Abstract

‘Crowdfunding’ is a method of raising money and finance to capitalize projects of various kinds. Drawing on the networking capabilities of the internet and software platforms, those seeking project funding appeal to potentially diverse audiences who are collectively referred to as ‘the crowd’. What practitioners, advocates and policymakers typically identify within crowdfunding is its ‘alternative’, ‘disruptive’ and ‘democratizing’ qualities; that is, it is held to be a novel, digitally rendered economic space which has the capacity to challenge established funding practices in banking, capital markets and venture capital networks, offering a more open and egalitarian source of capital for economic, social and cultural entrepreneurship. The paper develops the concept of ‘ecologies’, drawn from the geographies of money and finance literature, to advance a critical understanding of the crowdfunding economy that is sceptical of its apparent qualities. First, by encouraging the analysis of diverse and proliferative monetary and financial forms, the concept of ecologies enables an understanding that avoids the binary opposition of ‘capitalist/alternative’ economic forms and which differentiates between the variegated crowdfunding ecologies that have emerged to date. Second, by foregrounding the intermediation processes and credit–debt relations of monetary and financial ecologies, it is argued that crowdfunding may largely replicate rather than disrupt the extant institutional and debt dynamics of funding practices. Third, by emphasizing the socio-spatial effects of monetary and financial ecologies, attention is drawn to the need for further research into the unevenness that mitigates against crowdfunding being as open and egalitarian as its advocates claim.

Introduction

The purposes of this paper are two-fold. First, we want to develop a critical understanding of the relatively new but rapidly growing form of money and finance known as crowdfunding. Crowdfunding's purposive appeals to unspecified individuals (‘the crowd’) for capital to fund projects with specified outcomes are made possible by the networking capabilities of the internet, exploiting what Anderson (2006) has described its ‘long tail’; that is, an ability to aggregate geographically distributed resources and assets to build a critical mass which has agency. These processes, which we term ‘capitalizing on the crowd’, mark out crowdfunding as different from venture capital or other established funding practices organized through dedicated public and private institutions, whether branches of government or banks and financial market agencies. It is the distinctive character of these processes, moreover, which gives rise to what practitioners, advocates and policymakers typically identify as important within crowdfunding. Crowdfunding is widely held to be an ‘alternative’ digital economy which has the capacity to ‘disrupt’ established funding practices in banking, finance and venture capital markets (Nesta, 2013b), unleashing a ‘democratization’ of capital for economic, social and cultural entrepreneurship (Baeck et al., 2014; Dresner, 2014; Nesta, 2012, 2013a, 2013b). Our critical understanding of crowdfunding will therefore explicitly question the novelty of this digitally rendered economic space, the capacity it may hold to challenge extant funding practices and the extent to which it provides a more open and egalitarian source of capital for economic, social and cultural entrepreneurship.

When advancing a critical account of the crowdfunding economy, the second purpose of this paper is to do so by developing the concept of ‘ecologies’, drawn from the geographies of money and finance literature. At present, academic research into crowdfunding is limited but growing, and is primarily located in the fields of business studies and digital humanities. Research in business studies is typically preoccupied with teasing out why past projects were successful in attracting funding to provide lessons for future calls (e.g. Mollick, 2014) or proposing theoretical models to explain why different stages of start-up entrepreneurship may be most appropriately facilitated by crowdfunding (e.g. Belleflamme et al., 2014). In digital humanities, research is particularly interested in fandom and other affective energies that animate the crowdfunding of artists and performers, and typically casts doubt on the potential this holds for transforming the cultural industries from ‘the bottom-up’. The claims made about the ‘transformative potential of crowdfunding’ have also begun to be challenged by geographers such as Bieri (2015: 2431). Focusing on the capital that crowdfunding makes available for large-scale urban real estate and infrastructural projects in US cities, Bieri makes a connection to a long-standing geographical interest in the tendency within capitalism for flows of finance capital to switch from the circuit of production and into the built environment (Harvey, 2001). We share Bieri's (2015: 2431) desire to contest ‘the febrile speculation’ about crowdfunding and the oft-repeated claims that are made over ‘the future prospects of this method of financing’. However, our approach is different, and this changes the terms of debate by moving beyond concerns with the switching of capital between circuits and the (albeit increasingly significant) process of ‘crowdfunding the city’ (Bieri, 2015). Drawing upon and further developing the concept of monetary and financial ecologies, in this paper we stress that the processes of capitalizing on the crowd are variegated, intermediated and uneven, and it is on this basis that we question the apparently ‘alternative’, ‘disruptive’ and ‘democratizing’ qualities of crowdfunding.

The concept of monetary and financial ecologies was elaborated initially to account for the persistence during the 1990s of so-called relic forms of financial activity – high-cost door-to-door moneylending and household insurance – in poorer urban areas in the UK (Leyshon et al., 2004, 2006). These distinctive financial arrangements had survived the shift to an at-a-distance mode of financial product delivery and market assessment, both in the mainstream and what later came to be labelled as the ‘sub-prime’ sectors, in part due to the problems of risk assessment and payments collection in areas characterized by economic precarity. In the first instance, then, the concept of ecologies provokes an approach to geographies of money and finance that does not regard the operations of monetary and financial systems as singular and always already defined by the spatial–temporal logic of a global circuit of capital. Rather, geographies of money and finance are composed of an array of more or less discrete and dynamic constitutive ecologies that consist of specific arrangements which emerge and are more or less reproducible over time. These relational processes, which entail distinctive combinations of financial knowledge, institutional and intermediary techniques and expert and popular subjectivities, unfold across space and evolve in relation to geographical difference, so that distinctive ecologies emerge in different places.

While holding certain affinities with other relational concepts that inform research into geographies of money and finance – most notably, concepts such as network (e.g. Pollard, 2001), apparatus (e.g. Langley, 2015) and assemblage or agencement (e.g. Hall, 2011) – the concept of ecologies also draws explicit attention to ways in which the comings together of relational topologies are uneven in their proximities and connectivity, generating socio-spatial inclusions/exclusions and inequalities. Some people, places, institutions and so on are better connected than others, such that ecologies differ in their scope and resilience. As Lai (2016: 30) argues, ‘the ecologies concept can offer … topological finesse around questions of why particular sets of relations are more durable or porous, allowing for more precise consideration of power in relational thinking’. Its deployment has enabled economic geographers to explore the relationship between space, institutions and the socio-economic status of financial subjects in a range of contexts, ranging from studies of the impact of financialization on lived experience in deprived rural areas (Coppock, 2013) to the formation of more affluent financial ecologies surrounding private wealth management and independent financial advice in global cities such as London, New York and Singapore (Beaverstock et al., 2013; Lai, 2016). The concept has also emerged within cognate disciplines, such as anthropology, where Maurer (2015: loc 528) has drawn attention to ‘the complex money ecologies of people around the world, and people's elaborate and diverse repertoires for using money as they navigate and add to those ecologies’.

