Abstract

Introduction

In the digital era, digital transformation plays a significant role in enhancing corporate governance and has a comprehensive impact on firm performance (Brockhaus et al., 2023; Ribeiro-Navarrete et al., 2021). It has reshaped the relationship between firms and their stakeholders (Bharadwaj et al., 2013; Chierici et al., 2020), with this transformation accelerated by the COVID-19 pandemic (Priyono et al., 2020). Digital transformation relies on the application of digital technologies such as artificial intelligence (AI), big data, cloud computing, and blockchain (Manita et al., 2020). These technologies facilitate the identification, collection, storage, transmission, and processing of information. Digitalization of firms reduces information asymmetry and significantly contributes to corporate governance mechanisms (Brockhaus et al., 2023; Manita et al., 2020; Ribeiro-Navarrete et al., 2021), offering effective solutions to address agency problems. As corporate social responsibility (CSR) garners widespread public attention, the implications of digitization for CSR practices have recently attracted scholars’ interest. However, the literature presents mixed arguments on this issue. On the one hand, Govindan (2024) suggests that the integration of digitalization into CSR practices enhances firms’ engagement in CSR initiatives, while digital technologies improve firms’ capability to achieve CSR goals (Cardinali and De Giovanni, 2022). On the other hand, the process of digital transformation introduces new challenges for firms and negatively impacts CSR practices (Gwebu et al., 2018). Additionally, firms may be discouraged from disclosing CSR information due to increased monitoring (Jin and Mirza, 2023).

Because CSR reports are linked to firms’ favorability and legitimacy among various stakeholders (Du and Yu, 2021; Hawn and Ioannou, 2016), their credibility often comes under scrutiny. This is due to managers’ tendency to opportunistically overstate and manipulate these reports, leveraging their information advantage and self-serving motives, even when their actual behaviors may not align with stakeholders’ expectations (García-Sánchez et al., 2021). Furthermore, the non-mandatory nature of CSR reporting provides firms with greater discretion in information disclosure, resulting in a gap between CSR communication and actual performance, known as CSR decoupling (Carlos and Lewis, 2018; Tashman et al., 2019). Top executives sometimes employ CSR decoupling to mislead stakeholders (Shahab et al., 2021; Velte, 2023), though it can be risky and detrimental to firms (Marquis and Qian, 2014; Sauerwald and Su, 2019). A firm’s CSR strategy is closely linked to corporate governance mechanisms, including stakeholder supervision and the internal control system. Previous research has also explored the antecedents of CSR decoupling from a corporate governance perspective, including the establishment of governance committees (Gull et al., 2023), CEO power (Shahab et al., 2021), and various attributes of the board of directors (Ali Gull et al., 2022). CSR decoupling is often viewed as a type of agency problem stemming from information asymmetry between principals and agents.

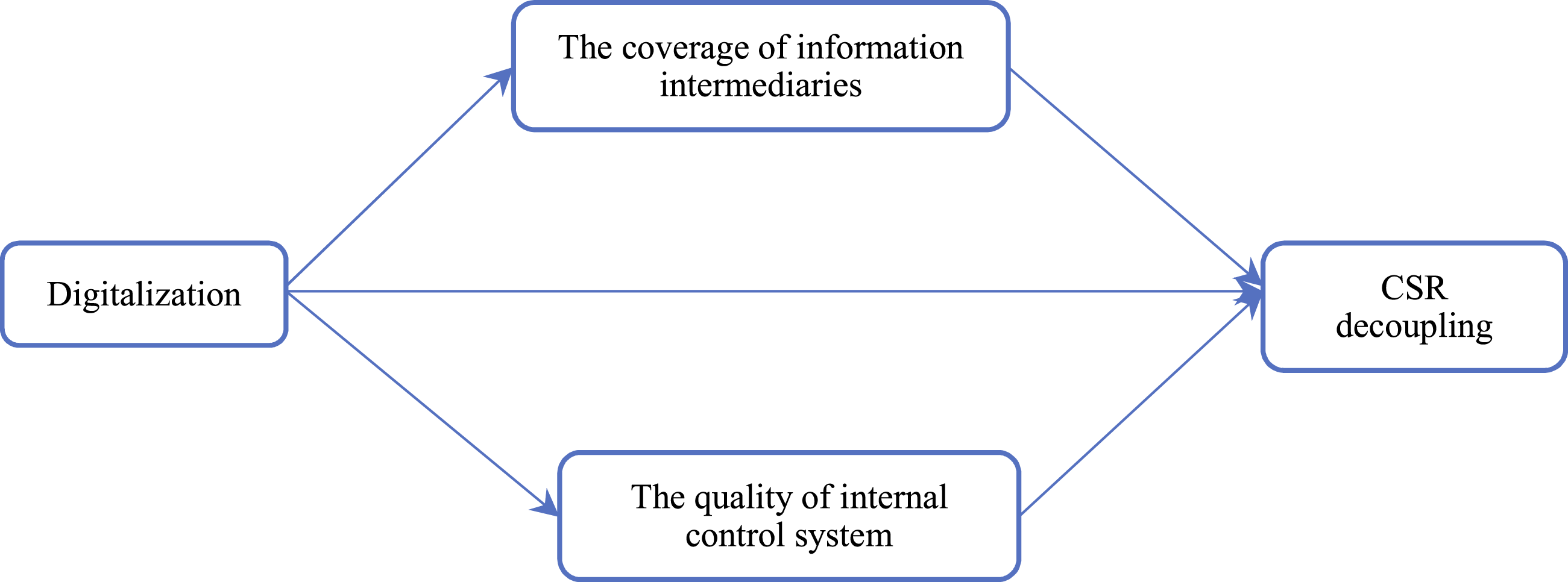

In this study, we investigate the effect of digitalization on CSR decoupling. Building upon prior research that suggests CSR decoupling is linked with corporate governance deficiencies (Gull et al., 2023), we explore how firm digitalization shapes the governance mechanisms, including the quality of the internal control system and the coverage of external information intermediaries, which in turn alleviates CSR decoupling. Information intermediaries, such as the media and analysts, closely monitor firms externally by disseminating information and assessments of firms’ behaviors and strategies. Their coverage garners widespread attention from the public and stakeholders, leading to negative reactions towards firms with malpractices and constraining managerial opportunism (Huang et al., 2021). And, the internal control system is designed to manage operational risk and ensure the reliability of information disclosure, a factor found to be related to firms’ engagement in CSR (Huang et al., 2022). Digital processing techniques, characterized by automated information collection, storage, and processing, enhance internal governance (Kache and Seuring, 2017; Keller et al., 2021).

Focused on whether and how digital transformation reduces CSR decoupling, this study aims to examine whether this relationship is mediated by the coverage of external information intermediaries and improved internal control quality, and extends the understanding of digital transformation by positioning it as a governance-enhancing mechanism that narrows the gap between CSR communication and actual performance. This study utilizes a sample of Chinese listed companies in the manufacturing sector from the Shanghai and Shenzhen stock-A markets spanning from 2015 to 2020. Empirical findings demonstrate a negative relationship between digitalization and CSR decoupling. And digital transformation is also found to be positively related to the coverage of information intermediaries and the quality of internal control systems, both of which effectively curb firms’ CSR decoupling behaviors. And they are verified as mediators in the relationship between digital transformation and CSR decoupling.

This study contributes to the literature on CSR decoupling and corporate governance. Prior research has emphasized that governance structures (Filatotchev and Nakajima, 2010), monitoring mechanisms (Zhang, 2021), and the information environment (Bentley-Goode et al., 2019) play key roles in shaping managerial behavior and strategic outcomes. In this context, digital transformation is not viewed simply as a technological upgrade but as a structural shift in how firms process information and constrain managerial discretion (Jiang, 2025). By examining the governance implications of digital transformation, this research extends the general management literature on digital strategy, particularly in relation to narrowing the “say–do” gap. It also offers practical implications for firms seeking to strengthen organizational governance through digitalization.

Literature review

Firms today must address the diverse needs of various stakeholders by engaging in Corporate Social Responsibility (CSR) initiatives alongside their pursuit of economic interests. However, a persistent challenge arises from the information asymmetry between firms and stakeholders, leading executives to sometimes overstate CSR performance in their communications with external stakeholders (Jain, 2017).

In the realm of CSR studies, “decoupling” refers to a strategic approach employed by firms to exaggerate their social responsibility in disclosure efforts, primarily aimed at enhancing their legitimacy. It is well-documented that CSR decoupling can have adverse effects on both firm performance (Knight, 2020) and legitimacy (Tashman et al., 2019). Scholars have extensively explored the antecedents of CSR decoupling, examining both internal and external factors. Overconfident (Sauerwald and Su, 2019) and powerful (Shahab et al., 2021) CEOs have been found to be associated with CSR decoupling. Conversely, CSR committees, board size, board independence, gender diversity, and board members’ tenure are negatively correlated with CSR decoupling (Ali Gull et al., 2022; Gull et al., 2023). Additionally, from a market supervision perspective, analyst coverage has been shown to mitigate CSR decoupling (Zhang, 2021). Emerging market multinational enterprises (EM-MNEs) tend to engage in CSR decoupling due to home country institutional voids and the degree of internationalization (Tashman et al., 2019). Recent research also emphasizes the role of stakeholder oversight and governmental structures. Public attention can reduce the gap between CSR disclosure and actual practices by increasing reputational pressure (He and Gan, 2025). Other external monitors, such as common institutional investors and high-quality auditors, also help curb CSR decoupling by improving disclosure credibility (Ding et al., 2025; Saeed et al., 2026). At the institutional level, greater administrative hierarchical distance may increase firms’ tendency to engage in CSR decoupling (Wang et al., 2025a). Recent evidence further underscores the important role of governance mechanisms in shaping CSR outcomes. For instance, board size exhibits a non-linear relationship with CSR performance (Ghosh et al., 2022), and CSR sustainability committees significantly enhance ESG performance (Ghosh and Sahu, 2026). Governance mechanisms have also been shown to moderate the CSR–firm performance relationship (Mondal and Sahu, 2025). Together, these findings reinforce the view that governance structures are central to understanding CSR-related behaviors.

