Abstract

This article examines recent plans for US municipalities to use the state legal power of eminent domain to forcibly acquire “underwater” mortgages (i.e. those with negative equity), and to refinance them on terms more favorable to the homeowners in question, as a way of addressing in a socially progressive way the nation’s ongoing foreclosure crisis. The article makes three main arguments. The first is that insofar as the plan threatens to disrupt prevailing norms of value distribution and risk bearing, it represents a fundamental challenge to the existing political economy of urban financial capitalism in the US and the law’s mediation thereof. The second is that value, risk, and their mediation through law must be understood in the context of geographical unevenness and shifting scales of legal governance. The third is that the geographical political economy associated with the eminent domain plan is about discourses—of risk, of markets, and indeed of law per se—no less than materialities; and that the two are indelibly linked, with discourses having material effects when, through law, they structure value and risk for the manifold actors who operate within the sphere of housing finance.

Introduction

If the global financial crisis which began in 2007 had many distinctive geographies, one such, in the context of the subprime US heartland of the crisis, was indubitably its urban- and housing-centered roots and repercussions. The freezing of financial markets flooded with toxic home loans was accompanied by and intimately connected to a freezing of domestic household economies in the form of foreclosure (termination) of individuals’ and families’ rights to their homes—plummeting house prices precluding the traditional fallback, in the event of mortgage-servicing affordability constraints, of equity-based refinancing. There were nearly three million foreclosure filings nationwide in 2010 alone, with more than a million homes being physically repossessed in the same year (CNN Money, 2014).

Some eight years on from the beginning of the crisis, existing responses to the foreclosure crisis are commonly seen to have failed. The two most notable such interventions have both been federal initiatives. The first is the Home Affordable Refinance Program, which enables homeowners with “underwater” mortgages—those, in other words, with negative equity, where the market value of the home is lower than the outstanding balance on the mortgage—to refinance onto lower interest rates, but which is limited by its availability to mortgages that are both “performing” (i.e. not in payment default) and guaranteed by one of two government-sponsored enterprises, Fannie Mae and Freddie Mac. The second is the Home Affordable Modification Program, under which financial institutions are incentivized to reduce the monthly payments of qualifying borrowers, which is to be done: first by reducing interest rates; then, if necessary, by delaying payment of the mortgage principal; and finally, again if necessary, by forbearing principal. Yet, partly by dint of eligibility restrictions, and notwithstanding a modest-if-uneven recovery of house prices, neither program has made much of a dent in the negative-equity phenomenon and associated foreclosure threat. At the beginning of 2014, 9.3 million properties, representing nearly 20% of all mortgaged homes, were reported as still being “deeply” underwater (borrowers owing at least 25% more on their mortgage than the homes were worth in current market prices) (CNN Money, 2014).

It is in this gnarly context that an alternative plan for assisting pressured homeowners has emerged. First mooted in the early months of 2012, continuing to circulate in the period since then, and attracting, in the process, supporters and opponents alike, the plan in question remains, at the time of writing (in mid-2015), exactly that: a plan—it has not yet been put into action. But whether it ultimately materializes or not, the plan warrants close and critical scrutiny: for its innovative and radical form, for its potential effects, and for its illustration of significant dimensions of the relationship between financial capitalism, risk, and law.

While the plan comes in various shapes and sizes, its basic elements are as follows

(cf. Figure 1). Local

municipalities would use eminent domain, a legal power known elsewhere as

expropriation, resumption, or compulsory purchase, to help homeowners with negative

equity to renegotiate the principal amounts of their mortgages at values closer to

prevailing market house prices, thus closing or narrowing the negative equity gap

and thereby reducing the risk of foreclosure. Specifically, the municipalities would

compel existing mortgagees—or, more commonly, investors in the (typically

securitized) mortgages—to sell them the existing underwater mortgages; they would

then refinance the mortgages, generally by reselling them to investors to maintain

the plan’s budget neutrality. It is eminent domain that would compel the

mortgagees/investors to sell. All that is required under the law is for the

government to show that property is being taken for “public use”—common uses invoked

in US courts in eminent domain cases more generally include stimulating economic

development, preventing or reversing blight, and eliminating dislocations in local

housing markets (Hockett,

2012: 168–169)—and to pay “just compensation” (typically construed as

fair market value) to the unwilling vendor.

1

While eminent domain ordinarily

entails seizure of physical property, it has frequently been interpreted by US

courts to allow for the taking of intangible property, such precedents thus

foregrounding the proposed extension to mortgage seizure. Key stakeholders in the mortgage eminent domain

plan.

This article examines the plan itself and its fortunes to date, focusing in particular on the resistance it has elicited. We make three principal, linked arguments.

First, the plan represents a fundamental challenge to the existing political economy of urban financial capitalism in the US and the law’s mediation thereof. If value—its sources, accumulation, and distribution—is the core of political economy then the eminent domain proposal is emphatically a proposal of political–economic moment: a new front in an ongoing and wider conflict over value, its periodic “destruction,” and who bears the costs. The mainstream financial sector, wherein the lion’s share of originators of and investors in the US’s underwater mortgages are found, has closed ranks in opposition to the plan precisely in view of the implications it is seen to bear for the (re)distribution of value between investor/mortgagee and the borrower–mortgagor. Yet, the plan is ultimately as much about risk—the risk of devaluation—and its distribution as it is about value, and in demonstrating this the article adds to the work of those (e.g. Ashton, 2011; Johnson, 2013) who have recently sought to integrate considerations of financial risk into a political–economic literature that has historically downplayed them. The law figures in this political–economic drama as a crucial field where value and risk outcomes are rendered negotiable and are, accordingly, contested and (re)produced.

Second, value, risk, and their mediation through law must be understood in the context of geographical unevenness and shifting scales of legal governance. The eminent domain plan in practice responds to local crisis conditions and is predicated on mobilizing what have historically been locally oriented legal powers in the service of a locally defined “public” framed by the geographies of the subprime crisis. What makes the plan “public,” according to its proponents, is that it rescues homeowners partly in order to mitigate foreclosure’s secondary “spillover” effects on neighboring owners and local governments. Yet, debate about the legality and economics of the plan takes place within a context of law making and financial reform at the federal and state scales. Crucially, the attempt to use the law’s “public purpose” for mortgage restructuring places this particular, localized legal power—and discourses surrounding its proper use—into direct conflict with political–legal initiatives at national and state scales, at which countervailing norms of risk and value are being reinstituted (Ashton, 2011).