The remainder of the paper proceeds in four parts. First, ‘Crowdfunding as ‘alternative’?’ begins by briefly introducing the evolution and organization of crowdfunding. It situates the seemingly ‘alternative’ character of this economy against the backdrop of concentrated and centralized capital investment and in the context of wider debates about the transformations wrought by the rise of digital economies and the so-called FinTech sector (e.g. Arvidsson and Peitersen, 2013; Benkler, 2006; Christi, 2016; Kostakis and Bauwens, 2014). This part of the paper also underscores how the concept of ecologies can enable analyses of diverse and proliferative monetary and financial forms. This leads us to avoid the binary of capitalist/alternative that typically frames understandings of crowdfunding, but instead to differentiate between the more or less discrete ecologies of crowdfunding that have emerged to date; that is, donation, rewards, equity, fixed income and peer-to-peer lending. Second, ‘Crowdfunding as ‘disruption’?’ foregrounds intermediation and credit–debt relations within monetary and financial ecologies. We argue that, despite their present diversity, crowdfunding ecologies may largely reproduce rather than disrupt the extant intermediation and debt dynamics of capital allocation practices. Third, ‘Crowdfunding as ‘democratization’?’ places emphasis on the socio-spatial consequences of crowdfunding ecologies and calls for further research into the open and egalitarian qualities claimed by advocates of crowdfunding. The final section concludes the paper.

Crowdfunding as ‘alternative’?

The crowdfunding economy operates according to principles similar to those that underpin ‘crowdsourcing’ (Howe, 2009), a method for accessing ideas, knowledge and solutions from geographically distributed digital communities (Brinks and Ibert, 2015). Crowdfunding channels money and finance to animate economic, social and cultural entrepreneurship, typically providing capital for projects initiated by a range of actors and institutions which can be as diverse as artists and performers, charitable and community projects, as well start-up businesses, small- and medium-sized enterprises (SMEs) and real estate investment companies. Crowdfunding has grown very quickly in a short period of time, and in doing so, as we outline later, has produced its own distinctive monetary and financial ecologies. In the UK, rapid expansion of crowdfunding began in 2011 and continues apace (Baeck et al., 2014; Nesta, 2013a). Measured by the aggregate value of flows, the UK crowdfunding economy grew by over 160% between 2012 and 2015, reaching £3.2 billion, equivalent to 4% of new lending to SMEs (Baeck et al., 2014; Zhang et al., 2016). Crowdfunding has also expanded globally (Espsoti, 2014), raising an estimated $16.2 billion in 2014 (The Economist, 2015a). This was expected to rise to $34 billion by the end of 2016, exceeding the volume of money invested in venture capital funds (The Economist, 2016a). The largest crowdfunding economies by volume are in the US and Europe, with the UK industry possessing the most breadth and variety. London-based platforms are regarded as world-leading innovators (Alloway and Jenkins, 2015; Moules, 2014).

Mobilizing funds to initiate entrepreneurial ventures certainly predates capitalism, let alone the emergence of joint-stock companies (McLaren, 2013). However, over the last four decades or so there has been a strong tendency for retail banks to lend to consumers rather than SMEs (Erturk and Solari, 2007), and the provision of capital for new ventures has become increasingly narrow, as institutional investors and large financial institutions, including venture capital firms, have become the primary intermediaries for funding entrepreneurial projects and company start-ups (Zook, 2004). Share ownership may have widened considerably to include the ‘fortunate forty’ per cent of the population in the US and UK (Froud et al., 2002), but this is primarily the result of transformations in occupational and personal pensions that concentrates capital and centralizes fund management decisions in the hands of professional institutional investors (Langley, 2008). This process of concentration and centralization has been resistant even to politically motivated efforts to broaden the active investment base, such as the attempt to build a ‘shareholding democracy’ in the UK during the 1980s and 1990s through the privatization of public assets and institutions. To the extent that direct and active shareholding increased through privatization, it tended to be in the regions of the UK where it was already prevalent, such as London and the South East, reflecting existing geographies of wealth, disposable income and personal investment intermediaries (Martin, 1999).

The development of the internet created the opportunity for individuals, firms and communities seeking funding for the launch of projects and ventures to appeal to new audiences beyond the community of professional investors and specialized institutions which dominated the provision of capital. The pioneers of what became known as crowdfunding initially conformed to what Lewis (2001) has described as ‘interest-based economics’, where fan communities were mobilized to fund artistic projects that would not otherwise reach fruition. Lewis credits the UK rock band Marillion as the first to stumble across what would subsequently be categorized as crowdfunding. Their appeal to fandom, emotion and affect was replicated by a growing number of creative artists, who offered their output and/or presence in return for money (Leyshon et al., 2016). Such processes of capitalizing on the crowd were gradually formalized through the emergence of organized crowdfunding platforms. Over time, and particularly since 2008, crowdfunding has evolved to cover more activities, with much of the recent rapid growth being generated through platforms that operate in markets which increasingly compete more directly with traditional financial institutions.

Although it emerged as a subset of crowdsourcing practices and from specific digital communities of fans and activists, the crowdfunding economy is now typically framed by practitioners, policy makers and economic commentators in one of two related ways. First, crowdfunding is positioned as an ‘alternative’ form of financial behaviour, in that it is has an institutional base and structure that is demonstratively different from mainstream capitalist finance (e.g. Baeck et al., 2014; Zhang et al., 2016). Here crowdfunding appears as something of an antidote to the oligopolistic concentration and centralization of capital investment, a digital economy that necessarily cuts against the grain of the mainstream and the traditional, and which has the remedial and ameliorative capacity to make funding available to individuals and institutions that would otherwise be excluded from capital allocations. Such positioning of crowdfunding invites comparisons with the diverse monetary forms of local currency systems. Drawing on notions of the crowd and its agency – albeit defined by factors such as locality, co-presence and sociality (Lee et al., 2004; North, 1999) – local currency systems seek to introduce new possibilities for exchange. Making available resources that would otherwise lie idle – like time, skills or everyday assets – local currency systems create ‘alterative’ monetary forms which enable individuals and their communities to derive mutual benefits through the provision and purchase of various goods and services.

Second, crowdfunding has been more recently framed as a constituent part of ‘FinTech’, a term that refers to a wider set of changes that The Economist (2015a) describes as the outcome of a ‘combination of geeks in T-shirts with venture capital’. Here crowdfunding is recast as having emerged through a fusion of the technological prowess of Silicon Valley with the financial acumen of Wall Street and, in particular, the City of London, conveniently co-located in East London alongside the high technology cluster of ‘Silicon Roundabout’ (McWilliams, 2015). FinTech is broadly understood as comprised of three main fields: new payments systems, including cryptographic, blockchain-based currencies such as Bitcoin (Maurer, 2015; Tapscott and Tapscott, 2016) which offer the prospect of a transparent and secure ledger to record transactions (The Economist, 2015b); new forms of risk calculation, which expand the sources of information to assess creditworthiness beyond the measures traditionally used by credit scoring and credit rating firms to create new metrics against which ‘trust’ can be conferred on borrowers (The Economist, 2015a); and new forms of lending, which includes crowdfunding and peer-to-peer lending. This positioning of crowdfunding as a FinTech industry (rather than as an ‘alternative’ economy) fills it with a rather different set of fixed and singular meanings and disruptive purposes. By definition, it is difficult to comprehend crowdfunding as simultaneously a creation of the coming together of the most dynamic sites of contemporary capitalism and an alternative to established capitalist banking and finance.

