100”—an annual ranking of the 100 most influential figures in the global art world (ArtReview, 2022). We then examined the follow-lists of these accounts to surface additional art-focused users with large audiences. To ensure comprehensive coverage, we augmented this set with official accounts of leading galleries, major biennials and fairs, museum directors, and respected art publications—each meeting our definition of an expert by virtue of both authority and reach.

Using the Twitter API, we retrieved 10,161 tweets from 53 such experts, with Andy Warhol emerging as the most frequently cited artist. To account for each expert’s relative influence, individual tweets were weighted by their retweet counts before aggregation. Sentiment scores for expert posts were calculated using the same Twitter-RoBERTa-base-sentiment model described above for public tweets. Table 8 provides an overview of expert accounts, their characteristics and mean sentiment values.

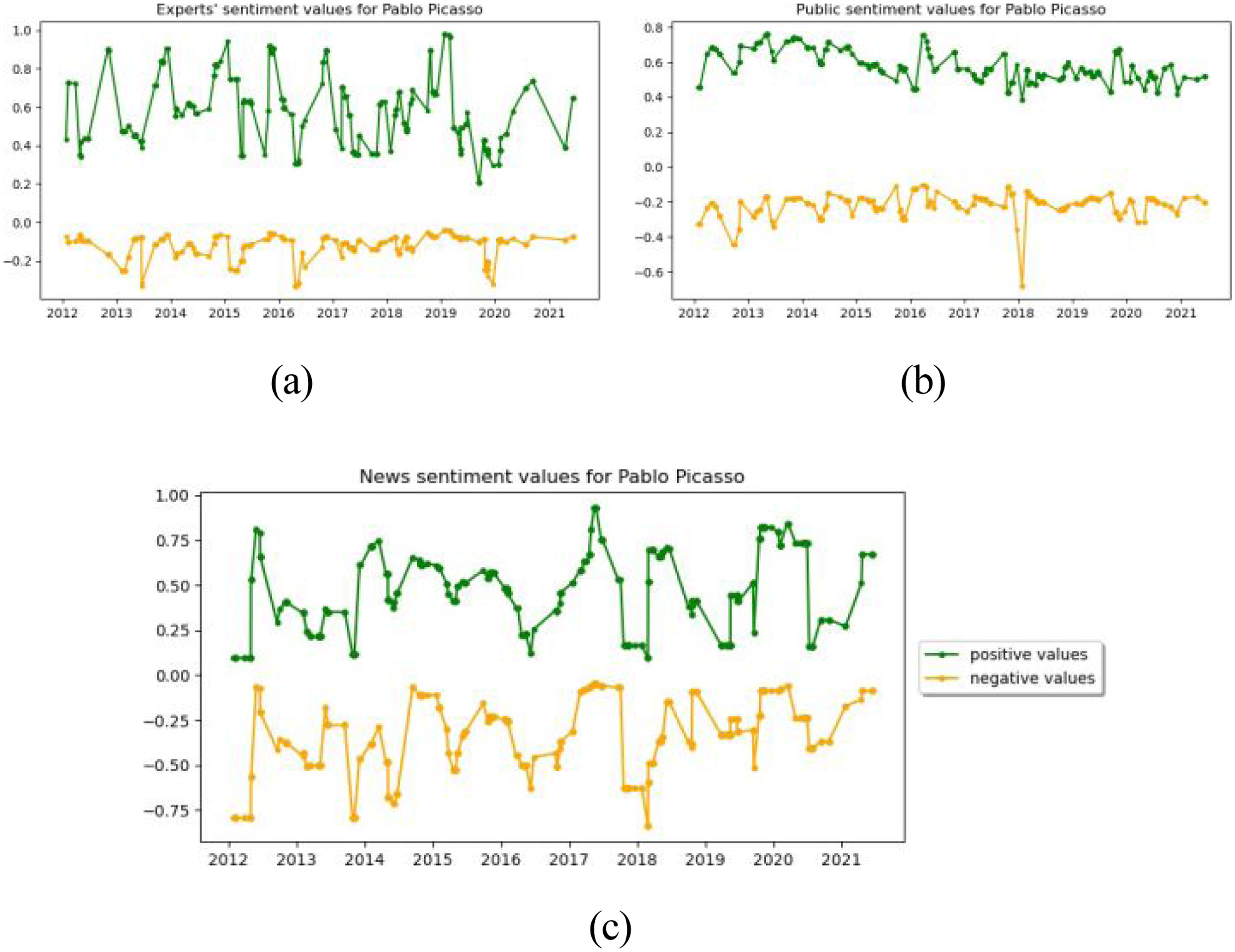

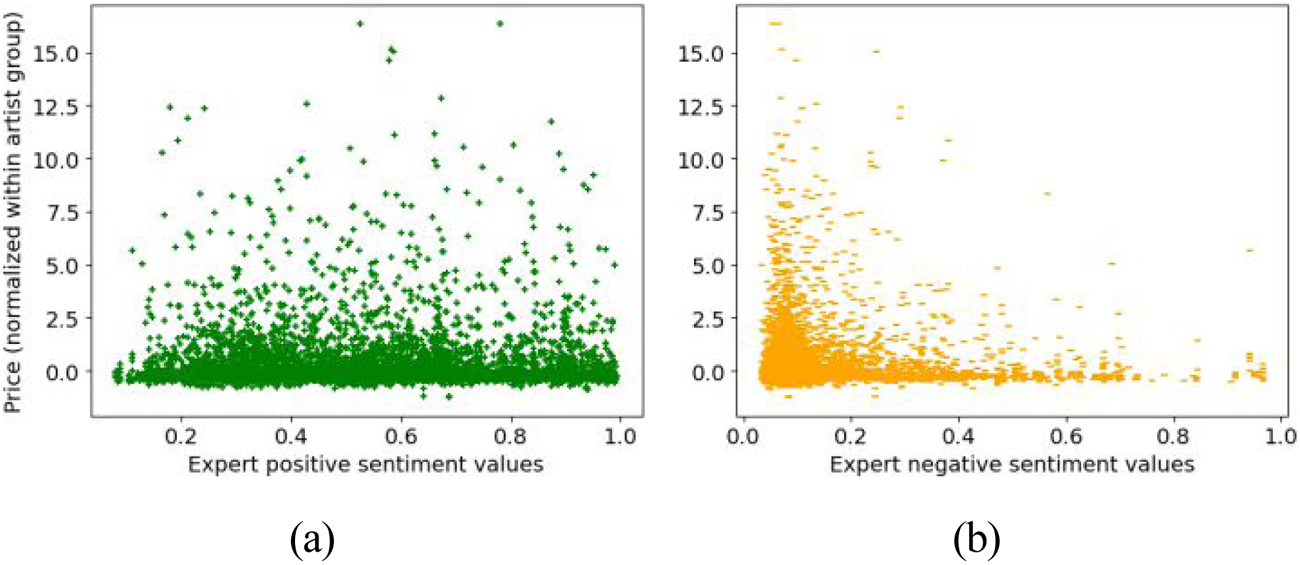

Figure 2 presents the temporal trajectories of positive and negative sentiment from experts, the general public, and news sources in the sixty-day window preceding each sale of Pablo Picasso’s works. For visual clarity, negative-sentiment scores have been inverted. In Figure 3, we plot normalized within-artist prices against expert sentiment. Whereas positive expert sentiment exhibits no discernible pattern, higher negative sentiment is systematically associated with lower normalized prices, consistent with the hypothesized deterrent effect of adverse professional appraisals.

(a) Expert Positive and Negative Sentiment Scores for all Sales of Pablo Picasso’s Paintings (Negative Values Inverted for Clarity). (b) Public Sentiment Scores for Picasso’s Sold Works. (c) News Sentiment Scores for Picasso’s Sold Works.

Scatterplots of Normalized Painting Prices within Each Artist Group Against (a) Positive Expert Sentiment and (b) Negative Expert Sentiment.