Third, the article submits that the geographical political economy associated with the eminent domain plan is about discourses—of risk, of markets, and indeed of law per se—no less than materialities; and that the two are indelibly linked. Political–economic conflicts over value and risk are (shaped by) discursive conflicts, featuring, in the eminent domain case, forceful arguments about the law and about the market principles upheld by the law, which is to say discursive figurations of “the law’s markets” (Christophers, 2015). The article demonstrates how the financial sector deploys discourses of law and markets to prevent the implementation of policies that are inimical to the creation of new postrecessionary norms and expectations of risk. Those discourses are often deeply contradictory phenomena: the financial industry’s self-representation as a quintessentially (and rationally) risk-taking and -bearing sector is belied by the externalization of risk to actors such as the government and mortgagors.

These discourses have material effects when, through law, they structure value and risk for the manifold actors who operate within the sphere of housing finance, from investors to homeowners. And, if value is the immediate political–economic issue at stake in the eminent domain plan, and the immediate reason for Wall Street’s opposition to it, then risk is the deeper, more decisive issue. In its radical potential to rewrite the terms of the whole existing risk calculus of US mortgage finance, the eminent domain plan poses an arguably existential threat to the mainstream financial sector. If the plan were to proceed, it would not only effect a present-day redistribution of value, but, through precedent, it would raise the prospect of future, unpredictable principal write-downs—anathema to an industry concerned to render risk visible, calculable, and manageable where it cannot simply offload it onto others. The two sections of the article are arranged around these two key tropes—of value and risk—respectively.

Value

Taking value locally

The plan to invoke the legal power of eminent domain to ease financial pressures on US homeowners at risk of foreclosure needs to be situated in relation not just to contemporary financial crisis but also, briefly, to the essential nature of that power. As in other countries, eminent domain allows the state—at whatever scale—to take private property where the incumbent owner is unwilling to sell, if (as already indicated) it pays “just” compensation and can demonstrate the taking is for a public use. The property thus acquired can then be used either directly by the state itself—e.g. for transportation infrastructure, public utilities, government buildings, and so forth—or it can be transferred to private third parties, for instance for private redevelopment purposes (e.g. Becher, 2014; Christophers, 2010), if the state is nonetheless able to show that the all-important public use criterion is still effectively met.

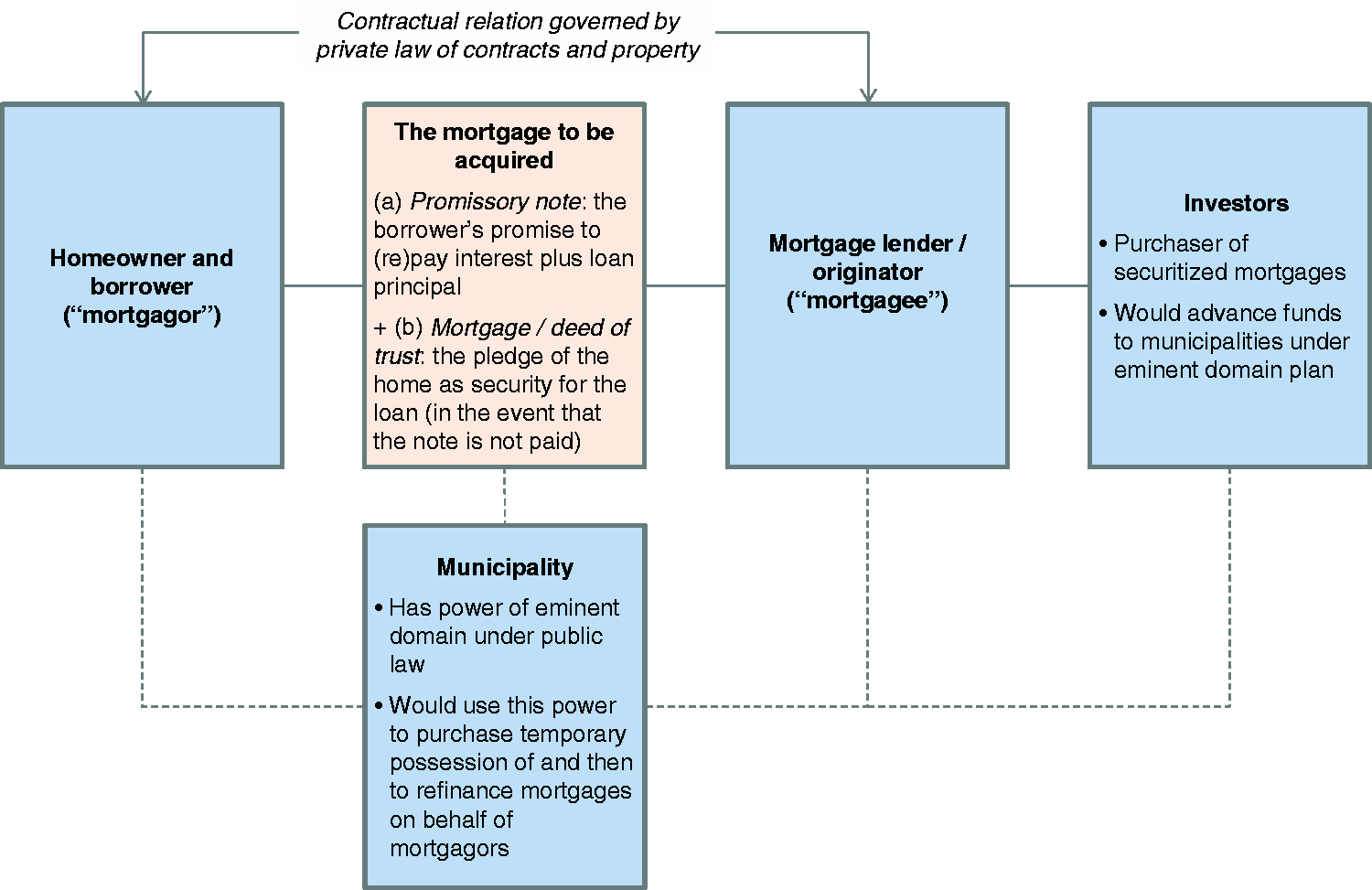

The details of the plan in question have been spelled out most clearly by a Cornell Law School professor, Robert Hockett, who has emerged as the academic legal community’s most prominent advocate of the plan, and whose writings (Hockett, 2012, 2013) we therefore draw upon here. In short, Hockett proposes that private investors would advance funds to local governments, which would use eminent domain to condemn and discharge selected mortgage notes and associated deeds of trust, then underwriting new mortgages at discounted repayment schedules for the homeowners whose existing mortgages were seized. These new mortgages would be conveyed to the investor group that had advanced monies to the local government.