The concept of monetary and financial ecologies provokes an understanding of the crowdfunding economy that does not turn on the binary of capitalist/alternative (see, more broadly, Fuller et al., 2010; Leyshon et al., 2003). As Lai (2016: 28) summarizes, this is a concept that ‘recasts the financial system as a coalition of smaller constitutive ecologies, such that distinctive groupings of financial knowledge and practices emerge in different places with uneven connectivity and material outcomes’. Not only is it a concept that encourages the careful teasing out of the multiplicity and variegation of monetary and financial forms within and across what is typically taken to be capitalist money and finance, but it also connects with a wider movement in the geographical literature to decentre and pluralize the ‘capitalocentric’ study of economy (Gibson-Graham, 1996, 2006). Adjudicating whether crowdfunding is either an alternative digital economy or a manifestation of the financial and technological dynamism of capitalism is to make a fundamental error of understanding: it necessarily forecloses an analysis of the heterogeneity and diversity of the economic modalities that characterized crowdfunding at its outset and have endured. The binary categories of capitalism/alternative are not mutually exclusive within the universe of the crowdfunding economy; in other words, crowdfunding is not either/or, but both/and (see Maurer, 2013).

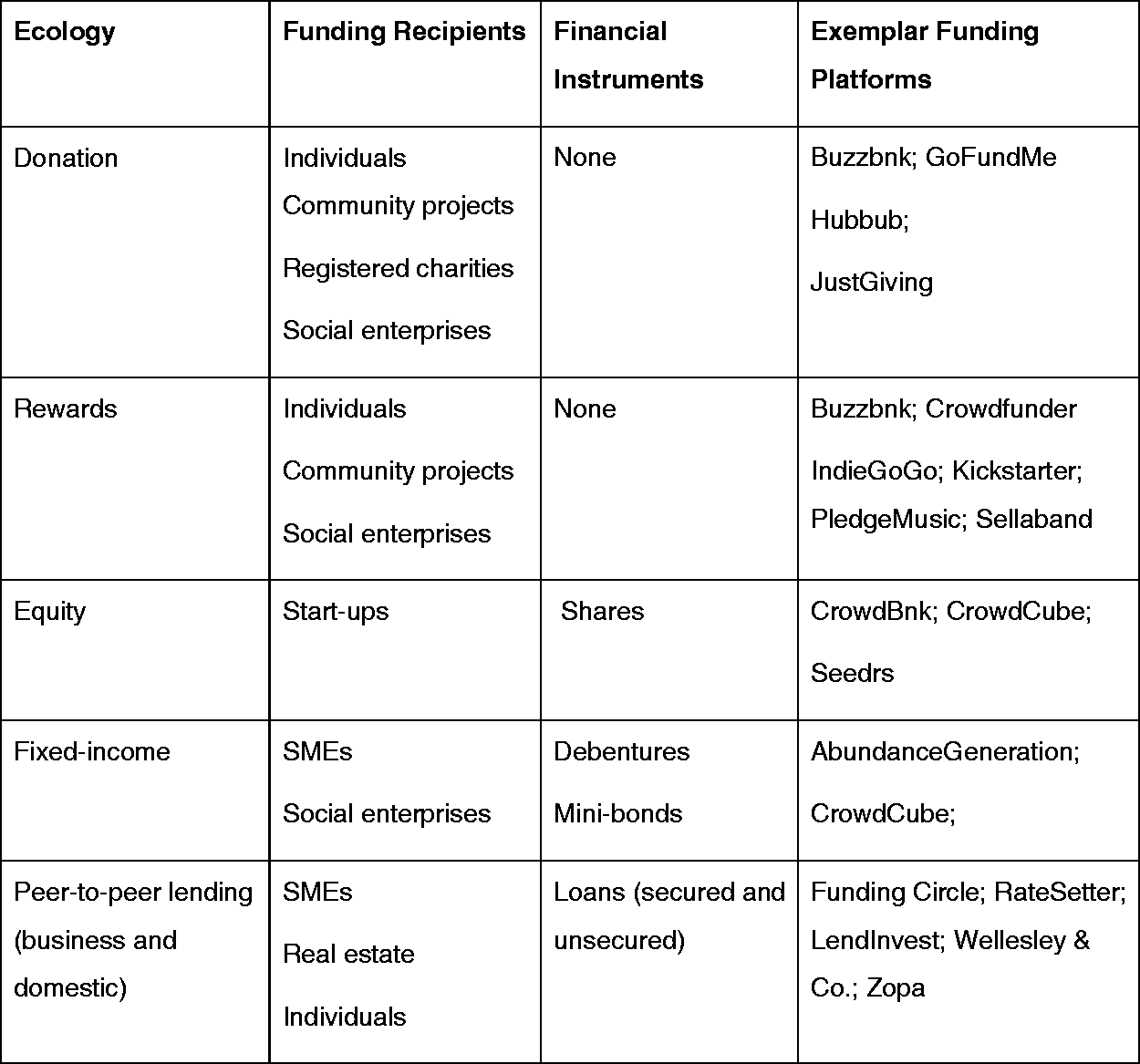

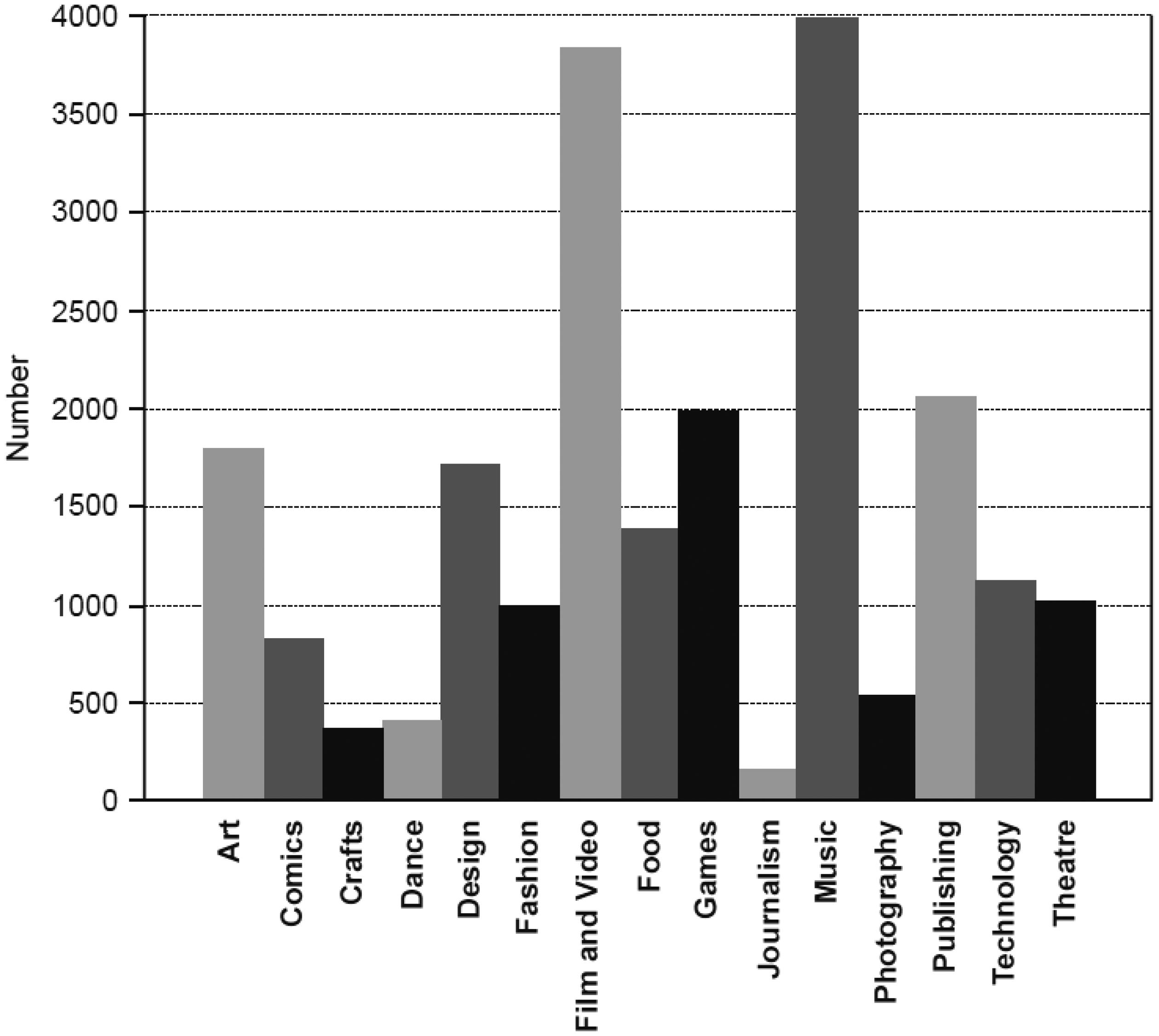