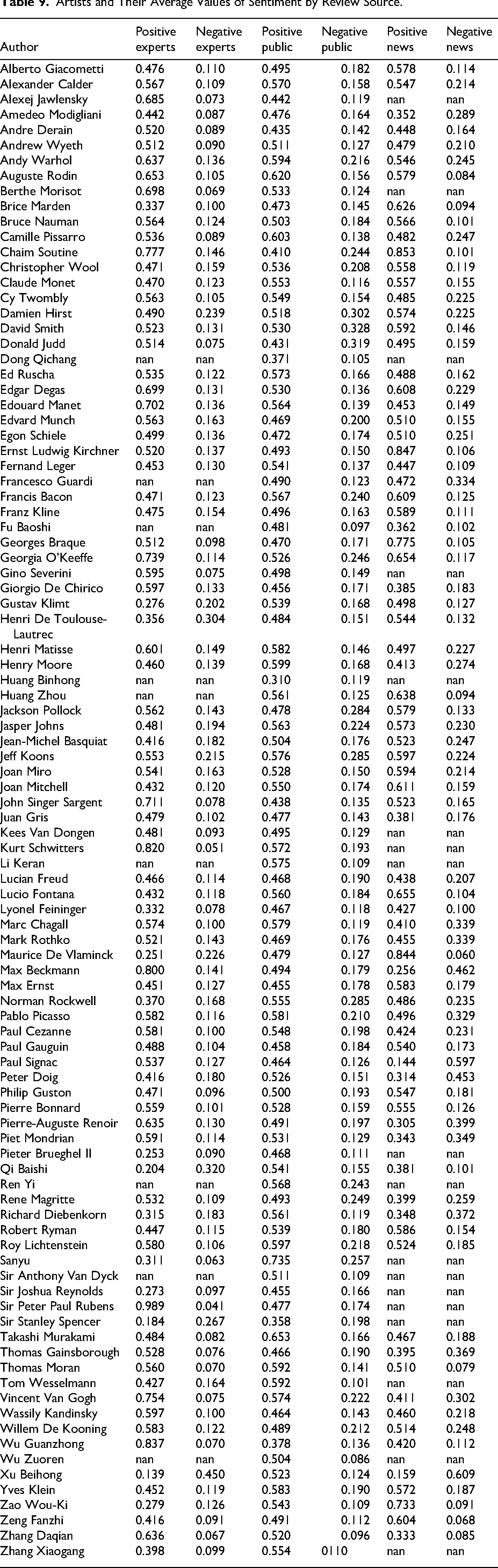

In addition to professional voices, we incorporated journalistic sentiment by assembling a corpus of 10,104 articles published in The New York Times (including the International New York Times and the International Herald Tribune) under the ‘Arts’ and ‘Fashion & Style’ sections. To ensure relevance, we retained only those articles in which the target artist’s name appeared at least twice—once in the headline or snippet and again in the lead paragraph—thus filtering out brief or tangential mentions. Because the headline and lead provide a concise summary of the article’s tone, we extracted sentiment exclusively from these segments. Table 9 lists every artist in our sample alongside their mean sentiment scores across all three review sources. Records lacking journalistic coverage or expert tweets in the 60-day pre-auction window were excluded from the corresponding regression models.

Method

To evaluate our first two hypotheses, we estimate a hedonic pricing model incorporating artist-specific fixed effects via ordinary least squares (OLS). This specification is standard in the literature and facilitates the identification of the marginal contribution of each characteristic to final auction prices (Cinefra et al., 2019; Stepanova, 2019). We employ artist rather than painting fixed effects because, even when a work appears more than once on the secondary market, its repeat-sale observations are often incomplete in our data.

For each source of sentiment

To guard against multicollinearity, we omit highly collinear attributes and employ variance-inflation checks during model selection.

In order to explore heterogeneity across market segments—since different buyer motivations and genre conventions may affect price formation (Prieto-Rodriguez & Vecco, 2021)—we further estimate moderation models. Specifically, we interact each sentiment measure with our binary indicator for investment intent (i.e. whether the painting was later resold), allowing the coefficient on sentiment to vary by buyer type. This approach parallels the cluster-based moderation analysis of Plotkina and Munzel (2016) and enables us to gauge how financial motives amplify or dampen sensitivity to online opinions.

Results

Experts and News Sentiment

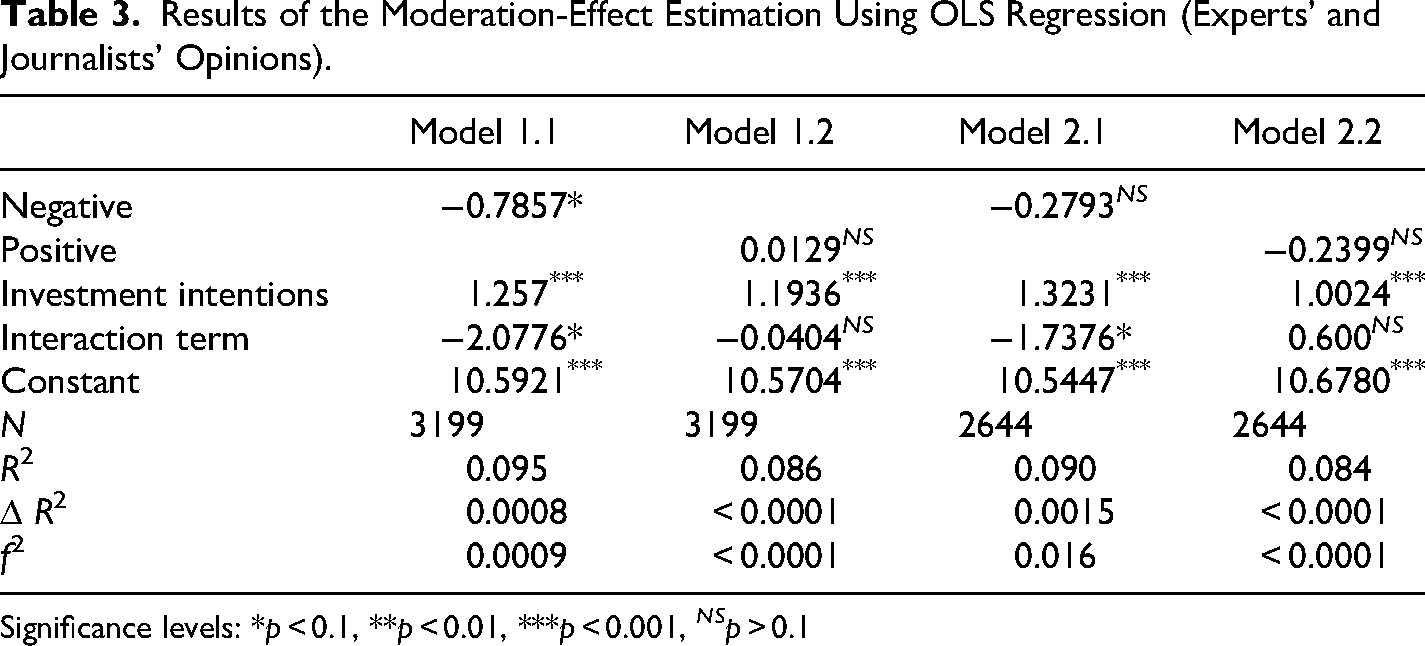

We begin by estimating two baseline hedonic regressions that include either the negative or the positive expert-sentiment measure. As shown in Table 3, negative expert sentiment is significantly associated with lower log-prices (

Results of the Moderation-Effect Estimation Using OLS Regression (Experts’ and Journalists’ Opinions).

