Abstract

Recent decades have witnessed an increasing integration of developing countries into global value chains (GVCs). This growing participation in global production sharing has raised hopes for economic upgrading within such value chains. However, globalization has intensified international competition, and achieving economic upgrading is not an easy task. Moreover, the social consequences of participating in GVCs are not always positive; however, they have received considerably less attention in the literature. This paper suggests a simple and parsimonious approach to measuring economic and social upgrading (and downgrading) in GVCs. Applying this parsimonious methodology and using quantitative secondary data, we analyze how widespread upgrading has been in four selected manufacturing GVCs: apparel, wood furniture, automotive, and mobile phones. We also investigate to what extent downgrading is part of the reality and undertake a comparative analysis across GVCs, regions and country groups (developing vs. developed countries). We find that the promise of industrial upgrading through participation in GVCs does not materialize for everyone. Indeed, economic upgrading has taken place in just over a quarter of the countries in our sample, among them mainly developing countries. Finally, we examine the relationship between economic performance and social performance in the different GVCs to investigate whether or not economic upgrading is typically associated with social upgrading. While patterns differ across GVCs, we find that economic upgrading is more likely to occur simultaneously with social upgrading than without, and vice versa. Our analysis, thus, suggests that economic upgrading is conducive to, but not sufficient for, social upgrading to occur.

Keywords

Introduction

Facilitated by the liberalization of goods and capital markets and fueled by reductions in transportation and communication costs, the international geography of production changed significantly in the later decades of the 20th century as multinational corporations and lead firms increasingly offshored production processes and tasks. This has led to the emergence of transnational production networks and global value chains (GVCs) linking groups of producers across the world in order to supply markets in different countries.

It is commonly argued that this international fragmentation of production provides developing nations the opportunity of participating in global trade in a way that was not possible before. Developing countries are no longer required to develop capabilities to produce entire products and to directly compete with advanced nations, but can instead focus on specializing in certain stages of the production process. Indeed, the offshoring of production by lead firms has provided a stepping stone for developing country suppliers to integrate into the global economy and to enter the production of products that are more sophisticated than the goods they typically produce. Participation in GVCs is often seen as bearing potential for propelling economic development because, in addition to generating income, it can facilitate access to external and diversified markets, technology and knowledge transfer, and capability-building through learning.

However, participation in GVCs can also lock firms and countries in activities where they rely on low labor and production costs as their key competitive advantage with little value added and meager prospects for learning and spillover effects. In fact, lead firms often outsource those activities that are characterized by low skill and technology requirements and low entry barriers, which fuels competition among suppliers, making it difficult for them to capture value-added and raise profits and wages (Kaplinsky, 2005).

Therefore, in order to benefit from the opportunities offered by the globalization of production, firms and indeed entire industries within a country need to economically upgrade. The question is how widespread such economic upgrading really is and, in case it actually takes place, how beneficial it is for local producers and workers. This paper suggests a framework to address this question. Using a parsimonious approach, based on a narrow set of indicators and quantitative secondary and internationally comparable data, it looks at key exporting countries in four selected GVCs (apparel, wood furniture, automotive, and mobile phones manufacturing) and tries to gauge the extent to which economic as well as social upgrading have occurred during the past decade.

Such an approach enables us to make comparisons across countries (e.g. developing versus developed), regions, and GVCs. It, thus, allows us to provide a bird’s-eye view on economic and social upgrading in GVCs, which complements the existing case study literature and more detailed studies of individual value chains. It also enables us to undertake initial investigations on the relationship between economic performance and social performance. Is economic upgrading typically associated or correlated with social upgrading or not? Indeed, concerns are growing that the economic gains of integrating into GVCs do not necessarily translate into social improvements.

The paper is structured as follows: “GVCs and upgrading: Some critical considerations” section critically presents key conceptual considerations on GVCs and upgrading which provide the basis for our empirical investigations. “Methodology and selection of GVCs and countries” section describes the methodology used for the analysis. “Upgrading dynamics in the four GVCs” section presents the findings on economic and social upgrading trajectories for each GVC. “Comparative analysis across the four GVCs” section provides a cross-GVC analysis and focuses on the relationship between economic and social upgrading (where the concurrence of the two will be called “overall upgrading”). “Conclusions and critical remarks” section concludes and points to critical considerations and possible further research.

GVCs and upgrading: Some critical considerations

Earlier literature emphasized that participation in GVCs can offer firms in developing countries the chance to obtain access to new markets and technologies, and to acquire knowledge and information from lead firms (Gereffi, 1994; Pietrobelli and Rabellotti, 2006). However, participation itself requires firms to have or develop a certain degree of competitiveness.

Two broad trajectories can be distinguished: the low road and the high road to competitiveness. Low road is the trajectory of firms who are locked into low value-addition activities and who fight to stay competitive on the basis of their low costs, mainly achieved through squeezing wage rates and profit margins. High road is sustaining or improving competitiveness through innovation, increasing productivity, and enhancing quality (Milberg and Houston, 2005). In the GVC literature, the latter is typically referred to as economic upgrading.

In their seminal and widely cited work, Humphrey and Schmitz (2002) identified four forms of economic upgrading: i) process upgrading (increasing efficiency through the reorganization of production or introduction of new technologies), ii) product upgrading (the move towards more sophisticated or higher-quality product lines), iii) functional upgrading (increasing the range of functions performed or changing the mix of activities towards higher-value tasks), iv) inter-chain upgrading (capitalizing on capabilities acquired in one chain to enter another, technologically more advanced chain). These have become a standard reference in GVC literature.

However, this categorization of upgrading neglects other forms in which firms (or networks of firms) can increase—and have increased—their gains from participating in cross-border value chains. In an effort to include such other forms, Morris and Staritz (2014) introduce the concepts of channel upgrading (market diversification towards new buyers or new geographic or product markets 1 ) and supply chain upgrading (establishing or strengthening backward linkages within supply chains).

Yet, other strategies that firms have been using to enhance their competitive edge and their benefits from GVC participation can still not be captured by any of these six upgrading categories. Examples of such other strategies include efforts by firms to strengthen relations and coordination with other firms, to achieve economies of scale and scope (e.g. offering a portfolio of related products that differ in quality, for instance), to improve reliability and consistency of supply, or to increase flexibility and reduce lead times. In view of this, Ponte and Ewert (2009: 1639) criticize the conventional taxonomy and definition of upgrading types as too narrow and often imprecise. They point out, for example, that the categories of product and process upgrading do not “explicitly capture other venues of ‘doing things more competently’”. Furthermore, they argue that product and functional upgrading do not necessarily come with value addition and that improvements in production processes are not always about producing more efficiently (the focus of the process upgrading category) but can also be about enhancing compliance with technical and safety regulations and/or with private standards.

Meanwhile, Coles (2011) and Coles and Mitchell (2011) acknowledge that economic upgrading can also be driven by deepening horizontal coordination (i.e. intensifying collaboration between firms, e.g. through collective structures, within a functional node of the value chain to achieve a strategic balance between competition and cooperation) and vertical coordination (i.e. strengthening relationships between different functional nodes to move away from one-off spot transactions towards longer-term business relations) among GVC actors, highlighting yet another aspect of the wide range of upgrading possibilities.

The above examples of critical literature, thus, suggest an approach to economic upgrading that is both less normative (i.e. upgrading is not necessarily equated with ‘moving up the value chain’) and broader, whereby upgrading is more modestly about “reaching a better deal” (Ponte and Ewert, 2009) that balances rewards and risks and leads to more stable returns, e.g. through longer-term contracts and/or coordination (see also Gibbon, 2008). Such a “better deal” can even imply firms strategically deciding to go for what in the traditional GVC literature would be considered product downgrading if this allows them to secure a stable and profitable supplier position in the chain (Ponte and Ewert, 2009).

While the much appreciated efforts within the GVC literature to capture and reflect upon the complexity of firms’ actions to ensure competitiveness develop further, it seems the distinction between some of the terminologies becomes less clear-cut. In particular, does upgrading and becoming more competitive, for example, mean the same? The approach used in this paper will illustrate that it does not.

While earlier GVC studies focused on economic upgrading, the consequences of such upgrading on workers were significantly less researched, and are only recently receiving more attention. The term social upgrading is commonly used in the literature to describe improvements in the wellbeing of workers. In its broad sense, it encompasses both measurable standards (e.g. wages, type of employment, working hours, and social protection) as well as non-quantifiable aspects (e.g. enabling rights such as non-discrimination and harassment, freedom of association and empowerment) (Barrientos et al., 2011). Similarly to economic upgrading, the extent of social upgrading will largely be influenced by factors such as GVC governance, sector specificities, firm-level efforts, and public policies. Labor regulations and labor unions are also critical, as well as opportunities for acquiring new skills relevant for employment (Selwyn, 2013).

As international competitiveness depends at least to some degree on production costs, there is pressure on supplier firms to lower the cost of factors of production, which includes wages. Indeed, differentials in factor costs and regulatory stringency (e.g. on labor or environmental standards) are important determinants of lead firms’ decisions on the location of investment and production. In labor-intensive sectors, in particular, integration of developing country suppliers into GVCs is frequently driven by low wages as well as unstable employment arrangements and precarious labor conditions (Barrientos et al., 2011; Plank and Staritz, 2013). For this reason, concerns are growing that even where participation in GVCs yields economic benefits, these might not translate into new, better or more stable jobs. In the worst case, economic upgrading may be linked to degradation of working conditions and other forms of social downgrading (Gereffi, 2014), particularly for irregular and informal workers.

Case study literature has started to shed light on the relationship between economic upgrading and social consequences of GVC participation. Nadvi (2004) finds significant positive impacts on wages in the garment and horticulture industries across several countries, while Bair and Gereffi (2001) report improvements in labor conditions in the Torreon cluster in Mexico. In a study of the Moroccan garment sector, Rossi (2013) finds that process upgrading is associated with social upgrading, as increased efficiency in production leads to reduction in excessive overtime hours and improvements in labor (e.g. health and safety) standards. The relationship between product upgrading and social upgrading, she states, is less clear.

As suppliers are pressured by lead firms to maximize quality while reducing costs and ensuring flexibility and short lead times, different types of workers can have different experiences: For skilled workers, who ensure quality of production and who are employed under regular contracts, working conditions can improve while less skilled irregular workers, who ensure prices can be kept low and flexibility high, tend to experience social downgrading through low wages, precarious working conditions, or discrimination at the workplace (Barrientos et al., 2011).

To sum up, economic and social upgrading are complex, multi-dimensional and often contested processes. Economic upgrading can be understood as firms—or indeed networks of firms or entire sectors—embarking on a high road to competitiveness through productivity increases and quality improvements. 2 This is in contrast to a low road trajectory where firms try to compete on the basis of cost-cutting and profit-squeezing. Moreover, firms can also improve their gains from GVC participation through intensifying horizontal and vertical coordination and reaching better deals with other GVC actors. Economic downgrading, on the other hand, is associated with a loss of competitiveness. Meanwhile, social upgrading is often assumed to be a side effect or almost automatic consequence of economic upgrading but research on this topic has begun only recently. Case studies show mixed results but suggest that in some cases economic upgrading is associated with social upgrading; however, a systematic investigation is still missing. These critical conceptual considerations and initial case study findings form the backbone of our methodology and the empirical analysis to follow.