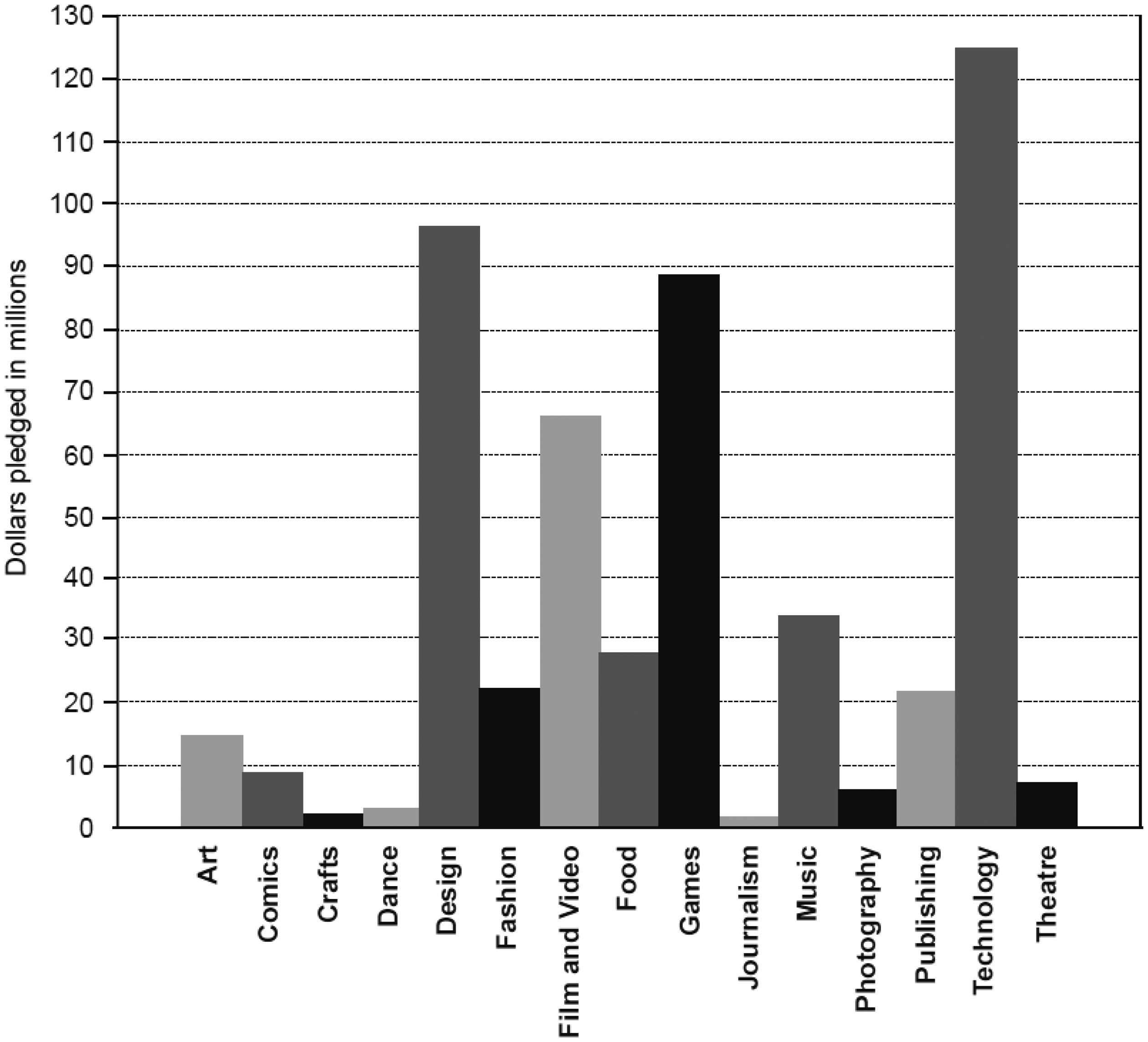

By way of illustration, and with particular reference to crowdfunding in the UK which is marked by its variety (e.g. Moules, 2014), we suggest a typology to differentiate between the five principal and more or less discrete monetary and financial ecologies that have emerged to date; that is, donation, rewards, equity, fixed income and peer-to-peer lending (see Figure 1). The pledges and symbolic compensation of donation crowdfunding closely resemble those found in the monetary ecologies of charity and gift giving. The monetary ecology of rewards crowdfunding, meanwhile, has parallels with the making of consumer payments by way of pre-ordering and ‘co-producing’ retail products (Arvidsson and Peitersen, 2013), or receiving future discounts and markers of prestige of some kind. These two crowdfunding ecologies are composed, then, of monetary transactions and exchanges that could be categorized, following Gibson-Graham (2006: 71), as ‘non-market’ and ‘alternative market’. The volume of money that travels through them is significant, especially for the capitalization of projects in the creative and artistic sectors. The most high profile crowdfunding platform operating across the donation and rewards ecologies in the US and UK is Kickstarter. Established in New York in 2009, by January 2016 Kickstarter had channelled more than $2 billion towards almost 100,000 projects. This money was raised from over 10 million backers who between them made over 27.5 million pledges.