Figure 1 positions the key stakeholders in the plan relative to the property (the mortgage) to be seized. It should be noted, however, that the depiction is highly simplified; for the sake of clarity, it omits, for example, both mortgage servicers (which collect and disburse loan payments) and securitization trusts (which represent the pooled interests of end investors and oversee disbursements to them), and it does not distinguish between first and second lien loans. 2 It should also be noted that the loans that Hockett recommends targeting, as well as being underwater (i.e. where homes are at high risk of foreclosure), are specifically private-label securitized loans. These have thus far proven difficult to modify or restructure, due largely to the range of actors—including servicers, trustees, and second lien holders—who are unwilling or unable to modify mortgage debt. 3

To fully grasp the nature, implications and prospects of the plan as it has been advanced in particular places, it is necessary to recognize and understand its geographical dimensions. We therefore start with these. In short, the plan has been formulated locally and, if it is eventually implemented, will be actioned locally. There are at least three important reasons for this spatial specificity.

First, the localized nature of the plan reflects the reality of the localized—or, better, highly geographically differentiated—nature of the phenomena (housing market crisis, household indebtedness, and ultimately foreclosure) to which the plan represents a response. We would express it like this: the conditions that the plan aims to rectify represent a particularly vivid manifestation of repeated rounds of the uneven geographical development to which the US urban landscape has historically been so prone. Recent research has identified significant and complex variation in such conditions between regions, between strong- and weak-market metropolitan areas, and between urban and suburban neighborhoods within those metropolitan areas (Anacker, 2015; Dong and Hansz, 2015; Immergluck, 2010). Since the landscape of residential value and its social dislocations is not spatially even, it is unsurprising that the impetus to address such dislocations through legal–financial measures is not even, either. Hockett (2012: 150) makes this exact point in trumpeting the potential instrumentality of “the states and their municipalities – townships, cities, counties, and kindred units of local government”: “For the problem itself is essentially, in its first instance, local in character.” According to legal scholar Marissa Schaffer (2014: 237): “an optimal solution would likely focus on the hardest-hit areas and be subject to local oversight,” especially given that “local officials may have greater insight into the specific nature of the problems.”

Second, the flip side of this argument is that while there are very good reasons to anticipate vigorous local mobilization, an expectation of meaningful and productive intervention at the national scale—intervention which, as we saw in the “Introduction” section, has not been forthcoming—is far harder to argue for. Partly, as Hockett (2012: 143) suggests, this is a matter simply of distance: “the first costs and immediate urgency of our nation’s self-worsening mortgage crisis are experienced more directly by the localities in which mortgaged property is located than by the more remotely located federal government.” It would clearly be wrong, however, to suggest that such distance is either natural or unbridgeable. In the context of the neoliberalized US political economy, it is an active product of federal policy. Such policy, as Gotham and Greenberg (2014), among others, have argued, has for many years been characterized by the devolution of responsibility to the local state. Accordingly, the federal state has remained (actively) “remote” in the wake of the financial crisis, Peck (2012: 627–629) showing that “the practice [of austerity] has been both normalized and localized” and that, in view of such “devolved austerity measures,” we should understand the “extreme” political economy associated with austerity in terms of “a distinctively urban crisis.” Local agitation to use eminent domain to help pressured households represents a countermovement against this trend and against the federal abandonment underwriting it.

Third and lastly, there is the nature of eminent domain itself, not so much as written legal doctrine but as it has been interpreted and applied in the US as historical–geographical legal practice. In terms specifically of its proposed (local) spatial circumscription, the plan to use this law to acquire mortgages represents, Hockett (2012: 159–162) argues, “a familiar and altogether orthodox exercise of the eminent domain power,” jurisdiction “over matters of real property, trust and estates, contract, and commercial law – the stuff of housing, home-ownership, real estate, and mortgage finance” historically vesting “almost exclusively” with individual states and with the municipalities to which such states unilaterally delegate legal authority. Urban governments used these delegated powers to clear and rebuild urban infrastructure during the period of federally funded urban renewal programs from the 1940s through the 1970s; more recently, cash-strapped urban governments have used the same powers to lure and retain private capital as federal monies—not just for urban renewal, but for a host of urban-focused housing and social programs—have dried up during multiple rounds of austerity. The regressive application of eminent domain—exemplified by the high-profile Kelo case in New London, Connecticut, which reached the US Supreme Court in 2005—has made it a bête noire of perceived government overreach and incompetence, at the behest of elites. In this respect, using eminent domain to restructure mortgages also represents something of a countermovement against its use by economic and political elites to attempt to restore profitability in the face of deindustrialization and disinvestment.

This brings us to the actual places and peoples which, in the midst of the foreclosure crisis, have been considering renewing this longstanding history of local mobilization of eminent domain powers—and to the specific geolegal institutional configurations they have created, or sought to create, toward this end. The plan to use eminent domain to take underwater mortgages first surfaced in meaningful fashion in California, where declines in residential property prices were among the steepest nationwide. 4 In June 2012, the Board of Supervisors of San Bernardino County created a Joint Powers Authority (JPA) incorporating the county and two of its largest municipalities (Ontario and Fontana) and explicitly gave this new body the power to purchase mortgage debt, through eminent domain if necessary. In the face of opposition from the financial industry and with a lack of local support, however, the JPA soon backed off, leaving it to another Californian city, Richmond, to take up the eminent domain baton. Richmond city council voted in favor of the plan and sent notices to 624 homeowners—who, to be eligible, had to be current on their mortgage payments and not have second liens—announcing its intention to buy their mortgage notes at 80% of their home’s (diminished) fair market value. The victory of progressive candidates in mayoral and council elections in November 2014 has given the proposal and its supporters renewed impetus.