Significance levels: *p < 0.1, **p < 0.01, ***p < 0.001, NS p > 0.1

Next, we augment each specification with an interaction term between expert sentiment and our investment-intent dummy. Models 1.1 and 1.2 in Table 3 report these estimates. In Model 1.1 (negative sentiment), the main effect remains negative and significant (

Finally, to capture the distinct role of journalistic coverage, we replace the expert sentiment variable with our news-sentiment measure. The corresponding hedonic model shows that both negative news sentiment (\,

Public Sentiment

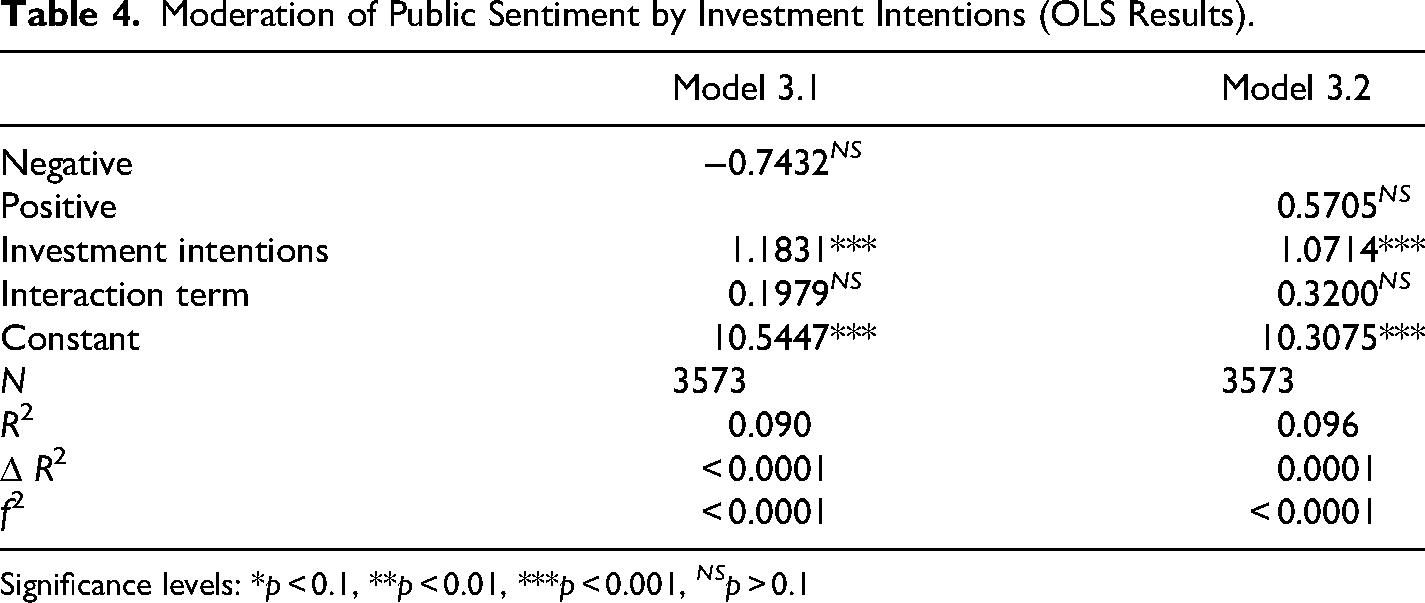

We next assess the contribution of broader public opinion to auction outcomes. As shown in Model 3.1, an increase in negative public sentiment is associated with a statistically significant reduction in prices (

To investigate whether investment motivations moderate this relationship, Models 3.1 and 3.2 incorporate interaction terms between the binary “investment intentions” indicator and public sentiment (negative and positive, respectively). As detailed in Table 4, neither the interaction coefficients nor the main sentiment term lose significance once this moderator is included (

Moderation of Public Sentiment by Investment Intentions (OLS Results).

Significance levels: *p < 0.1, **p < 0.01, ***p < 0.001, NS p > 0.1

Robustness of the Results

(a) Alternative Sentiment Measures

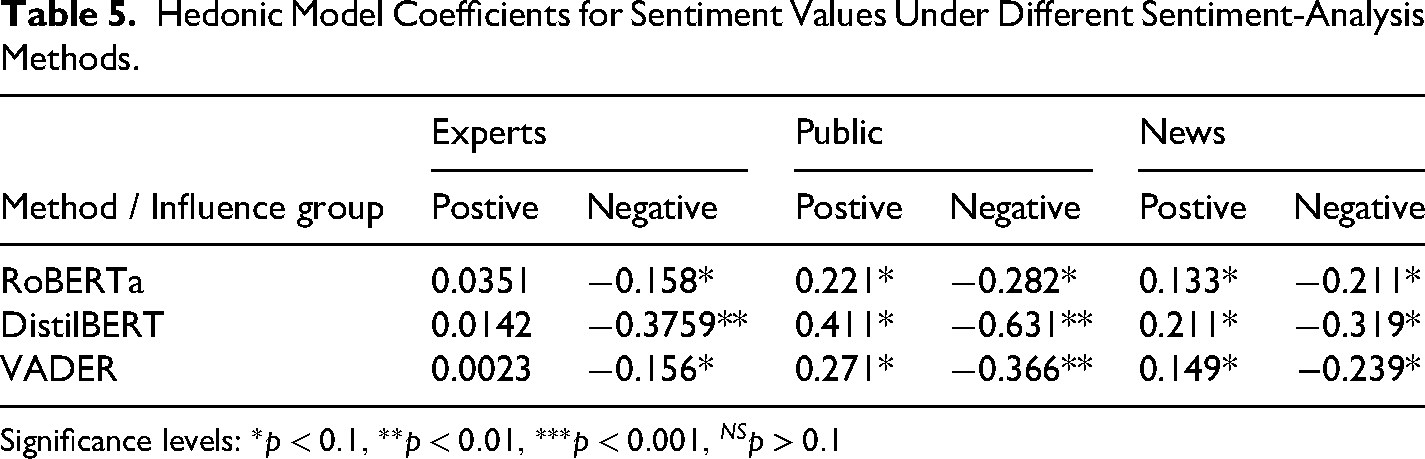

To assess the sensitivity of our findings to the choice of sentiment-analysis technique, we applied three distinct approaches, following (Agarwal et al., 2021). Our primary classifier, Twitter-RoBERTa, was pre-trained on 124 million tweets (January 2018–December 2021). As an alternative transformer, we used the DistilBERT-base multilingual cased model (Yuan, 2023), which—via a zero-shot DeBERTa pipeline—handles over 100 languages. Finally, we incorporated the lexicon-and-rule based VADER algorithm (Hutto & Gilbert, 2014), optimised for social-media text. Although each method entails its own assumptions and trade-offs, our objective is not to benchmark classifiers but to verify that the core econometric conclusions remain invariant. Table 5 reports the estimated sentiment-coefficients under each method. While t-statistics and levels of significance vary slightly, the overall pattern of effects is unchanged.

Hedonic Model Coefficients for Sentiment Values Under Different Sentiment-Analysis Methods.

Significance levels:

(b) Heterogeneity of Sentiments Impact by Art Historical Period

Although individual specialists often focus on particular periods (e.g., an Impressionist curator versus a Post–War gallerist), the social-media messages we analyse are public-facing micro-posts, not peer-reviewed monographs. These short statements are addressed to the broad art-market audience and are routinely retweeted across stylistic boundaries. In practice, museum directors, blue-chip dealers and senior critics comment on—and trade statistics for—multiple art historical periods, since major auction houses present Impressionist, Modern and Contemporary lots side-by-side and price movements in one sector quickly spill into the others.