1

Kickstarter has 15 categories of project, with the share of pledges and successfully funded projects illustrated in Figures 2 and 3.

Principal monetary and financial ecologies of crowdfunding in the UK. Number of funding pledges, by project category, Kickstarter (source: Kickstarter, https://www.kickstarter.com/help/stats?ref=about_subnav). Value of funding pledges, by project category, Kickstarter (source: Kickstarter, https://www.kickstarter.com/help/stats?ref=about_subnav).

The crowdfunding economy in the UK also includes three ecologies where monetary and market exchange is explicitly financial in orientation. The world's first equity and fixed-income crowdfunding platforms, Crowdcube and Abundance Generation, both launched in 2011, and have subsequently been joined by several competitors. Such platforms ensure that the crowdfunding economy includes investment ecologies which have strong parallels with those found in venture capital and capital markets. Finally, peer-to-peer (P2P) circuits extend loans to business and domestic borrowers. This lending has grown rapidly: in 2015 business P2P accounted for 47% and consumer P2P for 28% of total UK crowdfunding (Zhang et al., 2016). In the ecology of P2P business lending, the aggregated and interest-bearing funds of creditors are allocated to the projects of relatively well-established SMEs. The most recent expansion in P2P business lending in the UK has been marked, moreover, by the proliferation of platforms and practices which make possible secured loans to residential and commercial real estate ventures (Langley, 2016; Zhang et al., 2016), mirroring developments identified in the US by Bieri's (2015) ‘crowdfunding the city’ research. Meanwhile, in the ecology of P2P domestic lending those receiving unsecured loans from the crowd are anonymous and not project based: would-be borrowers are not made known to lenders, but pooled and differentiated according to credit scores and/or the duration of their loan requests. In the US, the P2P domestic lending ecology – dominated by two platforms, Prosper and Lending Club (founded in 2005–2006) – has accounted for the greatest share of the expanded scale of flows in the crowdfunding economy (Aitken, 2015).

Our typology of the UK's crowdfunding economy is suggestive of a set of dynamic and diverse monetary and financial ecologies that require further investigation through empirical research. For example, crowdfunding ecologies may be bringing about new distributions of money, credit and debt over space, channelling funds to projects in places that might otherwise be excluded from mainstream finance. This might be particularly the case with donation and rewards ecologies, as crowdfunding provides an opportunity for funding that is more akin to gifting than financial claim. There are parallels here to the exploration of geographies of foreign aid and development (Mawdsley, 2012), and it would seem especially apposite to consider the ways in which digital economies can mobilize and share resources and assets between geographically distributed and connected communities of interest. Indeed, rewards crowdfunding is routinely categorized as part of the so-called sharing economy which is predicated on ‘taking underutilized assets and making them accessible online to a community, leading to a reduced need for the ownership of those assets’ (Stephany, 2015: 3). The sharing economy is not a gift economy, for the underlying motive in the former is to create value by mobilizing (and earning fees from) the ‘excess capacity’ of accumulated and underutilized assets (Chase, 2015). Moreover, the sharing economy may be seen as an attempt to colonize the social economy, and in so doing ‘is a reflection of capitalism's need to find new profit opportunities in aspects of social life once shielded from the market’ (Stephany, 2015: 8). The best known examples of sharing economy business models utilize excess capacity in physical assets such as cars (e.g. Uber) and property (e.g. Airbnb), but crowdfunding platforms also perform this function as they ‘get “slack to the pack”, that slack being spare cash’ (Stephany, 2015: 102), with this otherwise idle money being put to potentially productive use by funding projects.

Meanwhile, and with reference to its rapidly expanding equity, fixed income and P2P lending ecologies, the expansion and proliferation of crowdfunding is already the focus for economic geography research concerned with the marketization of this digital space economy (Langley, 2016). Here the growth of crowdfunding may largely serve to replicate established monetary and financial ecologies. As crowdfunding platforms seek to outcompete mainstream financial institutions on the basis of efficiency and effectiveness – derived from the absence of legacy costs from branch networks and lighter regulatory burdens – they attempt to capture extant flows of money and finance and take control of (i.e. re-concentrate and re-centralize) capital investment processes. Moreover, as platforms in the UK now target not only ‘the crowd’ but also attempt to attract funds in search of a return from institutional investors, there may be an advantage for equity, fixed income and P2P crowdfunding platforms to be co-located in large financial centres. In the terms of a celebratory Financial Times article on the development of the crowdfunding economy, the diversity of the sector in the UK is translated into a key strength of London as a global centre (Moules, 2014). We explore these propositions further in the next two sections of the paper which will critically evaluate the claims made for crowdfunding's capacity to disrupt and democratize extant arrangements for the allocation of capital.

Crowdfunding as ‘disruption’?

In the mid-to-late 1990s, Christensen (1997) coined the influential notion of ‘disruptive innovation’ to update Schumpeter's concept of ‘creative destruction’ for the digital age. It refers to any innovation occurring at ‘the bottom’ of a market that makes a product or service more widely accessible to consumers, and thereby challenges the offerings and business models of incumbent firms ‘at the top’. According to Stephany (2015: 148), claiming an ability to ‘disrupt’ existing markets for profit has become an almost obligatory part of the mission statement for new tech start-ups. While the ubiquity of claims to disruptive innovation often feeds scepticism (see, for example, King and Baatartogtokh, 2015), the exception seems to be crowdfunding and the broader FinTech sector. For example, Pignal (2015) has argued that ‘there is no doubt that “disruption” has at least reached finance, an industry so regulated and politically connected that it once seemed above the threat of new entrants’. The evidence cited for this disruption is that 50 global FinTech companies were transacting business worth over $1 billion at the end of 2015, and that a select few can reasonably expect to be ‘doing business in the tens of billions of dollars – at least if their exponential growth rates hold’.

Banking losses and post-crisis regulatory compliance costs have displaced innovation from the traditional domains of the financial sector. New forms of so-called smart money and social finance have taken hold that, for their proponents at least, demonstrate the disruptive power of financial market innovation which can solve a host of socio-economic and environmental problems (Nicholls et al., 2012; Palmer, 2015). Post-crisis innovation and experimentation across the crowdfunding economy, encouraged by judicious policy nudges, may be an example of monetary and financial disruption which is less voracious and less wedded to the worst excesses of financialized capitalism. Indeed, both the UK and US governments have enacted policies that seek to exploit crowdfunding's disruptive potential to openup new funding for entrepreneurialism. Through the British Business Bank, the Department of Business, Innovation and Skills has funded loans to SMEs through crowdfunding platforms. 2 HM Treasury (2014) made it possible for funds channelled into crowdfunding to be included, for tax purposes, under the new regime for Individual Savings Accounts. Meanwhile, the Financial Conduct Authority (2013, 2014) implemented new regulations to provide consumer protections for those contributing funds via crowdfunding platforms. In the US, provisions within the 2012 Jumpstart Our Business Start-ups Act made it permissible for equity crowdfunding to provide an alternative source of venture capital to new businesses (Mollick, 2014).