Meanwhile, various other municipalities across the US, ranging in scale from Newark and Irvington in New Jersey to New York City itself, have actively mooted similar plans. The City of Newark has advanced its own plan nearly as far as Richmond, and local advocates are now coordinating their campaign with nonprofits in other cities. This national-level strategic coordination has become all the more important since the passage of the 2014 Congressional “cromnibus” spending bill, which included a provision barring federal backing for any mortgage seized through eminent domain. While the plan’s reliance on private investors may inure it somewhat to federal sanction, the cromnibus restriction has prompted national-level discussion about whether and how the plan can proceed without federal support.

Value in question

As highlighted in the “Introduction” section, the eminent domain plan has drawn sharply negative responses from mainstream financial institutions, and it is not hard to see why. What they see, in the most immediate and simplistic of senses, is the threat of being compelled to sell assets (mortgage debts) at a significant discount to the effective price paid for them (i.e. the quantum of the original loan provided, net of any principal repayments received), which is the price that contractually underwrites not only the amount of principal remaining to be repaid but also the level of ongoing periodic interest payments: a financial asset based on an original advance of $300,000, for example, to fund purchase of a $350,000 property, and on which no principal has yet been repaid, but now to be compensated by a redemption payment from a local municipality of only $250,000, the market price of the property having declined to that level. What they see, in other words, is value destruction.

Yet this “value,” and the nature of its purported destruction, is actually a far from straightforward matter. It rarely is: value is, in George Henderson’s (2004) felicitous phrasing, a “many-headed hydra.” How then might we productively make sense of this slippery thing called “value” in the mortgage eminent domain context? Four observations are essential.

First, it is critical to recognize that value is, here as elsewhere, a calculative and representative matter no less than an objective, material one. As episodes such as the LIBOR interest-rate-benchmark manipulation scandal have forcefully shown (Ashton and Christophers, 2015), representations of financial health, and of value metrics more broadly, are not neutral, passive re-presentations of independent financial realities—they shape the realities they describe, the very ability of institutions to generate and maintain value in the first place. Accounting standards are emblematic in this respect: they “influence the asset values they only pretend to measure” (Mügge and Stellinga, 2014: 2; original emphasis). It was thus predictable that as US house prices plummeted in the early months of the financial crisis, accounting standards became a hotly disputed matter. Banks that had been only too happy to conform to fair value accounting (FVA)—which shows assets, in this case mortgage debt, at current market values—during the boom balked at doing so as the market slumped, complaining that “FVA forced them to translate falling asset prices into losses even when they had no intention of selling the assets concerned” (Mügge and Stellinga, 2014: 12–13) and now arguing for historical cost accounting (which shows assets at acquisition value) instead.

Financial-sector opposition to the eminent domain plan must be read in the precise same light. It, too, would force banks and other institutional investors to confront asset-value losses when they have “no intention of selling,” preferring rather to—in the vernacular of the industry—“extend and pretend” the loans in question in the hope of market recovery. “Involuntary sales,” wrote one supporter of the plan (Miller, 2012), “would end fictitious valuations and require an immediate accounting loss.” Interpreting the financial industry’s resistance as, in the words of another commentator (Schaffer, 2014: 260), an “unwillingness to recognize losses that it has already incurred, but thus far has been able to mask,” the thrust of the critique of this resistance is hence that eminent domain would impact value as follows: it “would not cause losses but reveal losses” (Miller, 2012; original emphasis).

But this reading is clearly not quite right. Yes, accounting matters; and yes, involuntary sale at deflated values would reveal losses in the accounting thereof. It is not correct, however, to claim that losses have already been incurred, and nor, therefore, that eminent domain would not in some sense “cause” losses. The reason—and here we speak to a second crucial property of value under capitalism—is that for all the continuous, circulatory nature of the processes by which capitalist value is created, reinvested, and expanded anew, value for individual capitals is explicitly not continuous. It is a process punctuated by the radical discontinuities that are the events of buying and selling assets: moments when underlying movements in value are “fixed.” Notwithstanding declines in the prices of the properties on which they are secured, the “losses” nominally incurred by banks on distressed home loans are only “paper” losses until what the financial sector calls “liquidity events” definitively lock those losses in. So, if eminent domain would not actually—physically—cause losses per se, it would do more than just reveal them: it would cause losses to be realized.

This recognition, in turn, serves to highlight a third pivotal aspect of value. It is much more than merely “economic.” If the aforementioned underlying processes of value generation and reinvestment are shaped by extra-economic forces (as we widely recognize them to be: think “cultural economy” and, of course, “political economy”), then this is even more evidently the case when it comes to the question of those moments when value is “fixed.” Put it like this: if such moments are necessary for losses or gains to be realized, then who decides that the time to effect such a fixing has arrived, not to mention the quantitative level of the fixing? Sometimes the decision is mutual and voluntary, where buyers and sellers meet in “free” markets, agree a price, and lock in value oscillations accordingly. Often, though, the decision occurs very differently, and the eminent domain scenario would clearly be one such. Even if the amount of compensation paid to investors in the underwater mortgages would be “objectively” based on prevailing house-market prices, there would be nothing objective about the decision to fix. Value would—for the investor—be destroyed because the local state has decided that it has been. “Value” is, in this sense, overtly political. This, too, is to be expected: since such a fixing event would be, at its core, a (re)distributive event (value relations originally posited through loan origination being radically reposited, in new configurations, through forced loan redemption), it could scarcely be otherwise.

The political nature of value’s fixing had been equally in evidence during the above-mentioned period when falling house prices suddenly put accounting conventions in the spotlight. For, not only did the capitalist state—broadly conceived—lobby the International Accounting Standards Board (IASB) not to apply FVA (“pressure on the IASB was so intense,” note Mügge and Stellinga (2014: 13), “that, without due process, it amended IAS 39 in October 2008, suspending market-based valuations for many assets”). But, through its “independent” central banks, it did everything in its power to ensure that those losses in value being resisted representationally did not have to be substantively realized (fixed), either. In fact this, in large part, was what the “unconventional” monetary policy called quantitative easing initially was about: a politically inspired initiative not to compel the refixing of value ostensibly precipitated by declining US house prices. “What the actions of injecting liquidity ultimately entailed,” writes Paul Langley (2014: 53; emphasis added), “was the minting of base money, in the form of bank reserves, in order that the commodified debts which were circulating as assets in the global financial markets did not have to be liquidated.” (Value had not been destroyed, because it was decided that it had not been.) Or, in the words of Perry Mehrling (2011: 134), the US Federal Reserve, in purchasing swathes of mortgage-backed securities, was insuring “not the payments that the debtor had promised to make but rather the market value of the promise itself.” This distinction, and its signaling of for whom value was being insured, is critical.