Digital transformation is defined in this study as a comprehensive strategic renewal rather than the adoption of a single technology (Aránega et al., 2023; Song et al., 2025). It involves utilizing digital technologies to optimize business processes, strategies, capabilities, products, services, and repositioning within business networks (Bharadwaj et al., 2013; Manita et al., 2020). Prior research suggests that digital transformation not only enhances organizational efficiency but also triggers substantial changes in organizational strategies and structures (Hanelt et al., 2020; Vial, 2019; Ye et al., 2025). For instance, the growing integration of digital assets into financial markets underscores the broader strategic implications of digitalization (Jana and Sahu, 2025). As organizational elements and processes become digitalized, operational efficiency is affected, and the firm’s information environment and governance structure may also be reshaped (Sun et al., 2024). This transformation significantly enhances organizational transparency, influencing strategic outcomes (Brockhaus et al., 2023; Ribeiro-Navarrete et al., 2021) and reshaping the relationship between firms and their stakeholders (Bharadwaj et al., 2013; Chierici et al., 2020), and it is found to be positively related to innovation and sustainable performance (Lu et al., 2023). Importantly, digital transformation mitigates information asymmetry and strengthens corporate governance mechanisms (Brockhaus et al., 2023; Manita et al., 2020; Ribeiro-Navarrete et al., 2021). Since corporate governance aims to align the interests of owners, managers, and stakeholders (Jensen and Meckling, 1976) and reduce conflicts of interest (Jacoby et al., 2019), digital technologies provide new opportunities to address agency problems (Filatotchev and Nakajima, 2010; Safieddine, 2009; Sama et al., 2022). Therefore, digital transformation acts as a governance-enhancing resource that provides a robust theoretical basis for aligning internal operations with external CSR expectations.

In the corporate governance literature, both internal and external governance mechanisms have been emphasized (Filatotchev and Nakajima, 2010), with agency theory frequently employed to analyze corporate governance problems (Safieddine, 2009). At the core of the agency problem is information asymmetry between executives and shareholders, leading to the design and implementation of various corporate governance mechanisms to alleviate this issue. These mechanisms encompass information disclosure guidelines (García-Sánchez et al., 2022), the internal control system (Boulhaga et al., 2023), and external monitoring and supervision (Zhang, 2021). Numerous studies have examined how external information intermediaries (Bentley-Goode et al., 2019) and internal control systems (Hoitash et al., 2009) contribute to reducing agency problems and enhancing organizational efficiency. Reliable information disclosure helps bridge information gaps between managers and shareholders, thereby reducing agency costs within organizations.

In addition to mandated information disclosure, investors seek information about firm performance from various sources. Media and financial analysts play pivotal roles as major information intermediaries in the market (Bentley-Goode et al., 2019). Media coverage significantly influences public opinion about firms and their attitudes towards various stakeholders (Luo et al., 2019). Financial analysts not only disseminate information in the capital market but also conduct in-depth assessments of various activities of firms through interpreting and monitoring publicly disclosed information by listed companies (Hu et al., 2021). The judgments and recommendations of financial analysts are highly valued by investors for their objectivity, professionalism, and prudence (Zhang, 2021).

The Committee of Sponsoring Organizations of the Treadway Commission (COSO) issued the Internal Control - Integrated Framework in 1992, outlining the triple purposes of internal control (IC): enhancing business performance, financial reporting, and compliance with regulations. A well-functioning IC system not only improves trustworthy financial reporting but also leads to greater operational efficiency. Prior studies have linked deficiencies in the IC system to self-serving behaviors of managers and financial reporting restatements (Bentley-Goode et al., 2017; Järvinen and Myllymäki, 2016). A robust IC system significantly reduces agency costs (Hoitash et al., 2009). Research has explored various corporate governance attributes, including board structure, role performance, and financial expertise, which critically affect the quality of internal control (Nalukenge et al., 2017). An effective internal audit is essential for internal control (Spira and Page, 2003). Recent studies have recognized information technology as a component of internal controls (Kaawaase et al., 2021), with empirical evidence showing that a firm’s IT capability enhances the effectiveness of both internal control and external audit (Chen et al., 2014).

The COSO framework, a leader in ensuring the effectiveness of internal control, identifies five components: control environment, risk assessment, control activities, information and communication, and monitoring (Brown et al., 2014). The use of IT can impact any of these components related to the achievement of financial reporting, operational, or compliance objectives for an entity (AICPA, 2006). Reliable information disclosure relies on effective IT-based internal control systems, as a well-established IC system increases the reliability of financial reporting and the sense of responsibility among information providers (Stoel and Muhanna, 2011). Studies have also highlighted the significance of internal control quality in relation to social responsibility, with implications such as moderating the relationship between environmental, social, and governance (ESG) ratings and corporate performance (Boulhaga et al., 2023) and integrating ESG concerns into business operations (Harasheh and Provasi, 2023).

Hypothesis development

Digital transformation and CSR decoupling

CSR communication is often decoupled from CSR performance (Zhang, 2021) as firms tend to overstate their CSR achievements to enhance their reputation and gain legitimacy among stakeholders. For instance, greenwashing involves firms exaggerating their environmental performance (de Freitas Netto et al., 2020). However, these practices can harm firms, particularly when they come under intense scrutiny (Berrone et al., 2017). The root of this decoupling between actions and words lies in the information asymmetry between managers and public investors. Notably, analyst coverage has been found to be negatively related to CSR decoupling (Zhang, 2021), while effective internal governance mechanisms dampen CSR decoupling activities (Ali Gull et al., 2022; Gull et al., 2023). Firms’ digital transformation enhances the transparency of the information environment, reshapes their relationship with external stakeholders, and amplifies the impact of their investments in social issues.

First, the implementation of comprehensive digital solutions in organizational strategies (Soluk and Kammerlander, 2021) and the integration of digital technologies into products and services enable digital management of relationships with suppliers and customers (Jian et al., 2021; Soluk and Kammerlander, 2021). This not only facilitates the collection and aggregation of management information but also makes it difficult for managers to manipulate or exaggerate facts in their communications. With the development of social network platforms and advancements in communication technologies, firms’ internal activities are more exposed in the market, attracting increased public attention and enhancing behavioral visibility (Leonardi and Treem, 2020). This increased visibility grants the public better access to firm information, making it easier for stakeholders to monitor and evaluate an organization’s behavior (Schnackenberg and Tomlinson, 2016). Consequently, digitalization improves both the internal and external information environment, reducing information asymmetry in agency relationships, a major source of symbolic management. Through digitalization, firms’ communication with stakeholders strengthens, and their internal strategic behaviors become more accessible to the public (Chierici et al., 2020). The organizational transparency enhanced by digital transformation makes it harder for managers to manipulate information and disguise facts in their reporting (Schnackenberg and Tomlinson, 2016). Therefore, with digitalization, it becomes challenging and costly for managers to engage in information manipulation and CSR decoupling behaviors.

Second, digital systems, including enterprise resource planning (ERP) systems, management information systems, digital supply chain management, and digital marketing, digitize, record, quantify, and assess managers’ performance in an automated manner. Historic behaviors are traceable within these systems (Cenamor et al., 2017), and, importantly, they enable digital management of relationships with critical stakeholders (Aghazadeh et al., 2023; Soluk and Kammerlander, 2021). Digital techniques strengthen the bond between firms and their stakeholders and boost transparency in both internal and external environments. The open, inclusive, and shareable nature of digital information promotes transparency across different departments. This not only creates an atmosphere of intense monitoring over managers’ behaviors but also allows various stakeholders to express their appeals and demands. Stakeholders wield more influence over firm performance and strategic decisions, as different groups are no longer isolated. They play a more powerful role in corporate decision-making (Jian et al., 2021; Meng et al., 2022), compelling executives to adopt a more earnest approach to CSR and CSR information disclosure.

Digital transformation is negatively associated with CSR decoupling.

The coverage of information intermediaries

According to agency theory (Jensen and Meckling, 1976), information asymmetry between managers and external stakeholders creates monitoring difficulties and agency costs (Akerlof, 1970). Information intermediaries, such as analysts and the media, therefore function as important external governance mechanisms by monitoring management and reducing information gaps in capital markets. Digital transformation reshapes firms’ information environment by enhancing transparency and traceability (Sun et al., 2025). Through the digitalization, recording, and aggregation of organizational activities, previously opaque processes are converted into observable and verifiable data (Salvi et al., 2021), thereby mitigating information asymmetry between firms and external stakeholders (Muslu et al., 2019). With the enhancement of data availability and standardization, the costs for external intermediaries to acquire and process information are significantly reduced. Analysts and the media rely on credible information to verify corporate disclosures and form evaluations (Huang et al., 2017). Programmed and transparent digital procedures reduce executives’ exclusive control over information (Wang et al., 2025b) and further lower intermediaries’ search and verification costs (Chen et al., 2021; Saxton et al., 2020), thereby enhancing the feasibility of external oversight. In addition, digital transformation increases firms’ behavioral visibility (Gui and Hou, 2025). This process is often accompanied by strategic renewal and business model innovation (Björkdahl, 2020; Ribeiro-Navarrete et al., 2021), making such firms more likely to attract market attention. Consequently, information intermediaries have stronger incentives to follow and report on digitalized firms.