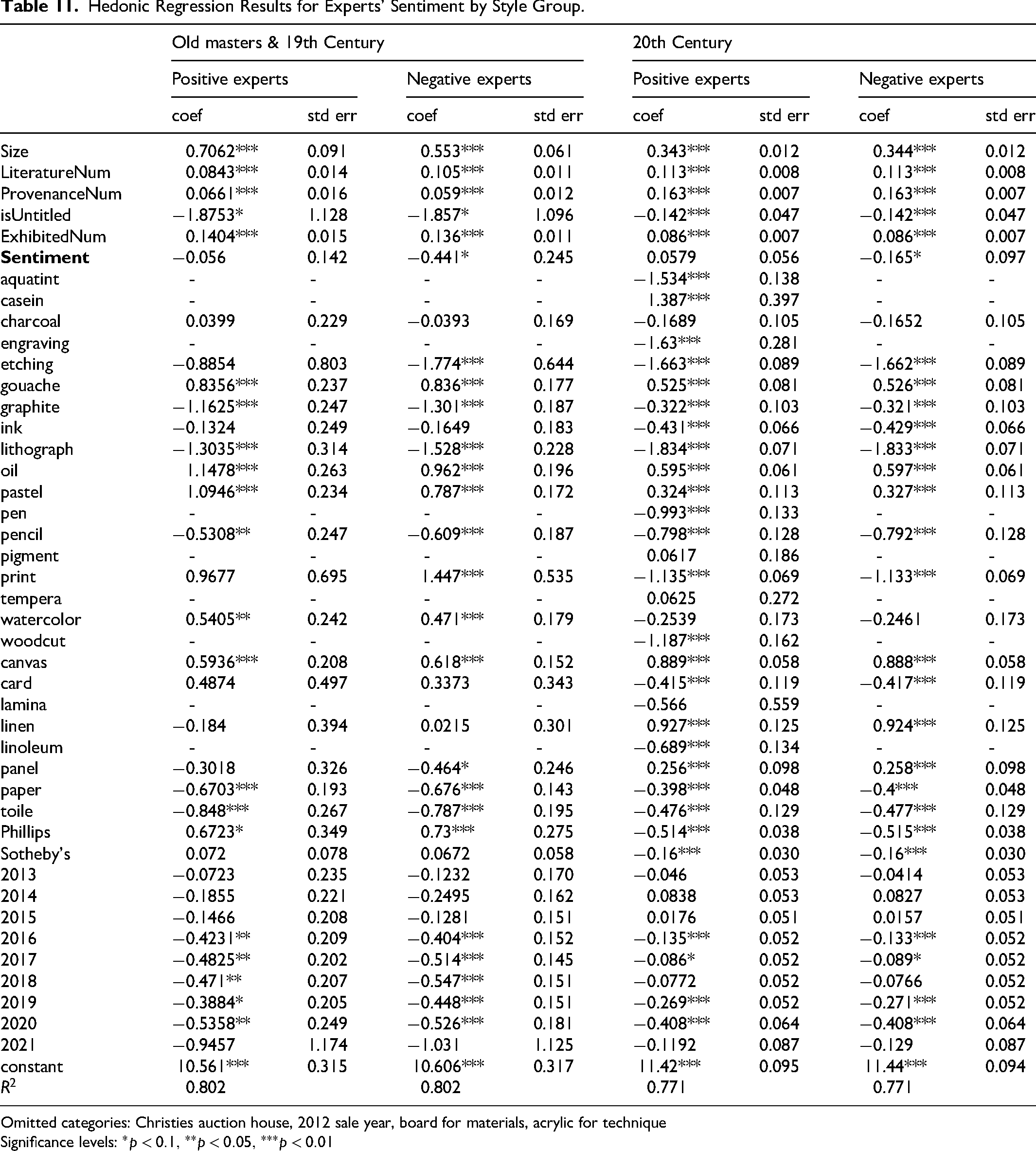

To confirm that art historical period-specific differences do not drive our results, we re-estimated the hedonic model after splitting the dataset into two style clusters:

Old Masters + 19th Century 20th Century: from Modern to Contemporary (merged to stabilize estimates, since their transaction dates overlap)

Table 6 reports the key coefficients and a formal Wald (Z) test of coefficient equality.

Test of Equality of Expert Sentiment Effects Across Art Historical Periods.

With p-values of

News articles and public tweets are, by construction, cross-period sources. A pilot split of paintings into the same two art historical period clusters alters the news- and public-sentiment coefficients by less than

Discussion

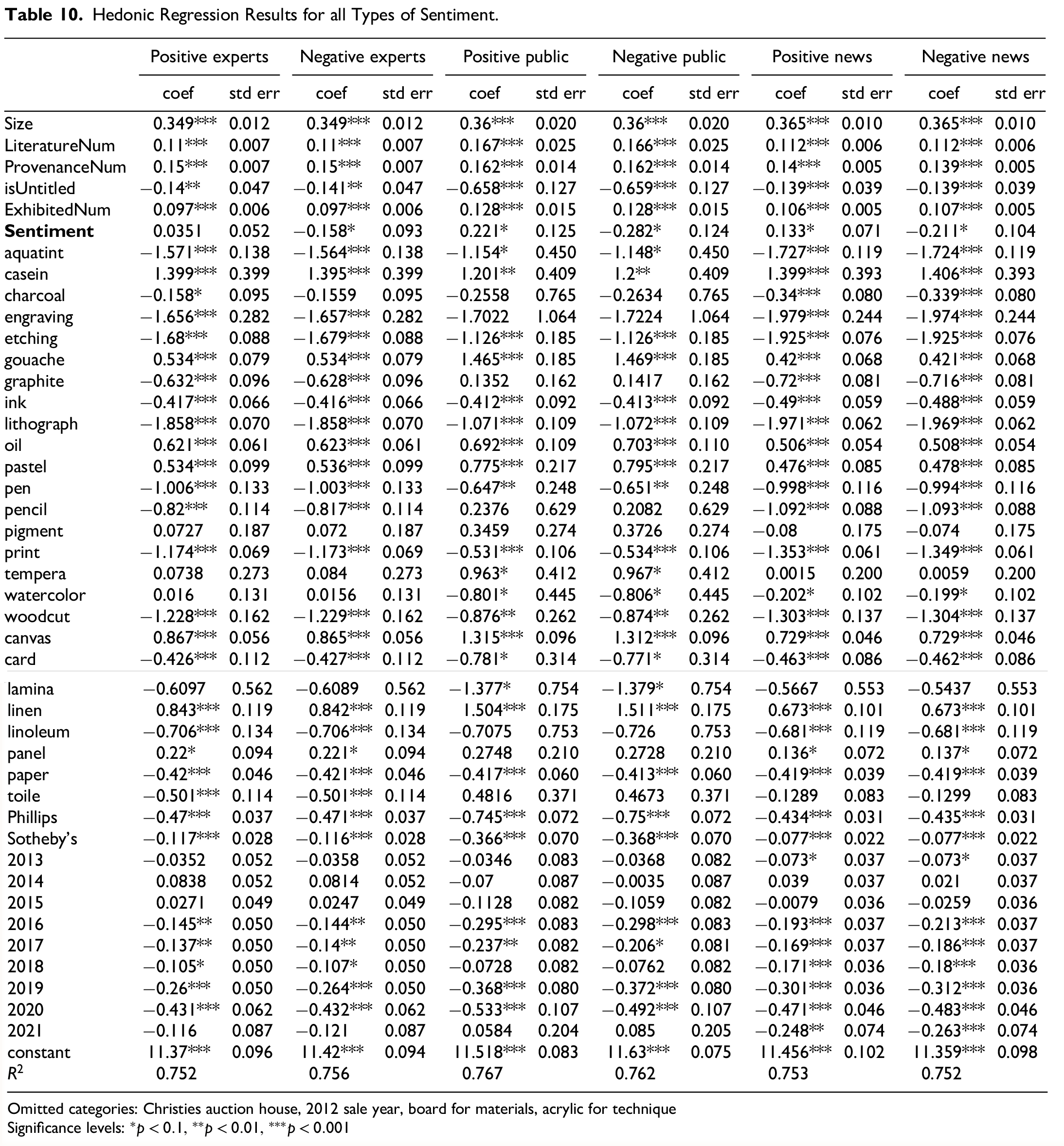

Our empirical findings largely corroborate significant research on hedonic price determinants in the art market. Consistent with Cinefra et al. (2019) and Zhukova et al. (2019), we observe a robust, positive relationship between the physical area of a painting and its realized price, as well as a significant premium associated with prior mentions in the literature. While the geographic location of the auction house (city dummies) does not always attain individual significance, the joint effect of auction–house indicators remains highly significant across all specifications, echoing the conclusions of Stepanova (2019). Likewise, the influence of various material and technique attributes on price is reaffirmed (see Table 10). The consistency of the results obtained relative to the period of consideration is supported by separate regressions summarized in Table 11.

Turning to sentiment measures, negative evaluations—whether expressed by experts, journalists, or the broader public—consistently depress prices. In contrast, positive sentiment only reaches statistical significance when originating from the general public. This asymmetry mirrors well–documented behavioral biases in other domains, such as online marketplaces (Plotkina & Munzel, 2016) and hotel bookings (Sparks & Browning, 2011), where consumers disproportionately attend to negative information. Even verified experts’ positive tweets fail to command a measurable uplift in price, perhaps because positive commentary is so ubiquitous that it no longer provides incremental informational value. Conversely, negative expert and journalistic signals retain credibility and salience—an effect observed in travel–service contexts by Kusumasondjaja et al. (2012).