And so we arrive at value’s fourth and final vital characteristic. Like all political fixings, the one we are primarily concerned with in this article—that ventured by Richmond et al, and summarily rejected by big finance—is necessarily discursively constituted. Narratives are pivotal insofar as forcibly locking-in and apportioning movements in value, or preventing this from happening, requires more or less overt explanations of rationale. We have already alluded to the fundamental case for invoking eminent domain, but it is the case against that is the more instructive here because not only does this narrative draw more categorically on legal arguments and on figuring of “the law’s markets” (cf. the “yes” campaign’s necessary appeal to public-use claims), but, viewed in historical context, it tells us much more about value in relation to contemporary financial capitalism.

Too big to fail (TBTF) or small enough to fail?

To appreciate this point, consider how the financial industry has fought back against the eminent domain proposals. Already by the end of the very month in which San Bernardino created its JPA, some 18 industry trade bodies—including the American Bankers Association, the Association of Mortgage Investors, the Securities Industry and Financial Markets Association (SIFMA), The Financial Services Roundtable, and the like—had come together to flatly decry the initiative. 5 The terms in which they did so are salutary. The plan, they insisted, both raised “very serious legal and constitutional issues” and “would also be immensely destructive to US mortgage markets.” Their concern, then, was for the integrity of the law and of the markets secured by law. The central legal issue here, it was claimed, was that the use of eminent domain would undermine “the sanctity of the contractual relationship between a borrower and creditor”, thus destabilizing not only (contract) law per se but the markets reliant on this contractual stitching. 6 SIFMA rehearsed this same narrative in even stronger terms in a letter sent by its president to the Federal Deposit Insurance Corporation (FDIC) two months later (Ryan, 2012). Stressing above all the inviolability of protecting market integrity, and railing against those (in California) who “have advocated solutions that would impair the foundations of mortgage finance by fundamentally changing the contractual relationship between borrower and lender,” President Ryan wrote: “We, at SIFMA, have always valued the FDIC’s focus on the importance of preserving market-based solutions to the stress in the housing markets.”

All of which would perhaps be more understandable, and would perhaps have attracted a more sympathetic reading from those outside the financial industry, were it not for the fact that it came hard on the heels of an episode during which a somewhat “looser” industry commitment to the integrity of markets, and of the laws securing their efficient operation, was in evidence, and which thus illuminates the contradictory nature of hegemonic law-and-market discourses. We refer here to the “rescuing” of the financial sector and its leading institutions, Lehman Brothers and selected others aside, at the height of the financial crisis. 7 Certainly, there were those who argued against a bail-out on the grounds that to rescue insolvent institutions was to interfere in normal market processes; markets, they said, should be allowed to do their work, and if this meant (more) financial institutions failing, then so be it. But such voices did not emanate from the financial sector itself. Rather, they issued from institutions—the likes of the UK’s Institute of Economic Affairs—really committed to “free” markets in a more-than-just-contingent way.

The financial sector, by contrast, opportunely put aside its professed insistence on “market-based solutions” to market stress. When the problem at hand was the solvency and survival of America’s financial institutions rather than of its ordinary householders, the industry was entirely comfortable with market norms being shelved and with government, backed by taxpayers (those same ordinary householders), stepping into the breach, as it did with the recapitalization-based rescue of American International Group. There was a stated rationale for such exceptions, of course, although interestingly not one ever accepted by free-market economists any more than by Marxians: that the institutions in question were “too big to fail.” But this rationale merely serves to highlight the stark normative disjuncture vis-à-vis the mortgage eminent domain scenario: that while major financial institutions must be rescued on account of being TBTF, ordinary householders do not need to be rescued for they are, individually and collectively, small enough to fail. This disjuncture is only rendered starker by the fact, easily overlooked, that the two scenarios in question—at-risk financial institutions on the one hand, at-risk homeowners on the other—are in fact two sides of the same coin, turning as they do on the same underlying set of problematic financial instruments: those “toxic” home loans, constituting assets for the former constituency and liabilities, in all senses of the word, for the latter.

The discursive contradiction between the two scenarios, meanwhile, extends further still. For, where the financial industry’s opposition to the use of eminent domain to arrest the foreclosure crisis is justified by a putative regard for the integrity both of markets and of the (contract) law sustaining them, its readiness to accept state support when it faced imminent crisis, in 2008–9, entailed a relaxed attitude to the laws of the markets as well as to the sanctity of markets themselves. In this case, however, the laws in question were not contract but competition (antitrust) laws. The latter, for more than a century, have been central to the ideology of market-based capitalism in the US: “free” markets demand effective competition laws; those laws maintain market freedoms and efficiencies precisely by identifying and rooting out “market power” (the power to manipulate, as opposed to obey, markets). But without a word of protest from the nominally market-preservationist financial industry, the US government’s antitrust rules were abruptly waived or relaxed at the height of the financial crisis to allow mega-mergers—Bank of America with Merrill Lynch, J.P. Morgan with Bear Stearns, Wells Fargo with Wachovia—that rode roughshod over market competition concerns (Christophers, 2013).

The bailout and eminent domain cases, in sum, have seen the industry display obverse standpoints on the sanctity of markets and market laws. As with accounting reform, the industry’s aim is precisely to preserve the value in and of financial institutions. In the case of eminent domain, however, the “public uses” recognized in case law allow for the entry of local government and community leaders to use their own extraordinary grievance to turn the law to quite different ends.

Risk

Resisting devaluation

In their ongoing attempts to stop the eminent domain plan in its tracks, the plan’s opponents have drawn upon strategies ranging well beyond the appeals to uphold market and legal integrity discussed in the previous section. They have, for instance, repeatedly pointed to difficulties associated with the fact that the loans targeted for seizure are typically securitized—such difficulties ostensibly being both logistical (how on earth to neatly extract individual, underwater loans from securitized bundles?) and legal (do the securitization trusts that represent the interests of the ultimate investors actually have the right to sell such loans, even under state compulsion?). They have also played a dubious social-conscience card: what about those poor folks, many of them in the working classes, with pensions invested in the loans now to be forcibly devalued? Perhaps most tellingly of all, however, they have made threats. One such has been the threat of costly litigation, for instance around the question of the “fair” value of compensation. But more important still have been veiled threats to redline—i.e. withdraw future mortgage financing from—any areas actually going ahead with the plan. This last threat has been made, more or less explicitly, by SIFMA (e.g. Medina, 2012), by its allies in Congress (see Zibel, 2012), and even by the Federal Housing Finance Agency (Benson, 2013).