Methodology and selection of GVCs and countries

This paper analyzes economic and social upgrading in four GVCs and for over 30 countries in each GVC to provide a broader picture of upgrading trends and shifts. With this we aim to scale up the scope of analysis which until now has predominantly been that of individual case studies. While this clearly means that many of the details that in-depth case studies can provide on individual experiences are lost, our approach allows us to identify upgrading dynamics and patterns across GVCs and countries from a bird’s-eye view. In order to facilitate the assimilation of such a large quantity of information, the paper adopts a parsimonious methodology using country-level data which is quantifiable and internationally comparable. We therefore view our paper as complementing the case study literature, and vice versa.

Economic upgrading

As part of our parsimonious approach, we follow Kaplinsky and Readman’s (2005) and Amighini’s (2006) definition,

whereby a country has experienced economic upgrading in a

given GVC if it: (1) increased its export unit values

3

relative to the industry average,

and (2) increased its world export market share.

Conversely, a decline in both indicators is interpreted as economic downgrading within the respective GVC. Export unit values are commonly used as surrogates for prices and, consequently, as proxies for product quality (Aiginger, 1997). We use the growth differential between a country’s export unit values and the global industry average as one indicator. This gives a better idea of performance relative to the world average and, in a sense, allows us to take account of sectoral inflation (e.g. price increases of inputs that affect producers worldwide). 4 In principle, however, an increase in (relative) export unit values can be the result of rising production costs rather than successful upgrading (reflecting, for example, inefficiencies in production or an increase in the technology gap relative to the frontier). For this reason, we use the change in world export market shares as a complementary indicator in our analysis. In order to capture the dynamic nature of upgrading (or downgrading) as a process, it is essential to look at changes in these complementary indicators over time. 5

In “Upgrading dynamics in the four GVCs” section, we use this parsimonious approach to

map countries’ upgrading performance in 2 × 2 scatter charts (with one of the two

indicators plotted on each axis, respectively) which allows us to group countries into

four types of upgrading performance (see Figures 1, 3, 5, and 7). Countries appearing in the upper-right quadrant

of these scatter plots are deemed economic upgraders. However, while the indicators allow

us to observe the outcomes of economic upgrading processes,

they do not reveal which of the different upgrading forms actually led to this performance

outcome. Simultaneous progress on the two indicators might reflect product, functional,

process, channel or supply chain upgrading (or a mix thereof) or, more broadly, instances

of “reaching a better deal”, as described in “GVCs and upgrading: Some critical

considerations” section.

6

Meanwhile, countries located in the lower-left quadrant of these 2 × 2 scatter charts are

classified as downgraders.

7

The remaining two quadrants will show the “intermediate cases” which

have experienced progress on one indicator but decline on the other. These include

countries that have improved their competitiveness, as reflected in increased world export

market shares, while decreasing relative unit values, possibly indicating either a low road to competitiveness or successful process upgrading and

other firm-level achievements with similar effects (such as improved horizontal and

vertical coordination within GVCs, increased economies of scale and scope, or enhanced

reliability and consistency of supply). Our methodology, thus, allows us to broadly

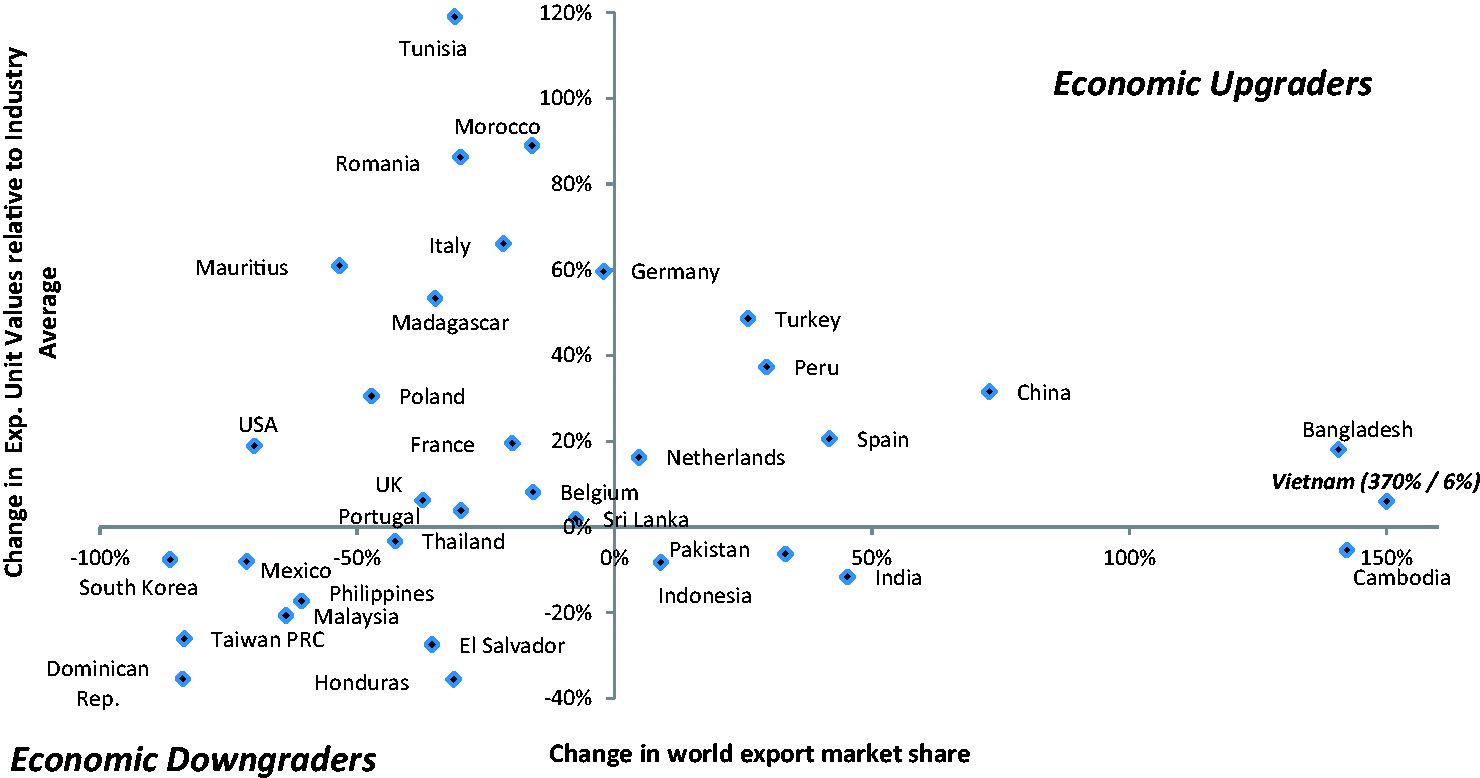

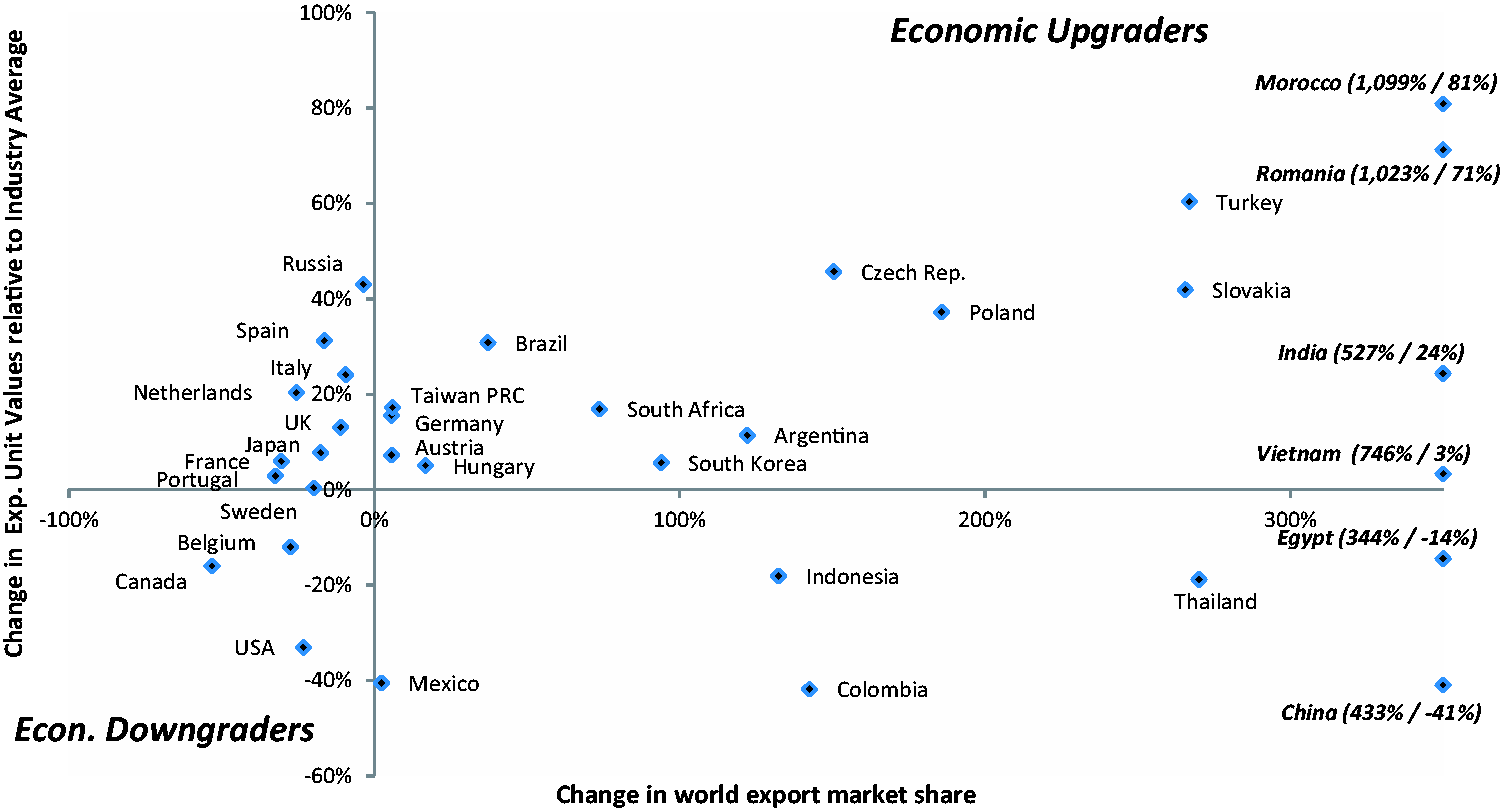

capture different instances of competitiveness improvements and upgrading. Economic upgrading and downgrading in the apparel GVC