Digital transformation is positively correlated with the coverage of information intermediaries.

The supervision and governance exerted by external stakeholders in their interactions with firms have a profound impact on corporate decisions and behaviors (Kim et al., 2024; Scott, 2008). Digital transformation significantly enhances transparency in production and management, fosters increased external attention on a firm, and enhances stakeholders’ supervisory capabilities. This, in turn, motivates firms to proactively participate in CSR activities and reduces their tendency to manipulate CSR information in their reports (Hu et al., 2021).

Information intermediaries and stakeholders remain vigilant in monitoring essential information about firms from various sources. Their discussions and coverage of firms aim to address information asymmetry in the capital market (Bushee et al., 2010; Naqvi et al., 2021). When significant disparities between CSR disclosure and performance are detected, firms come under heavy pressure, leading to a loss of legitimacy and reputation (Li et al., 2017). For instance, negative media reports regarding a firm’s pollution practices can prompt government authorities to take punitive measures (Tang and Tang, 2016). In firms subject to greater analyst coverage, executives’ shortsighted and self-serving actions have a more substantial impact on investors (Xu et al., 2016), and analysts play a pivotal role in deterring top management’s misconduct in information disclosure (Huang et al., 2021). Therefore, in addition to their direct monitoring role, public information intermediaries can redirect market and public attention toward a firm, broadening the scope of supervision.

In summary, digital transformation enhances organizational transparency, attracting increased attention from information intermediaries, and consequently, the decoupling of CSR disclosure from actual CSR performance is mitigated (Lyon and Montgomery, 2013; Zhang, 2021).

The coverage of information intermediaries mediates the relationship between digital transformation and CSR decoupling.

The quality of internal control system

According to the agency theory (Jensen and Meckling, 1976), information asymmetry and conflicts of interest generate agency costs, which require both external and internal governance mechanisms. While information intermediaries provide market-level oversight, internal control systems function as the core internal governance mechanism that constrains managerial opportunism and strengthens organizational monitoring. Digital transformation acts as a governance-enhancing mechanism that strengthens the internal control environment. First, digitalization reconfigures the control environment by shifting from manual supervision to automated and system-driven monitoring. Through programmed and standardized digital processes (Jans et al., 2022), the execution of internal procedures is less dependent on managerial discretion, reducing the likelihood of deviations from control objectives (Goldfarb and Tucker, 2017). Second, digital systems constrain the space for managerial opportunism through automated data collection and real-time processing. As organizational activities become traceable and verifiable (Boulhaga et al., 2023; Haislip and Richardson, 2018), data manipulation or misconduct becomes more difficult (Wang et al., 2025a). Furthermore, digital transformation is often associated with flatter organizational structures and greater cross-departmental collaboration (Camarinha-Matos et al., 2019; Kretschmer and Khashabi, 2020; Nambisan et al., 2019; Trushkina et al., 2020). Traditional information silos across departments are reduced (Paul et al., 2024), and internal information sharing and mutual monitoring are strengthened (Li et al., 2021). Internal control thus shifts from a top-down supervisory mechanism to a more distributed governance structure. Therefore, digital transformation contributes to improvements in the quality of the internal control system.

Digital transformation is positively correlated with internal control quality.

Adhering to legal and ethical standards is an essential objective of internal control. The quality of internal control is intricately linked to the achievement of operational and financial objectives (Boulhaga et al., 2023; Chang et al., 2019). Furthermore, studies have demonstrated that internal control enhances the credibility of a firm’s information disclosure (Gal and Akisik, 2020; Hoitash et al., 2009). Recent research has shown that firms are increasingly integrating environmental, social, and governance (ESG) issues into their internal control objectives (Harasheh and Provasi, 2023). Internal control serves to detect and prevent organizational misconduct (Jin and Mirza, 2023), ensuring the attainment of specific objectives. Thus, it plays as a mediating factor in the relationship between digital transformation and CSR decoupling. By improving the quality of firms’ internal control, digital transformation enhances organizational capabilities in fraud detection and prevention, increases the cost of malpractice by employees, and inhibits deviations in organizational behavior from legal and ethical standards.

First, within the agency relationship, executives may tend to exaggerate their achievements in social issues due to impression management and opportunistic motivations. This exaggeration can result in CSR decoupling as their claims may diverge from actual performance. Implementing strict audits and assurances on disclosed information can mitigate this issue, although it comes at a cost. A body of research has argued that robust internal control enhances the reliability of financial or non-financial information disclosure (Bentley-Goode et al., 2017; Hoitash et al., 2009). Therefore, effective internal control effectively addresses the misalignment between CSR disclosure and CSR performance (García-Sánchez et al., 2021).

Second, in business practice, the internal control system has started to prioritize CSR performance as a major objective (Boulhaga et al., 2023; Harasheh and Provasi, 2023). Effective internal control positively influences CSR performance, as CSR gains increasing importance in corporate governance (Lau et al., 2014). The essential purpose of governance is shifting from profit maximization to maximizing stakeholder benefits through social responsibility (Rodriguez-Gomez et al., 2020). It has been found that sound internal control is negatively related to risk-taking behaviors (Tian et al., 2022). Effective internal control discourages socially irresponsible behaviors, safeguards stakeholders’ legitimate rights, and promotes the achievement of CSR objectives. With effective internal control systems in place, various stakeholders find it easier to express their concerns, communicate with decision-makers, and participate in supervising firms’ operations (Meng et al., 2022). Consequently, a high-quality internal control system fosters greater CSR performance, reduces CSR risk, and diminishes the likelihood of managers engaging in CSR decoupling behaviors.

In summary, empowered by digital technologies, firms can establish a higher-quality internal control system that mitigates the discrepancy between CSR communication and CSR performance.

Internal control quality mediates the relationship between digital transformation and CSR decoupling.

Based on these hypotheses, the conceptual framework of this study can be delineated as Figure 1. Conceptual framework.

Data and methods

Sample and data

The manufacturing sector has been a major focus of digital transformation (Müller et al., 2018) and plays a key role in the Chinese economy. Manufacturing firms have been among the most active adopters of digital technologies, providing a suitable setting for examining the governance implications of digitalization. Since the “Digital China” strategy was first deployed in 2015, we begin our sample period in that year. Selecting this starting point helps us accurately track how the policy change has shaped corporate behavior over time. For this study, we utilized a sample of Chinese companies from the manufacturing industry listed on the Stock A market of the Shenzhen and Shanghai stock exchanges from 2015 to 2020. The firm-level data were provided by the China Stock Market & Accounting Research (CSMAR) Database and the Chinese Research Data Services Platform (CNRDS) databases.

To ensure data validity, we followed established procedures in prior studies: (1) we excluded companies under special treatment (ST) and particular transfer (PT) listings, as they operate under abnormal conditions; (2) we removed firm-year observations with missing values; and (3) we applied winsorization to the top and bottom 1% of the distribution for each financial variable. Since CSR decoupling data can only be obtained from firms that disclose CSR reports, our final sample consisted of 2140 firm-year observations, derived from the initial pool of 8028 observations. Although this restriction reduces the sample size, it is consistent with prior CSR decoupling studies and reflects the institutional reality that CSR disclosure remains partially voluntary in China.