What to make of such threats? It would be easy to suppose that the proposed exacting of such vengeance represents a disproportionate response. 8 Any exclusionary industry practices would potentially risk running afoul of redlining laws. 9 Moreover, the numbers of mortgages involved in the eminent domain plan—amounting to hundreds, not thousands, in Richmond, for example—scarcely seem to justify the intensity of the backlash.

If the financial industry and its supporters saw in the plan dangers only to value in the here and now, and only in the immediate locality of the plan’s mooted enactment, then regarding the redlining threat as an overreaction would perhaps indeed be justified. But this is not the case. The financial sector actually (correctly) perceives much deeper dangers to accompany the plan, and these explain much of its hostility. Such dangers relate not to devaluation of the specific mortgages targeted for seizure in the present but to the risk of comparable devaluation—on a much wider, indeed potentially limitless, scale—in the future. To understand the magnitude of this risk, it needs to be contextualized by reference to the finance sector’s own risk discourse.

Risk’s discourse

That the substantial rewards available to financial institutions and financiers reflect the taking and bearing of substantial proprietary risks is a sine qua non of the discourse of capitalist finance. That such risk-taking and bearing occurs in relation to mortgage finance, in particular, is alleged to be manifested in what became, from the early 1990s, the finance sector’s favored approach to segmenting US residential mortgage markets—the practice of so-called risk-based pricing. According to the theory of such pricing, lenders faced more significant risks in financing some borrowers than they did others. The level of such risk, crystallized in a notional probability of default, was seen to depend on borrowers’ qualifications, employment history, and the presence of certain “risk” factors (e.g. low income, poor credit scores, etc.). Risk-based pricing—charging higher rates of interest to more risky households—was presented as the industry’s rational, scientific approach to such risk. The need to adopt such an approach was prima facie evidence that the risk existed and was borne by banks.

There was and is an important geolegal component to this positing of the financial sector as substantive bearer of risk. And it is crucial in the present context because it has been brought to bear forcefully in regard to the eminent domain plan. Governments—local or national—may only exercise the power of eminent domain over property within their jurisdiction. If it is easy to “site” tangible property, however, what of intangibles such as mortgages? Where are mortgages legally located and hence whose jurisdiction do they lie within? “The only complication at all that is introduced into eminent domain analysis by intangible property,” writes Hockett (2012: 165), “has to do with the effect that intangibility has on state courts’ jurisdiction, since intangibles cannot be literally spatially ‘located’.”

The financial sector’s answer to this particular conundrum flows directly from its perspective on mortgage-finance risk and on the industry’s purported assumption thereof: since mortgagees—or, in the common securitization scenario, investors in the underlying loans—bear the risk (and price it accordingly), then it stands to reason that the law should “locate” the promissory note that is the mortgage debt coterminously with the risk attached to it. In other words, wherever the investor is located, so is the risk, and so also therefore is the intangible property that the likes of Richmond are trying to take. This, in any event, has been SIFMA’s legal argument, first formally supplied to it by advisors O’Melveny & Myers LLP in a memorandum written in July 2012 in response to the original San Bernardino proposal. Noting that the proposal “disavows any attempt to seize homes or physical property located in San Bernardino County, but instead asserts eminent domain authority over the promissory notes themselves,” and asserting that while “local property is pledged as security for the notes… it does not necessarily follow that the JPA’s jurisdiction over that property would give the JPA jurisdiction over the notes themselves,” the authors (Dellinger et al., 2012: 11–12) wrote that in “almost all” cases “the notes are not physically held in the County or even in the state – they have been sold and securitized, and now are held by document custodians for the securitizations in locations across the country.” As such, the notes “may be beyond the reach of the JPA’s powers of eminent domain.” A “California government entity should no more be able to confiscate notes held out of state than Los Angeles could confiscate a car parked in New Hampshire.”

If, in such ways, the financial sector figures itself as significant risk bearer, then the future-facing risks seen to be associated with the eminent domain plan can be—and are—weaved into the same narrative, viz.: These rogue local states are pushing even more risk our way, so we will have to do what we have always (rationally) done, which is to price for it. The particular risk that lenders see, of course, is essentially that of precedent and moral hazard (see e.g. Hallman, 2013). If one municipality goes down the eminent domain road, who is to say that others will not do likewise? Equally, what is to stop opportunistic homeowners simply defaulting intentionally on their mortgage payments in the hope/expectation that their local government will eventually step in, eminent domain power in hand, and bail them out? Either way, the future, post eminent domain exercise, looks much more risky, and needs to be priced differently than in the past. Redlining (withdrawing finance altogether) constitutes the ultimate price premium. But more modest premiums to compensate for the perceived increase of risk have also been mooted, with economists (e.g. Miceli and Pancak, 2013) dutifully on hand to model simulations of what this rational reconfiguration of risk-based pricing might look like.

In sum, the financial sector’s self-portrait, both in the years running up to the financial crisis and in the years since (when the eminent domain plan has materialized), is of an industry bearing and responding judiciously to significant, mortgage-related risk.

Yet, this still leaves us with a puzzle. Namely, why has the financial sector been quite so hostile to the eminent domain plan? After all, if the sector indeed bears and rationally prices risk, then surely the perceived increase in risk that would accompany use of eminent domain to seize mortgages could also simply be borne and rationally priced. Why the aggressive media campaigns to discredit the proposal and its protagonists, why the threats of litigation, why the furious lobbying of Capitol Hill (see DePillis, 2013)? Why, in short, would extension and modulation of existing risk-based pricing practices not suffice?

The answer, we argue, lies in the gap between discourses and realities of risk. In relation to mortgage finance, not only does the finance sector not always price in the ways its discursive figuration suggests, but neither does it bear risk to anything like the extent it claims. As such, a future featuring the threat of eminent domain-based mortgage seizure portends not simply greater risk so much as a qualitatively different risk calculus for the financial industry, one far removed from that to which the industry has historically become accustomed. Significant and poorly visible risk has historically been, and remains today, very much the exception for the industry rather than the rule, whatever its claims to the contrary; risk has been shouldered primarily by the industry’s counterparties, especially where mortgage finance is concerned. And, seen in this light, fierce resistance to meaningful harbingers of change to the existing risk calculus—particularly initiatives to shift the relative burden of risk toward the financial sector and to make such risk more normal and less exceptional—is entirely to be expected.