(2000–2012). Note: In all graphs, countries written in bold and italic letters are

outliers which were relocated within the graph to enhance legibility with figures in

parentheses being the actual values. Source: UNCOMTRADE

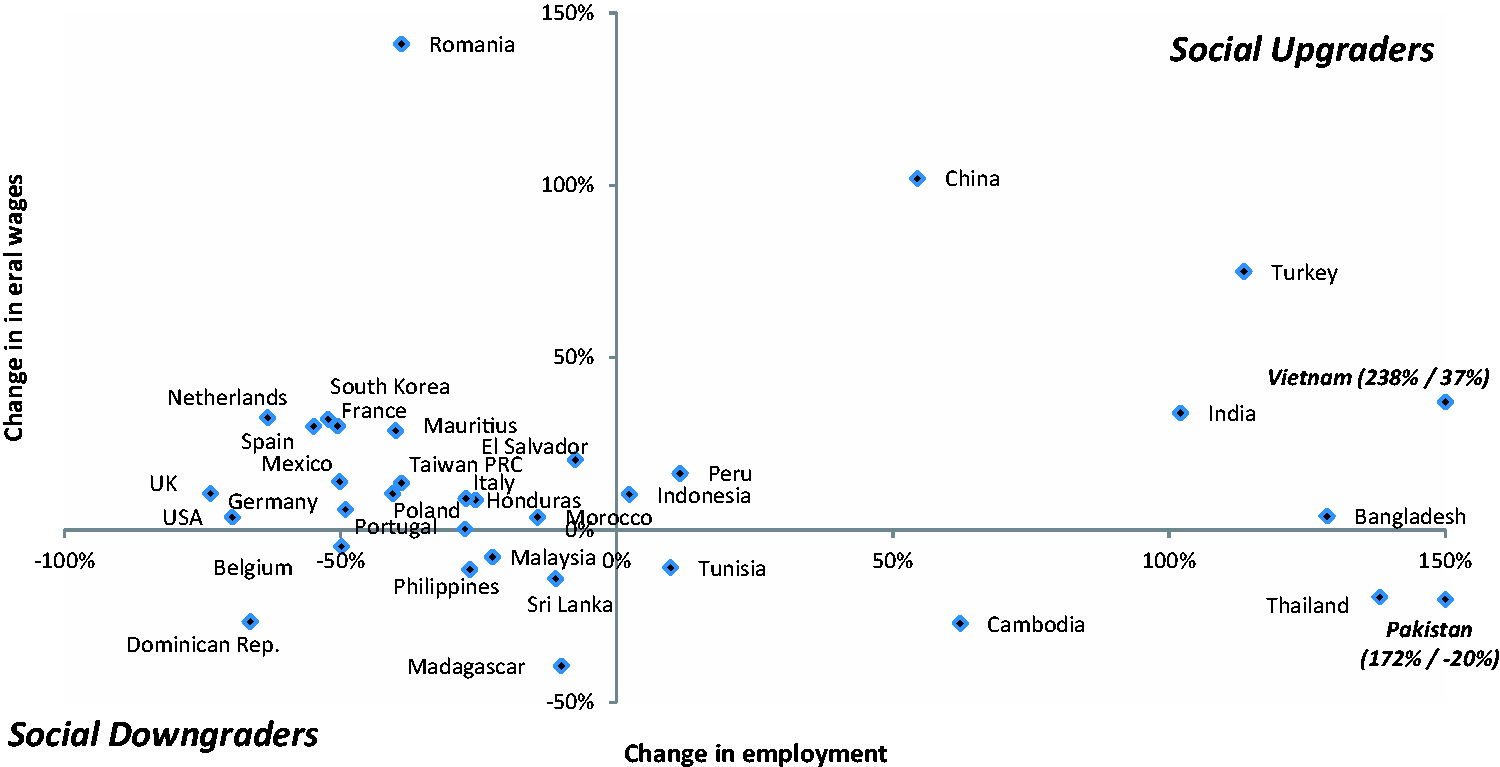

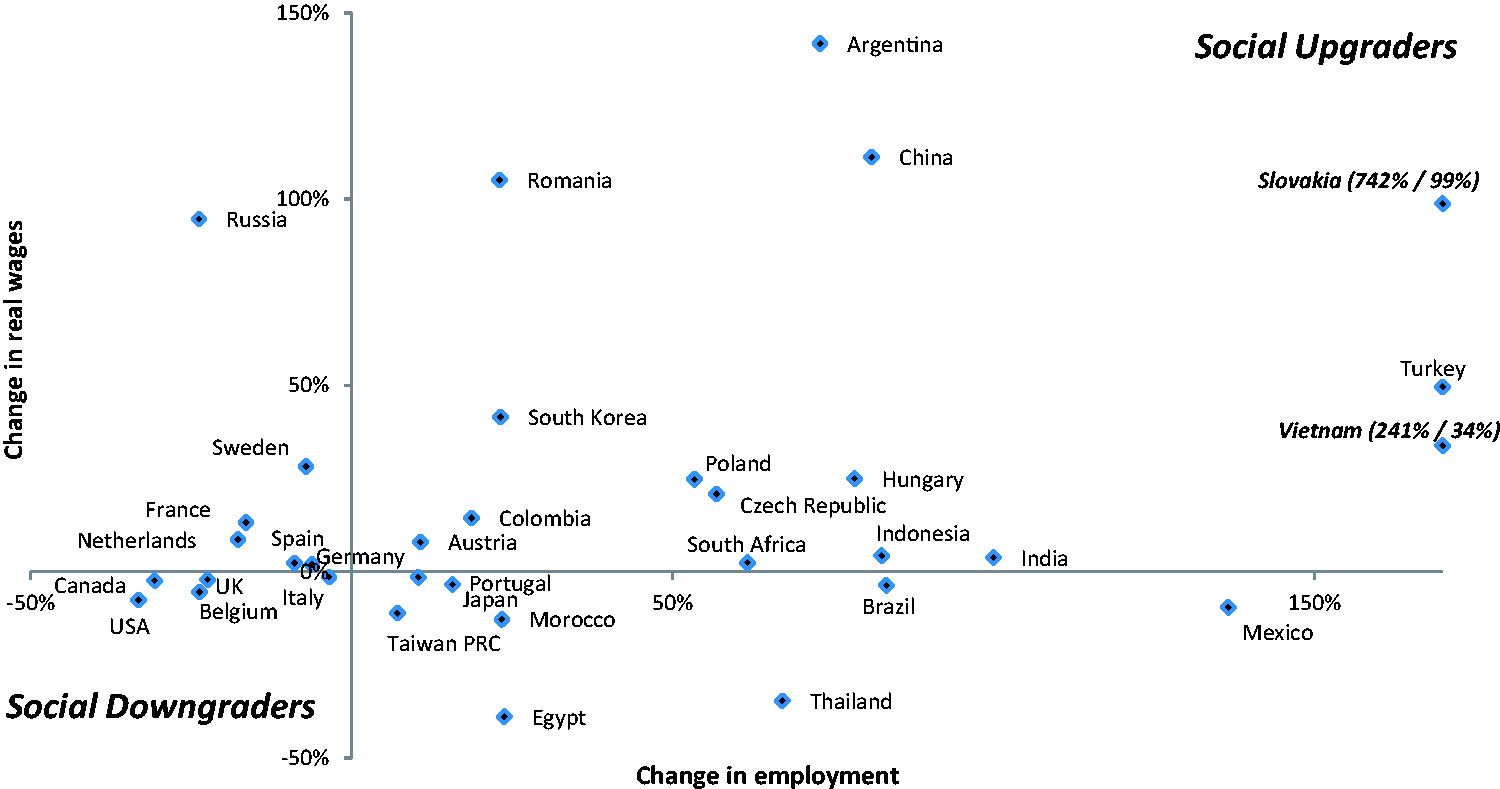

database. Social upgrading and downgrading in the apparel GVC (2000–2012).

Source: UNIDO INDSTAT4 and World Bank Global Economic Monitor (GEM) databases,

Taiwanese Directorate-General of Budget, Accounting and Statistics (DGBAS), Institut

National de la Statistique (INS) de Tunisie. Economic upgrading and downgrading in the wood furniture GVC

(2000–2012). Source: UNCOMTRADE database. Social upgrading and downgrading in the wood furniture GVC

(2000–2012). Source: UNIDO INDSTAT4, UNIDO INDSTAT2 and World Bank GEM

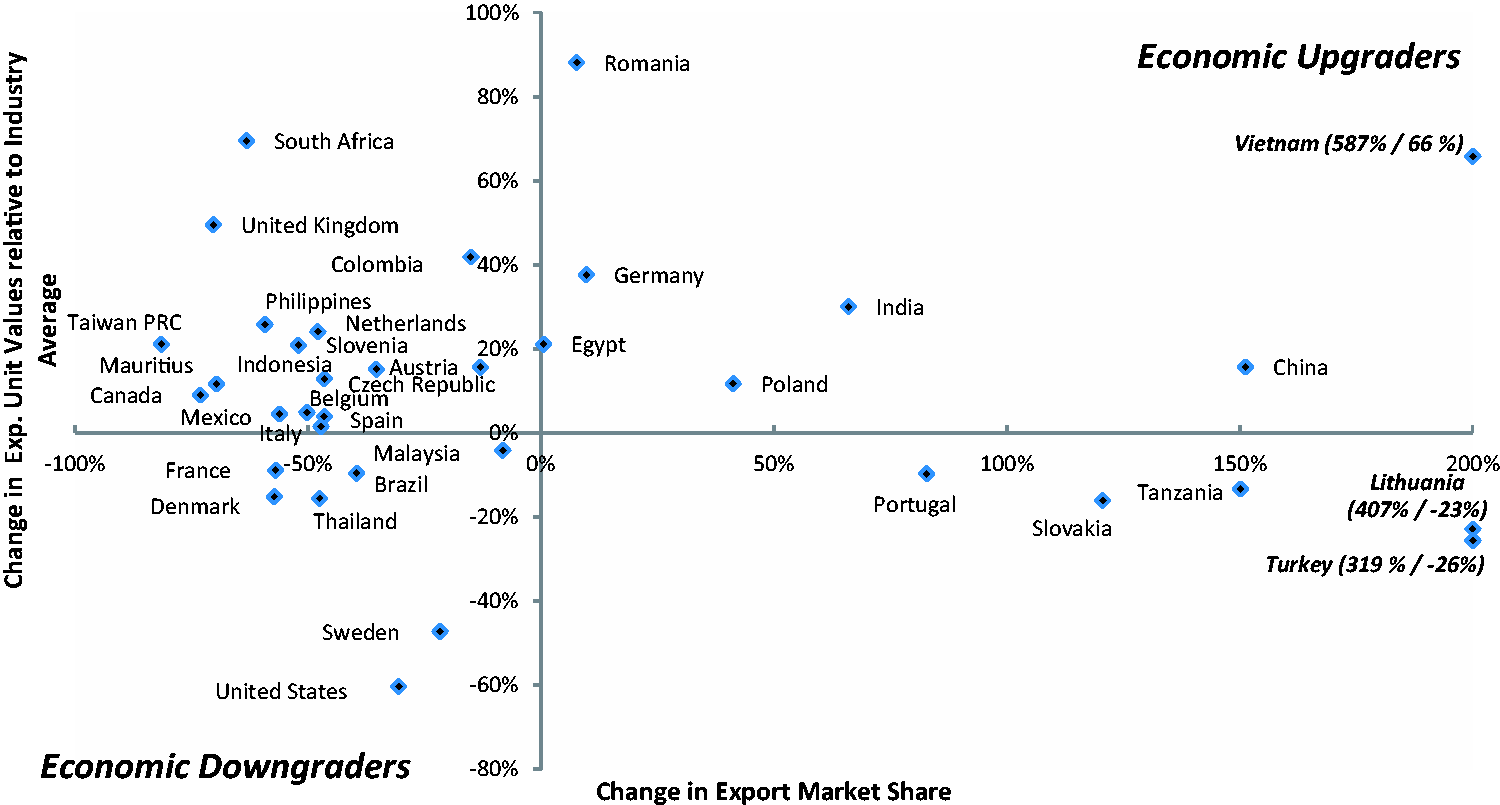

databases. Economic upgrading and downgrading in the automotive GVC

(2000–2012). Source: UNCOMTRADE database. Social upgrading and downgrading in the automotive GVC