Variable definitions and model specification

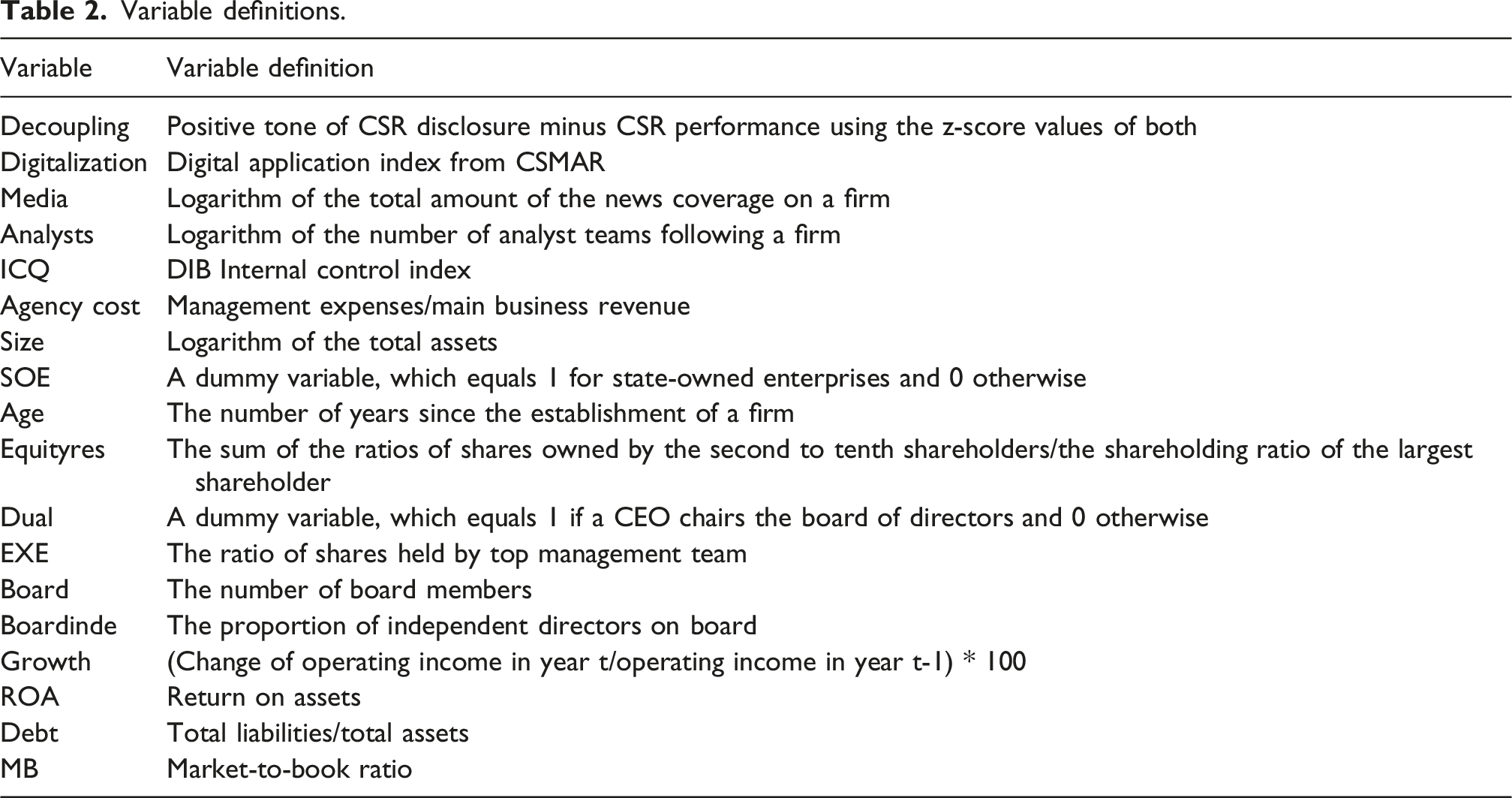

Dependent variable

CSR decoupling

CSR decoupling is defined as the misalignment between firms’ symbolic CSR communication and their substantive CSR performance. Following Zhang (2021), we operationalize this construct by comparing the optimistic tone of CSR reports with external CSR performance ratings. Both variables are standardized prior to calculation. While the dominant approach often focuses on disclosure breadth or volume (Marquis and Qian, 2014; Tashman et al., 2019), we suggest that tone captures a more nuanced and intentional dimension of symbolic management. Unlike disclosure breadth, which is increasingly subject to standardized reporting frameworks and external auditing, narrative tone remains an area in which managerial discretion is relatively high. An excessively optimistic tone, when uncoupled from actual performance, reflects an intentional effort to shape stakeholder perceptions and reinforce perceived legitimacy—a core manifestation of CSR decoupling (Sauerwald and Su, 2019). By standardizing and comparing the evaluative orientation (tone) with substantive outcomes (ratings), our measure identifies the communicative gap between a firm’s self-presentation and its actual social impact.

The optimistic tone within CSR reports is assessed using a content analysis approach. This analysis is based on an emotional term list and is quantified as the frequency of positive words minus the frequency of negative words then divided by the total frequency of both. The data for this analysis were sourced from the WinGo Textual Analytics Database, and the calculation is represented by equation (1).

Independent variable

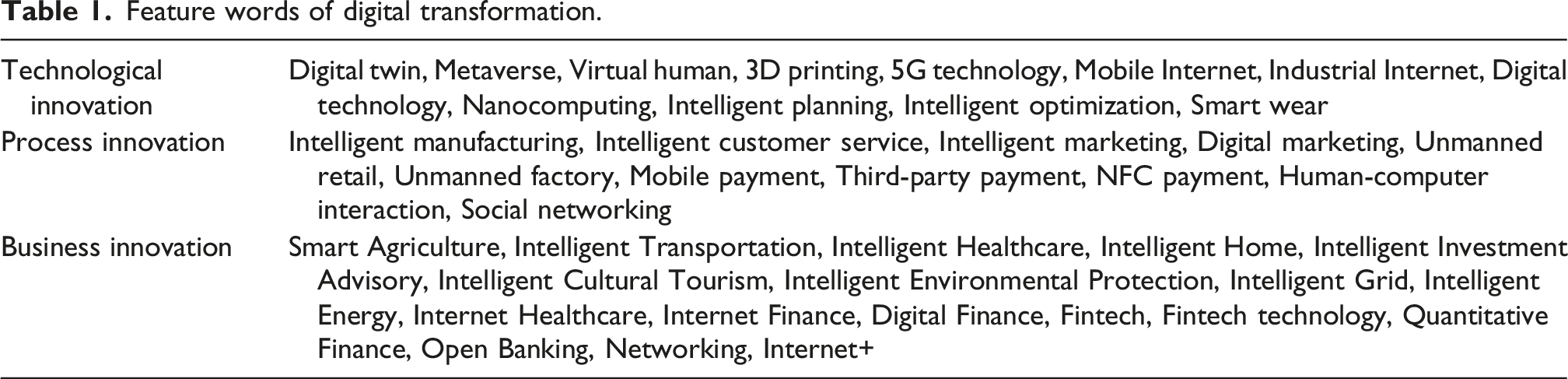

Digital transformation

Feature words of digital transformation.

Mediating variables

(1) The coverage of external information intermediaries. Media and analysts, as two major information intermediaries, have a significant impact on a firm’s external information environment. For this study, we used both media and analyst coverage as proxies alternatively. In line with Jiang et al. (2022), data on media coverage (Media) were extracted from the CNRDS database, which includes news articles from over 600 prominent Chinese newspapers. Media coverage was operationalized as the logarithm of the total number of news articles covering a firm in a given year. For analyst coverage (Analysts), consistent with prior studies such as Zhang (2021), data were gained from the CSMAR database. It was calculated as the logarithm of the number of analyst teams following a firm. (2) The quality of internal control system (ICQ). For assessing the quality of the internal control system, we employed the DIB Internal Control Index of Chinese Listed Companies, developed by the DIB Internal Control and Risk Assessment Database (ICRAD). This index is widely recognized in the literature (Li et al., 2019) and comprises five elements: internal environment, risk assessment, information and communication, control activities, and internal supervision. It serves as a reflection of the degree of perfection of the internal control system. Moreover, given that agency costs are primarily associated with deficiencies in internal control (Jensen, 2005), we also considered agency cost as an alternative measure, which is measured as the ratio of management expenses to business revenue.

Control variables and baseline model

Firm size (Size) and age (Age) are common controls in CSR studies, because they are closely related to corporate legitimacy, which motivate firms’ engagement in CSR (Wickert et al., 2016; D’ Amato and Falivena, 2020). The motivation of state-owned enterprises (SOE) toward CSR is different from that of non-SOEs, and there is a huge difference between SOEs and non-SOEs in their resource endowments and external institutional demands (Zeng et al., 2022). SOEs face stronger government monitoring on CSR implementation, which may limit their tendency toward CSR decoupling (Marquis and Qian, 2014). We introduce a dummy variable denoted as SOE, which equals 1 for SOEs and otherwise 0.

The concentration of shareholders’ ownership (Equityres) is in a close relationship with CSR (Ang et al., 2021), which is calculated by the sum of the ownership of the second to the tenth shareholders divided by that of the largest one. A more balanced ownership structure strengthens monitoring over management, potentially reducing the likelihood of CSR decoupling (Yu et al., 2020). Managerial ownership (EXE) aligns managers’ interests with those of shareholders, reducing the incentive to engage in symbolic CSR behavior that deviates from actual performance (Oh et al., 2011), which is captured by the ratio of top management ownership. The board of directors is mainly in charge of strategic decision making, and its characteristics are closely related to CSR strategies (Zhao et al., 2022) and CSR decoupling (Sauerwald and Su, 2019; Shahab et al., 2021). Accordingly, board size, board independence, and CEO-chairman duality are controlled for. Board size (Board) indicates the number of board members, and board independence (Boardinde) is the ratio of independent directors to the total number. CEO-chairman duality (Dual) is controlled for by a dummy variable, which equals 1 if a CEO chairs the board of directors and otherwise 0.

Firm profitability is closely associated with CSR. Variables related to profitability are added, including return on assets (ROA) and income growth (Growth). Financially healthy firms typically face weaker performance pressure and thus have less motivation to rely on symbolic CSR to manage stakeholder impressions, reducing the likelihood of CSR decoupling. Moreover, the market-to-book ratio (MB) also reflects the growth potential in future, and high-valuation firms often face greater market scrutiny, which increases the reputational costs of engaging in CSR decoupling. Financial leverage (Debt) is defined as the ratio of liability to total assets. Highly leveraged firms face greater financial pressure, which may incentivize them to rely on symbolic CSR communication to maintain legitimacy while limiting substantive CSR investment, thereby increasing CSR decoupling (Bothello et al., 2023; Mishra and Modi, 2013).

Variable definitions.