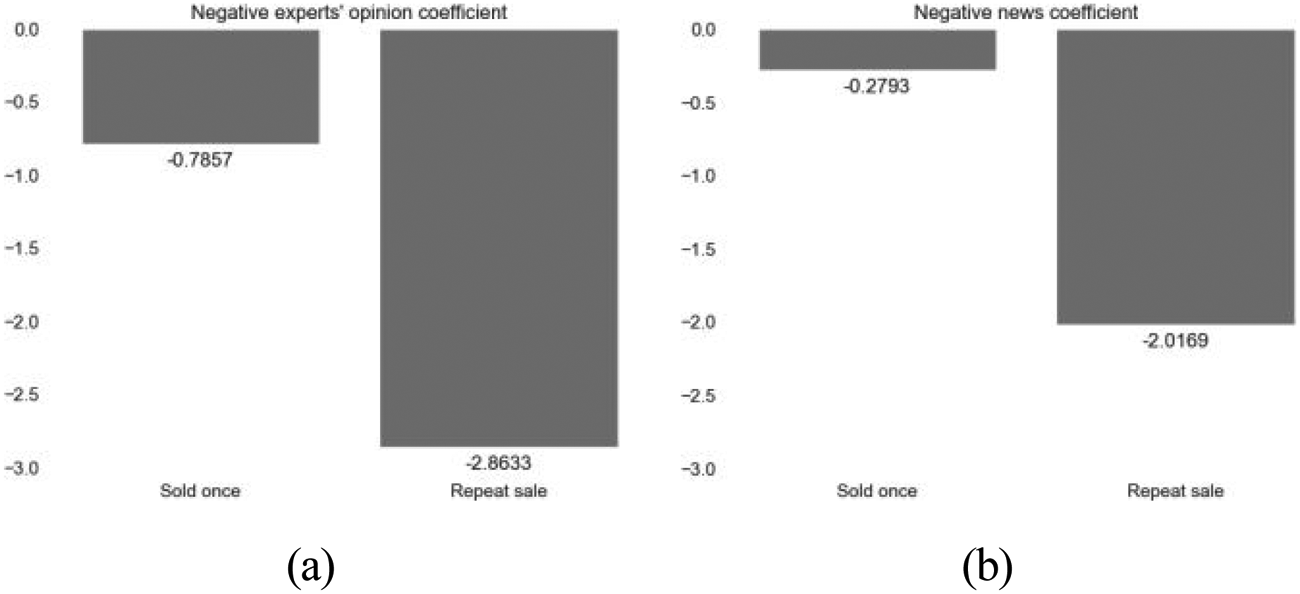

Figure 4 illustrates how negative expert and news sentiment interact with investment intentions. Paintings purchased with resale in mind exhibit a significantly larger price reaction to adverse expert and journalistic commentary. This heightened sensitivity aligns with the broader rise of impact investing (Deloitte, 2019), in which financial buyers demand that their acquisitions carry minimal reputational or provenance risk (Warne Monroe, 2018). In practice, an auction house may even refuse to sell works with dubious provenance, reflecting investors’ preference for assets whose cultural and legal standing are beyond reproach.

Marginal Effects of Negative Sentiment on Log Price: (a) Expert Tweets; (b) News Articles.

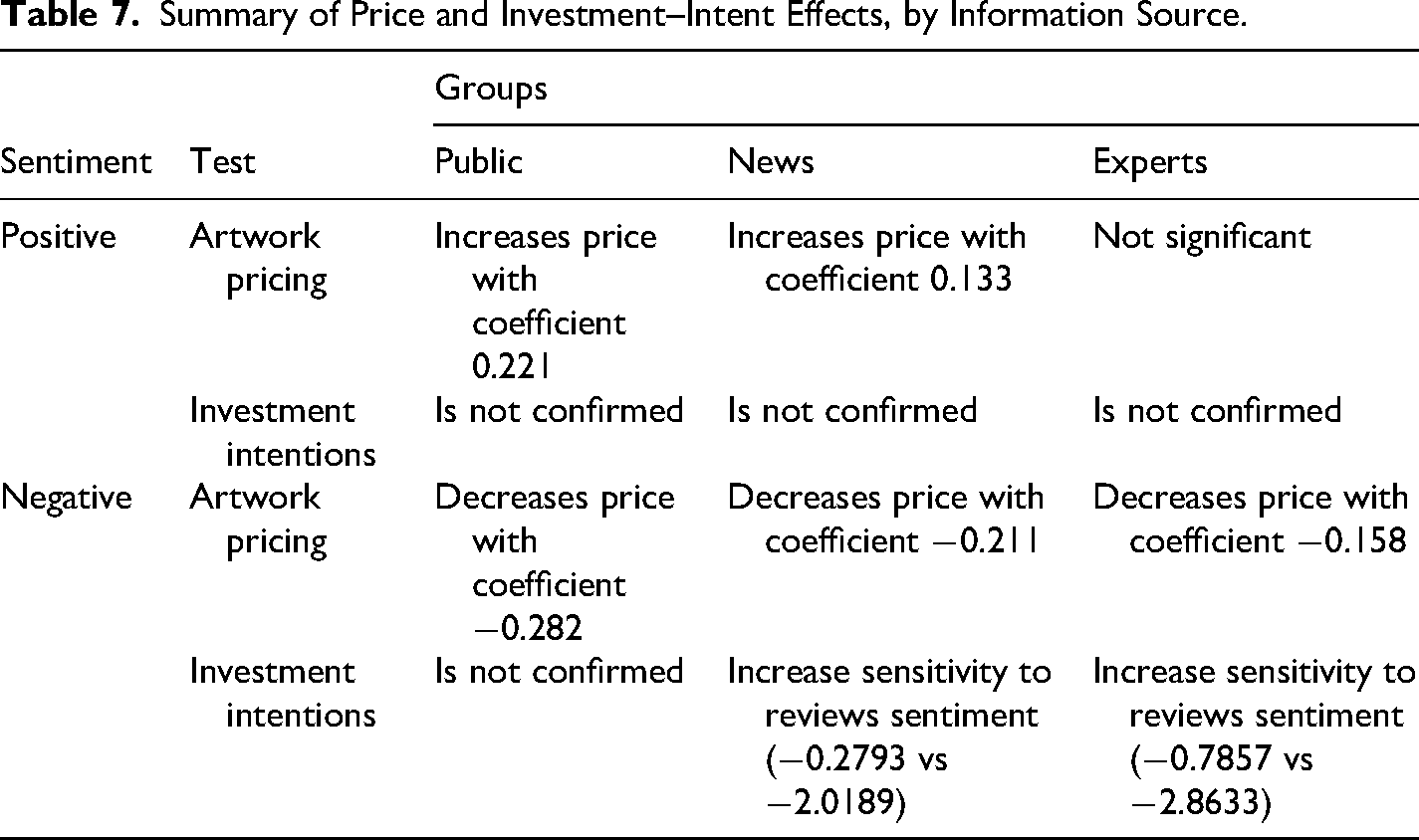

Table 7 ranks our findings by intervenor sophistication: public sentiment shows the clearest positive pricing effect, news sentiment occupies an intermediate position, and expert sentiment exerts the strongest negative influence—particularly when investments are at stake. This gradient underscores the layered nature of information transmission in the secondary art market, where the interplay between cultural valuation and economic valuation is mediated by agents of varying authority.

Summary of Price and Investment–Intent Effects, by Information Source.

In sum, our results validate the theoretical model: artist fame (and thus economic value) is shaped by a succession of social signals—from expert tweets to journalistic coverage to mass public commentary—that collectively determine prices. Moreover, the differential impact of negative sentiment and its amplification when financial stakes are high highlights the dual cultural and investment roles that artworks now occupy.