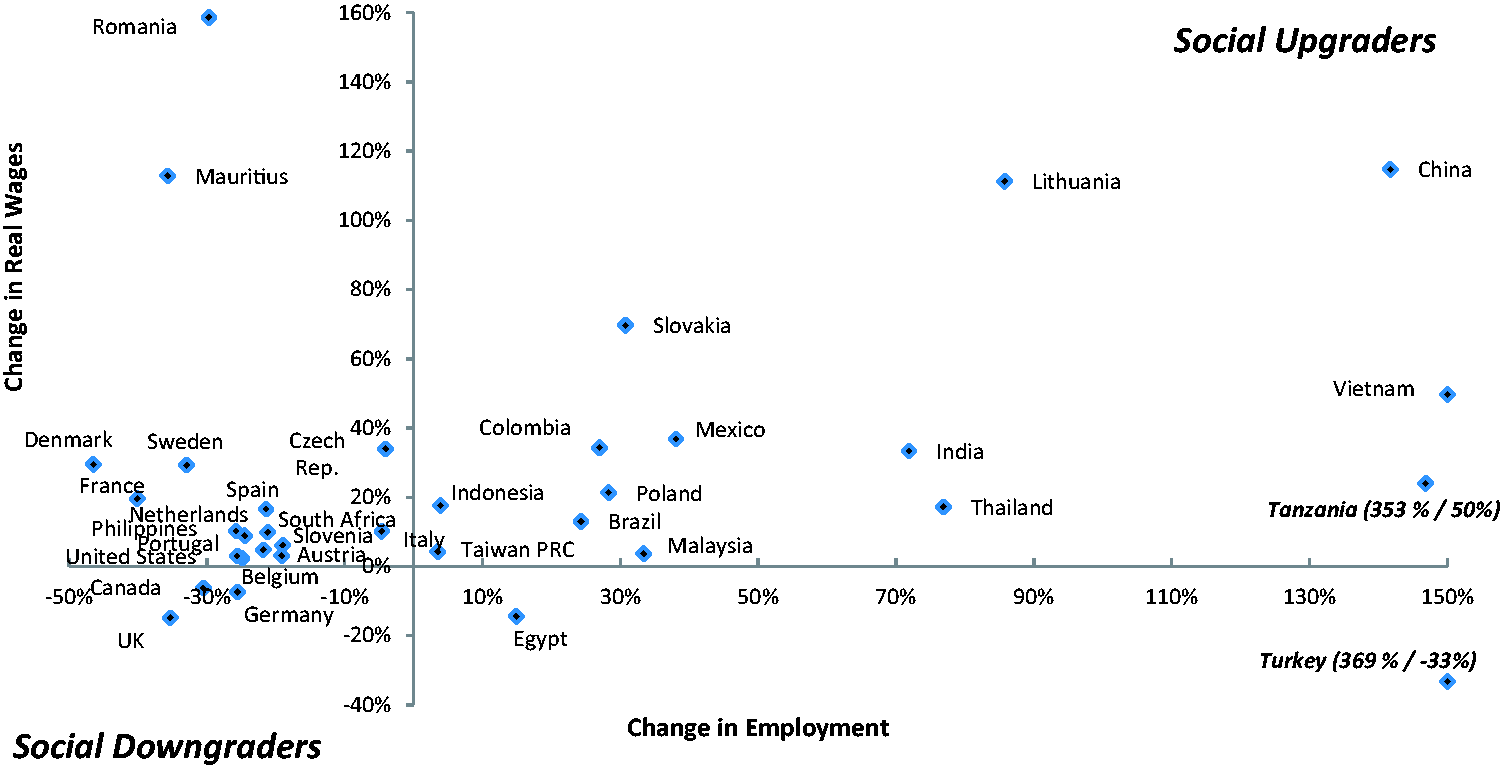

(2000–2012). Source: UNIDO INDSTAT4 and World Bank GEM databases, Ministerio de

Trabajo, Empleo y Seguridad Social (Argentina), Institutul National de Statistica

(Romania), Taiwanese DGBAS. Economic upgrading and downgrading in the mobile phones GVC

(2000–2012). Source: UNCOMTRADE database.

Social upgrading

Following Bernhardt and Milberg

(2013), a country is defined to have experienced social

upgrading in a given GVC when there was a combination of: (1) an increase in employment and (2) an increase in real wages.

Through the creation of jobs, labor is given the possibility to earn an income, and, if they are formal, may provide social insurance and certain employee benefits. Real wages, on the other hand, can be used to measure how much workers benefit economically from the value created by GVC-related production in their country. This is clearly an oversimplification of the concept of social upgrading as it looks at only two of a long list of possible indicators for measuring it, and while real wages may be associated with quality of employment, they are too weak an indicator to draw any wider conclusions about improvements in overall working conditions (such as hours of work, freedom of association, safety at work, etc.). Unfortunately sector-level data on working conditions and labor standards are generally not available in an internationally comparable manner. The data required for the two indicators we adopt, however, are more widely available and hence allow for cross-country comparisons. In line with the economic analysis, these two indicators will be used to plot countries’ social upgrading performances in 2 × 2 scatter diagrams.

An important caveat which needs to be emphasized is that these data typically do not cover the informal sector and do not sufficiently account for irregular employment like temporary or contractual work (where working conditions and pay are usually worse than in regular jobs). As a result, they exclude a large segment of workers, particularly in developing countries. Given this lack of reliable data on irregular employment, we do not know whether social upgrading/downgrading is accompanied by a rise or fall of precarious jobs. 8

GVC selection and country samples

The parsimonious approach outlined above is used to analyze the upgrading dynamics in four manufacturing GVCs: apparel, wood furniture, automotive, and mobile phones. This selection was made in order to cover a spectrum of GVCs with different degrees of technological sophistication, ranging from what are usually considered low-tech (apparel, wood furniture) to mid-tech (automotive) and high-tech sectors (mobile phones). Additionally, it allows us to cover differing governance structures, as both buyer-driven (apparel, wood furniture) and producer-driven chains (automotive, mobile phones) (see Gereffi, 1994) are analyzed. Moreover, all four sectors have globalized rapidly in recent decades, experiencing dynamic cross-border trade and a relatively high degree of developing country participation. While these GVCs also involve non-manufacturing activities (including R&D, product design, logistics, branding and marketing), our analysis focuses on the manufacturing segment of these chains. 9

In each of these GVCs, we analyze the 25 countries with the largest world market shares in 2012 to cover the most important supplier countries. However, in order to avoid a selection bias towards “winners” or “economic upgraders”, we also added those countries that were among the top-25 world exporters in the year 2000 (but no longer in 2012). Finally, to ensure a certain regional balance, we added the most important supplier countries of each region that was not or under-represented. In total, this resulted in a sample size of around 35 countries for each GVC.

Upgrading dynamics in the four GVCs

This section provides an analysis of economic and social upgrading and downgrading dynamics over the last decade in the four GVCs of interest. For each GVC, we look at the group of countries in each quadrant of the economic upgrading graphs and discuss how these countries have been doing on the social front during the same period. This will allow us to identify interesting upgrading patterns but also to already shed some light on the relationship between economic and social upgrading (downgrading) in the individual GVCs.

Apparel GVC

In recent years, the geography of apparel manufacturing has changed and the supply of apparel products has become increasingly concentrated in a few countries and regions, those being mainly East, Southeast, and South Asia. 10 This trend was accelerated by the expiration of the Multi-Fibre Arrangement (MFA) in 2005, which had governed international garment trade since 1974, as well as by the global economic crisis that started in 2008 (Gereffi and Frederick, 2010; Lopez-Acevedo and Robertson, 2012).

This shift towards the East can also be seen in Figure 1, which shows countries that have gained world export market shares at the right-hand side of the vertical axis. Seven countries have managed to combine these market share gains with export unit value growth in excess of the world average and, thus, to economically upgrade between the years 2000 and 2012. This group is dominated by Asian countries (China, Bangladesh, Vietnam, Turkey) but, interestingly, also includes two advanced economies (Netherlands, Spain) besides Peru. Have these countries that have experienced economic upgrading also improved in terms of social outcomes? Figure 2 shows that five of these countries (all but Netherlands and Spain) were indeed able to increase both employment and real wages in the apparel sector, i.e. to socially upgrade. The two European countries have had a reduction in jobs in the sector while increasing wages for those remaining, probably indicating improvements in productivity.

Four countries—all of them Asian economies—have increased their market shares while decreasing relative unit values. Two of them (India and Indonesia) experienced social upgrading (see Figure 2). The two other countries in this group (Cambodia and Pakistan) have seen an increase in apparel employment but a drop in real wages. This might indicate that they have gone down the low road to competitiveness whereby their participation in GVCs has allowed them to gain access to markets but without undergoing much economic upgrading and rather by pushing down prices. The social performance of India and Indonesia, on the other hand, might be an indication that they have achieved some degree of process upgrading with efficiency gains in production helping to lower costs and improving competitiveness which then translated into favorable social outcomes. Alternatively (or in addition), it could be a sign that Indian and Indonesian apparel firms have sought to enhance their market presence by increasing exports despite experiencing decreasing prices, or that they pursued channel upgrading where a shift of end markets led to lower-priced exports. The observed growth in the volume of exports may, in turn, have allowed employment and wages to increase. Case studies can help to clarify which trajectory a given country actually followed.

In contrast to the countries mentioned so far, 23 countries of our sample were unable to increase world market share in the apparel sector. Fourteen of them have combined an increase in unit values with a decrease in market share, showing up in the upper-left quadrant of Figure 1. This group includes many high-income countries, along with all the African countries in our sample, as well as two Eastern European countries. While some of these countries may have been facing increasing costs or have become comparatively less efficient in production, therefore losing competitiveness in international markets, other countries may be focusing on high-value products within the apparel sector as they enter niche markets. When looking at Figure 2, we see that 10 of the 14 countries undergoing this trajectory have increased real wages while shedding jobs in the sector. These are mainly the more developed countries of our sample, suggesting that this reflects a move out of apparel production as part of structural change processes.