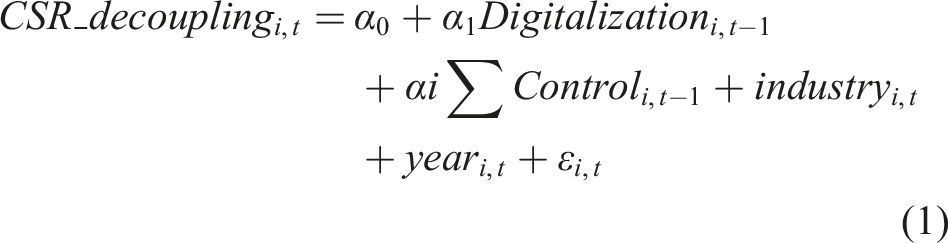

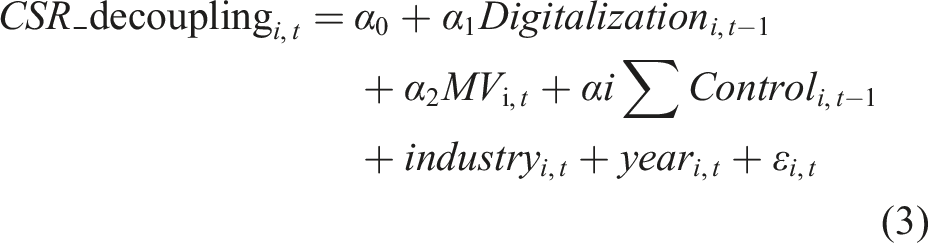

To examine the effect of digital transformation on CSR decoupling and test the related mediators, three steps of regressions are constructed as follows:

Empirical results

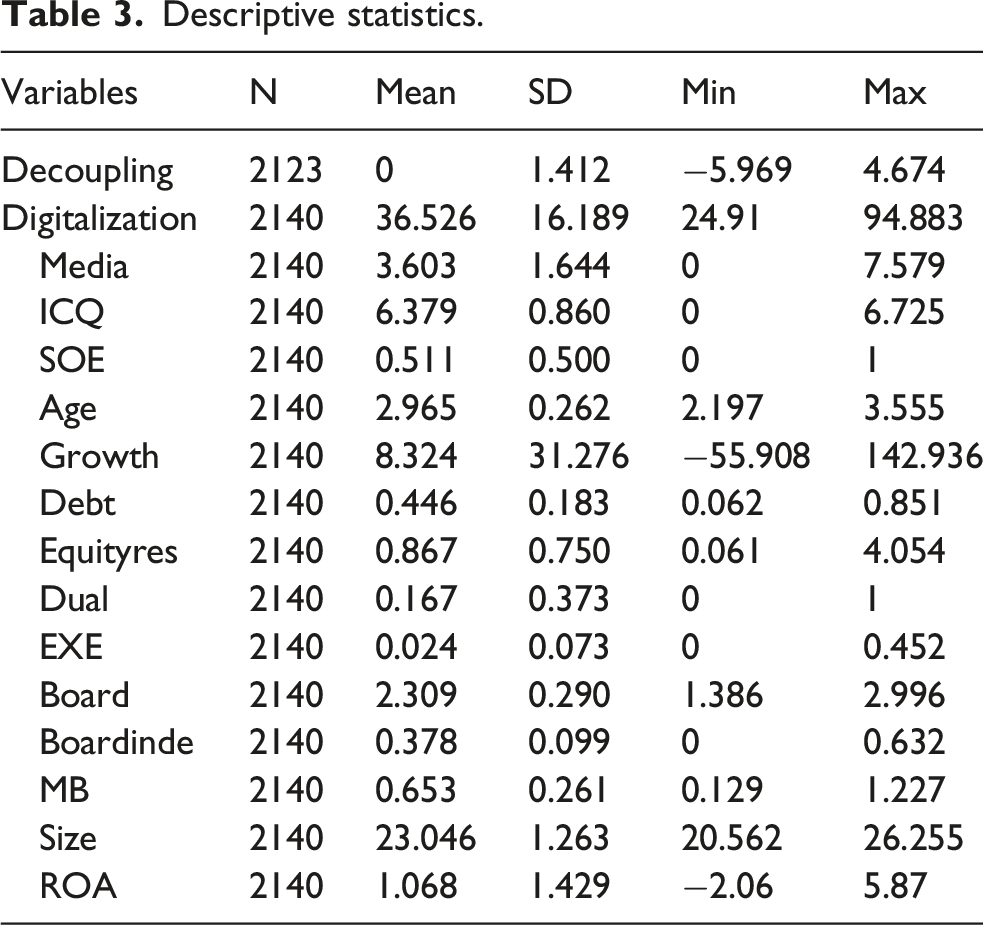

Descriptive statistics

Descriptive statistics.

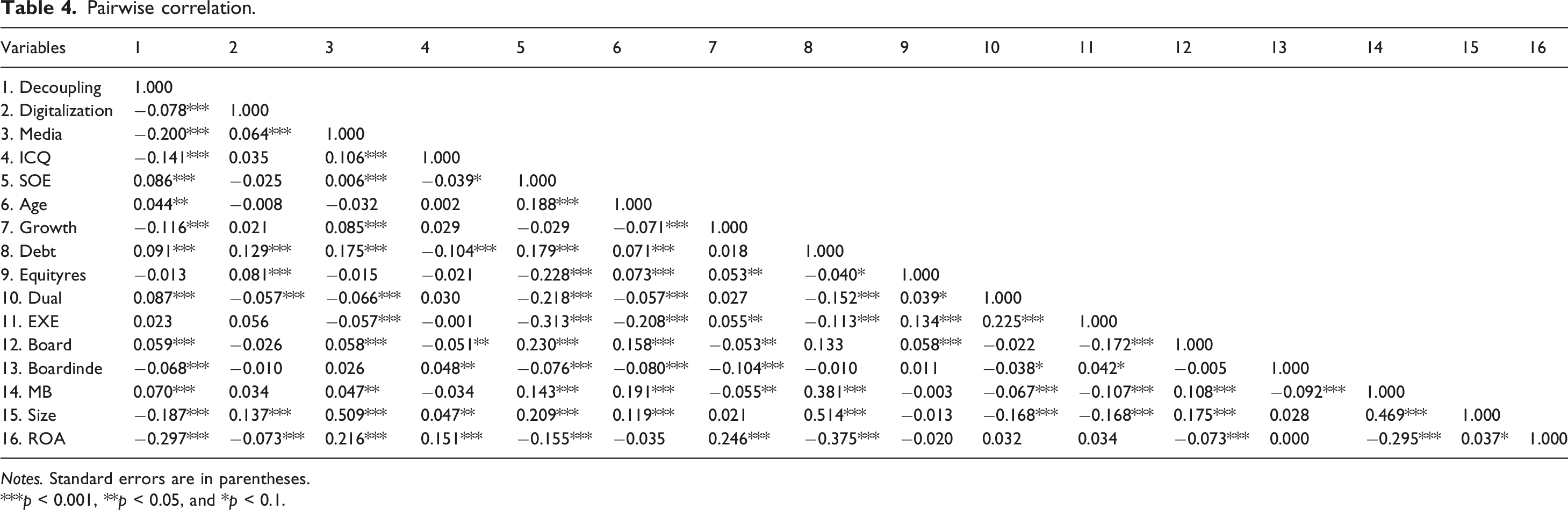

Pairwise correlation.

Notes. Standard errors are in parentheses.

***p < 0.001, **p < 0.05, and *p < 0.1.

Regression results

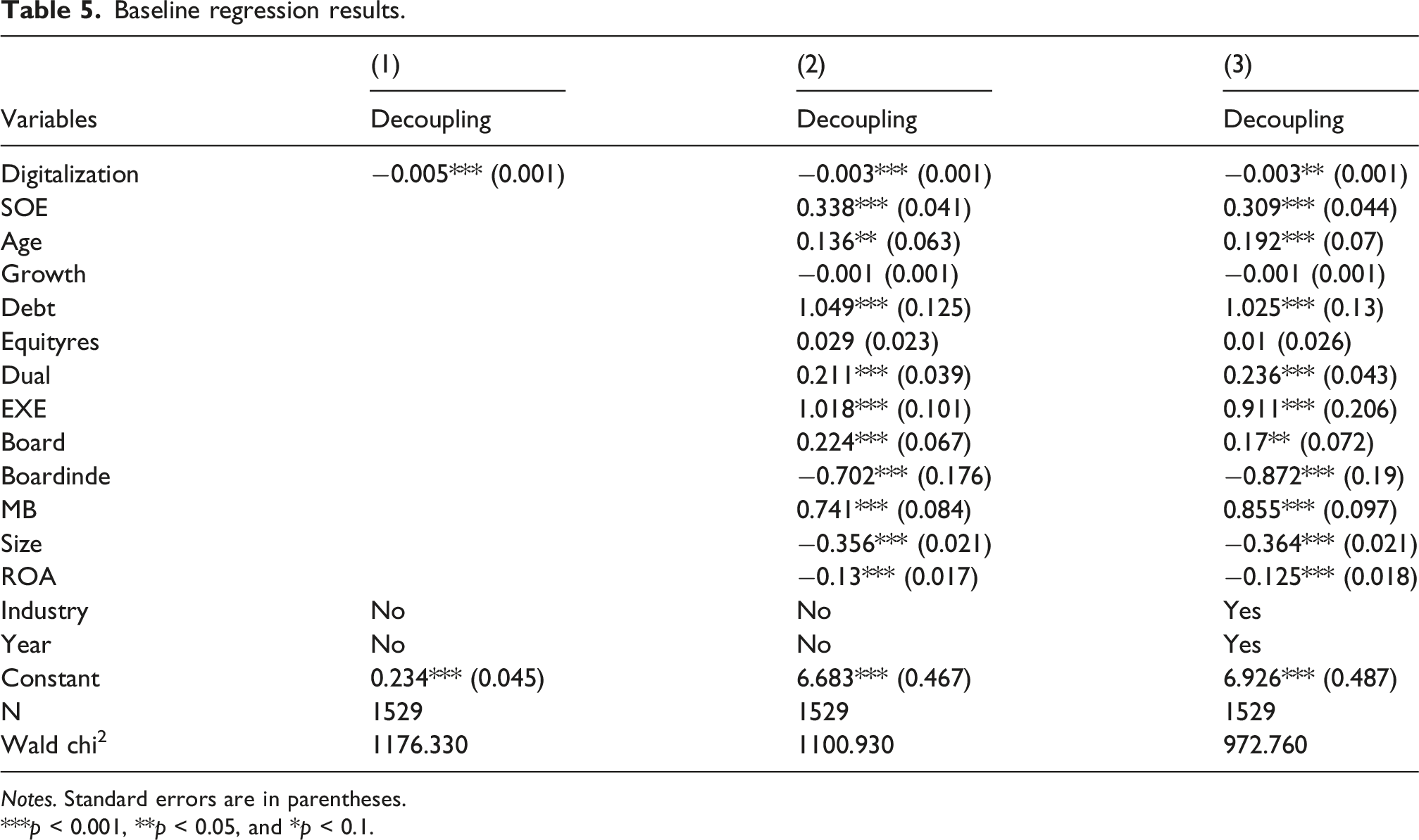

Baseline regression results.