However, any assessment of these disruptive forces should give careful consideration not only to the diversity of the crowdfunding economy's monetary and financial ecologies, but to the intermediation and credit–debt relations which are constitutive of those ecologies. As Lai (2016) has suggested, the critical analytical purchase afforded by the concept of ecologies – especially as it might elucidate the constitutive relational entanglements that make possible monetary and financial arrangements – can be significantly strengthened by paying greater attention to intermediation as a particular and distinctive form of market institutional agency. In this respect, we note that the concept of ‘intermediation’ is being utilized more widely to understand the demise and rise of institutions during a period of post-crisis structural change in global finance. If we foreground the intermediation of the monetary and financial ecologies of crowdfunding, moreover, attention is drawn to the techniques and practices of platforms as sites of intermediation across all five of the principal ecologies outlined above (Langley and Leyshon, 2016; Srnicek, 2016). This diminishes the claim that the apparently two-sided and ‘disintermediated’ exchanges of crowdfunding are genuinely different to, and disruptive of, the traditional practices of banking which intermediate between savers and borrowers. Crowdfunding may be described as ‘zero-sum lending’: unlike fractional banking, it does not create private money or leverage debt in order to generate income However, profitable intermediation by crowdfunding platforms necessarily turns on earning fee income in return for aggregating and distributing funds, and fees have also become increasingly important to banking profits in recent decades (Erturk and Solari, 2007).

The concept of intermediation therefore requires reworking to more fully elucidate the institutional dynamics of crowdfunding. In broad terms, it is more accurate to consider the monetary and financial ecologies of crowdfunding as entailing re-intermediation rather disintermediation (French and Leyshon, 2004). The re-intermediary business models of leading UK platforms are variously rooted in digital retailing and venture capital spin-offs from mainstream finance. New business relationships are also being generated between crowdfunding platforms, on the one hand, and banks or investment funds, on the other (Alloway and Jenkins, 2015; Evans, 2015). This is leading to hybridized forms of re-intermediation that dissipate the purported disruption heralded by the rise of the crowdfunding economy. In the US, for example, the leading P2P domestic lenders began by aggregating and directing the savings of the crowd, but now increasingly channel capital provided by institutional investors into loans that, for the most part, are used by individuals and households for the purposes of refinancing existing debts at lower rates of interest. At Prosper, 80% of loans that they intermediated in March 2014 were provided by hedge funds, pension funds, sovereign wealth funds and foreign banks (Chase, 2015: 115–116). In short, as an apparently disruptive force that unsettles extant monetary and financial arrangements, crowdfunding actually bears the very strong imprint of established intermediary business models and practices.

Subjecting crowdfunding's disruptive capacities to critical scrutiny is also greatly assisted, we would argue, by foregrounding the credit–debt relations of monetary and financial ecologies. Contemporary social theories of money continue to move away from a classical emphasis on how monetary calculations squeeze-out social values (Gilbert, 2005; Zelizer, 2011). They stress that monetary exchange is actually a credit–debt relation that produces claims and obligations which extend into society and well beyond the transaction itself, and that the circulation of monetary claims and obligations are freighted with communicative socio-economic motivations and meanings (Dodd, 2014; Ingham, 2004; Konings, 2015). We are reminded, then, that while all crowdfunding creates monetary claims and obligations through digital payments infrastructures (in particular, the PayPal and Amazon payments systems (see Simon, 2011)), the distinct values, enthusiasms and affects of ‘the crowd’ that circulate and are communicated in each of the five crowdfunding ecologies are equally important. Appraisals of the role and potential of crowdfunding in the music industry (Leyshon, 2014; Leyshon et al., 2016), as well as work in the digital humanities (Bennett et al., 2015), indicates that gifting money in donation and rewards crowdfunding is infused with fandom for creative artists of various kinds. Yet, a broad spectrum of ‘orders of worth’ (Boltanski and Thévenot, 2006) are likely to be present across diverse crowdfunding ecologies. Thus, fandom and affect are likely to be key drivers in donation and rewards crowdfunding, but within the three financial ecologies the behavioural sentiments that animate monetary circulations may be more instrumental and closely resemble those in mainstream financial markets (Financial Conduct Authority, 2013). Here the monetary ecology of crowdfunding may be less a disruption to traditional banking and finance than a supplement which, at present, mobilizes the passions of investors because it offers relatively high returns due to a confluence of the efficiencies of digital business models and post-crisis low interest rates.

For the entrepreneurial subjects who successfully secure capital from the crowd, moreover, the disruption to extant debt dynamics promised by crowdfunding may also prove to be somewhat hollow. The credit–debt relations produced across the monetary and financial ecologies of crowdfunding are certainly multiple: as anthropological research tends to stress, more broadly, the contingent dyadic unity of credit–debt can lead to relational forms which can enable the building of community solidarities (Graeber, 2011; Peebles, 2010; cf. Lazzarato, 2012). And, in donation and rewards crowdfunding, the obligations take a non-monetary form that contrasts with the repayment requirements of a bank loan. This may appear to be advantageous to debtors. Yet, in donation and rewards crowdfunding non-monetary obligations can weigh heavily on those seeking to keep their promises to the crowd in ways that echo the reciprocal requirements of gift exchange. Similarly, the credit–debt relations of the three financial ecologies of crowdfunding differ from those of mainstream capital markets in a crucial respect: there are limited secondary markets in crowdfunding at present, such that creditors cannot easily liquidate their relations with debtors. Each of the three financial forms of crowdfunding also display varying levels of connectivity, patience and tolerance between funders and fundraisers, but whether these distinctive features of crowdfunding's debt dynamics are disruptive of the prevailing allocation of capital in support of entrepreneurship is open to question, issues which we attend to in detail in the next section.

Crowdfunding as ‘democratization’?

Claims that crowdfunding ‘democratizes’ the allocation of capital to entrepreneurs (Nesta, 2012) are worthy of critical attention, not least because of the powerful gatekeeping role played by banks and other investment intermediaries is widely acknowledged in critical accounts of entrepreneurship (Dannreuther and Perren, 2013). Claims that technology can bring about a broader process of social democratization are longstanding, but have been particularly prevalent since the rise of the internet and the possibilities its ubiquity offers for bringing about a new form of citizenship (e.g. Barlow, 1996; Raymond, 1999). However, such broad political claims are generally considered to be unsustainable and contradictory (Best and Wade, 2009; Morrison, 2009), and they are beyond the scope of this paper. We focus here on more modest claims that technological democracy, through the related processes of ‘disruption’ discussed earlier, undermines incumbent gatekeepers and affords the entry of participants to various economic and social processes into which they would have previously been denied access. In the case of crowdfunding, the claim that we subject to critical scrutiny is that it democratizes access to capital to fund projects.

Given how the concept of monetary and financial ecologies leads us to emphasize diversity within the crowdfunding economy, it is important to note that each of the five crowdfunding ecologies tends to capitalize different kinds of entrepreneurial projects. Crowdfunding may not enable a more egalitarian distribution of investment capital per se, but the diversity of the multiple monetary and financial ecologies that are held together in the crowdfunding economy may nonetheless create new opportunities and possibilities. For example, monetary pledges by friends, family and enthusiasts in donation and rewards crowdfunding have become a well-established source of capital for the ‘cultural entrepreneurship’ of musicians, filmmakers, authors and artists (Harris, 2013; Nesta, 2014). The ‘social entrepreneurship’ of community and charitable projects also receives funding within these ecologies. The three financial ecologies, in contrast, typically fund the commercial projects of start-ups, SMEs or real estate investors. Certain commercial projects may blur these distinctions and contain elements of cultural and/or social entrepreneurship (Buckingham et al., 2012), but they are predicated on providing a return on investment.