Figure 1 reveals that nine countries actually experienced economic downgrading in the apparel GVC, those being Central American and Caribbean countries (Dominican Republic, El Salvador, Honduras, Mexico) as well as newly industrializing economies and late industrializers in Asia (Malaysia, Philippines, South Korea, Taiwan Province of China (PRC), Thailand). While it may be the case that firms, especially within this latter group of countries, have simply not succeeded in upgrading their production, it is likely that some of these economies are undergoing structural change towards sectors of higher value addition, making the downgrading within the apparel sector not necessarily a negative experience for the economy as a whole. Among the nine economic downgraders, five have experienced increases in real wages and decreases in employment while there are also three cases of social downgrading.

Looking briefly at the relationship between economic and social performance in the apparel GVC we find that economic upgrading has more commonly gone hand in hand with social upgrading than without, and it is always associated with an increase in real wages for the (formal) workers. Furthermore, among our sample countries there are more cases of what we will call “overall upgrading”, i.e. a combination of both economic and social upgrading, than overall downgrading. However, the majority of the countries have not upgraded on either front.

Wood furniture GVC

Similar to the apparel GVC, the global wood furniture sector has seen a certain degree of concentration in production throughout the past decade as well as a shift from Western Europe and North America eastwards, particularly to China (see also Kaplinsky and Readman, 2005), which increased its world market share from 14% to 33% between 2000 and 2012.

Looking at Figure 3 we notice that seven of the 35 countries in the sample (a fifth) have undergone economic upgrading, therefore having succeeded in moving along the high road of integrating into the wood furniture GVC. All these cases are emerging economies with the exception of Germany. Roughly half of them (four of the seven), namely all the Asian economies of this group and Poland, have also enjoyed social upgrading (with increases in both real wages and employment; see Figure 4). The remaining three countries have had varying social performances.

The lower-right quadrant of Figure 3 shows that five countries have increased market share and decreased relative unit values in the wood furniture GVC. This possibly reflects achievements in terms of process upgrading, which may indeed have been the case in the three countries that at the same time have experienced social upgrading (Lithuania, Slovakia, Tanzania). Channel upgrading or expanding export volumes based on mass production are also possible explanations for this performance. In Turkey, by contrast, employment increased while wages decreased, suggesting it went down the low road to competitiveness based on cost-cutting.

Just like in the apparel GVC, the majority of countries went through an economic trajectory whereby they have increased unit values relative to world average while losing world market shares (16 countries; see Figure 3). The countries within this group are either developed or industrializing nations. Half of these countries (the majority of them developed countries) have seen real wage increases with a contraction of employment opportunities in the sector (see Figure 4). This again, can be an indication of specialization within the GVC on the export of products that are of higher value, rather than failed upgrading. Five other countries in this group have experienced social upgrading (despite world market share losses) while the remaining three were social downgraders.

As Figure 3 shows, there were as many economic downgraders as there were economic upgraders in the wood furniture GVC, namely seven, of which four are developed economies. All four developed economies saw employment decrease and real wages increase. The remaining three economic downgraders (Brazil, Malaysia, Thailand), surprisingly, managed to upgrade socially.

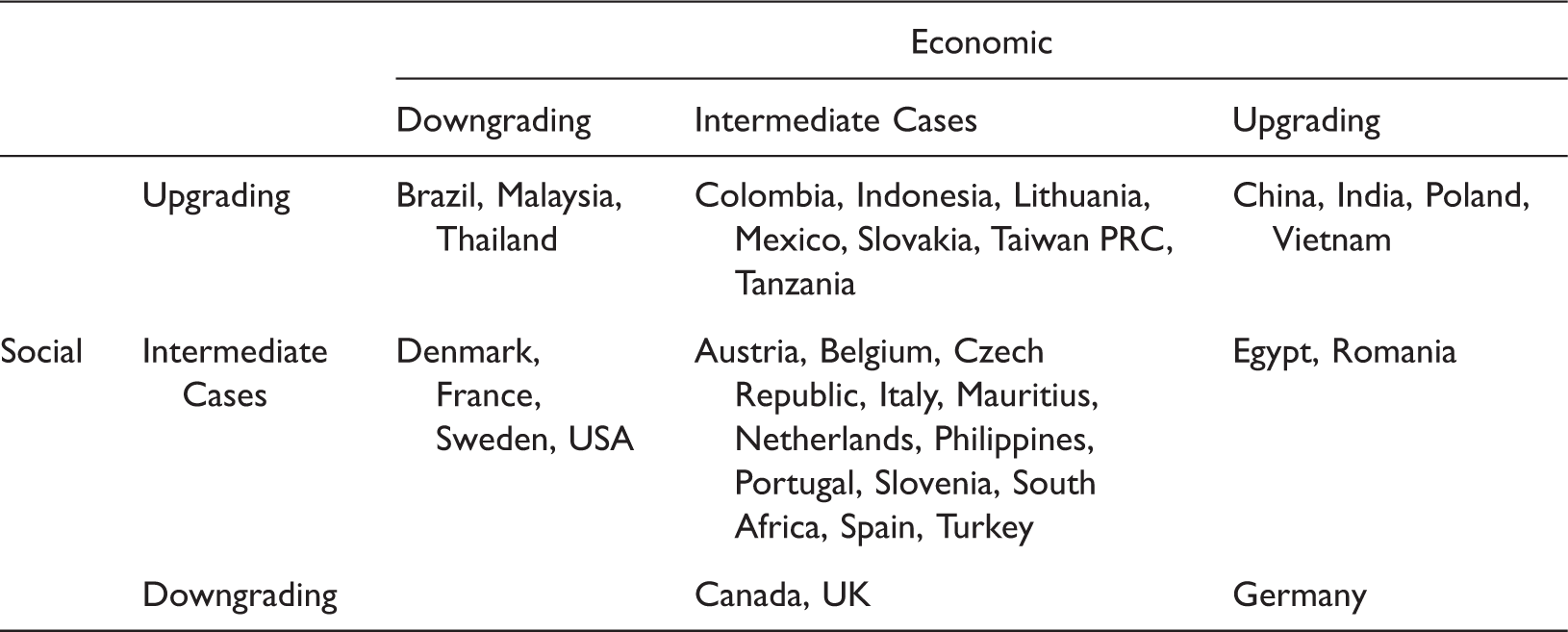

To sum up, in our sample there are four cases of overall upgrading (China, India, Poland, Vietnam) where economic upgrading and social upgrading occurred side-by-side, while there are no overall downgraders. More surprising, however, is that there are twice as many countries that have managed to upgrade socially (all being developing countries) than upgrade economically in the wood furniture GVC. While none of the social upgraders were developed countries, Germany is the only developed economy that has managed to economically upgrade. More generally, there seems to be less correlation between economic and social upgrading in the wood furniture GVC than in the apparel GVC examined above.

Automotive GVC

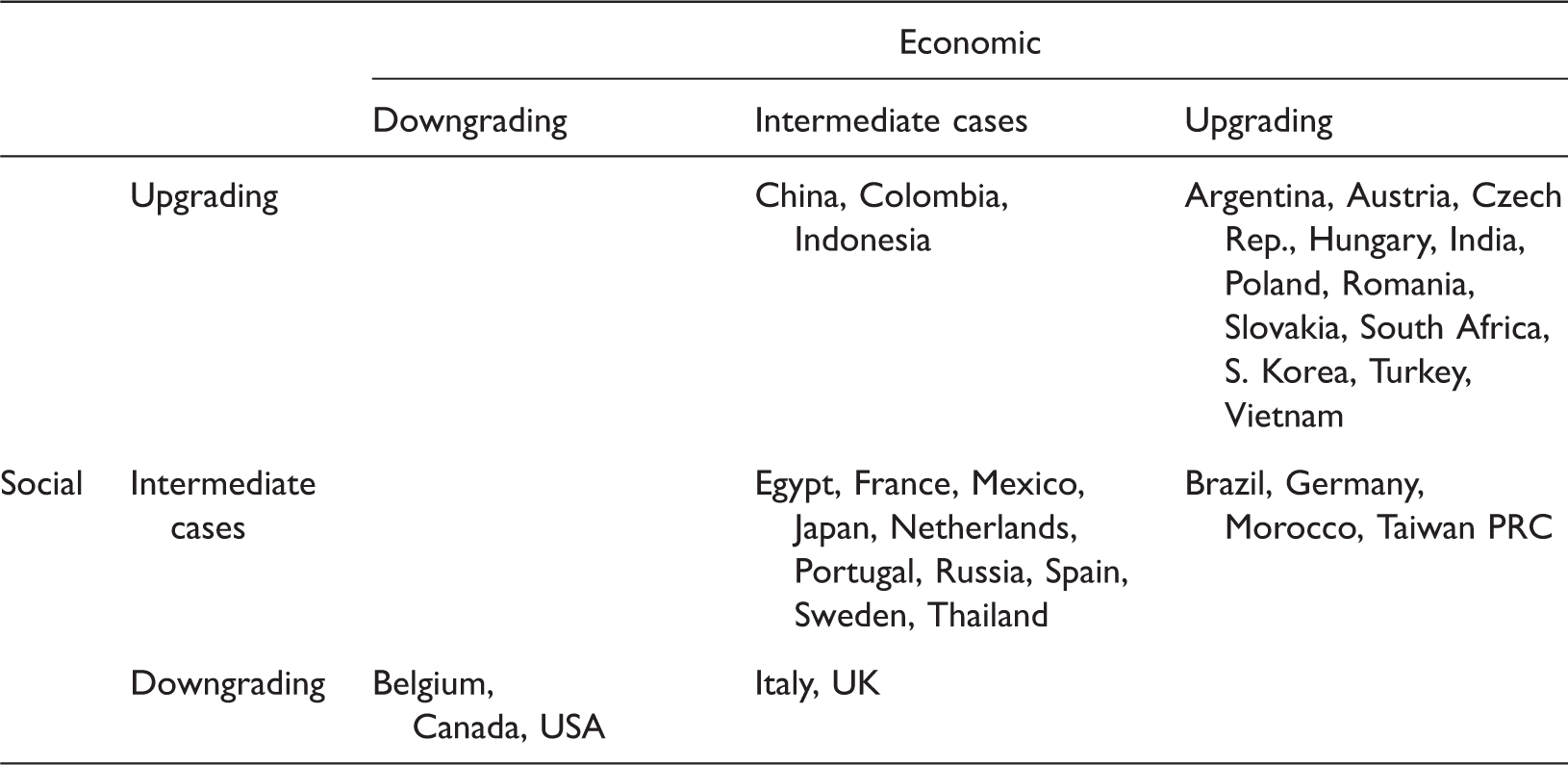

The automotive GVC is the only value chain within our analysis where we did not see a trend towards concentration and where the industry expanded across more countries. In particular, developing countries and emerging markets were able to enhance their importance as producers and suppliers in the automotive GVC. These geographical shifts have been motivated not only by lower operating costs in these countries and their proximity to (high-income) end markets but increasingly also by the intention to conquer the dynamic domestic markets of large emerging economies (Sturgeon and Van Biesebrock, 2011). However, while we are seeing increasing participation of developing countries in this GVC, production and trade are still dominated by (lead) firms from advanced economies in North America (USA, Canada), Asia (Japan), and Europe (Germany, France, UK, Spain, Italy). At the same time, the recent global economic crisis has accelerated pre-crisis trends of shifts in the geography of automotive production towards the developing world so that the future might see a dwindling of Northern countries’ predominance (Sturgeon et al., 2009).