Notes. Standard errors are in parentheses.

***p < 0.001, **p < 0.05, and *p < 0.1.

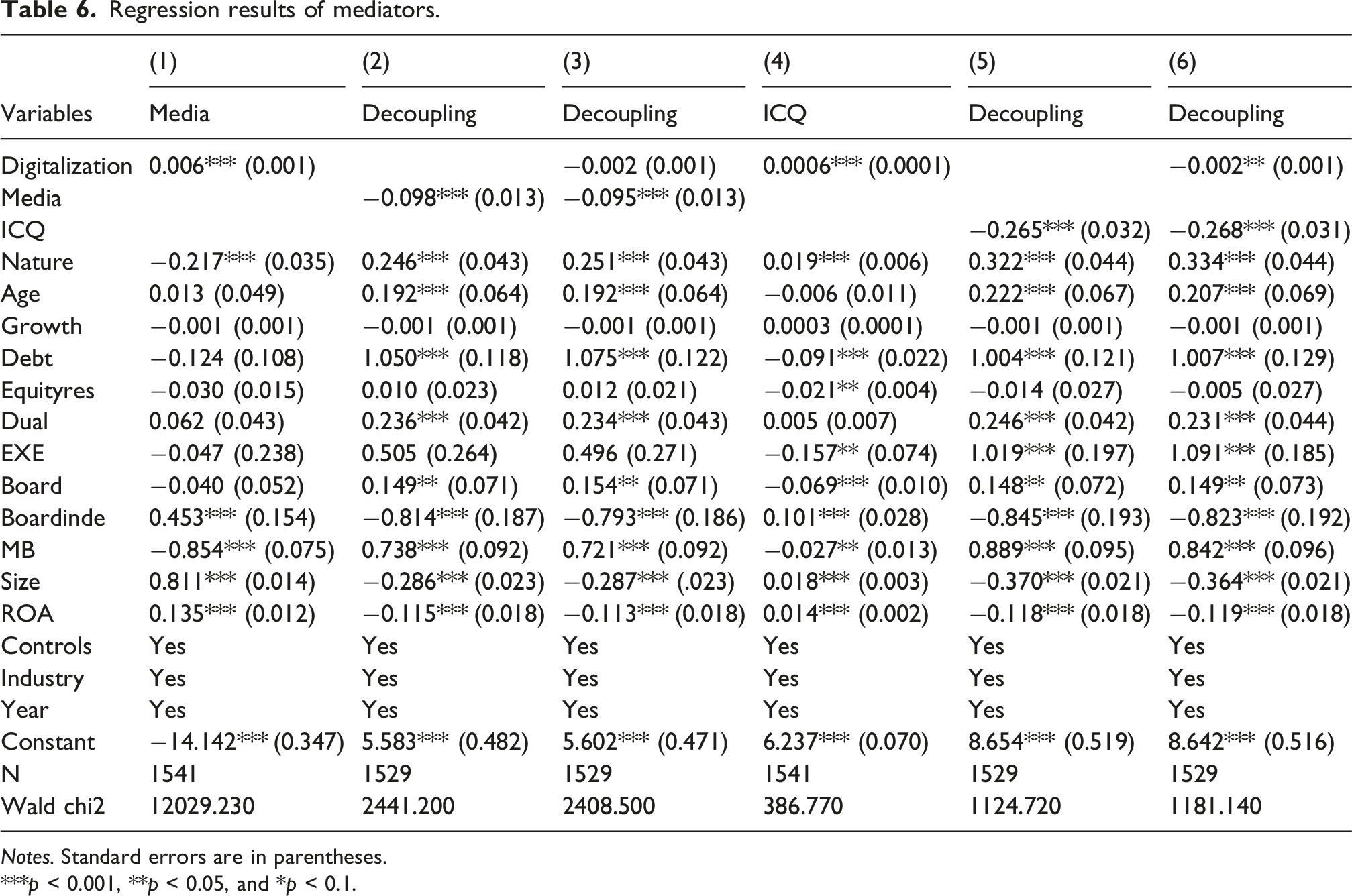

Regression results of mediators.

Notes. Standard errors are in parentheses.

***p < 0.001, **p < 0.05, and *p < 0.1.

posits that digital transformation is in a positive correlation with internal control quality. Model 4 shows that the coefficient of Digitalization is significantly positive (β = 0.0006 and p < 0.01), supporting Hypothesis 3a. Furthermore, Hypothesis 3b predicts a mediating role that internal control quality plays in the negative correlation between Digitalization and CSR decoupling. In Model 5, internal control quality (ICQ) is shown to be in a significant and negative relationship with CSR decoupling (β = −0.265 and p < 0.01), and in Model 6, Digitalization and ICQ are included. And based upon the results, a Sobel’s test is performed, of which the mediation effect is significant (p < 1%), which accounts for 6.9% of the total effect. Therefore, Hypothesis 3b is confirmed.

Robustness and endogeneity tests

Regression results using alternative measures of CSR decoupling.

Notes. Standard errors are in parentheses.

***p < 0.001, **p < 0.05, and *p < 0.1.

Regression results using alternative measures of mediators.

Notes. Standard errors are in parentheses.

***p < 0.001, **p < 0.05, and *p < 0.1.

Two-stage least squares (2SLS) regression results.

Notes. Standard errors are in parentheses.

***p < 0.001, **p < 0.05, and *p < 0.1.

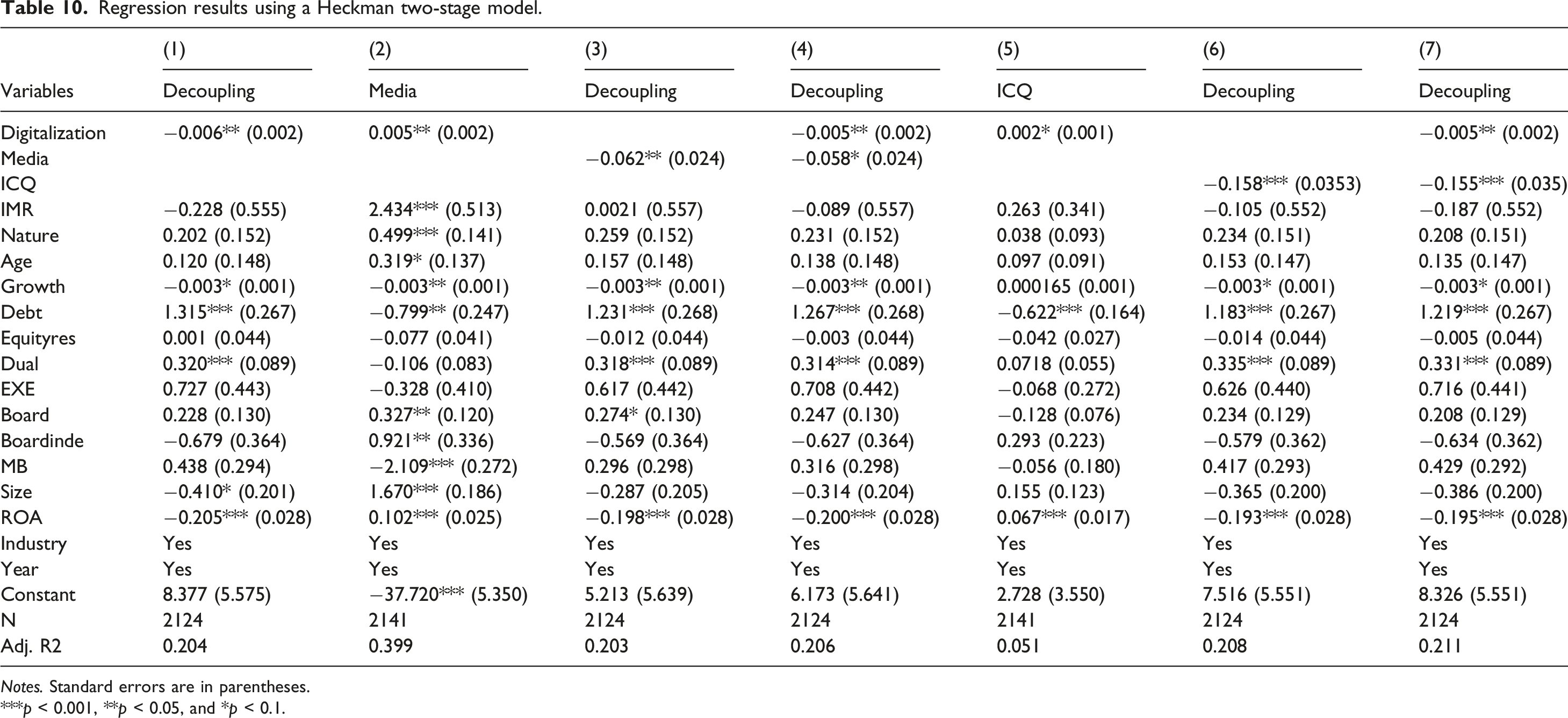

Regression results using a Heckman two-stage model.