Because of the emphasis that it places on the socio-spatial outcomes of monetary and financial arrangements, the concept of monetary and financial ecologies encourages further critical reflection on the purported democratizing qualities of crowdfunding. As Leyshon et al. (2004: 626) argue, thinking in terms of ecologies (rather than networks and other similar concepts) provokes an explicit concern with ‘effects’ and ‘consequences’ of discrete relational arrangements of money and finance, especially ‘the spatial implications of the working through of relations through networks’. It follows that a crucial issue for future, geographical research into crowdfunding's democratizing capacities is the extent to which it may challenge the uneven geographies of entrepreneurship, including its place-based agglomeration, by attracting new investment audiences that may be motivated by different concerns beyond a narrow focus on maximizing financial return. This may create new possibilities that run counter to long-run processes that have generated uneven spatial development, opening up possibilities for a form of market generated but non-exploitative ‘green-lining’ of investment that traditionally has been the preserve of dedicated institutions, such as community development banks and/or government agencies (Li et al., 2002; Wyly et al., 2004).

Through an analysis of the music-based rewards crowdfunding site, Sellaband, Agrawal et al. (2015) argue that online platforms are able to successfully attract geographically distant investors to overcome the recognized bias towards colocation. They argue that the ability of artists to attract equity funding over space demonstrates ‘that what appears to be a geographic distance effect is mostly a social effect’; in other words, while ‘it is likely that colocation influences the likelihood of establishing social connections, it is pre-existing social relationships that serve as the mechanism through which geographic distance matters’ (271). In this sense, as Agrawal et al. suggest, it may be that crowdfunding can challenge the received understanding of capitalizing ventures where, despite widely available knowledge and techniques, being in the right place at the right time is significant in producing successful entrepreneurship. Crowdfunding has the potential to challenge established notions of the ‘right place’ by appealing over the heads of traditional audiences for investment, hailing new subjects that may be connected to ventures through digitally mediated ties of affect and enthusiasm. Indeed, it may be that the crowdfunding economy has the ability to bring together geographically distributed funders and fundraisers according to the logic of the internet's ‘long tail’. Those with shared interests who are separated by physical distance may create online ecologies that centre on particular crowdfunding platforms and allied nodal points (i.e. social media forums, chatrooms, hashtags, etc.). In that sense, crowdfunding dissolves distance and erodes the inequities of location in the way that, as Zook (2005) shows, is the case for many internet-based businesses in the United States located in remote and less favoured regions. It also may also pose a challenge to established understandings of agglomeration, where localized information and knowledge spillovers are regarded as key to entrepreneurship (Henry and Dawley, 2011; Martin and Sunley, 2003). Regional and urban ‘clusters’ of related industries and institutions have been shown to operate more efficiently and to exhibit entrepreneurialism due to concentrations of technologies, infrastructures, pools of knowledge and other inputs that include appropriate and adequate sources of capital.

Nonetheless, it remains the case that any claims that crowdfunding broadens and more equitably distributes opportunities to access capital for entrepreneurship should be treated with considerable caution. It needs to be recognized, for instance, that whether an entrepreneurial project receives funding from the crowd is highly contingent from the outset, and that contingencies vary across the different crowdfunding ecologies. This is because the initial eliciting of funding is itself a highly competitive process. It is by differentiating between projects, and thereby deciding which is worthy of capitalizing and which is not, that the collective intelligence and ‘wisdom of the crowds’ (Surowiecki, 2004) is said to be brought to bear (cf. Borch, 2012). For example, roughly half of all crowdfunding campaigns in the UK fail to raise sufficient funding to allow projects to proceed (Nesta, 2013b). Successful campaigns have also been shown to require the mobilization of social and cultural capital in ways that have equity and exclusionary effects (Davidson and Poor, 2014). Such effects are especially apparent in crowdfunding's financial ecologies. For example, more women than men raise funds in donation and rewards ecologies in the UK, but women are in the minority amongst those raising funds in P2P business lending (24%) and in equity crowdfunding (22%) (Baeck et al., 2014: 15). Those contributing funds to donations and rewards ecologies, meanwhile, tend to be drawn relatively broadly from across the income and age spectrum. In contrast, high net worth individuals usually provide funds in equity crowdfunding, and it is men aged 55 and over, with incomes in excess of £50,000, who are the typical funders of P2P business and domestic loans (pp. 15–17). Similar patterns have been revealed in the US. Smith (2016) found that female funders are overwhelmingly motivated by the desire to help someone in need, which was a reason for giving to crowdfunding platforms in 75% of women surveyed, compared to 58% of men. Meanwhile, men are more motivated to give to support new products or innovations (42%) than are women (27%).

Competition for capital is also enshrined through various intermediary practices of crowdfunding platforms, not least the ‘all-or-nothing model’. This requires that projects seeking funding set a target to be achieved within a short-term timescale, typically 1–3 months. Indeed, many platforms encourage the shortest possible campaign. If a project fails to reach its target by the deadline would-be funders have their investment returned. The model's logic is that short deadlines provide a ‘proof of concept’, and an indication of future demand, without which a project is less likely to deliver on its objectives. Additional barriers to entry are erected by platform intermediation. In the financial ecologies of crowdfunding, platforms screen projects prior to listing, drawing on external credit checks and evaluations of the business cases made for working capital or expansion. Investors are also encouraged to undertake their own due diligence when selecting between projects (Langley, 2016).

Moreover, the ability of crowdfunding to democratize capital allocation across space – overcoming geographical barriers that discriminate against entrepreneurs based in remote locations (Zook, 2004) – should be qualified because crowdfunding ecologies would actually seem to depend on the intersections of digital networks and place-based clusters. In the UK's crowdfunding economy, for example, both the location of platform intermediaries and landscape of credit–debt relations favour London and the South East. Many platforms in the UK crowdfunding sector are embedded in a place-based urban cluster centred on East London's so-called FinTech sector (McWilliams, 2015). While these platforms can reach distributed investment audiences and entrepreneurial ventures, the geography of crowdfunding in the UK remains highly uneven. This is revealed by an analysis of the regional distribution of funders and fundraising across equity-based rewards and peer-to-peer consumer lending platforms in the UK (Baeck et al., 2014). London and the South East are the most active regions in the UK crowdfunding economy overall: those providing funds or fundraising are most frequently located in these regions. Yet, this is a tendency which is especially pronounced in crowdfunding's financial ecologies. For example, 26% of those raising rewards crowdfunding are located in London, a figure that rises to 41% in the equity crowdfunding. Add the rest of the South East and the result is that over half (52%) of those raising funds for start-up enterprises through equity crowdfunding are found in these two regions (Baeck et al., 2014: 18–19). In P2P domestic lending, meanwhile, 25% of borrowers live in London and the South East, but 37% of funders are located in these two regions (Baeck et al., 2014: 18). Assuming that borrowers continue to meet the repayment obligations, the aggregations and distributions of P2P domestic lending over time will lead to an inflow of revenue into London and the South East. Although these figures refer to funders and borrowers, and not the actual volume of funds, they suggest that London is likely to be a net importer of capital to support projects, be they equity based or rewards crowdfunding. And, along with the rest of the South East, it is also likely to be an exporter of capital to fund P2P consumer lending. This net import and export of different forms of crowdfunded capital would likely work in London's favour, as money is imported to capitalize productive new projects and ventures, yet is exported to earn income from personal indebtedness within the rest of the UK.