Indeed, all advanced economies in our sample except Austria and Germany lost world market shares. In fact, all the 12 countries in our sample that lost world market shares are developed economies. Nine of these still increased relative unit values of their automotive exports (see upper-left quadrant in Figure 5) which might reflect losses in competitiveness but is equally likely to reflect processes of structural change whereby lower-value manufacturing activities are offshored while specialization in higher-value automotive exports increases. Among these nine countries with increased relative unit values and market share losses, five saw employment losses but real wage increases (again, supporting the positive structural change argument), two were social downgraders while the remaining two increased employment but reduced real wages (see Figure 6).

Examining economic upgrading trends more specifically, we find in Figure 5 that almost half of the countries in our sample (16 out of 34) qualify as economic upgraders. Eleven of these (practically two-thirds) were also social upgraders, implying that they have embarked on a high road to integrating into the automotive GVC. Such cases where economic and social upgrading took place simultaneously were found across the globe with no clear domination of any region, and for countries at different stages of development (developed, emerging or developing). The relationship between economic and social upgrading therefore seems very strong in the automotive GVC, significantly stronger than in the other GVCs.

Meanwhile, six countries gained world market shares but experienced a decrease in relative export unit values (see lower-right quadrant in Figure 5), including Latin American and Asian countries as well as Egypt. While half of them were social upgraders, the other half was only able to increase employment and had a reduction in real wages. The latter can be expected for countries that follow the low road as they need to squeeze prices to stay competitive.

Three countries were economic downgraders: Belgium, Canada, and the USA. All three also experienced social downgrading in the automotive GVC. This is another indication that economic and social performance are quite strongly related in this GVC – which is again reinforced by the fact that the automotive GVC had the most cases of overall upgrading (the combination of economic and social upgrading) among all four GVCs examined.

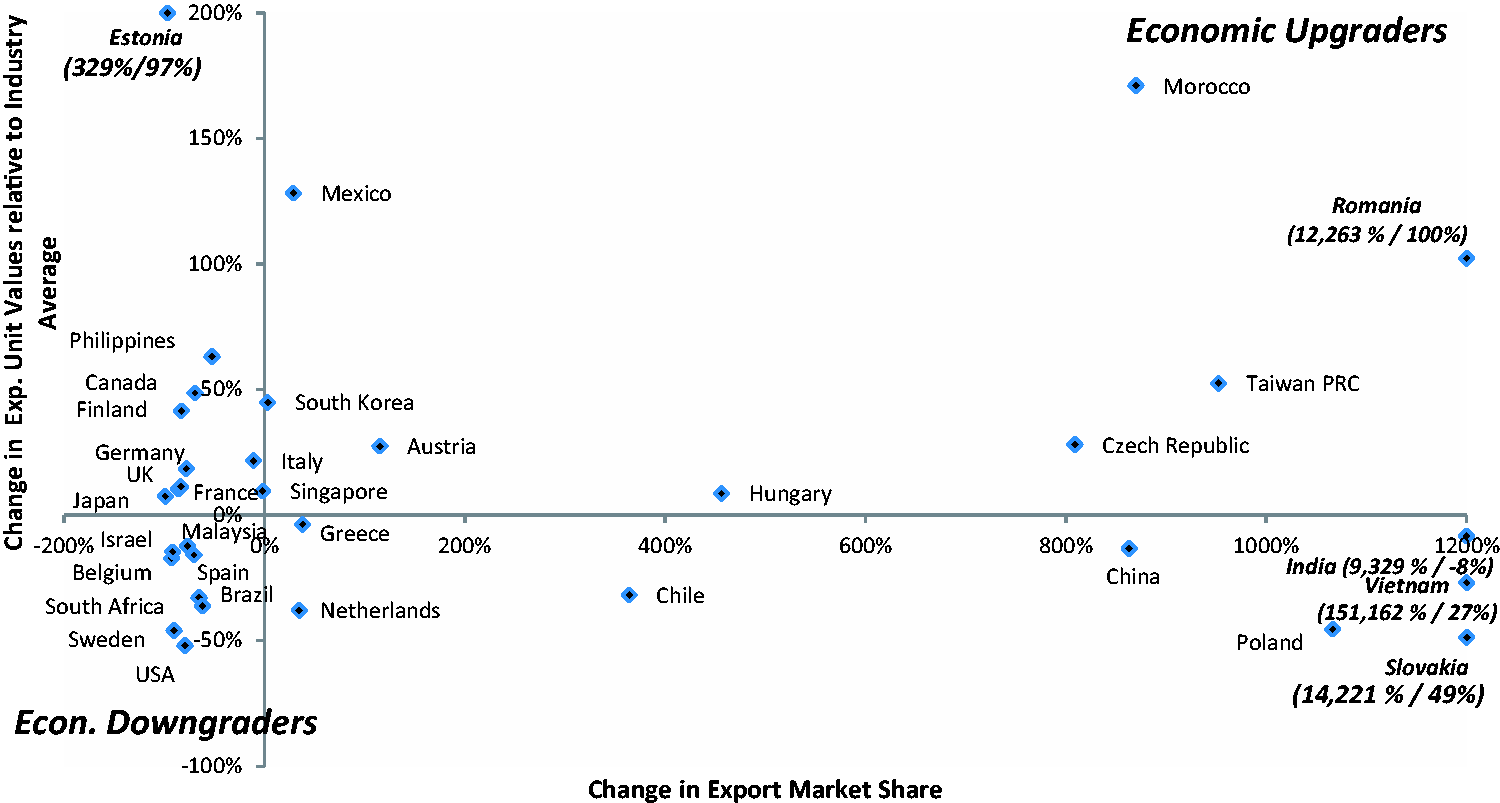

Mobile phones GVC

Similar to the two low-tech sectors in our sample, the mobile phone manufacturing GVC has also witnessed a slight consolidation in the number of dominant producer countries. Simultaneously, there has been an increase in participation of developing economies, particularly from Asia and Eastern Europe. This simultaneous consolidation and shift eastwards was also previously observed by Lee and Gereffi (2013). The role of China deserves particular attention. While in 2000 Germany had the largest world export market share with 12%, by 2012 China’s exports in the mobile phone GVC accounted for more than 50% of the world’s. This has naturally had implications on the world market shares of other economies.

Still, eight countries have managed to economically upgrade in the mobile phones GVC,

among them only one developed country, Austria (see Figure 7). Six of these were also social upgraders.

The two exceptions, Austria and Mexico, have seen rising real wages and declining

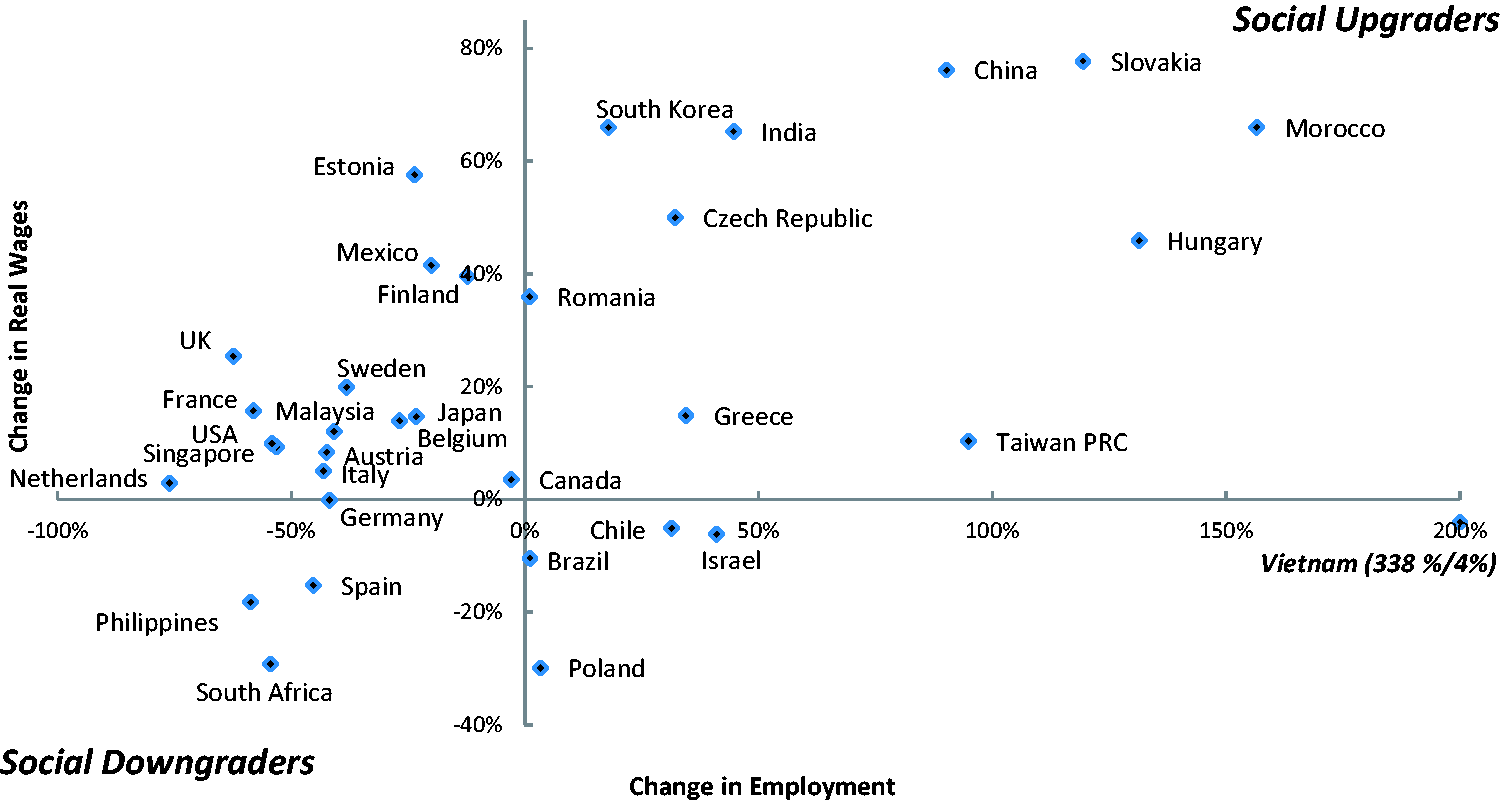

employment (see Figure 8). Social upgrading and downgrading in the mobile phones GVC

(2000–2012). Source: UNIDO INDSTAT4, UNIDO INDSTAT2 and World Bank GEM

databases.

Another eight countries (half of them European) have gained world market shares but not increased unit values relative to world average. These countries have had varying experiences in terms of social outcomes. Four of them were social upgraders while in the Netherlands the mobile phones sector shed employment but saw increasing real wages (see Figure 8), possibly indicating achievements in process upgrading, channel upgrading, or the strategic decision to increase export volumes at lower relative prices. In the three remaining countries in this group employment increased while real wages went down, suggesting they have followed a low road trajectory.