Notes. Standard errors are in parentheses.

***p < 0.001, **p < 0.05, and *p < 0.1.

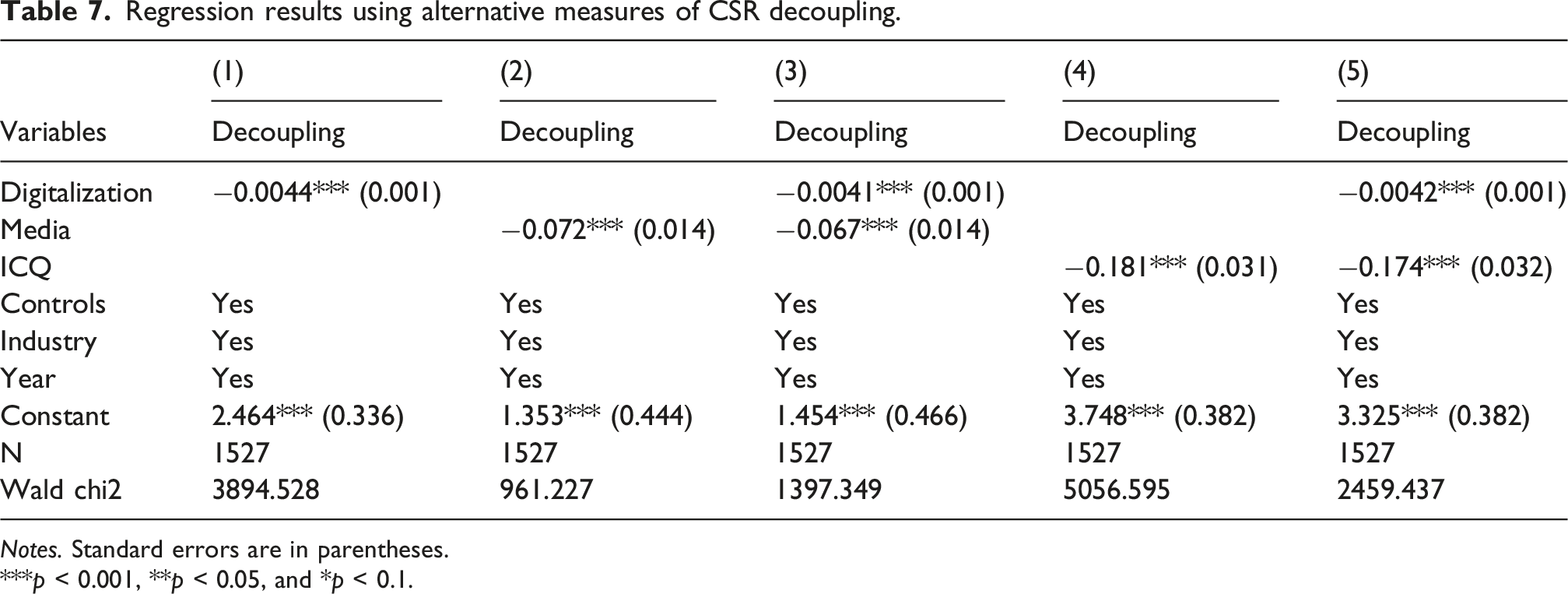

Robustness tests

To further validate our results, we construct an alternative measure of CSR decoupling by replacing the “say” dimension with a CSR disclosure index from the CSMAR database. This index is based on 12 disclosure items and is standardized before being differenced from the standardized Hexun CSR performance score. As shown in Table 7, Digitalization remains significantly negatively associated with CSR decoupling (Model 1). In addition, Media and ICQ remain significantly negatively related to CSR decoupling, and the coefficient on Digitalization stays negative and significant after these variables are introduced (Models 3 and 5). These results are consistent with the baseline findings and support the robustness of our conclusions.

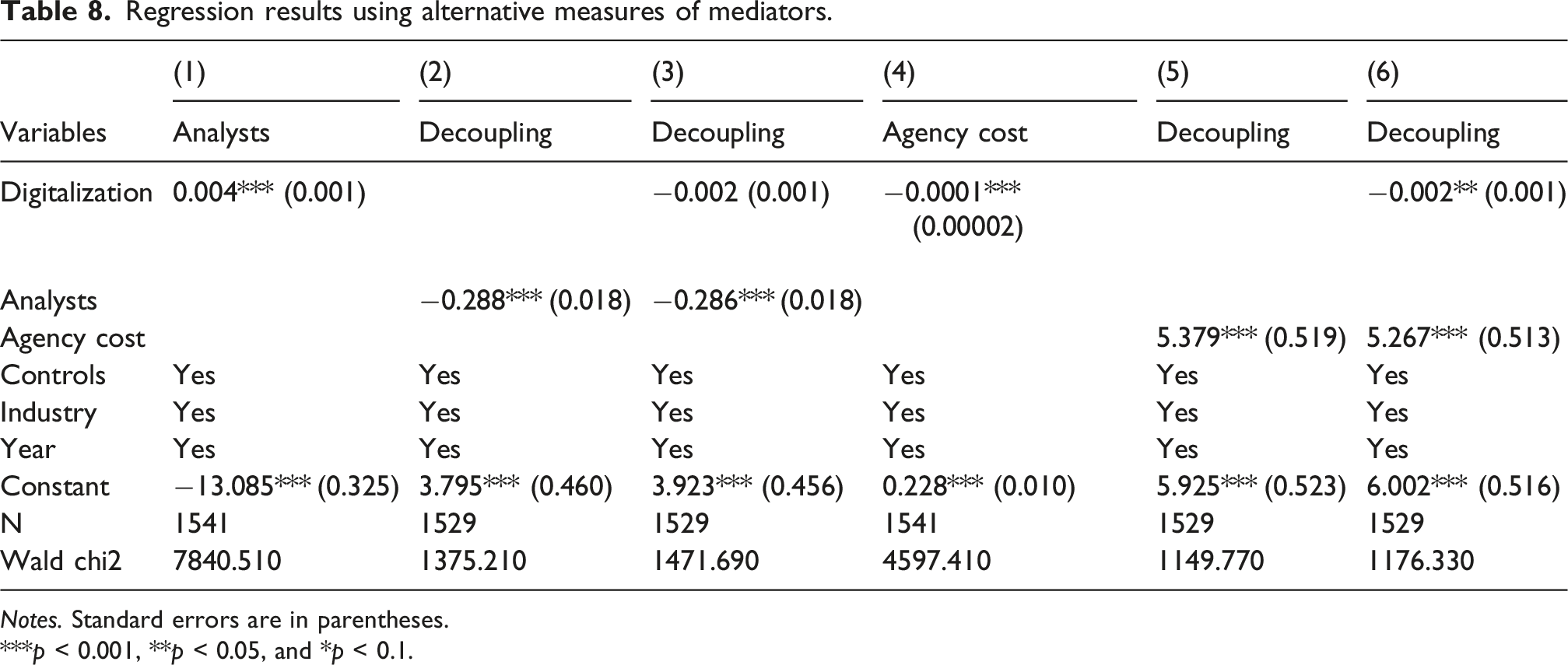

Considering that financial analysts are another important information intermediary, and agency cost is a reliable proxy for internal control quality, we further examine the mediating effects of analysts’ coverage and agency cost on the relationship between digital transformation and CSR decoupling. In Table 8, Models 1–3 and 4–6 present the results for the two mediators, respectively.

In Model 1, Digitalization is found to have a significant and positive association with Analysts, and Models 2 and 3 show that Analysts is negatively correlated with Decoupling, which provides further support to the mediating role of information intermediaries between digital transformation and CSR decoupling. Moreover, in Model 4, Digitalization is found to be in a negative association with agency cost, and in Models 5 and 6, agency cost is positively correlated with CSR decoupling. Therefore, the mediation of internal control system in the relationship between digital transformation and CSR decoupling is further corroborated. And these results remain robust.