Conclusions

This paper has offered an analysis of the emergent and rapidly growing economy of crowdfunding by drawing upon and developing the concept of ‘ecologies’ from the geographies of money and finance literature. Specifically, we have made a series of conceptual and analytical manoeuvres that have clarified and deepened the notion of monetary and financial ecologies, on the one hand, while critically questioning the purported ‘alternative’, ‘disruptive’ and ‘democratizing’ qualities of crowdfunding, on the other hand. The concept of ecologies directs analysis to diverse and proliferative monetary and financial forms. Accordingly, with particular reference to the UK, we have outlined the anatomy of the five main crowdfunding ecologies that have emerged to date and highlighted how such diversity problematizes the tendency to frame the crowdfunding economy through the binary of capitalist/alternative. Connecting with research that highlights the dynamic ambivalences of monetary and financial forms, we suggested that crowdfunding is an ‘alternative’ space of money and finance only in the strict sense of the word's Latin root (alternare), ‘implying oscillation, a movement back and forth between an “is” and an “as if” rather than a specification of an ontology’ (Maurer, 2013: 415). The paper has also developed the concept of monetary and financial ecologies in two further respects: it has foregrounded the role of intermediary institutions and credit–debt relations in the coming together of monetary and financial ecologies, and it has emphasized the uneven socio-spatial effects of monetary and financial ecologies. Each of these conceptual moves, respectively, informed our consideration of the claims made for crowdfunding's disruptive and democratizing capacities and, to conclude, we want to reflect further and more broadly on these claims.

Firms that embark on strategies to disrupt markets have two targets in sight: incumbent firms that they wish to usurp through cheaper and more efficient means of production and/or service delivery, and the regulatory structures that help to configure and define existing markets and the behaviours within them. In sweeping away incumbents, therefore, disruptive firms also call for new more transparent systems of regulation. In the contemporary period, this is best illustrated in the blockchain ledger used by cryptocurrencies which is not only publically open for inspection, but highly resistant to tampering and fraud (Maurer, 2015). When crowdfunding is measured against even this relatively narrow and largely economic definition of the objective of disruption – leaving aside the possibility that it may also contribute to a socially progressive democratization of the allocation of capital – our analysis suggests that, at present, it comes up well short. In the donation and rewards ecologies of crowdfunding, intermediary platforms have tended not to sweep away incumbents, but fill a funding gap created by the concentration and centralization of capital investment and exacerbated by the retrenchment of traditional funders of cultural activity, such as public funding bodies subject to the politics of austerity and increasingly parsimonious private sector companies. Across its financial ecologies, meanwhile, crowdfunding perhaps has greater potential to disrupt incumbent firms and regulations because, as noted earlier, it appears to offer efficiency and, to date at least, a lower rate of default. Moreover, the inability of investors to pass off their debt obligations in secondary markets may be the most socially progressive quality of the disruptive force of crowdfunding, especially given the importance of securitization and secondary and derivative markets in debt for enabling financialization in the past 30 years or so (Leyshon and Thrift, 2007). However, even here, the capacity of crowdfunding to be disruptive is based on an assumption that it carries forward the disintermediation of finance. But this overlooks both the re-intermediary strategies of crowdfunding platforms that we discussed above, and that many of the companies and ventures raising money through crowdfunding have done so because they have been rejected by traditional venture capital firms as they failed to meet their more exacting standards: crowdfunding investors may, according to Stephany (2015: 105), simply be ‘less fussy’.

Our analysis also underlines that crowdfunding's democratizing credentials – opening up investment capital to a much wider constituency of entrepreneurship than hitherto – needs to be carefully qualified. In rewards and donation crowdfunding ecologies, access to capital for all manner of projects may well have been made available in a way that would not have been previously possible. It is also the case that while social and cultural entrepreneurs are not under pressure to meet monetary obligations and realize financial returns for their ‘investors’, they nonetheless run the risk of turning supporters and fans into opponents and anti-fans if they do not deliver on their promises, with potentially serious implications for livelihoods (Leyshon et al., 2016). The capital made available through these particular crowdfunding ecologies also comes without the close engagement, guidance and mentoring that often accompanies venture capital funding. Moreover, while access to capital is certainly contingent and unequal in a range of ways, it is highly likely to be sharply impacted by the uneven geographies of digital and place-based clustering. Within crowdfunding's financial ecologies, meanwhile, the initial success of platforms as providers of capital for entrepreneurship would appear to be in the process of encouraging collaboration and eventually integration with mainstream finance, as established institutions use the strength of their balance sheets to absorb their emergent intermediary competitors. As the crowdfunding economy develops further we suspect that its financial ecologies could also prove to have cyclical temporal dimensions. A brief flowering of albeit uneven democratization may be followed, for instance, by a return to processes of capital concentration and centralization as incumbents absorb crowdfunding platforms and other FinTech start-ups. Equally, even if the financial ecologies of crowdfunding were to prove increasingly successful at carrying forward the democratization of capital, then this may actually create problems (and possibly a crisis) at a later date. In Stephany's (2015: 105) terms, ‘If vast quantities of fresh capital from individuals become available, too much money could chase too few worthy investment opportunities’. Similar concerns are shared by The Economist (2016b) in a report on the rapid growth of P2P lending in China. While P2P lenders usefully offer new investment opportunities and direct funding to parts of the economy traditionally neglected by the state-owned banks, the failure rate among P2P lenders is high. By 2015, a third of all such companies experienced operational difficulties, ranging from ‘halted operations, disputes, frozen withdrawals or … bosses who have absconded’ (The Economist, 2016b). As the Global Financial Crisis so starkly illustrated, the extension of credit–debt relations to borrowers previously deemed to constitute a high level of ‘default risk’ always confronts incalculable uncertainties. There is a danger, in short, that too much democratization of capital could ultimately lead to a crisis and collapse of crowdfunding's financial ecologies.

Footnotes

Acknowledgements

Earlier versions of this paper were presented at The Insurance Institute of London (London, November 2014), the Association of American Geographers Annual Conference (Chicago, April 2015), Nesta (London, May 2015) and at the ESRC seminar ‘Microenterprise, technology and big data: new forms of digital enterprise and work and ways to research them’ (Southampton, October 2016). We are grateful to participants for helpful comments and suggestions, as we are too for the insightful comments of Sarah Hall and Kean Lim on an earlier draft of this paper.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.