By contrast, seventeen countries in our sample have lost world export market shares. In nine of them this happened alongside an increase in relative export unit values; apart from the Philippines and Estonia, they were all developed countries (see Figure 7). The vast majority of these countries (with the exception of the Philippines) have had increases in real wages with job cuts (see Figure 8). This is in line with the idea that these countries are increasingly concentrating in the higher-value and less labor-intensive segments of the mobile phones GVC.

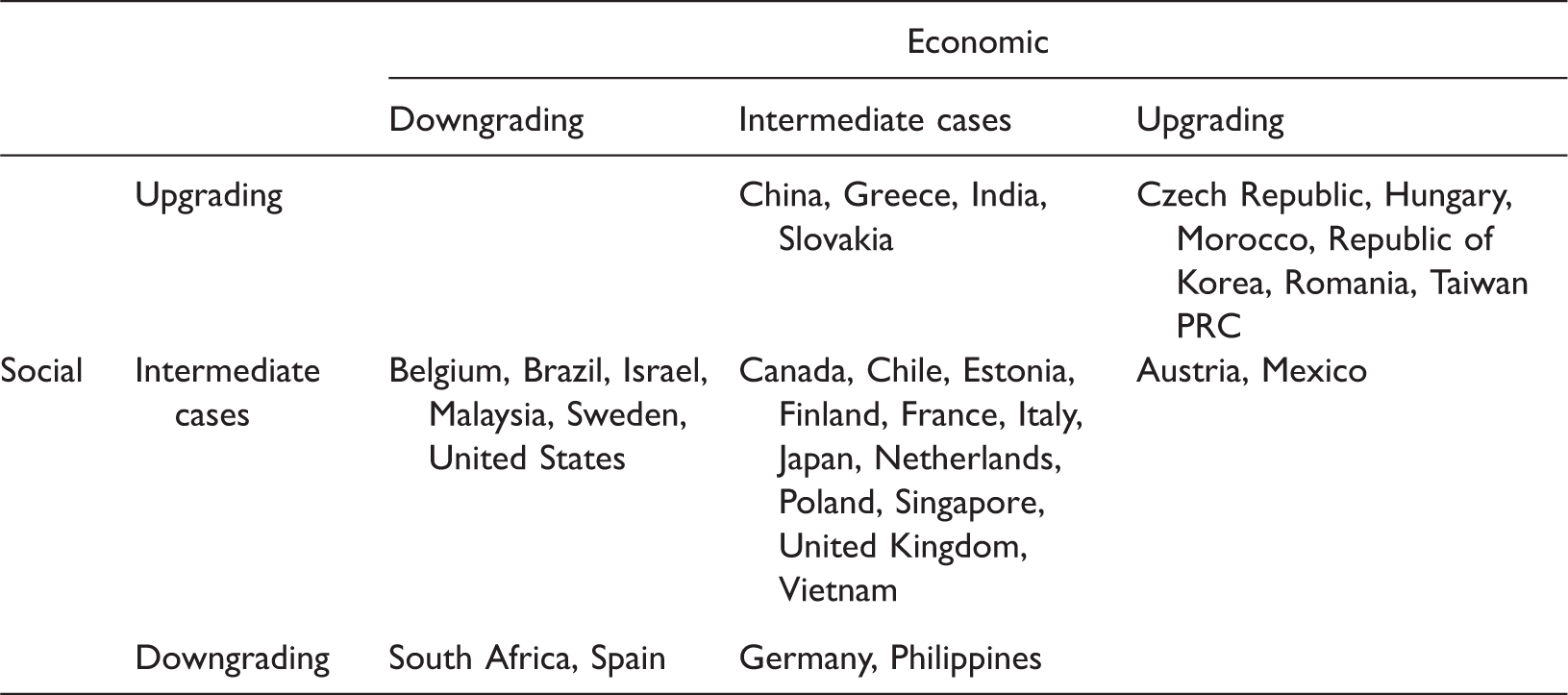

Finally, there are eight cases of economic downgrading, and they spread across different geographic locations. From this group, only South Africa and Spain have also experienced social downgrading. The remaining six economic downgraders have gone through quite interesting social performance trajectories: In four of them, the mobile phones sector shed workers at the same time that real wages increased, whereas in the other two countries employment increased but real wages fell.

All in all, social upgrading has been slightly more common in the mobile phones GVC than economic upgrading. Interestingly, there was only one developed country that was able to upgrade in any form, that being Austria which managed to economically upgrade. Meanwhile, six countries have experienced overall upgrading and two countries overall downgrading.

Comparative analysis across the four GVCs

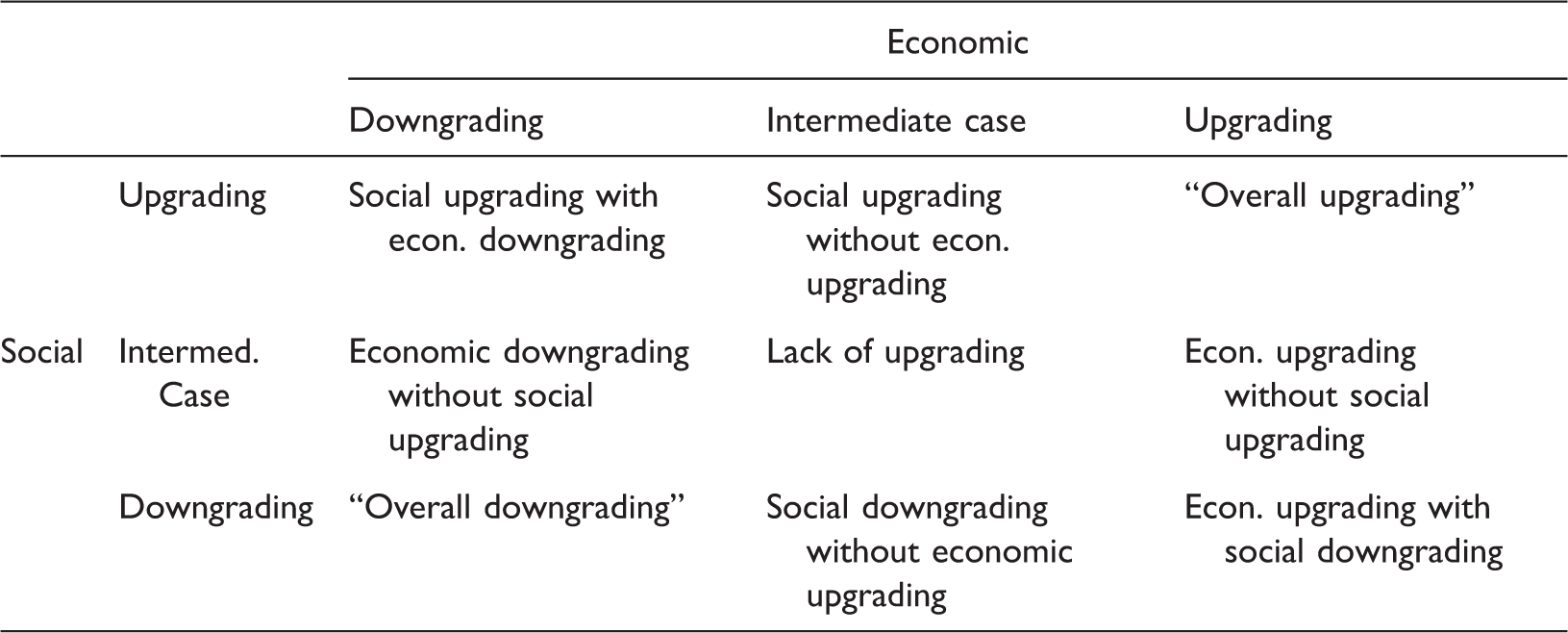

Prototype matrix for mapping economic and social upgrading/downgrading dynamics.

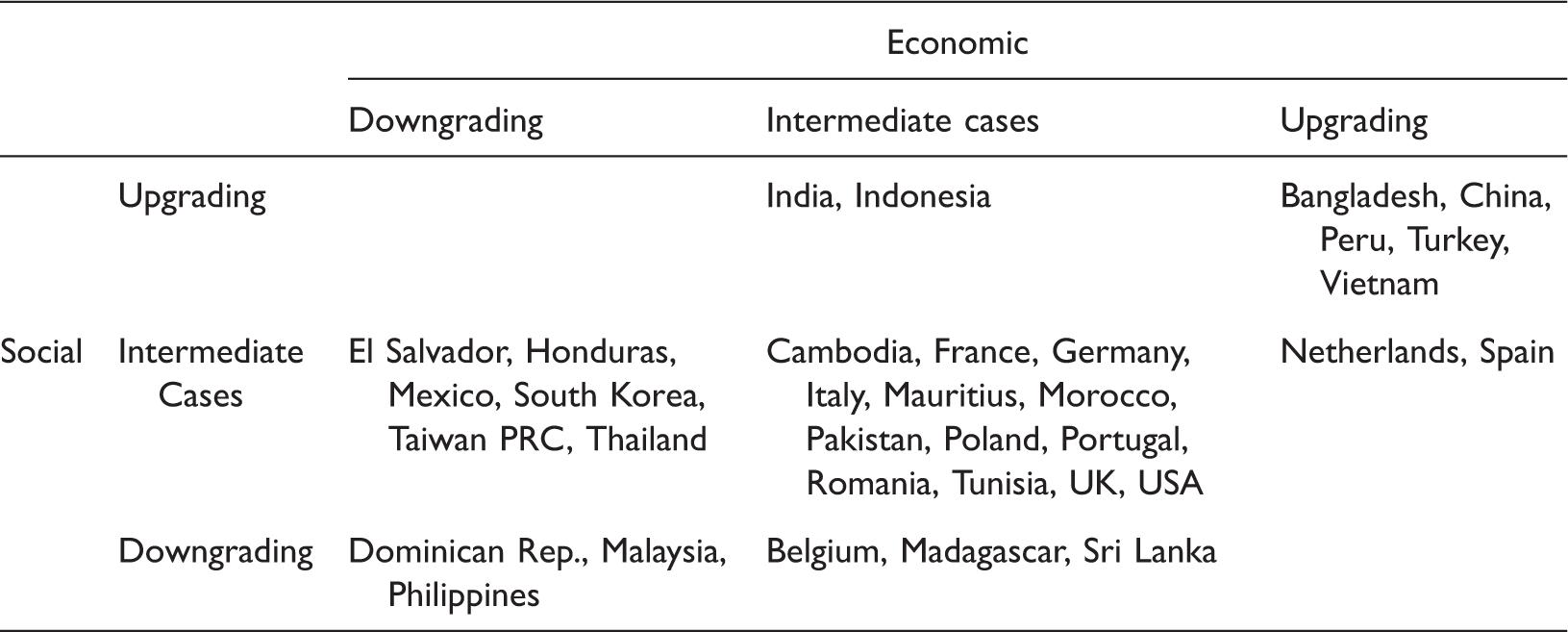

Economic and social upgrading/downgrading in the apparel GVC.

Economic and social upgrading/downgrading in the wood furniture GVC.

Economic and social upgrading/downgrading in the automotive GVC.