Risk’s reality: The financial exception

Consider first of all risk-based pricing per se. The practice as extolled by the finance sector turns out to be something of a caricature of the reality. As noted earlier, proponents of risk-based pricing maintain that the differences in the cost of home loans provided to different categories of customer are explained by the different levels of risk that lending to them ostensibly poses, which reflects in turn their objective individual risk profiles. But Wyly et al. (2009) argue that this is simply not the case. Lending patterns and costs during the height of the US subprime debacle, when “the share of African Americans pushed into high-cost loans shot up from 37% to 54%, and the share for Latinas and Latinos jumped from 25% to 46%,” cannot be satisfactorily understood, they submit, without explanatory recourse, at least in part, to processes of predatory pricing along race and ethnicity lines. “Even after accounting for a wide range of demand-side factors, African Americans and Latinas/Latinos approved for credit were still twice as likely as otherwise identical non-Hispanic whites to wind up with high-cost loans in 2006” (349). 10

The notion that financial institutions bear significant levels of proprietary

risk in relation to mortgage assets—whether they have priced them strictly

according to risk or not—is also highly problematic.

11

In this regard, the critical

calculative technology we need to understand is not risk-based pricing but asset

“risk weighting.” All regulated financial institutions are required to fund at

least part of their balance sheet with equity capital rather than debt. But the

amount of equity they must hold has conventionally been calculated as a

percentage—5, 10, or 15%, say—not of the simple total value of their assets per

se but of the total risk-weighted value of these assets. This

regulation reflects the fact that certain classes of assets are considered much

more risky than others. A loan to the US government might have had a zero risk

weight, for example, requiring no equity capital to be held; a loan to a

biotechnology startup would likely have had a high weight and thus require

significant equity financing. Amit Tyagi (2014) recently discussed risk

weights specifically for mortgages thus: When it comes to mortgages, the standard risk weight is 35% (down from

50% a decade ago). But banks can use internal mathematical models to

calculate their own risk weights. This is akin to marking one’s own exam

paper… Consider, for example, a $200,000 bank loan to buy a $235,000

home. If the bank attaches a 10% risk weight to the loan, the

risk-weighted equivalent is $20,000. If the amount of bank capital

needed to protect that risk-weighted equivalent is 10%, then the bank

requires just $2,000 of its own capital to fund the mortgage, $198,000

of which the bank itself borrows.

The skin, rather, is the home “owner’s”—and, of course, that of the taxpayer, who, in times of crisis, may be called upon to stabilize the accumulated pyramid of interlocking finance-sector debt obligations enabled by this attenuated regulatory approach to individual financial-institution risk assumption. But the fact that the risk burden of mortgage debt is borne primarily by the mortgagor is not a matter of risk weights and capital adequacy regulations alone. As Atif Mian and Amir Sufi (2014: 12) have shown, the relative “seniority” of claims on the underlying asset is also highly material in the event of house price declines and debt serviceability constraints, the mortgagee enjoying the “senior” claim to the homeowner’s “junior” one. The upshot of this particular risk configuration, Mian and Sufi maintain, is that financial markets palpably fail to fulfill what is ostensibly one of their main purposes—“to help people in the economy share risk.” By explicitly protecting banks and their creditors, our present financial system “concentrates risk squarely on the debtor,” with the home equity possessed by the mortgaged homeowner being “much riskier than the mortgage held by the bank.” Their conclusion? “The financial system actually works against us, not for us” (original emphasis).

Significantly—and, for opponents of the proposals to seize mortgage debts through eminent domain, troublingly—it appears to be the case that the law is effectively on Mian and Sufi’s side where the question of the location of the principal risk burden (and the mortgage debt crystallizing it) is concerned. As we have seen, SIFMA’s legal advisers have queried whether municipalities in California have the right to seize debts ultimately owned by investors situated in other jurisdictions; in their stated view, the main risk is borne by such investors, so the debt should perforce be legally sited with them. But their assessment was a cautious one. They argued (with emphasis now added) that securitized underwater mortgages “may be beyond the reach of the JPA’s powers of eminent domain”; that a California government entity “should no more be able to confiscate notes held out of state than Los Angeles could confiscate a car parked in New Hampshire.”

According to Hockett

(2012: 165), however, legal precedents firmly indicate otherwise; and

hence the caution shown by SIFMA’s advisers was justified. Hockett claims that

“in general, courts find the situs of a debt instrument to be

in the domiciliary state of the debtor, and the situs of real

estate mortgage debt in particular to be the state in which the mortgaged

property is itself located.” Moreover, where the mortgage debtor herself lives

in the mortgaged home (as required under the Richmond plan), the state enjoys both in rem jurisdiction over the debt

and the property securing it, and due process-consistent in

personam jurisdiction over the creditor/mortgagee, both of

these ultimately in virtue of the territorial jurisdiction it has over

the space in which the mortgagee and her home are respectively domiciled

and located.

To conceptualize this distinctive existing constellation of mortgage-debt risk distribution under contemporary financial capitalism, in turn, we can draw on the work of Philip Ashton (2011). Examining what he describes as two “signal” moments in the recent history of US mortgage markets—the late 1980s banking crisis and the post-2007 mortgage crisis—Ashton shows that something extremely telling happened in risk terms. Risk that was genuinely threatening to capital, in other (Ashton’s) words “system-threatening risk,” was rapidly isolated and sequestered. In the process, capital, and the regulatory bodies arrayed around it, was able to secure broader norms of risk creation and distribution which—from capital’s perspective—are, almost by definition, relatively non-risky. Ashton characterizes the distinctive orientation to risk signaled in these moments as “the financial exception.” It is an exception (wherein risk is the exception) that is ever present, but which needs to be actively invoked only in those “exceptional,” crisis-ridden moments when favorable risk-lite norms are rendered precarious.