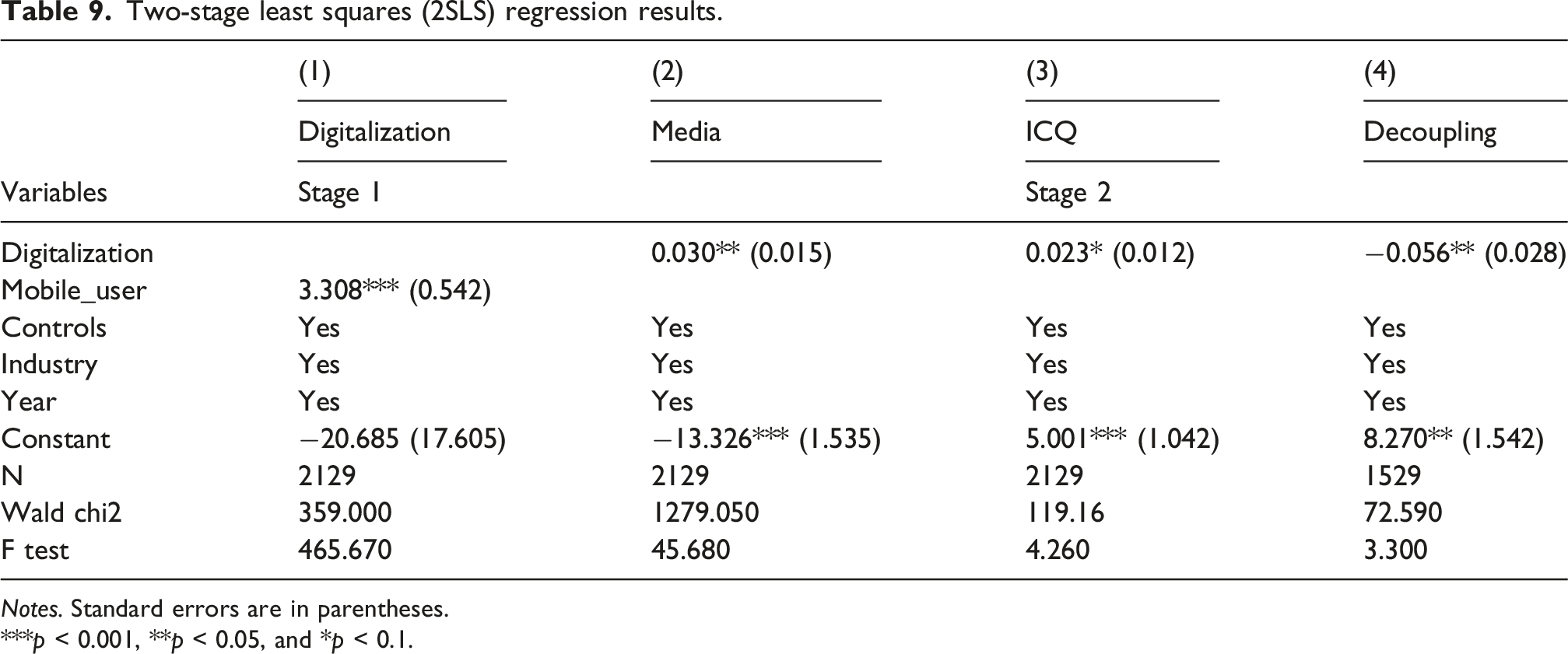

Endogeneity tests

Considering that there may be some unobservable factors affecting a firm’s digitalization and CSR strategies, the relationship between digital transformation and CSR decoupling may be subject to some endogenous problems. We choose the number of Mobile Internet user scale among provincial total population (Mobile_user) as an instrumental variable, which reflects the overall development of digital economy in a region and is a major external condition for firms’ implementation of digital technologies. The empirical results are presented in Table 9. The weak instrument test with F-statistic is greater than 10, which rules out the possibility of weak instrumental variables. Models 2 and 4 present the second-stage regression results, which remain consistent.

Sample selection bias test

The dependent variable, CSR decoupling, is measured based upon CSR reports, which may result in a sample-selection bias, because a part of the listed companies does not issue CSR reports. Following some prior studies (Sauerwald and Su, 2019), we conduct a two-stage Heckman test to address this potential bias, and Table 10 reports the result. At the first stage of the Heckman model, we performed a probit regression on whether a company releases a CSR report, and the residuals were employed to construct a selection bias control factor (the inverse Mills ratio, denoted as IMR). Meanwhile, we use the aforementioned digital transformation index at the provincial level as an exogenous variable in the first stage. After IMR is controlled for in the regressions, the results are shown to be largely consistent with the results we reported above.

Discussion and conclusion

This study examines the effect of digital transformation on CSR decoupling, based on a panel data of the Chinese listed companies in manufacturing sector from 2015 to 2020. Drawing on the perspective of corporate governance and adopting textual analysis methodology, it is shown from the results that digital transformation is negatively related to CSR decoupling. Meanwhile, digital transformation enhances the coverage of information intermediaries (media and analysts) and the quality of internal control, by which CSR decoupling could be mitigated.

Theoretical contributions

This research contributes to the literature in three ways. Firstly, this research enriches our understanding of the strategic implications of digital transformation. Digitalization has been widely recognized for its impact on various aspects of firm performance (Ribeiro-Navarrete et al., 2021), risk-taking (Tian et al., 2022), and operational efficiency (Björkdahl, 2020). Additionally, digital technologies facilitate communication with external stakeholders (Brockhaus et al., 2023) and enhance the efficiency and effectiveness of corporate governance mechanisms (Manita et al., 2020). Nevertheless, digital technologies can sometimes lead to unintended consequences for firms, such as data breaches and the amplification of organizational inequalities, which present new challenges (Syed, 2019; Gwebu et al., 2018; Trittin-Ulbrich et al., 2021). Additionally, digital transformation may discourage managers from disclosing CSR information due to increased oversight from a variety of stakeholders (Jin and Mirza, 2023). This study highlights CSR decoupling as a critical consequence of governance shortcomings, specifically the misalignment between communication and actual performance. This misalignment poses risks to firms and misleads stakeholders in their decision-making processes (Carlos and Lewis, 2018; García-Sánchez et al., 2021; Zhao et al., 2022). By investigating digitalization as a potential remedy for CSR decoupling, this study expands our knowledge of how digital strategies can impact organizational strategic outcomes.

Secondly, it extends our knowledge on the antecedents of CSR decoupling, a phenomenon that poses risks to firms, investors, and stakeholders alike. Corporate governance mechanisms have been recognized as pivotal in addressing CSR decoupling (Ali Gull et al., 2022), and previous research has identified associations between the characteristics of CEO and the board of directors with CSR decoupling (Sauerwald and Su, 2019; Shahab et al., 2021). This study explores digital transformation as a novel approach to mitigate CSR decoupling. By leveraging digital technologies and adopting digitalization strategies, firms can enhance their corporate governance, thus offering solutions to persistent challenges in conventional governance structures. Importantly, this study underscores the mediating roles played by internal control system and external information intermediaries in the relationship between digitalization and CSR decoupling. The full mediation indicates that media coverage is the main pathway linking digital transformation to lower CSR decoupling. This means digital transformation does not reduce decoupling automatically. Rather, it makes firm information more transparent and strengthens external oversight, which limits symbolic CSR. These mediating roles suggest that digital strategies of a firm can trigger improvements in both internal and external governance mechanisms to combat CSR decoupling behaviors.

While our findings suggest that digital transformation is associated with lower CSR decoupling, these effects may not be universal. The governance benefits of digitalization are likely to vary across firms and contexts. For example, firms facing financial constraints may experience resource trade-offs, as investments in digital infrastructure could crowd out substantive CSR activities and encourage more symbolic compliance. In addition, digital transformation presents a paradox: although digital technologies can enhance transparency and monitoring, they may also strengthen firms’ capacity for impression management, enabling symbolic CSR practices that are harder for outsiders to detect. The results indicate that within the current Chinese institutional context, the transparency and monitoring effects associated with digitalization tend to outweigh these potential opportunistic tendencies. Nevertheless, the effectiveness of digital transformation remains contingent upon external scrutiny and organizational conditions.

Thirdly, this research makes a contribution to the corporate governance literature by reinforcing the understanding that corporate governance mechanisms are closely tied to CSR engagement and the overstatement of CSR performance in communications. Prior studies have examined governance committees (Gull et al., 2023) and analyst coverage (Zhang, 2021) as key factors influencing CSR-related behaviors. Furthermore, scholars have explored top management team characteristics as antecedents to these issues. Given the persistent challenge of information asymmetry and agency problems in CSR disclosure, digital techniques emerge as potent tools to address these problems and enhance corporate governance mechanisms’ efficiency and effectiveness. This study demonstrates how digital transformation improves the overall governance environment and internal control, thus mitigating CSR decoupling.

Practical implications

This study offers practical implications for addressing CSR decoupling. Given the self-serving motivations of executives and information asymmetry between executives and investors, the overstatement of CSR performance in communications is indicative of corporate governance limitations. While various mechanisms have been designed and implemented to mitigate agency conflicts related to CSR decoupling, such as governance committees (Gull et al., 2023), analyst coverage (Zhang, 2021), global reporting initiative (GRI) reporting guidelines, and external assurance of CSR reports (García-Sánchez et al., 2022), these have not fully resolved the issue in practice. This study suggests that digital technologies offer powerful solutions to intractable management problems and can serve as a potent remedy for CSR decoupling by enhancing the overall corporate governance environment.

Limitations and suggestions for future research

However, it’s important to acknowledge certain limitations to this study. Firstly, the measurement of CSR decoupling is constrained by the availability of CSR reports, which may introduce sample selection bias, particularly in China where not all firms issue CSR reports. Although the study employs a Heckman model to address this concern, it remains a potential limitation. Secondly, the study focuses on a panel of Chinese listed manufacturing companies, which is a major field of digital transformation. Results and implications may differ significantly in other industries where the process of digitalization and its consequences are distinct from those in manufacturing. Moreover, our finding that digital transformation mitigates CSR decoupling is consistent with prior studies showing that better governance quality helps reduce CSR decoupling in different national contexts (Bothello et al., 2023; Velte, 2023). However, digitalization may also increase greenwashing among Chinese firms (Jia et al., 2025). This suggests that the governance effects of digitalization may vary by context and deserve further cross-country examination. Thirdly, although tone is a sensitive indicator for capturing managerial impression management and symbolic communication, it may not fully reflect structural forms of decoupling, such as discrepancies in the specific scope or depth of CSR activities. Future research could adopt multi-dimensional measures that integrate various disclosure characteristics and rhetorical strategies to further validate the robustness of our findings. Lastly, apart from the external information environment and internal control system, other governance mechanisms linking digitalization to CSR decoupling may exist, such as regulatory inspections and audit quality. Future research could further examine the boundary conditions highlighted in this study. Factors such as financial constraints, institutional pressures, and regional marketization may shape how digital transformation influences CSR decoupling. Exploring these moderating effects would contribute to a more nuanced understanding of when digital transformation mitigates or potentially intensifies CSR decoupling.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study is supported by Shanghai Philosophy and Social Science Planning Project (Grant No. 2019EGL014) and the National Natural Science Foundation of China (Grant Nos. 71972125 and 72271153).

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.