Each country’s economic performance is displayed on the horizontal axis while its social performance is plotted on the vertical axis. This allows grouping countries into different performance clusters with the following interpretations: The countries in the top right-hand cell are “overall upgraders” (combining economic upgrading with social upgrading), while countries in the bottom left-hand cell are “overall downgraders” (combining economic downgrading with social downgrading). Countries appearing in the two left-hand cells of the top row have experienced social upgrading without economic upgrading, whereas countries located in the two lower cells of the right column are economic upgraders without social upgrading. Finally, countries reported in the four cells in the lower left-hand corner are cases of “lack of upgrading” in the sense that they did not experience upgrading on either front (social or economic). The following cross-GVC analysis compares, firstly, economic trajectories, secondly, social trajectories and, finally, the relationship between the two.

Economic upgrading

Our parsimonious approach to economic upgrading reveals considerable variation across the four GVCs. Interestingly, among our sample countries, economic upgrading has been more common in complex sectors with a higher degree of technological sophistication (where GVCs are mostly producer-driven) than in sectors with lower technology intensity (mainly buyer-driven). While the apparel and the wood furniture GVCs each had seven economic upgraders, the automotive and mobile phones GVCs had eight and 16, respectively.

This shows that economic upgrading is not as easily achieved as suggested by the case study literature which often focuses on success stories (Milberg and Winkler, 2011). As the flipside of the pattern described above, among our sample countries, economic downgrading has been more common in low-tech than in higher-tech sectors.

Overall, advanced economies have less often undergone economic upgrading than developing economies. In most cases, this was due to their loss of world market shares to dynamic emerging market economies, which are gaining importance as producers and exporters. This loss in world market shares, particularly in low-tech sectors, is commonly accompanied by a rise in export unit values for these countries. This can, in principle, reflect a loss of cost competitiveness or, conversely, a shift in the composition of their export baskets towards higher-value products (mirroring processes of structural change in the economic configuration of these countries).

Conversely, there are quite a number of supplier countries in the developing world that have gained market shares but not managed to increase the relative value of the products they export. While they can all be considered to have increased competitiveness, this group contains cases where countries have gone down the low road to competitiveness, as they cut costs, as well as cases where countries have undergone process upgrading or other forms of increasing efficiency and raising export volumes (e.g. through channel upgrading or better vertical or horizontal coordination).

Social upgrading

As with economic upgrading, patterns of social upgrading vary quite a bit across GVCs. Social achievements have been quite widespread in the wood furniture and automotive GVCs (with 14 cases of upgrading in each) but also in the mobile phone manufacturing (ten social upgraders). Social upgrading has been most tenuous in the apparel sector and was achieved by only seven countries in our sample. It seems that workers are under particular pressure in the apparel sector where production is labor-intensive. This is confirmed by the fact that social downgrading has been most common in the apparel GVC with six cases of downgrading. Interestingly, however, the number of social downgraders among our sample countries was lower than the number of social upgraders in every value chain.

More generally, with the exception of automotives, job cuts have been very common across GVCs, as have been real wage increases. This combination of job losses and wage increases has been particularly pronounced in developed countries, which may reflect structural transformation processes in these economies.

Compared to the economic realm, it seems that upgrading has been more widespread in the social sphere while, conversely, downgrading has been more common in the economic domain. In fact, with the exception of the automotive GVC, the number of social upgraders exceeded the number of economic upgraders, and the number of economic downgraders exceeded the number of social downgraders in all the GVCs analyzed here.

Overall upgrading

Economic and social upgrading/downgrading in the mobile phone GVC.

Developed countries were more often able to go through economic upgrading (eight cases) than through social upgrading (two cases), while developing countries had the opposite experience, enjoying more social upgrading (43 cases) than economic upgrading (32 cases).

What do the tables tell us about the relationship between economic and social change? Are economic and social upgrading taking place in parallel? The cells in the diagonal from the bottom-left to the top-right include those countries where the social performance corresponds to the economic performance. By contrast, for countries that appear in the off-diagonal cells we can observe that economic and social performance did not concur. Looking at the diagonal cells of Tables 2–5 and counting all GVCs together, we find that in more than half of the countries the direction of economic and social change is the same. In the automotive GVC the relationship is strongest, while in the wood furniture GVC the relationship is weakest.

Across the four value chains, there is no case of economic upgrading with outright social downgrading, with the single exception of Germany in the wood furniture GVC. Moreover, in each GVC, there are only a few (between two to five) cases of economic upgrading without social upgrading, with the highest number in the automotive sector. At the same time, there are very few countries that have achieved social upgrading without economic upgrading (except in the wood furniture sector). In all four GVCs, the number of overall upgraders exceeds both the number of countries that have undergone economic upgrading without social upgrading as well as the number of countries that have experienced social upgrading without economic upgrading (with the exception of the wood furniture GVC).

Looking for regional trends, we find that the majority of overall upgraders across the four GVCs are Asian or Eastern European while there are also some cases of countries from the MENA 11 region and Latin America. As previously mentioned, there is only one case (Austria) of a developed country with overall upgrading. Similar to the experience of many developed countries in our samples, some newly industrialized economies such as South Korea or Taiwan PRC have been overall or at least economic upgraders in the two higher-technology sectors (automotive and mobile phones), while losing competitiveness in the sectors with lower technological sophistication. These countries seem to experience structural change within the manufacturing sector. By contrast, not only for China but also Vietnam we observe that they undergo rapid and broad-based industrialization. They remain competitive and overall upgraders in the two low-tech sectors (apparel and wood furniture), and Vietnam even in the mid-tech sector (automotive), while failing to have overall upgrading in the high-tech sector, due to the lack of economic upgrading.

Conclusions and critical remarks

Applying a parsimonious approach to measuring economic and social upgrading in four manufacturing GVCs we find that, while a number of countries do experience economic upgrading, the promise of industrial upgrading through participation in GVCs does not materialize for everyone. Indeed, we find that just over a quarter of the cases in our sample have experienced economic upgrading. Overall upgrading, i.e. the concurrence of both economic upgrading and social upgrading, has therefore been rather scarce in our sample. However, our analysis reveals that in those cases where economic upgrading does take place, it is indeed more likely to be accompanied by social upgrading than not, which indicates some positive relationship between the two.

Yet, it is important to emphasize that patterns differ across GVCs. The relationship between economic and social upgrading seems to be strongest in the automotive value chain. The chain where the relationship seems weakest is the wood furniture industry. This is mostly due to the fact that many countries experienced social upgrading without economic upgrading. Meanwhile, the apparel GVC has seen most economic downgrading, though in many cases this was not accompanied with social downgrading. A similar pattern is observed in the mobile phone GVC. These latter findings hint towards the fact that social performance can be, and is, determined by factors other than the country’s economic upgrading performance.

The bulk of countries in our sample did not experience clear-cut upgrading or downgrading. For example, quite a number of developing countries recorded increasing world export market shares with decreasing unit values relative to industry averages. This can be the result of efficiency gains due to successful process upgrading or improved coordination within the GVC, or of successful implementation of other firm strategies (such as achieving economies of scale and scope or improving reliability and consistency of supply) which are often not captured by traditional upgrading analyses. In some cases, however, this can also be the result of lead firms exercising pressure on suppliers to maintain low prices, forcing the suppliers onto a low road to competitiveness so that they struggle to upgrade. Looking at the countries’ social performances helped to identify which of these trajectories was more likely to apply. Meanwhile, many developed economies experienced increased unit values with market share losses, and similarly employment decreases with wage increases, possibly reflecting processes of structural change in the configuration of their economies.

In fact, similar patterns of upgrading or downgrading can have different underlying mechanisms. Our methodology allowed us to observe the outcomes of upgrading attempts and processes and, thereby, to capture, in broad terms, different types of upgrading and enhanced competitiveness. However, while this ensures we can report on all cases where supplier countries have “reached better deals” within GVCs, as Ponte and Ewert (2009) call it, our approach does not permit us to neither identify the specific form of upgrading (or downgrading) nor the underlying factors that have driven a country’s performance. Therefore, case study literature is needed to shed light on more specific information hiding beneath our data.

Our concept of “overall upgrading” can serve as a point of departure for a more holistic theory of upgrading that integrates economic, social and ideally even environmental aspects of GVC participation. Such a theory would reflect on the underlying mechanisms that drive the relationship between economic and social outcomes, accounting for possible trade-offs, thereby helping to improve our understanding of the conditions which typically lead to either overall favorable outcomes (a “virtuous upgrading circle”) or unfavorable outcomes (a “vicious downgrading circle”). From our analysis we know that positive developments in one area are not always accompanied by positive developments in the other domain.

However, some caveats have to be borne in mind when interpreting our findings. First, while our parsimonious approach to defining and measuring upgrading allowed comparisons across countries, regions and GVCs, it is not able to capture qualitative facets of social upgrading such as increased compliance with labor standards or other improvements in working conditions. Nonetheless, cases such as the deadly collapse of the Rana Plaza building in Bangladesh housing clothing factories, the recent violent protests requesting higher minimum wages in Cambodia and the alerting number of suicides in Chinese Foxconn factories are just a few examples of precarious working conditions which need to be discussed as part of the reality of the increasing international fragmentation and therefore competition in production.

Second, the official data we use do not cover informal firms or workers – which in many developing countries account for 70% or more of the labor force 12 —where entitlements and social benefits are typically non-existent and labor laws not enforced. Also, the data do not sufficiently account for irregular employment arrangements like temporary or contractual work where wages and social security benefits are usually worse and job insecurity much higher than in regular jobs. Due to this lack of data, it is unfortunately not possible to include such analysis into our work at this stage.

Third, the approach and terminology used here might seem to suggest that upgrading is always desirable in any given GVC. However certain sectors or chains offer little prospects for learning, productivity increases or technological progress and, thus, are less promising with regard to longer-term economic development. If developing countries focus their upgrading efforts on these chains and allocate an increasing amount of resources to these sectors, they risk being trapped in a low road trajectory to development (Milberg and Houston, 2005). Lack of economic upgrading (or even downgrading) in a given GVC as measured by the indicators adopted here, therefore, can be a positive thing if it is a side effect or manifestation of the structural change an economy is undergoing.

Future research might add precision and rigor to the analysis of economic and social upgrading by using information on working conditions as well as data on trade in value-added, once such data become available at a more disaggregated sectoral level and for a wider range of countries. Another issue that deserves heightened attention in future research is the impact of integrating and upgrading in GVCs on inequality—both within and across countries. For quite a number of countries in our sample we observed a decline in sectoral employment coupled with a rise in real wages—is this an indication of increasing inequality? Finally, while initial efforts have been undertaken (Staritz et al., 2011), future research should aim at improving our understanding about how and to what extent the observed regionalization of value chains fosters or hinders both economic and social upgrading in developing countries.

Footnotes

Acknowledgements

The views expressed herein are those of the authors and do not necessarily reflect the views of MDRI-CESD or UNIDO. Particular thanks are due to Amanda Janoo for substantial contributions to a previous version of the paper. The authors also gratefully acknowledge helpful comments on earlier drafts by Gary Gereffi, Will Milberg, John Pickles, Shamel Al-Azmeh and three anonymous referees. All remaining errors are ours.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.