Conclusion

Our analysis demonstrates that the secondary art market is highly responsive to sentiment signals emanating from individuals with varying degrees of influence and expertise. The advent of social media platforms has dismantled traditional gatekeeping structures, enabling a broader array of art-world actors—from blue-chip collectors and museum directors to art journalists and casual enthusiasts—to broadcast their judgments in real time. This accelerated flow of information allows prospective buyers to aggregate and interpret vast quantities of qualitative data prior to purchase, thereby reshaping the relationship between authors of cultural goods and their audiences.

We identify three distinct opinion sources: (1) market professionals (collectors, critics, exhibition directors) whose assessments carry the greatest technical authority; (2) art journalists and editors, who translate professional discourse for a mass readership; and (3) the general public, whose aggregated commentary reflects diffuse market sentiment. Empirically, social-media posts by the public track positively with auction prices, while negative reviews—whether from experts or from mainstream news outlets—exert a uniformly downward pressure. Moreover, for works purchased with resale in mind, negative professional and journalistic signals are especially potent, underscoring the heightened risk-aversion of investment-oriented buyers.

Future work should widen the scope of opinion sources—incorporating, for example, gallery newsletters, podcast transcripts, and international press—and refine proxies for investment intent (e.g., linking buyer identities or resale horizons). Such extensions will further illuminate how layered information environments shape asset valuation in this uniquely opaque market.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Taisia Pimenova's research for this paper was supported by a grant from the Russian Science Foundation (Project No.24-28-01441).

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Appendix

Description of Expert Accounts and Their Sentiment Values. Artists and Their Average Values of Sentiment by Review Source. Hedonic Regression Results for all Types of Sentiment. Omitted categories: Christies auction house, 2012 sale year, board for materials, acrylic for technique Significance levels: Hedonic Regression Results for Experts’ Sentiment by Style Group. Omitted categories: Christies auction house, 2012 sale year, board for materials, acrylic for technique Significance levels:

Username

Tweets count

Followers

Positive sentiment

Negative sentiment

Retweets count

Mean

Std

Mean

Std

Mean

Std

MuseumModernArt

478

5280555

5.877

4.179

0.977

1.085

115.575

111.050

Tate

519

4715698

6.470

4.311

0.883

1.011

103.877

97.136

yokoono

3

4563452

5.542

3.200

2.356

3.246

129.000

110.689

metmuseum

603

4298648

6.300

4.390

0.738

0.890

99.017

90.567

Guggenheim

407

3396867

4.782

3.594

0.519

0.556

63.054

60.016

GettyMuseum

143

1323284

3.798

2.703

0.496

0.628

34.923

32.378

CentrePompidou

112

1082775

2.241

1.571

0.783

1.000

24.321

20.369

whitneymuseum

455

1045210

2.247

1.626

0.325

0.344

18.925

17.087

LACMA

331

1033500

3.246

2.094

0.366

0.325

25.834

20.930

ArtBasel

98

770370

1.535

0.888

0.303

0.187

17.480

13.607

brooklynmuseum

50

657332

1.834

1.325

0.327

0.571

10.380

9.718

jerrysaltz

337

548044

2.115

1.966

0.844

1.245

20.757

30.404

newmuseum

18

399990

1.006

0.604

0.169

0.162

5.333

7.491

aiww

10

390135

1.597

1.229

0.418

0.451

11.900

10.159

Gagosian

1036

389870

1.264

0.922

0.188

0.226

8.061

9.907

takashipom

74

330817

0.730

0.685

0.170

0.146

5.338

5.834

Artforum

96

307292

0.663

0.818

0.342

0.448

4.865

6.746

MoMAPS1

59

291430

1.142

0.926

0.364

0.559

5.695

6.109

JeffKoons

59

231000

1.804

1.372

0.318

0.307

12.610

11.455

theartmarket

320

205220

0.978

0.984

0.957

1.141

12.812

12.923

Stedelijk

89

203155

1.610

1.263

0.262

0.251

8.921

10.772

ArtObserved

2364

159495

0.863

0.804

0.220

0.267

5.752

7.544

artmarket

363

83654

0.346

0.428

0.180

0.314

2.028

2.766

davidzwirner

280

83334

0.810

0.692

0.107

0.090

3.521

3.887

ArtTactic

1138

74989

0.513

0.505

0.238

0.381

2.353

2.633

hirst_official

105

71580

1.024

1.047

0.187

0.269

8.295

10.631

hragv

92

63237

0.474

0.655

0.329

0.598

3.511

7.510

robertasmithnyt

32

53087

1.544

1.259

0.573

0.774

14.188

18.991

olafureliasson

5

52685

1.744

0.779

0.202

0.103

8.800

5.891

HUObrist

33

32080

0.400

0.527

0.201

0.464

1.576

2.264

cmonstah

10

31729

0.657

0.925

0.344

0.404

3.400

4.402

artstagesg

2

29715

0.621

0.878

0.034

0.047

1.000

1.414

RichardPrince4

9

23568

0.703

0.353

1.375

0.840

8.889

5.110

juliaxgulia

3

23198

0.176

0.202

0.629

0.867

1.667

1.528

SarahLDouglas

49

22944

0.234

0.401

0.125

0.235

0.898

1.489

rpogrebin

94

15580

0.279

0.512

0.099

0.192

1.436

3.732

Sirsargent

5

15210

0.780

0.973

0.965

1.183

13.800

16.873

nespector

24

13837

0.630

0.633

0.073

0.077

1.625

1.765

SearleAdrian

32

13778

1.069

1.346

0.698

0.788

6.406

7.882

annepasternak

18

13455

0.441

0.618

0.159

0.322

1.444

1.977

FabYab

8

11574

0.303

0.439

0.045

0.077

0.375

0.518

StuartComer

15

10048

0.651

0.661

0.114

0.091

4.467

5.617

mbalshaw

3

8631

0.740

1.282

0.037

0.064

1.667

2.887

LegacyRussell

5

7721

0.212

0.291

0.137

0.278

0.600

0.894

ceciliaalemani

29

6527

0.183

0.394

0.027

0.055

0.379

0.677

SadieColesHQ

13

6445

0.357

0.489

0.038

0.047

0.923

1.256

chusmartinez

3

4491

0.546

0.946

0.063

0.110

1.000

1.732

SophiaAlMaria

2

3594

1.001

0.031

0.129

0.011

4.000

0.000

MatthewMarks

124

2659

0.318

0.449

0.072

0.076

1.524

2.093

AmyCappellazzo

2

1723

0.644

0.021

0.004

0.111

0.000

0.000

CCB_Castello

2

1357

0.373

0.010

0.267

0.092

3.000

0.000

Tom_Trevor

1

895

0.000

-

0.000

-

0.000

-

arzion

1

476

0.313

-

0.285

-

1.000

-

Author

Positive experts

Negative experts

Positive public

Negative public

Positive news

Negative news

Alberto Giacometti

0.476

0.110

0.495

0.182

0.578

0.114

Alexander Calder

0.567

0.109

0.570

0.158

0.547

0.214

Alexej Jawlensky

0.685

0.073

0.442

0.119

nan

nan

Amedeo Modigliani

0.442

0.087

0.476

0.164

0.352

0.289

Andre Derain

0.520

0.089

0.435

0.142

0.448

0.164

Andrew Wyeth

0.512

0.090

0.511

0.127

0.479

0.210

Andy Warhol

0.637

0.136

0.594

0.216

0.546

0.245

Auguste Rodin

0.653

0.105

0.620

0.156

0.579

0.084

Berthe Morisot

0.698

0.069

0.533

0.124

nan

nan

Brice Marden

0.337

0.100

0.473

0.145

0.626

0.094

Bruce Nauman

0.564

0.124

0.503

0.184

0.566

0.101

Camille Pissarro

0.536

0.089

0.603

0.138

0.482

0.247

Chaim Soutine

0.777

0.146

0.410

0.244

0.853

0.101

Christopher Wool

0.471

0.159

0.536

0.208

0.558

0.119

Claude Monet

0.470

0.123

0.553

0.116

0.557

0.155

Cy Twombly

0.563

0.105

0.549

0.154

0.485

0.225

Damien Hirst

0.490

0.239

0.518

0.302

0.574

0.225

David Smith

0.523

0.131

0.530

0.328

0.592

0.146

Donald Judd

0.514

0.075

0.431

0.319

0.495

0.159

Dong Qichang

nan

nan

0.371

0.105

nan

nan

Ed Ruscha

0.535

0.122

0.573

0.166

0.488

0.162

Edgar Degas

0.699

0.131

0.530

0.136

0.608

0.229

Edouard Manet

0.702

0.136

0.564

0.139

0.453

0.149

Edvard Munch

0.563

0.163

0.469

0.200

0.510

0.155

Egon Schiele

0.499

0.136

0.472

0.174

0.510

0.251

Ernst Ludwig Kirchner

0.520

0.137

0.493

0.150

0.847

0.106

Fernand Leger

0.453

0.130

0.541

0.137

0.447

0.109

Francesco Guardi

nan

nan

0.490

0.123

0.472

0.334

Francis Bacon

0.471

0.123

0.567

0.240

0.609

0.125

Franz Kline

0.475

0.154

0.496

0.163

0.589

0.111

Fu Baoshi

nan

nan

0.481

0.097

0.362

0.102

Georges Braque

0.512

0.098

0.470

0.171

0.775

0.105

Georgia O’Keeffe

0.739

0.114

0.526

0.246

0.654

0.117

Gino Severini

0.595

0.075

0.498

0.149

nan

nan

Giorgio De Chirico

0.597

0.133

0.456

0.171

0.385

0.183

Gustav Klimt

0.276

0.202

0.539

0.168

0.498

0.127

Henri De Toulouse-Lautrec

0.356

0.304

0.484

0.151

0.544

0.132

Henri Matisse

0.601

0.149

0.582

0.146

0.497

0.227

Henry Moore

0.460

0.139

0.599

0.168

0.413

0.274

Huang Binhong

nan

nan

0.310

0.119

nan

nan

Huang Zhou

nan

nan

0.561

0.125

0.638

0.094

Jackson Pollock

0.562

0.143

0.478

0.284

0.579

0.133

Jasper Johns

0.481

0.194

0.563

0.224

0.573

0.230

Jean-Michel Basquiat

0.416

0.182

0.504

0.176

0.523

0.247

Jeff Koons

0.553

0.215

0.576

0.285

0.597

0.224

Joan Miro

0.541

0.163

0.528

0.150

0.594

0.214

Joan Mitchell

0.432

0.120

0.550

0.174

0.611

0.159

John Singer Sargent

0.711

0.078

0.438

0.135

0.523

0.165

Juan Gris

0.479

0.102

0.477

0.143

0.381

0.176

Kees Van Dongen

0.481

0.093

0.495

0.129

nan

nan

Kurt Schwitters

0.820

0.051

0.572

0.193

nan

nan

Li Keran

nan

nan

0.575

0.109

nan

nan

Lucian Freud

0.466

0.114

0.468

0.190

0.438

0.207

Lucio Fontana

0.432

0.118

0.560

0.184

0.655

0.104

Lyonel Feininger

0.332

0.078

0.467

0.118

0.427

0.100

Marc Chagall

0.574

0.100

0.579

0.119

0.410

0.339

Mark Rothko

0.521

0.143

0.469

0.176

0.455

0.339

Maurice De Vlaminck

0.251

0.226

0.479

0.127

0.844

0.060

Max Beckmann

0.800

0.141

0.494

0.179

0.256

0.462

Max Ernst

0.451

0.127

0.455

0.178

0.583

0.179

Norman Rockwell

0.370

0.168

0.555

0.285

0.486

0.235

Pablo Picasso

0.582

0.116

0.581

0.210

0.496

0.329

Paul Cezanne

0.581

0.100

0.548

0.198

0.424

0.231

Paul Gauguin

0.488

0.104

0.458

0.184

0.540

0.173

Paul Signac

0.537

0.127

0.464

0.126

0.144

0.597

Peter Doig

0.416

0.180

0.526

0.151

0.314

0.453

Philip Guston

0.471

0.096

0.500

0.193

0.547

0.181

Pierre Bonnard

0.559

0.101

0.528

0.159

0.555

0.126

Pierre-Auguste Renoir

0.635

0.130

0.491

0.197

0.305

0.399

Piet Mondrian

0.591

0.114

0.531

0.129

0.343

0.349

Pieter Brueghel II

0.253

0.090

0.468

0.111

nan

nan

Qi Baishi

0.204

0.320

0.541

0.155

0.381

0.101

Ren Yi

nan

nan

0.568

0.243

nan

nan

Rene Magritte

0.532

0.109

0.493

0.249

0.399

0.259

Richard Diebenkorn

0.315

0.183

0.561

0.119

0.348

0.372

Robert Ryman

0.447

0.115

0.539

0.180

0.586

0.154

Roy Lichtenstein

0.580

0.106

0.597

0.218

0.524

0.185

Sanyu

0.311

0.063

0.735

0.257

nan

nan

Sir Anthony Van Dyck

nan

nan

0.511

0.109

nan

nan

Sir Joshua Reynolds

0.273