None of this, to be sure, is entirely new. If we wind the clock back almost exactly a century, we find, in Thorstein Veblen’s Theory of Business Enterprise (1912), a penetrating if truncated analysis of how capitalism was already configured in such a way as to shift financial risk away from finance capital. Of course, Veblen was writing well before residential mortgage finance had begun to assume anything like the centrality to capital circulation that it enjoys today. But, if we substitute mortgaged homeowners for the nonfinancial corporations that Veblen considered in relation to finance capital (“traffic in vendible capital” being the phrase he used to refer to the latter’s work), then his account reads as an early figuring of precisely the type of risk calculus we are concerned with in this article. He makes three central points, all equally pertinent to the case in hand.

First, Veblen (1912:

166) maintained that the risk taken by finance capital was considerably less

material than commonly assumed: “What speculative risk there is in these lines

of business is incidental, and it neither affords the incentive to engaging in

these pursuits nor does it bound the scope of their bearing upon economic

affairs.” Those engaged in what he called “ordinary” (i.e. nonfinancial) lines

of business took just as much risk. Indeed, Veblen ventured that as near as one may confidently hold an opinion on so dark a question, the

certainty of gain, though perhaps not the relative amount of it, seems

rather more assured in the large-scale manipulation of vendible capital

than in business management with a view to a vendible

product.

Second, there was a very good explanation for why the risk assumed by finance

capital was less substantial than typically believed, and for why, as a result,

profit was more or less certain. The reason was simple: risk was systematically

transferred to counterparties, in Veblen’s case nonfinancial

corporations—“the manipulations involved in this traffic in vendible capital

commonly impose increased risks upon the business concerns engaged in industry.”

The business of the latter, he went on, is rendered more hazardous than it might be in the absence of this

financiering traffic in vendible capital. The manipulations carry risk,

not so much to the manipulators as such, as to the corporations whose

properties are the subject of manipulation.

(166–167)

Third, lastly, and “of prime importance” (both for Veblen and for us), the risks associated with such traffic in vendible capital displayed a further vital attribute which—for the traffickers, at least—rendered those risks tolerable and, pace Ashton, specifically not “system-threatening.” This attribute was their visibility: finance capital could, to a significant degree, envision and thus accommodate the risks occasioned by its activities. Veblen put it like this (167): “the manipulators have the advantage of being able, in great part, to foresee the nature, magnitude, and incidence of the risks which they create.”

So it is with mortgage finance today; and in the final reckoning it is this—for finance capital—highly propitious risk calculus that the eminent domain plan most fundamentally challenges.

The plan constitutes, in fact, the very antithesis of the inherently conservative “financial exception” delineated by Ashton. It is, for one thing, being mooted in theoretically non-exceptional times, after the worst of the financial crisis has (for the banks) abated, and as house prices are recovering; it thus threatens to sever the connection, crucial for the maintenance of the existing risk calculus, between crisis and market intervention (the latter being necessitated only by the former). Furthermore, it threatens to crystallize precisely the type of meaningful risk sharing between creditors and debtors that Mian and Sufi (2014) advocate, making risk the norm for finance capital—as it already is for mortgagors—by raising the enduring prospect of future principal write-downs. And it is this latter possibility, of course, that really changes the game: for if, pace Veblen, finance capital likes risk to be visible, calculable, and manageable (and thus not terribly risky), risk in an inherently uncertain post eminent domain world would be anything but.

Mortgage finance has long been banks’ bread and butter, whether in a simple originate-to-hold bank-based financial system or, latterly, in today’s originate-to-distribute, market-based, securitization-driven system. Indeed the slogan “safe as houses,” as Aalbers and Christophers (2014) observe, has only come to be associated with home ownership, and the putative financial security thereof, in recent decades. It originally referred, for reasons that should by now be obvious, to the relative risklessness of mortgage lending, the safety being that of the mortgagee, not the mortgagor; its transference to the locus of home ownership was an adulteration (and one that the financial sector was presumably all too happy to countenance). But if US municipalities succeed in seizing mortgage debts by eminent domain and revaluing them in the process, the landscape of risk associated with mortgage financing would potentially be changed for good. It would, we surmise, be “safe as houses” no more. “No wonder,” then (Miller, 2012), that “eminent domain mortgage seizures scare Wall Street.”

Concluding remarks

How scared should Wall Street actually be? The commentator who thus signaled Wall

Street’s anxiety—the then (now former) congressman Brad Miller—was equivocal. On the

one hand, he recognized (Miller, 2012) that America’s biggest banks have used their political power in Washington to defeat any

effort that would effectively reduce foreclosures, such as allowing judicial

modification of mortgages in bankruptcy, allowing a federal agency to use

eminent domain to buy mortgages, or providing teeth for the chronically

ineffective Home Affordable Modification Program, because those efforts

would also require the immediate recognition of losses on

mortgages.

We have to say, however, that we are considerably less sanguine than Miller. Granted, Wall Street’s power in Washington may have less direct salience to municipal than federal policy. But Wall Street is hardly impotent vis-à-vis the local politics of Main Street, either directly (given, for example, municipalities’ reliance on successful bond issues and, in respect of these, on favorable credit ratings) or indirectly—to discount the local implications of the finance sector’s power in Washington, after all, is to discount the power of the federal polity to shape municipal ones. In this context it is noteworthy that just five days after Miller’s opinion piece was published (in July 2012), it was reported in The Wall Street Journal (Timiraos, 2012) that the White House was skeptical of the San Bernardino plan. By the end of the year, as we have seen, that plan had been abandoned.

More broadly, we would return to the critical distinction we have made between value and risk. Value—in this case, the immediate threat of devaluation of a relatively small number of mortgage assets in a handful of localities—is one thing, and clearly something that the finance sector could comfortably handle. But risk—the risk of opening the door to wholesale reconfiguration of the entire risk calculus according to which mortgage finance is currently constituted—is another thing altogether. We expect that legislation and litigation will continue to place intense pressure on local governments whose eminent domain plans jeopardize that existing risk calculus. These plans, after all, strike directly at the prerogatives that the financial sector so assiduously and successfully defended during the financial crisis and in its aftermath, even in the shadow of catastrophe: that is, the right to structure and restructure the relationship between investment risk, asset values, and law to its exclusive benefit.

Footnotes

Acknowledgments

The authors who contributed equally to the research and writing would like to thank Sarah Knuth, Shaina Potts, Ben Teresa, and three anonymous referees for close and constructive readings of various drafts of this article, which helped significantly in improving it. The usual disclaimers apply.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.