0.097

0.455

0.166

nan

nan

Sir Peter Paul Rubens

0.989

0.041

0.477

0.174

nan

nan

Sir Stanley Spencer

0.184

0.267

0.358

0.198

nan

nan

Takashi Murakami

0.484

0.082

0.653

0.166

0.467

0.188

Thomas Gainsborough

0.528

0.076

0.466

0.190

0.395

0.369

Thomas Moran

0.560

0.070

0.592

0.141

0.510

0.079

Tom Wesselmann

0.427

0.164

0.592

0.101

nan

nan

Vincent Van Gogh

0.754

0.075

0.574

0.222

0.411

0.302

Wassily Kandinsky

0.597

0.100

0.464

0.143

0.460

0.218

Willem De Kooning

0.583

0.122

0.489

0.212

0.514

0.248

Wu Guanzhong

0.837

0.070

0.378

0.136

0.420

0.112

Wu Zuoren

nan

nan

0.504

0.086

nan

nan

Xu Beihong

0.139

0.450

0.523

0.124

0.159

0.609

Yves Klein

0.452

0.119

0.583

0.190

0.572

0.187

Zao Wou-Ki

0.279

0.126

0.543

0.109

0.733

0.091

Zeng Fanzhi

0.416

0.091

0.491

0.112

0.604

0.068

Zhang Daqian

0.636

0.067

0.520

0.096

0.333

0.085

Zhang Xiaogang

0.398

0.099

0.554

0110

nan

nan

Positive experts

Negative experts

Positive public

Negative public

Positive news

Negative news

coef

std err

coef

std err

coef

std err

coef

std err

coef

std err

coef

std err

Size

0.349***

0.012

0.349***

0.012

0.36***

0.020

0.36***

0.020

0.365***

0.010

0.365***

0.010

LiteratureNum

0.11***

0.007

0.11***

0.007

0.167***

0.025

0.166***

0.025

0.112***

0.006

0.112***

0.006

ProvenanceNum

0.15***

0.007

0.15***

0.007

0.162***

0.014

0.162***

0.014

0.14***

0.005

0.139***

0.005

isUntitled

0.14**

0.047

0.141**

0.047

0.658***

0.127

0.659***

0.127

0.139***

0.039

0.139***

0.039

ExhibitedNum

0.097***

0.006

0.097***

0.006

0.128***

0.015

0.128***

0.015

0.106***

0.005

0.107***

0.005

0.0351

0.052

0.158*

0.093

0.221*

0.125

0.282*

0.124

0.133*

0.071

0.211*

0.104

aquatint

1.571***

0.138

1.564***

0.138

1.154*

0.450

1.148*

0.450

1.727***

0.119

1.724***

0.119

casein

1.399***

0.399

1.395***

0.399

1.201**

0.409

1.2**

0.409

1.399***

0.393

1.406***

0.393

charcoal

0.158*

0.095

0.1559

0.095

0.2558

0.765

0.2634

0.765

0.34***

0.080

0.339***

0.080

engraving

1.656***

0.282

1.657***

0.282

1.7022

1.064

1.7224

1.064

1.979***

0.244

1.974***

0.244

etching

1.68***

0.088

1.679***

0.088

1.126***

0.185

1.126***

0.185

1.925***

0.076

1.925***

0.076

gouache

0.534***

0.079

0.534***

0.079

1.465***

0.185

1.469***

0.185

0.42***

0.068

0.421***

0.068

graphite

0.632***

0.096

0.628***

0.096

0.1352

0.162

0.1417

0.162

0.72***

0.081

0.716***

0.081

ink

0.417***

0.066

0.416***

0.066

0.412***

0.092

0.413***

0.092

0.49***

0.059

0.488***

0.059

lithograph

1.858***

0.070

1.858***

0.070

1.071***

0.109

1.072***

0.109

1.971***

0.062

1.969***

0.062

oil

0.621***

0.061

0.623***

0.061

0.692***

0.109

0.703***

0.110

0.506***

0.054

0.508***

0.054

pastel

0.534***

0.099

0.536***

0.099

0.775***

0.217

0.795***

0.217

0.476***

0.085

0.478***

0.085

pen

1.006***

0.133

1.003***

0.133

0.647**

0.248

0.651**

0.248

0.998***

0.116

0.994***

0.116

pencil

0.82***

0.114

0.817***

0.114

0.2376

0.629

0.2082

0.629

1.092***

0.088

1.093***

0.088

pigment

0.0727

0.187

0.072

0.187

0.3459

0.274

0.3726

0.274

0.08

0.175

0.074

0.175

print

1.174***

0.069

1.173***

0.069

0.531***

0.106

0.534***

0.106

1.353***

0.061

1.349***

0.061

tempera

0.0738

0.273

0.084

0.273

0.963*

0.412

0.967*

0.412

0.0015

0.200

0.0059

0.200

watercolor

0.016

0.131

0.0156

0.131

0.801*

0.445

0.806*

0.445

0.202*

0.102

0.199*

0.102

woodcut

1.228***

0.162

1.229***

0.162

0.876**

0.262

0.874**

0.262

1.303***

0.137

1.304***

0.137

canvas

0.867***

0.056

0.865***

0.056

1.315***

0.096

1.312***

0.096

0.729***

0.046

0.729***

0.046

card

0.426***

0.112

0.427***

0.112

0.781*

0.314

0.771*

0.314

0.463***

0.086

0.462***

0.086

lamina

0.6097

0.562

0.6089

0.562

1.377*

0.754

1.379*

0.754

0.5667

0.553

0.5437

0.553

linen

0.843***

0.119

0.842***

0.119

1.504***

0.175

1.511***

0.175

0.673***

0.101

0.673***

0.101

linoleum

0.706***

0.134

0.706***

0.134

0.7075

0.753

0.726

0.753

0.681***

0.119

0.681***

0.119

panel

0.22*

0.094

0.221*

0.094

0.2748

0.210

0.2728

0.210

0.136*

0.072

0.137*

0.072

paper

0.42***

0.046

0.421***

0.046

0.417***

0.060

0.413***

0.060

0.419***

0.039

0.419***

0.039

toile

0.501***

0.114

0.501***

0.114

0.4816

0.371

0.4673

0.371

0.1289

0.083

0.1299

0.083

Phillips

0.47***

0.037

0.471***

0.037

0.745***

0.072

0.75***

0.072

0.434***

0.031

0.435***

0.031

Sotheby’s

0.117***

0.028

0.116***

0.028

0.366***

0.070

0.368***

0.070

0.077***

0.022

0.077***

0.022

2013

0.0352

0.052

0.0358

0.052

0.0346

0.083

0.0368

0.082

0.073*

0.037

0.073*

0.037

2014

0.0838

0.052

0.0814

0.052

0.07

0.087

0.0035

0.087

0.039

0.037

0.021

0.037

2015

0.0271

0.049

0.0247

0.049

0.1128

0.082

0.1059

0.082

0.0079

0.036

0.0259

0.036

2016

0.145**

0.050

0.144**

0.050

0.295***

0.083

0.298***

0.083

0.193***

0.037

0.213***

0.037

2017

0.137**

0.050

0.14**

0.050

0.237**

0.082

0.206*

0.081

0.169***

0.037

0.186***

0.037

2018

0.105*

0.050

0.107*

0.050

0.0728

0.082

0.0762

0.082

0.171***

0.036

0.18***

0.036

2019

0.26***

0.050

0.264***

0.050

0.368***

0.080

0.372***

0.080

0.301***

0.036

0.312***

0.036

2020

0.431***

0.062

0.432***

0.062

0.533***

0.107

0.492***

0.107

0.471***

0.046

0.483***

0.046

2021

0.116

0.087

0.121

0.087

0.0584

0.204

0.085

0.205

0.248**

0.074

0.263***

0.074

constant

11.37***

0.096

11.42***

0.094

11.518***

0.083

11.63***

0.075

11.456***

0.102

11.359***

0.098

0.752

0.756

0.767

0.762

0.753

0.752

Old masters & 19th Century

20th Century

Positive experts

Negative experts

Positive experts

Negative experts

coef

std err

coef

std err

coef

std err

coef

std err

Size

0.7062***

0.091

0.553***

0.061

0.343***

0.012

0.344***

0.012

LiteratureNum

0.0843***

0.014

0.105***

0.011

0.113***

0.008

0.113***

0.008

ProvenanceNum

0.0661***

0.016

0.059***

0.012

0.163***

0.007

0.163***

0.007

isUntitled

1.128

1.096

0.047

0.047

ExhibitedNum

0.1404***

0.015

0.136***

0.011

0.086***

0.007

0.086***

0.007

0.142

0.245

0.0579

0.056

0.097

aquatint

-

-

-

-

0.138

-

-

casein

-

-

-

-

1.387***

0.397

-

-

charcoal

0.0399

0.229

0.169

0.105

0.105

engraving

-

-

-

-

0.281

-

-

etching

0.803

0.644

0.089

0.089

gouache

0.8356***

0.237

0.836***

0.177

0.525***

0.081

0.526***

0.081

graphite

0.247

0.187

0.103

0.103

ink

0.249

0.183

0.066

0.066

lithograph

0.314

0.228

0.071

0.071

oil

1.1478***

0.263

0.962***

0.196

0.595***

0.061

0.597***

0.061

pastel

1.0946***

0.234

0.787***

0.172

0.324***

0.113

0.327***

0.113

pen

-

-

-

-

0.133

-

-

pencil

0.247

0.187

0.128

0.128

pigment

-

-

-

-

0.0617

0.186

-

-

print

0.9677

0.695

1.447***

0.535

0.069

0.069

tempera

-

-

-

-

0.0625

0.272

-

-

watercolor

0.5405**

0.242

0.471***

0.179

0.173

0.173

woodcut

-

-

-

-

0.162

-

-

canvas

0.5936***

0.208

0.618***

0.152

0.889***

0.058

0.888***

0.058

card

0.4874

0.497

0.3373

0.343

0.119

0.119

lamina

-

-

-

-

0.559

-

-

linen

0.394

0.0215

0.301

0.927***

0.125

0.924***

0.125

linoleum

-

-

-

-

0.134

-

-

panel

0.326

0.246

0.256***

0.098

0.258***

0.098

paper

0.193

0.143

0.048

0.048

toile

0.267

0.195

0.129

0.129

Phillips

0.6723*

0.349

0.73***

0.275

0.038

0.038

Sotheby’s

0.072

0.078

0.0672

0.058

0.030

0.030

2013

0.235

0.170

0.053

0.053

2014

0.221

0.162

0.0838

0.053

0.0827

0.053

2015

0.208

0.151

0.0176

0.051

0.0157

0.051

2016

0.209

0.152

0.052

0.052

2017

0.202

0.145

0.052

0.052

2018

0.207

0.151

0.052

0.052

2019

0.205

0.151

0.052

0.052

2020

0.249

0.181

0.064

0.064

2021

1.174

1.125

0.087

0.087

constant

10.561***

0.315

10.606***

0.317

11.42***

0.095

11.44***

0.094

0.802

0.802

0.771

0.771